#US Vegetable Oil Market Forecast

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has been banned in Indonesia for providing people with access to pornographic content.

Text

US Vegetable Oil Market Outlook for Forecast Period (2023 to 2030)

The US Vegetable Oil is Expected to Grow at a Significant Growth Rate, and the Forecast Period is 2023-2030, Considering the Base Year as 2022.

US Vegetable Oil is a type of edible oil derived from various plant sources, such as seeds, fruits, nuts, or vegetables. It plays a crucial role in cooking, baking, and food preparation worldwide. The extraction process typically involves crushing or pressing the plant's seeds or fruits to obtain the oil, which is then refined to remove impurities. US Vegetable Oils are rich in essential fatty acids, like omega-3 and omega-6, and they provide a significant source of energy and nutrients in the human diet.

Common examples of US Vegetable Oils include soybean oil, sunflower oil, canola oil, corn oil, and olive oil, each with its distinctive flavor and culinary properties. Besides culinary uses, US Vegetable Oils find application in various industries, such as cosmetics, pharmaceuticals, and biofuels, making them versatile and indispensable commodities in modern society.

Leading players involved in the US Vegetable Oil Market include:

Archer Daniels Midland Company (ADM) (US), Bunge North America (US), Cargill, Incorporated (US), Wilmar International (USA) LLC (US), Louis Dreyfus Company LLC (US), Ag Processing Inc (AGP) (US), Richardson Oilseed Limited (USA) (US), Ventura Foods LLC (US), Darling Ingredients Inc. (US), The J.M. Smucker Company (US), AAK USA Inc. (US), CHS Inc. (US), IFFCO USA (US), The Hain Celestial Group Inc. (US), The Hershey Company (US), The Andersons Inc. (US) and Other Major Players."

Get Full PDF Sample Copy of Report: (Including Full TOC, List of Tables & Figures, Chart) @

The latest research on the US Vegetable Oil market provides a comprehensive overview of the market for the years 2023 to 2030. It gives a comprehensive picture of the global US Vegetable Oil industry, considering all significant industry trends, market dynamics, competitive landscape, and market analysis tools such as Porter's five forces analysis, Industry Value chain analysis, and PESTEL analysis of the US Vegetable Oil market. Moreover, the report includes significant chapters such as Patent Analysis, Regulatory Framework, Technology Roadmap, BCG Matrix, Heat Map Analysis, Price Trend Analysis, and Investment Analysis which help to understand the market direction and movement in the current and upcoming years. The report is designed to help readers find information and make decisions that will help them grow their businesses. The study is written with a specific goal in mind: to give business insights and consultancy to help customers make smart business decisions and achieve long-term success in their particular market areas.

Market Driver:

One significant driver propelling the growth of the US Vegetable Oil Market is the increasing awareness among consumers regarding the health benefits associated with vegetable oils. With rising concerns over lifestyle diseases like obesity, diabetes, and cardiovascular ailments, consumers are gravitating towards healthier cooking oils. Vegetable oils, particularly those rich in unsaturated fats like olive oil and avocado oil, are perceived as healthier alternatives to traditional options like palm oil or hydrogenated oils. This shift in consumer preferences towards healthier oils is fueling the demand and driving market growth.

Market Opportunity:

An emerging opportunity within the US Vegetable Oil Market lies in the development and promotion of sustainable and eco-friendly production practices. With growing environmental consciousness among consumers, there is a rising demand for vegetable oils produced through sustainable methods that minimize environmental impact. This presents an opportunity for manufacturers to invest in technologies such as eco-friendly cultivation practices, efficient water usage, and renewable energy sources for oil extraction processes. Additionally, emphasizing certifications like organic and fair trade can further enhance market opportunities by appealing to environmentally and socially conscious consumers.

If You Have Any Query US Vegetable Oil Market Report, Visit:

Segmentation of US Vegetable Oil Market:

By Type

Palm Oil

Soybean Oil

Rapeseed Oil

Sunflower Oil

Olive Oil

Others

By Nature

Organic

Conventional

By Packaging Type

Cans

Bottles

Pouches

Others

By Application

Food Industry

Pharmaceutical

Cosmetics & Personal

Animal Feed

Industrial

By Distribution Channels

Hypermarkets/Supermarkets

Convenience Stores

Online Retail

Wholesale Distributors

Specialty Stores

Owning our reports (For More, Buy Our Report) will help you solve the following issues:

Uncertainty about the future?

Our research and insights help our clients to foresee upcoming revenue pockets and growth areas. This helps our clients to invest or divest their resources.

Understanding market sentiments?

It is imperative to have a fair understanding of market sentiments for a strategy. Our insights furnish you with a hawk-eye view on market sentiment. We keep this observation by engaging with Key Opinion Leaders of a value chain of each industry we track.

Understanding the most reliable investment centers?

Our research ranks investment centers of the market by considering their returns, future demands, and profit margins. Our clients can focus on the most prominent investment centers by procuring our market research.

Evaluating potential business partners?

Our research and insights help our clients in identifying compatible business partners.

Acquire This Reports: -

About Us:

We are technocratic market research and consulting company that provides comprehensive and data-driven market insights. We hold the expertise in demand analysis and estimation of multidomain industries with encyclopedic competitive and landscape analysis. Also, our in-depth macro-economic analysis gives a bird's eye view of a market to our esteemed client. Our team at Pristine Intelligence focuses on result-oriented methodologies which are based on historic and present data to produce authentic foretelling about the industry. Pristine Intelligence's extensive studies help our clients to make righteous decisions that make a positive impact on their business. Our customer-oriented business model firmly follows satisfactory service through which our brand name is recognized in the market.

Contact Us:

Office No 101, Saudamini Commercial Complex,

Right Bhusari Colony,

Kothrud, Pune,

Maharashtra, India - 411038 (+1) 773 382 1049 +91 - 81800 - 96367

Email: [email protected]

#US Vegetable Oil#US Vegetable Oil Market#US Vegetable Oil Market Size#US Vegetable Oil Market Share#US Vegetable Oil Market Growth#US Vegetable Oil Market Trend#US Vegetable Oil Market segment#US Vegetable Oil Market Opportunity#US Vegetable Oil Market Analysis 2023#US Vegetable Oil Market Forecast#US Vegetable Oil Industry#US Vegetable Oil Industry Size

0 notes

Text

Agricultural Enzymes Market Regional Insights and Global Forecast

Agricultural Enzymes Market Growth Strategic Market Overview and Growth Projections

The global agricultural enzymes market size was valued at USD 316.66 million in 2022. It is estimated to reach USD 548.77 million by 2031, growing at a CAGR of 6.3% during the forecast period (2023–2031).

The latest Global Agricultural Enzymes Market by straits research provides an in-depth analysis of the Agricultural Enzymes Market, including its future growth potential and key factors influencing its trajectory. This comprehensive report explores crucial elements driving market expansion, current challenges, competitive landscapes, and emerging opportunities. It delves into significant trends, competitive strategies, and the role of key industry players shaping the global Agricultural Enzymes Market. Additionally, it provides insight into the regulatory environment, market dynamics, and regional performance, offering a holistic view of the global market’s landscape through 2032.

Competitive Landscape

Some of the prominent key players operating in the Agricultural Enzymes Market are

Bayer CropScience

BASF SE

Stoller USA Inc.

Corteva Agriscience

Elemental Enzymes

American Vanguard Corporation

Bioworks Inc.

Syngenta AG.

Get Free Request Sample Report @ https://straitsresearch.com/report/agricultural-enzymes-market/request-sample

The Agricultural Enzymes Market Research report delivers comprehensive annual revenue forecasts alongside detailed analysis of sales growth within the market. These projections, developed by seasoned analysts, are grounded in a deep exploration of the latest industry trends. The forecasts offer valuable insights for investors, highlighting key growth opportunities and industry potential. Additionally, the report provides a concise dashboard overview of leading organizations, showcasing their effective marketing strategies, market share, and the most recent advancements in both historical and current market landscapes.Global Agricultural Enzymes Market: Segmentation

The Agricultural Enzymes Market segmentation divides the market into multiple sub-segments based on product type, application, and geographical region. This segmentation approach enables more precise regional and country-level forecasts, providing deeper insights into market dynamics and potential growth opportunities within each segment.

By Type

Phosphatases

Dehydrogenases

Ureases

Proteases

Other Enzyme Types

By Applications

Crop Protection

Fertility

Plant Growth Regulation

By Crop Type

Grains and Cereals

Oil Seeds and Pulses

Fruits and Vegetables

Other Crop Types

Stay ahead of the competition with our in-depth analysis of the market trends!

Buy Now @ https://straitsresearch.com/buy-now/agricultural-enzymes-market

Market Highlights:

A company's revenue and the applications market are used by market analysts, data analysts, and others in connected industries to assess product values and regional markets.

But not limited to: reports from corporations, international Organization, and governments; market surveys; relevant industry news.

Examining historical market patterns, making predictions for the year 2022, as well as looking forward to 2032, using CAGRs (compound annual growth rates)

Historical and anticipated data on demand, application, pricing, and market share by country are all included in the study, which focuses on major markets such the United States, Europe, and China.

Apart from that, it sheds light on the primary market forces at work as well as the obstacles, opportunities, and threats that suppliers face. In addition, the worldwide market's leading players are profiled, together with their respective market shares.

Goals of the Study

What is the overall size and scope of the Agricultural Enzymes Market market?

What are the key trends currently influencing the market landscape?

Who are the primary competitors operating within the Agricultural Enzymes Market market?

What are the potential growth opportunities for companies in this market?

What are the major challenges or obstacles the market is currently facing?

What demographic segments are primarily targeted in the Agricultural Enzymes Market market?

What are the prevailing consumer preferences and behaviors within this market?

What are the key market segments, and how do they contribute to the overall market share?

What are the future growth projections for the Agricultural Enzymes Market market over the next several years?

How do regulatory and legal frameworks influence the market?

About Straits Research

Straits Research is dedicated to providing businesses with the highest quality market research services. With a team of experienced researchers and analysts, we strive to deliver insightful and actionable data that helps our clients make informed decisions about their industry and market. Our customized approach allows us to tailor our research to each client's specific needs and goals, ensuring that they receive the most relevant and valuable insights.

Contact Us

Email: [email protected]

Tel: UK: +44 203 695 0070, USA: +1 646 905 0080

0 notes

Text

Cottonseed Oil Market Forecast: Trends and Growth

Cottonseed oil, derived from the seeds of cotton plants, is widely used in food processing, frying, cosmetics, and biodiesel production. Over the years, the cottonseed oil market has seen steady growth, fueled by its affordability, versatility, and applications across various industries. As we look ahead, the market dynamics are shaped by several factors, including consumer health concerns, environmental sustainability, and advancements in technology. This article explores the projected growth of the cottonseed oil market, key drivers, challenges, and emerging trends that will influence its future trajectory.

Market Overview

Cottonseed oil holds a significant share in the global vegetable oils market. Known for its mild flavor and high smoke point, cottonseed oil is commonly used in cooking, especially for frying and baking. It is also employed in the manufacturing of processed foods, snack foods, and salad dressings. Additionally, cottonseed oil is gaining traction in personal care products, such as soaps, lotions, and shampoos, due to its beneficial properties for skin care.

The cottonseed oil market is expected to grow in the coming years, driven by demand in both food and industrial applications. However, market growth will be influenced by various factors, including competition from other oils, shifting consumer preferences, and global environmental concerns.

Key Drivers of the Cottonseed Oil Market

Growing Demand for Processed Foods The demand for packaged and processed foods continues to rise globally, particularly in emerging markets. This trend has directly increased the demand for edible oils, including cottonseed oil. The oil’s use in frying, snacks, and fast-food products, combined with its affordability, makes it a popular choice among food manufacturers.

Affordable and Versatile Oil Cottonseed oil remains one of the most cost-effective oils, offering a wide range of applications at a relatively low price point compared to other premium oils like olive and avocado oil. Its mild flavor and high smoke point make it ideal for deep frying and cooking, which fuels its popularity among restaurants, fast-food chains, and households.

Expansion of Cotton Cultivation Cotton is one of the most widely cultivated crops globally, with major cotton-producing countries like China, India, the United States, and Brazil driving supply. As cotton production continues to grow, cottonseed oil production is poised to increase as well, ensuring a stable supply of the oil for the global market.

Biofuel Production The global push towards renewable energy sources and biofuels has created an additional avenue for the cottonseed oil market. Cottonseed oil is being explored as a feedstock for biodiesel production, making it an attractive option for countries focusing on reducing their carbon footprint and promoting cleaner energy sources.

Challenges Facing the Cottonseed Oil Market

Health Concerns A major challenge faced by the cottonseed oil market is the growing health concerns over its fatty acid profile. Cottonseed oil contains a high level of omega-6 fatty acids and trans fats, which have been associated with adverse health effects, particularly in relation to heart health. As consumers become more health-conscious, the demand for oils with better nutritional profiles, such as olive and canola oils, may affect cottonseed oil’s growth.

Environmental Impact of Cotton Farming Cotton farming is water-intensive and often relies heavily on pesticides and fertilizers, leading to environmental concerns regarding water use and soil degradation. As sustainability becomes a more prominent issue for consumers, there is increasing demand for environmentally friendly, non-GMO, and organic products, including oils. This could potentially limit the market for conventionally produced cottonseed oil.

Intense Competition The cottonseed oil market faces stiff competition from other vegetable oils such as soybean oil, sunflower oil, and palm oil. These oils not only offer competitive prices but are also perceived as healthier alternatives in some regions, especially in developed markets. This competition may dampen cottonseed oil’s market share, particularly in regions where consumers are increasingly health-conscious.

Price Volatility Cottonseed oil is closely tied to the price of cotton, which is subject to fluctuations due to weather conditions, global demand, and crop yields. Price volatility in cotton farming directly impacts the cost of cottonseed oil production, potentially limiting profitability for manufacturers and leading to higher prices for consumers.

Emerging Trends in the Cottonseed Oil Market

Healthier Variants and Product Innovation As consumers demand healthier oils, manufacturers are exploring ways to improve the fatty acid profile of cottonseed oil. Innovations such as cold-pressed and non-GMO cottonseed oils are gaining popularity. Offering blends of cottonseed oil with other oils that have more favorable health attributes could also help manufacturers meet the evolving needs of health-conscious consumers.

Sustainability Initiatives With environmental sustainability becoming an essential factor for both producers and consumers, the cottonseed oil industry is likely to see more efforts aimed at sustainable farming practices. This includes reducing water usage, minimizing pesticide application, and focusing on organic cotton cultivation. Such efforts could appeal to eco-conscious consumers and help mitigate the environmental concerns surrounding cottonseed oil production.

Growth in Emerging Markets The cottonseed oil market has significant growth potential in emerging economies, particularly in regions like Asia-Pacific, Africa, and Latin America. Rising disposable incomes, changing lifestyles, and increasing urbanization are leading to higher consumption of processed foods, creating an opportunity for cottonseed oil to tap into new markets. These regions are expected to become key drivers of market growth in the coming years.

Rising Demand for Biodiesel The biofuel market, particularly biodiesel made from vegetable oils, is expected to continue growing as countries aim to reduce their dependence on fossil fuels. Cottonseed oil’s potential as a biodiesel feedstock opens up new opportunities in this sector, helping to diversify its uses beyond food.

Market Outlook

The cottonseed oil market is expected to experience moderate growth in the next decade, driven by increased demand in food processing, biofuel production, and cosmetics. However, challenges such as health concerns, competition from other oils, and environmental sustainability issues will continue to shape the market landscape. To capitalize on growth opportunities, manufacturers will need to focus on product innovation, sustainability practices, and expanding into emerging markets.

Overall, the cottonseed oil market is poised for steady growth, but its success will depend on how effectively the industry can address these challenges and adapt to the evolving consumer landscape.

Get Free Sample and ToC : https://www.pristinemarketinsights.com/get-free-sample-and-toc?rprtdtid=NDc1&RD=Cottonseed-Oil-Market-Report

0 notes

Photo

VEGOILS-Palm oil falls on Dalian weakness and stronger ringgit KUALA LUMPUR, Nov 18 (Reuters) - Malaysian palm oil futures fell in early trade on Monday, tracking weakness in rival Dalian oils and pressured by a stronger ringgit. The benchmark palm oil contract FCPOc3 for February delivery on the Bursa Malaysia Derivatives Exchange slid 93 ringgit, or 1.84%, to 4,960 ringgit ($1,111.86) a metric ton, as of 0247 GMT. The contract rose 2.5% in the previous session. FUNDAMENTALS Dalian's most-active soyoil contract DBYcv1 fell 1.4%, while its palm oil contract DCPcv1 lost 1.24%. Soyoil prices on the Chicago Board of Trade BOcv1 were up 0.02%. Palm oil tracks price movements of rival edible oils, as they compete for a share of the global vegetable oils market. The ringgit MYR=, palm's currency of trade, strengthened 0.16% against the dollar, making the commodity more expensive for buyers holding foreign currencies. Oil prices edged up after fighting between Russia and Ukraine intensified over the weekend, although concerns about fuel demand in China, the world's second-largest consumer, and forecasts of a global oil surplus weighed on markets. Stronger crude oil futures make palm a more attractive option for biodiesel feedstock. Chicago soy futures rose for a second session on concerns that China's removal of export incentives for used cooking oil, a low-cost feedstock that many U.S. biofuels makers use instead of domestically produced soyoil, could curtail imports. Palm oil may revisit its Nov. 11 high of 5,202 ringgit per metric ton, as the strong gain from the Nov. 14 low of 4,826 ringgit suggests a resumption of the uptrend, Reuters technical analyst Wang Tao said. MARKET NEWS Global stocks began the week on firmer footing ahead of a highly anticipated earnings release from Nvidia, while in Japan, a speech from its central bank's head left markets none the wiser on the country's rate outlook.

0 notes

Text

Bioenergy Market: Role in Achieving Global Decarbonization Targets

The Bioenergy Market size was valued at USD 124.32 billion in 2023 and is expected to grow to USD 228.41 billion by 2031 and grow at a CAGR of 7.9 % over the forecast period of 2024–2031.

The global bioenergy market is expected to experience significant growth from 2024 to 2031, fueled by the growing demand for renewable energy solutions, government policies promoting sustainability, and innovations in bioenergy technologies. Bioenergy, which includes solid biomass, liquid biofuels, biogas, and other bio-based energy sources, is emerging as a key component in the transition to cleaner and more sustainable energy systems. The market is experiencing growth across various applications, including power generation, heating, and transportation, driven by the need to reduce reliance on fossil fuels and lower greenhouse gas emissions.

Market Segmentation

By Product Type

Solid Biomass:

Solid biomass, derived from plant-based materials like wood chips, agricultural residues, and dedicated energy crops, is one of the most commonly used forms of bioenergy. It is primarily used in power generation and heating applications, replacing conventional fossil fuels in boilers, furnaces, and power plants.

Liquid Biofuel:

This category includes bioethanol, biodiesel, and advanced biofuels produced from feedstocks such as corn, sugarcane, and vegetable oils. Liquid biofuels are widely used in transportation as an alternative to gasoline and diesel, offering a cleaner energy source for vehicles.

Biogas:

Biogas is produced from the anaerobic digestion of organic materials such as agricultural waste, food waste, and sewage sludge. It is primarily used in power generation and heating applications and is gaining traction as a clean energy source for decentralized energy systems.

Others:

This segment includes emerging forms of bioenergy such as algae-based biofuels, which have a higher energy yield than traditional feedstocks, and other advanced bioenergy sources. These products are expected to gain importance in the coming years due to their potential to meet diverse energy needs.

By Feedstock

Agricultural Waste:

Agricultural residues like straw, rice husks, and corn stover are abundant feedstocks used for bioenergy production. These materials are often considered waste, but they are increasingly utilized to generate power, heat, and biofuels, offering both environmental and economic benefits.

Wood Waste:

Wood waste, including sawdust, wood chips, and bark, is one of the primary feedstocks for solid biomass production. It is widely used in both residential and industrial heating systems and power plants, especially in regions with abundant forestry resources.

Solid Waste:

Municipal solid waste, industrial waste, and food waste are gaining attention as feedstocks for biogas production. The conversion of waste to energy not only helps reduce landfill accumulation but also offers a sustainable solution for waste management.

Others:

Other feedstocks include algae, food scraps, and sewage sludge. These feedstocks are part of emerging trends in bioenergy, offering higher efficiency in energy production and lower carbon emissions.

By Application

Power Generation:

Bioenergy is increasingly used for renewable power generation, both on a small scale (e.g., biomass-fired power plants) and large scale (e.g., biogas-based electricity generation). Solid biomass and biogas are the primary sources for power generation, as they can provide continuous and reliable electricity with lower emissions compared to conventional fossil fuels.

Heat Generation:

Bioenergy is also widely used in heating applications for both residential and industrial purposes. Solid biomass, such as wood pellets and chips, is used in boilers and furnaces, while biogas is utilized in combined heat and power (CHP) systems.

Transportation:

Liquid biofuels, particularly bioethanol and biodiesel, are commonly used in the transportation sector as alternatives to conventional gasoline and diesel fuels. These biofuels help reduce carbon emissions and contribute to energy security by decreasing reliance on petroleum-based fuels.

Others:

Bioenergy also finds applications in various industries such as chemicals, food and beverage, and hydrogenation processes, where bio-based feedstocks are used to produce bio-based chemicals, fuels, and other products.

By Region

North America:

The United States and Canada are significant players in the global bioenergy market. North America has established biofuel industries, particularly in the U.S., where bioethanol production is a major contributor to the market. The region also benefits from a large agricultural base and advanced technologies for bioenergy production.

Europe:

Europe remains one of the largest markets for bioenergy, driven by the European Union’s ambitious renewable energy goals and policy support. Countries like Germany, Sweden, and the UK are at the forefront of bioenergy adoption, particularly in biogas, biofuels, and biomass power generation.

Asia Pacific:

The Asia Pacific region is expected to experience the fastest growth in the bioenergy market, particularly in countries like China, India, and Japan. These countries have vast agricultural resources and are increasingly focusing on renewable energy projects to address rising energy demand and environmental concerns.

Latin America:

Latin America, with countries like Brazil and Argentina, has significant bioenergy potential. Brazil is a global leader in bioethanol production, especially from sugarcane, and other Latin American countries are expanding their bioenergy capabilities in power generation and biofuel production.

Middle East & Africa (MEA):

The MEA region is gradually adopting bioenergy, particularly in areas like waste-to-energy projects and biofuels. Countries in the region are focusing on diversifying their energy mix and investing in renewable energy solutions, including bioenergy.

Key Drivers of Market Growth

Government Support and Regulations: Policies promoting renewable energy adoption, including subsidies for biofuels, tax incentives for bioenergy projects, and stricter emissions regulations, are driving the growth of the bioenergy market.

Technological Advancements: Continuous innovations in bioenergy technologies are improving the efficiency and scalability of bioenergy systems. The development of advanced biofuels and biogas upgrading technologies is enabling the industry to meet growing energy demands.

Sustainability and Carbon Reduction Goals: The increasing global focus on sustainability and reducing greenhouse gas emissions is accelerating the transition to bioenergy, which is considered a cleaner and more sustainable energy source compared to fossil fuels.

Energy Security and Independence: As countries seek to reduce their reliance on imported fossil fuels, bioenergy offers a reliable and indigenous energy source that can contribute to national energy security.

Market Outlook and Forecast

The global bioenergy market is expected to grow significantly over the forecast period (2024–2031). The market is anticipated to benefit from technological advancements, regulatory support, and increasing demand for clean and sustainable energy solutions. By product type, solid biomass and liquid biofuels are expected to continue dominating the market, while biogas production and advanced biofuels are projected to gain share in the coming years.

Read Complete Report Details of Bioenergy Market 2024–2031@ https://www.snsinsider.com/reports/bioenergy-market-3330

Conclusion

Bioenergy is a key component of the global energy transition, offering sustainable solutions for power generation, heat production, and transportation. The market’s expansion will be driven by innovations in technology, increasing government support, and the global push towards reducing carbon emissions. As bioenergy becomes a more significant part of the renewable energy mix, it is poised to play a crucial role in shaping the future of global energy systems.

About Us:

SNS Insider is a global leader in market research and consulting, shaping the future of the industry. Our mission is to empower clients with the insights they need to thrive in dynamic environments. Utilizing advanced methodologies such as surveys, video interviews, and focus groups, we provide up-to-date, accurate market intelligence and consumer insights, ensuring you make confident, informed decisions. Contact Us: Akash Anand — Head of Business Development & Strategy [email protected] Phone: +1–415–230–0044 (US) | +91–7798602273 (IND)

0 notes

Text

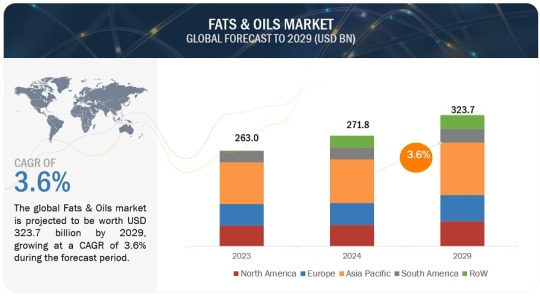

Fats and Oils Market Set for Rapid Growth: Trends, Innovations, and Consumer Demands Driving Expansion

The global fats and oils market is projected to be valued at USD 271.8 billion in 2024, with a compound annual growth rate (CAGR) of 3.6%, expected to reach USD 323.7 billion by 2029. This market is undergoing significant transformations and innovations. The demand for fats and oils goes beyond culinary uses, impacting various sectors, including animal feed, oleochemicals, and biofuels.

Vegetable oils and animal fats are essential components in the food industry, contributing to the texture, flavor, and shelf life of processed foods. Palm, rapeseed, sunflower, and soybean oils are the most widely used oils worldwide, thanks to their versatile applications in both food and non-food products. Animal fats, such as butter and lard, are particularly important in baking, where they are prized for their rich, distinctive flavors.

Fats and Oils Market Trends

Here are some key trends in the Fats and Oils Market:

Health Consciousness: As consumers become more health-conscious, there’s a growing demand for healthier fats, such as olive oil, avocado oil, and coconut oil. This shift is leading to the popularity of oils with favorable fatty acid profiles and beneficial nutrients.

Plant-Based Oils: The trend toward plant-based diets is driving the demand for oils derived from plants. Oils like sunflower, canola, and palm oil are gaining traction due to their versatility and health benefits. Sustainable Sourcing: Environmental sustainability is becoming increasingly important for consumers and manufacturers. Brands are seeking sustainably sourced oils and fats, leading to a rise in certifications like RSPO (Roundtable on Sustainable Palm Oil).

Functional Fats: There is a growing interest in functional fats that offer additional health benefits, such as omega-3 and omega-6 fatty acids. These are often marketed for their heart health benefits and ability to support cognitive function.

Food Innovation: The food and beverage industry is continually innovating with new formulations that incorporate unique fats and oils to enhance flavor, texture, and nutritional value. This includes the use of fats for plant-based and alternative protein products.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=6198812

Vegetable Sources of Fats and Oils Expected to Lead Market Share During the Forecast Period.

Vegetable-based oils are expected to maintain the largest share of the fats and oils market throughout the forecast period. This dominance can be attributed to their versatility, health benefits, and wide availability. Oils from sources like soybean, palm, and sunflower are commonly used in cooking and food processing due to their broad range of applications and consumer preference for healthier alternatives to animal fats. These oils offer essential fatty acids and are considered more beneficial for health. Moreover, innovations in agricultural practices and biotechnology have boosted vegetable oil production, ensuring a consistent and cost-effective supply. Their adaptability in both food and industrial uses reinforces their leading role in the market.

The Food Application Segment is Projected to Dominate the Fats and Oils Market Share Throughout the Forecast Period.

In the application segment, the food industry is projected to hold the largest share of the fats and oils market throughout the forecast period. Fats and oils play a vital role in enhancing flavor, texture, and preservation across various food products. They are essential in cooking and baking, providing desirable characteristics like crispiness and richness. Additionally, fats and oils act as carriers for fat-soluble vitamins and flavors, boosting consumer appeal. The growing demand for processed and convenient foods, coupled with an increasing interest in diverse culinary experiences, further drives the dominance of food applications in this market segment.

Top Fats and Oils Companies

The key players in the market are ADM (US), Wilmar International Ltd (Singapore), Cargill, Incorporated (US), Bunge (US), Kaula Lumpur Kepong Berhad (Malaysia), Olam Agri Holdings Pte Ltd (India), Manildra Group (Australia), Mewah Group (Singapore), Associated British Foods plc (UK), United Plantations Berhad (Malaysia), Ajinomoto Co., Inc. (Japan), Fuji Oil Co., Ltd. (Japan), Oleo-Fats (Philippines), Borges Agricultural and Industrial Edible Oils, S.A.U. (Spain), K S Oils Limited (India), CSM Ingredients (US), SD Guthrie International Zwijndrecht Refinery B.V. (Netherlands), Musim Mas Group (Singapore), Richardson International Limited (Canada), and AAK AB (Sweden).

#Fats and Oils Market#Fats and Oils#Fats and Oils Market Size#Fats and Oils Market Share#Fats and Oils Market Growth#Fats and Oils Market Trends#Fats and Oils Market Forecast#Fats and Oils Market Analysis#Fats and Oils Market Report#Fats and Oils Market Scope#Fats and Oils Market Overview#Fats and Oils Market Outlook#Fats and Oils Market Drivers#Fats and Oils Industry#Fats and Oils Market Companies

0 notes

Text

Agricultural Enzymes Market Applications in Organic and Conventional Farming

Agricultural Enzymes Market Growth Strategic Market Overview and Growth Projections

The global agricultural enzymes market size was valued at USD 316.66 million in 2022. It is estimated to reach USD 548.77 million by 2031, growing at a CAGR of 6.3% during the forecast period (2023–2031).

The latest Global Agricultural Enzymes Market by straits research provides an in-depth analysis of the Agricultural Enzymes Market, including its future growth potential and key factors influencing its trajectory. This comprehensive report explores crucial elements driving market expansion, current challenges, competitive landscapes, and emerging opportunities. It delves into significant trends, competitive strategies, and the role of key industry players shaping the global Agricultural Enzymes Market. Additionally, it provides insight into the regulatory environment, market dynamics, and regional performance, offering a holistic view of the global market’s landscape through 2032.

Competitive Landscape

Some of the prominent key players operating in the Agricultural Enzymes Market are

Bayer CropScience

BASF SE

Stoller USA Inc.

Corteva Agriscience

Elemental Enzymes

American Vanguard Corporation

Bioworks Inc.

Syngenta AG.

Get Free Request Sample Report @ https://straitsresearch.com/report/agricultural-enzymes-market/request-sample

The Agricultural Enzymes Market Research report delivers comprehensive annual revenue forecasts alongside detailed analysis of sales growth within the market. These projections, developed by seasoned analysts, are grounded in a deep exploration of the latest industry trends. The forecasts offer valuable insights for investors, highlighting key growth opportunities and industry potential. Additionally, the report provides a concise dashboard overview of leading organizations, showcasing their effective marketing strategies, market share, and the most recent advancements in both historical and current market landscapes.Global Agricultural Enzymes Market: Segmentation

The Agricultural Enzymes Market segmentation divides the market into multiple sub-segments based on product type, application, and geographical region. This segmentation approach enables more precise regional and country-level forecasts, providing deeper insights into market dynamics and potential growth opportunities within each segment.

By Type

Phosphatases

Dehydrogenases

Ureases

Proteases

Other Enzyme Types

By Applications

Crop Protection

Fertility

Plant Growth Regulation

By Crop Type

Grains and Cereals

Oil Seeds and Pulses

Fruits and Vegetables

Other Crop Types

Stay ahead of the competition with our in-depth analysis of the market trends!

Buy Now @ https://straitsresearch.com/buy-now/agricultural-enzymes-market

Market Highlights:

A company's revenue and the applications market are used by market analysts, data analysts, and others in connected industries to assess product values and regional markets.

But not limited to: reports from corporations, international Organization, and governments; market surveys; relevant industry news.

Examining historical market patterns, making predictions for the year 2022, as well as looking forward to 2032, using CAGRs (compound annual growth rates)

Historical and anticipated data on demand, application, pricing, and market share by country are all included in the study, which focuses on major markets such the United States, Europe, and China.

Apart from that, it sheds light on the primary market forces at work as well as the obstacles, opportunities, and threats that suppliers face. In addition, the worldwide market's leading players are profiled, together with their respective market shares.

Goals of the Study

What is the overall size and scope of the Agricultural Enzymes Market market?

What are the key trends currently influencing the market landscape?

Who are the primary competitors operating within the Agricultural Enzymes Market market?

What are the potential growth opportunities for companies in this market?

What are the major challenges or obstacles the market is currently facing?

What demographic segments are primarily targeted in the Agricultural Enzymes Market market?

What are the prevailing consumer preferences and behaviors within this market?

What are the key market segments, and how do they contribute to the overall market share?

What are the future growth projections for the Agricultural Enzymes Market market over the next several years?

How do regulatory and legal frameworks influence the market?

About Straits Research

Straits Research is dedicated to providing businesses with the highest quality market research services. With a team of experienced researchers and analysts, we strive to deliver insightful and actionable data that helps our clients make informed decisions about their industry and market. Our customized approach allows us to tailor our research to each client's specific needs and goals, ensuring that they receive the most relevant and valuable insights.

Contact Us

Email: [email protected]

Tel: UK: +44 203 695 0070, USA: +1 646 905 0080

#Agricultural Enzymes Market Market#Agricultural Enzymes Market Market Share#Agricultural Enzymes Market Market Size#Agricultural Enzymes Market Market Research#Agricultural Enzymes Market Industry#What is Agricultural Enzymes Market?

0 notes

Text

Ethoxylates Industry In-depth Analysis and Forecast Report, 2030

The global ethoxylates market was valued at USD 12.1 billion in 2023 and is anticipated to grow at a compound annual growth rate (CAGR) of 2.9% from 2024 to 2030. Ethoxylates are experiencing heightened demand due to their versatility across various industries, such as paints and coatings, textile processing, personal care, agriculture, and pulp and paper. This demand is further driven by trends toward low-rinse detergents, increased use of ethoxylates in healthcare, and a rising preference for eco-friendly alternatives, including alcohol ethoxylates in cosmetic applications.

Ethoxylates are synthesized by combining ethylene oxide (EO) or other epoxides with different substances, such as alcohols, acids, amines, or vegetable oils, at specific molar ratios to create compounds with tailored properties. Their unique hydrophobic (water-repelling) and hydrophilic (water-attracting) characteristics enable them to dissolve effectively in both oil and water, providing high efficacy in reducing surface tension between various liquids or between liquids and gases. These qualities, along with easy water solubility, surface wetting, and minimal aquatic toxicity, make them ideal for a range of formulations.

Gather more insights about the market drivers, restrains and growth of the Ethoxylates Market

There is growing demand for bio-based ethoxylates due to heightened consumer awareness of environmental health and the adverse effects of synthetic chemicals. Bio-based ethoxylates, which are derived from renewable sources like plant oils, sugars, and fatty acids, offer a sustainable and eco-friendly alternative. They have a lower carbon footprint and avoid releasing hazardous by-products, making them well-suited for green applications in personal care, agrochemicals, and industrial cleaning. This trend is expected to accelerate bio-based ethoxylates market growth over the coming years.

Ethoxylated alcohols, in particular, enhance the foaming, wetting, solubility, and degreasing properties of detergents, making them highly effective for removing grease from fabrics. As population growth and disposable incomes increase, particularly in developing regions, so does the demand for high-efficiency laundry detergents and washing machines, leading to a notable increase in liquid detergent consumption.

Application Segmentation Insights:

In 2023, the household and personal care segment held the largest revenue share, accounting for 32.9% of the market. This growth is due to ethoxylates’ broad usage in producing household cleaning products, including liquid and powder laundry detergents, dishwashing detergents, fabric softeners, window and carpet cleaners, oven cleaners, air fresheners, and hard surface cleaners. Ethoxylates help these products achieve effective cleaning, wetting, and foaming, which are essential properties for household cleaning applications.

The pharmaceutical industry is anticipated to experience the fastest CAGR of 3.7% over the forecast period. In pharmaceutical manufacturing, ethoxylates are used as emulsifying agents in the formulation of ointments, tablets, syrups, and gels. Rising rates of chronic diseases, attributed to environmental pollution and general health neglect, create demand for innovative pharmaceutical formulations, thus driving the need for ethoxylates in drug formulation. Additionally, demand for generic pharmaceuticals, particularly in developing nations, is expected to boost the consumption of ethoxylates used in these products.

In conclusion, the ethoxylates market is poised for steady growth driven by their increasing use across industries and the shift toward eco-friendly, bio-based options. The expanding applications of ethoxylates, particularly in household care and pharmaceuticals, underscore their critical role in meeting global consumer demands for effective and sustainable products.

Order a free sample PDF of the Ethoxylates Market Intelligence Study, published by Grand View Research.

#Ethoxylates Market Research#Ethoxylates Market Forecast#Ethoxylates Market Size#Ethoxylates Industry

0 notes

Text

Ethoxylates Market Size, Growth Drivers & Global Opportunities, 2030

The global ethoxylates market was valued at USD 12.1 billion in 2023 and is anticipated to grow at a compound annual growth rate (CAGR) of 2.9% from 2024 to 2030. Ethoxylates are experiencing heightened demand due to their versatility across various industries, such as paints and coatings, textile processing, personal care, agriculture, and pulp and paper. This demand is further driven by trends toward low-rinse detergents, increased use of ethoxylates in healthcare, and a rising preference for eco-friendly alternatives, including alcohol ethoxylates in cosmetic applications.

Ethoxylates are synthesized by combining ethylene oxide (EO) or other epoxides with different substances, such as alcohols, acids, amines, or vegetable oils, at specific molar ratios to create compounds with tailored properties. Their unique hydrophobic (water-repelling) and hydrophilic (water-attracting) characteristics enable them to dissolve effectively in both oil and water, providing high efficacy in reducing surface tension between various liquids or between liquids and gases. These qualities, along with easy water solubility, surface wetting, and minimal aquatic toxicity, make them ideal for a range of formulations.

Gather more insights about the market drivers, restrains and growth of the Ethoxylates Market

There is growing demand for bio-based ethoxylates due to heightened consumer awareness of environmental health and the adverse effects of synthetic chemicals. Bio-based ethoxylates, which are derived from renewable sources like plant oils, sugars, and fatty acids, offer a sustainable and eco-friendly alternative. They have a lower carbon footprint and avoid releasing hazardous by-products, making them well-suited for green applications in personal care, agrochemicals, and industrial cleaning. This trend is expected to accelerate bio-based ethoxylates market growth over the coming years.

Ethoxylated alcohols, in particular, enhance the foaming, wetting, solubility, and degreasing properties of detergents, making them highly effective for removing grease from fabrics. As population growth and disposable incomes increase, particularly in developing regions, so does the demand for high-efficiency laundry detergents and washing machines, leading to a notable increase in liquid detergent consumption.

Application Segmentation Insights:

In 2023, the household and personal care segment held the largest revenue share, accounting for 32.9% of the market. This growth is due to ethoxylates’ broad usage in producing household cleaning products, including liquid and powder laundry detergents, dishwashing detergents, fabric softeners, window and carpet cleaners, oven cleaners, air fresheners, and hard surface cleaners. Ethoxylates help these products achieve effective cleaning, wetting, and foaming, which are essential properties for household cleaning applications.

The pharmaceutical industry is anticipated to experience the fastest CAGR of 3.7% over the forecast period. In pharmaceutical manufacturing, ethoxylates are used as emulsifying agents in the formulation of ointments, tablets, syrups, and gels. Rising rates of chronic diseases, attributed to environmental pollution and general health neglect, create demand for innovative pharmaceutical formulations, thus driving the need for ethoxylates in drug formulation. Additionally, demand for generic pharmaceuticals, particularly in developing nations, is expected to boost the consumption of ethoxylates used in these products.

In conclusion, the ethoxylates market is poised for steady growth driven by their increasing use across industries and the shift toward eco-friendly, bio-based options. The expanding applications of ethoxylates, particularly in household care and pharmaceuticals, underscore their critical role in meeting global consumer demands for effective and sustainable products.

Order a free sample PDF of the Ethoxylates Market Intelligence Study, published by Grand View Research.

#Ethoxylates Market Research#Ethoxylates Market Forecast#Ethoxylates Market Size#Ethoxylates Industry

0 notes

Text

Corn Oil Market Forecast: Growth Trends and Insights

The corn oil market has witnessed steady growth over the past decade, driven by its versatile uses in food, industrial, and cosmetic applications. As consumer preferences shift toward healthier, plant-based oils, corn oil has carved out a significant niche. With increasing demand in the food industry, its growing role in biofuel production, and advancements in extraction technology, the corn oil market is expected to experience further expansion. This article examines the forecast for the corn oil market, focusing on key growth drivers, challenges, and regional dynamics.

Market Growth Drivers

Health-Conscious Consumer Trends

The rising awareness about health and wellness among consumers is one of the most significant drivers of the corn oil market. Corn oil is rich in polyunsaturated fats, particularly omega-6 fatty acids, which have been associated with improved heart health when consumed in moderation. The growing popularity of plant-based oils, as part of balanced diets aimed at reducing the intake of saturated fats, has directly contributed to the increased demand for corn oil. As more consumers opt for healthier cooking and eating habits, corn oil’s reputation as a heart-healthy alternative to animal fats is expected to propel its market growth in the coming years.

Growth in Processed and Packaged Food Consumption

The demand for processed and packaged foods has been consistently rising, particularly in urban areas, where busy lifestyles drive the need for convenience foods. Corn oil is extensively used in the food processing industry due to its light flavor, high smoke point, and affordability. It is commonly used in frying, baking, and as a base for salad dressings, sauces, and margarines. With the continued rise in the consumption of processed foods, the demand for corn oil in food manufacturing is expected to grow steadily, contributing to the overall expansion of the market.

Increasing Demand for Biofuels

Another major factor driving the growth of the corn oil market is the increasing demand for biofuels. Corn oil is a key feedstock for biodiesel production, especially in North America, where large-scale corn cultivation and biofuel policies create a favorable environment for the use of corn oil as a renewable energy source. Governments around the world are pushing for renewable energy sources to reduce reliance on fossil fuels and combat climate change. As biofuels become an integral part of the energy transition, the demand for corn oil is expected to increase, particularly in markets like the U.S. and Brazil, where biofuel production is a significant industry.

Technological Advancements in Extraction Methods

The development of new technologies for oil extraction is also expected to boost the supply of corn oil. Advancements in cold-pressing, solvent extraction, and refining techniques are enhancing the yield and quality of corn oil. These innovations make it possible to extract oil more efficiently from corn kernels while maintaining the nutritional integrity of the oil. As extraction methods become more cost-effective and sustainable, manufacturers are better positioned to meet the growing global demand for corn oil.

Challenges Affecting the Market

Fluctuating Raw Material Prices

One of the primary challenges facing the corn oil market is the price volatility of corn. As the price of corn fluctuates due to factors such as crop yields, weather conditions, and global demand, corn oil prices may also experience similar volatility. This can affect the stability of the market and impact profit margins for producers. Additionally, price fluctuations in corn may lead to higher production costs, which could be passed on to consumers, potentially dampening demand.

Competition from Other Vegetable Oils

The corn oil market faces intense competition from other vegetable oils, such as soybean oil, sunflower oil, and canola oil. These oils are often considered healthier alternatives and are readily available at competitive prices. Corn oil’s market share may be challenged by the increasing popularity of these oils, especially in regions where they are more locally available and cost-effective. To maintain its position, corn oil producers will need to differentiate their products by emphasizing health benefits, sustainability, and quality.

Environmental and Sustainability Concerns

The large-scale cultivation of corn, particularly for industrial applications like biofuels, raises concerns about environmental sustainability. Corn farming can lead to soil depletion, water usage concerns, and the need for chemical fertilizers and pesticides. Environmental groups and consumers are increasingly aware of the ecological impact of agricultural practices, and any negative perception of corn farming could influence the corn oil market. Manufacturers must address these concerns by promoting sustainable farming practices and eco-friendly production methods.

Regional Insights

North America

North America is the largest producer and consumer of corn oil, particularly in the United States, where corn is a staple crop. The U.S. corn oil market benefits from the country’s vast agricultural resources and well-established biofuel industry. As the demand for biofuels grows, the corn oil market is expected to continue to thrive, driven by both domestic and international demand for renewable energy. Additionally, the health-conscious trends in North America, especially among millennials, will further boost corn oil consumption in the food sector.

Asia Pacific

The Asia Pacific region is expected to witness significant growth in the corn oil market due to increasing urbanization, changing lifestyles, and rising disposable incomes. Countries like China and India are experiencing a shift toward healthier cooking oils as more people become aware of the benefits of vegetable oils. The demand for corn oil in food processing and cosmetics is expected to rise in these countries, making Asia Pacific one of the fastest-growing regions in the corn oil market.

Europe

Europe represents another important market for corn oil, particularly in countries like Germany, France, and Italy. The demand for healthier and sustainable cooking oils is growing in Europe, and corn oil is increasingly being recognized as a viable option. Moreover, the European Union’s emphasis on renewable energy and biofuels is likely to support the growth of the corn oil market in the region, particularly in biodiesel production.

Market Outlook

The global corn oil market is poised for steady growth over the next several years, driven by health trends, increasing applications in biofuels, and rising demand for processed foods. Despite challenges such as raw material price volatility and competition from other vegetable oils, the market’s growth prospects remain robust. Technological advancements in extraction and growing awareness of the health benefits of corn oil will continue to support the demand for this versatile oil.

As sustainability becomes increasingly important, producers who invest in sustainable practices and innovative technologies are likely to lead the market. The corn oil market is expected to expand across North America, Asia Pacific, and Europe, with North America continuing to be the largest market due to its strong biofuel industry and consumer preferences for healthier oils.

Get Free Sample and ToC : https://www.pristinemarketinsights.com/get-free-sample-and-toc?rprtdtid=NDc0&RD=Corn-Oil-Market-Report

0 notes

Text

GRAINS-Wheat rises after dropping to 2-1/2-month low on surging US dollar CANBERRA, Nov 14 (Reuters) - Chicago wheat futures rose on Thursday after plunging to a 2-1/2-month low in the previous session as the U.S. dollar surged to its strongest in a year, making U.S. farm exports less competitive on global markets. Corn and soybean futures also steadied after three consecutive days of declines due to the dollar's pressure, a faltering vegetable oil rally and concerns that a debt swap announced by China last week will fail to stoke its economy. FUNDAMENTALS The most-active wheat contract on the Chicago Board of Trade Wv1 was up 0.5% at $5.43-1/2 a bushel at 0152 GMT after falling to $5.36-1/2, lowest since Aug. 29. CBOT soybeans Sv1 rose 0.4% at $10.11-1/4 a bushel and corn Cv1 climbed 0.2% to $4.27-1/4 a bushel. The dollar .DXY rose to its strongest since Nov 2023 after U.S. consumer price data showed progress toward low inflation has slowed, which could result in fewer interest rate cuts by the Federal Reserve next year. "Wheat prices are poised for a possible retest of the August lows as rains improve the outlook for both the Black Sea and U.S. Southern Plains and as the markets remove some of the war premium from the market on expectations that the Ukraine war will come to an end," StoneX analyst Arlan Suderman said. The Rosario grains exchange cut its estimate for Argentina's 2024-25 wheat harvest by 700,000 metric tons to 18.8 million tons due to a drought, but raised its 2024-25 soybean forecast thanks to recent rains. Farm office FranceAgriMer lowered forecasts for French 2024-25 soft wheat exports within and outside the European Union, with total shipments now expected to plunge 40% after one of the country's worst harvests in 40 years. Soybeans lost support from a rally in vegetable oils, with CBOT and Dalian soyoil and Malaysian palm oil futures falling sharply this week. BOZ24, DBYcv1, FCPOc3 China's soybean imports are likely to drop to 98.8 million tons in the marketing year ending Sept 2025 from 109.4 million tons in the prior year, an executive of China National Cereals, Oils and Foodstuffs Corporation (COFCO) said. American farmers are worried that President-elect Donald Trump's sweeping tariffs will curb their China access, but they could also lure companies, hungry for domestic supplies, to build more U.S. crushing plants. MARKETS NEWS A gauge of global stocks fell for a second straight session on Wednesday and longer-dated U.S. Treasury yields rose in choppy trade as investors assessed the latest U.S. inflation data and the Fed's path of interest rates.

0 notes

Text

Argan Oil Market Blossoms! 🌿 Forecasted Growth from $0.5B in 2023 to $1.2B by 2033 with a Strong 9.2% CAGR!

Argan oil Market : Argan oil, often called “liquid gold,” has become a highly sought-after product in the beauty and wellness industry due to its rich nutrient profile and versatile benefits. Extracted from the kernels of the argan tree, native to Morocco, this oil is packed with essential fatty acids, antioxidants, and Vitamin E, which makes it a powerful moisturizer and rejuvenator for hair, skin, and nails. Many swear by argan oil’s ability to reduce dryness, improve skin elasticity, and even minimize signs of aging. With growing consumer interest in natural and organic beauty solutions, argan oil continues to shine as a go-to choice for achieving healthy, glowing skin.

To Request Sample Report :https://www.globalinsightservices.com/request-sample/?id=GIS32166 &utm_source=SnehaPatil&utm_medium=Article

Beyond beauty, argan oil is also finding its way into culinary uses due to its nutty flavor and health benefits when used in cooking. Rich in heart-healthy fats, it’s being used as a finishing oil for salads, couscous, and roasted vegetables. As more consumers focus on holistic health and wellness, argan oil’s versatility is making it a staple in both beauty routines and kitchens worldwide. This rising popularity is pushing demand for ethically-sourced and sustainably-produced argan oil, reinforcing the importance of eco-conscious and fair-trade practices.

#ArganOil #NaturalBeauty #OrganicSkincare #LiquidGold #EcoFriendlyBeauty #MoroccanOil #BeautyEssentials #SkinCareRoutine #HealthyGlow #HairCareEssentials #WellnessTrends #BeautyFromNature #NaturalGlow #HolisticHealth #EcoConscious

0 notes

Text

Global Glucaric Acid Market Analysis 2024: Size Forecast and Growth Prospects

The glucaric acid global market report 2024 from The Business Research Company provides comprehensive market statistics, including global market size, regional shares, competitor market share, detailed segments, trends, and opportunities. This report offers an in-depth analysis of current and future industry scenarios, delivering a complete perspective for thriving in the industrial automation software market.

Glucaric Acid Market, 2024 report by The Business Research Company offers comprehensive insights into the current state of the market and highlights future growth opportunities.

Market Size - The glucaric acid market size has grown strongly in recent years. It will grow from $0.98 billion in 2023 to $1.06 billion in 2024 at a compound annual growth rate (CAGR) of 8.7%. The growth in the historic period can be attributed to pharmaceutical demand, food additive adoption, environmental awareness, government regulations, R&D innovation, sustainable chemical demand, industrial cleaning applications, and personal care product demand.

The glucaric acid market size is expected to see strong growth in the next few years. It will grow to $1.50 billion in 2028 at a compound annual growth rate (CAGR) of 9.1%. The growth in the forecast period can be attributed to a focus on a focus on green chemistry, bio-based polymer integration, capacity expansion, diversification in agriculture and textiles, and increased adoption of green packaging solutions. Major trends in the forecast period include glucaric acid in green packaging, bio-based material exploration, sustainable polymer integration, renewable energy applications, biotechnological production methods, eco-friendly construction materials, and collaborative innovation efforts.

Order your report now for swift delivery @ https://www.thebusinessresearchcompany.com/report/glucaric-acid-global-market-report

Scope Of Glucaric Acid Market The Business Research Company's reports encompass a wide range of information, including:

1. Market Size (Historic and Forecast): Analysis of the market's historical performance and projections for future growth.

2. Drivers: Examination of the key factors propelling market growth.

3. Trends: Identification of emerging trends and patterns shaping the market landscape.

4. Key Segments: Breakdown of the market into its primary segments and their respective performance.

5. Focus Regions and Geographies: Insight into the most critical regions and geographical areas influencing the market.

6. Macro Economic Factors: Assessment of broader economic elements impacting the market.

Glucaric Acid Market Overview

Market Drivers - The rising demand for eco-friendly and bio-based chemicals is expected to propel the growth of the glucaric acid market going forward. Eco-friendly and bio-based chemicals refer to substances produced from renewable resources using processes that have minimal environmental impact, promote sustainability, and reduce reliance on fossil fuels. The rising demand for eco-friendly and bio-based chemicals is driven by increasing environmental concerns and regulatory pressures to reduce carbon footprints and pollution. Glucaric acid is used in eco-friendly and bio-based chemicals as a biodegradable alternative for various applications, including detergents, corrosion inhibitors, and food additives. For instance, in December 2022, according to the International Energy Agency, a France-based government agency, demand for vegetable oil, waste, and residue oils and fats increased by 56% to 79 million metric tons in the 2022–2027 period. Moreover, wastes and residues are expected to be used for 13% of biofuel production in 2027, up from 9% in 2021. The rising demand for eco-friendly and bio-based chemicals will drive the growth of the glucaric acid market.

Market Trends - Major companies operating in the glucaric acid market are focusing on adopting innovations in production processes, such as full-scale glucaric acid fermentation, to provide cost-effective, high-purity, and environmentally friendly alternatives for various industrial applications. Full-scale glucaric acid fermentation utilizes microorganisms to convert glucose-containing raw materials into glucaric acid. For instance, in November 2021, Kalion Inc., a U.S.-based biotech company, completed its first full commercialization of its glucaric acid product through custom manufacturing at Evonik in Europe. Kalion's KSPG40 glucaric acid is a potent corrosion inhibitor, surpassing phosphates in water treatment. Additionally, Kalion provides the pharmaceutical market with high-purity calcium glucarate, reducing residue on ignition (ROI) by up to 50% compared to alternatives. This milestone enables the company to fulfill current customer commitments and demands while offering limited quantities for additional customers interested in evaluating their high-purity glucaric product.

The glucaric acid market covered in this report is segmented –

1) By Type: Calcium D-Glucarate, Pure Glucaric Acid, D-Glucaric Acid-1,4-Lactone, Potassium Sodium D-Glucarate, Other Types 2) By Application: Detergents, Healthcare, Food Manufacturing, Corrosion Inhibitors, Other Applications 3) By Sales Channel: Direct Sale, Indirect Sale

Get an inside scoop of the glucaric acid market, Request now for Sample Report @ https://www.thebusinessresearchcompany.com/sample.aspx?id=16068&type=smp

Regional Insights - North America was the largest region in the glucaric acid market in 2023. Asia-Pacific is expected to be the fastest-growing region in the forecast period. The regions covered in the glucaric acid market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East, Africa.

Key Companies - Major companies operating in the glucaric acid market are The Archer Daniels Midland Company, BASF SE, LyondellBasell Industries, Merck KGaA, Koninklijke DSM N.V, Sinochem Group, Roquette Frères SA, Novozymes A/S, Jungbunzlauer Suisse AG, Toronto Research Chemicals Inc, Codexis Inc., Cayman Chemical Company, Tokyo Chemical Industry Co. Ltd, Biosynth Ltd, Chemrez Technologies Inc, Parchem Fine & Specialty Chemicals, Santa Cruz Biotechnology Inc, Rennovia Inc, Alfa Chemistry, Rivertop Renewables, Haihang Industry Co Ltd, CHEMOS GmbH & Co KG, AK Scientific Inc, Kalion Inc, PMP Inc, Shandong Baovi Energy Technology Co Ltd, Otto Chemie Pvt Ltd, Glentham Life Sciences Limited

Table of Contents 1. Executive Summary 2. Glucaric Acid Market Report Structure 3. Glucaric Acid Market Trends And Strategies 4. Glucaric Acid Market – Macro Economic Scenario 5. Glucaric Acid Market Size And Growth ….. 27. Glucaric Acid Market Competitor Landscape And Company Profiles 28. Key Mergers And Acquisitions 29. Future Outlook and Potential Analysis 30. Appendix

Contact Us: The Business Research Company Europe: +44 207 1930 708 Asia: +91 88972 63534 Americas: +1 315 623 0293 Email: [email protected]

Follow Us On: LinkedIn: https://in.linkedin.com/company/the-business-research-company Twitter: https://twitter.com/tbrc_info Facebook: https://www.facebook.com/TheBusinessResearchCompany YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ Blog: https://blog.tbrc.info/ Healthcare Blog: https://healthcareresearchreports.com/ Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model

0 notes

Text

The dairy-free shortening market is projected to grow from USD 22,605.5 million in 2024 to approximately USD 37,412 million by 2032, reflecting a compound annual growth rate (CAGR) of 6.50%. The dairy-free shortening market is experiencing rapid growth, driven by increased consumer demand for plant-based products, health concerns related to dairy, and rising awareness of dietary restrictions like lactose intolerance and veganism. Dairy-free shortening, a fat-based product primarily made from vegetable oils, is often used in baking, cooking, and food production as a substitute for traditional dairy butter or lard. It has gained popularity due to its versatility, shelf stability, and ability to meet the growing demand for plant-based and allergen-free food ingredients. Here, we’ll explore the key market drivers, consumer preferences, challenges, and future prospects of the dairy-free shortening industry.

Browse the full report https://www.credenceresearch.com/report/dairy-free-shortening-market

Market Drivers and Growth Factors

1. Rising Demand for Plant-Based Products A surge in veganism and the adoption of plant-based diets are major drivers for the growth of the dairy-free shortening market. According to studies, consumers are increasingly inclined towards plant-based foods due to health concerns, environmental awareness, and ethical considerations. This shift has created a fertile ground for the dairy-free shortening market, as it caters to vegans and others avoiding animal-based products.

2. Health and Dietary Considerations A growing number of people are developing lactose intolerance, milk allergies, or have digestive issues related to dairy consumption. For these consumers, dairy-free alternatives, including shortening, provide a safer and healthier option. Additionally, the rise of ketogenic, gluten-free, and allergen-free diets has driven the adoption of dairy-free shortening, which can be formulated to fit into these specialized diets.

3. Awareness of Environmental Impact Sustainability and environmental concerns are shaping consumer behavior, and the plant-based food industry benefits from this shift. Traditional dairy production has a higher environmental impact, involving significant water use, greenhouse gas emissions, and land requirements. By contrast, dairy-free shortening, primarily derived from plant oils like palm, coconut, or soy, offers a lower carbon footprint, appealing to environmentally conscious consumers.

4. Innovative Product Development and Distribution Channels Manufacturers are responding to market demand with innovative dairy-free shortening products that cater to both household consumers and the foodservice industry. Improved formulations that mimic the texture and taste of butter have made dairy-free shortenings more appealing for baking and cooking, which broadens their applications. The market’s expansion is further facilitated by e-commerce platforms, allowing consumers easier access to specialized products.

Key Trends in the Dairy-Free Shortening Market

1. Shift to Organic and Non-GMO Ingredients With the rising demand for clean-label products, many manufacturers are opting for organic, non-GMO ingredients in their dairy-free shortenings. Organic coconut oil, palm oil, and other natural oils are popular choices, as they appeal to health-conscious consumers and adhere to stricter quality standards. The organic segment within dairy-free shortening has been growing steadily as consumers seek healthier options without artificial additives.

2. Diversification of Ingredient Sources Traditional vegetable oils, like palm and coconut, have dominated the market. However, newer sources such as avocado oil, olive oil, and even algal oil are being explored for their unique flavor profiles and health benefits. This diversification is allowing companies to cater to varying consumer tastes and dietary needs.

3. Focus on Sustainable Sourcing The sustainability of sourcing ingredients, particularly palm oil, is a concern among environmentally aware consumers. To address this, some companies are using certified sustainable palm oil or exploring alternative oils with a lower environmental impact. This focus on sustainable sourcing not only enhances brand image but also addresses the ethical and environmental demands of the market.

4. Growth in E-commerce and Direct-to-Consumer Sales The rise of e-commerce has significantly boosted the dairy-free shortening market by allowing manufacturers to reach a wider audience. Companies are increasingly adopting direct-to-consumer (DTC) models to market their products, allowing for better control over branding, customer engagement, and market insights. This trend has accelerated during the pandemic as more consumers opted for online shopping.

Market Challenges

1. Price Sensitivity and Production Costs Dairy-free shortenings are often more expensive than traditional butter or margarine, which can limit their appeal to cost-conscious consumers. The use of premium ingredients and sustainable practices can drive up production costs, creating a challenge in markets with high price sensitivity.

2. Regulatory and Labeling Challenges The dairy-free shortening industry faces regulatory hurdles related to labeling and claims. Manufacturers must adhere to local and international regulations on ingredient labeling, especially in terms of “non-dairy” or “plant-based” claims, which can vary from one market to another. This requires companies to be vigilant about compliance to avoid potential legal issues.

3. Texture and Flavor Limitations While there have been significant advancements in formulation, some consumers still prefer the taste and texture of traditional butter. Developing dairy-free shortenings that perfectly mimic the sensory properties of dairy butter remains a challenge, particularly for high-end baking applications.

Future Outlook

The future of the dairy-free shortening market appears promising, driven by continuous innovations in product formulation, diversification of raw material sources, and expansion into emerging markets. As more consumers adopt plant-based lifestyles and prioritize sustainability, the demand for dairy-free shortening is expected to grow. Additionally, advancements in food technology may enable producers to further improve the taste, texture, and nutritional profile of these products, making them more competitive with traditional shortenings.

Key Player Analysis:

Groupe Danone

The Hain Celestial Group

The Whitewave Foods Company

Good Karma Foods

GraceKennedy Group

Blue Diamond Growers, Inc.

SunOpta, Inc.

Oatly A.B.

Vitasoy International Holdings Limited

Nutiva Inc.

Segmentation:

By Product Type:

Beverages

Milk

Dairy-Free Kefir

Bakery Products

By Application:

Household

Commercial

By Region:

North America

US

Canada

Mexico

Europe

Germany

France

UK

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Browse the full report https://www.credenceresearch.com/report/dairy-free-shortening-market

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

Canada Soybean Oil Market (2024-2032): Growth, Health Trends

The Canada soybean oil market size reached an estimated production volume of 330 thousand metric tons (MT) in 2020. The market has been experiencing steady growth, driven by increasing consumer health consciousness and the rising demand for biodiesel, in which soybean oil serves as a key feedstock. As more industries recognize the versatility and profitability of soybean oil, both as a cooking ingredient and as an essential component in the biofuel industry, the market is expected to expand steadily over the forecast period of 2024 to 2032. Leading players such as Centra Foods, Bunge Limited, and Cargill, Incorporated are positioning themselves to capitalize on this growth by innovating and optimizing their production processes.

Market Outlook (2024-2032)

The outlook for the Canadian soybean oil market is highly positive. With an increasing number of health-conscious consumers and the government’s push toward renewable energy solutions, particularly biodiesel, the market is expected to see significant growth. Soybean oil, being one of the most widely used vegetable oils in Canada, plays a crucial role in various sectors, including food production, cosmetics, and renewable energy. With the rising awareness around the health benefits of soybean oil, which is low in saturated fats and high in polyunsaturated fats, its demand as a healthier cooking option is also on the rise.