#H2 Receptor Antagonist Market Key Countries

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr Inc. is funded by 13 investors.

Text

The Gastrointestinal Agents Market is projected to grow from USD 59,863.47 million in 2023 to USD 92,867.89 million by 2032, reflecting a compound annual growth rate (CAGR) of 5.00%.The gastrointestinal (GI) agents market is a rapidly growing sector within the global pharmaceutical industry, driven by the increasing prevalence of gastrointestinal disorders, advancements in drug development, and rising awareness about digestive health. This article explores the key trends, market drivers, challenges, and future outlook of the gastrointestinal agents market.

Browse the full report at https://www.credenceresearch.com/report/gastrointestinal-agents-market

Overview of the Gastrointestinal Agents Market

Gastrointestinal agents are medications used to treat disorders of the digestive system, including conditions like gastroesophageal reflux disease (GERD), irritable bowel syndrome (IBS), peptic ulcers, Crohn's disease, and ulcerative colitis. These agents are categorized into several classes, such as antacids, proton pump inhibitors (PPIs), H2 receptor antagonists, laxatives, antidiarrheals, and antiemetics. The global gastrointestinal agents market has witnessed significant growth due to the rising incidence of these disorders, coupled with lifestyle changes, aging populations, and increasing adoption of unhealthy diets.

Key Market Drivers

1. Rising Prevalence of Gastrointestinal Disorders: The increasing incidence of GI disorders is a major driver of the market. According to the World Gastroenterology Organization, gastrointestinal diseases affect millions of people worldwide, with a particularly high prevalence in developed countries due to sedentary lifestyles, poor diet, and high levels of stress.

2. Aging Population: The growing aging population is another critical factor contributing to market growth. Older adults are more susceptible to gastrointestinal issues due to age-related changes in the digestive system, making them a key demographic for GI agents.

3. Advancements in Drug Development: Ongoing research and development activities have led to the introduction of novel GI agents that offer improved efficacy and safety profiles. Biologics and targeted therapies, for example, are gaining traction in the treatment of inflammatory bowel diseases (IBD) like Crohn's disease and ulcerative colitis.

4. Increased Awareness and Diagnosis: Enhanced awareness about digestive health and the availability of advanced diagnostic tools have resulted in the early detection and treatment of GI disorders, further boosting the demand for gastrointestinal agents.

5. Rising Healthcare Expenditure: Increased healthcare spending, particularly in emerging economies, has improved access to healthcare services and medications, propelling the growth of the GI agents market.

Challenges Facing the Market

1. Side Effects and Safety Concerns: Many gastrointestinal agents, especially long-term treatments such as PPIs, have been associated with side effects like kidney issues, infections, and bone fractures. Safety concerns can lead to regulatory restrictions and affect market growth.

2. High Cost of Advanced Therapies: The cost of new biologics and targeted therapies can be prohibitive for patients and healthcare systems, particularly in low- and middle-income countries. This cost barrier may limit market expansion in some regions.

3. Generic Competition: The expiration of patents for several blockbuster drugs has led to the entry of generic versions, which, while increasing accessibility, have also intensified competition and put pressure on market prices.

Future Outlook and Opportunities

The gastrointestinal agents market is poised for continued growth, with several opportunities on the horizon:

1. Innovation in Drug Delivery Systems: Innovations in drug delivery systems, such as delayed-release formulations, are expected to enhance the effectiveness of GI agents and improve patient compliance.

2. Personalized Medicine: The development of personalized medicine approaches, where treatment is tailored based on genetic and environmental factors, is gaining momentum. This approach promises to optimize treatment outcomes for GI disorders, particularly IBD.

3. Expansion in Emerging Markets: Emerging markets, including Asia-Pacific and Latin America, offer significant growth opportunities due to improving healthcare infrastructure, increasing disposable incomes, and growing awareness about GI disorders.

4. Digital Health and Remote Monitoring: The integration of digital health technologies and remote monitoring solutions is expected to improve the management of chronic GI conditions, enabling better patient outcomes and driving the demand for GI agents.

Key Player Analysis

Johnson & Johnson

Pfizer Inc.

AstraZeneca

AbbVie Inc.

Takeda Pharmaceuticals

Bayer AG

GlaxoSmithKline plc.

Sanofi

Allergan

Boehringer Ingelheim

Segments:

Based on Type:

Dietary Supplements

Drugs

Antacids

Anti-diarrheal Agents

Anti-emetics

H2 Blockers

Laxatives

Proton Pump Inhibitors

Based on Disease Type:

Constipation

Diarrhoea

Gastroesophageal Reflux Disease

Inflammatory Bowel Disease

Peptic Ulcer Disease

Based on Route of Administration:

Oral

Parenteral

Rectal

Based on End-User:

Homecare

Hospitals & Clinics

Based on Distribution Channel:

Offline Pharmacies

Online Pharmacies

Based on the Geography:

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/gastrointestinal-agents-market

About Us:

Credence Research is committed to employee well-being and productivity. Following the COVID-19 pandemic, we have implemented a permanent work-from-home policy for all employees.

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

Global Gastritis Treatment Market Is Estimated To Witness High Growth Owing To Increasing Prevalence of Gastritis

The global Gastritis Treatment Market is estimated to be valued at USD 162.2 million in 2021 and is expected to exhibit a CAGR of 4% over the forecast period 2022-2029, as highlighted in a new report published by Coherent Market Insights. A) Market Overview: Gastritis is a condition characterized by the inflammation of the lining of the stomach. It can be caused by various factors such as infection, excessive alcohol consumption, prolonged use of non-steroidal anti-inflammatory drugs (NSAIDs), and autoimmune diseases. The Gastritis Treatment Market products includes pharmaceutical drugs, proton pump inhibitors (PPIs), H2 receptor antagonists, antacids, and antibiotics. The need for gastritis treatment products arises due to the increasing prevalence of gastritis worldwide. According to the World Gastroenterology Organisation (WGO), gastritis affects approximately 50% of the global population. The rising incidence of risk factors such as H. pylori infection, unhealthy lifestyle habits, and the growing aging population contribute to the increasing demand for gastritis treatment products. B) Market Key Trends: One key trend in the gastritis treatment market is the increasing adoption of combination therapy. Combination therapy involves the simultaneous use of two or more drugs to achieve a synergistic effect in treating gastritis. This approach helps in improving treatment outcomes and reducing the risk of drug resistance. For instance, a combination therapy of proton pump inhibitors and antibiotics is often prescribed for the eradication of H. pylori infection. The use of combination therapy is expected to drive market growth during the forecast period. Technological: The development of advanced diagnostic techniques such as endoscopy and molecular tests has improved the accuracy and efficiency of gastritis diagnosis, leading to better treatment outcomes. D) Key Takeaways: 1: The global gastritis treatment market is expected to witness high growth, exhibiting a CAGR of 4% over the forecast period. This growth can be attributed to increasing prevalence of gastritis and the rising demand for treatment products. The market is driven by factors such as H. pylori infection, unhealthy lifestyle habits, and the growing aging population. 2: In terms of regional analysis, North America is expected to dominate the gastritis treatment market due to the high prevalence of gastritis in the region. Asia Pacific is anticipated to be the fastest-growing region, owing to the increasing healthcare expenditure and improving healthcare infrastructure in countries like India and China. 3: Key players operating in the global gastritis treatment market include Otsuka Indonesia PT, AstraZeneca PLC, Zydus Cadila Healthcare Limited, Novartis AG, and others. These companies focus on product development, partnerships, and collaborations to strengthen their market position. In conclusion, the global gastritis treatment market is projected to grow significantly over the forecast period. Increasing prevalence of gastritis and the adoption of combination therapy are key trends driving market growth. Political initiatives, economic factors, changing social habits, and technological advancements further contribute to the expansion of the market. North America is expected to dominate the market, while Asia Pacific is anticipated to witness the highest growth. Key players in the market include Otsuka Indonesia PT, AstraZeneca PLC, Zydus Cadila Healthcare Limited, and Novartis AG, among others.

#Proton Pump Inhibitors#Gastritis Treatment Market#Gastritis Treatment Market Share#Gastritis Treatment Market Size#Gastritis Treatment Market Demand

0 notes

Text

0 notes

Text

Global H2 Receptor Antagonist Market Size, Share, Development, Growth And Demand Forecast To 2026

Global H2 Receptor Antagonist Market Size, Share, Development, Growth And Demand Forecast To 2026

“Global H2 Receptor Antagonist Sales Market (Sales, Revenue and competitors Analysis of Major Market) from 2014-2026” the new research report adds in kandjmarketresearch.com research reports database. This Research Report spread across 105 Pages, with summarizing Top companies and supports with tables and figures.

A fresh specialized intelligence report published by KandJ Market Research with…

View On WordPress

#Covid-19 Impact on H2 Receptor Antagonist#H2 Receptor Antagonist#H2 Receptor Antagonist Demand#H2 Receptor Antagonist Industry#H2 Receptor Antagonist Market#H2 Receptor Antagonist Market Analysis#H2 Receptor Antagonist Market CAGR#H2 Receptor Antagonist Market Forecast#H2 Receptor Antagonist Market Growth#H2 Receptor Antagonist Market Key Countries#H2 Receptor Antagonist Market key player#H2 Receptor Antagonist Market Revenue#H2 Receptor Antagonist Market Sales#H2 Receptor Antagonist Market Share#H2 Receptor Antagonist Market Size#H2 Receptor Antagonist Market Trends#H2 Receptor Antagonist Research Report

0 notes

Text

GERD Drugs and Devices Market Demand Analysis, Statistics, Industry Growth Research Report till 2027

The Global GERD Drugs and Devices market Report offers extensive knowledge and information about the GERD Drugs and Devices market pertaining to market size, market share, growth influencing factors, opportunities, and current and emerging trends. The report is formulated with the updated and latest information of the GERD Drugs and Devices market further validated and verified by the industry experts and professionals. The report additionally sheds light on the emerging growth opportunities in the business sphere that are anticipated to bolster the growth of the market.

Gastroesophageal Reflux Disease is growing due to the intake of analgesics, smoking, decrease in the prevalence of Helicobacter pylori infection, consumption of certain types of food and drinks, high body mass index (BMI), family history of GERD, and limited physical activity. The growing incidence of the disease will drive the demand for the GERD drug and devices market.

The factors impacting the growth of the market are the rise in the trend of self-medication and increased awareness of GERD. Moreover, the constant occurrence of GERD disorders, as well as changes in lifestyle, are propelling the market demand. The expiration of the patent on most of the drugs is paving the way for new over the counter and generic drugs. The poor reimbursement of procedures and devices, low safety, and efficacy are restricting the adoption of the GERD drugs and devices market.

Click the link to get info@ https://www.emergenresearch.com/industry-report/gerd-drugs-and-devices-market

Some Key Highlights of Report

In November 2020, Sandoz Inc. announced it had shipped pantoprazole sodium to supply the hospitals for injection, 40 mg to Civica Rx. It is a part of a multiyear collaboration for the reduction in supply shortages with several other pipeline medicines.

H2 blockers are a group of drugs that reduces the amount of acid produced by the cell lining of the stomach. They are also known as histamine H2-receptor antagonists but are also known as H2 blockers. They include ranitidine, cimetidine, nizatidine, and famotidine, among others.

The MUSE or Medigus Ultrasonic Surgical Endostapler is an extensive endoscopic device that incorporates the latest technological advancement for the delivery of patient-friendly option for Transoral Fundoplication, the procedure intended for the treatment of GERD.

Overview of the TOC of the Report:

Introduction, Scope, and Overview

Opportunities, Risks, and Drivers

Competition landscape analysis with sales, revenue, and price

Extensive Profiling of the key competitors with the sales figures, revenue, and market share

Regional analysis with sales, revenue, and market share for each region for the forecast period

Country-wise analysis of the GERD Drugs and Devices market by type, application, and manufacturers

GERD Drugs and Devices Market Segmentation based on types

GERD Drugs and Devices Market segmentation based on applications

Historical and forecast estimation

Competitive Landscape:

Furthermore, the report includes an in-depth analysis of the competitive landscape. The segment covers a comprehensive overview of the company profiles along with product profiles, production capacities, products/services, pricing analysis, profit margins, and manufacturing process developments. The report also covers strategic business measures undertaken by the companies to gain substantial market share. The report provides insightful information about recent mergers and acquisitions, product launches, collaborations, joint ventures, partnerships, agreements, and government deals.

Key participants include Johnson & Johnson, AstraZeneca PLC, Takeda Pharmaceutical Company Limited, Pfizer Inc., Novartis AG, GlaxoSmithKline Plc, Merck & CO., Inc., Boston Scientific Corporation, Eisai Co., Ltd., and Ironwood Pharmaceuticals, Inc., among others.

For the purpose of this report, Emergen Research has segmented into the global GERD Drugs and Devices Market on the basis of route of administration, drug type, device type, and region:

Route Of Administration Outlook (Revenue, USD Billion; 2017-2027)

Oral

Parenteral

Drug Type Outlook (Revenue, USD Billion; 2017-2027)

H2 Receptor Antagonist

Proton Pump Inhibitor (PPIs)

Antacids

Device Type Outlook (Revenue, USD Billion; 2017-2027)

MUSE –Medigus Ultrasonic Surgical Endostapler

LINX Management System

Stretta Therapy

Bravo Reflux Testing System

Digitrapper reflux testing system

Others

Key takeaways of the Global GERD Drugs and Devices Market report:

The report sheds light on the fundamental GERD Drugs and Devices market drivers, restraints, opportunities, threats, and challenges.

It elaborates on the new, promising arenas in the leading GERD Drugs and Devices market regions.

It examines the latest research & development projects and technological innovations taking place in the key regional segments.

The research report reviews the regulatory framework for creating new opportunities in various regions of the GERD Drugs and Devices market

It focuses on the new revenue streams for the players in the emerging markets.

Furthermore, the report offers vital details about the rising revenue shares and the sizes of the key product segments.

Thank you for reading our report. Customization of the report is available. To know more, please connect with us, and our team will ensure the report is customized as per your requirements.

Take a Look at our Related Reports:

healthcare it market

https://www.google.bi/url?q=https://www.emergenresearch.com/industry-report/healthcare-it-market

coal tar market

https://www.google.bi/url?q=https://www.emergenresearch.com/industry-report/coal-tar-market

ir spectroscopy market

https://www.google.bi/url?q=https://www.emergenresearch.com/industry-report/ir-spectroscopy-market

eubiotics market

https://www.google.bi/url?q=https://www.emergenresearch.com/industry-report/eubiotics-market

nanotechnology market

https://www.google.bi/url?q=https://www.emergenresearch.com/industry-report/nanotechnology-market

ed-tech and smart classroom market

https://www.google.bi/url?q=https://www.emergenresearch.com/industry-report/ed-tech-and-smart-classroom-market

digital payment market

https://www.google.bi/url?q=https://www.emergenresearch.com/industry-report/digital-payment-market

signal conditioning modules market

https://www.google.bi/url?q=https://www.emergenresearch.com/industry-report/signal-conditioning-modules-market

About Us:

At Emergen Research, we believe in advancing with technology. We are a growing market research and strategy consulting company with an exhaustive knowledge base of cutting-edge and potentially market-disrupting technologies that are predicted to become more prevalent in the coming decade.

Contact Us:

Eric Lee

Corporate Sales Specialist

Emergen Research | Web: www.emergenresearch.com

Direct Line: +1 (604) 757-9756

E-mail: [email protected]

Visit for More Insights: https://www.emergenresearch.com/insights

Explore Our Custom Intelligence services | Growth Consulting Services

0 notes

Text

Erosive Esophagitis Market Trends 2030 | Erosive Esophagitis Market 2030

Gastroesophageal reflux disease (GERD) is caused by an abnormal reflux of gastric contents into the esophagus. According to the presence of esophageal mucosal breaks; GERD can be divided into two groups, erosive esophagitis and nonerosive reflux disease (NERD).

The term “erosive esophagitis,” which denotes esophageal mucosal erosive changes, has several synonyms: recurrent, reflux, regurgitant, peptic and marginal esophagitis. The term “erosive esophagitis,” is used for it covers mucosal changes other than erosion or ulceration and occurs without reflux or peptic activity.

DelveInsight's "Erosive Esophagitis (EE) Market Insights, Epidemiology, and Market Forecast-2030" report delivers an in-depth understanding of the Erosive Esophagitis (EE) , historical and forecasted epidemiology as well as the Erosive Esophagitis (EE) market trends in the United States, EU5 (Germany, Spain, Italy, France, and United Kingdom) and Japan.

Geographies covered are:

The United States, EU5 (Germany, France, Italy, Spain, and the United Kingdom), and Japan

Click here and get access to free sample pages of the report.

Erosive Esophagitis (EE) Disease Overview

Erosive esophagitis is diagnosed based on the Los Angeles classification and was divided into two categories: mild (grades A and B) and severe (grades C and D).

Patients with GERD with the typical reflux syndrome associated with erosive esophagitis and hiatal hernia can have mucosal eosinophilia, which often is confined to the distal esophagus. It is not clear what proportion of patients with GERD present with these features, but it is likely to be less than 10%.” In the same study, it was found that from 2003 to 2006, there were approximately 10,570 hospital admissions annually for erosive esophagitis.

Acid suppression with a H2 receptor antagonists (H2RAs) and proton pump inhibitors (PPIs) are a standard treatment for gastroesophageal reflux disease and erosive esophagitis in adults and increasingly is becoming first-line therapy for children aged 1–17 years.

The DelveInsight Erosive Esophagitis (EE) market report gives a thorough understanding of the Erosive Esophagitis (EE) by including details such as disease definition, symptoms, causes, pathophysiology, diagnosis and treatment.

Erosive Esophagitis (EE) Epidemiology

The most commonly encountered predisposing factors for Erosive Esophagitis are those related to defects at the esophagogastric junction, such as esophageal hiatal hernia, anatomic variants (short esophagus, intrathoracic stomach, direct esophagogastric junction), and physiologic dysfunction or deglutinative "chalasia“. A total of 23 contributing factors have been encountered, the most prominent of which are hyperacidity, hypersecretion, changes in esophagogastric tonicity, increase in intragastric pressure, and mucosal trauma.

The Erosive Esophagitis (EE) epidemiology division provide insights about historical and current Erosive Esophagitis (EE) patient pool and forecasted trend for every seven major countries. It helps to recognize the causes of current and forecasted trends by exploring numerous studies and views of key opinion leaders.

Key Findings

· In persons with GERD symptoms, about 20% are found to have erosive esophagitis, while ulcers or strictures are found in less than 5% of all patients with erosive esophagitis.

· As per findings of a study titled “High Rate of Clinical and Endoscopic Relapse After Healing of Erosive Peptic Esophagitis in Children and Adolescents” , (2014), Children with healed erosive esophagitis have up to 83% clinical relapse and of the 83%, 45% had endoscopic relapse.

Request for free sample pages of the report: https://www.delveinsight.com/sample-request/erosive-esophagitis-market

Erosive Esophagitis (EE) Drug Chapters

The dynamics of the Erosive Esophagitis market is anticipated to change in the coming years owing to the approval of the upcoming therapy. Key player, such as Takeda/Phathom Pharmaceutical, Ironwood Pharma, Daewoong Pharmaceutical, Luoxin Pharmaceutical and others is involved in developing a drug based on a novel class of P-CABs.

Erosive Esophagitis (EE) Market Outlook

The spectrum of GERD ranges from nonerosive to erosive or complicated disease (ulcer, columnar metaplasia, and stricture), each of which is thought likely to progress if either left untreated or not treated adequately. The goals of treating GERD are to resolve symptoms, heal esophagitis, and prevent complications. Treatment options include lifestyle modifications, medical management with antacids and antisecretory agents, and mechanical therapies.

Owing to their superior ability to inhibit gastric acid secretion compared with H2 receptor antagonists (H2RAs), proton pump inhibitors (PPIs) remain the mainstay of long-term therapy for GERD and hence for Erosive Esophagitis. Studies comparing H2-blockers and PPIs have demonstrated that the latter has superior healing rates and decreased relapse rates.

The Erosive Esophagitis market outlook of the report helps to build the detailed comprehension of the historic, current, and forecasted Erosive Esophagitis (EE) market trends by analyzing the impact of current therapies on the market, unmet needs, drivers and barriers and demand of better technology.

Expected launch of upcoming therapies shall fuel the growth of the Erosive Esophagitis market during the forecast period, i.e., 2020–2030.

To download sample pages of our market report, visit: https://www.delveinsight.com/sample-request/erosive-esophagitis-market

Visit our repository of reports: https://www.delveinsight.com/report-store.php

#Erosive Esophagitis market#Erosive Esophagitis market trends#Erosive Esophagitis market share#Erosive Esophagitis market size#Erosive Esophagitis market research reports

0 notes

Text

Polymeric Materials for the Development of Dual↓Working Gastroretentive Drug Delivery Systems. A Breakthrough Approach

Abstract

Oral route is the most convenient and widely used method of drug administration, representing about 90% of all therapies used. It displays great advantages, such as being non-invasive, easy to administer (with the consequent high patient compliance) and cost-effective. However, serious drawbacks to conventional oral dosage forms are imposed by the gastrointestinal tract. Large fluctuations in drug bioavailability are found due to the influence of physiological factors such as variations in pH, high enzymatic activity and gastric emptying. This is the reason why frequent drug administrations are required to maintain the therapeutic plasma level of the drug. Gastroretentive Drug Delivery Systems (GRDDS) have emerged as an ideal approach to overcome these drawbacks. They are designed to prolong the gastric residence time (GRT) of the dosage forms in the stomach so that the time between dose administration is lengthened. Although their development has partially overcome the drawbacks associated with conventional dosage form, further work is needed on its shortcomings. The overall objective of this minireview is to highlight the opportunities from the development of dual-working polymeric materials, suitable for their use as GRDDS with improved GRT and capable of overcoming common drawbacks associated with conventional GRDDS. This could be achieved by a combination of properties such as buoyancy, swelling, porosity, and bioadhesion of the synthesized materials.

Keywords: Biopolymers; Biodegradability; Delayed Gastric Emptying Devices; Porous Matrices; Microspheres; Dds; Bioavailability; Extended Release; Personalized Healthcare

Introduction

Spain, with a population of 46.7 million people, is one of the countries with longer life expectancies in the word. The data have been improving substantially in the last two decades reaching the outstanding figures of 80.2 years for males and 85.8 years for women in 2017 (Figure 1). However, the population is aging, and their quality of life is not optimal. Most of our elders suffer from chronic diseases that must be treated continuously for long periods of time with the consequent enormous impact on people’s lives. But they do not have the exclusivity of suffering from chronic disorders; a relevant segment of middle-age population is getting into treatment of several diseases such as diabetes, cardiovascular diseases, neurological disorders, and chronic respiratory diseases, just to mention a few examples. This fact draws a notable impact on the Healthy life expectancy (HALE)1 of the population. According to the Institute for Health Metrics and Evaluation (GBD 2017, University of Washington), life expectancy and HALE differ substantially from each other, not only for the Spaniards, but also for all the population from developed countries. As an example, and for comparative reasons, Table 1 records the figures for both parameters, life expectancy and HALE, for population from Western Europe and Spain.

Globally, the market for pharmaceutical spending was expected to surpass $1.3 trillion by 2018 [1]. Notably, the main difficulties encountered in achieving effective treatment are related to transport and precise delivery of drugs to specific damaged organs or tissues, because releasing the right amount of drug at the exact location at the suitable rate is not a trivial issue. In this sense, scientific policies should focus on: (a) promoting research on more effective drugs and, to a greater extent, (b) supporting research on more effective drug delivery systems.

Foot Note

1number of years that a person at a given age can expect to live in good health, considering mortality and disability.

Thus, the global outcomes obtained by this research support strategy would conduct to more successful chemotherapeutic effects. For example, some chronic and disabling pathologies, which exert a marked negative impact on human welfare (such as diabetes, Parkinson and peptic ulcer diseases), are treated by the oral administration of active pharmaceutical ingredients (APIs)2. As detailed below, the bioavailability of APIs used in the treatment of these disorders experience fluctuations that may endanger the health of patients. To highlight the relevance of this health problem, Table 2 records the most relevant epidemiological parameters for these three disorders for the inhabitants of Spain and Western Europe.

Foot Note

2Any substance or mixture of substances intended to be used in the manufacture of a drug product and that, when used in the production of a drug, becomes an active ingredient in the drug product. Such substances are intended to furnish pharmacological activity or other direct effect in the diagnosis, cure, mitigation, treatment or prevention of disease or to affect the structure and function of the body

3The sum of years lost due to premature death (YLLs) and years lived with disability (YLDs). DALYs are also defined as years of healthy life lost.

4The total number of cases of a given disease in a specified population at a designated time. It is differentiated from INCIDENCE, which refers to the number of new cases in the population at a given time.

5The number of new cases of a given disease during a given period in a specified population. It also is used for the rate at which new events occur in a defined population. It is differentiated from prevalence, which refers to all cases, new or old, in the population at a given time.

Oral route is the most convenient and widely used method of drug administration, representing about 90% of all therapies used [2]. It displays great advantages, such as being non-invasive, easy to administer (with the consequent high patient compliance) and cost-effective; they are also easy to store and transport, and the formulations can be modified flexibly. However, serious drawbacks to conventional DDS are imposed by the gastrointestinal tract (GIT). Large fluctuations in drugs’ bioavailability are found due to the influence of physiological factors such as variations in pH, high enzymatic activity as well as gastric emptying. In addition, rapid gastrointestinal transit can prevent not only the complete drug release from the dosage form, but also the full drug intake in the absorption zone (most drugs are absorbed in stomach or the upper part of small intestine) with the consequent loss of dose effectiveness. This is the reason why frequent drug administrations are required to maintain the therapeutic plasma level of the drug.

Gastroretentive Drug Delivery Systems (GRDDS)

Gastroretentive Drug Delivery Systems (GRDDS) have emerged as an ideal approach to overcome the mentioned-above drawbacks. Their main goal is to prolong the gastric residence time (GRT) of the dosage forms in the stomach up to several hours, so that the time between dose administration is lengthened and the drug release proceeds at the desired rate depending on their therapeutic use [3].

Consequently, GRDDS can play a key role in a. Prolonging the liberation in stomach of drugs with local activity in the stomach or the upper part of the intestine (Amoxicillin, for eradication of Helicobacter pylori in peptic ulcer diseases, Table 3) [4].

b. Slowing down the release of drugs soluble at acidic pH (Ranitidine, H2-receptor antagonists);

c. And prolonging the release of drugs with narrow absorption window, i.e., with low absorption in the lower part of the GIT (Levodopa and Carbidopa, drugs used in the treatment of Parkinson disease), and drugs with low bioavailability such as the antidiabetic Metformin.

Main advantages of current GRDDS

a. The benefit of low density/floating systems is rooted on the buoyancy of the dosage in the gastrointestinal fluids. Its bulk density must be lower than that found in gastric fluids (1.004 to 1.010 g/mL). The bulk density is the density value reached after a lag time that depends on the swelling rate of the polymer used in the formulation. This property can be improved by the incorporation of wicking agent or swelling enhancers [5- 9]. Moreover, the use of effervescent combinations, joint to the swelling characteristic, can improve the overall floating behavior of the dosage form [10].

b. Bio(muco)adhesive devices have also been formulated as GRDDS. The dosage forms are designed to be attached to the stomach wall and survive gastrointestinal motility for a longer period. The use of mucoadhesive polymers is necessary [11].

c. Swelling and expandable systems (or “plug type systems” due to their pyloric sphincter blocking attribute) have achieved significant success both in vitro and in vivo in order to retain the dosage form in the stomach [11]. Once the polymer meets the gastric fluid, it absorbs water and swells [12]. The selection of a polymer with the appropriate molecular weight and swelling properties is crucial to enable the dosage form to exhibit sustained-release behavior.

Inconveniences to overcome for the optimal final performance of the pharmaceutical formulations

a. Low density/floating systems require high levels of fluid in the stomach to float and work effectively. They also may stick to each other and provoke obstruction in the GIT, causing gastric irritation. Additionally, formulations consist of a blend of drug and low-density polymers; therefore, the release kinetics of the drug cannot be changed without changing the floating properties of the dosage form and vice versa.

b. Bioadhesive formulations adhere to the stomach mucosa, which is covered by mucus to protect it. The constant turnover of this protection mucus layer, joint to the high stomach hydration, might decrease the bioadhesion of the polymers.

c. Swelling and expandable systems are difficult in maintaining the structural integrity; they may cause bowel obstruction, intestinal adhesion, and gastropathy if they are not constituted by an easily hydrolysable, biodegradable polymers. Although the development of simple-working GRDDS has partially helped to overcome the drawbacks associated with conventional dosage form, further work is needed on its shortcomings. We propose herein the development of two types of dual-working polymeric materials, suitable for use in GRDDS, which will substantially lengthen the GRT.

New Polymeric Systems towards the Development of GRDDS with Substantial Gains Compared to Known Systems

The preparation of new polymeric materials with optimal properties for the development of efficient dual-working gastroretentive drug delivery systems (GRDDS) is a breakthrough approach. It can improve the bioavailability of selected oral drugs within an authentic biological matrix, which may benefit the 43.4 million people that suffer from diabetes, Parkinson disease and peptic ulcer today in Western Europe (Table 3). This innovative technology will provide reliable dosing of the drugs to the target location and ultimately, the in vitro detection, ensuring proper drug management, enabling personalized healthcare. To achieve it, two routes have been identified to provide disruptive enabling technologies which allows the formation of dual-working GRDDS able to overcome common drawbacks associated to previous systems: (a) The combination of swelling expanding properties with buoyance features is a low-explored concept for improved gastro-retention attributes; (b) the combination of muco-adhesion and floating mechanism.

Therefore, it could be of interest the development of:

I. Floating expandable materials (System A), able to behave not only as swelling-expandable GRDDS with improved mechanical properties, but also as floating devices.

II. Reversible bioadhesive hydrogels (RBH)/low-density microspheres composites (System B). These devices present the advantages of bioadhesive systems in combination with lowdensity/ floating approaches (Figure 2).

The substantial gains of the target materials over conventional systems are summarized as follows:

Floating expandable materials, over conventional porous systems

i. A substantial improvement in the final mechanical strength of the system, keeping its efficacy over time.

ii. The porous structure will not depend on pH and keep swell over time.

iii. Their floating properties will length their GRT.

iv. The highly porous structure will allow the inclusion of large quantities of drugs, if required.

Reversible bioadhesive hydrogels / low-density microspheres composites over conventional floating systems and bioadhesive GRDDS

i. Thiomers-based hydrogels will enhance the bioadhesive properties of the global composite.

ii. As the gel breaks down and separates from the mucosa, floating microspheres will be delivered, increasing the GRT of the loaded drug.

iii. It is known that small-sized floating dosage forms are less likely to be evacuated from the stomach by the migrating myoelectric complex (MMC),f thus prolonging the GRT.

iv. Due to their size, risk reduction of obstruction in the GIT will be achieved.

v. As the floating microspheres carry the drug into it, drug release kinetics can be modified by just adjusting the number of microspheres in the final formulation, without affecting to their floating properties.

Preparation of expandable superporous hydrogels (SPHs) with floating properties (System A)

Interpenetrating polymeric networks (IPNs) are unique “alloys” of cross-linked polymers in which at least one network is synthesized and/or cross-linked in the presence of the other [13]. Depending on the chosen polymer, they enable the formation of SPHs (Figure 3), which can absorb large amounts of water or aqueous fluids (10–1000 times of their original weight or volume) in short periods of time. The formation of (semi) IPN based on hydrophilic natural occurring polymers (sodium alginate, hyaluronic acid and chitosan), or synthetic water-soluble polymers (PVA, and Carbopol®) could be ani interesting choice. The second polymer will grow into the colloidal medium by means of an orthogonal polymerization/complexation method. The interconnected porous patterns of the new SPHs can encapsulate large doses of hydrophilic drugs, such as Metformin and Ranitidine (Table 3), making them ideal as GRDDS [14]. It is relevant to highlight that these systems must rapidly swell and expand, as well as maintain their integrity in the harsh stomach environment while releasing the pharmaceutical active ingredient [15]. Therefore, the physical entanglement of the polymer chains is a key factor and could help improve the mechanical strength and resiliency of the material. Moreover, floating properties (Table 4 & Figure4) will be imparted by the free volume generated into the hydrophilic matrices, with the help of comb- like materials [16]. Porosity, swelling properties, floatability and drug loading and release behaviors can be controlled by the appropriate choice of network forming polymers and their rate.

Development of Reversible Bioadhesive Hydrogels/ Low-Density (Floating) Nano/Microspheres Composites (System B)

For the development of reversible bioadhesive hydrogels/lowdensity microspheres composites, properties, materials needed, and polymerization procedures are summarized in Figure 4.

Preparation of floating micro (nano)spheres as lipophilic drug carriers

Being poly(meth)acrylates biocompatible materials with extensive use in humans,[18,19] the preparation of amphiphilic materials based on (meth)acrylate and (meth)acrylamide derivatives, capable of self-assemble in core-shell structures could be of great interest. To achieve it, extensively tested living polymerization techniques have been already used such as Atom Transfer Radical Polymerizations (ATRP), [20] Oxyanionic Polymerizations [21] and Reversible Addition-Fragmentation Chain Transfer Polymerizations (RAFT) [22,23]. They have demonstrated to be excellent tools for the preparation of amphiphilic block-copolymers. Macromonomers based on PEG, poly(monoglycerol methacrylate) (PGMA), POEGMA, PPO and PDMS will also be used in the polymerization process. They will provide flexibility and low density/floating properties to the final assembled particles (Table 4 & Figure 4).

Thiomers. Preparation from natural occurring polysaccharides

Thiolated polymers or “thiomers”, which display thiol bearing side chains, have proved to behave very effectively as mucoadhesive. Their bioadhesive mechanism is based on thiol/ disulfide exchange reactions. Thiomers can form disulphide linkages between them and cysteine-rich subdomains of mucus glycoproteins in the mucus gel layer. This also occurred between the disulphide linkages from polymer backbone and thiol groups in the mentioned glycoproteins [24]. In order to improve the mucoadhesive properties of the materials to use (Table 4), thiolation can be a straightforward method [25]. Although thiolation of natural occurring polymers has already been conducted, [25]. low degree of functionalization were achieved in most cases [26] probably because the sulfhydryl groups are prone to oxidation. The thiolation of natural (chitosan and sodium alginate) and commercial polymers [Carbopol® and poly(vinyl alcohol) PVA] can be conducted by amide-coupling chemistry and the use of thiol-protected molecules such pyridyl disulfide reactants [27]. Based on our experience [28,29] the formation of disulphide containing monomers for polymer total synthesis, can also be addressed.

Flexible chains: Preparation of bioadhesive comb-like polymers

Entanglement seems to be one of the preferred modes of mucin molecular association. Chain flexibility is critical for interpenetration and entanglement with the mucus gel (Table 4 & Figure 4) [30]. It has been demonstrated that the incorporation of flexible polymer chains into a hydrogel can promote its mucoadhesion by movement of the polymer chains from hydrogel to mucosa [31]. Hence, the use of flexible comb-type polymers based on PEG, PEGMA, PPO and PDMS will be the first choice. They provide an extra bonus on free volume in hydrogels since physiological temperature is well-above their glass transition temperatures (Tg).

Conclusion

The benefit of prolonging the release of therapeutic molecules in the stomach whilst reducing the side effects associated with them is evident. The current prescribed, non personalized, traditional oral dosage approach generally involves relatively high doses of the drug in the hope that a portion, although minor, will go to the target tissues. Not only does this overdose lead to a nonsignificant efficiency in combating patients’ disease, it also leads to major side effects. Embeddeding the drugs into dual-working GRDDS that posses a double retartant systems for drug delivery, will conduct to a significant improvement in the sustainable drug release over longer time periods. Accurately time delivery of the selected drugs is the only method to reduce drug dosages, mitigate side effects on the other healthy tissues and increased rapidity of the action. In addition, by the designed methods it is possible to maintain the therapeutic drug releases while time intervals between doses is shortened, with the consequent reduction in patient’s discomfort. Development of these systems is a key deliverable of the current mini-review.

For more Open Access Journals in Juniper Publishers please click on: https://juniperpublishers.com/

For more articles in Academic Journal of Polymer Science please click on: https://juniperpublishers.com/ajop/index.php

0 notes

Text

Gastroesophageal Reflux Disease (GERD) therapeutics market is estimated to be USD 4.34 billion by 2025

Industry Insights

The global Gastroesophageal Reflux Disease (GERD) therapeutics market size was valued at USD 5.66 billion in 2016 and by is estimated to be USD 4.34 billion by 2025, it is anticipated to observe a decrease in its revenue at a negative CAGR of -2.9%. Expiration of patented blockbuster drugs, which are indicated for the management of disorders of acid reflux is major restraining factors for this market.

With strong clinical pipelines and patent litigations, the market continues to experience significant changes. Proton pump inhibitors (PPI) and antagonists of histamine H2 receptor have the importance in current scenario of the market.

Upon loss of patent protection of formerly leading branded drugs, generic molecules with low-price can ingest the sales of the branded ones up to 90%. Rising number of companies being exposed to price scrutiny associated with shift in the focus of government on the promotion of consumer convenience will stimulate further reduction of drug prices. Although market turnover is affected by the expiration of major patents and the demand of drugs used to reduce acid, due to the increasing prevalence of heartburn, is anticipated to increase in the upcoming years.

The devices of GERD serves as a substitute for management of heartburn, because of low rate of success and failure in clinical trials. Hence, very limited acceptance of devices of GERD management contribute for the rising demand of drugs having acid neutralizing property, as the major therapy approach.

Nevertheless, the advent of devices which are minimally invasive to address anatomical defects are gaining popularity coupled with supportive evidence from clinical data for performing various procedures including trans oral fundoplication, which helps in preventing reflux of non-acid and acid contents. The adoption of these devices have been further reinforced in the U.S. in 2016 with the advent of a CPT code (43210) which helps in facilitating reimbursement process.

Drug Type Insights

In 2016, market was dominated by the antacids segment and is anticipated to keep its top position over the forecast period. Most preferred first-line therapy for infrequent and mild symptoms is antacids, as the therapy neutralize the secretion of gastric acid immediately. Convenient OTC (over-the-counter) accessibility various forms such as syrups, powders and tablets is accountable for the extreme adoption. Moreover, the AHFS (American Hospital Formulary services), amongst other countries, enlisted over 120 preparations too advocate.

In 2016, the second largest segment was found to be PPIs as it is the most common medication prescription type for the diseases such as heartburn. Generics inflow leading to the loss of exclusiveness of popular drugs, including Prilosec and Nexium, is estimated to negatively affect the sales of branded versions. A further decrease is appearing more with the expected expiration of other patented drugs, such as Dexilant.

Regional Insights

In 2016, the largest region was found to be North America in terms of share for GERD market. Every year, GERD symptoms are experienced by more than 80 million people in the U.S., of which, approximately 25 million patients suffer from acid reflux and heartburn daily and approximately 60 million patients monthly.

Moreover, outpatient clinic visits for GERD disorder in the U.S. has been increased in the past few years because of the more prone geriatric population to develop acid reflux and heartburn. On the contrary, the Asia Pacific is estimated to witness the fastest growth rate. The increasing geriatric population and dietary and lifestyle risk factors such as diet with high fat and obesity, is anticipated to drive the growth. In developing countries, the inclination towards self-medication is quickly increasing because of the affordability and availability of OTC antacids as in China and India.

Competitive Insights

Competitive market, which is generics-driven is creating a pressure on the prices of drug with decreased retail sales, which will stimulate stationary growth in future. Companies producing them range from high to medium on the basis of competitive rivalry. Eisai Co., Ltd.; AstraZeneca PLC; GlaxoSmithKline PLC; Johnson & Johnson and Takeda Pharmaceutical Co., Ltd.; are some of the top key players. In addition, Daewoong Pharmaceutical Co., Ltd.; SRS Pharmaceuticals Pvt. Ltd.; SFJ Pharmaceuticals Group and Ironwood Pharmaceuticals, Inc. are some emerging companies.

Among others, RaQualia Pharma, Inc. and Ironwood Pharmaceuticals, Inc. are focusing more on development of new generic molecules, which involves novel and existing drug mechanisms as a part of the strategy to enter into the competition. Many generic players are also trying to focus on these spaces in an attempt to capture a larger share by the new version to replace the patent expired drugs.

Read full research report:

https://www.millioninsights.com/industry-reports/gastroesophageal-reflux-disease-gerd-therapeutics-market

Download free request sample:

https://www.millioninsights.com/industry-reports/gastroesophageal-reflux-disease-gerd-therapeutics-market/request-sample

#Gastroesophageal Reflux Disease (GERD) Therapeutics#GERD#Healthcare#Antacids#H2 Receptor Blockers#Proton Pump Inhibitors

0 notes

Text

Gastroesophageal Reflux Disease (GERD) Therapeutics Market Share, Top Key Players, Price, Revenue and Growth Rate Forecast 2025

The global Gastroesophageal Reflux Disease (GERD) therapeutics market size was valued at USD 5.66 billion in 2016 and by is estimated to be USD 4.34 billion by 2025, it is anticipated to observe a decrease in its revenue at a negative CAGR of -2.9%. Expiration of patented blockbuster drugs, which are indicated for the management of disorders of acid reflux is major restraining factors for this market.

With strong clinical pipelines and patent litigations, the market continues to experience significant changes. Proton pump inhibitors (PPI) and antagonists of histamine H2 receptor have the importance in current scenario of the market.

Request a Sample PDF Copy of This Report @ https://www.millioninsights.com/industry-reports/gastroesophageal-reflux-disease-gerd-therapeutics-market/request-sample

Market Synopsis of Gastroesophageal Reflux Disease (GERD) Therapeutics Market:

Upon loss of patent protection of formerly leading branded drugs, generic molecules with low-price can ingest the sales of the branded ones up to 90%. Rising number of companies being exposed to price scrutiny associated with shift in the focus of government on the promotion of consumer convenience will stimulate further reduction of drug prices. Although market turnover is affected by the expiration of major patents and the demand of drugs used to reduce acid, due to the increasing prevalence of heartburn, is anticipated to increase in the upcoming years.

The devices of GERD serves as a substitute for management of heartburn, because of low rate of success and failure in clinical trials. Hence, very limited acceptance of devices of GERD management contribute for the rising demand of drugs having acid neutralizing property, as the major therapy approach.

Nevertheless, the advent of devices which are minimally invasive to address anatomical defects are gaining popularity coupled with supportive evidence from clinical data for performing various procedures including trans oral fundoplication, which helps in preventing reflux of non-acid and acid contents. The adoption of these devices have been further reinforced in the U.S. in 2016 with the advent of a CPT code (43210) which helps in facilitating reimbursement process.

Drug Type Insights

In 2016, market was dominated by the antacids segment and is anticipated to keep its top position over the forecast period. Most preferred first-line therapy for infrequent and mild symptoms is antacids, as the therapy neutralize the secretion of gastric acid immediately. Convenient OTC (over-the-counter) accessibility various forms such as syrups, powders and tablets is accountable for the extreme adoption. Moreover, the AHFS (American Hospital Formulary services), amongst other countries, enlisted over 120 preparations too advocate.

In 2016, the second largest segment was found to be PPIs as it is the most common medication prescription type for the diseases such as heartburn. Generics inflow leading to the loss of exclusiveness of popular drugs, including Prilosec and Nexium, is estimated to negatively affect the sales of branded versions. A further decrease is appearing more with the expected expiration of other patented drugs, such as Dexilant.

View Full Table of Contents of This Report @ https://www.millioninsights.com/industry-reports/gastroesophageal-reflux-disease-gerd-therapeutics-market

Get in touch

At Million Insights, we work with the aim to reach the highest levels of customer satisfaction. Our representatives strive to understand diverse client requirements and cater to the same with the most innovative and functional solutions.

0 notes

Text

Gastroesophageal Reflux Disease Therapeutics Market 2025: Report Focusing on Opportunities, Revenue & Market Driving Factors

4th January 2021 – The global Gastroesophageal Reflux Disease (GERD)therapeutics market size was valued at USD 5.66 billion in 2016 and by is estimated to be USD 4.34 billion by 2025, it is anticipated to observe a decrease in its revenue at a negative CAGR of -2.9%. Expiration of patented blockbuster drugs, which are indicated for the management of disorders of acid reflux is major restraining factors for this market. With strong clinical pipelines and patent litigations, the market continues to experience significant changes. Proton pump inhibitors (PPI) and antagonists of histamine H2 receptor have the importance in current scenario of the market.

Upon loss of patent protection of formerly leading branded drugs, generic molecules with low-price can ingest the sales of the branded ones up to 90%. Rising number of companies being exposed to price scrutiny associated with shift in the focus of government on the promotion of consumer convenience will stimulate further reduction of drug prices. Although market turnover is affected by the expiration of major patents and the demand of drugs used to reduce acid, due to the increasing prevalence of heartburn, is anticipated to increase in the upcoming years.

The devices of GERD serve as a substitute for management of heartburn, because of low rate of success and failure in clinical trials. Hence, very limited acceptance of devices of GERD management contributes for the rising demand of drugs having acid neutralizing property, as the major therapy approach. Nevertheless, the advent of devices which are minimally invasive to address anatomical defects are gaining popularity coupled with supportive evidence from clinical data for performing various procedures including trans oral fundoplication, which helps in preventing reflux of non-acid and acid contents. The adoption of these devices has been further reinforced in the U.S. in 2016 with the advent of a CPT code (43210) which helps in facilitating reimbursement process.

Access Gastroesophageal Reflux Disease (GERD) Therapeutics Market Report with TOC @ https://www.millioninsights.com/industry-reports/gastroesophageal-reflux-disease-gerd-therapeutics-market

In 2016, market was dominated by the antacids segment and is anticipated to keep its top position over the forecast period. Most preferred first-line therapy for infrequent and mild symptoms is antacids, as the therapy neutralizes the secretion of gastric acid immediately. Convenient OTC (over-the-counter) accessibility various forms such as syrups, powders and tablets is accountable for the extreme adoption. Moreover, the AHFS (American Hospital Formulary services), amongst other countries, enlisted over 120 preparations too advocate. In 2016, the second largest segment was found to be PPIs as it is the most common medication prescription type for the diseases such as heartburn. Generics inflow leading to the loss of exclusiveness of popular drugs, including Prilosec and Nexium, is estimated to negatively affect the sales of branded versions. A further decrease is appearing more with the expected expiration of other patented drugs, such as Dexilant.

In 2016, the largest region was found to be North America in terms of share for GERD market. Every year, GERD symptoms are experienced by more than 80 million people in the U.S., of which, approximately 25 million patients suffer from acid reflux and heartburn daily and approximately 60 million patients monthly. Moreover, outpatient clinic visits for GERD disorder in the U.S. has been increased in the past few years because of the more prone geriatric population to develop acid reflux and heartburn. On the contrary, the Asia Pacific is estimated to witness the fastest growth rate. The increasing geriatric population and dietary and lifestyle risk factors such as diet with high fat and obesity, is anticipated to drive the growth. In developing countries, the inclination towards self-medication is quickly increasing because of the affordability and availability of OTC antacids as in China and India.

Competitive market, which is generics-driven is creating a pressure on the prices of drug with decreased retail sales, which will stimulate stationary growth in future. Companies producing them range from high to medium on the basis of competitive rivalry. Eisai Co., Ltd.; AstraZeneca PLC; GlaxoSmithKline PLC; Johnson & Johnson and Takeda Pharmaceutical Co., Ltd.; are some of the top key players. In addition, Daewoong Pharmaceutical Co., Ltd.; SRS Pharmaceuticals Pvt. Ltd.; SFJ Pharmaceuticals Group and Ironwood Pharmaceuticals, Inc. are some emerging companies. Among others, RaQualia Pharma, Inc. and Ironwood Pharmaceuticals, Inc. are focusing more on development of new generic molecules, which involves novel and existing drug mechanisms as a part of the strategy to enter into the competition. Many generic players are also trying to focus on these spaces in an attempt to capture a larger share by the new version to replace the patent expired drugs.

Request a Sample Copy of Gastroesophageal Reflux Disease (GERD) Therapeutics Market Report @ https://www.millioninsights.com/industry-reports/gastroesophageal-reflux-disease-gerd-therapeutics-market/request-sample

0 notes

Text

Upper GI series Market Analysis, Share, Size, Trends And Industry Growth

An upper gastrointestinal (UGI) series is radiographic examination of the GI tract for any abnormalities. It is also known as constant radiography. The global upper GI series market by Market Research Future takes a look at the various diseases affecting the GI tract, developments in X-rays, and new projections for the period of 2017 to 2023 (forecast period). The impact of the COVID-19 pandemic and analysis of its effects as well as the opportunities for the technology are also discussed in the report.

Upper GI series market Scope

The global upper GI series market is expected to grow at a CAGR of 4.5% during the forecast period. Huge prevalence of GI disorders is one of the primary drivers of the market. The large healthcare expenditure allocated to detection of GI distress can fuel the market. GI disorders had accounted for close to USD 110 billion in 2005 in the U.S. alone. The interest of the pharmaceutical industry as well as large patient pool can be lucrative for the market in the long run.

Developments in cost-effective treatments, government research for GI disorders, and the large geriatric populace are other drivers of the market. Effective treatments such as acid suppressants, histamine H2 receptor antagonists, and proton pump inhibitors are expected to drive the market to great heights.

But high costs of treatment can impair market growth.

Upper GI series market Segmentation

The global upper GI series market is segmented by test type, imaging material, application, and end users.

On the basis of test type, it is divided into standard barium upper GI series and double-contrast upper GI series.

On the basis of imaging material, the market is segmented into barium swallow, barium follow-through, and barium meal. The barium swallow segment is likely to fetch huge returns for the global upper GI series market owing to its ability to detect abnormalities in esophagus, stomach, and intestines.

On the basis of application, the market is segmented into ulcers, esophageal reflux, esophageal varices, hiatal hernias, and others.

On the basis of end users, it is segmented into hospitals, clinics & laboratories, and others.

Upper GI series market Regional Analysis

Geographically, the global upper GI series market looks at the regions of the Americas, Asia Pacific (APAC), Europe, and the Middle East & Africa (MEA).

The Americas accounted for the largest market share for upper GI series. Factors driving market growth are the large patient population, well-developed healthcare, and increasing geriatric population. Reimbursement policies as well as adoption of advanced diagnostic methods can create plenty of opportunities for the upper GI series market. Approval of the use of disposable devices has paved the way for new strides for the industry in the region. Recently, Boston Scientific gained approval for the use of disposable duodenoscopes for diagnosis of bile duct disorders in the U.S.

Europe is the second largest market, followed by Asia Pacific. The region is expected to be lucrative due to revised codes to be outlined for upper GI series by reputed healthcare associations. A well-developed healthcare network and trained personnel in radiography can facilitate the growth of the upper GI series market.

APAC is the fastest growing market for upper GI series due to presence of many developing countries and cost effective treatments. Change in eating habits and alarming cases of hepatitis C can spur the need for constant radiography. Lastly, the MEA region has the least market share.

Upper GI series market Competition

GastroIntestinal Specialists LLC., Alfa Wassermann SPA, Cadila Pharmaceuticals Limited, Purdue Pharma L.P., Novadaq Technologies Inc., AstraZeneca, Eisai Co., Ltd, and Ironwood Pharmaceuticals Inc. are key players of the global upper GI series market.

Obtain Premium Research Report Details, Considering the impact of COVID-19 @ https://www.marketresearchfuture.com/reports/upper-gi-series-market-826

#Upper GI series market#Upper GI series market Size#Upper GI series market Share#Upper GI series market Growth#Upper GI series market Analysis

0 notes

Text

By 2026, Ranitidine Market To Surpass US$ 485.4 Million - Coherent Market Insights

Ranitidine Market To to exhibit a CAGR of 1.8% over the forecast period (2018 - 2026).

Request for Sample PDF Copy:

https://www.coherentmarketinsights.com/insight/request-pdf/2131

Description:

Healthcare professionals have been keenly interested in the treatment of gastroesophageal reflux disease (GERD) and stomach & intestinal ulcer owing to its increasing prevalence. GERD is common health problem, which leads to serious medical complications and further huge medical expense in its diagnosis and treatment. The two most frequently observed symptoms associated with GERD are heartburn and acid regurgitation. Usually, over-the-counter antacids, proton pump inhibitor, and H-2 receptor blockers are used to decrease the effects of stomach acids or to block acid production.

Ranitidine is a histamine H2 antagonists and available as both over-the-counter (OTC) and prescription drug, indicated in the treatment of gastroesophageal reflux disease (GERD). Ranitidine decreases the acid production from stomach for up to 12 hours. Also, ranitidine is commonly used in erosive esophagitis, peptide ulcer disease, and Zollinger–Ellison syndrome. It could be taken orally or intravenously.

The global ranitidine market size was valued at US$ 412.4 Mn in 2017, and is expected to witness a CAGR of 1.8% over the forecast period (2018 – 2026).

Global Ranitidine Market Share (%), By Application: 2018 & 2026

Ranitidine | Coherent Market Insights

Source: Coherent Market Insights Analysis (2018)

Growing Research and Development (R&D) on Ranitidine is expected to Boost Market Growth

Various government and private research organizations are increasingly engaged in research and development studies to increase the efficacy of ranitidine and examine possible potential of ranitidine to increase future scope of ranitidine market.

Furthermore, various clinical trials are currently undergoing to identify and compare efficacy between ranitidine and other proton pump inhibitors such as esomeprazole and rabeprazole to measure gastric acid reduction in stomach. With the result of these studies, the efficacy of ranitidine is expected to improve and offer better treatment regimes in reducing excessive gastric acid production in the near future.

For instance, in November 2015, a study to compare the efficacy of rabeprazole extended release (ER) 50 mg versus ranitidine 150 mg in treating erosive gastroesophageal reflux disease (eGERD) is currently in Phase III clinical stage.

Global Ranitidine Market Share (%), By Form: 2018 & 2026

Ranitidine | Coherent Market Insights

Source: Coherent Market Insights Analysis (2018)

Rising Cases of Various Gastric Ulcers and Digestive Diseases is expected to Increase Growth of the market

High prevalence of gastroesophageal reflux disease (GERD), intestinal & stomach ulcers, esophagitis, heartburn, and other digestive diseases due to unhealthy lifestyle, changing dietary patterns will lead to increase in demand for ranitidine-based medications in the near future. According to Florida Hospital, 2018 U.S. data statistics, in the U.S. over 60 million adults suffer from acid reflux symptoms every month. Furthermore, the source states that each day an estimated 25 million of the 60 million adults suffers from acid reflux symptoms. Also, according to the same source, about 20% of people with acid reflux will develop gastroesophageal reflux disease (GERD) in the near future.

Heartburn with or without regurgitation is identified as one of the prime symptoms of gastroesophageal reflux disease (GERD). According to World Gastroenterology Organization (WGO), 2015, prevalence of GERD is rapidly increasing worldwide, with differences reported in prevalence ranging from 2.5% to 6.6% in Eastern Asia while slightly higher up to 13.8% to 25.8% in North America.

The reason for high prevalence of GERD is not entirely clear, however, it appears to be correlated with increasing prevalence of obesity, and several dietary factors. In obese patients, excess belly fat exert more pressure on the stomach, which causes backflow of acid causing heartburn. Increasing number of obese patients across the globe will indirectly increase GERD cases and this is expected to fuel growth of ranitidine market. According to World Health Organization (WHO), in 2016, over 1.9 billion adults aged 18 years and above were overweight, of which over 650 million were obese, worldwide. Furthermore, GERD is associated with possible risk of Barrett’s esophagus: a premalignant condition that damages the esophagus tube.

However, stringent regulatory guidelines of FDA in the manufacturing of finished drugs will limit growth of ranitidine market. For instance, in March 2018, the Ministry of Food and Drug Safety, South Korea banned the imports of 150 mg Zantac (ranitidine) supplied by GlaxoSmithKline (GSK) Korea, for 4 months (March to June 2018) due to its different shape and coatings. According to the same source, South Korea’s Ministry of Food and Drug Safety report, GSK violated Pharmaceutical Affairs Act by changing the approved shape of Zantac. Zantac is supposed to be white and round with thin film-coatings on both side, while GSK distributed Zantac with thick coated film and also coating around some of the tablets were slightly broken. Changes in color, taste, and packaging might hurt the safety and efficacy of drugs, which directly affects the quality of product.

Furthermore, one of the major challenges in determining prevalence of GERD is to identify the patients’ suffering with the condition. Patients suffering with GERD-related symptoms do not consult healthcare professionals until the symptom gets severe. . Direct costs associated with GERD disease include costs of over-the-counter and prescription medications, physician office and hospital visits, surgical costs, and costs of treating other possible complications such as Barrett's esophagus and esophageal adenocarcinoma, which may result from the disease. This is expected to limit the growth of ranitidine market, over the forecasted period.

Key players operating in the global ranitidine market include GlaxoSmithKline plc, Boehringer Ingelheim GmbH, Strides Pharma Science Limited (StridesShasun), Tocris Bioscience (R & D Systems), Merck KGaA, and Sun Pharmaceutical Industries Limited among others.

About Us: Coherent Market Insights is a global market intelligence and consulting organization focused on assisting our plethora of clients achieve transformational growth by helping them make critical business decisions. We are headquartered in India, having office at global financial capital in the U.S. Our client base includes players from across all business verticals in over 150 countries worldwide. We do offer wide range of services such as Industry analysis, Consulting services, Market Intelligence, Customized research services and much more. We have expertise in many fields such as healthcare, chemicals and materials, Automation, semiconductors, electronics, energy, food and beverage, packaging and many more. Visit our website to know more.

Buy Report Here:

https://www.coherentmarketinsights.com/insight/buy-now/2131

Contact Us: Mr. Shah Coherent Market Insights 1001 4th Ave. #3200 Seattle, WA 98154 Tel: +1-206-701-6702 Email: [email protected]

0 notes

Text

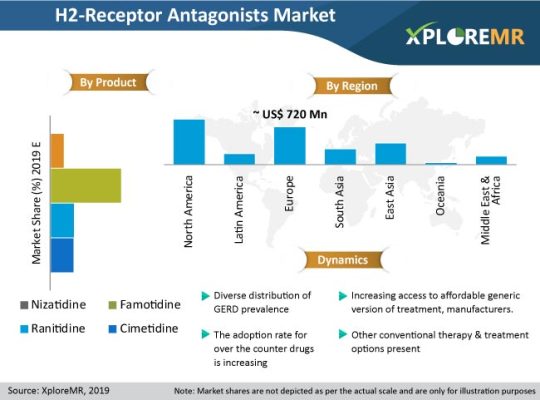

Global H2 Receptor Antagonist Market research to Hold a High Potential for Growth by 2019-2029

The ~US$ 2.6 billion market for H2 receptor antagonist has been envisaged to witness lethargic growth prospects over the years to come., according to a recent research study of XploreMR. The research report for H2-receptor antagonists market elaborates the dynamics that are related to the growth and fragmented nature of the market. The market is expected to expand at a considerable rate, which can be majorly attributed to the growing incidence of gastroesophageal reflux disease (GERD) as well as the increasing adoption rate of H2-receptor antagonists.

Research shows that the growing adoption of proton-pump inhibitors is a major factor due to which the H2-receptor antagonists market is likely to witness sluggish growth over the forecast period. In terms of influencing factors, presence of generic OTC H2-receptor antagonists and prevalence of GERD and peptic ulcer population are the clear. A present, the disease trend observed around the world indicates that eastern countries are more prone to regurgitation-dominant GERD and western countries observe heartburn-dominant GERD.

Get Sample Copy of this Report @ https://www.xploremr.com/connectus/sample/3989

The H2-receptor antagonists market has not been experiencing considerable growth over the past few years owing to the availability of generic medications, growth in the number of local players, as well as the adverse effects associated with the consumption of H2-receptor antagonists. There are severe health risks associated with the consumption of H2-receptor antagonists, which include headaches, fatigue, abdominal pain, diarrhea, and drowsiness. The use of H2-receptor antagonists for patients with renal difficulties, hepatic impairment, or patients who are aged 50 years, can lead to adverse effects to the central nervous system. Drug interactions with the use of H2-receptor antagonists may go wrong at times, and a therapeutic increase in gastric pH is likely to disrupt the mechanism of drugs that require an acidic environment for dissolution.

Evolving Adoption Patterns, Driven by Strong Alternative Competitors

Consumer preference has changed for H2-receptor antagonists, which limits the market growth for H2-receptor antagonists. The market is already experiencing tough competition from other valuable alternatives, and present effects associated with the consumption of these drugs makes it even worse for manufacturers to label their products. Advisory labels for H2-receptor antagonists is mandatory, however, the present physical differences among consumers can lead to difficulties that they are not aware of.

The demand-side trends, which show increasing access to affordable generic versions of treatment, are indicating low spending for treatment, which is offsetting the increasing spending on branded drugs. The adoption of H2-receptor antagonists has changed over the years with the introduction of Zantac, which is considered to be the first billion-dollar drug to face growing competition from proton-pump inhibitors. There are other occasionally used alternative drug types available for cases, which include potassium-competitive acid blockers, antacids, and cytoprotective agents.

Request for Check Discount @ https://www.xploremr.com/connectus/check-discount/3989

Although the H2-receptor antagonists market is mature and highly competitive, most segments of the H2-receptor antagonists market are either saturated or nearing saturation. Extensive pricing competition among generic manufacturers facilitate a continuous demand growth, which is in relation to the adoption of H2-receptor antagonists. Most of the major players in the pharmaceutical industry are manufacturing proton-pump inhibitors.

The adoption and clinical benefits associated with proton-pump inhibitors are larger in number, hence, a smaller number of manufacturers are present in the H2-receptor antagonists market. Clinically better products with affordable pricing can still act as significant influencers for this H2-receptor antagonists market. In the face of global volatility, manufacturers gain profits due to the reliability, productivity, and awareness offered by loyal consumers.

Targeting countries for marketing H2-receptor antagonists is most important as the emergence and presence of generic manufacturers has led to a more competitive market structure. Moreover, entering a H2-receptor antagonists market with many local players providing drugs at a considerably low cost is a challenge for most of the global manufacturers.

Request Methodology of this Report @ https://www.xploremr.com/connectus/request-methodology/3989

At present, the global H2-receptor antagonists market is highly fragmented, with the presence of few global manufacturers and a large number of regional manufacturers. Some of the key H2-receptor antagonist manufacturers include Alembic Pharmaceuticals Ltd, Cipla Ltd., Torrent Pharmaceuticals Ltd., Sanofi S.A., Abbott, Glenmark Pharmaceuticals Ltd., Teva Pharmaceutical Industries Ltd., Cadila Healthcare Ltd, and GlaxoSmithKline Plc.

About us: XploreMR is one of the world’s leading resellers of high-quality market research reports. We feature in-depth reports from some of the world’s most reputed market research companies and international organizations. We serve across a broad spectrum – from Fortune 500 to small and medium businesses. Our clients trust us for our unwavering focus onquality and affordability. We believe high price should not be a bottleneck for organizations looking to gain access to quality information. Our team comprises an eclectic mix of experienced market research specialists, search engine specialists, web designers, online marketers, and business writers. The team is highly committed to going above and beyond, and serving the research needs of our clientele. Contact us:

111 North Market Street, Suite 300, San Jose, CA 95113, United States Tel: +1-669-284-0108 E-mail: [email protected] Website: www.xploremr.com

0 notes

Text

Scleroderma Diagnostics and Therapeutics Market Analysis and Forecast 2018-2023