#Printed Electronics Market Share

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has been providing a Korean-language service since 2013.

Text

#3D Printed Electronics Market Share#3D Printed Electronics Market Analysis#3D Printed Electronics Market Overview

0 notes

Text

The United States printed electronics market size is projected to exhibit a growth rate (CAGR) of 16.60% during 2024-2032.

#United States Printed Electronics Market#United States Printed Electronics Market share#United States Printed Electronics Market trends#United States Printed Electronics Market forecast#United States Printed Electronics Market growth

0 notes

Text

Automotive 3D Printing Market - Forecast(2024 - 2030)

Automotive 3D Printing Market Overview

Automotive 3D printing market is expected to reach $1.8 billion by 2026 at a CAGR of 11.1% during the forecast period 2021-2026, owing to increasing research and development activities and innovations which is strengthening the automotive industry worldwide. Similarly, with a huge capital investment in automotive technology, several manufacturers are focusing on light weight vehicles to decrease the fuel consumption and low emission. Among all the R&D activities, 3D printing in automotive has come up with a rapid pace and gaining attention in the global automotive industry for rapid prototyping. According to the Chinese Passenger Car Association (CPCA), demand for electric car is growing progressively. This is due to the rising development of lightweight automobile parts utilizing 3D automobile printing technologies. The Chinese Government has rendered the development of additive manufacturing technologies a priority in the region. International companies are urged to create subsidiaries, although some domestic companies are also driven by government policies. Collaboration with other industry leader companies to incorporate various technology such as stereo lithography, selectrive laser sintering and digital light processing into their manufacturing process and create innovative product innovations would help them achieve strategic edge over their competitors.

Automotive 3D Printing Market Report Coverage

The report: “Automotive 3D Printing Market – Forecast (2021-2026)”, by IndustryARC covers an in-depth analysis of the following segments of the Automotive 3D Printing market

By Material: Metals, Polymer, Others (Ceramic and Glass) By Technology: Stereolithography, Selective Laser Sintering, Electron Beam Melting (EBM), Fused Disposition Modeling, Laminated Object Manufacturing, Three Dimensional Inject Printing, Others By Application: Prototyping & Tooling, Manufacturing Complex Components, Research, Development & Innovation, Others By Geography: North America (U.S, Canada, Mexico), South America(Brazil, Argentina and others), Europe(Germany, UK, France, Italy, Spain, Russia and Others), APAC(China, Japan India, SK, Aus and Others), and RoW (Middle east and Africa)

Request Sample

Key Takeaways

Automotive 3D printing in North America is growing at significant rate owing to the stringent governmental regulations regarding automobiles and auto parts are regulated through the National Highway Traffic Safety Administration (NHTSA) and the U.S Environmental Protection Agency (EPA).

The exceptional growth prospects of the electric vehicles market is a major growth factor for the 3D printing automotive market owing to its importance in electric vehicles.

The automotive OEMs are partnering with the leading 3D printing companies like Stratatsys, Shining 3D, SLM Solutions are largely concentrating on the technologies like stereo lithography, fused deposition modeling, and Laser sintering.

Automotive 3D Printing top 10 companies include Stratasys Inc., 3D System, Materialise NV, Renishaw PLC, SLM Solutions, ExOne, Envisiontec Inc., EOS, Arcam AB, Autodesk, Inc., among others.

Automotive 3D Printing Market Segment Analysis - By Application

Manufacturing complex components is growing at a highest CAGR of 12.1% in the forecast period. Complex components with internal cavities require multiple subcomponents held together by a variety of processes in the standard subtractive manufacturing process. As 3D printing is in nature an additive, it can create identical parts as single objects, allowing for less inspections and improved efficiency in the workflow. With Additive Manufacturing, designs with complex geometries only distribute build material where conformity with automotive performance standards is strategically necessary. 3D-printed pieces often weigh less than half of the weight of their cast or machined counterparts. A single click away from the mouse dramatically attenuates the design process with on-the-fly alterations. Moreover, early adopters used one-of-a-kind printed prototypes for wind tunnel testing in the automotive industry. In addition additive Manufacturing processes provide cost-effective alternatives to traditional automotive component manufacturing, especially complex and unique parts. Further additive manufacturing helps companies to create complex designs that require fewer parts for these components to be produced. As a result, companies may reduce the assembly time and also experience a decrease in quality problems. Delphi, an Irish tier 1 supplier to the automotive industry, used a metal 3D printing method known as Selective Laser Melting to produce a single piece aluminium diesel pump. With this, the company achieved a remarkable reduction in the number of parts available for the pump, thereby avoiding a few post-processing steps and simplifying the assembly process. The end result was a finished product of higher quality as it reduced the low-time fluid and is less vulnerable to leakage, with lower manufacturing costs. Hence these factors are analysed to drive the market in the forecast period 2020-2025.

Inquiry Before Buying

Automotive 3D Printing Market Segment Analysis - By Technology

Selective Laser Sintering (SLS) in automotive 3D Printing is growing at a CAGR of 13.5% in the forecast period. Selective Laser Sintering is an additive manufacturing or 3d printing technology that can be used for processing many types of materials such as polymers, metals, ceramics, and composites to create complex parts. It's areas of applications include automotive, aerospace tooling, biomedical as well as architecture. In addition SLS technology based 3d printing helps in building much stronger and durable prototypes than other technologies, thus causing its demands over applications ranging from low volume production to rapid prototyping of automotive parts and components. Such factors have been helping this technology towards boosting its growth in the 3d printing automotive market in the forecast period. Moreover, this technology has been considered to be one of the fastest as well as widely used 3d printing process due to it scalability of printing multiple automotive parts simultaneously, thus maximizing the build space for the auto manufacturers. Due to this, auto manufacturers are able to build high amount of parts and fixtures within less time intervals, thus boosting their productivity standards. Since this technology has been helping in reducing additional costs for automakers, many major automotive companies have been highly shifting towards adopting selective laser sintering 3d printing for building vehicle parts more easily along with cost efficiency. As a part of this, recently FAW-Volkswagen Automotive Co. Ltd, a joint venture between FAW Group, Volkswagen and Audi revealed about producing prototypes for more than 5,000 parts a year deploying laser sintering technology. Further deployment of 3d printing technology across the automotive industry helped in reducing the overhead operational costs along with speeding up the design iteration process, thus driving its demands in the automotive sector in the forecast period 2021-2026.

Automotive 3D Printing Market Segment Analysis- By Geography

Automotive 3D printing in North America is growing at significant rate of 12.2% CAGR through 2026 owing to the stringent governmental regulations regarding automobiles and auto parts are regulated through the National Highway Traffic Safety Administration (NHTSA) and the U.S Environmental Protection Agency (EPA). Such regulations are related to improve the vehicle safety standards as well as reduce the vehicle emissions. Such factors have been creating high deployments of electric vehicles in the country, in order to comply with such laws, thereby boosting the market growth of 3d printing technology. Moreover, rising growth of automobiles has caused the various automakers to shift towards advanced technologies in order to increase mass production of vehicles more efficiently within lesser time intervals along with reducing fuel consumption. As a part of this, one of the major U.S auto manufacturer, General Motors had invested in Autodesk’s software with 3d printing in effort to produce lighter vehicle parts through mass reduction and parts consolidation. Deploying of such lighter auto parts eventually helps in cutting the high fuel consumption costs for the customers, thus driving the automobiles demands. Such initiatives have been helping in boosting the growth of 3d printing in automotive market in the forecast period 2021-2026.

Schedule a Call

Automotive 3D Printing Market Drivers

Impressive Growth of Electric Vehicles

The market for electric vehicles is growing all across the globe, however, the electric vehicle market growth in China is quite significant. The exceptional growth prospects of the electric vehicles market is a major growth factor for the 3D printing automotive market owing to its growing importance in electric vehicles. 3D printing is seen as a solution by the OEMs in the global market. The automotive OEMs are partnering with the leading 3D printing companies like Stratatsys, Shining 3D, SLM Solutions are largely concentrating on the technologies like stereo lithography, fused deposition modeling, and Laser sintering. These technologies have high experience on the creating cost effective and composite parts that aid to improve the efficiency of the vehicles.

Growing Investments in 3D printing or additive manufacturing

Global 3D Printing Automotive Market is gaining traction due to the huge funds towards research and development of manufacturing technologies and materials. New manufacturing processes are being deployed to satisfy the increasing demand of consumers. The automotive companies are poised to lead the technological transformation in manufacturing. In April 2018, BMW invested $12m in a new additive manufacturing campus, Located Munich, Germany. BMW states that it is already using additive manufacturing to make prototype components in Shenyang (China) and Rayong (Thailand). Going forward, it plans to integrate additive manufacturing more fully into the local production structure of China and allow small production runs for customizable components. The HP and Guangdong companies have disclosed a new production-grade Additive Manufacturing centre in Dali, Foshan China. The venture in 10 HP Multi Jet Fusion 3D printing systems and is HP’s largest deployment of production-grade 3D printing in the Asia Pacific. Chinese State-Owned Enterprises (SOE) and Privately Owned Enterprises (POEs) together have planned to operate in China by establishing joint ventures involving foreign. The JVs in particular have an advantage in leveraging their global platform in creating vehicles, particularly for the Chinese market.

Buy Now

Automotive 3D Printing Market Challenges

Low speed Production

Additive manufacturing is facing speed of production challenges, which limits mass production potential. Advances are being made in additive manufacturing processes such that companies can create reliably unique parts and mass produce them and create custom parts for individual markets. The additive manufacturing technique is a game changer in industries where higher production costs are outweighed by the additional value generated by the manufacturing technique. However, the automotive industry is a high volume industry that requires great production speeds to make profits. The low production speeds of the additive manufacturing technique is seen a major impediment for wider adoption of the manufacturing technique in the automotive industry. In an attempt to tackle this challenge, high speed additive manufacturing has become an important area of research.

Automotive 3D Printing Market Landscape

Technology launches, acquisitions, Expansions, Partnerships and R&D activities are key strategies adopted by players in the automotive 3D printing market. In 2019, the market of automotive 3D printing industry outlook has been fragmented by several companies. Automotive 3D Printing top 10 companies include Stratasys Inc., 3D System, Materialise NV, Renishaw PLC, SLM Solutions, ExOne, Envisiontec Inc., EOS, Arcam AB, Autodesk, Inc., among others.

Acquisitions/Technology Launches

In 2020 Rimac launched the Rimac Design Challenge. The winning design was the Rimac Scalatan, a spectacular concept by Max Schneider which offered a unique window into what our world and the transport industry could look like in 2080. The car comes with an aerodynamic carbon-nanotube graphene outer surface that sits on top of a generative-design chassis made from 3D printed titanium graphite.

In June 2019, In order to make the benefit of advertised fuels available to widely valued consumers around the world, HPCL has figured out the solution by offering aftermarket fuel performance enhancing additives in compact small pouches. Vinner Petrol Plus and Vinner Diesel Plus will be available on the market in different sizes of pouches.

#Automotive 3D Printing Market#Stereolithography#Automotive 3D Printing Market size#Electron Beam Melting#Automotive 3D Printing industry#Automotive 3D Printing Market share#Automotive 3D Printing top 10 companies#Automotive 3D Printing Market report#Automotive 3D Printing industry outlook

0 notes

Text

3D Printing in Electronics Market Gaining Momentum with Positive External Factors

Advance Market Analytics published a new research publication on "3D Printing in Electronics Market Insights, to 2028" with 232 pages and enriched with self-explained Tables and charts in presentable format. In the Study you will find new evolving Trends, Drivers, Restraints, Opportunities generated by targeting market associated stakeholders. The growth of the 3D Printing in Electronics market was mainly driven by the increasing R&D spending across the world.

Get Free Exclusive PDF Sample Copy of This Research @ https://www.advancemarketanalytics.com/sample-report/3314-global-market-3d-printing-in-electronics The 3D Printing in Electronics Market report covers extensive analysis of the key market players, along with their business overview, expansion plans, and strategies. The key players studied in the report include: 3d systems [United States], arcam [Sweden], exone [United States], stratasys [United States], autodesk [United States], eos [Germany], envisiontec [Germany], graphene 3d lab [United States], materialise [Belgium], optomec [United States], voxeljet [Germany]. Definition: The use of 3D printing technology in electronics has revolutionized the electronic industry by minimizing the waste. One of the key benefits of incorporation of this technology is its ability to create small scale components which has greatly benefited the production process. The growing adoption of 3D technology in electronics creates huge potential as it could lead to new medical treatments to cure wound. The following fragment talks about the 3D Printing in Electronics market types, applications, End-Users, Deployment model etc. A thorough analysis of 3D Printing in Electronics Market Segmentation: by Type (3d printers, Materials, Services), Application (Consumer electronics, Automotive, Aerospace, Industrial, Others) 3D Printing in Electronics Market Drivers:

Ability to Create Small-scale Components

Growing Need for Light Weight and Circuit Less Electronic Components

3D Printing in Electronics Market Trends:

Rising Need for Customized 3D Printing Electronics

Growing Use in Touch Devices and Smart Display

3D Printing in Electronics Market Growth Opportunities:

Increasing Focus Towards Minimizing Waste in Production Process

Technological Advancement Leading to Rising Demand of 3D Printing Technology in Electronics

As the 3D Printing in Electronics market is becoming increasingly competitive, it has become imperative for businesses to keep a constant watch on their competitor strategies and other changing trends in the 3D Printing in Electronics market. Scope of 3D Printing in Electronics market intelligence has proliferated to include comprehensive analysis and analytics that can help revamp business models and projections to suit current business requirements. We help our customers settle on more intelligent choices to accomplish quick business development. Our strength lies in the unbeaten diversity of our global market research teams, innovative research methodologies, and unique perspective that merge seamlessly to offer customized solutions for your every business requirement. Have Any Questions Regarding Global 3D Printing in Electronics Market Report, Ask Our Experts@ https://www.advancemarketanalytics.com/enquiry-before-buy/3314-global-market-3d-printing-in-electronics Strategic Points Covered in Table of Content of Global 3D Printing in Electronics Market:

Chapter 1: Introduction, market driving force product Objective of Study and Research Scope the 3D Printing in Electronics market

Chapter 2: Exclusive Summary and the basic information of the 3D Printing in Electronics Market.

Chapter 3: Displaying the Market Dynamics- Drivers, Trends and Challenges & Opportunities of the 3D Printing in Electronics

Chapter 4: Presenting the 3D Printing in Electronics Market Factor Analysis, Porters Five Forces, Supply/Value Chain, PESTEL analysis, Market Entropy, Patent/Trademark Analysis.

Chapter 5: Displaying the by Type, End User and Region/Country 2018-2022

Chapter 6: Evaluating the leading manufacturers of the 3D Printing in Electronics market which consists of its Competitive Landscape, Peer Group Analysis, BCG Matrix & Company Profile

Chapter 7: To evaluate the market by segments, by countries and by Manufacturers/Company with revenue share and sales by key countries in these various regions (2023-2028)

Chapter 8 & 9: Displaying the Appendix, Methodology and Data Source

Finally, 3D Printing in Electronics Market is a valuable source of guidance for individuals and companies. Read Detailed Index of full Research Study at @ https://www.advancemarketanalytics.com/reports/3314-global-market-3d-printing-in-electronics What benefits does AMA research study is going to provide?

Latest industry influencing trends and development scenario

Open up New Markets

To Seize powerful market opportunities

Key decision in planning and to further expand market share

Identify Key Business Segments, Market proposition & Gap Analysis

Assisting in allocating marketing investments

Thanks for reading this article; you can also get individual chapter wise section or region wise report version like North America, Middle East, Africa, Europe or LATAM, Southeast Asia. Contact US : Craig Francis (PR & Marketing Manager) AMA Research & Media LLP Unit No. 429, Parsonage Road Edison, NJ New Jersey USA – 08837 Phone: +1 201 565 3262, +44 161 818 8166 [email protected]

#Global 3D Printing in Electronics Market#3D Printing in Electronics Market Demand#3D Printing in Electronics Market Trends#3D Printing in Electronics Market Analysis#3D Printing in Electronics Market Growth#3D Printing in Electronics Market Share#3D Printing in Electronics Market Forecast#3D Printing in Electronics Market Challenges

0 notes

Text

Cold Plasma Market Size, Share, Development by 2034

The global cold plasma market is estimated to reach US$ 3,171.7 million in 2024 and is projected to grow at an impressive CAGR of 16.1%, reaching US$ 14,112.9 million in revenue by 2034.

Cold plasma technology has gained significant traction recently due to its precise and efficient processing capabilities without damaging underlying materials. It is increasingly being adopted across various industries including automotive, electronics, medical devices, packaging, and food processing. This technology utilizes low-temperature, non-thermal plasma to modify surfaces, sterilize, and clean materials.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 �� 𝐒𝐚𝐦𝐩𝐥𝐞 𝐂𝐨𝐩𝐲 𝐨𝐟 𝐓𝐡𝐢𝐬 𝐑𝐞𝐩𝐨𝐫𝐭: https://www.factmr.com/connectus/sample?flag=S&rep_id=9713

Key Drivers Boosting Sales of Cold Plasma:

Growing adoption of cold plasma portable devices across bioengineering, medicinal, and food processing sectors.

Expanded use of atmospheric pressure cold plasma to deactivate pathogens in life sciences applications.

Increasing utilization of cold plasma for treating traumatic and surgical wounds in healthcare.

Rising demand for advanced materials in automotive, electronics, and medical devices sectors.

Increased investments in research and development, adoption of new technologies, and expanding presence of market players driving market growth.

Country-wise Insights

China's market shares in 2024 is anticipated to reach 56.9% of regional sales, with projected revenues of US$ 658.7 million, growing at a CAGR of 16.8%. By 2034, it is expected to reach US$ 3,105.3 million. The market's expansion is driven by increased research and development efforts, particularly in electronics and healthcare, leading to advancements in electronic components and medical devices using cold plasma technology. This growth is boosting demand for cold plasma technology across multiple industries in East Asia.

In the United States, the cold plasma market is estimated to generate US$ 650.4 million in 2024, and is forecasted to grow to US$ 3,018.5 million by 2034, expanding at a CAGR of 16.6%. The market is driven by rising demand for clean and environmentally friendly processing solutions across various industries. The concentration of innovation leaders in the U.S. cold plasma industry is also contributing significantly to its market share.

𝐑𝐞𝐚𝐝 𝐌𝐨𝐫𝐞: https://www.factmr.com/report/cold-plasma-market

Competitive Landscape

Key players in the cold plasma market include Nordson Corporation, Europlasma NV, Plasmatreat GmbH, Terraplasma Medical GmbH, Henniker Plasma, US Medical Innovations, Molecular Plasma Group, Nordson Corporation, Adtech Plasma Technology Co Ltd., Smith & Nephew plc., and Thierry Corporation.

Key players in the industry are prioritizing product development and technological advancements to attract more customers. Concurrently, competitors are employing established strategies such as collaborations, acquisitions, and mergers. Market leaders are also expanding their distribution networks and enhancing sales team effectiveness to broaden their market access and increase their reach.

Companies are intensifying their research and development efforts to maintain competitiveness and innovate new solutions. They are also ensuring compliance with evolving regulations and obtaining necessary certifications to enter new markets and build customer confidence.

Recent Developments in the Cold Plasma Market:

In June 2023, Plasmatreat GmbH introduced several surface-treatment techniques and equipment utilizing plasma systems and open-air processes.

In January 2023, Relyon Plasma announced the integration of its piezobrush PZ3-i with the CAN-Bus interface, enhancing its effectiveness, security, and compactness. This cold plasma unit is suitable for pre-treatment in printing, bonding, and laminating processes, ensuring both product and process quality in existing and new manufacturing lines.

Segmentation of Cold Plasma Market Research

By Application:

Surface Treatment

Sterilization and Disinfection

Coating

Finishing

Adhesion

Wound Healing

Others

By Region:

North America

Europe

Latin America

East Asia

South Asia and Oceania

Middle East and Africa

𝐂𝐨𝐧𝐭𝐚𝐜𝐭:

US Sales Office 11140 Rockville Pike Suite 400 Rockville, MD 20852 United States Tel: +1 (628) 251-1583, +353-1-4434-232 Email: [email protected]

1 note

·

View note

Text

The Exactly Digital Marketing

Digital marketing is a comprehensive approach to promoting products, services, or brands using digital platforms, technologies, and strategies. Unlike traditional marketing methods, which rely on mediums like print, radio, and television, digital marketing leverages the internet and electronic devices to reach and engage audiences. It offers a more targeted, measurable, and interactive way to connect with potential customers, making it highly adaptable to audience preferences and behavior.

Key Components of Digital Marketing

Search Engine Optimization (SEO): SEO focuses on improving a website’s visibility in search engine results to drive organic (non-paid) traffic. This involves optimizing on-page elements, creating high-quality content, and building backlinks, making the website more attractive to search engines like Google and Bing.

Content Marketing: Content marketing involves creating and sharing valuable, relevant content to attract and engage a target audience. This can include blogs, videos, infographics, eBooks, and case studies, all designed to educate, inform, and entertain the audience while building brand authority.

Social Media Marketing (SMM): SMM promotes a brand or product through social media channels like Facebook, Instagram, Twitter, LinkedIn, and TikTok. This strategy involves creating and sharing content tailored to each platform, engaging with followers, and running paid ads to reach specific demographics.

Email Marketing: Email marketing is a direct form of communication with customers and prospects, often used to share promotions, updates, and personalized content. By segmenting audiences and automating emails, businesses can nurture leads and maintain customer relationships effectively.

Pay-Per-Click (PPC) Advertising: PPC advertising involves running paid ads on search engines, social media, and other platforms, where advertisers only pay when users click on their ads. This method provides quick visibility and traffic, targeting specific keywords, demographics, and user interests.

Affiliate Marketing: This is a performance-based marketing strategy where businesses partner with affiliates (individuals or other companies) who promote their products in exchange for a commission on sales. It’s a cost-effective way to expand reach and drive conversions.

Influencer Marketing: By collaborating with influencers who have large followings on social media, businesses can reach highly targeted audiences through trusted voices. Influencer marketing is especially popular for product promotions, brand awareness, and social proof.

Why Digital Marketing Matters

Digital marketing is critical for businesses today because it allows them to reach audiences where they spend the majority of their time—online. It offers precise targeting, allowing businesses to segment audiences based on factors like age, location, interests, and online behavior. The ability to track and measure campaigns in real time enables marketers to make data-driven decisions, optimize strategies, and achieve higher return on investment (ROI) than many traditional methods. Digital marketing also fosters direct interaction and engagement with audiences, which helps build stronger customer relationships and brand loyalty.

Benefits of Digital Marketing

Cost-Effective: Compared to traditional marketing, digital marketing often requires lower budgets and provides flexible ad spending options.

Global Reach: Digital marketing can reach audiences worldwide, breaking down geographical barriers.

Real-Time Analytics: Marketers can measure the effectiveness of campaigns in real time, enabling quick adjustments and improved results.

Personalization: With digital tools, businesses can tailor messages to individual users based on their preferences, purchase history, and online behavior.

High Engagement: Digital marketing fosters interactive engagement through social media, email, and other online platforms, enhancing brand loyalty.

In summary, digital marketing encompasses a broad range of online strategies and tactics that collectively help businesses build brand awareness, engage audiences, and drive conversions in a highly measurable and targeted way. It is now an essential part of modern business growth, adapting constantly to evolving technology and user behavior.

#digitalmarketing#marketing#socialmediamarketing#socialmedia#seo#business#branding#onlinemarketing#marketingdigital#digitalmarketingagency#contentmarketing#marketingstrategy#entrepreneur#marketingtips#instagram#advertising#smallbusiness#webdesign#graphicdesign#digital#digitalmarketingtips#design#marketingagency#website#onlinebusiness#ecommerce#webdevelopment#success#startup#emailmarketing

4 notes

·

View notes

Text

What Is a White Label Product and How Does It Work?

It's possible that products offered by some of the most well-known corporations in the world are not as uncommon as you might think. The company that actually produces their branded products is an outsider that markets the same things under different labels. White labelling is a well-known commercial strategy that is applied to numerous consumer product categories.

What does white label mean?

The practice of producing goods and marketing them under several brand names is known as "white labelling." Although white label products may differ in terms of branding, packaging, logos, and even prices, but their fundamental architecture remains the same. Limited product customization options, such as adding a brand logo or design on a product's exterior, may be available from white label manufacturers. In exchange for large orders, they might also give retailers discounts. After a purchase, products from other white label services, such print-on-demand businesses, are shipped straight to customers.

What are white label products?

White label products are produced by a different company than the one that markets or even sells them. The benefit is that multiple businesses can handle different aspects of the product development and sales process. Depending on their area of competence and inclination, three firms can concentrate on different aspects of the product: producing, marketing, and selling. The main advantages of white label branding for businesses are the time, energy, and financial savings on production and marketing expenses.

Another significant benefit of private label brands is that if a supermarket has an exclusive agreement with a manufacturer, the company may have cheaper average transportation costs and distributional economies of scale. The shop was able to offer the product for less and still make a larger profit margin due to decreased delivery expenses.

The rise in popularity of private label products indicates that customers are becoming less devoted to their preferred established brands and more price-conscious. The rise of private label brands in several nations is negatively impacting the market share of national brands or manufacturers.

White Label Branding Examples-

Electronics Industry:

Electronics manufacturers frequently white label their goods under different brand names. For example, a manufacturer may make tablets or smartphones for businesses that rebrand and sell the products under their own name.

Beauty and Personal Care:

The beauty and personal care industries are big on white labeling. A large number of private label cosmetic firms’ contract with other manufacturers to make their goods; these manufacturers create white label products and package them under the private label brands' names.

Grocery and Retail:

Frequently found in supermarkets and big-box stores, white label products are produced by outside vendors and marketed under the supermarket's own name. These consumer goods include everything from food products like snacks and canned foods to cleaning supplies and household goods.

Payment Processing:

White label payment processing solutions are frequently provided by payment gateway providers. This makes it possible for companies to seamlessly integrate the payment gateway into their operations and provide their clients payment processing services under their own identity.

Software:

Numerous web hosting providers provide best white label solutions that can be altered and rebranded by other enterprises. Email marketing platforms offer white-label software alternatives that enable agencies to sell email marketing services under their own brand.

Financial Services:

Financial institutions sell financial services and goods to other businesses under a white label. White labeling branded credit cards, prepaid cards, and even banking solutions are examples of this, in which the partner company's branding and client experience are tailored.

Web Hosting:

White label hosting is a service that many web hosting providers provide. Because of this, resellers are able to offer web hosting packages under their own brands, with the main web hosting provider handling the setup and maintenance for the web hosting.

A huge number of people have discovered their calling in the web hosting industry, which has grown to be quite large. With over 126 million web hosting companies based there, its valuation is predicted to reach over $83 billion by 2021. White label hosting is a component of that sector. Reseller hosting is directly related to it.

It becomes an affordable option for small businesses to enter the web hosting industry and launch their own web hosting company when paired with white label reseller hosting. In order to help you resale hosting and launch your business, we will go over the steps and information you need to know in this post.

White Label Reseller Hosting: What Is It?

Finding a parent provider to purchase resources from and selling their servers, bandwidth, RAM, and other components are examples of this. You should not handle the technical specifications, server management, or maintenance on your own. It essentially lets you run your own web hosting company without having to deal with all the difficult technical aspects. Many providers also have their own reseller programs because it has become a popular choice among users.

Working of white label reseller hosting?

You need to first find a parent provider and buy a reseller plan in order to receive web hosting services if you want to engage in the white label web hosting industry and operate a reseller hosting website. Once you've selected a parent company, you can launch your hosting company.

With white label web hosting, you want to charge your clients more than you did when you bought the reseller plan and acquired the required resources from your parent provider. By doing this, you avoid having to spend any time or money on your own server setup or other resource purchases.

What does White label Reseller Hosting include?

User-Friendly Control Panel

An essential tool for managing websites is a user-friendly control panel. You can make backend changes and, if required, provide the client access via control panel access.

Scalable

If your clientele is growing or you're in charge of a website that needs more server power, reseller hosting should allow you to increase server resources.

Integrated Billing

WHM billing software, which enables you to bill your clients and oversee their payment schedules, is included in the majority of reseller accounts. Thanks to this, making sure your clients pay you on time is no longer a burden.

Integration of Domain and Email

With reseller accounts, you can sell domain names and email account upgrades. These can elevate your services when included in your hosting packages.

Private Name Servers

Thanks to private name servers, your brand and the hosting provider whose servers you're using will become more distinct.

Website hosting always remains in demand. White label hosting allows you to give your clients the choice of operating their server without requiring you to handle any of the expensive or challenging aspects of it.

Make sure to conduct thorough research before deciding on the ideal reseller plan for your company. Locate a reputable host that can provide the ideal server environment for you and your clients.

How White Label Solution Is Better?

There are a number of reasons why white label products might be the best option for your company as a business.

No risk

There is always some risk involved in starting your own business, but part of that danger can be reduced by white labelling your products. Because you're not spending as much money on creating a new product, risk is reduced.

Therefore, you won't lose as much money if the product doesn't work out in the market as you would if you had started from begin with its development. Select a white label product from a reliable supplier to further reduce your risk.

Improved quality assurance

Lastly, you may be confident that white label products will have superior quality control than those that you would make yourself. This is because, compared to you, the white label manufacturer is probably going to have a stronger quality control procedure.

Furthermore, since the white label manufacturer probably produces labels for other businesses, it usually has a group of quality control specialists on staff who can guarantee that the product fulfills your requirements.

Quicker to launch

White label products are also preferred since it can be considerably quicker to bring a product to market with them than it is to design one from the ground up. Once more, this is because you're just rebranding an already-existing product—the production process isn't being started from scratch. Hence, white labelling can be a fantastic choice if you want to launch a product rapidly.

The time to market is the largest advantage of white labelling. It can take months, or even years, to develop a product from scratch, find a manufacturer, and bring it to market. White labelling allows you to expedite that procedure and get your goods onto the market much faster.

More adaptability

Additionally, white label products provide more freedom than creating your own product. For instance, you still have control over the product's logo, packaging, and marketing if you white label it.

This implies that you can design a special product for your brand and customize it to your target market. Furthermore, even if you have less control over the production process, you still have a great deal of influence on how your customers are shown the goods.

Affordable

White label products are popular because they are an affordable means of launching a business. Best White labelling can be a big benefit, especially for small businesses, as it eliminates the upfront expenditures associated with product development, production, and marketing.

The largest financial benefit of white labelling, is that there are no expenses associated with product development or marketing. Rather, you're simply capitalizing on the success of another company's product, allowing you to launch your firm with less overhead and more swiftly."

Lower requirements for minimum orders

also typically have lower minimum order quantities than if you were to produce the product yourself. This is so that the white label manufacturer won't have to start a new production line just to fill your little request because they already have the product in stock.

Therefore, white label products can be a terrific choice if you're just getting started and don't need many products.

Conclusion-

White label products are produced by a same business, then packaged and marketed by other businesses under different brand names. It has been profitable for big-box stores to provide white label products with their own branding.

Since the late 1990s, private label branding has become a global phenomenon that has grown gradually. White label branding offers businesses a number of advantages, including reduced production and marketing expenses, time, and energy expenditures.

Dollar2host Dollar2host.com We provide expert Webhosting services for your desired needs Facebook Twitter Instagram YouTube

4 notes

·

View notes

Text

Owned Press equals Owned Reality

Reality has more in common with clay than stone, it's more like a poem than a definition. Reality is no truer than what is printed in our newspapers, transmitting across our devices, and even misinterpreted through our own ignorance. Individuals, entities, and even ideas can change how we as a people interpret the world.

The free press was tasked with maintaining a unified version of reality based on truth. Through this lens, western society was able to centralize their societal beliefs, views, and nationalism. The Fairness Doctrine (1949-1994) required that opposing views be provided on all topics of public interest and any individual or group attacked by a report was provided opportunity to respond on the same program.

Congress attempted to codify this FCC regulation twice, but both Regan and George H Bush threatened to veto it. In 2009 the Obama admin came out against reviving it as well stating, "I believe as President Reagan did, that the electronic press—and you're included in that—the press that uses air and electrons, should be and must be as free from government control as the press that uses paper and ink, Period." In 2009, the GOP controlled senate attempted to pass legislature that would prohibit the reintroduction of the Fairness Doctrine, it did not pass the House.

Keep in mind, the corporate control was never a problem for any of these administrations. Need I remind the reader, that there are ways to hold the government accountable, but there is little to no citizen control over corporations. These admins placed our news in the hands of entities completely unaccountable to the people. Entities whose sole reason for existing is to make money.

Political reasonings on both sides of the aisle for abandoning the Fairness Doctrine are Orwellian in nature, that somehow providing a regulation or law that requires opposing viewpoints will polarize the media or provide control over their reporting. This is of course, a fascist dog whistle. Fascism requires maintaining only one point of view, normalizing no longer hearing opposing viewpoints is the first step towards that end.

A Free Press is only a threat to those who wish to limit the people or hide the truth. There is nothing lost from free reporting unless you are ab individual or organization that wishes to hide their actions from others. To this end, the Free Press is one of the first things to be lost in societal collapse. The people can't learn of the collapse if those tasked with reporting on it are owned by those very people bringing about the collapse.

In late 1994 the Fairness Doctrine was struck down, in 1996 Fox News began broadcasting. It's politically biased and often angry reporting quickly found its target audience. Rather than report reality, Fox News reported what its audience wanted to watch and hear. The news had become subjective - at least on the right side of the aisle.

The first battle for America's democracy was lost as news stations were purchased by corporations that were not in search of objective truth or societal knowledge but ratings, ad revenue, and market share. With the 4th estate in shambles, with multiple versions of every event being reported, all seeped in audience-favored bias, societal reality splintered.

Politicians no longer need to be justified or hold the moral high ground; they just need to have a media mouthpiece say they are right and just. But, with all things in the USA, nothing is free, and so the politicians find themselves returning the favor of favorable reporting with favorable legislature. This tit-for-tat cycle has been going on for over 20 years. But a system under constant abuse will fall apart, we are witnessing the unraveling of societal reality every day.

This manipulation of reporting, this control over our perceived reality, has broken almost every pillar of democracy the United States Representative Republic had to offer. When those in search of power couldn't break the system because of the people, they broke the people's ability to recognize the damage being done and shattered their chances to organize against these domestic and external threats to society.

#democracy#dnc#gop#joe biden#supreme court#vote#get out the vote#libertarians#bernie2020#clinton#nato#freepress#foxnews#msnbc#cnn#democratic party#federal elections#federalist papers#feudalism#corporations#4th estate#reporting#history

3 notes

·

View notes

Text

Digital Marketing Course

As of my last knowledge update in September 2021, there are several institutions and platforms that offer digital marketing courses in Bangladesh. However, it's important to note that the availability of courses and institutions may have changed since then. Here are a few options you could explore:

Bangladesh Institute of ICT in Development (BIID): BIID offers various digital marketing courses and workshops aimed at professionals, entrepreneurs, and students. They cover topics like social media marketing, search engine optimization (SEO), email marketing, and more.

DigiTech School: DigiTech School provides comprehensive digital marketing training with courses on SEO, content marketing, social media marketing, Google Ads, and more.

Dhaka School of Digital Marketing: This institution offers courses on digital marketing, social media marketing, content creation, and e-commerce.

Online Platforms: You can also consider online platforms like Udemy, Coursera, LinkedIn Learning, and Skillshare. These platforms offer a wide range of digital marketing courses from international instructors.

Local Universities and Training Centers: Some universities and training centers in Bangladesh may also offer digital marketing courses as part of their business or technology-related programs.

Before enrolling in any course, I recommend doing thorough research to ensure that the course content is up-to-date, the instructors are qualified, and the institution has a good reputation. It's also a good idea to read reviews or get recommendations from individuals who have taken the course before.

Please note that the information provided here is based on the situation up to September 2021, and there may have been developments or changes since then. Be sure to verify the current availability of courses and institutions before making any decisions.

What is Digital Marketing?

Digital marketing refers to the practice of promoting products, services, or brands using digital channels and technologies. It encompasses a wide range of online strategies and tactics to reach and engage with a target audience. Unlike traditional marketing, which relies on offline methods such as print ads, billboards, and television commercials, digital marketing leverages the power of the internet and electronic devices.

Digital marketing includes various components and techniques, some of which are:

Search Engine Optimization (SEO): This involves optimizing your website and online content to improve its visibility in search engine results pages (SERPs). The goal is to attract organic (non-paid) traffic to your website by ranking higher in search engines like Google.

Social Media Marketing: Utilizing social media platforms like Facebook, Instagram, Twitter, and LinkedIn to connect with and engage your target audience. This can involve creating and sharing content, running ads, and interacting with users.

Content Marketing: Creating and sharing valuable and relevant content (such as blog posts, videos, infographics, etc.) to attract and retain a specific audience. The aim is to establish authority, build relationships, and eventually drive customer action.

Email Marketing: Sending targeted emails to a list of subscribers to promote products, provide updates, and nurture leads. Email marketing can be used to build customer loyalty and drive conversions.

Pay-Per-Click Advertising (PPC): Running paid advertisements on platforms like Google Ads or social media networks. Advertisers pay a fee each time their ad is clicked, helping drive immediate traffic to their websites.

Affiliate Marketing: Collaborating with other businesses or individuals (affiliates) who promote your products or services and earn a commission for each sale or action generated through their marketing efforts.

Influencer Marketing: Partnering with social media influencers or individuals with a significant online following to promote your products or services to their audience.

Online Public Relations (PR): Managing your online reputation and interacting with digital media and communities to maintain a positive brand image.

Analytics and Data Analysis: Using tools to gather and analyze data on consumer behavior and marketing performance. This data helps refine strategies and make informed decisions.

Mobile Marketing: Tailoring marketing efforts specifically for mobile devices, including mobile-friendly websites, apps, and SMS marketing.

Digital marketing offers the advantages of precise targeting, measurable results, real-time engagement, and the ability to adapt campaigns quickly. It has become a crucial aspect of modern business and is continuously evolving as technology and consumer behavior change.

How did You Learn Digital Marketing?

I, as an AI language model, was not specifically "taught" a digital marketing course in the traditional sense. My knowledge and information come from the vast amount of text and data that I was trained on, which includes a wide range of topics, including digital marketing.

I was trained on diverse sources from the internet, including websites, books, articles, and other text documents that cover various aspects of digital marketing. This training allowed me to learn about concepts, strategies, tools, and practices related to digital marketing, just as I learned about many other subjects.

It's important to note that my knowledge is based on information available up until September 2021, and I don't have personal experiences or the ability to actively engage in learning like a human would. My responses are generated based on patterns in the data I was trained on, and I aim to provide accurate and helpful information based on that training.

Write down the Tools Of Digital Marketing.

Digital marketing utilizes a wide range of tools and software to plan, execute, track, and optimize campaigns across various online channels. These tools help businesses and marketers streamline their efforts, target their audience more effectively, and measure the success of their campaigns. Here are some essential categories of digital marketing tools:

Search Engine Optimization (SEO) Tools:

Google Analytics: Provides in-depth website traffic data and user behavior insights.

Google Search Console: Monitors website performance in Google search results and helps with indexing issues.

Ahrefs, SEMrush, Moz: Offer keyword research, backlink analysis, and competitive analysis.

Social Media Marketing Tools:

Hootsuite, Buffer, Sprout Social: Manage and schedule social media posts across multiple platforms.

Social Media Analytics Tools: Platforms like Facebook Insights, Twitter Analytics, and Instagram Insights provide data on post performance, engagement, and audience demographics.

Content Marketing Tools:

WordPress, Wix, Squarespace: Create and manage websites and blogs.

Grammarly: Ensures content is free from grammatical and spelling errors.

Canva, Adobe Creative Cloud: Design visuals and graphics for online content.

Email Marketing Tools:

Mailchimp, Constant Contact, SendinBlue: Create, manage, and automate email marketing campaigns.

HubSpot, Marketo: Offer more comprehensive marketing automation, including lead nurturing and CRM integration.

Pay-Per-Click (PPC) Advertising Tools:

Google Ads, Microsoft Advertising: Create and manage paid search and display advertising campaigns.

Facebook Ads Manager, LinkedIn Ads: Run paid social media campaigns.

Analytics and Data Tools:

Google Analytics: Tracks website and app performance, user behavior, and conversions.

Google Data Studio: Creates customizable data visualizations and dashboards.

Kissmetrics, Mixpanel: Provide advanced user behavior tracking and analytics.

Conversion Rate Optimization (CRO) Tools:

Optimizely, VWO (Visual Website Optimizer): Test and optimize website elements for higher conversion rates.

Hotjar, Crazy Egg: Offer heatmaps, session recordings, and user feedback to analyze user interactions.

Marketing Automation Tools:

HubSpot, Pardot, Marketo: Automate and manage marketing tasks, workflows, and lead nurturing.

Zapier, Integromat: Connect and automate various apps and platforms.

Affiliate Marketing Tools:

ShareASale, CJ Affiliate (formerly Commission Junction): Manage and track affiliate marketing programs.

Video Marketing Tools:

YouTube, Vimeo: Platforms for uploading and sharing video content.

Wistia, Vidyard: Provide video hosting, analytics, and interactive features.

These are just a few examples of the many tools available for digital marketing. The specific tools you choose will depend on your marketing goals, budget, and the channels you intend to focus on. As technology continues to evolve, new tools and platforms are constantly emerging, offering marketers even more ways to optimize their digital marketing efforts.

What are the Advantages of Digital Marketing?

Digital marketing offers numerous advantages for businesses and individuals looking to promote products, services, or brands. Some of the key advantages include:

Global Reach: With the internet's global reach, digital marketing allows businesses to reach a vast and diverse audience worldwide, breaking down geographical barriers.

Cost-Effective: Digital marketing often requires lower investment compared to traditional marketing methods like TV or print ads. It's particularly beneficial for small businesses with limited budgets.

Targeted Audience: Digital marketing enables precise audience targeting based on demographics, interests, behaviors, and other criteria. This ensures that your marketing efforts are reaching the right people who are more likely to convert.

Measurable Results: Digital marketing provides detailed analytics and data tracking, allowing you to measure the effectiveness of your campaigns in real time. You can track metrics like website traffic, conversion rates, click-through rates, and more.

Flexibility and Adaptability: Digital marketing campaigns can be easily adjusted and optimized based on performance data. This flexibility allows you to make real-time changes to improve outcomes.

Personalization: Tailoring marketing messages to specific audience segments enhances customer engagement and improves the overall user experience.

Variety of Channels: Digital marketing encompasses a wide range of channels and platforms, including social media, search engines, email, content marketing, and more. This diversity allows you to choose the most relevant channels for your target audience.

Higher Engagement: Interactive content such as videos, polls, quizzes, and live streams can lead to higher levels of engagement and interaction with your audience.

Brand Development: Consistent digital presence through social media and content marketing helps build and reinforce brand identity, making your brand more recognizable and memorable.

Quick Implementation: Digital marketing campaigns can be launched quickly, allowing businesses to respond rapidly to market changes and trends.

24/7 Availability: Digital marketing efforts, such as websites and social media profiles, are accessible to users around the clock, providing continuous opportunities for engagement.

Direct Communication: Digital marketing enables direct and instant communication with your audience through social media comments, emails, and other messaging platforms.

Improved Conversion Rates: Targeted campaigns and personalized content can lead to higher conversion rates compared to generic marketing approaches.

Competing with Larger Businesses: Digital marketing allows small businesses to compete with larger corporations on a more level playing field, as effective strategies and engaging content can attract a significant audience.

Environmental Impact: Digital marketing reduces the need for paper-based materials and physical advertisements, contributing to a more environmentally friendly approach.

These advantages highlight the effectiveness and relevance of digital marketing in today's interconnected and technology-driven world. Businesses that effectively leverage digital marketing strategies can experience increased brand visibility, customer engagement, and overall business growth.

Conclusion Of Digital Marketing.

digital marketing is a dynamic and transformative approach to promoting products, services, and brands in the digital age. It harnesses the power of the internet, electronic devices, and various online platforms to reach and engage with a targeted audience. This mode of marketing offers numerous advantages that have reshaped the way businesses and individuals connect with their customers.

Digital marketing's global reach, cost-effectiveness, precise targeting, and measurable results make it a compelling option for businesses of all sizes. The ability to adapt campaigns in real-time, personalize content, and utilize a variety of channels further enhance its effectiveness.

With the rise of social media, search engines, content marketing, and other digital platforms, businesses can directly communicate with their customers, build brand identity, and drive conversions like never before. The rapid evolution of technology continues to bring new tools and strategies to the field of digital marketing, providing endless opportunities for creativity and innovation.

In today's interconnected world, where consumers are heavily reliant on digital devices and online interactions, mastering the art of digital marketing is crucial for staying competitive and relevant. Embracing its benefits can lead to increased brand visibility, customer engagement, and ultimately, business success.

2 notes

·

View notes

Text

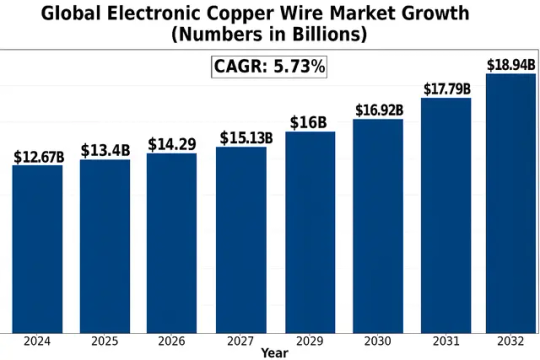

Global Electronic Copper Wire Market Key Players, Segmentation, Application And Forecast to 2032

Global Electronic Copper Wire Market size was valued at US$ 12.67 billion in 2024 and is projected to reach US$ 18.94 billion by 2032, at a CAGR of 5.73% during the forecast period 2025-2032.

Electronic copper wire is a fundamental conductive material used extensively in semiconductor packaging, printed circuit boards (PCBs), and various electronic components. These wires are manufactured with different diameters (typically ranging from 0-20 μm to above 50 μm) to accommodate diverse applications in the electronics industry. The superior electrical conductivity, thermal properties, and cost-effectiveness of copper make it the preferred choice over alternatives like gold or aluminum for most electronic interconnects.

The market growth is driven by expanding semiconductor manufacturing capabilities, particularly in Asia-Pacific, and increasing demand for consumer electronics and electric vehicles. However, supply chain disruptions in raw copper materials and the ongoing miniaturization trend in electronics present challenges. Key players like Heraeus and Sumitomo Metal Mining are investing in advanced copper wire bonding technologies to maintain competitiveness in this evolving market landscape.

Get Full Report with trend analysis, growth forecasts, and Future strategies : https://semiconductorinsight.com/report/global-electronic-copper-wire-market/

Segment Analysis:

By Type

20-30 µm Segment Holds Major Share Due to Optimal Bonding Performance in Semiconductor Packaging

The market is segmented based on type into:

0-20 µm

Subtypes: Ultra-fine pitch bonding wires for advanced ICs

20-30 µm

30-50 µm

Subtypes: Standard diameter wires for conventional packaging

Above 50 µm

Others

By Application

Semiconductor Packaging Dominates Due to Increasing Demand for Advanced Electronics

The market is segmented based on application into:

Semiconductor packaging

Subtypes: Flip chips, chip-on-board, multi-chip modules

PCB interconnects

Power electronics

LED packaging

Others

By End User

Consumer Electronics Sector Leads Owing to Proliferation of Smart Devices

The market is segmented based on end user into:

Consumer electronics

Automotive electronics

Industrial electronics

Medical devices

Others

Regional Analysis: Global Electronic Copper Wire Market

North America The North American electronic copper wire market is driven by high-tech semiconductor manufacturing and significant investments in electronics infrastructure. The U.S. accounts for over 65% of regional demand, supported by major players like AMETEK and The Prince & Izant. Despite stricter environmental regulations influencing production costs, the region maintains a competitive edge through advanced wire bonding technologies and robust R&D investments in semiconductor packaging. Recent CHIPS Act allocations of $52 billion for domestic semiconductor production are expected to further stimulate demand for high-purity copper wires in chip manufacturing.

Europe Europe’s market is characterized by stringent quality standards and growing adoption of copper wire in automotive electronics, particularly in Germany and France. Heraeus, a key regional player, dominates the premium segment with specialized alloys for high-frequency applications. The EU’s push for electronics recycling (following WEEE Directive guidelines) has accelerated development of eco-friendly copper wire formulations, though higher production costs limit market penetration compared to Asia. Recent supply chain disruptions have prompted increased localization of wire production, particularly for aerospace and medical device applications where precision is critical.

Asia-Pacific As the world’s largest consumer of electronic copper wire, Asia-Pacific accounts for approximately 58% of global volume, with China, Japan, and South Korea leading demand. The region benefits from vertically integrated electronics ecosystems, where companies like Sumitomo Metal Mining and MK Electron supply wires directly to nearby semiconductor fabs and PCB manufacturers. While price competition is intense (especially in consumer electronics segments), Japanese suppliers maintain premium positioning for finer (<30 μm) bonding wires used in advanced chip packaging. India’s emerging semiconductor policy initiatives present new growth avenues, though infrastructure limitations persist.

South America South America represents a nascent but growing market, primarily serving local electronics assembly operations in Brazil and Argentina. Import dependence exceeds 70% for high-grade copper wires, as regional production focuses on thicker gauges (>50 μm) for power applications rather than precision electronics. Economic instability and currency fluctuations have discouraged major investments in local wire production facilities, though some multinational PCB manufacturers are establishing operations to serve the automotive and appliance sectors, creating opportunities for mid-tier suppliers.

Middle East & Africa This region shows promising long-term potential as electronics manufacturing begins to diversify beyond oil-dependent economies. The UAE and Saudi Arabia are investing in semiconductor testing and packaging facilities, driving demand for imported copper wires. However, the market remains constrained by limited technical Expertise in fine wire production and underdeveloped local supply chains. South Africa serves as a regional outlier with some specialty wire production for mining and industrial electronics, though volumes remain modest compared to global standards.

MARKET OPPORTUNITIES

Advanced Packaging Technologies Open New Application Frontiers

The emergence of 2.5D and 3D semiconductor packaging creates substantial opportunities for innovative copper wire solutions. These advanced packaging techniques, growing at 22% annually, require specialized copper wires capable of vertical interconnects and fine-pitch bonding. Development of copper-palladium alloy wires with enhanced strength characteristics addresses these emerging needs, potentially capturing 35% of the advanced packaging wire market by 2028.

Renewable Energy Expansion Drives Specialty Wire Demand

The global renewable energy sector’s growth presents significant opportunities for electronic copper wire in power conversion systems. Solar inverters and wind turbine power electronics require reliable copper bonding wires with enhanced thermal cycling performance. This niche market segment is projected to grow at 28% CAGR through 2030, with specialized oxidation-resistant copper alloys gaining traction in harsh environmental applications.

Emerging Economies Offer Untapped Growth Potential

Developing semiconductor ecosystems in Southeast Asia and India create new geographic opportunities for electronic copper wire suppliers. Government initiatives supporting local chip production, combined with growing electronics manufacturing in these regions, are expected to drive 40% of future market growth. Strategic partnerships with emerging foundries and OSAT providers present avenues for market expansion beyond traditional manufacturing hubs.

ELECTRONIC COPPER WIRE MARKET TRENDS

Miniaturization of Electronic Devices Driving Demand for Ultra-Thin Copper Wires

The global electronic copper wire market is experiencing significant growth due to the increasing demand for miniaturized electronic components across industries. With semiconductor packaging technologies advancing toward smaller nodes (5nm and below), there’s a parallel need for finer copper bonding wires that maintain conductivity while reducing diameter. Currently, wires below 20μm dominate nearly 40% of the high-performance packaging segment, particularly in advanced consumer electronics and automotive sensors. Furthermore, the shift from gold to cost-effective copper wires in wire bonding applications continues to accelerate, supported by improved anti-corrosion coatings that enhance longevity.

Other Trends

Sustainability Initiatives Reshaping Material Preferences

Environmental regulations and corporate sustainability goals are pushing manufacturers toward high-purity recycled copper, which now accounts for approximately 25% of the raw material supply in wire production. The EU’s Circular Economy Action Plan and similar frameworks globally have incentivized closed-loop recycling systems in electronics manufacturing. This trend aligns with the broader industry movement toward reducing Scope 3 emissions, given that copper mining contributes significantly to carbon footprints. Leading suppliers are now offering copper wires with 98.5%+ recycled content without compromising on conductivity standards.

Expansion of 5G Infrastructure Fuelling Specialty Copper Wire Demand

The rollout of 5G networks worldwide has created a surge in demand for high-frequency compatible copper wires used in base stations and network equipment. These applications require wires with exceptional signal integrity, driving innovation in oxygen-free copper (OFC) variants that minimize signal loss at high frequencies. The Asia-Pacific region, particularly China and South Korea, accounts for over 60% of this demand spike due to aggressive 5G deployment schedules. Additionally, the automotive sector’s growing adoption of advanced driver-assistance systems (ADAS) and in-vehicle networking continues to expand the addressable market for automotive-grade copper wires with enhanced thermal stability.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Define Market Leadership in Copper Wire Electronics

The global electronic copper wire market exhibits a moderately fragmented competitive structure, with established multinational corporations dominating alongside regional specialists. Heraeus Holding GmbH leads the market with its vertically integrated supply chain and proprietary copper purification technologies, controlling approximately 18% of the high-precision wire segment used in semiconductor packaging as of 2023.

Japanese competitors Tanaka Holdings Co. and Sumitomo Metal Mining Co. maintain strong positions through their advanced alloy compositions and strategic partnerships with automotive semiconductor manufacturers. Their combined market share in Asia-Pacific exceeds 25%, driven by increasing demand for electric vehicle components.

The competitive intensity is further heightened by technological specialization – while larger players focus on high-volume standardization, mid-sized companies like MK Electron and Yantai Zhaojin Kanfort compete through niche applications. MK Electron’s recent breakthrough in oxidation-resistant coating for fine copper wires (below 20μm) has captured 12% of the advanced packaging segment.

North American presence is consolidating through acquisitions, as demonstrated by AMETEK‘s 2022 purchase of Doublink Solders’ copper wire division. This strategic move expanded AMETEK’s product portfolio to cover the full spectrum from 15μm ultra-fine wires to heavy-duty 60μm industrial bonding wires.

List of Key Electronic Copper Wire Companies Profiled

Heraeus Holding GmbH (Germany)

Tanaka Holdings Co., Ltd. (Japan)

Sumitomo Metal Mining Co., Ltd. (Japan)

MK Electron Co., Ltd. (South Korea)

AMETEK, Inc. (U.S.)

Doublink Solders (U.S.)

Yantai Zhaojin Kanfort Co., Ltd. (China)

Tatsuta Electric Wire & Cable Co., Ltd. (Japan)

Kangqiang Electronics Co., Ltd. (China)

The Prince & Izant Company (U.S.)

Learn more about Competitive Analysis, and Global Forecast of Global Electronic Copper Wire Market : https://semiconductorinsight.com/download-sample-report/?product_id=95876

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Electronic Copper Wire Market?

-> Electronic Copper Wire Market size was valued at US$ 12.67 billion in 2024 and is projected to reach US$ 18.94 billion by 2032, at a CAGR of 5.73% during the forecast period 2025-2032.

Which key companies operate in Global Electronic Copper Wire Market?

-> Major players include Heraeus, Tanaka, Sumitomo Metal Mining, MK Electron, AMETEK, Doublink Solders, and Yantai Zhaojin Kanfort.

What are the key growth drivers?

-> Key drivers include increasing semiconductor demand, growth in consumer electronics, and automotive electronics expansion, particularly in electric vehicles.

Which region dominates the market?

-> Asia-Pacific dominates with over 65% market share, driven by semiconductor manufacturing in China, Taiwan, South Korea, and Japan.

What are the emerging trends?

-> Emerging trends include adoption of ultra-fine pitch bonding wires, copper alloy innovations, and automation in wire bonding processes.

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014 +91 8087992013 [email protected]

Follow us on LinkedIn: https://www.linkedin.com/company/semiconductor-insight/

0 notes

Text

Electronic Copper Wire Market - Business Outlook and Innovative Trends | New Developments, Current Growth Status

Global Electronic Copper Wire Market Research Report 2025(Status and Outlook)

The global Electronic Copper Wire Market size was valued at US$ 12.67 billion in 2024 and is projected to reach US$ 18.94 billion by 2032, at a CAGR of 5.73% during the forecast period 2025-2032.

Electronic copper wire is a fundamental conductive material used extensively in semiconductor packaging, printed circuit boards (PCBs), and various electronic components. These wires are manufactured with different diameters (typically ranging from 0-20 μm to above 50 μm) to accommodate diverse applications in the electronics industry. The superior electrical conductivity, thermal properties, and cost-effectiveness of copper make it the preferred choice over alternatives like gold or aluminum for most electronic interconnects.

The market growth is driven by expanding semiconductor manufacturing capabilities, particularly in Asia-Pacific, and increasing demand for consumer electronics and electric vehicles. However, supply chain disruptions in raw copper materials and the ongoing miniaturization trend in electronics present challenges. Key players like Heraeus and Sumitomo Metal Mining are investing in advanced copper wire bonding technologies to maintain competitiveness in this evolving market landscape.

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis. https://semiconductorinsight.com/download-sample-report/?product_id=95876

Segment Analysis:

By Type

20-30 µm Segment Holds Major Share Due to Optimal Bonding Performance in Semiconductor Packaging

The market is segmented based on type into:

0-20 µm

Subtypes: Ultra-fine pitch bonding wires for advanced ICs

20-30 µm

30-50 µm

Subtypes: Standard diameter wires for conventional packaging

Above 50 µm

Others

By Application

Semiconductor Packaging Dominates Due to Increasing Demand for Advanced Electronics

The market is segmented based on application into:

Semiconductor packaging

Subtypes: Flip chips, chip-on-board, multi-chip modules

PCB interconnects

Power electronics

LED packaging

Others

By End User

Consumer Electronics Sector Leads Owing to Proliferation of Smart Devices

The market is segmented based on end user into:

Consumer electronics

Automotive electronics

Industrial electronics

Medical devices

Others

Regional Analysis: Global Electronic Copper Wire Market

North America The North American electronic copper wire market is driven by high-tech semiconductor manufacturing and significant investments in electronics infrastructure. The U.S. accounts for over 65% of regional demand, supported by major players like AMETEK and The Prince & Izant. Despite stricter environmental regulations influencing production costs, the region maintains a competitive edge through advanced wire bonding technologies and robust R&D investments in semiconductor packaging. Recent CHIPS Act allocations of $52 billion for domestic semiconductor production are expected to further stimulate demand for high-purity copper wires in chip manufacturing.

Europe Europe’s market is characterized by stringent quality standards and growing adoption of copper wire in automotive electronics, particularly in Germany and France. Heraeus, a key regional player, dominates the premium segment with specialized alloys for high-frequency applications. The EU’s push for electronics recycling (following WEEE Directive guidelines) has accelerated development of eco-friendly copper wire formulations, though higher production costs limit market penetration compared to Asia. Recent supply chain disruptions have prompted increased localization of wire production, particularly for aerospace and medical device applications where precision is critical.

Asia-Pacific As the world’s largest consumer of electronic copper wire, Asia-Pacific accounts for approximately 58% of global volume, with China, Japan, and South Korea leading demand. The region benefits from vertically integrated electronics ecosystems, where companies like Sumitomo Metal Mining and MK Electron supply wires directly to nearby semiconductor fabs and PCB manufacturers. While price competition is intense (especially in consumer electronics segments), Japanese suppliers maintain premium positioning for finer (<30 μm) bonding wires used in advanced chip packaging. India’s emerging semiconductor policy initiatives present new growth avenues, though infrastructure limitations persist.

South America South America represents a nascent but growing market, primarily serving local electronics assembly operations in Brazil and Argentina. Import dependence exceeds 70% for high-grade copper wires, as regional production focuses on thicker gauges (>50 μm) for power applications rather than precision electronics. Economic instability and currency fluctuations have discouraged major investments in local wire production facilities, though some multinational PCB manufacturers are establishing operations to serve the automotive and appliance sectors, creating opportunities for mid-tier suppliers.

Middle East & Africa This region shows promising long-term potential as electronics manufacturing begins to diversify beyond oil-dependent economies. The UAE and Saudi Arabia are investing in semiconductor testing and packaging facilities, driving demand for imported copper wires. However, the market remains constrained by limited technical Expertise in fine wire production and underdeveloped local supply chains. South Africa serves as a regional outlier with some specialty wire production for mining and industrial electronics, though volumes remain modest compared to global standards.

List of Key Electronic Copper Wire Companies Profiled

Heraeus Holding GmbH (Germany)

Tanaka Holdings Co., Ltd. (Japan)