#Global Cooking Oils & Fats Industry

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr’s website traffic is steadily declining.

Text

Vegetable Oil Industry in India

The vegetable oils industry in India is a significant sector that plays a crucial role in the country's economy and food supply. India is one of the largest consumers and importers of vegetable oils globally due to its large population and dietary preferences.

The vegetable oils industry in India involves the production, processing, and marketing of various types of edible oils derived from plants. Some of the commonly used vegetable oils in India include palm oil, soybean oil, sunflower oil, mustard oil, groundnut oil, cottonseed oil and coconut oil.

Here are some key aspects of the vegetable oils industry in India:

Production: India produces a certain amount of vegetable oils domestically, primarily from oilseeds such as soybeans, groundnuts, rapeseed/mustard, sunflower, and sesame. However, domestic production is insufficient to meet the country's growing demand, leading to a significant reliance on imports.

Imports: India is one of the largest importers of vegetable oils in the world. The country imports vegetable oils from various countries such as Indonesia, Malaysia, Argentina, Ukraine, and others. Palm oil constitutes a significant portion of the imports, followed by soybean oil and sunflower oil.

Consumption: Vegetable oils are a staple ingredient in Indian cuisine and are used extensively for cooking purposes. The growing population, changing dietary patterns, and increasing urbanization have contributed to the rising consumption of vegetable oils in the country.

Processing: Vegetable oils are extracted from oilseeds through mechanical or solvent extraction methods. The oilseeds are processed in oil mills or solvent extraction units to obtain crude oil, which undergoes refining processes to produce refined vegetable oils.

Government Policies: The Indian government has implemented various policies to support the vegetable oils industry, promote domestic production, and reduce import dependency. These policies include subsidies, minimum support prices for oilseeds, research and development initiatives, and trade regulations.

Health Considerations: In recent years, there has been an increasing focus on the health aspects of vegetable oils. Consumers are becoming more conscious of factors such as trans fats, saturated fats, and overall nutritional value. This has led to a growing demand for healthier vegetable oil options and increased awareness of oil labeling and quality standards.

It's important to note that the vegetable oils industry is subject to market fluctuations, global commodity prices, weather conditions, and government policies, which can impact production, prices, and trade dynamics. For the most up-to-date information and statistics on the vegetable oils industry in India, it is advisable to refer to industry reports, trade publications, and official government sources.

2 notes

·

View notes

Text

Reposted from mastodon, long post under the cut

OP posted by me. I guess it does look like I’m making a definitive statement:

Because I'm seeing Discourse on this, here's my take as a non-vegan who's interested in resilient food systems/lifestyles.

I just don't think it matters that much if you're vegan or not. In my limited understanding, it would be better if we As A Society consumed less meat/dairy/eggs/leather/etc produced by the industrial animal agriculture system and if you're able to swear it off completely I think that's great. But also it would be better if we consumed less plant products produced by the industrial plant agriculture system because it's also polluting and full of human rights abuses.

So in my view, it's as always, less about "what individual consumption choices should I make in the context of the global industrial capitalist system" but "what choices are available that make myself and my community more resilient in the face of that system"

When looking at how to fulfill one's needs and those of one's community in ways that are less dependent on fragile, destructive global supply chains, i.e. growing/foraging food hyperlocally, in many locales a more plant-heavy diet is likely going to be the most feasible and safest. In my view that's the main reason it's worth experimenting with reducing the amount of animal products you consume.

(Also I don't say this type of thing often but omg vegans it's literally hurting your cause to pretend meat and dairy and eggs aren't good. They're amazing and sometimes there really is no good substitute.)

(AND vegans (namely white vegans LBR) learn to cook challenge, you not knowing how to use seasoning, fats and oils, or just how to cook vegetables properly, is the reason non-vegans think vegan food is bad.)

Reply from some rando who doesn’t follow me:

I'll preface this by saying that everyone's diet is their own choice, and there are like a billion factors that go into it, most outside of any individual's control. I personally am vegetarian even though I think it would be better for me to be vegan, so I'm not one to make absolute statements about what people should or should not be eating.

There are definitely lib vegans out there who think their personal decision to not eat meat, ride a bike, and shop at whole foods is going to personally save the planet. But I really don't think vegans as a whole buy into that philosophy nowadays, it's mostly an image promoted by companies trying to sell vegan products (which my stance on is beyond the scope of this already too long reply)

A big part of the reality of the situation is the inherent inefficiency of using arable land to produce animal feed. You're right that plant agriculture has a lot of problems, but the best way to reduce those problems, is the reduce the amount of plant matter we grow for animal feed. Around 70-80% of the worlds soy crops are solely dedicated to animal feed. Most calories fed to animals are metabolized by the animal to keep itself alive, even comparing specifically protein intake to protein output has the same issues. This is also ignoring the costs of transporting animal feed to the animals themselves, water usage, waste byproducts from industrial farming, and other issues that I'm sure you're already aware of.

There are small scale farms and traditional hunting practices that either do not suffer from or heavily mitigate the vast majority of these issues, but it's not possible to produce enough meat from these to meet the current demand in the west (mostly America honestly).

I think hyperlocality and foraging is interesting and has a place, but is not specifically the solution for all areas. I think here you're again pointing to the land usage of agriculture as a major issue, and again I'd agree, but I'd also say the solution is reducing or eliminating the amount of crops grown for livestock.

As for the last 2 points, I rarely if ever see any vegans saying that animal products don't taste good, and there are also plenty of omnis who can't cook so this is a really weird point to make IMO.

My response:

Well first off, I'm working off the belief that it's not wrong in principle to kill and eat animals or use other parts of them. That's a whole other discussion but it's important to make this clear.

Nothing of what you said really contradicts what I said or believe. I should also be clear that I'm not trying to write a dissertation here and most of what I post on the internet tends to be just me brain-dumping and throwing shit at the wall and are not necessarily the totality of what I believe or meant to be a well-rounded argument.

I'm very aware of the high percentage of crops that goes into animal feed, and I think it's undeniable that as a whole it's imperative that overall meat consumption should be *reduced*, especially in places like the US. I also think if more people made personal choices to reduce their own consumption of animal products, it would be a lot easier to see that reduction on a nationwide scale.

I would say *a part of* the solution is reducing the amount of crops grown for livestock but I don't think we should expect that to be *the* solution, for one thing, the calories and nutrition people would have been getting from animal products will need to be replaced with an equivalent amount from plant sources.

This post is literally just about the debates I've been seeing about whether people, individually, should be vegan, and on that level, like I said, I just don't think this debate is worth having. If people like being vegan I think that's great and I love vegan food and I personally have been working on gradually transitioning over to more plant-based options. But as I said I think the main reason to do that is more for purposes of de-accustoming oneself from a lifestyle that's so dependent on global supply chains that as we've seen are incredibly fragile and also have complex and devastating impacts on the planet and people. I think for a lot of people, a more resilient lifestyle will necessarily be one that involves fewer animal products.

But if someone can't or just doesn't want to be vegan it's just not a huge deal and it doesn't mean they hate animals, and it's a waste of time to try to convert those people. I just think there are more interesting conversations to be had about our food systems.

The parentheticals are not part of my main point lol hence the parentheses, and they're mostly sarcastic, but I literally do see people downplaying the role meat and animal products play in people's livelihoods (and not just in food applications), and I've had a depressing number of horrible bland vegan stews and also a ton of amazing vegan dishes where the difference was literally spices and proper application of Maillard reactions, and it just makes me sad that someone might try something from the first category and think that's all vegan food is. It's not that deep.

Anyways.

6 notes

·

View notes

Text

Air Fryer Market Competitive Landscape: An In-Depth Look at Industry Growth and Future Demand

The air fryer market has experienced a dramatic surge in popularity over the past few years, driven by consumer demand for healthier cooking solutions, convenience, and the growing trend of home cooking. This kitchen appliance, which uses hot air circulation to cook food with little to no oil, offers a healthier alternative to traditional frying methods. As a result, the air fryer market is expanding rapidly, with projections indicating continued growth in the coming years. In this article, we will explore the competitive landscape of the air fryer industry, examining key players, market dynamics, and future demand.

Market Growth and Drivers

The air fryer market has witnessed exponential growth, with demand fueled by an increasing awareness of healthy eating habits. With rising health concerns related to obesity, diabetes, and heart disease, many consumers are turning to air fryers as a way to prepare fried foods with fewer calories and less fat. The ease of use, quick cooking times, and versatility of air fryers in preparing a wide variety of dishes have also contributed to their growing popularity.

In addition to health-conscious consumers, the COVID-19 pandemic played a significant role in accelerating the adoption of air fryers. As people spent more time at home, there was an increased interest in cooking appliances that could help them create restaurant-quality meals with minimal effort. The rising trend of cooking enthusiasts and influencers promoting air fryer recipes on social media platforms like Instagram and YouTube has further fueled interest in these appliances.

Competitive Landscape

The air fryer market is highly competitive, with numerous global and regional players vying for market share. Some of the leading companies in the market include Philips, Ninja, COSORI, Breville, and Instant Brands. These companies have introduced a wide range of air fryer models, catering to different consumer preferences and needs, from compact models suitable for small households to larger, more advanced units designed for families or commercial use.

Philips, one of the pioneers in air fryer technology, continues to maintain a strong market presence, thanks to its innovative features such as the Fat Removal Technology, which separates and captures excess fat during cooking. On the other hand, Ninja has gained significant traction with its multi-functional air fryers that offer versatility for baking, roasting, grilling, and dehydrating, alongside air frying.

COSORI, a newer player in the market, has built a reputation for offering high-quality air fryers at affordable prices, which has made it popular among budget-conscious consumers. Breville and Instant Brands, known for their high-end kitchen appliances, have also capitalized on the air fryer trend by offering premium models equipped with smart technology and sleek designs.

Trends Shaping the Market

Several trends are influencing the air fryer market's future growth:

Smart Technology Integration: Many manufacturers are incorporating smart features, such as Wi-Fi connectivity and compatibility with mobile apps, allowing users to control and monitor their air fryer remotely. This trend is particularly popular among tech-savvy consumers who seek convenience and precision in their cooking.

Product Innovation: Companies are constantly innovating to improve the efficiency and functionality of air fryers. From expanding the range of preset cooking programs to designing more energy-efficient models, innovation remains a key driver in the competitive landscape.

Sustainability: As environmental concerns continue to rise, manufacturers are focusing on sustainability by using eco-friendly materials and improving the energy efficiency of their products. This is in response to growing consumer preferences for sustainable products that have a lower environmental impact.

Future Demand and Market Outlook

The demand for air fryers is expected to continue growing, driven by increasing health consciousness, rising disposable incomes, and growing urbanization. As more consumers adopt healthier lifestyles and cooking habits, air fryers will remain a popular choice. Additionally, as manufacturers continue to innovate, the functionality of air fryers will expand, making them an even more attractive option for home cooks.

In conclusion, the air fryer market is set to experience sustained growth, with an increasingly competitive landscape shaped by product innovation, consumer preferences, and evolving trends in technology and sustainability. As the industry continues to mature, both established and emerging players will need to stay ahead of these trends to maintain their market share and capitalize on future demand.

Get Free Sample and ToC : https://www.pristinemarketinsights.com/get-free-sample-and-toc?rprtdtid=NDk1&RD=Air-Fryer-Market-Report

#AirFryerMarketIndustryForecast#AirFryerMarketDemandTrends#AirFryerMarketCompetitiveLandscape#AirFryerMarketGrowthAnalysis#AirFryerMarketValueVolumeAnalysis

0 notes

Text

Biodiesel Production Cost Analysis: Key Insights for Competitive Advantage

In the drive towards sustainable energy, biodiesel has emerged as a promising alternative fuel, offering reduced emissions and environmental benefits over traditional fossil fuels. Produced from renewable resources such as vegetable oils, animal fats, and recycled cooking oils, biodiesel is increasingly used in transportation, heating, and industrial applications. Understanding the production cost of biodiesel is crucial for businesses and policymakers aiming to optimize their energy strategy, enhance cost-effectiveness, and promote sustainable practices. Procurement Resource provides in-depth insights into the factors influencing biodiesel production costs to help businesses stay competitive in the rapidly evolving energy landscape.

Request a Free Sample for Biodiesel Production Cost Reports

If you're looking to understand the cost structure of biodiesel production, Procurement Resource offers free sample reports to give you a comprehensive view of cost breakdowns, pricing trends, and strategic insights.

Request a Free Sample -https://www.procurementresource.com/production-cost-report-store/biodiesel/request-sample

Why Biodiesel? A Clean and Renewable Energy Source

As industries worldwide seek greener energy solutions, biodiesel offers a viable alternative due to its renewable nature and ability to reduce greenhouse gas emissions. Unlike conventional diesel, biodiesel can be used in existing diesel engines without modification, making it accessible and cost-effective for many sectors. Additionally, biodiesel production generates fewer emissions, and the fuel itself is biodegradable, providing further environmental advantages. With growing attention on carbon reduction and sustainable energy practices, biodiesel is poised to play an essential role in the future energy mix.

Understanding the Factors Behind Biodiesel Production Costs

Biodiesel production involves a complex process with multiple cost-driving factors, including feedstock prices, production technology, labor, and regulatory requirements. Here is a detailed breakdown of the components influencing biodiesel production costs:

1. Feedstock Costs

The primary raw materials for biodiesel production are vegetable oils (such as soybean or canola oil), animal fats, and waste cooking oils. Feedstock costs constitute the largest portion of biodiesel production expenses, often accounting for 70-80% of the total. The prices of these feedstocks are highly variable, influenced by global agricultural markets, weather conditions, and supply chain disruptions. For example, a poor crop yield can lead to higher feedstock prices, which directly impacts biodiesel production costs.

Read the Full Report - https://www.procurementresource.com/production-cost-report-store/biodiesel

Monitoring feedstock costs is essential for businesses to manage biodiesel production expenses effectively. The volatility in feedstock prices highlights the importance of tracking market trends and adopting cost-effective procurement strategies.

2. Production Technology and Energy Costs

Biodiesel production involves converting oils and fats into biodiesel through a process called transesterification. This process requires significant energy input in the form of heat and electricity, making energy costs a substantial component of biodiesel production. Rising energy prices can impact production expenses, emphasizing the need for efficient energy management and technology optimization in biodiesel facilities.

Moreover, advancements in production technology, such as enzyme-based processes or innovative catalysts, can enhance efficiency and reduce costs. However, implementing these technologies often requires significant capital investment. By investing in advanced production methods, businesses can improve productivity and reduce operational costs in the long run.

3. Labor and Operational Costs

Labor costs vary by region and contribute to the overall expenses associated with biodiesel production. Skilled labor is required to operate complex equipment and ensure safe handling of chemicals and processes. Operational expenses also include costs for maintaining equipment, safety measures, and compliance with environmental regulations. Regular maintenance is essential to prevent downtime and reduce repair costs, as unplanned shutdowns can lead to financial losses.

Environmental and Regulatory Costs

As the demand for cleaner energy grows, environmental regulations on biodiesel production are becoming increasingly stringent. Compliance with these regulations is crucial for companies to avoid penalties and continue operations. In some regions, biodiesel producers are required to invest in pollution control technology or carbon offset programs to reduce environmental impact. Although these measures add to production costs, they are essential for meeting regulatory standards and maintaining a positive public image.

Failure to adhere to regulatory requirements can result in fines or legal issues, making it essential for biodiesel producers to prioritize compliance. Tracking regulatory trends and adjusting production practices accordingly can help companies manage costs effectively.

Ask an Analyst for In-Depth Insights

Our analysts at Procurement Resource go beyond providing raw data. They offer expert insights into the market trends and drivers that influence biodiesel production costs, helping companies make informed strategic decisions.

Ask an Analyst - https://www.procurementresource.com/production-cost-report-store/biodiesel/ask-an-analyst

What Our Biodiesel Production Cost Reports Include

At Procurement Resource, our biodiesel production cost reports cover all aspects of the production process, providing businesses with a competitive edge. Here’s what you can expect from our reports:

Detailed Cost Breakdown: Our reports offer a comprehensive view of all cost factors in biodiesel production, from feedstock prices and energy usage to labor and regulatory expenses.

Real-Time Data and Forecasts: With constantly changing market dynamics, our reports provide the latest data and future projections, helping companies make data-driven decisions.

Price Trends and Market Analysis: Monitoring price trends is crucial for businesses relying on biodiesel for operations. We track price movements to help companies anticipate changes and adapt their strategies accordingly.

Benchmarking and Comparison: By comparing your production costs with industry benchmarks, our reports help you identify areas for cost reduction and efficiency improvements.

Procurement Insights: Effective procurement is essential for managing biodiesel production costs. Our reports offer practical strategies for optimizing the supply chain, improving cost management, and ensuring sustainability.

The Benefits of Partnering with Procurement Resource

With Procurement Resource, businesses gain access to data-driven intelligence that supports decision-making and procurement strategies. Our Biodiesel Production Cost Reports simplify the procurement process, improve supply chain management, and provide insights for navigating complex market challenges.

Procurement Resource offers customized reports to address the unique needs of each business, from cost management and regulatory compliance to identifying market opportunities. Our team of experienced analysts is committed to providing guidance that aligns with your operational goals, enabling you to remain competitive in a dynamic market.

Request Your Free Sample Report Today

If you're ready to optimize your biodiesel procurement process, we encourage you to request a free sample report from Procurement Resource. Our reports provide you with essential knowledge and tools to manage biodiesel-related expenses, enhance operational efficiency, and stay ahead in the competitive energy landscape.

Request a Free Sample - https://www.procurementresource.com/production-cost-report-store/biodiesel/request-sample

Contact Us

Company Name: Procurement Resource Contact Person: Ben Kingsley Email: [email protected] Toll-Free Numbers: USA & Canada: +1 307 363 1045 UK: +44 7537171117 Asia-Pacific (APAC): +91 1203185500 Address: 30 North Gould Street, Sheridan, WY 82801, USA

0 notes

Text

The Margarine Industry and Market: Trends, Growth, and Opportunities

The margarine industry, an integral part of the global food sector, has witnessed significant changes in recent years, driven by shifts in consumer preferences, health trends, and innovations in food technology. Historically regarded as a cheaper alternative to butter, margarine has evolved into a versatile and innovative product, offering a range of applications beyond simple spreadables. This blog explores the current state of the margarine market, the factors influencing its growth, and the opportunities it presents for manufacturers and investors.

Market Overview of Margarine

The global margarine market is projected to be valued at USD 22.67 billion in 2024 and is expected to reach USD 25.54 billion by 2029, growing at a compound annual growth rate (CAGR) of 2.42% from 2024 to 2029.

Margarine is a spread typically made from vegetable oils, emulsifiers, and sometimes dairy products. It was first introduced in the late 19th century as a cheaper alternative to butter, which was expensive and in limited supply. Over the years, margarine has adapted to changing dietary habits, with various formulations catering to different segments of the population—ranging from low-fat, low-sodium versions to vegan and non-GMO options.

Globally, the margarine market is substantial, with a growing consumer base in emerging economies, particularly in Asia-Pacific and Latin America. In developed regions like North America and Europe, however, the market has matured, and growth is driven primarily by product innovation, health-conscious formulations, and shifts toward plant-based diets.

Key Market Drivers

Several factors are currently influencing the margarine industry:

a) Health and Wellness Trends

As consumers become more health-conscious, there has been a rising demand for products with healthier ingredients. The use of vegetable oils like olive oil, sunflower oil, and canola oil in margarine formulations, for instance, offers healthier alternatives to butter, which is high in saturated fats. Margarine manufacturers are increasingly focusing on reducing trans fats and offering options with lower cholesterol levels. Some margarine products are enriched with omega-3 fatty acids, vitamins, and other nutrients to appeal to health-conscious consumers.

Additionally, the demand for plant-based and dairy-free products has surged with the rise of vegan and lactose-free diets, which has opened new avenues for the margarine market. Plant-based margarine, often made from sunflower, soybean, or coconut oils, has been gaining popularity among consumers seeking vegan alternatives.

b) Convenience and Versatility

The growing demand for convenience foods has benefitted the margarine market, as it is easy to use and has a long shelf life. Margarine serves a variety of functions, including use as a spread, in baking, frying, and even in confectionery products. Manufacturers are increasingly creating multipurpose margarines, such as those designed for high-heat cooking, which allow for greater convenience in the kitchen. This versatility is one of the reasons margarine continues to be a staple in many households.

c) Evolving Consumer Preferences

The ongoing shift towards plant-based diets and cleaner labels is another major factor shaping the margarine market. Consumers are becoming more selective about what they eat, demanding transparency regarding ingredients and nutritional content. In response, margarine brands are opting for simpler, more natural ingredients, and many are avoiding the use of artificial additives, preservatives, or genetically modified organisms (GMOs).

d) Increasing Global Population and Urbanization

With global population growth and increased urbanization, demand for processed and packaged foods is rising, which includes margarine. Urban consumers, especially in developing countries, are shifting away from traditional fats like animal-based oils and butter in favor of more affordable and accessible margarine products. Additionally, the rising middle class in emerging markets, including parts of Asia, Africa, and Latin America, is further fueling the demand for convenience-based food products like margarine.

Competitive Landscape

The margarine market is highly competitive, with several multinational companies dominating the industry. Major players in the margarine market include:

Unilever: One of the largest producers of margarine globally, Unilever markets its margarine products under well-known brands such as Flora, Bertolli, and Country Crock.

Kraft Heinz: Known for its range of margarine products under the brands like Parkay and Miracle Whip.

Bunge Limited: A significant player in the oils and margarine space, particularly in North America and Latin America.

Cargill: Offers a variety of margarine products under different brand names across various regions.

In addition to these established players, there are several regional and smaller brands focusing on niche markets, such as organic or vegan margarines, that are gaining traction.

Challenges in the Margarine Industry

Despite its growth, the margarine market faces several challenges, including:

Health Concerns: Despite the elimination of trans fats from most margarine products, concerns over the health impact of certain oils, such as palm oil, remain a challenge. Additionally, some consumers continue to associate margarine with unhealthy fats, despite its evolution.

Price Fluctuations of Raw Materials: The prices of vegetable oils, especially palm oil, can be volatile due to climatic conditions, trade policies, and geopolitical factors, affecting the cost structure of margarine production.

Consumer Skepticism: Some consumers still prefer butter, associating it with a more natural or traditional product. This has led to challenges in convincing these consumers to switch to margarine, despite its health benefits.

Opportunities and Future Outlook

The margarine market is expected to continue growing, albeit at a slower pace in mature regions. However, significant growth opportunities exist in emerging markets and in product innovation.

Innovation in Product Formulations: The future of the margarine industry lies in developing healthier and more sustainable product options. For example, margarine products made from high-quality, non-GMO oils or those with added functional ingredients (such as probiotics, vitamins, and plant-based proteins) are becoming increasingly popular.

Sustainability Initiatives: With rising concerns about the environmental impact of food production, margarine manufacturers are exploring more sustainable sourcing of ingredients, particularly palm oil, and are focusing on reducing the carbon footprint of their products.

Growth in Plant-Based Alternatives: The plant-based food movement is expected to be one of the key drivers of growth for margarine, as consumers increasingly demand dairy-free, vegan, and non-GMO options.

Expansion into Emerging Markets: As the middle class grows in developing regions, particularly in Asia-Pacific and Africa, there is a massive potential to expand the margarine market through targeted marketing campaigns, affordable product options, and tailored offerings that suit local culinary preferences.

Conclusion

The margarine industry, while facing some challenges, continues to grow and innovate in response to changing consumer demands. Healthier formulations, plant-based alternatives, and sustainable sourcing practices are likely to dominate the future of the market. Manufacturers who can adapt to these trends, embrace sustainability, and provide value to consumers will be well-positioned to capitalize on the opportunities in this evolving market.

As the margarine industry moves forward, it is clear that consumer preferences, health-conscious choices, and the demand for convenient, versatile food options will continue to shape its trajectory, offering both challenges and growth potential for stakeholders across the supply chain.

For a detailed overview and more insights, you can refer to the full market research report by Mordor Intelligence https://www.mordorintelligence.com/industry-reports/margarine-market

#margarine market#margarine market size#margarine market share#margarine market trends#margarine market growth#margarine market report

0 notes

Text

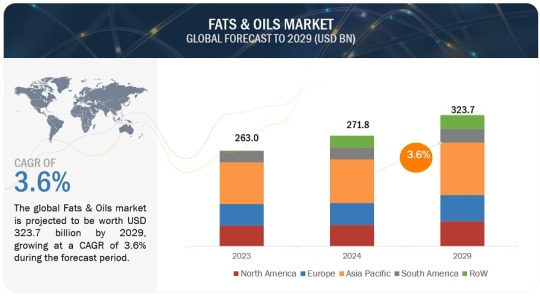

Fats and Oils Market Set for Rapid Growth: Trends, Innovations, and Consumer Demands Driving Expansion

The global fats and oils market is projected to be valued at USD 271.8 billion in 2024, with a compound annual growth rate (CAGR) of 3.6%, expected to reach USD 323.7 billion by 2029. This market is undergoing significant transformations and innovations. The demand for fats and oils goes beyond culinary uses, impacting various sectors, including animal feed, oleochemicals, and biofuels.

Vegetable oils and animal fats are essential components in the food industry, contributing to the texture, flavor, and shelf life of processed foods. Palm, rapeseed, sunflower, and soybean oils are the most widely used oils worldwide, thanks to their versatile applications in both food and non-food products. Animal fats, such as butter and lard, are particularly important in baking, where they are prized for their rich, distinctive flavors.

Fats and Oils Market Trends

Here are some key trends in the Fats and Oils Market:

Health Consciousness: As consumers become more health-conscious, there’s a growing demand for healthier fats, such as olive oil, avocado oil, and coconut oil. This shift is leading to the popularity of oils with favorable fatty acid profiles and beneficial nutrients.

Plant-Based Oils: The trend toward plant-based diets is driving the demand for oils derived from plants. Oils like sunflower, canola, and palm oil are gaining traction due to their versatility and health benefits. Sustainable Sourcing: Environmental sustainability is becoming increasingly important for consumers and manufacturers. Brands are seeking sustainably sourced oils and fats, leading to a rise in certifications like RSPO (Roundtable on Sustainable Palm Oil).

Functional Fats: There is a growing interest in functional fats that offer additional health benefits, such as omega-3 and omega-6 fatty acids. These are often marketed for their heart health benefits and ability to support cognitive function.

Food Innovation: The food and beverage industry is continually innovating with new formulations that incorporate unique fats and oils to enhance flavor, texture, and nutritional value. This includes the use of fats for plant-based and alternative protein products.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=6198812

Vegetable Sources of Fats and Oils Expected to Lead Market Share During the Forecast Period.

Vegetable-based oils are expected to maintain the largest share of the fats and oils market throughout the forecast period. This dominance can be attributed to their versatility, health benefits, and wide availability. Oils from sources like soybean, palm, and sunflower are commonly used in cooking and food processing due to their broad range of applications and consumer preference for healthier alternatives to animal fats. These oils offer essential fatty acids and are considered more beneficial for health. Moreover, innovations in agricultural practices and biotechnology have boosted vegetable oil production, ensuring a consistent and cost-effective supply. Their adaptability in both food and industrial uses reinforces their leading role in the market.

The Food Application Segment is Projected to Dominate the Fats and Oils Market Share Throughout the Forecast Period.

In the application segment, the food industry is projected to hold the largest share of the fats and oils market throughout the forecast period. Fats and oils play a vital role in enhancing flavor, texture, and preservation across various food products. They are essential in cooking and baking, providing desirable characteristics like crispiness and richness. Additionally, fats and oils act as carriers for fat-soluble vitamins and flavors, boosting consumer appeal. The growing demand for processed and convenient foods, coupled with an increasing interest in diverse culinary experiences, further drives the dominance of food applications in this market segment.

Top Fats and Oils Companies

The key players in the market are ADM (US), Wilmar International Ltd (Singapore), Cargill, Incorporated (US), Bunge (US), Kaula Lumpur Kepong Berhad (Malaysia), Olam Agri Holdings Pte Ltd (India), Manildra Group (Australia), Mewah Group (Singapore), Associated British Foods plc (UK), United Plantations Berhad (Malaysia), Ajinomoto Co., Inc. (Japan), Fuji Oil Co., Ltd. (Japan), Oleo-Fats (Philippines), Borges Agricultural and Industrial Edible Oils, S.A.U. (Spain), K S Oils Limited (India), CSM Ingredients (US), SD Guthrie International Zwijndrecht Refinery B.V. (Netherlands), Musim Mas Group (Singapore), Richardson International Limited (Canada), and AAK AB (Sweden).

#Fats and Oils Market#Fats and Oils#Fats and Oils Market Size#Fats and Oils Market Share#Fats and Oils Market Growth#Fats and Oils Market Trends#Fats and Oils Market Forecast#Fats and Oils Market Analysis#Fats and Oils Market Report#Fats and Oils Market Scope#Fats and Oils Market Overview#Fats and Oils Market Outlook#Fats and Oils Market Drivers#Fats and Oils Industry#Fats and Oils Market Companies

0 notes

Text

Sunflower Oil: A Healthy, Versatile Ingredient for the Modern Kitchen

The global sunflower oil market is experiencing steady growth due to increased demand for healthier edible oils and the widespread use of sunflower oil across various food and industrial applications. According to the report, the sunflower oil market is projected to grow at a CAGR of over 6% from 2022 to 2028. The market, which was valued at USD 19 billion in 2022, is anticipated to reach approximately USD 29 billion by 2028.

What is Sunflower Oil?

Sunflower oil is a popular edible oil derived from sunflower seeds. Known for its high levels of unsaturated fats, particularly oleic acid, sunflower oil is widely recognized for its health benefits, making it a favored choice for cooking and food preparation. Sunflower oil also finds applications in cosmetics, biofuels, and the pharmaceutical industry.

Get Sample pages of Report: https://www.infiniumglobalresearch.com/reports/sample-request/42276

Market Dynamics and Growth Drivers

The global sunflower oil market’s growth is attributed to several key factors:

Increasing Health Awareness: As consumers become more health-conscious, demand for sunflower oil, which is low in saturated fats and high in essential fatty acids, is on the rise. Its beneficial effects on heart health have bolstered its popularity among consumers looking for healthier cooking options.

Rising Demand in Food and Beverage Industry: Sunflower oil is extensively used in cooking, frying, and salad dressings. With the food and beverage industry’s growth, particularly in emerging economies, demand for sunflower oil is expected to continue rising.

Industrial Applications: Sunflower oil’s versatility has increased its applications in the cosmetics and pharmaceutical industries, where it is used in skin care and therapeutic products due to its moisturizing and anti-inflammatory properties.

Biofuel Production: As biofuel becomes a viable alternative to traditional fossil fuels, sunflower oil is gaining traction in biofuel production. Many countries are adopting biofuels as part of their energy transition efforts, further supporting market growth.

Regional Analysis

Europe: Europe is a significant market for sunflower oil, with countries like Russia and Ukraine being major producers. The region’s demand is driven by the food and cosmetics industries, as well as growing biofuel usage.

Asia-Pacific: Rapidly urbanizing regions such as India and China are experiencing high demand for sunflower oil. The rising population and growing disposable incomes have contributed to a greater demand for premium cooking oils, including sunflower oil.

North America: North America shows moderate growth in the sunflower oil market. Health-conscious consumers are increasingly adopting sunflower oil in their diets, and the food and beverage industry’s growth supports further market expansion.

Latin America, Middle East & Africa: These regions are witnessing steady demand growth due to increasing adoption of sunflower oil in food preparation and industrial applications. The growing middle-class population in these regions also contributes to the market’s expansion.

Competitive Landscape

The global sunflower oil market is competitive, with several prominent players dominating the space. Key players include:

Cargill, Inc.: One of the largest producers of sunflower oil, Cargill offers a range of edible oils and focuses on product innovation and sustainable sourcing.

Archer Daniels Midland Company (ADM): ADM is a major player in the edible oil market, known for its extensive distribution network and focus on high-quality, health-focused products.

Bunge Limited: Bunge has a strong presence in the sunflower oil market, emphasizing sustainable agricultural practices and offering a diverse portfolio of oils for food and industrial use.

Kernel Holding: As one of the largest producers of sunflower oil in Eastern Europe, Kernel Holding is a key player in the global market, especially in regions that rely on imports.

Conagra Brands, Inc.: Known for its range of edible oils, Conagra focuses on consumer demand for health-focused products and is a major supplier in North America.

Report Overview : https://www.infiniumglobalresearch.com/reports/global-sunflower-oil-market

Challenges and Opportunities

While the market is set for growth, it faces challenges such as fluctuating raw material prices and weather-related impacts on crop yield. Climate variability, in particular, can affect sunflower crop production, impacting supply and pricing.

However, the growing trend toward sustainable agriculture and the rising demand for biofuel present substantial growth opportunities. Innovations in crop production and processing methods can further enhance production efficiency and product quality.

Conclusion

The global sunflower oil market is on a growth trajectory, expected to increase from USD 19 billion in 2022 to around USD 29 billion by 2028, with a CAGR of over 6% during the forecast period. Driven by health-conscious consumers, the food and beverage industry’s expansion, and demand in industrial applications, the sunflower oil market is poised for steady growth. As consumer preference for healthier oils continues to rise, the market’s future remains promising, bolstered by ongoing innovations and the expanding global food sector.

0 notes

Text

The dairy-free shortening market is projected to grow from USD 22,605.5 million in 2024 to approximately USD 37,412 million by 2032, reflecting a compound annual growth rate (CAGR) of 6.50%. The dairy-free shortening market is experiencing rapid growth, driven by increased consumer demand for plant-based products, health concerns related to dairy, and rising awareness of dietary restrictions like lactose intolerance and veganism. Dairy-free shortening, a fat-based product primarily made from vegetable oils, is often used in baking, cooking, and food production as a substitute for traditional dairy butter or lard. It has gained popularity due to its versatility, shelf stability, and ability to meet the growing demand for plant-based and allergen-free food ingredients. Here, we’ll explore the key market drivers, consumer preferences, challenges, and future prospects of the dairy-free shortening industry.

Browse the full report https://www.credenceresearch.com/report/dairy-free-shortening-market

Market Drivers and Growth Factors

1. Rising Demand for Plant-Based Products A surge in veganism and the adoption of plant-based diets are major drivers for the growth of the dairy-free shortening market. According to studies, consumers are increasingly inclined towards plant-based foods due to health concerns, environmental awareness, and ethical considerations. This shift has created a fertile ground for the dairy-free shortening market, as it caters to vegans and others avoiding animal-based products.

2. Health and Dietary Considerations A growing number of people are developing lactose intolerance, milk allergies, or have digestive issues related to dairy consumption. For these consumers, dairy-free alternatives, including shortening, provide a safer and healthier option. Additionally, the rise of ketogenic, gluten-free, and allergen-free diets has driven the adoption of dairy-free shortening, which can be formulated to fit into these specialized diets.

3. Awareness of Environmental Impact Sustainability and environmental concerns are shaping consumer behavior, and the plant-based food industry benefits from this shift. Traditional dairy production has a higher environmental impact, involving significant water use, greenhouse gas emissions, and land requirements. By contrast, dairy-free shortening, primarily derived from plant oils like palm, coconut, or soy, offers a lower carbon footprint, appealing to environmentally conscious consumers.

4. Innovative Product Development and Distribution Channels Manufacturers are responding to market demand with innovative dairy-free shortening products that cater to both household consumers and the foodservice industry. Improved formulations that mimic the texture and taste of butter have made dairy-free shortenings more appealing for baking and cooking, which broadens their applications. The market’s expansion is further facilitated by e-commerce platforms, allowing consumers easier access to specialized products.

Key Trends in the Dairy-Free Shortening Market

1. Shift to Organic and Non-GMO Ingredients With the rising demand for clean-label products, many manufacturers are opting for organic, non-GMO ingredients in their dairy-free shortenings. Organic coconut oil, palm oil, and other natural oils are popular choices, as they appeal to health-conscious consumers and adhere to stricter quality standards. The organic segment within dairy-free shortening has been growing steadily as consumers seek healthier options without artificial additives.

2. Diversification of Ingredient Sources Traditional vegetable oils, like palm and coconut, have dominated the market. However, newer sources such as avocado oil, olive oil, and even algal oil are being explored for their unique flavor profiles and health benefits. This diversification is allowing companies to cater to varying consumer tastes and dietary needs.

3. Focus on Sustainable Sourcing The sustainability of sourcing ingredients, particularly palm oil, is a concern among environmentally aware consumers. To address this, some companies are using certified sustainable palm oil or exploring alternative oils with a lower environmental impact. This focus on sustainable sourcing not only enhances brand image but also addresses the ethical and environmental demands of the market.

4. Growth in E-commerce and Direct-to-Consumer Sales The rise of e-commerce has significantly boosted the dairy-free shortening market by allowing manufacturers to reach a wider audience. Companies are increasingly adopting direct-to-consumer (DTC) models to market their products, allowing for better control over branding, customer engagement, and market insights. This trend has accelerated during the pandemic as more consumers opted for online shopping.

Market Challenges

1. Price Sensitivity and Production Costs Dairy-free shortenings are often more expensive than traditional butter or margarine, which can limit their appeal to cost-conscious consumers. The use of premium ingredients and sustainable practices can drive up production costs, creating a challenge in markets with high price sensitivity.

2. Regulatory and Labeling Challenges The dairy-free shortening industry faces regulatory hurdles related to labeling and claims. Manufacturers must adhere to local and international regulations on ingredient labeling, especially in terms of “non-dairy” or “plant-based” claims, which can vary from one market to another. This requires companies to be vigilant about compliance to avoid potential legal issues.

3. Texture and Flavor Limitations While there have been significant advancements in formulation, some consumers still prefer the taste and texture of traditional butter. Developing dairy-free shortenings that perfectly mimic the sensory properties of dairy butter remains a challenge, particularly for high-end baking applications.

Future Outlook

The future of the dairy-free shortening market appears promising, driven by continuous innovations in product formulation, diversification of raw material sources, and expansion into emerging markets. As more consumers adopt plant-based lifestyles and prioritize sustainability, the demand for dairy-free shortening is expected to grow. Additionally, advancements in food technology may enable producers to further improve the taste, texture, and nutritional profile of these products, making them more competitive with traditional shortenings.

Key Player Analysis:

Groupe Danone

The Hain Celestial Group

The Whitewave Foods Company

Good Karma Foods

GraceKennedy Group

Blue Diamond Growers, Inc.

SunOpta, Inc.

Oatly A.B.

Vitasoy International Holdings Limited

Nutiva Inc.

Segmentation:

By Product Type:

Beverages

Milk

Dairy-Free Kefir

Bakery Products

By Application:

Household

Commercial

By Region:

North America

US

Canada

Mexico

Europe

Germany

France

UK

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Browse the full report https://www.credenceresearch.com/report/dairy-free-shortening-market

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

Oilseed Market Forecast: Breaking Down Growth Trends, Challenges, and Opportunities

The global oilseed market has seen remarkable growth, driven by rising demand for edible oils, biofuels, and plant-based protein products. Oilseeds like soybeans, sunflower, and canola are essential to many industries, offering versatile applications and a high-profit margin. With continued expansion, the market is projected to reach new heights in the coming decade, underscoring its relevance in global agriculture, food, and energy sectors.

In this blog, we will explore the oilseed market’s growth trajectory, analyze key players, examine market segmentation, consider regulatory constraints, and forecast the future of this crucial market.

Market Growth & Size

The oilseed market has exhibited steady growth in recent years, primarily due to increasing consumer demand for healthy cooking oils, biofuel production, and plant-based protein. By the end of 2024, the global oilseed market is expected to be valued at approximately $280 billion, with a projected compound annual growth rate (CAGR) of around 5-6% over the next eight years. This growth is largely driven by:

Rising Demand for Edible Oils: Health-conscious consumers are shifting toward oils rich in unsaturated fats, creating high demand for products derived from soybeans, sunflower, and canola seeds.

Biofuel Expansion: Governments worldwide are promoting biofuels to reduce carbon emissions, spiking demand for oilseeds as a biofuel feedstock.

Increased Use in Animal Feed: Oilseed meals, a by-product of oil extraction, are essential in the animal feed industry for high-protein feed.

Key Companies in the Oilseed Market

The oilseed market is dominated by major players, each contributing to market expansion through innovation and sustainability initiatives. Key companies include:

Archer Daniels Midland Company

Bunge Limited

Cargill Inc.

Wilmar International Ltd.

Louis Dreyfus Company

These companies lead in processing, production, and distribution of oilseeds, constantly evolving to meet rising consumer and industrial demands while navigating economic and regulatory challenges.

Legal Constraints & Limitations

The oilseed market is subject to several regulatory standards and limitations, affecting production, processing, and distribution.

Agricultural Policies and Subsidies: Many countries provide subsidies and implement policies favoring domestic oilseed production, but tariffs and import restrictions affect international trade and competition.

Environmental Regulations: Oilseed production often involves pesticide use and water consumption, attracting strict regulations to minimize environmental impact.

Biofuel Regulations: With biofuel demand increasing, policies incentivizing renewable energy production impact oilseed processing and pricing, requiring compliance with carbon emission standards.

Market Limitations

Despite its growth, the oilseed market faces challenges:

Weather-Dependent Production: Oilseed crops are susceptible to weather conditions, impacting yield and availability.

Volatile Prices: Prices fluctuate due to factors like geopolitical tensions, environmental changes, and shifts in consumer demand.

Supply Chain Issues: Processing oilseeds involves multiple stages, with disruptions in any segment potentially affecting overall production and supply.

Market Segmentation by Product and Application

By Product Type

Oilseeds are diversified by type, with each type having unique applications across food, industrial, and agricultural sectors:

Soybeans: Predominantly used for oil extraction and protein-rich meals in animal feed.

Sunflower Seed: Valued for its oil content, commonly used in cooking oil, cosmetics, and biofuels.

Canola: Known for its heart-healthy oil, canola is widely used in food industries and as biofuel.

Peanuts: Beyond culinary uses, peanut oil is a valuable cooking medium due to its high smoke point.

Others: This includes seeds like sesame and flax, which are gaining popularity for health applications.

By Application

Oilseed applications are segmented based on their end-use industries:

Edible Oils: The food industry is the largest consumer of oilseeds, producing oils used for cooking, margarine, and other culinary purposes.

Biofuels: With the push for greener energy, oilseeds are increasingly processed into biodiesel, contributing to reduced carbon emissions.

Animal Feed: High-protein oilseed meals, derived from soybeans and canola, are a staple in livestock diets, essential for animal growth and health.

Industrial Uses: Oilseeds are also utilized in non-food industries, including cosmetics, pharmaceuticals, and even lubricants.

Future Forecast: Trends and Opportunities

The oilseed market is projected to experience continued growth due to several emerging trends and opportunities:

Demand for Plant-Based Proteins: As plant-based diets rise in popularity, oilseeds are expected to serve as a primary protein source for various meat alternatives.

Advancements in Genetic Modification: GM oilseeds with enhanced resistance to pests and environmental stressors can potentially increase yields and lower production costs.

Sustainable Production Methods: With a focus on reducing environmental impact, companies are investing in sustainable farming practices to make oilseed production more eco-friendly.

Increased Biofuel Demand: As countries worldwide aim to reduce reliance on fossil fuels, biofuels derived from oilseeds are expected to play a major role in sustainable energy solutions.

Conclusion

The oilseed market is a dynamic segment within global agriculture, driven by diverse applications in food, fuel, and industrial products. With rising consumer health consciousness, demand for plant-based protein, and biofuel industry expansion, the market outlook remains positive. Key players continue to innovate, while sustainability and regulatory compliance shape the industry’s direction. Over the next decade, the oilseed market will likely continue its upward trajectory, playing a vital role in fostering a sustainable future for agriculture and energy.

Contact Us for more information on the Oilseed Market Research 2023–2030 Forecast : Or Phone Call us :

USA — +1 507 500 7209 | India — +91 750 648 0373

Browse More Articles

Offshore Support Vessels Market Size

Oilfield Chemicals Market Growth

Orthopedic Prosthetics Market Trends

0 notes

Text

Canada Soybean Oil Market (2024-2032): Growth, Health Trends

The Canada soybean oil market size reached an estimated production volume of 330 thousand metric tons (MT) in 2020. The market has been experiencing steady growth, driven by increasing consumer health consciousness and the rising demand for biodiesel, in which soybean oil serves as a key feedstock. As more industries recognize the versatility and profitability of soybean oil, both as a cooking ingredient and as an essential component in the biofuel industry, the market is expected to expand steadily over the forecast period of 2024 to 2032. Leading players such as Centra Foods, Bunge Limited, and Cargill, Incorporated are positioning themselves to capitalize on this growth by innovating and optimizing their production processes.

Market Outlook (2024-2032)

The outlook for the Canadian soybean oil market is highly positive. With an increasing number of health-conscious consumers and the government’s push toward renewable energy solutions, particularly biodiesel, the market is expected to see significant growth. Soybean oil, being one of the most widely used vegetable oils in Canada, plays a crucial role in various sectors, including food production, cosmetics, and renewable energy. With the rising awareness around the health benefits of soybean oil, which is low in saturated fats and high in polyunsaturated fats, its demand as a healthier cooking option is also on the rise.

Simultaneously, the use of soybean oil as a feedstock for biodiesel has gained traction due to its environmental benefits and cost-effectiveness. As Canada pushes for cleaner energy alternatives and reduced greenhouse gas emissions, soybean oil’s role in biodiesel production is set to expand further.

Report Overview

This report provides a detailed analysis of the Canadian soybean oil market, highlighting market size, key drivers, challenges, segmentation, and the latest developments. The report also offers insights into the industry’s major players and emerging trends. The analysis focuses on how market dynamics are evolving and what growth opportunities lie ahead for stakeholders.

Market Size

2020 Market Volume: 330 thousand MT

2032 Forecasted Market Value: The market is expected to grow steadily due to the increasing demand for health-conscious food options and biodiesel production, although exact projections in MT are yet to be finalized.

The growth of the Canadian soybean oil market is expected to be fueled by both increased domestic consumption and growing exports of biodiesel and soybean-based products.

Market Dynamics

Market Drivers

Rising Health-Conscious Consumers: Soybean oil is widely recognized for its health benefits, such as being low in saturated fat and high in essential fatty acids like omega-3s. As more Canadians prioritize healthier lifestyles and dietary choices, the demand for soybean oil as a cooking and salad oil is increasing.

Biodiesel Demand: Soybean oil’s use as a feedstock for biodiesel production has gained significant momentum due to the Canadian government’s focus on reducing carbon emissions and promoting renewable energy. Biodiesel made from soybean oil is a cleaner-burning alternative to fossil fuels, and its production supports the agricultural sector.

Growing Food Industry: The food industry is one of the primary consumers of soybean oil. The rising demand for processed and packaged foods, coupled with the increasing trend toward plant-based diets, is boosting the use of soybean oil in food production.

Export Potential: Canada’s robust agricultural sector has allowed it to become a major exporter of soybean products. The growing global demand for plant-based oils, both for food and fuel, presents significant export opportunities for Canadian soybean oil producers.

Key Market Challenges

Volatility in Soybean Prices: Soybean prices are subject to fluctuations due to weather conditions, trade policies, and global supply chain disruptions. These price changes can affect the profitability of soybean oil production.

Competition from Other Vegetable Oils: Soybean oil faces stiff competition from other oils like canola, sunflower, and palm oil, which may be preferred in certain regions for their price or specific culinary properties.

Environmental Concerns: While biodiesel from soybean oil is a cleaner energy alternative, concerns around the environmental impact of large-scale soybean cultivation, such as deforestation and water use, can pose challenges to the growth of this market.

Segmentation

The Canadian soybean oil market can be segmented based on application, end-user, and region.

By Application:

Food: Soybean oil is extensively used in food processing, baking, frying, and as a salad oil. It is a staple in households and restaurants due to its neutral flavor and health benefits.

Industrial: Beyond the kitchen, soybean oil finds applications in various industries, including cosmetics and pharmaceuticals, where it is used as a base for ointments, creams, and other personal care products.

Biodiesel: A significant portion of soybean oil is used in the production of biodiesel, contributing to the renewable energy sector.

By End-User:

Household Consumption: Soybean oil is a popular choice in Canadian households for everyday cooking and frying due to its nutritional benefits.

Commercial and Industrial: The commercial food industry and biodiesel production facilities are key end-users, with large volumes of soybean oil being used in food processing, manufacturing, and fuel production.

Recent Developments

Sustainability Initiatives: Leading companies in the market, such as Bunge Limited and Cargill, are focusing on sustainable sourcing of soybeans. These initiatives include partnerships with farmers to promote sustainable agricultural practices that reduce environmental impact.

Technological Advancements in Biodiesel Production: Recent advancements in biodiesel production technology have made the process more efficient and cost-effective. Companies are increasingly investing in research and development to improve biodiesel yields from soybean oil.

Plant-Based Food Growth: The rise in plant-based diets and products, such as soy-based meat alternatives, is driving demand for soybean oil as an ingredient. This trend is expected to continue, supporting growth in the food application segment.

Component Insights

Soybean Oil as Feedstock for Biodiesel: The use of soybean oil as a key component in biodiesel production is gaining traction due to its lower environmental impact compared to traditional fuels. The Canadian government’s push for renewable energy sources is encouraging the growth of this market segment.

Food Application: In the food sector, soybean oil is favored for its versatility, neutral taste, and health benefits. Its use in cooking, frying, and salad dressings continues to grow, driven by consumer demand for healthier oils.

End-User Insights

Households: Soybean oil’s popularity in Canadian kitchens is growing as more consumers seek healthier cooking options that are low in saturated fats. Its affordability and availability make it a preferred choice for everyday use.

Commercial Food Processing: The commercial food industry relies heavily on soybean oil for processing and manufacturing a wide range of food products. Its use is particularly high in frying oils and snack food production.

Biodiesel Producers: Biodiesel production is one of the fastest-growing applications for soybean oil. As governments and industries move toward cleaner energy solutions, the demand for soybean oil in biodiesel production is set to increase.

Regional Insights

Ontario and Quebec: These provinces are major producers of soybean oil in Canada due to their strong agricultural sectors. They are also key consumers, driven by large populations and industrial activities in food processing and biodiesel production.

Western Canada: With vast agricultural lands, Western Canada plays a growing role in soybean production and processing, providing opportunities for expansion in both domestic and export markets.

Key Players

Centra Foods: Specializes in providing bulk soybean oil for the foodservice and food processing industries.

Bunge Limited: A global leader in agribusiness, Bunge is heavily involved in the production of soybean oil and its use in biodiesel.

Cargill, Incorporated: Cargill provides a wide range of agricultural products, including soybean oil, with a focus on sustainability and innovation.

Archer Daniels Midland Company (ADM): ADM is a major player in the processing and distribution of soybean oil, with a strong presence in Canada.

Viterra Inc.: A leading agricultural network, Viterra supports the soybean oil market through its extensive supply chain and processing capabilities.

Key Market Trends

Health-Focused Consumer Preferences: Increasing awareness of the health benefits of soybean oil is driving consumer demand for healthier cooking oils.

Sustainability in Agriculture: Companies are focusing on sustainable soybean cultivation practices to meet both environmental standards and consumer expectations for eco-friendly products.

Rising Biodiesel Production: The demand for soybean oil in biodiesel production is growing rapidly, supported by government policies encouraging the use of renewable energy.

6 FAQs

What is driving the growth of the Canada soybean oil market? The market is driven by increasing consumer health consciousness, demand for biodiesel, and the growing food processing industry.

What is the expected market size by 2032? While the market volume was 330 thousand MT in 2020, it is expected to grow significantly, driven by demand for healthier cooking oils and renewable energy.

Who are the major players in the soybean oil market? Key players include Centra Foods, Bunge Limited, Cargill, Inc., Archer Daniels Midland Company (ADM), and Viterra Inc.

Which sectors are driving demand for soybean oil? The food processing, biodiesel production, and household cooking sectors are the primary drivers of demand.

What challenges does the soybean oil market face? Key challenges include price volatility of soybeans and competition from other vegetable oils.

What are the key trends in the market? Trends include the rising demand for plant-based foods, increased use of soybean oil in biodiesel, and a focus on sustainable agriculture.

0 notes

Text

Nutritious and Chemical Free Oil | Swasthaessentials

In recent years, the demand for healthy and organic products has surged, as more individuals become aware of the benefits of choosing natural over processed. In Rajasthan, one brand stands out in the pursuit of health-conscious consumers: Swasthaessentials. Specializing in nutritious and chemical-free oils, Swasthaessentials is committed to promoting well-being and sustainability.

The Importance of Choosing the Right Oil

Cooking oils play a crucial role in our diets, providing essential fats and nutrients. However, many commercially available oils are refined and laden with chemicals, which can detract from their nutritional value. Swasthaessentials takes a different approach, offering oils that are not only pure but also rich in essential fatty acids, vitamins, and antioxidants.

What Sets Swasthaessentials Apart?

Chemical-Free Production: Swasthaessentials sources its oils from organically grown seeds, ensuring that no harmful pesticides or synthetic fertilizers are used. This commitment to purity means that their oils are free from harmful chemicals, making them a healthier choice for consumers.

Cold-Pressed Techniques: Utilizing traditional cold-pressing methods, Swasthaessentials preserves the natural flavors and nutrients of the oils. This process ensures that the oils retain their health benefits, providing a superior alternative to heavily processed oils.

Variety of Oils: From mustard and sesame to almond and coconut oil, Swasthaessentials offers a diverse range of oils tailored to various culinary needs and health preferences. Each oil is selected for its unique nutritional profile and potential health benefits.

Local Sourcing: By sourcing ingredients locally, Swasthaessentials supports Rajasthan’s farmers and promotes sustainable agriculture. This not only helps the local economy but also reduces the carbon footprint associated with transporting goods over long distances.

Health Benefits of Nutritious Oils

Choosing chemical-free oils from Swasthaessentials can have numerous health benefits:

Heart Health: Oils like mustard and olive are rich in unsaturated fats, which can help lower cholesterol levels and reduce the risk of heart disease.

Anti-Inflammatory Properties: Many oils contain antioxidants and anti-inflammatory compounds that can help combat chronic inflammation and promote overall health.

Skin and Hair Care: Oils such as almond and coconut are renowned for their moisturizing properties, making them excellent choices for skincare and haircare routines.

Supporting a Sustainable Future

By choosing Swasthaessentials, consumers are not just making a healthier choice for themselves but are also contributing to a more sustainable future. The brand’s dedication to organic farming and eco-friendly practices aligns with the growing global movement towards sustainable living.

Contact Us Today!

🌐 : https://swasthaessentials.com/

☎: +91 7793814774

🏡: Opp. Tulsi Niketan School, Kumbha Nagar, Hiran Magri,Sector-4, Udaipur (Raj.) – 313002

Conclusion

In a world increasingly dominated by processed foods, Swasthaessentials offers a refreshing alternative with its range of nutritious, chemical-free oils. By prioritizing health, sustainability, and local sourcing, this Rajasthan-based brand is setting a standard for quality and integrity in the food industry. Embrace the goodness of nature and elevate your culinary experience with Swasthaessentials—where health meets tradition.

0 notes

Text

TIMING RIGHT FOR MALAYSIA TO INTRODUCE USED COOKING OIL FUTURES KUALA LUMPUR, Oct 15 (Bernama) -- It is the perfect time to introduce used cooking oil (UCO) futures in light of the growing emphasis on sustainability in the palm oil industry, according to an industry expert. IcebergX Sdn Bhd senior proprietary trader David Ng told Bernama that Malaysia’s UCO industry could play an important role in Sustainable Aviation Fuel (SAF) gaining popularity. In Malaysia, an estimated 540,000 tonnes of waste cooking oil (WCO) from vegetables, mainly palm and animal fats, are discarded yearly without being treated. WCO is recognised as a raw material for the biodiesel process and has great potential. “We are slowly seeing wide adoption of UCO as part of biofuel blending requirements. “Biodiesel blending mandates will greatly influence the UCO market; prices and supply of feedstock, in this case, crude palm oil (CPO), will also determine the availability of UCO in the market,” Ng said. Malaysia is implementing B20 mandates for the transport sector in certain regions, with the idea of preparing the entire supply chain for B30 to promote renewable energy use, reduce greenhouse gas emissions, and support the local palm oil industry. Therefore, Ng believes higher biodiesel demand will create greater demand for UCO, pushing UCO prices higher. “The main price drivers are crude oil and feedstock prices, such as the price of CPO. “A high oil price environment will greatly incentivise producers to blend more UCO with crude mineral oil. Government policies or mandates for biofuel programs will also be another major price driver,” he stated when asked about factors that could influence UCO futures pricing. Malaysia, among the main producers of CPO, serves as a benchmark for pricing, playing a crucial role in the global palm oil market. Its pricing influences international markets and sets standards for trade in palm oil products. In 2023, Malaysia produced 18.55 million tonnes of CPO, an increase from 18.42 million tonnes in the previous year. Bursa Malaysia recently confirmed its plan to introduce a new futures contract for used cooking oil, pending industry consultation and regulatory approval. The move was driven by increasing demand for biofuel feedstock.

0 notes

Text

Biodiesel Market Trends and Projections for Future Growth 2024 - 2032

The biodiesel market is experiencing robust growth as the world increasingly shifts towards renewable energy sources and sustainable practices. Biodiesel, a renewable alternative to traditional diesel, is derived from organic materials such as vegetable oils and animal fats. This article explores the current state of the biodiesel market, its key drivers, challenges, and future trends.

Introduction to Biodiesel

Biodiesel is a biodegradable fuel made through the transesterification process, which converts fats and oils into fatty acid methyl esters (FAME). It can be used in diesel engines with little or no modification, making it a versatile and environmentally friendly alternative to petroleum-based diesel. As governments and industries aim to reduce greenhouse gas emissions and reliance on fossil fuels, biodiesel has emerged as a viable solution.

How Biodiesel is Produced

Biodiesel production involves several key steps:

1. Feedstock Selection

Biodiesel can be produced from various feedstocks, including:

Vegetable Oils: Soybean, canola, palm, and sunflower oils are commonly used.

Animal Fats: Tallow and poultry fat are viable sources.

Used Cooking Oils: Recycling waste oils contributes to sustainability.

2. Transesterification Process

The selected feedstock undergoes a chemical reaction with an alcohol (usually methanol) in the presence of a catalyst. This process separates the glycerin from the fats or oils, resulting in biodiesel and glycerin as by-products.

3. Purification

The crude biodiesel is purified to remove impurities and residual catalysts, resulting in a final product that meets quality standards, such as ASTM D6751 in the U.S. and EN 14214 in Europe.

Market Overview

Current Market Size and Growth

The global biodiesel market has seen significant expansion in recent years. Increased awareness of environmental issues, rising fossil fuel prices, and government incentives for renewable energy sources are driving this growth. Analysts project that the market will continue to expand, with a compound annual growth rate (CAGR) of around 6-8% over the next several years.

Key Segments of the Market

By Feedstock

Vegetable Oils: Dominating the market due to high availability and established production processes.

Animal Fats: Gaining traction as a sustainable feedstock.

Waste Oils: Increasingly important for sustainability and cost-effectiveness.

By Application

Transportation: The largest segment, where biodiesel is used as a direct substitute or blended with petroleum diesel.

Power Generation: Utilized in stationary engines and generators.

Industrial Applications: Employed in various industrial processes and as a lubricant.

By Geography

North America: Leading the market, driven by favorable government policies and growing demand for renewable energy.

Europe: Strong focus on sustainability and strict regulations promoting biodiesel use.

Asia-Pacific: Rapid growth due to increasing energy needs and investments in renewable technologies.

Market Drivers

Growing Demand for Renewable Energy

As the global focus shifts towards sustainable energy sources, the demand for biodiesel is increasing. It plays a crucial role in reducing greenhouse gas emissions and enhancing energy security.

Government Initiatives and Incentives

Many governments worldwide are implementing policies and incentives to promote biodiesel production and use. These include tax credits, blending mandates, and subsidies that encourage the adoption of renewable fuels.

Technological Advancements

Continuous innovations in biodiesel production technologies are improving efficiency and reducing costs. Advances in feedstock processing and refining techniques are enabling higher yields and better-quality biodiesel.

Challenges Facing the Market

Feedstock Availability and Prices

The availability and prices of feedstocks can be volatile, influenced by agricultural production, climate conditions, and market demand. This can impact biodiesel production costs and profitability.

Competition from Other Renewable Fuels

The biodiesel market faces competition from other renewable fuels, such as ethanol and renewable diesel. These alternatives may appeal to certain sectors or applications, posing challenges for biodiesel adoption.

Regulatory Challenges

Navigating the complex regulatory landscape can be challenging for biodiesel producers. Compliance with quality standards, environmental regulations, and safety requirements can add to operational costs.

Future Outlook

Increasing Adoption of Advanced Biodiesel Technologies

The future of the biodiesel market lies in the development of advanced production technologies, such as second and third-generation biodiesel from non-food feedstocks (e.g., algae, waste oils). These technologies promise to enhance sustainability and reduce competition with food crops.

Expansion in Emerging Markets