#depreciation tax

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

The average Tumblr user visits about 67 pages every month.

Text

Here's a hypothetical: What if you won the lottery tomorrow? You get 10 million dollars to spend; however you wish. What would you do with that amount of money?

Personally, I'd buy a house, invest 1 million, give 2 million to my family, and then use the remaining 7 million for charity.

at a 4% quarterly interest rate, I'd make 120k a year just off my investments, which is twice the average income in my city. and I wouldn't have any debt, or have to make payments on a house or for rent. I'd be very very rich by anyone's standards.

With the remaing 7 mil, I'd donate a bunch of money to local queer organizations that have impacted my life heavily. I'd also give a bunch to some local food banks and housing programs, and give a bunch to rainbow railroad. that 7 million could probably have a huge impact on the lives of a ton of people.

Jeff bezos has a net worth of 208.7 billion dollars, over 2000 times bigger than our hypothetical amount.

Is that ethical? is it ok, morally, to sit on that much money, when it could do so much good?

What would you do, if tommorow, you had 208,700,000,000 dollars?

#socialism#wealth gap#jeff bezos#tumblr#i know that the 208.7 billion is in stocks#but you can sell stocks!#he probably couldnt immediately sell them all#and hed probably end up with less than that after taxes and depreciation etc#but hed still have a fuck ton of money

4 notes

·

View notes

Text

The Role Of Depreciation In Business Tax Planning

Depreciation plays a key role in business tax planning by allowing companies to deduct the cost of assets over time, reducing taxable income. This helps improve cash flow and tax savings. Experts offering tax planning for small business owners in Fort Worth, TX can assist in maximizing depreciation benefits, ensuring compliance while optimizing deductions to boost overall financial health and stability.

0 notes

Text

3 Types Of Depreciation Methods To Reduce Property Tax! - Cut My Taxes

Do you know depreciation has a tax impact? It is used to calculate the cost value of any property. Read here to know the depreciation methods https://www.cutmytaxes.com/3-types-of-depreciation-methods-to-reduce-property-tax/

0 notes

Text

Cannabis tax compliance: planning for potential rescheduling

Michael D. Harlow, CPA, Managing Partner – Cannabis Industry, Office and Travis Butler, CPA, Incoming Partner, CohnReznick As in many areas, people across the cannabis industry are wondering: What does the changing administration mean for my business? This area is still broadly unpredictable, as much will depend on who is chosen for the Cabinet and where they stand on cannabis. The DEA hearing to…

#depreciation#IRS 280E tax code#R&D credit#Rescheduling#taxes#Uniform Capitalization Rules (UNICAP)

0 notes

Text

Cost segregation is a technical process where short-life items are separated from long life items. It typically doubles or triples depreciation during the first five years of ownership. https://www.whatiscostsegregation.com/

#component depreciation#o'connor tax reduction experts#cost segregation real estate calculator#cost segregation study calculator

0 notes

Text

Owning rental property offers several financial advantages, but one of the most compelling reasons to invest in real estate is the numerous tax benefits it provides. Whether you are a seasoned investor or a first-time property owner, understanding these tax advantages can significantly improve your profitability.

0 notes

Text

Tax Planning for Companies: How to Utilize Depreciation and Amortization

Depreciation and amortization are essential tax planning tools that companies can use to reduce taxable income and improve cash flow. These accounting methods allow businesses to allocate the cost of assets over time rather than expensing them in a single year. Properly utilizing depreciation and amortization can lead to significant tax savings, making them integral components of an effective tax strategy.

Understanding Depreciation and Amortization

Both depreciation and amortization are methods of expensing the cost of long-term assets. However, they apply to different types of assets:

Depreciation: This applies to tangible assets like machinery, buildings, and equipment. Depreciation spreads the cost of these assets over their useful life.

Amortization: This applies to intangible assets such as patents, trademarks, and goodwill. Like depreciation, amortization allocates the cost of these intangible assets over their estimated useful life.

Both depreciation and amortization reduce taxable income by recognizing the expense over time, rather than when the asset is purchased.

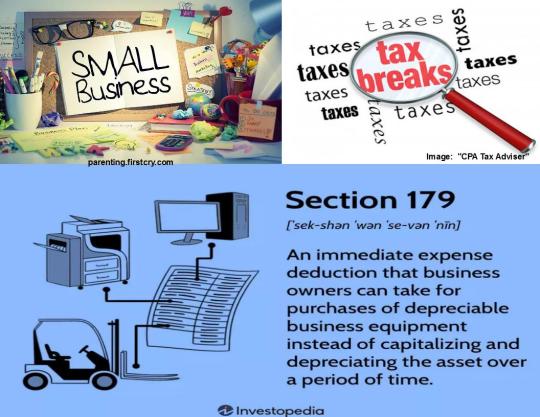

Accelerating Depreciation with Section 179 and Bonus Depreciation

In many cases, businesses can accelerate depreciation through Section 179 deductions and bonus depreciation. These options allow companies to write off a larger portion of an asset’s value in the first year, providing immediate tax relief.

Section 179: This provision allows businesses to deduct the full cost of qualifying assets (such as equipment or software) in the year they are placed in service, up to a specified limit. For 2024, the limit is $1,160,000, with a phase-out threshold of $2.89 million. Section 179 is particularly beneficial for small and medium-sized businesses that invest heavily in equipment or technology.

Bonus Depreciation: Under the Tax Cuts and Jobs Act (TCJA), businesses can take advantage of 100% bonus depreciation on qualifying assets (new or used) placed in service. This allows businesses to deduct the entire cost of the asset in the first year. This provision is temporary, and scheduled to phase out over the next few years, so businesses should act quickly to maximize their deductions.

Using both Section 179 and bonus depreciation, businesses can reduce their taxable income substantially in the year of purchase, freeing up cash for other investments or operational expenses.

Utilizing the Straight-Line Method for Long-Term Assets

For assets that don’t qualify for accelerated depreciation methods, companies often use the straight-line depreciation method, which spreads the cost evenly over the asset’s useful life. This method provides predictable and stable deductions year after year. It is particularly useful for assets like buildings or property that have a long useful life, ensuring companies can reduce their taxable income consistently over time.

Amortization of Intangible Assets

Intangible assets, such as patents, trademarks, and copyrights, can also be amortized over their useful life. Unlike depreciation, which can be calculated using multiple methods, amortization is generally done using the straight-line method. By amortizing intangible assets, businesses can deduct a portion of their investment annually, reducing taxable income without affecting cash flow.

For example, if a company purchases a patent for $500,000 with a 10-year useful life, it would be able to deduct $50,000 each year for 10 years. This ongoing deduction provides tax benefits while the asset continues to contribute to the business.

Strategic Tax Planning with Depreciation and Amortization

To optimize tax savings, companies should strategically plan the timing and selection of depreciation and amortization methods. For example, by combining accelerated depreciation in the first few years with straight-line depreciation afterward, businesses can balance short-term tax relief with long-term savings. Additionally, when purchasing new assets, companies should evaluate the benefits of Section 179 and bonus depreciation to maximize immediate deductions.

Keeping Accurate Records and Compliance

Proper documentation is crucial when utilizing depreciation and amortization for tax purposes. Companies should keep detailed records of their assets, including purchase prices, dates of acquisition, and estimated useful lives. Regularly reviewing depreciation schedules with the experts offering tax planning for companies in Fort Worth, TX ensures that companies remain compliant with tax laws and avoid any potential audits or penalties.

Conclusion

Depreciation and amortization are powerful tools for tax planning, allowing businesses to reduce their taxable income and increase cash flow. By strategically using accelerated depreciation methods like Section 179 and bonus depreciation, as well as implementing regular amortization for intangible assets, companies can significantly lower their tax burden. Proper record-keeping and expert guidance from are essential to ensuring compliance and maximizing these tax-saving opportunities.

0 notes

Text

Maximizing Depreciation Deductions for Your Trucking Business with a Tax Expert

In the trucking industry, equipment such as trucks, trailers, and other vehicles is a significant investment. One way to ease the financial burden of these capital expenditures is by utilizing depreciation deductions, which allow businesses to recover the cost of these assets over time. However, maximizing these deductions requires a solid understanding of tax laws and proper record-keeping. This is where a tax expert specializing in trucking can help. Working with a tax expert ensures that your depreciation deductions are optimized, providing substantial financial benefits.

Understanding Depreciation for Trucks and Equipment

Depreciation allows trucking businesses to deduct a portion of the cost of their trucks and equipment each year, reflecting the wear and tear that occurs over time. The IRS allows different methods for calculating depreciation, such as the Modified Accelerated Cost Recovery System (MACRS). Under MACRS, vehicles like trucks fall into a 5-year depreciation class, meaning you can write off a portion of the truck's value annually for five years.

A tax expert familiar with trucking industry specifics can help determine the most efficient depreciation method for your business. They will ensure that you choose the method that offers the greatest financial advantage based on your business's needs.

Bonus Depreciation

A significant tax benefit that trucking businesses can leverage is bonus depreciation. Under recent tax laws, businesses can deduct a large portion of an asset's cost in the first year it is placed into service. As of recent tax reforms, businesses can claim 100% bonus depreciation on qualified assets, including new and used trucks, for a limited time.

A tax expert will help you navigate these rules to ensure that you maximize the first-year deduction. This upfront savings can be particularly beneficial for trucking companies that purchase or lease multiple vehicles in a single year. By claiming bonus depreciation, you can significantly reduce your taxable income, leaving more cash flow available for operating expenses or further investments.

Section 179 Deduction

Another useful tax tool is the Section 179 deduction, which allows businesses to deduct the full purchase price of qualifying equipment in the year it is purchased, subject to certain limits. For trucking companies, this means that if you purchase a truck or other qualifying equipment, you could potentially deduct the entire cost (up to a limit) right away, instead of spreading the deduction over multiple years.

However, Section 179 has specific rules, including annual deduction limits, phase-out thresholds, and a requirement that the equipment must be used more than 50% for business purposes. A tax expert can ensure that your business qualifies for the maximum allowable Section 179 deduction, while also considering how this interacts with bonus depreciation and other deductions.

Keeping Accurate Records

To take full advantage of depreciation deductions, accurate records are essential. This includes keeping track of the purchase price, dates of acquisition, and usage percentage of your trucks and equipment. A tax expert can help ensure that these records are organized and up to date, reducing the risk of errors and simplifying the process if you are audited by the IRS.

Strategic Depreciation Planning

A tax expert will also assist in strategic planning, helping you determine the best timing for purchasing or selling assets. By analyzing your business's cash flow, tax situation, and plans, a tax professional can guide you on how to structure your purchases to maximize tax savings. They can also advise on how to handle disposals of assets to avoid unexpected tax consequences.

Conclusion

Maximizing depreciation deductions for your trucking business can provide significant financial relief, but it requires careful planning and expert knowledge. Working with a tax expert offering tax services for truck drivers ensures that you take full advantage of available tax benefits like MACRS, bonus depreciation, and Section 179. By keeping accurate records and strategically planning your depreciation strategy, you can minimize your taxable income, improve cash flow, and invest more in your business’s growth.

0 notes

Text

Navigating Tax Deductions for Home-Based Businesses: A Personal Guide

If you're running a home-based business, you're likely aware that managing your finances and taxes can be both exciting and daunting. One of the silver linings of this journey is the opportunity to leverage tax deductions that can significantly reduce your taxable income. As someone who’s navigated these waters firsthand, I’m here to share some personal insights and practical tips to help you make the most of those deductions.

1. Understand What Qualifies as a Home-Based Business

First things first—let’s clarify what constitutes a home-based business. Generally, if you’re running a business from your home, whether it’s a full-time gig or a side hustle, you’re eligible for certain tax deductions. The key is that your home must be used regularly and exclusively for business purposes.

2. The Home Office Deduction

One of the most talked-about deductions is the home office deduction. To qualify, your workspace must meet two criteria:

Regular Use: The space must be used consistently for business activities.

Exclusive Use: It should be set aside specifically for business—your dining room doesn’t count unless it’s exclusively for work.

There are two methods for claiming this deduction:

Simplified Method: You can deduct $5 per square foot of your home office, up to 300 square feet. This method is straightforward and requires less paperwork.

Regular Method: This involves calculating the actual expenses related to your home office. You’ll need to determine the percentage of your home used for business and apply this percentage to various expenses like mortgage interest, utilities, and repairs.

3. Deducting Business Expenses

Business expenses that are necessary and ordinary can be deducted. These include:

Utilities and Internet: You can deduct a portion of your utility bills and internet service if they are used for business purposes. Keep detailed records of these expenses and be prepared to justify their business use.

Supplies and Equipment: Office supplies, computers, printers, and other equipment are deductible. If you purchase a significant piece of equipment, like a high-end computer, you might need to depreciate it over several years.

Professional Services: Fees paid to accountants, consultants, and other professionals related to your business can be deducted. Make sure to keep all invoices and receipts.

4. Travel and Meals

When you travel for business, you can deduct expenses such as airfare, lodging, and even a portion of your meals. However, there are some rules:

Travel: The travel must be primarily for business. If you mix business with pleasure, you can only deduct expenses related to the business portion of your trip.

Meals: You can typically deduct 50% of meal costs if they are directly related to business activities. This includes meals with clients or business meetings.

5. Vehicle Expenses

If you use your vehicle for business, you can deduct expenses in one of two ways:

Standard Mileage Rate: Multiply the miles driven for business by the IRS standard mileage rate (which changes annually).

Actual Expenses: Deduct the actual costs associated with using your vehicle for business, such as gas, oil changes, and maintenance. This method requires detailed record-keeping.

6. Home Depreciation

If you own your home, you can potentially deduct depreciation on the portion of your home used for business. This is a more complex area, and it’s crucial to consult with a tax professional to ensure you’re calculating this correctly and understanding its implications, especially since it could affect the sale of your home.

7. Consult a Tax Professional

While this guide provides a starting point, consulting a tax professional can help ensure you’re taking full advantage of all possible deductions and complying with tax laws. They can provide personalized advice based on your specific business situation.

0 notes

Text

UPDATE Small Business Instant Depreciation Tax Break Increase

The Section 179 deduction for 2024 is $1,220,000, which is an increase of $60,000 from 2023’s limit. This means U.S. companies can deduct the full purchase price of ALL qualified equipment purchases, up to the limit of $1,220,000. In addition, the “total equipment purchase” limit has been raised to $3,050,000 (up from $2.89 million in 2023).

View On WordPress

0 notes

Text

https://www.expertcostseg.com/cost-segregation-case-study/

An IRS-approved technique that functions well in all 50 states is cost segregation. Building depreciation allocations through cost segregation result in savings. Visit https://www.expertcostseg.com/cost-segregation-study-results-city/ to learn more.

0 notes

Text

Maximize deductions and royalties in the printing and publishing industry with effective tax strategies. Learn how printing equipment depreciation and optimized royalties can minimize tax liabilities and boost profitability. #Printing #Publishing #TaxStrategies #Depreciation #Royalties

1 note

·

View note

Text

The Role Of Depreciation In Business Tax Planning

Depreciation is a key concept in business tax planning, providing companies with an opportunity to lower their taxable income by allocating the cost of assets over their useful life. For businesses, understanding and leveraging depreciation can be a valuable tool for reducing tax liability while ensuring compliance with IRS rules.

What is Depreciation?

Depreciation refers to the process of deducting the cost of a tangible asset over its expected useful life. Commonly depreciated assets include equipment, machinery, buildings, and vehicles. Instead of writing off the full cost of an asset in the year it was purchased, businesses can deduct a portion of its value each year. This allows businesses to reflect the gradual wear and tear of these assets while simultaneously reducing their taxable income.

Why is Depreciation Important in Tax Planning?

For businesses, depreciation offers several benefits in tax planning:

Tax Deductions: Depreciation provides annual deductions that reduce taxable income, lowering the business’s overall tax liability. This can result in substantial tax savings, especially for companies with significant investments in assets.

Cash Flow Management: The depreciation deduction is non-cash, meaning it doesn’t affect a company’s cash flow directly. By lowering taxes, it frees up cash that can be reinvested into the business or used to cover other operational costs.

IRS Compliance: Businesses must adhere to the IRS’s rules regarding depreciation schedules and methods. Failure to properly apply depreciation could lead to penalties or missed opportunities for tax savings.

Methods of Depreciation

There are several methods for calculating depreciation, and businesses must choose the one that best aligns with their needs:

Straight-Line Depreciation: This method spreads the cost of the asset evenly over its useful life. It is simple and predictable, making it the most commonly used method.

Declining Balance Method: This method accelerates the depreciation process, allowing businesses to deduct a higher amount in the earlier years of an asset's life. This can be particularly beneficial for businesses looking to maximize deductions in the short term.

Section 179 Deduction: Under Section 179 of the IRS tax code, businesses can expense the full cost of certain qualifying assets in the year of purchase, up to a specific limit. This provides an immediate tax deduction but is subject to certain restrictions.

Strategic Use of Depreciation

To make the most of depreciation, businesses need a strategic approach to planning. This means not only applying the right depreciation method but also managing the timing of deductions to align with the company’s financial and tax situation.

For instance, a business in a high-revenue year may benefit from using accelerated depreciation to reduce its tax bill. Conversely, businesses anticipating lower revenue may prefer to spread deductions evenly over time. Understanding how depreciation affects the overall tax strategy requires careful forecasting and analysis.

The Role of Experts in Strategic Business Tax Planning

While depreciation is an essential part of tax planning, it can be complex, especially when considering the many variables that can influence tax outcomes. Experts offering services in strategic business tax planning in Fort Worth, TX can guide businesses through the process of selecting the right depreciation methods, timing deductions appropriately, and ensuring compliance with all applicable regulations. These professionals help optimize the tax strategy, ensuring businesses take full advantage of available deductions while avoiding common pitfalls.

In conclusion, depreciation is a powerful tool in business tax planning. By strategically utilizing depreciation methods, businesses can reduce their taxable income, manage cash flow, and maximize tax savings. Engaging with tax planning experts can further refine this process, ensuring businesses leverage depreciation to their fullest advantage while staying in compliance with tax laws.

0 notes

Text

Navigating Tax Considerations for Commercial Property Owners in 2024

View On WordPress

#1031x#2024#beilercampbellcommercial#commercial property#Commercial Real Estate#CRE#CREi#depreciation#deprectiation#financial#investing#investments#opportunity zones#property ownership#tax assessments#tax credits#tax season#tax time#taxes

1 note

·

View note

Text

((Uh, no it doesn't! Lol))

0 notes

Text

Bonus depreciation takes many forms, including Section 179 depreciation. There have been scores of depreciation programs that give property owners additional depreciation since the Tax Code was introduced in 1913. Of course, additional depreciation increases expenses, with a non-cash expense. https://www.bonusdepreciationcalculator.com/

#Cost segregation study#component depreciation#o'connor tax reduction experts#cost segregation real estate calculator

0 notes