#Raw material suppliers Market Research Report

Text

Commercial Oven Market:Market Analysis 2023| Recorded Hyper Growth in the Future – 2030- Claims Allied Market Research.

The commercial oven market is experiencing significant growth and will grow exponentially in the coming years. Commercial oven is providing features like baking, grilling and reheating. It is preferred in various restaurants and hotels because food is prepared in large quantities. Manufacturers are taking proper care of energy conservation, energy saver because the consumers are demanding that oven from which they can save the cost of electricity. The demand for commercial oven has increased due to the high preference for food made in the oven. The commercial oven is designed in such a way that it can be only used in commercial places, not in households because of its heavy material. It can be used for a full day and can hold electric power to reduce the effects of shocks.

Request To Sample :- https://www.alliedmarketresearch.com/request-toc-and-sample/9772

COVID-19 ScenarioAnalysis:

COVID-19 pandemic has severely affected the commercial oven market. The supply of commercial oven is being stopped because China is the main supplier of this industry wherein raw material and finished products are imported. The electronic industry is facing issues like production, supply, and increase of prices. If the trade barriers remain the same, then it can increase the prices of commercial oven, which will further lead to a decrease in the sale of the commercial oven.

Top Impacting Factors: Market Scenario Analysis, Trends, Drivers andImpact Analysis

The demand for commercial ovens is increased in restaurants, hotels, and bakeries because of the taste preferences of the customer decline from traditional food. The increase in the consumption of pizzas, burgers, and pastries, has increased the requirement of ovens. The growing increase in the employment level, increase in disposable income, and change in living standards have increased the growth of the global commercial market. With the rise in the trend of working women, they can contribute less time in the kitchen, and mostly depend on restaurants, hotels, and bakeries for food.

Request To Customization:- https://www.alliedmarketresearch.com/request-for-customization/9772

As they have to order, and they get their meal at their doorstep. The main contribution of increase the demand for the commercial oven is from online platformssuch as Zomato and Swiggy, wherein food can be ordered and the consumer can also get discounts, which has contributed to the growth of the commercial oven market. The commercial oven is segmented into different types of grillers, convection oven, and solo oven. Conventional oven is used for the heating purpose in which heat is equally distributed inside the oven and is mostly used in the restaurants and bakeries. Whereas solo oven used for boiling purpose in which baking and grilling is not possible. So, the different hotels according to their requirement of preparing the food, prefer different types of oven.

North America holds the highest revenue share in the commercial oven market owing to high demand for technology according to the preference of the customer. These countries can spend on these items. China is one of the major suppliers of the commercial oven because of the affordable raw material and finished product. China is scanning the market and checking the taste and preferences of the customer. Technology up-gradation is one of the major tools, which increases the demand for commercial oven.

LIMITED-TIME OFFER – Buy Now & Get Exclusive 15 % Discount on this Report @ https://www.alliedmarketresearch.com/checkout-final/bb5f5360b18b82e7cea62961b2e73a64

Key Benefits of the Report:

This study presents the analytical depiction of the commercial oven market along with the current trends and future estimations to determine the imminent investment pockets.

The report presents information related to key drivers, restraints, and opportunities along with detailed analysis of the commercial oven market share.

The current market is quantitatively analyzed to highlight the Commercial Oven Market growth scenario.

Porter’s five forces analysis illustrates the potency of buyers & suppliers in the market.

The report provides a detailed global thermistor market analysis based on competitive intensity and how the competition will take shape in coming years.

About Us:-

Allied Market Research (AMR) is a full-service market research and business-consulting wing of Allied Analytics LLP based in Portland, Oregon. Allied Market Research provides global enterprises as well as medium and small businesses with unmatched quality of "Market Research Reports" and "Business Intelligence Solutions." AMR has a targeted view to provide business insights and consulting to assist its clients to make strategic business decisions and achieve sustainable growth in their respective market domain.

Pawan Kumar, the CEO of Allied Market Research, is leading the organization toward providing high-quality data and insights. We are in professional corporate relations with various companies and this helps us in digging out market data that helps us generate accurate research data tables and confirms utmost accuracy in our market forecasting. Each and every data presented in the reports published by us is extracted through primary interviews with top officials from leading companies of domain concerned. Our secondary data procurement methodology includes deep online and offline research and discussion with knowledgeable professionals and analysts in the industry.

Contact:

David Correa

5933 NE Win Sivers Drive

#205, Portland, OR 97220

United States

USA/Canada (Toll Free):

+1-800-792-5285, +1-503-894-6022

UK: +44-845-528-1300

Hong Kong: +852-301-84916

India (Pune): +91-20-66346060

Fax: +1(855)550-5975

[email protected]

Web: www.alliedmarketresearch.com

Allied Market Research Blog: https://blog.alliedmarketresearch.com

Follow Us on | Facebook | LinkedIn | YouTube |

2 notes

·

View notes

Text

Rising Power Consumption to Drive the Portable Power Station Market

Triton Market Research presents the Global Portable Power Station Market report segmented by Power Source Type (Solar Power, Direct Power), by Usage Type (Off-Grid Power, Emergency Power, Other Usage Types), by Capacity Range (Below 500 Wh, 501-1500 Wh, Above 1500 Wh), by Battery Type (Sealed Lead-Acid Batteries, Lithium-Ion Batteries), by Geographical Region (North America, Europe, Middle East and Africa, Asia-Pacific, Latin America), discussing Market Summary, Industry Outlook, Market Drivers, Market Challenges, Market Opportunities, Competitive Landscape, Research Methodology & Scope, and Global Market Size, Forecast, & Analysis (2022-2028).

According to the report by Triton Market Research, the Global Portable Power Station Market is likely to develop with a CAGR of 5.6% during the forecast years from 2022 to 2028.

Request Free sample:

https://www.tritonmarketresearch.com/reports/portable-power-station-market#request-free-sample

Portable power stations offer distinct benefits over conventional generators, such as, they do not require the use of fuel, propane, or kerosene to function. This saves the costs and efforts on engine maintenance, thus making portable power stations more preferable for usage. Also, they are compact in size, which offers convenience and ease of carrying. Owing to numerous such advantages, the global market is anticipated to witness notable growth in the years to come.

However, the high price of battery-operated portable power stations and the long charging times taken by solar-powered portable power stations are likely to hamper the market’s development.

North America leads the global market for portable power stations, and held the largest revenue share in 2021. According to statistics from the North American Camping Report 2021, the number of households participating in camping activities reached nearly 48.2 million in 2020. This surge in camping activities, such as fishing, trekking, hiking, and climbing, across the region, has boosted the adoption of portable power stations to ensure continuous power supply to people whilst outdoors.

Suaoki, Duracell Inc, Goal Zero, Lion Energy LLC, Scott Electric, Bluetti, Anker Technology, Shenzhen Chafon Technology Co Ltd, Chargetech, Hyundai Power Products, EcoFlow, Drow Enterprises Co Ltd, AllPowers Industrial International Co Ltd, Jackery Inc, and Midland Radio Corporation are some of the notable players in the portable power station market.

The portable power station market has a diverse and evolving ecosystem. The key stakeholders include raw material providers, manufacturers, and suppliers. Raw material and component manufacturers supply various materials and components to product manufacturers, who then use them to design and manufacture the final products. These products are then supplied to end-users via different mediums, including direct sales via company distributors and third-party sales via third-party distributors.

Contact Us:

Phone: +44 7441 911839

#Portable Power Station Market#Portable Power Station#energy industry#power industry#market research report#market research reports#triton market research

2 notes

·

View notes

Text

Portable Garage Fan Market Size,Volume,Revenue Trends Analysis Report 2024-2030

Global Info Research announces the release of the report “Global Portable Garage Fan Market 2024 by Manufacturers, Regions, Type and Application, Forecast to 2030” . This report provides a detailed overview of the market scenario, including a thorough analysis of the market size, sales quantity, average price, revenue, gross margin and market share.The report provides an in-depth analysis of the competitive landscape, manufacturer’s profiles,regional and national market dynamics, and the opportunities and challenge that the market may be exposed to in the near future. Global Portable Garage Fan market research report is a comprehensive analysis of the current market trends, future prospects, and other pivotal factors that drive the market.

Portable garage fans refer to those fan products that are compact in design, small in size, light in weight or equipped with wheels for easy movement, and can provide effective ventilation and cooling functions in spaces such as garages.

According to our (Global Info Research) latest study, the global Portable Garage Fan market size was valued at US$ million in 2023 and is forecast to a readjusted size of USD million by 2030 with a CAGR of %during review period.

This report is a detailed and comprehensive analysis for global Portable Garage Fan market. Both quantitative and qualitative analyses are presented by manufacturers, by region & country, by Type and by Application. As the market is constantly changing, this report explores the competition, supply and demand trends, as well as key factors that contribute to its changing demands across many markets. Company profiles and product examples of selected competitors, along with market share estimates of some of the selected leaders for the year 2024, are provided.

Market Segmentation

Portable Garage Fan market is split by Type and by Application. For the period 2019-2029, the growth among segments provides accurate calculations and forecasts for consumption value by Type, and by Application in terms of volume and value.

Market segment by Type: Battery-powered Fan、Plug-in Fan、Rechargeable Fan

Market segment by Application:Commercial、Home

Major players covered: EGO POWER+、MULE、Tornado、Lasko、DeWalt、Pelonis、Air King、Maxx、Mounto、Milwaukee、Shark

The content of the study subjects, includes a total of 15 chapters:

Chapter 1, to describe Portable Garage Fan product scope, market overview, market estimation caveats and base year.

Chapter 2, to profile the top manufacturers of Portable Garage Fan, with price, sales, revenue and global market share of Portable Garage Fan from 2019 to 2024.

Chapter 3, the Portable Garage Fan competitive situation, sales quantity, revenue and global market share of top manufacturers are analyzed emphatically by landscape contrast.

Chapter 4, the Portable Garage Fan breakdown data are shown at the regional level, to show the sales quantity, consumption value and growth by regions, from 2019 to 2030.

Chapter 5 and 6, to segment the sales by Type and application, with sales market share and growth rate by type, application, from 2019 to 2030.

Chapter 7, 8, 9, 10 and 11, to break the sales data at the country level, with sales quantity, consumption value and market share for key countries in the world, from 2017 to 2023.and Portable Garage Fan market forecast, by regions, type and application, with sales and revenue, from 2025 to 2030.

Chapter 12, market dynamics, drivers, restraints, trends and Porters Five Forces analysis.

Chapter 13, the key raw materials and key suppliers, and industry chain of Portable Garage Fan.

Chapter 14 and 15, to describe Portable Garage Fan sales channel, distributors, customers, research findings and conclusion.

Our Market Research Advantages:

Global Perspective: Our research team has a strong understanding of the company in the global Portable Garage Fan market.Which offers pragmatic data to the company.

Aim And Strategy: Accelerate your business integration, provide professional market strategic plans, and promote the rapid development of enterprises.

Innovative Analytics: We have the most comprehensive database of resources , provide the largest market segments and business information.

About Us:

Global Info Research is a company that digs deep into global industry information to support enterprises with market strategies and in-depth market development analysis reports. We provide market information consulting services in the global region to support enterprise strategic planning and official information reporting, and focuses on customized research, management consulting, IPO consulting, industry chain research, database and top industry services. At the same time, Global Info Research is also a report publisher, a customer and an interest-based suppliers, and is trusted by more than 30,000 companies around the world. We will always carry out all aspects of our business with excellent expertise and experience.

0 notes

Text

Understanding the Industrial Lubricants Industry: Trends and Insights

Introduction

The industrial lubricants industry plays a crucial role in the smooth operation of machinery across various sectors, from manufacturing to automotive. These lubricants are essential for reducing friction, minimizing wear and tear, and improving the overall efficiency of equipment. In this blog, we’ll explore the key trends, market drivers, challenges, and future outlook for the industrial lubricants market.

Market Overview

The Industrial Lubricants Market is estimated to be 22.07 billion liters in 2024 and is projected to reach 26.06 billion liters by 2029, growing at a CAGR of 3.38% during the forecast period from 2024 to 2029.

The global industrial lubricants market is experiencing steady growth, driven by several factors:

Increased Industrial Activities: As industries expand and modernize, the demand for high-quality lubricants to ensure optimal machinery performance is rising.

Technological Advancements: Innovations in lubricant formulations are leading to the development of high-performance products that offer enhanced protection and efficiency.

Regulatory Compliance: Stricter environmental regulations are prompting industries to shift towards eco-friendly lubricants, further driving market growth.

Key Trends

Shift to Bio-Based Lubricants: There is a growing preference for bio-based lubricants due to their environmental benefits. These products are derived from renewable sources and offer reduced toxicity.

Focus on Sustainability: Manufacturers are increasingly adopting sustainable practices in lubricant production, including recycling and waste reduction initiatives.

Integration of Smart Technologies: The incorporation of IoT and data analytics in lubrication management systems is improving predictive maintenance and operational efficiency.

Major Market Segments

By Product Type: The market is segmented into hydraulic fluids, metalworking fluids, general-purpose lubricants, and others. Each segment has its specific applications and benefits.

By End-User Industry: Key sectors include automotive, manufacturing, energy, and construction. Each sector has unique lubricant requirements based on operational conditions and machinery types.

Challenges Facing the Industry

Despite the growth potential, the industrial lubricants market faces several challenges:

Fluctuating Raw Material Prices: The prices of base oils and additives can be volatile, impacting production costs and pricing strategies.

Competition from Alternative Solutions: The emergence of non-lubrication technologies may pose a threat to traditional lubricants in certain applications.

Regulatory Hurdles: Navigating complex regulations concerning lubricant formulations and environmental standards can be challenging for manufacturers.

Future Outlook

The industrial lubricants market is expected to continue its growth trajectory in the coming years. With increasing industrialization, particularly in developing regions, and a growing emphasis on sustainability, the demand for innovative and high-performance lubricants will remain strong. Companies that invest in research and development, focus on eco-friendly solutions, and leverage smart technologies are likely to thrive in this evolving landscape.

Conclusion

The industrial lubricants industry is vital for ensuring the efficient operation of machinery across various sectors. By staying abreast of market trends and addressing emerging challenges, businesses can capitalize on the opportunities within this dynamic market. Whether you're a manufacturer, supplier, or end-user, understanding the intricacies of the industrial lubricants market will position you for success in the future.

For a detailed overview and more insights, you can refer to the full market research report by Mordor Intelligence

#industrial lubricants industry size#industrial lubricants industry share#industrial lubricants industry analysis

0 notes

Text

The Rise of Natural Ingredients Prompts Growth in the Beauty Supplements Market

The beauty supplements market consists of oral dietary supplements aimed at enhancing physical beauty by nourishing skin, hair, and nails from within. Beauty supplements contain vitamins, minerals, proteins, omega fatty acids, and other natural ingredients that are beneficial for overall health as well as skin, hair, and nail quality. They are available in the form of tablets, capsules, powders, soft gels and liquids. Beauty supplements offer several advantages over topical treatments like lotions and potions as they work from inside out to impart natural glow, strengthen hair follicles and improve skin elasticity. With rising health concerns, the demand for clean label products made from organic and natural ingredients is on the rise.

The Global Beauty Supplements Market is estimated to be valued at US$ 2979.84 Mn in 2024 and is expected to exhibit a CAGR of 5.5% over the forecast period between 2024 To 2031.

Key Takeaways

Key players operating in the Beauty Supplements market are Presto Geosystems, Polymer Group Inc., Strata Systems Inc., Armtec Infrastructure Inc., Maccaferri SPA, PRS Mediterranean Ltd., Maccaferri SPA, and Tensar International Ltd.

The Beauty Supplements Market Growth is witnessing high increasing demand for products with natural ingredients among health-conscious consumers. Various vitamins, minerals and antioxidant-rich supplements are gaining popularity for their ability to deliver results without any side effects.

The market is further strengthened by expansion of key players into international markets. Leading companies are focusing on geographic expansions and product launches catering to specific regional consumer needs to boost sales in foreign markets.

Market Key Trends

One of the key Beauty Supplements Market Size and Trends witnessed in the beauty supplements market is the rise of customized formulations. Manufactures are offering customized beauty supplements tailored to an individual's age, gender, skin and hair type. Through online consultations and diagnostic tests, they provide personalized recommendations and formulations targeted towards the unique nutritional needs of each consumer. This has increased customer stickiness and engagement with the brands.

Porter’s Analysis

Threat of new entrants: Dietary supplement industry has moderate barriers for new companies to enter due to regulations and capital requirements.

Bargaining power of buyers: Buyers have moderate bargaining power due to availability of substitutes and differentiation in products.

Bargaining power of suppliers: Suppliers have moderate bargaining power as raw materials for supplements are commoditized.

Threat of new substitutes: Threat of substitutes is moderate as new product innovations can disrupt the market.

Competitive rivalry: Industry faces high competition due to several large players.

Geographical Regions

North America currently dominates the beauty supplements market in terms of value, with the United States being the major contributor. Factors such as increasing spending on beauty and wellness products, rising awareness regarding the benefits of beauty supplements and presence of major manufacturers driving market growth in the region.

Asia Pacific region is expected to be the fastest growing market for beauty supplements during the forecast period. Increasing disposable incomes, growing health and wellness trends driving demand for nutritional and dietary supplements from countries like China and India will support market expansion. Rising urbanization and evolving consumer lifestyles are additional factors fueling market development opportunities across Asia Pacific.

Get more insights on Beauty Supplements Market

Unlock More Insights—Explore the Report in the Language You Prefer

French

German

Italian

Russian

Japanese

Chinese

Korean

Portuguese

Vaagisha brings over three years of expertise as a content editor in the market research domain. Originally a creative writer, she discovered her passion for editing, combining her flair for writing with a meticulous eye for detail. Her ability to craft and refine compelling content makes her an invaluable asset in delivering polished and engaging write-ups.

(LinkedIn: https://www.linkedin.com/in/vaagisha-singh-8080b91)

#Coherent Market Insights#Beauty Supplements Market#Beauty Supplements#Skin Health#Hair Growth#Nail Strength#Collagen#Anti-Aging#Glowing Skin#Vitamins For Beauty#Biotin#Hyaluronic Acid#Beauty Nutrition#Antioxidants

0 notes

Text

Biochar 2024 Industry Size, Status, Analysis and Forecast 2030

Biochar Industry Overview

The global biochar market size was estimated at USD 541.8 million in 2023 and is expected to grow at a compound annual growth rate (CAGR) of 13.9% from 2024 to 2030. Increasing product consumption in producing organic food and its ability to enhance soil fertility & plant growth are expected to be key factors driving market growth. The European Biochar Certificate has passed regulations on its direct utilization in soil across several European countries including Austria and Switzerland. Biochar is a charcoal derived by controlled heating of waste materials, such as agricultural waste, wood waste, forest waste, and animal manure. Among all end-uses, it is widely used in a soil amendment to reduce pollutants and toxic elements and to prevent reducing moisture level, soil leaching, and fertilizer runoff.

Gather more insights about the market drivers, restrains and growth of the Biochar Market

Environmental awareness, cheaper cost of raw materials, and cohesive government policies for waste management are key factors anticipated to create greater avenues for market expansion. The industry comprises the organized and unorganized sectors owing to a strong presence of a few large-scale manufacturers and a growing number of small- and medium-scale manufacturers, especially in North America and Europe. Counties in Asia Pacific and Middle East are expected to grow at a sluggish rate with a lack of product awareness and its long-term advantages. Manufacturing of high-quality biochar requires heavy capital investment. As a result, several companies have exited the market place in the past few years.

In rural areas of countries, such as China, Japan, Brazil, and Mexico, a large amount of this product is produced in collaboration with research groups and institutions. The number of organized players in the industry manufacturing high-quality products is expected to increase with the growing demand for organic food. The full potential of this product is yet to be realized in other sectors than the agricultural sector. It is used as a fabric additive in the textile industry, as a raw material in the manufacturing of building materials, and as a shield against electromagnetic radiation in electronics industry.

Growing demand from the food sector is expected to be an extremely important factor in boosting market growth. The product usage in the water treatment process is anticipated to be another important application in near future supported by rising demand for water treatment facilities, especially in emerging economies. Moreover, the production of biochar using biogas and crop residue is expected to complement market growth. The raw materials required for product manufacturing are wood waste, forest waste, agricultural waste, and animal manure. These are mainly procured from suppliers of the wood and forest-based product sector.

Companies, such as Georgia-Pacific, Weyerhaeuser, and West Fraser, are among the few major suppliers of wood pellets and residue to various manufacturers. The EU Commission and the U.S. (Environmental Protection Agency) EPA are the regulatory authorities governing the market. It has made regulations related to the use of products in agricultural production and waste management. Several new rules have been released by the U.S. EPA regarding the production and by the EU commission regarding product manufacturing & consumption. As the product is still in the preliminary stage, there are huge opportunities for the development of blended products in future.

Browse through Grand View Research's Agrochemicals & Fertilizers Industry Research Reports.

• The global neem extracts market size was valued at USD 1.89 billion in 2023 and is expected to grow at a CAGR of 11.3% from 2024 to 2030. The major driving factor for the neem extract market is its prominence in the health and wellness sector as they are used in nutraceuticals and dietary supplements due to their bioactive components.

• The global forage seed market size was estimated at USD 4.71 billion in 2023 and is projected to grow USD 6.19 billion by 2030, growing at a CAGR of 4.0% from 2024 to 2030. Owing to the demand for high-quality seeds used in livestock feed is experiencing significant growth, primarily driven by the increasing global livestock population.

Biochar Market Segmentation

Grand View Research has segmented the global biochar market based on technology, application, and region:

Biochar Technology Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

• Pyrolysis

• Gasification

• Others

Biochar Application Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

• Agriculture

• Animal Farming

• Industrial Uses

• Other Applications

Biochar Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

• North America

o U.S.

o Canada

o Mexico

• Europe

o Germany

o UK

o France

o Sweden

o Denmark

• Asia Pacific

o China

o India

o Japan

o Australia

o Malaysia

• Central & South America

• Middle East & Africa

Order a free sample PDF of the Biochar Market Intelligence Study, published by Grand View Research.

Key Companies profiled:

• Biochar Products, Inc.

• Biochar Supreme, LLC

• ArSta Eco

• Carbon Gold Ltd

• Airex Energy Inc.

• Pacific Biochar Benefit Corporation

Key Biochar Company Insights

• In July 2023, a consortium of Canadian and French companies, including Airex Energy, Groupe Rémabec, and SUEZ, invested C$80 million to construct North America’s largest biochar production facility.

• In July 2023, Eco Allies, a Stereovision subsidiary, announced that Eco Allies, Inc. and Biochar Now, LLC have expanded their J/V's terms. A second plant in Mexico is added, and an increase in the number of kilns for each plant to be built goes from 120 to 180, or 360 kilns in total.

0 notes

Text

Graphics Film Market, Drivers, Future Outlook | BIS Research

Graphics Film refers to a type of film used in graphic design, printing, or industrial applications, typically involving a thin layer of material that can be applied to surfaces for aesthetic or functional purposes. It is often used to create high-quality images, patterns, or text on a variety of surfaces, such as glass, metal, plastic, or walls.

According to BIS the Global Graphics Film Market , the market size was valued at $28.33 Billion in 2023, and it is expected to grow with a CAGR of 5.50% during the forecast period 2023-2033 to reach $48.42 billion by 2033.

Graphics Film Overview

Graphic design is the art and practice of creating visual content to communicate messages or ideas. By combining elements such as typography, imagery, color, and layout, graphic designers craft designs that convey meaning and engage viewers.

Key Aspects of Graphic Designing Includes

Typography

Imagery

Layout

Color Theory

Market Segmentation

By End Users

Automotive

Promotional & Advertising

Industrial

Others

By Product Type

Polyethylene

Polypropylene

Polyvinyl chloride

Others

By Technology

Flexography

Rotogravure

Offset

Digital

By Region

North America

Europe

Asia-Pacific

Rest-of-the-World

Download the Report Click Here !

Demand Drivers and Challenges

The following are the demand drivers

Surge in Vehicle Personalization

Cost Advantage of Graphics Film Wrapping

The market is expected to face some limitations as well due to the following challenges

• Fluctuation in Raw Material Prices

Request a sample of this report on the Graphics Film Market

Recent Developments in the Global Graphics Film Market

In March 2021, Avery Dennison Graphics Solutions marked the launch of the newly upgraded Supreme Wrapping Film with twelve new colors in its Rugged Range and Sleek Satin collections.

In June 2023, FDC Graphic Films, Inc. announced the expansion of the Reno Warehouse facility, which would increase the company’s shipping capabilities of graphic film products to West Coast suppliers by 30%.

In July 2022, Avery Dennison launched its largest collection of automotive window films in Southeast Asia.

In October 2023, FDC Graphic Films, Inc. launched a new holographic film, Lumina FDC 3400, ideal for general-purpose graphics, short-term signage/graphics, decals, labels, and lettering.

Graphics Film Future Outlook

Graphics film, used widely in applications such as advertising, vehicle wraps, signage, and packaging, has a promising future driven by technological advancements and evolving market demands. Several key trends are shaping its outlook:

Growth In Digital Printing: The rise of digital printing technologies is enhancing the versatility and quality of graphics films.

Sustainability and Eco Friendly Materials - As industries shift toward sustainability, the demand for environmentally friendly graphics films is rising.

Smart Films and Interactive Graphics - Future innovations could include "smart" graphics films that incorporate technologies like LED lighting, touch-sensitivity, or thermochromic properties.

Enhanced Durability and Performance - Innovations in film materials will likely lead to enhanced durability, UV resistance, and weatherproof properties.

Access more detailed Insights on Advanced Materials,Chemicals and Fuels Research Reports

Conclusion

Graphics film has established itself as a versatile, high-impact solution across industries, from advertising and vehicle wrapping to packaging and signage.

As the industry moves forward, innovations in digital printing, material science, and sustainability are driving its evolution.

In conclusion, the future of graphics film is marked by technological progress, expanding markets, and increased sustainability efforts. Its flexibility, durability, and evolving capabilities make it a critical component of modern visual communication strategies, positioning it for sustained growth and relevance in a rapidly changing world.

0 notes

Text

Pharmaceutical Solvents Market: Forecast, Growth, and Opportunities

Introduction to Pharmaceutical Solvents Market

The Pharmaceutical Solvents Market plays a crucial role in the formulation of drugs, serving as carriers or dissolvers for active pharmaceutical ingredients (APIs). Solvents such as alcohols, acetone, and ethers are essential in the manufacturing process of tablets, injectables, and topical medications. The demand for pharmaceutical solvents is driven by the expanding pharmaceutical industry, stringent quality standards, and the rising prevalence of chronic diseases. However, market growth faces challenges such as environmental regulations and the volatility of raw material prices, pushing manufacturers toward green solvents.

The Pharmaceutical Solvents Market is Valued USD 3.87 billion in 2024 and projected to reach USD 5.9 billion by 2032, growing at a CAGR of 4.70% During the Forecast period of 2024-2032.It includes various organic and inorganic compounds, with applications ranging from synthesis to purification. Increasing demand for APIs, the growing prevalence of chronic and lifestyle diseases, and the rise of biopharmaceuticals are pushing market expansion. Geographically, North America and Europe dominate, but emerging economies are quickly catching up due to rising healthcare expenditures and growing pharmaceutical production capabilities.

Access Full Report :https://www.marketdigits.com/checkout/3431?lic=s

Major Classifications are as follows:

By Chemical Group

Alcohol

Isopropanol

Propylene Glycol

Butanol

Amine

Aniline

Diphenylamine

Methylethanolamine

Trimethylamine

Ester

Acetyl Acetate

Ethyl Acetate

Butyl Acetate

Ether

Diethyl Ether

Anisole

Polyethylene Glycol

Chlorinated Solvents

Carbon Tetrachloride

Dichloromethane

Other

Chelating Agents

Acetone

Key Region/Countries are Classified as Follows:

◘ North America (United States, Canada,)

◘ Latin America (Brazil, Mexico, Argentina,)

◘ Asia-Pacific (China, Japan, Korea, India, and Southeast Asia)

◘ Europe (UK,Germany,France,Italy,Spain,Russia,)

◘ The Middle East and Africa (Saudi Arabia, UAE, Egypt, Nigeria, and South

Key Players of Pharmaceutical Solvents Market

BASF SE,The Dow Chemical Company, Eastman Chemical Company, Merck KGaA, Thermo Fisher Scientific Inc., Honeywell International Inc.,Avantor, Inc., Solvay S.A.,Archer Daniels Midland Company, LyondellBasell Industries Holdings B.V., Mitsubishi Chemical Corporation, Celanese Corporation, INEOS Group Limitedand others.

Market Drivers in Pharmaceutical Solvents Market

Increase in pharmaceutical production: The rise in the production of generic and branded drugs fuels the demand for high-quality solvents.

Growth in R&D: As pharmaceutical companies invest heavily in research, particularly in biologics and specialty medicines, the need for effective solvents rises.

Technological advancements: Innovations in solvent formulation, including green solvents, offer opportunities for reducing environmental impact while maintaining efficacy.

Market Challenges in Pharmaceutical Solvents Market

Environmental concerns: Solvents contribute to pollution, and many are classified as hazardous. Regulatory bodies are increasingly pushing for greener alternatives.

Raw material volatility: Fluctuations in the cost of raw materials used in solvent production can lead to unpredictable pricing structures.

Stringent regulations: Pharmaceutical-grade solvents are subject to rigorous quality standards, which can increase manufacturing costs and create barriers for new market entrants.

Market Opportunities of Pharmaceutical Solvents Market

Sustainable solvents: Developing eco-friendly, biodegradable, and non-toxic solvent alternatives can meet regulatory demands and attract environmentally-conscious manufacturers.

Expanding generics market: The increasing demand for generic drugs in emerging economies opens doors for solvent suppliers, especially those offering cost-effective solutions.

R&D in biologics: The growth of biotechnology and biologics-based therapies creates a need for specialized solvents with unique properties.

Conclusion:

The Pharmaceutical Solvents Market is poised for steady growth, driven by the expanding pharmaceutical industry and innovations in biopharmaceuticals. While challenges such as environmental regulations and volatile raw material costs persist, the push for sustainable practices and green solvents presents new opportunities for market players. Technological advancements and increased demand from emerging economies are expected to sustain momentum, ensuring the market remains integral to pharmaceutical production

0 notes

Text

Fasteners Procurement Intelligence: A Comprehensive Guide

The fasteners category is anticipated to grow at a CAGR of 4.42% from 2023 to 2030. APAC holds the largest category share of over 40% and it is expected to be the fastest growing region during the forecast period. The increased use in the construction and automotive industries is driving considerable growth in the fasteners category. These fasteners are semi-permeant or occasionally permeant solutions, and the development of the construction industry, research and development initiatives, urban real estate infrastructure, and technological developments in the production of lightweight goods for the automotive and other industrial sectors are all factors that have an impact on their growth. The creation of innovative and novel industrial fasteners also helps the category growth.

In the building sector, they are employed to temporarily link two or more things together. As the industry demands strength and accuracy, building and construction fasteners are employed in heavy-duty applications to link materials together. Different fastening forms are employed in the construction industry, including stainless steel, alloy steel, and carbon steel. Nuts, bolts, washers, screws, and rivets are typical examples of building construction items. To ensure secure and sturdy construction, each infrastructure project needs a different kind of fastening product. Due to its affordability, strength, and workability, carbon steel is used to make the majority of products. The demand for industrial fasteners is increased by the fact that stainless steel is the most popular building material because of its strength, resistance to heat, and resistance to corrosion.

Corrosion resistance qualities will spur significant investment in the creation of new products, meeting consumer demand. During the projection period, rising consumer emphasis on residential and commercial building aesthetics will fuel industry expansion in the use of cable management and building exteriors. However, the negative aspect of working with fasteners is that they typically require special tools for setting up, which can increase project costs and complexity. Other types require extra steps like pre-drilling holes or applying thread-locking compounds, which adds extra labor and time to installation. Not to mention, depending on the application, some types may not be strong enough or sufficiently resilient for prolonged use, which could lead to expensive repairs in the future if not handled effectively from the start. It has been noted that these costs limit the category growth.

Order your copy of the Fasteners Procurement Intelligence Report, 2023 - 2030, published by Grand View Research, to get more details regarding day one, quick wins, portfolio analysis, key negotiation strategies of key suppliers, and low-cost/best-cost sourcing analysis

The fasteners category is fragmented and highly competitive in nature, with various large and small-scale manufacturers in China, Taiwan, Thailand, and Japan. Opportunities for new companies should arise from the rising need for inventive and application-specific industrial fastener designs. Over the projection period, rising raw material costs and high-volume manufacturing by the established companies are anticipated to be the main obstacles for new entrants. Furthermore, major fastener producers are likely to have an edge over small-scale competitors due to technological expertise and a strong customer base. For instance:

• In July 2023, next-generation FLEXTORQ® Impact Driver Bits were introduced by DEWALT, a division of Stanley Black & Decker Inc. These are created with fasteners and engineered for durability, advancing and improving driver bit technology for fastening applications.

• In January 2023, Birmingham Fasteners and Supply Inc. purchased Pacific Coast Bolt Corp. to diversify its manufacturing. The goal was to boost its presence in the commercial fastener market and provide customer service to clients across the United States.

• In September 2021, LINC Systems, LLC, a commercial fastener and packaging distributor platform, announced the acquisition of Air-O Fasteners. The deal was to expand the company's foothold in the Western United States.

Raw material, labor, machinery & equipment, and energy form the major cost components of this category. Raw material is the largest cost component accounting for around 60% - 70% of the total cost followed by labor at roughly 20%. The war between Russia and Ukraine has affected the supply of raw materials (copper, aluminum, etc.), as Russia produces roughly 4% of the world's copper and about 6% of its aluminum. The fasteners category is an example of an industry where suppliers implement cost-plus pricing model. This is because fasteners are typically low-cost, commodity products with little differentiation between brands. As a result, companies in this industry often compete on price, and cost-plus pricing is a simple and easy way to set prices that are competitive.

China, and India are among the most of the preferred sourcing destinations in this category.China has a robust manufacturing industry and offers a wide range of suppliers with diverse capabilities and cost-effective production options. India is a popular destination for metalworking processes due to its established manufacturing sector. For sourcing fasteners, research the market to understand the types, quality, and prices available. Develop a sourcing strategy by identifying the needs, budget, and potential suppliers. Build relationships with suppliers to get the best prices and quality fasteners. Negotiate prices, especially if buying in bulk. Document all the terms & conditions to avoid discrepancies. Monitor suppliers to ensure they meet the agreed quality standards. Use a variety of sources for the best prices and quality.

Fasteners Procurement Intelligence Report Scope

• Fasteners Category Growth Rate: CAGR of 4.42% from 2023 to 2030

• Pricing growth Outlook: 3% - 5% (annual)

• Pricing Models: Cost-plus pricing model, fixed-fee pricing model, discount pricing model

• Supplier Selection Scope: Cost and pricing, Past engagements, Productivity, Geographical presence

• Supplier selection criteria: Quality assurance, service level agreement, environmental compliance, lead times, technical specifications, operational capabilities, regulatory standards and mandates, category innovations, and others

• Report Coverage: Revenue forecast, supplier ranking, supplier matrix, emerging technology, pricing models, cost structure, competitive landscape, growth factors, trends, engagement, and operating model

Browse through Grand View Research’s collection of procurement intelligence studies:

• Flooring Services Procurement Intelligence Report, 2023 - 2030 (Revenue Forecast, Supplier Ranking & Matrix, Emerging Technologies, Pricing Models, Cost Structure, Engagement & Operating Model, Competitive Landscape)

• Fixed Line Services Procurement Intelligence Report, 2023 - 2030 (Revenue Forecast, Supplier Ranking & Matrix, Emerging Technologies, Pricing Models, Cost Structure, Engagement & Operating Model, Competitive Landscape)

Key companies profiled

• Arconic Fastening Systems and Rings

• Acument Global Technologies Inc.

• ATF Inc.

• Dokka Fasteners AS

• LISI Group

• Nippon Industrial Fasteners Company

• Hilti Corporation

• MW Industries Inc.

• Birmingham Fasteners and Supply Inc.

• SESCO Industries Inc.

Brief about Pipeline by Grand View Research:

A smart and effective supply chain is essential for growth in any organization. Pipeline division at Grand View Research provides detailed insights on every aspect of supply chain, which helps in efficient procurement decisions.

Our services include (not limited to):

• Market Intelligence involving – market size and forecast, growth factors, and driving trends

• Price and Cost Intelligence – pricing models adopted for the category, total cost of ownerships

• Supplier Intelligence – rich insight on supplier landscape, and identifies suppliers who are dominating, emerging, lounging, and specializing

• Sourcing / Procurement Intelligence – best practices followed in the industry, identifying standard KPIs and SLAs, peer analysis, negotiation strategies to be utilized with the suppliers, and best suited countries for sourcing to minimize supply chain disruptions

#Fasteners Procurement Intelligence#Fasteners Procurement#Procurement Intelligence#Fasteners Market#Fasteners Industry

0 notes

Text

Food Contract Manufacturing Market Analysis, Size, Share, Growth, Trends, and Forecasts by 2031

In the Food Contract Manufacturing market, a myriad of players collaborates to deliver an extensive array of food products. This interconnected network involves manufacturers, suppliers, and distributors working synergistically to bring innovative and high-quality food items to the market. The industry is not confined to a specific domain; instead, it permeates various segments, ranging from snacks and beverages to frozen foods and ready-to-eat meals.

𝐆𝐞𝐭 𝐚 𝐅𝐫𝐞𝐞 𝐒𝐚𝐦𝐩𝐥𝐞 𝐑𝐞𝐩𝐨𝐫𝐭:https://www.metastatinsight.com/request-sample/2579

Top Companies

Fibro Foods Private Limited

Hindustan Foods Limited

Hearthside Food Solutions LLC

Nikken Foods Co.,Ltd.

Christy Quality Foods (CQF)

Romix Foods Limited

HACO Holding AG

SK Food Group

Pacmoore Products Inc.

STOCKMEIER Group

Kilfera Food Manufacturers Ltd

SternMaid

Thrive Foods LLC.

Dominion Liquid Technologies

Omniblend Pty Ltd.

One of the defining features of the Global Food Contract Manufacturing market is its adaptability to changing consumer preferences. As culinary tastes evolve, the industry responds by embracing innovation and customization. Contract manufacturers engage in a continuous process of research and development to understand and incorporate the latest trends in flavors, ingredients, and packaging. This adaptability ensures that the market remains relevant and dynamic in the ever-changing landscape of the food sector.

Access Full Report @https://www.metastatinsight.com/report/food-contract-manufacturing-market

Collaboration and flexibility define the relationships within the Global Food Contract Manufacturing market. Manufacturers partner with clients to co-create products that align with specific brand identities and market demands. This collaborative approach extends beyond traditional business transactions, fostering long-term partnerships that contribute to the mutual growth of both parties. The market thrives on open communication, enabling seamless coordination throughout the production process.

Efficiency is a cornerstone of the Global Food Contract Manufacturing market. With a focus on optimizing resources and streamlining processes, manufacturers strive to deliver cost-effective solutions without compromising on quality. This emphasis on efficiency allows brands to bring products to market swiftly, meeting consumer demands in a timely manner and capitalizing on emerging opportunities.

Quality assurance is paramount in the Global Food Contract Manufacturing market. Manufacturers adhere to stringent standards and regulations to ensure the safety and integrity of the products they produce. This commitment to quality extends to every aspect of the manufacturing process, from sourcing raw materials to the final packaging. Rigorous testing and adherence to industry best practices underscore the industry's dedication to delivering safe and reliable food products.

The Global Food Contract Manufacturing market stands as a dynamic and interconnected sector within the broader food industry. Through collaboration, adaptability, efficiency, and a commitment to quality, this market plays a vital role in shaping the diverse array of food products available in the market. As consumer preferences continue to evolve, the industry remains poised to embrace innovation and deliver solutions that cater to the ever-changing culinary landscape.

Global Food Contract Manufacturing market is estimated to reach $296.3 Million by 2031; growing at a CAGR of 9.3% from 2024 to 2031.

Contact Us:

+1 214 613 5758

#FoodContractManufacturing#FoodContractManufacturingMarket#FoodContractManufacturingindustry#marketsize#marketgrowth#marketforecast#marketanalysis#marketdemand#marketreport#marketresearch

0 notes

Text

Automotive Power Electronics Market - Forecast(2024–2030)

Automotive Power Electronics Market Overview

Automotive Power Electronics Market Size is valued at $5.4 Billion by 2030, and is anticipated to grow at a CAGR of 4.2% during the forecast period 2024 -2030. The automotive power #electronics market is experiencing significant growth, driven #primarily by the increasing demand for #electric vehicles (EVs). This surge is fueled by a global shift towards sustainable transportation and stringent emission #regulations. The rapid #technological advancements in #semiconductor materials and power management solutions are enhancing the efficiency and performance of automotive power electronics, thereby #accelerating market expansion.

Additionally, consumer preferences are evolving towards vehicles that offer better energy efficiency, safety, and convenience, all of which are enabled by sophisticated power electronic systems. Manufacturers are investing heavily in research and development to innovate and stay competitive in this dynamic market. Furthermore, government incentives and subsidies for EVs are further propelling the adoption of automotive power electronics. This market trajectory is expected to continue its upward trend, as the integration of power electronics in vehicles becomes more prevalent, aligning with the broader goals of energy conservation and environmental sustainability.

Sample Report:

COVID-19/Russia-Ukraine War Impact

The COVID-19 pandemic significantly disrupted the automotive power electronics market, initially causing production halts and supply chain disruptions. As factories shut down and demand for vehicles plummeted, manufacturers faced challenges in maintaining operations and meeting financial targets. However, the pandemic also accelerated the adoption of electric vehicles (EVs), driven by increased awareness of environmental issues and government incentives. This shift spurred innovations in power electronics, essential for EVs’ efficiency and performance. Consequently, despite short-term setbacks, the industry experienced a renewed focus on developing advanced power electronics solutions, paving the way for long-term growth and resilience in a post-pandemic era.

The Russo-Ukraine War has significantly impacted the automotive power electronics sector, primarily through disruptions in the supply chain and fluctuations in raw material prices. The conflict has caused instability in the region, affecting the production and transportation of essential components like semiconductors and rare earth metals, crucial for power electronics. This disruption has led to increased costs and delays, compelling manufacturers to seek alternative sources and adjust their supply chains. Additionally, the economic sanctions imposed on Russia have further strained international trade relations, exacerbating the challenges faced by the automotive industry. Consequently, companies are re-evaluating their strategies to mitigate risks and ensure resilience in their operations, focusing on diversifying suppliers and investing in local manufacturing capabilities to reduce dependency on geopolitically sensitive regions.

Inquiry Before Buying:

Automotive Power Electronics Market

The report “Automotive Power Electronics Market Forecast (2024–2030)”, by Industry ARC, covers an in-depth analysis of the following segments of the Automotive Power Electronics Market:

By Component: Microcontroller Unit, Power Integrated Circuit, Sensors, Others

By Vehicle Type: Passenger Cars, Commercial Vehicles

By Electric Vehicle Type: Battery Electric Vehicles, Hybrid Electric Vehicles, Plug-In Hybrid Electric Vehicles

By Application: Powertrain & Chassis, Body Electronics, Safety & Security, Infotainment & Telematics, Energy Management System, Battery Management System

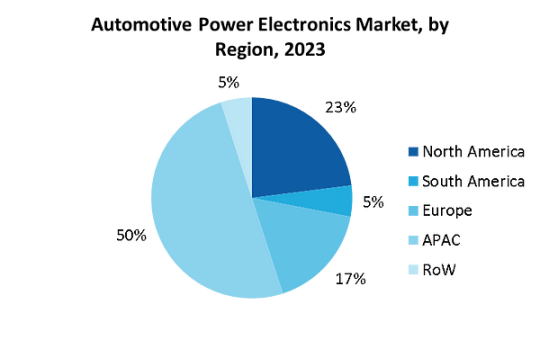

By Geography: North America (USA, Canada, and Mexico), South America (Brazil, Argentina, Colombia, Chile, and Rest of South America), Europe (UK, Germany, France, Italy, Netherlands, Spain, Russia, and Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia, Indonesia, Malaysia, and Rest of APAC), and Rest of the World (Middle East, and Africa)

Key Takeaways

Asia-Pacific dominated the Automotive Power Electronics market with a share of around 50% in the year 2023.

The automotive industry’s need to meet stricter safety regulations and reduce emissions, coupled with rising consumer demand for electric vehicles, will propel the growth of the automotive power electronics market throughout the forecast period.

Apart from this, thrust to equip vehicles with advanced power solutions is driving the growth of Automotive Power Electronics market during the forecast period 2024–2030.

For More Details on This Report — Request for Sample

Automotive Power Electronics Market Segment Analysis — By Vehicle Type

The demand for automotive power electronics in passenger cars is escalating due to government initiatives promoting the integration of advanced electronics. This surge is driven by policies aimed at enhancing vehicle efficiency, safety, and environmental performance. For instance, in March 2024, the European Union introduced new regulations mandating the inclusion of advanced driver-assistance systems (ADAS) in all new cars, significantly boosting the need for sophisticated power electronics. Similarly, the U.S. government has increased funding for electric vehicle (EV) infrastructure, encouraging automakers to incorporate more power-efficient electronic components. Additionally, China’s recent tax incentives for electric and hybrid vehicles, announced in January 2024, have accelerated the adoption of power electronics to improve performance and range. These initiatives are fostering innovation and production of cutting-edge electronic components, such as inverters and onboard chargers, essential for modern passenger cars. As a result, automotive manufacturers are increasingly investing in power electronics to comply with regulations, meet consumer expectations, and gain a competitive edge in the evolving market.

Schedule a Call :

Automotive Power Electronics Market Segment Analysis — By Electric Vehicle Type

The demand for automotive power electronics in hybrid electric cars is rapidly increasing due to the global imperative to decarbonize the transport sector and reduce reliance on fossil fuels. Governments worldwide are implementing stringent regulations and incentives to promote the adoption of hybrid and electric vehicles. In January 2024, the European Union introduced enhanced subsidies for hybrid vehicle purchases, coupled with stricter emission standards, significantly boosting the market for power electronics. Similarly, the U.S. launched the “Clean Transport Initiative” in April 2023, providing substantial tax breaks and grants for hybrid car manufacturers to innovate and scale up production. Additionally, Japan’s latest energy policy, announced in February 2024, includes a comprehensive plan to phase out internal combustion engines, further propelling the demand for hybrid vehicles equipped with advanced power electronics. These components, such as power inverters, converters, and battery management systems, are essential for enhancing the efficiency and performance of hybrid electric cars. As a result, automotive companies are accelerating investments in power electronics technology to meet regulatory requirements, cater to consumer preferences, and contribute to a sustainable future.

Automotive Power Electronics Market Segment Analysis — By Geography

On the basis of geography, Asia-Pacific held the highest segmental market share of around 50% in 2023, The Asia-Pacific region is the largest market for automotive power electronics, driven by high vehicle production rates and the increasing adoption of advanced electronics in automobiles. Countries like China, Japan, and South Korea are leading in vehicle manufacturing, with major automakers integrating sophisticated power electronic components to enhance vehicle efficiency and performance. For example, in March 2024, Toyota introduced a new hybrid model equipped with cutting-edge power electronics, significantly improving energy management and fuel efficiency. Similarly, BYD in China launched an electric vehicle series in February 2024, featuring advanced inverters and converters, which contribute to extended driving ranges and faster charging times. These innovations reflect the region’s robust focus on technological advancements and sustainable transportation solutions. The strategic partnerships between automotive giants and technology firms, such as Hyundai’s collaboration with LG Electronics to develop next-generation battery management systems in April 2023, further underscore the region’s leadership in this sector. This confluence of high production volumes and technological integration ensures that the Asia-Pacific market remains at the forefront of automotive power electronics development.

Buy Now:

Automotive Power Electronics Market Drivers

The rising market for the electric vehicles is the key factor driving the growth of Global Automotive Power Electronics market

The growing demand for automotive power electronics is being significantly driven by the expanding electric vehicle (EV) market. As global initiatives to reduce carbon emissions intensify, consumers and manufacturers alike are shifting towards EVs, which rely heavily on power electronics for various critical functions. These components, including inverters, converters, and battery management systems, are essential for optimizing the performance, efficiency, and range of electric vehicles. Automakers are ramping up production of EVs, incorporating advanced power electronics to meet regulatory standards and consumer expectations for sustainability and high performance. The technological advancements in power electronics are also enabling faster charging, improved energy management, and enhanced vehicle safety, further boosting their demand. Consequently, the automotive industry is experiencing a surge in innovation and investment in power electronics to support the burgeoning EV market, positioning it as a pivotal element in the future of transportation.

Automotive Power Electronics Market Challenges

The high cost of electric vehicles is expected to restrain the market growth

The high cost of electric vehicles (EVs) negatively impacts the automotive power electronics market by limiting consumer adoption and market growth. Despite the technological advancements and environmental benefits of EVs, their higher price compared to traditional vehicles remains a significant barrier. This cost premium is largely due to expensive components such as batteries and advanced power electronics systems, including inverters and converters, which are essential for EV functionality. As a result, potential buyers are often deterred by the initial investment required, slowing the transition to electric mobility. Consequently, manufacturers face challenges in achieving economies of scale, which further drives up costs. This cyclical issue restricts market expansion and inhibits broader implementation of power electronics innovations, ultimately stalling progress towards widespread EV adoption and the associated benefits of reduced emissions and improved energy efficiency in the automotive sector.

Automotive Power Electronics Industry Outlook

Product launches, mergers and acquisitions, joint ventures and geographical expansions are key strategies adopted by players in the Automotive Power Electronics Market. The key companies in the Automotive Power Electronics Market are:

STMicroelectronics N.V.

Infineon Technologies AG

Fuji Electric Co., Ltd.

NXP Semiconductors N.V.

Renesas Electronics Corporation

Toshiba Corporation

Mitsubishi Electric

Huawei Digital Power

Robert Bosch GmbH

Hitachi Energy

Recent Developments

In May 2022, STMicroelectronics joined forces with Microsoft to make development of highly secure IoT devices easier.

In March 2023, Infineon Technologies announced the acquisition of GaN Systems, a global leader in gallium nitride (GaN)-based power conversion solutions. This move strengthened Infineon’s position in the market.

For more Automotive Market reports, please click here

0 notes

Text

How Modular Construction is Revolutionizing the Building Industry

The global modular construction market size is expected to reach USD 162.40 billion by 2030, registering a CAGR of 7.5% over the forecast period, according to a new report by Grand View Research, Inc. This growth can be attributed to growing infrastructural development and building activities in developing countries around the globe. Rapid urbanization and industrialization are expected to increase the number of new projects, primarily in the commercial and industrial building sectors. This is likely to fuel the growth of the modular construction industry across the globe. Increasing technological advancements in the building industry coupled with the advantages provided by modular construction such as reduced building schedule, reduced cost, greater flexibility, reuse, and less material waste are contributing to the product demand in the market.

The relocatable modular construction (RMC) market is expected to witness rapid growth as temporary housing for emergency and relief operations has gained popularity over the past decade. These buildings are made to be repurposed and transported to various building sites. Government initiatives and regulations toward sustainability and a green environment are expected to fuel the market growth over the forecast period.

Using wood in modular construction is advantageous due to its favorable properties as a material. Wood is used in modular construction to create exterior wall panels including additional layers for insulation, vapor barrier, siding, waterproofing, and drywall. Moreover, global concerns regarding sustainability and increasing awareness about wood as a building material among consumers are the factors likely to augment the growth of the market over the forecast period.

Growing commercial sector in Asia Pacific on account of rising penetration of multinational brands backed with favorable trade policies are expected to propel the market growth. Increasing construction of office spaces, shopping malls, lodging spaces and other utility spaces across the region are likely to provide a major boost to the adoption of modular construction.

The manufacturers of modular construction prefer to maintain strategic relationships with raw material suppliers in order to avoid disruptions in raw material supply. In addition, manufacturers do not depend on a single source to procure raw materials to ensure the steady supply of raw materials and avoid volatility in terms of sourcing, thereby limiting the bargaining power of suppliers.

Leading companies are implementing the latest modular construction techniques and solutions to drive innovation in the modular construction sector. For instance, in March 2017, Bureau Veritas, Setec Bâtiment, Agence Coste Architectures, and Bouygues Construction partnered to work on innovative Building Information Modeling (BIM) processes. These processes enable technical inspectors and health & security protection coordinators to assess buildings and structures directly based on the digital model and allows principal contractors to sign off directly on the same digital model.

For More Details or Sample Copy please visit link @: Modular Construction Market Report

Modular Construction Market Report Highlights

The permanent segment accounted for the largest revenue share of 64.1% in 2021. This is attributed to the several advantages of off-site construction such as high-quality control compared to traditional building methods.

The steel material segment accounted for a major share of 41.5% in 2022, owing to its characteristics due to which structural steel is used in building materials and can be welded into different shapes and grades.

The residential application segment was valued at USD 47.85 billion in 2022 and is further forecasted to grow rapidly by 2030. The residential application segment includes single-family houses, multi-story residential buildings, and rental housing properties. Modular construction is witnessing rapid adoption in residential applications on account of its ability to significantly reduce building costs and time.

The European region accounted for the largest revenue share in 2022 and is forecast to grow at a CAGR of 7.1% by 2030. The primary driving factor is expected to be the rising influx of migrants necessitating the building of temporary and permanent housing structures in the region.

Modular construction market is characterized by the presence of various established players with a strong financial base resulting in high barriers for new entrants in this market. High initial capital required for developing buildings with modular construction is expected to lower the threat of new entrants in the market.

Gain deeper insights on the market and receive your free copy with TOC now @: Modular Construction Market Report We have segmented the global modular constructionmarket report based on product, material, application, and region.

#ModularConstruction#SustainableBuilding#ConstructionInnovation#PrefabBuildings#ConstructionTrends#ModularArchitecture#OffsiteConstruction#BuildingEfficiency#ModularHousing#ConstructionTechnology#GreenConstruction#ModernBuildingMethods#ConstructionSolutions

0 notes

Text

Fire Door Inspection Service Market Size, volume, Revenue, Trends Analysis Report 2024-2030

On 2024-9-26 Global Info Research released【Global Fire Door Inspection Service Market 2024 by Manufacturers, Regions, Type and Application, Forecast to 2030】. This report includes an overview of the development of the Fire Door Inspection Service industry chain, the market status of Consumer Electronics (Nickel-Zinc Ferrite Core, Mn-Zn Ferrite Core), Household Appliances (Nickel-Zinc Ferrite Core, Mn-Zn Ferrite Core), and key enterprises in developed and developing market, and analysed the cutting-edge technology, patent, hot applications and market trends of Fire Door Inspection Service.

Fire door inspection service refers to a professional service designed to ensure the safety and compliance of fire doors. This service is usually provided by an agency or company with relevant qualifications and experience. They will conduct a detailed inspection of the fire door to confirm whether it meets the requirements of national or local fire regulations and standards.

The global Fire Door Inspection Service market size is expected to reach $ million by 2030, rising at a market growth of %CAGR during the forecast period (2024-2030).

This report studies the global Fire Door Inspection Service demand, key companies, and key regions.

This report is a detailed and comprehensive analysis of the world market for Fire Door Inspection Service, and provides market size (US$ million) and Year-over-Year (YoY) growth, considering 2023 as the base year. This report explores demand trends and competition, as well as details the characteristics of Fire Door Inspection Service that contribute to its increasing demand across many markets.

Market segment by Type: Wooden Door、Metal Door

Market segment by Application:Commercial Building、Industrial Plant、Residential

Major players covered: Fire Door Inspection Solutions、The Fire Door Inspection、Safelincs、Firedoor Assessment、UL、Halspan、Chubb、Aspect、FD Fire Door、Allmar、FPA、ASSA ABLOY、KCC Group

Market segment by region, regional analysis covers: North America (United States, Canada and Mexico), Europe (Germany, France, United Kingdom, Russia, Italy, and Rest of Europe), Asia-Pacific (China, Japan, Korea, India, Southeast Asia, and Australia),South America (Brazil, Argentina, Colombia, and Rest of South America),Middle East & Africa (Saudi Arabia, UAE, Egypt, South Africa, and Rest of Middle East & Africa).

The content of the study subjects, includes a total of 15 chapters:

Chapter 1, to describe Fire Door Inspection Service product scope, market overview, market estimation caveats and base year.

Chapter 2, to profile the top manufacturers of Fire Door Inspection Service, with price, sales, revenue and global market share of Fire Door Inspection Service from 2019 to 2024.

Chapter 3, the Fire Door Inspection Service competitive situation, sales quantity, revenue and global market share of top manufacturers are analyzed emphatically by landscape contrast.

Chapter 4, the Fire Door Inspection Service breakdown data are shown at the regional level, to show the sales quantity, consumption value and growth by regions, from 2019 to 2030.

Chapter 5 and 6, to segment the sales by Type and application, with sales market share and growth rate by type, application, from 2019 to 2030.

Chapter 7, 8, 9, 10 and 11, to break the sales data at the country level, with sales quantity, consumption value and market share for key countries in the world, from 2017 to 2023.and Fire Door Inspection Service market forecast, by regions, type and application, with sales and revenue, from 2025 to 2030.

Chapter 12, market dynamics, drivers, restraints, trends and Porters Five Forces analysis.

Chapter 13, the key raw materials and key suppliers, and industry chain of Fire Door Inspection Service.

Chapter 14 and 15, to describe Fire Door Inspection Service sales channel, distributors, customers, research findings and conclusion.

Data Sources:

Via authorized organizations:customs statistics, industrial associations, relevant international societies, and academic publications etc.

Via trusted Internet sources.Such as industry news, publications on this industry, annual reports of public companies, Bloomberg Business, Wind Info, Hoovers, Factiva (Dow Jones & Company), Trading Economics, News Network, Statista, Federal Reserve Economic Data, BIS Statistics, ICIS, Companies House Documentsm, investor presentations, SEC filings of companies, etc.

Via interviews. Our interviewees includes manufacturers, related companies, industry experts, distributors, business (sales) staff, directors, CEO, marketing executives, executives from related industries/organizations, customers and raw material suppliers to obtain the latest information on the primary market;

Via data exchange. We have been consulting in this industry for 16 years and have collaborations with the players in this field. Thus, we get access to (part of) their unpublished data, by exchanging with them the data we have.

From our partners.We have information agencies as partners and they are located worldwide, thus we get (or purchase) the latest data from them.

Via our long-term tracking and gathering of data from this industry.We have a database that contains history data regarding the market.

Global Info Research is a company that digs deep into global industry information to support enterprises with market strategies and in-depth market development analysis reports. We provides market information consulting services in the global region to support enterprise strategic planning and official information reporting, and focuses on customized research, management consulting, IPO consulting, industry chain research, database and top industry services. At the same time, Global Info Research is also a report publisher, a customer and an interest-based suppliers, and is trusted by more than 30,000 companies around the world. We will always carry out all aspects of our business with excellent expertise and experience.

0 notes

Text

Protective Coatings Market Forecast a Steady Growth at 4.8% CAGR, by 2031

The global protective coatings market is estimated to surge at a CAGR of 4.8% from 2023 to 2031. Transparency Market Research projects that the overall sales revenue for protective coatings is estimated to reach US$ 22.8 billion by the end of 2031.

The influence of smart coating technologies is transforming the landscape. Smart coatings, featuring self-healing properties and real-time monitoring capabilities, are gaining traction. These coatings enhance longevity and reduce maintenance costs, catering to industries seeking advanced protective solutions.

The demand for antimicrobial coatings presents a prominent driver. The global health crisis has intensified the focus on antimicrobial solutions. Protective coatings with antimicrobial properties find applications in healthcare, public spaces, and transportation, contributing to a heightened emphasis on hygiene and safety.

For More Details, Request for a Sample of this Research Report: https://www.transparencymarketresearch.com/protective-coatings-market.html

Customization and tailored coating solutions play an integral role. Industry-specific requirements prompt a shift towards personalized coatings. Manufacturers offering tailored solutions, addressing unique needs in sectors like electronics and renewable energy, drive market differentiation and growth.

The rise of sustainable raw materials influences the market. The quest for sustainability extends to raw materials used in coatings. Suppliers incorporating renewable and bio-based materials align with the industry's eco-friendly evolution, contributing to the transformative journey of the protective coatings market.

Key Findings of the Market Report

Polyurethane resin type leads the protective coatings market, offering superior durability, versatility, and corrosion resistance across diverse applications globally.

Water-borne formulations lead the protective coatings market, gaining prominence for their eco-friendliness, low VOC content, and enhanced safety features.

Building & construction stands as the leading end-use industry in the protective coatings market, driven by infrastructure development and renovation projects.

Protective Coatings Market Growth Drivers & Trends

Ongoing innovations in protective coatings, including nanotechnology and smart coatings, drive market growth by enhancing durability, corrosion resistance, and performance across diverse applications.

Global infrastructure projects stimulate demand for protective coatings in construction, contributing to market expansion.

Growing emphasis on eco-friendly and sustainable coatings fuels the development of environmentally responsible protective solutions, aligning with changing consumer preferences and stringent regulations.

Rapid industrial growth in emerging economies, particularly in Asia Pacific, escalates demand for protective coatings across manufacturing, oil and gas, and automotive sectors.

Increasing concerns about fire safety drive the adoption of fire-resistant coatings, particularly in construction and transportation, shaping a significant trend in the protective coatings market.

Global Protective Coatings Market: Regional Profile

The North American protective coatings market, led by the United States, holds a significant share. Robust infrastructural development and a mature industrial sector drive demand. Stringent environmental regulations prompt innovations in eco-friendly coatings. Key players like PPG Industries and Sherwin-Williams leverage advanced technologies, contributing to the region's prominence in the global protective coatings landscape.