#Solar Vehicle Market Challenges

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

12.7% of mobile users access Tumblr.

Text

Solar Vehicle Market: Ready To Fly on high Growth Trends

Market Research Forecast released a new market study on Global Solar Vehicle Market Research report which presents a complete assessment of the Market and contains a future trend, current growth factors, attentive opinions, facts, and industry validated market data. The research study provides estimates for Global Solar Vehicle Forecast till 2032. The Solar Vehicle Market size was valued at USD 383.4 USD Million in 2023 and is projected to reach USD 1389.90 USD Million by 2032, exhibiting a CAGR of 20.2 % during the forecast period. Key Players included in the Research Coverage of Solar Vehicle Market are: Sono Motors GmbH (Germany), Lightyear (Netherlands), VENTURI (Monaco), Nissan (Japan), Mahindra & Mahindra Limited (India), Toyota Motor Corporation (Japan), Ford Motor Company (U.S.), Volkswagen AG (Germany), Daimler AG (Germany), Tesla, Inc (U.S.) What's Trending in Market: Rising Adoption of Automation in Manufacturing to Drive Market Growth Market Growth Drivers: Increasing Demand for Forged Products in Power, Agriculture, Aerospace, and Defense to Drive Industry Expansion The Global Solar Vehicle Market segments and Market Data Break Down Vehicle Type: Passenger Vehicles and Commercial Vehicles","Battery Type: Lithium Ion, Lead Acid, and Others","Solar Panel: Monocrystalline and Polycrystalline GET FREE SAMPLE PDF ON Solar Vehicle MARKET To comprehend Global Solar Vehicle market dynamics in the world mainly, the worldwide Solar Vehicle market is analyzed across major global regions. MR Forecast also provides customized specific regional and country-level reports for the following areas.

• North America: United States, Canada, and Mexico. • South & Central America: Argentina, Chile, Colombia and Brazil. • Middle East & Africa: Saudi Arabia, United Arab Emirates, Israel, Turkey, Egypt and South Africa. • Europe: United Kingdom, France, Italy, Germany, Spain, Belgium, Netherlands and Russia. • Asia-Pacific: India, China, Japan, South Korea, Indonesia, Malaysia, Singapore, and Australia.

Extracts from Table of Contents Solar Vehicle Market Research Report Chapter 1 Solar Vehicle Market Overview Chapter 2 Global Economic Impact on Industry Chapter 3 Global Market Competition by Manufacturers Chapter 4 Global Revenue (Value, Volume*) by Region Chapter 5 Global Supplies (Production), Consumption, Export, Import by Regions Chapter 6 Global Revenue (Value, Volume*), Price* Trend by Type Chapter 7 Global Market Analysis by Application ………………….continued More Reports:

https://marketresearchforecast.com/reports/car-rental-leasing-market-3007 For More Information Please Connect MR Forecast Contact US: Craig Francis (PR & Marketing Manager) Market Research Forecast Unit No. 429, Parsonage Road Edison, NJ New Jersey USA – 08837 Phone: (+1 201 565 3262, +44 161 818 8166) [email protected]

#Global Solar Vehicle Market#Solar Vehicle Market Demand#Solar Vehicle Market Trends#Solar Vehicle Market Analysis#Solar Vehicle Market Growth#Solar Vehicle Market Share#Solar Vehicle Market Forecast#Solar Vehicle Market Challenges

0 notes

Text

Excerpt from this story from Grist:

At a laboratory in Newark, New Jersey, a gray liquid swirls vigorously inside a reactor the size of a small watermelon. Here, scientists with the mining technology startup Still Bright are using a rare metal, vanadium, to extract a common one, copper, from ores that are too difficult or costly for the mining industry to process today.

If the promising results Still Bright is seeing in beakers and bottles can be replicated at much larger scales, it could unlock vast copper resources for the energy transition.

till Bright isn’t the only company seeking to revolutionize copper production. A handful of startups with similar goals have announced partnerships with major mining firms and scooped up tens of millions of dollars of investment. These companies claim their technology can help meet humanity’s surging appetite for the metal, while driving down the industry’s environmental footprint.

“We’re facing unprecedented demand for copper, and that’s really tied to the electrification of everything,” Still Bright chief of staff Carter Schmitt told Grist.

The world cannot reach its climate goals without copper, which plays a central role in the technologies needed to decarbonize. Copper wiring is at the core of the world’s electricity networks, which will have to expand enormously to bring more renewable energy online. Wind turbines, solar panels, electric vehicles, and lithium-ion batteries all rely on the mineral, too. As the market for these technologies grows, the clean energy sector’s demand for the 29th element is expected to nearly triple by 2040.

At the same time, copper miners are exhausting their best-quality reserves. Copper that is economical to mine is found in rocks known as ores, and grades of the ores that miners are exploiting — the concentration of copper contained in them — have declined steadily over the past 20 years. Meanwhile, easy-to-process minerals near the surface are giving way to more challenging ones deeper down. And the current standard procedure for extracting the metal from the majority of ores results in a lot of pollution.

7 notes

·

View notes

Text

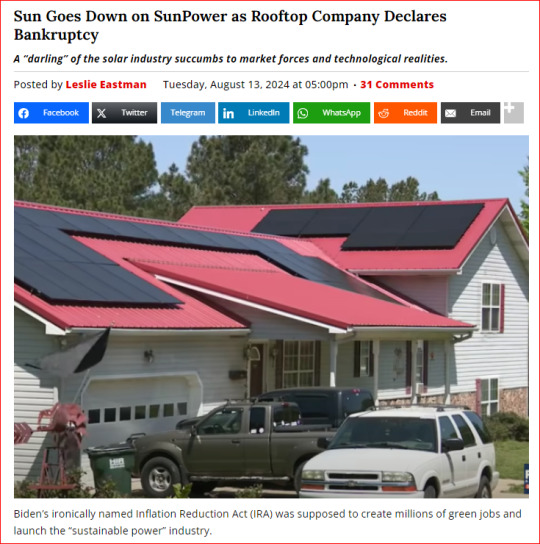

Biden’s ironically named Inflation Reduction Act (IRA) was supposed to create millions of green jobs and launch the “sustainable power” industry.

Subsidies flowed to support electric vehicles, wind farms, and solar energy. We have been covering the slowdown in the EV market, and residents of the East Coast are questioning all the promises made by the wind energy companies after the Vineyard Wind blade failure.

Now, it’s time to turn our attention to solar power. SunPower, the company that provides solar panels to many Californian homes in the sunny Coachella Valley area, filed for bankruptcy this week.

It is the latest development in a saga that has seen the company facing numerous serious and seemingly escalating challenges over the past several months, including allegations about executives’ misconduct related to the company’s financial statements and a recent decision that SunPower would no longer offer new solar leases. Days after the latter announcement, Coachella Valley-based Renova Energy, which markets and installs SunPower systems, said it was ending its partnership with SunPower and temporarily pausing operations after not receiving required payments from SunPower. SunPower’s executive chairman wrote in a letter posted on the company’s website on Monday that the company had reached an agreement to sell certain divisions of its business and suggested it was looking for one or more buyers to take on the rest, including the company’s responsibilities to maintain solar systems it has previously sold or leased.

It is important to note that SunPower was the industry’s “darling” to understand the magnitude of this development.

Founded in 1985 by a Stanford professor, SunPower was, for the past two decades, a darling of the solar industry. The company helped build America’s biggest solar plant, called Solar Star and located near Rosamond, California, and has installed solar panels on more than 100,000 homes. The company’s stock price has fluctuated dramatically, peaking during the solar stock frenzy of late 2007. As recently as January 2021, SunPower’s valuation momentarily reached $10 billion, buoyed by the expansion of its residential solar panels program. But since then, the company’s value has cratered — and this year, its situation became particularly dire.

It is also important to note that earlier this month, the bankruptcy of a solar-powered company in South Florida created an array of problems on the South Coast of California. Subcontractors are scrambling to find ways to guarantee payment for work on homes with equipment from the firm.

Meanwhile, homeowners are regretting their misplaced trust in eco-activists and city officials.

The business — Electriq Power Inc. — was putting solar panels and batteries on Santa Barbara rooftops at no expense to homeowners and with the blessings of the cities of Santa Barbara, Goleta, and Carpinteria. But then Electriq filed Chapter 7 on May 3, freezing all its operations. This prompted one of its subcontractors, Axiom 360 of Grover Beach, to place mechanics liens on homes for which it had yet to be paid. This preserves Axiom’s options for full payment of its installation work and is not unusual among contractors. But for homeowners who didn’t expect any financial outlay, it came as a shock, especially as the recording notice lists foreclosure in 90 days among the penalties. “You’re helping the environment. You’re not paying high rates to Southern California Edison,” said homeowner Randy Freed, explaining why he signed on to Electriq’s PoweredUp Goleta program. He was pleased with the savings in the solar array and storage batteries, but then he received the mechanics lien in June. The possibility of foreclosure was unanticipated, Freed said, and he’d relied on the cities’ endorsements. “It’s a great program; we’ve checked them out,” he recalled the cities saying on a postcard he received.

Hot Air's Beege Welborne takes an in-depth look at the cascade of warnings that indicate SunPower and the residential solar market are in serious trouble. She also hits on a point that is true for all green energy schemes: Today’s technology cannot keep up with the promises being made about tomorrow.

The technology side still hasn’t ironed itself out and may never with as saturated as the market is. With interest rates as high as they are and home prices through the roof, no one wants to pay a fortune for something that’s not rock solid. …That “sustainable” growth is only possible once all the artificial supports are knocked away and the technology proves viable and worth the cost once and for all.

Of course, the solar industry isn’t helped by the fact that the cost savings for customers aren’t quite as lavish as originally promised.

12 notes

·

View notes

Text

‘Financing represents the ultimate chokepoint,’ Christophers writes, ‘the point at which renewables development most often becomes permanently blocked.’ Investors aren’t choosing between ‘clean’ and ‘dirty’ electricity generation, but judging opportunities across a wide range of asset classes. Capitalists’ sole concern, as Marx observed, is how to turn money into more money, and it’s not clear that renewables are a very good vehicle for doing this, regardless of how cheap they are to run.

The problem, from the perspective of investors, is ‘bankability’. Investors want as much certainty as possible regarding future returns on their investments, or else they require a hefty premium for accepting additional uncertainty. The challenge for the renewables sector is how to persuade investors that they can make reliably high returns in a market with highly volatile prices, low barriers to entry and nothing to stabilise revenues. The very policies that were introduced to bring electricity costs down – marketisation and competition – have made the financial sector wary. Whenever renewables appear to be doing well, new providers rush in, driving down prices, and therefore profits, until investors get cold feet all over again.

What investors crave is price stability, or predictability at least. Risk is one thing, but fundamental uncertainty is another. Industries characterised by a high degree of concentration, longstanding monopoly power and government support are far easier to incorporate into financial models, because there are fewer unknowns. Judged in terms of decarbonisation, the most successful policies reviewed in The Price Is Wrong are not those which reduce the price of electricity, which would be in the interest of consumers, but those which stabilise it for the benefit of investors. Meanwhile, the extraction and burning of fossil fuels remains a more dependable way of making the kind of returns that Wall Street and the City have come to expect as their due. This is an industry with more dominant players, much higher barriers to entry, and which was largely established (and financed) long before the vogue for marketisation took hold.

Despite the exuberance over the falling costs of solar and wind power, Christophers doubts ‘whether a single example of a substantive and truly zero-support’ renewables facility ‘actually exists, anywhere in the world’. What’s especially galling is that, to the extent renewable electricity remains hooked on subsidies, this isn’t money that is ending up in savings for consumers, but in the profits of developers and the portfolios of asset managers. Paradoxically, the ideology that promoted free markets and a culture of enterprise (against conglomeration and monopoly) has enforced this sector’s reliance on the state. The lesson Christophers draws is that electricity ‘was and is not a suitable object for marketisation and profit generation in the first place’. Ecologically speaking, neoliberalism could scarcely have come at a worse time.

What can be done? It is clearly no good hoping that electricity markets will drive the energy transition, when it’s financial markets that are calling the shots. The option that has come to the fore in recent years, led by the Biden administration, is the one euphemistically called ‘de-risking’, which in practice means topping up and guaranteeing the returns that investors have come to expect using tax credits and other subsidies. The Inflation Reduction Act, signed by Biden in the summer of 2022, promises a giant $369 billion of these incentives over a ten-year period. This at least faces up to the fact that much of the power to shape the future is in the hands of asset managers and banks, and it is their calculations (and not those of consumers) that will decide whether or not the planet burns. There is no economic reason why a 15 per cent return on investment should be considered ‘normal’, and there is nothing objectively bad about a project that pays 6 per cent instead. The problem, as Christophers makes plain, is that investors get to choose which of these two numbers they prefer, and no government is likely to force BlackRock to make less money anytime soon. "

#feministdragon#feministdragon reinventing our economy#radical feminism#radfem#women's liberation#human rights#women's rights#women's rights are human rights#radfems do interact#radical feminists do interact#radical feminist safe

8 notes

·

View notes

Text

Hydrogen Is the Future—or a Complete Mirage!

The green-hydrogen industry is a case study in the potential—for better and worse—of our new economic era.

— July 14, 2023 | Foreign Policy | By Adam Tooze

An employee of Air Liquide in front of an electrolyzer at the company's future hydrogen production facility of renewable hydrogen in Oberhausen, Germany, on May 2, 2023. Ina Fassbender/ AFP Via Getty Images

With the vast majority of the world’s governments committed to decarbonizing their economies in the next two generations, we are embarked on a voyage into the unknown. What was once an argument over carbon pricing and emissions trading has turned into an industrial policy race. Along the way there will be resistance and denial. There will also be breakthroughs and unexpected wins. The cost of solar and wind power has fallen spectacularly in the last 20 years. Battery-powered electric vehicles (EVs) have moved from fantasy to ubiquitous reality.

But alongside outright opposition and clear wins, we will also have to contend with situations that are murkier, with wishful thinking and motivated reasoning. As we search for technical solutions to the puzzle of decarbonization, we must beware the mirages of the energy transition.

On a desert trek a mirage can be fatal. Walk too far in the wrong direction, and there may be no way back. You succumb to exhaustion before you can find real water. On the other hand, if you don’t head toward what looks like an oasis, you cannot be sure that you will find another one in time.

Right now, we face a similar dilemma, a dilemma of huge proportions not with regard to H2O but one of its components, H2—hydrogen. Is hydrogen a key part of the world’s energy future or a dangerous fata morgana? It is a question on which tens of trillions of dollars in investment may end up hinging. And scale matters.

For decades, economists warned of the dangers of trying through industrial policy to pick winners. The risk is not just that you might fail, but that in doing so you incur costs. You commit real resources that foreclose other options. The lesson was once that we should leave it to the market. But that was a recipe for a less urgent time. The climate crisis gives us no time. We cannot avoid the challenge of choosing our energy future. As Chuck Sabel and David Victor argue in their important new book Fixing the Climate: Strategies for an Uncertain World, it is through local partnership and experimentation that we are most likely to find answers to these technical dilemmas. But, as the case of hydrogen demonstrates, we must beware the efforts of powerful vested interests to use radical technological visions to channel us toward what are in fact conservative and ruinously expensive options.

A green hydrogen plant built by Spanish company Iberdrola in Puertollano, Spain, on April 18, 2023. Valentine Bontemps/AFP Via Getty Images

In the energy future there are certain elements that seem clear. Electricity is going to play a much bigger role than ever before in our energy mix. But some very knotty problems remain. Can electricity suffice? How do you unleash the chemical reactions necessary to produce essential building blocks of modern life like fertilizer and cement without employing hydrocarbons and applying great heat? To smelt the 1.8 billion tons of steel we use every year, you need temperatures of almost 2,000 degrees Celsius. Can we get there without combustion? How do you power aircraft flying thousands of miles, tens of thousands of feet in the air? How do you propel giant container ships around the world? Electric motors and batteries can hardly suffice.

Hydrogen recommends itself as a solution because it burns very hot. And when it does, it releases only water. We know how to make hydrogen by running electric current through water. And we know how to generate electricity cleanly. Green hydrogen thus seems easily within reach. Alternatively, if hydrogen is manufactured using natural gas rather than electrolysis, the industrial facilities can be adapted to allow immediate, at-source CO2 capture. This kind of hydrogen is known as blue hydrogen.

Following this engineering logic, H2 is presented by its advocates as a Swiss army knife of the energy transition, a versatile adjunct to the basic strategy of electrifying everything. The question is whether H2 solutions, though they may be technically viable, make any sense from the point of view of the broader strategy of energy transition, or whether they might in fact be an expensive wrong turn.

Using hydrogen as an energy store is hugely inefficient. With current technology producing hydrogen from water by way of electrolysis consumes vastly more energy than will be stored and ultimately released by burning the hydrogen. Why not use the same electricity to generate the heat or drive a motor directly? The necessary electrolysis equipment is expensive. And though hydrogen may burn cleanly, as a fuel it is inconvenient because of its corrosive properties, its low energy per unit of volume, and its tendency to explode. Storing and moving hydrogen around will require huge investment in shipping facilities, pipelines, filling stations, or facilities to convert hydrogen into the more stable form of ammonia.

The kind of schemes pushed by hydrogen’s lobbyists foresee annual consumption rising by 2050 to more than 600 million tons per annum, compared to 100 million tons today. This would consume a huge share of green electricity production. In a scenario favored by the Hydrogen Council, of the United States’ 2,900 gigawatts of renewable energy production, 650 gigawatts would be consumed by hydrogen electrolysis. That is almost three times the total capacity of renewable power installed today.

The costs will be gigantic. The cost for a hydrogen build-out over coming decades could run into the tens of trillions of dollars. Added to which, to work as a system, the investment in hydrogen production, transport, and consumption will have to be undertaken simultaneously.

Little wonder, perhaps, that though the vision of the “hydrogen economy” as an integrated economic and technical system has been around for half a century, we have precious little actual experience with hydrogen fuel. Indeed, there is an entire cottage industry of hydrogen skeptics. The most vocal of these is Michael Liebreich, whose consultancy has popularized the so-called hydrogen ladder, designed to highlight how unrealistic many of them are. If one follows the Liebreich analysis, the vast majority of proposed hydrogen uses in transport and industrial heating are, in fact, unrealistic due to their sheer inefficiency. In each case there is an obvious alternative, most of them including the direct application of electricity.

Technicians work on the construction of a hydrogen bus at a plant in Albi, France, on March 4, 2021. Georges Gobet/AFP Via Getty Images

Nevertheless, in the last six years a huge coalition of national governments and industrial interests has assembled around the promise of a hydrogen-based economy.

The Hydrogen Council boasts corporate sponsors ranging from Airbus and Aramco to BMW, Daimler Truck, Honda, Toyota and Hyundai, Siemens, Shell, and Microsoft. The national governments of Japan, South Korea, the EU, the U.K., the U.S., and China all have hydrogen strategies. There are new project announcements regularly. Experimental shipments of ammonia have docked in Japan. The EU is planning an elaborate network of pipelines, known as the hydrogen backbone. All told, the Hydrogen Council counts $320 billion in hydrogen projects announced around the world.

Given the fact that many new uses of hydrogen are untested, and given the skepticism among many influential energy economists and engineers, it is reasonable to ask what motivates this wave of commitments to the hydrogen vision.

In technological terms, hydrogen may represent a shimmering image of possibility on a distant horizon, but in political economy terms, it has a more immediate role. It is a route through which existing fossil fuel interests can imagine a place for themselves in the new energy future. The presence of oil majors and energy companies in the ranks of the Hydrogen Council is not coincidental. Hydrogen enables natural gas suppliers to imagine that they can transition their facilities to green fuels. Makers of combustion engines and gas turbines can conceive of burning hydrogen instead. Storing hydrogen or ammonia like gas or oil promises a solution to the issues of intermittency in renewable power generation and may extend the life of gas turbine power stations. For governments around the world, a more familiar technology than one largely based on solar panels, windmills, and batteries is a way of calming nerves about the transformation they have notionally signed up for.

Looking at several key geographies in which hydrogen projects are currently being discussed offers a compound psychological portrait of the common moment of global uncertainty.

A worker at the Fukushima Hydrogen Energy Research Field, a test facility that produces hydrogen from renewable energy, in Fukushima, Japan, on Feb. 15, 2023. Richard A. Brooks/AFP Via Getty Images

The first country to formulate a national hydrogen strategy was Japan. Japan has long pioneered exotic energy solutions. Since undersea pipelines to Japan are impractical, it was Japanese demand that gave life to the seaborne market for liquefied natural gas (LNG). What motivated the hydrogen turn in 2017 was a combination of post-Fukushima shock, perennial anxiety about energy security, and a long-standing commitment to hydrogen by key Japanese car manufacturers. Though Toyota, the world’s no. 1 car producer, pioneered the hybrid in the form of the ubiquitous Prius, it has been slow to commit to full electric. The same is true for the other East Asian car producers—Honda, Nissan, and South Korea’s Hyundai. In the face of fierce competition from cheap Chinese electric vehicles, they embrace a government commitment to hydrogen, which in the view of many experts concentrates on precisely the wrong areas i.e. transport and electricity generation, rather than industrial applications.

The prospect of a substantial East Asian import demand for hydrogen encourages the economists at the Hydrogen Council to imagine a global trade in hydrogen that essentially mirrors the existing oil and gas markets. These have historically centered on flows of hydrocarbons from key producing regions such as North Africa, the Middle East, and North America to importers in Europe and Asia. Fracked natural gas converted into LNG is following this same route. And it seems possible that hydrogen and ammonia derived from hydrogen may do the same.

CF Industries, the United States’ largest producer of ammonia, has finalized a deal to ship blue ammonia to Japan’s largest power utility for use alongside oil and gas in power generation. The CO2 storage that makes the ammonia blue rather than gray has been contracted between CF Industries and U.S. oil giant Exxon. A highly defensive strategy in Japan thus serves to provide a market for a conservative vision of the energy transition in the United Sates as well. Meanwhile, Saudi Aramco, by far the world’s largest oil company, is touting shipments of blue ammonia, which it hopes to deliver to Japan or East Asia. Though the cost in terms of energy content is the equivalent of around $250 per barrel of oil, Aramco hopes to ship 11 million tons of blue ammonia to world markets by 2030.

To get through the current gas crisis, EU nations have concluded LNG deals with both the Gulf states and the United States. Beyond LNG, it is also fully committed to the hydrogen bandwagon. And again, this follows a defensive logic. The aim is to use green or blue hydrogen or ammonia to find a new niche for European heavy industry, which is otherwise at risk of being entirely knocked out of world markets by high energy prices and Europe’s carbon levy.

The European steel industry today accounts for less than ten percent of global production. It is a leader in green innovation. And the world will need technological first-movers to shake up the fossil-fuel dependent incumbents, notably in China. But whether this justifies Europe’s enormous commitment to hydrogen is another question. It seems motivated more by the desire to hold up the process of deindustrialization and worries about working-class voters drifting into the arms of populists, than by a forward looking strategic calculus.

In the Netherlands, regions that have hitherto served as hubs for global natural gas trading are now competing for designation as Europe’s “hydrogen valley.” In June, German Chancellor Olaf Scholz and Italian Prime Minister Giorgia Meloni inked the contract on the SoutH2 Corridor, a pipeline that will carry H2 up the Italian peninsula to Austria and southern Germany. Meanwhile, France has pushed Spain into agreeing to a subsea hydrogen connection rather than a natural gas pipeline over the Pyrenees. Spain and Portugal have ample LNG terminal capacity. But Spain’s solar and wind potential also make it Europe’s natural site for green hydrogen production and a “green hydrogen” pipe, regardless of its eventual uses, in the words of one commentator looks “less pharaonic and fossil-filled” than the original natural gas proposal.

A hydrogen-powered train is refilled by a mobile hydrogen filling station at the Siemens test site in Wegberg, Germany, on Sept. 9, 2022. Bernd/AFP Via Getty Images

How much hydrogen will actually be produced in Europe remains an open question. Proximity to the point of consumption and the low capital costs of investment in Europe speak in favor of local production. But one of the reasons that hydrogen projects appeal to European strategists is that they offer a new vision of European-African cooperation. Given demographic trends and migration pressure, Europe desperately needs to believe that it has a promising African strategy. Africa’s potential for renewable electricity generation is spectacular. Germany has recently entered into a hydrogen partnership with Namibia. But this raises new questions.

First and foremost, where will a largely desert country source the water for electrolysis? Secondly, will Namibia export only hydrogen, ammonia, or some of the industrial products made with the green inputs? It would be advantageous for Namibia to develop a heavy-chemicals and iron-smelting industry. But from Germany’s point of view, that might well defeat the object, which is precisely to provide affordable green energy with which to keep industrial jobs in Europe.

A variety of conservative motives thus converge in the hydrogen coalition. Most explicit of all is the case of post-Brexit Britain. Once a leader in the exit from coal, enabled by a “dash for gas” and offshore wind, the U.K. has recently hit an impasse. Hard-to-abate sectors like household heating, which in the U.K. is heavily dependent on natural gas, require massive investments in electrification, notably in heat pumps. These are expensive. In the United Kingdom, the beleaguered Tory government, which has presided over a decade of stagnating real incomes, is considering as an alternative the widespread introduction of hydrogen for domestic heating. Among energy experts this idea is widely regarded as an impractical boondoggle for the gas industry that defers the eventual and inevitable electrification at the expense of prolonged household emissions. But from the point of view of politics, it has the attraction that it costs relatively less per household to replace natural gas with hydrogen.

Employees work on the assembly line of fuel cell electric vehicles powered by hydrogen at a factory in Qingdao, Shandong province, China, on March 29, 2022. VCG Via Getty Images

As this brief tour suggests, there is every reason to fear that tens of billions of dollars in subsidies, vast amounts of political capital, and precious time are being invested in “green” energy investments, the main attraction of which is that they minimize change and perpetuate as far as possible the existing patterns of the hydrocarbon energy system. This is not greenwashing in the simple sense of rebadging or mislabeling. If carried through, it is far more substantial than that. It will build ships and put pipes in the ground. It will consume huge amounts of desperately scarce green electricity. And this faces us with a dilemma.

In confronting the challenge of the energy transition, we need a bias for action. We need to experiment. There is every reason to trust in learning-curve effects. Electrolyzers, for instance, will get more affordable, reducing the costs of hydrogen production. At certain times and in certain places, green power may well become so abundant that pouring it into electrolysis makes sense. And even if many hydrogen projects do not succeed, that may be a risk worth taking. We will likely learn new techniques in the process. In facing the uncertainties of the energy transition, we need to cultivate a tolerance for failure. Furthermore, even if hydrogen is a prime example of corporate log-rolling, we should presumably welcome the broadening of the green coalition to include powerful fossil fuel interests.

The real and inescapable tradeoff arises when we commit scarce resources—both real and political—to the hydrogen dream. The limits of public tolerance for the costs of the energy transition are already abundantly apparent, in Asia and Europe as well as in the United States. Pumping money into subsidies that generate huge economies of scale and cost reductions is one thing. Wasting money on lame-duck projects with little prospect of success is quite another. What is at stake is ultimately the legitimacy of the energy transition as such.

In the end, there is no patented method distinguishing self-serving hype from real opportunity. There is no alternative but to subject competing claims to intense public, scientific, and technical scrutiny. And if the ship has already sailed and subsidies are already on the table, then retrospective cost-benefit assessment is called for.

Ideally, the approach should be piecemeal and stepwise, and in this regard the crucial thing to note about hydrogen is that to regard it as a futuristic fantasy is itself misguided. We already live in a hydrogen-based world. Two key sectors of modern industry could not operate without it. Oil refining relies on hydrogen, as does the production of fertilizer by the Haber-Bosch process on which we depend for roughly half of our food production. These two sectors generate the bulk of the demand for the masses of hydrogen we currently consume.

We may not need 600 million, 500 million, or even 300 million tons of green and blue hydrogen by 2050. But we currently use about 100 million, and of that total, barely 1 million is clean. It is around that core that hydrogen experimentation should be concentrated, in places where an infrastructure already exists. This is challenging because transporting hydrogen is expensive, and many of the current points of use of hydrogen, notably in Europe, are not awash in cheap green power. But there are two places where the conditions for experimentation within the existing hydrogen economy seem most propitious.

One is China, and specifically northern China and Inner Mongolia, where China currently concentrates a large part of its immense production of fertilizer, cement, and much of its steel industry. China is leading the world in the installation of solar and wind power and is pioneering ultra-high-voltage transmission. Unlike Japan and South Korea, China has shown no particular enthusiasm for hydrogen. It is placing the biggest bet in the world on the more direct route to electrification by way of renewable generation and batteries. But China is already the largest and lowest-cost producer of electrolysis equipment. In 2022, China launched a modestly proportioned hydrogen strategy. In cooperation with the United Nations it has initiated an experiment with green fertilizer production, and who would bet against its chances of establishing a large-scale hydrogen energy system?

The other key player is the United States. After years of delay, the U.S. lags far behind in photovoltaics batteries, and offshore wind. But in hydrogen, and specifically in the adjoining states of Texas and Louisiana on the Gulf of Mexico, it has obvious advantages over any other location in the West. The United States is home to a giant petrochemicals complex. It is the only Western economy that can compete with India and China in fertilizer production. In Texas, there are actually more than 2500 kilometers of hardened hydrogen pipelines. And insofar as players like Exxon have a green energy strategy, it is carbon sequestration, which will be the technology needed for blue hydrogen production.

It is not by accident that America’s signature climate legislation, the Inflation Reduction Act, targeted its most generous subsidies—the most generous ever offered for green energy in the United States—on hydrogen production. The hydrogen lobby is hard at work, and it has turned Texas into the lowest-cost site for H2 production in the Western world. It is not a model one would want to see emulated anywhere else, but it may serve as a technology incubator that charts what is viable and what is not.

There is very good reason to suspect the motives of every player in the energy transition. Distinguishing true innovation from self-serving conservatism is going to be a key challenge in the new era in which we have to pick winners. We need to develop a culture of vigilance. But there are also good reasons to expect certain key features of the new to grow out of the old. Innovation is miraculous but it rarely falls like mana from heaven. As Sabel and Victor argue in their book, it grows from within expert technical communities with powerful vested interests in change. The petrochemical complex of the Gulf of Mexico may seem an unlikely venue for the birth of a green new future, but it is only logical that the test of whether the hydrogen economy is a real possibility will be run at the heart of the existing hydrocarbon economy.

— Adam Tooze is a Columnist at Foreign Policy and a History Professor and the Director of the European Institute at Columbia University. He is the Author of Chartbook, a newsletter on Rconomics, Geopolitics, and History.

#Hydrogen#Battery-Powered Electric Vehicles (EVs)#Chuck Sabel | David Victor#Iberdrola Puertollano Spain 🇪🇸#Green Hydrogen#Hydrogen Council of the United States 🇺🇸#Hydrogen Economy#Airbus | Aramco | BMW | Daimler Truck | Honda | Toyota | Hyundai | Siemens | Shell | Microsoft#Japan 🇯🇵 | South Korea 🇰🇷 | EU 🇪🇺 | UK 🇬🇧 | US 🇺🇸 | China 🇨🇳#Portugal 🇵🇹 | Germany 🇩🇪 | Namibia 🇳🇦#European-African Cooperation

2 notes

·

View notes

Text

With the vast majority of the world’s governments committed to decarbonizing their economies in the next two generations, we are embarked on a voyage into the unknown. What was once an argument over carbon pricing and emissions trading has turned into an industrial policy race. Along the way there will be resistance and denial. There will also be breakthroughs and unexpected wins. The cost of solar and wind power has fallen spectacularly in the last 20 years. Battery-powered electric vehicles (EVs) have moved from fantasy to ubiquitous reality.

But alongside outright opposition and clear wins, we will also have to contend with situations that are murkier, with wishful thinking and motivated reasoning. As we search for technical solutions to the puzzle of decarbonization, we must beware the mirages of the energy transition.

On a desert trek a mirage can be fatal. Walk too far in the wrong direction, and there may be no way back. You succumb to exhaustion before you can find real water. On the other hand, if you don’t head toward what looks like an oasis, you cannot be sure that you will find another one in time.

Right now, we face a similar dilemma, a dilemma of huge proportions not with regard to H2O but one of its components, H2—hydrogen. Is hydrogen a key part of the world’s energy future or a dangerous fata morgana? It is a question on which tens of trillions of dollars in investment may end up hinging. And scale matters.

For decades, economists warned of the dangers of trying through industrial policy to pick winners. The risk is not just that you might fail, but that in doing so you incur costs. You commit real resources that foreclose other options. The lesson was once that we should leave it to the market. But that was a recipe for a less urgent time. The climate crisis gives us no time. We cannot avoid the challenge of choosing our energy future. As Chuck Sabel and David Victor argue in their important new book Fixing the Climate: Strategies for an Uncertain World, it is through local partnership and experimentation that we are most likely to find answers to these technical dilemmas. But, as the case of hydrogen demonstrates, we must beware the efforts of powerful vested interests to use radical technological visions to channel us towards what are in fact conservative and ruinously expensive options.

In the energy future there are certain elements that seem clear. Electricity is going to play a much bigger role than ever before in our energy mix. But some very knotty problems remain. Can electricity suffice? How do you unleash the chemical reactions necessary to produce essential building blocks of modern life like fertilizer and cement without employing hydrocarbons and applying great heat? To smelt the 1.8 billion tons of steel we use every year, you need temperatures of almost 2,000 degrees Celsius. Can we get there without combustion? How do you power aircraft flying thousands of miles, tens of thousands of feet in the air? How do you propel giant container ships around the world? Electric motors and batteries can hardly suffice.

Hydrogen recommends itself as a solution because it burns very hot. And when it does, it releases only water. We know how to make hydrogen by running electric current through water. And we know how to generate electricity cleanly. Green hydrogen thus seems easily within reach. Alternatively, if hydrogen is manufactured using natural gas rather than electrolysis, the industrial facilities can be adapted to allow immediate, at-source CO2 capture. This kind of hydrogen is known as blue hydrogen.

Following this engineering logic, H2 is presented by its advocates as a Swiss army knife of the energy transition, a versatile adjunct to the basic strategy of electrifying everything. The question is whether H2 solutions, though they may be technically viable, make any sense from the point of view of the broader strategy of energy transition, or whether they might in fact be an expensive wrong turn.

Using hydrogen as an energy store is hugely inefficient. With current technology producing hydrogen from water by way of electrolysis consumes vastly more energy than will be stored and ultimately released by burning the hydrogen. Why not use the same electricity to generate the heat or drive a motor directly? The necessary electrolysis equipment is expensive. And though hydrogen may burn cleanly, as a fuel it is inconvenient because of its corrosive properties, its low energy per unit of volume, and its tendency to explode. Storing and moving hydrogen around will require huge investment in shipping facilities, pipelines, filling stations, or facilities to convert hydrogen into the more stable form of ammonia.

The kind of schemes pushed by hydrogen’s lobbyists foresee annual consumption rising by 2050 to more than 600 million tons per annum, compared to 100 million tons today. This would consume a huge share of green electricity production. In a scenario favored by the Hydrogen Council, of the United States’ 2,900 gigawatts of renewable energy production, 650 gigawatts would be consumed by hydrogen electrolysis. That is almost three times the total capacity of renewable power installed today.

The costs will be gigantic. The cost for a hydrogen build-out over coming decades could run into the tens of trillions of dollars. Added to which, to work as a system, the investment in hydrogen production, transport, and consumption will have to be undertaken simultaneously.

Little wonder, perhaps, that though the vision of the “hydrogen economy” as an integrated economic and technical system has been around for half a century, we have precious little actual experience with hydrogen fuel. Indeed, there is an entire cottage industry of hydrogen skeptics. The most vocal of these is Michael Liebreich, whose consultancy has popularized the so-called hydrogen ladder, designed to highlight how unrealistic many of them are. If one follows the Liebreich analysis, the vast majority of proposed hydrogen uses in transport and industrial heating are, in fact, unrealistic due to their sheer inefficiency. In each case there is an obvious alternative, most of them including the direct application of electricity.

Nevertheless, in the last six years a huge coalition of national governments and industrial interests has assembled around the promise of a hydrogen-based economy.

The Hydrogen Council boasts corporate sponsors ranging from Airbus and Aramco to BMW, Daimler Truck, Honda, Toyota and Hyundai, Siemens, Shell, and Microsoft. The national governments of Japan, South Korea, the EU, the U.K., the U.S., and China all have hydrogen strategies. There are new project announcements regularly. Experimental shipments of ammonia have docked in Japan. The EU is planning an elaborate network of pipelines, known as the hydrogen backbone. All told, the Hydrogen Council counts $320 billion in hydrogen projects announced around the world.

Given the fact that many new uses of hydrogen are untested, and given the skepticism among many influential energy economists and engineers, it is reasonable to ask what motivates this wave of commitments to the hydrogen vision.

In technological terms, hydrogen may represent a shimmering image of possibility on a distant horizon, but in political economy terms, it has a more immediate role. It is a route through which existing fossil fuel interests can imagine a place for themselves in the new energy future. The presence of oil majors and energy companies in the ranks of the Hydrogen Council is not coincidental. Hydrogen enables natural gas suppliers to imagine that they can transition their facilities to green fuels. Makers of combustion engines and gas turbines can conceive of burning hydrogen instead. Storing hydrogen or ammonia like gas or oil promises a solution to the issues of intermittency in renewable power generation and may extend the life of gas turbine power stations. For governments around the world, a more familiar technology than one largely based on solar panels, windmills, and batteries is a way of calming nerves about the transformation they have notionally signed up for.

Looking at several key geographies in which hydrogen projects are currently being discussed offers a compound psychological portrait of the common moment of global uncertainty.

The first country to formulate a national hydrogen strategy was Japan. Japan has long pioneered exotic energy solutions. Since undersea pipelines to Japan are impractical, it was Japanese demand that gave life to the seaborne market for liquefied natural gas (LNG). What motivated the hydrogen turn in 2017 was a combination of post-Fukushima shock, perennial anxiety about energy security, and a long-standing commitment to hydrogen by key Japanese car manufacturers. Though Toyota, the world’s no. 1 car producer, pioneered the hybrid in the form of the ubiquitous Prius, it has been slow to commit to full electric. The same is true for the other East Asian car producers—Honda, Nissan, and South Korea’s Hyundai. In the face of fierce competition from cheap Chinese electric vehicles, they embrace a government commitment to hydrogen, which in the view of many experts concentrates on precisely the wrong areas i.e. transport and electricity generation, rather than industrial applications.

The prospect of a substantial East Asian import demand for hydrogen encourages the economists at the Hydrogen Council to imagine a global trade in hydrogen that essentially mirrors the existing oil and gas markets. These have historically centered on flows of hydrocarbons from key producing regions such as North Africa, the Middle East, and North America to importers in Europe and Asia. Fracked natural gas converted into LNG is following this same route. And it seems possible that hydrogen and ammonia derived from hydrogen may do the same.

CF Industries, the United States’ largest producer ammonia, has finalized a deal to ship blue ammonia to Japan’s largest power utility for use alongside oil and gas in power generation. The CO2 storage that makes the ammonia blue rather than gray has been contracted between CF Industries and U.S. oil giant Exxon. A highly defensive strategy in Japan thus serves to provide a market for a conservative vision of the energy transition in the United Sates as well. Meanwhile, Saudi Aramco, by far the world’s largest oil company, is touting shipments of blue ammonia, which it hopes to deliver to Japan or East Asia. Though the cost in terms of energy content is the equivalent of around $250 per barrel of oil, Aramco hopes to ship 11 million tons of blue ammonia to world markets by 2030.

To get through the current gas crisis, EU nations have concluded LNG deals with both the Gulf states and the United States. Beyond LNG, it is also fully committed to the hydrogen bandwagon. And again, this follows a defensive logic. The aim is to use green or blue hydrogen or ammonia to find a new niche for European heavy industry, which is otherwise at risk of being entirely knocked out of world markets by high energy prices and Europe’s carbon levy.

The European steel industry today accounts for less than ten percent of global production. It is a leader in green innovation. And the world will need technological first-movers to shake up the fossil-fuel dependent incumbents, notably in China. But whether this justifies Europe’s enormous commitment to hydrogen is another question. It seems motivated more by the desire to hold up the process of deindustrialization and worries about working-class voters drifting into the arms of populists, than by a forward looking strategic calculus.

In the Netherlands, regions that have hitherto served as hubs for global natural gas trading are now competing for designation as Europe’s “hydrogen valley.” In June, German Chancellor Olaf Scholz and Italian Prime Minister Giorgia Meloni inked the contract on the SoutH2 Corridor, a pipeline that will carry H2 up the Italian peninsula to Austria and southern Germany. Meanwhile, France has pushed Spain into agreeing to a subsea hydrogen connection rather than a natural gas pipeline over the Pyrenees. Spain and Portugal have ample LNG terminal capacity. But Spain’s solar and wind potential also make it Europe’s natural site for green hydrogen production and a “green hydrogen” pipe, regardless of its eventual uses, looks in the words of one commentator looks “less pharaonic and fossil-filled” than the original natural gas proposal.

How much hydrogen will actually be produced in Europe remains an open question. Proximity to the point of consumption and the low capital costs of investment in Europe speak in favor of local production. But one of the reasons that hydrogen projects appeal to European strategists is that they offer a new vision of European-African cooperation. Given demographic trends and migration pressure, Europe desperately needs to believe that it has a promising African strategy. Africa’s potential for renewable electricity generation is spectacular. Germany has recently entered into a hydrogen partnership with Namibia. But this raises new questions.

First and foremost, where will a largely desert country source the water for electrolysis? Secondly, will Namibia export only hydrogen, ammonia, or some of the industrial products made with the green inputs? It would be advantageous for Namibia to develop a heavy-chemicals and iron-smelting industry. But from Germany’s point of view, that might well defeat the object, which is precisely to provide affordable green energy with which to keep industrial jobs in Europe.

A variety of conservative motives thus converge in the hydrogen coalition. Most explicit of all is the case of post-Brexit Britain. Once a leader in the exit from coal, enabled by a “dash for gas” and offshore wind, the U.K. has recently hit an impasse. Hard-to-abate sectors like household heating, which in the U.K. is heavily dependent on natural gas, require massive investments in electrification, notably in heat pumps. These are expensive. In the United Kingdom, the beleaguered Tory government, which has presided over a decade of stagnating real incomes, is considering as an alternative the widespread introduction of hydrogen for domestic heating. Among energy experts this idea is widely regarded as an impractical boondoggle for the gas industry that defers the eventual and inevitable electrification at the expense of prolonged household emissions. But from the point of view of politics, it has the attraction that it costs relatively less per household to replace natural gas with hydrogen.

As this brief tour suggests, there is every reason to fear that tens of billions of dollars in subsidies, vast amounts of political capital, and precious time are being invested in “green” energy investments, the main attraction of which is that they minimize change and perpetuate as far as possible the existing patterns of the hydrocarbon energy system. This is not greenwashing in the simple sense of rebadging or mislabeling. If carried through, it is far more substantial than that. It will build ships and put pipes in the ground. It will consume huge amounts of desperately scarce green electricity. And this faces us with a dilemma.

In confronting the challenge of the energy transition, we need a bias for action. We need to experiment. There is every reason to trust in learning-curve effects. Electrolyzers, for instance, will get more affordable, reducing the costs of hydrogen production. At certain times and in certain places, green power may well become so abundant that pouring it into electrolysis makes sense. And even if many hydrogen projects do not succeed, that may be a risk worth taking. We will likely learn new techniques in the process. In facing the uncertainties of the energy transition, we need to cultivate a tolerance for failure. Furthermore, even if hydrogen is a prime example of corporate log-rolling, we should presumably welcome the broadening of the green coalition to include powerful fossil fuel interests.

The real and inescapable tradeoff arises when we commit scarce resources—both real and political—to the hydrogen dream. The limits of public tolerance for the costs of the energy transition are already abundantly apparent, in Asia and Europe as well as in the United States. Pumping money into subsidies that generate huge economies of scale and cost reductions is one thing. Wasting money on lame-duck projects with little prospect of success is quite another. What is at stake is ultimately the legitimacy of the energy transition as such.

In the end, there is no patented method distinguishing self-serving hype from real opportunity. There is no alternative but to subject competing claims to intense public, scientific, and technical scrutiny. And if the ship has already sailed and subsidies are already on the table, then retrospective cost-benefit assessment is called for.

Ideally, the approach should be piecemeal and stepwise, and in this regard the crucial thing to note about hydrogen is that to regard it as a futuristic fantasy is itself misguided. We already live in a hydrogen-based world. Two key sectors of modern industry could not operate without it. Oil refining relies on hydrogen, as does the production of fertilizer by the Haber-Bosch process on which we depend for roughly half of our food production. These two sectors generate the bulk of the demand for the masses of hydrogen we currently consume.

We may not need 600 million, 500 million, or even 300 million tons of green and blue hydrogen by 2050. But we currently use about 100 million, and of that total, barely 1 million is clean. It is around that core that hydrogen experimentation should be concentrated, in places where an infrastructure already exists. This is challenging because transporting hydrogen is expensive, and many of the current points of use of hydrogen, notably in Europe, are not awash in cheap green power. But there are two places where the conditions for experimentation within the existing hydrogen economy seem most propitious.

One is China, and specifically northern China and Inner Mongolia, where China currently concentrates a large part of its immense production of fertilizer, cement, and much of its steel industry. China is leading the world in the installation of solar and wind power and is pioneering ultra-high-voltage transmission. Unlike Japan and South Korea, China has shown no particular enthusiasm for hydrogen. It is placing the biggest bet in the world on the more direct route to electrification by way of renewable generation and batteries. But China is already the largest and lowest-cost producer of electrolysis equipment. In 2022, China launched a modestly proportioned hydrogen strategy. In cooperation with the United Nations it has iniated an experiment with green fertilizer production, and who would bet against its chances of establishing a large-scale hydrogen energy system?

The other key player is the United States. After years of delay, the U.S. lags far behind in photovoltaics batteries, and offshore wind. But in hydrogen, and specifically in the adjoining states of Texas and Louisiana on the Gulf of Mexico, it has obvious advantages over any other location in the West. The United States is home to a giant petrochemicals complex. It is the only Western economy that can compete with India and China in fertilizer production. In Texas, there are actually more than 2500 kilometers of hardened hydrogen pipelines. And insofar as players like Exxon have a green energy strategy, it is carbon sequestration, which will be the technology needed for blue hydrogen production.

It is not by accident that America’s signature climate legislation, the Inflation Reduction Act, targeted its most generous subsidies—the most generous ever offered for green energy in the United States—on hydrogen production. The hydrogen lobby is hard at work, and it has turned Texas into the lowest-cost site for H2 production in the Western world. It is not a model one would want to see emulated anywhere else, but it may serve as a technology incubator that charts what is viable and what is not.

There is very good reason to suspect the motives of every player in the energy transition. Distinguishing true innovation from self-serving conservatism is going to be a key challenge in the new era in which we have to pick winners. We need to develop a culture of vigilance. But there are also good reasons to expect certain key features of the new to grow out of the old. Innovation is miraculous but it rarely falls like mana from heaven. As Sabel and Victor argue in their book, it grows from within expert technical communities with powerful vested interests in change. The petrochemical complex of the Gulf of Mexico may seem an unlikely venue for the birth of a green new future, but it is only logical that the test of whether the hydrogen economy is a real possibility will be run at the heart of the existing hydrocarbon economy.

4 notes

·

View notes

Text

Sirens Market Research by Key players, Type and Application, Future Growth Forecast 2022 to 2032

In 2022, the global sirens market is expected to be worth US$ 170.1 million. The siren market is expected to reach US$ 244.0 million by 2032, growing at a 3.7% CAGR.

The use of sirens is expected to increase, whether for announcements or on emergency vehicles such as ambulances, police cars, and fire trucks. A siren is a loud warning system that alerts people to potentially dangerous situations as they happen.

Rapidly increasing threats and accidents have resulted in more casualties and missed business opportunities in developing economies. Demand for sirens is expected to rise during the forecast period as more people use security solutions.

As a result of rising threats and accidents in developing economies, the number of victims and lost business opportunities has rapidly increased. Adopting security solutions, such as sirens, is an effective way to deal with these challenges. Long-range sirens are used in mining and industrial applications, whereas motorised sirens are used in home security. Hand-operated sirens are used when there is no power or when a backup is required.

Some additional features of sirens include a solar panel upgrade system to keep the batteries charged and a number of digital communication methods, including Ethernet, satellite, IP, fiber optic and others. Sirens have conformal coatings on their electronics, which help protect them against harsh environments. Some of the systems are made in such a way that they can be expanded or scaled depending on future capabilities.

Omni-directional sirens can be used in areas of high noise levels and those with large population densities as they provide a greater area of coverage. Sirens have external controls with triggers, which can be customized according to needs. The lightening types of sirens include bulb revolving, LED flashing and xenon lamp strobe. The loud speakers in sirens are adopted from latest piezoelectric ceramic technology.

Get a Sample Copy of this Report @ https://www.futuremarketinsights.com/reports/sample/rep-gb-4274

Other sirens are hydraulic or air driven and mostly find applications in plants and factories. Lithium batteries have replaced alkaline batteries in sirens now, since lithium batteries need not be replaced for several years. Modern sirens use latest technologies and find applications in civil defense, emergency vehicles, security systems and others. Typically, sirens are made of stainless steel, aluminum or UV stabilized polycarbonate to avoid corrosion and are equipped with protection cages. An LED flashing siren has a light source with a semi-permanent lifespan and it is used in places where bulb replacement is a problem.

Region-wise Outlook

In the global sirens market, the dominant share is held by the U.S., India, China, Japan, Australia, Germany, Singapore and the UAE. This can be attributed to the demand for security solutions in developed as well as developing economies.

The regional analysis includes:

North America (U.S., Canada)

Latin America (Mexico. Brazil)

Western Europe (Germany, Italy, France, U.K, Spain)

Eastern Europe (Poland, Russia)

Asia-Pacific (China, India, ASEAN, Australia & New Zealand)

Japan

The Middle East and Africa (GCC Countries, S. Africa, Northern Africa)

The report is a compilation of first-hand information, qualitative and quantitative assessment by industry analysts, inputs from industry experts and industry participants across the value chain. The report provides in-depth analysis of parent market trends, macro-economic indicators and governing factors along with market attractiveness as per segments. The report also maps the qualitative impact of various market factors on market segments and geographies.

Market Participants

Some of the key market participants identified in the global siren market are Acoustic Technology Inc., Sentry Siren Inc., MA Safety Signal Co. Ltd, Whelen Engineering Co. Inc., Federal Signal Corporation, B & M Siren Manufacturing Co., Projects Unlimited Inc., Phoenix Contact, Mallory Sonalert Products and Qlight USA Inc.

Rising population and rapid urbanization have led to an increase in demand for security solutions. The need for implementation of security has paved way for the use of electronic equipment on a large scale globally, which in turn has created opportunities for the global sirens market. As these products are durable with a high voltage capacity and easy to install, they find high selling propositions. Characteristics and properties of electronic and pneumatic equipment play a vital role in security solutions, thereby driving the global sirens market with a rise in diverse end-user applications, such as industrial warning systems, community warning systems, campus alert systems and military mass warning systems.

Report Highlights:

Detailed overview of parent market

Changing market dynamics in the industry

In-depth Polishing / Lapping Film market segmentation

Historical, current and projected market size in terms of volume and value

Recent industry trends and developments

Competitive landscape

Strategies of key players and products offered

Potential and niche segments, geographical regions exhibiting promising growth

A neutral perspective on market performance

Must-have information for market players to sustain and enhance their market footprint.

Browse Detailed Summary of Research Report with TOC @ https://www.futuremarketinsights.com/reports/sirens-market

Key Segments

Product Type:

Electronic

Electro-mechanical

Rotating

Single/dual toned

Omnidirectional

By Application:

Civil defense

Industrial signaling

Emergency vehicles

Home/vehicle safety

Security/warning systems

Military use

Others

By Installation Type:

Wall mounting

Self-standing

Water proof connector

By Regions:

North America

Europe

Asia Pacific

Latin America

MEA

2 notes

·

View notes

Text

Rail Wheel and Axle Market Analysis by Size, Share, Growth, Trends up to 2033

During the forecast period, the global rail wheel and axle market size is expected to expand at a steady CAGR of 5.6%. At its present growth rate, the global market for rail wheels and axles is expected to be worth $4,402.3 million by the year 2023. In 2033, the demand for rail wheel and axle is projected to reach US$ 7603.4 Mn.

Competitive Landscape

The global rail wheel and axle market is highly competitive, with many companies operating in this space. These companies are engaged in a range of activities, including the production of rail wheels and axles, the repair and maintenance of these products, and the supply of related services.

There are several key players in the global rail wheel and axle market, including Amsted Rail, ArcelorMittal, Bradken, GE Transportation, Klöckner Pentaplast, Lucchini RS, NSSMC, Vyatka, and Wabtec. These companies are well-established players with a strong presence in the market and a reputation for producing high-quality products.

Overall, the global rail wheel and axle market is highly competitive, with a diverse range of companies operating in this space. Companies in the market are constantly seeking ways to differentiate themselves from their competitors, such as through the development of new technologies or the expansion of their product offerings.

For more information: https://www.futuremarketinsights.com/reports/rail-wheel-and-axle-market

Due to the growing sophistication of rail networks and trains, as well as the present trend toward autonomous technology, train makers are devoting significant resources to R&D to develop lighter materials for wheels and axles for freight trains, passenger trains, and short-distance trains.

Nearly 7 billion people take trains each year, and they all want to travel as quickly, easily, and economically as possible. It's for this reason that the research and development of fully driverless trains is continuing to advance. Computerized monitoring systems installed on autonomous trains can detect problems with rail wheels and axles.

There are numerous benefits to using a solar rail system instead of traditional diesel trains. Diesel-powered trains usually have two engine cars. In contrast, solar-powered trains use solar gears in place of traditional gears. Solar panels have been put on the bogie roofs, and electric motors and batteries have been installed in the second diesel compartment.

The electrical needs of railway engines, which normally require 750 V to 800 V to move the rails, may be met by solar panels set atop trains providing voltages of 600 V to 800 V. Demand for these trains is likely to rise, which is good news for manufacturers of rail wheels and axles.

The rail wheel and axle market is an important segment of the global rail transportation industry. Rail wheel and axle products are essential components of rail vehicles, such as trains, trams, and subway cars, and are used to support and propel these vehicles. There are several factors that are driving the global rail wheel and axle market, including growth in rail transportation, urbanisation and population growth, environmental concerns, and technological advancements.

However, the demand for rail wheel and axle is also facing several restraints or challenges, including high capital costs, cyclical demand, a complex supply chain, competition from other modes of transportation, and regulatory challenges. Despite these challenges, the rail wheel and axle market is expected to continue growing in the coming years, driven by increasing demand for rail transportation and ongoing technological advancements in the industry.

Key Takeaways

It is estimated that the US market for rail wheel and axle will be worth $570.8 million in 2022.

Market value in China, the world's second largest economy, is projected to reach $878 million by 2026, expanding at a CAGR of 6% from 2023 to 2033.

Over the projection horizon, both Japan and Canada are predicted to grow at rates of 2.9% and 3.8%, respectively.

The demand for rail wheel and axle in Germany is projected to expand by 3.3% this year.

2 notes

·

View notes

Text

The Rise of Alternative Fuels: How is This Disrupting the Global Oil Market?

The energy sector is undergoing a seismic shift as alternative fuels emerge as viable and sustainable options to fossil fuels. This transition, driven by technological advancements, environmental concerns, and changing consumer preferences, is reshaping the global oil market. The rise of alternative fuels is not just an energy revolution but also a disruption with far-reaching implications for geopolitics, economies, and the oil industry.

Understanding Alternative Fuels

1. What Are Alternative Fuels?

Alternative fuels refer to energy sources other than traditional fossil fuels like oil, coal, and natural gas. These include biofuels, hydrogen, electricity, and synthetic fuels. They are often derived from renewable resources, making them a cleaner and more sustainable choice.

2. Why Are They Gaining Traction?

The adoption of alternative fuels is fueled by several factors:

Environmental Concerns: Rising awareness about climate change and the harmful effects of greenhouse gas emissions has spurred the search for cleaner energy.

Government Policies: Policies like carbon taxes, subsidies for renewable energy, and stringent emission standards are accelerating the transition.

Technological Innovations: Advances in battery technology, fuel cells, and biofuel production have made alternative fuels more efficient and cost-effective.

Impact on the Global Oil Market

3. Declining Oil Demand in Key Sectors

One of the most significant impacts of alternative fuels is the declining demand for oil in sectors like transportation and power generation:

Electric Vehicles (EVs): The rise of EVs, powered by electricity, is reducing the reliance on gasoline and diesel. Leading automakers are investing heavily in EV development, further eroding oil demand.

Biofuels in Aviation: Airlines are increasingly adopting biofuels as a sustainable alternative, challenging the dominance of jet fuel.

4. Price Volatility

The shift towards alternative fuels introduces new uncertainties in the oil market, leading to price volatility. As demand fluctuates and new energy sources gain prominence, traditional oil producers face challenges in maintaining price stability.

5. Investment Diversion

Investors are diverting funds from fossil fuel projects to renewable energy ventures. This shift is evident in the growing number of divestment campaigns and the rise of green bonds, which finance renewable energy initiatives.

Geopolitical Implications

6. Redefining Energy Powerhouses

The rise of alternative fuels is redistributing geopolitical power. Countries rich in renewable resources or leading in technological innovation are emerging as new energy leaders, challenging traditional oil-rich nations.

7. Energy Independence

Alternative fuels provide an opportunity for countries to reduce dependency on oil imports, enhancing energy security. For example, the widespread adoption of solar and wind energy can make nations less vulnerable to geopolitical conflicts in oil-producing regions.

Challenges and Opportunities

8. Challenges for the Oil Industry

The oil industry faces significant challenges as it adapts to the rise of alternative fuels:

Stranded Assets: Investments in oil exploration and infrastructure risk becoming obsolete as demand declines.

Regulatory Pressures: Oil companies must navigate increasingly stringent environmental regulations.

9. Opportunities in Diversification

While the rise of alternative fuels poses challenges, it also presents opportunities for traditional oil companies:

Investing in Renewables: Many oil giants are diversifying into renewable energy projects, such as wind and solar power.

Developing Biofuels: Oil companies are leveraging their expertise to produce and market biofuels, tapping into the growing demand for sustainable energy.

The Future of Energy Markets

10. Integration of Multiple Energy Sources

The energy market of the future will likely be a blend of traditional and alternative sources. Oil will continue to play a role in sectors like petrochemicals, while alternative fuels dominate transportation and electricity generation.

11. Innovation as a Driving Force

Innovation will be the key to accelerating the adoption of alternative fuels. Advances in storage technologies, production methods, and infrastructure development will determine the pace of the transition.

Conclusion

The rise of alternative fuels marks a transformative period in the global energy landscape. While it disrupts traditional oil markets, it also opens up avenues for innovation, collaboration, and sustainable growth. For stakeholders in the energy sector, embracing this change is not just an option but a necessity to thrive in a rapidly evolving market.

Looking for insights and solutions to navigate the dynamic energy landscape? Visit Valor International Holding for expert advice and innovative strategies.

0 notes

Text

Liquid Organic Hydrogen Carriers Market Fueled by Efficient and Stable Hydrogen Solutions

The Liquid Organic Hydrogen Carrier (LOHC) market is poised to revolutionize the hydrogen economy, with its valuation forecasted to rise from USD 0.89 billion in 2023 to over USD 1.6 billion by 2030. With a compound annual growth rate (CAGR) of 5.4% between 2024 and 2030, this market holds immense potential to change the energy landscape. Let’s delve into what’s driving this growth and why LOHC is the key to the future of clean energy.

What Are Liquid Organic Hydrogen Carriers (LOHC)?

LOHCs are organic chemical compounds capable of absorbing and releasing hydrogen through chemical reactions. These carriers offer a stable, safe, and efficient method for storing and transporting hydrogen, making them ideal for large-scale hydrogen distribution systems.

Download Sample Report @ https://intentmarketresearch.com/request-sample/liquid-organic-hydrogen-carrier-market-3042.html

Key Features of LOHCs

Stability: Unlike gaseous hydrogen, LOHCs are stored in liquid form at room temperature, reducing storage risks.

Efficiency: They provide a high hydrogen density, optimizing transportation efficiency.

Safety: LOHC technology eliminates the risks associated with high-pressure hydrogen storage systems.

The Rising Demand for Hydrogen as Clean Energy

As the world seeks to reduce its carbon footprint, hydrogen is emerging as a leading contender for clean energy solutions. Here’s why:

Global Carbon Emission Goals: Nations are setting ambitious goals to achieve net-zero emissions.

Industrial Applications: Hydrogen is being adopted in steel production, ammonia synthesis, and refineries.

Transportation Fuel: Hydrogen-powered vehicles, including fuel-cell electric vehicles (FCEVs), are gaining traction.

Why LOHC Technology?

While hydrogen holds promise, its adoption depends on efficient storage and transport solutions. LOHC technology addresses these challenges by:

Simplifying Infrastructure Needs: It uses existing liquid fuel infrastructure for transportation.

Enhancing Safety: Hydrogen stored in LOHC is non-explosive and less hazardous.

Reducing Costs: It minimizes the need for expensive cryogenic tanks.

Market Segmentation in the LOHC Industry

By Carrier Type

Toluene-Based LOHC: Widely used due to its availability and performance reliability.

Perhydro-Dibenzyltoluene: Offers improved storage capabilities.

N-Ethylcarbazole: Known for high hydrogen absorption efficiency.

By Application

Stationary Applications: Power plants and industries rely on LOHC for hydrogen storage.

Transportation Sector: Supports hydrogen fuel delivery systems for automobiles and aviation.

Regional Analysis of the LOHC Market

North America

Leading the transition to hydrogen economy.

Strong government support and investments in green technologies.

Europe

Accelerated hydrogen adoption due to stringent climate regulations.

Active research in LOHC technologies by nations like Germany and the Netherlands.

Asia-Pacific

Rapid industrialization and growing focus on clean energy.

China, Japan, and South Korea are prominent contributors.

Access Full Report @ https://intentmarketresearch.com/latest-reports/liquid-organic-hydrogen-carrier-market-3042.html

Technological Advancements in LOHC

Catalyst Innovation: Developing better catalysts to enhance hydrogen release and absorption efficiency.

Material Advancements: Exploring alternative LOHC compounds for improved performance.

Integration with Renewable Energy Sources: Aligning LOHC technology with solar and wind energy for sustainable hydrogen production.

Challenges in the LOHC Market

High Initial Investment Costs: Technology adoption requires substantial infrastructure development.

Energy Losses: Efficiency drops during hydrogen absorption and release processes.

Limited Awareness: Many industries lack a clear understanding of LOHC potential.

Future Outlook for the LOHC Market

With ongoing technological advancements and increasing adoption across sectors, the LOHC market is expected to overcome current challenges. Industry collaborations, regulatory support, and public awareness campaigns will likely expedite the integration of LOHC technologies into mainstream energy systems.

FAQs

1. What are the primary advantages of LOHC over traditional hydrogen storage?