#environmentalregulations

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Kazakhstan’s Minister of Communications and Informatics has blocked the Tumblr site because it contained 60 sites of terrorism, extremism, and pornography in 2015.

Text

R-134A Refrigerant Market, Global Outlook and Forecast 2025-2030

R 134A Refrigerant Market Size, Demand & Supply, Regional and Competitive Analysis 2025-2031

Market Size

The global R-134A refrigerant market was valued at US$ 142.1 million in 2022 and is projected to decline to US$ 84 million by 2030, exhibiting a Compound Annual Growth Rate (CAGR) of -7.3% during the forecast period from 2022 to 2030.

Definition

R-134A, also known as 1,1,1,2-Tetrafluoroethane, is a hydrofluorocarbon (HFC) refrigerant widely used in refrigeration and air conditioning systems. It is commonly used as a replacement for CFC-12 (Freon-12) due to its lower ozone depletion potential. R-134A is known for its efficiency, safety, and non-ozone-depleting properties, making it an essential component in automotive air conditioning systems, home appliances, and refrigeration units. Download a free Sample Report PDF

R-134A is favored in systems that require a non-flammable refrigerant with minimal environmental impact. However, as global regulations around climate change and global warming potential (GWP) have evolved, there has been a growing shift towards refrigerants with lower GWPs, such as R-1234yf and natural refrigerants. This shift is expected to impact the R-134A market significantly over the coming years.

Key Characteristics of R-134A Refrigerant:

Environmentally friendly: Non-ozone-depleting and safer for the environment compared to older refrigerants like CFC-12.

Wide applications: Used in automotive air conditioning, refrigeration, and commercial cooling systems.

Phase-out trend: Due to its relatively high GWP, R-134A is being phased out in favor of more eco-friendly alternatives, though it is still widely used in certain industries.

Market Growth Projections:

Current Market Size (2022): US$ 142.1 million

Projected Market Size (2030): US$ 84 million

CAGR (2022-2030): -7.3%

This decline can be attributed to increasing regulatory pressures for environmentally safer refrigerants, such as R-1234yf, and the global shift towards adopting low-GWP alternatives. As a result, industries that have been relying on R-134A are transitioning to these new refrigerants, thus impacting the overall market dynamics.

Historical Market Trends:

In recent years, R-134A's market share has been eroded by emerging refrigerants with much lower global warming potential. Historically, R-134A was highly popular due to its low toxicity, non-flammability, and efficiency in refrigeration and air conditioning systems. However, international agreements like the Kigali Amendment to the Montreal Protocol and the Paris Climate Agreement have mandated the reduction of high-GWP substances, pushing for the adoption of greener alternatives.

Global R-134A Refrigerant: Market Segmentation Analysis

This report provides a deep insight into the global R-134A Refrigerant market, covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance the potential profit. Furthermore, it provides a simple framework for evaluating and assessing the position of the business organization. The report structure also focuses on the competitive landscape of the Global R-134A Refrigerant. This report introduces in detail the market share, market performance, product situation, operation situation, etc., of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the R-134A Refrigerant in any manner.

Market Segmentation (by Application)

Automotive Air Conditioning

Refrigeration Systems

Commercial Cooling Systems

Home Appliances

Market Segmentation (by Type)

Industrial-Grade R-134A

Automotive-Grade R-134A

Key Company

Honeywell International

Chemours Company

Daikin Industries

Arkema S.A.

Kraton Polymers

Access To The Full Report

#R134ARefrigerant#RefrigerantMarket#MarketForecast#GlobalMarket#HVACIndustry#CoolingSolutions#AutomotiveAC#IndustrialRefrigeration#MarketTrends#Fluorochemicals#ClimateControl#MarketGrowth#RefrigerationIndustry#EnvironmentalRegulations#IndustryAnalysis#SustainableCooling

0 notes

Text

Turbine Oil Market

𝐓𝐡𝐞 𝐅𝐮𝐭𝐮𝐫𝐞 𝐨𝐟 𝐓𝐮𝐫𝐛𝐢𝐧𝐞 𝐎𝐢𝐥 𝐌𝐚𝐫𝐤𝐞𝐭 𝐢𝐧𝐝𝐮𝐬𝐭𝐫𝐲 (𝐋𝐚𝐭𝐞𝐬𝐭 𝐏𝐃𝐅) | IndustryARC™

The Turbine Oil Market Size is forecast to reach $ 2018.9 Million by 2030, at a CAGR of 3.9% during forecast period 2024–2030.

➡️ 𝑫𝒐𝒘𝒏𝒍𝒐𝒂𝒅 𝑺𝒂𝒎𝒑𝒍𝒆 𝑹𝒆𝒑𝒐𝒓𝒕

The Turbine Oil Market refers to the global industry encompassing the production, distribution, and use of specialized lubricants designed for turbines. These oils are used in various turbine systems, including steam turbines, gas turbines, and hydraulic turbines, across industries such as power generation, aviation, marine, and industrial manufacturing.

𝐀𝐩𝐩𝐥𝐢𝐜𝐚𝐭𝐢𝐨𝐧𝐬:

Power Generation: Steam and gas turbines in power plants.

Industrial Use: Turbines used in manufacturing processes.

Aviation: Jet engines and auxiliary power units (APUs).

Marine: Turbines in ships for propulsion and power.

➡️ 𝑭𝒐𝒓 𝑴𝒐𝒓𝒆 𝑰𝒏𝒇𝒐𝒓𝒎𝒂𝒕𝒊𝒐𝒏

𝐒𝐡𝐢𝐟𝐭 𝐓𝐨𝐰𝐚𝐫𝐝 𝐒𝐲𝐧𝐭𝐡𝐞𝐭𝐢𝐜 𝐋𝐮𝐛𝐫𝐢𝐜𝐚𝐧𝐭𝐬:

Synthetic turbine oils are gaining traction due to superior performance, longer service life, and better resistance to extreme temperatures and oxidation.

𝐅𝐨𝐜𝐮𝐬 𝐨𝐧 𝐒𝐮𝐬𝐭𝐚𝐢𝐧𝐚𝐛𝐢𝐥𝐢𝐭𝐲:

Increased demand for environmentally friendly and biodegradable turbine oils, driven by stringent environmental regulations and corporate sustainability goals.

➡️By Now

𝐆𝐫𝐨𝐰𝐢𝐧𝐠 𝐑𝐞𝐧𝐞𝐰𝐚𝐛𝐥𝐞 𝐄𝐧𝐞𝐫𝐠𝐲 𝐒𝐞𝐜𝐭𝐨𝐫:

Expansion of wind, hydro, and solar power generation, which relies on turbine systems, is driving demand for specialized turbine oils.

➡️ 𝐤𝐞𝐲 𝐏𝐥𝐚𝐲𝐞𝐫𝐬 : Royal Dutch Mint | ExxonMobil | bp | TotalEnergies Recrutement Gérance station-service | TotalEnergies | Chevron | Chevron Phillips Chemical Company | Idemitsu Kosan Co., Ltd | Digital Turbine | Triveni Turbine Limited | L.A. Turbine (LAT), A Chart Industries Company | Turbine Surface Technologies | Advanced Turbine Engine Company | Leistritz Turbine Technology | Turbine Blades UK | Turbine Leipzig e.V.

#TurbineOil#SyntheticLubricants#BioBasedOils#RenewableEnergy#Sustainability#LubricantInnovation#PowerGeneration#IndustrialGrowth#EnvironmentalRegulations#PredictiveMaintenance

0 notes

Text

NEMA Orders Sand Transporters to Secure Permits Under New Regulations

The National Environment Management Authority (NEMA) has mandated all sand transporters to acquire permits in line with the newly established environmental guidelines.

In a statement issued on February 18, 2025, NEMA instructed those engaged in sand harvesting to apply for the necessary licenses via its official portal. Director-General Mamo Boru Mamo highlighted that the regulations, which were introduced under the Environmental Management and Coordination (Sand Harvesting) Regulations of 2024, aim to promote sustainable sand use while safeguarding the environment.

“The primary goal of these regulations is to facilitate responsible sand extraction practices, ensuring both environmental protection and resource sustainability,” the statement emphasized.

0 notes

Text

Trump’s Election Win Spells Bad News for the Auto Industry

Trump’s Election Win Spells Bad News for the Auto Industry With Donald Trump securing a second presidential term, the auto industry braces for significant disruptions. His first term was characterized by attempts to weaken environmental regulations impacting the sector, and as a candidate in 2024, Trump has pledged to continue this trend through aggressive trade policies and a retreat from climate change commitments. Here’s what the future may hold for the auto industry under a Trump administration. Electric Vehicle Adoption at Risk One of the cornerstone policies of the previous administration was the Inflation Reduction Act of 2022, which included substantial incentives for electric vehicle (EV) adoption. This Act mandated that to qualify for the clean vehicle tax credit, vehicles must have final assembly in North America and increasing amounts of U.S.-sourced battery components. However, these policies face strong opposition from the Republican Party. During his first term and throughout his campaign, Trump has been vocal against EVs, claiming that "all-electric is not going to work." He promised to eliminate the electric vehicle mandate on his first day in office, directly challenging the Biden administration's goal of achieving 50% EV adoption by 2030. The Project 2025 policy document, developed by the Heritage Foundation, reflects a lack of support for EVs, advocating for the freedom of Americans to choose their vehicles without government coercion. The Trump campaign has indicated that if he returns to office, California's waiver regarding emissions standards would be revoked, limiting the regulatory framework that currently applies to 16 states and the District of Columbia. Fuel efficiency regulations set to take effect in two years are now likely in jeopardy. The previous administration had already taken steps to undermine existing standards, casting doubt on the future of electric vehicle initiatives in the U.S. Automakers may revert to a focus on larger, less fuel-efficient vehicles, such as SUVs and trucks, particularly as companies like Ford report substantial losses in their EV divisions. Mixed Outlook for Automakers For established automakers like Toyota and Stellantis, which have been slower to adopt EV technology compared to their European and Korean rivals, Trump's election could provide a temporary reprieve. The shift away from stringent EV regulations may allow them to focus on traditional combustion engines without the pressure to transition to electric models rapidly. The Zero Emission Transportation Association (ZETA) has expressed a willingness to collaborate with the incoming administration to maintain the U.S.’s competitive edge in automotive innovation. They emphasize the need for policies that ensure the development and deployment of EV technologies by American workers in U.S. factories. Tesla's Position under Trump In contrast, Tesla is likely to fare better under a Trump administration. CEO Elon Musk has increasingly aligned himself with Republican causes, significantly contributing to Trump's reelection campaign. This shift could position Musk favorably for a potential cabinet role, which could shield Tesla from rigorous regulatory scrutiny, particularly concerning its driver assistance systems. While some analysts express concern that a cabinet position could detract from Musk’s focus on Tesla, the automaker stands to benefit from ongoing funding initiatives, such as the National Electric Vehicle Infrastructure (NEVI) program, which aims to expand fast charging stations across the U.S. Potential for Increased Import Tariffs The new administration is expected to escalate efforts to protect U.S. auto manufacturing from foreign competition, particularly from China. Under Biden, a 100% import tariff was imposed on Chinese-made EVs, and this protectionist sentiment is likely to grow under Trump. Trump's previous rhetoric about abolishing federal taxes in favor of import tariffs could lead to significant price increases for imported vehicles and parts. German automakers, already facing stock declines, may feel the impact of these policies, especially as they rely on the U.S. market while maintaining manufacturing facilities within the country. Conclusion Trump’s return to the White House signals a challenging landscape for the auto industry, particularly concerning electric vehicle adoption and environmental regulations. While some automakers may find temporary relief from stringent policies, the overall direction appears to favor traditional vehicles and protectionist measures that could reshape the industry for years to come. Thank you for taking the time to read this article! Your thoughts and feedback are incredibly valuable to me. What do you think about the topics discussed? Please share your insights in the comments section below, as your input helps me create even better content. I’m also eager to hear your stories! If you have a special experience, a unique story, or interesting anecdotes from your life or surroundings, please send them to me at [email protected]. Your stories could inspire others and add depth to our discussions. If you enjoyed this post and want to stay updated with more informative and engaging articles, don’t forget to hit the subscribe button! I’m committed to bringing you the latest insights and trends, so stay tuned for upcoming posts. Wishing you a wonderful day ahead, and I look forward to connecting with you in the comments and reading your stories! Read the full article

#autoindustry#DonaldTrump#electricvehicles#environmentalregulations#importtariffs#InflationReductionAct#Tesla

0 notes

Text

Construction Lubricants Market - Forecast(2024 - 2030)

Construction Lubricants Market Overview

The Construction Lubricants Market size is estimated to reach US$12.5 billion by 2030, after growing at a CAGR of 3.8% over the forecast period 2024–2030. Construction lubricants are used to reduce friction between moving parts or surfaces and to improve the efficiency of construction machines and it includes hydraulic fluid, automatic transmission fluid, compressor oil, grease and engine oil. Lubricants are used to reduce friction in construction equipment such as bulldozers, dump trucks, draglines, scrapers and shovels and other heavy machinery.

The global expansion of the construction sector is one of the primary reasons driving the growth of the construction lubricants market. The rising need for high-quality lubricants in a variety of construction activities, as well as the growing popularity of synthetic oil-based lubricants due to advantageous qualities such as water solubility, are driving the market growth. The covid-19 pandemic majorly impacted the construction lubricants market due to restricted production, supply chain disruption, logistics restrictions and a fall in demand. However, with robust growth and flourishing applications across major construction industries the construction lubricants industry is anticipated to grow rapidly over the forecast period.

Sample Report:

Market Snapshot

Construction Lubricants Market Report Coverage

The “Construction Lubricants Market Report — Forecast (2024–2030)” by IndustryARC, covers an in-depth analysis of the following segments in the construction lubricants industry. By Base Oil — Mineral Oil, Synthetic Oil and Bio-Based Oil. By Type — Hydraulic Oil, Engine Oil, Gear Oil, Automatic Transmission Fluid, Compressor Oil, Grease and Others. By Equipment — Earthmoving Equipment, Material Handling Equipment, Electrical & Electronics, Heavy Construction Vehicles and Others. By Application — Commercial and Residential. By Geography — North America (the USA, Canada and Mexico), Europe (UK, Germany, France, Italy, Netherlands, Spain, Belgium and the Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia and New Zealand, Indonesia, Taiwan, Malaysia and Rest of APAC), South America (Brazil, Argentina, Colombia, Chile and Rest of South America), Rest of the World [Middle East (Saudi Arabia, UAE, Israel and Rest of the Middle East) and Africa (South Africa, Nigeria and Rest of Africa)].

Key Takeaways

The Asia-Pacific region dominates the construction lubricants market size, owing to the region’s high economic growth rate and high investment in the construction industry.

The expanding construction activities, as well as the upgrading of heavy machinery, are the primary driving factors influencing the construction lubricants market.

However, technological developments are limiting market growth by reducing equipment size and lubricant consumption in the construction industry.

For More Details on This Report — Request for Sample

Inquiry Before Buying:

Construction Lubricants Market Segment Analysis — by Base Oil

Synthetic Oil held a significant share in the Construction Lubricants market share in 2023 and is forecasted to grow at a CAGR of 3.3% over the forecast period 2024–2030, owing to the extensive characteristics provided by synthetic oil over other base oil types such as mineral oil and bio-based oil. Synthetic oils are base oils and additives that improve an engine’s overall performance. When compared to traditional mineral oil-based lubricants, synthetic oils offer improved performance, lower maintenance costs and address environmental concerns. As a result of the increased focus on emissions and expanding consumer awareness about the benefits of synthetic oils, there is a large demand for synthetic oils, which is contributing to the revenue growth of the global

construction lubricants market size.

Construction Lubricants Market Segment Analysis — by Application

The Commercial held a significant share in the Construction Lubricants market share in 2023 and is forecasted to grow at a CAGR of 4.1% during the forecast period 2024–2030, owing to the significant use of construction lubricants in the commercial sector. Construction lubricants lower corrosion and friction while increasing the longevity of the machine’s moveable elements. The commercial construction sector is expanding globally owing to a robust economy and solid market fundamentals for commercial real estate, as well as an increase in government initiatives for public works and institutional buildings. For Instance, Argentina has proposed a commercial building proposal of $428 million dollars. As part of the Plan Argentina Hace, the Ministry of Public Works said in January 2022 that it would invest ARS10.6 trillion ($91 billion) to complete 3,131 new infrastructure works and projects around the country. With the rise in commercial activities across the globe, the demand for construction lubricants is anticipated to rise for various applications, which is projected to boost the market growth in the commercial industry during the forecast period.

Schedule a Call:

Construction Lubricants Market Segment Analysis — by Geography

The Asia-Pacific region held the largest share in the Construction Lubricants market share in 2023. The fuelling demand and growth of construction lubricants in this region are influenced by flourishing demand from construction industries, along with fuelling construction activities across APAC. The building and construction sector is growing rapidly in Asia-Pacific owing to a major development in infrastructural projects, emphasis on affordable housing units and modular building technology. According to the Department for Promotion of Industry and Internal Trade (DPIIT), In India, Between April 2000 and September 2023, foreign direct investment (FDI) in the construction development (townships, housing, built-up infrastructure and construction development projects) and construction (infrastructure) activity sectors totalled US$26.4 billion and US$32 billion, respectively. According to the International Trade Administration, the construction sector in China is projected to grow at an average of 8.6% from the year 2022 to 2030. Furthermore, the Make in India campaign by the Government of India plans to achieve infrastructural investment worth US$965.5 million by the year 2040. With the robust growth of the building and construction industry in Asia-Pacific, the demand for construction lubricants for equipment such as hydraulic fluid, engine oil, grease and others in construction will rise. Thus, with the high growth of construction lubricants in construction applications, it is anticipated that the demand for the construction lubricants industry will flourish during the forecast period.

Construction Lubricants Market Drivers

Government Initiatives Bolstering the Growth of the Commercial Sector:

Construction Lubricants reduce corrosion and frictio n while increasing the longevity of machine moveable parts, which drives the market growth of construction lubricants in the commercial industry. The demand for Construction Lubricants is rapidly growing as government investment in the commercial industry increases. For instance, Kansai International Airport in Japan will spend about 100 billion yen (US $683 million) by 2025 to upgrade the larger terminal, to increase space for international flights at the country’s №2 hub. The Indian Union Budget of February 2023 aims to build 50 additional airports, aerodromes, helipads, and water routes to enhance connectivity. The health facility revitalization component of the national health insurance indirect grant in South Africa has been allocated R4.4 billion (US $23.3 million) over the medium term (2022–2025). These grants are aimed at accelerating the construction, maintenance, upgrading and rehabilitation of new and existing health system infrastructure. Over the medium term, the department aims to construct or revitalise 92 health facilities through the indirect grant and conduct major maintenance work or refurbishment on a further 200 facilities. The Union Budget 2023 also allocated Rs 76,431 crore (US $9.3 billion) to the Ministry of Housing and Urban Development (MoHUA) with the aim of aiding the completion of stalled housing projects. As a result of all these initiatives, the demand for construction lubricants for equipment such as hydraulic fluid, engine oil, grease and others in construction will rise. Thus, with the high growth of construction lubricants in the commercial industry, it is anticipated that the demand for the construction lubricants industry will flourish during the forecast period.

Buy Now:

Bolstering Growth of the Residential Industry:

Construction Lubricants have seen a huge increase in their use in residential areas. The residential industry uses a variety of equipment that require construction lubricants in order to eliminate breakdowns and reduce friction. Additionally, individuals are remodeling their homes in accordance with trends to improve their visual appeal of the same. Due to these comprehensive qualities and Urbanisation, the market for construction lubricants for the residential industry is growing. For instance, the residential construction industry in Canada displayed a notable upswing in august. Statistics Canada reported a 1.6% surge in investment to $11.9 billion, with single-family homes rising by 2.4% to $5.9 billion and multi-unit constructions climbing 0.9% to $6.0 billion. According to Japan’s Ministry of Land, Infrastructure, Transport and Tourism, the construction reported a 5% rise in housing construction within the public sector in 2023. Thus, with the high growth of construction lubricants in the residential industry, it is anticipated that the demand for the construction lubricants industry will flourish during the forecast period.

Construction Lubricants Market Challenge

Fluctuations in Crude Oil Prices

Fluctuations in crude oil prices continue to be one of the main challenges in the construction lubricants market. Construction lubricants are essentially petrochemicals derived from Brent crude oil. Rising crude oil prices cause raw material price volatility, posing substantial hurdles for manufacturers in the construction lubricants market. For instance, the Brent crude oil price increased from US$86.51/bbl in Jan 2022 to US$122.71/bbl in June 2022 and then decreased to US$74.84/bbl in June 2023. This results in a considerable increase in construction lubricant prices, which drives up manufacturing costs and reduces manufacturers’ profit margins, thereby limiting the construction lubricants market growth.

Construction Lubricants Industry Outlook

Technology launches, acquisitions and R&D activities are key strategies adopted by players in the construction lubricants market. The top 10 companies in the Construction Lubricants market are:

Royal Dutch Shell

ExxonMobil

BP p.l.c.

Chevron Corporation

TotalEnergies SE

Petrochina Company

LUKOIL

Indian Oil Corporation

Sinopec

Fuchs Petrolub SE

Recent Developments

In May 2023, BIGBEN’s introduction of ScaffOil represented a significant leap in construction lubricants. This eco-friendly, high-performance product tailored for scaffolding and construction offers weather resilience and superior penetrating power. Its focus on durability and operational efficiency aligns with evolving demands in this sector.

In June 2022, Volvo Construction Equipment launched Volvo Hydraulic Oil 98611 HO103, revolutionizing the construction lubricants market. This oil extends drain intervals in Volvo’s crawler excavators to 3,000 hours, enhancing equipment performance and longevity. Featuring optimized fuel efficiency, reduced oil consumption, and environmental benefits, it offers diverse viscosity options, marking a significant advancement in lubricant technology.

In March 2022, BPCL, launched four new MAK lubrication products. Each product is intended to improve customer performance, dependability and durability

For more Chemicals and Materials Market reports, please click here

#lubrication#efficiency#equipmentlongevity.#syntheticlubricants#performance#sustainability#biodegradablelubricants#ecofriendly#heavyduty#highperformancelubricants#wearandtear#energyefficient#operatingcosts.#predictivemaintenance#iotlubrication#downtime#machinelife.#innovation#environmentalregulations#longlasting#offroadvehicles#constructionmachinery.#advancedlubrication#corrosionprotection#reducedemissions.#greaselubrication#hydraulicfluids#smoothoperation#maximumperformance#extremeconditions.

0 notes

Text

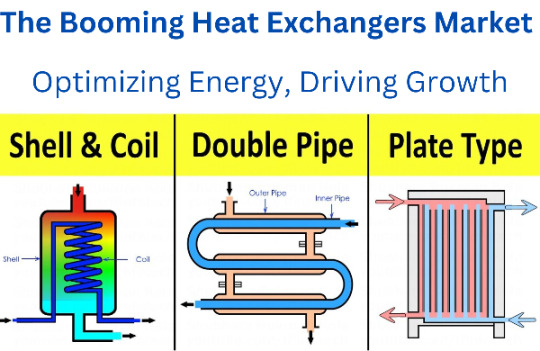

Heat Exchangers Market Landscape: Detailed Analysis of Size, Share, and Emerging Trends

The global heat exchangers market size is expected to reach USD 26.26 billion by 2030, registering at a CAGR of 5.4% from 2024 to 2030, according to a new report by Grand View Research, Inc. Rising demand from various industries, including chemical & petrochemical, and power generation, along with an increasing focus on improving efficiency standards is expected to drive the market.

Heat Exchangers Market Report Highlights

The demand for plate & frame heat exchangers is anticipated to witness growth at a CAGR of 6.1% from 2024 to 2030 on account of its simple & compact structure coupled with their ability to increase capacity easily by adding new plates to the system

The shell & tube segment led the market and accounted for 35.6% of the global revenue in 2023

Asia Pacific heat exchanger demand is likely to grow at a CAGR of 6.8% over the forecast period

The demand for heat exchangers in Saudi Arabia is expected to witness a CAGR of 4.5% owing to the presence of a robust oil & gas industry coupled with the growth in the manufacturing sector attributed to the government’s diversification efforts

For More Details or Sample Copy please visit link @: Heat Exchangers Market Report

The presence of favorable government regulations in the emerging economies of China, India, Brazil, and Mexico about setting up new manufacturing facilities is expected to spur the demand for heat exchangers in various industries. In addition, upcoming nuclear power projects, particularly in the Asia Pacific, are anticipated to drive market growth during the forecast period.

Technological advancements coupled with constant efforts and investments by major market participants in product innovation and research & development are expected to increase the market competitiveness over the coming years. The adoption of novel techniques of additive manufacturing in the production of heat exchangers is likely to complement industrial growth.

The COVID-19 pandemic has severely impacted several economies worldwide. Containment measures, including lockdowns imposed by various countries to curb the spread of COVID-19, have resulted in limiting the operations of manufacturing facilities, thereby negatively impacting the demand for heat exchangers in 2020.

#ThermalManagement#EngineeringSolutions#IndustrialHeating#CoolingSystems#EnergySystems#EcoFriendlyTech#PowerGeneration#ProcessEngineering#HeatTransfer#CleanEnergy#MechanicalEngineering#TechInnovation#EnvironmentalRegulations#HVAC#RenewableEnergy

0 notes

Text

House Republicans' Bill Threatens Environment & Health: What You Need to Know #EnergyandEnvironmentalPolicyAct #environmentalregulations #fossilfuelindustry #houserepublicans #renewableenergyprograms

#Politics#EnergyandEnvironmentalPolicyAct#environmentalregulations#fossilfuelindustry#houserepublicans#renewableenergyprograms

0 notes

Text

Japanese businesses saving money with "cool biz" #coolbiz #environmentalregulations #japancoolbiz #Japan #japanesebusinesses

0 notes

Text

Revolutionary Blockchain-Based SCEMS: Driving a Greener Future

In a groundbreaking move to combat climate change, Hyundai Motor and Kia Corporation have successfully deployed their revolutionary blockchain-based Supplier CO2 Emission Monitoring System (SCEMS) on the Hedera mainnet. This pioneering system is designed to preemptively address local and global environmental regulations while fostering sustainable supply chains within both companies and their cooperative partners.

Calculating Carbon Emissions Across the Entire Supply Chain

The core objective behind the creation of SCEMS is to accurately calculate carbon emissions throughout the entire supply chain. By gaining access to reliable data from their suppliers' operations, Kia and Hyundai Motor can now monitor the sources of raw materials, the production process, and the transportation of products in real-time. This heightened transparency enables the companies to take proactive steps in reducing their carbon footprint and promoting eco-friendly practices across the automotive industry.

Empowering Suppliers with Efficiency and Accuracy

One of the most significant advantages of the SCEMS is the relief it brings to suppliers from time-consuming and costly carbon emission management. Leveraging the power of artificial intelligence (AI) and high-performance blockchain technology, this system empowers business partners to efficiently monitor and manage carbon emissions at their respective workplaces. By streamlining data collection and analysis, suppliers can now ensure compliance with environmental standards while optimizing their operations for a greener future.

Sustainable Practices for a Greener Tomorrow

Hyundai Motor and Kia Corporation's adoption of the SCEMS aligns perfectly with their vision for a sustainable future. As leaders in the automotive industry, both companies are committed to reducing their ecological impact and promoting responsible practices across their supply chains. By harnessing the potential of blockchain technology, they have taken a giant leap towards building a more sustainable and eco-conscious tomorrow.

Unlocking New Avenues of Innovation

The deployment of SCEMS on the Hedera mainnet opens up exciting possibilities for further innovation. As the system continues to gather invaluable data on carbon emissions and sustainability metrics, it lays the groundwork for future advancements in environmental management and clean technologies. This data-driven approach empowers researchers, policymakers, and automotive enthusiasts to collaborate on finding solutions to the most pressing environmental challenges.

Conclusion

Hyundai Motor and Kia Corporation's blockchain-based Supplier CO2 Emission Monitoring System (SCEMS) represents a monumental leap forward in the automotive industry's fight against climate change. By utilizing cutting-edge technology, they are leading the way in proactive carbon emission management and sustainable supply chain practices. As this revolutionary system continues to evolve and drive positive change, it brings us one step closer to a greener, cleaner, and more sustainable world. For more articles visit: Cryptotechnews24 Source: Cryptonews.net Image: The Coin Republic Read the full article

0 notes

Text

A Protected Farming Structure Maximizes Crop Yield and Profitability

Explore the world of protected farming structures and how they empower farmers at Shastram Plant Nursery to regulate environmental factors, ensuring year-round crop cultivation and enhanced profitability.

For More Information contact us: +91 97730 17705 Visit: https://bit.ly/3x24VKj

#ProtectedFarming#GreenhouseTechnology#CropYield#ProfitableFarming#ClimateControl#YearRoundCultivation#SustainableAgriculture#AgTech#FarmingInnovation#ShastramNursery#EnvironmentalRegulation#MaximizeProfit#CropManagement#ModernFarming

0 notes

Text

Industrial Noise Control Market Making Waves – Projected to Reach $7.5B by 2034! 🔊

Industrial Noise Control Market is expanding rapidly, driven by increasing industrialization, stringent environmental regulations, and a growing emphasis on workplace safety. This market includes solutions such as acoustic panels, silencers, enclosures, and barriers designed to mitigate noise pollution, enhance operational efficiency, and comply with regulatory standards. The demand for industrial noise control technologies is surging as industries prioritize employee health and sustainable practices.

To Request Sample Report : https://www.globalinsightservices.com/request-sample/?id=GIS22904 &utm_source=SnehaPatil&utm_medium=Article

The acoustic panels segment dominates the market, recognized for its effectiveness in reducing noise pollution in manufacturing and industrial environments. Acoustic enclosures are the second-largest segment, valued for their ability to contain noise at the source. Regionally, North America leads the market, benefiting from a strong regulatory framework and well-established industrial base. Europe follows closely, supported by governmental initiatives focused on reducing industrial noise pollution. Within these regions, the United States and Germany emerge as key players, given their advanced industrial infrastructures and commitment to noise mitigation solutions.

Market growth is further fueled by technological advancements and increased investments in research and development. In 2024, the market was estimated at 320 million units, with projections to reach 510 million units by 2028. Acoustic panels currently hold the largest market share at 45%, followed by silencers at 30%, and enclosures at 25%. The manufacturing sector is a significant driver of this demand, as industries seek to comply with noise regulations while improving workplace conditions. Major market players such as Saint-Gobain, Acoustical Surfaces, and IAC Acoustics are shaping the competitive landscape through innovative product offerings and global expansion strategies.

#industrialnoisecontrol #noisepollution #soundproofing #workplacesafety #acousticpanels #noisereduction #noisemitigation #soundbarriers #manufacturingindustry #constructiontech #sustainableindustry #acousticsolutions #occupationalhealth #environmentalregulations #industryinnovation #soundmanagement #acousticengineering #smartmanufacturing #greenbuilding #industrialacoustics #soundproofingtechnology #acousticinsulation #noisecancellation #safeworkplaces #constructionindustry #manufacturingtech #regulatorycompliance #transportationsector #oilgasindustry #powergeneration #foodprocessing #pharmaceuticalindustry #engineeringexcellence #industrialsolutions #silentoperations #acousticresearch #digitalnoisecontrol #noisemapping #noisemonitoring #infrastructuredevelopment #innovativetechnology #globalmarket #futureofindustry #sounddampening #smartconstruction #industrialdevelopment

0 notes

Text

Industrial Waste Management Market Poised for $1,800 Billion by 2034

Industrial Waste Management Market encompasses the collection, treatment, and disposal of waste generated by industrial activities. This sector includes services and technologies for managing hazardous and non-hazardous waste, recycling, and waste-to-energy solutions. It aims to minimize environmental impact while adhering to regulatory standards, thereby supporting sustainable industrial operations and promoting resource recovery.

To Request Sample Report : https://www.globalinsightservices.com/request-sample/?id=GIS21917 &utm_source=SnehaPatil&utm_medium=Article

The industrial waste management market is witnessing robust growth, driven by stringent regulations and increasing environmental awareness. The recycling segment leads the market, propelled by its cost-effectiveness and sustainability benefits. Waste-to-energy conversion emerges as the second-highest performing sub-segment, fueled by the need for alternative energy sources and efficient waste disposal methods. Hazardous waste management is also gaining traction due to heightened regulatory scrutiny and the necessity for specialized treatment solutions.

Regionally, North America dominates the market, supported by advanced waste management infrastructure and strong regulatory frameworks. Europe follows closely, with its focus on circular economy principles and waste reduction initiatives. Asia-Pacific is rapidly emerging as a key player, attributed to its industrial expansion and urbanization, which amplify waste generation. Within Asia-Pacific, China and India are the top-performing countries, driven by their large industrial bases and increasing governmental focus on sustainable waste management practices.

Market Segmentation

Type: Solid Waste, Liquid Waste, Sludge, Hazardous Waste, Non-Hazardous Waste

Product: Compactors, Shredders, Balers, Waste Containers, Recycling Equipment

Services: Collection, Recycling, Landfill, Incineration, Composting, Waste to Energy

Technology: Mechanical Biological Treatment, Advanced Thermal Treatment, Anaerobic Digestion, Pyrolysis, Gasification

Application: Manufacturing, Construction, Chemical Industry, Oil and Gas, Mining, Agriculture

Form: Powder, Liquid, Granular

Material Type: Metal, Plastic, Glass, Paper, Organic

Process: Sorting, Separation, Decontamination

End User: Municipal, Industrial, Commercial, Institutional

Equipment: Cranes, Conveyors, Loaders, Excavators

In 2024, the Industrial Waste Management Market handled approximately 2.5 billion metric tons of waste. The recycling segment dominates with a market share of 45%, driven by increasing environmental awareness and stringent regulations. Landfill holds 30%, while incineration accounts for 25%, reflecting a shift towards more sustainable waste management practices. The recycling segment’s prominence underscores a global trend towards circular economy models, where waste is viewed as a resource rather than a liability. Key players like Waste Management Inc., Veolia Environment, and Suez Environment hold significant shares, leveraging advanced technologies to optimize operations.

#industrialwastemanagement #recyclingindustry #wastetoenergy #sustainability #circulareconomy #environmentalprotection #wastemanagementsolutions #greenenergy #ecofriendly #wastereduction #hazardouswastemanagement #cleanenergy #renewableresources #urbanwastemanagement #industrialrecycling #zerowaste #resourceefficiency #greentechnology #industrialwaste #environmentalregulations #wasteinnovation #energymanagement #climateaction #wasteprocessing #sustainablemanufacturing #plasticrecycling #metalrecycling #wasteconversion #industrialcleanup #wastecollection #pollutioncontrol #renewablewaste #biodegradable #smartwastemanagement #circularsolutions #industrialgrowth #advancedwastetreatment #greenmanufacturing #environmentalsustainability #globalwastemanagement

0 notes

Text

"Biodegradable Industrial Lubricants Market to Grow from $3.8 Billion in 2024 to $7.2 Billion by 2034, with a 6.5% CAGR"

Biodegradable Industrial Lubricants Market is experiencing robust growth, driven by the rising demand for sustainable solutions across industries. These lubricants, derived from renewable sources, offer a natural breakdown in the environment, making them ideal for industries such as automotive, marine, and manufacturing. With increasing environmental regulations and a global focus on sustainability, biodegradable lubricants are becoming a key solution to minimize the environmental impact of traditional petroleum-based products.

To Request Sample Report: https://www.globalinsightservices.com/request-sample/?id=GIS10874 &utm_source=SnehaPatil&utm_medium=Article

The hydraulic fluids segment leads the market, accounting for 45% of the share, due to its widespread use in various industrial applications and eco-friendly attributes. Gear oils follow closely at 30%, with advancements in formulation that improve performance while reducing environmental impact. The demand for greases is also growing, driven by the need for eco-friendly alternatives in industrial machinery and construction.

Regionally, Europe stands at the forefront, with its strong industrial base and proactive environmental policies encouraging the adoption of biodegradable lubricants. North America follows, with growing adoption in sectors such as construction, agriculture, and manufacturing, largely due to regulatory compliance and sustainability goals. Countries like Germany and the United States are spearheading this transition, thanks to their technological advancements and commitment to reducing carbon footprints.

In 2023, the Biodegradable Industrial Lubricants Market reached a volume of 320 million liters, with projections to grow to 500 million liters by 2033. Key players in the market include ExxonMobil, Shell, and TotalEnergies, who are leading innovation with advanced formulations and sustainable sourcing. As the market expands, technological advancements, eco-innovation, and a commitment to sustainability will continue to shape the industry’s future.

#BiodegradableLubricants #SustainableLubricants #EcoFriendlySolutions #HydraulicFluids #GearOils #Greases #SustainableManufacturing #GreenTech #EcoInnovation #EnvironmentalRegulations #RenewableEnergy #CarbonFootprintReduction #SustainableIndustry #CleanEnergy #EcoFriendlyProducts #EnvironmentalImpact #CircularEconomy #GreenManufacturing #SustainableFuture #TechInnovation #ClimateAction

0 notes

Text

Here’s a compilation of the ten most pressing challenges facing the trucking industry today. It’s crucial that we bring these issues into the conversation and engage in meaningful discussions to explore potential solutions. While some of these problems are often overlooked, others receive attention; however, we must unite and address each of these concerns collectively.

1. Driver Shortage: A significant lack of qualified drivers continues to challenge the industry, impacting delivery capabilities.

2. Low Pay: Many drivers feel that compensation does not reflect the demands of the job, especially with long hours and time away from home.

3. Rising Fuel Costs: Fluctuating fuel prices can take a considerable toll on operating expenses.

4. Regulatory Compliance: Keeping up with complex regulations, including hours of service and electronic logging requirements, can be burdensome.

5. Supply Chain Disruptions: Various factors, including global events, can lead to delays and increased costs.

6. Maintenance and Repair Costs: Expenses for maintaining trucks can be high, and unexpected repairs can lead to downtime.

7. Technology Adoption: While beneficial, integrating new technologies can be costly and requires time for training.

8. Insurance Costs: Rising insurance premiums are an ongoing concern for trucking companies.

9. Environmental Regulations: New regulations focused on reducing emissions can increase operational costs.

10. Working Conditions: Long hours, time away from home, and a lack of adequate rest facilities can affect driver well-being.

If you want to dive deeper into any specific problem, don’t hesitate to ask!

😮🚛💨🔩💰🔧🚧🦺⚖️📉🙏🔨📎👋

1. #TruckingIndustry

2. #TruckingProblems

3. #DriverShortage

4. #LowPay

5. #FuelCosts

6. #SupplyChainIssues

7. #DriverSafety

8. #LongHours

9. #TruckMaintenance

10. #RegulatoryCompliance

11. #InsuranceCosts

12. #TechnologyInTrucking

13. #EnvironmentalRegulations

14. #FreightWages

15. #TruckerLife

16. #LogisticsChallenges

17. #Haulage

18. #RoadSafety

19. #TruckDriverStruggles

20. #TruckingCommunity

1 note

·

View note

Text

MRU Instruments- Applications and Uses of Multifunctional Manometer

Basically, a manometer is used to measure the pressure and that pressure exerted by still liquid or gas. It relies on the hydrostatic equilibrium in which the pressure at any particular point in a fluid at rest is due to the actual weight of the overlying fluid.

Applications:

It is a powerful tool that can be used for pressure monitoring applications in processing industries.

It can also be used to monitor the air and gas pressure of the compressor.

A manometer can be used to measure the static pressure and vacuum pressure.

Mercury absolute manometers are mostly employed in power plants.

Uses:

If you want to directly measure pressure values, you can use a multi-functional manometer. Pressure measurements can be utilized to determine flow rates, fluid levels, product density, and other parameters around various industries, measuring the pressure of a material is a crucial part of the processing industry. Getting accurate and defined data is important in determining the quality and consistency of the particular product which can be achieved with high-quality products with MRU Instruments.

#MRUInstruments#multi-functional manometer#gas detection instruments#oilandgas#petroleum#EnvironmentalRegulations#small hand-held devices

3 notes

·

View notes

Text

Trump's Words Could Jeopardize His Environmental Rollbacks, Too

Generally, environmental regulations can’t be killed with the stroke of the president’s pen. Instead the administration must undertake the same rulemaking process used to create regulations to undo them. And that process can’t be "arbitrary and capricious" -- the bright line standard established in the 71-year-old Administrative Procedure Act that governs federal rulemaking.

In practice, that means agencies must provide a good explanation for rescinding a regulation -- by demonstrating the factual, legal and policy justifications. They also must stick to the considerations laid out in the legislation. For instance, that means they can’t weigh cost when determining how stringent to make ozone standards because the Supreme Court has unanimously found that those considerations weren’t in the original statute.

#Trump #EnvironmentalRegulation #USPolitics

https://www.bloomberg.com/news/articles/2017-03-22/trump-s-words-could-jeopardize-his-environmental-rollbacks-too

2 notes

·

View notes