#Loan Moratorium

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Celebrities use Tumblr as well.

Text

Apply loan now and enjoy conveniet EMIs , Get free consultation 84888 44116, seamless documentation process, affordable interest rates, and flexible tenure.

#financeyourdreams#financialempowerment#home loan#home loan agency in ahmedabad#housing loan agency in ahmedabad#loan consultation in ahmedabad#loan services provider in ahmedabad#moratorium finserv

0 notes

Text

0 notes

Text

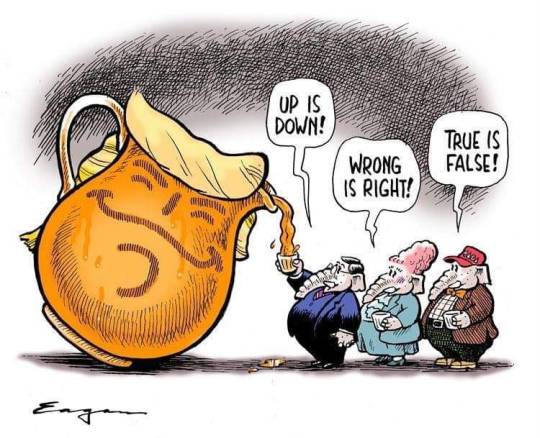

Harris and Schumer Target the Supreme Court

Democrats make clear that if they win, they’ll push measures to destroy the judiciary’s independence.

By

David B. Rivkin Jr. and Andrew M. Grossman -- Wall Street Journal

Democrats have made clear that if they win the presidency and Congress in November, they will attempt to take over the Supreme Court as well. Shortly after ending his re-election campaign, President Biden put forth a package of high-court “reforms,” including term limits and a “binding” ethics code designed to infringe on judicial authority. Kamala Harris quickly signed on, and Majority Leader Chuck Schumer has made clear that bringing the justices to heel is a top priority.

Democrats proclaim their devotion to democratic institutions, but their plan for the court is an assault on America’s basic constitutional structure. The Framers envisioned a judiciary operating with independence from influences by the political branches. Democratic “reform” proposals are designed to change the composition of the court or, failing that, to influence the justices by turning up the political heat, as President Franklin D. Roosevelt achieved with his failed 1937 court-packing plan.

Now as then, the court stands between a Democratic administration and its ambitions. The reformers’ beef is precisely that the court is doing its job by enforcing constitutional and statutory constraints on the powers of Congress and the executive branch.

Roosevelt sought to shrug off limits on the federal government’s reach. What’s hamstrung the Obama and Biden administrations is the separation of powers among the branches. President Obama saw his signature climate initiative, the Clean Power Plan, stayed by the court, which later ruled that it usurped Congress’s lawmaking power. The Biden administration repeatedly skirted Congress to enact major policies by executive fiat, only for the courts to enjoin and strike them down. That includes the employer vaccine mandate, the eviction moratorium and the student-loan forgiveness plan.

That increasingly muscular exercises of executive power have accompanied the left’s ascendance in the Democratic Party coalition is no coincidence. The legislative process entails compromise and moderation, which typically cuts against radical goals. That was the lesson self-styled progressives took from ObamaCare, which they’ve never stopped faulting for failing to establish a government medical-insurance provider to compete directly with private ones. Similarly, Congress has always tailored student-loan relief to reward public service and account for genuine need.

Then there’s the progressive drive for hands-on administration of the national economy by “expert” agencies empowered to make, enforce and adjudicate the laws. The Supreme Court has stood as a bulwark against the combination of powers that James Madison pronounced “the very definition of tyranny.” Decisions from the 2023-24 term cut back on agencies’ power to make law through aggressive reinterpretation of their statutory authority, to serve as judge in their own cases, and to evade judicial review of regulations alleged to conflict with statute. By enforcing constitutional limits on the concentration of power in agencies, the Roberts court has fortified both democratic accountability and individual liberty.

That explains the Democratic Party’s attacks on the court. The New York Times’s Jamelle Bouie recently praised Mr. Biden for identifying the court as the “major obstacle to the party’s ability” to carry out its agenda and commended the president’s “willingness to challenge the Supreme Court as a political entity.” That explains the ginned-up “ethics” controversies: The aim is to discredit the court, as has become the norm in political warfare.

An even bigger lie is the refrain that the court is “out of control” and “undemocratic.” Consider the most controversial decisions of recent terms. Dobbs v. Jackson Women’s Health Organization (2022) returned the regulation of abortion to the democratic process. West Virginia v. EPA(2022) and Loper Bright Enterprises v. Raimondo (2024) constrained agencies’ power to say what the law is, without denying Congress’s power to pursue any end. Securities and Exchange Commission v. Jarkesy (2024) elevated the Seventh Amendment right to a jury in fraud cases over the SEC’s preference to bring such cases in its own in-house tribunals. And Trump v. U.S. (2024), the presidential immunity ruling, extended the doctrine of Nixon v. Fitzgerald (1982) to cover criminal charges as well as lawsuits, without altering the scope of presidential power one iota.

Meanwhile, the administrative state has scored wins in some of this year’s cases. In Consumer Financial Protection Bureau v. Community Financial Services Association, the justices rejected a challenge to the CFPB’s open-ended funding mechanism. A ruling to the contrary could have spelled the agency’s end. In Moody v. NetChoice, it reversed a far-reaching injunction restricting agencies’ communications with social-media companies seeking to censor content. And in Food and Drug Administration v. Alliance for Hippocratic Medicine, it reversed another injunction, against the FDA over its approval of an abortion pill. The last two decisions were notable as exercises of judicial restraint. In both cases, the court found the challengers lacked standing to sue.

What Mr. Biden, Ms. Harris, Mr. Schumer and their party are attempting to do is wrong and dangerous. They aim to destroy a branch of federal government. For faithfully carrying out its role, the court faces an unprecedented attack on its independence, beyond even Roosevelt’s threats. Unlike then, however, almost every Democratic lawmaker and official marches in lockstep, and the media, which were skeptical of Roosevelt’s plan, march with them.

As Alexander Hamilton observed, the “independence of the judges” is “requisite to guard the Constitution and the rights of individuals” from the actions of “designing men” set on “dangerous innovations in the government.” The political branches have forgone their own obligation to follow the Constitution, which makes the check of review by an independent judiciary all the more essential. Ms. Harris and Mr. Schumer would put it under threat.

Mr. Rivkin served at the Justice Department and the White House Counsel’s Office in the Reagan and George H.W. Bush administrations. Mr. Grossman is a senior legal fellow at the Buckeye Institute. Both practice appellate and constitutional law in Washington.

#wall street journal#us supreme court#kamala harris#kamala#harris#Walz#Biden#Obama#Schumer#Pelosi#AOC#Democrats#trump 2024#trump#president trump#america#americans first#america first#donald trump#repost#ivanka#joe biden#republicans#gop

49 notes

·

View notes

Note

I find your post about policy disingenuous. 1) because making it seem like; "it's just about Palestine" is incredibly racist in ways I don't have the spoons to explain right now. But 2), your list leaves out the very real and very racist policy actions that Biden has taken against prisoners and immigrants. Under Biden the situation in prisons and at the border has gotten considerably worse than under Trump. He literally has more children in cages than Trump ever did. But apparently children in cages are only bad when Cheeto Man does it.

I'm not the one making it "just about Palestine", the people screaming "Genocide Joe!" are the ones making it just about Palestine. I'm trying to get people to look at literally any other issue besides Palestine - that's the entire reason I made that chart, to PROVE there's so much more at stake than "just Palestine". Stop blaming single-issue voters on ME when you're actually angry at THEM.

I am in fact currently going through the entire list because a different Anon claimed Biden is not "for" any of the things on the list. It is going to take a long time. But I will tackle your specific concerns.

Biden and immigration

It is frankly unfair to compare the number of people at the border under Biden to Trump's era, because their immigration policies are very different.

Yes, immigration at the border gone up since Biden took office. Most of the encounters at the borders have been with asylum seekers. And yes, technically there are more children "in cages" that there was when Trump was in office... because Trump wasn't letting children into the country at all. Biden is not turning them away, unlike Trump, who cited "COVID concerns" as his reason for turning starving and dehydrated children away from the border. In Trump's case, this was actually just straight up racism, because he hates Mexicans. He also hates Muslims, and enacted many immigration and travel bans against people from majority-Muslim nations. So yeah, of course there were less people being processed through immigration centers: Trump was turning them all away.

Your comparison, therefore, is extremely disingenuous. I don't think kids in custody is good, but I also think it's slightly better than kids dying of thirst in the desert or being forced to return to unsafe places.

Source: Politifact Fact-Check

Biden and prison reform

As for Biden's actions towards prisoners: Biden has been big on criminal justice reform his entire term. Here is a list of some things (among many more) he has done for criminal justice reform:

A majority of the people he nominated to appoint to courts around the country were people of color and/or women, in an effort to increase diversity in the criminal justice system.

He placed a moratorium on the death penalty.

He ordered the Department of Justice to not renew contracts with private (for-profit) prisons for federal prisoners.

He has pardoned and commuted many federal sentences for non-violent drug-related crimes (he has no control over non-federal convictions).

He provided grants to encourage the hiring of people with prior convictions.

He enacted a program to ensure prisoners leaving prison were given proper temporary IDs, which the were not in the past.

He pardoned federal offenses for the simple possession and use of marijuana.

He expanded Pell grants for prisoners to be able to obtain degrees during and after they leave prison

Added more options for prisoners with loans to consolidate and get onto repayment plans as low as $0 a month.

He enacted the First Step act, which facilitates prisoner reentry to society, rehabilitation, and reduces prisoner numbers in federal prison, including the release of over 30,000 prisoners.

He reduced the checking of criminal records in hiring processes for federal positions, enabling more people to be hired to those positions.

Added 19 new recidivism-reduction programs (programs to reduce the chances someone will end up back in jail).

This is not an exhaustive list. He has done EVEN MORE for criminal justice reform than this. You can just google this stuff, it's not hard to find.

Sources:

WhiteHouse.Gov

NBC News

Times.Com

17 notes

·

View notes

Text

I got an ask this morning that I've taken some time to consider. I will not be replying directly to it, because its an anon, and someone claiming to be a mutual for years so if they wanna talk they can dm me, but this can be a more full breakdown than an ask can reasonably get.

I've posted proof of the cost of my roommates last ($500) appointment within the past two weeks. If anyone wants to dm me for more proof, I really don't mind.

Those who have been following me for years probably remember why I don't feel safe sharing much info outside of dms at all. It's stalking and abuse, but if anyone needs more details, I dont mind answering that either.

We have been in various stages of getting out of homelessness and seeking treatment for disability for a while now. Fought for my roommate's legal documents for years. A lot of this stuff has been going on for years before we ever asked for help online or otherwise. We got evicted as soon as the rent moratorium ended, and not long after, we got covid that almost killed us. That left me permanently more disabled and left my roommate with a brand new disability on top of the existing ones. For a point of reference, even before the pandemic, I was his full-time caregiver. I still am.

On that note, he spent most of this time last year in and out of the hospital. I am still his full-time caregiver. He still has thousands in unpaid hospital bills. Again, dm me, I do not mind providing proof of all of this. I have his medical records and permission to share them if I remove the super sensitive info such as social security number.

My posts are generally phrased similarly or the same because if I think I phrased it correctly the first time, I will phrase it that way again. I am autistic, and people who talk to me enough to get to know me know I speak on scripts, and I am very repetitive. The people in my life irl remark on it. I don't really know what else to say, except I'm far from the only person on here who does that. I'm not even the only person who does that for the same reasons. I update my posts when I get a notification, and I check my email frequently most days. I do not thank every person who helps us, and I'm sorry. I try, and will keep trying.

Food is our biggest cost due to me and my roommate both having life threatening allergies to dairy, soy, and gluten. I don't know if you can understand how expensive that is until you live it. We are trying to reduce costs though. We have a garden, are expanding to that daily, as well as a greenhouse that was already here when we moved in which we have filled. And fruit trees and berry bushes.

And pretty importantly, all of the supplies have been given/loaned to us by a family member. A lot of the plants were previously planted and came out of dormancy in the last few weeks because it's currently spring. If half of what we have planted now does well, we will be fine on food. If anyone wants proof of all that, I would actually be overjoyed to share about our progress in that. I am really proud of our plants.

I have been looking for a job, I've mentioned that in posts before, but I am still applying. I am a full-time caretaker of a disabled person while also being disabled. I am limited to online work. If anyone has anything I can apply for oh my god I would appreciate it. I will be doing yard sales now that its warmer to help unclutter that previously mentioned family member's house of antiques and collectibles, and I'll get money from that. I do commissions at my art blog @theartistrans I have been doing gig shit and trading labor for goods and dogsitting. I don't have a regular 9-5, but I work.

And I do have a second roommate. She just largely takes care of her own for now, although that's been on and off some in the past as major things happened in her life.

2 notes

·

View notes

Text

SPEECH BY THE GOVERNMENT OF CHINA

1 June, 2022

The embezzlement of government funds by top leaders of the country, and the failure to take adequate steps toward the betterment of the nation’s political, social, and economical landscape has come under international scrutiny. The government of the People’s Republic of China has seen the events taking place in the country and is displeased by the use of the funds at the disposal of the parliament.

"This government views this as a misuse of the funds it has made available to the country through its loans and is henceforth lifting the moratorium on loan payments. It is halting any ongoing discussions on the possibility of restructuring Sri Lanka’s debt and demands the government of Sri Lanka begin payment of the loans immediately, with the first payment scheduled at the beginning September 2022

4 notes

·

View notes

Text

Please help me overcome my financial crisis and secure my future

I am struggling with my finances for a while now. Despite my best efforts, unable to generate enough income to cover my expenses as my bills have passed my income. I have been forced to rely on credit cards and loans to meet the bills, and my debt has been growing steadily. I am now at a point where I am struggling to make even the minimum payments on my debts, and I am facing the very real possibility of bankruptcy.

I am reaching out to you today because I am in urgent need of $50,000 or INR 45 lakhs(4,500,000) so that i can do partial payment of my debt and my total debt with various banks is $98000 or INR 84 Lakhs(total debt with banks).This will help me pay off my existing debts, cover my basic living expenses. With your help, I can get back on my feet and start building a better future for myself and my family.

I run a website called My Finance Managers (https://myfinancemanagers.com/), where I manage funds for my clients. Unfortunately, due to my own mistake in hiring the wrong people to manage the funds, I incurred huge losses from the stock market in the last 6 months. These losses wiped out all my savings and the entire loan taken from banks. I lost some of the amounts in crypto currencies which are out of trading now. As a result, I am currently living off credit cards and only able to pay the minimum due. The loan taken from the banks to pay off the losses has now become unmanageable, and the bank executives are chasing me for the money. I am left with no other option but to seek help online or face dire consequences. This has been a very bad experience for me, and I am struggling to stay afloat. However, I am determined to turn my situation around and get back on my feet. With your help, I can pay off my debts and start fresh.

If I am able to secure this amount, I will use it to pay off my existing debts and cover my basic living expenses. This will allow me to get out of the cycle of debt and start building a solid financial foundation.

There are several ways that you can help support me:

1. Donate: If you are in a position to do so, please consider making donation via various methods. Every little bit helps, and your support could make a huge difference in my life.

2. Share: Even if you are not able to donate, you can still help by sharing my campaign with your friends and networks. The more people who see my story, the more likely I am to reach my goal.

3. Encourage: Finally, your words of encouragement and support mean the world to me. Knowing that there are people out there who believe in me and my dreams gives me the strength and motivation to keep going, even when times are tough.

Any help financially or any opportunity to clear my debt i am looking to take. My situation is very worst that i have tried to negotiate with the bankers and try to extend the moratorium period but as the payments are delayed they are helpless.

I am also willing to repay the amount when i am financially strong. If anyone has any guidance or advice on how to handle this situation, it would be greatly appreciated. I am determined to turn things around and get back on track, but I cannot do it alone. Any help or support would be greatly appreciated.

I kindly request you to donate any amount possible to you.

Thank you for taking your time for me. With your help, I know that I can turn my financial struggles into success.

Please help with kind heart!!

Pay krishna surya using PayPal.Me

Go to paypal.me/krishnav556 and type in the amount. Since it's PayPal, it's easier and more secure. Don't have a PayPal…

paypal.me

You can contact/WhatsApp me on +918977426208 to know more details of my financial situation or you need more information to help.

From the bottom of my heart i thank all the persons who have come forward help me. Your help would save a family.

#finance#financial help#help help help#bankrupt#debt consolidation#funding#stock market#crypto currency#urgent funds#please donate#anything helps#urgent

7 notes

·

View notes

Text

Not to make a threat on a public official's life but whoever is responsible for making decisions around federal student loan servicers transferring loans to other servicers should have a philosophical bounty on their head.

My credit score has been top Fucking notch since sophomore year because as someone who grew up poor/lower income whatever, I was dedicated as shit to maintaining that one single chance. My credit card and my student loans are my only accounts. The credit card is maxed out as fuck rn and I'm considering my options so I went looking for some personal loans while I wait for this payment to hit my account next week. Why the fuck did my credit score come back as 425? Good question! Let's investigate!

Discover got rid of their credit monitoring last year and my life was just enough of a mess that it wasn't a priority until the student loans became an issue again. Slip #1. I checked my credit score on a different site and found that it had slipped from 768 to 648 in January. And why was that? Well, according to them, my student loans were gone. Vanished. Didn't exist. Poof.

Signed into the Great Lakes portal and low and behold my loans had been sold (or so I thought) to NelNet. Great. This is not the first time I have heard of this happening so while I'm not surprised I'm pissed off and now I have to deal with this shit. I called NelNet and thankfully the customer service person was really nice so I got down to the nitty gritty of the situation pretty fast and she was helpful too.

So basically, without notifying me or even trying to contact me, my loans were transferred to NelNet. Not sold, transferred at the demand of the Department of Education. Why? Because they have complete control over where my loans are held. True and morally reprehensible.

Let's list the ways in which this transfer has messed with my life:

As a very kind gift one of my parents made a payment on my interest before I graduated and before the moratorium went into place. NelNet does not have record of this payment. I have had to ask said parent to dig through their records and try to find it because it wasn't a regular transaction it was something specific like an education account or something.

When I changed my name, and then again when I got married, I had to submit a bunch of information to Great Lakes to get that all changed over. I never got a confirmation for either of these but they assured me it had been done. They do have record of my name change but not my marriage.

This is what could be potentially fucking over my credit score, but it is also possible that the credit bureaus can legally penalize my score for this. A big part of my score is the longevity of this account. The customer service person could not answer if this account would be considered an entirely new one or if it would carry over. If that's the case (and my loans aren't forgiven with Biden's shit), I'm legitimately going to start looking for people to file a class action lawsuit.

MY CREDIT SCORE DROPPED OVER 100 POINTS THAT'S INSANE

I didn't know about this!!! My previous servicer didn't call me they didn't try to get in contact with me!!!!!!!!! This could have completely fucked my whole life if I didn't look at loans!!! NelNet did try to contact me about this probably about two weeks ago but I disregarded it because I knew NelNet was a loan servicer and I get spam calls from people pretending to be with financial institutions all the time.

Anyways I'm gonna come after someone's pussylips for this shit and it's not gonna be pretty. I'm not a capitalist by any means and my credit score ~doesn't define me~ obviously but like hell am I gonna let the Department of fucking Education be the reaper of my immediate financial future. I'm coming for their asses.

12 notes

·

View notes

Photo

LETTERS FROM AN AMERICAN

April 3, 2023

Heather Cox Richardson

On Saturday, April 1, the emergency measures Congress put in place to extend medical coverage at the beginning of the Covid-19 pandemic expired. This means that states can end Medicaid coverage for people who do not meet the pre-pandemic eligibility requirements, which are based primarily on income. As many as 15 million of the 85 million people covered by Medicaid could lose coverage, although most will be eligible for other coverage either through employers or through the Affordable Care Act. The 383,000 who will fall through the cracks are in the 10 states that have refused to expand Medicaid.

The pandemic prompted the United States to reverse 40 years of cutbacks to the social safety net. These cuts were prescribed by Republican politicians who argued that concentrating money upward would promote economic growth by enabling private investment in the economy. That “supply side” economic policy, they said, would expand the economy so effectively that everyone would prosper. In 2017, Republicans passed yet another tax cut, primarily for the wealthy and for corporations, to advance this policy.

As the economy fell apart during the coronavirus pandemic, though, it was clear the government must do something to shore up the tattered social safety net, and even Republicans got on board fast. On March 6, 2020, Trump signed the Coronavirus Preparedness and Response Supplemental Appropriations Act, allocating $8.3 billion to fund vaccine research and give money to states and local governments to try to stop the spread of the virus. On March 18, he signed the Families First Coronavirus Response Act, which provided food assistance, sick leave, $1 billion in unemployment insurance, and Covid testing. On the same day, the Federal Housing Administration put moratoriums on foreclosure and eviction for people with government-backed loans.

On March 27, Congress passed the Coronavirus Aid, Relief, and Economic Security Act (CARES), which appropriated $2.3 trillion, including $500 billion for companies, $349 billion for small businesses, $175 billion for hospitals, $150 billion to state and local government, $30.75 billion for schools and universities, individual one-time cash payments, and expanded unemployment benefits.

Trump signed another stimulus package on April 24, 2020, which appropriated another $484 billion. And on December 27, 2020, he signed another $900 billion stimulus and relief package.

When he took office, President Joe Biden promised to rebuild the American middle class. He and the Democratic Congress began to shift the government’s investment from shoring up the social safety net to repairing the economy. On March 19, 2021, he signed the American Rescue Plan into law, putting $1.9 trillion behind economic stimulus and relief proposals.

Biden signed the Infrastructure Investment and Jobs Law, also known as the Bipartisan infrastructure Act, on November 15, 2021, putting $1.2 trillion into so-called hard infrastructure projects: roads and bridges and broadband.

On August 9, 2022, he signed the CHIPS and Science Act, putting about $280 billion in new funding behind scientific research and the manufacturing of semiconductors. And days later, on August 16, Biden signed the Inflation Reduction Law, putting billions behind addressing climate change and energy security while also raising money to pay for new policies and to reduce the deficit by raising taxes on corporations and the wealthy, funding the Internal Revenue Service to stop cheating, and permitting Medicare to negotiate with pharmaceutical companies over drug prices.

This dramatic investment in the demand side, rather than the supply side, of the economy helped to spark record inflation, compounded by supply chain issues that created shortages and encouraged price gouging. To combat that inflation, the Federal Reserve has been raising interest rates. Numbers released Friday show that inflation cooled in February, suggesting that the Federal Reserve is seeing the downward trend it has been hoping for, although there is concern that the sudden decision of the Organization of the Petroleum Exporting Countries (OPEC) this weekend to slash production of crude oil might drive the price of oil back up, dragging prices with it.

That investment in the demand side of the economy also meant that the child poverty rate in the U.S. fell almost 30%, while food insufficiency fell by 26% in households that received the expanded child tax credit. The U.S. economy recovered faster than that of any other G7 nation after the worst of the pandemic. Wages for low-paid workers grew at their fastest rate in 40 years, with real income growing by 9%. MIddle-income workers’ wages grew by only between 2.4% and 3.9% after inflation, but that, too, was the biggest jump in 40 years. Unemployment has fallen to its lowest level since 1969, and a record 10 million people have applied to start small businesses.

This public investment in the economy has attracted billions in private-sector investment—chipmakers have planned almost $200 billion of investments in 17 states—while it has also pressured certain companies to act in the public interest: the three major insulin producers in the U.S., making up 90% of the market, have all capped prices at $35 a month.

As the economy begins to smooth out, Biden and members of his administration are touting the benefits of investing in the economy “from the bottom up and the middle out.” They have emphasized that they are working to support unions and the rights of consumers, taking on “junk fees,” noncompete agreements, and nondisparagement clauses. After the collapse of the Silicon Valley Bank, the administration has suggested that deregulation of banking institutions went too far, and Biden has continued to push increased support for child care and health care.

A recent Associated Press–NORC poll shows that while 60% of Americans say the federal government spends too much money, they actually want increased investment in specific programs: 65% want more on education (12% want less); 63% want more on health care (16% want less); 62% want more on Social Security (7% want less); 58% want more spending on Medicare (10% want less); 53% want more on border security (23% want less); and 35% want more spending on the military (29% want less).

This puts the political parties in an odd spot. A week ago, Biden and members of the administration began barnstorming the country to highlight how their policy of “Investing in America” has been building the economy: “unleashing a manufacturing boom, helping rebuild our infrastructure and bring back supply chains, lowering costs for hardworking families, and creating jobs that don’t require a four-year degree across the country,” as the White House puts it.

Meanwhile, the Republicans are doubling down on the idea that such investments are a waste of money, and are forcing a fight over the debt ceiling to try to slash the very programs that the administration is celebrating. Ignoring that the 2017 Trump tax cuts and spending under Trump added about 25% to the debt, they are focusing on Biden’s policies and demanding that the government balance the budget in 10 years without raising taxes and without cutting defense, veterans benefits, Social Security, or Medicare, which would require slashing everything else by an impossible 85%, at least (some estimates say even 100% cuts wouldn’t do it).

As David Firestone put it today in the New York Times: “Cutting spending…might sound attractive to many voters until you explain what you’re actually cutting and what effect it would have.” Republicans cut taxes and then complain about deficits “but don’t want to discuss how many veterans won’t get care or whose damaged homes won’t get rebuilt or which dangerous products won’t get recalled.” Firestone noted that this disconnect is why the House Republicans cannot come up with a budget. “The details of austerity are unpopular,” Firestone notes, “and it’s easier to just issue fiery news releases.”

LETTERS FROM AN AMERICAN

HEATHER COX RICHARDSON

#kookaid#Republican Kool-Ade#budget#Federal Government spending#pandemic#medicare#medicaid#income inequality#Corrupt GOP

9 notes

·

View notes

Text

Finding the Right Loan: A Guide to Loan Options and Choosing the Best Fit for You

Introduction

Finding the right loan product to fit your needs can be a challenging process. With so many options like personal loans, home loans, and business loans, how do you know which is best suited for you? In this post, we'll provide an overview of the major loan products available and factors to consider when choosing one, as well as how Loans Mantri can help simplify the loan application process.

Loans Mantri is an online loan marketplace that partners with over 30 top financial institutions in India including names like HDFC Bank, ICICI Bank, and Axis Bank. No matter what type of loan you need, Loans Mantri aims to provide customized options and a seamless application experience through their digital platform.

Whether you need funds for personal expenses, purchasing real estate, business financing or any other purpose, Loans Mantri can match you with the ideal lending product for your requirements from their network. Their online eligibility calculators and tools remove the guesswork from determining what loans you can qualify for based on your income, credit score and other details.

This post will walk through the key loan products offered through Loans Mantri and outline the most important points to factor in when deciding which option works for your financial situation. We'll also provide tips on how to apply and what to expect when going through Loans Mantri for your financing needs. Let's get started!

Types of Loans Available

Here are some of the major loan products offered through Loans Mantri's platform:

Personal Loans - These unsecured loans can be used for almost any personal purpose like debt consolidation, wedding expenses, home renovation, medical needs, or any other requirements. Interest rates are competitive and loan amounts can range from ₹50,000 to ₹25 lakhs based on eligibility.

Home Loans - Also called mortgage loans, these are for purchasing, constructing or renovating a residential property. Home loans offer extended repayment tenures of up to 30 years and relatively lower interest rates. The property becomes collateral against the loan amount.

Business Loans - Loans Mantri offers financing for a wide range of business needs like working capital, equipment purchases, commercial vehicle loans, construction requirements and more. Loan amounts can be from ₹10 lakhs to multiple crores.

Loan Against Property - By using your existing property as collateral, you can get a secured, high-value loan in return through this product. Interest rates are lower and you can get up to 50% of your property's current market value.

Other Loan Products - Loans Mantri also facilitates other lending options like credit cards, line of credit, gold loans, insurance financing, merchant cash advance for businesses etc. as per eligibility.

Factors to Consider When Choosing a Loan

When looking at the various loan options, here are some key factors to take into account:

- Loan amount required and ideal repayment tenure

- Interest rates and processing/administration fees

- Your repayment capacity based on income and expenses

- Purpose of the loan - personal needs, business growth, property purchase etc.

- Collateral availability for secured loans like home and property loans

- Flexibility in repayment - moratorium periods, EMIs, tenure etc.

- Prepayment and foreclosure charges, if any

Evaluating these parameters will help identify the loan that Aligns to your financial situation. Loansmantri's online tools also help estimate factors like eligibility amounts, EMIs, interest rates etc. to simplify decision making.

Applying for a Loan on Loans Mantri

The application process with Loans Mantri is quick, transparent and fully digital:

- Use the eligibility calculator to get an estimated loan amount you can qualify for.

- Fill out the online application by providing basic personal and financial details.

- Loans Mantri will run a soft credit check to view your credit score and report. This helps match products to your profile.

- Compare personalized loan quotes from multiple partner banks and NBFCs.

- Submit any required KYC documents and income proofs online.

- The application gets forwarded to the lender for further processing and approval.

- Track status directly through your Loansmantri dashboard. Get assistance from customer support if needed.

Conclusion

Loans Mantri aims to be a one-stop platform for all your lending needs. Their intuitive tools and partnerships with leading financial institutions help identify and apply for the ideal loan product for any purpose. Consider your requirements carefully and evaluate all options before choosing the right loan for your financial situation. With Loans Mantri, the entire process from application to disbursal can be completed digitally for an easier financing experience.

2 notes

·

View notes

Text

Education Loan for Abroad Studies: Explore Student Loans

An investment in knowledge pays the best interest! And if the knowledge is attained at a top-tier and premium university then it is sure to elevate your career to the next level. However, the unfortunate reality is that the cost of studying in a reputed college is usually quite steep. And studying in a good college overseas is an even more expensive proposition.

Education loans for abroad studies help students, irrespective of their financial status, realize their dream of studying in one of the best universities in the world.

Numerous banks and other lenders now provide foreign education loans for students who want to study abroad. These lenders have different education loan schemes on offer, but choosing the one that is right for you is not an easy task. And that is where GyanDhan helps.

We match you with that lender, which is the best education loan for abroad studies that suits your profile and needs perfectly, and then help secure the loan approval in the most seamless and hassle-free manner.

What is the Maximum Loan Limit For Education Loans to Study Abroad?

In secured education loans, students can apply for student loans of up to INR 1.5 cr. In foreign education loans without collateral, students can apply for study loans of up to INR 45 Lakhs. This loan amount limit can increase or decrease depending on the applicant’s and co-applicant’s profile, country, course, etc.

How to Apply for Abroad Education Loans?

The steps to apply for a loan for financing the studies abroad are:

Step-1: Check your loan eligibility online.

Step-2: Get expert loan counseling to compare the options available.

Step-3: Select a lender and apply online.

Step-4: Get the customized education loan document checklist.

Step-5: Submit the required education loan documents either online or get documents picked up from your home by our representative.

Step-6: Get the property & other legal evaluations done (in secured loans).

Step-7: Get the loan sanction letter after the education loan approval from the lender.

How to Choose the Best Overseas Education Loan?

Taking an education loan to supplant the cost of education overseas is the right choice. Depending on the amount and your profile, financial institutions can finance even 100% of the cost of the course.

However, to get the best education loan option, one needs to carefully analyze the following key aspects of the various options available. When you apply to GyanDhan, we do this analysis for you. In case you do the loan comparison yourself, consider these factors:

Interest Rate: Even a 1% increase in the education loan interest rate has a substantial financial effect. Example - Loan Amount: Rs. 30,00,000, Loan Repayment in: 5 years after you graduate, Course Duration: 2 years; While at 10%, you’ll pay Rs. 9.7 lakhs in interest, at 11%, you’ll pay Rs. 10.9 lakhs - that’s a difference of 1.2 lakhs for just 1%!. Also, historical changes done by any lender in its interest rates should also be considered.

Repayment Holiday/Moratorium Period: It is a specified period during the loan tenure in which the borrower is exempt from making repayments. Loans with a moratorium period have a big plus, as you don’t have to worry about making repayments while you study overseas.

Tax Rebate: Education loans for foreign studies taken from Indian banks are special in that the entire amount paid as interest is exempt from income tax. This has a huge impact: Example - Loan Amount: Rs. 30,00,000, Marginal tax bracket: 30%, Repayment in: 5 years after graduation, Course Duration: 2 Years, ROI: 10%... If your loan has tax rebate, you can save Rs. 2.9 lakhs!

Margin Money: The amount that you need to pay from your own pocket while the rest is paid by the bank. If a bank offers a 0% margin, it means they’ll fund all your education expenses in the offered loan amount.

Hidden Fees: There are numerous hidden fees that your lender might be charging you and when accumulated these will cost you a considerable amount, such as:

Forex Margin: Some lenders charge a forex conversion charge when the overseas education loan is sanctioned in INR and disbursed in some other currency. This can be as high as 1.5%, which translates to Rs. 45,000 for a loan amount of Rs. 30 lakhs.

Processing Fees: This varies from zero to as high as 2%. For a loan of Rs. 30,00,000, the processing fees can be as high as Rs. 60,000

Cost of Credit Life Insurance: Some lenders make it mandatory for the applicant to go in for credit life insurance with their education loan scheme so that their loan amount is protected against any unfortunate eventualities. If the premium amount is on the higher side then it eventually increases the cost of the education loan as well.

Mandatory Cross-Sell: Some lenders try to cross-sell other policies before sanctioning the education loan, even though it is not required on the applicant’s end.

Interest Rate in Different Currencies: Often students face a dilemma of choosing over an education loan in USD with a lower interest rate or an equivalent amount in INR with a higher interest rate. By the previous trend of the rising prices of US$ to INR conversion rates, it is a smart choice to go for the loan amount in INR even though it may come with a higher interest rate.

As you can see, by selecting the right overseas education loan, the reduction in cost can be as high as 5-6%.

Which is the Cheapest Education Loan in India to Study Abroad?

Public sector banks offer the State Bank or BoB lowest interest rates on loans for foreign education compared to private banks & NBFCs. If your institution is listed in BOB’s premium list of colleges, Bank of Baroda offers the cheapest education loan for abroad studies. Otherwise, the State Bank of India offers the cheapest education loans. However, the extent of the cheap education loan in India depends on several factors including the applicant’s profile, co-applicant’s financial profile, target country, target course, etc.

Are you eligible for an abroad education loan? Check here.

3 notes

·

View notes

Text

Fortune: ‘YOLO’ spenders are propping up the economy, says Wharton professor Jeremy Siegel—but they’re about to run out of cash

Different times in last eighteen months probable times when recession was predicted but did not occur make me wonder whether analyzing certain economic data or certain economic indicator works?

1. Regularly Reading few credible news outlets on economic news

2. reading difficult 2022 winter as recession trigger from predicted volatility in energy prices

3. reading inverted yield curve since July 2022,

4. end of stimulus related COVID payments,

5. end of COVID related moratoriums,

6. rise of inflation to 9% in June 2022 and corresponding decrease in inflation with Fed rate hikes not intended to cause recession but slight increase in unemployment and slight slowdown translated as not extreme unemployment, minimal wage growth with stable prices termed as soft landing,

7. Rise in used car prices followed by stability in used car prices

8. Reasoning of delay between end of stimulus payments and rise of credit card debts, depletion of savings in people's bank accounts

9. Not all Student loans forgiven while only certain such as below 20k student loans forgiven and the other student loans coming due, auto loans borrowed at higher rates as potential issue

10. Commercial real estate as another reason to cause recession

11. Household debt/ credit card debt risen to certain level

12. California as bell weather state signaling recession

But economy has shown no weakening signs

And now, after over 1 year, a Wharton Prof thinks another event could trigger due to its timing:

"last good stretches for the economy before the summer ends and credit card bills come due.” He added that in the past, when students return to school in September and October

Let's see what happens!!

If/ when recession does occur, what indicators do economists follow or whether economists really have deep insight or traders such as Michael Burry, George Soros, would like to reverse engineer how one can predict after next boom business cycle which could be from 2024 to ..... Let's say 2028 or any such future year.

3 notes

·

View notes

Text

"A car is ... something you just have to have, not unlike healthcare, housing, or, increasingly, higher education. We have social movements in each of these other arenas; we have Housing for All, we have College for All, we have Medicare for All, but we don’t have Transportation for All yet. And it deserves a movement. One-fifth of household income goes to transportation, it is such an inescapable necessity. We found during the pandemic, for example, people were prioritizing their car payments over all other payments. And unlike the eviction moratorium or suspension of student loan payments, car payments were not suspended.

"Moreover, if you are a car owner you are red meat for whoever wants to prey upon you, whether it is police, auto lenders, or state agencies interested in extracting data about your conduct. You are the object of predation and you have no choice."

Andrew Ross to Chenjerai Kumanyika, "Car Creditocracy: An Interview with Julie Livingston & Andrew Ross," Public Books, 4/4/23. Regarding their book, Cars and Jails: Freedom Dreams, Debt and Carcerality.

4 notes

·

View notes

Text

We evaluate the effects of the 2020 student debt moratorium that paused payments for student loan borrowers. Using administrative credit panel data, we show that the payment pause led to a sharp drop in student loan payments and delinquencies for borrowers subject to the debt moratorium, as well as an increase in credit scores. We find a large stimulus effect, as borrowers substitute increased private debt for paused public debt. Comparing borrowers whose loans were frozen with borrowers whose loans were not frozen due to differences in whether the government owned the loans, we show that borrowers used the new liquidity to increase borrowing on credit cards, mortgages, and auto loans rather than avoid delinquencies. The effects are concentrated among borrowers without prior delinquencies, who saw no change in credit scores, and we see little effects following student loan forgiveness announcements. The results highlight an important complementarity between liquidity and credit, as liquidity increases the demand for credit even as the supply of credit is fixed.

2 notes

·

View notes

Text

my provider not making me do a full phq9 at every visit anymore like i won’t kill myself the day the loan moratorium ends

3 notes

·

View notes

Text

What is CSIS ? (interest free education loan)

"Central Sector Interest Subsidy Scheme" (CSIS) provides full interest subsidy during the moratorium period ( i.e Course period + 1 Year) on modern education loans without any collateral security and third-party guarantee, for pursuing technical/professional courses in India.

To get Eligible for this scheme:

Students having parental income up to Rs. 4.5 lakhs per annum. - Students enrolled in professional/ technical courses only from NAAC accredited institutions or professional/ technical programmes accredited by NBA or Institutions of National Importance or Central Funded Technical Institutions (CFTIs). - CSIS is only applicable for domestic colleges and not for foreign institutions.

Source: Central Sector Interest Subsidy Scheme, 2009

1 note

·

View note