#Coal Tar Market Demand

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Mobile Tumblr US users spend an average of 4.04 minutes per session on the app.

Text

Cresol Market: Applications and Market Dynamics Driving Growth up to 2033

Market Definition

The Cresol Market includes the production and use of cresol isomers: ortho-cresol, meta-cresol, and para-cresol. These organic compounds are derived from coal tar or petroleum and are known for their antiseptic and preservative properties. Cresol is widely used in applications such as chemical intermediates, disinfectants, resins, plasticizers, and in the production of vitamin E. Due to its versatility and efficacy, cresol plays a significant role in various industrial sectors, including pharmaceuticals, agriculture, and manufacturing.

To Know More @ https://www.globalinsightservices.com/reports/cresol-market

The global cresol market is anticipated to expand from $1.2 billion in 2023 to $2.1 billion by 2033, reflecting a CAGR of 5.8% over the forecast period.

Market Outlook

The Cresol Market is poised for growth, driven by increasing demand from end-use industries such as chemicals, pharmaceuticals, and electronics. One of the primary factors fueling the market is the rising need for chemical intermediates in the production of agrochemicals and antioxidants. In the pharmaceutical industry, cresol serves as a key raw material in synthesizing essential compounds, including vitamin E, which is seeing increased demand as a dietary supplement and additive in animal feed. The growing emphasis on health and wellness is expected to support the market’s expansion.

The use of cresol in the production of high-performance resins and laminates for the electronics industry is also gaining traction, as the demand for advanced electronic components and devices rises globally. Additionally, cresol’s antimicrobial and antiseptic properties make it a valuable ingredient in disinfectants and industrial cleaners, especially as hygiene and sanitation standards become more stringent in the wake of global health concerns.

However, the market faces challenges, such as environmental regulations and health hazards associated with cresol exposure. Regulatory bodies have implemented strict guidelines to limit emissions and ensure safe handling and disposal of cresol-based products, which can increase production costs and complexity for manufacturers. Furthermore, fluctuations in raw material prices and supply chain disruptions may impact market dynamics.

Despite these challenges, the Cresol Market is expected to experience steady growth, supported by ongoing research and development efforts to enhance production processes and develop safer, more sustainable products. Innovations in the field, coupled with the rising adoption of cresol in emerging markets, present opportunities for future expansion. Companies are also exploring bio-based cresol alternatives to meet the increasing demand for environmentally friendly solutions, paving the way for a more sustainable market landscape.

Request the sample copy of report @ https://www.globalinsightservices.com/request-sample/GIS32249

0 notes

Text

Carbon Black Prices Trend | Pricing | News | Database | Chart

The global carbon black market has witnessed dynamic changes in recent years, influenced by factors such as raw material costs, demand from end-use industries, and regulatory frameworks. Carbon black, a critical component in tire manufacturing, paints, plastics, and inks, remains a key commodity in industrial applications worldwide. Price fluctuations in the carbon black market are shaped by a combination of supply-demand dynamics, feedstock costs, and geopolitical events impacting global trade.

One of the primary drivers of carbon black prices is the cost of its feedstock, which is typically derived from oil or coal tar. Crude oil price volatility significantly affects the cost structure of carbon black production. When oil prices rise, the cost of carbon black feedstock, such as carbon black oil (CBO) or coal tar, also increases, leading to higher production costs. Conversely, lower crude oil prices generally provide some relief to carbon black manufacturers, potentially translating to more competitive pricing. However, the relationship between crude oil prices and carbon black prices is not always linear due to other contributing factors, such as refinery capacity, feedstock availability, and production efficiency.

Demand from the automotive and tire industries is another critical factor influencing carbon black prices. The automotive sector, as a major consumer of tires, directly impacts the carbon black market. An increase in vehicle production drives higher demand for tires, thereby boosting the need for carbon black. In periods of robust automotive market performance, carbon black prices tend to rise due to heightened demand. Conversely, economic slowdowns or disruptions in vehicle production often lead to reduced demand, placing downward pressure on carbon black prices. Moreover, the growing adoption of electric vehicles (EVs) is reshaping the dynamics of the tire industry and, by extension, the carbon black market. EV tires often require higher performance specifications, which could influence the types and grades of carbon black in demand.

Get Real time Prices for Carbon Black: https://www.chemanalyst.com/Pricing-data/carbon-black-42

Regional factors also play a pivotal role in determining carbon black prices. Asia-Pacific, particularly China and India, dominates the global carbon black production landscape. These countries benefit from lower production costs, driven by abundant feedstock availability and less stringent environmental regulations compared to Western markets. Consequently, Asia-Pacific producers often set the benchmark for global carbon black prices. On the other hand, North America and Europe face higher production costs due to stricter environmental standards and higher labor expenses, which can lead to regional price disparities. Additionally, trade policies, tariffs, and anti-dumping duties imposed by various countries further influence regional pricing trends.

Environmental regulations and sustainability initiatives are increasingly shaping the carbon black market. Governments worldwide are implementing stringent measures to reduce carbon emissions and environmental pollution, which directly impact the production processes of carbon black manufacturers. These regulations often necessitate the adoption of cleaner technologies, thereby increasing production costs. For instance, the shift toward gas-based carbon black production as opposed to traditional oil or coal-based methods is a response to regulatory pressures. While this transition supports environmental goals, it also affects the pricing structure of carbon black products.

The rise of sustainable alternatives and recycled carbon black (rCB) is another noteworthy trend influencing market dynamics. Recycled carbon black, derived from end-of-life tires and other rubber products, offers a more environmentally friendly solution compared to virgin carbon black. While still a nascent segment, the rCB market is gradually gaining traction, supported by advancements in pyrolysis technologies and increasing environmental awareness. The growing availability of rCB could exert downward pressure on conventional carbon black prices, particularly in markets with stringent sustainability mandates.

Global supply chain disruptions have also played a significant role in recent carbon black price fluctuations. Events such as the COVID-19 pandemic and geopolitical conflicts have impacted the supply of raw materials and disrupted transportation networks. These disruptions have, at times, led to supply shortages and increased costs for carbon black manufacturers, thereby pushing up market prices. Furthermore, capacity expansions or closures by major manufacturers can also influence market dynamics. New production facilities coming online can alleviate supply constraints and stabilize prices, while plant shutdowns or capacity reductions tend to create supply bottlenecks, leading to price spikes.

Another factor shaping the carbon black market is the innovation and development of specialty grades. Specialty carbon black grades are used in high-performance applications such as advanced coatings, electronics, and specialty polymers. These grades command higher prices due to their superior properties and the complexity of their manufacturing processes. The rising demand for specialty carbon blacks in niche applications is adding a premium to overall market pricing. Additionally, manufacturers are investing heavily in research and development to enhance product quality, which also influences the cost structure.

In the context of market competitiveness, the carbon black industry is characterized by the presence of both established global players and regional manufacturers. Leading companies such as Cabot Corporation, Birla Carbon, and Orion Engineered Carbons dominate the market with their extensive product portfolios and global reach. These players often have better control over pricing due to their economies of scale and advanced manufacturing capabilities. Meanwhile, smaller regional players focus on cost competitiveness and localized supply, contributing to price variations across different markets.

In conclusion, carbon black prices are influenced by a multifaceted interplay of factors, including feedstock costs, industrial demand, regional dynamics, regulatory frameworks, and emerging trends in sustainability and technology. As industries continue to evolve and prioritize environmental considerations, the carbon black market is likely to see further shifts in pricing strategies and product innovations. Stakeholders in this market must navigate these complexities to remain competitive and adapt to the changing landscape of industrial materials.

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Carbon Black#Carbon Black Price#Carbon Black Prices#Carbon Black Pricing#Carbon Black News#Carbon Black Price Monitor

0 notes

Text

Trends in JSW Steel Prices: Key Factors and Future Projections

JSW Steel, a major player in India's steel industry, has been a critical contributor to meeting the country's growing demand for steel. The company’s pricing trends offer essential insights for

industries that rely heavily on steel, such as construction, automotive, and infrastructure. For businesses, developers, and investors, understanding the fluctuations in JSW Steel prices is crucial to making informed financial and project decisions. This article will explore the latest developments in JSW Steel prices, examine the factors that drive these shifts, and consider the likely trajectory of future prices.

Analyzing the Recent Trends in JSW Steel Prices

In recent years, JSW Steel prices have experienced notable fluctuations driven by various economic, industrial, and geopolitical factors. As of 2024, prices remain elevated compared to pre-pandemic levels, largely due to heightened demand and increased production costs. The Indian government’s extensive infrastructure initiatives, such as the Smart Cities Mission and the National Infrastructure Pipeline, have led to consistent demand, further bolstering JSW Steel prices in the domestic market.

JSW Steel prices have also been influenced by global factors. The COVID-19 pandemic had lasting effects on global supply chains, causing significant disruptions in the availability and cost of raw materials. The recent Russia-Ukraine conflict exacerbated these challenges, contributing to supply constraints across Europe and Asia. In response, JSW Steel adjusted its prices to account for the increased costs of critical resources like iron ore and coking coal. Although the company has made strides to secure a stable raw material supply through acquisitions and backward integration, global disruptions in mining and logistics still impact its production costs and, consequently, its pricing.

Factors Affecting JSW Steel Prices

1. Raw Material Availability and Costs

The availability and price of essential raw materials, such as iron ore, coking coal, and scrap metal, are primary factors impacting JSW Steel prices. Fluctuations in the global market prices of these materials lead to direct changes in production costs. Recent years have seen significant volatility in iron ore and coking coal prices, primarily due to logistical challenges, trade restrictions, and shifts in mining output.

To mitigate the volatility of raw material prices, JSW Steel has invested in securing its own mining assets, aiming for a stable supply of high-quality materials. However, the company’s reliance on imports for certain resources means that it remains sensitive to international market changes and geopolitical influences. Furthermore, the steelmaking process is energy-intensive, and rising energy costs have placed additional pressure on the company’s production expenses.

Environmental regulations are another factor affecting raw material costs and availability. As countries enact stricter environmental policies, access to certain raw materials may be restricted, or production costs could rise due to the need for cleaner, more sustainable operations. In response, JSW Steel has committed to sustainable practices, investing in energy-efficient and environmentally-friendly production processes. While this approach may result in higher costs initially, it supports JSW’s long-term competitiveness and aligns with the global shift toward green steel.

2. Economic Policies and Global Market Conditions

The economic policies and trade agreements of major steel-producing and -consuming nations greatly impact JSW Steel prices. In India, government policies aimed at stimulating infrastructure development have led to increased steel demand, which supports higher prices. Initiatives such as affordable housing projects and investments in road, rail, and port facilities create a steady demand for steel, positively impacting JSW Steel’s pricing.

On the international front, tariffs and trade restrictions influence the competitive landscape. For instance, tariffs imposed by the United States on steel imports led to price increases within the U.S., impacting demand and creating opportunities for local players like JSW to expand in other markets. Additionally, trade tensions or sanctions between steel-producing nations can affect global supply, which in turn influences JSW’s pricing strategy.

Geopolitical events, such as the Russia-Ukraine conflict, have also had far-reaching effects on the steel market. As major suppliers of steel and iron ore, Russia and Ukraine’s output disruptions have led to increased prices in several markets. Such geopolitical shifts create ripple effects across global supply chains, making it more challenging for JSW Steel to maintain stable pricing, especially if replacement suppliers charge a premium.

Inflation is yet another factor affecting JSW Steel prices. Rising inflation drives up costs for raw materials, energy, and labor, all of which impact the price of steel. This situation is particularly evident in India, where inflationary pressures on resources and transport have led to overall increases in steel production costs. As a result, JSW Steel has had to adjust its prices accordingly to ensure profitability while meeting rising demand.

Future Outlook for JSW Steel Prices

Looking ahead, the future of JSW Steel prices will be shaped by multiple factors, including infrastructure expansion, technological advancements, and environmental regulations. India’s ambitious infrastructure goals indicate that demand for steel will remain robust, which could provide strong support for JSW’s pricing. As the company continues to expand production capacity and optimize its operations, it is well-positioned to meet the projected demand while managing costs effectively.

However, potential challenges could arise. Any slowdown in global economic activity, such as a recession or a decline in key steel-consuming industries like automotive and construction, could dampen demand and place downward pressure on prices. Additionally, if global steel production increases significantly, a supply surplus may drive prices down. This is especially relevant as other major steel-producing countries like China and the United States adjust their production output in response to domestic and international demand.

Conclusion: Navigating the Trends in JSW Steel Prices

JSW Steel prices are influenced by a mix of local demand, raw material costs, and global economic conditions. The company’s ability to navigate these factors while investing in sustainable practices and production capacity expansions will be crucial for maintaining its position in a competitive industry. With a favorable demand outlook driven by India’s infrastructure projects, JSW Steel is well-prepared to meet market needs, though it must remain adaptive to external challenges, from geopolitical uncertainties to rising environmental standards.

If you are looking for best quality jsw steel, please visit our website : www.steeloncall.com or you can contact us through our toll-free number: 18008332929

#JSWSteelPrices #SteelMarket #SteelIndustryTrends #SustainableSteel #SteelOutlook

1 note

·

View note

Text

Anthracene Market — Forecast(2024–2030)

Anthracene Market size is forecast to reach US$440.3 million by 2030, after growing at a CAGR of 4.1% during 2024–2030. Anthracene is a three-fused benzene ring solid polycyclic aromatic hydrocarbon (PAH) with the formula C14H10 and is often found in coal tar. Anthracene is extensively utilized in the manufacture of red dye alizarin, insecticides, anti-cancer agents, wood preservatives, organic light-emitting diodes, and more. The rapid growth in the number of cancer patients has increased the demand for anti-cancer agents. With cancer incidence on the rise, there is a consequential surge in the demand for anti-cancer agents, and anthracene plays a pivotal role in this context. Anthracene derivatives are integral components of various pharmaceuticals and therapeutic agents designed to combat cancer. As research and development in oncology intensify, anthracene’s significance as a key building block in anti-cancer drug formulations is amplifying.

The market’s trajectory is intricately linked to advancements in cancer treatment, making anthracene a critical element in the pharmaceutical industry’s ongoing efforts to address the global cancer burden thereby, fueling the anthracene market growth. Another factor assisting the growth of the global anthracene market is the increasing production of coal tar. The anthracene market is benefiting from the escalating production of coal tar, a key source of anthracene. Increased coal tar output meets the rising demand for anthracene, particularly in the pharmaceutical and chemical sectors. Furthermore, the flourishing textile industry is also expected to drive the anthracene market substantially during the forecast period.

Request Sample

Anthracene Market COVID-19 Impact

The COVID-19 outbreak had a significant effect on the agriculture, electronics, textile, and furniture industry. Due to this the demand for anthracene significantly reduced, which affected the overall market growth. According to the Vietnam Textile and Apparel Association (VITAS). Aside from restrictions, the textile industry faced plenty of issues, including production bottlenecks, fluctuating raw material prices, transportation issues, a scarcity of skilled workers, the sale of textile products, and reduced export/import orders. The COVID-19 pandemic caused significant disruptions in the textile industry, including production, exports, and logistics management. The first disruption occurred in production during the first quarter (Q1) of 2020 when China went into lockdown, causing shortages of materials. The second disruption in exports started in Q2 2020 when COVID-19 spread to the export destinations. As a result, these back-to-back disruptions badly affected the textile industry globally, resulting in a downdrift in anthracene market revenue.

Report Coverage

The report: “Anthracene Market — Forecast (2024–2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the anthracene market.

By Application: Wood Preservatives, Pesticides (Insecticides, Herbicides, and Fungicides), Plasticizers, Drugs (Anti-Cancer Agent, Anti-Psoriatic Agent, and Others), Dyes & Coatings (Conformal Coating, Red Dye Alizarin, and Others), Electronics (Organic Light-Emitting Diodes, Transistors, Photovoltaic, and Others), scintillators, and Others.

By Geography: North America (USA, Canada, and Mexico), Europe (UK, Germany, France, Italy, Netherlands, Spain, Russia, Belgium, and Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia and New Zealand, Indonesia, Taiwan, Malaysia, and Rest of APAC), South America (Brazil, Argentina, Colombia, Chile, and Rest of South America), Rest of the World (Middle East, and Africa).

Inquiry Before Buying

Key Takeaways

● Asia-Pacific dominates the Anthracene market, owing to the expanding pharmaceutical, textile, and electronics industries in the region. Increasing per capita income coupled with the increasing population is the major factor that is driving the pharmaceutical, textile, and electronics industries in the region.

● Anthracene is expected to grow into a major market owing to its utility in identifying situations such as radiation leaks. Following the radiation leak in Japan, there has been an increase in demand for proper radiation leak-checking equipment at nuclear reactor sites all over the world. This is expected to boost the market for anthracene, which is used in scintillators as a luminescent material.

For More Details on This Report — Request for Sample

Anthracene Market Segment Analysis — By Application

The dyes & coatings segment held the largest share in the anthracene market in 2023 and is forecasted to grow at a CAGR of 3.8% during 2024–2030, owing to the increasing demand for anthracene to manufacture conformal coating and red dye alizarin. Anthracene is colorless in nature but exhibits a blue fluorescence under ultraviolet light. Thus, it is used in the production of red dye alizarin and coatings. Anthracene is commonly used as a UV tracer in conformal coatings applied to printed circuit boards. The anthracene tracer permits UV inspection of the conformal coating. It’s one of the most important feedstocks for anthraquinone production. Vat dyes are a class of water-insoluble dyes that can be easily reduced to a water-soluble, usually colorless leuco form that readily impregnates fibers and textiles. Anthraquinone is a common and important raw material in the production of vat dyes. Their main characteristics are brightness and fastness. And such extensive application of anthracene in the dyes & coatings industry is estimated to fuel the anthracene market growth during the forecast period.

Buy Now

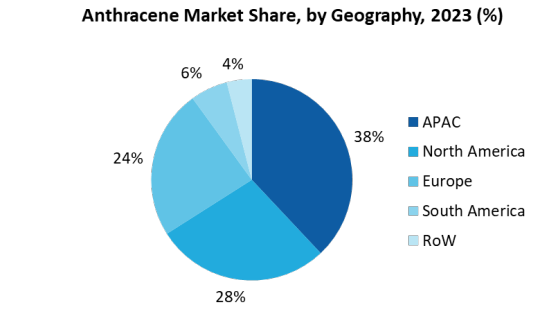

Anthracene Market Segment Analysis — By Geography

Asia-Pacific region held the largest share in the anthracene market in 2023 up to 34% and is estimated to grow at a CAGR of 4.6% during 2024–2030, owing to the flourishing textile and printed circuit board industry in the region, which is accelerating the demand for anthracene in the region. India’s textile and apparel market was valued at US$108.5 billion in 2015 and is projected to rise to US$226 billion by 2023, with a compound annual growth rate of 8.7% between 2009 and 2023. The Government of India is strongly encouraging the manufacturing and usage of Printed circuit boards in the country. It has launched many initiatives such as ‘Make in India’, ‘Digital India’, and more. By easing the tax regime and lowering bureaucratic barriers, the government hopes to encourage manufacturers to set up more local plants in the country. This is expected to bring in a significant positive impact on the overall printed circuit board demand. Thus, the increasing demand for textiles and printed circuit boards in the region is set to drive the anthracene industry in Asia-Pacific during the forecast period.

Anthracene Market Drivers

Increasing Prevalence of Cancer Patients

The anthracene-9,10-dione (anthraquinone) derivatives are a particularly valuable class in the development of anticancer drugs. Since the discovery of these chemotypes, medicinal chemists have been drawn to anthracycline antibiotics because of their outstanding antitumor potency. Doxorubicin, mitoxantrone, and more recently epirubicin, idarubicin, and valrubicin are anthraquinone-based drugs that have been successfully used in the treatment of hematological and solid tumors. World Health Organization (WHO) says cancer is one of the leading causes of death worldwide. According to World Health Organisation 2023, An estimated 10 million people died from cancer worldwide, and there were 20 million new instances of the disease. Over the next 20 years, there will be a 60% rise in the cancer burden, placing additional strain on communities, individuals, and health systems. In low- and middle-income nations, the biggest increases in the global burden of cancer cases are expected to occur, with an estimated 30 million more cases worldwide by 2040. Due to this increase in the number of cancer patients the demand for anti-cancer agents will significantly increase, owing to which the Anthracene market will exhibit rapid growth over the forecast period.

Soaring Demand from the Agriculture Industry

Anthracene is extensively used in the agriculture sector as herbicides, insecticides, and fungicides. The world population is gradually increasing. With the population steadily growing, enough crops must be produced each year to provide food to people. And pesticides such as herbicides, insecticides, and fungicides play an important role in providing crops with the nutrients they need to grow and enhance crop yield. Thus, to improve the crop yield within the same area of arable lands and provide crops proper nutrients, pesticides are being extensively utilized during crop production. According to European Commission in March 2023, Italian rice is mostly grown in northern regions of Lombardy. Italy is the world’s only grower of types such as Arborio and Carnaroli that are most suitable for the popular Italian dish risotto. With the increasing crop production, there is an increasing demand for pesticides, which is driving the anthracene market in the agriculture sector.

Anthracene Market Challenges

Various Hazards Associated with Anthracene

If inhaled through contaminated air, anthracene has harmful effects on the body. The Occupational Safety and Health Administration’s (OSHA) Hazardous Substance List includes anthracene. When someone inhales it, their lungs are first and foremost damaged. If a person works at a hazardous waste site where polycyclic aromatic hydrocarbons (PAH) are disposed of, there is a high risk of inhaling anthracene and polycyclic aromatic hydrocarbons (PAH). Similarly, it can enter one’s body through foods and beverages. When a person’s skin comes into contact with creosote, roofing tar, heavy oils, or coal tar, as well as contaminated soil containing PAHs, there is a risk of exposure. Once inside the human body, the polycyclic aromatic hydrocarbon (PAH) can spread and target fat tissues. The kidneys, liver, and fat tissues in the human body may be affected. When people are exposed to it, it can harm their health by irritating their eyes, skin, and respiratory tract. When exposed to the environment, it can also cause fire and explosion. Thus, these hazards associated with anthracene are anticipated to hamper the anthracene market.

Anthracene Market Landscape

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the Anthracene market. Anthracene market top companies include:

1. Fisher Scientific

2. Tokyo Chemical Industry Co., Ltd.

3. CHEMOS GmbH & Co. KG

4. Santa Cruz Biotechnology, Inc.

5. Haihang Industry Co., Ltd.

6. Wego Chemical Group

7. Glentham Life Sciences

8. Spectrum Chemical

9. Merck KGaA

10. Henan Daken Chemical Co., Ltd.

0 notes

Text

Global Needle Coke Market, Market Size, Market Share, Key Players | BIS Research

The Global Needle Coke Market refers to the industry segment focused on the development, production, and distribution of building materials that have a reduced carbon footprint compared to traditional materials. These materials are designed to minimize greenhouse gas emissions throughout their lifecycle—from extraction, manufacturing, and transportation to use and disposal.

The global needle coke market was valued at $3.05 billion in 2023, and is expected to grow at a CAGR of 7.99% and reach $6.58 billion by 2023

Market Overview

Needle coke is a high-quality carbon material primarily used in the production of graphite electrodes, which are essential for electric arc furnaces in the steelmaking industry. Needle coke has a unique needle-like structure, high thermal conductivity, and low coefficient of thermal expansion, making it a crucial material for industries requiring strong, heat-resistant carbon.

Types of Needle Coke

Petroleum based needle coke - Derived from petroleum refining byproducts, particularly decant oil or slurry oil.

Coal based needle coke- Produced from coal tar, a byproduct of the coke-making process in steel production.

Download the TOC and get more information @ Global Needle Coke Market

Key Applications

Graphite Electrodes for steelmaking - The primary application of needle coke is in the production of graphite electrodes, which are essential in electric arc furnaces (EAF) used for steel production.

Lithium Ion Batteries - Needle coke is used to produce synthetic graphite anodes for lithium-ion batteries, a critical component in electric vehicles (EVs) and energy storage systems.

Major Key Players

Asbury Carbons

Gazpromneft

China Petroleum & Chemical Corporation

Shandong Jingyang Technology Co. Ltd

GrafTech International

Download the sample page click here@ Global Needle Coke Market

Market Demand Driver: Carbon Reduction Mandates and Environmental Standards

The needle coke market is poised for significant growth, propelled by the increasing adoption of the electric arc furnace (EAF) steelmaking process and the mounting pressure to achieve carbon neutrality targets. Sustainability considerations are reshaping the steel industry; the EAF process offers a more environmentally conscious approach compared to the traditional basic oxygen furnace (BOF) method. This shift favors needle coke, a critical material for EAF graphite electrode production

Future Outlook

The needle coke market is expected to witness sustained growth due to rising steel production through electric arc furnaces and increasing lithium-ion battery demand for electric vehicles and energy storage systems. However, environmental regulations, supply chain constraints, and price volatility will continue to shape the industry.

The market outlook is shaped by several key trends:

Rising Demand in Steelmaking

Expansion of Electric Vehicle (EV) Market

Supply Constraints

Technological Advancements

Conclusion

The global needle coke market is positioned for substantial growth, driven by increasing demand from the steel industry and the expanding electric vehicle (EV) market. As electric arc furnaces (EAF) gain traction in steel production and lithium-ion battery usage surges, the need for high-quality needle coke will rise. However, supply constraints, environmental concerns, and production challenges may create volatility in the market.

0 notes

Text

Toluene and Derivatives Market Analysis: Assessing Growth Opportunities

Toluene and its derivatives are essential chemicals with diverse industrial applications, playing crucial roles in sectors such as chemicals, petrochemicals, paints, coatings, and pharmaceuticals. This blog explores the dynamics of the global toluene and derivatives market, analyzing key drivers, applications across industries, emerging trends, and future growth opportunities.

Understanding the Toluene and Derivatives Market:

Toluene (C7H8) is a colorless, aromatic hydrocarbon solvent derived from petroleum and coal tar. It serves as a precursor for various chemicals and industrial products, including benzene, xylene, toluene diisocyanate (TDI), and trimethylbenzene, among others.

Market Dynamics:

Benzene and Xylene Production: Toluene is a primary raw material in the production of benzene and xylene, which are essential chemicals used in manufacturing plastics, resins, synthetic fibers, and pharmaceuticals.

Toluene Diisocyanate (TDI) Production: Toluene is a key feedstock for the production of TDI, a crucial component in polyurethane foams, coatings, adhesives, and flexible foam products used in construction, automotive, and furniture industries.

Solvents and Coatings: Toluene finds extensive use as a solvent in paints, coatings, adhesives, inks, and cleaning agents due to its excellent solvency properties, fast evaporation rate, and compatibility with various resins.

Pharmaceuticals and Chemicals: Toluene derivatives are utilized in the production of pharmaceuticals, dyes, explosives, rubber chemicals, and specialty chemicals, contributing to diverse industrial applications.

Applications Across Industries:

Chemicals and Petrochemicals: Benzene, xylene, TDI, trimethylbenzene production.

Coatings and Paints: Solvent in paints, coatings, adhesives, and inks.

Polyurethane Industry: TDI for polyurethane foams, sealants, and adhesives.

Pharmaceuticals and Specialty Chemicals: Intermediate chemicals for various applications.

Market Trends:

Focus on Sustainable Feedstocks: Industry shifts towards bio-based and renewable feedstocks for toluene derivatives production to align with sustainability goals and reduce environmental impact.

Technological Advancements: Innovations in production processes, catalyst technologies, and recycling methods enhance efficiency, reduce costs, and promote circular economy practices in the toluene and derivatives market.

Regulatory Compliance: Stringent regulations and standards related to chemical safety, emissions, and product quality drive investments in cleaner production methods and product innovations.

Future Prospects:

The global toluene and derivatives market is poised for continued growth, driven by increasing demand from key industries, technological advancements, and sustainability initiatives. Investments in R&D, green chemistry, and circular economy models will shape the market's evolution and competitiveness.

Conclusion:

Toluene and its derivatives play indispensable roles in various industrial sectors, offering versatile solutions for chemical manufacturing, coatings, polyurethane production, and specialty chemicals. Navigating the market requires awareness of trends, regulatory landscapes, and technological innovations. With a focus on sustainability, innovation, and market diversification, the toluene and derivatives market presents promising opportunities for growth and advancements in global industrial processes and products.

0 notes

Text

Analyzing Mesitylene Production Cost Report

Latest report titled “Mesitylene Production Cost Report” by Procurement Resource, a global procurement research and consulting firm, provides an in-depth cost analysis of the production process of Mesitylene. Mesitylene, also known as 1,3,5-trimethylbenzene, is an aromatic hydrocarbon compound with various industrial applications, including as a solvent, intermediate in chemical synthesis, and component in fuel additives. Understanding the production cost of mesitylene is essential for manufacturers to ensure profitability, competitiveness, and sustainability. This article aims to explore the intricacies of mesitylene production cost, examining the underlying factors, recent trends, and strategies for cost optimization.

Procurement Resource study is based on the latest prices and other economic data available. It also offers additional analysis of the report with detailed breakdown of all cost components (capital investment details, production cost details, economics for another plant location, dynamic cost model). In addition, the report incorporates the production process with detailed process and material flow, capital investment, operating costs along with financial expenses and depreciation charges.

Request For Sample: https://www.procurementresource.com/production-cost-report-store/mesitylene/request-sample

Procurement Resource’s detailed report describes the stepwise consumption of material and utilities along with a detailed process flow diagram. Furthermore, the study assesses the latest developments within the industry that might influence Mesitylene production cost, looking into capacity expansions, plant turnarounds, mergers, acquisitions, and investments.

Procurement Resource Assessment of Mesitylene Production Process:

From Distillation Process: This report presents the detailed production methodology and cost analysis of Mesitylene industrial production across Mesitylene manufacturing plants. The production process begins with the treatment of acetone with sulfuric acid, where sulfuric acid acts as a dehydrating agent. This reaction causes the distillation of acetone, ultimately yielding mesitylene or 1,3,5-trimethylbenzene as the final product.

Product Definition:

Mesitylene, or 1,3,5-trimethylbenzene, is an aromatic hydrocarbon with the chemical formula C9H12. It is a colorless, flammable liquid with a distinctive odor, consisting of a benzene ring with methyl groups attached at the 1st, 3rd, and 5th positions. Insoluble in water, it is soluble in various organic solvents such as ethanol, ethyl ether, and acetone. Mesitylene's melting and boiling points are approximately -44.8 °C and 164.7 °C, respectively, with a density of 0.86 g/cm3 at 25 °C. Primarily used as a chemical intermediate and solvent, mesitylene is vital in the production of coatings, printing chemicals, sealants, and adhesives. It serves as a combustible additive in fuels and finds applications in plastics, dyestuffs, inks, and toners. Naturally occurring in coal tar, mesitylene is also synthetically produced by distilling acetone. Its versatility and role in various chemical processes make it a valuable compound in the chemical industry.

Market Drivers:

The demand for mesitylene is primarily driven by its role as a chemical solvent in various downstream industries, including dyestuffs, plastics, and petrochemicals. Its use in formulating adhesives, sealants, and dyestuff chemicals contributes significantly to its demand in the chemical market. Additionally, its incorporation in the production of petrochemicals and fuels enhances its global demand. Mesitylene is characterized as a volatile and combustible fluid with strong solvency properties. Its applications in manufacturing plastics, coating chemicals, and derivatives like mesityl oxide further bolster its demand and impact its overall procurement.

1. Overview of Mesitylene Production:

Mesitylene can be produced through several methods, including the catalytic alkylation of benzene with propylene, the thermal cracking of hydrocarbons, and the dehydrogenation of 2,4,6-trimethylcyclohexanone. Among these methods, catalytic alkylation is the most common industrial process for mesitylene production.

Catalytic Alkylation Process:

Raw Material Preparation: The primary raw materials for mesitylene production include benzene and propylene. Benzene, a widely available aromatic hydrocarbon, serves as the aromatic ring precursor, while propylene, a by-product of petroleum refining, acts as the alkylating agent.

Alkylation Reaction: Benzene and propylene are fed into a reactor containing a solid acid catalyst, such as aluminum chloride or zeolites. Under controlled temperature and pressure conditions, propylene reacts with benzene to form mesitylene and other alkylated benzene compounds.

Separation and Purification: The reaction mixture undergoes separation to isolate mesitylene from other reaction products and unreacted starting materials. Separation techniques such as distillation, extraction, and chromatography are employed to purify mesitylene to the desired level.

Refining and Quality Control: The purified mesitylene undergoes further refining steps to remove impurities and ensure product quality. Quality control measures, including analytical testing and certification, verify compliance with industry standards and specifications.

Packaging and Distribution: The refined mesitylene is packaged into drums, containers, or tankers for distribution to end-users in various industries, including chemical manufacturing, pharmaceuticals, and coatings.

2. Factors Influencing Mesitylene Production Cost:

Several factors influence the production cost of mesitylene:

Raw Material Costs: The prices of raw materials such as benzene and propylene directly impact production costs. Fluctuations in raw material prices, influenced by market demand, supply availability, and geopolitical factors, can affect overall production expenses.

Catalyst Usage and Regeneration: The cost of solid acid catalysts used in the alkylation process, as well as the frequency of catalyst regeneration or replacement, impact production costs. Catalyst efficiency, activity, and stability are critical factors affecting process economics.

Energy Consumption: The production process involves energy-intensive operations such as heating, mixing, and distillation. Energy costs, including electricity, steam, and fuel, significantly contribute to production expenses and are subject to market fluctuations.

Process Efficiency: The efficiency of the alkylation reaction, separation, and purification processes affects production yields, product quality, and resource utilization. Optimization of reaction conditions, catalyst activity, and process parameters can improve efficiency and reduce production costs.

Labor Costs: Skilled labor is required for operating production equipment, monitoring processes, and performing quality control tests. Labor costs, including wages, benefits, and training expenses, constitute a significant portion of production costs.

3. Recent Trends in Mesitylene Production Cost:

Recent trends in the chemical industry have influenced mesitylene production costs:

Technological Advancements: Advances in catalysis, process intensification, and automation have improved production efficiency and reduced costs. Continuous innovation in catalyst design, reactor engineering, and control systems contributes to cost competitiveness.

Feedstock Availability: Changes in the availability and pricing of feedstocks such as benzene and propylene, driven by shifts in petrochemical markets and refining capacities, impact production costs and supply chain dynamics.

Environmental Regulations: Compliance with environmental regulations, including emissions standards, waste management, and sustainability initiatives, necessitates investments in pollution abatement measures and regulatory compliance monitoring, increasing production costs.

Market Demand and Competition: Fluctuations in market demand, competitive pressures, and changing customer preferences influence pricing strategies and cost optimization efforts among mesitylene manufacturers. Cost-effective production methods and value-added services are essential for maintaining market share and profitability.

4. Strategies for Cost Optimization:

To optimize mesitylene production costs, manufacturers can implement various strategies:

Raw Material Optimization: Explore alternative feedstock sources, negotiate favorable pricing terms with suppliers, and invest in feedstock diversification to mitigate price volatility and supply chain risks.

Catalyst Selection and Regeneration: Evaluate catalyst performance, activity, and longevity to minimize catalyst usage and regeneration costs. Invest in catalyst research and development to improve efficiency and reduce catalyst-related expenses.

Energy Efficiency: Implement energy-saving technologies, equipment upgrades, and heat integration strategies to reduce energy consumption and lower operating costs. Conduct energy audits and optimization studies to identify opportunities for efficiency improvements.

Process Optimization: Continuously optimize reaction conditions, process parameters, and purification techniques to improve yield, selectivity, and product quality while reducing resource consumption and waste generation.

Supply Chain Management: Streamline supply chain logistics, optimize inventory management, and foster strategic partnerships with suppliers and distributors to reduce transportation costs and minimize supply chain disruptions.

Conclusion:

In conclusion, the production cost of mesitylene is influenced by a multitude of factors, including raw material costs, catalyst usage, energy consumption, process efficiency, and market dynamics. By understanding these factors and implementing strategic approaches for cost optimization, manufacturers can enhance competitiveness, improve profitability, and ensure the affordability and availability of mesitylene for various industrial applications. Continuous innovation, process optimization, and sustainability initiatives are essential for navigating challenges and sustaining long-term success in the mesitylene production industry.

Contact Us:

Company Name: Procurement Resource Contact Person: Leo Frank Email: [email protected] Toll-Free Number: USA & Canada – Phone no: +1 307 363 1045 | UK – Phone no: +44 7537 132103 | Asia-Pacific (APAC) – Phone no: +91 1203185500 Address: 30 North Gould Street, Sheridan, WY 82801, USA

0 notes

Text

Needle Coke Market Size and Share: An In-depth Examination of Market Metrics

The Needle Coke market is estimated to be valued at US$ 2.99 Bn in 2023 and is expected to exhibit a CAGR of 10% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Overview:

Needle coke is a specialty type of petroleum coke used in the production of ultra-high power graphite electrodes, which are primarily used in electric arc furnaces for steel production. It has high mechanical strength and electrical conductivity properties essential for graphite electrode production. Needle coke is produced by thermal cracking and isles heating of coal tar pitch or petroleum pitch residue under oxygen-free conditions. Market Dynamics:

The rising demand for needle coke market from the graphite electrode industry is the major factor driving the growth of the market. Graphite electrodes are used for melting scrap steel in electric arc furnaces. With the increasing steel production globally, particularly in developing economies such as China and India, the demand for graphite electrodes has increased substantially over the years. According to World Steel Association, crude steel production increased from 1,808 million tons in 2018 to 1,895 million tons in 2019. This rising steel production is augmenting the demand for needle coke from the graphite electrode industry. Additionally, limited availability of substitutes for needle coke in ultra-high power graphite electrode manufacturing is another factor fueling the needle coke market growth. SWOT Analysis

Strength: Needle coke has high electrical conductivity and chemical resistance which makes it ideal for graphite electrodes used in electric arc furnaces for steelmaking. It has low coefficient of thermal expansion and high dimensional stability at high temperatures. It is available in large piece size suitable for graphite electrodes upto 4.5m in length.

Weakness: Needle coke manufacturing process requires petroleum pitch as raw material. Fluctuations in crude oil prices directly impact the production cost. High capital investment is required to set up needle coke production facilities.

Opportunity: Increasing steel production driven by growth in construction and automotive industries worldwide presents growth opportunity for needle coke. Expanding graphite electrodes manufacturing capacity, especially in Asian countries will drive the demand for needle coke.

Threats: Strict environmental regulations limiting coke oven operations could impact the supply of needle coke. Alternative materials like scrap-based electric arc furnace production may reduce the demand for graphite electrodes.

Key Takeaways

The global Needle Coke market is expected to witness high growth, exhibiting CAGR of 10.% over the forecast period, due to increasing steel production worldwide driven by growth in construction and automotive industries. Regional analysis: Asia Pacific dominates the global needle coke market, accounting for over 50% share of the total market in 2023. China, Japan and India are major consumers as well as producers in the region. Growing steel industry especially in China and India is driving the growth of needle coke market in Asia Pacific. North America is the second largest market for needle coke led by the US. Presence of large automotive industry and shale gas production is fueling the market growth in this region. Key players operating in the Needle Coke market are Baosteel Group, C-Chem Co. Ltd, China National Petroleum Corporation, ENEOS Corporation, Kaifeng Pingmei New Carbon Material Technology Co. Ltd (KFCC), Mitsubishi Chemical Corporation, Phillips 66 Company, PMS Tech (a joint venture of POSCO Chemtech and Mitsubishi Chemical), Seadrift Coke L.P. (GrafTech International), Shandong Jing Yang Technology Co. Ltd, Shandong Yida Rongtong Trading Co. Ltd, Shanxi Hongte Coal Chemical Co. Ltd, and Sinosteel Corporation. The market is highly consolidated with top five players accounting for over 50% of the total production capacity. Key players are focused on capacity expansion plans and long term supply agreements with graphite electrode manufacturers.

0 notes

Text

Naphthalene Price | Prices | Pricing | News | Database | Chart

Naphthalene is a crucial chemical compound in various industrial applications, playing a significant role in the production of numerous products such as mothballs, plastics, and dyes. Over the years, naphthalene prices have experienced fluctuations due to a myriad of factors, including raw material availability, energy costs, global demand trends, and regulatory changes. Understanding the dynamics behind the pricing of naphthalene is essential for stakeholders in industries that depend on this versatile compound.

One of the primary factors influencing naphthalene prices is the cost of raw materials, primarily crude oil and coal tar, from which naphthalene is derived. Since naphthalene is a hydrocarbon, it is closely linked to the oil market, and any changes in crude oil prices can have a direct impact on its production cost. Global oil prices have been notably volatile in recent years due to geopolitical tensions, supply chain disruptions, and shifting policies concerning fossil fuels. As a result, naphthalene prices tend to mirror these fluctuations. When crude oil prices surge, the cost of producing naphthalene also rises, leading to higher market prices. Conversely, when oil prices stabilize or decline, there is usually a corresponding decrease in naphthalene prices.

Get Real Time Prices for Naphthalene: https://www.chemanalyst.com/Pricing-data/naphthalene-1130

In addition to raw material costs, energy prices are another significant factor affecting naphthalene prices. Manufacturing naphthalene requires substantial energy input, especially in the extraction and distillation processes. Therefore, the cost of electricity, natural gas, and other energy sources can significantly influence the price of naphthalene. Energy prices can be affected by a variety of external factors, including government policies on energy production, global energy supply-demand balance, and regional disruptions. When energy prices rise, the cost of producing naphthalene increases, which is then passed on to consumers in the form of higher prices.

Global demand also plays a pivotal role in determining naphthalene prices. The compound is widely used in the construction, chemical, and textile industries, among others. When there is a surge in demand from these sectors, it can lead to higher naphthalene prices. For instance, during periods of robust economic growth, industrial activity tends to increase, thereby driving up the demand for chemicals like naphthalene. Similarly, the development of new applications for naphthalene in sectors such as pharmaceuticals or electronics can create fresh demand, pushing prices higher. Conversely, during economic downturns, when industrial activity slows, demand for naphthalene may decrease, leading to a drop in prices.

Another factor that has a substantial impact on naphthalene prices is regulatory and environmental policies. In recent years, there has been a growing global focus on environmental sustainability, which has led to stricter regulations on the production and use of chemicals. Naphthalene, being a polycyclic aromatic hydrocarbon, is subject to stringent regulations in many countries due to its potential environmental and health risks. Compliance with these regulations often necessitates the adoption of cleaner and more expensive production methods, which in turn raises the cost of naphthalene. Furthermore, in regions where environmental regulations are more rigorous, there may be additional costs related to waste disposal and emissions control, further driving up the price of naphthalene.

In addition to environmental regulations, trade policies and tariffs can also influence naphthalene prices. Many countries impose tariffs on imported chemicals, including naphthalene, to protect domestic industries. Changes in trade policies, such as the imposition of new tariffs or the removal of existing ones, can have an immediate impact on naphthalene prices. For instance, if a major exporter of naphthalene faces higher tariffs in its target markets, it may raise its prices to offset the added costs, leading to a global price hike. On the other hand, if trade barriers are reduced, the increased competition in the market may drive prices down.

Supply chain disruptions can also cause significant price fluctuations in the naphthalene market. Natural disasters, geopolitical tensions, and logistical challenges can all affect the supply of raw materials needed to produce naphthalene, as well as the transportation of the finished product. For example, if a major supplier of coal tar or crude oil experiences a production shutdown, the reduced availability of raw materials can lead to a supply crunch, driving up naphthalene prices. Similarly, disruptions in transportation networks, such as port closures or shipping delays, can affect the timely delivery of naphthalene, creating temporary shortages and price spikes.

Moreover, competition among producers also affects naphthalene prices. The naphthalene market is highly competitive, with numerous manufacturers vying for market share. Companies that can produce naphthalene more efficiently or at a lower cost often gain a competitive edge, allowing them to offer more competitive prices. Technological advancements in production processes can also help reduce manufacturing costs, leading to lower prices for consumers. However, if a major producer exits the market or scales back production, it can reduce the overall supply of naphthalene, causing prices to rise.

Currency exchange rates are another factor that can influence naphthalene prices, especially in international trade. Since naphthalene is traded globally, fluctuations in exchange rates can affect the price of imported or exported naphthalene. For instance, if the currency of a major exporting country depreciates relative to the currencies of its trading partners, the price of naphthalene in international markets may decrease, making it more competitive. Conversely, if the currency strengthens, the price of naphthalene may rise, potentially reducing demand in price-sensitive markets.

Finally, market speculation and investor sentiment can also contribute to short-term price volatility in the naphthalene market. Just like other commodities, naphthalene prices can be influenced by speculators who buy and sell based on their expectations of future market trends. If investors believe that naphthalene prices will rise due to anticipated supply shortages or increased demand, they may buy in bulk, driving up prices in the short term. Conversely, if they expect prices to fall, they may sell off their holdings, causing a temporary dip in prices.

In conclusion, naphthalene prices are influenced by a complex interplay of factors, including raw material costs, energy prices, global demand, regulatory policies, trade dynamics, supply chain disruptions, competition, currency exchange rates, and market speculation. Understanding these factors is essential for businesses and consumers who rely on naphthalene, as it allows them to anticipate price changes and make informed purchasing decisions. By keeping an eye on these variables, stakeholders can better navigate the volatile naphthalene market and manage the financial impact of price fluctuations.

Get Real Time Prices for Naphthalene: https://www.chemanalyst.com/Pricing-data/naphthalene-1130

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Naphthalene#Naphthalene Price#Naphthalene Prices#Naphthalene Pricing#Naphthalene News#Naphthalene Price Monitor#Naphthalene Database#Naphthalene Price Chart

0 notes

Text

Pipe Coatings Market Beyond Boundaries: Global Reach and Market Penetration Strategies

The pipe coatings market plays a pivotal role in safeguarding pipelines across various industries, from oil and gas to water and wastewater. These coatings serve as a protective shield, preventing corrosion and enhancing the longevity of pipelines. This dynamic market has witnessed significant growth owing to the surge in infrastructure projects globally. This article delves into the key factors driving the pipe coatings market, emerging trends, and the major players shaping the industry.

Market Dynamics

The surge in global infrastructure development, particularly in emerging economies, has been a driving force behind the robust growth of the pipe coatings market. Rapid urbanization, coupled with the need for efficient transportation of liquids and gases, has escalated the demand for pipeline systems. This, in turn, has increased the requirement for high-quality coatings to ensure the longevity and reliability of these pipelines.

Furthermore, environmental regulations and the rising awareness of the adverse effects of corrosion have prompted industries to invest heavily in protective coatings. These coatings not only prevent corrosion but also reduce maintenance costs, making them an economically viable choice for pipeline operators.

Types of Pipe Coatings

The pipe coatings market encompasses a wide array of coating types tailored to specific applications. Fusion-bonded epoxy coatings, for instance, are renowned for their excellent corrosion resistance and durability. Similarly, polyurethane coatings offer exceptional abrasion resistance, making them ideal for pipelines subjected to harsh environments. Other types such as polyethylene, coal tar, and concrete coatings cater to diverse industrial requirements.

Technological Advancements

Recent technological advancements have revolutionized the pipe coatings industry. The introduction of nanotechnology in coating formulations has led to coatings with superior barrier properties, extending the lifespan of pipelines even further. Additionally, innovations in application techniques, such as robotic spray systems, have improved the efficiency and precision of coating processes.

Market Challenges

While the pipe coatings market shows immense promise, it is not without its challenges. The fluctuating prices of raw materials, particularly in the case of specialty coatings, pose a significant hurdle for manufacturers. Moreover, stringent environmental regulations and the need for eco-friendly coatings are pushing the industry towards sustainable alternatives, prompting manufacturers to invest in research and development.

Conclusion

The pipe coatings market stands as a critical component of the global infrastructure landscape. With the increasing demand for efficient transportation of fluids, the need for high-quality coatings to protect pipelines will continue to surge. As technology continues to advance, the industry is poised for further innovation and growth, ensuring pipelines remain reliable and durable for generations to come.

#Pipe Coatings Market Share#Pipe Coatings Market Growth#Pipe Coatings Market Demand#Pipe Coatings Market Trend#Pipe Coatings Market Analysis

0 notes

Text

Understanding The Market Forecast For Cosmetic Colorants

Cosmetic colorants play an important role in many cosmetic products. The cosmetic industry relies heavily on dyes and pigments to provide color for a wide range of cosmetic products. Dyes and pigments are the two main categories of colorants in cosmetics. In cosmetics, dyes are used to color products such as nail paints, hair color, lip products, foundations, blushes, mascaras, and eye makeup.

They are derived from chemically refined petroleum oil or coal-tar derivatives that contain heavy metals, such as zinc oxide and titanium dioxide. Chemical clarity is vital for facial makeup compositions that use cosmetic pigments. Regulatory requirements for personal care products are strict for leading cosmetic color manufacturers. Since foundations and compacts are becoming more popular, the cosmetic pigment market is expected to grow much faster.

According to market forecasts, the global market for cosmetic dyes is forecast to grow at an unexpected CAGR from 2023 to 2028. In addition, the cosmetic dye market size is projected to be USD 412.7 million by 2028, a 4.6% CAGR due to the COVID-19 pandemic, from USD 316 million in 2022. What's next? The global cosmetic colorants market will continue to grow constantly in the next five years.

If you are searching for meaningful information on the global cosmetic colorants market and its size, competitors' landscape, and trends, then you have come to the right place. In this blog, you will learn about the global market prediction for cosmetic colorants in 2023.

So, let's get into it!

The Uses Of Dyes and Pigments in Cosmetics

It depends on the end product's desired characteristics whether pigments or dyes are used in lip makeup formulations or other purposes. leading cosmetic color manufacturers use higher concentrations of dyes to create a matte look, while they use pigments to create a glossy look. As the face makeup industry requires a high volume of pearlescent pigments, product innovation in the pearlescent pigment sector is increasing. In addition, the cosmetic dyes market will witness growth during the forecast period due to the increasing demand for matte lipsticks.

Global Cosmetic Colorants Market Overview

As consumers become more aware of the use of personal care products in developing economies, the market is forecast to be driven by an increase in the demand for cosmetic products such as hair color, lip products, eye makeup, and others. The increasing young population and improved living standards as a result of industrialization & urbanization are forecast to increase the market growth in the coming years. Moreover, the latest trends in the fashion industry and the introduction of natural dyes will boost the market growth.

On the other hand, the market is facing some restraints and challenges which can stop its significant growth at a certain level. These market restraints include the high cost of natural dyes and the toxic and harmful effects of dyes used in cosmetics. Furthermore, cosmetic companies are highly recommended for buying cosmetic colorants from leading cosmetic dyes manufacturers in India which offers superior quality dyes at affordable prices.

Factors Driving The Growth of the Cosmetic Colorants Market

Rising awareness of cosmetic products and cosmetic product expenditures in emerging economic countries like India and China drive the cosmetic colorants market. In addition, the cosmetic colorants market will also prosper when Asian economies improve and strengthen in the next few years. Therefore, several factors have led to the current growth of the Asian cosmetic industry, including increased consumer purchasing power, an improved fashion consciousness, and industry participants spending readily on promotional activities.

Role of Pigments in Cosmetic Colorants Market Growth

Color additives are the most often dyes used in toiletries, while pigments are commonly used in color cosmetics. Synthetic colorants are found to be shiny and brighter and offer more vibrant colors with higher durability and improved PH value than natural ones. The use of pigments in the cosmetic industry has significantly improved in the past recent years. Due to this fact, pigments held the largest share of the cosmetic colorants market.

Moreover, eco-friendly products have increased industry responsibility to improve product ranges with an improved focus on R&D, with a greater focus on being more selective. It would ensure that colorants with superior quality and high performance would meet market expectations. Additionally, cosmetic color manufacturers will increase the emphasis on the use of cutting-edge technologies that could restrain the growth rate of the cosmetic colorants market.

Cosmetic Dyes Market Trends

Cosmetics industry growth and the increasing demand for personal care products drive the global cosmetic dyes market. There has been a strong surge in social media exposure and celebrity endorsements since the ever-growing social media platforms and celebrities influencing the marketing of cosmetics, personal care products, and grooming products. As a result, consumers are becoming increasingly conscious of their individual appearance and changing beauty standards.

In light of this, consumers have become more wealthy and changed their lifestyles, which is facilitating the growth of cosmetic products for skin and sun care. Furthermore, premier color manufacturers and exporters have introduced organic cosmetic dyes made from naturally sourced ingredients due to the increased prevalence of dermatological disorders.

In turn, this is providing an impetus to the growth of the market, since it protects the skin from harmful effects and allergies caused by chemical dyes. In addition, cosmetic dyes are extensively used in the production of various hair colors, which is another factor stimulating growth. Moreover, a changing climate is also expected to contribute to growth in the market, as will the introduction of innovative product variants with enhanced quality.

Global Cosmetic Dyes Market: Key Segmentation

There are many uses for cosmetic colorants, including make-up, skin care, hair care, fragrances, and personal hygiene. The products are generally colored using pigments. Several end-user industries produce a significant amount of colorants for use in cosmetics in the Asia Pacific region, which is mainly due to a large number of export-oriented manufacturing capacities and an intense domestic demand.

Increasing cosmetic manufacturers in that particular region are driving market growth. In addition to the growth of the cosmetic colorants market, the anticipated economic stability in Europe will help its manufacturing sector. And the US has a significant contribution to North America, which will remain the key region. Following are some of the leading companies in the cosmetic colorant market.

BASF SE

LANXESS

Hridhan Chem

Huntsman Corporation

Merck KGaA

Clariant

Moreover, you can find various types of cosmetic dyes available in the market, and they can also be categorized by application, geography, and type.

Cosmetic Dyes Market Based on Type

The market can be categorized into Natural Dyes and Synthetic Dyes based on Type. The increasing demand for cosmetics and personal care products is one of the factors contributing to this. And you can also find Natural dye holding the biggest market share.

Natural Dye

Synthetic Dye

Cosmetic Dyes Market Based on Application

You can categorize various products according to their application, including lip products, nail products, eye makeup, facial makeup, hair color products, toiletries, etc. A number of factors may be contributing to the increase in the popularity of hair color for covering gray hair, including the willingness of people to experiment with their hair color. During the forecasted period, a high CAGR is expected in the Hair Color Products segment.

Hair Color Products

Eye Makeup

Facial Makeup

Nail Products

Lip Products

Toiletries

Others

Cosmetic Dyes Market Based on Geography

According to regional analysis, the Global Cosmetic Dyes Market is segmented into North America, Europe, Asia Pacific, and the Rest of the World. Increasing demand for cosmetic dyes in various applications and changing trends will lead to Europe capturing the largest share of the market by 2023 for hair coloring in this region.

North America

Europe

Asia Pacific

Rest of the world

What’s Next?

You can also find a strong consumer market dominated by food and beverage producers, building and construction professionals, packaging, textiles, personal care products, pharmaceuticals, and other industries. Due to the steady demand for foods, the market for foods and beverages can achieve significant valuations. Moreover, the textile segment is expected to contribute to market growth, considering the high consumption rate of apparel.

Several industries reliant on colorants, such as construction, textiles, and paint, can command demand for these chemicals. Due to attractive packaging designs and consumer preferences for eco-friendly packaging, the packaging segment may also contribute to market growth. Hence, there are a number of factors that contribute to the global cosmetic colorants market growth in 2023 and beyond.

If you have any questions or need more information on the global cosmetic colorants market growth, please contact us.

0 notes

Text

Types of Graphite & Development in Graphite Mining

The demand for graphite will rise in tandem with the rise in demand for electric vehicles, computers, tablets, and cell phones. Find out more about it from graphite mining companies.

Many companies have jumped into the race to develop the next graphite mine in recent years. Improved batteries with increased storage capacity have become critical to global growth due to the rapid development of alternative energy sources for many applications. As a result, demand for lithium, cadmium, and graphite has increased; particularly for high purity, large-sized graphite flakes, which can command a significant premium in the current market.

Graphite is one of three types of elemental carbon, the others being coal and diamond. Because of its extreme softness and greasiness in its natural form, it has a black to steel grey colour and usually leaves a black streak on the hand when touched. Even the smallest particles are opaque.

Graphite Types

Graphite is one of the most thermodynamically stable allotropes of carbon. Graphite has been used by the top graphite mining companies in india because of these properties.

The graphite market includes detailed information on the sector's key players. Natural graphite and synthetic graphite are the two types of graphite. Other subcategories of natural graphite include flake graphite, amorphous graphite, and high crystalline graphite.

High Crystalline - Crystalline graphite has a purity of about 90% and ranges in size from 1 cm to 1 m in thickness. The crystalline graphite is derived from crude oil deposits that eventually turned into graphite. This is also known as vein graphite, lump graphite, or crystalline vein graphite, and it is currently only extracted in Sri Lanka. High crystalline graphite has a carbon content ranging from 90% to 99%. The viability of using this type of graphite in most industrial applications is limited due to its scarcity and high cost.

Amorphous- Despite being referred to as "amorphous," it is naturally crystalline. Of all the natural graphites, it contains very less amount of graphite.

Synthetic - Synthetic graphite is a manufactured product created by heating amorphous carbon materials to high temperatures. The primary feedstocks used in the production of synthetic graphite in the United States are calcined petroleum coke and coal tar pitch. As a result, it is up to ten times more expensive to produce than natural graphite, making it less appealing for use in most applications.

Flake: Flake is a common component of metamorphic rocks, ranging from 5% to 40%. Flake graphite can be found in a variety of locations.

The price of synthetic graphite is said to be volatile. Synthetic graphite electrodes were charged over 800% more. Its current high price is due to a scarcity of raw materials. Meteorologists use modern topographic survey tools to support environmentally sustainable mining. Furthermore, the Mine and Mineral Act establishes a simple, clear, and convenient method for allocating mining leases. Illegal mining carries a severe penalty, and any such actions are strongly condemned.

Conclusion

Abhinna Investment is now one of India's top graphite mining companies. So we concentrate on things like prospecting, mine design, and construction.

0 notes

Text

Coal Tar Market Size and Gross Margin Analysis to 2022 by Million Insights

27 Jun 2019 - Global Coal Tar Market is predicted to grow significantly in the forecast period owing to the increasing applications of coal tar in medical & industrial segment and sealing of roads. Coal tar is basically a thick liquid and a byproduct of the formation of coal gas and coke from coal. Coal tar is used in combination with ultraviolet light therapy. It is also used as medication on the skin to cure flaking, itching, and scaling due to disorders like seborrheic dermatitis or psoriasis. Medically, coal tar is a drug called ‘keratoplastics’ and works by shedding dead cells of the top layer and reduces the growing of the skin cells. This reduces scaling & dryness and reduces itching from the skin disorders.

The rising demand in the medical and industrial sector, and sealing of public roads are majorly driving the growth of coal tar market. Tar cannot be efficiently used in the extracted state since it is normally heated at high temperatures for the particular application. High cost of heating furnace is not affordable by the end users which hampers the growth of coal tar market. Nevertheless, increase in industrial applications like production of gasoline oil and diesel through in-power generation and high-pressure hydrogenation for heating boilers is predicted to boost worldwide demand for coal tar in future, thereby driving the coal tar market.

Request a Sample Copy of This Report @ https://www.millioninsights.com/industry-reports/coal-tar-market-outlook

The market is categorized on the basis of product, applications, end user and geography. On the basis of product, market is divided into high temperature coal tar, medium temperature coal tar, and low temperature coal tar. Based on application, market is split into pitch, pine tar, birch tar, carbon black, wash oil and others. On the basis of end user, market is divided into pavement sealcoats, medical industries and other sectors. Geographically, market is segmented as North America, Europe, Asia Pacific, and RoW (Rest of the World). North America, especially Canada is predicted to hold larger market for coal tar market due to extensive industrial use.

The key players in coal tar market include Baowu Steel Group, OCI, Baoshun, JFE Chemical, Koppers, Himadri Chemicals & Industries, Huanghua Xinnuo Lixing, POSCO, Rain Industries Limited, Sunlight Coking, Nippon Steel & Sumitomo Metal, and Shanxi Coal and Chemical.

Market Segment:

Key Applications

• Chemical Processing

• Carbon Black

Key Regions

• North America

• Europe

• Asia Pacific

• Middle East and Africa

• South America

Key Vendors

• AM

• Erdemir

• EVRAZ

• Metinvest

• MMK

• NLMK

• SEVERSTAL

• request free sample to get a complete list of companies

View Full Report with TOC @ https://www.millioninsights.com/industry-reports/coal-tar-market-outlook/request-sample

#Coal Tar Market Report#Coal Tar Market Demand#Coal Tar Market Share#Coal Tar Market growth#Coal Tar Market Forecast

0 notes

Text

Top seven tips commonest industrial Roofing Types

What’s the weather like today? If you'll tell it’s hot and sunny (or raining!) simply by sitting within your windowless office, it's going to be time to seem at the well-being of your commercial roofing system.

When looking the marketplace for a replacement roof, the foremost necessary factor to stay in mind is that the overall health of the building. Factors just like the longevity of the roof, typical weather variations and energy potency are critical.

Each commercial roof kind has its professionals and cons, and creating a choice is harder than ever before because of the variety of choices available.