#GAAP vs. IFRS

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

In February 2021, Tumblr had 518.6 million blog accounts.

Text

#International Financial Reporting#GAAP vs. IFRS#Corporate Financial Reporting#Accounting Best Practices#job skills#workplace skills#Financial Reporting Standards#GAAP#IFRS#Indian Accounting Standards

0 notes

Text

The Hidden Power of Accrual: Why It’s the Unsung Hero of Good Accounting

If you’ve ever peeked into the world of accounting, chances are you’ve heard the word “accrual” thrown around. Maybe it sounded complicated, overly technical, or like something only big corporations worry about. But here’s the thing: accruals aren’t just accounting jargon. They’re actually one of the most important tools for making sure your financial records truly reflect the reality of your…

View On WordPress

#accounting period#accounting principles#accounting software#accrual#accrual accounting#accrued expenses#accrued revenue#adjusting journal entries#bookkeeping#business decision-making#business expenses#cash basis vs accrual basis#deferred revenue#earned income#economic reality#end-of-period adjustments#estimated expenses#financial accuracy#Financial Management#financial reporting#financial statements#GAAP#IFRS#importance of accruals#Invoicing#matching principle#prepaid expenses#real-time accounting#revenue recognition#small business accounting

0 notes

Text

Accounting Dissertation Help with Research-Ready Topics for 2025

Writing a dissertation can be a daunting task, especially in a specialized field like accounting. The need to select the right topic, follow academic standards, conduct credible research, and maintain clarity throughout the document makes the entire process quite demanding. For students aiming to craft a strong dissertation in 2025, seeking proper Dissertation Help becomes a strategic step toward academic success.

This article offers comprehensive insight into how students can approach their accounting dissertations effectively. It also includes a curated list of research-ready topics that are relevant and impactful for the upcoming academic year.

Why Is Dissertation Help Important in Accounting?

Accounting is more than just numbers. It’s a combination of finance, analytics, law, strategy, and ethics. This complexity often makes it challenging to choose the right research focus and develop a coherent, evidence-based dissertation. Here’s why dissertation help is particularly valuable in this field:

Expert guidance ensures proper structure, methodology, and academic tone.

Topic validation helps in identifying areas with available data and future research potential.

Literature review support provides access to scholarly sources and peer-reviewed material.

Formatting and referencing help maintain compliance with APA, MLA, or other academic styles.

By taking advantage of professional support, students can focus on analysis and creativity rather than formatting and structure.

How to Choose the Right Accounting Dissertation Topic

Choosing a dissertation topic is the foundation of the entire project. A good topic should be:

Relevant to current trends

Feasible with available resources

Aligned with your academic goals

Interesting enough to sustain motivation

Students are encouraged to explore real-world issues and emerging areas in the accounting field. Avoid overly broad or excessively niche topics unless you have deep knowledge and access to resources.

Top Accounting Dissertation Topics for 2025

To help you get started, here’s a list of research-ready topics that align with current industry developments and academic interests:

1. The Impact of ESG (Environmental, Social, Governance) Reporting on Corporate Financial Performance

Explore how non-financial reporting is influencing investment decisions and overall company performance.

2. Blockchain Technology in Accounting: Disruption or Enhancement?

Examine the integration of blockchain into accounting systems and its implications on auditing, transparency, and fraud detection.

3. Forensic Accounting and Financial Fraud Detection in the Digital Age

Focus on how forensic accountants are evolving their methods to keep up with cybercrimes and digital manipulation.

4. The Influence of Artificial Intelligence on Financial Auditing

Analyze the pros and cons of using AI tools for internal audits and risk management.

5. The Role of Behavioral Accounting in Budgeting and Forecasting

Investigate how cognitive biases and human behavior influence financial planning in organizations.

6. Comparative Study: IFRS vs. GAAP in Cross-Border Accounting Practices

Assess the difficulties and advantages companies face when transitioning between these two accounting standards.

7. Sustainability Accounting and Its Role in Corporate Strategy

Evaluate how sustainability reporting is becoming a core element of business strategy and performance evaluation.

8. The Effectiveness of Tax Avoidance Strategies in Multinational Corporations

Discuss the ethical, legal, and financial dimensions of tax planning techniques.

9. Audit Quality and Auditor Independence in Listed Companies

Study the balance between maintaining long-term client relationships and ensuring audit quality.

10. The Future of Cloud-Based Accounting: Security Risks and Advantages

Explore how cloud technology is transforming accounting processes and the risks it poses for data security.

What Makes an Accounting Dissertation Successful?

Beyond topic selection, your dissertation needs to meet certain academic expectations to stand out:

1. Clear Research Objectives

Start with well-defined goals. What are you trying to discover, prove, or analyze? Having precise research questions helps streamline your investigation.

2. Strong Literature Review

This section demonstrates your understanding of the existing body of knowledge. Focus on scholarly journals, government reports, and recent publications to give your work a solid foundation.

3. Appropriate Methodology

Choose a methodology that suits your topic — whether qualitative, quantitative, or mixed methods. Explain your data collection process, sample size, and analysis techniques clearly.

4. Data Analysis and Interpretation

Use tools like SPSS, Excel, or R to process your data. More importantly, interpret the results in light of your research questions and objectives.

5. Critical Thinking

Show your ability to analyze problems from multiple perspectives. Do not merely describe findings; evaluate their implications and limitations.

Common Challenges Students Face

While help is available, many students still face difficulties such as:

Time constraints

Poor topic alignment

Limited access to scholarly sources

Unclear academic guidelines

These issues can delay progress or compromise the quality of the final dissertation. Seeking dissertation help early can prevent such setbacks and keep your academic journey on track.

Conclusion

Writing a dissertation in accounting is a significant academic milestone. With proper planning, topic selection, and the right dissertation help, students can navigate this challenge successfully. As 2025 brings new trends and technological advancements in finance and auditing, students have exciting opportunities to explore fresh perspectives and contribute meaningful research to the field.

Choosing a relevant, research-ready topic and following academic standards is the key to a well-crafted dissertation. Whether you’re a final-year undergraduate or a postgraduate student, now is the perfect time to start preparing your accounting dissertation with confidence and clarity.

FAQs about Dissertation Help in Accounting

Q1. What is the ideal length of an accounting dissertation? Most dissertations are between 10,000 to 15,000 words. However, the requirement may vary by institution.

Q2. Can I change my topic after submitting my proposal? Yes, but you may need approval from your supervisor, especially if the new topic significantly changes your research direction.

Q3. Do I need to use primary data for my dissertation? Not necessarily. Secondary data analysis is also acceptable, depending on your topic and methodology.

Q4. How important is referencing in a dissertation? Very important. Accurate referencing demonstrates academic integrity and helps avoid plagiarism.

Q5. When should I start writing my dissertation? Start early — ideally right after your proposal is approved. Allocate time for research, writing, revisions, and proofreading.

1 note

·

View note

Text

How Finance Leaders Future-Proof Operations with SAP + Outsourcing

In 2025, the role of finance leaders has evolved beyond managing budgets and reviewing reports. Today’s CFOs and financial controllers are expected to drive strategy, manage risk, ensure compliance, and lead digital transformation — all while keeping operations lean and efficient.

To meet these growing demands, many finance leaders are embracing a powerful combination: SAP + outsourced bookkeeping. Together, they’re creating a scalable, future-ready finance function that helps businesses grow smarter — not just faster.

Here’s how this approach is helping finance leaders build resilient, high-performing operations.

The Pressure on Modern Finance Teams

The financial landscape is more complex than ever. Businesses now face challenges like:

Global expansion and multi-currency transactions

Evolving regulatory and compliance requirements

Increased demand for real-time financial data

Rising costs of in-house talent and technology

Higher expectations from investors and stakeholders

These challenges demand more than just a basic bookkeeping setup — they require a strategic, technology-enabled solution that can scale with the business. That’s where SAP-driven outsourced bookkeeping comes in.

What Is SAP + Outsourcing?

SAP is one of the world’s most trusted ERP (Enterprise Resource Planning) platforms. It automates and integrates critical business functions like accounting, payroll, inventory, CRM, and reporting.

Outsourced bookkeeping, meanwhile, involves partnering with a third-party provider to manage daily financial tasks such as:

Transaction recording

Invoicing and billing

Bank reconciliations

Financial reporting

Compliance support

When finance leaders combine SAP’s power with outsourced expertise, they create a finance infrastructure that’s built for long-term growth and agility.

Key Benefits for Finance Leaders

1. Real-Time Financial Visibility

One of SAP’s biggest advantages is real-time access to financial data. Dashboards and live reporting features allow finance leaders to track:

Cash flow

Profitability

Expenses

Budget vs. actuals

Instead of waiting for end-of-month reports, CFOs and decision-makers can now act on insights instantly — reducing delays and improving responsiveness.

2. Scalable and Flexible Operations

As businesses grow, their finance operations often become more complex. SAP’s robust infrastructure supports:

Multi-entity and multi-currency accounting

Global compliance frameworks

Integration with CRMs, HR, and supply chain systems

Outsourcing partners with SAP expertise can scale services as needed — whether your business is entering a new market or acquiring a new company. Finance leaders get the flexibility to grow without friction.

3. Cost Optimization

Hiring and retaining skilled finance professionals — especially those with SAP experience — can be expensive. Outsourcing offers a cost-effective alternative, giving companies access to expert support without the overhead.

Plus, SAP’s automation capabilities reduce the need for manual data entry and redundant processes, freeing up resources for higher-value strategic work.

4. Improved Accuracy and Compliance

SAP is built to support international accounting standards like GAAP and IFRS. Its automation features help eliminate human error, ensure consistent data entry, and keep audit trails intact.

Combined with a knowledgeable outsourced bookkeeping team, finance leaders can confidently meet deadlines, stay compliant, and be always audit-ready.

5. Faster Reporting and Decision-Making

Time-consuming manual reports are a thing of the past. SAP generates financial statements, forecasts, and analytics on demand. Your outsourced team maintains these reports and customizes them based on your business needs.

For finance leaders, this means faster decision-making, stronger forecasting, and data-backed strategic planning.

6. Focus on Core Strategy

Outsourcing allows internal finance teams to move away from repetitive tasks and focus on:

Financial planning and analysis (FP&A)

Risk management

Growth strategy

Investment planning

By offloading operational bookkeeping to SAP-powered experts, finance leaders can redirect their time and energy to initiatives that drive business success.

A Future-Ready Finance Stack

In 2025 and beyond, finance is no longer just about keeping the books clean — it’s about building a resilient, adaptable, and insight-driven operation. SAP offers the technology backbone, while outsourcing delivers the flexibility and expertise.

When combined, they enable finance leaders to:

Adapt quickly to market changes

Maintain financial health during rapid growth

Support complex business models with ease

Stay compliant across global markets

Final Thoughts

Finance leaders who embrace SAP + outsourcing are taking proactive steps to future-proof their operations. This modern model reduces costs, enhances visibility, improves compliance, and sets the foundation for long-term, sustainable growth.

If you’re still relying on outdated systems or siloed teams, now is the time to evolve. With the right outsourcing partner and SAP infrastructure in place, your finance function can move from reactive to strategic — and lead the way forward.

0 notes

Text

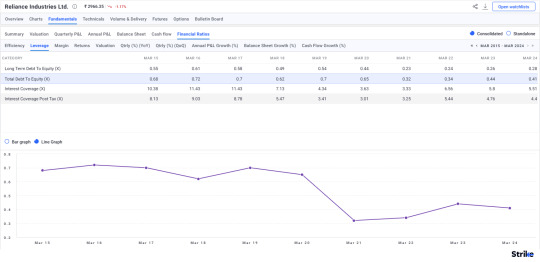

✅ Complete Guide to Debt to Equity Ratio: What It Means and Why It Could Make or Break a Company

Understanding a company’s financial health isn't just for seasoned investors. One of the most telling indicators is the Debt to Equity Ratio (D/E) — a powerful gauge of how a company finances its operations. Whether you're analyzing Tata Motors, investing in Infosys, or reviewing your own startup’s balance sheet, this ratio helps you see the financial risk clearly.

Let’s break it all down — no jargon, no fluff, and all with insights from both global principles and the Indian stock market 🧾

📊 What Exactly Is the Debt to Equity Ratio?

In simple words, the Debt to Equity Ratio shows how much debt a company uses to finance its assets relative to shareholder equity. It’s a measure of financial leverage — and tells you whether a company is overburdened with debt or conservatively managed.

🔍 Formula: D/E Ratio = Total Liabilities / Shareholder's Equity

For instance, if a company has ₹100 crore in debt and ₹50 crore in equity, the D/E ratio is 2. This means the company is using ₹2 of debt for every ₹1 of equity.

🏛 Recognized by financial bodies like FASB, SEC, and aligned with accounting principles such as GAAP and IFRS, this ratio is central to evaluating corporate solvency.

🚨 Why the Debt to Equity Ratio Isn’t Just a Number

The D/E ratio isn’t just about math — it reveals business philosophy, risk appetite, and even future performance potential.

✅ Low D/E Ratio: Indicates conservative financing, lower risk. Often seen in tech and IT firms like Infosys, which had a D/E ratio of nearly 0.02 in FY24, showing minimal reliance on debt.

⚠️ High D/E Ratio: May suggest aggressive growth, risk-taking, or financial stress. Companies like Tata Motors or Vedanta have historically shown higher D/E ratios due to capital-intensive operations.

🧠 Even legendary investors like Warren Buffett and Benjamin Graham emphasized examining leverage before investing in any stock.

📘 Here’s How to Calculate Debt to Equity Ratio Using a Balance Sheet

Let’s say you’re analyzing a company’s financials on Strike Money, a powerful charting tool tailored for Indian traders. You navigate to the balance sheet tab.

➡️ Look under Liabilities: Add both long-term and short-term borrowings. ➡️ Under Equity: Take shareholder’s funds, retained earnings, and reserves.

Plug into the formula and voilà — you’ve got the D/E ratio 💡

Using Strike Money, you can also plot historical trends to see how a company’s financial structure evolves over time — a great way to predict future moves 📈

📍 So, What’s a "Good" Debt to Equity Ratio in India?

There’s no universal “perfect” number — it depends on the industry and business model.

🏗️ Infrastructure/Manufacturing (e.g., L&T): D/E of 1.5 to 2 is considered normal 💻 IT Services (e.g., TCS, Wipro): D/E below 0.2 is ideal 🏦 Banking & Finance (e.g., HDFC, ICICI): D/E often above 5, but that’s typical due to their nature of operations

🎯 A 2023 report by CRISIL highlighted that Indian listed companies, on average, maintained a D/E ratio of 0.9 post-COVID, as they became cautious about debt due to interest rate hikes and global volatility.

🧪 Real Examples from Indian Companies You Know

🎯 Tata Motors: As of FY24, Tata Motors had a D/E ratio of 2.04, reflecting its high capital expenditure in EV and international ventures.

🧘 Infosys: Maintains a near-zero debt policy. Its D/E ratio has stayed under 0.05 for over a decade, making it a darling of conservative investors.

📦 Zomato: The food delivery player had a D/E ratio close to 0.12 in FY24 — thanks to equity-heavy funding rounds during its startup phase and IPO.

💡 If you’re investing or analyzing these companies, the D/E ratio gives insight into whether they’re managing growth or gambling on it.

🔍 High vs Low D/E Ratio: What Should You Really Worry About?

🟥 High Debt to Equity Ratio Risks: ⚠️ Higher interest payments → Pressure on profit margins ⚠️ Vulnerability to interest rate hikes → As seen post-2022 RBI hikes ⚠️ Lower credit ratings → Higher cost of future borrowing ⚠️ Potential for default → Especially in economic downturns (e.g., IL&FS Crisis in India)

🟩 Low D/E Ratio Pros: ✅ Stability → Attractive to long-term investors ✅ Better borrowing power when needed ✅ Stronger balance sheet in recession periods

But beware: too low a D/E ratio might also suggest under-utilization of available capital — which can be a red flag for growth investors 🚩

🔄 Debt vs Equity Financing: Which Makes Sense for Businesses?

When raising capital, companies often choose between debt and equity. Each has pros and cons.

💸 Debt Financing 🔹 No loss of ownership 🔹 Interest is tax-deductible 🔹 But comes with repayment obligation

📊 Equity Financing 🔹 No repayment burden 🔹 More flexibility 🔹 But dilutes ownership and control

In 2024, a survey by NASSCOM found that over 68% of Indian startups preferred equity over debt, citing investor interest and lower short-term liability.

However, traditional giants like Reliance Industries use a blend — borrowing strategically while also raising funds through rights issues or bonds.

🧠 What Top Investors and Analysts Say About Leverage

🔮 Warren Buffett: "If you’re smart, you don’t need leverage. If you’re dumb, it’ll ruin you.”

📖 Benjamin Graham, in The Intelligent Investor, advised always checking how a company funds growth — D/E ratio being key.

📉 In the 2008 Global Financial Crisis, over-leveraged firms collapsed like dominoes. Indian companies with high debt, such as Kingfisher Airlines, also failed spectacularly.

Knowing how much debt is "too much" is more important than ever in a volatile global economy.

💡 How to Use Strike Money to Analyze D/E Ratio Like a Pro

🛠️ Strike Money, a rising favorite among Indian retail investors, lets you: 🔍 Search by stock name and access financial ratios in seconds 📉 Visualize D/E ratio trends across years 🔔 Set alerts for sudden spikes in leverage

If you’re managing a portfolio or just analyzing a stock pre-earnings, Strike Money gives you the insight edge — fast, reliable, and visually intuitive.

🔎 When Should You Worry About the D/E Ratio?

📌 You should raise an eyebrow if: ❗ The D/E ratio suddenly doubles YoY ❗ It exceeds industry average by over 50% ❗ There's declining earnings alongside rising debt ❗ Interest coverage ratio is below 2

In these cases, it's time to dig deeper into financial statements, cash flows, and management commentary. Sometimes, the D/E ratio is a symptom of a deeper issue, not just a cause.

📚 Expert Resources to Dive Deeper

✅ Bloomberg and Morningstar: For ratio trends ✅ SEBI filings: To view detailed debt instruments ✅ RBI Bulletins: For macro insights on borrowing ✅ Company Investor Relations (IR) pages: For D/E breakdowns ✅ Strike Money: Best for real-time Indian market data and charts

According to a McKinsey 2023 study, companies with optimized capital structures (balanced D/E ratios) showed 20–30% higher valuation multiples than over-leveraged peers.

❓ FAQ: What Investors Ask About Debt to Equity Ratio

❓ What is a healthy debt to equity ratio? 👉 Between 0.5 and 1 is generally healthy. But it depends on industry norms.

❓ Can a D/E ratio be negative? 👉 Yes, if equity is negative — usually a big red flag 🚩

❓ How often should I check a company’s D/E ratio? 👉 Quarterly, or during major capital raising events

❓ Is high D/E always bad? 👉 Not necessarily. It can mean aggressive expansion — but needs strong earnings to back it up

❓ What’s the difference between debt ratio and D/E ratio? 👉 Debt ratio = Total Debt / Total Assets 👉 D/E = Total Debt / Shareholder Equity

🏁 Final Thoughts: Make D/E Ratio Part of Every Financial Check

Understanding the Debt to Equity Ratio isn’t just for accounting nerds — it’s an essential skill whether you’re an investor, a founder, or a finance student.

Before making any investment or strategic decision, ask: ➡️ How is this company funding its growth? ➡️ Is it leveraging wisely or borrowing blindly?

Keep tools like Strike Money in your pocket, and let the D/E ratio guide your financial radar.

0 notes

Text

Managerial Accounting and Control – Key Concepts

Financial vs. Managerial Accounting

Financial accounting and managerial accounting serve different purposes.

Users:

Financial accounting produces standardized reports (balance sheet, income statement, cash flows) for external users – investors, creditors, regulators – and follows GAAP/IFRS rules .

In contrast, managerial accounting provides detailed analyses to internal management to aid decisions .

Time focus:

Financial reports are wholly historical (past periods) , whereas managerial accounting uses historical data plus budgets and forecasts to look forward . Precision & Detail: Financial statements aggregate data into broad categories (e.g. total “Cost of Goods Sold”), while managerial reports drill down into products, segments, or activities with granular detail .

Regulation:

Financial accounting is highly regulated for public disclosure; managerial accounting is flexible and not bound by external standards . Common mistakes include treating managerial data as audited (it may involve estimates) or ignoring relevant internal details in financial reports.

Planning, Controlling, and Decision-Making Framework

Managerial accounting is built on three pillars:

Planning,

Controlling,

Decision-making .

In planning, managers set targets and budgets (sales forecasts, production schedules). In controlling, they compare actual performance to these targets and use variance analysis to identify issues. Decision-making uses cost analyses (e.g. break-even, make-or-buy) to choose among alternatives. For example, a sales budget drives production and labor plans; exceeding the sales target might trigger bonuses, while falling short can reduce compensation . Overall, this framework ensures efficient use of resources and aligns operations with strategy. (Common errors include not updating budgets when conditions change or ignoring both quantitative and qualitative decision factors.)

Cost Classifications: Direct vs Indirect; Fixed vs Variable vs Mixed

Costs are classified by traceability and behavior. Direct costs can be traced easily to a product or service (e.g. raw materials in a product, wages of assembly workers) . Indirect costs cannot be traced to one product (e.g. factory rent, electricity, supervisor salaries) and are usually allocated as overhead . By behavior, variable costs change in total with volume (e.g. shipping costs per unit, $1 per unit cups) , while fixed costs stay the same in total across the relevant range (e.g. $3,500 rent per month) . A mixed (semi-variable) cost has both parts (e.g. a utility bill with a fixed base fee plus usage charge) . Within the relevant range, total cost can be modeled as:

Total Cost = Fixed Cost + (Variable Cost per Unit × Number of Units)

Manufacturing vs. Non-manufacturing Costs

In manufacturing firms, manufacturing (product) costs include three categories:

Direct Materials: Raw materials that become part of the finished product (e.g. wood for furniture) .

Direct Labor: Labor costs of workers who physically make the product (e.g. machine operators) .

Manufacturing Overhead: All other factory costs (indirect materials, indirect labor, utilities, depreciation of equipment, factory insurance, etc.).

The sums of these are often grouped: Prime cost = DM + DL , Conversion cost = DL + MOH , and Total manufacturing cost = DM + DL + MOH . Non-manufacturing (period) costs include selling and administrative expenses. For example, marketing/advertising and sales staff salaries are selling costs, while executive pay and office utilities are administrative costs . These are not tied to production.

Product Costs vs. Period Costs

All costs are ultimately either product costs or period costs. Product costs are the manufacturing costs (DM, DL, MOH) that are inventoriable: they are capitalized on the balance sheet as inventory and expensed as Cost of Goods Sold when sold . For example, direct materials and factory overhead on a product become part of inventory. In contrast, period costs are non-manufacturing expenses that are expensed in the period incurred . These include SG&A like office rent, advertising, and CFO salary . In short: if a cost is related to making a product, it’s a product cost; otherwise it’s a period cost . A common error is mislabeling costs (e.g. treating office rent as product cost instead of period).

Managerial Perspectives

Managers use accounting within broader business contexts. Key perspectives include:

Ethics: Managerial accounting depends on trust and integrity. Ethical behavior is “the foundation of managerial accounting” – biased or falsified data render all analysis meaningless . Professional accountants follow codes (IMA/CIMA) that stress honesty, fairness, and responsibility . Always question whether data is complete and reported objectively.

Strategy: Accounting supports strategy by linking numbers to the company’s competitive plan. Strategy is a firm’s “game plan for attracting customers by distinguishing itself from competitors” . Cost reports help choose which products or segments to invest in. For instance, a low-cost producer strategy would emphasize activity-based costing to cut unnecessary overhead, while a differentiation strategy might allocate more to quality metrics.

Enterprise Risk Management (ERM): Managers identify and quantify risks (market, credit, operational) and plan responses. ERM is defined as “a process used by a company to identify its risks and develop responses to them to be assured of meeting its goals” . Relevant costs include potential losses, insurance, or contingency budgets. Accounting data is used to forecast how different risk scenarios affect profits.

Corporate Social Responsibility (CSR): Companies consider social, environmental, and stakeholder impacts. CSR means managers consider “the needs of all stakeholders when making decisions” . For example, waste disposal or carbon emissions may be tracked as part of costs (using full-cost or environmental costing methods). Non-financial metrics (customer satisfaction, community impact) complement financial reports in a CSR perspective.

Process Management: This involves streamlining business processes (like Lean). A business process is “a series of steps followed to carry out some task” . Managerial accounting measures costs and performance at each process step (e.g. cost per production line, cycle time). By analyzing process costs, managers can eliminate bottlenecks. For example, tracking cost per unit by process highlights inefficiencies.

Leadership: Beyond numbers, managerial accountants often advise and lead teams. Leadership skills help interpret data, communicate insights, and motivate employees toward goals. As one teaching note suggests, leadership skills allow managers to unite people and implement the firm’s strategy (e.g. fair compensation systems that reward performance) .

Each perspective guides what and how information is reported. For example, ethical issues remind managers to exclude sunk costs and report honestly; strategic context determines which segments matter most; ERM reminds us to include contingency costs; CSR adds measures beyond profit; process management focuses on continuous cost reduction; and leadership ensures the data drives action.

Cost Behavior Analysis and Relevant Range

Understanding cost behavior is crucial for forecasting. The relevant range is the normal operating span in which our cost assumptions hold . Within this range, fixed costs are fixed (in total) and variable costs scale linearly. For example, if a machine produces up to 1,000 units/day, costs (like depreciation or utilities) can be estimated reliably up to that point; beyond it, new costs (a second machine) would emerge, altering the cost function . Typical mistake: applying a fixed-cost assumption far outside the relevant range (e.g. assuming one factory rent covers 200% capacity).

The high-low method estimates mixed costs using only the highest- and lowest-activity data points . Steps: (1) Identify the periods with highest and lowest activity and note their total costs. (2) Compute the variable cost per unit as:

( Cost_high – Cost_low ) ÷ ( Activity_high – Activity_low )

For example, if maintenance cost was $1,060 at 1,460 units and $932 at 1,100 units, the variable cost/unit = (1,060–932)/(1,460–1,100) = $0.356 . (3) Calculate fixed cost by subtracting total variable cost from one of the totals. Using the high point: $1,060 – (1,460×0.356) = $540 fixed . (4) Write the cost formula: Total Cost = $540 + $0.356 × Units . Note this approximation uses only two points (ignoring the shape between), so it may be rough if data are erratic .

Differential, Opportunity, and Sunk Costs

When making decisions, not all costs are relevant.

Differential (Incremental) Cost: The difference in cost between two alternatives. E.g. if Option A costs $10,000 and B costs $8,000 annually, the differential cost of A vs. B is $2,000 . Similarly, differential revenue is the revenue difference. Decisions are based on comparing differential revenues and costs.

Opportunity Cost: The foregone benefit when one alternative is chosen over another. It isn’t recorded in accounting books but is crucial. For example, quitting a $25,000 job to return to school incurs an opportunity cost of $25,000 (the lost salary) . Every choice has one – e.g. using a machine for product A means losing whatever B it could have made. Managers should include opportunity costs as relevant (e.g. the rental income given up by using a building for production).

Sunk Cost: A cost already incurred and unchangeable by current decisions. For example, a machine bought years ago is now obsolete; its original purchase price cannot be recovered . Sunk costs should be excluded from decision analysis because they remain the same regardless of the choice . A common pitfall is letting sunk costs (like past R&D) influence new decisions; instead, focus on future costs and benefits.

In summary: use differential and opportunity costs in “what-if” analyses (they are relevant), but ignore sunk costs (they are irrelevant) .

Contribution Margin and Income Statement Formats

Contribution Margin (CM) is defined as Sales – Variable Costs .

It represents the amount available to cover fixed costs and contribute to profit. For example, if a product sells for $100 and has $40 of total variable cost (materials, labor, commissions), the contribution margin is $60 per unit . CM can be expressed in total, per unit, or as a ratio (% of sales) . It’s widely used for break-even and target-profit analysis (e.g. Break-even units = Total Fixed Costs ÷ CM per unit).

There are two common income statement formats: Traditional (absorption) and Contribution (variable costing). Both yield the same net income, but differ in presentation .

Traditional Income Statement: Used for external reporting. It first subtracts product (COGS) from sales to get Gross Profit, then subtracts period costs (selling & admin) to get net income. Expenses are grouped as product vs. period costs.

Contribution Income Statement: Used internally for decision-making. It first subtracts all variable costs from sales to get Total Contribution Margin, then subtracts total fixed costs to arrive at net income. Here expenses are classified by behavior (variable vs. fixed) .

Both statements reconcile to the same profit, but the contribution format highlights how volume affects profit. A typical mistake is misallocating fixed costs or failing to separate variable costs when preparing these statements, which can obscure break-even analysis.

#BUS346#Managerial Accounting & Control#Summer2025#accounting basics#cost accounting#mba#mba core#session notes#11 june 2025#financial VS managerial#cost classicication#cost behavior#planning#controlling#decision making#manufacturing costs#high low method#relevant range#sunk cost#opportunity cost#differential cost#erm#csr#leadership#ethics in accounting#accounting#budgeting#cost formulas

0 notes

Text

What distinguishes global accounting firms from local firms in Hyderabad?

When you’re searching for accounting firms in Hyderabad, you’ll quickly notice there’s a world of difference between the global giants and the local specialists. But what exactly sets them apart? Let’s break it down in a way that’s easy to digest, especially if you’re considering a service provider like Paysquare.

Global Reach vs. Local Expertise: The Big Divide

Global accounting firms in Hyderabad bring an international flavor to the table. They often cater to multinational corporations, offering services that span borders. Think exposure to international accounting standards like IFRS and US GAAP, and handling complex, cross-border financial transactions. Their teams are trained to navigate the intricacies of global compliance, risk consulting, and international tax structures. If your business has global ambitions or operations, these firms might seem like the obvious choice2.

On the flip side, local accounting firms in Hyderabad tend to focus on domestic clients. They’re deeply familiar with Indian tax laws, GST, and regulatory requirements. Their expertise is rooted in the local business environment, making them a great fit for homegrown startups and SMEs looking for hands-on, personalized service.

Why Paysquare Stands Out Among Accounting Firms in Hyderabad

Paysquare is a service provider that understands both sides of the coin. While many accounting firms in Hyderabad stick to either global or local strengths, Paysquare blends the best of both worlds. Here’s how:

Deep knowledge of Indian compliance and tax regulations

Personalized attention for each client, big or small

Ability to scale services as your business grows, whether you’re local or expanding globally

A team that stays updated with both domestic and international accounting practices

Choosing the Right Accounting Firms in Hyderabad: What Matters Most?

Do you need international expertise or a partner who knows the local market inside out?

Are you seeking a firm that can grow with your business?

Is personalized service a priority for you?

Paysquare ticks all these boxes, making it a standout among accounting firms in Hyderabad.

Conclusion

The choice between global and local accounting firms in Hyderabad comes down to your business needs. If you want a partner who offers the global perspective with a local touch, Paysquare is the name to remember. They bridge the gap, ensuring your business gets the best of both worlds—right here in Hyderabad.

0 notes

Text

Brand Equity vs. Brand Value: Key Differences and Why They Matter – A Valuation Perspective

.

In the context of valuation, brands often hold significant weightage—sometimes even more an physical assets. However, one common gap is the usage of the terms brand equity and brand value interchangeably. Brand Equity and Brand Value is essentially different from each other and carry unique implications in the context of valuation. Understanding these differences are pertinent for investors, analysts, brand custodians, and executives looking to maximize a company’s worth.

Understanding the Core Concepts

What is Brand Equity?

Brand equity refers to the perceived value of a brand in the eyes of consumers. It is nurtured gradually through impeccable product or service quality, emotional connect, superior customer experience, and consistent marketing. Even at a higher price, customers are more likely to pick a brand with strong Brand Equity than competitors. Key components of brand equity include:

Brand awareness

Perceived quality

Brand associations

Customer loyalty

Emotional connection

It is not recorded on a balance sheet unless acquired, but it has a profound effect on a company’s ability to generate sustainable revenue.

What is Brand Value?

Brand value, on the other hand, is the monetary worth of a brand. It answers the question: How much is this brand worth if we had to sell or license it today? It is a financial measure used in:

Mergers & acquisitions

Licensing deals

Financial reporting (especially under IFRS and GAAP)

Investor presentations

What is Brand Valuation?

Brand Valuation is the process of calculating the brand value. Typically used Brand Valuation Methods include:

Royalty Relief Method – Estimating how much a company would have to pay to license its own brand.

Excess Earnings Method – Calculating the profits attributable solely to the brand.

Cost-Based Method – Adding up the cost to build the brand (less commonly used).

Key Differences at a Glance

Aspect

Brand Equity

Brand Value

Definition

Perceived consumer value and emotional resonance

Financial valuation in currency terms

Nature

Qualitative and subjective

Quantitative and objective

Measurement

Surveys, brand tracking, loyalty scores

DCF models, royalty relief, or market comps

Use Case

Marketing strategy and customer engagement

M&A, licensing, financial reporting

Accounting Presence

Only when acquired (part of goodwill)

Recognized as intangible asset in valuations

Focus

Brand perception and customer behavior

Monetized impact of brand on cash flows

Why the Distinction Matters in Valuation

Equity Fuels Value: Brand equity is an input to brand value. Without strong brand equity, a brand’s financial worth declines. For instance, a brand like Apple or Nike commands high value because of decades of equity built through customer trust and emotional affinity.

Valuation Accuracy: During mergers or acquisitions, a misconception between brand equity and brand value can lead to underpricing or overvaluation. In order to value a brand with precision, analysts need to be aware of how brand equity influences projected cash flows, risk premiums, and growth rates.

Strategic Resource Allocation: Marketing and finance teams must collaborate. High brand equity suggests that increased investment in marketing may yield disproportionately higher returns. From a valuation perspective, this insight is critical when modeling future performance or allocating capital.

Licensing & Monetization: Brand value is crucial when a company seeks to license its brand or use it as collateral. For example, Coca-Cola’s ability to leverage its brand for licensing depends on a robust and well-defined Brand Valuation—not just on consumer affection.

Impairment and Reporting: Under accounting standards like IFRS 3 and ASC 805, brands acquired in business combinations are recorded at fair value. Understanding the gap between market sentiment (equity) and accounting estimates (value) is necessary for impairment testing and audit defensibility.

While brand equity is the strategic asset rooted in perception and loyalty, brand value is the financial outcome derived from that asset. One cannot exist sustainably without the other in a well-functioning business. For companies, aligning brand equity-building strategies with financial valuation frameworks creates not just stronger brands—but more valuable businesses.

Real-World Examples: How Equity and Value Play Out

Example 1: Apple Inc.

Apple has some of the highest brand equity globally, thanks to its superior product quality, strong customer loyalty, and a sleek design. Apple’s substantial recurring revenue streams are a result of its high equity, enabling it to retain clients effectively and charge premium rates.

In terms of brand value, Apple has been ranked as the most valuable brand globally across multiple studies, reflecting its positive future cash flows and a higher command of the market.

Example 2: Kraft Heinz’s Write-Down

In 2019, Kraft Heinz took a $15.4 billion write-down on the value of its Kraft and Oscar Mayer brands. This was a clear signal that the brand value had fallen dramatically—due to changing consumer preferences and reduced pricing power.

Although the brands still had some brand equity (recognition and familiarity), their ability to generate future earnings had declined. Hence, their accounting value as intangible assets needed to be adjusted down.

Conclusion

As intangible assets increasingly dominate corporate balance sheets, the ability to distinguish and measure both brand equity and brand value becomes a competitive advantage. From a valuation perspective, this distinction drives better decision-making, more accurate financial modeling, and ultimately, stronger investor confidence.

At ValAdvisor, a leading Valuation Services company in India, our dedicated team of experts specializes in determining the value of a business or assets, for transactions, accounting, taxation, regulatory, financing, distressed asset resolution, litigation, insurance, strategic, planning, and operational purposes. Our expertise in various advanced models and simulation techniques helps us in delivering reliable and accurate valuations. Rely on us to offer customized solutions empowering you to make well-informed decisions with assurance.

Frequently Asked Questions (FAQs)

Q) Can a brand have high equity but low value?

A brand might have strong emotional connections and recognition (high brand equity) but still lack profitability or monetization strategies, leading to low brand value. For example, a beloved nonprofit brand may have high equity but minimal Financial Value due to its limited revenue-generating potential.

Q) Is brand equity recorded on the balance sheet?

Brand equity is an intangible, perception-based asset and is not recorded on the balance sheet unless the brand is acquired. In such cases, it is included within goodwill or separately valued as an intangible asset during a purchase price allocation.

Q) Why is brand value important in mergers and acquisitions?

Brand value impacts the buying price in M&A transactions. A strong brand can substantially enhance a company’s valuation. Since a strong brand drives regular revenue, pricing power, and higher customer loyalty—it can dramatically increase the interest of investors in the company.

Q) Can brand equity be improved to increase brand value?

Constant marketing inputs along with improved customer experience across touchpoints helps improve brand equity. Over time, improving brand equity can benefit in terms of higher sales, better margins, thereby leading to a higher brand value.

#Brand Equity#Brand Valuation Methods#Financial reporting#Brand Valuation#Valuation Services company in India#ValAdvisor#Val Advisor

0 notes

Text

CFA Level 2 vs Level 1: The Wake-Up Call Every Candidate Needs

If you’ve recently cleared CFA Level 1, congratulations—but brace yourself. Level 2 is not just the next step; it’s a complete evolution in complexity, preparation, and expectation. Many candidates underestimate the leap in difficulty between these two levels. While Level 1 tests your ability to recall and understand concepts, Level 2 demands application, synthesis, and mastery of analytical tools in real-world scenarios.

This blog is delving into the fundamental distinction between CFA Level 1 and Level 2, covering not only the curriculum but also the mindset adjustment, exam format, workarounds you must survive—and thrive. If you believe you are going down the same road twice, think again.

1. Breadth to Depth: The Curriculum Change

CFA Level 1 is generally characterized as a general overview of investment and finance concepts. You cover a broad spectrum of subjects—from ethics to economics, financial reporting, and portfolio management. It's introductory.

Level 2 delves deeper into the substance of valuation, equity analysis, derivatives, and fixed income. Each reading is not a mere review; each requires interpretation and application. Contestants are required to analyze case studies, read between the lines of financial reports, and apply formulas in a variety of scenarios.

For instance, while Level 1 may require you to compute a simple Net Present Value (NPV), Level 2 will demand that you evaluate the assumptions upon which those computations are made and modify them in light of changing circumstances. The degree of sophistication can prove daunting if you haven't prepared.

2. Item Sets: Another Animal

Actually, the most infamous difference between Level 1 and Level 2 is the structure. Level 1 employs single, isolated multiple-choice questions. Each is an independent question, and you can most often identify the subject it's probing.

In Level 2, items are clustered together in "item sets" or mini case studies. Each consists of a vignette and then six questions. The vignette might be a lengthy company financial statement, a memo on an investment strategy, or a compliance discussion with regulatory agencies. The twist? You must read it carefully because the questions not only test recall but your capacity for interpreting and inferring meaning from the information.

Many candidates struggle with time management here. Reading lengthy passages and interpreting them before even attempting the questions is a significant shift in approach.

3. Heavier Emphasis on Financial Reporting and Equity Valuation

While Level 1 introduces financial reporting and analysis, Level 2 takes it several steps further. You’ll find yourself deeply engaged with IFRS vs. US GAAP differences, evaluating complex accounting treatments, and adjusting financial statements for fair comparisons.

Equally, equity valuation becomes much more rigorous. The course work involves sophisticated models such as Residual Income, Free Cash Flow, and Multiples-based valuations. You must not only know how to use these models but also when and why to use one versus another.

4. Conceptual Understanding is Not Enough

At Level 1, memorization can usually suffice. Flashcards and formula sheets are a godsend there.

At Level 2, this is not enough. Candidates need to show analytical thinking. Take the Ethics section—although the Code of Ethics is the same, the vignettes become much more complex, with several violations and unclear situations that need judgment and interpretation.

You’re expected to think like a portfolio manager, not just a student. The exam will often test more than one Learning Outcome Statement (LOS) within a single item set, making rote learning ineffective.

5. Preparation Timeline and Study Plan

A common trap is assuming the same preparation strategy that worked for Level 1 will suffice for Level 2. It won’t. Level 2’s material is denser and more technical.

Although the CFA Institute suggests 300 hours per level, the majority of successful Level 2 candidates indicate that they spent 350–400 hours. Why? Because learning and applying valuation concepts, reading extensive case-based material, and practicing under time constraints takes depth and repetition.

Begin early. Don't wait until the final weeks to practice exams. Include mock exams in your study schedule at least a month prior to the test to develop endurance and flexibility.

6. New Trends and Developments in CFA Level 2

In 2024, the CFA Institute released changes to its Level 2 curriculum with a greater emphasis on practical, technology-related subjects. Modules on AI in finance, ESG integration, and actual portfolio construction have been introduced to meet market demands. This change makes the exam more applicable but also more difficult for those who are not from technical backgrounds.

Furthermore, with computer-based testing, the candidates must also learn to navigate digital interfaces. While the core content is demanding, learning to move around the screen, to refer to exhibits, and to handle on-screen calculators provides an additional challenge.

7. Psychological Load: The Mental Game

A lesser discussed—but no less significant—difference is the psychological challenge. Level 2 candidates often work full-time jobs, have family and social commitments, and have to deal with the pressure of a more challenging syllabus. Burnout is a reality.

Being consistent, pacing your study, and taking breaks to rest are essential. Unlike Level 1, where momentum can keep you going, Level 2 penalizes cramming. It pays off deliberate, systematic study.

Use active recall, spaced repetition, and peer discussion groups to aid your retention. And never forget the power of planned revision in the last month.

8. Career Relevance: Why Level 2 Matters

Level 2 has been called the analyst level because the remit of a financial analyst extends into the daily exposures put forth in the exam. Modeling and valuation-type questions are presented in seemingly practical contexts of asset management, equity research, and investment banking.

Above-and-beyond the progress toward the charter, passing Level 2 gives you the ability to convince an employer that you can pull together analyses, interpret financial statements, and make investment decisions. Therefore, this level has tremendous weightage on job interviews and promotion.

In Mumbai, for instance, the booming finance and investment sector is witnessed increased demand of mid-levels holding advanced analytical credentials. With firms expanding asset management and fintech operations, professionals undertaking the CFA course in Mumbai hold an unequivocal advantage, especially post-Level 2.

Conclusion: Step Up, Don't Just Step Forward

Level 2 is not harder because it is next within the L1; and it is harder because it basically turns a conceptual understanding into real-world application. Interpretation is required of instructors; mastery is demanded by curriculum, while time is just about against you.

But it can be done with the right strategies, proper preparation in advance, and with the right mindset.

With financial centers all over India expanding, cities such as Mumbai are witnessing more aspirants invest in professional growth. Taking admission in a CFA Training Program in Mumbai is increasingly becoming a sought-after choice for those who wish to acquire an edge in a competitive job market. Nevertheless, no book or program can replace persistent effort and a strong resolve towards the process.

So breathe deeply, open up that first Level 2 reading—and prepare to level up.

0 notes

Text

ACCA vs CPA vs MBA Finance – Choosing the Best Path in Accounting

Are you confused about whether to pursue ACCA, CPA USA, or an MBA in Finance? 🤔 You’re not alone. In today’s dynamic financial landscape, making the right career choice is crucial.

Here’s your complete guide 🧭 to help you decide, along with expert resources, interview tips, and course links from top finance education platforms like NorthStar Academy.

📘 ACCA vs CPA USA – Which Suits You Best?

If you're trying to choose between ACCA and CPA USA, read this insightful comparison: 👉 ACCA vs CPA USA – Which Is Better for Your Career?

Whether you want IFRS exposure or US GAAP experience, this blog breaks down every key point.

🎓 ACCA or MBA in Finance?

Both are prestigious paths, but they serve different goals. If you're debating between professional certification and a management degree, check this out: 🔗 ACCA vs MBA Finance – What Is the Difference?

💼 Job Interviews Coming Up? Be Prepared

Step into the interview room with confidence. Here’s a go-to resource: 📄 Top Accounting Interview Questions and Answers

And don’t miss: ❌ 10 Common Accounting Interview Mistakes You Should Avoid

🧠 What Recruiters Look for in You

Success isn’t just about qualifications. Employers want real-world skills. Read this blog to find out what really matters: 👉 Essential Skills Employers Look for in Accounting Professionals

🇮🇳 ACCA vs CA India – What’s Right for Indian Students?

Still unsure whether to go global with ACCA or stick with CA in India? Here’s a Medium blog that explains it perfectly: 📘 ACCA vs CA India – Which Is Better for Indian Accountants?

🚀 Ready to Begin?

If you’re leaning toward ACCA, take your first step with one of the top institutes: 🎯 NorthStar Academy ACCA Course

Or explore everything from CPA to CMA here: 🌐 NorthStar Academy – Official Website

✅ Quick Links Recap:

ACCA vs CPA: https://northstaracad.com/blogs/acca-vs-cpa-usa-which-is-better-for-your-career

ACCA vs MBA Finance: https://northstaracad.com/blogs/acca-vs-mba-finance-what-is-the-difference

Interview Questions: https://northstaracad.com/blogs/accounting-interview-questions-and-answers

Interview Mistakes Blog: https://yashwanthblogger1234.blogspot.com/2025/05/10-common-accounting-interview-mistakes.html

Skills Blog: https://www.tumblr.com/edupurpose/782686611364331520/essential-skills-employers-look-for-in-accounting?source=share

ACCA vs CA India: https://medium.com/@yashwanthbasvaraj/acca-vs-ca-india-which-is-better-for-indian-accountants-f76299d78922

ACCA Course Details: https://northstaracad.com/acca-course-details

Website: https://northstaracad.com

0 notes

Text

0 notes

Text

Deferred Revenue vs. Accrued Revenue: Key Accounting Differences

Deferred income and accrued income are two key accounting concepts that determine how businesses report their earnings. While deferred income is paid before products or services are consumed, accumulated income is money generated but not yet received. Accurate financial reporting, accounting standard compliance, and effective cash flow management all rely on understanding of these concepts. This ensures that businesses comply with the law, maintain transparency, and avoid tax issues.

What is accrued revenue?

Accrued revenue is income a company generates but has not yet been paid for. Usually, accrued income arises when goods or services are given or completed before payment is received. Accrued income appears on the balance sheet as an asset—more accurately as a receivable—indicating that the company is entitled to payment for given goods or services. As soon as the company is paid, the realized income is cash; its financial records are updated suitably.

Examples of Accrued Revenue

Professional Services – In December a consulting company offers advise services; in January it bills the customer.

Interest Income – A bank earns interest on a loan but does not receive payment until the next quarter.

Utility Companies – Before billing, electricity companies accrue income then bill consumers after use.

What is deferred revenue?

Deferred revenue, often known as unearned income, is money received by a company for goods or services not yet delivered or completed. Paying a firm in advance causes the money to display under deferred income under liabilities on the balance sheet. This shows how dedicated the business is to offer future goods or services. As the company satisfies its supply-chain promise, the deferred money is gradually dropped and shown on the income statement as actual revenue.

Examples of Deferred Revenue

Subscription Services – Although an annual membership price is paid upfront, a magazine publisher delivers the publications over a period of time.

Advance Payments for Goods – Before ever delivering the finished item, a manufacturing business gets an order deposit.

Software Licenses – A software firm sells a one-year license but recognizes revenue incrementally over the contract duration.

Difference between Deferred Revenue and Accrued Revenue

Feature

Deferred Revenue

Accrued Revenue

Definition

Revenue received before delivering goods/services

Revenue earned but not yet received

Accounting Treatment

Recorded as a liability initially

Recorded as an asset under accounts receivable

Impact on Financial Statements

Increases liabilities until earned

Increases assets until payment is collected

Examples

Subscription fees, advance payments, prepaid rent

Consulting services, interest income, postpaid utilities

Recognition Timing

Recognized over time as goods/services are provided

Recognized when earned, even if payment is pending

Why Understanding These Concepts is Important?

Maintaining financial accuracy, compliance, and general corporate health depends on a grasp of these ideas. Here's the rationale:

Accurate Financial Reporting – Proper recognition of Deferred Revenue and Accrued Revenue ensures that financial statements reflect a company’s actual financial position.

Compliance with Accounting Standards – Using IFRS and GAAP's revenue recognition guidelines helps you avoid legal and regulatory problems.

Effective Cash Flow Management – Differentiating between cash received and revenue earned helps businesses manage their finances efficiently.

Investor and Stakeholder Confidence – Transparent financial statements increase investor trust and provide a clearer picture of business health.

Tax Implications – Correct categorization might result in tax fines or missed deductions as taxable income depends on recognized income.

Challenges in Managing Deferred and Accrued Revenue

Despite their significance, companies can struggle to manage these revenue sources:

Complexity in Tracking – Big companies with several sources of income might find it difficult to precisely track postponed and accumulated income.

Accounting Software Limitations - Not all program solutions effectively separate and automate income recognition.

Regulatory Changes – Standard changes in financial reporting criteria, including IFRS 15, need for constant adaption to follow rules.

Audit and Compliance Risks – Inaccurate identification might lead to financial misstatements, therefore influencing audits and compliance evaluations.

The Role of Accounting Software in Revenue Recognition

Modern accounting systems automate journal entries, financial statement generation, and compliance monitoring to facilitate the management of deferred income and accumulated revenue. Advanced solutions guarantee that income recognition aligns with contract criteria and delivery timelines by interacting with client invoicing systems.

Questions to understand your ability

What’s the deal with accrued revenue?

a) You get paid before doing the work. b) You earn it, but you haven’t seen a penny yet. c) You make money only after delivering the goods. d) It’s basically an expense, not revenue.

Answer: b) You earn it, but you haven’t seen a penny yet. Why? Because accrued revenue means you’ve done the work or delivered the product, but the money’s still on its way. Simple, right?

When you’ve got deferred revenue, where does it show up on the balance sheet?

a) As cash sitting in your pocket. b) As a liability because you owe the goods/services. c) Under "prepaid expenses" as a future expense. d) Straight-up as a revenue gain.

Answer: b) As a liability because you owe the goods/services. Why? You’ve already taken the money, but you still have to deliver. It’s a liability until you pull through with the product or service.

Which of the following screams “accrued revenue” in action?

a) You’re paid upfront for a one-year magazine subscription. b) You get a down payment for a custom product. c) The bank earns interest but hasn’t seen the money yet. d) You sell goods before the customer hands over cash.

Answer: c) The bank earns interest but hasn’t seen the money yet. Why? Accrued revenue is earned but not yet paid. Interest income grows over time, but the cash won’t arrive until later.

When dealing with deferred revenue, how does it mess with your financial statements?

a) It boosts your assets until the cash hits. b) It raises your liabilities until the service is provided. c) It increases your equity immediately. d) It slashes the cost of goods sold.

Answer: b) It raises your liabilities until the service is provided. Why? Though it resides in the liabilities part of your balance sheet until you provide the products or services, you already have the cash. It then starts to generate income.

Why should you even care about deferred and accrued revenue?

a) To help you with your tax returns. b) To manage cash flow and keep financials in check. c) To follow marketing trends. d) To lower costs on your balance sheet.

Answer: b) To manage cash flow and keep financials in check. Why? Understanding the variations between these two income sources guarantees accurate financial statements. It also helps with cash flow management and keeps you out of tax hotbeds.

Conclusion

In financial accounting, both deferred and accrued revenue are somewhat important as they affect corporate decisions, taxes, and financial statements. Accrued Revenue accounts for earnings still to be earned; Deferred Revenue describes pre-earned payments. Good control of this income guarantees correct financial reporting, regulatory compliance, and efficient cash flow management. Using accounting software allows companies to simplify income recognition procedures, therefore lowering mistakes and improving financial openness.

#AccountingBasics#AccruedRevenue#DeferredRevenue#FinancialStatements#RevenueRecognition#AccountingPrinciples

0 notes

Text

Understanding the Key Differences Between IFRS and GAAP: A Comprehensive Guide

International Financial Reporting Standards (IFRS) is a set of accounting principles developed by the International Accounting Standards Board (IASB). It is widely used across the globe, especially in Europe, Asia, and other international markets. IFRS aims to create a common language for business affairs so that financial statements are transparent and comparable across countries.

In the world of financial reporting, two major accounting standards dominate global and domestic markets: International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP). These frameworks ensure consistency, reliability, and transparency in financial statements, but they have key differences that impact businesses, investors, and financial professionals.

For companies operating internationally or providing accounting services for small business in USA, understanding the Difference between IFRS and GAAP is essential. This article explores the difference between IFRS and GAAP, providing insights into their key features, applications, and impact on financial reporting.

What is IFRS?

Key Features of IFRS:

Principle-Based Approach: IFRS is more flexible and allows professional judgment in reporting financial transactions.

Global Adoption: More than 140 countries use IFRS, making it the preferred standard for international business.

Fair Value Accounting: IFRS emphasizes fair value measurement, leading to more dynamic financial reporting.

What is GAAP?

Generally Accepted Accounting Principles (GAAP) is a set of accounting rules and standards used primarily in the United States. The Financial Accounting Standards Board (FASB) oversees GAAP regulations to ensure consistency in financial reporting for businesses operating within the country.

Key Features of GAAP:

Rule-Based Approach: GAAP provides strict guidelines, reducing room for interpretation.

US-Centric Framework: GAAP is mandatory for publicly traded companies in the U.S.

Historical Cost Accounting: Emphasizes historical cost over fair value, leading to more conservative financial reporting.

For businesses seeking accounting services for small business in USA, understanding GAAP compliance is crucial to avoid legal and financial risks.

Key Differences Between IFRS and GAAP

Now that we understand the basics, let’s explore the difference between IFRS and GAAP in various financial reporting aspects.

1. Conceptual Approach: Principle-Based vs. Rule-Based

IFRS follows a principle-based approach, allowing flexibility in interpretation and financial judgment.

GAAP is rule-based, meaning financial reporting follows strict, detailed regulations with minimal room for interpretation.

2. Inventory Accounting: LIFO vs. FIFO

Under GAAP, businesses can use both Last-In-First-Out (LIFO) and First-In-First-Out (FIFO) inventory accounting methods.

Under IFRS, the LIFO method is prohibited because it does not reflect the actual flow of inventory costs.

For companies involved in accounting services for small business in USA, knowing which inventory valuation method applies is crucial for tax and financial reporting.

3. Revenue Recognition

IFRS recognizes revenue based on the principle that a company should record revenue when it is earned and measurable.

GAAP provides detailed, industry-specific guidelines for revenue recognition, ensuring consistency across industries.

4. Treatment of Intangible Assets

IFRS allows companies to recognize intangible assets, such as research and development costs, if they are expected to generate future economic benefits.

GAAP requires intangible assets to be recognized only if acquired, making it a more conservative approach.

5. Fair Value vs. Historical Cost Accounting

IFRS promotes fair value accounting, meaning assets and liabilities are recorded at their current market value.

GAAP relies on historical cost accounting, meaning assets are recorded at their original purchase price.

This difference significantly impacts financial statements, particularly in industries with rapidly changing asset values.

6. Presentation of Financial Statements

IFRS requires a statement of changes in equity, providing more transparency in financial position.

GAAP does not mandate this statement, making financial reports less detailed in terms of equity changes.

For businesses looking for accounting services for small business in USA, understanding financial statement presentation is crucial for compliance and decision-making.

7. Consolidation of Financial Statements

IFRS uses a control-based model, meaning financial statements are consolidated based on the control a company has over another entity.

GAAP follows a risk-and-reward model, meaning consolidation depends on the financial risk exposure of the parent company.

8. Lease Accounting

IFRS treats most leases as finance leases, requiring them to be recorded on the balance sheet.

GAAP differentiates between operating leases and finance leases, leading to different reporting structures.

For companies offering accounting services for small business in USA, lease classification and reporting are critical for compliance with financial standards.

Impact of IFRS and GAAP on Businesses

1. International vs. Domestic Business

Companies operating globally benefit from IFRS, as it allows easier financial comparison and cross-border transactions.

Companies operating only in the U.S. must comply with GAAP, ensuring standardized domestic reporting.

2. Investment and Financial Decision-Making

Investors using IFRS-based reports can compare companies internationally.

GAAP-based reports provide detailed financial disclosures, which are useful for U.S.-focused investors.

3. Taxation and Compliance

GAAP-based reporting is required for tax filings in the U.S.

Companies using IFRS may need additional adjustments for U.S. tax compliance.

Which Accounting Standard Should Your Business Follow?

For businesses, choosing between IFRS and GAAP depends on their market presence, regulatory requirements, and financial reporting needs.

Businesses operating globally should consider IFRS for easier financial consolidation and reporting.

Businesses in the U.S. must follow GAAP to comply with regulatory standards.

Companies seeking accounting services for small business in USA must ensure their financial statements align with GAAP standards to avoid compliance issues.

Conclusion

The difference between IFRS and GAAP plays a significant role in financial reporting, investment decisions, and compliance. IFRS provides flexibility and international comparability, whereas GAAP ensures strict regulatory adherence for U.S.-based companies.

For businesses in need of accounting services for small business in USA, working with financial experts familiar with both IFRS and GAAP is crucial for accurate reporting and compliance. Understanding the difference between IFRS and GAAP helps businesses make informed financial decisions, maintain transparency, and stay compliant with accounting regulations.

Whether you're a multinational corporation or a small business in the U.S., choosing the right accounting framework ensures financial success and regulatory compliance.

0 notes

Text

ERP vs. Accounting Software: What are the Differences and Benefits?

When managing finances and operations, businesses often find themselves choosing between ERP (Enterprise Resource Planning) software and Traditional Accounting Software. While both help track financial transactions, they serve different purposes. Let’s dive into the key differences and benefits of each to help you make an informed decision for your business.

Understanding the Basics

What is Accounting Software?

Accounting software is designed primarily to handle financial transactions, bookkeeping, invoicing, payroll, and tax management. Popular tools like QuickBooks, Tally, and Xero help businesses streamline their accounting operations.

What is ERP Software?

ERP software is an integrated system that manages multiple business functions beyond accounting. It includes modules for finance, HR, inventory, supply chain, CRM, and more. ERP systems like Microsoft Dynamics 365 Business Central, SAP, and Oracle NetSuite provide a centralized platform for complete business management.

Key Differences Between ERP and Accounting Software

Benefits of ERP Over Accounting Software

1) 360-Degree Business Visibility

Unlike standalone accounting software, ERP offers a holistic view of business operations, improving decision-making with real-time data.

2) Improved Efficiency and Automation

ERP automates not just accounting but also supply chain, HR, procurement, and CRM, reducing manual work and errors.

3) Scalability for Growth

As businesses expand, ERP adapts to changing needs, making it a future-ready investment compared to limited accounting tools.

4) Enhanced Compliance & Security

ERP solutions comply with industry regulations (GST, IFRS, GAAP, etc.) and offer advanced security features for data protection.

5) Better Decision-Making

With advanced analytics and AI-driven insights, ERP software like Microsoft Dynamics 365 Business Central empowers businesses with data-driven decisions.

Which One Should Your Business Choose?

If your business primarily deals with basic financial transactions, accounting software might be sufficient. However, if you aim for growth, process automation, and cross-department collaboration, an ERP system is the better choice.

Why Choose JRS Dynamics for ERP Software?

JRS Dynamics Info Solutions, we specialize in implementing Microsoft Dynamics 365 Business Central to help businesses streamline operations and drive growth. Here’s why we are the preferred ERP partner:

Expertise & Experience: Our team has extensive experience in ERP implementation across industries.

Tailored Solutions: We customize ERP solutions to fit your unique business needs.

Seamless Integration: We ensure smooth integration with your existing systems and processes.

Continuous Support: Our dedicated support team provides ongoing assistance to maximize ERP efficiency.

Cost-Effective Solutions: We offer scalable ERP solutions that provide high ROI and business value.

Final Thoughts

While accounting software is a great starting point for small businesses, ERP solutions provide an all-in-one approach for end-to-end business management. If you’re looking to upgrade from accounting software to a powerful ERP system, JRS Dynamics Info Solutions can help you implement Microsoft Dynamics 365 Business Central, tailored to your needs.

Ready to take your business to the next level? Contact JRS Dynamics Today and explore how an ERP can revolutionize your operations!

1 note

·

View note

Text

Understanding the Key Differences Between IFRS and GAAP: A Comprehensive Guide

In the world of financial reporting, two major accounting standards dominate global and domestic markets: International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP). These frameworks ensure consistency, reliability, and transparency in financial statements, but they have key differences that impact businesses, investors, and financial professionals.

For companies operating internationally or providing accounting services for small business in USA, understanding the Difference between IFRS and GAAP is essential. This article explores the difference between IFRS and GAAP, providing insights into their key features, applications, and impact on financial reporting.

What is IFRS?

International Financial Reporting Standards (IFRS) is a set of accounting principles developed by the International Accounting Standards Board (IASB). It is widely used across the globe, especially in Europe, Asia, and other international markets. IFRS aims to create a common language for business affairs so that financial statements are transparent and comparable across countries.

Key Features of IFRS:

Principle-Based Approach: IFRS is more flexible and allows professional judgment in reporting financial transactions.

Global Adoption: More than 140 countries use IFRS, making it the preferred standard for international business.

Fair Value Accounting: IFRS emphasizes fair value measurement, leading to more dynamic financial reporting.

What is GAAP?

Generally Accepted Accounting Principles (GAAP) is a set of accounting rules and standards used primarily in the United States. The Financial Accounting Standards Board (FASB) oversees GAAP regulations to ensure consistency in financial reporting for businesses operating within the country.

Key Features of GAAP:

Rule-Based Approach: GAAP provides strict guidelines, reducing room for interpretation.

US-Centric Framework: GAAP is mandatory for publicly traded companies in the U.S.

Historical Cost Accounting: Emphasizes historical cost over fair value, leading to more conservative financial reporting.

For businesses seeking accounting services for small business in USA, understanding GAAP compliance is crucial to avoid legal and financial risks.

Key Differences Between IFRS and GAAP

Now that we understand the basics, let’s explore the difference between IFRS and GAAP in various financial reporting aspects.

1. Conceptual Approach: Principle-Based vs. Rule-Based

IFRS follows a principle-based approach, allowing flexibility in interpretation and financial judgment.

GAAP is rule-based, meaning financial reporting follows strict, detailed regulations with minimal room for interpretation.

2. Inventory Accounting: LIFO vs. FIFO

Under GAAP, businesses can use both Last-In-First-Out (LIFO) and First-In-First-Out (FIFO) inventory accounting methods.

Under IFRS, the LIFO method is prohibited because it does not reflect the actual flow of inventory costs.