#asset rich cash poor solutions

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has a low social media market share in South America.

Text

Put Offer In - Waiting For Outcome on Cafe Venue

It’s Friday 1st November and I just put an offer in for a cafe venue in Falmouth. Apparently I might hear back tomorrow. It is exciting whatever the outcome. I’m trying to stop myself getting too attached to this venue as there are more. However, very few have big windows facing the harbour and views beyond. Firstly, I got out the spreadsheet given to me by Oxford Innovation. From the accounts I…

#asset rich cash poor solutions#Becoming a new business owner#buying your first real business#creating a social hub#female business strategy#finding a purpose#gathering information#implenenting new ideas#lifestyle business#lifestyle business ownership#making savings and efficiencies#marketing strategy and implementation#nuts and bolts#nuts and bolts of running a business#Ongoing concern#planning to take a leap into business ownership#running a team#seed network#side hustle#starting a business#taking on a retail or online business#team leadership#teamwork

0 notes

Text

Unlock Quick Cash with Your Property: Apply for an Instant Loan Against Property

Struggling to Get a Loan Without Salary Slips or ITR? Here’s Your Solution

Have you been rejected for a personal loan just because you don’t have proof of income? You’re not alone. Thousands of self-employed individuals, shopkeepers, and small business owners in India face this every day. But there's good news — you can still get an instant loan using your property. It’s called a Loan Against Property (LAP), and yes, you don’t need income proof to get started.

What Is an Instant LAP Loan & Why Everyone’s Talking About It

A Loan Against Property (LAP) is a secured loan using property as collateral. You pledge your owned residential or commercial property and get a loan up to 75% of its market value. It’s one of the easiest ways to raise large funds without selling your assets.

You can use the funds for any purpose — from expanding your business to handling personal emergencies. It’s an ideal mortgage loan for personal or business use.

No Income Proof? No Problem! Here's How You Can Still Qualify

Many people ask, “Can I get a LAP without salary slips or ITR?” The answer is YES! Lenders now offer LAP for the self-employed without ITR or formal income documents. They evaluate your repayment ability through property value and alternative income proofs.

You can show:

Business turnover

Rental income

Bank statement patterns

This makes it a game-changer for India’s vast self-employed and informal sector.

Who Can Apply for a LAP Without Income Proof?

You are eligible if you:

Are between 21 to 65 years old

Own a residential or commercial property with a clear title

Have a basic credit profile (score not mandatory for all lenders)

The criteria to qualify for LAP are flexible, especially on digital lending platforms.

Property Rich but Cash Poor? Convert Real Estate into Liquid Money

If you’ve got property but need urgent funds, why not use it smartly? A loan against residential or commercial property helps you unlock its value without selling it.

Choose a residential property with lower interest rates. Go with a commercial for higher valuation. Both are accepted by most banks and NBFCs.

What’s the Interest Rate for LAP in India Right Now?

Comparing current mortgage loan interest rates in India is key to making the right choice. Here's a quick table:

Compare these best interest rates on loans against property to find your perfect match.

Plan Your Loan: Use the LAP EMI Calculator

Before applying, use a monthly repayment calculator for LAP. It helps you:

Estimate your monthly EMI

Choose the right loan tenure

Avoid repayment stress

Online calculators are available on most lender websites.

Need Money Fast? Get Quick LAP Disbursal Without Hassle

Emergencies don’t wait. Whether it’s a medical issue or an urgent investment, you need funds quickly. Many lenders now offer quick disbursal LAP for urgent needs, with approvals in 24-72 hours.

Apply online, upload documents, and get your loan processed without stepping into a branch.

100% Online Application: How to Apply for LAP Digitally

No branch visits. No queues. You can now apply for LAP through digital platforms:

Visit the lender's website

Fill online form

Upload KYC and property documents

Get a verification call and approval

Receive funds in your account

Fast, paperless, and secure!

Real Story: How LAP Helped a Small Business Grow

Reema, a boutique owner from Pune, needed funds to expand before the wedding season. With no ITR or salary slips, she used her shop space to get a LAP loan. The entire process took just 3 days. Her sales doubled that month.

This is the power of LAP, especially when you don’t have traditional income documents.

Documents You’ll Need (Minimum Paperwork)

Aadhaar and PAN card

Property documents

Passport-sized photo

Any alternate income proof (if available)

Minimal hassle, maximum outcome.

FAQs

1. Can I get LAP without income documents? Yes. Many lenders approve LAP based on property value and bank statements, without ITR or salary slips.

2. Which property can I use for LAP? You can use residential, commercial, or even rented property, depending on the lender’s policy.

3. How fast is LAP disbursed? Some NBFCs offer disbursal within 24-48 hours, especially for online applications.

4. Do I need a high credit score? Not necessarily. A decent score helps, but some lenders consider property value more than credit score.

5. Can I close the LAP before tenure ends? Yes, most lenders allow part-payment or full closure with little or no penalty after 6-12 months.

Final Takeaway: Don’t Let Documents Delay Your Dreams

A loan against property without income proof is not just a financial product — it’s an opportunity. If you own property, why wait? Turn your real estate into liquid capital, solve your financial needs quickly, and move forward without the burden of heavy documentation.

Apply today and take control of your financial freedom!

#secured loan using property as collateral#mortgage loan for personal or business use#current mortgage loan interest rates in India#monthly repayment calculator for LAP#criteria to qualify for LAP#best interest rates on loan against property#LAP for self-employed without ITR#loan against residential or commercial property#quick disbursal LAP for urgent needs#apply for LAP through digital platforms

0 notes

Text

Why Business Families Struggle With Liquidity?

Introduction

Business families have historically contributed significantly to wealth creation, employment, and economic growth. However, many struggle with liquidity despite having substantial wealth. Liquidity refers to the ability to access cash or easily convertible assets, which is essential for sustaining operations, fueling growth, and handling unexpected financial challenges. Unfortunately, business families often find themselves asset-rich but cash-poor, limiting their financial flexibility.

This article explores why business families face liquidity challenges, covering factors such as concentrated wealth in illiquid assets, emotional business ties, succession planning, tax burdens, and economic downturns. We will also discuss strategic solutions to improve liquidity management.

1. Wealth Locked in Illiquid Assets

Business families frequently have most of their wealth tied up in real estate, privately held business equity, and legacy assets, limiting access to liquid funds.

Key Factors:

Private Ownership: Unlike publicly traded companies, family businesses have restricted share trade options.

Asset-Heavy Investments: Capital is often invested in land, equipment, and facilities, reducing cash availability.

Limited External Financing: Many lenders hesitate to fund family businesses with unpredictable cash flow.

2. Emotional Business Attachment

Family businesses are often more than financial assets; they carry emotional and generational significance, making liquidity-related decisions complex.

Consequences:

Unwillingness to Sell: Owners resist selling assets or shares even when financially necessary.

Legacy Preservation Over Liquidity: Maintaining family control takes precedence over financial flexibility.

Unwise Investments: Emotional choices may lead to investments that do not generate liquidity.

3. Succession Planning and Liquidity Struggles

Transferring leadership and ownership across generations can create liquidity challenges if not planned properly.

Key Issues:

Buyout Burdens: Retiring family members often require significant payouts, straining liquidity.

Inheritance Conflicts: Disputes over ownership can drain financial resources and delay liquidity decisions.

Lack of Structured Planning: Poor financial planning during transitions leads to sudden liquidity crises.

4. Tax Liabilities Impacting Liquidity

Family businesses face significant tax burdens during ownership transitions and asset sales, affecting cash flow.

Major Tax Challenges:

Estate and Inheritance Taxes: Transferring wealth across generations can lead to high tax obligations, forcing asset sales.

Capital Gains Tax: Selling assets for liquidity may trigger substantial tax payments, reducing net cash flow.

Poor Tax Planning: Without proper tax strategies, families may face unexpected financial stress.

5. Economic Downturns and Market Volatility

Economic downturns, industry shifts, and recessions can create unexpected liquidity challenges for family businesses.

Effects of Market Instability:

Revenue Declines: Reduced consumer spending leads to lower income and restricted cash flow.

Debt Burden Increases: Economic downturns make it harder to meet existing debt obligations.

Difficult Fundraising: Lenders and investors become hesitant to support struggling businesses.

6. Generational Financial Priorities Differ

Different generations within a family business may have conflicting financial priorities, impacting liquidity management.

Key Conflicts:

Conservative vs. Growth Strategies: Older members focus on stability, while younger ones seek expansion.

Profit Reinvestment vs. Payouts: Differing views on reinvesting profits or distributing dividends.

Varied Risk Appetite: Generational gaps create inconsistent liquidity approaches.

7. Weak Financial Governance

Many family businesses lack formal financial governance structures, making liquidity management inconsistent.

Governance-Related Issues:

Unstructured Decision-Making: Unclear financial leadership leads to erratic cash flow management.

Financial Opacity: Poor record-keeping obscures true liquidity positions.

No Defined Liquidity Plan: Cash reserves can be depleted without a replenishment strategy.

8. Over-Reliance on Debt Financing

Excessive debt usage can lead to liquidity struggles, especially during downturns.

Debt-Related Risks:

High Interest Payments: Reduces available cash for operations.

Restrictive Loan Covenants: Lenders impose conditions that limit financial flexibility.

Potential Defaults: Failure to meet debt obligations can trigger liquidity crises.

Strategies for Improving Liquidity

Despite these challenges, business families can take steps to strengthen their liquidity position.

1. Diversifying Investments

Holding liquid assets like stocks, bonds, and reserves provides financial flexibility.

Exploring new revenue streams can reduce reliance on a single business.

2. Implementing Strong Financial Governance

Establishing clear liquidity policies ensures structured cash flow management.

Conducting regular financial audits increases transparency.

3. Improving Succession and Tax Planning

Structured succession planning prevents liquidity crises during leadership changes.

Tax-efficient wealth transfer strategies help reduce financial burdens.

4. Maintaining Emergency Reserves

Setting aside contingency funds helps businesses survive downturns.

Accessing credit lines as backup liquidity ensures stability.

Conclusion

Business families face liquidity challenges due to wealth concentration in illiquid assets, emotional decision-making, succession complexities, tax burdens, economic downturns, governance gaps, and debt dependency. However, strategic financial planning, governance improvement, and investment diversification can enhance liquidity management, ensuring long-term financial stability.

By addressing these challenges, family businesses can safeguard both their legacy and financial health for future generations.

1 note

·

View note

Text

How To Make $10,000 Fast As A Student – Easy Ways To Make Money While Studying https://ift.tt/teYBaLG https://www.youtube.com/watch?v=Sp7krX8_TUs How to Make $10,000 as a Student: Side Hustles and High-Income Skills | #makemoney Want to earn $10,000 while balancing classes? In this video, I’ll show you the top side hustles and high-income skills that can help students make money fast. These strategies can help you earn extra cash while building valuable skills, from tutoring to freelancing and marketing yourself. Don’t forget to like, subscribe, and share if you found these tips helpful. Let’s achieve financial freedom together! This video is about How To Make $10,000 Fast As A Student – Easy Ways To Make Money While Studying. But It also covers the following topics: Top Side Hustles For Students Best Student Jobs For Extra Cash Make Extra Money Fast As A Student Stay Connected With Us. Want to achieve financial freedom? Subscribe for comprehensive budgeting tips, investment insights, fun financial challenges, and money-saving hacks. https://www.youtube.com/@Money-Minds-Mastery99/?sub_confirmation=1 ============================= Important Links to Follow Secure Crypto Trading: Ensure your trades are safe and efficient. https://ift.tt/RxumbDF Advanced Trading Tools: Enhance your trading strategy with these tools. https://ift.tt/USOqQtf Reliable Crypto Wallet: Protect your assets with this secure wallet. https://ift.tt/VfvNnP4 Market Analysis Platform: Access in-depth market analysis. https://ift.tt/QENbsnI Crypto Trading Course: Learn to trade like a pro. https://ift.tt/xM7I3f2 Real-Time Trading Alerts: Get timely trading alerts to stay ahead. https://ift.tt/Op4CUTM Investment Strategies: Explore diverse investment strategies. https://ift.tt/YnO1wUB Crypto Portfolio Tracker: Easily track your portfolio. https://ift.tt/OH4eMvD Comprehensive Market Insights: Get the latest market insights. https://ift.tt/sairRWF DeFi Platform: Engage in decentralized finance. https://ift.tt/xqBkW4b Crypto Tax Solutions: Simplify your crypto taxes. https://ift.tt/ZSGKhNj Crypto Staking Service: Earn rewards by staking your crypto. https://ift.tt/U5xAr9C Expert Trading Signals: Receive expert trading signals. https://ift.tt/2DEpBq6 Educational Crypto Course: Master crypto trading with this course. https://ift.tt/sWGa1VA Top Exchange Platform: Trade on a reliable exchange. https://ift.tt/H4RBn3d Crypto Investment Guide: Learn how to invest in crypto effectively. https://ift.tt/GZA4sgq Secure Wallet: Keep your crypto safe. https://ift.tt/IhcoU7T Recommended Playlist Cryptocurrency https://www.youtube.com/playlist?list=PLLJJ6S5qrEZgSQ4cqfSYBiFvlutoe8Q2i WATCH OUR OTHER VIDEOS: How to Take Control of Your Finances: 10 Essential Financial Tips | MoneyMinds Mastery https://www.youtube.com/watch?v=28vfSWZdFcw 10 Secrets To Wealth: How The Rich Keep Getting Richer | MoneyMinds Mastery https://www.youtube.com/watch?v=ebV3Vj4Cvdg&t=45s 10 Easy Budgeting Hacks For Beginners To Save Money Fast (No Boring Tips!) | MoneyMinds Mastery https://www.youtube.com/watch?v=6QtrrwjSBLQ&t=52s 10 Powerful Assets To Grow Your Wealth Quickly: Financial Freedom Tips! | MoneyMinds Mastery https://www.youtube.com/watch?v=OO71KaOCD2w&t=20s 10 Money Wasting Habits Poor People Have That Rich People Avoid | MoneyMinds Mastery https://www.youtube.com/watch?v=CRCfAvcYDO4&t=19s ============================= #makemoney #studenthustle #earnextra #highincomeskills #sidehustles #studentlife © MoneyMinds Mastery from MoneyMinds Mastery https://www.youtube.com/channel/UCouqbXaGeyniezuDNQIXH8w via MoneyMinds Mastery https://ift.tt/SMKJ06X November 06, 2024 at 03:28PM

0 notes

Text

Achieve Infinite Wealth In Real Estate Through Private Money - Cameron Christiansen & Anthony Paso

Private Money Academy Conference:

Free Report:

Anthony Faso, CPA, and Cameron Christiansen are founders of Infinite Wealth Consultants and hosts of the Infinite Wealth Podcast. A proud U.S. Army veteran and self-described “recovering” CPA, Anthony has worked at the world’s largest accounting firm and served as CFO of a chain of restaurants.

However, after the 2008 recession, he realized that the solution to financial freedom would never be found in the latest Wall Street-created financial product.

As he was discovering what his path to financial independence would look like, he was also teaching and coaching individuals and business owners about money and investing. Having been a small business owner for eight years, Cameron was frustrated with investment solutions proposed by traditional financial advisors.

This frustration is what led him to discover infinite banking and real estate investing. After advising others for over a decade, Cameron now brings his expertise in passive income generation and cash flow analysis to his partnership with Anthony.

As followers of the principles of Robert Kiyosaki, the author of Rich Dad, Poor Dad, Anthony, and Cameron help their clients to be financially independent not just in dollars, but also in sense.

They educate clients on making sound financial decisions and coach them on investing in assets that have certainty, control, and collateral. Infinite Wealth clients are not subject to the roller coaster of the stock market.

Timestamps:

00:01 - Raising Private Money Without Asking For It

05:07 - The Discovery Of Infinite Banking.

06:36 - People Want Income, Passive And Immediate.

15:26 - Bank Cash-Safe, Liquid, Asset Protected, Compounds.

16:33 - Encourage Clients To Store Money In Policy.

19:55 - Benefits Of Infinite Banking For Tax-Free Retirement

23:13 - Comparing Returns: Traditional Banking vs Infinite Banking.

24:38 - Connect with Anthony Faso & Cameron Christiansen: https://www.InfiniteWealthConsultants.com/RaisingPrivateMoney/

27:07 - 401k and Government Credit Plans Have Drawbacks.

30:10 - 401k Liquidated To Start A Policy, Consider Careful Planning.

32:55 - Real Estate Investment: Words Savings, Investing, Speculating.

Have you read Jay’s new book: Where to Get The Money Now?

It is available FREE (all you pay is the shipping and handling) at

What is Private Money? Real Estate Investing with Jay Conner

Jay Conner is a proven real estate investment leader. He maximizes creative methods to buy and sell properties with profits averaging $67,000 per deal without using his own money or credit.

What is Real Estate Investing? Live Private Money Academy Conference

youtube

YouTube Channel

Apple Podcasts:

Facebook:

#youtube#flipping houses#private money#real estate#real estate investing for beginners#real estate investing#raising private money#jay conner#foreclosures#passive income

0 notes

Text

AM Bridge Loans – The Swiss Army Knife of Financing Solutions

In this edition of the Launchpad Series – we introduce the most widely-used tool for property investors at the moment, A Bridge Loan – often considered the “Swiss Army Knife” of financing solutions.

What are bridge loans?

A bridge loan is a type of asset-based, short-term loan, typically taken out for a few months to a couple of years pending the arrangement of longer-term financing or an exit, such as the sale. It is used to ‘bridge’ the gap during times when financing is critical but not readily available.

Bridge loans let homebuyers take out a mortgage against their current home to make the down payment on their new home. A bridge loan may also be a suitable choice for you if you want to purchase a new home before your current house has sold. This financing structure may also be beneficial to businesses that need to cover operating costs while waiting for long-term funding.

Introducing AM Bridge!

AM Bridge – A liquidity tool once reserved for the wealthy is now available for everyone!

Real Estate investors are often asset rich but cash poor. On paper, their net worth may be significant, but their wealth can be tied up in real estate or other businesses. Accessing such funds might mean sacrificing a stake in their business or surrendering some influence over its future – neither of which may be appealing.

It is not always the case that a real estate investor has a few hundred thousand dollars just sitting in the bank readily available to fund a property immediately. Even if they do, they may not wish to tie all their cash upon one property. In today’s market, the property that investors want could be in high demand and needs to be acted on quickly; these could be higher-yielding investments that need immediate funding. Having access to large sums of cash quickly and easily is what HNW investors have had at their disposal for decades. America Mortgages has now made this powerful liquidity tool available to everyone.

How is it used?

Here are some popular uses of “Bridging” Loans:

– Filling the contingency sale of an old property before you can purchase the new property. You can take a Bridge Loan and use your old house as collateral for the loan. The proceeds can then be used to pay a down payment for the new house and cover the costs of the loan. In most cases, the lender will offer a bridge loan worth approximately 80% of both houses’ combined value.

– To purchase based on the asset value of the new build so the borrower can meet the final payment before delivery.

– For the initial purchase until entitlement or for refinancing after a cash purchase until entitlement.

– To purchase greenfield land to begin commercial development. Once certain stages of development have been completed, it’s easier to obtain traditional bank financing.

– Cash-out Bridge Loan for short term personal or business use.

The Market

The pandemic has created a boom in the bridge loan market in several ways.

Firstly, it has created an economic environment filled with uncertainties, and as a result, more businesses need capital as soon as possible and can’t afford to wait for a traditional loan. They will thus turn to bridge loans.

Secondly, with the threat of the Delta variant and the increased number of companies delaying return-to-office plans, many are looking for new homes in more spacious areas. However, with how hot the property market is – data from Zillow show that houses are currently on the market for an average of 6 days only. Hence, it is critical for buyers to purchase their house as soon as possible to avoid disappointment. But, they may not have sold their old house yet and do not have enough money for this new house, which is why a bridge loan would be extra helpful.

Thirdly, there has been an accelerated trend of people migrating to Sunbelt cities due to greater job opportunities. This has driven up rents in these cities – the Phoenix area had the biggest rent increase in July, up 17% from a year ago. Due to the profitability of the rental trade, more developers and businesses are looking to acquire multifamily rental units. Short-term commercial bridge loans will provide them with the needed flexibility to take on such assets while they look for permanent financing options. This will help businesses get their assets to perform at maximum potential.

The Problem

When an American Mortgage bridge loan specialist gets a request for short term financing, they ask three things;

Where is the asset?

What is the value and the outstanding debt?

What situation are you trying to solve?

Number 3 is the most crucial and often the hardest to rationalize. Even the wealthiest people have used short-term bridge financing to access liquidity even when “conventional” options are still possible. This is mainly due to the time and effort required to obtain long-term financing. Cash-flow, credit issues, or asset use may prohibit a “conventional” bank loan. When time is a factor in a transaction, it is important to see the opportunity cost in not closing quickly or obtaining a simplified equity release.

Our Solution

Typically, the timeline for traditional bank loan processing from origination to closing is longer than most borrowers prefer for a time-sensitive funding solution or if the project lacks sufficient stable cash flow. The short-term nature of bridge loans generally allows alternative lenders to provide an approval decision and funding with greater speed than a more traditional lender. At America Mortgages, we’ve funded loans in as little as a couple of days since the initial contact.

To allow for such a speedy funding process, the sponsor’s expected property value and experience to execute the business plan are the determining factors in the decision-making process. For this reason, the loans are commonly non-recourse, which is another benefit to the borrower.

Bridge loans are often the preferred funding option for uses such as:

– Highly structured transactions

– Discounted note payoffs

– Lease-up stabilization

– Redevelopment of existing properties

– Repositioning of a tired or underperforming asset

– Property acquisitions with a short closing timeline (or challenges on the property or sponsor)

– Recapitalizations/Debt Restructuring or Partner Buyouts

– Other uses on a case-by-case basis depending on borrowers specific funding needs, where traditional funding sources like banks or insurance companies will have a hard time approving such loan requests.

– Lending to foreign nationals with a “same-as-cash” basis

Short-Term vs Long-Term

Unlike short-term financing, longer-term financing is susceptible to the regulatory hurdles associated with securing long-term fixed-rate mortgages. This is why bridge loans are often provided by unregulated lenders, family offices, or in some cases, HNW investors. In addition to the regulatory scrutiny, banks or insurance companies require, the sponsor’s credit history and financial strength also take a front seat in the credit decision for long-term loans. Keep in mind, America Mortgages will never work with “lend-to-own” investors and lenders. Our goal is to find you a solution that works with your situation with a long-term solution and exit from the bridge loan.

While bridge loans are the preferred option for many specific financing needs, several downsides come with short-term financing that is meant to fund projects. When assets need work, lenders will consider these higher risks and, therefore, charge higher interest rates.

Additionally, bridge lenders generally do not exceed 70%-85% of the property cost basis to limit their financial exposure. However, this leverage is higher than traditional lenders would advance for the same project. This is because bridge lenders rely on the sponsor to fix the issues, which made the property ineligible for long-term financing in the first place. This enables the asset to become stabilized and ready for exit through a sale or by refinancing the property through traditional channels.

Reference: https://usbridgeloans.com/am-bridge-loans-the-swiss-army-knife-of-financing-solutions/

0 notes

Text

Taking the Plunge - Buying a café venue to run as a profitable business

Starting with coffee and then expanding business – Image by Pexels from Pixabay I am sure no one is following this or believes what I say after so many false starts. Online courses, music promotion, editorial publicity, websites for artists, organising artshows, how to guides and carboot sales with help organising homes. Now I have a chance to focus on one thing – a business – and to test my…

#asset rich cash poor solutions#Becoming a new business owner#business#buying your first real business#coffee#creating a social hub#female business strategy#finding a purpose#food#gathering information#implenenting new ideas#lifestyle business#lifestyle business ownership#making savings and efficiencies#marketing strategy and implementation#news#nuts and bolts#nuts and bolts of running a business#Ongoing concern#planning to take a leap into business ownership#running a team#seed network#side hustle#starting a business#taking on a retail or online business#team leadership#teamwork#travel

0 notes

Text

Control Your Money & Return in command of Your Daily Life

If you would be rich, think about preserving and also getting”

----- Benjamin Franklin (1706-1790)

There is not any faster way to private and economic. Getting unique entails lengthy numerous years of willpower, effort, thrift, and sensible utilization of assets. Those that get rich quick usually do it since: they earned millions of $ $ $ $ on lotto duped others within a swindle or inherited lots of money from the well-off daddy or relative.

However if we return to the root of the problem, it might be important to check with, Why are a few folks poor?”

One of the primary reasons why so many people are inadequate or continue to be far away from getting unique is encapsulated in two terms: financial mismanagement. Fiscal mismanagement is approximately squandering one's useful resource on stuff or pursuits which do not carry fruit or bring about additional revenue. Mismanagement of finances can also be one of several common causes of marital difficulty plus a source of huge stress in individuals.

A lot of people have fallen to the debts capture and from now on really feel totally unmanageable of the existence and funds.

Exactly what can the standard particular person do to better control her or his funds? There is no need to get an economics scholar or a fund expert to escape debts as well as prevent the period of living from income to income. To obtain back to normal with regards to your hard earned money and ventures, consider the following recommendations:

1. Eliminate Your Debts, Stay away from Pointless Shelling out

Should you be like most people, visa or mastercard curiosity monthly payments actually adhere to a large portion of your regular monthly income. The solution is simple: pay out-away from your existing personal debt and get away from generating further lending options or needless purchases. Eliminate debt as fast as you can. Make a list of payables and prioritize either by starting on things that get the increased interest or those that could be easily repaid. The choice of which financial debt to spend-away very first is dependent upon your paying capacity, or even the amount that you obtain from the regular monthly budget to negotiate your debt. An additional hint is always to educate your lender to create intelligent obligations on your own checking or bank account to help you steer clear of delayed transaction costs as well as other penalty charges from your bank card organization. Avoid missing obligations considering that the ingredient attention on your loan or credit rating will have an impact on your financial placement.

2. Provide an Urgent Profile

After repaying each and every debts, the next task is to start out upon an intense savings program. There are numerous cost savings programs you should begin. One plan is to get an Crisis Accounts. Generally set-aside a minimum of 5 Percent to 10% of your paycheck from cafelavista as savings. When your price range allows it, save a separate total fund your urgent fund which you can use for unpredicted expenditures, sudden loss of employment, medical facility expenses, along with other unexpected spending. Having at least six month's amount of your earnings for an urgent fund is really a doable goal. Nonetheless, be sure that you make use of the urgent account for unexpected emergency reasons only rather than for unimportant shelling out.

3. Take A Look At Your Company's Retirement life Strategy

Retirement life plans help men and women reserve dollars that they could use after they relocate. A 401(k) is really a retirement living plan that had been called following a segment of the us Inner Earnings Computer code. The business-subsidized plan operates by establishing aside a percentage of your employee's salary which, subsequently, is purchased mutual funds, stocks, along with other assets in the cash marketplace. Another choice is to make investments the amount of money in organization inventory. The main advantage of the 401(k) is that the program is taxes-deferred.

4. Pension to the Personal-Hired

When you are personal-used or fit in with an unincorporated business, you can study the possible benefits associated with the Keogh Strategy which allows personal-employed people set aside approximately 15% of the cash flow or they may participate in a joint fund organization making auto contributions or you may get a pension strategy.

5. Spend Your Money

When protecting a number of your challenging-acquired cash is a superb commence, leaving behind all of it inside the banking institution may not give you the outcomes you want. Get informed about assets along with other fiscal equipment you can use to create your dollars make greater than what you will be currently getting from your financial institution. The first step is to learn about unaggressive and lively revenue. You need to also discover ways to examine and select assets that will earn more money in the end. Reciprocal money, shares, along with other expenditure options are accessible for anyone to review and take into account.

6. Handle Your Hard Earned Money On the web

For those who have an online-competent personal computer at home or at work, it is possible to deal with your financial situation on the web. You can check your balance and credit history assertions, move money, shell out your debts, and monitor the standing of your own price savings using your bank's on-line method.

Certainly, there is no faster way to prosperity. Dwelling the good lifestyle requires organizing, placing desired goals, willpower, a lot of sacrifice. Eliminating get worried and anxiety and panic attacks over financial hardships is not an impossible project. When you conserve and commit sensibly, it will be easy to prepare the tough times that are sure to can come and you can have adequate to experience daily life, which is the reason we must take control of our budget.

1 note

·

View note

Text

The current episode of WITH with Gabriel Zucman has some good bits: he argues that tax jurisdiction shopping probably isn’t something the US has to worry about, because being a citizen resident outside the country isn’t enough to avoid US taxes, and renouncing your citizenship comes with a tax on unrealized capital gains--Warren proposes making this a 40% wealth tax, in addition to her annual wealth tax, which would be pretty funny IMO. He also argues that combating mundane tax avoidance schemes is mostly a matter of political will. Europe hasn’t tended to have that, which is why European wealth taxes have not seen much success; fortunately, in the US, the idea of a wealth tax is wildly popular, among supporters of both parties.

The only argument he can muster against Hayes weakly suggesting that maybe it’s better for Bill Gates to spend Bill Gates’ money than the US government spend Bill Gates’ money is that relying on private charity is undemocratic, and while I think that’s true, I wish he’d given over half a sentence as to why. “Undemocratic” by itself is kind of waffly, and not super convincing. The real answer I think is that politics often points to needs of the electorate that billionaires overlook or outright refuse to fulfill--one half of one percent of Warren Buffet’s net worth annually could, for instance, do wonders for Nebraska’s public schools--and even in the most generous reading, where this is nothing more than the result of coordination problems among charitable foundations run by rich people, we have a mechanism for solving that particular suite of allocation issues, and it’s called a legislature and a state or federal budget.

The biggest rejoinder of course is that the US government also spends a lot of money on awful things like wars. However, I think the rejoinder to that rejoinder is that the politicians more likely to enact wealth taxes seem the least enthusiastic about wars: Warren and Sanders are no Biden or Clinton (to say nothing of Cruz) and so as a practical matter I feel like the likelihood of US tax revenue being spent on mass murder is going to be strongly anticorrelated with actually increased tax revenue. (If Bernie Sanders starts arguing we need to bomb Tehran, I promise to revise my position accordingly.) But even if there were no correlation in either direction, I still feel like the consistent position would be to vote for wealth taxes and against war.

There’s another argument against wealth taxes that I think is quite good--that is, that (say) Jeff Bezos’s hundred-billion dollar net worth is a theoretical number, and is as high as it is at least in part because it is owned by Jeff Bezos. You can’t treat assets, especially ownership stakes in publicly-traded corporations, as though they’re equivalent to piles of cash in a vault, even if we attach numbers to them that indicate they’re in some sense similar. Forcing Bezos to sell some small part of those assets annually to meet an arbitrary tax demand might not yield the expected revenue for the US government, and having Bezos, who apparently doesn’t suck at his job, hand over control of these assets to other people might be bad for the economy as a whole in the long run.

To this, I would say: sort of, but that’s actually kinda the point. First, I’m pessimistic and I think it’s very, very hard to overestimate the amount of wealth that very rich people have that’s the product of rent-seeking, favorable regulation, and luck, rather than innate capability. But even if it were true that Jeff Bezos is one hundred billion times smarter and more capable in a general sense than One-Dollar Bob who runs the convenience store next to my house but is up to his eyeballs in back child support payments, then by virtue of his talents and abilities, he is always going to enjoy an outsized proportion of wealth and prosperity compared to poor ol’ Bob. After all, Warren and Sanders are not proposing a law saying all billionaires as of January 1, 2021 are to be taxed until they’re wearing half a boot for a hat and living in an old boxcar--I think Warren’s proposed tax is like 2% above 50 million and 6% above a few billion? I.e., you can be close to filthy stonking rich as you like by the average person’s reckoning, and be liable for bupkis under Warren’s tax (even better if you live in a low cost-of-living state like Nebraska!); this is a far cry from seizing the means of production and setting up a guillotine in front of the NYSE.

I think it’s a good thing not to have huge swathes of the economy in the hands of a small number of people. I think it’s a good thing because I think rich people largely aren’t nearly as competent as we alieve they are; we often operate under the opposite, rosier end of the just world intuition, and forget how much wealth depends on things like favorable tax codes, exploitation of labor, and rent seeking. Fuzzy concerns about “democracy” aside, I think a small number of private individuals not responsible to the electorate are going to be worse about directing their wealth to publicly useful ends, even if they are highly motivated to do so. And even if we got very lucky, and we had a generation of billionaires in the US who were, every single one, deeply committed to extremely important humanitarian projects like eradicating malaria, we could at best treat such a thing as a fluke. The problem with absolute monarchy is that even when you get a great king, his successor can be a real jackass, and there’s nothing you can do about it. The heuristic that private property--not mere personal possessions, but an abstract imperium over the ends of the labor of thousands or tends of thousands of people a major shareholder may never meet, reified as a thing like a physical possession in law--ought to be endlessly deferred to, even when such property is hoarded until someone has command over the equivalent of 4% of California’s GDP, relies for the continued good functioning of the economy, and the wise application of that power, on mechanisms of succession that, like the peasant in the Kingdom of Prussia, many interested parties simply have no say in, and to which few tools of institutional improvement can be applied from the outside. In short, there’s no reason to think that even if Bezos is good at his job, his kids won’t suck at theirs, and ruin a lot of people’s livelihoods as a result.

The real solution to my mind would be to heavily reorganize the economy in the direction of giving workers a far greater stake in the companies they work for, and requiring democratic methods of workplace management. That’s a far more radical approach, though; by contrast, a wealth tax--a gentle nudge in the direction opposite the accumulation of vast fortunes, but by no means an iron law against it--is a positively delicate instrument.

#i am aware that if you think all forms of taxation are theft#then a wealth tax is probably morally equivalent to me murdering your family and burning your house down#but if you think all forms of taxation are theft#then you and I probably have a more fundamental rift in our starting assumptions than can be resolved on tumblr

17 notes

·

View notes

Text

Equity Release - A Quick Guide to the Different Schemes

Collateral Release is the term used to describe a financial solution that is available in the UK for those who are 55 or over. The term again covers the financial sector, with Equity Release Schemes, Lifetime Mortgages and Home Reversion Plans being that products that are available. The first thing to note is that equity release schemes, equity release mortgages and lifetime mortgage are generally one in the same thing, with the terms being used interchangeably. Each of these products refers to a financial product that releases profit for homeowners aged 55 or over. The money is released from the equity in their property, with the amount being good property value and the age of the youngest applicant. The amount that can be released starts at around 21% for those previous 55, and increases at approximately 1% per annum up to a maximum of 56% at age 90. The maximum amount readily available drawdown will change between providers. Essentially all equity release schemes operate by releasing a lump sum that could be spent however you wish. Now this may be for home improvements, to supplement ongoing pension income and state positive aspects, for the holiday of a lifetime, or simply to assist your loved ones such as children or grandchildren. The options available when releasing collateral are either as a maximum lump sum as per the previous percentages, or as a minimum lump sum around £10, 000 with the balance being made available as an equity release drawdown facility. Equity release drawdown is usually set for a minimum release of between £2000 and £2500. After you have released funds, interest is rolled up against the asking for, generally at a fixed rate of interest for life. This means that you know from outset exactly how the debt will increase over time. For example a group sum of £10, 000 at a fixed rate of 7% will grow to £19672 after 10 years, and £38697 after 20 years once the rolled up interest is added to the original borrowing. Compare this to a lump sum of claim £30, 000 which would grow to £59, 000 over 10 years at a fixed rate of 7%, and the selling point of equity release drawdown option is clear to see. It is worth noting that different providers offer the option to protect a percentage of the property for those wishing to protect an amount for inheritance, i. e. protecting 50% of the property value. The following certainly provides peace of mind, but will reduce the maximum amount that can be released from the property as the aforementioned percentages may be based on the reduced amount of the unprotected portion of the property. Equity Release Lifetime Mortgages really can provide a solution for those which were asset rich but cash poor, and can make the difference between just getting by, or actually experiencing and enjoying retirement and old age. They're not for everyone though, and obtaining advice from one of the many equity relieve advisers in the market is to be recommended. This will help provide you with an appreciation of both the pros and cons associated with Equity Release. For instance: - Pros You can remain living in your property for the rest of your life There are no monthly payments to be made The debt is usually repaid only when the last surviving applicant passes away, the property is sold, or a move into long term care. No negative equity ensures ensure you can never owe more than the property is worth Cons Releasing equity can affect entitlements to means tested benefits. Since interest rolls up over time, the reduction in equity could make it difficult to move home, or downsize. As the attraction rolls up the amount that can be left to your beneficiaries reduces. Home Reversion Plans Unlike Lifetime Mortgages where people retain complete ownership of the property, Home Reversion Schemes work on the basis that you can sell anything from 20% to help 100% of your property to the Home Reversion Company, with any amount not sold, being held in rely on. Home Reversion is only a small part of the Equity Release market, as many people view them as being poor value. Using other equity release schemes you benefit from any capital growth in the property as you retain ownership, whereas after getting sold a percentage of your home to a reversion company, any increase in the value of that portion belongs to them alone. Much like all financial products there is rarely a perfect solution, and so taking time to review all the information available to you is likely to be time well wasted.

1 note

·

View note

Text

Aiming to give away 5% annually

Let me preface this with this: I’m not rich.

I’m not in the top 1% of wealth. I don’t even know if I’m in the top 10-20% of wealth. I have no fixed assets such as real estate, etc. I don’t really have any savings.

But I’m not poor either. I’m pretty sure I’m in the top 50% of wealth at least, or maybe more. I work in software, which is not astronomical pay, but is pretty decent, and there is always a job somewhere. I don’t have any debt (but I go up and down, last year I ended 3 years of debt). I also just started investing in shares again late last year, with about 30% of my annual salary in stocks.

Why am I talking about this?

Well, spiritually I feel like I’m letting down humanity if I don’t help people who are homeless in some way. The most common way I’ve tried to help in the past decade is by walking with a dollar or 2 in my pocket at all times. When I see someone needing it, I take it out and give it to them. No questions, no judgement.

But I came to the realization recently that in the past 1-2 years I’ve been doing that less, because 95% of my transactions now are done using Apple Pay, or in-app ordering. Heck, most days I don’t even carry my wallet with me anymore, let alone use cash!

So what can be done in the Apple Pay era?

youtube

The video above is one fine example.

Donating to charities is also ok. But I’ve never felt great about it because:

There’s no guarantee all of it is going to reach the people who actually need it.

There’s usually arbitrary rules to distribute the donations, like food stamps, etc. I personally prefer to donate with the intention of having no judgement whatsoever on what and how the recipient chooses to use it.

Charities however, are the best solution for bigger problems, such as finding a cure for AIDS. Even though the bigger outlets still suffer from the 2 problems above, I’m ok with donating to these causes that I can’t play a role in helping to fix.

But homelessness is also fixable at a grassroots level!

So do I create my own charity?

That seems kind of crazy. Isn’t that only for rich people, like Bill & Melinda Gates, and actors?

Or is it? Why. The heck. Not?

Ok so maybe not a charity, technically. Like if I create a “Mike Charity” and put it out on Facebook etc for people to donate to, doesn’t that still not solve the 2 problems above? i.e., other people have no idea what I’m using that money for.

So I’ve decided that once a year I’m just going to literally walk in the street and give 5% of my wealth away, to anyone sleeping or begging on the streets.

I would prefer to give it away and help people in need rather than live in a bubble. Say for example if I have a total of $20,000 saved up or invested, I’ll be giving away $1000. No conditions. If I have $5000, I’ll be giving away $250. Etc.

I might donate some of this away as food, but the important thing is not to cast any judgement on people receiving this cash or food and how they’re going to use it. Take away people’s choice and you take away their humanity.

Why now?

I have this constant instinctive tendency to want to save up and build up all of my life’s wealth first, then give it away at the end of my life. Because I might fall under hard times, or I might be unemployed, or either myself or someone in my family might get sick, or I might get in a car accident, etc.

I’ve had a lot of financial ups and downs since leaving the parental nest as an adult, so the temptation to build a massive rainy day fund overwhelmingly appeals to my inner reason.

But when I think about it:

I can technically give away 5% annually and it will make almost no difference to any personal hardship. Just a difference to comfort I can live without.

Why save up all my life and make massive donations towards the end of life or on my deathbed, and only help people then within a relatively short timeframe? Instead I can distribute the timeframe, and help people now.

Anyone can join me for this walk if they want to do the same - this is the charity, simply just join me in walking and giving.

I haven’t decided when exactly I’ll do this yet, perhaps around thanksgiving or Christmas.

I don’t personally believe in karma, this isn’t karma motivated. But I’m ok if you do.

I do believe that individuals can do more to bridge the wealth gap without relying on governments or charities to take ownership of that, and risking corruption. Governments and charities have done an incredible amount to benefit the world though, especially in the past century. This isn’t anti-government or anti-charity sentiment.

I just simply think it’s time to progress to the next level. The middle class is bigger than it’s ever been, and we don’t need to wait any longer to help at an individual level. I’m not waiting for anyone else to join me, but the invitation is there if you want to.

9 notes

·

View notes

Text

Mongolia has a Universal Basic Income (UBI)

A universal basic income (UBI) is a monetary payment made by the government to all citizens. It is not dependent on income or assets and aims to reduce poverty and increase financial security without requiring excessive bureaucratic interference.

UBI has been offered as a solution to a variety of issues, including job loss, income stagnation, and social discrimination. However, there are many unanswered concerns concerning how successful UBI is in combating poverty.

The concept of a basic income, in which everyone receives a small sum of money regardless of job status, is gaining traction. It's a program that reformers and futurists alike support because it has the potential to eliminate poverty, reduce inequality, eliminate patronizing bureaucracy, eliminate the fear of mass unemployment, and raise the value society places on worthy endeavors.

Despite widespread concerns that providing people with free money will disincentivize them from working, Iran's statewide universal cash-transfer program has found no evidence to substantiate those allegations. According to a paper published by economists Djavad Salehi-Isfahani and Mohammad H. Mostafavi-Dehzooei, recipients did not become work-averse, and some even worked more.

The system began in 2011 when Iran implemented a statewide cash-transfer policy to compensate for significant reductions in bread, water, power, heating, and fuel subsidies. Each household received a monthly payment equal to around 29 percent of the median income, or about $1.50 per day.

Mongolia is a mineral-rich East Asian republic located between Russia and China. Its export-driven economy is primarily reliant on minerals, which account for 90% of the country's GDP.

The Mongolian government began experimenting with a universal resource-financed stipend for children in 2004. This was superseded in 2010 by the Human Development Fund (HDF), which was funded via mining dividends and provided monthly cash transfers to all citizens between 2010 and 2012.

As co-owners, individuals received direct and equal portions of their country's riches, providing a unique perspective on public ownership and revenue sharing in the mineral industry. However, HDF expenditures far outstripped mining revenues, resulting in a fund deficit.

A universal basic income (UBI) is a social safety program that pays all residents a fixed monthly payment regardless of their wages or employment status. It has acquired widespread traction as a means of alleviating poverty while simultaneously protecting workers from the threat of automation.

India already boasts a plethora of welfare programs, ranging from free rice to housing allowances for low-income families. They are, however, frequently ineffective and plagued by corruption and leakages.

Several experiments in India have shown that unconditional cash transfers to the poor improve nutrition, debt, asset building, and a variety of other livelihood indicators.

However, adopting a UBI would necessitate significant changes to the current welfare infrastructure, which could be hindered by the need to implement and monitor benefits. Furthermore, it is projected to be expensive.

According to a recent analysis in India, a system of this magnitude may cost up to Rs15.6 trillion every year, putting a significant strain on the state's budget. It would also necessitate a significant amount of administrative work as well as significant technology and infrastructure improvements.

UBI is a universal cash payment sent on a regular basis to all members of the community, regardless of employment status or income level. It is intended to be individual, unconditional, universal, and frequent, and it is intended to challenge present practices by being delivered in cash.

Because of concerns that technology and artificial intelligence would displace workers at an unprecedented rate, many Americans have revived their interest in universal basic income. A program like this is intended to ease the transition for those at risk, stabilize salaries across the board, and encourage inhabitants to explore retraining and alternate forms of work.

In recent years, many municipal governments have initiated guaranteed-income experimental programs. These programs provide participants with a high level of stability, but they are also fraught with difficulties. Cook County in Illinois, for example, has the most of these programs.

0 notes

Text

How to Become a Successful Investor

Investing in the stock market is one of the most profitable and the riskiest kind of investments. Nowadays, in most cases, investment allocation is a result of flowing cash to the assets where the current return and risk are satisfied a certain investor expectation. There are some differences between such participants on the stock market as investors and traders. However, a classical investor and trader are both aim at gaining money. History evidences the different cases, when an investor started with a small amount of money and eventually became very rich, or on the contrary, when a millionaire lost all investments on the stock market and became poor. What is the most important quality that separates the winners from the losers on the stock market? The answer is simple - it is knowledge in investing, either that is based on collected wisdom by other investors or gained through making own mistakes. Anyway, the following basic principles could be useful to remember:

Never invest all your money in the stock market, especially, if you are a beginner. Common recommended portion of invested money in stocks is from 25% to 50% of your total budget.

Never invest all money in one stock - always diversify among several stocks in different sectors.

Always watch closely general market conditions, especially, when bear market is about to start. Be prepared by selling most holdings in advance.

Never rush with investment solution. Carefully watch financial quarterly reports, news, and macroeconomics trends before making any decision.

Never let your emotions prevail over a rational disciplined approach.

To improve return/risk ratio, use reliable software tools that embody the investors' concentrated wisdom.

All stocks are volatile without exception. There will be always a certain probability that something suddenly will go wrong with any stock. Even the best stocks can depreciate.

USA recent researches show توصيات الأسهم الامريكيه that an average investor has around $250,000 investment assets and more than half investors uses brokerage advices. Investing is popular for both genders almost equally. For the last decades, the expectation of most investors decreased from about 30% to about 10% of annual return on investment. Most investors prefer a long-term type of investments with less than five transactions per year. Not everyone is able to succeed in investing. Most losses in investing happen because of lack of knowledge, over-confidence, impatience, greed, fear, and different delusions. An experienced investor knows that there is a direct proportion between time spent to increase investing skills and return on investment.

#توصيات الأسهم الامريكيه#توصيات الاسهم الامريكيه علي التليجرام#الاستثمار بالاسهم الامريكيه#الاستثمار بالبورصه الامريكيه#دورات تعليم الاسهم الامريكية#التداول بالاسهم الامريكية#تحليل الأسهم الامريكية#موقع توصيات مجانية#الأسهم الأمريكية توصيات

1 note

·

View note

Text

Utilizing An Reverse Mortgage To Pay for Long Maintenance and Steer Clear of A Nursing Home

AARP, the Federal National Mortgage Association, American Bar Association (ABA) and the National Council On Aging provide consumer information about reverse mortgages. The ABA passed a resolution supporting Reverse Mortgages in August of 1995. What is it about Reverse Mortgages that instills dread in some Older Americans? Yet another misconception is that Reverse Mortgages are more expensive than other mortgages. The truth is that closing costs average only about one (1 ) ) percentage more than a normal FHA mortgage could be on the exact same property. The Reverse Mortgage might even be lower in cost because of the simple fact that traditional mortgages can charge more compared to (two ) percentage origination fee enabled on all Reverse Mortgages. Since the Reverse Mortgage is really just a"non-recourse" loan the most the estate will likely probably be asked to pay to the lender could be your value of the house at the time of repayment. This holds true even if your home worth dropped or the borrower dwelt to a unusually old age. One of the most popular misconception is" Should I obtain a ReverseMortgage I might lose my home". I often hear this when I'm advising elders about intending options associated with long-term maintenance. The simple fact is that the federal government expects that the home has to stay in the name of the borrowers just. As the Reverse Mortgage can be a mortgage, a lien is placed on the property like the rest of the mortgages. This guarantees the bank will eventually be repaid however for only the total amount owed that is principle, interests, and closing costs, exactly like every mortgage. A reverse mortgage is just a way of borrowing money from the amount you've already taken care of the home. You are freeing up money which would otherwise only be open for you if you purchased your home. You can remain inside your home till you perish, without making monthly obligations. The mortgage is repaid when the borrower dies or sells your house. The remainder of the equity in your house will go to the homeowner's home. In accordance with the research, out of the nearly 28 million households age 62 and older, some 13.2 million are candidates for reverse mortgages. Assuming the average salary of men aged 65 and over would be $28,000 and $15,000 for women, he added,"This analysis indicates that unlocking those resources can help an incredible number of'house rich, cash poor' seniors purchase the long-term maintenance services that they feel best suit their needs." Yet another myth regarding reverse mortgages would be that the home goes into the http://ge.tt/71zG65u2/v/0 lender after the loan becomes due at passing or if the last survivor permanently leaves your house. In my experience, the amount of the loan of approved is generally roughly half of the appraised value of your home. (The older the employer, the greater the total amount available for borrowing since it's presumed that the capital will be available for a briefer period. Each one the equity left once payment on the lender, goes to the heirs or estate of their debtor. This is exactly the identical procedure followed by regular traditional mortgages. "There has been a good deal of speculation if reverse mortgages could possibly be part of the remedy to the world's long-term care financing issue," said NCOA President and CEO James Firman. "It's apparent that reverse mortgages have significant potential to help many seniors to cover long-term care services in your home" Since the ReverseMortgage may be brilliant and safe option for elderly Americans, it's crucial to fix the significant misconceptions associated with them and invite senior homeowners to create an informed decision regarding whether a ReverseMortgage is logical for them. Given that the urban myths of ReverseMortgage are removed, a skilled homeowner may ask, how can I obtain more comprehensive details? Is your regional bank the solution? Most regional and local banks usually do not offer Reverse Mortgages. Because longterm maintenance insurance takes you to maintain good health, this planning option is not available to everyone, especially older applicants for the premiums may also be prohibitive. If you're at least 62 years of age and also you have your home, you might make use of a reverse mortgage to cover care at home or for a longterm maintenance insurance policy which differently can be unaffordable. Fears continue despite the enthusiastic endorsement of groups like AARP and the National Council on Aging.It should be said that Supplemental Security Income (SSI) and Medicaid may possibly be affected in the event that you transcend certain liquid asset levels. We can explain to you the way you can structure the loan so that a ReverseMortgage will not affect these advantages. In the event that you'd like to acquire specific info on a ReverseMortgage for yourself or a family member, contact Bob O'Toole in 1-800-375-0595 or send an e-mail to [email protected] Use Your Home to Stay at Home Program The National Council on the Aging, also with the support of both the Centers for Medicare and Medicaid Services (CMS) as well as the Robert Wood Johnson Foundation, is laying the ground work for a powerful public-private partnership to raise the usage of reverse mortgages to help pay for long-term maintenance. The best goal of this Use Your Home to Stay at Home(TM) program will be to raise the suitable use of reverse mortgages so that millions of homeowners can tap home equity to cover long-term maintenance services or insuranceplan. He serves on the board of directors of the National Association of Professional Geriatric Care Managers, also is a former editor of the Geriatric Care Management Journal. A frequent presenter on aging issues, Bob has contributed chapters to two books on senior care and geriatric care management issues and has written numerous articles on the delivery of senior care in the private marketplace. Seniors can choose to spend the cash out of the reverse mortgage as a lump sum, in a line of credit or at monthly obligations. Should they prefer a lump sum, as an example, they can pay to re sell their home to make kitchens and bathrooms simpler and more accessible - particularly essential to those who are becoming frail and in danger of falling. Should they choose a line of credit or monthly payments, then the typical reverse mortgage agent may use the funds to pay for just three decades of everyday home medical care, over six years of adult day care five times per week, or even to help family practitioners with outofpocket expenses and weekly respite care for 14 years. They could also use it in order to buy long-term maintenance insurance if they're eligible. Payments are available yearly, in a lump sum or the money can be used as a credit line. The capital received from the reverse mortgage are all taxfree. Alternatives to Long Term Care Insurance: With a Reverse Mortgage and Other Methods to Cover Long-term Care Costs More than ninetyfive (9-5 ) percentage of Reverse Mortgages approved will be the Federal Housing Administration (FHA) Home Equity Conversion Mortgage (HECM) loans. Such loans are ensured the complete protection of the United States Government through use of a two (two ) percent insurance fee paid on all FHA Reverse mortgages. It is possible to make utilize of the funds in the reverse mortgage to pay the price of home-health care. As the loan has to be paid back in the event that you cease to live in the house, long-term maintenance outside the house can not be paid to get a reverse equity loan unless a co-owner of the property who participates continues to live in the home. All land types are Reverse contingency eligible except manufactured (mobile) homes built before June 15, 1976 and also cooperatives (co ops ). Coops are expected to meet the requirements in the future when FHA problems final approval. Homes with existing mortgages which can be paid out of the equity can obtain Reverse Mortgages. According to the study, of the 13.2 million that are candidates for reverse mortgages, about 5.2 million have been either already receiving Medicaid or have reached financial risk of having Medicaid when they were faced with paying the high cost of long-term maintenance in home. This effectively vulnerable segment of the state's elderly population will be in a position to earn $309 billion in total by reverse mortgages which may help cover long-term care. These outcomes are all based on info from the 2000 University of Michigan Health and Retirement Study. Yet another cost factor is needless to say, the rate of interest. The FHA Reverse Mortgage interest rate is situated upon the one (1) year United States Treasury note instead of the prime rate, which many traditional mortgages use as their base. This offers the FHA ReverseMortgage an interest LOWER than many adjustable conventional mortgages. Another attractive feature of this financing tool would be that certain requirements for a Reverse Mortgage aren't nearly as restrictive as other loans. Since no re payment is made as long as you (1 ) ) surviving borrower remains in the house, there are NO income or credit conditions. Yet another condition is that both spouses must be sixtytwo (62) or older with no upper age limitation. The only other requirement is that the creditors must have the house or apartment without others on the deed. The house could also maintain a revocable trust provided that the borrowers that are eligible are the sole trustees. A brand new study from The National Council on the Aging (NCOA) implies that using reverse mortgages to cover long term maintenance in home has real capacity in fixing what remains a severe problem for many older Americans and their own families. "We've found that seniors that are good candidates for a reverse mortgage can easily get, typically, $72,128. These funds could possibly be utilised to pay for a broad assortment of direct services to help seniors age in place, including home maintenance, respite care or for retrofitting their homes," said manager Barbara Stucki, Ph.D."Utilizing reverse mortgages for all can mean the difference between staying at home or moving into a nursing home." Still the other offender is a Reverse Mortgage is taxable and affects Social Security and Medicare. That's not the case. Reverse Mortgage proceeds are not taxable as they're not considered income but is, in actuality, that loan. While the eligibility age is 62, it's ideal to wait until the early 70's or later. The older the borrower, the larger the amount of equity available. There are maximum limits fixed by the federal government annually about how much of this equity might be borrowed. Usually just about 50 percent of their worth of your home is offered in the kind of a reverse mortgage.

youtube

The wonderful benefit of this kind of mortgage is that -unlike most conventional mortgages-there are no monthly obligations. Not needing to worry about regular statements needs to be one of the greatest presents you could wish for in retirement. A big rationale is likely to become the simple fact that a good deal of misinformation is circulating about this very attractive fiscal tool for the ones who qualify. Older Americans often consult friends and family members that are very likely to Reverse Mortgage Lenders become misinformed themselves. In 2000, the nation spent $123 billion a year on long term maintenance for those age 65 and older, with the amount inclined to double within the next 30 years.

1 note

·

View note

Text

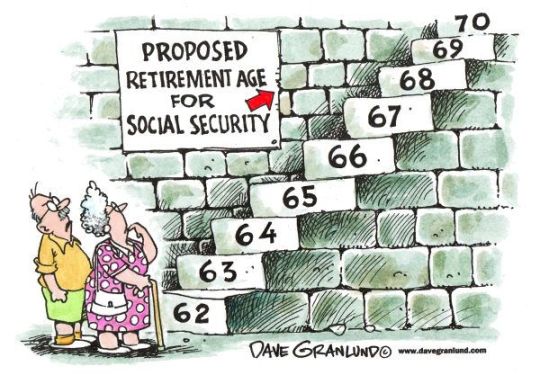

Why Do Republicans Want To Cut Social Security

New Post has been published on https://www.patriotsnet.com/why-do-republicans-want-to-cut-social-security/

Why Do Republicans Want To Cut Social Security

Warning: Republicans Are Plotting To Raid Social Security

Obama Cuts Social Security

Donald Trump is obsessed with defunding Social Security. In the midst of a catastrophic pandemic, millions of Americans are facing eviction and hunger if Congress doesnt act now to extend unemployment benefits. Essential workers are in desperate need of testing and protective equipment.

But Trump doesnt care. He has threatened to veto any COVID aid package that doesnt include a cut to the payroll taxSocial Securitys dedicated revenue. On Monday, Minority Leader Kevin McCarthy ;announced;that Congressional Republicans are on board with Trumps plan to defund our earned benefits.

As a response to the economic crisis, with 40 million unemployed in just the last few months, cutting Social Security contributions makes no sense. They are a poor economic stimulus. The money is paid out slowly over many months and fails to get cash into the pockets of;those who need it most;and will spend it immediately. Those shortcomings defeat the purpose of stimuluscreating needed economic activity. The only reason to support this policy over better targeted, more efficient measures is if your true goal is to undermine Social Security.

When reporters asked Senator Chuck Grassley for his thoughts on the Republican proposal, his response was refreshingly honest. Grassley;worried;that it might create political problems because Social Security people think we’re raiding the Social Security fund. And we are raiding it…

Republicans Aren’t Going To Take Away Social Security

Without beating around the bush, the Republican Party is often associated as being the party of the well-to-do — and the rich typically aren’t reliant in any way on Social Security income. There’s, therefore, been a long-running belief that Republicans would aim to do away with Social Security sometime in the future. This is nothing more than another in a long line of pervasive Social Security myths.

Both Democrat and Republican lawmakers on Capitol Hill have an understanding of the importance that Social Security plays in keeping some 22 million people currently receiving benefits above the federal poverty line. Though both parties may have suggested tweaking how revenue is generated for the program, neither party would remove or replace any of the three funding sources: the payroll tax on earned income, the taxation of benefits, and interest income on the program’s asset reserves.

In other words, no Republican is going to advocate scraping Social Security. And even if they did, the idea would have no chance of gaining traction in Congress.

They Haven’t Taken A Dime From The Social Security Program That Isn’t Accounted For

Another misconception is that the Republican Party stole money from the Social Security Trust and used it to fund wars. More specifically, Ronald Reagan, George H.W. Bush, and George W. Bush have come under intense scrutiny for borrowing from Social Security and “not putting the money back.”

However, the truth of the matter is that Congress has been able to “borrow” Social Security’s excess cash for five decades, and it’s happened under every single president over that stretch. In fact, the Social Security Administration is required by law to purchase special-issue bonds and certificates of indebtedness with this excess cash. Please note the emphasis on “required by law” that I’ve added above. The federal government isn’t simply going to sit on this excess cash it borrows from Social Security. It’s spending this cash on various line items, which may be wars and the defense budget, as well as education, healthcare, and pretty much any other expenditure you can think of.

This setup is actually a win-win for both parties. The federal government has a relatively liquid source of borrowing with the Social Security Trust, and the Trust is able to generate significant annual income from the interest it earns on its loans. Last year, $85.1 billion of the $996.6 billion that was generated by the program came from interest income.

Read Also: Who Is Right Republicans Or Democrats

How Urgent Is The Problem

The public already is pessimistic about Social Securitys future. A Pew Research Center study released last March found widespread worry among todays workers about the programs future 83 percent expected benefit cuts by the time they retire, and 42 percent did not expect to receive any benefits in retirement.

The public worry is understandable, but out of proportion, says Paul Van de Water, a senior fellow at the Center on Budget and Policy Priorities, a left-leaning think tank. The odds that benefits are going to disappear are as close to zero as possible, he said. But the continual talk about the financial problems leads people to worry excessively about it.

Despite public sentiment and trust fund projections, the next president and Congress may not feel pressure to act during the next four years. Much will depend on the balance of control in Congress and the White House.

The more power Democrats have, the more likely it is that there will be action, said Ms. Altman of Social Security Works. If Republicans stay in power, they will try for a bipartisan solution, but Democrats wont go for benefit cuts.

If the problem is not solved before the 2035 depletion date gets near, experts note that odds will favor restoring solvency to the trust funds with new revenue rather than benefit cuts.

What You Should Know About The Gop And Social Security

Who’s to blame for this mess? Well, some Americans would point their fingers specifically at Republicans in Congress. While they absolutely do take some of the blame, the inaction by Republicans and Democrats on Capitol Hill makes them equally culpable in exacerbating Social Security’s problems.

When it comes to Republicans and Social Security, here are the four things you absolutely need to know.

Don’t Miss: Republican Primary Popular Vote Totals

Do Republicans Misunderstand Social Security Or Just Feign Ignorance

Copy Link URLCopied!

Print

As a follow-up to our Tuesday post on the House GOPs assault on Social Security and its beneficiaries, its proper to take a closer look at the rationale for the attack.

To recap, the GOP caucus passed a rule making it much harder, if not impossible, to reallocate Social Security payroll tax revenue from the programs retirement fund to its disability fund. The latter is in imminent trouble, expected to run out of reserves next year. At that point, disability benefits will have to be slashed about 20%.

Reallocation is a crucial near-term fix, and something thats been done nearly a dozen times since the 1980s to keep both the disability and old-age funds solvent. The new GOP rule allows any member to block it.

Kathy Ruffing of the Center on Budget and Policy Priorities points us to this explanation from the provisions sponsor, Rep. Tom Reed of New York. His intention, he says, is to force us to look for a long term solution for SSDI rather than raiding Social Security to bail out a failing federal program. Retired taxpayers who have paid into the system for years deserve no less.

Ruffing calls this a revealing statement. So it is, in the sense that a big red F on a school paper reveals a pupils profound lack of understanding.