#Expandable Polystyrene Market Growth

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has been providing a Korean-language service since 2013.

Text

0 notes

Text

Unraveling the Growth Potential of the Geofoams Market: Global Outlook

The global geofoams market size is expected to reach USD 972.6 million by 2027, expanding at a CAGR of 2.7%, according to a new report by Grand View Research, Inc. Factors such as availability of geofoams at low cost coupled with its superior strength and durability are projected to fuel the market growth. Expansion of the construction industry across the globe coupled with the infrastructural developments in economies such as India, China, Brazil, Mexico, Saudi Arabia, and others is expected to propel the demand for geofoams over the forecast period. In addition, maintenance of the existing infrastructure in developed nations is likely to drive the growth of the market.

Geofoams Market Report Highlights

The expanded polystyrene geofoams segment accounted for USD 508.2 million in 2019 and is projected to expand at a CAGR of 3.1% from 2020 to 2027. The compatibility of the product has resulted in its increasing adoption for applications including roads and highway construction, building and infrastructure, and others

The road and highway construction application segment accounted for 38.07% of the total market and is projected to expand at a CAGR of 3.4% from 2020 to 2027 on account of the rising infrastructural growth across the developing economies including China, India, Brazil, UAE, Saudi Arabia, and others

Asia-Pacific accounted for USD 278.5 million in 2019 and is estimated to expand at a CAGR of 3.2% from 2020 to 2027 owing to the rising demand for road pavement, which is anticipated to further benefit the growth

China accounted for the highest market share in Asia Pacific on account of the rapidly expanding construction industry in the country

Europe market is estimated to expand at a CAGR of 2.8% owing to the rising number of construction and infrastructural activities in economies including Spain, Italy, and others

For More Details or Sample Copy please visit link @: Geofoams Market Report

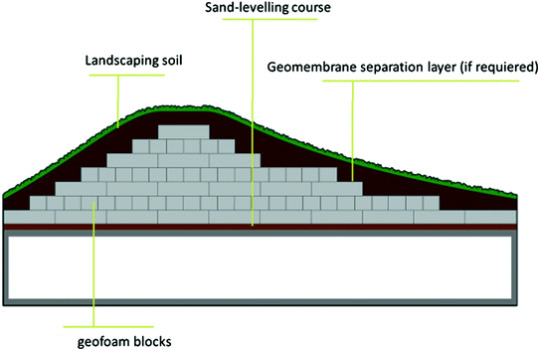

Geofoams are increasingly used in the construction industry as it helps in suppressing the noise and vibrations. In addition, it is easy to handle and does not require any special equipment for installation. The product is increasingly used in the railway track systems, below the refrigerated storage buildings, storage tanks, and others to avoid ground freezing.

The geofoams undergo chemical changes when it comes in contact with petroleum solvents. It turns into a glue-type substance, thereby losing its strength. This factor is projected to limit the use of geofoams in the construction industry which is projected to restrict the industry growth over the forecast period.

#Geofoam#Expanded polystyrene (EPS)#Geofoam blocks#Construction materials#Road and highway construction#Retaining walls#Geotechnical engineering#Soil stabilization#Environmental protection#Earthquake resistance#Noise and vibration control#Water management#Hydrostatic pressure#Thermal insulation#Structural stability

12 notes

·

View notes

Text

Ice Boxes Market Trends Increasing Consumer Preference for Durability and Functionality

The ice boxes market focuses on portable cooling solutions designed to preserve perishable goods, beverages, and food items during transport or outdoor activities. These products are widely used in camping, fishing, travel, and medical transport. The increasing popularity of outdoor activities and rising demand for sustainable, efficient cooling solutions is driving market growth.

1. Ice Boxes Market Trends: Rising Popularity of Outdoor Recreational Activities The increasing trend of outdoor activities such as camping, hiking, and fishing is a significant driver in the ice boxes market. As more consumers engage in outdoor recreation, the need for reliable cooling solutions is on the rise. Ice boxes are an essential part of outdoor equipment, and this trend is expected to continue growing, especially in developed regions.

2. Ice Boxes Market Trends: Technological Advancements in Insulation Materials Innovation in insulation technology is transforming the ice boxes market. Manufacturers are increasingly using advanced materials such as expanded polystyrene (EPS) and polyurethane foam, which enhance the cooling efficiency and longevity of ice boxes. These technological advancements are driving consumer interest in more durable, high-performance ice boxes that provide longer-lasting cooling.

3. Ice Boxes Market Trends: Increasing Consumer Preference for Durability and Functionality Consumers are increasingly prioritizing durability and functionality when choosing ice boxes. Market trends show that buyers now prefer models that offer superior insulation, enhanced portability, and added features such as built-in bottle openers, cup holders, and wheels. This trend is driven by the desire for convenience and long-term value in outdoor cooling solutions.

4. Ice Boxes Market Trends: Growth of Eco-Friendly and Sustainable Products As sustainability becomes a key factor in consumer purchasing decisions, the demand for eco-friendly ice boxes is rising. Research reveals that many buyers now prefer products made from recycled or sustainable materials, such as biodegradable insulation and recyclable plastics. Manufacturers are adapting to these preferences by offering more environmentally friendly ice boxes.

5. Ice Boxes Market Trends: Emergence of Smart Ice Boxes with Advanced Features The integration of smart technology into ice boxes is gaining traction in the market. Smart ice boxes that feature temperature control systems, real-time monitoring, and even GPS tracking are attracting tech-savvy consumers. These products offer greater convenience, especially for long trips or for use in remote areas where reliable cooling is essential.

6. Ice Boxes Market Trends: Influence of Online Retail and E-Commerce Growth Online retail and e-commerce have revolutionized the ice boxes market. The ease of purchasing products online, along with detailed product descriptions and customer reviews, has led to a shift in consumer buying habits. Manufacturers are increasingly focusing on online channels to reach a broader audience, making it easier for consumers to compare options and make informed purchases.

7. Ice Boxes Market Trends: Rising Demand for Compact and Portable Models With a growing number of consumers seeking compact and easy-to-carry cooling solutions, the market for portable ice boxes is expanding. Trends indicate that smaller, lightweight models are becoming increasingly popular, especially among urban dwellers and younger consumers. These ice boxes cater to short trips, picnics, and events where portability is a key consideration.

8. Ice Boxes Market Trends: Seasonal Demand Fluctuations and Sales Patterns The ice boxes market experiences seasonal fluctuations, with peak demand during warmer months when outdoor activities and events are most frequent. Research shows that the market also sees increased sales during holiday seasons and summer festivals. Understanding these seasonal patterns helps manufacturers and retailers align their production and marketing strategies with consumer demand.

9. Ice Boxes Market Trends: Shift Towards Multi-Functional and Versatile Products Today’s consumers seek multi-functional products that provide more than just basic cooling. As a result, ice boxes are evolving to offer additional features, such as being able to double as seats, tables, or storage units. This versatility appeals to those looking for products that serve multiple purposes, particularly for extended outdoor trips and events.

10. Ice Boxes Market Trends: Growth in Commercial and Medical Applications While consumer demand is a significant factor, research also highlights the growing use of ice boxes in commercial and medical applications. Medical transportation, including the storage and transport of vaccines, medicines, and biological samples, is contributing to market growth. The foodservice industry is also adopting ice boxes for short-term cold storage in mobile kitchens and food trucks.

Conclusion The ice boxes market is witnessing significant trends driven by consumer preferences for more efficient, eco-friendly, and multi-functional products. Advancements in insulation materials, smart technology integration, and the growing popularity of outdoor activities are all contributing to the market’s expansion. With seasonal demand fluctuations and emerging applications, manufacturers are focusing on innovation to meet diverse consumer needs in both the recreational and commercial sectors. As the market continues to evolve, it is clear that the future of ice boxes will be shaped by technological advancements, sustainability concerns, and a growing demand for versatile products.

0 notes

Text

Plastic Resin Market: Key Trends and Innovations Driving Industry Growth

The global plastic resin market size is expected to reach USD 1.07 trillion by 2030, according to a new report by Grand View Research, Inc. It is projected to expand at a 4.5% CAGR over the forecast period. The increasing consumption of plastic resins in construction, automotive, electrical, and electronics applications is boosting the market growth. Government intervention to reduce overall vehicle weight to improve fuel efficiency and reduce carbon emissions has prompted automakers to use resins to replace steel and aluminum in automotive components.

Favorable federal regulations on CO2 emissions set by agencies such as the National Highway Traffic Safety Administration and the Environmental Protection Agency (EPA), as well as EU initiatives to develop plastics applications for light-weight and fuel-efficient cars, are expected to fuel global growth and promote the market. However, the ongoing health crisis and the lockdown imposed by various governments to contain the spread of the coronavirus pandemic have led to a decline in the consumption of plastic resins. It is expected to further negatively impact the market growth in the years to come.

Strict restrictions governing the recyclability and deterioration of traditional building materials like metal and wood are likely to boost the demand for textiles in pipes, windows, cables, storage tanks, and other uses. Plastics are long-lasting and energy-efficient, as well as cost-effective and safe, which encourages their usage in construction. The global market is segmented into crystalline resin, non-crystalline resin, engineering plastics, and super engineering plastics by type. The crystalline resin was the largest segment, accounting for 61.9% of global sales in 2021. The crystalline resin segment mainly includes epoxy, polyethylene, and polypropylene resins.

Gather more insights about the market drivers, restrains and growth of the Plastic Resin Market

Plastic Resin Market Report Highlights

• Crystalline resins (epoxy, polyethylene, and propylene) segment accounted for a prominent share in the market by the end of 2023 and is further expected to witness maximum growth over the forecast period

• As of 2023, China accounted for the maximum revenue share in the market, with 40.24%. Rising consumer disposable income in the country and ascending demand for luxury cars are expected to have a positive impact on the automotive industry

• The advent of bio-based plastic resins has played a prominent role in food and beverage, and pharmaceutical applications. Polymers such as PET and PC are increasingly utilized in the beverages packaging and consumer goods sector

Plastic Resin Market Segmentation

Grand View Research has segmented the global plastic resin market report based on product, application, and region:

Plastic Resin Product Outlook (Volume, Tons; Revenue, USD Million, 2018 - 2030)

• Crystalline Resin

o Epoxy

o Polyethylene

o Polypropylene

• Non-crystalline Resin

o Polyvinyl Chloride (PVC)

o Polystyrene (PS)

o Acrylonitrile Butadiene Styrene (ABS)

o Polymethyl Methacrylate (PMMA)

• Engineering Plastic

o Nylon

o Polybutylene Terephthalate (PBT)

o Polycarbonate (PC)

o Polyamide

• Super Engineering Plastic

o Polyphenylene Sulfide (PPS)

o Polyether Ether Ketone (PEEK)

o Liquid Crystal Polymer (LCP)

Plastic Resin Application Outlook (Volume, Tons; Revenue, USD Million, 2018 - 2030)

• Packaging

o Food

o Beverage

o Medical

o Retail

o Others

• Automotive

• Construction

• Electrical & Electronics

o OA Equipment & Home Appliances

o Electronic Materials

o Others

• Logistics

• Consumer Goods

• Textiles & Clothing

o Clothing

o Industrial use

o Others

• Furniture & Bedding

• Agriculture

• Medical Devices

• Others

Plastic Resin Regional Outlook (Volume, Tons; Revenue, USD Million, 2018 - 2030)

• North America

o U.S.

o Canada

o Mexico

• Europe

o Germany

o U.K.

o France

o Italy

o Poland

o Spain

• China

• Asia

o India

o Japan

o Thailand

o Malaysia

o Indonesia

o Vietnam

o Singapore

o Philippines

• Pacific

• Central & South America (MEA)

o Brazil

o Argentina

• Middle East and Africa (MEA)

o Saudi Arabia

o UAE

o Oman

Order a free sample PDF of the Plastic Resin Market Intelligence Study, published by Grand View Research.

#Plastic Resin Market#Plastic Resin Market Size#Plastic Resin Market Share#Plastic Resin Market Analysis#Plastic Resin Market Growth

0 notes

Text

Cyclopentane Prices: Trend, Pricing and Forecast

The global cyclopentane market has been experiencing significant growth, driven by its increasing adoption across various industries, particularly in refrigeration and construction. Cyclopentane, a hydrocarbon compound, has emerged as an eco-friendly and energy-efficient alternative to traditional blowing agents and refrigerants, aligning with the global push for sustainable solutions. As environmental regulations become more stringent, the demand for cyclopentane as a non-ozone-depleting and low-global-warming-potential (GWP) substance has gained considerable traction. This shift is particularly evident in the insulation industry, where cyclopentane is used as a blowing agent in the production of polyurethane and polystyrene foams, crucial for energy-efficient building materials. The growing emphasis on green building certifications and energy conservation is further bolstering the market’s expansion.

The refrigeration industry represents a key driver for cyclopentane demand, as manufacturers increasingly adopt it in response to global regulatory frameworks such as the Kigali Amendment to the Montreal Protocol. Cyclopentane’s excellent thermal insulation properties make it an ideal choice for use in domestic refrigerators and freezers, as well as in commercial refrigeration systems. Its non-toxic and non-corrosive nature adds to its appeal, ensuring safe and efficient operations. Additionally, the rising disposable incomes and changing consumer lifestyles, particularly in emerging economies, are driving the growth of the refrigeration sector, thereby augmenting the demand for cyclopentane.

Get Real time Prices for Cyclopentane: https://www.chemanalyst.com/Pricing-data/cyclopentane-1512

In the construction sector, cyclopentane’s role as a blowing agent in foam insulation materials is pivotal. With the global construction industry expanding due to rapid urbanization and infrastructure development, the need for high-performance insulation solutions is escalating. Cyclopentane-based foams offer superior thermal performance, helping reduce energy consumption and greenhouse gas emissions. This aligns with the global focus on achieving net-zero carbon emissions, thereby propelling the adoption of cyclopentane in the construction domain. Moreover, government incentives and regulations promoting energy-efficient buildings further enhance its market prospects.

The Asia-Pacific region dominates the cyclopentane market, accounting for a significant share of global consumption. This can be attributed to the region’s robust industrial base, burgeoning construction activities, and expanding refrigeration market. Countries like China, India, and Japan are at the forefront of this growth, driven by favorable government policies, increasing investments in infrastructure, and a growing middle-class population. China, in particular, plays a pivotal role as a major producer and consumer of cyclopentane, supported by its extensive manufacturing capabilities and focus on environmental sustainability.

North America and Europe also hold substantial shares in the cyclopentane market, driven by stringent environmental regulations and the strong presence of advanced manufacturing industries. In these regions, the transition from high-GWP refrigerants and blowing agents to more sustainable alternatives is a critical factor driving demand. The European Union’s Green Deal and the United States’ focus on clean energy initiatives are key catalysts in promoting cyclopentane adoption. Additionally, ongoing research and development efforts aimed at enhancing the efficiency and application scope of cyclopentane further contribute to market growth in these regions.

The cyclopentane market is characterized by intense competition, with numerous players striving to capture market share through innovation and strategic collaborations. Leading manufacturers are investing in research and development to enhance the quality and performance of cyclopentane products, catering to the diverse needs of end-use industries. Moreover, strategic partnerships and mergers and acquisitions are prevalent, enabling companies to expand their geographical footprint and strengthen their market position. The emphasis on sustainable practices and compliance with environmental regulations remains a core focus for market participants, driving innovation and differentiation.

Challenges in the cyclopentane market include fluctuations in raw material prices and the potential health and safety risks associated with its handling and storage. However, advancements in manufacturing processes and the development of safer handling techniques are mitigating these concerns, ensuring a steady supply of high-quality cyclopentane. Furthermore, the growing awareness about the environmental benefits of cyclopentane over conventional alternatives is helping to overcome initial resistance to its adoption, particularly in price-sensitive markets.

The future of the cyclopentane market appears promising, with substantial opportunities emerging from technological advancements and the expanding scope of applications. The growing trend of sustainable development and energy efficiency across industries is expected to drive long-term demand. Additionally, the integration of cyclopentane with emerging technologies, such as smart refrigeration systems and advanced building materials, presents exciting possibilities for innovation and growth. As industries worldwide continue to align with global sustainability goals, cyclopentane’s role as a key enabler of eco-friendly solutions is set to gain even greater prominence.

In conclusion, the cyclopentane market is poised for robust growth, driven by its eco-friendly properties and expanding applications in key sectors like refrigeration and construction. The global focus on sustainability, coupled with favorable regulatory frameworks and technological advancements, is creating a conducive environment for the market’s expansion. While challenges such as raw material price volatility and safety concerns persist, ongoing innovations and industry collaborations are paving the way for a sustainable and prosperous future for cyclopentane. As industries and consumers alike prioritize energy efficiency and environmental conservation, cyclopentane is well-positioned to play a vital role in shaping a greener and more sustainable world.

Get Real time Prices for Cyclopentane: https://www.chemanalyst.com/Pricing-data/cyclopentane-1512

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Cyclopentane#Cyclopentane Price#Cyclopentane Prices#india#united kingdom#united states#germany#business#research#chemicals#Technology#Market Research#Canada#Japan#China

0 notes

Text

Foam Insulation Market Recovery Patterns Highlight Green Energy Impact on Building and Construction Industries

The global foam insulation market is undergoing a significant recovery after facing notable challenges due to the COVID-19 pandemic. The insulation industry, with foam insulation at its forefront, has experienced evolving market trends driven by technological innovation, regulatory shifts, and rising demand for energy-efficient solutions. The rebound is especially evident in the construction and building sector, complemented by advances in materials science, sustainable product innovations, and increased government investments.

Industry Overview

Foam insulation plays a crucial role in reducing energy consumption by minimizing heat transfer. Polyurethane, polystyrene, and polyisocyanurate foams are among the widely used variants, serving both residential and commercial sectors. Their applications span walls, roofs, and flooring systems to ensure energy efficiency. The market's downturn in 2020 was marked by disruptions in supply chains, halted construction activities, and reduced investments. However, a robust recovery trajectory was observed in 2021, continuing into 2025, supported by the green building movement and urbanization in emerging economies.

Driving Forces Behind the Market Recovery

Sustainability Initiatives Global awareness around climate change has led to significant uptake of foam insulation products that meet stringent energy efficiency standards. Governments and private entities are ramping up efforts to decarbonize construction projects, driving demand for sustainable insulation solutions.

Technological Advancements Innovations such as the development of spray polyurethane foams with enhanced R-value and reduced environmental impact have positioned foam insulation as a competitive and eco-friendly choice. The use of advanced robotics in insulation application is another factor enhancing efficiency.

Urbanization and Infrastructure Development Emerging markets are witnessing rapid infrastructure growth, leading to higher consumption of foam insulation materials. Retrofitting older buildings to meet modern energy codes further contributes to increased demand.

Government Subsidies and Incentives Global players benefit from tax credits, green certifications, and rebates for insulation upgrades. Regulations like zero-energy building mandates further incentivize foam insulation adoption.

Energy Crisis and Cost Reduction Fluctuations in global energy prices have heightened the focus on reducing consumption through efficient thermal insulation, reinforcing market growth.

Key Challenges and Opportunities

Despite positive recovery signs, the foam insulation market faces challenges such as fluctuating raw material prices, especially for petroleum-based foams, and regulatory hurdles related to environmental compliance. These obstacles have spurred a shift toward bio-based and recyclable insulation materials. The rise in innovation-driven partnerships and collaborations among key players also presents growth opportunities in untapped markets.

Regional Outlook

North America: High demand for residential retrofits and green buildings fuels steady market growth.

Europe: Regulatory mandates under the EU Green Deal prioritize advanced insulation solutions.

Asia-Pacific: Accelerated urbanization and government-backed housing initiatives boost the foam insulation sector.

Middle East & Africa: Construction booms tied to upcoming large-scale projects sustain regional momentum.

Market Recovery Patterns: A Strategic Perspective

The foam insulation market exhibits a distinct V-shaped recovery, characterized by rapid decline and subsequent growth. This rebound is underpinned by industrial adaptability, supply chain optimizations, and increased funding for energy efficiency initiatives. Experts anticipate further consolidation in the market as key players expand capacity and optimize product portfolios to meet evolving customer needs.

0 notes

Text

Thermal Insulation Packaging Market: An In-Depth Analysis

The thermal insulation packaging market is experiencing significant growth, driven by increasing demand for temperature-sensitive goods and advancements in packaging technologies. According to a report by Report Prime, the market is projected to expand from USD 26.50 billion in 2023 to USD 45.12 billion by 2030, at a compound annual growth rate (CAGR) of 7.90% during the forecast period.

Market Overview

Thermal insulation packaging involves materials and solutions designed to maintain the temperature of products during storage and transportation. This is particularly crucial for industries such as pharmaceuticals, food and beverages, and chemicals, where temperature control is essential to preserve product integrity.

Get Sample PDF

Key Drivers

Growing Demand for Temperature-Sensitive Products: The pharmaceutical and biotechnology sectors require stringent temperature control for products like vaccines and biologics. Similarly, the food industry demands thermal packaging to maintain the freshness of perishable items.

Expansion of E-commerce: The rise in online retailing of perishable goods has necessitated efficient thermal insulation solutions to ensure products reach consumers in optimal condition.

Regulatory Compliance: Stringent regulations regarding the transportation of temperature-sensitive goods compel industries to adopt reliable thermal insulation packaging to meet compliance standards.

Market Segmentation

The thermal insulation packaging market can be segmented based on product type, material, application, and region.

By Product Type:

Boxes: Widely used for shipping temperature-sensitive products.

Bags: Employed for smaller quantities requiring thermal protection.

Carton Liners: Used to line cartons, providing an additional layer of insulation.

Bubble Cushioning: Offers both insulation and protection against physical damage.

By Material:

Polystyrene: Includes expanded (EPS) and extruded (XPS) forms, known for excellent insulation properties.

Polyurethane (PUR): Offers superior thermal resistance, suitable for extreme temperature conditions.

Polyethylene: Commonly used due to its flexibility and durability.

Vacuum Insulated Panels (VIPs): Provide high thermal resistance in a thin profile, ideal for space-constrained applications.

Corrugated Fiber Board: An eco-friendly option with moderate insulation properties.

By Application:

Pharmaceuticals: Ensuring the efficacy of temperature-sensitive drugs and vaccines.

Food & Beverages: Maintaining the freshness and safety of perishable goods.

Chemicals: Preventing temperature-induced reactions during transport.

Horticulture Products: Protecting plants and flowers from temperature extremes.

Electronics: Safeguarding temperature-sensitive electronic components.

Regional Analysis

North America: Dominates the market due to advanced pharmaceutical and food industries, along with stringent regulatory standards.

Europe: Significant growth attributed to increasing demand for sustainable packaging solutions and a robust pharmaceutical sector.

Asia-Pacific: Expected to witness substantial growth owing to rapid industrialization, urbanization, and expanding e-commerce activities.

Middle East & Africa: Growth driven by the development of cold chain logistics and increasing pharmaceutical imports.

Latin America: Steady growth anticipated due to improving economic conditions and rising demand for temperature-sensitive goods.

Challenges

High Costs: Advanced thermal insulation materials like VIPs and PUR can be expensive, impacting adoption among cost-sensitive end-users.

Environmental Concerns: Disposal of non-biodegradable materials such as polystyrene poses environmental challenges, prompting a shift towards sustainable alternatives.

Supply Chain Complexity: Maintaining the integrity of thermal insulation packaging throughout complex supply chains requires meticulous planning and execution.

Opportunities

Sustainable Materials: Development of eco-friendly insulation materials presents opportunities for market growth, aligning with global sustainability trends.

Technological Advancements: Integration of smart technologies, such as temperature monitoring sensors, can enhance the functionality of thermal insulation packaging.

Emerging Markets: Expansion into developing regions with growing pharmaceutical and food industries offers potential for market penetration.

Recent Developments

Innovations in Sustainable Packaging: Companies are investing in research to develop biodegradable and recyclable thermal insulation materials to address environmental concerns.

Strategic Partnerships: Collaborations between packaging manufacturers and pharmaceutical companies are on the rise to develop customized solutions for specific temperature-sensitive products.

Regulatory Compliance Initiatives: Businesses are enhancing their packaging solutions to comply with evolving regulations, ensuring product safety and quality during transportation.

Conclusion

The thermal insulation packaging market is poised for robust growth, driven by increasing demand for temperature-sensitive products, advancements in packaging technologies, and a global emphasis on sustainability. However, challenges such as high costs and environmental concerns need to be addressed. Companies that invest in sustainable materials, technological innovations, and strategic partnerships are well-positioned to capitalize on emerging opportunities in this dynamic market.

0 notes

Text

Molded Plastic Market: Segmentation, Growth Trends, and Key Insights

The global molded plastic market is poised for significant growth, with a projected valuation of USD 1218.39 billion by 2033, up from USD 715.07 billion in 2024. This growth, driven by rising demand across various industries, including automotive, packaging, and electronics, underscores the importance of molded plastics as a critical component in modern manufacturing and consumer goods production.

Market Definition and Latest Trends

Molded plastics refer to plastic products manufactured using molding techniques such as injection molding, blow molding, and extrusion. These products are lightweight, durable, and cost-effective, making them ideal for various applications, including automotive parts, consumer goods, packaging materials, and electrical components. The molded plastic market includes various product types such as polyethylene, polypropylene, polystyrene, and polyethylene terephthalate, among others.

The latest trends in the molded plastic market reflect the ongoing shift toward sustainability, technological advancements, and the increasing demand for high-performance plastics in emerging applications. Notable trends include:

Sustainability Focus: As the world becomes more environmentally conscious, manufacturers are turning to bio-based and recyclable plastics, especially in packaging and automotive applications. The push toward circular economy models is expected to accelerate innovation in sustainable molded plastics.

Smart Plastics: The growing adoption of smart technologies in industries such as electronics and automotive is creating a demand for molded plastics with integrated functions like sensors, lighting, and communication capabilities. These advanced molded plastics are contributing to the development of the Internet of Things (IoT) and autonomous vehicles.

Technological Advancements: Newer, more efficient molding technologies, including 3D printing and multi-component injection molding, are enabling manufacturers to produce more complex and customized plastic components at a lower cost.

Growing Automotive Sector: The automotive industry remains a major consumer of molded plastics, especially with the rise in electric vehicles (EVs) and lightweight materials to improve fuel efficiency and reduce carbon emissions.

Get Free Request Sample Report @ https://straitsresearch.com/report/molded-plastic-market/request-sample

Growth Factors in the Molded Plastic Market

The molded plastic market is expected to experience strong growth due to several key factors:

Rapid Industrialization: As industries such as automotive, packaging, and construction continue to grow globally, the demand for molded plastic products is expanding. Manufacturers are increasingly turning to plastics to replace traditional materials like metals and glass due to the lightweight, cost-effective, and versatile properties of molded plastics.

Demand for Packaging Materials: The global packaging industry is one of the largest end-users of molded plastics. The rise in e-commerce and retail, especially in the food and beverage sector, has increased the need for plastic packaging solutions. The convenience, durability, and flexibility of molded plastics make them ideal for use in bottles, containers, and protective packaging.

Technological Advancements in Molding Techniques: The advancement of molding technologies such as injection molding and blow molding has improved the production efficiency, precision, and scalability of molded plastics, enabling manufacturers to meet increasing demand across multiple sectors.

Urbanization and Infrastructure Development: The growing urbanization and infrastructure development in emerging economies are fueling demand for plastic pipes, sheets, and other molded plastic products used in construction, plumbing, and electrical systems.

Opportunities in the Molded Plastic Market

The molded plastic market offers substantial opportunities for growth and innovation:

Sustainable Plastics: There is a growing demand for environmentally friendly plastics, including biodegradable, recyclable, and renewable materials. Companies that invest in developing sustainable molded plastics will have a competitive advantage as consumers and regulatory bodies continue to push for eco-friendly alternatives.

Emerging Applications: The growing adoption of electric vehicles (EVs), renewable energy systems, and medical devices provides ample opportunities for the molded plastic market. Lightweight, durable, and cost-effective plastic components are essential in EVs, solar panels, wind turbines, and medical equipment.

Expansion into Emerging Markets: Emerging economies in Asia-Pacific, Latin America, and the Middle East are seeing an increase in industrialization and consumer spending, driving demand for molded plastic products. Companies that expand their presence in these regions can benefit from the growing demand across various industries.

Buy Now @ https://straitsresearch.com/buy-now/molded-plastic-market

Key Players in the Molded Plastic Market

The molded plastic market is competitive, with several leading companies dominating the global landscape. These key players include:

LyondellBasell (Netherlands)

SABIC (Saudi Arabia)

INEOS (Switzerland)

DuPont (US)

ExxonMobil (US)

Sinopec (China)

Dow Inc (US)

BASF SE (Germany)

Eastman Chemical Company (US)

Chevron Corporation (US)

Formosa Plastics Corporation (Taiwan)

Solvay (Belgium)

China Plastics Extrusion Ltd. (China)

Lanxess AG (Germany)

Versalis (Italy)

LG Chem (South Korea)

Reliance Industries (India)

These companies are investing in research and development, focusing on innovations in molding technologies, sustainability, and expanding their global reach to maintain leadership in the market.

Market Segmentation of the Molded Plastic Market

The molded plastic market can be segmented based on product type, technology, and application.

By Product Type:

Polyvinyl Chloride (PVC)

Polypropylene (PP)

Polystyrene (PS)

Polyethylene (PE)

Polyurethane (PU)

Polyethylene Terephthalate (PET)

Others

By Technology:

Injection Molding

Blow Molding

Extrusion

Others

By Applications:

Packaging

Film

Automotive Parts

Corrugated Sheets

Bags and Pouches

Battery Cases

Bottles and Vials

Pipes

Containers

Filament Yarn

Wires and Cables

Others

Conclusion

The molded plastic market is on the verge of remarkable expansion, driven by technological advancements, growing demand across a wide range of industries, and an increased focus on sustainability. As businesses continue to innovate in molding technologies and sustainable materials, the market will continue to evolve and offer ample opportunities for both established players and new entrants.

For more information, please contact:

Straits Research Email: [email protected] Website: www.straitsresearch.com

This comprehensive report on the molded plastic market provides valuable insights into growth trends, opportunities, and the competitive landscape, offering critical information for stakeholders to make informed decisions in this evolving industry.

0 notes

Text

Plastic Waste Management Market: Role of Public-Private Partnerships

The Plastic Waste Management Market is projected to witness substantial growth, driven by increasing environmental concerns, regulatory pressures, and advancements in recycling technologies. With the global emphasis on sustainability, there is a growing demand for effective waste management solutions to mitigate plastic pollution and promote circular economy practices.

Read Complete Report Details of Plastic Waste Management Market: https://www.snsinsider.com/reports/plastic-waste-management-market-2929

Market Segmentation

By Polymer

PET (Polyethylene Terephthalate)

Widely used for beverage bottles and food containers.

High recyclability makes PET a focus area for waste management initiatives.

Polyvinyl Chloride (PVC)

Utilized in construction, medical devices, and packaging.

PVC waste poses unique challenges due to its chemical composition, leading to increased research in safe disposal and recycling methods.

Polypropylene (PP)

Common in packaging, automotive components, and textiles.

Recycling of PP is growing due to its widespread use in consumer goods.

High-density Polyethylene (HDPE)

Used for rigid containers, pipes, and grocery bags.

HDPE is valued for its high durability and ease of recycling.

Low-density Polyethylene (LDPE)

Found in films, wraps, and plastic bags.

Recycling of LDPE is challenging but increasingly prioritized.

Polyurethane (PU)

Used in furniture, automotive interiors, and insulation.

PU waste management is advancing with innovative recycling methods like chemical depolymerization.

Others

Includes specialty polymers like ABS, polystyrene, and bioplastics.

Recycling efforts for these materials are gaining traction due to technological innovations.

By Service

Collection

The first and most critical step in waste management.

Increasing adoption of structured collection systems in residential and industrial areas.

Incineration

Used for energy recovery from non-recyclable plastic waste.

Faces criticism for its environmental impact, but advancements in clean incineration technologies are addressing these concerns.

Landfills

A traditional method for plastic waste disposal.

Efforts to reduce landfill dependency are fueling alternative waste management solutions.

Recycling

Includes mechanical and chemical recycling methods.

Recycling is the most sustainable option and a primary focus for governments and industries worldwide.

By Source

Industrial

Includes waste generated from manufacturing processes.

Industrial plastic waste often has higher recyclability due to its relatively clean and homogenous nature.

Residential

Includes plastic waste from households, such as packaging and single-use plastics.

Residential waste management systems are expanding, particularly in urban areas.

Commercial

Includes plastic waste from businesses, retail, and hospitality sectors.

Commercial sources often generate significant amounts of packaging and disposable plastics.

By Application

Building & Construction

Plastic waste is generated from construction materials like PVC pipes, insulation, and flooring.

Recycling initiatives focus on reusing durable materials and reducing construction waste.

Consumer Products

Includes waste from items like electronics, furniture, and clothing.

Growth in e-waste recycling contributes significantly to this segment.

Packaging

The largest contributor to plastic waste globally.

Innovations in biodegradable and recyclable packaging are reshaping the segment.

Electrical & Electronics

Plastic is widely used in electronic casings and components.

Recycling efforts focus on recovering valuable materials from electronic waste.

Others

Includes automotive, agriculture, and healthcare applications.

Increasing attention to specialized recycling programs for niche industries.

By Region

North America

Focus on advanced recycling technologies and strict regulations.

The U.S. and Canada are key markets with robust waste management systems.

Europe

Leading the way in sustainable waste management practices.

EU directives and policies are driving innovations in recycling and circular economy adoption.

Asia-Pacific

The largest generator of plastic waste due to high population density and rapid industrialization.

Significant investments in waste management infrastructure in countries like China, India, and Japan.

Latin America

Growing awareness and government initiatives are driving improvements in waste collection and recycling.

Middle East & Africa

Developing waste management systems to tackle rising plastic pollution.

Increasing interest in waste-to-energy solutions.

Market Trends and Opportunities

Circular Economy Initiatives: Emphasis on designing products for recyclability and reusability to reduce waste generation.

Technological Advancements: Innovations in chemical recycling and AI-driven waste sorting systems are revolutionizing the market.

Government Regulations: Policies like single-use plastic bans and extended producer responsibility (EPR) are encouraging sustainable practices.

Consumer Awareness: Growing demand for eco-friendly products and recycling programs is reshaping the market landscape.

Corporate Commitments: Companies are pledging to use recycled plastics and improve waste management within their operations.

Market Outlook

The Plastic Waste Management Market is set to grow significantly as industries and governments collaborate to address global plastic pollution. Advances in recycling technologies, coupled with stricter regulations, are driving the adoption of sustainable practices. While challenges such as high costs and limited infrastructure remain, the rising awareness of environmental issues and increasing investments in waste management solutions will sustain market growth. The shift toward a circular economy model offers immense potential for innovation and development in this sector.

About Us:

SNS Insider is a global leader in market research and consulting, shaping the future of the industry. Our mission is to empower clients with the insights they need to thrive in dynamic environments. Utilizing advanced methodologies such as surveys, video interviews, and focus groups, we provide up-to-date, accurate market intelligence and consumer insights, ensuring you make confident, informed decisions.

Contact Us:

Akash Anand – Head of Business Development & Strategy

Phone: +1-415-230-0044 (US) | +91-7798602273 (IND)

0 notes

Text

The global insulation market is projected to grow from USD 61,365 million in 2024 to USD 103,094 million by 2032, representing a compound annual growth rate (CAGR) of 6.7%. The global insulation market has grown significantly in recent years, driven by increasing demand for energy efficiency, sustainability, and the ongoing expansion of construction and industrial sectors. Insulation plays a pivotal role in minimizing energy consumption, reducing greenhouse gas emissions, and enhancing the thermal comfort of buildings and industrial systems. This article delves into the current trends, key market drivers, challenges, and future opportunities shaping the insulation industry.

Browse the full report at https://www.credenceresearch.com/report/insulation-market

Market Overview and Size

As of 2024, the global insulation market is valued at over $60 billion, with projections indicating a compound annual growth rate (CAGR) of around 5% through 2030. The market's growth is primarily attributed to the rising adoption of energy-efficient solutions in residential, commercial, and industrial sectors. The demand for insulation materials such as fiberglass, mineral wool, polyurethane foam, and expanded polystyrene (EPS) has surged due to their effectiveness in thermal and acoustic insulation.

Key Market Drivers

Growing Focus on Energy Efficiency and Sustainability Governments and regulatory bodies worldwide are implementing stringent building codes and energy efficiency standards, pushing for the adoption of high-performance insulation materials. For example, policies like the European Union’s Energy Performance of Buildings Directive (EPBD) and the U.S. Department of Energy's energy codes promote the use of advanced insulation to achieve net-zero energy buildings.

Urbanization and Infrastructure Development Rapid urbanization in developing regions, particularly in Asia-Pacific and the Middle East, is fueling the demand for residential and commercial spaces. This growth drives the need for thermal insulation to enhance energy efficiency in new constructions and retrofitting projects.

Industrial Growth and Temperature Management Industrial processes often require temperature regulation to ensure efficiency and safety. Industries such as petrochemicals, food and beverages, and manufacturing are significant consumers of insulation materials, particularly in cold storage and high-temperature systems.

Climate Change Awareness With climate change becoming a pressing global issue, the insulation market is witnessing an increased focus on reducing carbon footprints. Insulation helps minimize heating and cooling loads, resulting in lower energy consumption and greenhouse gas emissions.

Insulation Types and Applications

Residential and Commercial Buildings Insulation in buildings includes wall, roof, floor, and HVAC insulation to reduce energy loss and improve comfort. Fiberglass and foam-based insulation materials dominate this segment due to their affordability and efficiency.

Industrial Applications High-temperature insulation materials, such as ceramic fibers and mineral wool, are essential in industries requiring thermal resistance for equipment and piping systems.

Acoustic Insulation With rising demand for noise reduction in urban areas and workplaces, acoustic insulation is becoming increasingly important. Materials like rock wool and foam are widely used for their sound-dampening properties.

Challenges Facing the Insulation Market

High Costs of Advanced Materials While traditional materials like fiberglass and EPS are cost-effective, newer, high-performance materials like aerogels are significantly more expensive, limiting their adoption.

Health and Environmental Concerns Certain insulation materials, such as fiberglass and polyurethane foam, have raised concerns over health risks and environmental impact during production and disposal.

Lack of Awareness in Emerging Markets Despite their long-term benefits, insulation adoption in some developing regions remains low due to limited awareness and lack of skilled labor.

Future Outlook

The insulation market is poised for robust growth, driven by technological advancements, government incentives, and increasing awareness of energy efficiency. Innovations in eco-friendly and recyclable materials, such as cellulose insulation and bio-based foams, are expected to reshape the industry. Moreover, smart insulation systems integrated with IoT technology could further enhance energy management and thermal regulation.

Key Player Analysis:

Owens Corning

Knauf Insulation

Saint-Gobain S.A.

Kingspan Group

Rockwool International A/S

BASF SE

Johns Manville Corporation (Berkshire Hathaway)

Dow Inc.

Armacell International S.A.

Huntsman Corporation

Segmentations:

By Product

EPS

XPS

Polyurethane

Polyurethane Foam

Polyvinyl Chloride

Cellulose

Glass Wool

Mineral Wool

Aerogel

Calcium Silicate

Others

By End User

Infrastructure

Construction

Industrial

HVAC

Transportation

Appliances

OEM

Others

By Distribution Channel

Online

Offline

By Geography

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/insulation-market

About Us:

Credence Research is committed to employee well-being and productivity. Following the COVID-19 pandemic, we have implemented a permanent work-from-home policy for all employees.

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

0 notes

Text

A Comprehensive Overview of Fresh Meat Packaging Market Landscape

The global fresh meat packaging market size is anticipated to reach USD 68.43 billion by 2030, according to a new report by Grand View Research, Inc. It is expected to expand at a CAGR of 4.0% during the forecast period. Rising demand for fresh seafood and meat products such as pork and beef coupled with awareness regarding the safety and nutritional value of these products is projected to drive the growth.

Poultry/mutton packaging occupied the maximum market share in 2023. High availability of chicken and mutton products in retail shops has contributed to the growth of this segment. However, beef packaging is expected to witness the fastest CAGR from 2024 to 2030. Beef is one of the excellent sources of protein, which is anticipated to contribute to the rising demand for fresh meat packaging from this segment.

Packaging materials made from polythene occupied the largest market share in 2023. This segment is anticipated to witness the fastest CAGR over the forecast period owing to elasticity and lower production cost of the material. Product innovation using packaging materials like polypropylene is anticipated to propel growth of the fresh meat packaging market during the forecast period.

The Modified Atmosphere Packaging (MAP) was the most prominent technology used for packaging fresh meat in 2023. This chemical-free packaging technology significantly increases the shelf-life of meat, which is expected to drive the growth of the segment during the forecast period.

North America occupied the largest market share in 2023 owing to increased consumption of beef in U.S. According to the National Center for Biotechnology Information (NCBI), the consumption of meat in U.S. is three times more than that of the other countries. This is expected propel the demand for fresh meat packaging. Asia Pacific, on the other hand, is anticipated to witness significant growth, with China being the largest contributor. However, China witnessed a decline in growth for pork meat due to the issues with safety standards, over the past years.

Gather more insights about the market drivers, restrains and growth of the Fresh Meat Packaging Market

Fresh Meat Packaging Market Report Highlights

• Flexible packaging is expected to advance at the fastest CAGR over the forecast period. This is owing to its versatility, convenience, and sustainability benefits.

• The polylactic acid (PLA) segment is expected to register the fastest growth from 2024 to 2030. This is owing to its exceptional sustainability profile, biodegradability, and renewable resource-based composition.

• Asia Pacific led the market with a revenue share of 42.4% in 2023. This is attributed to the region's growing population, increasing urbanization, and rising disposable income levels, which have driven the demand for convenient, safe, high-quality fresh meat products.

Fresh Meat Packaging Market Segmentation

Grand View Research has segmented the global fresh meat packaging market report based on type, material, and region:

Fresh Meat Packaging Type Outlook (Volume, Kilotons; Revenue, USD Billion, 2018 - 2030)

• Flexible

o Pouches & Bags

o Wraps & Films

• Rigid

o Clamshells

o Trays & Boxes

o Others

Fresh Meat Packaging Material Outlook (Volume, Kilotons; Revenue, USD Billion, 2018 - 2030)

• Plastic

o Polypropylene (PP)

o Polyethylene (PE)

o Polystyrene (PS)

o Polyvinyl Chloride (PVC)

o Polyethylene Terephthalate (PET)

o Others

• Paper & Paperboard

• Bagasse

• Polylactic Acid

• Others

Fresh Meat Packaging Regional Outlook (Volume, Kilotons; Revenue, USD Billion, 2018 - 2030)

• North America

o U.S.

o Canada

o Mexico

• Europe

o UK

o Germany

o France

o Italy

o Spain

• Asia Pacific

o Japan

o India

o China

o Australia

o South Korea

o Southeast Asia

• Latin America

o Brazil

o Argentina

• Middle East & Africa

o South Africa

o Saudi Arabia

o UAE

Order a free sample PDF of the Fresh Meat Packaging Market Intelligence Study, published by Grand View Research.

#Fresh Meat Packaging Market#Fresh Meat Packaging Market Size#Fresh Meat Packaging Market Share#Fresh Meat Packaging Market Analysis#Fresh Meat Packaging Market Growth

0 notes

Text

0 notes

Text

Flame Retardants Market Overview Analysis, Trends, Share, Size, Type & Future Forecast to 2034

Flame retardants are chemicals added to materials such as plastics, textiles, and coatings to inhibit ignition and prevent the spread of fire. They play a vital role in enhancing safety in industries like construction, electronics, and transportation.

The flame retardant market is expected to develop at a compound annual growth rate (CAGR) of 7.2% between 2024 and 2034, reaching USD 16,462.41 million in 2034, according to an average growth pattern. The market is projected to be at USD 9,845.59 million in 2024.

Get a Sample Copy of Report, Click Here: https://wemarketresearch.com/reports/request-free-sample-pdf/flame-retardants-market/1589

Types of Flame Retardants

Flame retardants can be classified into several categories based on their chemical composition and application:

Halogenated Flame Retardants (HFRs):

Contain chlorine or bromine.

Effective but controversial due to their potential environmental and health hazards.

Common in plastics and textiles.

Non-Halogenated Flame Retardants:

Phosphorus-based: Used in epoxy resins, polyurethane, and textiles.

Nitrogen-based: Effective for thermoplastics and synthetic fibers.

Mineral-based: Includes aluminum hydroxide and magnesium hydroxide, which act as heat absorbers.

Inorganic Flame Retardants:

Provide thermal stability and are used in applications where halogen-free products are required.

Intumescent Flame Retardants:

Expand when exposed to heat, forming a char layer that protects the underlying material.

Applications Across Industries

Construction: Used in insulation materials (polystyrene, polyurethane foams) and structural components to meet building codes for fire resistance.

Electronics & Electrical Equipment:

Protects circuit boards, cables, and plastic casings.

Ensures compliance with safety standards such as RoHS (Restriction of Hazardous Substances) and WEEE (Waste Electrical and Electronic Equipment).

Automotive & Transportation:

Essential in vehicle interiors, upholstery, and composite materials for safety.

Lightweight flame retardant materials help reduce vehicle weight and improve fuel efficiency.

Textiles:

Flame retardant treatments are applied to fabrics used in furniture, curtains, and protective clothing for industries like firefighting and military.

Aerospace:

Critical for materials used in aircraft interiors, cables, and structural components to meet stringent fire safety norms.

Flame Retardants Market Key Drivers

Rising Fire Safety Regulations: Governments and international organizations are imposing stricter fire safety norms, fueling the adoption of flame retardants in construction and consumer goods.

Growth in End-Use Industries:

Construction: Flame retardants are crucial for insulation materials and structural components.

Electronics: Their use in printed circuit boards, casings, and wires is essential for preventing fire hazards.

Transportation: Flame retardants enhance safety in automobiles, aircraft, and trains.

Urbanization and Infrastructure Development: The rapid growth in construction activities globally, especially in developing regions, is boosting demand.

Increased Awareness of Fire Hazards: Growing awareness about fire safety in households, workplaces, and public spaces supports market expansion.

Flame Retardants Market Challenges and Opportunities

Challenges:

High cost of production and raw materials for eco-friendly flame retardants.

Limited awareness and adoption in small-scale industries.

Balancing performance with environmental impact.

Opportunities:

Expanding markets in Asia-Pacific, Latin America, and Africa due to urbanization.

Development of multifunctional flame retardants that offer additional properties like UV resistance or antimicrobial effects.

Flame Retardants Market Segmentation,

By Type:

Alumina Trihydrate

Brominated Flame Retardant

Antimony Trioxide

Phosphorous Flame Retardant

Others

By Application:

Unsaturated Polyester Resins

Epoxy Resins

PVC

Rubber

Polyolefins

Others (Engineering Thermoplastics and PET)

By End User Industry:

Construction

Automotive & Transportation

Electronics

Others (Textiles, Aerospace, and Adhesives)

By Region:

North America

Latin America

Europe

East Asia

South Asia

Oceania

Middle East and Africa

Key companies profiled in this research study are,

The Flame Retardants Market is dominated by a few large companies, such as

BASF SE

Clariant AG

Huntsman Corporation

Israel Chemicals Limited (ICL)

Albemarle Corporation

·DuPont de Nemours, Inc.

Arkema S.A.

Solvay S.A.

Dow Chemical Company

Ferro Corporation

Nabaltec AG

Shanghai Pret Composites Co., Ltd.

Jiangsu Kuaima Chemical Co., Ltd.

Flame Retardants Industry: Regional Analysis

Asia Pacific Market Forecast

Asia Pacific will account for over 36% of the global flame retardant market in 2023. Due to the fast industrialization, urbanization, and expansion of construction, the Asia-Pacific region has the greatest percentage of flame retardants and the fastest rate of growth. The growing demand for electronics, textiles, and cars in countries like China and India is largely responsible for the company's growth.

European Market Forecast

The demand for non-toxic flame retardants is being driven by Europe's well-known emphasis on ecologically friendly activities and laws. The use of specific flame retardants is affected by stringent market-supporting rules like REACH (Registration, Evaluation, Authorization and Restriction of Chemicals). Flame retardants are widely used in the area's construction and automobile industries.

North America Forecast

The market for flame retardants is dominated by North America because of the region's strict fire safety laws, especially in the building and automotive sectors. The market is expanding as a result of the presence of significant producers and ongoing developments in flame retardant chemicals. Because of environmental concerns, non-halogenated flame retardants are becoming more and more popular in the region.

Conclusion:

The Flame Retardants Market plays a vital role in ensuring safety across diverse industries, from construction to electronics and transportation. As regulatory standards tighten and awareness about fire hazards grows, the demand for innovative, efficient, and eco-friendly flame retardant solutions is set to rise. While challenges such as environmental concerns and high costs of alternatives persist, advancements in technology, including bio-based and nanotechnology-based solutions, offer promising opportunities for sustainable growth.

With rapid urbanization and industrialization in emerging economies, coupled with the global push for safer, greener materials, the flame retardants market is poised for significant expansion in the coming years. Businesses that prioritize innovation and compliance with environmental regulations will be best positioned to thrive in this evolving landscape.

0 notes

Text

Revolutionizing Medicine Delivery: The Role of Cutting-Edge Pharmaceutical Packaging

Pharmaceutical Packaging Industry Overview

The global pharmaceutical packaging market size is expected to reach USD 265.70 billion by 2030, registering a CAGR of 9.7% from 2024 to 2030, according to a new report by Grand View Research, Inc., The increasing prevalence of chronic diseases coupled with the growth of the pharmaceutical industry is anticipated to augment the consumption of pharmaceutical packaging products.

Ban on counterfeit products in North America and Europe is expected to be a major driver for the market as major companies are likely to invest heavily in anti-counterfeit packaging products. Blow-Fill-Seal (BFS) technology allows customized design for high-quality containers with tamper-evident closures in multiple shapes and sizes. Therefore, the growing demand for anti-counterfeiting packaging along with the advent of technology is likely to support the growth of tamper-evident pharmaceutical packaging.

Companies are focusing on using sustainable materials for packaging owing to the rising concerns about the generation of packaging waste that is difficult to degrade. Bioplastic is likely to gain traction in the market as it is derived from renewable plant-based sources and is biodegradable unlike plastics and polymers derived from fossil fuels. In May 2022, SGD Pharma has launched the industry’s first Ready-to-Use sterile 100 ml molded glass vials. It is manufactured with SG EZ-fill packaging technology. Such novel sustainable packaging solutions are expected to boost the growth of the market.

Gather more insights about the market drivers, restrains and growth of the Pharmaceutical Packaging Market

Pharmaceutical manufacturers are likely to prefer blister packaging for tablets and capsules as these are more sustainable with minimal usage of packaging material as compared to rigid bottles. In addition, the transparency of blister packs provides a clear product display and provides tamper-resistant features. The outbreak of COVID-19 has significantly increased the demand for various pharmaceutical drugs across the world, thereby propelling the demand for pharmaceutical manufacturing and packaging. Rapid development and production of the vaccine in the year 2020 are anticipated to increase pharmaceutical manufacturing considerably, primarily benefitting the manufacturers of packaging vials in the near future.

Market players have been trying to increase their production capabilities as well as expand their geographic reach. In addition, companies are introducing and investing in high-tech packaging solutions in the changing environment. For instance, In April 2021, Amcor plc announced the development of recyclable Polyethylene-based thermoform blister packaging under the brand name AmSky. The development is aimed at sustainable packaging that can reduce carbon footprint. The product is expected to reduce carbon footprint up to 70%. Companies are expected to invest significantly in such developments in the coming years to strengthen their market position.

Browse through Grand View Research's Plastics, Polymers & Resins Industry Research Reports.

The global polytetrafluoroethylene market size was valued at USD 3.63 billion in 2023 and is projected to grow at a CAGR of 5.5% from 2024 to 2030.

The global medical grade silicone market size was valued at USD 601.7 million in 2024 and is expected to register a CAGR of 7.4% from 2025 to 2030.

Pharmaceutical Packaging Market Segmentation

Grand View Research has segmented the pharmaceutical packaging market on the basis of on material, product, drug delivery mode, end-use, and region:

Pharmaceutical Packaging Material Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

Plastics & Polymers

Polyvinyl Chloride (PVC)

Polypropylene (PP)

Homo

Random

Polyethylene Terephthalate (PET)

Polyethylene (PE)

HDPE

LDPE

LLDPE

Polystyrene (PS)

Others

Paper & Paperboard

Glass

Aluminium Foil

Others

Pharmaceutical Packaging Product Outlook (Revenue, USD Million, 2018 - 2030)

Primary

Plastic Bottles

Caps & Closures

Parenteral Containers

Syringes

Vials & Ampoules

Others

Blister Packs

Prefillable Inhalers

Pouches

Medication Tubes

Others

Secondary

Prescription Containers

Pharmaceutical Packaging Accessories

Tertiary

Pharmaceutical Packaging Drug Delivery Mode Outlook (Revenue, USD Million, 2018 - 2030)

Oral Drugs

Injectables

Topical

Ocular/ Ophthalmic

Nasal

Pulmonary

Transdermal

IV Drugs

Others

Pharmaceutical Packaging End-use Outlook (Revenue, USD Million, 2018 - 2030)

Pharma Manufacturing

Contract Packaging

Retail Pharmacy

Institutional Pharmacy

Pharmaceutical Packaging Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

US

Canada

Mexico

Europe

Germany

UK

France

Italy

Spain

Russia

Turkey

Asia Pacific

China

India

Japan

South Korea

Australia

Southeast Asia

Central & South America

Brazil

Argentina

Middle East & Africa

Saudi Arabia

UAE

South Africa

Egypt

Key Companies profiled:

Amcor plc

Becton, Dickinson, and Company

AptarGroup, Inc.

Drug Plastics Group

Gerresheimer AG

Schott AG

Owens Illinois, Inc.

West Pharmaceutical Services, Inc.

Berry Global, Inc.

WestRock Company

SGD Pharma

International Paper

Comar, LLC

Key Pharmaceutical Packaging Company Insights

The global market is highly competitive owing to the presence of numerous players across the globe. Moreover, key players are consolidating their market positions mainly by acquisitions, which is further intensifying the competition.

In November 2023, Amcor Plc, a renowned global company known for its development and production of environmentally conscious packaging solutions, revealed a Memorandum of Understanding (MOU) with NOVA Chemicals Corporate, a leading producer of sustainable polyethylene. The agreement includes the procurement of mechanically recycled polyethylene resin (rPE) from NOVA Chemicals Corporate, which will be utilized in the production of flexible packaging films. This initiative aligns with Amcor's dedication to promoting packaging circularity by increasing the utilization of rPE in flexible packaging applications.

In July 2023, Constantia Flexibles introduced a new pharmaceutical packaging solution called REGULA CIRC, which utilizes coldform foil. The packaging replaces conventional PVC with a PE sealing layer, resulting in a reduction in plastic content while increasing the proportion of aluminum. This optimization not only enhances the sustainability of the packaging but also improves material recovery during recycling processes.

In April 2023, Südpack introduced its PharmaGuard blister, a polypropylene-based blister packaging. This new product offers an outstanding water vapor barrier along with effective barrier resistance against UV and oxygen.

Order a free sample PDF of the Pharmaceutical Packaging Market Intelligence Study, published by Grand View Research.

0 notes

Text

Ethylbenzene Market Progress: Exploring Digital Transformation and Circular Economy Initiatives in 2024

The global ethylbenzene market is undergoing a significant transformation, driven by evolving consumer preferences, technological advancements, and regulatory changes. As a key intermediate in the production of styrene, which is a building block for numerous plastics and resins, ethylbenzene plays a vital role in the modern industrial economy. Here, we delve into the emerging trends that are shaping the future of this dynamic market.

Growing Demand for Styrene-Based Products-

Ethylbenzene’s primary use lies in the production of styrene monomer, which is integral to manufacturing polystyrene and acrylonitrile butadiene styrene (ABS). These materials find extensive applications in packaging, automotive components, electronics, and construction. With rapid industrialization in developing countries, the demand for styrene-based products is expected to see sustained growth. This, in turn, propels the ethylbenzene market forward.

Technological Advancements in Production Processes

The production of ethylbenzene has seen a marked improvement with the advent of innovative technologies. Catalytic processes are becoming more efficient, reducing operational costs and environmental impact. Companies are also exploring bio-based feedstocks as sustainable alternatives to conventional petroleum-based processes, addressing the growing demand for green chemistry in the industry.

Regulatory Impact on the Market

Stringent environmental regulations have a dual impact on the ethylbenzene market. On one hand, they drive innovation as manufacturers seek compliance through eco-friendly practices. On the other, they present challenges by increasing operational costs. For instance, regulations related to volatile organic compounds (VOCs) and emissions require manufacturers to adopt advanced mitigation technologies, adding to their capital expenditure.

Regional Market Dynamics-

The ethylbenzene market exhibits significant regional disparities. Asia-Pacific remains the dominant region, driven by China and India’s expanding manufacturing and construction sectors. Meanwhile, North America and Europe are focusing on sustainability and advanced materials, creating opportunities for high-performance styrene derivatives. Emerging markets in Latin America and Africa are also showing promise, with growing industrial activities and investment in infrastructure.

Sustainability and Circular Economy Initiatives-

Sustainability has emerged as a pivotal trend in the ethylbenzene market. Companies are investing in recycling technologies to recover styrene from post-consumer waste, reducing the reliance on virgin ethylbenzene. Such circular economy initiatives not only align with global environmental goals but also offer cost advantages in the long term.

Challenges in Raw Material Supply-

The availability and cost of raw materials, particularly benzene and ethylene, are critical factors influencing ethylbenzene production. Geopolitical tensions, trade restrictions, and fluctuating crude oil prices contribute to market volatility. Companies are increasingly diversifying their supply chains and exploring alternative sources to mitigate these risks.

Increasing Focus on R&D and Innovation-

Research and development (R&D) efforts are driving the discovery of novel applications and improved production methods for ethylbenzene. From advanced catalysts to process optimization, these innovations promise to enhance efficiency and broaden the application scope of ethylbenzene and its derivatives.

Competitive Landscape and Strategic Collaborations-

The ethylbenzene market is characterized by intense competition, with major players focusing on mergers, acquisitions, and partnerships to strengthen their market presence. Collaborations between petrochemical giants and research institutions are fostering innovation and expanding market opportunities.

Digital Transformation in Operations-

Digital tools, including artificial intelligence (AI) and big data analytics, are being leveraged to optimize production processes and supply chain management. Real-time monitoring and predictive maintenance are enabling manufacturers to reduce downtime and improve overall operational efficiency.

Future Outlook-

The future of the ethylbenzene market appears promising, with robust demand across various end-use industries and a strong focus on sustainability and technological innovation. While challenges persist, such as regulatory pressures and raw material volatility, the industry’s adaptability and commitment to progress ensure its continued growth.

0 notes

Text

Expanded Polystyrene (EPS) Packaging Market: Growth, Trends, and Future Outlook

Expanded Polystyrene (EPS) packaging has become a cornerstone in various industries due to its lightweight, cost-effectiveness, and excellent protective properties. As the global demand for efficient packaging solutions rises, the EPS packaging market is poised for significant growth. This article delves into the current market landscape, key drivers, segmentation, regional insights, and future prospects of the EPS packaging industry.

Market Overview

As of 2023, the global EPS packaging market was valued at approximately USD 10.05 billion. Projections indicate that this market will reach around USD 13.58 billion by 2030, exhibiting a compound annual growth rate (CAGR) of 4.40% during the forecast period.

Request Sample Report

Key Market Drivers

E-commerce Expansion: The surge in online shopping has heightened the need for reliable packaging solutions that ensure product safety during transit. EPS packaging, with its shock-absorbing properties, has become a preferred choice for protecting goods in the e-commerce sector.

Growth in the Retail Sector: The expanding retail industry demands efficient packaging to preserve product integrity and extend shelf life. EPS packaging offers insulation and protection, making it suitable for a wide range of retail products.

Sustainability Initiatives: EPS is recyclable and contributes to reducing environmental impact. Advancements in recycling technologies have enhanced the sustainability profile of EPS packaging, aligning with global environmental goals.

Market Segmentation

The EPS packaging market can be segmented based on density, application, and region.

By Density:

15.0-19.9 kg/m³: Suitable for lightweight applications requiring moderate protection.

20.0-29.9 kg/m³: Ideal for general-purpose packaging with balanced strength and cushioning.

30-34.9 kg/m³ and above: Used for heavy-duty applications demanding high durability and impact resistance.

By Application:

Food and Beverage: EPS packaging maintains temperature and protects perishable items, ensuring food safety and quality.

Electronic Appliances: Provides cushioning and protection for delicate electronic devices during shipping and handling.

Healthcare: Ensures the safe transport of medical equipment and temperature-sensitive pharmaceuticals.

Others: Includes applications in automotive parts, consumer goods, and industrial products.

Regional Insights

North America: A mature market with steady demand, driven by the robust e-commerce and electronics sectors.

Asia Pacific: Expected to witness the highest growth rate due to rapid industrialization, urbanization, and increasing disposable incomes in countries like China and India.

Europe: Focuses on sustainable packaging solutions, with stringent regulations promoting the use of recyclable materials like EPS.

Middle East & Africa: Emerging markets with growing demand for efficient packaging solutions in the food and construction industries.

Competitive Landscape