#Global Automotive Battery Management System Market

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Forty percent of Tumblr users are between the ages of 18 to 25.

Text

Automotive Battery Management System Market Set for Explosive Growth

Market Research Forecast released a new market study on Global Automotive Battery Management System Market Research report which presents a complete assessment of the Market and contains a future trend, current growth factors, attentive opinions, facts, and industry validated market data. The research study provides estimates for Global Automotive Battery Management System Forecast till 2032. The Automotive Battery Management System Marketsize was valued at USD 8.25 USD Billion in 2023 and is projected to reach USD 23.56 USD Billion by 2032, exhibiting a CAGR of 16.17 % during the forecast period. Key Players included in the Research Coverage of Automotive Battery Management System Market are: Robert Bosch GmbH (Germany), Continental AG (Germany), Toshiba Corporation (Japan), Intel Corporation (U.S.), NXP Semiconductors NV (Netherlands), Analog Devices, Inc. (U.S.), Denso Corporation (Japan), Johnson Matthey, Inc. (U.K.), LG Chem, Ltd. (South Korea), Midtronics, Inc. (U.S.) What's Trending in Market: Rising Adoption of Automation in Manufacturing to Drive Market Growth Market Growth Drivers: Increasing Demand for Forged Products in Power, Agriculture, Aerospace, and Defense to Drive Industry Expansion The Global Automotive Battery Management System Market segments and Market Data Break Down Propulsion Type: BEV, PHEV, and HEV","Vehicle Type: Passenger Cars and Commercial Vehicles GET FREE SAMPLE PDF ON Automotive Battery Management System MARKET To comprehend Global Automotive Battery Management System market dynamics in the world mainly, the worldwide Automotive Battery Management System market is analyzed across major global regions. MR Forecast also provides customized specific regional and country-level reports for the following areas.

• North America: United States, Canada, and Mexico. • South & Central America: Argentina, Chile, Colombia and Brazil. • Middle East & Africa: Saudi Arabia, United Arab Emirates, Israel, Turkey, Egypt and South Africa. • Europe: United Kingdom, France, Italy, Germany, Spain, Belgium, Netherlands and Russia. • Asia-Pacific: India, China, Japan, South Korea, Indonesia, Malaysia, Singapore, and Australia.

Extracts from Table of Contents Automotive Battery Management System Market Research Report Chapter 1 Automotive Battery Management System Market Overview Chapter 2 Global Economic Impact on Industry Chapter 3 Global Market Competition by Manufacturers Chapter 4 Global Revenue (Value, Volume*) by Region Chapter 5 Global Supplies (Production), Consumption, Export, Import by Regions Chapter 6 Global Revenue (Value, Volume*), Price* Trend by Type Chapter 7 Global Market Analysis by Application ………………….continued More Reports:

https://marketresearchforecast.com/reports/automotive-usage-based-insurance-market-2982 For More Information Please Connect MR ForecastContact US: Craig Francis (PR & Marketing Manager) Market Research Forecast Unit No. 429, Parsonage Road Edison, NJ New Jersey USA – 08837 Phone: (+1 201 565 3262, +44 161 818 8166)[email protected]

#Global Automotive Battery Management System Market#Automotive Battery Management System Market Demand#Automotive Battery Management System Market Trends#Automotive Battery Management System Market Analysis#Automotive Battery Management System Market Growth#Automotive Battery Management System Market Share#Automotive Battery Management System Market Forecast#Automotive Battery Management System Market Challenges

0 notes

Text

Global top 13 companies accounted for 66% of Total Frozen Spring Roll market(qyresearch, 2021)

The table below details the Discrete Manufacturing ERP revenue and market share of major players, from 2016 to 2021. The data for 2021 is an estimate, based on the historical figures and the data we interviewed this year.

Major players in the market are identified through secondary research and their market revenues are determined through primary and secondary research. Secondary research includes the research of the annual financial reports of the top companies; while primary research includes extensive interviews of key opinion leaders and industry experts such as experienced front-line staffs, directors, CEOs and marketing executives. The percentage splits, market shares, growth rates and breakdowns of the product markets are determined through secondary sources and verified through the primary sources.

According to the new market research report “Global Discrete Manufacturing ERP Market Report 2023-2029”, published by QYResearch, the global Discrete Manufacturing ERP market size is projected to reach USD 9.78 billion by 2029, at a CAGR of 10.6% during the forecast period.

Figure. Global Frozen Spring Roll Market Size (US$ Mn), 2018-2029

Figure. Global Frozen Spring Roll Top 13 Players Ranking and Market Share(Based on data of 2021, Continually updated)

The global key manufacturers of Discrete Manufacturing ERP include Visibility, Global Shop Solutions, SYSPRO, ECi Software Solutions, abas Software AG, IFS AB, QAD Inc, Infor, abas Software AG, ECi Software Solutions, etc. In 2021, the global top five players had a share approximately 66.0% in terms of revenue.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 16 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

2 notes

·

View notes

Text

Automotive Aftermarket Market Consumer Behavior and Industry Shifts to 2033

The automotive aftermarket industry is a crucial sector that supports the automotive ecosystem by providing replacement parts, accessories, and services after the sale of the original vehicle. With the increasing number of vehicles on the road, technological advancements, and evolving consumer preferences, the aftermarket industry is undergoing significant transformations. This article explores the key trends shaping the automotive aftermarket, challenges, opportunities, and market forecasts leading up to 2032.

Market Overview

The global automotive aftermarket industry is projected to grow at a robust pace due to factors such as increased vehicle longevity, growing demand for customization, and advancements in e-commerce. According to market research, the industry was valued at approximately XX billion in 2022 and is expected to exceed XX billion by 2032, registering a CAGR of XX% over the forecast period.

Download a Free Sample Report:- https://tinyurl.com/ywcj7x7n

Key Market Drivers

1. Increasing Vehicle Longevity and Maintenance Demand

Modern vehicles are built to last longer, with the average vehicle lifespan exceeding 12 years in major markets such as the U.S. and Europe. As cars age, the demand for replacement parts, repairs, and maintenance services increases, driving aftermarket growth.

2. Technological Advancements and Digitalization

Telematics and IoT Integration: Smart diagnostics and predictive maintenance enabled by IoT are becoming more prevalent, allowing consumers and service providers to identify and address issues before breakdowns occur.

E-commerce Expansion: Online platforms such as Amazon, eBay, and dedicated auto part marketplaces are revolutionizing the way consumers purchase aftermarket parts.

3D Printing: The rise of additive manufacturing is enhancing the ability to produce replacement parts quickly and cost-effectively, reducing dependency on traditional supply chains.

3. Rising Demand for Vehicle Customization

Consumers are increasingly looking for ways to personalize their vehicles, whether for aesthetic improvements or performance enhancements. This trend is particularly strong among younger generations who seek aftermarket accessories such as upgraded infotainment systems, performance exhausts, and custom wheels.

4. Expansion of Electric Vehicles (EVs)

While traditional combustion engine vehicles dominate the aftermarket, the rise of electric vehicles is reshaping the industry. EVs require fewer mechanical components but demand specialized services for battery replacements, software upgrades, and advanced diagnostic tools. Companies investing in EV-specific aftermarket solutions are expected to gain a competitive edge.

Challenges Facing the Automotive Aftermarket

1. Supply Chain Disruptions

Global supply chain constraints, exacerbated by the COVID-19 pandemic and geopolitical conflicts, have led to shortages in raw materials and increased costs for automotive parts.

2. Regulatory Compliance

Stricter emissions regulations and evolving government policies impact the aftermarket industry, requiring businesses to adapt by offering environmentally friendly products and adhering to compliance standards.

3. Competition from OEMs

Original Equipment Manufacturers (OEMs) are increasingly entering the aftermarket space by offering extended warranties and proprietary service programs, making it challenging for independent aftermarket players to compete.

4. Skilled Labor Shortages

The demand for skilled technicians proficient in handling modern vehicle technologies, including hybrid and EV maintenance, is outpacing supply. Investment in workforce training is critical for sustained growth.

Opportunities in the Automotive Aftermarket

1. Digital Transformation and E-commerce Expansion

Companies that leverage digital platforms for direct-to-consumer sales, AI-driven recommendations, and efficient logistics management will capture a larger market share.

2. Growth in Emerging Markets

Developing regions such as Asia-Pacific, Latin America, and Africa present significant opportunities due to increasing vehicle ownership, expanding road infrastructure, and rising disposable incomes.

3. Sustainability and Green Aftermarket Products

The push for eco-friendly automotive solutions, such as remanufactured parts, biodegradable lubricants, and recyclable materials, is gaining traction among consumers and regulatory bodies alike.

Market Forecast to 2032

North America: Expected to maintain a steady growth trajectory, driven by strong aftermarket sales in the U.S. and Canada.

Europe: Growth will be driven by advancements in EV aftermarkets and strict regulatory policies encouraging green solutions.

Asia-Pacific: Anticipated to witness the fastest growth due to increasing vehicle sales, a large aging vehicle population, and booming e-commerce platforms.

Latin America & Middle East: Steady expansion is expected, backed by rising urbanization and growing investments in the automotive sector.

Conclusion

The automotive aftermarket industry is poised for substantial growth in the coming decade, driven by digitalization, rising vehicle longevity, and increasing consumer demand for customization. While challenges such as supply chain disruptions and regulatory changes pose hurdles, opportunities in emerging markets, green products, and e-commerce expansion present lucrative avenues for industry players. Businesses that invest in innovation and adaptability will thrive in the evolving landscape of the automotive aftermarket industry through 2032.

Read Full Report:-https://www.uniprismmarketresearch.com/verticals/automotive-transportation/automotive-aftermarket

0 notes

Text

Automotive Semiconductor Market - Forecast(2025 - 2031)

Automotive Semiconductor Market Overview

Automotive Semiconductor market size is forecast to reach US$91 billion by 2030, after growing at a CAGR of 7.8% during 2024-2030. The automotive semiconductor market is primarily driven by the growing demand for advanced vehicle technologies, such as ADAS (Advanced Driver Assistance Systems), infotainment systems, and autonomous driving features. This surge in technology adoption is crucial for enhancing vehicle performance and safety and is supported by regulatory pressures. Stringent emissions and safety standards, like the EU's Euro 7, require sophisticated semiconductor solutions to ensure compliance. Additionally, the rise of electric vehicles (EVs) significantly impacts the market, as these vehicles require specialized semiconductor technologies for battery management systems, powertrain control, and charging infrastructure. Automobile manufacturers are incorporating advanced semiconductor technologies to improve vehicle performance and fuel economy, making their offerings more appealing to consumers.

The automotive semiconductor market is experiencing rapid growth driven by two primary factors- the surge in EV production and the increasing demand for advanced infotainment and connectivity features. Governments worldwide are aggressively promoting EV adoption to address climate change, exemplified by the US aiming for 50% EV sales by 2030 and the EU's plan to phase out internal combustion engines by 2035. Simultaneously, consumers are seeking sophisticated in-car entertainment and connectivity, with nearly 80% of new US cars now equipped with connected technology. These trends underscore the critical role of semiconductors in powering EV battery management, powertrain control, and complex infotainment systems.

Report Coverage

The report "Automotive Semiconductor Market Report – Forecast (2024-2030)" by IndustryARC covers an in-depth analysis of the following segments of the automotive semiconductor market.

By Vehicle Type: Passenger Vehicles, Light Commercial Vehicle (LCV), Heavy Commercial Vehicle (HCV)

By Fuel Type: Petrol, Diesel, EV, Hybrid Vehicles

By Components: Power Semiconductors, Sensors, Memory Devices, Microcontrollers (MCUs), Connectivity Solutions, Analog ICs, ASICs, FPGAs and Others

By Application: Powertrain Control, Body Electronics, Chassis Control, Safety Systems, Infotainment System, Advanced Driver Assistance Systems (ADAS) and Others

By Geography: North America (USA, Canada, and Mexico), Europe (UK, Germany, Italy, France, Spain, Netherlands, Russia, Belgium, and Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Australia and New Zealand, Taiwan, Indonesia, Malaysia, and Rest of Asia Pacific), South America (Brazil, Argentina, Colombia, Chile, and Rest of South America), and RoW (Middle East and Africa)

Request Sample

Key Takeaways

• Asia Pacific is emerging as a leading market due to the rapid expansion of the automotive industry and technological advancements in the region. • The increasing adoption of electric and hybrid vehicles is significantly boosting the demand for automotive semiconductors. • Advances in driver assistance and safety systems are driving innovation and growth in the automotive semiconductor industry.

Automotive Semiconductor Market Segment Analysis – By Type

The Passenger vehicles represent the largest segment in the automotive semiconductor market due to several key factors. Firstly, the sheer volume of passenger vehicles far surpasses that of commercial vehicles. According to the International Organization of Motor Vehicle Manufacturers (OICA), global passenger vehicle sales reached approximately 65 million units in 2023, compared to around 23 million units for commercial vehicles. Additionally, the adoption of advanced driver assistance systems (ADAS) and in-car entertainment systems is more prevalent in passenger vehicles, driving the demand for semiconductors. The rising consumer demand for electric and hybrid vehicles, which rely heavily on semiconductor components for battery management and power control, also contributes to the growth of this segment.

Inquiry Before Buying

Automotive Semiconductor Market Segment Analysis – By Application

The automotive semiconductor market is experiencing robust growth, driven by a diverse range of applications including Advanced Driver Assistance Systems (ADAS), infotainment systems, powertrain control, body electronics, chassis control, and safety systems. ADAS, led by technologies like collision avoidance and lane departure warning, is the dominant segment, with a 20% reduction in collisions in 2023 as reported by the National Highway Traffic Safety Administration (NHTSA). ADAS requires a wide variety of sensors for monitoring the vehicle's prompt surroundings and the drivers, thereby driving the demand for semiconductors. ADAS applications use numerous types of sensors to provide safety attributes such as automated parking assistance, lane departure warning systems, cruise control and collision avoidance systems. In the European Union, the Vehicle General Safety Regulation introduced in 2022, also mandates ADAS applications including intelligent speed assistance, reverse detection of vulnerable road users such as pedestrians and cyclists with driver distraction detection and warning. In September 2023, NHTSA announced several ADAS-related vehicle safety initiatives. Thus, the increasing adoption of ADAS leads to an increased demand for semiconductors.

Automotive Semiconductor Market Segment Analysis – By Geography

The Asia Pacific region dominated the automotive semiconductor market in 2023, driven by significant contributions from major economies like China, Japan, and South Korea. China’s NEV sector has seen rapid growth, with significant increases in output, sales, and exports. By July 2023, NEV output hit 20 million units. In H1 2023, output grew 42.4% YoY to 3.79 million units, sales rose 44.1% to 3.75 million units, and exports surged 160% to 534,000 units. Additionally, in economies like India the increasing automotive production, with government efforts to promote EV adoption and develop local semiconductor manufacturing facilities also boost the market. For instance, data from the Indian government's Vahan website shows that from April 2023 to March 2024, India saw the purchase of 1,665,270 EVs, averaging 4,562 EVs sold each day.

Schedule a Call

Automotive Semiconductor Market Drivers

Increasing Demand for Advanced Vehicle Technologies to Drive Market Growth

The automotive semiconductor market is experiencing rapid expansion fuelled by the increasing integration of Advanced Driver Assistance Systems (ADAS). ADAS technologies, encompassing features such as adaptive cruise control, lane departure warning, and automatic emergency braking, are becoming indispensable in modern vehicles. These systems rely heavily on sensors and cameras to gather real-time data about the driving environment. To process this data efficiently and make split-second decisions, sophisticated semiconductor components are required. As consumers place a growing emphasis on vehicle safety and convenience, the demand for ADAS features is surging. Consequently, automotive manufacturers are investing heavily in these technologies, driving up the need for advanced semiconductors. This confluence of factors has created a robust and expanding market for semiconductor manufacturers catering to the automotive industry.

Rise of Electric Vehicles Boosting Demand for Specialized Semiconductor Technologies

The surge in electric vehicle (EV) adoption is another major driver of the automotive semiconductor market. EVs require specialized semiconductor technologies for battery management systems, powertrain control, and charging infrastructure. According to the International Energy Agency (IEA), global EV sales exceeded 14 million in 2023, with a year-on-year growth of 35%. This rapid increase in EV adoption is driving the demand for advanced semiconductor solutions that can efficiently manage the unique requirements of electric powertrains and charging systems. Automobile manufacturers are increasingly incorporating these semiconductor technologies to improve vehicle performance and fuel economy, making their offerings more appealing to consumers and further stimulating market growth.

Automotive Semiconductor Challenges

Supply Chain Disruption

One significant challenge in the Automotive Semiconductor market is the supply chain disruption. According to the U.S. Department of Commerce, the semiconductor shortage has severely impacted vehicle production timelines and increased costs across the automotive industry. This disruption has been largely driven by a combination of pandemic-related production halts, geopolitical tensions, and surges in demand for electronic components in various sectors. Automakers have faced prolonged delivery times for new vehicles, as well as higher costs for both manufacturing and consumer purchases. The shortage has also forced manufacturers to reallocate available chips to higher-margin vehicles, further complicating inventory management and delaying the availability of other models.

Buy Now

Automotive Semiconductor Market Outlook

Key strategies in the automotive semiconductor market include technological advancements, strategic partnerships, and R&D activities. Major players in the sector include:

NXP Semiconductors N.V.

Infineon Technologies AG

Texas Instruments Inc.

Renesas Electronics Corporation

STMicroelectronics N.V.

Qualcomm Incorporated

Broadcom Inc.

Bosch

Valeo

On Semiconductor Corporation

#Automotive Semiconductor Market#Automotive Semiconductor Market Size#Automotive Semiconductor Market Share#Automotive Semiconductor Market Analysis#Automotive Semiconductor Market Revenue#Automotive Semiconductor Market Trends#Automotive Semiconductor Market Growth#Automotive Semiconductor Market Research#Automotive Semiconductor Market Outlook#Automotive Semiconductor Market Forecast

0 notes

Text

Tin-Plated Copper Busbar Market: Trends, Growth, and Future Insights

What Is the Tin-Plated Copper Busbar Market?

Tin-plated copper busbars are conductive bars used for power distribution in electrical systems. The tin coating enhances corrosion resistance, conductivity, and durability, making them ideal for applications in power distribution, automotive, industrial machinery, and renewable energy.

The global Tin-Plated Copper Busbar market is projected to grow from USD 1.2 billion in 2023 to USD 1.8 billion by 2030, at a CAGR of 5.5%, driven by increasing demand for efficient power transmission and the expansion of renewable energy infrastructure.

What Are the Key Applications of Tin-Plated Copper Busbars?

Power Distribution: Used in electrical panels, switchgear, and circuit breakers.

Renewable Energy: Essential for solar and wind power systems due to high conductivity and weather resistance.

Automotive Industry: Used in EV battery systems and power electronics.

Industrial Equipment: Helps in power transmission in heavy machinery and manufacturing plants.

Data Centers & Telecom: Supports high-power distribution in data centers and communication networks.

Where Is the Tin-Plated Copper Busbar Market Growing the Fastest?

North America: Growth driven by increased investment in energy-efficient infrastructure and electric vehicle production.

Europe: Rising demand from renewable energy projects and strict energy regulations.

Asia-Pacific: The fastest-growing region, fueled by rapid industrialization and expansion of the power sector in China, India, and Japan.

Middle East & Africa: Increasing use in power transmission and industrial applications.

What Are the Challenges in This Market?

Fluctuating Copper Prices: The cost of raw materials impacts pricing and market stability.

Competition from Aluminum Busbars: Aluminum is a cheaper alternative, though less conductive than copper.

Manufacturing Complexity: Tin-plating adds extra production steps and costs.

What’s Next for the Tin-Plated Copper Busbar Market?

Integration with Smart Grids: Increased use in advanced power distribution systems.

Expansion in Electric Vehicles (EVs): Growing adoption in EV power management.

Advanced Coating Technologies: Innovations to improve performance and reduce material costs.

Conclusion

The Tin-Plated Copper Busbar Market is witnessing strong growth, driven by demand for efficient power transmission in industrial, automotive, and renewable energy applications. As industries transition to smarter and more sustainable energy solutions, the need for high-performance busbars will continue to rise. Looking for insights on the power distribution industry? Mark & Spark Solutions can help you stay ahead in this evolving market. Visit our website for more details.

0 notes

Text

High Voltage Capacitor Market Trends: Growth, Challenges, and Emerging Opportunities in the Global Industry

The high voltage capacitor market is witnessing significant growth due to the rising demand for energy storage solutions in industrial, power generation, and transmission applications. These capacitors play a crucial role in stabilizing electrical networks, ensuring efficient energy transfer, and managing power fluctuations. As technological advancements and the need for energy efficiency continue to drive the market, it is essential to examine key trends, challenges, and future opportunities shaping the industry.

Market Growth Drivers Rising Demand for Renewable Energy: The shift towards sustainable energy sources, such as wind and solar power, has increased the demand for high voltage capacitors. These capacitors are essential for managing the power generated from renewable sources and ensuring stability in electrical grids. Expansion of Smart Grid Infrastructure: Governments and energy companies worldwide are investing in smart grids, which require advanced capacitor technologies for efficient power transmission and distribution. Smart grids enhance energy efficiency, reduce transmission losses, and improve overall power system reliability. Growing Industrial and Consumer Electronics Sector: The expansion of industrial automation and the increasing adoption of consumer electronics have led to a surge in demand for high voltage capacitors. These capacitors are widely used in power-intensive applications, including electric vehicles (EVs), telecommunications, and industrial machinery. Technological Advancements in Capacitor Materials: Innovations in capacitor materials, such as the development of ceramic and polymer-based capacitors, are enhancing performance and durability. These advancements contribute to improved energy storage efficiency and reduced maintenance costs. Market Challenges High Initial Costs and Maintenance Requirements: The production and installation of high voltage capacitors require significant investment. Additionally, regular maintenance is necessary to ensure operational efficiency, which can be a challenge for cost-sensitive industries. Raw Material Supply Chain Disruptions: The availability and cost of raw materials, such as aluminum, polypropylene, and ceramics, impact the production and pricing of high voltage capacitors. Supply chain disruptions, geopolitical tensions, and fluctuating commodity prices pose risks to market stability. Stringent Regulatory Standards: High voltage capacitors must comply with stringent safety and environmental regulations. Adhering to these standards requires manufacturers to invest in compliance measures, increasing overall production costs. Future Outlook and Opportunities Adoption of Energy Storage Systems: The rising adoption of energy storage systems for grid stabilization and load balancing presents significant opportunities for high voltage capacitor manufacturers. These capacitors enhance the efficiency of battery storage systems and support peak load management. Development of High-Performance Capacitors for EVs: With the global push towards electric mobility, the demand for high voltage capacitors in EVs is expected to grow. Capacitors are integral to EV powertrains, inverters, and charging infrastructure, making them a critical component in the evolving automotive industry. Expansion in Emerging Markets: Rapid industrialization and urbanization in emerging economies, such as India, China, and Brazil, are fueling the demand for high voltage capacitors. Infrastructure development projects and increasing energy consumption further boost market growth in these regions. Integration of AI and IoT in Capacitor Monitoring: The integration of artificial intelligence (AI) and the Internet of Things (IoT) in capacitor monitoring systems allows for predictive maintenance, real-time performance tracking, and enhanced operational efficiency. This technological evolution is expected to drive future market expansion. Conclusion The high voltage capacitor market is poised for robust growth, driven by the demand for renewable energy, smart grids, and advanced industrial applications. While challenges such as high costs and regulatory compliance persist, emerging opportunities in energy storage, electric mobility, and digital monitoring solutions present a promising outlook. Manufacturers and stakeholders must adapt to evolving technologies and market trends to stay competitive in this dynamic industry.

0 notes

Text

India's Electric Vehicle Revolution: Driving Towards a Sustainable Future

The EV revolution in India is about more than replacing internal combustion engines with batteries. It's about reimagining urban mobility, creating new job markets, and positioning India as a global leader in sustainable transportation.

Various government-backed initiatives are leading efforts to facilitate this shift across India by streamlining services and promoting eco-friendly options to shape the future of EV adoption.

The Expanding Significance of EVs in India

India faces substantial pressure to reduce carbon emissions, with transportation a significant source. The government has introduced policies encouraging electric vehicle adoption as part of a larger net-zero emissions goal by 2070. Initiatives such as the FAME program offer manufacturers and consumers subsidies and incentives, accelerating EV uptake nationwide.

However, hurdles like minimal charging facilities, high costs, and consumer hesitation have slowed progress.

Accelerating India’s EV Shift

Supporting Government Programs

The government is promoting EV incentives with schemes like FAME subsidies and tax benefits. These initiatives incorporate incentives directly into pricing so consumers appreciate an EV's actual cost. For instance, buyers can easily tally potential savings from rebates and lower taxes. Streamlining these savings into purchases makes EVs more accessible to average Indian consumers.

Expanding Charging Infrastructure

The growth of a robust charging infrastructure is crucial for the widespread adoption of electric vehicles in India. Efforts are underway to establish extensive public charging networks in urban areas, along highways, and at popular destinations. These charging stations are being set up at diverse locations such as shopping malls, parking lots, petrol pumps, and office complexes, making it more convenient for EV owners to charge their vehicles while going about their daily routines.

Technological Advancements Driving EV Adoption

Battery Technology Improvements

The heart of any EV is its battery. Rapid advancements in battery technology address key concerns like range anxiety and charging times. Manufacturers are working on developing more efficient, longer-lasting, and faster-charing batteries. These innovations make EVs more practical for everyday use in diverse climates and terrains.

Smart EV Features

Modern EVs are not just about electric powertrains - they are becoming smart, connected vehicles. Features like regenerative braking, smart energy management systems, and over-the-air updates make electric vehicles more efficient and user-friendly. These technological advancements are helping to attract savvy consumers to the EV market.

The Role of Automotive Industry

Local manufacturing Push

The government’s ‘Make in India’ initiative encourages domestic EV production. Many automakers invest heavily in EV manufacturing capabilities, from small electric scooters to full-sized electric cars. The local manufacturing push is expected to reduce costs and make EVs more affordable for the mass market.

Research and Development

Indian automotive companies are ramping up their R&D efforts in EV technology. These efforts are positioning India as a potential global hub for EV innovation, from developing new EV platforms to innovating in battery management systems.

The Road Ahead: India’s EV Vision

As India's auto sector evolves, various players are enabling the transition to electric vehicles. Simplifying buying processes and furthering sustainability are key factors shaping the Indian market.

Ongoing plans include widening EV selection and supporting charging infrastructure development. With India emerging among the world's largest EV markets, the role of these initiatives in this transformation will only expand.

Conclusion

India's EV shift is transforming car ownership mindsets. Various stakeholders are leading the charge to make EVs affordable, convenient, and sensible for average Indian consumers. These efforts are pioneering a more sustainable automotive future in India by easing the buying process and championing eco-awareness.

In this evolving landscape, online car-buying platforms like ACKO Drive play a crucial role. ACKO Drive, for instance, simplifies the car-buying process by providing an online marketplace for cars, including electric vehicles. By offering easy comparisons, personalised financing options, and educational resources, such platforms are helping to accelerate EV adoption in India.

0 notes

Text

Hybrid Batteries Market Size, Share, and Future Forecast 2024-2032

Introduction:

Hybrid batteries are becoming increasingly popular as industries look for energy storage solutions that can meet the growing demand for high-efficiency, durable, and cost-effective power systems. These batteries combine multiple energy storage technologies to deliver superior performance, especially in applications such as electric vehicles, renewable energy storage, and grid stabilization. With an increasing focus on sustainable energy and the need to reduce carbon footprints, hybrid batteries are emerging as a viable option for both consumers and businesses alike.

Hybrid Batteries Market is expected to see substantial growth in the coming years. The development of hybrid batteries that combine the strengths of lithium-ion technology and supercapacitors allows for a balance of energy density, fast charging capabilities, and long-term reliability. The market is driven by growing investments in renewable energy, electric vehicles, and the increasing need for energy-efficient solutions in various sectors. As these batteries offer improved performance over traditional standalone energy storage systems, demand for them is expected to continue rising.

Market Trends:

Increasing Adoption in Electric Vehicles (EVs) – Hybrid batteries are increasingly being used in electric vehicles to provide both high power output and long-range performance.

Integration with Renewable Energy Systems – Hybrid batteries are being used to store energy from renewable sources such as solar and wind, ensuring more efficient energy management.

Technological Advancements – Continuous research and development are driving innovations in hybrid battery technology, enhancing energy density, lifespan, and charging speeds.

Growing Focus on Sustainability – With a global emphasis on reducing carbon emissions, hybrid batteries are emerging as a more sustainable option compared to traditional battery systems.

Integration with Grid Systems – Hybrid batteries are gaining attention for their role in energy storage and grid stabilization, particularly in smart grid systems.

Growth Drivers & Challenges:

Growth Drivers:

Increased adoption of electric vehicles and renewable energy solutions.

Rising demand for efficient energy storage solutions in industrial and residential sectors.

Technological innovations improving the performance and affordability of hybrid batteries.

Government incentives and policies promoting the use of energy-efficient solutions.

Challenges:

Despite the growing demand for hybrid batteries, challenges remain. High initial costs associated with the production and integration of hybrid battery systems can limit widespread adoption, especially in developing regions. Additionally, the need for specialized infrastructure to support hybrid battery systems, such as charging stations and grid connectivity, can pose logistical challenges. The technology’s complexity and the lack of standardized solutions across industries are also factors hindering the market’s growth. Furthermore, concerns about the availability of raw materials for battery production and recycling remain significant obstacles.

Future Outlook:

The Hybrid Batteries Market is expected to experience strong growth driven by innovations in battery technology, increased investments in electric vehicle infrastructure, and the rising need for renewable energy storage solutions. As hybrid batteries continue to evolve, with improvements in efficiency, cost-effectiveness, and environmental sustainability, the demand is likely to expand across multiple sectors. Particularly, the automotive industry and renewable energy sectors will be key drivers of market growth. Furthermore, advancements in charging infrastructure and government initiatives aimed at promoting clean energy solutions will provide additional momentum to the market.

Conclusion:

The Hybrid Batteries Market is poised for significant expansion, driven by the growing adoption of electric vehicles, renewable energy, and the need for advanced energy storage solutions. While challenges such as high initial costs and infrastructure limitations exist, the future outlook remains promising as technology advances and economies of scale improve. The market is expected to benefit from continued innovation and support from regulatory policies, positioning hybrid batteries as a key component in the transition to sustainable energy systems.

Read More Insights @ https://www.snsinsider.com/reports/hybrid-batteries-market-4678

Contact Us:

Akash Anand – Head of Business Development & Strategy

Phone: +1-415-230-0044 (US) | +91-7798602273 (IND)

0 notes

Text

Stainless Steel Round Bar Prices, News, Trend, Graph, Chart, Monitor and Forecast

The Stainless Steel Round Bar market has seen significant fluctuations in recent years, driven by various factors including global demand, raw material costs, and macroeconomic conditions. Stainless steel round bars are widely used across industries such as construction, automotive, aerospace, and manufacturing due to their strength, corrosion resistance, and durability. The pricing of these bars is influenced by several key components, including the costs of raw materials like nickel, chromium, and iron, as well as energy costs, production capacities, and international trade policies. As a result, stakeholders in the stainless steel market continuously monitor these factors to make informed decisions regarding production, procurement, and investment.

The demand for stainless steel round bars has been on an upward trajectory, primarily due to the growth in infrastructure projects worldwide. Developing economies in Asia, particularly China and India, have witnessed robust construction activities, which have fueled the need for high-quality stainless steel products. Moreover, the automotive sector's shift toward electric vehicles (EVs) has increased the demand for stainless steel components, given their application in battery casings, exhaust systems, and structural parts. As the demand for EVs continues to rise, the stainless steel round bar market is expected to benefit from this growth trend, contributing to an increase in prices over time.

Get Real time Prices for Stainless Steel Round Bar: https://www.chemanalyst.com/Pricing-data/stainless-steel-round-bar-1499

Raw material prices are among the most critical determinants of stainless steel round bar prices. Nickel, a key ingredient in stainless steel production, has experienced volatile price movements due to supply constraints and geopolitical tensions. Indonesia, one of the largest nickel producers, has implemented export restrictions to support its domestic processing industry, causing fluctuations in global nickel prices. Similarly, chromium and iron ore prices have seen variations based on mining activities, transportation costs, and changes in global demand. These raw material price shifts directly impact stainless steel round bar prices, creating challenges for manufacturers in maintaining stable pricing strategies.

Energy costs also play a significant role in determining the market prices of stainless steel round bars. Steel production is an energy-intensive process, with electricity and natural gas being major cost components. Global energy price trends, driven by geopolitical events, policy changes, and market dynamics, influence production costs for steel manufacturers. For instance, the energy crisis in Europe, triggered by geopolitical conflicts, has resulted in higher production costs, leading to increased prices for stainless steel products. As energy prices continue to fluctuate, manufacturers must adapt their production practices to manage costs effectively.

Global trade policies and economic conditions further impact stainless steel round bar prices. Tariffs, trade agreements, and import-export regulations affect the flow of raw materials and finished products across borders. For example, the United States' imposition of tariffs on steel imports has led to price adjustments in domestic markets, influencing supply and demand dynamics. Additionally, economic factors such as inflation, currency exchange rates, and interest rates have indirect effects on the market by influencing production costs and consumer purchasing power.

The COVID-19 pandemic brought unprecedented challenges to the stainless steel round bar market. Disruptions in supply chains, labor shortages, and fluctuating demand created a volatile pricing environment. However, the market demonstrated resilience, with recovery driven by increased infrastructure investments, especially in emerging markets. As countries implemented stimulus packages to revive their economies, the construction and manufacturing sectors received significant boosts, contributing to the stabilization and subsequent growth of stainless steel round bar prices.

Sustainability trends are also shaping the stainless steel round bar market. With growing environmental concerns and stringent regulations regarding carbon emissions, manufacturers are increasingly adopting eco-friendly practices. The use of recycled steel, energy-efficient production methods, and innovations in materials technology contribute to cost variations in the market. As the industry moves toward greener practices, production costs may rise initially but are expected to stabilize as technologies become more efficient and widely adopted.

Looking ahead, the stainless steel round bar market is expected to maintain a steady growth trajectory, driven by continued infrastructure development, technological advancements, and the expansion of various end-use industries. The rise in renewable energy projects, such as wind and solar farms, will further contribute to the demand for stainless steel components, given their application in turbine structures, support systems, and energy storage facilities. Additionally, advancements in manufacturing processes, such as the adoption of electric arc furnaces and digital monitoring systems, are likely to enhance production efficiency and influence market prices.

In conclusion, the pricing dynamics of stainless steel round bars are shaped by a complex interplay of factors, including raw material costs, energy prices, global demand, and trade policies. As industries continue to evolve and new applications for stainless steel emerge, market participants must stay informed about these influencing factors to navigate the competitive landscape successfully. The adoption of sustainable practices, technological innovations, and strategic investments will play crucial roles in determining the future trajectory of stainless steel round bar prices in the global market.

Get Real time Prices for Stainless Steel Round Bar: https://www.chemanalyst.com/Pricing-data/stainless-steel-round-bar-1499

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Stainless Steel Round Bar#Stainless Steel Round Bar Price#India#united kingdom#united states#Germany#business#research#chemicals#Technology#Market Research#Canada#Japan#China

0 notes

Text

Power Electronics Market to Reach $51.3 Billion by 2034 with Steady 5.3% CAGR

At a compound annual growth rate (CAGR) of 5.3%, the power electronics market is expected to develop significantly over the next ten years, from USD 30.7 billion in 2024 to USD 51.3 billion by 2034. Power electronics, which uses semiconductor devices to manage and convert electrical power, is becoming more and more popular across a range of sectors, especially in industrial automation, electric vehicles (EVs), and renewable energy.

With the ongoing shift towards clean energy and the rapid expansion of the EV market, power electronics are playing a critical role in improving energy efficiency and managing electrical power across multiple sectors. The market’s growth is underpinned by technological advancements in power semiconductor devices such as IGBTs and MOSFETs, as well as the growing demand for high-efficiency power solutions.

Request a Sample of this Report: https://www.futuremarketinsights.com/report-sample#5245502d47422d31303234

Key Takeaways from the Market Study

The Power Electronics Market is projected to grow at a CAGR of 5.3% from 2024 to 2034, reaching a valuation of US$ 51.3 billion by 2034.

The increasing penetration of renewable energy systems and electric vehicles is significantly boosting demand for power electronics.

Asia-Pacific is expected to dominate the market, driven by rapid industrialization and strong growth in the automotive and renewable energy sectors.

The energy & power and automotive segments will likely be key contributors to market growth over the forecast period.

Drivers and Opportunities

Several key factors are driving the growth of the Power Electronics Market. One of the primary drivers is the global push for renewable energy sources such as solar and wind power, which require power electronic devices to convert and manage energy efficiently. With many countries aiming to reduce carbon emissions, the installation of renewable energy systems is expected to surge, creating a significant demand for power electronics in inverters, converters, and power management systems.

The rise of electric vehicles (EVs) is another major growth driver. Power electronics are essential for the functioning of EVs, playing a critical role in battery management, motor control, and charging infrastructure. As EV adoption accelerates globally, the demand for power electronics is expected to rise sharply.

Additionally, the growing trend of industrial automation and the adoption of smart grids are presenting lucrative opportunities for market players. As industries increasingly adopt energy-efficient systems, power electronics are becoming essential for optimizing electrical power use in smart manufacturing and grid systems.

Components Insights

The Power Electronics Market is segmented based on components, including power discrete, power modules, and power ICs. Among these, power modules are expected to witness significant growth due to their widespread use in high-power applications such as solar inverters, EV powertrains, and industrial motor drives.

Power integrated circuits (ICs) are also gaining traction, particularly in consumer electronics and telecommunication devices, where compact and efficient power solutions are required. The demand for power discrete components, including diodes, transistors, and thyristors, is expected to remain strong in various industrial and automotive applications.

Application Insights

The Power Electronics Market finds extensive applications in industries such as automotive, energy & power, consumer electronics, and industrial automation. The automotive sector, especially in the context of electric and hybrid vehicles, is expected to be one of the largest contributors to market growth. Power electronics are used in electric vehicle charging systems, battery management systems, and traction inverters, all of which are vital for EV performance.

In the energy & power sector, the growing adoption of solar and wind energy solutions is driving the need for power converters and inverters, which manage the conversion of renewable energy into usable power. Additionally, the rise of smart grids is fueling the demand for advanced power electronics that improve energy distribution and efficiency.

The consumer electronics segment also represents a growing market, as power electronics are increasingly used in portable devices, smartphones, and laptops to improve battery performance and energy efficiency.

Deployment Insights

The Power Electronics Market is witnessing both on-premise and cloud-based deployments, with on-premise solutions dominating sectors like automotive and energy, where high power efficiency and reliable control are essential.

Cloud-based deployment is becoming increasingly popular in smart energy management systems and industrial automation, enabling real-time monitoring and control over power systems remotely. This trend is expected to grow, particularly in smart city projects and the integration of IoT-enabled devices.

Key Companies & Market Share Insights

Leading companies in the Power Electronics Market include Infineon Technologies AG, ON Semiconductor Corporation, Texas Instruments Incorporated, Mitsubishi Electric Corporation, Fuji Electric Co., Ltd., and Toshiba Corporation. These companies are focusing on developing innovative solutions that cater to the rising demand for high-efficiency power devices across multiple industries.

The competitive landscape is characterized by strategic partnerships, mergers, and acquisitions. For example, Infineon Technologies AG expanded its product portfolio by acquiring Cypress Semiconductor, which enhanced its capabilities in power management solutions. ON Semiconductor has been investing heavily in research and development to produce energy-efficient devices aimed at the automotive and industrial sectors.

Recent Developments

Mitsubishi Electric introduced a new line of SiC (silicon carbide) power modules aimed at improving the efficiency of power inverters in EVs and renewable energy systems.

Texas Instruments launched an innovative range of GaN (gallium nitride) power transistors that offer superior performance in high-power applications, including EVs and industrial automation systems.

Fuji Electric expanded its production capacity for IGBT modules, which are in high demand for solar power installations and electric vehicles, to address the increasing global demand for energy-efficient solutions.

0 notes

Text

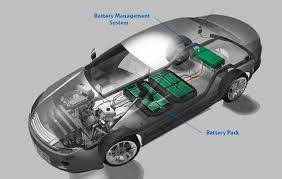

Automotive Battery Management System Market To Witness the Highest Growth Globally in Coming Years

The report begins with an overview of the Automotive Battery Management System Market 2025 Size and presents throughout its development. It provides a comprehensive analysis of all regional and key player segments providing closer insights into current market conditions and future market opportunities, along with drivers, trend segments, consumer behavior, price factors, and market performance and estimates. Forecast market information, SWOT analysis, Automotive Battery Management System Market scenario, and feasibility study are the important aspects analyzed in this report.

The Automotive Battery Management System Market is experiencing robust growth driven by the expanding globally. The Automotive Battery Management System Market is poised for substantial growth as manufacturers across various industries embrace automation to enhance productivity, quality, and agility in their production processes. Automotive Battery Management System Market leverage robotics, machine vision, and advanced control technologies to streamline assembly tasks, reduce labor costs, and minimize errors. With increasing demand for customized products, shorter product lifecycles, and labor shortages, there is a growing need for flexible and scalable automation solutions. As technology advances and automation becomes more accessible, the adoption of automated assembly systems is expected to accelerate, driving market growth and innovation in manufacturing. Automotive Battery Management System Market Size, Share & Industry Analysis, By Type (Lithium-ion, Lead Acid, Nickel-based), By Connection Topology (Centralized , Distributed , Modular), By Vehicle type (Electric Vehicles, E-bikes) And Regional Forecast 2021-2028

Get Sample PDF Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/105479

Key Strategies

Key strategies in the Automotive Battery Management System Market revolve around optimizing production efficiency, quality, and flexibility. Integration of advanced robotics and machine vision technologies streamlines assembly processes, reducing cycle times and error rates. Customization options cater to diverse product requirements and manufacturing environments, ensuring solution scalability and adaptability. Collaboration with industry partners and automation experts fosters innovation and addresses evolving customer needs and market trends. Moreover, investment in employee training and skill development facilitates seamless integration and operation of Automotive Battery Management System Market . By prioritizing these strategies, manufacturers can enhance competitiveness, accelerate time-to-market, and drive sustainable growth in the Automotive Battery Management System Market .

Major Automotive Battery Management System Market Manufacturers covered in the market report include:

Some of the major companies that are present in the automotive battery management system market include Thyssenkrupp AG, Nippon Steel Integrated Battery Management LLC, Braynt Racing Inc., Arrow Precision Ltd., Maschinenfabrik Alfing Kessler GmbH, Mahindra CIE, Tianrun Battery Management Co., Ltd., among others.

Owing to this, many Battery Management manufacturers are developing advanced Battery Management with improved fatigue strength, reliability, and quality. Also, the crankshafts are manufactured with the latest trend of steelmaking processes by materials with high strength, and this factor is also expected to drive the automotive Battery Management market.

Trends Analysis

The Automotive Battery Management System Market is experiencing rapid expansion fueled by the manufacturing industry's pursuit of efficiency and productivity gains. Key trends include the adoption of collaborative robotics and advanced automation technologies to streamline assembly processes and reduce labor costs. With the rise of Industry 4.0 initiatives, manufacturers are investing in flexible and scalable Automotive Battery Management System Market capable of handling diverse product portfolios. Moreover, advancements in machine vision and AI-driven quality control are enhancing production throughput and ensuring product consistency. The emphasis on sustainability and lean manufacturing principles is driving innovation in energy-efficient and eco-friendly Automotive Battery Management System Market Solutions.

Regions Included in this Automotive Battery Management System Market Report are as follows:

North America [U.S., Canada, Mexico]

Europe [Germany, UK, France, Italy, Rest of Europe]

Asia-Pacific [China, India, Japan, South Korea, Southeast Asia, Australia, Rest of Asia Pacific]

South America [Brazil, Argentina, Rest of Latin America]

Middle East & Africa [GCC, North Africa, South Africa, Rest of the Middle East and Africa]

Significant Features that are under offering and key highlights of the reports:

- Detailed overview of the Automotive Battery Management System Market .

- Changing the Automotive Battery Management System Market dynamics of the industry.

- In-depth market segmentation by Type, Application, etc.

- Historical, current, and projected Automotive Battery Management System Market size in terms of volume and value.

- Recent industry trends and developments.

- Competitive landscape of the Automotive Battery Management System Market .

- Strategies of key players and product offerings.

- Potential and niche segments/regions exhibiting promising growth.

Frequently Asked Questions (FAQs):

► What is the current market scenario?

► What was the historical demand scenario, and forecast outlook from 2025 to 2032?

► What are the key market dynamics influencing growth in the Global Automotive Battery Management System Market ?

► Who are the prominent players in the Global Automotive Battery Management System Market ?

► What is the consumer perspective in the Global Automotive Battery Management System Market ?

► What are the key demand-side and supply-side trends in the Global Automotive Battery Management System Market ?

► What are the largest and the fastest-growing geographies?

► Which segment dominated and which segment is expected to grow fastest?

► What was the COVID-19 impact on the Global Automotive Battery Management System Market ?

Table Of Contents:

1 Market Overview

1.1 Automotive Battery Management System Market Introduction

1.2 Market Analysis by Type

1.3 Market Analysis by Applications

1.4 Market Analysis by Regions

1.4.1 North America (United States, Canada and Mexico)

1.4.1.1 United States Market States and Outlook

1.4.1.2 Canada Market States and Outlook

1.4.1.3 Mexico Market States and Outlook

1.4.2 Europe (Germany, France, UK, Russia and Italy)

1.4.2.1 Germany Market States and Outlook

1.4.2.2 France Market States and Outlook

1.4.2.3 UK Market States and Outlook

1.4.2.4 Russia Market States and Outlook

1.4.2.5 Italy Market States and Outlook

1.4.3 Asia-Pacific (China, Japan, Korea, India and Southeast Asia)

1.4.3.1 China Market States and Outlook

1.4.3.2 Japan Market States and Outlook

1.4.3.3 Korea Market States and Outlook

1.4.3.4 India Market States and Outlook

1.4.3.5 Southeast Asia Market States and Outlook

1.4.4 South America, Middle East and Africa

1.4.4.1 Brazil Market States and Outlook

1.4.4.2 Egypt Market States and Outlook

1.4.4.3 Saudi Arabia Market States and Outlook

1.4.4.4 South Africa Market States and Outlook

1.5 Market Dynamics

1.5.1 Market Opportunities

1.5.2 Market Risk

1.5.3 Market Driving Force

2 Manufacturers Profiles

Continued…

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Contact Us:

Fortune Business Insights™ Pvt. Ltd.

US:+18339092966

UK: +448085020280

APAC: +91 744 740 1245

#Automotive Battery Management System Market#Automotive Battery Management System Market Share#Automotive Battery Management System Market Size#Automotive Battery Management System Market Trends

0 notes

Text

Automotive Over-The-Air (OTA) Market Revenue Analysis: Growth, Share, Value, Scope, and Insights

"Automotive Over-The-Air (OTA) Market Size And Forecast by 2030

The revenue analysis and revenue forecast for the Automotive Over-The-Air (OTA) Market reveal a promising upward trajectory, driven by innovative product offerings, strategic collaborations, and expanding applications. With leaders in the industry focusing on enhanced customer experiences and operational efficiency, the market continues to present lucrative opportunities for growth. The report provides a detailed overview of these trends and their implications for the market’s future.

Data Bridge Market Research analyses that the Global Automotive Over-The-Air (OTA) Market which was USD 4.13 Billion in 2022 is expected to reach USD 20.97 Billion by 2030 and is expected to undergo a CAGR of 22.50% during the forecast period of 2022 to 2030

Get a Sample PDF of Report - https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-automotive-ota-market

Which are the top companies operating in the Automotive Over-The-Air (OTA) Market?

The Top 10 Companies in Automotive Over-The-Air (OTA) Market include well-established names that lead the industry with their innovative products and strong market presence. These companies are recognized for their quality, reliability, and ability to meet the evolving needs of consumers. each known for their significant contributions and competitive strategies that drive growth and maintain their leadership in the industry.

**Segments**

- **By Technology**: The automotive OTA market can be segmented based on technology into Firmware Over-the-Air (FOTA) and Software Over-the-Air (SOTA). FOTA allows for updating the embedded software in Electronic Control Units (ECUs), enhancing vehicle performance and functionality. On the other hand, SOTA focuses on updating applications and features that are controlled by software layers.

- **By Application**: The market can also be segmented by application, including vehicle health monitoring, predictive maintenance, infotainment, telematics, and others. The adoption of OTA updates for vehicle health monitoring and predictive maintenance is increasing to prevent system failures and reduce maintenance costs, driving market growth.

- **By Vehicle Type**: In terms of vehicle type, the automotive OTA market is segmented into passenger cars and commercial vehicles. The passenger car segment holds a significant share due to the increasing integration of advanced electronic systems and connected features in modern vehicles, necessitating regular software updates and enhancements.

- **By Electric Vehicle Type**: With the rise of electric vehicles (EVs), the market can be further segmented based on EV type, including Battery Electric Vehicles (BEVs) and Plug-in Hybrid Electric Vehicles (PHEVs). OTA updates are crucial for EVs to ensure optimal battery management, performance, and range, leading to a substantial demand for OTA solutions in the electric vehicle segment.

**Market Players**

- **Airbiquity, Inc.**: A leading provider of connected vehicle services and OTA software solutions, Airbiquity offers a comprehensive OTA platform that enables automakers to securely manage and update vehicle software remotely.

- **Blackberry QNX**: Known for its expertise in secure embedded software solutions, Blackberry QNX provides OTA update capabilities for automotive ECUs to ensure safe and reliable software updates over-the-air.

- **HARMAN International**: As a prominent player in the automotive infotainment and connectivity space, HARMAN International offers OTA solutions that enable seamless software updates for in-vehicle entertainment systems and telematics features.

- **Movimento**: Specializing in OTA technology for automotive manufacturers, Movimento provides secure and efficient software update solutions for vehicle ECUs, enhancing performance, security, and user experience.

The global automotive OTA market is poised for significant growth, driven by the increasing complexity of vehicle electronics, rising demand for connected features, and the transition towards electric vehicles. OTA technology offers numerous benefits, including cost-effective updates, improved cybersecurity, enhanced user experience, and compliance with evolving regulatory standards. Market players are focusing on developing advanced OTA platforms that ensure secure and efficient software updates for a wide range of automotive applications, propelling the market forward.

https://www.databridgemarketresearch.com/reports/global-automotive-ota-marketThe global automotive OTA market is witnessing strong growth propelled by the increasing digitalization and connectivity in vehicles. As automakers continue to integrate advanced electronic systems and connected features into modern vehicles, the demand for OTA solutions is on the rise. Automotive OTA technology allows for efficient and secure software updates over-the-air, enabling automakers to enhance vehicle performance, functionality, and user experience with minimal downtime and cost. The market is segmented based on technology, application, vehicle type, and electric vehicle type, reflecting the diverse needs and requirements within the automotive industry.

In terms of technology segmentation, Firmware Over-the-Air (FOTA) and Software Over-the-Air (SOTA) play key roles in updating embedded software and software layers in vehicles, respectively. FOTA updates are crucial for enhancing Electronic Control Units (ECUs) and overall vehicle performance, while SOTA focuses on updating applications and features controlled by software layers. This segmentation highlights the versatility and flexibility of OTA technology in addressing different aspects of vehicle software management and updates.

When considering the application segmentation of the automotive OTA market, key segments such as vehicle health monitoring, predictive maintenance, infotainment, and telematics drive market growth. The adoption of OTA updates for vehicle health monitoring and predictive maintenance is particularly significant as automakers seek to prevent system failures, reduce maintenance costs, and improve overall operational efficiency. The growing emphasis on connected features and digital services in vehicles further underscores the importance of OTA solutions in enhancing the user experience and ensuring seamless functionality.

Another important segmentation factor is based on vehicle type, with passenger cars and commercial vehicles representing distinct segments within the automotive OTA market. The passenger car segment holds a significant share due to the increasing integration of advanced electronic systems and connected features in modern vehicles. As automakers strive to deliver innovative features and services to consumers, the need for regular software updates and enhancements becomes paramount, driving the demand for OTA solutions in the passenger car segment.

With the rise of electric vehicles (EVs), the market can be further segmented based on EV type, including Battery Electric Vehicles (BEVs) and Plug-in Hybrid Electric Vehicles (PHEVs). OTA updates play a crucial role in ensuring optimal battery management, performance, and range in EVs, highlighting the importance of advanced software solutions in the electric vehicle segment. Overall, the segmentation of the automotive OTA market by technology, application, vehicle type, and electric vehicle type provides a comprehensive view of the diverse opportunities and challenges in the industry.

In conclusion, the global automotive OTA market is experiencing robust growth driven by the increasing complexity of vehicle electronics, the demand for connected features, and the transition towards electric vehicles. Market players are focused on developing advanced OTA platforms that offer secure and efficient software updates to meet the evolving needs of automakers and consumers. The future of the automotive OTA market looks promising, with continued innovation and technological advancements shaping the industry landscape.**Segments**

Global Automotive Over-The-Air (OTA) Market is segmented by Technology into Firmware and Software. The Firmware Over-the-Air (FOTA) technology focuses on updating the embedded software in Electronic Control Units (ECUs), enhancing vehicle performance and functionality. On the other hand, Software Over-the-Air (SOTA) technology is geared towards updating applications and features controlled by software layers within vehicles. This segmentation reflects the versatility of OTA technology in managing and updating different aspects of vehicle software to improve overall performance and user experience.

In terms of Vehicle Type segmentation, the market is categorized into Passenger Cars, Light Commercial Vehicles, and Heavy Commercial Vehicles. Passenger cars hold a significant share in the market due to the increasing integration of advanced electronic systems and connected features, necessitating regular software updates and enhancements to meet consumer demands and regulatory standards. Light and Heavy Commercial Vehicles also contribute to the market growth as they incorporate advanced technologies for improved efficiency and performance, driving the need for OTA solutions to ensure smooth operations.

The market segmentation by Propulsion includes Internal Combustion Engine vehicles and Electric vehicles. As the automotive industry shifts towards sustainability and electrification, Electric vehicles play a crucial role in the market growth. OTA updates are essential for Electric Vehicles (EVs) to optimize battery management, performance, and range, contributing to the increasing demand for advanced software solutions in the electric vehicle segment. Internal Combustion Engine vehicles also benefit from OTA technology to enhance operational efficiency and performance.

The Application segmentation of the automotive OTA market includes Electronic Control Unit (ECU), Infotainment, Safety & Security, Telematics Control Unit (TCU), and others. Each application segment plays a vital role in driving market growth, with a focus on enhancing vehicle functionality, safety, and connectivity. The adoption of OTA updates for ECU management, infotainment systems, and telematics features is crucial for automakers to provide seamless software enhancements and improve user experience in modern vehicles.

Electric Vehicle Type segmentation further classifies the market into Battery Electric Vehicles (BEVs), Hybrid Electric Vehicles, and Plug-In Hybrid Electric Vehicles (PHEVs). The growing popularity of electric propulsion systems in vehicles leads to an increased demand for OTA solutions tailored to the unique requirements of different electric vehicle types. BEVs and PHEVs benefit significantly from OTA updates to optimize performance, battery life, and overall efficiency, driving innovation and development in the electric vehicle segment.

**Market Players**

- DENSO CORPORATION (Japan) - Aptiv (U.S.) - Continental AG (Germany) - Garmin Ltd (U.S.) - Robert Bosch GmbH (Germany) - HARMAN International (U.S.) - Infineon Technologies AG (Germany) - BlackBerry Limited (Canada) - Lear (U.S.) - Qualcomm Technologies, Inc. (U.S.) - Verizon (U.S.) - NVIDIA Corporation (U.S.) - Xevo (U.S.) - Airbiquity Inc. (U.S.) - HERE (Netherlands)

The competitive landscape of the global automotive OTA market includes key players offering a wide range of OTA solutions and services to cater to the evolving needs of automakers and consumers. Major market players focus on innovation and technological advancements to develop advanced OTA platforms that ensure secure, efficient, and cost-effective software updates for various automotive applications. Collaborations, partnerships, and product launches are common strategies among market players to strengthen their market presence and expand their product offerings, driving competition and market growth in the automotive OTA sector.

Explore Further Details about This Research Automotive Over-The-Air (OTA) Market Report https://www.databridgemarketresearch.com/reports/global-automotive-ota-market

Key Insights from the Global Automotive Over-The-Air (OTA) Market :

Comprehensive Market Overview: The Automotive Over-The-Air (OTA) Market is expanding rapidly, driven by innovation and growing global demand across key regions.

Industry Trends and Projections: Automation, sustainability, and digital transformation are key trends, with strong growth projected over the next few years.

Emerging Opportunities: New growth opportunities are emerging in eco-friendly technologies and untapped regional markets.

Focus on R&D: Companies are heavily investing in R&D to develop next-gen technologies like AI, IoT, and sustainable solutions.

Leading Player Profiles: Market leaders, such as Company A and Company B, dominate due to strong portfolios and global distribution.

Market Composition: The market is fragmented, with both large corporations and emerging startups driving innovation.

Revenue Growth: The market is experiencing steady revenue growth, driven by both consumer demand and industrial applications.

Commercial Opportunities: Key commercial opportunities lie in expanding into emerging markets and forming strategic partnerships.

Find Country based languages on reports:

https://www.databridgemarketresearch.com/jp/reports/global-automotive-ota-markethttps://www.databridgemarketresearch.com/zh/reports/global-automotive-ota-markethttps://www.databridgemarketresearch.com/ar/reports/global-automotive-ota-markethttps://www.databridgemarketresearch.com/pt/reports/global-automotive-ota-markethttps://www.databridgemarketresearch.com/de/reports/global-automotive-ota-markethttps://www.databridgemarketresearch.com/fr/reports/global-automotive-ota-markethttps://www.databridgemarketresearch.com/es/reports/global-automotive-ota-markethttps://www.databridgemarketresearch.com/ko/reports/global-automotive-ota-markethttps://www.databridgemarketresearch.com/ru/reports/global-automotive-ota-market

Data Bridge Market Research:

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC: +653 1251 977

Email:- [email protected]"

0 notes

Text

Automotive Batteries - Technology, Trends, and Challenges

The evolution of automotive batteries is marked by significant technological advancements that continue to shape the power in vehicles. From traditional lead-acid batteries to lithium-ion solutions and other innovations, the automotive battery sector is progressing toward a more sustainable future in the transport industry.

This blog delves into the technology behind the essential battery components, current trends, and challenges faced by the industry, offering a glimpse into what lies ahead.

Understanding the Basics of Battery Technology

Automotive batteries are the core component of modern vehicles, providing the energy required to start engines, power accessories, and drive electric vehicles (EVs). What are the main types of automotive batteries? Automotive batteries are primarily categorized into lead-acid and lithium-ion types, with emerging technologies such as solid-state gaining traction.

Lead-acid batteries, a long-standing choice, are cost-effective and reliable, making them ideal for traditional internal combustion engine (ICE) vehicles. However, their relatively low energy density and limited lifespan pose challenges.

On the other hand, lithium-ion batteries, known for their high energy density and performance, have become the standard for EVs due to their ability to store more energy in a lighter package. Emerging technologies, such as solid-state and flow batteries, promise even greater efficiency and safety, signaling a transformative shift in battery design.

In the context of battery charge and discharge cycles, batteries rely on chemical reactions to store and release energy. The capacity and output of a battery depend on factors such as its chemistry, size, and operating conditions. External influences, including temperature, charging habits, and usage patterns, also play a crucial role in determining a battery’s performance and lifespan.