#U.S. Pharmaceutical Market Size

Text

According to latest report, the U.S. pharmaceutical market size was USD 602.19 billion in 2023, calculated at USD 639.22 billion in 2024 and is expected to reach around USD 1,093.79 billion by 2033, expanding at a CAGR of 6.15% from 2024 to 2033.

0 notes

Text

According to Nova One Advisor, the U.S. pharmaceutical logistics market size was exhibited at USD 26.55 billion in 2023 and is projected to hit around USD 58.39 billion by 2033, growing at a CAGR of 8.2% during the forecast period 2024 to 2033.

0 notes

Text

Cholesterol, often vilified as the main driver of heart disease, is actually an essential component of cellular health. It plays a crucial role in various biological functions, including building cell membranes, producing hormones, and aiding in the absorption of vitamins. Cholesterol is a necessary nutrient that our bodies cannot produce on their own, so it’s important to get vitamin D from sunlight and to consume foods that contain cholesterol to maintain healthy cholesterol levels.

But today, doctors are indoctrinated and incentivized to push statin drugs on people at an early age, while ignoring all the dietary and lifestyle factors that influence heart disease risk. The oversimplification of the causes of heart disease leads to widespread pill-pushing that benefits a statin drug industry that’s built on a history of lies.

Big Pharma capitalizing on heart disease myths

The pharmaceutical industry has long profited from the widespread belief that high cholesterol is a primary cause of heart disease. This notion has fueled a booming market for statin drugs, which have become a staple of cardiovascular care, forcefully interfering with cholesterol levels. Major pharmaceutical companies, including Pfizer, AstraZeneca, and Merck, have invested heavily in developing and marketing statin medications, reaping substantial financial rewards along the way.

According to Data Bridge Market Research, the U.S. statin market size was valued at $4.53 billion in 2023 and is projected to reach $5.10 billion by 2031. This growth is driven, in part, by the increasing prevalence of high cholesterol among adults, particularly those aged 40-59.

However, the link between high cholesterol and heart disease has been challenged over the past five years, with researchers pointing out manipulated, industry-sponsored studies that overstate the correlation between the two. The predatory financial interests of the pharmaceutical industry have played a significant role in shaping public perception and medical practice.

The American College of Cardiology developed a simple calculator that proposes to determine one’s risk of a heart attack or stroke within the next ten years. The calculator uses blood pressure, cholesterol level, smoking status and age to make this determination. This calculator is used to pressure patients into taking statins, while ignoring the various dietary and lifestyle factors that predispose a person to heart disease.

29 notes

·

View notes

Text

It turns out she’s down about ten pounds and happy about it. “Somebody once told me I had a size-zero personality, and they assumed that I was thinner than I was,” she tells me. “We don’t talk about it, but everybody knows it. Thin is power.”

Allison isn’t alone in seeming to be suddenly, unaccountably slimmer of late. She admitted to me — with the provision that I not use her real name — the reason, one that is increasingly common if still not quite openly discussed. For the past month, she’s been jabbing herself every week with Ozempic, the heavily advertised (“Oh, oh, oh, Ozempic,” to the tune, none too subtly, of the ’70s classic-rock hit “Magic”) diabetes miracle drug, which works by mimicking a naturally occurring hormone, GLP-1 (glucagon-like peptide one), to manage hunger and slow stomach emptying.

For diabetics, it lowers blood-sugar levels. It also subdues the imp of appetite. The pounds fly off. That’s why Allison, who is not diabetic, prediabetic, or even overweight, is on it. Doctors have wide latitude to prescribe drugs off label for anyone they think may medically benefit, and many patients have found doctors — or, failing that, nurse practitioners or medi-spas — ready to certify that they would. Or some, like Allison, find it through a peddler not particular about a prescription or in the web’s dark morass.

To get hers, Allison calls up a Los Angeles–based provider she has never seen or met, sends over $625, and is shipped a monthly supply. What she calls Ozempic is not the brand-name product pre-packaged in a sky-blue injector pen by Novo Nordisk, the Danish pharmaceutical company that makes and markets the drug. She receives generic semaglutide, the active ingredient in the medication, and has to mix and prepare it for injection herself, which — since semaglutide is under patent by Novo Nordisk until 2032 in the U.S. — suggests her meds are likely coming from a compounding pharmacy or a vendor selling research-grade ingredients. The lower price is also a tell: Ozempic retails for about $900 a month if your insurance doesn’t cover it.

17 notes

·

View notes

Text

US Industrial Boilers Market Size, Share And Growth Analysis

Industrial boilers are critical components in various manufacturing processes, providing a reliable source of heat or steam for a wide range of industrial applications in the United States. These boilers are used in industries such as chemical processing, food and beverage production, pharmaceuticals, refineries, and power generation. They come in various types, including fire-tube boilers, water-tube boilers, and electric boilers, each designed to meet specific industrial needs. The primary function of industrial boilers is to efficiently generate heat or steam to facilitate various industrial processes, contributing to the overall productivity and energy efficiency of manufacturing operations.

𝐆𝐞𝐭 𝐒𝐚𝐦𝐩𝐥𝐞 𝐑𝐞𝐩𝐨𝐫𝐭 𝐏𝐃𝐅: https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=9131

The demand for industrial boilers in the United States is influenced by several factors, including economic growth, regulatory requirements, and technological advancements. As industries expand and modernize, the need for efficient and environmentally compliant boiler systems has increased. Stringent environmental regulations have prompted industries to replace older, less efficient boilers with newer, cleaner technologies. The adoption of advanced combustion and control systems in industrial boilers has become crucial in meeting emissions standards and optimizing energy utilization. Additionally, the U.S. government's focus on energy efficiency and sustainability is driving industries to invest in modern industrial boilers to reduce energy consumption and operational costs.

The demand for industrial boilers in the United States is also influenced by the growth of key end-user industries. Sectors such as chemical processing, food and beverage, and power generation have a substantial impact on the demand for industrial boilers. For instance, the chemical industry relies on industrial boilers for various processes such as chemical reactions and distillation. Similarly, the food and beverage industry utilizes boilers for cooking, pasteurization, and sterilization. The expansion of these industries, coupled with the need for reliable and efficient heating solutions, contributes to the ongoing demand for industrial boilers in the U.S. Technological advancements are playing a significant role in shaping the demand for industrial boilers. The integration of digital controls, sensors, and advanced monitoring systems enhances the efficiency and safety of industrial boiler operations. Smart boilers with features like remote monitoring, predictive maintenance, and real-time performance optimization are gaining traction in the market. This trend aligns with the broader industrial shift towards Industry 4.0 principles, where connectivity and data-driven insights play a pivotal role in optimizing manufacturing processes. As industries in the United States continue to prioritize efficiency, safety, and sustainability, the demand for technologically advanced industrial boilers is expected to persist, driving innovation in the sector.

2 notes

·

View notes

Text

A strange thing happened in the eurozone economy at the end of last year. Despite widespread forecasts that the common currency area would plunge into recession and register negative growth in the last quarter of 2022, it managed to eke out a small gain of 0.1 percent. What is remarkable is not that Europe beat expectations, but that it was one small country—Ireland—whose surging economy single-handedly prevented the eurozone from slipping into the red.

Almost unbelievably, little Ireland, with a population of only 5 million, now has the economic scale to shift the growth statistics of the entire eurozone and its 343 million inhabitants. In 2022, Irish GDP growth of 12.2 percent compared to 3.5 percent in the eurozone as a whole. In absolute numbers, only Germany, France, and Italy contributed more than Ireland to eurozone GDP growth in 2021 and 2022. Ireland’s economic boom has enabled the country’s government to post a budget surplus of 1.6 percent of GDP, even as eurozone countries struggled with an average deficit of more than 3 percent.

Honestly, who wouldn’t want this luck of the Irish?

Look closely, however, and Ireland’s so-called economic miracle looks more than a little odd. The country’s growth is simultaneously both real and artificial. Much of it is driven by a handful of U.S. multinationals, which continue to route global sales and profits through their Irish operations to take advantage of Dublin’s lower business taxes. Although difficult and complex to calculate, Apple’s shifting of intellectual property assets to Ireland is estimated to have contributed half of Ireland’s miraculous 26 percent GDP growth in 2016. That bizarre fact inspired New York Times columnist Paul Krugman to ridicule Ireland’s “leprechaun economics”—and the Irish statistics office to move away from using GDP as a measure of economic growth.

Yet the surge of U.S. investment in Ireland is also real. In particular, Ireland’s role as a pharmaceuticals manufacturing hub dramatically increased during the COVID-19 pandemic. Nine out of the world’s top 10 drug companies have significant production facilities in Ireland. The U.S. State Department thinks the corporate build-out in Ireland will continue, given Ireland’s status as the only remaining English-speaking European Union country following Britain’s departure. That makes it easy for international companies to operate and enjoy barrier-free access to the EU’s single market.

It’s hard to exaggerate Ireland’s dependence on U.S. tech and pharma companies for investment and taxes. Corporate tax receipts are now the second-largest source of tax revenue (after income tax) for the Irish state: 27 percent of all tax income in 2022. The average was just 9 percent in the 38 member countries of the Organisation for Economic Co-operation and Development (OECD) in 2020, the last year for which data is available. This, in turn, is fueling an unprecedented torrent of tax income for the Irish government. Corporate tax revenues were up nearly 50 percent in 2022 alone.

Just 10 multinationals—all of them U.S.-based tech and pharmaceutical companies—now pay nearly 60 percent of Ireland’s corporate tax. Directly and indirectly, U.S. multinationals employ more than 375,000 people in Ireland, approximately 15 percent of the country’s labor force. Driven by investment from the United States, foreign multinationals now account for 53 percent of all payroll taxes paid by corporate employers.

Driven by the windfall in corporate tax receipts, the Irish government’s budget surplus is expected to swell further, to 10 billion euros in 2023 and 16 billion euros in 2024. Relative to the size of the economy, this would be equivalent to a U.S. budget surplus of more than 1 trillion dollars in 2024.

The problem for Ireland is that this singular dependence exposes the country to growing risks. Take the tech sector: As multinationals like Google, Microsoft, Meta, and Amazon see their profits shrink and slash jobs worldwide, it will not only hurt the Irish economy, but deprive Dublin of tax income as well.

What’s more, the threat to Ireland’s stability from its overdependence on U.S. companies is about to be multiplied. In 2021, nearly 140 tax jurisdictions, including Ireland, agreed to a major reform of how multinationals companies will be taxed in the future. Pillar 2 of these reforms—a minimum corporate tax rate of 15 percent for large companies—is already coming into effect. In 2024, Ireland’s corporate tax rate is due to increase to 15 percent from its current level of 12.5 percent, reducing its attractiveness as a tax haven compared to other countries. The United States also approved the minimum tax plan in August 2022, despite significant private sector and political opposition.

However, it is Pillar 1 of the OECD’s reforms that will dramatically erode Ireland’s future income from corporate taxes. This reform will reallocate a share of company profits to where sales (or users) are actually located. Previously, tax liability was calculated on where the company or its subsidiary was legally based, no matter how many profits it rerouted from other parts of the world for tax-avoiding purposes. For Ireland, the consequences are obvious: U.S. multinationals operating in the EU will be forced to divide some of their sales by member state, thus significantly reducing the amount of sales and profits that can be “booked” through Ireland. This reform is due to come into force in 2024. The end of Ireland’s windfall is therefore only a matter of time.

The Irish Department of Finance estimated in January that around half of Ireland’s corporate tax receipts—$10 billion—are “transitionary” and will be lost as the new tax rules are implemented. That translates to more than 10 percent of total government spending in 2022—more than the entire Irish education budget. This is putting the Irish government on the precipice of another financial disaster, little more than a decade after it had to be bailed out of impending bankruptcy by the European Commission, European Central Bank, and the International Monetary Fund. That disaster left Ireland with one of the highest per capita public debt levels in the world.

Regardless of the impending financial train wreck, however, Dublin is unlikely to wake up from its American dream anytime soon. Diversifying its economy and revenue sources away from U.S. multinationals would require Ireland to shift its economic and geopolitical orientation, downgrade (in Dublin’s eyes) its deep relationship with the United States, and seek greater integration into the EU economy and its myriad rules.

That’s because Ireland’s dependence on U.S. multinationals is just another expression of the country’s affinity with the United States—the “shared heritage” referenced by U.S. presidents from John F. Kennedy to Ronald Reagan to Joe Biden. These ties to the United States long precede Dublin’s embrace of European integration and make it unlikely that Ireland will ever have the same intensity of economic, cultural, and other ties to France, Germany, or the rest of the EU.

The approaching economic and fiscal train wreck resulting from the new tax rules requires a fundamental change of mindset from Irish policymakers. Squaring the circle—holding on to its deep U.S. ties while integrating more closely with the EU to diversify its economy—means Dublin must give a little (and lose a little) to both sides. Yet Ireland’s ability to navigate this conundrum is doubtful. Even though the coming changes have been plain for all to see, Dublin’s current Trade and Investment Strategy does not contain any concrete policies to mitigate the overdependence on U.S. investment flows. Although the document acknowledges that EU market opportunities are underutilized, it again recognizes the importance “markets such as the UK and the US, which offer familiarity with language and culture.”

If there is no short-term solution to Ireland’s financial vulnerabilities, a few longer-term needs stand out. Dublin should ensure that its current budget surplus is invested wisely to help diversify its drivers of growth. One such driver would be significant increases in public investment in housing and public transport infrastructure to bring the country closer to Western European standards. Ireland’s tax base should be widened to allow for a wider distribution of income sources. For example, In 2021, Ireland gained just 5 percent of its tax receipts from property taxes, compared to more than 11 percent in both Britain and the United States.

Most importantly, Ireland must deepen its trading relationships outside the English-speaking world. Notwithstanding the country’s 50-year membership of the EU, a dearth of foreign language teaching has created a monolingual business culture, which priorities existing links with the United States over the development of new markets, both within and outside the EU. This needs to change if Ireland is to build a sustainable economic model.

Biden—whose family, like so many in the United States, has Irish roots—said in 2021 that “everything between Ireland and the United States runs deep.” This is Ireland’s economic reality today. As the corporate tax boom ebbs, Ireland should ensure that its American dream doesn’t become a recurring economic and financial nightmare.

2 notes

·

View notes

Text

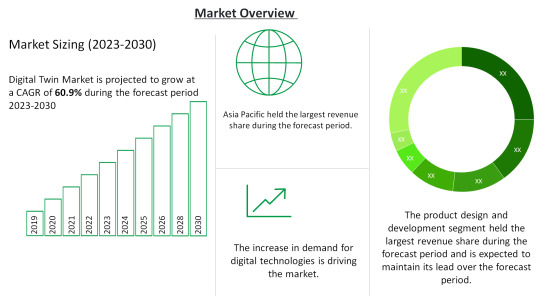

Digital Twin Market Size 2023-2030: ABB, AVEVA Group plc, Dassault Systemes

Digital Twin Market by Power Source (Battery-Powered, hardwired with battery backup, Hardwired without battery backup), Type (Photoelectric Smoke Detectors, Ionization Smoke Detectors), Service, Distribution Channel, and region (North America, Europe, Asia-Pacific, Middle East, and Africa and South America). The global Digital Twin Market size is 11.12 billion USD in 2022 and is projected to reach a CAGR of 60.9% from 2023-2030.

Click Here For a Free Sample + Related Graphs of the Report at: https://www.delvens.com/get-free-sample/digital-twin-market-trends-forecast-till-2030

Digital twin technology has allowed businesses in end-use industries to generate digital equivalents of objects and systems across the product lifecycle. The potential use cases of digital twin technology have expanded rapidly over the years, anchored in the increasing trend of integration with internet-of-things (IoT) sensors. Coupled with AI and analytics, the capabilities of digital twins are enabling engineers to carry out simulations before a physical product is developed. As a result, digital twins are being deployed by manufacturing companies to shorten time-to-market. Additionally, digital twin technology is also showing its potential in optimizing maintenance costs and timelines, thus has attracted colossal interest among manufacturing stalwarts, notably in discrete manufacturing.

The shift to interconnected environments across industries is driving the demand for digital twin solutions across the world. Massive adoption of IoT is being witnessed, with over 41 billion connected IoT devices expected to be in use by 2030. For the successful implementation and functioning of IoT, increasing the throughput for every part or “thing” is necessary, which is made possible by digital twin technology. Since the behavior and performance of a system over its lifetime depend on its components, the demand for digital twin technology is increasing across the world for system improvement. The emergence of digitalization in manufacturing is driving the global digital twin market. Manufacturing units across the globe are investing in digitalization strategies to increase their operational efficiency, productivity, and accuracy. These digitalization solutions including digital twin are contributing to an increase in manufacturer responsiveness and agility through changing customer demands and market conditions.

On the other hand, there has been a wide implementation of digital technologies like artificial intelligence, IoT, clog, and big data which is increasing across the business units. The market solutions help in the integration of IoT sensors and technologies that help in the virtualization of the physical twin. The connectivity is growing and so are the associated risks like security, data protection, and regulations, alongside compliance.

During the COVID-19 pandemic, the use of digital twin technologies to manage industrial and manufacturing assets increased significantly across production facilities to mitigate the risks associated with the outbreak. Amid the lockdown, the U.S. implemented a National Digital Twin Program, which was expected to leverage the digital twin blueprint of major cities of the U.S. to improve smart city infrastructure and service delivery. The COVID-19 pandemic positively impacted the digital twin market demand for twin technology.

Delvens Industry Expert’s Standpoint

The use of solutions like digital twins is predicted to be fueled by the rapid uptake of 3D printing technology, rising demand for digital twins in the healthcare and pharmaceutical sectors, and the growing tendency for IoT solution adoption across multiple industries. With pre-analysis of the actual product, while it is still in the creation stage, digital twins technology helps to improve physical product design across the full product lifetime. Technology like digital twins can be of huge help to doctors and surgeons in the near future and hence, the market is expected to grow.

Market Portfolio

Key Findings

The enterprise segment is further segmented into Large Enterprises and Small & Medium Enterprises. Small & Medium Enterprises are expected to dominate the market during the forecast period. It is further expected to grow at the highest CAGR from 2023 to 2030.

The industry segment is further segmented into Automotive & Transportation, Energy & Utilities, Infrastructure, Healthcare, Aerospace, Oil & Gas, Telecommunications, Agriculture, Retail, and Other Industries. The automotive & transportation industry is expected to account for the largest share of the digital twin market during the forecast period. The growth can be attributed to the increasing usage of digital twins for designing, simulation, MRO (maintenance, repair, and overhaul), production, and after-service.

The market is also divided into various regions such as North America, Europe, Asia-Pacific, South America, and Middle East and Africa. North America is expected to hold the largest share of the digital twin market throughout the forecast period. North America is a major hub for technological innovations and an early adopter of digital twins and related technologies.

During the COVID-19 pandemic, the use of digital twin technologies to manage industrial and manufacturing assets increased significantly across production facilities to mitigate the risks associated with the outbreak. Amid the lockdown, the U.S. implemented a National Digital Twin Program, which was expected to leverage the digital twin blueprint of major cities of the U.S. to improve smart city infrastructure and service delivery. The COVID-19 pandemic positively impacted the digital twin market demand for twin technology.

Regional Analysis

North America to Dominate the Market

North America is expected to hold the largest share of the digital twin market throughout the forecast period. North America is a major hub for technological innovations and an early adopter of digital twins and related technologies.

North America has an established ecosystem for digital twin practices and the presence of large automotive & transportation, aerospace, chemical, energy & utilities, and food & beverage companies in the US. These industries are replacing legacy systems with advanced solutions to improve performance efficiency and reduce overall operational costs, resulting in the growth of the digital twin technology market in this region.

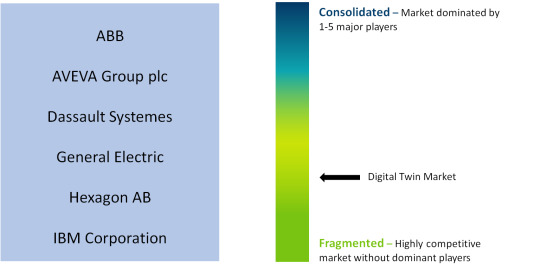

Competitive Landscape

ABB

AVEVA Group plc

Dassault Systemes

General Electric

Hexagon AB

IBM Corporation

SAP

Microsoft

Siemens

ANSYS

PTC

IBM

Recent Developments

In April 2022, GE Research (US) and GE Renewable Energy (France), subsidiaries of GE, collaborated and developed a cutting-edge artificial intelligence (AI)/machine learning (ML) technology that has the potential to save the worldwide wind industry billions of dollars in logistical expenses over the next decade. GE’s AI/ML tool uses a digital twin of the wind turbine logistics process to accurately predict and streamline logistics costs. Based on the current industry growth forecasts, AI/ML might enable a 10% decrease in logistics costs, representing a global cost saving to the wind sector of up to USD 2.6 billion annually by 2030.

In March 2022, Microsoft announced a strategic partnership with Newcrest. The mining business of Newcrest would adopt Azure as its preferred cloud provider globally, as well as work on digital twins and a sustainability data model. Both organizations are working together on projects, including the use of digital twins to improve operational performance and developing a high-impact sustainability data model.

Reasons to Acquire

Increase your understanding of the market for identifying the best and most suitable strategies and decisions on the basis of sales or revenue fluctuations in terms of volume and value, distribution chain analysis, market trends, and factors

Gain authentic and granular data access for Digital Twin Market so as to understand the trends and the factors involved in changing market situations

Qualitative and quantitative data utilization to discover arrays of future growth from the market trends of leaders to market visionaries and then recognize the significant areas to compete in the future

In-depth analysis of the changing trends of the market by visualizing the historic and forecast year growth patterns

Direct Purchase of Digital Twin Market Research Report at: https://www.delvens.com/checkout/digital-twin-market-trends-forecast-till-2030

Report Scope

Report FeatureDescriptionsGrowth RateCAGR of 60.9% during the forecasting period, 2023-2030Historical Data2019-2021Forecast Years2023-2030Base Year2022Units ConsideredRevenue in USD million and CAGR from 2023 to 2030Report Segmentationenterprise, platform, application, and region.Report AttributeMarket Revenue Sizing (Global, Regional and Country Level) Company Share Analysis, Market Dynamics, Company ProfilingRegional Level ScopeNorth America, Europe, Asia-Pacific, South America, and Middle East, and AfricaCountry Level ScopeU.S., Japan, Germany, U.K., China, India, Brazil, UAE, and South Africa (50+ Countries Across the Globe)Companies ProfiledABB; AVEVA Group plc; Dassault Systems; General Electric; Hexagon AB; IBM Corp.; SAP.Available CustomizationIn addition to the market data for Digital Twin Market, Delvens offers client-centric reports and customized according to the company’s specific demand and requirement.

TABLE OF CONTENTS

Large Enterprises

Small & Medium Enterprises

Product Design & Development

Predictive Maintenance

Business Optimization

Performance Monitoring

Inventory Management

Other Applications

Automotive & Transportation

Energy & Utilities

Infrastructure

Healthcare

Aerospace

Oil & Gas

Telecommunications

Agriculture

Retail

Other Industries.

Asia Pacific

North America

Europe

South America

Middle East & Africa

ABB

AVEVA Group plc

Dassault Systemes

General Electric

Hexagon AB

IBM Corporation

SAP

About Us:

Delvens is a strategic advisory and consulting company headquartered in New Delhi, India. The company holds expertise in providing syndicated research reports, customized research reports and consulting services. Delvens qualitative and quantitative data is highly utilized by each level from niche to major markets, serving more than 1K prominent companies by assuring to provide the information on country, regional and global business environment. We have a database for more than 45 industries in more than 115+ major countries globally.

Delvens database assists the clients by providing in-depth information in crucial business decisions. Delvens offers significant facts and figures across various industries namely Healthcare, IT & Telecom, Chemicals & Materials, Semiconductor & Electronics, Energy, Pharmaceutical, Consumer Goods & Services, Food & Beverages. Our company provides an exhaustive and comprehensive understanding of the business environment.

Contact Us:

UNIT NO. 2126, TOWER B,

21ST FLOOR ALPHATHUM

SECTOR 90 NOIDA 201305, IN

+44-20-8638-5055

[email protected]

WEBSITE: https://delvens.com/

#Digital Twin Market#Digital Twin#Digital Twin Market Size#Digital Twin Market Share#Semiconductors & Electronics

2 notes

·

View notes

Text

Smart Glove Market - Forecast (2021 - 2026)

The Smart Glove Market size is analyzed to grow at a CAGR of 9.6% during the forecast 2021-2026 to reach $4.67 billion by 2026. Smart Glove is considered as a wide range of Sensor technology gloves for advanced and customized solutions, such as hand protection, high-tech rehab device and other assistive device services. The Smart Gloves are designed electronic devices with microcontrollers to offer avant-garde opportunities for various kinds of application suitable to the business requirements, including industrial grade gloves and medical grade gloves, and thus, contribute to the Smart Glove market growth. The rapid prominence of the Internet of Things (IoT), artificial intelligence and connected devices, along with the increasing innovations in wearable health devices, smart personal protective equipment, integrated with GPS, wireless communication features and in-built voice assistance have supported the Smart Glove Industry development successfully. In fact, the growth of the market is also observed due to the growing advancement of the Bluetooth chip, flex sensors, microcontroller, and accelerometer. Furthermore, the progression of microencapsulation and nanotechnology pave the way for sensor technology which offers lucrative growth possibilities. The influx of brands like Samsung, Apple, and Fossil are broadening the functionalities, which further promotes Smart Glove Market.

Smart Glove Market Report Coverage

The report: “Smart Glove Industry Outlook – Forecast (2021-2026)”, by IndustryARC covers an in-depth analysis of the following segments of the Smart Glove Industry.

By Offerings: Software and Service

By Application: Fitness & Wellness, Specific Health Monitor, Infotainment, Ergonomic wearable and others

By Industry Verticals: Pharmaceuticals & Healthcare, Food & Beverages, Enterprise and Industrial, Consumer Electronics and others

By Geography: North America (U.S, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Russia and Others), APAC(China, Japan, India, South Korea, Australia and Others), South America(Brazil, Argentina and others)and RoW (Middle east and Africa).

Request Sample

Key Takeaways

The growing demand of wearable medical devices owing to the increasing awareness on fitness and a healthy lifestyle along with prominence of connected devices in Healthcare, contribute to the growth.

Asia Pacific is estimated to hold the highest share of 40% in 2020, followed by North America, owing to the significant adoption of IoT, large scale implementation of a wide range of ubiquitous systems, such as wearable computing and sensor technology across the several business verticals.

The advancements in consumer electronics with a wide range of technical advantages, including touch sensitive features and miniature designs, resulted into the market growth.

Smart Glove Market Segment Analysis – By Industry Verticals

By Industry Verticals, the Smart Glove Market is segmented into Pharmaceuticals & Healthcare, Food & Beverages, Enterprise and Industrial, Consumer Electronics and others. The Enterprise and Industrial segment held the major share of 37% in 2020, owing to the propensity for cutting-edge products and significant investment to pursue radical evolutions in commercial applications. In order to address the growing requirement of several end users across automotive, oil & gas, manufacturing and logistics, customizable smart gloves with built-in scanners are introduced for more effective operations. In April 2019, the manufacturer of a smart, wearable technology, ProGlove, unveiled its MARK 2 to a U.S. audience ProMat in Chicago. The new MARK 2 enables the user to scan up to 5 feet away from a device and can connect to a corporate network via Bluetooth Low Energy (BLE), with up to 15-hour charge battery. ProGlove provides hands-free scanning solutions across a number of industries, and thus, in September 2020, Panasonic announced a partnership with ProGlove, to combine the mobile computing solutions of the two companies in order to offer rugged, innovative and user-friendly wireless barcode scanners. The strategic collaboration is also formulated to deliver seamless as-a-stand-alone scanning solution with an embedded Panasonic’s voice picking solutions for the warehouse operations, supply chain, and inventory checking. Therefore, the growing demand of integrated gesture sensor solutions for dynamic workstations, and a more efficient working environment accelerated the demand of Smart Glove Market.

Inquiry Before Buying

Smart Glove Market Segment Analysis – By Geography

Asia Pacific is estimated to hold the highest share of 40% in 2020, followed by North America in Smart Glove Market. The early adoption of IoT, large scale implementation of a wide range of ubiquitous systems, such as wearable computing and sensor technology across the several business verticals, along with the growing interest of consumers towards ‘sensorized’ fitness wearable devices are estimated to drive the market in these regions. Furthermore, numerous research investments propel the innovations of soft and stretchable electronics design that propel a competitive edge to smart wearable solutions. In January 2021, HaptX Inc. announced the release of HaptX Gloves DK2. The HaptX Gloves DK2 is an upgraded design and the world's most advanced haptic feedback gloves, which deliver unprecedented realism, with more than 130 points of tactile feedback per hand. These gloves have astoundingly real-life superpowers with VR, XR, and robotics technologies to meet the demand of various enterprises for quality requirements. Hence, the promising demand of industrial wearable and other smart personal protective equipment in these regions are estimated to drive the Smart Glove Market.

Smart Glove Market Drivers

Growing prominence of healthcare wearable

The growing demand of wearable medical devices owing to the increasing awareness on fitness and a healthy lifestyle along with prominence of connected devices in Healthcare, contribute to the growth of Smart Glove Market. Moreover, the rise of high-tech devices to usher clinical-grade wearable with 3G and 4G connection led to various viable solutions. In July 2020, UCLA bioengineers designed a glove-like device that can translate American Sign Language (ASL) into English speech in real time through a smartphone app. The entire system is integrated upon a pair of gloves with thin, stretchable sensors to translate hand gestures into spoken words. Hence, the sizable demand of personalized care, specific health issue monitoring devices and user-friendly, compact medical wearable propelled the growth of the Smart Glove Market.

Schedule a Call

Advancements in consumer electronics

The advancements in consumer electronics with a wide range of technical advantages, including touch sensitive features and miniature designs, resulted into the growth of Smart Glove Market. The advent of digitalization and latest development in sensor technology to enhance user performances is further driving the market. In April 2019, British music tech company Mi.Mu, founded by Grammy award-winning artist Imogen Heap announced the release of newly designed Mi.Mu gloves, allowing artists to map hand gestures to music software. The new gloves of Mi.Mu are durable with a removable battery system that offers artists complete control over their musical performances. Moreover, the breakthrough innovation in microfibre sensor technology offers strain sensing capabilities that provides gesture-based control. In August 2020, A team of researchers from the National University of Singapore (NUS), led by Professor Lim Chwee Teck, developed a smart glove, known as 'InfinityGloveTM', which enables users to mimic numerable in-game controls using simple hand gestures. Therefore, the launch of sophisticated wearable electronics products, extensive glove's capabilities and rising usage of convenient-to-use devices are some of the factors that are estimated to drive the Smart Glove Market.

Smart Glove Market Challenge

High price of Smart Glove solution

The market of Smart Glove is expanding due to the significant technologies development, using the amalgamation of sensing and feedback operation to denote smarter systems. Thus, the commercially available devices, pertaining to smart glove features are prominently expensive, which is a major constraint that demotivated the rapid adoption. Thus, factors such as less sensible investment and unobtainability of some of the latest smart gloves technology around some regions due to high cost are likely to restrict the Smart Glove Market.

Market Landscape

Partnerships and acquisitions along with product launches are the key strategies adopted by the players in the Smart Glove Market. The Smart Glove Market top 10 companies include Apple Inc, Flint Rehab, Haptx, Lab Brother Llc, Maze Exclusive, Neofect, Samsung Electronics Co Ltd, Seekas Technology Co., Ltd, Vandrico Solution Inc, ProGlove, Workaround Gmbh and among others

Buy Now

Acquisitions/Technology Launches/Partnerships

In December 2019, HaptX, the leading provider of realistic haptic technology announced the partnership with Advanced Input Systems along with a Series A financing round of $12 million. This acquisition provides a great opportunity for HaptX as they can finance the production of the next generation of HaptX Gloves, which represents the world’s most realistic gloves for virtual reality and robotics, coupled with product development, manufacturing, and go-to-market collaboration.

In November 2019, Ansell Limited, a leading provider of safety solutions, announced a partnership with ProGlove, a renowned industrial wearable manufacturer. The acquisition is formed to deliver advanced hand protection solutions to ensure the personal protective equipment (PPE) compliance in the workplace.

For more Electronics Market reports, please click here

#Smart Glove Market price#Smart Glove Market Forecast#Smart Glove Market Growth#Smart Glove Market Report#Smart Glove Market Research#Smart Glove Market Share#Smart Glove Market Size#Smart Glove Market Trend#Smart Glove Market Outlook

2 notes

·

View notes

Text

The Human Genetics Market is projected to grow from USD 28665 million in 2024 to an estimated USD 59681.04 million by 2032, with a compound annual growth rate (CAGR) of 9.6% from 2024 to 2032.The human genetics market is experiencing rapid growth, driven by advancements in genomics, precision medicine, and the increasing understanding of the human genome's role in health and disease. The field of human genetics involves the study of genes, genetic variation, and heredity in humans, and its applications have far-reaching implications in healthcare, diagnostics, drug development, and personalized medicine. In this article, we will explore the current trends, key drivers, challenges, and future prospects of the human genetics market.

Browse the full report at https://www.credenceresearch.com/report/human-genetics-market

Overview of the Human Genetics Market

The global human genetics market has witnessed significant expansion in recent years, with the development of novel technologies such as next-generation sequencing (NGS), gene editing tools like CRISPR-Cas9, and advancements in bioinformatics. These technologies have made it possible to analyze genetic data more efficiently and accurately, providing valuable insights into disease mechanisms, inheritance patterns, and individual susceptibility to various health conditions. The market encompasses a wide range of products and services, including genetic testing, genome sequencing, gene therapy, pharmacogenomics, and molecular diagnostics.

Key Market Drivers

1. Rising Demand for Genetic Testing: Genetic testing has become a cornerstone in modern healthcare, enabling early detection and diagnosis of genetic disorders. It plays a crucial role in identifying genetic predispositions to conditions such as cancer, cardiovascular diseases, and neurological disorders. As awareness about genetic testing grows among both patients and healthcare providers, the demand for such tests is expected to rise. Moreover, direct-to-consumer (DTC) genetic testing services have gained popularity, allowing individuals to explore their genetic makeup and ancestry.

2. Precision Medicine Initiatives: The growing emphasis on precision medicine is a major driver of the human genetics market. Precision medicine aims to tailor medical treatments to individual patients based on their genetic, environmental, and lifestyle factors. By using genetic information to guide treatment decisions, healthcare providers can improve patient outcomes and reduce adverse drug reactions. As pharmaceutical companies invest in genomics-driven drug development, the demand for genetic research and testing is expected to surge.

3. Advances in Genomic Technologies: Technological advancements in genomics, particularly NGS, have revolutionized the way researchers and clinicians study the human genome. NGS allows for the rapid sequencing of entire genomes or specific genetic regions at a fraction of the cost of traditional methods. This has made large-scale genomic studies feasible and has paved the way for the identification of rare genetic variants associated with complex diseases. Additionally, gene editing technologies like CRISPR-Cas9 have opened new avenues for gene therapy and the correction of genetic mutations.

4. Government and Private Funding: Governments and private organizations worldwide are investing heavily in genomics research and healthcare innovations. For instance, initiatives like the U.S. National Institutes of Health’s (NIH) All of Us Research Program and the UK Biobank project are aimed at collecting large-scale genetic data to better understand the interplay between genetics and disease. These projects are expected to provide valuable resources for the development of new diagnostic tools and therapies.

Challenges Facing the Market

While the human genetics market holds tremendous promise, it is not without its challenges:

1. Ethical and Privacy Concerns: As genetic testing becomes more widespread, concerns over the privacy and security of genetic data are mounting. The potential misuse of genetic information by insurers, employers, or other third parties has raised ethical questions. Ensuring robust data protection measures and addressing ethical concerns are critical to maintaining public trust in genetic services.

2. High Costs of Genetic Testing and Therapies: Despite the declining cost of genome sequencing, genetic testing and gene therapies remain expensive for many patients. The high costs of these services, along with limited reimbursement from insurance providers, can hinder widespread adoption, particularly in low- and middle-income countries.

3. Regulatory Hurdles: The human genetics market is subject to stringent regulatory oversight, particularly for gene-editing technologies and gene therapies. Navigating complex regulatory frameworks and gaining approval for new genetic products can be a lengthy and costly process.

Future Prospects

The future of the human genetics market is bright, with several key trends poised to drive growth in the coming years:

1. Expansion of Personalized Medicine: The continued integration of genetic data into clinical practice will accelerate the shift towards personalized medicine. As researchers gain a deeper understanding of how genetics influence drug response, personalized treatment plans will become more prevalent, improving patient outcomes and reducing healthcare costs.

2. Emergence of AI and Machine Learning: The integration of artificial intelligence (AI) and machine learning into genomics research is expected to revolutionize data analysis. These technologies can analyze vast amounts of genetic data more efficiently, identifying patterns and correlations that may not be apparent through traditional methods. This will enhance our ability to predict disease risk and develop targeted therapies.

3. Increased Accessibility of Genetic Testing: As the cost of genomic technologies continues to decline, genetic testing will become more accessible to a broader population. This will allow for earlier disease detection, improved preventive care, and more targeted treatments, ultimately reducing the burden of genetic disorders.

Key Player Analysis:

Agilent Technologies,

Atrys Health (Spain)

Myriad Genetics,

Biomarker Technology (US)

biorad laboratories,

Bode technology,

Echevarne Laboratory (Spain)

Elabscience Biotechnology Inc (US)

Eurofins Megalab S.A (Spain)

FullGenomics (Spain)

GE healthcare,

GENinCode (UK)

Illumina,

LabCorp,

LGS Forensic,

Myriad Genetics (US)

NIMGenetics (Spain)

Orchid Cellmark,

Promega,

QIAGEN,

Sistemas Genómicos (Spain)

Synlab Group (Germany)

Thermo Fisher Scientific,

Segmentation:

By Type:

Genetic testing,

Genetic analysis,

Genetic research services.

By End User:

Hospitals and clinics,

Research and academic institutions,

Pharmaceutical and biotechnology companies.

By Region:

North America

The U.S

Canada

Mexico

Europe

Germany

France

The U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/human-genetics-market

About Us:

Credence Research is committed to employee well-being and productivity. Following the COVID-19 pandemic, we have implemented a permanent work-from-home policy for all employees.

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

Transportation Management System Market - Forecast(2024 - 2030)

Transportation Management System Market Overview

Transportation Management System Market Size is forecast to reach $23.36 billion by 2027, at a CAGR of 17.6% during 2022–2027. The transportation management system is a part of enterprise resource planning which is a subset of supply chain management through which enterprises are able to plan effectively for in- shipment of route planning documentation and others. #Transportation #management allows tracking freight that’s on the road and even #receiving alerts to any transit exceptions or unforeseen delays from one location. The increasing complexities of logistics & transportation have resulted in #connected warehouses to new mileage delivery services which ultimately #increases the value and presence of TMS, transforming the old industry into an exciting place to drive change in community #development. An increase in demand for consumer goods leads along with the usage of cloud computing to a greater requirement of trade and transportation accomplishing the need for fleet management. An increase in the volume of trade goods will have a direct implication on the number of transportation management solutions & services. Hence, these are some of the factors propelling the growth of the Transportation Management System market in the forecast period 2022–2027.

Report Coverage

The report: “Transportation Management System Market — Forecast Repost (2022–2027)” by Industry ARC, covers an in-depth analysis of the following segments in the Transportation Management System Market.

By Offering: Solution (Traffic & Route Management, Order Management, Audit, Rating, Billing, Payment & Claims management, Fleet Monitoring & Tracking, Staff management, Warehouse, Hub & Yard Management, Reporting & Analytics, Others), Services (Training & Education, System Integration, Support & Maintenance).

By Transportation Mode: Roadways, Railways, Airways, Maritime.

By Organization Size: Small & Medium Enterprises, Large Enterprises.

By Deployment: Cloud, On-Premises.

By End-Users: Healthcare & Pharmaceuticals, Manufacturing, Mining, Marine, Energy & Utilities, Retail & E-Commerce, Transportation & Logistics, Government, Others.

By Geography: North America (U.S, Canada, Mexico), South America (Brazil, Argentina and others), Europe (Germany, UK, France, Italy, Spain, Russia and Others), APAC (China, Japan India, SK, Aus and Others) and RoW (the Middle East and Africa).

Sample Report:

Key Takeaways

As the global demand for agricultural seeds is rising consistently, transportation management in the agricultural industry becomes even more vital in ensuring the agricultural production and food supply chain runs smoothly to prevent shortages across the world.

The Transportation Management Systems Market Size is witnessing significant growth in the U.S. due to the advent of Solar PV and wind power technologies, both of which are recognized for their intermittent nature and also account for a large portion of the renewable energy potential in the United States. The problem necessitates the development of more efficient battery energy storage devices.

Leading transport management solution providers in the U.S. are offering a multi-modal, automated solution through cloud-based services which helps organizations gain control of load planning/optimization, load tendering, carrier selection, shipping, tracking, freight audit and allocation of inbound and outbound shipments. These factors are increasing the transportation management system market share.

Global Transportation Management System Market, By Region, 2021

For more details on this report — Request for Sample

Transportation Management System Market Segment Analysis — By Organization Size

The SMEs is growing at a significant CAGR of 19.36 % in the forecast period. In the transportation management system market, the Small and Medium Enterprises (SMEs) category is expected to dominate and hold the largest market share. The transportation management software and services help SMEs improve overall business productivity by offering concise information with a faster response time. Implementing these applications in SMEs through cloud-based services can also help with tracking deliveries in real-time, increasing customer service and increasing supply chain management along with fleet management ultimately increasing the transportation management system market share. As digitalization affects the contours of organizations across industries, the concept of small and medium-sized business models is destined to take on many new connotations. Automation’s penetration in enterprises of all sizes, large and small, is now the sole avenue that creates a level playing field for both large and small organizations. It is safe to conclude that in the coming years, the seamless deployment of SME transportation management systems will be the core competency that differentiates businesses.

Inquiry Before Buying:

Transportation Management System Market Segment Analysis — By Offerings

The transportation management system for solution market was valued at $5,819.85 Mn in 2021 and is estimated to reach $14424.46 Mn by 2027, growing at around a CAGR of 16.27% during 2022–2027. The solution is sub-segmented into traffic & route management, order management, audit, rating, billing, payment & claims management, fleet monitoring & tracking, staff management, warehouse, hub & yard management, reporting & analytics and others. A transportation management solution acts as a logistics platform that uses technology to help businesses plan, execute and optimize the physical movement of goods, both incoming and outgoing, ensuring that the shipment is compliant and proper documentation is available. TMS provides visibility into day-to-day transportation operations, trade compliance information and documentation and ensures the timely delivery of freight and goods. Transportation management systems also streamline the shipping process and make it easier for businesses to manage and optimize their transportation operations, thus increasing the transportation management system market share.

Schedule A Call:

Transportation Management System Market Segment Analysis — By Geography

Transportation Management System Industry in the North American region held a significant market share of 34% in 2020. U.S. Transportation Management System Market Size was valued at $2192.74 Mn in 2021 and is estimated to reach $5069.98 Mn by 2027, growing at around a CAGR of 14.91% during 2022–2027. The growth of the U.S. Transportation Management System is majorly attributed to factors like the exceptional growth of e-commerce in the US which subsequently surged online purchases and raised retail sales. In order to fulfill the growing demand, distributors, retailers and manufacturers are adopting robust TMS for managing customer expectations and streamlining the shipping process, while making it easier for businesses to manage and optimize their transportation operations. Furthermore, the trend of automation has penetrated into every industry vertical in the U.S. including the supply chain management market. As a result, logistics processes need to be planned more quickly and in greater detail. The Transportation Management Solution perfectly coordinates the warehouse and the road. Hence, Transportation management solution has been widely adopted in the U.S. among manufacturers, distributors and third-party logistics providers (3PLs) as a part of streamlining planning and executing the physical movement of goods.

Transportation Management System Market Drivers

Digital transformation in the sector is projected to drive market expansion:

Integration of the latest technologies such as blockchain and artificial intelligence, to improve transportation management system capabilities is one of the most recent and popular trends. The increasing preference for cloud-based services, Cloud Computing, anti-theft GPS and IoT-enabled solutions to provide transparency and security is pushing the use of sophisticated transportation management systems. The introduction of AI-enabled, self-driving trucks, fleet management, as well as the continuous development of 5G networks, are expected to change the transportation Management System industry and create new potential for market growth. The desire for greater agility in transportation and logistics operations that enable businesses to generate better customer experiences is being driven primarily by the industry’s digital transformation. The Internet of Things (IoT), big data and artificial intelligence (AI), as well as its predictive capabilities, have resulted in smarter and more effective transportation operations and this will help to boost the market growth. AI-powered predictive analytics can assist transportation service providers in optimizing route planning and delivery timetables. Furthermore, the technology-based strategy provides increased asset performance through timely maintenance, resulting in fewer failures.

Growing demand for E-commerce projected to drive the market:

With the internet gaining momentum and influence in all aspects of daily life over the last 15 years, package transportation has seen an increase in its reach and influence increasing the transportation management system market size. Because of the popularity of e-commerce, a rising number of individuals are purchasing things online rather than visiting brick-and-mortar establishments. This dramatic shift in the e-commerce sector is forcing shippers to adjust their supply chains to new technologies such as cloud computing and new ways for consumers to purchase items online. The e-commerce sector is rapidly expanding as more consumers use online platforms and smart gadgets for this purpose. E-commerce is on course to overtake traditional sales channels. The need for scalability, flexibility and visibility throughout the supply chain is propelling the transportation system market. With the rising e-commerce market around the world, the online retail market is evolving at a rapid pace and customers are looking for highly tailored experiences, which support market growth. As the transportation and logistics industries expand, the desire for smarter, more efficient and faster shipping services becomes increasingly vital, contributing considerably to the growth of the transportation management system market.

Buy Now:

Transportation Management System Market Challenge

Concerns about data security are growing and this will hinder market growth:

The risks of data exploitation and theft are increasing as shippers, forwarders, transportation companies and infrastructure providers digitize their processes. Enterprises have confidential data that must be protected to avoid data breaches and theft, which can harm the reputation of the enterprise as a whole. Data from businesses can leak across the internet and be viewed by unauthorized individuals, which is an increasing worry. For example, Transportation Management System Industry necessitates multitenant architecture, in which a single version of the software operates on a server shared by numerous customers. In this case, subscribers of an enterprise may be able to examine the data of competitors. These security risks pertaining to illegal data access would endanger enterprise data security as well as competitive business position.

Transportation Management System Market Landscape

Product launches, acquisitions, Partnerships and R&D activities are key strategies adopted by players in the Transportation Management System top 10 companies are Oracle Corporation, SAP SE, C.H ROBINSON, TRIMBLE, Inc., Blujay Solutions, Blue Yonder, Inlet-Logistics, Manhattan Associates, Metro Infrasys Private Limited, Mercuryate International Inc., among others.

Recent Developments

In 2022, C. H. Robinson announced a long-term strategic partnership with Waymo on mutually exploring the practical application of autonomous driving technology in both logistics and supply chains.

In 2021, SAP Transportation Management announced merging with Sedna Systems to allow shippers to use both products to gain a whole new level of control over transportation management-related data

For more Information and Communications Technology related reports, please click here

0 notes

Text

Clinical Trials 2024 Industry Size, Demands, Growth and Top Key Players Analysis Report

Clinical Trials Industry Overview

The global clinical trials market size was valued at USD 80.7 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 6.49% from 2024 to 2030.

The market growth spiked in 2020 owing to the COVID-19 pandemic. This growth pattern was witnessed by both virtual clinical trials and traditional ones. Several companies invested heavily in novel drug development to minimize COVID-19 patient burden. One such example being, in 2020, Synairgen plc and Parexel collaborated on a Phase III study of Interferon-beta (IFN-beta) treatment for COVID-19. Furthermore, rapid technological evolution, rising prevalence of chronic diseases, globalization of clinical trials, penetration of personalized medicine and a rise in demand for CROs for conducting research activities is expected to positively impact the market growth.

Gather more insights about the market drivers, restrains and growth of theClinical Trials Market

In addition, the COVID-19 pandemic led to changing the ways of conducting upcoming or ongoing clinical trials. Regulatory agencies including the U.S. FDA, the European Medicines Agency (EMA), the National Institutes of Health (NIH), and China’s National Medical Products Administration among several others issued various guidelines for conducting trials during the pandemic to support the implementation of decentralized clinical trials and virtual services. The current scenario for research and development activities across the globe and the need for several new treatment options have also led to the adoption of fast-track clinical trials. Thus, aforementioned factors are estimated to offer new avenues to the clinical trials market growth.

Favorable government support and initiatives is another aspect boosting the market growth potential. For instance, the WHO launched Solidarity, an international clinical trial to determine effective treatment against COVID-19. [PS2] It includes comparing four treatment options against the standard of care to evaluate their effectiveness against the coronavirus. In May 2020, the WHO also announced an international alliance for simultaneously developing multiple candidate vaccines to prevent the spread of the coronavirus disease, calling this effort the Solidarity trial for vaccines.

Furthermore, the use of CRO services helps manufacturers/sponsors pay complete attention to the production capacity and enhance their in-house processes. The availability of the vast array of services from drug discovery to post marketing surveillance has further simplified processes for mid-size & small-scale pharmaceutical and biotechnological organizations by providing them the option to outsource research and development activities to reduce infrastructure investment. For instance, in November 2023, Syneos Health signed an agreement with GoBroad Healthcare Group. This collaborative initiative extended the company’s clinical trial capabilities into a more extensive array of therapeutic areas in China.

Browse through Grand View Research's Healthcare IT Industry Research Reports.

The global digital neuro biomarkers market size was estimated at USD 593.1 million in 2023 and is projected to grow at a CAGR of 25.3% from 2024 to 2030.

The global healthcare digital experience platform market size was valued at USD 1.26 billion in 2023 and is forecasted to grow at a CAGR of 12.5% from 2024 to 2030.

Clinical Trials Market Segmentation

Grand View Research has segmented the global clinical trials market based on phase, study design, indication, sponsor, indication by study design, and region:

Clinical Trials Phase Outlook (Revenue, USD Billion, 2018 - 2030)

Phase I

Phase II

Phase III

Phase IV

Clinical Trials Study Design Outlook (Revenue, USD Billion, 2018 - 2030)

Interventional

Observational

Expanded Access

Clinical Trials Indication by Study Design Outlook (Revenue, USD Billion, 2018 - 2030)

Autoimmune/Inflammation

Rheumatoid Arthritis

Multiple Sclerosis

Osteoarthritis

Irritable Bowel Syndrome (IBS)

Others

Pain Management

Chronic Pain

Acute Pain

Oncology

Blood Cancer

Solid Tumors

Other

CNS Condition

Epilepsy

Parkinson's Disease (PD)

Huntington's Disease

Stroke

Traumatic Brain Injury (TBI)

Amyotrophic Lateral Sclerosis (ALS)

Muscle Regeneration

Others

Diabetes

Obesity

Cardiovascular

Others

Clinical Trials Indication Outlook (Revenue, USD Billion, 2018 - 2030)

Autoimmune/Inflammation

Interventional

Observational

Expanded Access

Pain Management

Interventional

Observational

Expanded Access

Oncology

Interventional

Observational

Expanded Access

CNS Condition

Interventional

Observational

Expanded Access

Diabetes

Interventional

Observational

Expanded Access

Obesity

Interventional

Observational

Expanded Access

Cardiovascular

Interventional

Observational

Expanded Access

Others

Interventional

Observational

Expanded Access

Clinical Trials Sponsor Outlook (Revenue, USD Billion, 2018 - 2030)

Pharmaceutical & Biopharmaceutical Companies

Medical Device Companies

Others

Clinical Trials Service Type Outlook (Revenue, USD Billion, 2018 - 2030)

Protocol Designing

Site Identification

Patient Recruitment

Laboratory Services

Bioanalytical Testing Services

Clinical Trial Data Management Services

Others

Clinical Trials Regional Outlook (Revenue, USD Billion, 2018 - 2030)

North America

US

Canada

Europe

UK

Germany

France

Spain

Italy

Asia Pacific

India

Japan

China

Australia

South Korea

Latin America

Brazil

Mexico

Argentina

Colombia

Middle East & Africa

South Africa

Saudi Arabia

UAE

Key Companies profiled:

IQVIA

PAREXEL International Corporation

Pharmaceutical Product Development, LLC

Charles River Laboratory

ICON Plc

PRA Health Sciences

Syneos Health

Eli Lilly and Company

Novo Nordisk A/S

Pfizer

Clinipace

Recent Developments

In August 2023, Parexel & Partex entered a strategic partnership aimed at utilizing Artificial Intelligence (AI)-driven solutions to expedite the process of drug discovery and development for biopharmaceutical clients globally. The collaboration aimed to reduce risks associated with the assets in their respective portfolios.

In August 2023, Novo Nordisk announced to acquire Inversago Pharma. This acquisition was part of Novo Nordisk's strategic efforts to develop new therapies targeting individuals with obesity, diabetes, and other significant metabolic diseases

Order a free sample PDF of the Clinical Trials Market Intelligence Study, published by Grand View Research.

0 notes

Text

The U.S. Pharmaceutical market size was estimated at USD 0.85 billion in 2023 and is projected to hit around USD 1.46 billion by 2033, growing at a CAGR of 5.59% during the forecast period from 2024 to 2033. according to a new report by Nova One Advisor.

0 notes

Text

The U.S. pharmaceutical analytical testing outsourcing market size was exhibited at USD 4.50 billion in 2023 and is projected to hit around USD 9.07 billion by 2032, growing at a CAGR of 8.1% during the forecast period 2023 to 2032.

0 notes

Text

Cancer Biologics Market Future Outlook: Predictions and Analysis

The global cancer biologics market is projected to experience robust growth, with its market size expected to expand from USD 102.2 billion in 2023 to an impressive USD 195.5 billion by 2032. The market is set to grow at a compound annual growth rate (CAGR) of 7.5% during the forecast period from 2024 to 2032, driven by technological advancements in biologic therapies and an increasing global burden of cancer.

Cancer biologics are advanced therapeutic agents derived from living organisms or their products, such as proteins, DNA, and antibodies, designed to target specific cancer cells. Unlike traditional chemotherapy, biologics are often more precise and offer the potential to minimize damage to healthy cells, making them a preferred treatment option for various types of cancer.

Get Free Sample PDF: https://www.snsinsider.com/sample-request/4512

Key Drivers of Market Growth

Rising Cancer Incidence: The global rise in cancer cases is a significant factor propelling the demand for biologics. According to the World Health Organization (WHO), cancer is one of the leading causes of death globally, with millions of new cases diagnosed each year. As the global population ages, the incidence of cancer is expected to increase, driving the demand for effective and innovative treatment options like biologics.

Advances in Biotechnology and Immunotherapy: Recent advancements in biotechnology, particularly in immunotherapy and targeted therapies, are revolutionizing cancer treatment. Cancer biologics, such as monoclonal antibodies, cell-based therapies, and checkpoint inhibitors, have shown great promise in improving patient outcomes. The success of immuno-oncology therapies like CAR-T cell therapies and immune checkpoint inhibitors has expanded treatment options for patients and created a surge in market demand.

Personalized Medicine and Precision Oncology: The trend toward personalized medicine and precision oncology is another critical growth driver for cancer biologics. By tailoring treatments based on individual genetic profiles and tumor characteristics, biologics offer a more targeted approach to cancer treatment. This reduces the likelihood of adverse side effects and enhances treatment efficacy, particularly for patients with rare or aggressive cancers.

Favorable Regulatory Approvals: The regulatory landscape for cancer biologics has also improved in recent years, with several breakthrough therapies receiving fast-track approvals from regulatory bodies like the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA). These expedited approval processes have encouraged pharmaceutical companies to invest in research and development (R&D) for new biologics, accelerating the market’s growth.

Challenges and Opportunities

While the cancer biologics market holds great promise, several challenges remain. High development costs, complex manufacturing processes, and the need for advanced infrastructure to produce biologics can act as barriers for smaller biotech firms. Additionally, the cost of cancer biologic therapies can be prohibitively expensive, limiting access for patients in low- and middle-income countries.

However, significant opportunities exist, particularly in the areas of biosimilars and next-generation biologics. As patents for several blockbuster biologic drugs expire, the market for biosimilars—cheaper, highly similar alternatives—will expand, offering more affordable treatment options for cancer patients. Moreover, continuous innovation in biopharmaceuticals, including advancements in gene editing and cell-based therapies, will open new pathways for cancer treatment, further driving market growth.

Regional Insights

North America continues to dominate the cancer biologics market, attributed to its strong healthcare infrastructure, high levels of investment in R&D, and a large patient population. The U.S. market, in particular, benefits from government support for cancer research and early adoption of innovative therapies.

Europe follows closely, with significant investments in biotechnology and increasing access to advanced cancer treatments. The Asia-Pacific region is expected to witness the fastest growth during the forecast period due to rising cancer incidence, improving healthcare infrastructure, and increasing government initiatives to promote cancer research. Countries like China and India are becoming key players in the market, with growing R&D activities and expanding access to biologic treatments.

Future Outlook

The future of the cancer biologics market looks promising, with continued advancements in biotechnology, precision medicine, and immunotherapy expected to drive significant growth. With a projected CAGR of 7.5% from 2024 to 2032, the market is on track to nearly double in size, reaching USD 195.5 billion by 2032. Biologics will play a central role in the ongoing battle against cancer, offering new hope for patients and transforming cancer care worldwide.

In conclusion, the cancer biologics market is set for robust growth, driven by rising cancer incidence, advancements in biotechnology, and the increasing adoption of personalized medicine. From USD 102.2 billion in 2023, the market is expected to reach USD 195.5 billion by 2032, significantly impacting the global healthcare landscape.

Other Trending Reports

Smart Fertility Tracker Market

Venous Thromboembolism Treatment Market

Automated Liquid Handling Technologies Market

Digestive Health Supplements Market

0 notes

Text

eClinical Solutions Market: Competitive Insights and Precise Outlook | 2024-2031

Leading market research firm SkyQuest Technology Group recently released a study titled 'eClinical Solutions Market Global Size, Share, Growth, Industry Trends, Opportunity and Forecast 2024-2031,' This study eClinical Solutions report offers a thorough analysis of the market, as well as competitor and geographical analysis and a focus on the most recent technological developments. The research study on the eClinical Solutions Market extensively demonstrates existing and upcoming opportunities, profitability, revenue growth rates, pricing, and scenarios for recent industry analysis.

The research analysis on the global eClinical Solutions Market report 2024 offers a close watch on top industry rivals along with briefings on their company profiles, strategical surveys, micro as well as macro industry trends, futuristic scenarios, analysis of pricing structure, and an all-encompassing overview of the eClinical Solutions Market circumstances in the forecast period between 2024 and 2031. The global eClinical Solutions Market is a dynamic and rapidly evolving sector, encompassing the development, production, and distribution. This market is essential for improving global market and driving economic growth through innovation and industry advancements.

Market Growth

The eClinical Solutions Market has experienced robust growth over the past decade and is projected to continue expanding. Global eClinical Solutions Market size was valued at USD 7.18 Billion in 2022 and is poised to grow from USD 8.15 Billion in 2023 to USD 22.35 Billion by 2031, growing at a CAGR of 13.4 % in the forecast period (2024-2031). This growth is driven by several factors, including an aging global population, increasing prevalence of advancements in technology, and rising global expenditure.

Chance to get a free sample @ https://www.skyquestt.com/sample-request/eclinical-solutions-market

Detailed Segmentation and Classification of the report (Market Size and Forecast - 2031, Y-o-Y growth rate, and CAGR):

The eClinical Solutions Market can be segmented based on several factors, including product type, application, end-user, and distribution channel. Understanding these segments is crucial for companies looking to target specific markets and tailor their offerings to meet consumer needs.

Product

EDC & CDMS, CTMS, Clinical Analytics Platforms, RTSM, RIMS, eCOA Solutions, eTMF System, and Others

Delivery mode

Web-hosted Models, On-Premises, Licensed Enterprise Models, and Cloud-based Solutions

End Use

Pharmaceutical & Biopharmaceutical Companies, Contract Research Organizations, Consultancy Service Companies, Medical Device Manufacturers, Hospitals, Academic & Research Institutes

Get your customized report @ https://www.skyquestt.com/speak-with-analyst/eclinical-solutions-market

Following are the players analyzed in the report:

Oracle Corporation

Medidata Solutions, Inc.

Parexel International Corporation

Bioclinica, Inc.

OpenClinica (US)

DATATRAK International, Inc. (US)

CRF Health (UK)

Advarra (US)

MedNet Solutions, Inc. (US)

Bio-Optronics, Inc. (US)

eClinicalWorks LLC (US)

ArisGlobal LLC (US)

Regional Analysis

1. North America:

- The United States and Canada dominate the North American eClinical Solutions Market. The U.S. is the largest market globally, driven by advanced global infrastructure, high R&D investments, and significant eClinical Solutions consumption.

2. Europe:

- Europe is a significant player, with major eClinical Solutions Markets in Germany, France, and the United Kingdom. The region benefits from strong regulatory frameworks, high industry standards, and a robust R&D sector.

3. Asia-Pacific:

- This region is experiencing rapid growth, with countries like China and India leading the charge. Factors such as increasing industry access, growing middle-class populations, and expanding eClinical Solutions manufacturing capabilities contribute to this growth.

4. Latin America:

- Brazil and Mexico are key markets in Latin America. Growth in this region is driven by rising industry needs, increasing investments in industry infrastructure, and a growing demand for affordable medications.

5. Middle East and Africa:

- The eClinical Solutions Market in this region is expanding due to rising market spending, increased prevalence of diseases, and improvements in Market infrastructure, although the market is relatively smaller compared to other regions.

Future Outlook

The eClinical Solutions Market is poised for continued growth driven by technological advancements, expanding global market access, and increasing global industry needs. As the industry adapts to evolving challenges and seizes emerging opportunities, it is likely to see ongoing innovation and expansion, contributing significantly to global health and economic development.

Buy your full report: https://www.skyquestt.com/buy-now/eclinical-solutions-market

0 notes

Text

Chemical Injection Skid Market Analysis: Projected to Reach $2.8 Bn by 2034