#Lubricant Market Revenue

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr Inc. has $15.1M in annual revenue.

Text

Lubricant Market: Trends, Size & Key Industry Players

The global lubricant market is a vital component of the automotive, industrial, and machinery sectors, serving as a critical factor in ensuring the smooth functioning and longevity of equipment. Lubricants reduce friction, wear, and tear, leading to improved efficiency and performance in various applications. This market has shown robust growth over the years, driven by the increasing demand from end-use industries, technological advancements, and the expansion of the automotive sector. In this blog, we will explore the market size, share, and growth of the lubricant market, analyze current market trends, identify key players, discuss the challenges facing the market, and conclude with insights into its future trajectory.

Market Size, Share, and Growth

As of 2023, the global lubricant market was valued at approximately USD 163 billion. This market is expected to grow at a compound annual growth rate (CAGR) of 3.2% from 2024 to 2030, reaching a value of around USD 205 billion by the end of the forecast period. The growth of this market can be attributed to the rising demand for lubricants in emerging economies, the expansion of the automotive industry, and the increasing industrialization and mechanization of various sectors.

The automotive sector accounts for the largest share of the lubricant market, holding nearly 50% of the market revenue. This dominance is primarily due to the extensive use of lubricants in engine oils, gear oils, and transmission fluids, which are essential for the maintenance and efficiency of vehicles. The industrial segment follows closely, with significant demand from manufacturing, power generation, and other heavy machinery sectors.

Market Trends

Several key trends are shaping the growth and evolution of the lubricant market:

Shift Towards Synthetic and Bio-Based Lubricants: Environmental concerns and the need for sustainability have led to a significant shift from conventional mineral-based lubricants to synthetic and bio-based alternatives. Synthetic lubricants, known for their superior performance, longer life, and better thermal stability, are gaining traction, especially in developed markets. Bio-based lubricants, derived from renewable resources, are also seeing increased adoption due to their biodegradable nature and lower environmental impact.

Rising Demand from Emerging Markets: Emerging economies in Asia-Pacific, particularly China and India, are driving the demand for lubricants. Rapid industrialization, increasing automotive sales, and infrastructure development in these regions are key factors contributing to market growth. The Asia-Pacific region holds the largest market share, accounting for nearly 40% of the global lubricant consumption.

Technological Advancements: Innovation in lubricant formulation and production processes is a significant trend in the market. Companies are focusing on developing high-performance lubricants that offer better fuel efficiency, reduced emissions, and extended service intervals. Additionally, advancements in additive technology are enhancing the overall quality and functionality of lubricants.

Growing Focus on Energy Efficiency: Energy efficiency has become a critical factor in industrial operations and automotive applications. Lubricants that reduce friction and energy losses are in high demand, as they contribute to lower operating costs and improved sustainability. This trend is particularly evident in the manufacturing and transportation sectors, where energy efficiency is directly linked to profitability and environmental impact.

Key Market Players and Their Market Share

The global lubricant market is highly competitive, with several key players dominating the industry. These companies are involved in extensive research and development activities, mergers and acquisitions, and strategic partnerships to maintain their market positions. Some of the leading players in the lubricant market include:

Royal Dutch Shell Plc: Shell is a global leader in the lubricant market, holding a market share of approximately 12%. The company offers a wide range of lubricants under its Shell Helix, Shell Rimula, and Shell Tellus brands. Shell’s strong global presence, innovative product portfolio, and commitment to sustainability have helped it maintain a leading position in the market.

ExxonMobil Corporation: ExxonMobil is another major player in the lubricant industry, with a market share of around 10%. The company’s Mobil 1, Mobil Delvac, and Mobil SHC brands are well-known for their high performance and reliability. ExxonMobil’s focus on technological innovation and its extensive distribution network contribute to its strong market presence.

BP Plc (Castrol): BP, through its Castrol brand, holds a significant share of the lubricant market, estimated at 8%. Castrol’s lubricants are widely used in automotive, industrial, and marine applications. The company’s focus on developing environmentally friendly products and its strong brand reputation have been key factors in its success.

TotalEnergies SE: TotalEnergies is a prominent player in the global lubricant market, with a market share of approximately 7%. The company offers a diverse range of lubricants under its Total Quartz, Total Rubia, and Total Azolla brands. TotalEnergies’ commitment to sustainability and its extensive presence in emerging markets are driving its growth in the industry.

Chevron Corporation: Chevron, with its Havoline and Delo brands, holds a market share of around 6%. The company is known for its high-quality lubricants, which are used in a wide range of applications, including automotive, industrial, and marine sectors. Chevron’s focus on innovation and customer satisfaction has helped it maintain a strong position in the market.

Market Challenges

Despite the positive growth outlook, the lubricant market faces several challenges that could impact its development:

Environmental Regulations: Stringent environmental regulations regarding emissions and waste disposal are a significant challenge for the lubricant industry. Governments worldwide are implementing stricter standards to reduce environmental impact, which is driving the shift towards synthetic and bio-based lubricants. However, the high cost of these alternatives can be a barrier to their widespread adoption, particularly in price-sensitive markets.

Fluctuating Raw Material Prices: The lubricant industry is highly dependent on the availability and cost of raw materials, particularly crude oil. Fluctuations in crude oil prices can significantly impact the profitability of lubricant manufacturers. Additionally, the increasing demand for synthetic and bio-based lubricants is putting pressure on the supply of raw materials, leading to potential supply chain disruptions.

Technological Disruption: The rapid pace of technological advancement in the automotive and industrial sectors poses a challenge to the lubricant market. The development of electric vehicles (EVs), for example, requires less lubrication compared to traditional internal combustion engine vehicles. This shift could reduce the demand for automotive lubricants in the long term.

Market Fragmentation: The lubricant market is highly fragmented, with numerous small and medium-sized players competing with established giants. This fragmentation can lead to intense price competition, which can erode profit margins and hinder market growth. Additionally, the presence of counterfeit products in certain regions poses a challenge to maintaining product quality and brand reputation.

Conclusion

The global lubricant market is poised for steady growth in the coming years, driven by increasing demand from emerging economies, technological advancements, and the ongoing shift towards synthetic and bio-based products. However, the market faces significant challenges, including stringent environmental regulations, fluctuating raw material prices, and technological disruption. To navigate these challenges, industry players must focus on innovation, sustainability, and strategic partnerships. Companies that can adapt to changing market dynamics and meet the evolving needs of consumers will be well-positioned to succeed in this competitive landscape. In conclusion, the lubricant market remains a critical component of the global economy, supporting a wide range of industries and applications. While challenges exist, the market's resilience and adaptability suggest a promising future, with continued opportunities for growth and development.

#Lubricant Sector#Marine Lubricant Market#Global Lubricant Industry#Top 20 Lubricants Companies#Lubricant Market Players#Lubricant Market Revenue#Lubricant Market Size

0 notes

Text

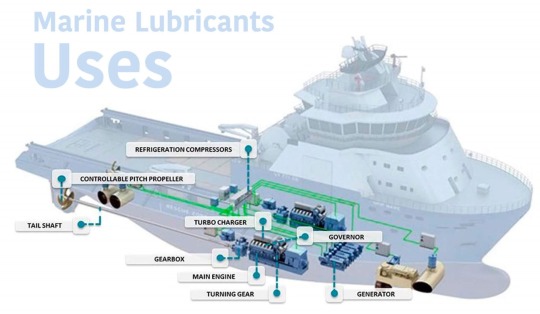

An In-Depth Analysis of the Marine Lubricants Industry : Lubricating the Future of Shipping

The global marine lubricants market size is expected to reach USD 10.27 billion by 2030, registering a CAGR of 4.2% over the forecast period, according to a new report by Grand View Research, Inc. Growing concerns regarding oceanic pollution caused by improper engine function and subsequent demand for fuel-efficient engines are estimated to trigger the growth of the market.

Growth in international trade, removal of trade barriers being the principal reason, is encouraging developing countries to concentrate more on the improvement of their infrastructure, such as roads, airports, and seaports, which play a vital role in the development of the economy. Product storage, along with the capacity to move large shipments, has placed the shipping industry in a very advantageous position.

Gain deeper insights on the market and receive your free copy with TOC now @: Marine Lubricants Market Report

Global shipping majors, just like other segments of the conventional transport industry, are increasingly getting integrated with emerging global logistics and supply chain activities, owing to both external and internal dynamics. These factors have aided industry participants in substantially consolidating their market position and supplementing their ocean freight income, subsequently stoking the demand for marine lubricants.

Engine oils dominated the market over 46.0% volume share in 2022. These products are widely used in high, medium, and slow speed marine engines to extend service life and protect interior components from high temperatures & pressure. Some lubricants even offer additive protection against crankcases, camshaft areas, under-crowns, and ring belts.

Other products such as refrigeration compressor oils are specifically formulated to perform in extreme temperature environments and consist of HFC, CFC, and ozone-friendly refrigerants. These lubricants significantly prevent congealing on valves.

#Marine Lubricants Market Size & Share#Marine Lubricants Market Latest Trends#Marine Lubricants Market Growth Forecast#COVID-19 Impacts On Marine Lubricants Market#Marine Lubricants Market Revenue Value

3 notes

·

View notes

Text

Exploring the Science Behind the Booming Hydrocolloids Market

The global hydrocolloids market size is expected to reach USD 17.83 billion by 2030, according to a new report by Grand View Research, Inc. The market is expected to expand at a CAGR of 6.0% from 2023 to 2030. Hydrocolloids find application in radiology as a suspending agent, suppositories, slow-release capsules, emulsions, surgical lubricants, and as a carrier of topical medicaments, which is expected to drive the market growth.

Rapid urbanization coupled with improved consumer lifestyle with more emphasis on healthy, diet-friendly, nutritious, and natural products is fueling the demand for convenience and packaged foods, which, in turn, is likely to propel product consumption. Additionally, growing consumer awareness regarding the benefits of nutritional food is further propelling the demand for hydrocolloids in developing countries, such as China and India.

Europe and North America are projected to play a substantial role even after losing their market share to Asia Pacific and Latin America. Asia Pacific and Latin America are expected to accomplish the highest gains in near future. A large number of health-conscious individuals are embracing a healthier lifestyle with the foremost importance on the healthy food choices offered by various food and beverage companies.

The key players in the hydrocolloids market are inclined towards new product launches, which is expected to augment the growth. In August 2018, Cargill announced its plans to invest USD 150 million in Brazil's production facility to keep up with the increasing demand for pectin.

Hydrocolloids Market Segmentation

Grand View Research has segmented the global hydrocolloids market based on product, function, application, and region:

Hydrocolloids Product Outlook (Volume, Kilotons, Revenue, USD Million, 2018 - 2030)

Gelatin

Xanthan Gum

Carrageenan

Alginates

Pectin

Guar Gum

Gum Arabic

Carboxy Methyl Cellulose

Agar

Locust Bean Gum

Hydrocolloids Function Outlook (Volume, Kilotons, Revenue, USD Million, 2018 - 2030)

Thickening

Gelling

Stabilizing

Others

Hydrocolloids Application Outlook (Volume, Kilotons, Revenue, USD Million, 2018 - 2030)

Food & Beverage

Pharmaceutical

Personal Care & Cosmetics

Others

Hydrocolloids Regional Outlook (Volume, Kilotons, Revenue, USD Million, 2018 - 2030)

North America

US

Canada

Europe

Germany

France

UK

Asia Pacific

China

Japan

India

Latin America

Brazil

Mexico

Middle East & Africa

List of Key Players

DuPont

Palsgaard

Nexira

Ingredion, Incorporated

Kerry

BASF

Ashland

CP Kelco U.S. Inc.

Glanbia Nutritionals

Darling Ingredients, Inc.

Tate & Lyle Plc

Cargill, Incorporated

Fuerst Day Lawson

Koninklijke DSM N.V.

The Archer Daniels Midland Company (ADM)

Order a free sample PDF of the Hydrocolloids Market Intelligence Study, published by Grand View Research.

0 notes

Text

A Deep Dive into the America Lubricants Market: Insights and Analysis

The America lubricants market is expected to reach USD 45.8 billion by 2030, registering a CAGR of 3.0% during the forecast period, as per the new report by Grand View Research, Inc. The growth is attributed to the increase in demand for the automotive and industrial segments within the region.

The lubricants market in America is expected to increase significantly, during the forecast period. The region's fast growth in the automotive and industrial end-use categories will bolster the enlargement. The major application markets, which account for more than 90.0% of the market share, are automotive and industrial manufacturing. The need for industrial applications is likely to be the largest contributor, owing to rising disposable incomes and strong employment figures. As a result of the changing pollution standards and the introduction of electric vehicles, the growth within the automobile industry is expected to be restrained. Top producers in the industry at present cater to the high-margin application sectors of aerospace and marine.

The development of better infrastructure and public transportation networks in emerging economies such as Argentina and Brazil has resulted in improving economic situations. Apart from that, people in the U.S. are increasingly choosing personal vehicles. This is likely to drive demand for the high-performance oil used in automobiles within the region during the forecast period.

Companies are strategically divesting assets and investing in upstream facilities, making the industry extremely competitive. Premium lubricants are projected to be the main driver of industry growth in the future. Companies are also seeking strategic alliances and collaborations, in order to enhance their brand image and invest in new product development.

Gather more insights about the market drivers, restrains and growth of the America Lubricants Market

America Lubricants Market Report Highlights

• Automotive segment accounted for 56.0% of revenue share in 2021. The growth is attributed to the increase in demand for passenger vehicles, commercial vehicles, and scooters. Growth in the consumption of personal vehicles is driving demand for the lubricant oil, used for maintaining vehicle

• Industrial segment is anticipated to grow at a CAGR of 3.1% from 2022 to 2030 in terms of revenue as there is a rising need for industrial vehicles owing to the infrastructural development, which in turn will drive demand for the product in the region

• Motorcycle vehicle type dominated the industry with USD 6.8 billion in 2021. The demand is anticipated to grow with an increase in consumption of the latest type of motorcycle by the young population of the region

• Aerospace segment is anticipated to witness a CAGR of 3.8% during the forecast period. The growth is anticipated due to the increase in the use of oil in aircraft. Aerospace lubricants are used to ensure reliability and provide long-lasting lubrication

• Companies have integrated throughout the value chain, to gain the competitive advantage

America Lubricants Market Segmentation

Grand View Research has segmented the America lubricants market report based on the vehicle type, end-use, and region:

America Lubricants Vehicle Type Outlook (Volume, Kilotons; Revenue, USD Million; 2018 - 2030)

• Motorcycle

• Others

America Lubricants End-use Outlook (Volume, Kilotons; Revenue, USD Million; 2018 - 2030)

• Industrial

• Automotive

• Marine

• Aerospace

America Lubricants Regional Outlook (Volume, Kilotons; Revenue, USD Million; 2018 - 2030)

• North America

o U.S.

o Mexico

• Latin America

o Argentina

o Brazil

Order a free sample PDF of the America Lubricants Market Intelligence Study, published by Grand View Research.

#America Lubricants Market#America Lubricants Market Size#America Lubricants Market Share#America Lubricants Market Analysis#America Lubricants Market Growth

0 notes

Text

Top 15 Market Players in Global Phosphite Esters Market

Top 15 Market Players in Global Phosphite Esters Market

Phosphite esters are widely used as antioxidants, stabilizers, and intermediates in polymers, coatings, and lubricants. With their critical applications in various industries, the global phosphite esters market is characterized by robust competition. Here are the top 15 players driving the market:

BASF SE BASF is a global leader in specialty chemicals, offering a wide range of phosphite esters used in polymer stabilization and industrial applications.

Clariant AG Clariant focuses on delivering high-performance phosphite esters designed for enhanced polymer durability and processing efficiency.

Addivant (SI Group) Addivant is recognized for its advanced phosphite-based antioxidants that improve the thermal and oxidative stability of polymers.

Dover Chemical Corporation Dover Chemical specializes in producing phosphite esters that act as efficient stabilizers in PVC, adhesives, and coatings.

Lanxess AG Lanxess offers innovative solutions, including phosphite esters for the plastics and rubber industries, with a focus on sustainability.

Solvay S.A. Solvay provides high-purity phosphite esters that cater to the demands of advanced polymer processing and industrial formulations.

Evonik Industries AG Evonik produces specialty phosphite esters that enhance the thermal stability and lifespan of polymer products.

Chemtura Corporation (Lanxess) Chemtura, now a part of Lanxess, develops high-performance phosphite esters for use in coatings, lubricants, and plastics.

Valtris Specialty Chemicals Valtris focuses on phosphite esters that serve as cost-effective stabilizers in industrial and polymer applications.

Milliken & Company Milliken provides phosphite-based stabilizers designed to improve the performance and longevity of thermoplastics.

ADEKA Corporation ADEKA is known for its innovative phosphite esters tailored for demanding applications in automotive and packaging materials.

PMC Group PMC Group offers a wide range of phosphite esters designed to enhance the performance of industrial polymers and resins.

Baerlocher GmbH Baerlocher provides phosphite esters for PVC stabilization, catering to the needs of the construction and automotive industries.

Italmatch Chemicals Italmatch specializes in phosphite esters used in lubricant additives and flame retardants, with a focus on high-performance applications.

Shandong Ruifeng Chemical Co., Ltd. A key player in Asia, Shandong Ruifeng produces cost-effective phosphite esters for polymer and industrial applications.

Request report sample at https://datavagyanik.com/reports/global-phosphite-esters-market/

Top Winning Strategies in Phosphite Esters Market

To remain competitive and capitalize on the growing demand for phosphite esters, market players are adopting various strategies that emphasize innovation, sustainability, and customer-centricity. Here are the top winning strategies:

Product Innovation and Customization Companies are focusing on R&D to develop advanced phosphite esters with improved thermal and oxidative stability, as well as tailored solutions for specific industries.

Sustainability and Eco-Friendly Formulations There is a significant push toward producing eco-friendly phosphite esters that comply with environmental regulations such as REACH and EPA standards.

Geographic Expansion Players are expanding their footprint in high-growth markets like Asia-Pacific and Latin America, driven by increased demand in construction, automotive, and packaging sectors.

Strategic Partnerships and Collaborations Collaborations with raw material suppliers and end-users enable companies to enhance their supply chain efficiency and address evolving market needs.

Focus on High-Growth Applications Targeting emerging applications such as biopolymers, advanced coatings, and high-performance lubricants is helping companies diversify their revenue streams.

Cost Optimization Manufacturers are optimizing production processes and adopting lean manufacturing practices to reduce costs and remain competitive in price-sensitive markets.

Regulatory Compliance and Certification Adherence to stringent global regulatory standards and certifications is critical to gaining customer trust and expanding into new markets.

Digital Transformation The adoption of advanced technologies such as artificial intelligence, IoT, and big data analytics is enabling companies to improve production efficiency and quality control.

Enhanced Supply Chain Management Strengthening supply chain networks and building resilience against disruptions is a key focus area for players in the phosphite esters market.

Merger and Acquisition Activities Acquiring regional and niche players allows companies to expand their product portfolio and strengthen their presence in key markets.

Customer Education and Technical Support Providing technical training and support to customers helps manufacturers build strong relationships and encourage product adoption.

Focus on Specialty Grades Developing specialty phosphite esters for niche applications such as high-performance polymers and bioplastics has become a lucrative strategy.

Strong Marketing and Branding Effective branding and targeted marketing campaigns are helping companies enhance their visibility and attract new customers.

Investment in Capacity Expansion Increasing production capacity to meet the rising demand for phosphite esters across industries is a critical strategy for growth.

Sustainable Packaging Solutions Companies are exploring innovative packaging solutions to improve product shelf life while reducing environmental impact.

By adopting these strategies, companies in the phosphite esters market are positioning themselves to address evolving industry demands and capture a larger share of the global market.

Request a free sample copy at https://datavagyanik.com/reports/global-phosphite-esters-market/

#Phosphite Esters Market#Phosphite Esters Production#market share#market players#market size#top trends#revenue#average price#market growth#competitive pricing strategies

0 notes

Text

Thailand Lubricant Market: A Key Player in Southeast Asia's Industrial and Automotive Growth

The lubricant market in Thailand is a vital component of the country’s industrial and automotive sectors. As one of Southeast Asia's most dynamic economies, Thailand’s robust industrial base, expanding automotive industry, and infrastructure development projects are driving the demand for high-quality lubricants.

The Thailand lubricants market is projected to have a volume of 811.16 million liters by 2025, with an expected growth to 901.30 million liters by 2030, reflecting a CAGR of 2.13% over the forecast period from 2025 to 2030.

Overview of Lubricants

Lubricants are substances used to reduce friction between moving parts, enhance performance, and extend the lifespan of machinery and engines. They are essential in industries such as automotive, manufacturing, construction, and power generation. Lubricants are broadly categorized into engine oils, industrial lubricants, hydraulic fluids, gear oils, and greases.

In Thailand, lubricants play a crucial role in supporting key sectors, including automotive manufacturing, transportation, agriculture, and heavy industries.

Key Drivers of Market Growth

1. Expanding Automotive Industry

Thailand is often referred to as the “Detroit of Asia” due to its strong automotive manufacturing base. As a leading exporter of vehicles and automotive components, the country generates significant demand for automotive lubricants. The growing number of vehicles on the road also boosts the demand for engine oils and transmission fluids.

2. Industrial Growth and Urbanization

Thailand’s industrial sector, including manufacturing, construction, and power generation, is expanding rapidly. This growth, coupled with urbanization and infrastructure development projects, is driving the consumption of industrial lubricants.

3. Rise in Infrastructure Projects

Government initiatives, such as the Eastern Economic Corridor (EEC) project, are fueling construction activities and the operation of heavy machinery, increasing the need for high-performance industrial lubricants.

4. Focus on Energy Efficiency

With rising energy costs and environmental concerns, industries are adopting lubricants that enhance energy efficiency and reduce wear and tear on machinery, contributing to market growth.

5. Growth in Agriculture

Thailand’s agricultural sector relies heavily on machinery such as tractors and harvesters. The increasing use of mechanized farming equipment is boosting the demand for agricultural lubricants.

Challenges in the Market

1. Competition from Low-Cost Alternatives

The availability of low-cost and counterfeit lubricant products poses a challenge to established brands, impacting market revenue.

2. Fluctuating Crude Oil Prices

As lubricants are derived from crude oil, price volatility in the global oil market can affect production costs and pricing strategies.

3. Environmental Regulations

Stringent environmental regulations regarding the disposal and use of lubricants pose challenges for manufacturers, requiring investments in eco-friendly formulations.

4. Increasing Demand for Electric Vehicles (EVs)

The rise of EVs, which require fewer lubricants compared to traditional internal combustion engine vehicles, presents a long-term challenge to the automotive lubricant segment.

Trends Shaping the Market

1. Shift Toward Synthetic Lubricants

Synthetic lubricants, known for their superior performance and longer drain intervals, are gaining popularity among consumers and industries in Thailand.

2. Development of Eco-Friendly Lubricants

There is a growing demand for bio-based and biodegradable lubricants that minimize environmental impact and comply with sustainability goals.

3. Growth of E-commerce Channels

The rise of e-commerce platforms is transforming the lubricant distribution landscape, allowing manufacturers to reach a wider audience, including small and medium enterprises (SMEs).

4. Adoption of Digital Solutions

Digitalization is enabling real-time monitoring of lubricant performance, predictive maintenance, and efficient inventory management in industrial applications.

5. Focus on High-Performance Lubricants

Industries are increasingly adopting high-performance lubricants that offer enhanced protection, reduce maintenance costs, and improve machinery efficiency.

Future Outlook

The Thailand lubricant market is poised for steady growth in the coming years, driven by industrialization, infrastructure development, and advancements in automotive technology. Key factors shaping the future include:

Increased Adoption of EV-Compatible Lubricants: The rise of EVs will create a niche market for specialty lubricants tailored for electric motors and thermal management systems.

Focus on Sustainability: Eco-friendly formulations and recycling initiatives will become central to market strategies.

Innovation in Additives: The development of advanced additives to enhance lubricant performance will remain a priority.

Regional Collaboration: Thailand’s integration into regional supply chains, particularly within ASEAN, will strengthen its position as a lubricant hub in Southeast Asia.

Growth in Renewable Energy: The expanding renewable energy sector will create new demand for lubricants used in wind turbines and solar power systems.

Conclusion

The lubricant market in Thailand is an essential driver of the country’s industrial and automotive sectors, supporting economic growth and modernization. While challenges such as environmental regulations and the rise of EVs present obstacles, opportunities in high-performance, eco-friendly, and synthetic lubricants are paving the way for future expansion.

As Thailand continues to embrace technological advancements and sustainability initiatives, the lubricant market is set to play a pivotal role in enabling efficiency, reliability, and innovation across industries. For stakeholders, investing in product innovation, digitalization, and eco-friendly solutions will be key to capitalizing on the market’s promising trajectory. For a detailed overview and more insights, you can refer to the full market research report by Mordor Intelligence: https://www.mordorintelligence.com/industry-reports/thailand-lubricants-market

#Thailand Lubricant Market#Thailand Lubricant Market Size#Thailand Lubricant Market Share#Thailand Lubricant Market Analysis#Thailand Lubricant Market Report

0 notes

Text

Automotive Bearing Market Insights: Revolutionizing Efficiency and Sustainability in Global Mobility Solutions

The automotive bearing market is a cornerstone of modern vehicle engineering, ensuring smooth operations and optimal functionality across diverse automobile components. Bearings play a crucial role in reducing friction, improving efficiency, and enhancing durability in cars, commercial vehicles, and specialty vehicles. With advancements in automotive technology, the demand for high-performance, lightweight, and energy-efficient bearings has surged. This blog delves into the key aspects of the automotive bearing market, including industry trends, growth drivers, challenges, and future opportunities.

Market Overview and Trends

The global automotive bearing market is experiencing significant growth, driven by rising vehicle production, technological innovations, and stringent fuel efficiency regulations. The introduction of electric and hybrid vehicles has further reshaped the industry, as these vehicles demand specialized bearings tailored for electric motors and regenerative braking systems. Key trends include the use of advanced materials such as ceramics and composites, integration of smart sensors into bearings, and a shift towards more eco-friendly lubricants.

Moreover, Industry 4.0 and IoT-enabled technologies have contributed to the rise of smart bearings. These advanced products offer real-time data on parameters like temperature, load, and lubrication, enhancing operational efficiency and predictive maintenance capabilities. Manufacturers are focusing on reducing the overall carbon footprint, which aligns with global sustainability objectives.

Key Growth Drivers

Increasing Vehicle Production: As global economies recover post-pandemic, the demand for personal and commercial vehicles is rising, fueling the need for automotive bearings.

Electrification of Vehicles: The transition to electric and hybrid vehicles requires innovative bearing designs to cater to unique operational demands.

Technological Innovations: Advancements in material science and manufacturing processes have resulted in lightweight, durable bearings with enhanced performance.

Stringent Emission Norms: Regulatory mandates worldwide have driven manufacturers to adopt energy-efficient components, boosting the adoption of advanced bearings.

Aftermarket Expansion: The growing vehicle fleet has accelerated demand in the aftermarket segment, further driving revenue growth.

Challenges and Constraints

While the market offers promising growth opportunities, certain challenges persist. Fluctuations in raw material prices can impact profitability, while complex supply chain dynamics post-pandemic pose additional concerns. Furthermore, the transition to electric vehicles requires a reorientation of traditional bearing design and manufacturing processes, demanding significant investment in research and development.

Regional Dynamics

Asia-Pacific: Dominates the automotive bearing market due to its large vehicle production capacity, especially in China, India, and Japan.

North America: Driven by high adoption rates of advanced technologies and robust electric vehicle markets.

Europe: Focused on sustainability and emission reduction, with key contributions from Germany and the Nordic countries.

Rest of the World: Emerging markets in South America and Africa are showing steady growth, driven by increasing automotive investments.

Future Opportunities

The automotive bearing market is set to benefit from collaborations and partnerships among OEMs, suppliers, and technology providers. The rise of autonomous vehicles and advanced driver assistance systems (ADAS) presents opportunities for innovative bearing solutions with high precision and reliability. Furthermore, investments in green technologies and renewable energy sources will continue to shape the future of the industry.

0 notes

Text

Fuel Additives Market

Fuel Additives Market Size, Share, Trends: BASF SE Leads

Shift towards bio-based fuel additives driving sustainable fuel solutions

Market Overview:

The global Fuel Additives market is projected to grow at a CAGR of 4.8% from 2024 to 2031. The market value is expected to increase significantly during this period. North America currently dominates the market, accounting for the largest share of global revenue. Key metrics include increasing demand for high-performance fuels, stringent environmental regulations, and growing automotive and aviation industries. The market is experiencing steady growth due to the rising need for improved fuel efficiency, reduced emissions, and enhanced engine performance across various sectors.

The fuel additives market is seeing a considerable transition towards bio-based and renewable options. This trend is being driven by growing environmental concerns and the demand for sustainable fuel solutions. Bio-based fuel additives, made from renewable sources including plant oils and waste biomass, are gaining popularity due to their lower carbon footprint and environmental impact. These additives improve lubricity, fuel stability, and reduce emissions, all of which align with global environmental goals. The adoption of bio-based additives is especially high in regions with tight environmental legislation, such as Europe and North America. As consumers and industries become more environmentally concerned, demand for these sustainable additives is likely to rise further, altering the gasoline additives landscape and spurring industry innovation.

DOWNLOAD FREE SAMPLE

Market Trends:

Increasingly strict pollution standards around the world are a primary driver for the gasoline additives business. To tackle air pollution and climate change, governments and environmental organisations are tightening automobile emission limits. This regulatory pressure is driving automakers and fuel companies to use innovative fuel additives that can minimise hazardous emissions while increasing fuel efficiency. For example, the European Union's Euro 6d emission rules, which went into effect in 2020, imposed stricter restrictions on nitrogen oxide (NOx) and particulate matter emissions from cars. Similarly, the U.S. Environmental Protection Agency's Tier 3 Vehicle Emission and Fuel Standards Program intends to cut smog-forming volatile organic compounds and nitrogen oxides by 80% from their current levels. These requirements have resulted in a 25% rise in the usage of cetane improvers in diesel fuel over the last five years, as they aid to reduce NOx emissions and improve fuel combustion efficiency.

The unpredictability in crude oil prices presents a substantial challenge to the gasoline additives sector. Many fuel additives are petroleum-based, hence their production costs are directly affected by crude oil prices. This volatility may result in uncertain pricing of fuel additives, reducing manufacturers' profit margins and potentially increasing expenses for end users. For example, during the 2020 oil price fall, the average cost of creating some fuel additives fell by 15-20%, resulting in temporary market volatility. However, as oil prices recovered dramatically in 2021, production costs rose again, creating pricing uncertainty in the fuel additives industry.

Market Segmentation:

Deposit control additives, often known as detergents, account for the biggest market share in the gasoline additives business. These additives help keep engines clean and efficient by preventing deposits from forming in fuel systems and combustion chambers. This segment's prominence can be ascribed to the widespread demand for deposit management across all fuel types and applications.

In recent years, the automotive sector has seen a growth in the use of sophisticated deposit control additives. For example, a large global oil corporation reported a 30% increase in the use of its premium deposit control ingredient in petrol compositions during the previous three years. This increase is primarily due to the increasing complexity of modern engines, which are more prone to performance problems caused by deposits.

The aircraft industry has also contributed to the expansion of deposit control additives. With a greater emphasis on fuel efficiency and engine longevity in aeroplanes, the use of these additives in aviation fuel has increased by 15% since 2020. Major airlines have recorded fuel efficiency gains of up to 2% after introducing advanced deposit control additives into their fuel management techniques, resulting in significant cost savings and lower emissions.

Market Key Players:

Afton Chemical Corporation

BASF SE

Chevron Oronite Company LLC

Evonik Industries AG

Innospec Inc.

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

PVC Additives Market-Industry Forecast, 2024–2030

PVC Additives Market overview

Request Sample Report :

Report Coverage

The report: “PVC Additives Market- Forecast (2024–2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the PVC Additives Industry.

By Type: Stabilizers, Impact Modifiers, Processing Aids, Lubricants, Plasticizers, Fillers, Others.

By Form: Granules, Powder, and Liquid.

By Fabrication Process: Extrusion, Injection Molding, Blow Molding and Others.

By Application: Pipes, Packaging, Furniture’s, Door and Windows, Cables, Medical Devices, Flooring, and Others.

By End Use: Building and Construction, Automotive industry, Textile Industry, Electrical and Electronics, Medical Industry, Food and Beverages, and Others.

By Geography: North America, South America, Europe, APAC, and RoW.

Key Takeaways

Asia Pacific dominates the PVC Additives market owing to rapid increase in building and construction sector.

Certain applications require higher impact strength than PVC would demonstrate normally.

The market drivers and restraints have been assessed to understand their impact over the forecast period.

The report further identifies the key opportunities for growth while also detailing the key challenges and possible threats.

The other key areas of focus include the various applications and end use industry in PVC Additives market and their specific segmented revenue.

Inquiry Before Buying:

PVC Additives Market Segment Analysis — By Type

Stabilizers held the largest share in the PVC Additives market in 2019. This growth is mainly attributed to the increasing demand for stabilizers in varied applications such as pipes & fittings, rigid & semi-rigid films, and others. Due to their superior properties, such as UV resistance, weathering and heat-aging, stabilizers are increasingly favored over other types of additives. To avoid premature degradation, many polymers are vulnerable to environmental degradation and require the addition of a stabilizer such as an antioxidant or UV absorbent. Hampered phenols and obstructed amine light stabilizers (HALS) deactivate emerging radicals, like air-oxidated peroxy compounds. UV absorbers dissipate UV radiation through the material by a method that is non-destructive. Monomers are added to free radical inhibitors as stabilizers to prevent premature polymerization.

PVC Additives Market Segment Analysis — By Forms

Granules held the largest share in the PVC Additives market in 2019. Granules help to increase the density of the freshly synthesized polymer since it lacks the flowing properties required to be processed by an extruder. Due to their plasticity property, they can be molded or shaped by application of heat. Other characteristics of plastic are its low electrical conductivity, low density, transparency and toughness which allowed it to be used for the creation of different products. In addition, plastic’s versatility has led to its use in a wide array of industries. In order to produce normal and high-strength concretes, 10%, 20%, and 30% replacement ratios by volume of PVC granules and powder are used.

PVC Additives Market Segment Analysis — By Fabrication Process

Extrusion held the largest share in the PVC Additives market in 2019. Extrusion is used mainly for handling large plastic volumes. The pellets, granules, chips, or powders are fed into the extruder and melted under high temperatures. PVC compounding is a process where additives are mixed with the base resin in order to obtain a homogenous mix. The additives are used either to enhance process capabilities or to improve product efficiency. The use of sizing parts will generate any length of profiles to the desired length. Co-extrusion allows the manufacture of semi-finished multi-layer products with special barrier properties.

PVC Additives Market Segment Analysis — By Application

Pipes is projected to witness highest share in PVC Additives market in 2019. This rise is mainly due to the growing demand for pipes & fittings in piping and plumbing, gas pipeline laying, and telecommunication and electrical cable sheathing. Due to the replacement of traditional concrete, iron, and steel-based pipes & fittings with PVC pipes in the building & construction industry, the market for PVC additives in the pipes & fittings segment is expected to witness significant development. The market for building materials is on high demand, with the continually growing population. The prerequisite for housing is pipes and fittings, which are a critical necessity. Urbanization with a large network of connections has contributed to an increase in drainage requirements. There is a growing demand for pipes and fittings to cope with advanced piping links, which in turn drives market growth. Globally, there has been a rising demand for rainwater harvesting system that has helped to heat up the pipe and fit market. In 2019, recently the commercial sector has slowed as the risk for a downturn in global construction increases due to COVID-19 pandemic which led to temporary lockdown of all economic activities across globe.

PVC Additives Market Segment Analysis — By End Use

Building and construction dominates the PVC Additives market growing at a CAGR of 6.00%. With the growing construction industry and its demand for PVC Additives particularly in the regions of Asia-Pacific, North America and Europe, the demand of PVC Additives for all kinds of buildings is expected to see an upsurge. Residential application segment is witnessing growth due to the rising penetration from untapped markets. First-mover advantage in untapped regions and relatively low acquisition costs remain key driving forces in this application market. Furthermore, R&D in PVC Additives will support the growth of the PVC Additives market.

Schedule A Call :

PVC Additives Market Segment Analysis — Geography

Asia-Pacific (APAC) dominated the PVC Additives market growing at CAGR of 41% followed by North America and Europe. APAC as a whole is set to continue to be one of the largest and fastest growing construction markets globally. Large and more developed markets such China, India, Japan, and South Korea are expected to grow more in the coming years. China is driving much of the PVC Additives market demand in Asia-Pacific region followed by India and Japan. Of the five fastest growing regions in construction sector, other than U.S. all are Asian countries including China and India who majorly drive the demand for construction investment in this regions. The strong and healthy growth in construction sector is associated with growing population and middle class economy, which tend to drive APAC residential construction market further and hence the PVC Additives market. The number of buildings that have illuminated PVC Additives is growing sharply in APAC region. The increasing number of new building constructions, along with the rise in the number of renovation projects has further propelled the market. Currently the construction industry has been affected due to COVID-19 pandemic where most of the industrial activity has been temporarily shut down. In in turn has affected the demand and supply chain as well which has been restricting the growth in year 2020.

PVC Additives Market Drivers

Replacement of conventional material with PVC will drive the market

PVC is replacing traditional building materials such as wood, metal, concrete and clay in many applications. Versatility, cost-effectiveness and excellent use record make it the most important polymer in the construction sector, accounting for 60%. These products are often lighter, less expensive and offer many performance advantages. Making it prominent material than conventional.

Rapid industrialization and infrastructure activity will augment the growth of PVC Additives

Improvement in economic climate along with boom in industrialization and infrastructure activity across the globe is leading the growth of PVC Additives. Oxford Economics has estimated global infrastructure investment needs to be $94 trillion between 2016 and 2040. This is 19 percent higher than would be delivered under current trends. With the increasing rate of industrialization and infrastructure activity, as a result of which PVC Additives growth is augmenting.

PVC Additives Market Challenges

Low R&D expenditure in the emerging markets and high maintenance cost will hamper the market to growth

Innovation is the key to developing new products, but most manufacturers are not investing much into R&D. Rather than cutting-edge technology, they invest in creating relevant technology. These factors are hampering the growth of the market. Because most of the pipes and fittings are located underground in the event of any malfunction or failure, the cost of repairs can be even greater.

Buy Now :

Market Landscape

Technology launches, acquisitions and R&D activities are key strategies adopted by players in the PVC Additives market. In 2019 the PVC Additives market has been consolidated by the top five players accounting for xx% of the share. Major players in the PVC Additives market are BASF SE, Arkema SA, Akzo Nobel N.V, Adeka Corporation, Clariant AG and Others.

Acquisitions/Technology Launches/ Product Launches

In April 2017, Lanxess Corporation has completed acquisition of Chemtura. With this acquisition, Lanxess significantly expands its market position for PVC additives. A notable sampling includes: the sale of its proprietary OBS (organic-based heat stabilizers) for rigid PVC applications to Baerlocher; the sale of the rest of its PVC additives business to Galata Chemicals.

Key Market Players

The Top 5 companies in the PVC Additives Market are:

BASF SE

Arkema SA

Akzo Nobel N.V

Adeka Corporation

Clariant AG

For more Chemicals and Materials Market reports — Please click here

0 notes

Text

Exploring Singapore's Air Compressor Market: Trends, Insights, and Forecasts Through 2033

The Singapore air compressor market is projected to surpass USD 269.5 million by 2033, with an expected CAGR of 7.58% from 2023 to 2033.

Get a Free Sample Report: https://www.sphericalinsights.com/request-sample/6679

Air Compressors: Transforming Industries with Advanced Technology

Air compressors convert ambient air into high-pressure energy, powering various applications like manufacturing, construction, and medical equipment. These devices utilize energy sources such as electricity, diesel, and natural gas. Modern air compressors integrate IoT for real-time monitoring, predictive maintenance, and performance optimization, enhancing efficiency and minimizing downtime. Additionally, AI-powered compressors predict failures and streamline maintenance, ensuring seamless operations across industries.

Purchase This Report Today: https://www.sphericalinsights.com/checkout/6679

Report Coverage

The report segments the Singapore air compressor market by regions and submarkets, forecasting revenue growth and analyzing trends. It highlights key drivers, challenges, and opportunities while detailing recent developments, competitive strategies, and major players. Core competencies of key players are evaluated across market sub-segments.

Driving Forces Behind Singapore's Air Compressor Market Growth

The growing adoption of air compressors across industries like construction and manufacturing, coupled with their energy efficiency, is fueling market demand. Advancements such as IoT integration and smart technologies for enhanced functionality and remote monitoring further boost the market. Additionally, the rise of automation systems enhances the reliability and efficiency of compressed air systems, driving market growth.

Unlock Discounts on This Report : https://www.sphericalinsights.com/request-discount/6679

Segmentation of the Singapore Air Compressor Market

Stationary Air Compressors Dominate by Type

The Singapore air compressor market is segmented into portable and stationary types, with the stationary segment expected to dominate during the forecast period. Stationary air compressors are favored for their cost-effectiveness, quiet operation, and exhaust-free functionality, making them ideal for indoor applications. Their growing use in household applications is a key driver of this segment's growth.

Oil-Injected Air Compressors Lead in Lubrication Type

Based on lubrication, the market is divided into oil-free and oil-injected/flooded air compressors. The oil-injected/flooded segment is anticipated to maintain the largest market share. These compressors provide superior performance by lubricating moving parts and sealing compressed air efficiently. Their robust demand stems from their reliability and effective cooling and lubrication capabilities.

List of Key Companies

Atlas Copco Group

Hitachi Ltd.

Ingersoll-Rand PLC

Siemens Energy AG

Kaeser Konpressoren

Elgi Equipment Limited

Anest Iwata

Sulzer Ltd.

Mitsubishi Heavy Industries, Ltd.

Others

Competitive Analysis of Singapore Air Compressor Market

The report provides a detailed analysis of key companies in the Singapore air compressor market, evaluating their products, business strategies, geographic presence, market share, and SWOT analysis. It also highlights recent developments, including innovations, partnerships, mergers, and strategic alliances, offering insights into the competitive landscape.

View the Complete Report: https://www.sphericalinsights.com/reports/singapore-air-compressor-market

Key Target Audience

Market Players

Investors

End-users

Government Authorities

Consulting And Research Firm

Venture capitalists

Value-Added Resellers (VARs)

About the Spherical Insights & Consulting

Spherical Insights & Consulting is a market research and consulting firm which provides actionable market research study, quantitative forecasting and trends analysis provides forward-looking insight especially designed for decision makers and aids ROI.

Which is catering to different industry such as financial sectors, industrial sectors, government organizations, universities, non-profits and corporations. The company's mission is to work with businesses to achieve business objectives and maintain strategic improvements.

CONTACT US:

For More Information on Your Target Market, Please Contact Us Below:

Phone: +1 303 800 4326 (the U.S.)

Phone: +91 90289 24100 (APAC)

Email: [email protected], [email protected]

Contact Us: https://www.sphericalinsights.com/contact-us

Follow Us: LinkedIn | Facebook | Twitter

#singaporeaircompressormarket#aircompressorsingapore#industrialaircompressors#singaporebusiness#marketanalysis#aircompressortechnology#singaporeindustries#compressormarket#industrialgrowth#sgmarkettrends

0 notes

Text

Bio-based Synthetic Lubricants in the Market: Driving Performance and Efficiency

Synthetic lubricants are a type of lubricating oil that is artificially created through chemical processes. They are designed to provide superior performance and offer several advantages over conventional mineral-based lubricants. Unlike mineral oils, which are derived from crude oil through refining processes, synthetic lubricants are formulated by synthesizing chemically engineered base oils and adding specific additives to enhance their performance characteristics. The base oils used in synthetic lubricants are typically made from polyalphaolefins (PAO), esters, polyalkylene glycols (PAG), or other synthesized hydrocarbons.

Gain deeper insights on the market and receive your free copy with TOC now @: Synthetic Lubricants Market Report

Bio-based synthetic lubricants are gaining attention as an alternative to petroleum-based lubricants. These lubricants are derived from renewable resources, such as vegetable oils or animal fats. Bio-based synthetic lubricants offer similar performance characteristics to their petroleum-based counterparts while reducing dependence on fossil fuels and lowering the carbon footprint. Synthetic lubricant manufacturers are focusing on developing specialized solutions for specific industries or applications. This includes lubricants tailored for high-performance racing vehicles, electric vehicles, wind turbines, food-grade applications, and more. These industry-specific lubricants are formulated to address unique requirements and challenges, providing optimal performance and protection. The synthetic lubricants industry has seen collaborations and partnerships between lubricant manufacturers and equipment manufacturers. This collaboration aims to optimize lubricant performance by aligning it with specific equipment requirements. Such partnerships often involve joint research and development efforts to create lubricants that are tailored to the needs of particular machinery or industries.

Moreover, Synthetic lubricants generally have longer service intervals compared to mineral-based lubricants. Their superior oxidation resistance and thermal stability contribute to cleaner engines, extended oil change intervals, and reduced maintenance costs. They are typically more expensive than mineral-based lubricants. The complex manufacturing processes and specialized base oils used in synthetic lubricants contribute to their higher cost. However, their extended service life and improved performance can offset the initial investment. Synthetic lubricants are commonly used in demanding applications, such as high-performance engines, racing vehicles, industrial machinery, and extreme operating conditions. Mineral-based lubricants are widely used in general automotive applications and some industrial applications. Semi-synthetic lubricants find applications in various industries, offering a balance between performance and cost.

#Synthetic Lubricants Market Size & Share#Global Synthetic Lubricants Market#Synthetic Lubricants Market Latest Trends#Synthetic Lubricants Market Growth Forecast#COVID-19 Impacts On Synthetic Lubricants Market#Synthetic Lubricants Market Revenue Value

0 notes

Text

The Future of Fatty Alcohol: Market Analysis and Projections

The global fatty alcohol market size is expected to reach USD 8.07 billion by 2030, according to a new study by Grand View Research, Inc. It is anticipated to register a CAGR of 5.7% from 2024 to 2030. Favorable government initiatives in a quest to minimize dependency on petrochemicals coupled with consumer shift towards organic personal care products is expected to drive global fatty alcohols market over the forecast period. Consistent supply of key raw material coupled with the price volatility is expected to a key challenge for market participants. Technological advancements coupled with increasing consumer preference for renewable chemicals are expected to create lucrative opportunities for market participants over the next seven years.

Soaps & detergents was the most dominant application segment and accounted for 54.6% of total market volume in 2014. Growing natural surfactants and emulsifiers demand in soaps & detergents industry is expected to fuel fatty alcohols demand in this segment over the forecast period. Personal care is expected to witness the highest growth of 4.6% from 2015 to 2022. Growing consumer preference towards organic personal care products is expected to increase penetration of fatty alcohols in this segment.

Fatty Alcohol Market Report Highlights

Long chain accounted for the largest market revenue share of 38.9% in 2023. Long-chain fatty alcohols, with 14-22 carbon atoms, are in high demand due to their versatile applications as surfactants, emulsifiers, and emollients in personal care products and industrial cleaners.

Soaps & detergents accounted for the largest market revenue share in 2023. Segment growth is driven by enhancements in living standards in developing economies and a growing focus on personal hygiene.

Asia Pacific fatty alcohol market dominated the global fatty alcohols market with a revenue share of 40.1% in 2023.

Fatty Alcohol Market Segmentation

Grand View Research has segmented the global fatty alcohol market on the basis of type, application, and region:

Fatty Alcohol Type Outlook (Revenue, USD Million, 2018 - 2030)

Short-Chain

Pure & Mid cut

Long Chain

Higher Chain

Fatty Alcohol Application Outlook (Revenue, USD Million, 2018 - 2030)

Soaps & Detergents

Personal Care

Lubricants

Plasticizers

Amines

Pharmaceutical Formulation

Other Applications

Fatty Alcohol Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

US

Canada

Mexico

Europe

Germany

UK

France

Italy

Spain

Asia Pacific

China

India

Japan

South Korea

Latin America

Brazil

Argentina

Middle East & Africa (MEA)

South Africa

Saudi Arabia

List of Key Players of Fatty Alcohol Market

Univar Solutions LLC

BASF SE

KLK OLEO

Wilmar International Ltd

VVF L.L.C.

Ecogreen Oleochemicals

Emery Oleochemicals

Arkema Group

Royal Dutch Shell Plc .com

Oleon NV

SABIC

Evyap Sabun Ya? Gliserin San. ve Tic. A.S.

Kao Corporation

Musim Mas Group

The Procter & Gamble Company

Order a free sample PDF of the Fatty Alcohol Market Intelligence Study, published by Grand View Research.

0 notes

Text

Condom Market: Key Trends and Innovations Driving Industry Growth

The global condom market size is anticipated to reach USD 20.73 billion by 2030, exhibiting a CAGR of 8.72% during the forecast period, according to a new report by Grand View Research, Inc. The market is expected to grow due to increasing awareness about the use of condoms for reducing the spread of HIV and other STIs, along with the availability of a variety of condom types to meet consumer preferences.

The market for condoms is expected to witness new opportunities arising from the integration of technological advancements, including the introduction of smart condoms, as well as the development of eco-friendly and sustainable condom options. These innovations could lead to a shift in consumer preferences and behaviors, resulting in future growth of the market. The i.Con Smart Condom, manufactured by British Condoms, marketed as the “world's first smart condom,” is in reality a ring that fits over a traditional condom and tracks various metrics related to sexual activity. This device measures parameters like thrust speed, calories burned, duration of the session, & span and even compares performance through an app.

Online platforms, such as Besharam, Amazon, JUMIA GROUP, Condom King, Clicks, shycart, Chemistdirect.co.uk, and Kasha Kenya, offer a wide range of condom brands and variations. The availability of condoms on e-commerce websites is helping customers avoid the need for face-to-face interaction when purchasing condoms, which is helping to overcome social prejudices and stigma surrounding their use. This is expected to further boost the demand for condoms through online channels.

Gather more insights about the market drivers, restrains and growth of the Condom Market

Condom Market Report Highlights

• In terms of material type, the latex segment held the largest share in 2023. Latex condoms are favored by customers for their compatibility with lubricants and sex toys. However, the non-latex sector is anticipated to exhibit rapid growth in the foreseeable future due to the efficacy, resilience, and adaptability of this material type.

• Based on product, the male segment has the largest market share in 2023. Male condoms are the mostly preferred option among couples, which results in higher demand and high segment growth

• Based on distribution channel, the public health distribution segment dominated the market in 2023. The e-commerce segment, on the other hand, is expected to grow at the fastest CAGR during the forecast period.

• Asia Pacific dominated the market in 2023 and is expected to register the fastest CAGR over the forecast period, due to various factors such as a large adult population, the presence of manufacturers involved in the export of condoms, and increasing awareness about sexual wellness products.

• In March 2023, Durex launched RealFeel condoms, a notable addition to the market made with polyisoprene to provide a skin-on-skin experience, enhancing comfort and sensitivity. These new launches reflect the growing popularity and innovation in the non-latex market, providing consumers with more choices and options for safe & pleasurable sexual experiences

Condom Market Report Segmentation

Grand View Research has segmented the global condom market based on material type, product, distribution channel, and region:

Condom Material Type Outlook (Revenue, USD Million, 2018 - 2030)

• Latex Condoms

• Non-latex Condoms

o Polyurethane and Polyisoprene

o Lambskin

o Nitrile Butadiene Rubber (NBR)

Condom Product Outlook (Revenue, USD Million, 2018 - 2030)

• Male Condoms

• Female Condoms

Condom Distribution Channel Outlook (Revenue, USD Million, 2018 - 2030)

• Public Health Distribution

• Drug Stores

• E-commerce

• Mass Merchandizers

Condom Regional Outlook (Volume in ‘000; Revenue, USD Million, 2018 - 2030)

• North America

o U.S.

o Canada

• Europe

o UK

o Germany

o France

o Italy

o Spain

o Sweden

o Denmark

o Norway

• Asia Pacific

o Japan

o China

o India

o Australia

o Thailand

o South Korea

• Latin America

o Brazil

o Mexico

o Argentina

• MEA

o South Africa

o Saudi Arabia

o UAE

o Kuwait

o Nigeria

o Kenya

o Zambia

o Zimbabwe

o Uganda

o Egypt

o Turkey

o Ghana

Order a free sample PDF of the Condom Market Intelligence Study, published by Grand View Research.

0 notes

Text

0 notes

Text

Fluid Dispensing Equipment Market Growth Strategic Market Overview and Growth Projections

The global fluid dispensing equipment market size was valued at USD 9.11 billion in 2021 and is projected to reach USD 14.76 billion by 2030 at a CAGR of 5.51% from 2022 to 2030.

The latest Global Fluid Dispensing Equipment Market by straits research provides an in-depth analysis of the Fluid Dispensing Equipment Market, including its future growth potential and key factors influencing its trajectory. This comprehensive report explores crucial elements driving market expansion, current challenges, competitive landscapes, and emerging opportunities. It delves into significant trends, competitive strategies, and the role of key industry players shaping the global Fluid Dispensing Equipment Market. Additionally, it provides insight into the regulatory environment, market dynamics, and regional performance, offering a holistic view of the global market’s landscape through 2032.

Competitive Landscape

Some of the prominent key players operating in the Fluid Dispensing Equipment Market are

Speedline Technologies

Musashi

ITW Dynatec

Valco

Dymax

GPD Global

Fisnar

Henline Adhesive Equipment

IVEK Corp.

Sulzer Mixpac.

Get Free Request Sample Report @ https://straitsresearch.com/report/fluid-dispensing-equipment-market/request-sample

The Fluid Dispensing Equipment Market Research report delivers comprehensive annual revenue forecasts alongside detailed analysis of sales growth within the market. These projections, developed by seasoned analysts, are grounded in a deep exploration of the latest industry trends. The forecasts offer valuable insights for investors, highlighting key growth opportunities and industry potential. Additionally, the report provides a concise dashboard overview of leading organizations, showcasing their effective marketing strategies, market share, and the most recent advancements in both historical and current market landscapes.Global Fluid Dispensing Equipment Market: Segmentation

The Fluid Dispensing Equipment Market segmentation divides the market into multiple sub-segments based on product type, application, and geographical region. This segmentation approach enables more precise regional and country-level forecasts, providing deeper insights into market dynamics and potential growth opportunities within each segment.

On the Basis of Products

Flux

Lubricant

Solder Paste

Adhesives and Sealants

Epoxy Adhesives

Epoxy Underfill

Conformal Coatings

Others

On the Basis of Types

Manual System

Automated Robotics System

On the Basis of Forms

Liquid Fluid

Gaseous Fluid

On the Basis of Application

Bonding

Filling

Lubricating

Sealing

On the Basis of End-Users

Medical Devices

Transportation

Construction

Electrical and Electronics

Semiconductor Packaging

Printed Circuit Boards

Food and Beverages

Others

Stay ahead of the competition with our in-depth analysis of the market trends!

Buy Now @ https://straitsresearch.com/buy-now/fluid-dispensing-equipment-market

Market Highlights:

A company's revenue and the applications market are used by market analysts, data analysts, and others in connected industries to assess product values and regional markets.

But not limited to: reports from corporations, international Organization, and governments; market surveys; relevant industry news.

Examining historical market patterns, making predictions for the year 2022, as well as looking forward to 2032, using CAGRs (compound annual growth rates)

Historical and anticipated data on demand, application, pricing, and market share by country are all included in the study, which focuses on major markets such the United States, Europe, and China.

Apart from that, it sheds light on the primary market forces at work as well as the obstacles, opportunities, and threats that suppliers face. In addition, the worldwide market's leading players are profiled, together with their respective market shares.

Goals of the Study

What is the overall size and scope of the Fluid Dispensing Equipment Market market?

What are the key trends currently influencing the market landscape?

Who are the primary competitors operating within the Fluid Dispensing Equipment Market market?

What are the potential growth opportunities for companies in this market?

What are the major challenges or obstacles the market is currently facing?

What demographic segments are primarily targeted in the Fluid Dispensing Equipment Market market?

What are the prevailing consumer preferences and behaviors within this market?

What are the key market segments, and how do they contribute to the overall market share?

What are the future growth projections for the Fluid Dispensing Equipment Market market over the next several years?

How do regulatory and legal frameworks influence the market?

Straits Research is dedicated to providing businesses with the highest quality market research services. With a team of experienced researchers and analysts, we strive to deliver insightful and actionable data that helps our clients make informed decisions about their industry and market. Our customized approach allows us to tailor our research to each client's specific needs and goals, ensuring that they receive the most relevant and valuable insights.

Contact Us

Email: [email protected]

Tel: UK: +44 203 695 0070, USA: +1 646 905 0080

0 notes

Text

PAG to acquire Manjushree Technopack for Rs 8,400 crore

Asia-Pacific-focused alternative investment firm PAG will acquire a majority stake in Manjushree Technopack, India’s largest rigid plastic packaging solution company, for Rs. 8,400 crore (approximately US$ 1 billion). The deal to acquire Manjushree Technopack will be PAG’s third billion-dollar deal this year and the largest it has done in India.

PAG considers the Asia Pacific region to be one of the fastest growing regions and by alternative investment, it looks at off-market opportunities. It has US$ 55 billion under management by over 300 global institutional investors. It manages four pan-Asian buyout funds and two growth funds with US$ 19 billion of capital under management and investments of over US$ 3 billion across various business sectors in India since 2009. Since the founding of its office in the country under the leadership of Nikhil Srivastava in 2019, it has so far invested US$ 1.7 billion.

Manjushree Technopack was established in 1979 and started its plastic container manufacturing operations in Bangalore in 1987. It has 20 plants across India for manufacturing plastic bottles and jars and PET hot-fillable bottles and pre-forms used by the food, beverages, pharmaceutical, cosmetic, agricultural chemicals, automotive lubricants, and numerous other consumer and industrial segments. The company says that its clients number over 110,000. It reported a revenue of Rs 2,130 crore in FY24, which is up from its reported revenue of Rs 2,096 crore in FY 2023 and RS 1,474 crore in FY22. It has an annual installed capacity of plastic containers and related materials of approximately 213,000 metric tons.

0 notes