#Recycled Carbon Fiber Market Forecast

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Mobile US users spent an average of 115.8 minutes on Tumblr app monthly.

Text

Recycled Carbon Fiber Market: Sustainability and Innovation Driving Growth

The recycled carbon fiber market is gaining momentum as industries seek sustainable alternatives to traditional materials. Recycled carbon fiber, known for its lightweight, high-strength, and cost-effective properties, is finding increasing applications across various sectors, including automotive, aerospace, construction, and sports equipment. As environmental concerns and resource efficiency become paramount, the market for recycled carbon fiber is poised for substantial growth. This article explores the current trends, key drivers, applications, and future outlook of the recycled carbon fiber market.

Market Overview

The global recycled carbon fiber market was valued at approximately USD 150 million in 2022 and is projected to reach USD 350 million by 2030, growing at a CAGR of around 11.5% during the forecast period. This growth is driven by the rising demand for sustainable materials, advancements in recycling technologies, and increasing applications in high-performance industries.

Key Drivers

1. Environmental Sustainability: As industries strive to reduce their environmental footprint, the demand for sustainable materials like recycled carbon fiber is increasing. Recycled carbon fiber offers a greener alternative to virgin carbon fiber, significantly reducing waste and lowering energy consumption during production.

2. Cost Efficiency: Recycled carbon fiber is more cost-effective than virgin carbon fiber, making it an attractive option for industries looking to optimize costs without compromising on performance. The lower price point is particularly beneficial for sectors like automotive and construction, where cost considerations are critical.

3. Technological Advancements: Innovations in recycling technologies are enhancing the quality and performance of recycled carbon fiber. Improved processes for fiber recovery and treatment are resulting in higher-quality recycled fibers that can compete with virgin fibers in demanding applications.

4. Regulatory Pressures: Governments and regulatory bodies worldwide are implementing stricter regulations to promote recycling and reduce landfill waste. These regulations are driving the adoption of recycled materials, including carbon fiber, across various industries.

For a comprehensive analysis of the market drivers:- https://univdatos.com/report/recycled-carbon-fiber-market/

Applications

Recycled carbon fiber is used in a variety of applications across multiple industries:

- Automotive: The automotive industry is a significant consumer of recycled carbon fiber, using it to produce lightweight, high-strength components that improve fuel efficiency and reduce emissions. Applications include interior and exterior parts, structural components, and under-the-hood parts.

- Aerospace: In the aerospace industry, weight reduction is critical for improving fuel efficiency and performance. Recycled carbon fiber is used in the manufacture of aircraft interiors, secondary structures, and other non-critical components where cost savings are essential.

- Construction: The construction sector uses recycled carbon fiber for reinforcing concrete and other building materials. Its high strength-to-weight ratio enhances the durability and longevity of structures while reducing overall weight.

- Sports Equipment: Recycled carbon fiber is increasingly used in the production of sports equipment such as bicycles, tennis rackets, and golf clubs. Its lightweight and high-strength properties enhance the performance and durability of these products.

- Consumer Goods: The consumer goods sector is also adopting recycled carbon fiber for various applications, including electronics, luggage, and outdoor gear. Its aesthetic appeal and performance benefits make it an attractive material for high-end products.

Regional Insights

The recycled carbon fiber market is geographically diverse, with significant growth observed in North America, Europe, and Asia-Pacific.

- North America: The North American market is driven by the automotive and aerospace industries' demand for sustainable materials. The presence of major manufacturers and advancements in recycling technologies also contribute to market growth.

- Europe: Europe is a significant player in the recycled carbon fiber market, with strong regulatory frameworks promoting recycling and sustainability. Countries like Germany, the UK, and France are leading in the adoption of recycled carbon fiber in various applications.

- Asia-Pacific: The Asia-Pacific region is experiencing rapid market growth, fueled by expanding industrial activities and increasing awareness of sustainability. China, Japan, and South Korea are key markets, with significant demand from the automotive and construction sectors.

For a sample report, visit:- https://univdatos.com/get-a-free-sample-form-php/?product_id=34471

Future Prospects

The future of the recycled carbon fiber market looks promising, with several trends expected to shape its trajectory:

- Increased Adoption in High-Performance Industries: As the quality of recycled carbon fiber continues to improve, its adoption in high-performance industries like aerospace and automotive is expected to increase. These industries will benefit from the material's cost efficiency and sustainability.

- Expansion in Emerging Markets: Emerging markets, particularly in Asia-Pacific and Latin America, are expected to drive significant demand for recycled carbon fiber. Growing industrial activities and rising environmental awareness in these regions will contribute to market expansion.

- Focus on Circular Economy: The emphasis on circular economy practices will drive the development and use of recycled carbon fiber. Companies will increasingly focus on creating closed-loop systems that minimize waste and maximize resource efficiency.

- Technological Innovations: Ongoing research and development will lead to further advancements in recycling technologies, enhancing the quality and performance of recycled carbon fiber. Innovations in fiber recovery, processing, and treatment will expand its application scope.

In conclusion, the recycled carbon fiber market is set for robust growth, driven by the increasing demand for sustainable materials, cost efficiency, and technological advancements. As industries continue to prioritize sustainability and resource efficiency, recycled carbon fiber will play a crucial role in shaping the future of materials science and industrial production.

Contact Us:

UnivDatos Market Insights

Email - [email protected]

Contact Number - +1 9782263411

Website -www.univdatos.com

#Recycled Carbon Fiber Market#Recycled Carbon Fiber Market Growth#Recycled Carbon Fiber Market Share#Recycled Carbon Fiber Market Forecast

0 notes

Text

The Recycled Carbon Fiber Market is expected to reach USD 155.92 million in 2023 and grow at a CAGR of 13.65% to reach USD 295.63 million by 2028. Toray Industries Inc., Procotex, Vartega Inc., Gen 2 Carbon Limited, Sigmatex are the major companies.

#Recycled Carbon Fiber Market Report#Recycled Carbon Fiber Industry Report#Recycled Carbon Fiber Market#Recycled Carbon Fiber Market Size#Recycled Carbon Fiber Market Share#Recycled Carbon Fiber Market Growth#Recycled Carbon Fiber Market Trends#Recycled Carbon Fiber Market Analysis#Recycled Carbon Fiber Market Forecast

0 notes

Text

Global Recycled Carbon Fiber Market Overview by Industry Size, Share, Future Trends, Growth Factors To 2028

The most recent research study provides a thorough investigation of the worldwide Recycled Carbon Fiber Market for the years 2022-2028, which is useful for companies of any size regardless of their sales. This survey investigation takes into account the significant market and industry strategy for COVID-19 in the years to come. The research that Recycled Carbon Fiber conducted on the market…

View On WordPress

#Recycled Carbon Fiber Market Analysis#Recycled Carbon Fiber Market Demand#Recycled Carbon Fiber Market Forecast#Recycled Carbon Fiber Market Growth Rate#Recycled Carbon Fiber Market Insights#Recycled Carbon Fiber Market Leading Players#Recycled Carbon Fiber Market Opportunities#Recycled Carbon Fiber Market Price#Recycled Carbon Fiber Market Share#Recycled Carbon Fiber Market Size#Recycled Carbon Fiber Market Trend#Recycled Carbon Fiber Market Value

0 notes

Text

The Global Polyacrylonitrile Fiber Market is projected to grow from USD 9,150.00 million in 2023 to an estimated USD 13,147.80 million by 2032, reflecting a compound annual growth rate (CAGR) of 4.11% from 2024 to 2032.Polyacrylonitrile (PAN) fibers, known for their superior strength, thermal stability, and chemical resistance, have become an integral component in various industries, including textiles, automotive, and aerospace. As global industries demand lightweight, durable, and cost-effective materials, the polyacrylonitrile fiber market is poised for significant growth. This article explores the current trends, market drivers, challenges, and future opportunities in the polyacrylonitrile fiber sector.

Browse the full report at https://www.credenceresearch.com/report/polyacrylonitrile-fiber-market

Market Overview

Polyacrylonitrile fibers are synthetic fibers derived from acrylonitrile, often used in the production of carbon fiber, which is renowned for its high tensile strength and lightweight properties. These fibers serve as precursors for carbon fiber manufacturing, making them essential in high-performance applications. With a growing focus on renewable energy, green technologies, and sustainability, the demand for PAN fibers is increasing in industries such as wind energy, automotive, and construction.

Key Drivers of Market Growth

Rising Demand for Carbon Fiber Carbon fiber, derived from PAN, has become a material of choice in industries that prioritize lightweight and high-strength materials. Its extensive use in aerospace for building fuel-efficient aircraft and in the automotive industry for lightweight vehicles to improve fuel efficiency has propelled the demand for PAN fibers.

Growth in the Textile Industry Polyacrylonitrile fibers are also used in textiles for manufacturing synthetic wool, thermal insulation fabrics, and outdoor wear. The increasing popularity of functional and performance-driven clothing is driving market expansion in this segment.

Sustainability Initiatives The global emphasis on reducing greenhouse gas emissions has led to increased adoption of carbon-neutral technologies, where PAN-based carbon fibers are instrumental. Renewable energy sectors, particularly wind power, rely on carbon fiber for manufacturing durable and lightweight turbine blades.

Technological Advancements Continuous advancements in polymer processing and fiber production have improved the cost-efficiency and performance of PAN fibers. Emerging methods of recycling and reusing PAN fibers are also gaining traction, aligning with global sustainability goals.

Challenges in the Market

Despite its promising growth prospects, the polyacrylonitrile fiber market faces several challenges:

High Production Costs The manufacturing process of PAN fibers, particularly for carbon fiber production, is energy-intensive and costly. This limits its affordability for some applications, particularly in developing markets.

Environmental Concerns The production of PAN fibers involves the use of toxic chemicals, raising concerns about its environmental impact. Strict environmental regulations may hinder production capabilities in certain regions.

Competition from Alternative Materials Advances in materials science have led to the development of alternative fibers and composites. These alternatives often offer similar or superior properties at lower costs, challenging PAN's market share.

Future Opportunities

The future of the polyacrylonitrile fiber market lies in innovation and sustainability. Companies investing in research to develop low-cost and eco-friendly PAN fibers are likely to gain a competitive edge. Additionally, the growing demand for electric vehicles, which rely on lightweight materials, presents a lucrative opportunity for market players. Emerging markets in Africa and the Middle East also offer untapped potential for PAN fiber applications in construction and energy sectors.

Key players

Shandong Haili

Jilin Chemical Fiber

Sateri

Fibrant

Jiangsu Sailboat Petrochemical

Xinjiang Tianye

Mitsubishi Chemical

Yantai Taihe

Tongkun Group

Samyang Corporation

Segments

Based on Type

Standard PAN

High Modulus PAN

Medium Modulus PAN

Carbon Fiber Precursor PAN

Based on Application

Apparel & Clothing

Automotive & Transportation

Construction

Industrial

Medical

Based on End User

Textiles

Automotive Parts

Construction Material

Industrial Composites

Medical Devices

Based on Yarn Type

Filament Yarn

Staple Fibre

Based on Region

North America

U.S.

Canada

Mexico

Europe

UK

France

Germany

Italy

Spain

Russia

Belgium

Netherlands

Austria

Sweden

Poland

Denmark

Switzerland

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Thailand

Indonesia

Vietnam

Malaysia

Philippines

Taiwan

Rest of Asia Pacific

Latin America

Brazil

Argentina

Peru

Chile

Colombia

Rest of Latin America

Middle East

UAE

KSA

Israel

Turkey

Iran

Rest of Middle East

Africa

Egypt

Nigeria

Algeria

Morocco

Rest of Africa

Browse the full report at https://www.credenceresearch.com/report/polyacrylonitrile-fiber-market

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

0 notes

Text

Basalt Fiber Market: Revolutionizing Industries with Sustainability and High Performance

Basalt fiber might not yet be a household name, but it’s quickly earning its place as a material that’s rewriting the rules in several industries. What makes basalt fiber stand out is its ability to combine sustainability with high performance—two qualities that industries today are desperate to balance.

Sourced from volcanic rock, basalt fibers are incredibly strong, lightweight, and resistant to extreme conditions. Unlike some conventional materials, their production doesn’t require harmful chemicals, making them an eco-friendly alternative. For industries like construction, automotive, wind energy, electronics, and marine, basalt fiber isn’t just an option—it’s a necessity for staying relevant in a world demanding greener and better-performing materials.

The global basalt fiber market is poised for significant growth, with an expected valuation of USD 279 million in 2023, and a projected Compound Annual Growth Rate (CAGR) of

12.5% throughout the forecasted period, aiming to reach USD 503 million by 2028.

The Unique Strength of Basalt Fiber

The appeal of basalt fiber goes beyond its novelty. It is naturally robust, boasting high tensile strength and resistance to corrosion. Imagine a material that can endure the harshest environments—extreme heat, chemicals, or even saltwater—without breaking down. That’s basalt fiber.

But what really excites engineers and designers is its versatility. It’s lightweight yet tough, cost-effective yet high-performing, and, perhaps most importantly in today’s climate-conscious world, recyclable and non-toxic.

Unlike carbon fiber, which can be expensive, or fiberglass, which may fall short in eco-credentials, basalt fiber is the perfect middle ground. Its production process—melting volcanic rock at high temperatures and pulling it into fibers—requires no additives, which keeps it clean and simple.

Applications Driving Basalt Fiber Demand

1. Building Stronger, Greener Infrastructure

In construction, basalt fiber is making waves as a revolutionary reinforcement material. For decades, we’ve relied on steel, but in environments prone to moisture or chemicals, steel corrodes, leading to costly repairs and maintenance. Basalt fibers offer a solution with corrosion resistance and durability that outlasts traditional materials.

Think of bridges, seawalls, or even underground tunnels—structures where durability is critical. Basalt fiber-reinforced concrete doesn’t just last longer; it’s also lighter, which reduces transportation costs and simplifies installation.

2. Transforming Automotive and Transportation

The automotive world is laser-focused on cutting weight to improve fuel efficiency and meet stringent emission norms. Basalt fiber fits perfectly into this equation. From car body panels to interior components, its strength-to-weight ratio is hard to ignore.

It’s also popping up in trucks, trains, and even shipping containers. A lighter vehicle isn’t just more fuel-efficient—it also reduces wear and tear on roads, making basalt fiber a win-win for the entire transportation ecosystem.

3. Boosting Wind Energy Efficiency

The renewable energy industry is turning to basalt fiber for its ability to handle stress and environmental extremes. Wind turbine blades, in particular, face constant mechanical and environmental challenges. Basalt fibers provide the strength, flexibility, and weather resistance needed to enhance blade performance and longevity.

For a sector trying to reduce costs while improving energy output, basalt fiber-based composites are becoming the go-to material.

4. Enhancing Electrical and Electronic Safety

Basalt fiber’s non-conductive properties make it a natural fit for the electrical and electronics industry. It’s used in circuit boards, insulation, and protective casings. With the growing emphasis on energy-efficient appliances and safer electronics, basalt fiber ensures products meet performance and safety standards.

5. Sailing Ahead in the Marine Industry

Saltwater is unforgiving, especially for traditional materials like steel or fiberglass. Basalt fiber’s resistance to saltwater and chemicals makes it ideal for marine applications like boat hulls, underwater pipelines, and fishing rods.

It’s lightweight, meaning ships and boats consume less fuel, contributing to greener maritime operations. For an industry battling both environmental and cost pressures, basalt fiber is a breath of fresh air.

Why Basalt Fiber is the Future

Sustainability Leads the Way

The days of choosing materials purely for performance are over. Sustainability is no longer optional. Basalt fiber’s eco-friendly production process—requiring no harmful additives���makes it a leader in sustainable materials.

Infrastructure Investments

With nations modernizing old infrastructure and building new projects, there’s a growing need for corrosion-resistant, durable materials. Basalt fiber fits the bill perfectly, ensuring longevity in everything from highways to high-rises.

Growing Demand in Emerging Markets

Emerging economies in regions like Asia-Pacific and the Middle East are adopting basalt fibers rapidly, thanks to their cost-effectiveness and versatility. These regions are investing heavily in infrastructure, automotive production, and renewable energy, making them hotbeds for basalt fiber adoption.

To know more download PDF Brochure :

Basalt fiber isn’t just a trend—it’s a material that aligns perfectly with the needs of modern industries. Whether it’s reducing carbon footprints, improving performance, or cutting costs, basalt fiber is proving its worth across sectors.

For experts in construction, automotive, wind energy, electronics, or marine industries, basalt fiber is no longer something to keep an eye on—it’s something to embrace. It’s not just the material of the future; it’s the material of today.

#Basalt Fiber Market#Sustainable Materials#Construction Materials#Automotive Industry#Wind Energy Components#Eco-Friendly Materials#Renewable Energy Materials

0 notes

Text

Polycarbonate Composites Market: Lightweight and Durable Innovations Driving Industrial Use up to 2033

The Polycarbonate Composites Market focuses on materials created by combining polycarbonate (PC) resin with reinforcing agents such as glass fibers, carbon fibers, or other fillers. These composites are well-known for their excellent impact resistance, high strength-to-weight ratio, optical clarity, and flame-retardant properties. The versatility of polycarbonate composites makes them widely used in applications across automotive, electronics, aerospace, construction, and healthcare industries.

To Know More @ https://www.globalinsightservices.com/reports/polycarbonate-composites-market

The polycarbonate composites market is anticipated to expand from $2.1 billion in 2023 to $4.3 billion by 2033, achieving a CAGR of 7.4%.

Market Outlook The Polycarbonate Composites Market is experiencing strong growth due to the increasing demand for lightweight yet durable materials in key industries. The automotive sector, in particular, is a significant driver, as manufacturers are seeking materials that reduce vehicle weight to improve fuel efficiency and meet stringent emission standards. Polycarbonate composites are becoming a preferred choice for automotive components such as headlamp lenses, interior parts, and glazing solutions due to their exceptional strength and lightweight characteristics.

In the electronics and electrical industry, the demand for polycarbonate composites is also surging. The materials’ excellent electrical insulation properties and high heat resistance make them suitable for producing enclosures, connectors, and electronic device casings. The growth of the consumer electronics market and the rising adoption of smart devices are contributing to increased usage of polycarbonate composites in this sector.

Aerospace and defense industries are turning to polycarbonate composites for applications that require high performance and safety, such as aircraft interiors, cockpit canopies, and ballistic-grade materials. The aerospace sector’s focus on weight reduction for fuel efficiency and enhanced durability further drives the demand for polycarbonate composites. Additionally, the construction industry is leveraging these materials for glazing applications and structural components where impact resistance and transparency are essential.

The market is witnessing innovations in composite manufacturing processes, such as the development of thermoplastic composites that offer advantages in recyclability and faster production cycles. Advancements in nanotechnology and surface modification techniques are also enhancing the properties of polycarbonate composites, expanding their application range and performance capabilities.

Environmental sustainability is a growing trend in the Polycarbonate Composites Market. Companies are investing in research and development to produce eco-friendly composites using bio-based polycarbonates and recycled materials. The push for sustainable materials aligns with global efforts to reduce plastic waste and promote the circular economy.

Asia-Pacific is expected to dominate the Polycarbonate Composites Market, driven by rapid industrialization, urbanization, and growing automotive and electronics manufacturing. Countries like China, Japan, and South Korea are leading in both production and consumption of polycarbonate composites. North America and Europe are also key markets, with strong demand from the automotive and aerospace sectors.

Request the sample copy of report @ https://www.globalinsightservices.com/request-sample/GIS32456

Research Objectives

Estimates and forecast the overall market size for the total market, across product, service type, type, end-user, and region

Detailed information and key takeaways on qualitative and quantitative trends, dynamics, business framework, competitive landscape, and company profiling

Identify factors influencing market growth and challenges, opportunities, drivers and restraints

Identify factors that could limit company participation in identified international markets to help properly calibrate market share expectations and growth rates

Trace and evaluate key development strategies like acquisitions, product launches, mergers, collaborations, business expansions, agreements, partnerships, and R&D activities

Thoroughly analyze smaller market segments strategically, focusing on their potential, individual patterns of growth, and impact on the overall market

To thoroughly outline the competitive landscape within the market, including an assessment of business and corporate strategies, aimed at monitoring and dissecting competitive advancements.

Identify the primary market participants, based on their business objectives, regional footprint, product offerings, and strategic initiatives

Request For Report Customization @ https://www.globalinsightservices.com/request-customization/GIS32456

Market Segmentation

In 2023, the Polycarbonate Composites Market demonstrated robust performance, with a market volume of 600 million metric tons and projections to reach 900 million metric tons by 2033. The automotive sector dominates the market share at 45%, driven by the industry’s demand for lightweight and durable materials. The electronics segment follows with a 30% share, benefiting from the increasing use of polycarbonate composites in consumer electronics. The construction segment holds a 25% share, supported by the material’s strength and versatility. Key players such as Covestro AG, SABIC, and Teijin Limited maintain substantial market presence, influencing sector dynamics.

Competitive pressures and regulatory frameworks significantly impact the Polycarbonate Composites Market. Companies are investing in sustainable production methods to comply with stringent environmental regulations. The EU’s Green Deal and similar policies worldwide are pushing for eco-friendly manufacturing processes. Future projections indicate a 10% annual increase in R&D expenditure, targeting innovations in recycling and material efficiency. The market outlook remains optimistic, with growth driven by advancements in composite technology and expanding applications across various industries. However, challenges such as fluctuating raw material prices and the need for technological advancements persist, necessitating strategic collaborations and investments in cutting-edge technologies.

Major Players

SABIC Innovative Plastics

Covestro

Teijin Limited

Mitsubishi Chemical Corporation

Chi Mei Corporation

LG Chem

Trinseo

Lotte Chemical

Asahi Kasei Corporation

Idemitsu Kosan

RTP Company

Plazit Polygal

PolyOne Corporation

Ensinger

Bayer MaterialScience

A. Schulman

SABIC

Sumitomo Chemical

Toray Industries

Mitsui Chemicals

Request For Discounted Pricing @ https://www.globalinsightservices.com/request-special-pricing/GIS32456

Research Scope

Scope – Highlights, Trends, Insights. Attractiveness, Forecast

Market Sizing – Product Type, End User, Offering Type, Technology, Region, Country, Others

Market Dynamics – Market Segmentation, Demand and Supply, Bargaining Power of Buyers and Sellers, Drivers, Restraints, Opportunities, Threat Analysis, Impact Analysis, Porters 5 Forces, Ansoff Analysis, Supply Chain

Business Framework – Case Studies, Regulatory Landscape, Pricing, Policies and Regulations, New Product Launches. M&As, Recent Developments

Competitive Landscape – Market Share Analysis, Market Leaders, Emerging Players, Vendor Benchmarking, Developmental Strategy Benchmarking, PESTLE Analysis, Value Chain Analysis

Company Profiles – Overview, Business Segments, Business Performance, Product Offering, Key Developmental Strategies, SWOT Analysis

For In-Depth Competitive Analysis, Buy Now @ https://www.globalinsightservices.com/checkout/single_user/GIS32456

About Us

With Global Insight Services, you receive:

10-year forecast to help you make strategic decisions

In-depth segmentation which can be customized as per your requirements

Free consultation with lead analyst of the report

Infographic excel data pack, easy to analyze big data

Robust and transparent research methodology

Unmatched data quality and after sales service

Contact Us:

Global Insight Services LLC

16192, Coastal Highway, Lewes DE 19958

E-mail: [email protected]

Phone: +1-833-761-1700

Website: https://www.globalinsightservices.com/

0 notes

Text

Polyethylene Terephthalate Market Insights: Market Share, Growth Trends, and Forecast for 2031

The global polyethylene terephthalate (PET) market was valued at USD 30.09 billion in 2022. It is projected to grow from USD 31.06 billion in 2023 to USD 40.65 billion by 2031, registering a compound annual growth rate (CAGR) of 3.4% during the forecast period (2023–2031).

Market Definition

Polyethylene terephthalate (PET) is a versatile plastic material widely used across various industries, primarily in packaging, textiles, and consumer goods. PET is one of the most commonly produced plastics globally, known for its strength, durability, and recyclability. It is made from the polymerization of terephthalic acid and ethylene glycol and is predominantly used in the production of plastic bottles, films, and fibers.

Get a Full PDF Sample Copy of the Report @ https://straitsresearch.com/report/polyethylene-terephthalate-market/request-sample

Market Dynamics: Key Trends, Growth Factors, and Opportunities

Key Trends:

Rising Demand for Sustainable Packaging Solutions: With the growing concern over plastic waste and environmental sustainability, there has been a marked shift toward using recyclable and eco-friendly materials. PET, being highly recyclable, has seen increased adoption in the packaging sector, especially for bottled water and other beverages. Brands are increasingly opting for recycled PET (rPET) to reduce their carbon footprint and contribute to sustainability efforts.

Technological Advancements in PET Recycling: The advancements in PET recycling technologies have improved the efficiency and cost-effectiveness of recycling processes. Innovations in chemical and mechanical recycling techniques are making it easier to repurpose PET waste into high-quality materials for reuse in packaging and other applications. These technological breakthroughs are expanding the scope of PET's lifecycle, promoting a circular economy.

Growth of E-commerce and Demand for Packaging: The rapid expansion of e-commerce and online retail platforms is driving the demand for packaging materials, including PET. With an increase in packaged goods for home delivery, PET’s durability and lightweight properties make it the preferred choice for packaging a variety of products, including food, beverages, and household items.

Key Growth Factors:

Strong Demand from the Packaging Industry: Packaging remains the dominant application for PET, accounting for a substantial share of the market. The increasing need for lightweight, durable, and cost-effective packaging materials, particularly in the food and beverage sector, is driving the demand for PET. The material's high barrier properties help preserve product freshness, which makes it ideal for packaging perishable goods like bottled water, carbonated beverages, and juices.

Expanding Use in Non-Packaging Applications: PET is gaining popularity beyond packaging, especially in textiles and automotive applications. In the textile industry, PET is used to produce fabrics for clothing, upholstery, and carpeting. Additionally, the automotive sector is adopting PET-based materials for various interior components, driven by the material’s lightweight and durable characteristics, which contribute to fuel efficiency and vehicle performance.

Consumer Preference for Convenience Packaging: As consumer preferences evolve, convenience and portability have become key factors in packaging design. PET’s ability to be molded into various shapes and sizes, its transparency, and its ability to preserve the contents make it the go-to material for single-serve and portable packaging solutions. This trend is particularly evident in the beverage and food packaging sectors.

Key Market Opportunities:

Adoption of Recycled PET (rPET): The growing trend of using recycled PET (rPET) presents significant opportunities for the market. As more companies focus on sustainability and reducing their environmental impact, the use of rPET in packaging is expected to surge. Governments around the world are also implementing stricter regulations on plastic waste, encouraging companies to adopt more recycled materials, thus boosting the demand for rPET.

Growth of Biodegradable PET (Bio-PET): The development of bio-based PET, or Bio-PET, made from renewable resources like sugarcane, offers a promising opportunity for the market. With rising consumer awareness of environmental issues, bio-PET is expected to witness increased adoption as an alternative to conventional PET in various applications, including packaging and textiles.

Expansion of PET Use in Emerging Markets: The demand for PET is growing rapidly in emerging markets such as India, China, and Southeast Asia due to rapid urbanization, increasing disposable incomes, and the expansion of retail and packaging industries. The availability of low-cost production options and the growing adoption of PET-based products are expected to drive market growth in these regions.

Market Segmentation

The global polyethylene terephthalate market is segmented by application, packaging application, and end-user industry. This segmentation allows for a detailed analysis of the market’s diverse applications and emerging opportunities.

By Application:

Packaging

Films & Sheets

Others

By Packaging Application:

Bottled Water

Carbonated Soft Beverages

Juices

Alcoholic Beverages

Thermoforming Trays

Food Packaging

Non-Food Packaging

Others

Access Detailed Segmentation @ https://straitsresearch.com/report/polyethylene-terephthalate-market/segmentation

Key Players in the Polyethylene Terephthalate Market

The polyethylene terephthalate market is highly competitive, with several global players leading the way in innovation, production, and sustainability efforts. Key market participants include:

Alpek S.A.B de C.V

BASF SE

DuPont de Nemours, Inc.

Indorama Ventures

Lanxess Corporation

Koninklijke DSM N.V.

Dhunseri Petrochem Ltd.

Eastman Chemical Company

Reliance Industries Ltd

Distrupol

Verdeco Recycling Inc

SRF Limited

RadiciPartecipazioni S.P.A.

Kolon Plastics

SABIC

These companies are focusing on product diversification, sustainable practices, and expanding their global presence to capitalize on the growing demand for PET across various sectors.

Regional Analysis

Dominated Region: Asia-Pacific Asia-Pacific is the dominant region in the global polyethylene terephthalate market, owing to the rapid industrialization and increasing demand for PET in packaging applications, particularly in countries like China, India, and Japan. The region's growing retail and e-commerce industries are also contributing to the high demand for PET packaging.

Fastest Growing Region: North America North America is expected to be the fastest-growing region for the polyethylene terephthalate market, driven by the increasing shift toward sustainable and eco-friendly packaging solutions. The rising adoption of rPET and the growing consumer preference for environmentally conscious brands are propelling market growth in this region.

Conclusion

The global polyethylene terephthalate market is poised for steady growth, with a projected market size of USD 40.65 billion by 2031. Driven by strong demand in packaging, textile applications, and the rising focus on sustainability, PET’s versatility and recyclability make it a key material in various industries. With new opportunities in recycled and biodegradable PET, the market is expected to continue evolving in line with environmental trends and consumer preferences.

For more information or to customize the report before purchasing, visit: https://straitsresearch.com/buy-now/polyethylene-terephthalate-market

About Us:

StraitsResearch.com is a leading market research and market intelligence organization, specializing in research, analytics, and advisory services along with providing business insights & market research reports.

Contact Us:

Email: [email protected] Tel: +1 646 905 0080 (U.S.), +44 203 695 0070 (U.K.) Website: https://straitsresearch.com/

0 notes

Text

Japan Thermoset Plastics Market Analysis 2032

Japan thermoset plastics market is expected to observe a CAGR of 5.38% during the forecast period FY2025-FY2032, rising from USD 5,107.88 million in FY2023 to USD 8,204.15 million in FY2032F. The growth of the market can be attributed to the quick development of the utilization of engineering plastics.

By FY2032, the thermoset plastics market in Japan is anticipated to grow due to the application of thermoset plastics market in Japan, driven by the nation’s ongoing development of its bio-based phenolic resins utilizing lignin and the quick development of integrated molding technology for carbon fiber-reinforced plastic. Therefore, it’s predicted that these developments would raise the need for thermoset polymers in several industries including steel, fertilizers, and the automobile industry.

Due to Japan’s stringent waste management and recycling laws, recycling technology and sustainable thermoset polymers are developing. NIPPON STEEL Chemical & Material Co., Ltd. supplies thermoset resin materials to enhance the durability and corrosion resistance of coatings applied to industrial facilities, bridges, and pipelines. This helps increase the demand for thermoset plastics.

For instance, Mitsui Chemicals Inc. and Microwave Chemical Co., Ltd. are developing chemical recycling technology using microwaves. Microwaves, used as household ovens and telecommunications, can directly and selectively transfer energy to materials, making conventional chemical processes more energy efficient. Environmentally friendly technology can reduce CO2 emissions and generate energy from renewable sources.

Saturated polyester resins, epoxy resins, and polyurethane foam manufacturing have increased significantly in the market, indicating a persistent need for these materials. Recent business changes that may affect the direction of thermoset plastic market in the future include advancements in manufacturing technology and the emergence of eco-friendly alternatives.

For instance, Daicel Corporation, specialist in innovative thermoset plastics solutions, is serving several industries including automotive, electronics, construction, and healthcare. Automotive parts, electrical components, building materials, and medical devices employ phenolic resins, epoxy resins, and polyurethane systems. Due to its concentration on these areas, Daicel is a reliable partner for companies looking for high-performance thermoset plastics solutions. It helps to propel innovation and sustainable growth in Japan’s industrial sector.

Thermoset Plastics Revolutionize Vehicle Lightweighting in EVs

Advance development in lightweight electric vehicles (EVs) has surged Japan’s thermoset plastic market. Players in Japan’s thermoset market are collaborating to develop advanced thermoset resin molding, while companies such as Nissei Plastic aim to optimize the injection pressure, which can help manufacturers create parts with tighter tolerances and improved quality. Overall, Japan’s automotive sector shows a bigger trend towards lightweight vehicles and sustainability, which can significantly impact the EV manufacturing while increasing the demand for thermoset plastics.

For instance, Celanese Corporation has launched two new polyamide solutions for electric vehicle powertrain components and battery applications. The Frianyl PA W-series flame-retardant polyamide solutions enable the production of large, thick-walled components for EV batteries. These solutions improve safety, design, and manufacturing efficiency. Applications include battery module housings and electronic box housings. The Frianyl PA W Series solutions have an excellent relative tracking index even after 1,000 hours of aging at 125 degrees Celsius. They offer remarkable long-term color stability, without visible changes to the naked eye or color laboratory measurements.

Wind Energy Industry Fuels Japan Thermoset Plastics Market Size

Wind energy generation promotes sustainability and economic progress by accelerating income creation through sophisticated recycling techniques in the thermoset plastics market. For instance, according to the Japan Wind Power Association (JWPA), by the end of FY2023, Japan’s total installed wind power capacity reached 5,213.4 MW. Due to breakthrough methods in small-molecule assistance, it is now possible to recycle wind turbine blades with up to 100% resin degradation yield for waste composite materials. Furthermore, as Japan and other countries increase their investments in wind power, using carbon fiber composites may generate economic growth while supporting sustainability in the market.

Increasing Utilization of Epoxy in Thermoset Plastics Dominates Japan Thermoset Plastics Market

Epoxy resins are essential thermoset polymers with unique characteristics and can be used in a wide temperature range. Epoxy has the highest contribution in Japan thermoset plastics market due to increasing use of epoxy in electrical components, paintbrush manufacturing, adhesives for structural usage, metal coatings, and high-tension electrical insulators increasing the demand of epoxy in thermoset plastics market in Japan. For instance, DIC’s epoxy resin curing agent, which can withstand temperatures up to 200 degrees Celsius and is recyclable, makes it easier to remold thermoset plastics, which were previously difficult to recycle.

Adoption of Injection Molding Technology in Japan Thermoset Plastics

As per the processing type, injection molding holds dominant market share due to its increasing usage in thermoset plastics leading to chemical crosslinking and hardening of polymer. Thermoset injection molding equipment generally includes a hydraulically driven clamping device for mold closure and an injection device for conveying materials, producing thermoset plastics used in the automobile industry and medical devices. Injection moldings offer advantages such as high production efficiency, intricate design capabilities, and consistent quality, making it a favored option among manufacturers for a wide range of applications.

South Japan Become the Highest Contributor in the Market

In 2024, the southern region of Japan has the highest share in Japan thermoset plastics market, followed by the north region. Japan’s regions are expected to experience a rise in power generation sector which will fuel the advancement of thermoset plastics. Thermoset plastics are successively employed in numerous applications, significantly contributing to the efficiency and reliability of power generation processes. For instance, NIPPON STEEL Chemical & Material Co., Ltd operates manufacturing plants across Japan, including Tokyo, Osaka, and Nagoya. The company continuously develops advanced technology and production capabilities to meet the demand for thermoset plastics.

Download Free Sample Report

Future Market Scenario (FY2025 – FY2032F)

As per Japan thermoset plastic market analysis, the demand for thermoset plastics will significantly increase over the forecast period, owing to rising demand from key End-use industries, including transportation, automotive, marine, aviation, power generation, oil, refinery, and others. Thermoset materials play a crucial role in the rising research and development activities for construction of wind turbine blades, solar panels, and other renewable energy infrastructure. For instance, the expansion of wind power generation capacities has expanded from 6.5 GW in FY2018 to 8.2 GW in FY2021 and solar power capacity has increased from 15.9 GW in FY2018 to 27.9 GW in FY2021. Additionally, thermoset plastics are heavily utilized for tanks, corrosion-resistant pipes, and insulation materials in the oil and refinery industries. As Japan continues to invest in infrastructure development and modernization of its oil and refinery facilities the demand for thermoset materials is expected to rise. Also, thermoset polymers are preferred within the maritime and aviation sectors because of their high strength-to-weight ratio and resistance to corrosion. Japan is predicted to become a maritime and aerospace-focused nation, which will increase demand for thermoset composites in shipbuilding, aircraft interiors, and structural components.

For instance, Daicel Corporation and Polyplastics Co., Ltd. partnered together to innovative thermoset plastic products with improved mechanical strength, flame retardancy, and heat resistance. The collaboration helps strengthen the companies’ competitive positions and differentiation in thermoset plastics market through technological leadership and product innovation, which will enhance their competitive standing in the thermoset plastics industry by means of technological leadership and product innovation.

Similarly, Microwave Chemical Co., Ltd. and Mitsui Chemicals Inc. are creating chemical recycling technology that can lower CO2 emissions and increase the energy efficiency of existing chemical operations using microwaves. The firm is engaged in the chemical recycling of plastics, including thermosetting sheet molding compound, flexible polyurethane foam, and waste from car shredders. Both businesses want to begin demonstration testing shortly following verification testing at a bench facility since early tests have yielded encouraging findings. The objective is to transform difficult plastic waste streams into premium materials that won’t sacrifice quality and are appropriate for delicate applications.

Report Scope

“Japan Thermoset Plastics Market Assessment, Opportunities and Forecast, FY2018-FY2032F”, is a comprehensive report by Markets and Data, that provides an in-depth analysis and qualitative and quantitative assessment of the current state of Japan thermoset plastics market, industry dynamics, and challenges. The report includes market size, segmental shares, growth trends, opportunities, and forecast between FY2025 and FY2032. Additionally, the report profiles the leading players in the industry, mentioning their respective market share, business model, competitive intelligence, etc.

Click here for full report- https://www.marketsandata.com/industry-reports/japan-thermoset-plastics-market

Latest reports-

Contact

Mr. Vivek Gupta 5741 Cleveland street, Suite 120, VA beach, VA, USA 23462 Tel: +1 (757) 343–3258 Email: [email protected] Website: https://www.marketsandata.com

0 notes

Text

Automotive Seat Frame market size is expected to be USD 15.65 Billion in 2030

The Automotive Seat Frame market is expected to grow from USD 11.74 Billion in 2024 to USD 15.65 Billion by 2030, at a CAGR of 4.90% during the forecast period.

The automotive seat frame market plays a crucial role in the overall vehicle manufacturing process, as it directly impacts comfort, safety, and design aesthetics. Seat frames are integral to supporting the structure of seats, ensuring durability, and enhancing passenger safety in different driving conditions. The market is driven by advancements in lightweight materials, ergonomic designs, and evolving regulations in vehicle safety.

Automotive seat frames integrated with sensors for temperature control, posture adjustments, and weight distribution are gaining traction. These innovations enhance the passenger experience and align with the trend toward smart vehicles. Manufacturers are exploring eco-friendly materials and processes to produce seat frames, reducing their carbon footprint. Recycling and using biodegradable materials are emerging as key trends in the market. The market is witnessing a shift toward customizable and modular seat frame designs to cater to varying consumer preferences and vehicle types. This trend is particularly prevalent in luxury and premium vehicles.

For More Insights into the Market, Request a Sample of this Report: https://www.reportprime.com/enquiry/sample-report/19897

Key Market Drivers

Increasing Vehicle Production The growing automotive sector, driven by the rising global demand for passenger and commercial vehicles, directly influences the need for advanced seat frame solutions. Emerging economies, in particular, are witnessing a surge in vehicle production, further boosting the market.

Demand for Lightweight Materials Lightweight seat frames made from materials like aluminum alloys and high-strength steel are gaining popularity as automotive manufacturers aim to improve fuel efficiency and reduce vehicle emissions. The shift toward electric vehicles (EVs) has also amplified the need for weight reduction, making lightweight seat frames a preferred choice.

Focus on Safety and Comfort Modern consumers prioritize safety and comfort, leading to innovations in seat frame designs. Features such as impact absorption, adjustable mechanisms, and ergonomic support are becoming standard requirements, pushing manufacturers to adopt cutting-edge technologies.

Growth of Electric Vehicles The increasing adoption of EVs has opened new opportunities in the market. Seat frame designs are evolving to accommodate the unique interiors and battery placement of electric vehicles.

Regional Analysis

The Asia-Pacific region dominates the automotive seat frame market, fueled by the high volume of vehicle production in countries like China, India, and Japan. Affordable labor and the presence of key manufacturers also contribute to the region’s leadership. North America remains a significant market due to its strong focus on innovation, advanced vehicle safety standards, and increasing adoption of EVs. Europe is driven by stringent emission regulations and a high demand for premium and luxury vehicles, encouraging advancements in lightweight and ergonomic seat frame designs.

Challenges

High Costs of Advanced Materials The use of lightweight and durable materials like carbon fiber increases manufacturing costs, making it challenging for manufacturers to maintain competitive pricing.

Supply Chain Disruptions Geopolitical tensions, raw material shortages, and logistical challenges have impacted the production and supply of automotive seat frames.

Balancing Comfort and Safety While innovation drives the market, achieving a balance between safety standards, comfort, and cost-effectiveness remains a challenge for manufacturers.

Get Full Access of This Premium Report: https://www.reportprime.com/checkout?id=19897&price=3590

Market Segmentations

By Type: Traditional Material, Magnesium Alloy, Other New Material

By Applications: Passenger Vehicle, Commercial Vehicle

Competitive Landscape

The automotive seat frame market features key players such as Faurecia, Toyota Boshoku, Johnson Controls, Magna, Camaco-Amvian, Lear, Brose, HYUNDAI DYMOS, TS TECH, Futuris Group, HANIL E-HWA, SI-TECH Dongchang, XuYang Group. These companies focus on research and development to stay competitive, leveraging technologies like 3D printing and advanced welding techniques.

Future Outlook

The automotive seat frame market is poised for significant growth, driven by advancements in materials, designs, and manufacturing processes. The shift toward EVs and smart vehicles will continue to create opportunities for innovation. Sustainability and customization will remain key focus areas, ensuring that manufacturers meet evolving consumer demands.

As the automotive industry embraces change, the seat frame market is set to play a pivotal role in shaping vehicle interiors of the future.

0 notes

Text

Composites Market: Analysis of Growth Drivers, Challenges, and Future Scope

The Composites Market has emerged as a key segment in global materials science, driven by increasing demand for lightweight, durable, and high-performance materials across diverse industries such as aerospace, automotive, construction, renewable energy, and consumer goods. Composites, made from fibers and resins, offer superior strength-to-weight ratios, corrosion resistance, and design flexibility, making them ideal for advanced applications.

Market Overview

The global composites market size was USD 99.91 billion in 2019 and is projected to reach USD 112.0 billion by 2027, exhibiting a CAGR of 6.88% during the forecast period. This growth is fueled by rising adoption in the aerospace and automotive sectors, innovations in renewable energy systems, and an increasing focus on sustainable materials.

Key Market Drivers

Lightweight Materials in Automotive and Aerospace

The growing demand for fuel efficiency and emission reduction has accelerated the adoption of lightweight composite materials in automotive and aerospace manufacturing.

Rising Use in Wind Energy

Wind turbines, particularly blades, rely on composite materials for their strength and weight-saving properties. The growth of renewable energy installations globally is a significant driver.

Infrastructure and Construction Applications

Composites are being increasingly used in construction for bridges, reinforcement, panels, and cladding due to their durability and resistance to environmental stressors.

Technological Advancements in Manufacturing

Innovations in production techniques such as 3D printing, automated fiber placement (AFP), and resin transfer molding (RTM) are enhancing the quality and cost-efficiency of composite manufacturing.

Focus on Sustainability

The development of bio-based and recyclable composites aligns with the growing push for environmentally sustainable materials.

Get a Free Sample PDF- https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/composites-market-102295

Market Segmentation

By Fiber Type

Glass Fiber Composites: Cost-effective and versatile, widely used in construction, automotive, and consumer goods.

Carbon Fiber Composites: High-strength, lightweight materials primarily used in aerospace, automotive, and sports applications.

Natural Fiber Composites: Emerging segment driven by sustainability trends and eco-friendly solutions.

By Resin Type

Thermoset Composites: Dominant due to their high strength and durability, used in aerospace and wind energy.

Thermoplastic Composites: Gaining traction for recyclability and faster processing times.

By End-Use Industry

Aerospace & Defense: The largest consumer of high-performance composites for structural applications.

Automotive: Increasing use for reducing vehicle weight and improving fuel efficiency.

Renewable Energy: Wind turbine blades and solar panel frames rely heavily on composites.

Construction & Infrastructure: Composites are used for corrosion-resistant and durable structures.

Consumer Goods: Sports equipment, electronics, and household products benefit from lightweight properties

By Region

North America: Leading market with significant aerospace and automotive production hubs.

Europe: Driven by stringent regulations promoting lightweight and energy-efficient materials.

Asia-Pacific: Fastest-growing region due to rising industrialization, construction, and manufacturing in China, India, and Japan.

Rest of the World: Moderate growth driven by infrastructure and renewable energy projects.

Key Challenges

High Production Costs

The cost of advanced fibers (e.g., carbon fiber) and specialized manufacturing techniques limits widespread adoption.

Recycling Limitations

Thermoset composites are difficult to recycle, posing challenges for sustainability.

Competition from Traditional Materials

Steel, aluminum, and other metals continue to compete with composites due to established infrastructure and lower costs.

Lack of Standardization

The absence of global standards for composite materials and processes can hinder market penetration.

Emerging Trends

Recyclable and Bio-Based Composites

Growing innovation in natural and bio-based resins is addressing sustainability challenges.

3D Printing and Additive Manufacturing

The integration of 3D printing technologies allows for customized and complex composite structures with reduced material waste.

Composites in Electric Vehicles (EVs)

The growing EV market is driving demand for lightweight composites in battery enclosures, body panels, and structural parts.

Advanced Composite Applications in Construction

Use of composites for bridge decks, reinforcing bars, and high-rise building panels is expanding.

Automated Manufacturing

Innovations in automation, including robotic systems for fiber placement and resin infusion, are increasing production efficiency.

Competitive Landscape

The composites market is characterized by intense competition, with key global players focusing on innovation, capacity expansion, and strategic partnerships. Notable companies include:

Toray Industries, Inc.

Hexcel Corporation

SGL Carbon SE

Owens Corning

Teijin Limited

Mitsubishi Chemical Holdings

Solvay S.A.

Huntsman Corporation

These players invest in research and development to create advanced, cost-effective, sustainable composite solutions.

Get More Info- https://www.fortunebusinessinsights.com/composites-market-102295

Future Outlook

The global composites market is poised for strong growth over the next decade, driven by increasing aerospace, automotive, renewable energy, and construction applications. The Asia-Pacific region is expected to dominate the market, while North America and Europe remain at the forefront of innovation and high-value applications. Sustainability and the adoption of advanced manufacturing technologies will play a critical role in shaping the market’s future.

Conclusion

The composites market represents a transformative segment in materials science, offering unparalleled strength, flexibility, and sustainability for diverse industries. As demand for lightweight and high-performance materials continues to grow, composites will remain central to innovation in aerospace, automotive, and renewable energy sectors. Companies that embrace advancements in technology and sustainable solutions are well-positioned to capitalize on the market's expanding opportunities.

0 notes

Text

Global Wood Plastic Composite Market Size & Industry Analysis (2024-2032)

The global wood plastic composite market size was USD 4.77 billion in 2019 and is projected to reach USD 9.03 billion by 2027, exhibiting a CAGR of 8.57% during the forecast period.

According to a research report by Fortune Business Insights™ the global wood plastic composites market is likely to gain impetus from their increasing application in kitchen accessories, home furniture, vehicle interiors, and car speakers. They are considered to be the highest growing plastic additives at present. This information is given by Fortune Business Insights™ in a recently published report, titled, “Wood Plastic Composites Market Size, Share & Industry Analysis and Regional Forecast, 2024-2032.”

Lists of all the manufacturers of wood plastic composites present in the market

Trex Company, Inc. (U.S.)

Seven Trust (China)

Meghmani Group (India)

Beologic (Belgium)

UFP Industries, Inc. (U.S.)

Fiberon LLC (U.S.)

Axion International, Inc. (U.S.)

Josef Ehrler GmbH & Co KG (Germany)

Croda International Plc (UK)

CertainTeed (U.S.)

Others

Drivers & Restraints-

Increasing Usage of Sustainable Fibers to Boost Growth

Wood plastic composites are green materials that have high potential in bringing about sustainability. They don’t contain excessive chemicals that may pose toxic for the environment and are durable in nature. Plant-based fibers are mainly used in reinforced plastics, instead of fibrous materials as they are cost effective, robust, highly stiff, and annually renewable. Such fibers also emit less carbon dioxide, have low density, and possess biodegradability properties. Numerous automakers worldwide are aiming to develop biodegradable or recyclable parts of vehicles by using sustainable wood plastic composites. They would aid in lowering fuel consumption and production cost, offering shatterproof performance under harsh weather conditions, enhance passenger safety, lower weight of the material, and improve acoustic performance. However, wood plastic composites require higher initial cost spending. It may obstruct growth.

Segment-

The WPC market can be segmented based on product type and application

a. By Product Type

Polyethylene (PE)-based WPC: This segment dominates the market due to its low cost and high durability. PE-based WPC is widely used in decking, siding, and fencing applications.

Polypropylene (PP)-based WPC: Known for its enhanced mechanical properties, PP-based WPC is mainly used in automotive and construction applications.

Polyvinyl Chloride (PVC)-based WPC: PVC-based WPC is favored for its high resistance to moisture and termites, making it ideal for exterior applications like cladding and windows.

Others (ABS, PLA, etc.): These are emerging materials in niche applications due to their unique properties, including recyclability and higher performance.

b. By Application

Building and Construction: This is the largest segment, accounting for over 70% of the total market share in 2023. WPC products are extensively used in decking, railings, windows, doors, and structural components.

Automotive: WPC is increasingly being adopted in the automotive sector for interior components like dashboards, trims, and door panels due to its lightweight, high strength, and ability to reduce vehicle weight.

Consumer Goods: This segment includes the use of WPC in the production of furniture, home décor items, and household accessories.

Others: Packaging and electronics are smaller but growing segments as companies explore the use of WPC materials for sustainable packaging and casings.

Challenges

Higher Initial Costs: WPC products are more expensive upfront than traditional wood materials, which may hinder their adoption in cost-sensitive markets.

Limited Awareness: In some regions, the knowledge about the benefits and applications of WPC remains limited, slowing down market penetration.

Opportunities

R&D and Innovation: Companies are investing in research and development to create advanced WPC products with enhanced performance properties, including better weather resistance, flexibility, and recyclability.

Recyclable and Bio-based WPC: The trend toward using bio-based polymers and fully recyclable materials is expected to open new opportunities for growth in the WPC market.

Regional Analysis-

Rapid Industrialization in China & India to Favor Growth in Asia Pacific

In terms of region, North America procured USD 2.24 billion revenue in 2019 stocked by the rising demand for environmentally-friendly solutions and products in this region. In addition to this, the rising application of wood plastic composites in decking would drive growth. In Asia Pacific, developing countries, such as China and India are experiencing rapid industrialization. Coupled with this, the improvements and modernizations in buildings and road construction activities would accelerate growth in this region. The Middle East and Africa and Latin America are set to exhibit steady growth fueled by the surging number of construction activities in both regions.

Get More Information: https://www.fortunebusinessinsights.com/wood-plastic-composite-market-102821

Competitive Landscape-

Key Companies Follow Acquisition Strategy to Gain Competitive Edge

The wood plastic composites market is fragmented with the presence of more than 100 organizations accounting for the total revenue across the globe. They are constantly investing huge sums in research and development activities to innovate their in-house wood plastic composites. Some of them are also adopting the strategy of mergers and acquisitions to enhance their product offerings. Below are a couple of the latest industry developments:

August 2018: Alvic Plastics Limited was acquired by BSW Group. This new deal would aid BSW in broadening its product portfolio and production capacity. It would also enable the company to bring in diversification to increase its range of products.

November 2015: Vannplastic Limited, a prominent manufacturer of wood plastic composite was acquired by the Boral Epwin Group for an initial consideration of approximately USD 5.67 million. It would aid Boral in widening its line of low maintenance building materials.

0 notes

Text

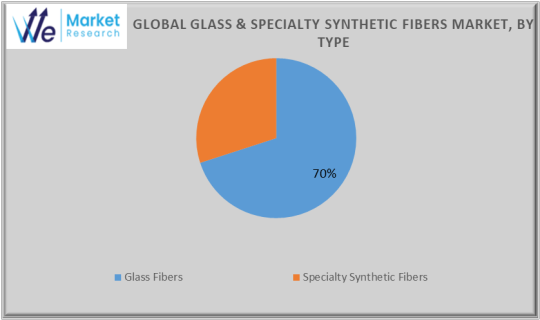

Glass Fibers & Specialty Synthetic Fibers Market Challenges, Analysis and Forecast to 2034

The Glass Fibers & Specialty Synthetic Fibers Market is a dynamic segment within the materials industry, driven by the increasing demand for lightweight, durable, and high-performance materials across various sectors. These fibers are engineered for applications that require superior mechanical properties, thermal stability, and resistance to environmental factors

The market for glass fiber and specialty synthetic fibers is expected to increase at a compound annual growth rate (CAGR) of 6.4% between 2024 and 2034. According to an average growth trend, the market is expected to reach USD 144.58 billion in 2034. The global market for glass fibers and specialty synthetic fibers is expected to generate USD 85.59 billion by 2024.

Get a Sample Copy of Report, Click Here: https://wemarketresearch.com/reports/request-free-sample-pdf/glass-and-specialty-synthetic-fibers-market/1603

Glass Fibers & Specialty Synthetic Fibers Market Growth Drivers

Urbanization and Infrastructure Growth:

Increasing investments in construction and urban development drive demand for glass fibers.

Rising Defense Budgets:

Governments worldwide are increasing investments in protective equipment using synthetic fibers.

Shift Toward Renewable Energy:

Wind energy projects favor glass fibers for turbine blades.

Advancements in Material Engineering:

Innovations are improving the properties and reducing production costs of synthetic fibers.

Specialty Synthetic Fibers: Types

Aramid Fibers:

Examples: Kevlar, Twaron.

High tensile strength and resistance to impact and heat.

Used in bulletproof vests, fire-resistant clothing, and ropes.

Carbon Fibers:

Lightweight and exceptionally strong.

Applications: Aerospace, sports equipment, automotive (luxury cars).

Ultra-High-Molecular-Weight Polyethylene (UHMWPE):

Examples: Dyneema, Spectra.

Extremely lightweight with high impact resistance.

Used in personal armor, fishing lines, and medical implants.

Polybenzimidazole (PBI):

High thermal and chemical stability.

Used in firefighting gear and aerospace insulation.

Polyimide Fibers:

Heat-resistant fibers ideal for use in high-temperature industrial applications.

Glass Fibers & Specialty Synthetic Fibers Market Challenges

High Costs of Specialty Fibers:

The manufacturing process for carbon and aramid fibers is resource-intensive.

Environmental Impact:

Synthetic fibers contribute to pollution if not recycled properly.

Competition from Emerging Materials:

Natural fibers like hemp and bamboo, as well as metal composites, are gaining attention.

Emerging Trends

Integration with Smart Technologies:

Development of fibers with embedded sensors for structural health monitoring.

Circular Economy Initiatives:

Companies are investing in recycling technologies for glass and synthetic fibers.

Hybrid Materials:

Combining glass and synthetic fibers to create composites with enhanced properties.

Glass Fibers & Specialty Synthetic Fibers Market Segmentation,

By Type

Glass Fibers

E-Glass

S-Glass

C-Glass

Others

Specialty Synthetic Fibers

Polyester

Nylon

Aramid

Carbon Fibers

Polypropylene (PP)

Others

By Application

Textile

Construction

Automotive

Aerospace & Defense

Marine

Consumer Goods

Packaging

Wind Energy

Others

Key companies profiled in this research study are,

The Global Glass Fibers & Specialty Synthetic Fibers Market is dominated by a few large companies, such as

Owens Corning

Jushi Group

PPG Industries

Saint-Gobain

China National Glass Industrial Group Corporation (CNG)

Nippon Electric Glass Co., Ltd.

Sika AG

DuPont

Solvay

Teijin Limited

Hyosung Corporation

Toray Industries

DSM (Dutch State Mines)

BASF

Asahi Kasei Corporation

Others

Glass Fibers & Specialty Synthetic Fibers Industry: Regional Analysis

Forecast for the North American market

North America will be a significant player in the glass fiber and specialized synthetic fiber industries, accounting for about 40% of the worldwide market in 2023. Due to its technological dominance and strong industrial base in the automotive, aerospace, and defense sectors, North America has a disproportionate amount. North America, particularly the United States, is a major market for glass fibers and specialty synthetic fibers.

Forecast for the European Market

Europe is an essential market for glass and specialty synthetic fibers due to the prevalence of the automobile and aerospace industries there. Countries like Germany, France, and the UK are investing in lightweight materials for cars and airplanes, which directly increases demand for fibers like glass and carbon fibers. The European Union's focus on sustainability and energy efficiency has led to a greater usage of advanced materials, such as carbon fibers for renewable energy applications like wind turbines and glass fibers for construction. Europe is the hub for research and development, particularly in the areas of lightweight composite materials and high-performance fibers for industrial applications.

Forecasts for the Asia Pacific Market

The growth of the Chinese, Japanese, and Indian industries is primarily responsible for the Asia-Pacific region's sharp increase in demand for glass fibers and specialty synthetic fibers. Particularly in countries like China, India, and Japan, the Asia-Pacific region is fast become increasingly urbanized and industrialized. This is driving the demand for glass fibers in the automotive, infrastructure construction, and building industries. The need for lightweight materials is rising in the Asia-Pacific automotive industry as a result of the rising popularity of electric vehicles (EVs) and fuel-efficient cars in countries like China and Japan. The need for glass and carbon fibers rises as a result.

Conclusion

The Glass Fibers & Specialty Synthetic Fibers Market is poised for robust growth, driven by advancements in material science, the increasing demand for lightweight and high-strength materials, and expanding applications across industries like construction, automotive, aerospace, and renewable energy. While challenges such as high production costs and environmental concerns persist, ongoing innovations in recycling and sustainable fiber production are paving the way for a greener future.

As industries worldwide prioritize efficiency, durability, and sustainability, the market for glass and specialty synthetic fibers is set to play a critical role in shaping the future of materials technology. With strong investments in R&D and the rise of eco-friendly initiatives, this market presents vast opportunities for growth and innovation.

0 notes

Text

Carpet Tile Market Forecast: Trends and Projections for the Future

The carpet tile market has been experiencing robust growth over the past few years, fueled by the increasing demand for flexible, sustainable, and easy-to-maintain flooring solutions. With diverse applications across both residential and commercial sectors, carpet tiles have become a popular choice for interior design projects. As consumer preferences evolve and sustainability becomes a key focus, the carpet tile market is expected to continue growing in the coming years. This article provides a detailed forecast of the carpet tile market, analyzing key trends, growth drivers, and challenges, while also highlighting the anticipated future trajectory of the market.

Market Overview

Carpet tiles, also known as modular carpets, consist of square or rectangular sections of carpet designed for easy installation and replacement. They offer flexibility in design and are suitable for a wide range of environments, from homes and offices to hospitality and retail spaces. The global carpet tile market is expected to grow steadily, with an anticipated compound annual growth rate (CAGR) of around 4-5% over the next few years. This growth is driven by the increasing demand for flooring solutions that are both practical and aesthetically pleasing.

The commercial real estate sector, in particular, is a key contributor to the growth of the carpet tile market. Offices, hotels, hospitals, and retail outlets are increasingly adopting carpet tiles for their cost-effectiveness, durability, and ease of maintenance. Additionally, the growing trend of flexible office spaces and the need for quick installation have further enhanced the appeal of carpet tiles.

Key Market Trends

Sustainability and Eco-Friendly Products

One of the most significant trends influencing the carpet tile market is the growing demand for sustainable products. With environmental concerns at the forefront, consumers and businesses are increasingly seeking eco-friendly alternatives to traditional flooring options. Carpet tile manufacturers are responding by integrating recycled materials, such as PET (polyethylene terephthalate) from plastic bottles, and bio-based fibers into their products.

Additionally, the rising popularity of green building certifications, such as LEED (Leadership in Energy and Environmental Design), is driving the demand for sustainable flooring solutions. Manufacturers are also focusing on reducing the carbon footprint during production processes and creating carpet tiles that are 100% recyclable at the end of their lifecycle. These trends are expected to continue shaping the carpet tile market in the forecast period, with sustainable products gaining a larger market share.

Customization and Design Flexibility

Carpet tiles offer greater design flexibility compared to traditional broadloom carpets, which is another driving factor in their popularity. The ability to mix and match colors, patterns, and textures enables consumers to create unique, personalized flooring solutions that meet their aesthetic and functional needs. This customization feature is especially appealing to commercial spaces such as offices, retail stores, and hospitality venues that require flooring solutions that align with their brand identity and design vision.

Incorporating modular tiles with different sizes, shapes, and textures also allows for easy layout modifications and the possibility of creating more dynamic, creative flooring schemes. As businesses and consumers continue to seek flooring solutions that provide flexibility and personalization, the demand for carpet tiles is expected to rise.

Technological Advancements in Manufacturing

Technological innovations in the manufacturing of carpet tiles are playing a crucial role in shaping the future of the market. Advances in production processes, such as improved dyeing techniques and the use of digital printing technologies, are making it easier for manufacturers to produce high-quality carpet tiles in a variety of designs, colors, and textures.

Additionally, developments in backing materials have improved the performance of carpet tiles, enhancing their durability, slip resistance, and ease of maintenance. These technological advancements are expected to drive the carpet tile market forward, offering consumers more choices and improving the overall appeal of carpet tiles as a flooring option.

Growth Drivers

Rise in Commercial Construction

The commercial real estate sector remains the largest contributor to the growth of the carpet tile market. As the demand for office spaces, hospitality venues, and retail outlets increases, so does the need for cost-effective and durable flooring solutions. Carpet tiles, with their easy installation and maintenance, are particularly appealing to the commercial sector. The rise of flexible and collaborative workspaces further boosts the demand for carpet tiles, as they offer the versatility required for evolving office designs.

Urbanization and Infrastructure Development