#Drug Allergens Market Growth

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has 4 main sources of revenue.

Text

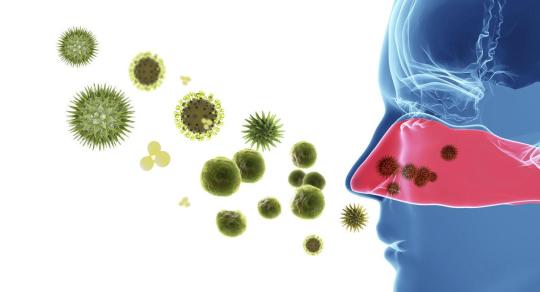

Allergy Diagnostics Industry worth $9.8 billion by 2029, with a CAGR of 11.0%

Allergy Diagnostics Market in terms of revenue was estimated to be worth $5.3 billion in 2024 and is poised to reach $9.8 billion by 2029, growing at a CAGR of 11.0% from 2024 to 2029 according to a new report by MarketsandMarkets™.

Download PDF Brochure

Browse in-depth TOC on “Allergy Diagnostics Market”

248 — Tables

57 — Figures

307 — Pages

The consumables segment is expected to account for the largest share in 2023.

The Allergy Diagnostics market, by product & service, has been segmented into consumables, instruments, and services. The consumables segment accounted for the largest share of the Allergy Diagnostics market in 2023. This segment is also anticipated to experience significant growth over the projected period. The increasing demand for rapid diagnosis of allergic patients which is driven by increasing number of allergic cases can be attributed for the larger share of this segment during the forecast period.

In Vivo test segment held the largest market share in the Allergy Diagnostics market.

Based on the test type, the Allergy Diagnostics market is segmented into in vivo tests and in vitro tests. In 2023, the in vivo tests segment accounted for the largest share of the Allergy Diagnostics market. The growth of this segment is mainly driven by the growing adoption of various in vivo tests, such as skin prick tests which is considered as the first line of diagnosis for allergy and favorable government support and guidelines.

Inhaled allergy segment held the largest market share in the Allergy Diagnostics market.

Based on the allergen, the Allergy Diagnostics market is segmented into inhaled allergens, food allergens, drug allergens, and other allergens. In 2023, the inhaled allergens segment accounted for the largest share of the Allergy Diagnostics market due to the rising environmental pollution, rising home dust & mites coupled with other factors such as pollen, fungus, mold, and dust, and switching lifestyles, including rise in indoor activities and exposure to indoor allergen.

North America dominates the global Allergy Diagnostics market

Based on the region, the Allergy Diagnostics market is segmented into North America, Europe, Asia Pacific, Latin America, Middle East & Africa. North America market is driven by availability of technologically advanced products and growing research on allergy by companies and government. The Asia Pacific segment is projected to register the highest CAGR during the forecast period. Developing healthcare infrastructure, lifestyle changes and climatic conditions, increased ozone and industrial pollution levels, and the rising demand for quality medical care are some of the major factors driving the growth of this regional market.

Request Sample Pages

Allergy Diagnostics Market Dynamics:

Drivers:

1. High incidence and heavy economic burden of allergic diseases

Restraints:

1. High pricing of allergy diagnostic instruments

Opportunities:

1. Integration of AI in allergy diagnosis

Challenge:

1. Shortage of allergists

Key Market Players of Allergy Diagnostics Industry:

Major players in Allergy Diagnostics market include Thermo Fisher Scientific Inc., (US), Siemens Healthineers AG (Germany), Danaher (US), and Canon, Inc. (Japan), Minaris Medical America, Inc. (US).

Breakdown of supply-side primary interviews by company type, designation, and region:

· By Company Type: Tier 1 (20%), Tier 2 (45%), and Tier 3 (35%)

· By Designation: C-level (30%), Director-level (20%), and Others (50%)

· By Region: North America (36%), Asia- Pacific (27%), Europe (25%), and Latin America- (7%) and MEA-(5%)

Get 10% Free Customization on this Report:

Recent Developments of Allergy Diagnostics Industry:

· In 2023, Canon has completed share transfer procedures with Resonac Corporation. This share transfer is intended to be used to purchase the Resonac subsidiaries Minaris Medical Co., Ltd. and Minaris Medical America, Inc. (collectively, “Minaris Medical”). After this share acquisition is finished, Minaris Medical — which runs companies that deal with automated analytical tools and in vitro diagnostic reagents — will be consolidated under Canon Medical.

· In 2023, Romer Labs Division Holding GmbH (Austria) acquired CPAK INTER Co., Ltd. (Thailand), a long-time distributor of Romer Labs solutions based in Bangkok. With the acquisition, Romer Labs has achieved yet another significant milestone in the quickly expanding Asian food safety industry.

· In 2022, The US Food & Drug Administration (FDA) has cleared ImmunoCAP Specific IgE (sIgE) Allergen Components for use in in vitro diagnostic testing for wheat and sesame allergies, according to a statement from Thermo Fisher Scientific, Inc. (US).

Allergy Diagnostics Market — Key Benefits of Buying the Report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall Allergy Diagnostics market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

· Analysis of key drivers (global rise in prevalence and heavy economic burden of allergic illnesses, growing environmental pollution, and insurance coverage), restraints (high costs of analyzers and access is limited to healthcare services), opportunities (use of mHealth and integration of AI in allergy diagnosis), and challenges (a few number of allergists and challenges during diagnosis of allergy) influencing the growth of the Allergy Diagnostics market

· Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the Allergy Diagnostics market.

· Market Development: Comprehensive information about lucrative markets — the report analyses the Allergy Diagnostics market across varied regions.

· Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the Allergy Diagnostics market

· Competitive Assessment: In-depth assessment of market ranking, growth strategies, and service offerings of leading players like Thermo Fisher Scientific Inc., (US), Siemens Healthineers AG (Germany), Danaher (US), and Canon, Inc. (Japan) [Minaris Medical America, Inc. (US)], among others in the Allergy Diagnostics market strategies.

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America’s best management consulting firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Earlier this year, we made a formal transformation into one of America’s best management consulting firms as per a survey conducted by Forbes.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines — TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the ‘GIVE Growth’ principle, we work with several Forbes Global 2000 B2B companies — helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Contact:

Mr. Rohan Salgarkar

MarketsandMarkets Inc.

1615 South Congress Ave.

Suite 103, Delray Beach, FL 33445

USA : 1–888–600–6441

UK +44–800–368–9399

Email: [email protected]

Visit Our Website: https://www.marketsandmarkets.com/

Content Source:

#Allergy Diagnostics Market#Inhaled Allergens Market Size#Food Allergens Market Share#Drug Allergens Market Growth

0 notes

Text

Isolator Gloves Market Size, Type, segmentation, growth and forecast 2023-2030

Isolator Gloves Market

The Isolator Gloves Market is expected to grow from USD 141.10 Million in 2022 to USD 228.10 Million by 2030, at a CAGR of 7.11% during the forecast period.

Get the Sample Report: https://www.reportprime.com/enquiry/sample-report/11101

Isolator Gloves Market Size

Isolator Gloves are a type of protective gloves that are designed to provide a barrier between the wearer's hands and harmful substances such as chemicals, viruses, and bacteria. The Isolator Gloves market research report includes an analysis of the market segment based on type, application, and region. The types of Isolator Gloves include Nitrile, Hypalon, EPDM, Neoprene, Latex, and Butyl. The primary applications of Isolator Gloves are in Electronics, Pharmaceutical, Food, Chemical, and Laboratory industries. The report covers the market players such as Ansell, PIERCAN, Renco Corporation, Safetyware Group, Inert Corporation, Jung Gummitechnik, Terra Universal, Honeywell, Nichwell, and Hanaki Rubber. The report also covers regulatory and legal factors specific to market conditions. Isolator Gloves are subject to strict regulations due to their use in critical industries, and market players must ensure compliance with standards set by regulatory bodies. The report provides an in-depth analysis of the Isolator Gloves market, including its market size, growth rate, competitive landscape, and future prospects.

Isolator Gloves Market Key Player

Ansell

PIERCAN

Renco Corporation

Safetyware Group

Inert Corporation

Buy Now & Get Exclusive Discount on this https://www.reportprime.com/enquiry/request-discount/11101

Isolator Gloves Market Segment Analysis

The Isolator Gloves market caters to a niche customer base, which includes pharmaceutical manufacturers, biotechnology companies, healthcare institutions, and medical device manufacturers. These gloves are extensively used in cleanroom environments to maintain hygiene, prevent contamination and ensure aseptic handling of drug substances and medical devices.

The driving factors for revenue growth in the Isolator Gloves market are the increasing demand for sterile pharmaceutical products, the growing prevalence of chronic diseases, and the strict regulatory requirements for cleanroom environments. Furthermore, the Isolator Gloves market is experiencing growth due to the ongoing research and development activities and technological advancements in the field of medical devices.

The latest trends followed in the Isolator Gloves market include the adoption of non-latex gloves to reduce the risk of latex allergy, increasing demand for powder-free gloves to minimize the transfer of allergens, and the use of vibration-dampening gloves to reduce hand fatigue in workers. Moreover, manufacturers are focusing on developing gloves with improved tactile sensitivity and flexibility, which can provide better user comfort and dexterity.

The major challenges faced by the Isolator Gloves market include the high cost of raw materials and production, stringent regulations for cleanroom environments, and increasing competition from local players in the market. Additionally, the COVID-19 pandemic has disrupted the supply chain and logistics operations, resulting in the temporary closure of manufacturing facilities and delays in delivering products to customers.

The report's main findings suggest that the Isolator Gloves market is projected to grow at a significant rate over the forecast period due to the increasing demand for sterile pharmaceutical products and the stringent regulatory requirements for cleanroom environments. Furthermore, the report recommends that manufacturers focus on developing eco-friendly and biodegradable gloves, as the demand for sustainable products is increasing. Moreover, manufacturers should prioritize improving their supply chain management and logistics operations to meet the market demands and maintain a competitive edge.

In conclusion, the Isolator Gloves market caters to a niche customer base, and the major factors driving revenue growth are the increasing demand for sterile pharmaceutical products and the strict regulatory requirements for cleanroom environments. The Isolator Gloves market is experiencing growth due to technological advancements and ongoing research and development activities. The latest trends in the market encompass the adoption of non-latex gloves, powder-free gloves, and vibration-dampening gloves. However, the Isolator Gloves market is also facing challenges due to high production costs, stringent regulatory requirements, and increasing competition from local players. The report's main recommendations include focusing on sustainable products, improving supply chain management, and logistics operations.

This report covers impact on COVID-19 and Russia-Ukraine wars in detail.

Purchase This Report: https://www.reportprime.com/checkout?id=11101&price=3590

Market Segmentation (by Application):

Electronics

Pharmaceutical

Food

Chemical

Laboratory

Information is sourced from www.reportprime.com

2 notes

·

View notes

Text

The Allergy Diagnostics Industry: Advancing Precision in Allergy Detection and Management

The allergy diagnostics industry plays a pivotal role in addressing a growing global health concern—allergies. Allergies impact millions of people worldwide, manifesting as respiratory issues, skin reactions, food intolerances, and even life-threatening anaphylaxis. As the prevalence of allergic diseases continues to rise due to environmental changes, urbanization, and genetic predisposition, effective diagnostics have become essential for accurate detection, prevention, and management of allergies.

The allergy diagnostics market has witnessed significant growth due to technological advancements, increased healthcare awareness, and the demand for personalized treatment. The Allergy Diagnostics Market is estimated to be valued at USD 6.31 billion in 2024 and is projected to reach USD 10.76 billion by 2029, growing at a compound annual growth rate (CAGR) of 11.25% during the forecast period (2024–2029).

Understanding Allergy Diagnostics

Allergy diagnostics involves identifying allergens that trigger immune system responses in individuals. Allergens can range from pollen, dust mites, and animal dander to specific foods, drugs, and insect venom. When exposed to allergens, sensitive individuals may exhibit symptoms such as sneezing, itching, swelling, or even severe reactions like anaphylaxis.

Accurate allergy diagnostics help healthcare providers determine the root cause of allergic reactions, enabling targeted treatment plans, including allergen avoidance, immunotherapy, and symptom management. Diagnostic methods typically include:

In Vivo Testing: Skin prick tests (SPT), intradermal tests, and patch tests conducted directly on patients.

In Vitro Testing: Blood-based tests like ImmunoCAP or enzyme-linked immunosorbent assays (ELISA) that identify allergen-specific Immunoglobulin E (IgE) antibodies.

With growing demand for precise and efficient allergy diagnostics, the industry is undergoing significant innovation to enhance accuracy and accessibility.

Key Drivers of Growth in the Allergy Diagnostics Industry

1. Increasing Prevalence of Allergic Diseases

The rising incidence of allergic conditions such as asthma, allergic rhinitis, eczema, and food allergies is a major driver for the allergy diagnostics industry. According to organizations like the World Health Organization (WHO), hundreds of millions of people suffer from allergies globally, with numbers expected to rise further due to environmental pollution, climate change, and urbanization.

Food allergies, in particular, have become a growing concern, especially among children, prompting a need for early and precise diagnostics to prevent life-threatening reactions.

2. Technological Advancements in Allergy Testing

The allergy diagnostics industry has seen significant technological advancements that enhance the accuracy, speed, and convenience of testing. In vitro testing methods, such as molecular diagnostics and advanced IgE assays, provide reliable results with minimal patient discomfort. Innovations like automated laboratory systems and point-of-care devices are transforming allergy diagnostics, making them more accessible and efficient.

Additionally, the development of multiplex testing allows clinicians to screen for multiple allergens simultaneously, saving time and resources while delivering comprehensive insights.

3. Growing Awareness About Allergy Management

Heightened awareness about allergies and their potential complications has led to increased adoption of diagnostic testing. Public health campaigns, patient education initiatives, and media coverage have emphasized the importance of identifying allergens early to mitigate severe reactions. Parents, in particular, are becoming more proactive in testing their children for food and environmental allergies.

Healthcare providers are also placing greater focus on preventive care, driving demand for reliable diagnostics as part of early allergy management strategies.

4. Demand for Personalized Allergy Treatments

The trend toward personalized medicine is fueling growth in the allergy diagnostics market. Allergy tests provide detailed insights into an individual’s sensitivities, enabling healthcare providers to tailor treatment plans. Personalized immunotherapy, antihistamines, and allergen avoidance strategies are more effective when based on accurate diagnostic data, improving patient outcomes.

5. Rising Healthcare Expenditure

Increased healthcare spending, particularly in developed economies, is driving investments in advanced diagnostic tools and technologies. Patients and healthcare providers are now more willing to adopt innovative allergy testing solutions that enhance diagnostic precision and improve long-term allergy management.

Challenges in the Allergy Diagnostics Industry

1. Lack of Awareness in Developing Regions

While awareness about allergies is rising globally, it remains limited in low- and middle-income countries. Many individuals in developing regions may not recognize allergy symptoms or seek timely diagnostic testing, leading to underdiagnosis and inadequate treatment. Improving awareness and accessibility remains a key challenge for industry stakeholders.

2. High Cost of Advanced Testing

Advanced allergy diagnostics, particularly molecular tests and multiplex assays, can be expensive, limiting their adoption in resource-constrained settings. While these methods provide high accuracy, affordability remains a barrier for both healthcare providers and patients.

3. Limited Access to Skilled Professionals

Effective allergy diagnostics require trained professionals to conduct tests, interpret results, and recommend appropriate treatment. A shortage of allergists, immunologists, and laboratory technicians in certain regions hampers the delivery of quality diagnostic services.

4. Regulatory Hurdles

Allergy diagnostic tools must meet stringent regulatory standards for safety, accuracy, and efficacy. Navigating these regulatory processes can delay product launches and market entry, particularly for new technologies and innovations.

Trends Shaping the Allergy Diagnostics Market

1. Rise of Molecular Allergy Diagnostics

Molecular diagnostics are revolutionizing allergy testing by providing detailed information about specific allergenic proteins within a substance. This precision allows clinicians to identify cross-reactivity between allergens and develop highly targeted treatment plans. Molecular diagnostics are gaining popularity for their ability to improve diagnostic accuracy and inform personalized care.

2. Increasing Adoption of Point-of-Care Testing

Point-of-care (POC) allergy testing is emerging as a convenient solution for rapid diagnosis, especially in primary care settings. POC devices provide quick results with minimal discomfort, enabling timely diagnosis and treatment without the need for extensive laboratory infrastructure.

3. Focus on Pediatric Allergy Testing

The rising prevalence of allergies among children has prompted a strong focus on pediatric allergy diagnostics. Non-invasive, painless testing methods are being developed to address the unique needs of pediatric patients, encouraging early diagnosis and intervention.

4. Integration of Artificial Intelligence (AI) in Diagnostics

The integration of AI and machine learning in allergy diagnostics is enhancing result interpretation and clinical decision-making. AI-powered algorithms analyze diagnostic data to identify patterns and predict allergic sensitivities, improving accuracy and efficiency.

5. Growing Use of Home-Based Allergy Testing Kits

The COVID-19 pandemic accelerated the adoption of home-based diagnostic tools, including allergy testing kits. These kits allow patients to collect samples at home and send them to labs for analysis, offering convenience and accessibility while maintaining diagnostic accuracy.

Conclusion

The allergy diagnostics industry is a critical component of modern healthcare, addressing the growing burden of allergic diseases worldwide. Driven by rising allergy prevalence, technological advancements, and increasing awareness, the industry is witnessing rapid innovation and growth.

While challenges such as affordability and limited access persist, trends like molecular diagnostics, AI integration, and point-of-care testing are reshaping the landscape, making allergy diagnostics more precise, accessible, and patient-friendly.

As healthcare systems embrace preventive care and personalized medicine, allergy diagnostics will play an increasingly vital role in improving patient outcomes, enhancing quality of life, and reducing the healthcare burden associated with allergic diseases. By advancing diagnostic accuracy and accessibility, the industry is empowering individuals to better manage allergies and enjoy healthier lives. For a detailed overview and more insights, you can refer to the full market research report by Mordor Intelligence: https://www.mordorintelligence.com/industry-reports/allergy-diagnostics-market

#Allergy Diagnostics Market#Allergy Diagnostics Market Size#Allergy Diagnostics Market Share#Allergy Diagnostics Market Analysis#Allergy Diagnostics Market Report

0 notes

Text

Cleanroom Disposable Gloves Market Growth Driven by Demand for High Standards of Hygiene and Safety

The cleanroom disposable gloves market is gaining significant traction due to its critical role in maintaining sterile environments across several sectors. Cleanroom gloves are designed to offer safety, cleanliness, and protection when handling sensitive materials, making them indispensable in industries such as pharmaceuticals, biotechnology, electronics, healthcare, and food processing.

Growth of the Cleanroom Disposable Gloves Market

The cleanroom disposable gloves market is witnessing rapid growth, driven by increasing awareness regarding hygiene and safety, stringent regulations for the healthcare and pharmaceutical industries, and the rising demand for infection control. These gloves are essential in preventing contamination during manufacturing, research, and development, especially in highly sensitive environments like cleanrooms that demand the highest standards of cleanliness.

The healthcare sector, in particular, remains one of the primary consumers of cleanroom gloves. Given the growing importance of infection control due to the global rise in diseases, especially in pandemic contexts, there has been a sharp increase in the demand for high-quality gloves in hospitals, clinics, laboratories, and healthcare facilities. Moreover, advancements in glove material technology and designs contribute to the market’s growth, with the development of new polymer compounds, texture variations, and flexibility being incorporated into gloves. Latex, nitrile, and vinyl remain among the most commonly used materials.

Industry-Specific Demand and Segmentation

Pharmaceuticals & Biotechnology: Cleanroom gloves are extensively used in pharmaceutical manufacturing plants to protect drugs and therapies from contamination. This is particularly important in sterile pharmaceutical product production, such as injectable medicines, insulin, and vaccines. Regulations in various countries demand strict adherence to cleanliness protocols, further driving the glove market in this sector.

Electronics: Cleanrooms in semiconductor manufacturing rely heavily on specialized gloves to prevent dust, static charge, and particles from affecting the delicate components being processed. The use of cleanroom gloves here is linked directly to product reliability and production efficiency.

Food Processing: The food industry also uses cleanroom gloves to maintain hygiene in high-risk processing areas. Gloves are utilized when handling pre-packaged foods, during cooking, and packaging, and they are especially critical in allergen-free environments where cross-contamination is a concern.

Regional Insights

Geographically, North America is the largest market for cleanroom disposable gloves. The region's stringent regulatory framework surrounding health and safety standards in manufacturing processes contributes heavily to the demand. Additionally, the increasing trend of automation in industries like semiconductor production amplifies the need for gloves to protect delicate equipment.

Europe follows closely, with increasing pharmaceutical and biotechnology research investments contributing to high demand for cleanroom gloves. On the other hand, the Asia-Pacific (APAC) region is poised for rapid growth due to the burgeoning healthcare industry, expanded electronics manufacturing capabilities, and the increasing focus on biotechnology research in China, India, and Japan.

Key Trends in the Cleanroom Disposable Gloves Market

Material Innovation: The gloves used in cleanrooms are transitioning from basic rubber materials to specialized formulations such as nitrile and polyurethane, which offer superior performance in sensitive environments. These materials exhibit excellent barrier protection and a reduction in the risk of allergic reactions compared to latex-based gloves.

Automation and Robotics: Increasing use of robots and automated systems in manufacturing, especially in the semiconductor industry, is influencing the gloves market. Cleanrooms in electronics sectors require both disposable gloves and protective clothing designed to ensure the integrity of the controlled environment.

Sustainability Efforts: The rise in environmental awareness is also encouraging manufacturers to adopt more sustainable materials in the production of disposable cleanroom gloves. Companies are focusing on biodegradable polymers or eco-friendly alternatives to minimize environmental impact.

Challenges to Overcome

The market faces challenges, including the rising costs of raw materials and the environmental issues related to the disposal of disposable gloves. Manufacturers are now focusing on creating recyclable or biodegradable gloves to address waste concerns.

Furthermore, the industry faces supply chain fluctuations, with disruptions caused by global demand surges, such as during the COVID-19 pandemic. While demand spikes create opportunities, meeting this need while ensuring the safety and quality standards of cleanroom gloves is a challenge for manufacturers.

Conclusion

The cleanroom disposable gloves market is poised for sustained growth across several sectors, particularly healthcare, pharmaceuticals, and electronics. As industry standards for contamination control become increasingly stringent and technology continues to evolve, the demand for advanced, efficient cleanroom gloves will only continue to rise. Innovation in materials, greater regulatory compliance, and environmental awareness will drive future market trends and open up new avenues for growth.

0 notes

Text

Food Flavors Market Dynamics and Forecast: An In-depth Study of Trends, Challenges, and Innovations

The food flavors market has witnessed substantial growth over the past several years, driven by changing consumer preferences, innovative technologies, and the increasing demand for healthier, more diverse food options. This in-depth study explores the key trends, challenges, and innovations shaping the future of the food flavors industry, while also offering a forecast for the coming years.

Market Trends

Health-Conscious Consumers One of the most prominent trends in the food flavors market is the shift towards healthier and more natural ingredients. Consumers are increasingly seeking products with fewer artificial additives, preservatives, and flavors. This has led to a surge in demand for natural, organic, and plant-based flavors that align with healthier eating habits. As people become more health-conscious, the market for low-sodium, low-sugar, and gluten-free products is expanding, forcing flavor companies to innovate with clean-label solutions.

Preference for Bold and Unique Flavors In addition to health concerns, consumers are becoming more adventurous with their food choices, desiring bold, exotic, and complex flavor profiles. The rising popularity of global cuisines has encouraged the exploration of ingredients such as sriracha, wasabi, turmeric, and other spices that offer a distinct taste. Ethnic flavors from regions like Asia, Africa, and the Middle East are gaining traction as consumers seek new culinary experiences. This trend has opened up a range of opportunities for companies to create unique blends that appeal to diverse palates.

Plant-Based and Vegan Foods The increasing adoption of plant-based diets has had a significant impact on the food flavors market. Plant-based foods, including meat and dairy substitutes, require specialized flavoring to replicate the taste and texture of traditional animal-based products. Companies are focusing on developing flavors like umami, which can mimic the savory taste of meats, in order to enhance the taste of plant-based alternatives. With veganism on the rise, the demand for plant-derived flavors continues to grow, providing a significant opportunity for innovation in this segment.

Personalization and Customization Another emerging trend in the market is the demand for personalized food experiences. As consumers seek products that suit their individual preferences and dietary needs, customized flavor profiles have become a key selling point. Advances in food technology and artificial intelligence (AI) have enabled manufacturers to develop bespoke flavoring systems that cater to specific tastes, allergens, and even genetic predispositions. This trend of customization is expected to grow as consumers become more aware of the links between diet, health, and well-being.

Challenges in the Food Flavors Market

Rising Raw Material Costs The increasing costs of raw materials for natural and organic flavoring ingredients pose a significant challenge to the food flavors market. Sourcing natural ingredients like fruits, herbs, and spices can be expensive, especially as demand rises. This price fluctuation impacts both manufacturers and consumers, making it crucial for companies to balance cost with the desire for high-quality products. Additionally, climate change and unpredictable weather patterns are affecting the supply of raw materials, leading to further price instability.

Regulatory and Labeling Challenges As the demand for clean-label products increases, food flavor companies must navigate a complex web of regulations regarding labeling and ingredient disclosure. Regulatory bodies in various regions, including the U.S. Food and Drug Administration (FDA) and the European Food Safety Authority (EFSA), impose strict rules on what can be included in food products and how they should be labeled. This creates challenges for flavor manufacturers, especially when it comes to communicating natural and synthetic ingredients transparently.

Consumer Sensitivity and Allergens Food allergies and sensitivities are on the rise, and consumers are becoming more cautious about what they consume. Flavor companies face the challenge of developing products that are both appealing and safe for a wide range of dietary restrictions. This includes creating flavors that are free from common allergens such as gluten, dairy, nuts, and soy. Meeting the growing demand for allergen-free products requires significant investment in research and development to ensure both safety and taste.

Innovations in the Food Flavors Market

Technological Advancements Technological innovation is playing a major role in the evolution of the food flavors market. Advances in artificial intelligence (AI), machine learning, and big data analytics allow companies to predict consumer preferences and develop flavors more quickly and efficiently. The use of AI in flavor development has enabled manufacturers to create more precise and customizable flavors that match specific consumer tastes, all while reducing time-to-market. Additionally, emerging technologies in fermentation and biotechnological methods are helping to produce more sustainable and scalable natural flavors.

Sustainability and Eco-friendly Flavors As environmental concerns continue to grow, sustainability has become a key focus for the food industry. The shift toward plant-based ingredients has driven the development of sustainable flavoring options that have a lower environmental footprint. Companies are now investing in sustainable sourcing, such as using renewable energy in production processes and opting for biodegradable or recyclable packaging. Innovations like precision fermentation, which allows the production of flavors without traditional farming methods, are also gaining traction as more sustainable alternatives to conventional flavor production.

Flavor Encapsulation Encapsulation technology has revolutionized the food flavors market by allowing for better control over flavor release and shelf life. This technology involves enclosing flavors in a protective coating that releases them at the right time, ensuring a longer-lasting taste experience. The benefits of encapsulation are particularly evident in beverages, snacks, and ready-to-eat meals, where the preservation of flavor over time is essential. This technology is becoming an important tool for manufacturers to enhance the consumer experience.

Forecast for the Food Flavors Market

Looking ahead, the food flavors market is expected to continue expanding at a steady pace, driven by the increasing demand for natural and customized flavors, plant-based products, and technological advancements. The market is predicted to grow at a compound annual growth rate (CAGR) of over 5% in the coming years, with North America and Europe leading the way due to their established food industries and consumer preferences for healthy, diverse flavors. The Asia-Pacific region, with its rapidly expanding middle class and growing interest in international cuisine, is also expected to become a major contributor to market growth.

As companies navigate challenges such as raw material costs, regulatory hurdles, and consumer sensitivity, the food flavors market will remain dynamic and highly competitive. Innovation in flavor technology, sustainability, and consumer-centric products will be crucial for success. By staying ahead of trends and embracing the opportunities in this evolving market, companies can position themselves for long-term growth in the global food flavors sector.

Request sample PDF Report : https://www.pristinemarketinsights.com/get-free-sample-and-toc?rprtdtid=NTEx&RD=Food-Flavors-Market-Report

#FoodFlavorsMarket#FoodFlavorsMarketTrends#FoodFlavorsMarketInsights#FoodFlavorsMarketGrowthOpportunities#FoodFlavorsMarketForecastAnalysis#FoodFlavorsMarketEmergingTrends

0 notes

Text

The global Clean Label Starch Market is projected to grow from USD 1,710 million in 2024 to USD 2,604.47 million by 2032, marking a compound annual growth rate (CAGR) of 5.4% during the forecast period. In the evolving food industry, clean-label ingredients have become a major focal point for both consumers and manufacturers. One of the essential clean-label ingredients experiencing significant growth is **clean label starch**. Characterized by its minimal processing and the absence of artificial additives, clean label starch aligns with the increasing consumer demand for transparency in ingredient lists. This article examines the dynamics of the clean label starch market, including key trends, growth drivers, challenges, and future outlook.Clean label starches are derived from natural sources such as corn, potato, rice, tapioca, and wheat. Unlike traditional modified starches, they do not undergo harsh chemical treatments and are generally labeled as “native starch” or the name of the plant source. These starches serve a variety of functions in the food industry, including as thickening agents, stabilizers, and texture enhancers.

Browse the full report https://www.credenceresearch.com/report/clean-label-starch-market

Key Market Drivers

Several factors are propelling the growth of the clean label starch market:

1. Consumer Demand for Transparency: Today’s consumers are more informed and health-conscious, prompting them to seek foods with natural, easy-to-understand ingredients. This trend is especially prominent in North America and Europe, where transparency around food ingredients is a top priority. With clean label starch, food companies can provide a recognizable ingredient that resonates with consumers looking to avoid artificial additives.

2. Shift Toward Plant-Based and Organic Foods: The clean eating movement and the rise in vegan and plant-based diets have had a positive impact on clean label starch demand. Plant-based food products often require clean label starches as binders or stabilizers, and these products benefit from having “natural” or “plant-based” ingredients that are also free from chemical modifications.

3. Increased Applications in Processed Foods: Clean label starches are finding new applications across a wide range of processed foods, including snacks, baked goods, soups, sauces, and ready-to-eat meals. The starch offers essential functional benefits such as thickening, stabilizing, and enhancing texture without compromising the product’s clean label status. These starches are also non-GMO and allergen-free, enhancing their appeal to a broader audience.

4. Support from Regulatory Standards: Government bodies around the world are increasingly encouraging clean label practices, especially in developed regions. In countries like the United States, the Food and Drug Administration (FDA) and the European Union’s regulations have set strict guidelines regarding labeling, encouraging manufacturers to adopt natural ingredients. Clean label starch fits well within these guidelines, contributing to its growing acceptance.

Key Challenges in the Market

While the clean label starch market is on an upward trajectory, it faces several challenges:

1. Higher Production Costs: Clean label starch is often more expensive to produce than traditional starch. Its manufacturing process requires specific raw materials and processing methods to ensure the absence of artificial additives, which can lead to higher costs. For cost-sensitive food manufacturers, this may limit its adoption, especially in markets where price sensitivity is a significant factor.

2. Functional Limitations: Clean label starches do not always perform at the same level as their chemically modified counterparts, particularly in extreme processing conditions like high heat or acidity. In applications that require high stability and texture retention, clean label starch may fall short, which poses a challenge for certain processed foods. Ongoing research and development are focused on enhancing these properties, but this limitation can still affect its adoption in highly specialized food products.

3. Supply Chain Constraints: Sourcing high-quality, non-GMO raw materials for clean label starch production can be challenging. As the demand for clean label starches grows, there is a need for a reliable supply chain that can support large-scale production without compromising quality. Market players are exploring partnerships with sustainable farmers and suppliers to ensure a steady supply of raw materials.

Market Trends and Opportunities

The clean label starch market is driven by evolving food trends and technological advancements that open up exciting opportunities for growth:

1. Emerging Markets and Expansion Opportunities: Although North America and Europe currently dominate the clean label starch market, there is a growing awareness of clean label products in Asia-Pacific and Latin America. As consumer preferences shift in these regions, companies are expanding their presence, which is expected to contribute to significant market growth.

2. Innovation in Product Formulation: Manufacturers are developing innovative clean label starches that improve stability, taste, and texture across a broader range of applications. Recent advancements focus on improving the functional capabilities of clean label starches to make them suitable for highly processed foods without compromising on quality. These innovations will likely drive demand in sectors like frozen foods and dairy alternatives.

3. Collaborations and Investments: Companies are investing in partnerships and acquisitions to expand their clean label starch offerings. Strategic collaborations with research institutions and raw material suppliers allow manufacturers to develop proprietary clean label starches with unique benefits, giving them a competitive edge.

Future Outlook

The clean label starch market is projected to continue its steady growth, driven by consumer demand for transparency, regulatory support, and the expanding application of these starches in diverse food products. Market players are likely to focus on improving the functional properties of clean label starches to enhance their performance in high-intensity applications.

Key Player Analysis:

Top Key Players

Cargill, Incorporated

Ingredion Incorporated

Tate & Lyle PLC

Archer Daniels Midland Company

Roquette Frères S.A.

BENEO GmbH

MGP Ingredients, Inc.

AGRANA Beteiligungs-AG

Avebe U.A.

KMC Kartoffelmelcentralen A.M.B.A

Segmentations:

Source

Wheat

Corn

Potato

Tapioca

Rice & Pea

Application

Food Industry

Bakery & Confectionery

Dairy & Desserts

Soups, Sauces & Dressings

Savory Snacks

Others

Animal Feed Industry

Pharmaceutical Industry

Others

Regions

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report https://www.credenceresearch.com/report/clean-label-starch-market

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

Montelukast Sodium Market 2024-2033 : Demand, Trend, Segmentation, Forecast, Overview And Top Companies

The montelukast sodium global market report 2024 from The Business Research Company provides comprehensive market statistics, including global market size, regional shares, competitor market share, detailed segments, trends, and opportunities. This report offers an in-depth analysis of current and future industry scenarios, delivering a complete perspective for thriving in the industrial automation software market.

Montelukast Sodium Market, 2024 report by The Business Research Company offers comprehensive insights into the current state of the market and highlights future growth opportunities.

Market Size - The montelukast sodium market size has grown strongly in recent years. It will grow from $3.52 billion in 2023 to $3.86 billion in 2024 at a compound annual growth rate (CAGR) of 9.6%. The growth in the historic period can be attributed to increasing respiratory disorders, an aging population, rising air pollution levels, growing awareness and education, and expansion in emerging markets.

The montelukast sodium market size is expected to see strong growth in the next few years. It will grow to $5.59 billion in 2028 at a compound annual growth rate (CAGR) of 9.7%. The growth in the forecast period can be attributed to approval and launch, clinical studies, patent expiry, regulatory changes, and physician prescribing patterns. Major trends in the forecast period include increased generic competition, a shift towards combination therapies, expansion in emerging markets, a focus on pediatric use, and digital health solutions.

Order your report now for swift delivery @ https://www.thebusinessresearchcompany.com/report/montelukast-sodium-global-market-report

The Business Research Company's reports encompass a wide range of information, including:

1. Market Size (Historic and Forecast): Analysis of the market's historical performance and projections for future growth.

2. Drivers: Examination of the key factors propelling market growth.

3. Trends: Identification of emerging trends and patterns shaping the market landscape.

4. Key Segments: Breakdown of the market into its primary segments and their respective performance.

5. Focus Regions and Geographies: Insight into the most critical regions and geographical areas influencing the market.

6. Macro Economic Factors: Assessment of broader economic elements impacting the market.

Market Drivers - The increasing prevalence of asthma is expected to propel the growth of montelukast sodium market going forward. Asthma is a chronic respiratory disorder marked by inflammation and constriction of the airways, resulting in repeated bouts of wheezing, breathlessness, chest tightness, and coughing. The prevalence of asthma is increasing due to environmental pollution, allergen exposure, genetic predisposition, urbanization, changes in lifestyle, and respiratory infections. Montelukast sodium is used in asthma as a leukotriene receptor antagonist, helping to prevent and manage asthma symptoms by blocking the action of leukotrienes, which contribute to airway inflammation and constriction. For instance, in September 2022, according to the National Health Service, a UK-based government department, hospital admissions for children with asthma in England and Wales surged by 149% between 2021 and 2022. The number of children admitted with asthma symptoms rose to 19,506, compared to 7,850 during the 2020 to 2021 period. Therefore, the increasing prevalence of asthma is driving the growth of montelukast sodium market.

Market Trends - Major companies operating in the montelukast sodium market are developing new drugs such as fexofenadine hydrochloride and getting them approved to expand their product portfolios and address the evolving needs of patients with allergic conditions. Fexofinadine hydrochloride is a second-generation antihistamine medication approved by the FDA for treating allergy symptoms and hay fever in adults and children. For instance, in December 2021, Morepen Laboratories received approval from the US Food and Drug Administration (USFDA) to market its generic anti-allergy drug, Fexofinadine Hydrochloride, in the American market. Fexofinadine hydrochloride, a widely used second-generation antihistamine, is employed to treat allergy symptoms and hay fever. This approval signifies a significant milestone for Morepen Laboratories, strengthening its position in the anti-allergy market.

The montelukast sodium market covered in this report is segmented –

1) By Product: Crystal-like, Form-less Or Amorphous 2) By Dosage Form: Tablets, Oral Solutions 3) By Application : Bronchospasm, Allergic Coryza, Asthma, Urticaria, Other Applications

Get an inside scoop of the montelukast sodium market, Request now for Sample Report @ https://www.thebusinessresearchcompany.com/sample.aspx?id=16123&type=smp Regional Insights - North America was the largest region in the montelukast sodium market in 2023. Asia-Pacific is expected to be the fastest-growing region in the forecast period. The regions covered in the montelukast sodium market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East, Africa.

Key Companies - Major companies operating in the montelukast sodium market are Pfizer Inc., Merck & Co. Inc., Sanofi Aventis SA, Teva Pharmaceuticals USA Inc., Hetero Labs Ltd., Sun Pharma Industries Ltd., Aurobindo Pharma Limited, Cipla Inc., Intas Pharmaceuticals Ltd., Seqens Group, Sanyo Chemical Industries Ltd., Morepen Laboratories, Neuland Laboratories Ltd., Medopharm Private Ltd., BEC Chemicals Pvt. Ltd, Delmar Chemicals Inc., Kimia Biosciences Ltd., Ortin Laboratories Ltd., MSN Laboratories Pvt Ltd., Vamsi Labs Ltd., LGM Pharma LLC, HRV Global Life Sciences, Sigmak Lifesciences, Akums Lifesciences Ltd., Anwita Drugs & Chemicals Pvt Ltd

Table of Contents 1. Executive Summary 2. Montelukast Sodium Market Report Structure 3. Montelukast Sodium Market Trends And Strategies 4. Montelukast Sodium Market – Macro Economic Scenario 5. Montelukast Sodium Market Size And Growth ….. 27. Montelukast Sodium Market Competitor Landscape And Company Profiles 28. Key Mergers And Acquisitions 29. Future Outlook and Potential Analysis 30. Appendix

Contact Us: The Business Research Company Europe: +44 207 1930 708 Asia: +91 88972 63534 Americas: +1 315 623 0293 Email: [email protected]

Follow Us On: LinkedIn: https://in.linkedin.com/company/the-business-research-company Twitter: https://twitter.com/tbrc_info Facebook: https://www.facebook.com/TheBusinessResearchCompany YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ Blog: https://blog.tbrc.info/ Healthcare Blog: https://healthcareresearchreports.com/ Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model

0 notes

Text

Regional Analysis of the Tablet Coating Market and Competitive Landscape

Tablet coating is a critical process in the pharmaceutical industry, primarily used to improve the stability, appearance, and efficacy of tablets. This process involves applying a layer of coating material onto the surface of a tablet core, which can serve various purposes, from masking unpleasant tastes and odors to controlling drug release rates and enhancing durability. Tablet coating materials include polymers, sugars, and colorants, which can be selected to suit the specific therapeutic needs of the medication. Advanced coating technologies have made it possible to create tablets with multiple functions, such as sustained-release, enteric coatings for delayed drug release, and protective layers to extend shelf life.

The tablet coating market size was projected at 8.82 (USD billion) in 2022 based on MRFR analysis. By 2032, the tablet coating market is projected to have grown from 9.45 billion USD in 2023 to 17.46 billion USD. During the forecast period (2024-2032), the tablet coating market's compound annual growth rate (CAGR) is anticipated to be approximately 7.06%.

Tablet Coating Analysis

Tablet Coating analysis shows that the demand for coated tablets is increasing across the pharmaceutical industry. This growth is driven by the benefits coating provides, such as improved patient adherence, especially for medications with bitter tastes. Additionally, coating helps to prevent tablet breakage and provides physical stability under various environmental conditions. Different coating techniques, such as sugar coating, film coating, and compression coating, have specific applications depending on the tablet’s intended use. An in-depth Tablet Coating analysis highlights a shift towards more sophisticated, multi-functional coatings that offer tailored release profiles and protect sensitive drug formulations. Innovations in coating materials and methods have also made production processes more efficient, helping manufacturers meet regulatory standards more easily.

Tablet Coating Market Trends

One of the main Tablet Coating market trends is the increased focus on functional and multi-layer coatings, which are engineered to release the active pharmaceutical ingredient (API) at targeted sites within the body. The rise of personalized medicine is also shaping market trends, as there is a need for coatings that cater to specific patient requirements, such as allergen-free or vegan coatings. Another significant trend in the Tablet Coating market is the adoption of aqueous coating processes as they reduce the use of organic solvents, making the process safer and more environmentally friendly. Additionally, advancements in coating machinery, including high-efficiency and automated systems, are enabling faster production and ensuring higher quality control.

Reasons to Buy the Reports

Detailed Market Insights: Comprehensive analysis of the Tablet Coating market, offering insights into current and emerging trends.

Competitive Analysis: In-depth evaluation of key players and their strategies, helping stakeholders understand competitive dynamics.

Technological Advancements: Information on innovative coating techniques and materials, essential for companies aiming to improve product performance.

Regulatory Information: Covers regulations affecting tablet coating processes, essential for compliance and quality assurance in pharmaceutical production.

Growth Forecasts: Offers projections on the future growth of the Tablet Coating market, aiding stakeholders in making informed investment decisions.

Recent Developments

Recent developments in the Tablet Coating market reflect ongoing efforts to enhance the quality and functionality of coated tablets. In 2023, several pharmaceutical companies announced the adoption of advanced coating techniques that improve the dissolution profiles of tablets, allowing for better-controlled release of APIs. Companies like BASF and Colorcon introduced eco-friendly coating solutions that eliminate the need for organic solvents, thereby reducing environmental impact. Additionally, new enteric coating materials have been developed to protect sensitive APIs from degradation in the stomach, ensuring they reach the intended site of absorption in the intestines. Automated tablet coating machines with advanced monitoring features have also been introduced to the market, helping to streamline the coating process and maintain high-quality standards. These advancements reflect the industry's commitment to innovation and the growing demand for versatile, high-performance tablet coating solutions.

Related reports:

pet sitting market

fungal keratitis treatment market

gastrointestinal stent market

gene therapy clinical trial service market

0 notes

Text

Popcorn Market 2024: Growth Trends, Industry Analysis, and Future Forecast

The popcorn market has been experiencing steady growth, driven by changing consumer preferences, the rise of healthy snacking trends, and increasing demand from cinemas, sports arenas, and home consumption. Popcorn has emerged as a favorite snack due to its affordability, versatility, and availability in various flavors. This blog explores the market size, growth, legal constraints, limitations, key companies, market segmentation, and future forecasts for the global popcorn market.

Market Growth & Size

The global popcorn market was valued at USD 10.1 billion in 2023, with projections to reach USD 15.3 billion by 2030. The market is expected to grow at a CAGR of 6.7% over the forecast period. This growth is primarily fueled by the increasing popularity of ready-to-eat (RTE) popcorn and microwave popcorn, as well as rising demand for gourmet flavors.

Key Growth Drivers:

Healthier Snacking: Popcorn is often seen as a healthier alternative to other snacks like chips and candy, especially when air-popped or lightly salted. As consumers become more health-conscious, they are opting for snacks that are low in calories and fat.

Convenience: The rise of RTE popcorn and microwaveable options has contributed significantly to the growth of the popcorn market, providing consumers with quick and easy snacking solutions.

Increased Home Entertainment: The growing popularity of home streaming services and the demand for home entertainment has led to an increase in at-home popcorn consumption.

Legal Constraints in the Popcorn Market

The popcorn industry is subject to various legal and regulatory constraints, particularly regarding food safety, labeling, and advertising.

Key Legal Constraints:

Food Safety Regulations: Popcorn manufacturers must adhere to food safety standards set by regulatory authorities such as the U.S. Food and Drug Administration (FDA) and European Food Safety Authority (EFSA). These regulations ensure that the products meet hygiene, safety, and quality standards.

Labeling Requirements: Companies are required to provide detailed nutritional information, including calorie counts, ingredients, and potential allergens. Misleading claims about health benefits or nutritional content are subject to strict scrutiny by regulators.

Advertising Regulations: In many regions, there are specific rules regarding how popcorn products can be marketed, particularly when targeting children. Claims regarding the health benefits of certain flavors or types of popcorn must be backed by scientific evidence.

Limitations of the Popcorn Market

Despite the strong growth trajectory, the popcorn market faces several challenges that may limit its expansion.

Key Limitations:

Price Sensitivity: Popcorn is a low-cost snack, and fluctuations in the prices of raw materials (corn, oil, flavorings) can significantly affect profit margins. This price sensitivity may restrict smaller companies from entering the market.

Health Concerns: While popcorn is considered a healthier snack, many commercially available popcorn products are high in sodium, artificial flavors, and unhealthy fats. These health concerns may affect consumer demand, particularly as people seek out healthier alternatives.

Competition from Alternative Snacks: The snack food industry is highly competitive, with alternatives like chips, nuts, and protein bars competing for the same market share. Innovations in these categories can impact the growth of the popcorn market.

Key Companies in the Popcorn Market

The popcorn market is highly competitive, with several large players dominating the global landscape. These companies focus on innovation, new flavors, and expanding their geographic reach to maintain their market positions.

Major Companies:

Conagra Brands (Orville Redenbacher’s): A leader in the RTE and microwave popcorn segments, Conagra Brands offers a wide range of popcorn products through its popular brand Orville Redenbacher’s.

Amplify Snack Brands (SkinnyPop): Known for its healthy, low-calorie popcorn, SkinnyPop has made a significant impact in the premium snack category. Its simple ingredient list appeals to health-conscious consumers.

The Hershey Company (Popcornopolis): Hershey’s acquisition of Popcornopolis has enabled the company to tap into the growing demand for gourmet popcorn, offering a range of sweet and savory flavors.

PepsiCo (Smartfood): Through its Frito-Lay division, PepsiCo has capitalized on the healthy snacking trend with Smartfood, a brand that offers flavored popcorn marketed as a better-for-you snack.

Campbell Soup Company (Snyder’s-Lance): Campbell’s expanded into the popcorn market with its purchase of Snyder’s-Lance, which produces the Lance popcorn brand.

Market Segmentation by Product and by Application

The popcorn market can be segmented by product type and application, allowing companies to target specific consumer needs and preferences.

By Product Type:

Ready-to-Eat (RTE) Popcorn: This segment includes pre-popped and packaged popcorn that is available in various flavors, such as cheese, caramel, and butter. RTE popcorn is one of the fastest-growing segments due to its convenience and wide range of flavors.

Microwave Popcorn: Microwaveable popcorn is a staple in many households due to its convenience and ability to be prepared quickly. It remains a popular choice for at-home movie nights and snacking.

Gourmet Popcorn: This premium segment includes popcorn varieties with unique flavors such as truffle, caramel, and chocolate-drizzled popcorn. Gourmet popcorn is particularly popular in the gift market and at high-end retailers.

By Application:

Home Consumption: With the rise of streaming platforms and in-home entertainment, popcorn consumption at home has increased significantly. Consumers are turning to both RTE and microwave popcorn for their snacking needs.

Cinemas and Theaters: Popcorn is traditionally associated with movie theaters, and despite challenges faced by the cinema industry, theater popcorn remains a significant part of overall market demand.

Sporting Events and Carnivals: Popcorn is a popular snack at sporting events, carnivals, and fairs, where it is often sold as part of the concession stand offerings.

Future Forecast for the Popcorn Market

The future outlook for the popcorn market is positive, with growth expected to continue as new products, flavors, and healthier options are introduced. Several trends are likely to shape the market’s growth over the coming years.

Key Future Trends:

Healthier Popcorn Varieties: As consumers become more health-conscious, there will be a shift toward popcorn products that are lower in fat, sodium, and artificial ingredients. Companies are likely to introduce more organic, gluten-free, and non-GMO options to cater to this demand.

Premium and Gourmet Popcorn: The gourmet popcorn segment is expected to see substantial growth, with consumers willing to pay more for high-quality, innovative flavors.

Sustainability: There will be a growing emphasis on sustainable packaging and production processes as companies aim to reduce their environmental footprint.

Forecast Growth:

The global popcorn market is expected to grow at a CAGR of 6.7%, reaching USD 15.3 billion by 2030. The increasing demand for healthy, convenient, and premium snacks will be key drivers of this growth.

Conclusion

The popcorn market is set to continue its steady growth, driven by health trends, convenience, and product innovation. Major companies like Conagra, Amplify Snack Brands, and PepsiCo are investing heavily in expanding their product lines and improving their market reach. However, the industry faces challenges related to price sensitivity and competition from other snack categories. As the demand for healthier and gourmet options grows, the future of the popcorn market looks promising, with sustained growth expected in both established and emerging markets.

Contact Us for more information on the Popcorn Market Research 2023–2030 Forecast : Or Phone Call us :

USA — +1 507 500 7209 | India — +91 750 648 0373

Browse More Articles

Polypropylene Market Trends

Polyurea Coatings Market Size

Population Health Management Market Overview

Ready Meals Market Growth

0 notes

Text

Peanut Allergy Treatment Market Size, Share, Key Drivers, Trends, Challenges and Competitive Analysis

"Peanut Allergy Treatment Market – Industry Trends and Forecast to 2028

Global Peanut Allergy Treatment Market, By Drug Type (Injectable Epinephrine, Antihistamines), Route of Administration (Oral, Injectable), Distribution Channel (Retail Pharmacies, Hospital Pharmacies, Online Pharmacies), Country (U.S., Canada, Mexico, Germany, Italy, U.K., France, Spain, Netherland, Belgium, Switzerland, Turkey, Russia, Rest of Europe, Japan, China, India, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific, Brazil, Argentina, Rest of South America, South Africa, Saudi Arabia, UAE, Egypt, Israel, Rest of Middle East & Africa) Industry Trends and Forecast to 2028

Access Full 350 Pages PDF Report @

**Segments**

- Allergen-Specific Immunotherapy - Epinephrine Auto-Injector - Anti-Inflammatory Drugs - Others

The peanut allergy treatment market can be segmented into different categories based on the type of treatment options available. Allergen-specific immunotherapy is a promising treatment approach that aims to desensitize the immune system to peanuts gradually. This method involves exposing individuals to small amounts of peanut allergen under controlled circumstances to build tolerance. Epinephrine auto-injectors are crucial for emergency situations where individuals experience severe allergic reactions known as anaphylaxis. Anti-inflammatory drugs such as corticosteroids may be prescribed to reduce inflammation and manage symptoms. Other treatments may include dietary management and alternative therapies.

**Market Players**

- Aimmune Therapeutics - DBV Technologies - DB Allergy - Allergy Therapeutics - Monsanto - Sanofi - Aravax

Several key players contribute significantly to the peanut allergy treatment market. Aimmune Therapeutics is known for its innovative product Palforzia, the first FDA-approved oral immunotherapy for peanut allergy. DBV Technologies focuses on developing Viaskin, an epicutaneous patch for immunotherapy delivery. DB Allergy offers diagnostic tools and therapeutic solutions for allergies, including peanut allergies. Allergy Therapeutics specializes in allergy vaccines and immunotherapy products. Sanofi, a multinational pharmaceutical company, has a presence in the peanut allergy treatment market through its research and development initiatives. Monsanto, a prominent player in agriculture, invests in biotechnology for developing allergy-resistant crops. Aravax is a biopharmaceutical company dedicated to creating novel treatments for food allergies, including peanuts.

https://www.databridgemarketresearch.com/reports/global-peanut-allergy-treatment-marketThe peanut allergy treatment market is witnessing significant growth and innovation driven by the increasing prevalence of peanut allergies worldwide. The focus on developing effective and safe treatment options has led to a surge in research and development activities by key players in the market. Allergen-specific immunotherapy, particularly oral immunotherapy, has emerged as a promising approach to desensitize individuals to peanuts gradually. This method holds the potential to transform the management of peanut allergies by reducing the risk of severe allergic reactions and improving quality of life for patients. The introduction of products like Palforzia by Aimmune Therapeutics and Viaskin by DBV Technologies has showcased the potential of immunotherapy in addressing peanut allergies.

In addition to immunotherapy, the market for epinephrine auto-injectors remains crucial for managing severe allergic reactions, such as anaphylaxis, in individuals with peanut allergies. The availability of user-friendly and portable auto-injectors has enhanced the emergency preparedness of patients and caregivers, emphasizing the importance of timely intervention during allergic episodes. Anti-inflammatory drugs, including corticosteroids, play a role in managing inflammation and symptoms associated with peanut allergies, providing supplementary support alongside allergen-specific immunotherapy and emergency treatments.

Moreover, dietary management and alternative therapies are gaining traction as complementary approaches to peanut allergy treatment. Dietary adjustments, such as strict avoidance of peanuts and label reading, are essential for preventing allergic reactions and ensuring the safety of individuals with peanut allergies. Alternative therapies, including herbal remedies and probiotics, are being explored for their potential immunomodulatory effects on allergic responses. The integration of these holistic approaches into patient care plans underscores the multidimensional nature of managing peanut allergies and the need for personalized treatment strategies.

Furthermore, the market landscape is characterized by the presence of leading pharmaceutical companies, biotechnology firms, and research organizations dedicated to advancing peanut allergy treatment options. Collaborative efforts among industry players, academic institutions, and regulatory bodies are driving innovation and fostering a conducive environment for bringing novel therapies to market. The continuous**Global Peanut Allergy Treatment Market**

- **Injectable Epinephrine** - **Antihistamines**

The global peanut allergy treatment market is experiencing significant growth and innovation, driven by the rising prevalence of peanut allergies worldwide. Allergen-specific immunotherapy, notably oral immunotherapy, has emerged as a promising approach to gradually desensitize individuals to peanuts, potentially transforming the management of peanut allergies by reducing severe allergic reactions and improving patients' quality of life. Key market players such as Aimmune Therapeutics, DBV Technologies, and Allergy Therapeutics are at the forefront of developing innovative treatment options in this segment.

Epinephrine auto-injectors play a critical role in managing severe allergic reactions, such as anaphylaxis, in individuals with peanut allergies. The availability of user-friendly and portable auto-injectors has improved emergency preparedness among patients and caregivers, emphasizing the importance of timely intervention during allergic episodes. Additionally, anti-inflammatory drugs, including corticosteroids, supplement allergen-specific immunotherapy and emergency treatments by managing inflammation and associated symptoms in peanut allergy patients.

Dietary management and alternative therapies are emerging as complementary approaches to peanut allergy treatment. Strict avoidance of peanuts, label reading, and dietary adjustments are essential in preventing allergic reactions and ensuring patient safety. Research into alternative therapies such as herbal remedies and probiotics for their potential immunomodulatory effects on allergic responses is ongoing, highlighting the holistic nature of peanut allergy management and the importance of personalized treatment strategies.

Table of Content:

Part 01: Executive Summary

Part 02: Scope of the Report

Part 03: Global Peanut Allergy Treatment Market Landscape

Part 04: Global Peanut Allergy Treatment Market Sizing

Part 05: Global Peanut Allergy Treatment Market Segmentation by Product

Part 06: Five Forces Analysis

Part 07: Customer Landscape

Part 08: Geographic Landscape

Part 09: Decision Framework

Part 10: Drivers and Challenges

Part 11: Market Trends

Part 12: Vendor Landscape

Part 13: Vendor Analysis

Peanut Allergy Treatment Key Benefits over Global Competitors:

The report provides a qualitative and quantitative analysis of the Peanut Allergy Treatment Market trends, forecasts, and market size to determine new opportunities.

Porter’s Five Forces analysis highlights the potency of buyers and suppliers to enable stakeholders to make strategic business decisions and determine the level of competition in the industry.

Top impacting factors & major investment pockets are highlighted in the research.

The major countries in each region are analyzed and their revenue contribution is mentioned.

The market player positioning segment provides an understanding of the current position of the market players active in the Personal Care Ingredients

Browse Trending Reports:

Threat Detection Systems Market Pipe Coating Market Fragrance Fixatives Market Mobile Campaign Management Platform Market Menstrual Cramps Treatment Market Roof Insulation Market Mobile Robotics Market Varnish Makers Market Urinary Incontinence Market Treatment Resistant Depression Market Robotic Prosthetics Market Neutropenia Market Polycystic Kidney Disease Adpkd Market Grain Analysis Market Solid State Solar Cell Market Panel Mount Industrial Display Market Automotive Mini Led Market

About Data Bridge Market Research:

Data Bridge set forth itself as an unconventional and neoteric Market research and consulting firm with unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email: [email protected]"

0 notes

Text

Allergy Diagnostics Market worth $9.8 billion by 2029

Allergy Diagnostics Market in terms of revenue was estimated to be worth $5.3 billion in 2024 and is poised to reach $9.8 billion by 2029, growing at a CAGR of 11.0% from 2024 to 2029 according to a new report by MarketsandMarkets™.

Download an Illustrative overview:

Browse in-depth TOC on "Allergy Diagnostics Market"

248 - Tables

57 - Figures

307 – Pages

The consumables segment is expected to account for the largest share in 2023.

The Allergy Diagnostics market, by product & service, has been segmented into consumables, instruments, and services. The consumables segment accounted for the largest share of the Allergy Diagnostics market in 2023. This segment is also anticipated to experience significant growth over the projected period. The increasing demand for rapid diagnosis of allergic patients which is driven by increasing number of allergic cases can be attributed for the larger share of this segment during the forecast period.

In Vivo test segment held the largest market share in the Allergy Diagnostics market.

Based on the test type, the Allergy Diagnostics market is segmented into in vivo tests and in vitro tests. In 2023, the in vivo tests segment accounted for the largest share of the Allergy Diagnostics market. The growth of this segment is mainly driven by the growing adoption of various in vivo tests, such as skin prick tests which is considered as the first line of diagnosis for allergy and favorable government support and guidelines.

Inhaled allergy segment held the largest market share in the Allergy Diagnostics market.

Based on the allergen, the Allergy Diagnostics market is segmented into inhaled allergens, food allergens, drug allergens, and other allergens. In 2023, the inhaled allergens segment accounted for the largest share of the Allergy Diagnostics market due to the rising environmental pollution, rising home dust & mites coupled with other factors such as pollen, fungus, mold, and dust, and switching lifestyles, including rise in indoor activities and exposure to indoor allergen.

North America dominates the global Allergy Diagnostics market

Based on the region, the Allergy Diagnostics market is segmented into North America, Europe, Asia Pacific, Latin America, Middle East & Africa. North America market is driven by availability of technologically advanced products and growing research on allergy by companies and government. The Asia Pacific segment is projected to register the highest CAGR during the forecast period. Developing healthcare infrastructure, lifestyle changes and climatic conditions, increased ozone and industrial pollution levels, and the rising demand for quality medical care are some of the major factors driving the growth of this regional market.

Request Sample Pages:

Allergy Diagnostics Market Dynamics:

Drivers:

High incidence and heavy economic burden of allergic diseases

Restraints:

High pricing of allergy diagnostic instruments

Opportunities:

Integration of AI in allergy diagnosis

Challenge:

Shortage of allergists

Key Market Players of Allergy Diagnostics Industry:

Major players in Allergy Diagnostics market include Thermo Fisher Scientific Inc., (US), Siemens Healthineers AG (Germany), Danaher (US), and Canon, Inc. (Japan), Minaris Medical America, Inc. (US).

Breakdown of supply-side primary interviews by company type, designation, and region:

By Company Type: Tier 1 (20%), Tier 2 (45%), and Tier 3 (35%)

By Designation: C-level (30%), Director-level (20%), and Others (50%)

By Region: North America (36%), Asia- Pacific (27%), Europe (25%), and Latin America- (7%) and MEA-(5%)

Get 10% Free Customization on this Report:

Recent Developments of Allergy Diagnostics Industry: