#Thermal Energy Storage Market share

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

If you dial 1-866-584-6757, you can leave an audio post for your followers.

Text

The global thermal energy storage market size was valued at USD 4.1 billion in 2019 and is projected to grow at a compound annual growth rate (CAGR) of 9.45% from 2020 to 2027.

Shifting preference towards renewable energy generation, including concentrated solar power, and rising demand for thermal energy storage (TES) systems in HVAC are among the key factors propelling the industry growth. Growing need for enhanced energy efficiency, coupled with continuing energy utilization efforts, will positively influence the thermal energy storage demand. For instance, in September 2018, the Canadian government updated a financial incentive plan “Commercial Energy Conservation and Efficiency Program” that offers USD 15,000 worth rebates for commercial sector energy upgrades.

Gather more insights about the market drivers, restrains and growth of the Thermal Energy Storage Market

The market in the U.S. is projected to witness substantial growth in the forthcoming years on account of increasing number of thermal energy storage projects across the country. For instance, in 2018, the U.S. accounted for 33% of the 18 under construction projects and 41% of the total 1,361 operational projects globally. Presence of major industry players in the country is expected to further propel the TES market growth in the U.S.

The U.S. Department of Energy (DoE) evaluates thermal energy storage systems for their safety, reliability, cost-effective nature, and adherence to environmental regulations and industry standards. It also stated that Europe and the Asia Pacific display higher fractions of grid energy storage as compared to North America. Rising need for a future with clean energy is prompting governments across the globe to take efforts towards developing innovative energy storage systems.

The primary challenge faced by the thermal energy storage sector is the economical storage of energy. An important advancement in this sector has been the usage of lithium-ion batteries. These batteries exhibit high energy density and long lifespans of 500 deep cycles, i.e. the number of times they can be charged from 20% to their full capacity before witnessing a deterioration in performance. They can also be utilized in electric vehicles, district cooling and heating, and power generation.

Thermal Energy Storage Market Segmentation

Grand View Research has segmented the global thermal energy storage market report on the basis of product type, technology, storage material, application, end user, and region:

Product Type Outlook (Revenue, USD Million, 2016 - 2027)

• Sensible Heat Storage

• Latent Heat Storage

• Thermochemical Heat Storage

Technology Outlook (Revenue, USD Million, 2016 - 2027)

• Molten Salt Technology

• Electric Thermal Storage Heaters

• Solar Energy Storage

• Ice-based Technology

• Miscibility Gap Alloy Technology

Storage Material Outlook (Revenue, USD Million, 2016 - 2027)

• Molten Salt

• Phase Change Material

• Water

Application Outlook (Revenue, USD Million, 2016 - 2027)

• Process Heating & Cooling

• District Heating & Cooling

• Power Generation

• Ice storage air-conditioning

• Others

End-user Outlook (Revenue, USD Million, 2016 - 2027)

• Industrial

• Utilities

• Residential & Commercial

Regional Outlook (Revenue, USD Million, 2016 - 2027)

• North America

o U.S.

o Canada

o Mexico

• Europe

o U.K.

o Russia

o Germany

o Spain

• Asia Pacific

o China

o India

o Japan

o South Korea

• Central & South America

o Brazil

• Middle East and Africa (MEA)

o Saudi Arabia

Browse through Grand View Research's Power Generation & Storage Industry Research Reports.

• The global energy storage for unmanned aerial vehicles market size was estimated at USD 413.25 million in 2023 and is expected to grow at a CAGR of 27.8% from 2024 to 2030.

• The global heat recovery steam generator market size was estimated at USD 1,345.2 million in 2023 and is projected to reach USD 1,817.0 million by 2030 and is anticipated to grow at a CAGR of 4.5% from 2024 to 2030.

Key Companies & Market Share Insights

Industry participants are integrating advanced technologies into the existing technology to enhance the product demand through the provision of improved thermal energy management systems. Furthermore, eminent players are emphasizing on inorganic growth ventures as a part of their strategic expansion. Some of the prominent players in the global thermal energy storage market include:

• BrightSource Energy Inc.

• SolarReserve LLC

• Abengoa SA

• Terrafore Technologies LLC

• Baltimore Aircoil Company

• Ice Energy

• Caldwell Energy

• Cryogel

• Steffes Corporation

Order a free sample PDF of the Thermal Energy Storage Market Intelligence Study, published by Grand View Research.

#Thermal Energy Storage Market#Thermal Energy Storage Industry#Thermal Energy Storage Market size#Thermal Energy Storage Market share#Thermal Energy Storage Market analysis

0 notes

Text

Thermal Energy Storage Market Dynamics: Innovations and Opportunities

Introduction

Thermal energy storage (TES) refers to technologies that provide long-term storage of heat or cold for later use. Unlike conventional batteries, TES systems stock thermal energy by utilizing heat transfer between a storage medium and a heat sink or source. TES promises to deliver energy stability, address intermittency issues associated with renewable sources like solar and wind, and reduce peak demand on generation systems. Need and Applications of Thermal Energy Storage

There are several factors driving the need for widespread implementation of TES technologies. One key factor is the intermittent nature of renewable sources like solar and wind which produce energy only when the sun shines or wind blows. TES allows excess thermal energy generated from such resources to be stored for later use when the source may not be available. Secondly, TES helps address demand-supply mismatch problems as heat can be stored during off-peak generation periods and supplied when demand peaks. This helps shave peak loads on the electric grid and reduce transmission congestion. TES also finds applications in buildings for space cooling and heating by buffering energy from HVAC systems. Other notable uses include industrial process heating/cooling and production of chilled water for air conditioning. TES Materials and Methods

A variety of materials and technologies are used for TES depending on the temperature range and period of storage required. Sensible heat storage systems store energy by altering the temperature of a solid or liquid storage medium like water, molten salts, rocks or phase change materials. Latent heat storage utilizes the heat released or absorbed during phase transition of substances like paraffin wax or water for storage. Thermochemical storage relies on reversible endothermic chemical reactions to store energy in chemical bonds. Other methods include cryogenic storage using liquefied air or hydrogen and temperature gradient exchange using metallic foams. Each approach has its technical and economic viability depending on the application. Commercial Applications of TES

Several commercial TES systems are currently operational worldwide to support solar thermal power plants and process heating applications. Andasol, located in Spain, was one of the first commercial plants to use molten salt storage achieving over 7 hours of full-load energy generation after sunset. Solar One and Solar Two projects in USA demonstrated 10 hours molten salt storage coupled with solar power towers. Industrial process heating levers TES vastly for processes requiring steam or heat treatment. Buildings have begun integrating TES in form of borehole thermal energy storage to provide summer cooling and winter heating. Moving forward, cost reductions through economies of scale and material innovations will make TES increasingly viable across sectors. R&D Focus and Future Potential

Significant research continues to emerge new storage materials, designs targeting specific heat applications and system optimization. PCMs ranging from biobased oils to graphene-enhanced composites are being examined for high density storage. Thermochemical storage employing reversible hydrolysis/dehydration of salt hydrates shows promise at high temperatures. Researchers are also modeling hybrid thermal-electric systems leveraging complementary storage abilities. Government incentives and industry partnerships are supportingseveral large-scale pilot projects worldwide. If technology and installation costs keep declining, TES could emerge as a mainstream approach to store tens of gigawatt-hours of thermal energy in the future. Integrated with solar, waste heat and smart grids, it may play a transformative role in global energy management. Conclusion

In conclusion, thermal energy storage is an important technology that helps maximize renewable energy generation, address intermittency issues and reduce grid loads from peak demand. It enables shifting of thermal loads in time by decoupling energy generation from use through versatile heat storage approaches. With further innovation and cost reductions, diverse TES solutions could soon help transition energy systems towards greater sustainability, flexibility and resilience worldwide. Looking ahead, hybrid multi-applications of TES will undoubtedly maximize its overall techno-economic and environmental benefits.

#Thermal Energy Storage Market Growth#Thermal Energy Storage Market Size#Thermal Energy Storage Market Share

0 notes

Text

Thermal Energy Storage Market Outlook On The Basis Of Product Type, Technology, Storage Material, Application, End User, Region And Forecast From 2027: Grand View Research Inc.

San Francisco, 16 May 2023: The Report Thermal Energy Storage Market Size, Share & Trends Analysis Report By Product Type, By Technology, By Storage Material, By Application, By End User, By Region, And Segment Forecasts, 2020 – 2027 The global thermal energy storage market size is expected to reach USD 7.74 billion by 2027, expanding at a CAGR of 9.45% from 2020 to 2027, according to a new…

View On WordPress

#Thermal Energy Storage Industry#Thermal Energy Storage Market#Thermal Energy Storage Market 2020#Thermal Energy Storage Market 2027#Thermal Energy Storage Market Revenue#Thermal Energy Storage Market Share#Thermal Energy Storage Market Size

0 notes

Text

#Thermal Energy Storage Market Size#Projections of Share#Trends#and Growth for 2022-2028 | 195 Pages Report#intellectualmarketinsights

0 notes

Text

#Thermal Energy Storage Market#Thermal Energy Storage Market size#Thermal Energy Storage Market share#Thermal Energy Storage Market trends#Thermal Energy Storage Market analysis#Thermal Energy Storage Market forecast#Thermal Energy Storage Market outlook

0 notes

Text

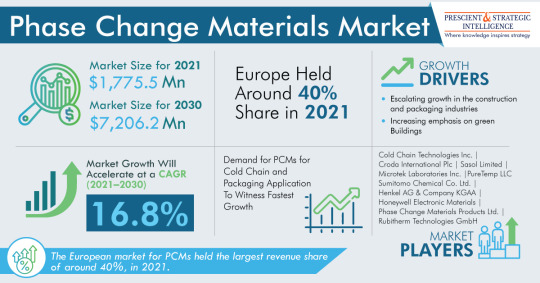

Transforming Industries: Phase Change Materials Market Insights

As stated by P&S Intelligence, the total revenue generated by the phase change materials market was USD 1,775.5 million in 2021, which will power at a rate of 16.8% by the end of this decade, to reach USD 7,206.2 million by 2030.

This has a lot to do with the increasing growth in the construction and packaging sectors and increasing importance on green buildings.

Cold chain and packaging category will grow at the highest rate, of above 17%, in the years to come. This can be mostly because of the surge in PCM requirement to sustain precise temperatures through the supply chain while lowering the emissions of carbon dioxide. Using ACs and electric fans to stay cool contributes to approximately 20% of the total electricity employed in buildings globally. The increasing requirement for space cooling is straining quite a few countries' power infrastructure, along with bringing about increased emissions.

With the enormous increase in the requirement for energy-efficient ACs, the requirement for PCMs will soar, as the electrical consumption of modified ACs with PCMs could be brought down by 3.09 kWh every day.

Europe dominated the industry with a share, of about 40%, in the recent past. The predisposition toward the acceptance of eco-friendly materials will power the PCM industry in the region. European regulatory associations, such as the SCANVAC, took more than a few initiatives for developing and promoting and effective building mechanical solutions and increase awareness pertaining to PCM applications.

The convenience of paraffin at a wide range of temperatures is a major reason for its appropriateness as an energy storage medium. Likewise, paraffin-based PCM is called a waxy solid paraffin, safe, dependable, noncorrosive, and economical material.

HVAC systems had the second-largest share, of about 30%, in phase change materials market in the recent past. This has a lot to do with the fact that PCM installation decreases fluctuations of temperature. HVAC with PCM supports in maintaining a steadier temperature and eliminating thermal uneasiness caused by alterations in temperature. It is because of the emphasis on green buildings, the demand for phase change materials will continue to rise considerably in the years to come.

#Phase Change Material Market#Phase Change Material Market Size#Phase Change Material Market Share#Phase Change Material Market Growth#Phase change materials (PCMs)#Thermal energy storage#Energy efficiency solutions#Heat management technology#Sustainable materials#Building insulation#HVAC systems#Thermal regulation#Cold chain logistics#Renewable energy storage#Temperature-sensitive packaging

0 notes

Text

Captivating Investment Opportunities in the Thriving Thermal Energy Storage Market

Thermal energy storage (TES) is a technology that allows for the storage of excess thermal energy produced during off-peak hours for later use. It plays a crucial role in managing the demand and supply fluctuations of energy, especially in the context of renewable energy sources. TES systems store thermal energy in the form of hot or cold fluids, phase-change materials (PCMs), or through thermochemical reactions, and then release it when required.

The Thermal Energy Storage Market has been experiencing significant growth in recent years, driven by several factors such as increasing focus on renewable energy integration, the need for energy efficiency, and growing environmental concerns. TES provides a reliable and efficient solution for grid stabilization, load shifting, and balancing energy demand.

The global thermal energy storage market size was valued at US$ 4.65 Billion in 2022 and is anticipated to witness a compound annual growth rate (CAGR) of 10.28% from 2023 to 2030. The global thermal energy storage market is expected to witness a significant growth during the forecast period. This is attributed to increasing adoption of renewable power generation and growing demand for HVAC thermal energy storage systems. Moreover, the rising concern over greenhouse gas emissions and increasing fuel prices are further expected to drive demand for advanced thermal energy storage systems.

Here are some key aspects and trends in the Thermal Energy Storage Market:

Types of Thermal Energy Storage:

a. Sensible Heat Storage: In this type, thermal energy is stored by heating or cooling a liquid or solid material, such as water, rocks, or concrete. b. Latent Heat Storage: It involves the phase change of a material, typically a PCM, which absorbs or releases heat during the transition from solid to liquid and vice versa. c. Thermochemical Storage: This method stores energy through reversible chemical reactions that absorb or release heat.

Applications:

a. Residential and Commercial Heating: TES can be used for space heating and hot water production in residential and commercial buildings. b. Industrial Processes: TES is employed in various industrial sectors, including food and beverage, chemical, and manufacturing, to optimize energy use and reduce peak energy demand. c. Power Generation: TES technologies enable efficient operation and load balancing in power plants, especially in concentrated solar power (CSP) systems. d. District Heating and Cooling: TES systems can be integrated into district energy networks, providing efficient heating and cooling solutions for communities. e. Grid Energy Storage: TES helps in storing excess energy generated from renewable sources and releasing it during periods of high demand, thus supporting grid stability and reducing reliance on fossil fuel-based power plants.

Market Drivers:

a. Renewable Energy Integration: TES facilitates the integration of intermittent renewable energy sources, such as solar and wind, by storing excess energy for use during periods of low generation. b. Energy Efficiency: TES improves the overall energy efficiency of systems by reducing energy waste and optimizing energy use. c. Environmental Concerns: Growing environmental awareness and the need to reduce greenhouse gas emissions are driving the adoption of TES as a sustainable energy storage solution. d. Government Initiatives: Supportive policies and incentives provided by governments across the globe are promoting the deployment of TES technologies.

Regional Market Outlook:

a. North America: The United States and Canada are witnessing significant growth in the TES market, driven by renewable energy targets and increasing adoption of TES in various industries. b. Europe: Countries like Germany, Spain, and Denmark are leading the TES market in Europe, primarily due to their focus on renewable energy and energy storage technologies. c. Asia Pacific: China, India, and Japan are experiencing rapid growth in the TES sector, supported by government initiatives, investments in renewable energy, and increasing industrialization. d. Middle East and Africa: The Middle East region, with its abundant solar resources, is adopting TES technologies for CSP systems, while African countries are exploring TES for off-grid and rural electrification projects.

Key Market Players:

a. CALMAC Corporation b. DN Tanks c. Abengoa Solar d. BrightSource Energy e. SolarReserve f. Tesla, Inc. g. Ice Energy h. Burns & McDonnell i. Goss Engineering j. Steffes Corporation

The Thermal Energy Storage Market is expected to witness significant growth in the coming years, driven by the increasing demand for renewable energy integration, grid stabilization, and energy efficiency. Advancements in materials, technologies, and the supportive regulatory environment will continue to fuel the market's expansion, leading to a more sustainable and reliable energy future.

0 notes

Text

#Global Molten Salt Solar Energy Thermal Storage Market Size#Share#Trends#Growth#Industry Analysis#Key Players#Revenue#Future Development & Forecast 2023-2032

0 notes

Text

"A 1-megawatt sand battery that can store up to 100 megawatt hours of thermal energy will be 10 times larger than a prototype already in use.

The new sand battery will eliminate the need for oil-based energy consumption for the entire town of town of Pornainen, Finland.

Sand gets charged with clean electricity and stored for use within a local grid.

Finland is doing sand batteries big. Polar Night Energy already showed off an early commercialized version of a sand battery in Kankaanpää in 2022, but a new sand battery 10 times that size is about to fully rid the town of Pornainen, Finland of its need for oil-based energy.

In cooperation with the local Finnish district heating company Loviisan Lämpö, Polar Night Energy will develop a 1-megawatt sand battery capable of storing up to 100 megawatt hours of thermal energy.

“With the sand battery,” Mikko Paajanen, CEO of Loviisan Lämpö, said in a statement, “we can significantly reduce energy produced by combustion and completely eliminate the use of oil.”

Polar Night Energy introduced the first commercial sand battery in 2022, with local energy utility Vatajankoski. “Its main purpose is to work as a high-power and high-capacity reservoir for excess wind and solar energy,” Markku Ylönen, Polar Nigh Energy’s co-founder and CTO, said in a statement at the time. “The energy is stored as heat, which can be used to heat homes, or to provide hot steam and high temperature process heat to industries that are often fossil-fuel dependent.” ...

Sand—a high-density, low-cost material that the construction industry discards [Note: 6/13/24: Turns out that's not true! See note at the bottom for more info.] —is a solid material that can heat to well above the boiling point of water and can store several times the amount of energy of a water tank. While sand doesn’t store electricity, it stores energy in the form of heat. To mine the heat, cool air blows through pipes, heating up as it passes through the unit. It can then be used to convert water into steam or heat water in an air-to-water heat exchanger. The heat can also be converted back to electricity, albeit with electricity losses, through the use of a turbine.

In Pornainen, Paajanen believes that—just by switching to a sand battery—the town can achieve a nearly 70 percent reduction in emissions from the district heating network and keep about 160 tons of carbon dioxide out of the atmosphere annually. In addition to eliminating the usage of oil, they expect to decrease woodchip combustion by about 60 percent.

The sand battery will arrive ready for use, about 42 feet tall and 49 feet wide. The new project’s thermal storage medium is largely comprised of soapstone, a byproduct of Tulikivi’s production of heat-retaining fireplaces. It should take about 13 months to get the new project online, but once it’s up and running, the Pornainen battery will provide thermal energy storage capacity capable of meeting almost one month of summer heat demand and one week of winter heat demand without recharging.

“We want to enable the growth of renewable energy,” Paajanen said. “The sand battery is designed to participate in all Fingrid’s reserve and balancing power markets. It helps to keep the electricity grid balanced as the share of wind and solar energy in the grid increases.”"

-via Popular Mechanics, March 13, 2024

--

Note: I've been keeping an eye on sand batteries for a while, and this is really exciting to see. We need alternatives to lithium batteries ASAP, due to the grave human rights abuses and environmental damage caused by lithium mining, and sand batteries look like a really good solution for grid-scale energy storage.

--

Note 6/13/24: Unfortunately, turns out there are substantial issues with sand batteries as well, due to sand scarcity. More details from a lovely asker here, sources on sand scarcity being a thing at the links: x, x, x, x, x

#sand#sand battery#lithium#lithium battery#batteries#technology news#renewable energy#clean energy#fossil fuels#renewables#finland#good news#hope#climate hope

1K notes

·

View notes

Text

Top 10 PEB Companies in India: Leaders in Pre-Engineered Building Solutions

India’s construction industry is rapidly evolving, and Pre-Engineered Buildings (PEBs) are at the forefront of this transformation. With their cost-effectiveness, faster construction, and sustainability, PEBs have become the preferred choice for industries like warehousing, manufacturing, logistics, and commercial infrastructure.

For businesses looking for trusted PEB manufacturers, here’s a look at the top 10 PEB companies in India, their strengths, and how they are contributing to the industry’s growth.

1. EPACK Prefab – A Leading Name in PEB Solutions

🏢 Established: 1999 📍 Headquarters: Greater Noida, Uttar Pradesh 🔹 Specialization: Custom PEB structures, modular buildings, and prefabricated solutions. 🌟 Why EPACK Prefab? ✔ Cutting-Edge Technology: Utilizes CNC machines, automation, and precision engineering for superior quality. ✔ Sustainable & Eco-Friendly: Focuses on recyclable materials and energy-efficient solutions. ✔ Diverse Industry Expertise: Serves warehouses, factories, airports, cold storage, and commercial buildings. ✔ Proven Success: Over 2,500 completed projects across India, with a strong portfolio in industrial and infrastructure developments.

EPACK Prefab is one of the many companies driving the PEB industry forward with innovation and expertise. Learn more about EPACK Prefab’s projects and solutions.

2. Kirby Building Systems India Pvt Ltd

📍 Hyderabad, Andhra Pradesh 🌟 Expertise: Global leader in pre-engineered steel building solutions with a strong presence in India.

3. Lloyd Insulations (India) Limited

📍 Mumbai, Maharashtra 🌟 Expertise: PEBs with a specialization in thermal and acoustic insulation for industrial buildings.

4. Zamil Steel Buildings India Pvt Ltd

📍 Chennai, Tamil Nadu 🌟 Expertise: High-durability steel structures with an international standard of engineering.

5. Interarch Building Products Pvt Ltd

📍 Noida, Uttar Pradesh 🌟 Expertise: Turnkey steel buildings, with a focus on innovation and modular designs.

6. Tata BlueScope Steel

📍 Pune, Maharashtra 🌟 Expertise: High-performance PEB solutions backed by Tata Steel’s legacy.

7. Larsen & Toubro Limited (L&T)

📍 Mumbai, Maharashtra 🌟 Expertise: Large-scale infrastructure projects, including industrial PEBs.

8. Everest Industries Limited

📍 New Delhi, India 🌟 Expertise: Prefabricated steel structures and roofing solutions.

9. Multicolor Steels

📍 Gurgaon, Haryana 🌟 Expertise: Affordable and customized PEB structures for various industries.

10. Steelbuild Infra Projects Pvt Ltd

📍 India 🌟 Expertise: Fast-growing PEB provider known for innovative and cost-effective solutions.

Why PEBs Are the Future of Construction in India?

✅ Faster Project Completion: PEB structures reduce construction time by 40-50%. Explore why PEBs are the future of construction. ✅ Cost Savings: Pre-engineered components minimize labor and material costs. ✅ Customizable & Scalable: Easily modified to meet expanding business needs. ✅ Eco-Friendly & Sustainable: Built with recyclable steel and energy-efficient materials. ✅ Durability & Strength: Steel structures ensure long-lasting, weather-resistant buildings.

Conclusion

As the PEB market in India continues to expand, industry leaders are setting benchmarks with their innovative solutions, high-quality manufacturing, and reliable project execution. Whether you’re looking for a warehouse, logistics hub, industrial facility, or commercial structure, choosing the right PEB manufacturer is key to a successful and cost-efficient project.

📢 What are your thoughts on the growth of PEBs in India? Share your insights in the comments below!

Read More - Why Pre-Engineered Commercial Buildings are a Smart Choice for Modern Construction?

#PEBCompanies#PreEngineeredBuildings#PEBIndustry#SteelBuildings#ModularConstruction#IndustrialSolutions#SustainableBuilding#ConstructionIndustry#PEBManufacturers#PrefabStructures#EPACK Prefab

1 note

·

View note

Text

Key Players in Military Vehicle Electrification Market

The Military Vehicle Electrification Market is poised for substantial growth, projected to expand from USD 4.1 Billion in 2023 to USD 20.4 Billion by 2030, at an impressive CAGR of 25.6%. This market surge is driven by technological advancements, operational efficiency, and environmental sustainability.

Electrification offers several tactical advantages, including reduced fuel dependency, enhanced stealth capabilities, and improved operational range. With militaries worldwide striving for modernization, investments in electric and hybrid military vehicles have escalated significantly.

Market Overview

Why is Military Vehicle Electrification Gaining Momentum?

The growing emphasis on sustainability and the reduction of carbon footprints has led to a shift toward electric and hybrid propulsion systems. The benefits of military vehicle electrification include:

Enhanced battlefield efficiency with reduced acoustic and thermal signatures

Lower operational costs and reduced dependency on fossil fuels

Advancements in battery technology, improving energy storage and rapid charging

Stealth capabilities that enable quiet operations and reduced detection

Download Pdf Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=55451533

Key Market Segments

The military vehicle electrification market consists of various segments, including battery types, vehicle types, and propulsion systems.

1. Based on Battery Type:

Lithium-Ion Batteries: Leading market share due to high energy density and fast charging.

Fuel Cells: Expected to grow rapidly due to longer operational range and sustainability benefits.

2. Based on Combat Vehicles:

Main Battle Tanks (MBTs): Rapid growth driven by the demand for electrified armored vehicles.

Autonomous/Semi-Autonomous Military Vehicles: Increasing investments in AI-driven warfare technologies.

3. Based on Propulsion System:

Hybrid Electric Vehicles (HEVs): Offering a balanced approach to energy efficiency and power.

Fully Electric Vehicles (EVs): Expected to register the highest CAGR of 27.3% during the forecast period.

Regional Insights

North America: Market Leader in Military Vehicle Electrification

North America is expected to dominate the market, driven by:

Strong defense budgets and government initiatives to modernize military fleets.

Leading defense contractors such as GM Defense, General Dynamics, and Oshkosh Corporation driving innovation.

Collaborations with tech firms for advancements in energy storage and propulsion systems.

Key Players in the Military Vehicle Electrification Market

Several defense companies are at the forefront of the military vehicle electrification revolution. Some of the leading players include:

1. Oshkosh Corporation (US)

Oshkosh is a dominant player in military vehicle electrification, with hybrid-electric solutions for tactical and combat vehicles. The company’s expertise in electrified combat support vehicles gives it a competitive edge.

2. GM Defense LLC (US)

GM Defense is leveraging its parent company’s expertise in electric vehicle technology to develop high-performance electric and hybrid military vehicles. The company has secured contracts to produce electrified Infantry Squad Vehicles (ISVs).

3. General Dynamics Corporation (US)

A major defense contractor, General Dynamics is actively developing hybrid-electric main battle tanks and other electrified platforms. The Abrams X MBT, revealed in 2022, features advanced hybrid-electric capabilities for stealth operations.

4. BAE Systems (UK)

BAE Systems has made significant advancements in electrified armored fighting vehicles. The company is involved in numerous projects that aim to integrate next-generation battery technologies and hybrid propulsion.

5. Leonardo S.p.A. (Italy)

Leonardo is focusing on electrification for defense logistics and armored transport vehicles. The company’s research in advanced energy storage systems is expected to drive further innovation.

6. Textron Inc. (US)

Textron is exploring electrified unmanned ground vehicles (UGVs) and tactical hybrid-electric solutions for military applications. Its focus on autonomous military platforms strengthens its market presence.

7. ST Engineering (Singapore)

ST Engineering is investing heavily in electric propulsion systems for armored vehicles. Its hybrid-electric technologies cater to both combat and support vehicles, emphasizing sustainability and performance.

8. Qinetiq (UK)

Qinetiq is a leading name in military innovation, focusing on electrified defense platforms and energy-efficient vehicle solutions. The company is known for its silent mobility technologies, enhancing stealth operations.

9. Polaris Inc. (US)

Polaris specializes in lightweight electrified military vehicles, including ATVs and tactical transport vehicles. The company’s focus on off-road and extreme-terrain applications makes it a key market player.

10. Aselsan AS (Turkey)

Aselsan is working on next-generation battery and energy storage solutions for military vehicles. Its expertise in defense electronics and hybrid systems positions it as a strong contender in the market.

11. Otokar Otomotiv ve Savunma Sanayi AS (Turkey)

Otokar is focusing on hybrid-electric military vehicles with high mobility and adaptability. Its innovations in armored transport and logistics vehicles are expected to boost its market share.

12. Krauss-Maffei Wegmann (Germany)

A leading name in main battle tank (MBT) electrification, Krauss-Maffei Wegmann is advancing hybrid drive technologies for combat vehicles.

Ask For Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=55451533

Market Challenges & Future Prospects

While the military vehicle electrification market is on an upward trajectory, challenges persist:

Power-to-Weight Ratio: The need for high-performance batteries without adding excessive weight.

Battery Durability & Lifecycle Issues: Ensuring reliability in harsh combat environments.

High Initial Costs: Significant R&D investments required for next-generation electrification technologies.

Future Trends

Hydrogen Fuel Cells: Growing adoption due to high energy density and quick refueling times.

Autonomous Military Vehicles: Increased integration of AI-driven, self-sustaining electric combat vehicles.

Modular Battery Systems: Enhancing operational flexibility with interchangeable energy modules.

The Military Vehicle Electrification Market is witnessing rapid transformation, fueled by advancements in battery technologies, hybrid propulsion, and stealth capabilities. As governments worldwide prioritize sustainability and operational efficiency, leading defense companies continue to invest in innovative electrification solutions.

The market’s future is promising, with technological breakthroughs in energy storage, electric drive systems, and AI integration paving the way for next-generation military fleets.

#military vehicle electrification#defense electrification#electric military vehicles#hybrid military vehicles#military battery technology#defense industry trends

0 notes

Text

Solar Powered Cold Storage Market Analysis, Trends, Share 2025-2033

The Reports and Insights, a leading market research company, has recently releases report titled “Solar Powered Cold Storage Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2025-2033.” The study provides a detailed analysis of the industry, including the global Solar Powered Cold Storage Market Analysis share, size, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights:

How big is the Solar Powered Cold Storage Market?

The global solar powered cold storage market was valued at US$ 5,563.4 Million in 2024 and is expected to register a CAGR of 11.4% over the forecast period and reach US$ 14,699.7 Million in 2033.

What are Solar Powered Cold Storage?

Solar-powered cold storage utilizes solar energy to power refrigeration or cold storage units. These systems convert sunlight into electricity through solar panels, which is then used to operate the refrigeration equipment. This technology is beneficial in areas with limited or unreliable access to electricity, particularly in off-grid or remote locations. Solar-powered cold storage is environmentally friendly, reducing dependence on fossil fuels and aiding in the fight against climate change. Moreover, these systems are cost-effective over time, relying on readily available solar energy for operation.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/1577

What are the growth prospects and trends in the Solar Powered Cold Storage industry?

The solar-powered cold storage market growth is driven by various factors. The solar-powered cold storage market is expanding rapidly, propelled by rising demand for sustainable, off-grid refrigeration solutions. These systems are especially favored in areas with limited access to electricity, offering a reliable and eco-friendly alternative to conventional cold storage methods. Government incentives and regulations promoting renewable energy adoption are also driving market growth. Additionally, technological advancements, including increased efficiency and affordability of solar panels and storage batteries, are further boosting the market. Hence, all these factors contribute to solar-powered cold storage market growth.

What is included in market segmentation?

The report has segmented the market into the following categories:

By Technology:

Solar Photovoltaic Systems

Solar Thermal Systems

By Storage Capacity:

Small Scale (Below 1000 cubic feet)

Medium Scale (1000 - 5000 cubic feet)

Large Scale (Above 5000 cubic feet)

By Application:

Agriculture

Food & Beverage

Pharmaceuticals

Chemicals

Others

By End-Use:

Commercial

Industrial

Agricultural

Segmentation By Region:

North America:

United States

Canada

Asia Pacific:

China

India

Japan

Australia & New Zealand

Association of Southeast Asian Nations (ASEAN)

Rest of Asia Pacific

Europe:

Germany

The U.K.

France

Spain

Italy

Russia

Poland

BENELUX (Belgium, the Netherlands, Luxembourg)

NORDIC (Norway, Sweden, Finland, Denmark)

Rest of Europe

Latin America:

Brazil

Mexico

Argentina

Rest of Latin America

The Middle East & Africa:

Saudi Arabia

United Arab Emirates

South Africa

Egypt

Israel

Rest of MEA (Middle East & Africa)

Who are the key players operating in the industry?

The report covers the major market players including:

Bright Biomethane

Ecozen Solutions

Promethean Power Systems

ColdHubs

Enexor BioEnergy

Sure Chill

Dulas Ltd.

SolCool One

Cold Chain Technologies

Eco-Fridge

SunDanzer

View Full Report: https://www.reportsandinsights.com/report/Solar Powered Cold Storage-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients globally.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd. 1820 Avenue M, Brooklyn, NY, 11230, United States Contact No: +1-(347)-748-1518 Email: [email protected] Website: https://www.reportsandinsights.com/ Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/ Follow us on twitter: https://twitter.com/ReportsandInsi1

#Solar Powered Cold Storage Market share#Solar Powered Cold Storage Market size#Solar Powered Cold Storage Market trends

0 notes

Text

Sandwich Panel Market 2025 Size, Share, Growth, Market Supply and Demand, Company Profiles, Trends, Component & Growth with Forecast

Sandwich panels have revolutionized various industries with their versatility, durability, and efficiency. These composite structures, consisting of two face sheets bonded to a lightweight core material, offer excellent thermal insulation, soundproofing, and structural integrity. The Sandwich Panel Market has been experiencing significant growth, driven by expanding construction activities, the demand for energy-efficient solutions, and advancements in material technologies.

Sandwich Panel Market Size was valued at USD 2.32 Billion in 2024. The sandwich panel industry is projected to grow from USD 2.53 Billion in 2025 to USD 5.42 Billion by 2034, exhibiting a compound annual growth rate (CAGR) of 8.9% during the forecast period (2025 - 2034).

Growing Construction Sector: One of the primary drivers propelling the sandwich panel market is the booming construction industry. With rapid urbanization and infrastructure development worldwide, there's a heightened demand for high-performance building materials that offer both sustainability and cost-effectiveness. Sandwich panels, with their ability to enhance energy efficiency and accelerate construction timelines, have become a preferred choice for residential, commercial, and industrial projects. From residential housing to warehouses, data centers to cold storage facilities, the versatility of sandwich panels is evident across diverse construction applications.

Focus on Energy Efficiency: In an era marked by increasing environmental consciousness and stringent regulations, energy efficiency has become a paramount concern for building owners and developers. Sandwich panels, with their superior thermal insulation properties, help reduce energy consumption and carbon emissions, thereby contributing to sustainability goals. The emphasis on green building practices and energy-efficient designs is driving the adoption of sandwich panels in both new constructions and retrofit projects. Governments worldwide incentivize the use of eco-friendly building materials, further bolstering the demand for sandwich panels in the construction sector.

Technological Advancements: Continuous innovation in material science and manufacturing processes has led to the development of advanced sandwich panel solutions. Manufacturers are investing in research and development to enhance the performance characteristics of sandwich panels, including fire resistance, acoustic insulation, and structural strength. The integration of cutting-edge technologies such as nanotechnology and 3D printing is opening up new possibilities for optimizing the properties of sandwich panels while reducing production costs. Additionally, the advent of smart building technologies has spurred the demand for sandwich panels embedded with sensors and IoT capabilities for real-time monitoring and control.

Market Challenges and Opportunities: Despite the favorable growth prospects, the sandwich panel market faces certain challenges, including volatile raw material prices, regulatory complexities, and competition from alternative building materials. Moreover, the COVID-19 pandemic has disrupted supply chains and construction activities, temporarily impacting market growth. However, as economies recover and construction projects resume, the demand for sandwich panels is expected to rebound swiftly. Manufacturers can leverage this opportunity by diversifying their product offerings, expanding into emerging markets, and embracing sustainable practices to gain a competitive edge.

Future Outlook: The sandwich panel market is poised for robust expansion in the coming years, driven by factors such as urbanization, infrastructure development, and the growing emphasis on sustainability. As the construction industry evolves, sandwich panels will continue to play a pivotal role in shaping the built environment, offering innovative solutions for architects, developers, and building owners. With ongoing advancements in materials, technologies, and design capabilities, the future of the sandwich panel market looks promising, promising sustainable, efficient, and aesthetically pleasing building solutions for the world's growing population.

MRFR recognizes the following Sandwich Panel Companies - DANA Group of Companies (UAE),INVESPANEL SL (Spain),Kingspan Group (Ireland),Building Component Solutions LLC (Saudi Arabia),Nucor Corporation (U.S.),Assan Panel A.S. (Turkey),Hoesch Siegerlandwerke GmbH (Germany),ArcelorMittal S.A. (U.S.),MANNI Group (Italy),Zhong Jie Group (China),Romakowski GmbH & Co. KG (Germany),Tata Steel Limited (India),NCI Building Systems Inc. (U.S.),Multicolor Steels India Pvt Ltd. (India),Sintex (India)

Related Reports

Vacuum Insulation Panel Market - https://www.marketresearchfuture.com/reports/vacuum-insulation-panels-market-2438 Polycarbonate Panels Market - https://www.marketresearchfuture.com/reports/polycarbonate-panels-market-7851

1 note

·

View note

Text

The Non-Concentrating Solar Collectors Market is expected to grow from USD 13,025 million in 2024 to USD 34,138.97 million by 2032, at a CAGR of 12.8%. The global transition towards renewable energy sources has been pivotal in shaping industries and technologies across the globe. Among the various renewable energy technologies, solar energy stands out for its scalability, reliability, and environmental benefits. Non-concentrating solar collectors, a vital segment within the solar energy domain, play a crucial role in harnessing solar energy efficiently. This article explores the non-concentrating solar collectors market, its current landscape, key drivers, and future prospects.Non-concentrating solar collectors, often referred to as flat-plate collectors or evacuated tube collectors, are devices designed to capture solar radiation and convert it into thermal energy. Unlike concentrating solar collectors, which focus sunlight onto a specific point to achieve high temperatures, non-concentrating collectors absorb sunlight over a larger surface area at lower temperatures, typically below 100°C.

Browse the full report at https://www.credenceresearch.com/report/non-concentrating-solar-collectors-market

Market Overview

The non-concentrating solar collectors market has seen steady growth over the past decade, driven by increasing global demand for clean energy solutions and advancements in solar thermal technologies. According to recent market analyses, the sector is poised for substantial expansion, with a compound annual growth rate (CAGR) projected in the range of 6% to 8% over the next five years.

Market Drivers

Rising Demand for Renewable Energy: Governments worldwide are actively promoting solar energy to reduce dependence on fossil fuels and curb greenhouse gas emissions. Non-concentrating solar collectors provide a cost-effective and energy-efficient way to achieve this.

Government Subsidies and Incentives: Financial incentives such as tax rebates, grants, and subsidies have encouraged residential and commercial users to adopt solar thermal systems, particularly in developing economies.

Technological Advancements: Innovations in materials and designs, such as improved heat transfer fluids and enhanced absorber coatings, have increased the efficiency and durability of non-concentrating solar collectors.

Growing Awareness of Environmental Sustainability: Consumers and industries are becoming more conscious of their carbon footprint, driving demand for renewable energy solutions like solar collectors.

Energy Cost Savings: Non-concentrating solar collectors reduce dependence on conventional energy sources, resulting in significant long-term cost savings for end-users.

Challenges in the Market

While the non-concentrating solar collectors market offers immense potential, it also faces challenges:

High Initial Costs: Despite long-term savings, the upfront installation costs can deter some consumers.

Seasonal Dependency: Solar thermal systems are less effective in regions with limited sunlight or during colder months.

Competition from Photovoltaics (PV): The growing adoption of solar PV systems for electricity generation has created competition for solar thermal technologies.

Future Outlook

The future of the non-concentrating solar collectors market appears promising, driven by:

Urbanization and Industrialization: Increased energy demand in urban areas and industries will propel adoption.

Integration with Smart Grids: Advanced systems that integrate solar thermal collectors with smart grids will improve energy efficiency.

Hybrid Systems: Combining non-concentrating collectors with PV systems or energy storage solutions will enhance their utility.

Key Player Analysis:

Vaillant GmbH

ABB Ltd

Viessmann Werke GmbH & Co. KG

Phoenix Solar Thermal Inc

Bosch Thermotechnik GmbH

Soltec Power Holdings S.A.

GREENoneTEC Solarindustrie GmbH

Apricus Solar Co., Ltd.

Solimpeks

SunMaxx Solar

Segments:

Based on Absorber Plates:

Copper

Aluminum

Steel Plates

Based on Application:

Residential

Commercial

Industrial

Non-Concentratin

Based on the Geography:

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/non-concentrating-solar-collectors-market

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

0 notes

Text

Building-Integrated Photovoltaics: $15.2B Market by 2034

Building-integrated Photovoltaics (BIPV) Facade Market is projected to grow significantly, expanding from $5.8 billion in 2024 to $15.2 billion by 2034, reflecting a compound annual growth rate (CAGR) of approximately 9.8%. This market focuses on the integration of photovoltaic materials into building facades, providing a dual purpose as both a functional architectural element and a renewable energy source. It encompasses a variety of innovative designs and technologies, offering solutions that not only enhance energy efficiency but also contribute to aesthetic appeal and sustainability in urban construction. Key components in the market include solar panels, advanced glazing systems, and energy management technologies, all of which play an essential role in the transition to green building practices and reducing carbon footprints.

To Request Sample Report: https://www.globalinsightservices.com/request-sample/?id=GIS10558 &utm_source=SnehaPatil&utm_medium=Article

The BIPV Facade Market is experiencing robust growth, fueled by the increasing adoption of renewable energy solutions in urban architecture. Among the various sub-segments, the glass segment leads the market, benefiting from advancements in transparent photovoltaic technologies that seamlessly integrate into modern building designs. The crystalline silicon segment also plays a significant role, appreciated for its high efficiency and cost-effectiveness. Regionally, Europe is at the forefront of market growth, driven by stringent energy regulations and a strong focus on sustainability. Germany, in particular, stands out due to its innovative architectural projects and government policies that support green building initiatives. North America follows as the second-highest performing region, with the United States leading the charge due to technological advancements and growing investments in green buildings. The overall market growth is supported by rising awareness of energy-efficient building solutions and the increasing trend toward net-zero energy construction projects.

Buy Now : https://www.globalinsightservices.com/checkout/single_user/GIS10558/?utm_source=SnehaPatil&utm_medium=Article

The market can be segmented into various categories, including types of photovoltaic technologies such as crystalline silicon, thin film, organic photovoltaics, and dye-sensitized solar cells. Products include solar panels, solar shingles, solar facade cladding, and transparent solar facades. Services provided in this market range from installation and maintenance to consulting and project management. Key technologies include Building-integrated Photovoltaics (BIPV), Building-Applied Photovoltaics (BAPV), smart building technology, and energy storage integration. Important components in these systems include solar cells, inverters, mounting systems, and monitoring systems. Applications span across residential, commercial, and industrial buildings, as well as public infrastructure. Materials used in BIPV facades include glass, polymers, metals, and ceramics, and installations can be categorized as either retrofits or new constructions. End users include architects, building owners, contractors, and energy service companies, with functionalities such as energy generation, thermal insulation, aesthetic enhancement, and noise reduction.

In 2023, the BIPV Facade Market was estimated at a volume of 320 million square meters, with projections indicating an increase to 580 million square meters by 2033. The commercial buildings segment holds the largest market share at 45%, followed by residential applications at 30% and industrial facilities at 25%. This distribution is driven by the increasing adoption of sustainable building practices and the growing demand for energy-efficient infrastructures. Key players in the market include First Solar, AGC Solar, and Onyx Solar, with First Solar focusing on thin-film technology and AGC Solar specializing in innovative glass solutions.

The competitive landscape is shaped by the strategic advancements of these companies and the regulatory framework, which includes incentives for renewable energy and stringent energy efficiency standards. As the market progresses, investment in research and development (R&D) and technological advancements will be crucial. A projected 15% increase in capital expenditure by 2033 is expected to accelerate growth. The market outlook remains positive, with significant opportunities in the commercial and residential sectors. However, challenges such as high initial costs and regulatory compliance still need to be addressed. The integration of advanced materials and smart grid solutions is expected to unlock new growth prospects.

In terms of geographical distribution, the Asia Pacific region is a key player in the BIPV Facade Market. Countries like China and Japan are leading the market due to their rapid construction activities and increasing focus on renewable energy. Government incentives and supportive policies further strengthen market growth, driven by urbanization and industrial expansion. North America is also a significant market, with the United States and Canada at the forefront, spurred by technological advancements and a strong commitment to green building standards. The region’s dedication to reducing carbon footprints and improving energy efficiency drives the market. Europe also plays a major role, with countries such as Germany and the United Kingdom experiencing substantial growth, supported by strict regulations on energy efficiency and sustainable construction practices. European Union initiatives to promote renewable energy usage also contribute to the market’s expansion.

#BIPV #BuildingIntegratedSolar #GreenBuilding #RenewableEnergy #SustainableConstruction #PhotovoltaicFacades #SolarTechnology #EnergyEfficiency #UrbanSustainability #NetZeroBuildings #SmartBuildings #EnergyGeneration #TransparentSolar #SolarPower #GreenArchitecture #CleanEnergySolutions #CarbonFootprintReduction #EcoFriendlyBuildings #RenewableEnergySolutions #SolarPanels #BIPVMarketGrowth

0 notes