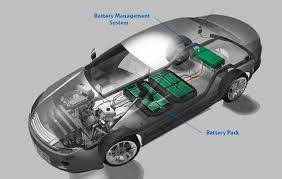

#Battery Management System Market Share Battery Management System Market Growth Battery Management System Market Demand Battery Management Sy

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr is available in 18 languages.

Text

Automotive Battery Management System Market Set for Explosive Growth

Market Research Forecast released a new market study on Global Automotive Battery Management System Market Research report which presents a complete assessment of the Market and contains a future trend, current growth factors, attentive opinions, facts, and industry validated market data. The research study provides estimates for Global Automotive Battery Management System Forecast till 2032. The Automotive Battery Management System Marketsize was valued at USD 8.25 USD Billion in 2023 and is projected to reach USD 23.56 USD Billion by 2032, exhibiting a CAGR of 16.17 % during the forecast period. Key Players included in the Research Coverage of Automotive Battery Management System Market are: Robert Bosch GmbH (Germany), Continental AG (Germany), Toshiba Corporation (Japan), Intel Corporation (U.S.), NXP Semiconductors NV (Netherlands), Analog Devices, Inc. (U.S.), Denso Corporation (Japan), Johnson Matthey, Inc. (U.K.), LG Chem, Ltd. (South Korea), Midtronics, Inc. (U.S.) What's Trending in Market: Rising Adoption of Automation in Manufacturing to Drive Market Growth Market Growth Drivers: Increasing Demand for Forged Products in Power, Agriculture, Aerospace, and Defense to Drive Industry Expansion The Global Automotive Battery Management System Market segments and Market Data Break Down Propulsion Type: BEV, PHEV, and HEV","Vehicle Type: Passenger Cars and Commercial Vehicles GET FREE SAMPLE PDF ON Automotive Battery Management System MARKET To comprehend Global Automotive Battery Management System market dynamics in the world mainly, the worldwide Automotive Battery Management System market is analyzed across major global regions. MR Forecast also provides customized specific regional and country-level reports for the following areas.

• North America: United States, Canada, and Mexico. • South & Central America: Argentina, Chile, Colombia and Brazil. • Middle East & Africa: Saudi Arabia, United Arab Emirates, Israel, Turkey, Egypt and South Africa. • Europe: United Kingdom, France, Italy, Germany, Spain, Belgium, Netherlands and Russia. • Asia-Pacific: India, China, Japan, South Korea, Indonesia, Malaysia, Singapore, and Australia.

Extracts from Table of Contents Automotive Battery Management System Market Research Report Chapter 1 Automotive Battery Management System Market Overview Chapter 2 Global Economic Impact on Industry Chapter 3 Global Market Competition by Manufacturers Chapter 4 Global Revenue (Value, Volume*) by Region Chapter 5 Global Supplies (Production), Consumption, Export, Import by Regions Chapter 6 Global Revenue (Value, Volume*), Price* Trend by Type Chapter 7 Global Market Analysis by Application ………………….continued More Reports:

https://marketresearchforecast.com/reports/automotive-usage-based-insurance-market-2982 For More Information Please Connect MR ForecastContact US: Craig Francis (PR & Marketing Manager) Market Research Forecast Unit No. 429, Parsonage Road Edison, NJ New Jersey USA – 08837 Phone: (+1 201 565 3262, +44 161 818 8166)[email protected]

#Global Automotive Battery Management System Market#Automotive Battery Management System Market Demand#Automotive Battery Management System Market Trends#Automotive Battery Management System Market Analysis#Automotive Battery Management System Market Growth#Automotive Battery Management System Market Share#Automotive Battery Management System Market Forecast#Automotive Battery Management System Market Challenges

0 notes

Text

Battery Management System (BMS) Market: Optimizing Performance and Safety in Energy Storage

The Battery Management System (BMS) market refers to the market for electronic systems that monitor and control the charging, discharging, and overall management of rechargeable batteries. BMS plays a crucial role in ensuring the safety, reliability, and optimal performance of batteries used in various applications, including electric vehicles (EVs), renewable energy storage systems, consumer electronics, and industrial applications.

The increasing demand for battery-powered devices and the growing adoption of electric vehicles are key factors driving the growth of the Battery Management System market. With the transition towards cleaner energy sources and the need to reduce greenhouse gas emissions, there has been a significant surge in the production and deployment of EVs and renewable energy storage systems, which rely on efficient battery management. Additionally, the increasing use of portable consumer electronics, such as smartphones, laptops, and tablets, has further fueled the demand for BMS solutions.

Battery Management System (BMS) Market: Key Components

Battery Control Unit (BCU): The BCU is the core component of the BMS that performs functions such as cell balancing, monitoring battery voltage, current, and temperature, and controlling charging and discharging processes.

Battery Monitoring Unit (BMU): The BMU is responsible for monitoring the state of individual battery cells, including their voltage, temperature, and state of charge (SoC). It provides real-time data to the BMS for decision-making and ensures the overall health of the battery pack.

Battery Charger: The BMS includes a battery charger that regulates the charging process, ensuring the battery is charged safely and efficiently. It controls the charging current, voltage, and charging profile based on the battery's specifications.

Human-Machine Interface (HMI): The HMI allows users to interact with the BMS, providing information on battery status, diagnostics, and alerts. It can be in the form of a display, touch screen, or software interface.

Communication Interface: BMS systems often incorporate communication interfaces such as CAN (Controller Area Network) or LIN (Local Interconnect Network) to enable data exchange between the BMS and other vehicle or system components.

Battery Management System (BMS) Market: Application Areas

Electric Vehicles (EVs): BMS plays a critical role in managing the performance, range, and longevity of batteries in electric vehicles. It ensures optimal charging, discharging, and thermal management, as well as protection against overcharging, over-discharging, and overheating.

Renewable Energy Storage Systems: BMS solutions are used in energy storage systems, such as those based on lithium-ion batteries, to manage the charging and discharging processes, optimize energy efficiency, and prolong battery life.

Consumer Electronics: BMS is employed in portable electronic devices, including smartphones, laptops, and tablets, to monitor and control the battery's performance, safety, and charging process.

Industrial Applications: BMS finds applications in various industrial sectors, such as telecommunications, UPS (Uninterruptible Power Supply) systems, and grid energy storage, where batteries are used for backup power and load balancing purposes.

Battery Management System (BMS) Market: Regional Outlook

The Battery Management System market is geographically diversified, with major regions including North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific dominates the market due to the presence of major EV manufacturers and increasing investments in renewable energy projects. North America and Europe also hold significant market shares, driven by the growing adoption of EVs and supportive government initiatives promoting clean energy solutions.

Battery Management System (BMS) Market: Key Players

Some of the key players operating in the Battery Management System market include:

Nuvation Engineering Johnson Matthey Battery Systems Lithium Balance A/S Navitas Systems LLC Valence Technology Inc. AVL List GmbH Texas Instruments Inc. Renesas Electronics Corporation Eberspächer Group LG Chem Ltd.

These companies focus on product innovation, strategic partnerships, and mergers and acquisitions to strengthen their market position and offer advanced BMS solutions to their customers.

Battery Management System (BMS) Market: Future Outlook

The Battery Management System market is expected to witness significant growth in the coming years. The increasing demand for electric vehicles, the expansion of renewable energy installations, and the rising need for efficient energy storage solutions will continue to drive the adoption of BMS. Technological advancements, such as the integration of artificial intelligence and machine learning algorithms in BMS, will further enhance the capabilities and performance of battery management systems, enabling safer and more efficient battery usage.

0 notes

Text

Battery Management System Market Set to Reach US$28.4 Bn by 2029: Accelerated Growth Expected

The global battery management system (BMS) market has been experiencing significant growth and is expected to continue its upward trajectory. Valued at US$4.6 billion in 2019, the BMS market is projected to reach a staggering US$28.4 billion by 2029, with a robust compound annual growth rate CAGR of 19.8% during the forecast period.

For More Industry Insights Read: https://www.fairfieldmarketresearch.com/report/battery-management-system-market

The accelerating adoption of electric vehicles (EVs) and hybrid electric vehicles (HEVs) is a major catalyst behind the surge in the battery management system market. As the world embraces sustainable and eco-friendly transportation solutions, the demand for efficient energy storage and battery management systems has skyrocketed. Lithium-ion batteries, renowned for their high energy and current densities, have become the go-to choice for EVs. However, ensuring the safe and optimal operation of these batteries is crucial. Battery management systems play a pivotal role in monitoring and controlling the charging and discharging processes, maximizing energy utilization while mitigating the risk of battery damage.

The battery management system market caters to a wide range of industries and applications, including energy storage, automotive, consumer electronics, healthcare, telecommunication, renewable energy, and military and defense sectors. Among these, the automotive industry is expected to retain its dominance in the battery management systems segment throughout the forecast period. The growing demand for electric and hybrid vehicles drives the need for advanced battery systems. Additionally, the communication and power generation sectors rely heavily on battery management systems for backup power solutions, such as uninterruptible power supplies (UPSs) and generators. Moreover, the deployment of high-voltage battery packs in stationary energy storage systems for electric vehicles further propels the market growth.

North America currently leads the global battery management system market, holding the largest market share. The region is home to several prominent players, including industry giants and emerging startups. The battery management system market in North America has been strongly influenced by the rapid adoption of EVs, HEVs, and favorable government initiatives. Government support and incentives for the development of hybrid and electric vehicles have significantly contributed to the market growth in this region. It is anticipated that North America will maintain its dominance throughout the forecast period.

Asia Pacific is poised to witness the highest growth rate in the battery management system market between 2022 and 2029. Countries such as China and India are experiencing a rapid shift towards electric vehicles and renewable energy solutions to address environmental concerns. Government initiatives and incentives promoting the adoption of EVs and HEVs have created substantial market opportunities for battery management systems in the region. The consumer electronics, telecom, and automotive industries in Asia Pacific also contribute significantly to the market growth.

Key players in the global battery management system market are actively pursuing strategies to strengthen their market presence. These strategies include new product launches, product upgrades, partnerships, agreements, business expansions, and mergers and acquisitions. Companies such as Analog Devices, Eberspächer, Elithion Inc, Johnson Matthey, Leclanché SA, Marelli Holdings Co., Ltd, Navitas System, LLC, Nidec Motor Corporation, Nuvation Energy, Panasonic Industry Co., Ltd, Sedemac, and Texas Instruments are at the forefront of driving innovation and advancements in battery management systems.

For More Information Visit: https://www.fairfieldmarketresearch.com/

#battery management system market#battery management system#battery management system market size#battery management system market share#battery management system market trends#battery management system market demand#battery management system market growth#battery management system market analysis#battery management system(BMS)#battery market#fairfield market research

0 notes

Text

Battery Energy Storage System Market drivers include growing renewable energy integration and smart grid modernization efforts

The Battery Energy Storage System (BESS) market is experiencing remarkable growth, driven by the increasing integration of renewable energy sources and the ongoing modernization of smart grid infrastructure. As global economies intensify their shift toward cleaner energy, BESS technology has emerged as a vital component in ensuring the reliability, flexibility, and sustainability of power systems. The convergence of renewable energy integration with smart grid modernization efforts is reshaping how energy is stored, distributed, and consumed, creating a robust foundation for market expansion.

Renewable Energy Integration as a Primary Market Driver

One of the most influential drivers of the BESS market is the widespread adoption of renewable energy technologies such as solar and wind power. These sources are inherently intermittent, generating power based on weather conditions rather than demand. Battery energy storage systems play a critical role in addressing this challenge by storing excess energy when generation is high and releasing it during periods of low production or peak demand.

Countries around the world are setting ambitious renewable energy targets to meet climate goals and reduce reliance on fossil fuels. According to the International Energy Agency (IEA), renewables accounted for nearly 30% of global electricity generation in 2023, and this share is expected to grow significantly in the coming decade. To manage the variability of these sources, robust energy storage solutions like lithium-ion, flow, and solid-state batteries are being increasingly deployed across utility, commercial, and residential sectors.

The synergy between solar power and battery storage is especially noteworthy. Solar photovoltaic (PV) installations are rising rapidly, and pairing them with BESS allows for better self-consumption, grid independence, and financial savings. In regions with high solar penetration, such as California and parts of Europe, battery storage is essential for grid stability and load balancing.

Smart Grid Modernization Boosting Demand

Another crucial factor propelling the BESS market is the transformation of traditional electrical grids into smart grids. Smart grids leverage advanced digital communication technologies to enhance the efficiency, reliability, and sustainability of electricity distribution. Battery energy storage systems are central to this transformation, offering grid operators enhanced control over supply and demand.

Smart grid modernization includes the deployment of advanced metering infrastructure, real-time monitoring systems, demand response capabilities, and decentralized energy resources. BESS units support these functions by enabling frequency regulation, voltage control, and peak shaving, thus improving overall grid resilience. Moreover, as electric vehicles (EVs) become more prevalent, the need for grid-responsive charging infrastructure is growing, further emphasizing the importance of scalable energy storage solutions.

Governments and utilities are investing heavily in smart grid projects to accommodate changing consumption patterns and integrate distributed energy resources. In the U.S., for example, the Department of Energy continues to fund programs aimed at enhancing grid flexibility and reliability through BESS implementation. Similarly, the European Union’s Green Deal and Digital Strategy encourage the use of smart technologies and energy storage to achieve carbon neutrality by 2050.

Technological Advancements and Cost Reductions

Technological progress and declining battery costs are making BESS more accessible and economically viable. Innovations in battery chemistry, such as the transition from conventional lithium-ion to lithium iron phosphate (LFP) and solid-state batteries, are improving energy density, safety, and lifecycle performance. These advancements contribute to reducing the total cost of ownership and expanding use cases across sectors.

Manufacturing scale-up and supply chain efficiencies are also playing a role in lowering prices. According to BloombergNEF, the cost of lithium-ion batteries has dropped by more than 80% over the past decade, a trend that is expected to continue with further industrial optimization. This price decline is crucial in encouraging widespread deployment, especially in emerging markets where capital costs have been a traditional barrier.

Policy Support and Regulatory Incentives

The regulatory landscape is increasingly favorable for battery storage projects. Governments worldwide are enacting policies that support renewable energy integration and incentivize energy storage deployment. These include tax credits, subsidies, grants, and favorable tariff structures. In the U.S., the Inflation Reduction Act provides significant tax incentives for standalone storage systems, while countries like China and India are incorporating storage into their national energy policies.

Clear regulatory frameworks and supportive market mechanisms are essential to attract investment and accelerate project development. Grid operators are also updating interconnection standards and grid codes to accommodate the influx of battery storage assets, fostering a more inclusive and dynamic energy ecosystem.

Conclusion

The Battery Energy Storage System market is on a strong growth trajectory, fueled by the dual forces of increasing renewable energy integration and the evolution of smart grid modernization efforts. As the world continues its transition toward sustainable energy, BESS will remain a cornerstone technology for enhancing grid stability, enabling clean energy adoption, and meeting future electricity demand. With technological innovations, supportive policies, and growing environmental awareness, the BESS market is poised to play an integral role in shaping the future of global energy infrastructure.

0 notes

Text

Data-Driven Decisions: An In-Depth Market Analysis of Residential Solar PV Inverter Market

Introduction

The global energy landscape is undergoing a transformative shift towards sustainability, and solar power has emerged as one of the most promising solutions. Within this domain, residential solar photovoltaic (PV) systems are increasingly being adopted by households aiming to reduce electricity bills and minimize their carbon footprint. At the heart of these systems lies the solar PV inverter, a critical component that converts direct current (DC) generated by solar panels into alternating current (AC) usable by home appliances.

The residential solar PV inverter market is witnessing robust growth due to favorable government policies, declining technology costs, and rising consumer awareness. This article explores the key trends, market dynamics, technological developments, and future outlook of the residential solar PV inverter industry through 2032.

Market Overview

The global residential solar PV inverter market was valued at approximately USD 4.3 billion in 2022, and it is projected to reach USD 9.8 billion by 2032, growing at a CAGR of 8.5% over the forecast period. The market growth is being fueled by a combination of energy decentralization, net metering incentives, and advancements in inverter technologies.

Leading markets include North America, Europe, and Asia-Pacific, with countries such as the U.S., Germany, China, and Australia at the forefront of adoption.

Download a Free Sample Report:-https://tinyurl.com/32ws2khd

Market Dynamics

Key Growth Drivers

Government Incentives and Renewable Policies Policies like feed-in tariffs, investment tax credits (ITCs), and subsidies for residential solar installations have significantly boosted demand. For instance, the U.S. federal solar ITC, extended through 2032, allows homeowners to deduct a portion of their installation costs.

Declining Cost of Solar Systems The cost of residential solar PV systems has dropped significantly over the past decade. Inverters, once a significant cost component, are now becoming more affordable, facilitating broader adoption.

Rising Electricity Costs Homeowners in regions with high utility rates are increasingly turning to solar as a cost-saving alternative, pushing demand for inverters that improve energy conversion efficiency and grid compatibility.

Advancements in Inverter Technology Modern inverters are no longer just DC-to-AC converters. They offer smart grid interaction, monitoring capabilities, energy storage integration, and even load management functionalities.

Growing Environmental Awareness With climate change concerns becoming more urgent, consumers are looking for ways to reduce their carbon emissions. Solar PV systems align perfectly with these values.

Market Segmentation

By Type

String Inverters

Microinverters

Central Inverters (used in hybrid home systems)

Microinverters are gaining popularity in residential installations due to their flexibility, shading tolerance, and module-level monitoring capabilities. However, string inverters remain the most widely used due to their cost-efficiency in typical residential settings.

By Phase

Single-Phase

Three-Phase

Single-phase inverters dominate the residential sector, especially in urban and suburban environments. However, three-phase inverters are used in larger residential buildings or luxury homes with higher load demands.

By Connectivity

Standalone

On-grid

Hybrid (grid + battery)

On-grid inverters are the most common, but hybrid inverters are rapidly gaining market share with the increasing adoption of residential energy storage systems like the Tesla Powerwall and LG Chem RESU.

By Power Rating

Less than 3 kW

3–10 kW

More than 10 kW

The 3–10 kW category holds the largest share, catering to typical residential energy consumption levels.

Regional Insights

North America

The U.S. remains a dominant force due to its strong policy support and early adopter consumer base. States like California, Texas, and Florida lead installations. Net metering and smart inverter mandates further accelerate market growth.

Europe

Germany, Italy, and Spain are the front-runners. The European Union’s “Fit for 55” package and other decarbonization initiatives are driving growth.

Asia-Pacific

China, Australia, Japan, and India present tremendous growth potential due to high solar irradiance, population density, and proactive solar policies. Australia, for example, has one of the highest rooftop solar penetration rates globally.

Middle East & Africa

Growing urbanization and grid unreliability in parts of Africa, along with increasing solar investments in the Middle East, are fostering interest in residential solar inverters.

Industry Trends

Integration with Battery Storage As the demand for energy independence grows, hybrid inverters that support battery storage are becoming standard in new installations.

Smart and Connected Inverters Inverters now offer Wi-Fi or Bluetooth connectivity, allowing users to monitor performance via mobile apps, receive fault alerts, and integrate with smart home systems.

AI and Machine Learning Integration Predictive maintenance, performance optimization, and automated grid interaction are being enhanced by AI capabilities in next-generation inverters.

Modular and Scalable Solutions Inverter manufacturers are designing systems that allow homeowners to scale their solar installations and energy storage as their needs grow.

Cybersecurity in Solar Networks With inverters increasingly connected to home networks and utility grids, cybersecurity has become a focal point for both manufacturers and regulators.

Challenges

High Initial Costs in Emerging Markets Despite declining costs, initial investments remain a barrier, especially in price-sensitive markets without strong government incentives.

Intermittency and Grid Integration Issues High penetration of residential solar can lead to grid instability. Smart inverters with grid-support functionalities are helping mitigate this, but standards and infrastructure must evolve.

Product Lifespan and Maintenance Inverters generally have shorter lifespans (10–15 years) than solar panels, leading to higher long-term maintenance and replacement costs.

Lack of Awareness in Certain Regions In developing countries, limited awareness and access to technical expertise can slow adoption.

Competitive Landscape

The residential solar PV inverter market features both global giants and regional specialists. Key players include:

SMA Solar Technology AG

Huawei Technologies Co., Ltd.

Sungrow Power Supply Co., Ltd.

Enphase Energy

SolarEdge Technologies

Fronius International GmbH

ABB Ltd.

Delta Electronics

Growatt New Energy

These companies compete on the basis of efficiency, features, customer support, and price. Many are also expanding into energy storage and smart home integration to provide end-to-end solutions.

Market Outlook to 2032

The residential solar PV inverter market is expected to flourish over the next decade, driven by:

Mass adoption of smart homes and home energy management systems

Decentralized energy production and prosumer models

Increased pairing with residential storage for off-grid capability

Emergence of vehicle-to-home (V2H) systems using electric vehicles as batteries

Policy support and technological innovation will continue to play pivotal roles in shaping the market trajectory.

Conclusion

The residential solar PV inverter market is poised for dynamic growth as households across the globe embrace clean energy solutions. Inverters are not only becoming more efficient and affordable but also more intelligent, connecting seamlessly with other smart devices and the energy grid.

With climate change at the forefront of global discourse and energy independence gaining value, the adoption of residential solar—powered by sophisticated inverters—will play a vital role in the sustainable transformation of our energy ecosystem.Read Full Report:-https://www.uniprismmarketresearch.com/verticals/energy-power/residential-solar-pv-inverter

0 notes

Text

Investing in Connection: Opportunities in the Automotive Relay Market

Automotive Relay Market Growth & Trends

The global Automotive Relay Market size is expected to reach USD 24.97 billion by 2030, registering a CAGR of 8.1% during the forecast period, according to a new report by Grand View Research, Inc. Increasing vehicular safety regulations in various regions across the globe is driving the automotive relay market. Further, increasing adoption of electric vehicles amongst passenger car segment end users has made automotive electronics including the automotive relay industry to gain significant market share.

Systems such as advanced driver assistance systems (ADAS), electronic stability control, electronic steering systems, brake-by-wire systems, and airbags are gaining momentum across the globe, owing to their safety and comfort benefits. Strict safety guidelines employ substantial pressure on Tier-1 suppliers and the OEMs to design improved safety systems for automobiles. Furthermore, there is a growing demand for enhanced comfort and convenience in automobiles.

Many governments provide lucrative offers to promote the selling and usage of Electric Vehicles EVs. Tax benefits are provided at the time of purchase. However, the extent of the exemption depends on the size of the batteries used in the vehicle. In the United States, insurance companies provide discounts on insurance policies to customers, and utility companies are offering low electricity rates. Also, few states offer credits to electric vehicle manufacturers and buyers for their costs and purchase of charging equipment. Many European countries follow incentive-based programs for promoting EVs. Countries, like Germany and Austria, offer tax exemptions and reductions.

Curious about the Automotive Relay Market? Download your FREE sample copy now and get a sneak peek into the latest insights and trends.

Automotive Relay Market Report Highlights

The increasing vehicular safety norms across the globe and the growing adoption of electric passenger car vehicles amongst end-users are expected to drive the market.

Electric automotive parts have diversified over the past decade, leading to an increase in the number of relays used as switching devices as well as variation in the required features of each relay

Asia Pacific is a key revenue-generating region and captured a significant market share in 2022. The region exhibits a high growth potential, which may be attributed to high vehicle demand in this region.

Automotive Relay Market Segmentation

Grand View Research has segmented the global automotive relay market based on product, vehicle type, application, and region:

Automotive Relay Product Outlook (Revenue, USD Million, 2017 - 2030)

PCB Relay

Plug-in Relay

High Voltage Relay

Others

Automotive Relay Vehicle Type Outlook (Revenue, USD Million, 2017 - 2030)

Passenger Vehicles

Commercial Vehicles

Electric Vehicles

Automotive Relay Application Outlook (Revenue, USD Million, 2017 - 2030)

Resistive Loads

HVAC

Capacitive Loads

Engine Management Module

Fog Lights

ABS Module

Front and Rear Beam

Inductive Loads

Power Window

Central Lock

Cooling Fan

Clutches

Automotive Relay Regional Outlook (Revenue, USD Million, 2017 - 2030)

North America

U.S.

Canada

Europe

UK

Germany

France

Asia Pacific

China

Japan

India

Australia

South Korea

Latin America

Brazil

Mexico

Middle East and Africa

United Arab Emirates (UAE)

Saudi Arabia

South Africa

Download your FREE sample PDF copy of the Automotive Relay Market today and explore key data and trends.

0 notes

Text

Waaree Energies shares surge 8% after Q4 profit jumps 34%, revenue up 36% on year

Shares of Waaree Energies surged over 8 percent on April 23 after the company reported a 34 percent jump in net profit to Rs 618.91 crore for the fourth quarter of the fiscal.

The shares of the company were trading at the highest level in nearly three months.

Waaree released its Q4FY25 results during the post-market hours of April 22, reporting a revenue from operation of Rs 4,003.93 crore, a rise of nearly 36 percent from a year ago. The company’s EBITDA meanwhile jumped over 116 percent YoY to Rs 1,060 crore during the reported quarter.

For the ongoing financial year, Waaree Energies has shared an EBITDA guidance in the rage of Rs 5,500–6,000 crore, and said that it is projecting ‘robust year on year growth in EBITDA on the back of strong demand realization and operational excellence’.

Speaking on the EBITDA outlook for FY26, Waaree Energies CEO and Whole Time Director Amit Paithankar said the quality of the company’s order book and execution capabilities will enable it to achieve the target.

“FY25 marks a pivotal inflection point in Waaree’s journey- a year where our strategy, scale, and execution converged to deliver industry-leading EBITDA performance of Rs. 3,123.20 crore. This performance underscores the strength of our execution capabilities and the quality of order book, with centred focus on margins. We see encouraging demand trends, which bodes well for future growth. Waaree is focused on both backward and forward integration, reflected in our expansion and investment plans including cell, ingot and wafer manufacturing, battery energy storage system, power infrastructure and inverters,” he added.

The CEO also informed that Waaree’s 1.6 GW module manufacturing facility is now operational in Texas, US. “This reinforces our commitment to the American market and underlines our local-for-local manufacturing philosophy. Our strategy of local manufacturing and supply chain management will help us navigate through the changing policy environment,” he added.

Intensify Research Services is a professional stock consultive firm in Indore in share market latest news. We provide expert investment advice and guidance to individuals and High Net-Worth Individuals (HNIs), valuable trading tips and strategy Visit us at Intensify Research Services to learn more.

#sharetrading#sharemarketing#stock market#stocks#shareinvestor#sharemarket#investment#stockinvestment#share this post#sharetrader

0 notes

Text

North America Industrial Air Filter Market Emerging Technologies, and Growth by Forecast (2021-2028)

The North America industrial air filter market is expected to reach US$ 3,459.78 million by 2028 from US$ 2,105.20 million in 2021. The market is estimated to grow at a CAGR of 7.4% from 2021 to 2028.

North America Industrial Air Filter Market Introduction

The industrial air filter market in North America is on a growth trajectory, largely propelled by the increasing levels of air pollution across the continent. This rise in pollution has necessitated the implementation of various clean air regulations by governing bodies, compelling numerous sectors to integrate air purification units into their systems, which is a primary driver of market expansion. Furthermore, the ongoing global increase in industrialization, particularly within sectors like cement, metal processing, pharmaceuticals, and chemicals, also significantly contributes to market growth. The heightened awareness of environmental issues is also leading to improved monitoring and management of pollutants, thereby supporting business growth in this industry. However, the substantial initial capital investment required for the manufacturing and installation of these components can pose a challenge to new entrants and limit overall sector competitiveness. Additionally, the longer operational life of air filter systems results in a slower replacement cycle, which can moderate market growth. On the other hand, technological advancements are yielding more effective and efficient air filtration solutions.

Download our Sample PDF Report

@ https://www.businessmarketinsights.com/sample/TIPRE00029267

North America Industrial Air Filter Strategic Insights

Strategic insights into the North America Industrial Air Filter market provide a data-rich examination of the industry's dynamics, encompassing current trends, key market players, and region-specific attributes. These insights offer actionable recommendations, enabling readers to gain a competitive edge by identifying untapped market niches or developing differentiated value propositions. By leveraging the power of data analytics, this intelligence assists industry participants, including investors and manufacturers, in anticipating market shifts. A forward-looking perspective is paramount, aiding stakeholders in foreseeing market changes and strategically positioning themselves for sustained success within this evolving region.

North America Industrial Air Filter Regional Insights

The geographic scope of the North America Industrial Air Filter market refers to the specific territories in which businesses operate and compete. A detailed understanding of local nuances, such as varying consumer preferences (for instance, the demand for specific plug types or battery backup durations), diverse economic conditions, and differing regulatory frameworks, is essential for formulating tailored market strategies. Businesses can expand their market presence by identifying underserved regions or adapting their product offerings to meet local needs.

North America Industrial Air Filter Market segmentation

The North America industrial air filter market is segmented into product, application, and country. The North America industrial air filter market has been categorized by the products as dust filters, mist filters, baghouse filters, cartridge collectors and filters, HEPA filters, wet scrubbers, and dry scrubbers. HEPA filters segment accounted for the largest market share in 2020. Based on application the North America industrial air filter market has been categorised as cements, food & beverages, metals, power generation, pharmaceuticals, chemical, oil & gas, and others. In 2020 the power generation segment accounted for highest share of application. Based on country, the North America industrial air filter market is segmented into the US, Canada, Mexico. The US held the largest market share in 2020.

Honeywell International, Inc.; Mann + Hummel GmbH; Nordic Air Filtration; Donaldson Company, Inc; General Filter Italia; Camfil Ab; Paul Corporation; Filtration Group Industrial; Sentry Air Systems, Inc.; And Air Filters, Inc. are among the key companies operating in the North America industrial air filter market.

About Us:

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications

#North America Industrial Air Filter Market#North America Industrial Air Filter Market Emerging Technologies#North America Industrial Air Filter Market Growth by Forecast

0 notes

Text

Power Integrated Module Market: Trends, Growth, and Future Opportunities

The Power Integrated Module (PIM) market is experiencing rapid expansion, driven by advancements in power electronics, the rise of electric vehicles (EVs), and the global push for energy efficiency. These compact modules, which integrate multiple power semiconductor devices like transistors, diodes, and passive components, are essential for optimizing power conversion in industries ranging from automotive to renewable energy. This article explores the current landscape, key trends, challenges, and future prospects of the Power Integrated Module market.

Market Overview and Growth Projections

The global Power Integrated Module market was valued at USD 2.03 billion in 2024 and is projected to grow at a CAGR of 8.61%, reaching USD 4.88 billion by 203425. This growth is fueled by:

Rising demand for energy-efficient solutions in industrial automation, consumer electronics, and EVs.

Government regulations promoting renewable energy and carbon emission reductions.

Technological advancements in semiconductor materials like Silicon Carbide (SiC) and Gallium Nitride (GaN), which enhance power density and thermal performance14.

Asia-Pacific dominates the market, accounting for the largest share due to strong manufacturing bases in China, Japan, and South Korea, along with increasing EV adoption511.

Key Drivers of the Power Integrated Module Market

1. Electrification of Automotive Industry

The shift from internal combustion engines to electric and hybrid vehicles is a major growth catalyst for the Power Integrated Module market. PIMs are critical in EVs for managing battery systems, motor control, and charging infrastructure. The global EV market is expected to grow at a 23.2% CAGR, further propelling demand for high-efficiency PIMs7.

2. Expansion of Renewable Energy Systems

Solar and wind power systems rely on PIMs for efficient energy conversion and grid integration. With governments worldwide investing in clean energy, the demand for Power Integrated Modules in inverters and energy storage solutions is surging46.

3. Miniaturization and High Power Density

The trend toward smaller, more efficient electronic devices is pushing manufacturers to develop compact PIMs with higher power density. Innovations in packaging technologies, such as 3D integration and embedded cooling, are enabling more efficient thermal management in power modules10.

Challenges in the Power Integrated Module Market

Despite strong growth, the market faces several hurdles:

High Manufacturing Costs: Advanced materials like SiC and GaN increase production expenses, limiting adoption in price-sensitive markets7.

Thermal Management Issues: High-power applications generate significant heat, requiring sophisticated cooling solutions to maintain reliability1.

Supply Chain Constraints: Shortages of raw materials like lithium and cobalt impact production timelines7.

Emerging Trends and Future Opportunities

1. AI and Smart Power Management

Artificial Intelligence is being integrated into Power Integrated Modules to optimize energy consumption in real time, particularly in EVs and industrial automation7.

2. Wide Bandgap Semiconductors (SiC & GaN)

These materials offer superior efficiency and faster switching speeds compared to traditional silicon, making them ideal for next-gen PIMs in high-power applications411.

3. Sustainable and Recyclable Modules

With increasing environmental regulations, manufacturers are focusing on eco-friendly PIM designs that reduce electronic waste10.

Conclusion

The Power Integrated Module market is poised for significant growth, driven by electrification, renewable energy adoption, and technological advancements. While challenges like high costs and thermal management persist, innovations in AI, wide-bandgap semiconductors, and sustainable designs present lucrative opportunities. As industries continue to prioritize energy efficiency, the demand for advanced PIMs will only accelerate, shaping the future of power electronics.

By staying ahead of these trends, businesses can capitalize on the expanding Power Integrated Module market and contribute to a more energy-efficient world.

1 note

·

View note

Text

Charging Ahead: The Business of Battery Cooling Plates in the EV Era

The global battery cooling plate market size is expected to reach USD 5.01 billion by 2030, growing at a CAGR of 37.4% from 2023 to 2030, according to a new report by Grand View Research, Inc. The increasing demand for electric vehicles (EVs) because of the ongoing decarbonization efforts and green energy initiatives is anticipated to be the key driver for market growth during the forecast period.

Battery electric vehicles (BEV) are anticipated to drive volume demand in the market. The BEVs use a battery pack to store electrical energy to power their motors. Battery cooling plates are widely utilized as heat dissipation is extremely important for the safety and optimum performance of the vehicle. The battery cooling plates are mainly used in liquid cooling, a widely used battery thermal management system technology.

The increase in the production of EV batteries is fueling market growth. For instance, as of June 2023, GM and Samsung SDI are building a new EV battery plant worth USD 3 billion in Indiana, U.S., as a joint venture. This will be GM’s fourth battery plant in the U.S. In addition, in May 2023, Hyundai and LG Energy announced a new EV battery plant in the U.S., worth USD 4.3 billion.

Indirect cooling held the largest revenue share of the market in 2022, and it is likely to continue its dominance during the forecast period. Like traditional internal combustion engines, the liquid coolant circulates through a system of pipes embedded into a battery cooling plate. It is the most widely used commercial technology, readily utilized by EVs. There is ongoing R&D to develop more efficient cooling methods.

Asia Pacific held the largest revenue share of the market in 2022 due to the highest volumes sold. Charging infrastructure is being developed at a rapid pace. Various tax incentives are being provided to buyers to encourage purchases. For instance, in June 2023, China offered the EV industry its largest package of tax breaks of USD 72.3 billion for over four years, aiming to boost the slowing auto sales.

Battery Cooling Plate Market Report Highlights

Based on process indirect cooling is anticipated to register the fastest CAGR of 37.5%, in terms of revenue, from 2023 to 2030. This cooling type is widely used in electric vehicles(EVs) because of its established technology, widely available coolant liquid, and economical cost

Based on application, BEV is anticipated to register the fastest CAGR of 42.1% in terms of revenue, during the forecast period. BEVs are purely battery-operated vehicles with zero carbon emissions and attract tax incentives for their production and purchase

Based on region, Asia Pacific is expected to register the fastest CAGR of 39.2%, in terms of revenue, over the forecast period. Various government initiatives are propelling the growth. For instance, the region is part of the Electric Vehicles Initiative (EVI), a forum to accelerate the adoption of EVs worldwide

In September 2021, MAHLE GmbH developed a new system for cooling batteries. The immersion cooling technology helps reduce charging time for EVs; thus, batteries can be smaller, resulting in more resource-efficient and low-cost EVs

Battery Cooling Plate Market Segmentation

Grand View Research has segmented the global battery cooling plate market based on process, application, and region:

Battery Cooling Plate Process Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

Direct Cooling

Indirect Cooling

Battery Cooling Plate Application Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

BEV

PHEV

Battery Cooling Plate Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

North America

US

Europe

Germany

France

UK

Netherlands

Asia Pacific

China

Japan

Central & South America

Middle East & Africa

Key Players in the Battery Cooling Plate Market

Bespoke Composite Panels

Dana Limited

Estra Automotive

KOHSAN Co., Ltd

MAHLE GmbH

Modine Manufacturing Company

Nippon Light Metals

Priatherm

SANHUA Automotive

Order a free sample PDF of the Battery Cooling Plate Market Intelligence Study, published by Grand View Research.

0 notes

Text

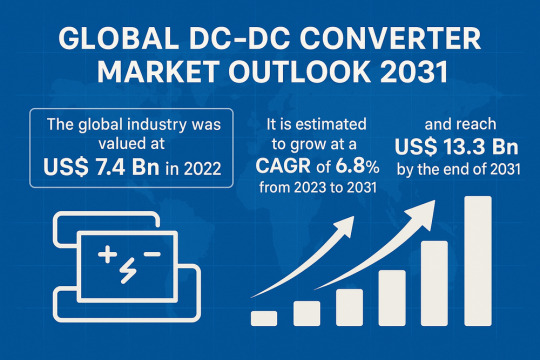

Technological Innovation Catalyzes Growth in the DC-DC Converter Market

The Global DC-DC Converter Market Outlook 2031 report reveals that the market, valued at USD 7.4 billion in 2022, is projected to expand at a CAGR of 6.8% from 2023 through 2031, reaching USD 13.3 billion by the end of 2031.

Market Overview: DC-DC converters are essential for managing power distribution across myriad electronic systems, converting input DC voltages to regulated outputs with high efficiency and minimal noise. From automotive and telecommunications to aerospace and renewable energy, these converters ensure optimal performance and reliability. In 2022, the global DC-DC converter market was valued at USD 7.4 billion. With surging demand for energy-efficient electronics and rapid electrification of transportation, the market is on track to achieve USD 13.3 billion by 2031, growing at a steady 6.8% CAGR.

Market Drivers & Trends

Energy Efficiency Imperative: As industries pursue greener operations and lower operating costs, high-efficiency DC-DC converters reduce energy losses and extend battery life in portable and off‑grid applications.

Electric Vehicle (EV) Adoption: Rising EV sales necessitate reliable DC-DC converters to step down high‑voltage battery output for auxiliary loads such as lighting, infotainment, and safety systems.

Technological Advancements: Innovations in wide‑bandgap semiconductors (e.g., SiC, GaN), digital control algorithms, and higher power density architectures are driving performance improvements and miniaturization.

Power Density & Integration: The trend toward compact, integrated power modules that combine control, protection, and conversion functions is reshaping customer expectations and creating new design opportunities.

Key Players and Industry Leaders

The global DC-DC converter landscape is highly fragmented, with numerous specialized and diversified vendors competing on quality, innovation, and customization:

ABB Ltd.

Advanced Energy Industries, Inc.

Bel Fuse Inc.

Delta Electronics, Inc.

FDK Corporation

FLEX Ltd.

Infineon Technologies AG

MEAN WELL Enterprises Co., Ltd.

Meggitt PLC

Murata Manufacturing Co., Ltd.

STMicroelectronics N.V.

TDK Corporation

Texas Instruments Incorporated

Vicor Corporation

XP Power

Other Key Players

Each company’s profile in the report includes an overview, financial performance, R&D focus, product portfolio, and strategic initiatives.

Download to explore critical insights from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=57555

Recent Developments

October 2023: Bel Fuse launched the 700DNG40-24-8, a liquid‑cooled 4 kW DC-DC converter for EV and HEV auxiliary systems.

September 2023: FLEX Ltd. introduced the 300 W PKU4317D series for telecom/datacom applications, featuring comprehensive protection against over-temperature, under-voltage, and short circuits.

March 2023: Bel Fuse rolled out the RDT-6Y series for railway applications, offering a 12:1 input range (14–160 VDC).

November 2021: Eaton eMobility secured a contract for a 24 V-to-12 V DC-DC converter in heavy‑duty battery-electric vehicles, emphasizing noise reduction and interference rejection.

November 2019: Delta Electronics debuted its B70SP series (500 W, 91.5% efficiency) for industrial and off-road electric vehicles.

Latest Market Trends

Isolated Converters Dominate: In 2022, isolated DC-DC converters commanded a 73.1% share, driven by safety isolation, noise suppression, and ground‑potential flexibility. This segment is forecast to grow at 6.2% CAGR through 2031.

Data Center Electrification: With the explosion of high‑performance computing, data center racks increasingly rely on dense DC-DC modules to manage power in space-constrained environments. The data center segment held an 18.5% share in 2022.

Modular, Scalable Architectures: Vendors are offering plug-and-play power blocks that can be paralleled or stacked to meet variable load demands, enhancing scalability and reducing development time.

Market Opportunities

Renewable Energy Integration: As solar and wind installations proliferate, DC microgrids and battery storage systems require efficient converters to balance generation, storage, and consumption.

5G & Edge Computing: Telecom base stations and edge data nodes demand high-reliability, compact converters to support continuous operation in diverse environments.

Industrial Automation & IIoT: Smart factories and robotics applications benefit from precision power control, enabling predictive maintenance and higher uptime.

Future Outlook

Analysts anticipate sustained expansion of the DC-DC converter market, underpinned by global electrification trends and stringent energy regulations. Innovation in digital control and AI‑driven power management is set to unlock further efficiency gains. By 2031, next‑generation converters will support higher voltage battery systems (>800 V), bidirectional power flow for vehicle‑to-grid (V2G) applications, and advanced fault‑tolerance features for critical infrastructure.

Market Segmentation

By Type

Isolated DC-DC Converter

Non‑isolated DC-DC Converter

By Power Range

Up to 100 W; 100–500 W; 500–1 000 W; 1 000–1 500 W; 1 500–2 000 W; Above 2 000 W

By Input Voltage

Up to 20 V; 20–40 V; 40–60 V; 60–100 V; Above 100 V

By Output Voltage

Up to 12 V; 12–24 V; 24–48 V; 48–72 V; 72–100 V; Above 100 V

By Brick Size

1/2, 1/4, 1/8, 1/16, 1/32 Brick; Full Brick

By Mounting

Chassis, Through‑Hole, SMD/SMT, DIN Rail, Others

By Application

Data Centers, Industrial Automation, Automotive, Aircraft/Spacecraft, Smartphones, Home Appliances, Computing Devices, Solar Inverters, Others

By End‑use Industry

Automotive & Transportation, Aerospace & Defense, Electronics & Semiconductor, IT & Telecom, Industrial, Energy & Utility, Others

By Region

North America, Europe, Asia Pacific, Latin America, Middle East & Africa

Why Buy This Report?

Comprehensive Analysis: Global and regional market sizing, historical data (2017–2021), and detailed forecasts (2023–2031).

Multi-layered Segmentation: Cross-segment insights by type, power range, voltage, mounting, application, and end‑use.

Competitive Landscape: In-depth profiles of 15+ key players, market share analysis, strategic initiatives, and recent developments.

Strategic Tools: Porter’s Five Forces, value chain analysis, and trend mapping to guide investment and product development.

Rich Data Package: Electronic report (PDF) plus Excel database for customized analysis.

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Forklift Market: Steady Growth Ahead as Material Handling Efficiency Gains Priority

The forklift trucks market size is projected to grow from USD 59.79 billion in 2025 to USD 70.87 billion by 2030, registering a compound annual growth rate (CAGR) of 3.46% during the forecast period.

Market Overview:

The forklift market is witnessing consistent growth driven by rising demand in warehousing, construction, and manufacturing industries. As global trade volumes increase and e-commerce continues to expand, the need for efficient material handling solutions is higher than ever. Forklift companies are investing heavily in electric and autonomous models to cater to sustainability goals and reduce operational costs. The global forklift market is also benefitting from government initiatives supporting industrial automation and logistics infrastructure upgrades, especially in emerging economies. These changes are significantly impacting the forklift market size and transforming the forklift industry landscape.

Key Trends:

Shift Toward Electric and Hybrid Forklifts Environmental concerns and rising fuel costs are accelerating the adoption of electric forklifts. Companies are transitioning from traditional IC engines to battery-powered models, influencing the forklift market share and promoting cleaner warehouse operations.

Growth of E-commerce & Warehousing Sector The global boom in online retail has led to rapid warehouse expansion. This growth fuels demand in the forklift trucks market, especially for compact, agile units capable of operating in high-density storage environments.

Integration of Telematics and IoT Smart forklifts equipped with telematics and IoT sensors are gaining traction. These innovations help in fleet management, predictive maintenance, and safety monitoring, adding a technological edge to the forklift industry.

Rising Demand for Forklift Maintenance Service Market As fleets grow and become more sophisticated, the forklift maintenance service market is emerging as a key segment. Preventive and predictive maintenance contracts are increasingly sought after to ensure minimal downtime and cost control.

Autonomous and Driverless Forklifts Advanced automation is leading to the development of autonomous forklift trucks, which are particularly useful in large-scale warehouses and repetitive operation zones. This innovation is redefining operational workflows in the forklift truck market.

Challenges:

High Initial Investment and Technology Costs Despite long-term savings, electric and autonomous forklifts often require significant upfront capital, which may hinder adoption by small to mid-sized businesses in the forklift market.

Skilled Labor Shortages Operating and maintaining modern forklift systems demands a skilled workforce. Shortages in trained operators and maintenance technicians can impact growth across the global forklift market.

Supply Chain Disruptions Global disruptions in chip supply, raw materials, and logistics can delay manufacturing and delivery of new units, affecting forklift companies’ ability to meet growing demand.

Conclusion:

The forklift market is undergoing a steady yet strategic transformation fueled by e-commerce, automation, and sustainability trends. From traditional IC forklifts to smart, electric, and autonomous systems, the evolution is shaping every facet of the forklift truck market. As forklift companies embrace innovation and expand maintenance offerings, the forklift market size is expected to see healthy growth through 2030. Stakeholders who adapt early to these trends will be well-positioned to capture significant forklift market share in the coming years.

For a detailed overview and more insights, you can refer to the full Forklift Market research report by Mordor Intelligence

#forklift market#forklift trucks market#global forklift market#forklift industry#forklift market share#forklift truck market#forklift market size

0 notes

Text

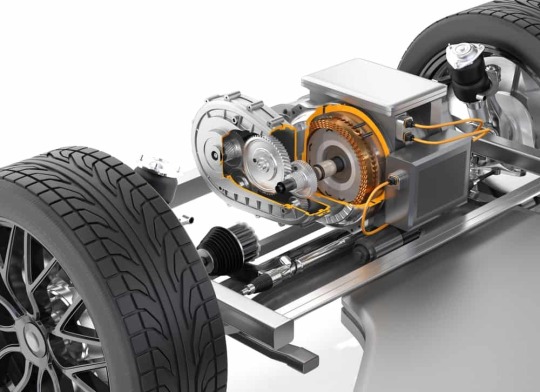

Electric Vehicle Motor Market Developments: Navigating a Revolution in Clean Mobility

The electric vehicle (EV) motor market is experiencing profound developments, transforming the landscape of the global automotive industry. As nations strive toward sustainable and low-emission transportation solutions, EV motors have emerged as a cornerstone of clean mobility. These motors, which convert electrical energy into mechanical energy to power EVs, are evolving rapidly due to advancements in technology, increased investment, and strong governmental support.

Growing Demand for Electric Vehicles

The foundation of developments in the EV motor market is the accelerating global demand for electric vehicles. Consumers and governments alike are gravitating toward EVs due to their environmental benefits, lower operating costs, and advancing technology. This increasing adoption is directly boosting demand for electric motors, as they are vital components of the EV drivetrain.

According to market analysts, the global EV motor market is projected to witness a compound annual growth rate (CAGR) exceeding 20% over the next decade. Factors such as climate change awareness, improved battery technologies, and expansion of EV infrastructure have played a key role in propelling this market forward.

Technological Advancements in EV Motors

Technological innovation has been a major driver of development in the EV motor market. The primary types of motors used in EVs include brushless DC motors (BLDC), permanent magnet synchronous motors (PMSM), and induction motors. Each motor type is evolving to meet demands for higher efficiency, lower maintenance, and reduced size and weight.

Recent developments include:

Increased Power Density: Engineers are developing motors with higher power-to-weight ratios, allowing vehicles to achieve better performance with less energy.

Integration with Inverters and Controllers: Next-generation EV motors often feature integrated inverters and control systems, optimizing power usage and enhancing driving experience.

Magnet-Free Motor Designs: To reduce reliance on rare earth materials, manufacturers are investing in magnet-free motor designs like switched reluctance motors (SRMs), which offer cost and supply chain benefits.

These innovations are essential for automakers aiming to deliver longer range, better acceleration, and more compact powertrains in their electric vehicle offerings.

Role of Key Players and Collaborations

Several automotive giants and emerging tech startups are investing heavily in the EV motor market. Companies such as Tesla, BYD, Bosch, Nidec Corporation, Siemens, and Toyota are pioneering new motor designs and manufacturing processes.

Collaborations and strategic partnerships are also shaping the market. For instance, major automakers are teaming up with motor manufacturers and research institutions to co-develop next-generation EV propulsion systems. Joint ventures allow for shared expertise and faster time-to-market for advanced motor solutions.

Regional Developments and Government Initiatives

Regionally, Asia-Pacific dominates the EV motor market, with China being the largest contributor due to its robust EV manufacturing base, government subsidies, and growing domestic demand. India, Japan, and South Korea are also investing in R&D and manufacturing capacities.

In Europe and North America, stringent emission regulations, zero-emission vehicle (ZEV) targets, and incentives for EV buyers are pushing automakers to accelerate the adoption of electric mobility and motor development. The European Union’s Green Deal and the U.S. Inflation Reduction Act are among the policies bolstering EV motor innovations and supply chain investments.

Challenges in the Market

Despite the optimistic outlook, the market faces challenges. High production costs, dependence on rare earth materials for magnets, and thermal management issues in motors are some hurdles. Addressing these requires continued innovation, especially in cost-effective manufacturing techniques and alternative materials.

Additionally, the integration of EV motors with autonomous driving technologies and vehicle-to-grid (V2G) systems introduces complexities that manufacturers must resolve to ensure seamless operation.

The Road Ahead: Emerging Trends

The future of the EV motor market lies in the development of smart and connected systems. Electric motors integrated with AI-powered diagnostics, real-time performance monitoring, and adaptive control mechanisms will soon become standard. Wireless motor control, over-the-air updates, and predictive maintenance are also expected to influence future designs.

Moreover, solid-state batteries and ultrafast charging technologies will reshape the requirements for motor performance, prompting manufacturers to rethink design and efficiency standards. Lightweight materials and modular construction will further define the next generation of EV motors.

Conclusion

The electric vehicle motor market is on an upward trajectory, powered by innovation, sustainability, and shifting consumer preferences. With continuous developments in motor technology, manufacturing efficiency, and government support, the industry is positioned to lead the green transportation revolution. Stakeholders across the automotive and energy sectors must now collaborate to accelerate these developments and make electric mobility mainstream on a global scale.

0 notes

Text

Electric Vehicle Telematics Market Expansion Strategies and Growth Opportunities to 2033

Introduction

As electric vehicles (EVs) accelerate toward mainstream adoption, telematics is emerging as a pivotal technology for maximizing efficiency, safety, and connectivity in the EV ecosystem. The Electric Vehicle Telematics Market—which encompasses technologies that combine telecommunications and informatics for monitoring and managing vehicle operations—is witnessing exponential growth.

From fleet tracking and vehicle diagnostics to real-time navigation and driver behavior analysis, EV telematics has become indispensable for original equipment manufacturers (OEMs), fleet operators, and end consumers. With the global EV market booming, telematics is evolving to meet the specific challenges and opportunities that electric mobility brings.

Market Overview

Market Size and Forecast

In 2023, the Electric Vehicle Telematics Market was valued at USD 3.4 billion and is projected to reach USD 12.6 billion by 2032, expanding at a CAGR of 15.5% during the forecast period. This surge is driven by:

Rising EV adoption worldwide

Growing demand for connected vehicle solutions

Regulatory mandates for vehicle safety and emissions monitoring

Increasing use of telematics in commercial EV fleets

Download a Free Sample Report:-https://tinyurl.com/575t4bn8

Key Market Drivers

Accelerated Electric Vehicle Adoption

The global push toward decarbonization and the ban on internal combustion engine (ICE) vehicles in several regions are encouraging consumers and businesses to switch to electric mobility. As more EVs hit the roads, the need for intelligent telematics systems grows in parallel to ensure optimized performance, safety, and service management.

Government Regulations and Safety Mandates

Countries across Europe, North America, and Asia-Pacific have mandated the integration of eCall, emission monitoring, and real-time vehicle tracking systems. These regulations are promoting telematics adoption, especially in electric commercial vehicles and public transport fleets.

Connected Vehicle Ecosystem Growth

Consumers today demand seamless, connected driving experiences. EV telematics enables real-time data sharing between the vehicle, user, OEMs, and third-party apps—supporting features like route optimization, remote diagnostics, predictive maintenance, and smart charging.

Fleet Management Optimization

Fleet operators benefit immensely from telematics-enabled EVs. Telematics platforms allow battery health monitoring, charging status tracking, driver behavior insights, and real-time route planning, thus reducing downtime and operational costs.

Market Segmentation

By Component

Hardware (GPS devices, OBD II, sensors, control units)

Software (fleet management platforms, analytics, APIs)

Services (consulting, cloud hosting, software integration)

While hardware forms the backbone of the telematics ecosystem, software and services are growing rapidly due to increasing demand for custom solutions and SaaS platforms.

By Type

Embedded

Integrated/Aftermarket

Tethered

Embedded telematics systems dominate the market due to OEM preference for factory-installed solutions offering better security, reliability, and data analytics integration.

By Application

Navigation & Route Optimization

Battery Monitoring

Remote Diagnostics

Vehicle Tracking

Driver Behavior Monitoring

Infotainment and Connectivity

Battery monitoring and vehicle tracking hold the highest share in EVs, while infotainment systems are also gaining traction as consumer expectations for connected experiences rise.

By Vehicle Type

Passenger EVs

Commercial EVs

Two- and Three-Wheelers

Commercial EVs, particularly in logistics, ride-hailing, and last-mile delivery, are a major driver due to the need for precise tracking and cost optimization.

Regional Insights

North America

The U.S. and Canada are early adopters of EV telematics due to strong EV infrastructure, tech-savvy consumers, and stringent safety standards. Government incentives for EVs and connected mobility are also supporting market growth.

Europe

Europe is the largest market, driven by strong regulatory frameworks like the European General Safety Regulation, widespread adoption of EVs, and OEM focus on smart vehicle technologies. Countries like Germany, the UK, and Norway lead in telematics integration.

Asia-Pacific

Fastest-growing region, led by China, Japan, South Korea, and India. China’s dominance in EV production and sales, combined with its investment in smart transportation systems, positions APAC as a high-potential market for EV telematics.

Latin America, Middle East, and Africa (LAMEA)

Though still emerging, adoption is growing due to rising EV imports, smart city projects, and international collaborations focused on sustainable mobility.

Emerging Trends

Artificial Intelligence and Predictive Analytics

AI-powered telematics platforms can analyze vehicle performance and driver data in real time to provide predictive maintenance alerts, route suggestions, and energy consumption forecasts, enhancing EV efficiency.

Integration with Vehicle-to-Everything (V2X) Communication

As autonomous and semi-autonomous EVs become reality, V2X—where vehicles communicate with infrastructure, networks, and each other—is becoming a key integration point for advanced telematics systems.

Cloud-Based Fleet Telematics Platforms

Cloud telematics solutions offer real-time access, scalability, and seamless software updates. This trend is especially relevant for fleet managers and mobility-as-a-service (MaaS) providers.

Data Monetization and Third-Party Integration

OEMs and service providers are looking to monetize telematics data by offering insights to insurance companies, smart city planners, and retail businesses, creating new revenue streams.

Telematics and Charging Infrastructure Sync

Future systems are being developed to integrate telematics data with EV charging networks, enabling dynamic charging recommendations, scheduling, and cost optimization for drivers and fleets.

Challenges

Data Privacy and Cybersecurity

Telematics involves continuous data transmission, raising concerns over data security, hacking, and user privacy. OEMs and tech firms must invest in robust cybersecurity frameworks and comply with privacy laws like GDPR.

High Costs of Advanced Telematics Systems

Despite decreasing hardware prices, full-featured telematics systems can be costly—posing adoption challenges for startups and small fleet operators, particularly in price-sensitive markets.

Standardization Issues

Lack of global standards in EV telematics protocols can hamper interoperability across regions and brands, especially in fleet operations involving multiple vehicle types and providers.

Key Players

The competitive landscape includes major automotive, tech, and telecom players who are focusing on partnerships, software innovation, and AI integration:

Geotab

TomTom

Verizon Connect

Continental AG

Bosch

LG Electronics

Tesla Inc.

Nissan Motor Corporation

Qualcomm Technologies Inc.

Teletrac Navman

These companies are increasingly investing in R&D to develop cloud-native, modular telematics platforms tailored for electric vehicles.

Future Outlook (2024–2032)

As electric mobility continues to evolve, EV telematics will become more than just a support system—it will be the digital backbone of electric transportation. Anticipated developments include:

Mass adoption of AI-enhanced telematics for autonomous EVs

Real-time charging optimization based on route, availability, and battery status

Subscription-based telematics services bundled with EV purchases

Widespread deployment in shared mobility platforms and MaaS

Deep integration with urban mobility and energy grid systems

Conclusion

The Electric Vehicle Telematics Market is experiencing a paradigm shift, where data-driven intelligence is key to unlocking the full potential of electric mobility. As OEMs, governments, and consumers embrace connected transportation, telematics will be central to optimizing EV performance, safety, and user experience. With innovations in AI, cloud, cybersecurity, and V2X, the industry is poised to play a foundational role in the future of transportation through 2032 and beyond.Read Full Report:-https://www.uniprismmarketresearch.com/verticals/automotive-transportation/electric-vehicle-telematics

0 notes

Text

More Than Just Monitoring: The Intelligence of Vehicle Battery Sensors

Vehicles Intelligence Battery Sensor Market Growth & Trends

The global Vehicles Intelligence Battery Sensor Market size was estimated at USD 2.96 billion in 2023 and is expected to grow a CAGR of 12.8% from 2024 to 2030. This growth can be attributed to the rapid electrification of the automotive industry. There is a surge in demand for advanced battery management systems due to increasing market shares of the electric vehicles (EVs) and hybrid vehicles. These intelligent sensors play a crucial role in monitoring battery health, optimizing performance, and extending battery life, which are critical factors for EV adoption.

Additionally, stringent emissions regulations worldwide are pushing automakers to incorporate more sophisticated battery technologies even in conventional internal combustion engine vehicles, further expanding the market for intelligent battery sensors. Technological advancements in sensor accuracy, reliability, and integration capabilities are also fueling market growth. Modern vehicle intelligence battery sensors can provide real-time data on battery status, predict potential issues, and communicate with other vehicle systems for improved overall performance. This integration with vehicle telematics and connected car systems is becoming increasingly important as consumers and manufacturers alike prioritize predictive maintenance and enhanced diagnostics. The ability of these sensors to contribute to improved vehicle safety and efficiency is a key factor driving their adoption across various vehicle types.

The market is also benefiting from the expanding automotive industry in developing countries. With the increasing regional vehicle production, the demand for advanced components like intelligent battery sensors is also increasing. Moreover, rising consumer expectations for longer battery life and improved vehicle range, particularly in EVs, are pushing manufacturers to invest in more sophisticated battery management solutions. This trend is not limited to new vehicles, the aftermarket segment is also seeing growth as owners of older vehicles seek to upgrade their battery management systems.

The market landscape is also being shaped by emerging trends in vehicle design and consumer preferences. As automakers increasingly focus on lightweight materials and compact designs to improve fuel efficiency and EV range, there's a growing need for smaller, more efficient battery sensors that can deliver high performance in limited spaces. Additionally, the rise of autonomous vehicles and advanced driver assistance systems (ADAS) is creating new applications for intelligent battery sensors, as these technologies require consistent and reliable power management. Furthermore, the push towards circular economy principles in the automotive sector is driving interest in battery sensors that can facilitate easier recycling and second-life applications for EV batteries. These evolving market dynamics, coupled with the increasing complexity of vehicle electrical systems, are expected to create new opportunities for innovation and market expansion in the vehicle intelligence battery sensor sector over the forecast period.

Curious about the Vehicles Intelligence Battery Sensor Market? Download your FREE sample copy now and get a sneak peek into the latest insights and trends.

Vehicles Intelligence Battery Sensor Market Report Highlights

The passenger car segment held the largest revenue share of 64.2% in 2023 and is expected to maintain its dominance from 2024 to 2030 due to the higher production volumes and increasing demand for these sensors.

The Hall Effect sensor segment's dominant position, captured 52.2% of the market revenue share in 2023 in the market’s technology segment.

The battery management system segment held the largest revenue share of 41.1% in 2023 and is expected to maintain its dominance from 2024 to 2030, which is mainly attributed to its critical role in optimizing battery performance and longevity.

The North American vehicles intelligence battery sensor market is experiencing growth driven primarily by the rapid adoption of electric and hybrid vehicles in the region.

Vehicles Intelligence Battery Sensor Market Segmentation

Grand View Research has segmented the global vehicles intelligence battery sensor market report based on vehicle type, technology, application, and region.

Vehicle Type Outlook (Revenue, USD Million, 2017 - 2030)

Passenger Cars

Commercial Vehicles

Technology Outlook (Revenue, USD Million, 2017 - 2030)