#Battery Control Market Trends

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has a 66 index score for customer satisfaction in the US.

Text

Battery Control Technology Market Business Overview and Upcoming Outlook 2032

Overview of the Battery Control Technology Market:

Battery Control Technology Market Overview: The battery control technology market encompasses various technologies and solutions designed to monitor, manage, and optimize the performance of batteries used in a wide range of applications, including consumer electronics, electric vehicles, renewable energy storage systems, and industrial equipment. These technologies play a crucial role in extending battery life, improving efficiency, ensuring safety, and enhancing overall performance.

Growth Trends and Factors Driving Demand:

Rising Adoption of Electric Vehicles (EVs): The increasing shift towards electric vehicles as a more environmentally friendly transportation option has led to a growing demand for advanced battery control technologies. These technologies are essential for managing battery health, charging/discharging cycles, and thermal management in EVs.

Renewable Energy Storage: The integration of renewable energy sources like solar and wind power into the grid has created a need for efficient energy storage solutions. Battery control technologies are crucial for optimizing energy storage systems, enabling smooth power delivery, and ensuring grid stability.

Consumer Electronics: The proliferation of smartphones, laptops, wearables, and other portable electronic devices has driven the demand for high-performance batteries with advanced control and management features, such as fast charging and power optimization.

Industrial Applications: Industries such as telecommunications, data centers, and manufacturing rely on backup power solutions and energy storage systems. Battery control technologies are used to ensure reliable power supply during outages and manage energy consumption.

IoT and Connectivity: The Internet of Things (IoT) and connected devices require efficient and reliable battery control technologies to optimize power consumption, enhance device performance, and enable remote monitoring and management.

Focus on Battery Safety: Safety is a critical concern in battery applications. Battery control technologies help monitor battery conditions, detect potential issues like overcharging and overheating, and implement safety measures to prevent accidents.

Advancements in Battery Management Systems (BMS): Battery management systems have evolved to include sophisticated control algorithms, real-time monitoring, predictive maintenance capabilities, and communication interfaces for seamless integration into various applications.

Research and Development: Ongoing research and development efforts aim to improve battery chemistries, enhance energy density, and develop more efficient battery control technologies, thereby driving further demand in the market

Battery control technology offers several key benefits across various industries and applications. Here are some of the key benefits:

Enhanced Battery Performance: Battery control technology helps optimize battery performance by actively managing charging and discharging cycles, maintaining optimal voltage levels, and preventing overcharging or over-discharging. This results in improved battery efficiency, longer lifespan, and better overall performance.

Extended Battery Life: By monitoring and controlling critical battery parameters, such as temperature and state of charge, battery control technology can help extend the operational life of batteries. This is particularly important in applications like electric vehicles and renewable energy storage systems, where battery replacement costs can be significant.

Improved Safety: Battery control technology includes safety features such as overvoltage protection, overcurrent protection, and thermal management. These safety mechanisms help prevent battery damage, reduce the risk of fires or explosions, and enhance overall system safety.

Optimized Charging and Discharging: Smart battery control systems can dynamically adjust the charging and discharging rates based on real-time conditions, load requirements, and user preferences. This ensures efficient energy utilization and prevents situations where batteries are stressed or underutilized.

Fast Charging: Battery control technology enables faster charging without compromising safety or battery health. It can manage high-power charging processes while maintaining safe temperature levels and preventing degradation.

Intelligent Energy Management: In applications like renewable energy storage systems and microgrids, battery control technology allows for intelligent energy management. It enables the storage and release of energy at optimal times, maximizing the utilization of renewable energy sources and reducing reliance on conventional power sources.

Remote Monitoring and Management: Many battery control systems are equipped with remote monitoring and management capabilities. This enables real-time tracking of battery performance, health, and status, allowing for proactive maintenance and minimizing downtime.

Predictive Maintenance: Advanced battery control technology can analyze data over time to predict battery health and performance degradation. This enables operators to schedule maintenance and replacement activities before major issues arise, reducing unexpected failures and downtime.

Integration with IoT and Smart Systems: Battery control technology can integrate with Internet of Things (IoT) platforms and smart systems, allowing for seamless communication, data sharing, and coordination with other devices and applications.

Environmental Impact: By optimizing battery usage and extending their lifespan, battery control technology contributes to reducing electronic waste and conserving valuable resources. Additionally, in applications like electric vehicles and renewable energy storage, it supports the transition to cleaner and more sustainable energy solutions.

Cost Savings: Improved battery performance and extended lifespan lead to reduced replacement and maintenance costs. Efficient energy utilization and demand-side management can also result in cost savings, especially in industrial and commercial applications.

We recommend referring our Stringent datalytics firm, industry publications, and websites that specialize in providing market reports. These sources often offer comprehensive analysis, market trends, growth forecasts, competitive landscape, and other valuable insights into this market.

By visiting our website or contacting us directly, you can explore the availability of specific reports related to this market. These reports often require a purchase or subscription, but we provide comprehensive and in-depth information that can be valuable for businesses, investors, and individuals interested in this market.

“Remember to look for recent reports to ensure you have the most current and relevant information.”

Click Here, To Get Free Sample Report: https://stringentdatalytics.com/sample-request/battery-control-technology-market/12283/

Market Segmentations:

Global Battery Control Technology Market: By Company

• A123 systems LLC.

• Ford Motor Co.

• GE Energy LCC.

• Toyota Motor Corp.

• Sony Electronic Inc.

• Samsung SID Co. Ltd.

• Sanyo electric Co. Ltd.

• Panasonic Corp.

• L.G Chem LTD.

• Honda Motor Co. Ltd.

Global Battery Control Technology Market: By Type

• Smart Batteries

• Chargers

• Conditioners.

Global Battery Control Technology Market: By Application

• Automotive

• Traction, Marine and Aviation

• Portable Products

• Stationary (UPS, Emergency, Remote)

• On-road Electric Vehicles

Global Battery Control Technology Market: Regional Analysis

The regional analysis of the global Battery Control Technology market provides insights into the market's performance across different regions of the world. The analysis is based on recent and future trends and includes market forecast for the prediction period. The countries covered in the regional analysis of the Battery Control Technology market report are as follows:

North America: The North America region includes the U.S., Canada, and Mexico. The U.S. is the largest market for Battery Control Technology in this region, followed by Canada and Mexico. The market growth in this region is primarily driven by the presence of key market players and the increasing demand for the product.

Europe: The Europe region includes Germany, France, U.K., Russia, Italy, Spain, Turkey, Netherlands, Switzerland, Belgium, and Rest of Europe. Germany is the largest market for Battery Control Technology in this region, followed by the U.K. and France. The market growth in this region is driven by the increasing demand for the product in the automotive and aerospace sectors.

Asia-Pacific: The Asia-Pacific region includes Singapore, Malaysia, Australia, Thailand, Indonesia, Philippines, China, Japan, India, South Korea, and Rest of Asia-Pacific. China is the largest market for Battery Control Technology in this region, followed by Japan and India. The market growth in this region is driven by the increasing adoption of the product in various end-use industries, such as automotive, aerospace, and construction.

Middle East and Africa: The Middle East and Africa region includes Saudi Arabia, U.A.E, South Africa, Egypt, Israel, and Rest of Middle East and Africa. The market growth in this region is driven by the increasing demand for the product in the aerospace and defense sectors.

South America: The South America region includes Argentina, Brazil, and Rest of South America. Brazil is the largest market for Battery Control Technology in this region, followed by Argentina. The market growth in this region is primarily driven by the increasing demand for the product in the automotive sector.

Visit Report Page for More Details: https://stringentdatalytics.com/reports/battery-control-technology-market/12283/

Reasons to Purchase Battery Control Technology Market Report:

• To gain insights into market trends and dynamics: this reports provide valuable insights into industry trends and dynamics, including market size, growth rates, and key drivers and challenges.

• To identify key players and competitors: this research reports can help businesses identify key players and competitors in their industry, including their market share, strategies, and strengths and weaknesses.

• To understand consumer behavior: this research reports can provide valuable insights into consumer behavior, including their preferences, purchasing habits, and demographics.

• To evaluate market opportunities: this research reports can help businesses evaluate market opportunities, including potential new products or services, new markets, and emerging trends.

• To make informed business decisions: this research reports provide businesses with data-driven insights that can help them make informed business decisions, including strategic planning, product development, and marketing and advertising strategies.

About US:

Stringent Datalytics offers both custom and syndicated market research reports. Custom market research reports are tailored to a specific client's needs and requirements. These reports provide unique insights into a particular industry or market segment and can help businesses make informed decisions about their strategies and operations.

Syndicated market research reports, on the other hand, are pre-existing reports that are available for purchase by multiple clients. These reports are often produced on a regular basis, such as annually or quarterly, and cover a broad range of industries and market segments. Syndicated reports provide clients with insights into industry trends, market sizes, and competitive landscapes. By offering both custom and syndicated reports, Stringent Datalytics can provide clients with a range of market research solutions that can be customized to their specific needs

Contact US:

Stringent Datalytics

Contact No - +1 346 666 6655

Email Id - [email protected]

Web - https://stringentdatalytics.com/

#Battery Control Technology#Energy Storage Solutions#Battery Management Systems#Smart Battery Technology#Battery Monitoring#Battery Control Software#Energy Management#Battery Efficiency#Battery Safety#Battery Performance Optimization#Energy Storage Management#Battery Control Innovations#Battery Control Algorithms#Grid Integration#Renewable Energy Integration#Battery Charging Technology#Battery Discharging Technology#Battery Control Market Trends#Battery Control Industry#Global Energy Market#Energy Storage Trends#Battery Technology Advancements.

0 notes

Text

The Road Ahead – Navigating the Future of the Automotive Industry

🌍 Market Overview

The Global automotive industry Market Size is evolving rapidly, driven by technological advancements, sustainability initiatives, and changing consumer preferences. Automakers are embracing electric vehicles (EVs), autonomous technology, and digital transformation to stay ahead.

Download a Free Sample : https://rb.gy/iwh4in

📈 Growth Drivers

✅ Electrification – Rise in EV adoption due to sustainability goals and government incentives. ✅ Autonomous Vehicles – Investments in self-driving technology from major players like Tesla, Waymo, and GM. ✅ Connectivity & IoT – Smart features, in-car AI, and enhanced safety tech. ✅ Urbanization & Mobility Services – Growth of ride-sharing and subscription-based vehicle models.

⚠️ Key Challenges & Factors

🚧 Chip Shortages – Semiconductor supply chain disruptions affecting production. 🚧 Regulatory Hurdles – Stricter emissions policies worldwide. 🚧 Consumer Preferences – Shift towards SUVs and electric mobility. 🚧 Raw Material Costs – Fluctuations in lithium, nickel, and other EV battery components.

🔥 Emerging Trends

🔹 EV Market Boom – Tesla, Rivian, and legacy automakers expanding electric fleets. 🔹 Hydrogen Fuel Cell Tech – Toyota & Hyundai leading innovations. 🔹 Sustainable Manufacturing – Recycling initiatives & carbon-neutral plants. 🔹 Software-Defined Vehicles – Over-the-air (OTA) updates & AI-driven enhancements.

Related Urls :

https://www.sphericalinsights.com/reports/automotive-blockchain-market https://www.sphericalinsights.com/reports/china-halal-logistics-market

#AutomotiveIndustry 🚗 |#EVRevolution ⚡ |#CarTrends 🚘 |#FutureOfMobility 🌍 |#AutoTech 🔧 |#ElectricVehicles 🔋 |#AutonomousCars 🤖 |#GreenMobility 🌱 |#CarManufacturing 🏭 |#SmartCars 📡 |#SustainableTransport 🚀 |#AutoInnovation 🔥 |#NextGenVehicles 🚙 |#AutomotiveMarket 📈 |#MobilitySolutions 🚦

2 notes

·

View notes

Text

China Recruitment Results 2025: Trends, Insights, and Analysis

As the arena's second-biggest economy, China is still a primary player within the international exertions marketplace. The today's recruitment effects from 2025 display key trends and insights across industries, demographics, and regions. Companies, activity seekers, and policymakers alike can gain from know-how these shifts, as they replicate China's evolving economic landscape, expertise priorities, and marketplace demands.

Recruitment Process In China

1. Strong Recovery in Recruitment Activity

In 2025, China’s recruitment market noticed a incredible rebound, following years of pandemic-associated disruptions and financial uncertainty. According to statistics from a couple of human resources and exertions market tracking agencies, general job openings in China increased through about 12% 12 months-on-12 months. This growth turned into frequently driven via sectors which include generation, renewable power, superior production, and modern-day offerings, which includes finance and healthcare.

The surge in recruitment pastime is basically attributed to China’s push closer to monetary modernization and innovation, aligning with the government’s "14th Five-Year Plan" and its vision for incredible development. Furthermore, easing COVID-19 restrictions inside the past two years has revitalized domestic demand, especially in urban centers like Shanghai, Shenzhen, and Beijing, wherein expertise demand stays high.

2. Sector-by using-Sector Breakdown

Technology Sector

China’s tech enterprise stays one in every of the most important recruiters in 2025, with hiring increasing with the aid of 15% in comparison to 2024. Companies running in regions such as synthetic intelligence (AI), semiconductor production, cloud computing, and 5G/6G network infrastructure are main the demand. In precise, the AI and automation sectors skilled document-breaking recruitment, as agencies throughout numerous industries put into effect virtual transformation techniques.

Manufacturing and New Energy

Advanced manufacturing—together with robotics, aerospace, and electric vehicles (EVs)—recorded an eleven% uptick in hiring. With China striving to grow to be a global leader in EV production and inexperienced technology, recruitment in battery generation, renewable energy engineering, and environmental technology has also elevated. The expansion of sun and wind electricity initiatives in inland provinces which include Inner Mongolia and Xinjiang has opened new activity opportunities out of doors main metropolitan hubs.

Financial and Business Services

Financial offerings confirmed a moderate but consistent 7% increase in hiring, in particular in fintech, funding banking, and risk management roles. The fast adoption of virtual finance systems and the growth of inexperienced finance initiatives contributed to this upward fashion. Similarly, prison and compliance departments saw a surge in call for, as stricter regulatory requirements and international exchange dynamics precipitated corporations to strengthen their internal controls.

Healthcare and Life Sciences

China’s growing old populace and the authorities's focus on enhancing healthcare infrastructure have boosted hiring within the medical and pharmaceutical sectors. Hospitals, biotech firms, and healthtech startups elevated recruitment via nine% yr-on-12 months. Special emphasis become placed on roles associated with scientific research, clinical trials, and public fitness management, reflecting China's ambitions to beautify its healthcare resilience.

Three. Regional Disparities in Recruitment

While Tier 1 towns like Beijing, Shanghai, Guangzhou, and Shenzhen hold to dominate in phrases of activity vacancies, there was a major uptick in hiring in Tier 2 and Tier 3 towns, which includes Chengdu, Hangzhou, Xi’an, and Suzhou. The government’s urbanization strategy and nearby improvement rules are riding this shift. Inland provinces and less-advanced regions are actually attracting extra investment, main to activity advent in industries along with logistics, e-trade, and smart production.

This geographic diversification is also related to the upward thrust of far off work, as agencies come to be more bendy in hiring talent from diverse locations. As a end result, skilled specialists are now not limited to standard financial hubs and are finding competitive possibilities in rising cities.

4. Recruitment Challenges: Skills Gaps and Talent Shortages

Despite the overall high quality recruitment results, several sectors pronounced continual demanding situations, specially regarding skills shortages in high-tech and specialised fields. For instance, the semiconductor enterprise keeps to stand a essential gap in skilled engineers and researchers, while the inexperienced electricity area is struggling to find sufficient skilled task managers and technical experts.

Soft abilties consisting of leadership, go-cultural communique, and trouble-fixing also continue to be in excessive demand, mainly as Chinese organizations make bigger their global operations. Talent shortage has led to accelerated competition among employers, riding up salaries for niche roles and prompting groups to make investments extra heavily in inner schooling and improvement packages.

Five. Demographic Shifts: Youth Employment and Aging Workforce

Youth employment remains a complicated problem in China. While job opportunities for younger graduates have grown along financial recuperation, excessive competition and high expectancies hold to pose demanding situations. The countrywide young people unemployment charge stood at about 14% in early 2025, slightly decrease than in 2024 but nonetheless a subject for policymakers.

In reaction, the authorities has expanded employment subsidies, vocational education initiatives, and entrepreneurship programs focused on young human beings. Additionally, more college students are choosing internships, apprenticeships, and industry-connected educational pathways to decorate employability earlier than commencement.

Meanwhile, the getting old group of workers provides its very own set of challenges. Industries including manufacturing, logistics, and healthcare are increasingly more searching out ways to preserve older employees through re-skilling applications and flexible work preparations.

6. Trends in Hiring Practices

Recruitment practices in China are evolving, with organizations leveraging AI-pushed recruitment equipment, virtual exams, and facts analytics to streamline hiring processes. Many organizations now prioritize candidate experience, the use of era to lessen time-to-lease and improve engagement at some point of the recruitment cycle.

Campus recruitment remains a key approach for principal agencies, mainly in sectors which includes generation, finance, and engineering. However, there may be a developing desire for hiring candidates with realistic revel in, main to greater collaboration between universities and companies to offer industry-relevant guides and internships.

Diversity and inclusion are also gaining traction. Companies are increasingly dedicated to gender balance and hiring talent from numerous backgrounds, which include ethnic minorities and worldwide candidates, specially within the tech and R&D sectors.

7. Outlook for 2025 and Beyond

Looking in advance, China’s recruitment panorama is predicted to remain dynamic. The persisted improvement of emerging sectors consisting of quantum computing, biotechnology, smart towns, and the metaverse will create new employment opportunities, specially for skills with interdisciplinary ability sets.

Policy shifts, which includes similarly liberalization of the hard work market and supportive measures for small and medium corporations (SMEs), may also stimulate job advent. Additionally, the emphasis on sustainable improvement and digital innovation is in all likelihood to reshape hiring priorities, with an growing awareness on inexperienced jobs and virtual literacy.

However, geopolitical uncertainties, change tensions, and worldwide monetary fluctuations will remain key elements influencing China’s hard work marketplace within the close to destiny. Businesses and activity seekers alike will need to stay agile, adapting to changing financial situations and technological advancements.

#Recruitment Process In China#12th pass students apply#college pass students apply china government recruitment result

2 notes

·

View notes

Text

Top Trends Transforming the Porous Silicon Substrates Market Worldwide

Unveiling the Future of Porous Silicon Substrates

The porous silicon substrates market is undergoing a remarkable transformation, driven by burgeoning applications in microelectronics, biomedical engineering, and optoelectronics. With a projected compound annual growth rate (CAGR) of 8.2% from 2023 to 2030, this niche yet increasingly critical sector is poised for robust expansion globally. We examine the technological, geographic, and competitive dynamics shaping the market’s trajectory and offer detailed, region-specific insights and segmentation analysis.

Request Sample Report PDF (including TOC, Graphs & Tables): https://www.statsandresearch.com/request-sample/40260-global-porous-silicon-substrates-market

Key Porous Silicon Substrates Market Segmentation and Growth Drivers

Microporous, Mesoporous, and Macroporous: The Three Pillars of Porosity

Porous silicon substrates are categorized based on their pore diameters:

Microporous Silicon Substrate (<2 nm): Dominates the global market due to high surface area and superior chemical reactivity. Extensively used in drug delivery systems and photonic applications.

Mesoporous Silicon Substrate (2–50 nm): Gaining prominence in biosensing and energy storage applications.

Macroporous Silicon Substrate (>50 nm): Preferred for microfluidic devices and high-power electronics due to enhanced mechanical stability.

Microporous substrates maintain the largest share, supported by substantial research investment and extensive deployment across consumer electronics and healthcare industries.

Get up to 30%-40% Discount: https://www.statsandresearch.com/check-discount/40260-global-porous-silicon-substrates-market

End-Use Vertical Analysis: From Semiconductors to Biomedical Frontiers

Consumer Electronics

The consumer electronics sector represents the largest end-use segment, where porous silicon substrates enhance thermal management, EMI shielding, and battery performance. The trend toward miniaturization and flexible electronics further accelerates demand.

Healthcare

In the healthcare domain, porous silicon’s biocompatibility and controlled biodegradability make it an ideal material for biosensors, drug delivery platforms, and tissue engineering. Innovations in nanomedicine and implantable devices are expanding its usage rapidly.

Others

Other applications span environmental monitoring, energy harvesting, and optoelectronics, with emerging interest in using porous silicon in photovoltaics and gas sensors.

Porous Silicon Substrates Market Regional Insights: Mapping Global Growth

North America

The North American market is witnessing steady growth driven by rising R&D investment, particularly in the United States. Strategic collaborations between semiconductor companies and research institutions are fueling innovation in next-generation porous materials.

Asia-Pacific

China dominates the Asia-Pacific market with heavy investment in semiconductor innovation and digital infrastructure. National initiatives supporting AI chips, quantum computing, and MEMS technologies are fostering exponential demand. Meanwhile, Japan, South Korea, and India are emerging as strategic contributors due to technological adoption and government-backed funding schemes.

Europe

The United Kingdom led the European market in 2021 and continues to do so due to its strong industrial base and focus on biomedical innovation. Germany and France follow closely, supporting market growth through precision engineering and cross-border collaboration in chip manufacturing.

Middle East & Africa and South America

These regions, although in nascent stages, are witnessing growth through smart infrastructure development, IoT adoption, and international investments aimed at local semiconductor capabilities. Countries like Brazil and UAE are gradually integrating porous silicon technology into renewable energy and industrial automation initiatives.

Competitive Landscape: Key Players Shaping the Porous Silicon Substrates Market

Several global and regional players are competing through technological innovation, strategic partnerships, and vertical integration.

Notable Companies:

Refractron Technologies Corp – Known for robust material innovations and cross-sector applications.

NGK Spark Plug – Leverages its ceramic expertise for cutting-edge porous silicon deployment.

NORITAKE CO., LIMITED – Integrates nanotechnology into its porous silicon solutions.

Porous Silicon – Specializes in biomedical and photonic applications.

Siltronix Silicon Technologies – Focused on high-purity silicon wafers with advanced porosity control.

SmartMembranes GmbH, Microchemicals GmbH, and others contribute through focused niche innovations.

These firms differentiate by targeting specific porosity levels and application niches, ensuring steady technological evolution.

Porous Silicon Substrates Market Dynamics and Strategic Outlook

Porous Silicon Substrates Market Drivers

Growing demand for miniaturized, high-efficiency electronics

Expansion in biomedical research and implantable systems

Increased adoption in MEMS and NEMS technologies

R&D focus on biodegradable electronics

Porous Silicon Substrates Market Challenges

Complex and costly fabrication processes

Integration hurdles with existing semiconductor ecosystems

Limited commercial scalability in some emerging use cases

Porous Silicon Substrates Market Opportunities

Untapped potential in photovoltaics and water purification

Emerging markets prioritizing semiconductor sovereignty

Integration in next-gen 6G networks and wearable bio-devices

Future Outlook: The Path to 2030

By 2030, the porous silicon substrates market is expected to reach unprecedented heights, underpinned by multi-disciplinary innovation and cross-border collaboration. Strategic investments, government incentives, and research acceleration will be crucial to unlocking the next phase of growth.

Purchase Exclusive Report: https://www.statsandresearch.com/enquire-before/40260-global-porous-silicon-substrates-market

Conclusion

The global porous silicon substrates market stands at a pivotal point. With its proven utility in critical applications and accelerating innovation across sectors, this technology will remain foundational in the evolution of advanced electronics, medical devices, and nanostructured systems. Stakeholders that harness its potential early through targeted R&D, regional expansion, and strategic alliances will shape the future of this rapidly growing domain.

Our Services:

On-Demand Reports: https://www.statsandresearch.com/on-demand-reports

Subscription Plans: https://www.statsandresearch.com/subscription-plans

Consulting Services: https://www.statsandresearch.com/consulting-services

ESG Solutions: https://www.statsandresearch.com/esg-solutions

Contact Us:

Stats and Research

Email: [email protected]

Phone: +91 8530698844

Website: https://www.statsandresearch.com

1 note

·

View note

Text

Fastening Power Tool Market Key Drivers, Trends, Growth, Analysis And Report To 2034

Fact.MR, in its newly released research study, states that the fastening power tool market across the world is expected to be valued at US$ 3,502.1 million in 2024. Global fastening power tool demand is predicted to rise at 6.4% CAGR and reach a market worth of US$ 6,512.5 million by the end of 2034.

The market for fastening power tools is forecast to witness growth opportunities in emerging economies due to the innovations in products, which are a vital factor in supporting competitiveness in the market of power tools. Continued innovation, particularly in lightweight, ergonomic, and easy-to-use power tools, supports more efficiency, safety, and overall satisfaction in use.

For More Insights into the Market, Request a Sample of this Report: https://www.factmr.com/connectus/sample?flag=S&rep_id=9262

What is Hindrance Factor for the Demand for Fastening Power Tool?

"Cyclicality of End User Industries to Restrain the Market Growth"

The cyclicality of end-user industries such as construction and manufacturing has a great influence on the demand for fastening power tools. The industries are subject to economic fluctuations, and their ups and downs directly affect the demand for tools applied in fastening operations.

During down economies, there is usually decreased investment in construction. Spending less on new construction projects, either residential or commercial, results in decreased demand for fastening power tools utilized in construction applications.

Country-wise Insights

The United States is estimated to hold 67.1% of the North American market in 2034. The increasing activity in construction and infrastructure projects in the United States, such as residential, commercial, and public infrastructure, is a major driver of the need for fastening power tools.

China is predicted to account for a 56.1% revenue share in the East Asia market in 2034. Initiatives led by the government, like the Made in China 2025 strategy, aim at technological upgrading of the manufacturing industry. The policies can propel the use of advanced fastening power tools.

Japan is expected to have a 29.5% revenue share in the East Asia market by 2034. Japan is a pioneer in technological advancement. Continuous development in power tool technology, such as the integration of smart and IoT capabilities, can fuel the uptake of high-end fastening tools in the Japanese market.

Category-wise Insights

On the basis of product type, worldwide demand for fastening power tool is expected to increase substantially in the rebar tier segment due to continuous development of technology in rebar tier tools, including lightweight and portable designs, longer battery life, and better tying ability.

Competitive Landscape

Major players in the fastening power tool market are adopting a range of strategies to realize their objectives. The strategies involve embracing innovation, adopting rigorous product quality control mechanisms, establishing strategic alliances, maximizing supply chain management systems, and continuously improving their products and technologies.

For example,

In 2022, Bosch Power Tools, the world leader in power tools and accessories, introduced a formidable product combination engineered to dominate tough surfaces. The GBH18V-28DC 18V Brushless Connected Ready SDS-plus® Bulldog™1-1/8-inch Rotary Hammer and the GDE28D SDS-plus® Dust Collection Attachment expand Bosch's comprehensive rotary hammer technology portfolio.

With its high impact energy, accurate drilling capacity, and built-in dust extractor to reduce airborne particles, the GBH18V-28DC hammer and GDE28D attachment provide the extra power required for productive work on any jobsite while emphasizing safety with innovative product design.

and E. Fein GmbH, DEWALT, Hilti Corporation, Hitachi Koki Co., Makita Corporation, MAX Co., Ltd., Sumake Industrial Co., Techtronic Industries Co. Ltd., Wacker Neuson SE, and Xindalu Electronic Technology Co., Ltd. are among the major participants in the market for fastening power tools.

Browse Full Report: https://www.factmr.com/report/fastening-power-tool-market

Segmentation of Fastening Power Tool Market Report

By Product Type:

Rebar Tier

Corrugated Fasteners

Nailer Machine

Screw System

Hog Ring Tool

Stapler

By Mode of Sales:

Retailers

Distributors

Online

By Region:

North America

Europe

East Asia

Latin America

Middle East & Africa

South Asia & Oceania

Check out More Related Studies Published by Fact.MR:

Ready-to-Eat Wet Soup Market https://www.factmr.com/report/4582/ready-to-eat-wet-soup-market

Ready to Eat Soup Marke https://www.factmr.com/report/282/ready-to-eat-soup-market

Functional Dairy Ingredients Market https://www.factmr.com/report/642/functional-dairy-ingredient-market

Plant-based Probiotics Market https://www.factmr.com/report/plant-based-probiotic-market

𝐂𝐨𝐧��𝐚𝐜𝐭:

US Sales Office 11140 Rockville Pike Suite 400 Rockville, MD 20852 United States Tel: +1 (628) 251-1583, +353-1-4434-232 Email: [email protected]

1 note

·

View note

Text

An Overview of UK Home Small Domestic Appliances Market: Trends and Insights

The UK home small domestic appliances (SDA) market has seen significant growth driven by evolving consumer lifestyles, technological innovations, and a growing focus on energy efficiency and sustainability. From kettles and toasters to handheld vacuums and smart kitchen gadgets, SDAs are becoming indispensable in UK households.

Buy the Full Report for More Category Insights into the UK Home Small Domestic Appliances Market

Download a Free Sample Report

Here’s an analysis of the key trends and insights shaping the market in 2024.

1. Market Size and Growth

The SDA market in the UK is expected to grow at a CAGR of 4-6% from 2023 to 2028, driven by post-pandemic shifts in home-based lifestyles.

Rising disposable income and increasing interest in premium and smart appliances are fueling demand.

2. Key Consumer Trends

a. Smart and Connected Appliances

Voice control integration (via Alexa, Google Assistant) and IoT-enabled SDAs are gaining traction.

Popular products: Smart kettles, Wi-Fi-enabled coffee makers, and robotic vacuum cleaners.

b. Health and Wellness Focus

Growing interest in air fryers, blenders, and juicers as consumers focus on healthier lifestyles.

Increased demand for air purifiers and humidifiers due to rising concerns over indoor air quality.

c. Sustainability and Energy Efficiency

UK consumers are prioritizing eco-friendly appliances with lower energy consumption, such as energy-efficient kettles and low-wattage irons.

Brands offering repairable and recyclable products are seeing stronger loyalty.

d. Compact and Space-Saving Designs

Urban living and smaller households drive demand for multi-functional and compact SDAs, such as 2-in-1 steamers or combination microwaves.

3. Product-Specific Insights

Kitchen Appliances

Coffee Machines:

Premium brands like Nespresso and De’Longhi dominate, with demand for bean-to-cup and pod-based machines increasing.

Air Fryers:

Brands like Tefal and Ninja lead as air fryers become a household staple.

Consumers prioritize larger capacities and multi-functionality.

Cleaning Appliances

Robotic Vacuum Cleaners:

Growing adoption of smart robotic vacuums from brands like iRobot and Eufy.

Consumers value mapping technologies and self-emptying features.

Handheld Vacuums:

Brands like Dyson continue to dominate the cordless vacuum segment, driven by innovations in battery life and suction power.

Personal Care Appliances

Growth in electric toothbrushes, hair dryers, and grooming kits, driven by brand diversification and targeted marketing.

4. Retail and Distribution Trends

E-commerce Boom:

Online channels like Amazon, Argos, and Currys are witnessing robust growth, fueled by convenience and competitive pricing.

Omni-Channel Experiences:

Retailers are integrating digital and in-store experiences, such as AR demos for products.

Subscription Models:

Brands offering subscription plans for products like coffee machines and vacuum filters are seeing higher customer retention.

5. Competitive Landscape

Key Players

Dyson:

Leader in cordless vacuum and air purifier segments, with a focus on cutting-edge design and functionality.

Ninja:

Dominates the air fryer market and continues to expand into other SDAs like blenders and multi-cookers.

Philips:

Strong presence in personal care and kitchen appliances, with a growing focus on energy efficiency.

Breville:

Known for kettles, toasters, and sandwich makers, with a strong mid-market appeal.

Market Share Dynamics

Premium brands like Dyson and Nespresso dominate the high-end segment.

Mid-range brands (e.g., Tefal, Morphy Richards) maintain steady growth by balancing affordability and quality.

New entrants offering smart or niche eco-friendly solutions are gradually gaining market share.

6. Challenges and Opportunities

Challenges

Economic Pressures:

Inflation and rising energy costs may deter discretionary spending on premium SDAs.

Supply Chain Disruptions:

Component shortages and logistical issues continue to affect manufacturing and delivery timelines.

Opportunities

Sustainability:

Brands investing in energy-efficient and recyclable products are likely to capture eco-conscious consumers.

Customization:

Offering customizable products (e.g., personalized coffee settings or modular vacuum components) can differentiate brands.

7. Future Outlook

Smart Home Integration:

Growth in smart home adoption will drive demand for IoT-enabled SDAs.

Health and Wellness Products:

Continued interest in products supporting healthy lifestyles, such as air purifiers and low-fat cooking appliances.

Sustainability Leadership:

Companies embracing circular economy principles will gain a competitive edge.

The UK small domestic appliances market is poised for steady growth, underpinned by consumer preferences for convenience, sustainability, and technology-driven innovation. Players who align their strategies with these evolving trends will be best positioned to thrive.

2 notes

·

View notes

Text

2025 Rivian R1S and R1T Updates

June 7, 2024

Rivian has unveiled the second generation of its R1S mid-size SUV and R1T pickup truck for 2025, featuring significant updates under the hood and minor visual changes. Both models now offer an 850-hp Tri-Motor configuration and an improved Quad Motor setup with 1025 hp.

Battery Enhancements

The 2025 R1 models come with three battery options: Standard, Large, and Max. The Standard pack now uses a lithium-iron-phosphate (LFP) chemistry, simplifying service and reducing complexity. The Large pack’s usable capacity has decreased to 109.4 kWh, providing up to 330 miles of range. The Max pack offers up to 410 miles for the R1S and 420 miles for the R1T. Charging rates remain at 220 kW for all but the Standard battery, which is capped at 200 kW.

Powertrain Improvements

The default Dual Motor powertrain remains at 533 hp and 610 pound-feet of torque, while the Performance version maintains 665 hp and 810 pound-feet. The new Tri-Motor setup produces 850 hp and 1103 pound-feet of torque. The revised Quad Motor model now boasts 1025 hp and 1198 pound-feet of torque. Rivian claims the 1025-hp R1S can accelerate to 60 mph in under 2.5 seconds, with the 850-hp version doing it in 2.9 seconds.

Chassis and Technology Upgrades

Rivian has reworked the suspensions for improved ride and handling. New Pirelli tires and 22-inch aero wheels are introduced, along with updated lighting elements featuring animated light bars and an Adaptive Drive Beam. The electrical architecture has been streamlined from 17 to 7 control units, enhancing serviceability and reducing costs. The updated infotainment system now uses AI, and advanced driver-assistance features include 11 cameras and 5 radars.

Pricing and Availability

The 2025 R1S Dual Motor starts at $77,700, with the Large battery at $84,700, and the Max pack at $91,700. The new Tri-Motor model with the Max pack starts at $107,700. The R1T prices remain the same at $71,700 for the Dual Motor with the Standard battery, but the Large and Max pack versions are now $78,700 and $85,700, respectively. The Tri-Motor R1T with the Max battery starts at $101,700. The R1S Dual Motor is currently available, with the R1T following soon. The Tri-Motor variants are expected this summer, and the Quad Motor models later in the year.

Conclusion

Rivian’s 2025 updates to the R1S and R1T enhance range, performance, and technology. These improvements, along with a streamlined production process, position Rivian’s flagship models as more competitive in the evolving electric vehicle market.

Trending topics on google

Understanding the Recent H5N2 Avian Flu Case in MexicoTagged Rivian R1S and R1T new look

2 notes

·

View notes

Text

I bought Nothing Ears! (2024)

Picture credit to PCMag.

I'm a very big fan of the Nothing aesthetic but haven't committed to any of their non-earbuds products, because unfortunately I like having specs and RAM more than I like having LEDs on the back of my phone. That said I've bought all of their flagship earbuds at this point and liked the Ear (1)s enough to later buy the Ear (2)s, and after unfortunately setting one earbud through the laundry and the case simultaneously deciding it didn't want to charge the remaining earbud, I am now in possession of Nothing Ears at $150.

What a horrible naming scheme they've got going! They're already giving up the (1) (2) thing and not doing (3) and just dropping that. Now it's not clear what the latest model is actually supposed to be without checking release dates. Ear (1), Ear (2), Ear (A) floor models, and Ear? Fuck off.

Despite the schizophrenic reuse of their own case and earbud design for the third generation in a row and their inability to settle on a name after giving up the (Numbered) aesthetic the Ears are excellent, they fit comfortably into the ear, have pinch touch-controls on the stem, and look super sleek. The default controls are intuitive and have forward/reverse/play already bound, with a pinch-and-hold maneuver flipping through noise-cancellation settings. Pinch controls also aren't susceptible to water, unlike some Google Pixel Buds Pro I have that seize their touch controls if my fingers are damp. Pairing is quick and can be done with two devices simultaneously. Low-lag mode is still just as anemic as it is on any other wireless headset that claims the feature, I really don't think it's gonna happen for any earbuds at this point, just stop trying to give us wireless as a replacement for wired.

Noise cancellation on Nothing earbuds have an excellent bonus in that you can actually use the feature with just one earbud in. Very good for noisy work environments that still require you be attentive (like mine) or if you just don't want the volume at 75% of the way up on your phone just to hear everything. Transparency mode being the only available setting on basically any other wireless in-ears can eat me, I want to make just one ear feel full sometimes. Either way Nothing's algorithm for transparency mode and noise-cancellation is actually very good, and noise-cancellation especially shines for the aforementioned purpose of using it as a form of volume control. Detail in sound is not lost with noise-cancellation, but can be lost with transparency mode.

Sound quality is quite good, Nothing Ears come equipped with ceramic drivers (more of a marketing point than an actual benefit) and a mostly complete equalizer in the Nothing X app. A bass boost feature and a much more generalized equalizer feature also exist. Supports the AAC, LDAC, LHDC 5.0, and SBC audio codecs. Battery life is estimated by Nothing to be 8 1/2 hours on a full charge for both buds and a cumulative 40 1/2 hours with a full case charge. Sound comes across to me as fairly balanced but trends a bit towards bassy, which is a good thing in an earbud or TWS headphone.

I'm overall very pleased with the Nothing Ears and do recommend them as a $150 offering, but I'm not pleased that the Ear (A) floor model equivalent does not have Qi charging. I haven't tried Xiaomi's buds in a fat minute so I can't say anything about how they compare to Buds 4 Pro or Buds 5 Pro, but I do know Xiaomi's typically budget earbuds are getting heftier in price (5 Pro are at $100 now) and Nothing is $150 for a very solid option in the more "flagship earbuds" space while still being compatible with both iOS and Android. Xiaomi also dropped Qi charging on anything above the Redmi Buds 3 Pro which totals at $50, so I don't think it's a cost thing for them to have just stopped offering Qi charging. There are also Earfun earbuds at the same RB3P price-point with Qi charging.

#nothing#nothing ear#earbuds#headphones#wireless headphones#wireless earbuds#tech#look at my flop reviews boy

3 notes

·

View notes

Text

Knock knock, KaiOS.

The ephemeral taste of innovating nearly obsolete bricks might be reaching its inevitable demise.

Nokia 8110 4G displayed in a kiosk at Mobile World Congress 2018. Image courtesy of Kārlis Dambrāns.

Despite the recent boom of feature phone sales over digital minimalism and dopamine detox trends, the future for KaiOS remains bleak as they fail to be consistent with their promises, thus miserably lagging against established giants in the market.

The good start

KaiOS is a partially open-source operating system developed by the Hong Kong-based company, KaiOS Technologies Inc. It was initially released in October 2017 and was forked from Boot 2 Gecko. Their name is from the Chinese for open – 开 (kāi) which “captures the idea of being inclusive.”

In just one year, they have overtaken Apple’s iOS as the second most popular operating system in India, with Android remaining on top, despite losing their 9% market share. In that same timeframe as well, they managed to sell around 450 million devices worldwide. Furthermore, their platform is compatible to WhatsApp, Twitter, YouTube, Google Maps, and Google Assistant.

To oversimplify things, KaiOS took the Boot 2 Gecko code (based from FirefoxOS) and modified it to run on hardware similar to that of feature phones and added the KaiOS Store. Other than that, they also implemented recent innovations that are becoming today’s standard, like 4G LTE and 5G, GPS, and Wi-Fi. By doing so, they effectively just created a separate phone segment, which some people call as the quasi-smartphones or smart feature phones.

KaiOS specifically chose the hardware present in their devices for an appealing approach to developing markets, like India and Pakistan, to bridge the digital divide and bring cheaper internet access. They removed the touch screen which they consider as the most costly part of the device, and replaced it with a cheaper T9 keypad input. Additionally, their devices only need 256MB to work and are also compatible with cost-efficient Spreadtrum chipsets.

What went wrong

By doing so, they effectively avoided the mistakes that Mozilla made. They chose a target audience first and offered them a product. They made an operating system out of the web but used that as a tool rather than the end goal, the latter being their approach to the digital divide. But not all products are perfect on their own, as their approach is a double-edged sword.

The T9 keypad meant that the apps had to be optimized to work on such inputs. Likewise, dissimilar to FirefoxOS, not all webpages can run on KaiOS devices due to hardware restraints. Such disadvantages make it an appealing short-term solution while their users save up for better entry-level Android devices.

Platform immaturity

The platform is still quite immature, despite five years since its initial launch. Some users claimed that their devices sometimes cannot receive calls, and crashes on related functions constantly. The battery also does not live up to its expectations and provides a ‘disappointing’ performance. Additionally, the calendar’s sync and date functionality is unstable, the alarm clock doesn’t ring from time to time, and the lack of note-taking, file browsing, multitasking, and wide audio format support. Besides, the platform lacked proper app quality control, bug reports, and feedback system, along with a slew of advertisements. Perhaps, the most lambasted functionality of the platform is the T9 input. Users characterized the input as slow and unreliable, thus ineffective for efficient user interface navigation. The predictive text input, which might sound good, is something they’d rather have disabled due to its restraints such as inaccurate suggestions and buggy input.

Some have mentioned that users may be over-estimating KaiOS and pitching it against smartphone platforms. Then on, we can’t deny that a platform still has to be stable and reliable, albeit hardware-restricted. Some went on to compare the system to its older counterparts such as Nokia’s Series 40, Microsoft’s Lumia, Vodafone’s MobiWire, and Blackberry’s Blackberry 10, which the users characterized as more ‘stable.’

Unfortunately, version 2.5.4 onwards faced a downward trend as certain apps were no longer maintained and supported, due to the decrease of development activity. For instance, the optimized Google and YouTube apps have been pulled out from the app store, around the same time as the update. In version 3, WhatsApp support has already been dropped and new app submissions to the store also plummeted. Google Assistant, the primary tool for users to voice type and issue commands (albeit stripped-down in comparison to Android), also dropped KaiOS support last June 30, 2021. Some users reached out to the company regarding this matter, to which they replied that they are developing an in-house voice assistant alternative. Until now, it is nowhere near worldwide coverage, given the limited devices it was shipped upon.

The company and its partners

Even more worse, the problem rests beyond that. The project development of has been consistent enough until the COVID-19 pandemic. According to the company’s blog statement “the growth was still not like how we achieved in the pre-COVID times, but these numbers and new partnerships are going up and in the right direction in this second year of the pandemic.”

In 2022, the project updates has since then plummeted. There weren’t any major announcements across all their social media platforms, even from the company website. Their Github repositories are no exception as well, as they still haven’t received any commits until now. Their only active repo is the gecko-b2g, which serves as the operating system base.

It is not implicit that their users are complaining about the bugs and speculating on the project’s downfall but it seems that they have no proper public relations and customer support as the company fails to actively respond to these messages.

Nokia

Nokia, or should we say, HMD Global has been a primary partner of KaiOS Technologies over the years. They manufactured the higher-end devices of the platform that were considerably the most popular in KaiOS’ lineup, such as the Nokia 6300 4G, Nokia 2780 Flip, and the Nokia 8110 4G.

Regardless, their approach is somehow vague as enthusiasts are confused over what their target audience is supposed to be, and what were they trying in the first place. Their approach started with the reboot of their classic devices, so it’s safe to assume that their target consumers are the ones who are nostalgic over their retro bricks. HMD, for a matter of fact, might have just been the worst example of a KaiOS partner.

Their devices are the most expensive ones of the platform, almost close to the entry-level Android Go smartphones. HMD Global has also been long criticized over the failure to deliver software updates from KaiOS to their devices, as they provide only about a year of support for these. The users also cannot help to complain over the significant bloatware present in such a limited hardware they provide.

Just recently, HMD Global took a step back from this approach and cherished their barebones Series 30 and Series 30+ platforms once again. Their last KaiOS device is the 2780 Flip from November 2022 and was then on followed by a series of Android Go and dumbphones from their C and 1xx series. In a reply to a user inquiry, they reportedly blamed KaiOS as the Google Assistant support for the platform was dropped.

Alcatel and TCL

Alcatel and TCL are also major partners of KaiOS. In fact, TCL Corporation is the largest shareholder of KaiOS Technologies. Both of them are popular for their Go Flip line. Despite the successes of Go Flip 1, 2, 3, and V, they didn’t get to experience the luxury of getting updated to the latest version of the OS, unlike the Go Flip 4. A user reached out to the company, to which they replied that they are still planning to serve these said updates to such devices, although there is still no update to talk of until now.

Unfortunately, similar to HMD Global, they seem to be diverging away from the platform as recent releases from both manufacturers are focused on midrange to high-end Android devices, as well as the Tab series of TCL.

Jio

The Indian telecommunications company, Reliance Jio Infocomm Limited is the catalyst of KaiOS’ takeover against Apple in the country, all thanks to their aggressive marketing approach. They offered the competitively priced JioPhone for free to their users who are subscribed to their data plans.

Unluckily, even Jio is also straying away from KaiOS. There have been rumors that the JioPhone and the JioPhone 2 have been discontinued, as they are no longer sold. They last received the version 0258 update back on May 22, 2021, and clearly missed version 3.0 by a long shot. On June 24, 2021, Reliance Jio announced the JioPhone Next, a budget Android Go smartphone made in collaboration with Google. Recently this year, they partnered with Karbonn to release the Jio Bharat K1 Karbonn and V2 to provide access to UPI payments, Jio ecosystem, and cheaper 4G to the rural areas of India that remain untapped by recent advancements in technology.

What happened?

Fast forward to August 2023, users speculate that the project has already died out due to lack of activity and stagnation since the release of 3.0. Their company's social media platforms are inactive, except for the usual, seemingly AI-generated content every national holiday across countries. On the other hand, KaiOS Technologies partnered with the cybersecurity firm Trustonic to expand their device affordability efforts in Africa. There have also been infrequent new device releases for the platform, such as the AT&T Cingular Flex in February, Cricket Debut Flex in June, and Logan Technology’s Panita this August. Truth be told, I find this section rather short and lacking. Unfortunately, I could say the same for the company’s recent efforts. Nonetheless, I hope that things eventually get better. As users worldwide expected a reliable feature phone platform, all these issues contributed to a downward trend of interest for KaiOS. It seems that they might end up like FirefoxOS, failing to keep up and desolate in the past. Whether they wake up to innovate again, or continue dormant and inevitably die out is up for them to decide.

For now, one thing’s for sure, if they fail to address these issues, they’ll be no better than the obsolete bricks of the bygone era.

5 notes

·

View notes

Text

The Power of UI/UX Design: Enhancing User Experiences

Introduction: In today's digital age, where user interfaces and experiences play a crucial role in capturing and retaining users, the significance of UI/UX design cannot be overstated. UI (User Interface) design focuses on creating visually appealing and intuitive interfaces, while UX (User Experience) design ensures that the overall user journey is seamless, engaging, and satisfying. This blog post dives into the world of UI/UX design, exploring its importance, principles, and the impact it has on businesses and users alike.

Understanding UI Design: UI design encompasses the visual aspects of a digital product, such as websites, mobile applications, and software interfaces. It involves selecting colors, typography, icons, and layouts to create an aesthetically pleasing and cohesive user interface. Effective UI design aims to enhance usability, guide users through the interface effortlessly, and create a positive first impression.

Key aspects of UI design: a. Consistency: Maintaining visual consistency throughout the interface helps users navigate smoothly, as they become familiar with the design patterns and elements. b. Accessibility: Designing interfaces that are accessible to users with disabilities ensures inclusivity and expands the product's reach. c. Visual Hierarchy: Organizing information using appropriate contrast, size, and spacing allows users to prioritize and focus on essential elements.

Exploring UX Design: UX design focuses on the overall user experience by understanding user behavior, needs, and goals. It involves research, user testing, and iterative design to create intuitive and delightful experiences. A well-executed UX design enables users to accomplish tasks efficiently, creates emotional connections, and encourages user loyalty.

Key aspects of UX design: a. User Research: Understanding the target audience's preferences, motivations, and pain points is crucial for designing a product that meets their needs effectively. b. Information Architecture: Organizing and structuring content in a logical and intuitive manner helps users find information quickly and easily. c. Usability Testing: Conducting user tests at various stages of the design process uncovers usability issues and allows for improvements based on real user feedback.

The Business Impact of UI/UX Design: Investing in UI/UX design yields several benefits for businesses, ultimately contributing to their success and growth. a. Enhanced User Satisfaction: Intuitive interfaces and seamless experiences result in satisfied users who are more likely to engage with the product, recommend it to others, and become loyal customers. b. Increased Conversions: Well-designed interfaces with clear calls to action and intuitive navigation can boost conversion rates, leading to higher sales and revenue. c. Competitive Advantage: In a saturated market, a superior UI/UX design sets a product apart, attracting users and establishing a competitive edge over rivals. d. Reduced Development Costs: Identifying and addressing usability issues early in the design process minimizes the need for costly redesigns and rework down the line.

Trends and Evolving Practices: UI/UX design is an ever-evolving field, and staying up to date with the latest trends and best practices is vital for designers. Some current trends include: a. Dark Mode: Providing a dark-themed interface option for users, which is not only visually appealing but also reduces eye strain and saves battery life on certain devices. b. Microinteractions: Adding small, subtle animations and interactive elements to delight users and provide feedback on their actions. c. Voice User Interfaces (VUI): With the rise of smart speakers and voice assistants, designing interfaces that can be controlled and navigated through voice commands is gaining prominence.

Conclusion: In a world where user experiences define the success of digital products, UI/UX design plays a critical role. The collaboration between UI and UX designers results in aesthetically pleasing interfaces that are easy to use, efficient, and memorable. By prioritizing UI/UX design, businesses can drive user satisfaction, increase conversions, and gain a competitive advantage in today's digital landscape. As technology continues to evolve, staying attuned to the latest trends and user preferences will be key to creating outstanding UI/UX experiences that truly resonate with users.

4 notes

·

View notes

Text

The Future is Gritty: Trends in the Bonded Abrasive Market

The Bonded Abrasive Market is a critical component of the global manufacturing and metalworking ecosystem. Bonded abrasives are made by combining abrasive grains with a bonding material like resin, clay, or glass, and are used in operations such as grinding, cutting, polishing, and finishing. As precision engineering and high-performance materials gain prominence, the demand for efficient and durable abrasive tools is accelerating.

Bonded abrasives serve a wide range of sectors including automotive, aerospace, construction, electronics, heavy machinery, and metal fabrication.

Market Overview

Bonded abrasives are formed into various shapes—such as wheels, segments, and sticks—and used in both manual and automated grinding systems. Common abrasive materials include aluminum oxide, silicon carbide, cubic boron nitride (CBN), and diamond, each tailored for specific surfaces and applications. As industries demand tight tolerances, smoother finishes, and faster throughput, the market for advanced bonded abrasives continues to expand.

Key Market Trends

Automation in Metal Fabrication

The rise of CNC grinding and robotic systems has increased the need for high-precision bonded abrasives that can deliver consistent performance over long cycles.

Emergence of Superabrasives

Diamond and CBN-based bonded abrasives are gaining traction for high-end applications such as aerospace components and semiconductor polishing.

Growing Demand from Automotive and Aerospace

With growing production of vehicles and aircraft, bonded abrasives are used extensively in engine, transmission, and structural component finishing.

Customized Abrasives for Advanced Materials

Manufacturers are developing abrasives suited for titanium, carbon fiber, ceramics, and other hard-to-machine materials.

Growth Drivers

Industrialization and Infrastructure Development

The demand for construction equipment, machine tools, and metal fabrication drives abrasive consumption globally, especially in emerging economies.

Rise in Precision Engineering

Sectors like defense, energy, and electronics require micron-level surface finishes, pushing demand for fine-grit bonded abrasives.

Resurgence of Manufacturing in North America and Europe

Reshoring of manufacturing and investment in smart factories is boosting the demand for high-efficiency abrasives.

Rapid Expansion of the Electric Vehicle (EV) Industry

EV motor components, battery housings, and lightweight frames require specialized grinding and finishing processes using bonded abrasives.

Challenges in the Bonded Abrasive Market

Volatility in Raw Material Prices

Cost fluctuations in abrasive minerals and bonding agents can impact production economics and pricing.

Environmental and Health Concerns

Dust generation and disposal of used abrasives require regulatory compliance and environmental safety measures.

Skill Shortages

Skilled workers are essential for operating grinding machines and interpreting abrasive wear, especially in manual and semi-automated setups.

Competition from Coated Abrasives

In certain polishing and light grinding applications, coated abrasives may be preferred due to their flexibility and lower cost.

Future Outlook

Eco-Friendly and Low-Dust Bonded Abrasives

Manufacturers are developing new formulations that reduce particulate emissions and improve operator safety.

3D Printing of Abrasive Tools

Additive manufacturing is emerging as a method to design customized and geometrically complex abrasive tools.

Integration with Smart Machinery

Bonded abrasives are being paired with sensors and digital controls for real-time wear monitoring and adaptive grinding.

Surging Demand in Asia-Pacific

Countries like China, India, and South Korea are leading in automotive and electronics manufacturing, accelerating bonded abrasive consumption.

Conclusion

The Bonded Abrasive Market is evolving with the demands of modern industry—offering greater precision, efficiency, and performance. As global industries gear up for tighter tolerances, advanced materials, and sustainable production, bonded abrasives will continue to play a pivotal role in shaping the future of manufacturing.

0 notes

Text

Laser Tracker Market Size Enhancing Precision in Industrial Metrology

The Laser Tracker Market Size is gaining significant momentum as manufacturers across industries seek high-precision, non-contact measurement solutions for complex 3D inspection and alignment applications. These devices play a pivotal role in ensuring product accuracy, quality control, and efficient assembly, especially in sectors like aerospace, automotive, and heavy machinery. According to Market Size Research Future, the market is projected to reach USD 1.12 billion by 2030, growing at a CAGR of 11.5% from USD 460 million in 2023.

Market Size Overview

Laser trackers are highly accurate instruments that use laser beams to track the position of a target in 3D space. They are primarily used to inspect large components, align machinery, and reverse engineer complex structures. These systems offer greater mobility, improved accuracy, and faster inspection compared to traditional tools like theodolites and measuring arms.

The growing trend of industrial automation and the increasing demand for real-time quality assurance are accelerating the adoption of laser trackers. As production tolerances tighten and product complexity increases, laser tracking technology is becoming indispensable in advanced manufacturing environments.

Market Size Segmentation

The Laser Tracker Market Size can be segmented based on:

By Component:

Hardware

Software

Services

By Application:

Quality Control and Inspection

Alignment

Reverse Engineering

Calibration

By End-User:

Automotive

Aerospace & Defense

Energy & Power

Architecture & Construction

Manufacturing

Others

By Region:

North America

Europe

Asia-Pacific

Rest of the World

Key Market Size Trends

1. Integration with Industry 4.0

Laser trackers are being integrated into smart factories as part of the broader Industry 4.0 movement. The ability to feed precise 3D data into digital twins and automation systems is transforming how industries approach metrology and quality assurance.

2. Wireless and Portable Devices

Modern laser trackers now feature wireless connectivity, battery-powered operation, and compact designs—enabling easy deployment on factory floors, construction sites, and remote industrial locations.

3. High-Precision Engineering

The increasing need for sub-micron precision in applications like turbine blade manufacturing, satellite component assembly, and EV battery inspection is expanding the role of laser trackers.

4. Growth of Reverse Engineering Applications

Laser trackers are widely used in reverse engineering to reconstruct digital models of legacy components or complex geometries, especially in aerospace maintenance and tooling reproduction.

5. Cloud-Based Data Analysis

Vendors are now offering cloud-enabled platforms for storing and analyzing measurement data in real-time. This enhances collaboration, traceability, and integration across global manufacturing networks.

Segment Insights

By Application Insight:

Quality control and inspection lead the application segment, accounting for the largest market share. Laser trackers significantly reduce measurement time while improving accuracy in validating product dimensions.

By End-User Insight:

The aerospace & defense sector remains the dominant end user, leveraging laser trackers for the alignment of aircraft fuselage, wings, and engines. The automotive industry is also a fast-growing segment, particularly for inspection of chassis, body-in-white (BIW), and powertrain components.

By Component Insight:

Hardware holds the highest share due to the high cost of the laser tracker device itself, including laser emitters, sensors, and reflectors. However, software and services are gaining traction for enhancing usability, remote access, and predictive diagnostics.

End-User Insights

Aerospace & Defense:

Laser trackers ensure precision assembly and alignment of large components, such as airframes and propulsion systems. They are used extensively during maintenance, repair, and overhaul (MRO) activities.

Automotive Industry:

Laser trackers streamline inspection processes on the shop floor, verifying complex surfaces, verifying welding accuracy, and assisting in robot calibration for manufacturing precision.

Construction and Infrastructure:

Used in large-scale infrastructure projects, laser trackers help maintain alignment, level, and positioning accuracy in steel fabrication, bridge construction, and modular building assembly.

Energy & Power:

In energy sectors like wind, nuclear, and oil & gas, laser trackers ensure the proper fit and alignment of turbines, pressure vessels, and pipework installations.

Key Players

Several companies lead innovation in the laser tracker space through new product launches, strategic partnerships, and software integration:

FARO Technologies, Inc. – A global leader offering lightweight and portable laser trackers with intuitive software.

Hexagon AB (Leica Geosystems) – Known for its high-precision Absolute Tracker series used in industrial metrology and research labs.

API (Automated Precision Inc.) – Offers advanced measurement solutions with wireless capabilities and real-time data processing.

Carl Zeiss AG – Leverages its metrology expertise to provide trackers integrated into quality control systems.

Nikon Metrology Inc. – Offers laser trackers with integrated automation and enhanced 3D metrology performance.

Kreon Technologies – Specializes in laser tracking solutions for complex surface analysis and reverse engineering.

Future Outlook

The laser tracker market is poised for robust growth, driven by advancements in AI, real-time analytics, and robotics. As manufacturing ecosystems evolve, these devices will be integrated more tightly into automated workflows, enabling self-correcting systems and zero-defect production lines.

Moreover, growing demand in emerging economies and increased adoption in small-to-mid-size enterprises will further propel market expansion. Focus areas for future development include increasing measurement range, boosting accuracy, and reducing the cost of deployment.

Conclusion

The Laser Tracker Market Size is transforming industrial metrology by enabling faster, more accurate, and more versatile measurements. As industries continue to prioritize quality assurance, automation, and innovation, laser tracking systems will remain at the core of precision engineering.

Trending Report Highlights

Explore other emerging technologies influencing precision manufacturing and electronics:

Beam Bender Market Size

Depletion Mode Junction Field Effect Transistor Market Size

Logic Semiconductors Market Size

Semiconductor Wafer Transfer Robots Market Size

US Warehouse Robotics Market Size

Single Multi Stage Semiconductor Coolers Market Size

Gas Concentration Sensor Market Size

Thermal Management in Consumer Electronics System Market Size

Underfill Dispensers Market Size

Wet Chemicals Market Size

Taiwan Robotics Market Size

0 notes

Text

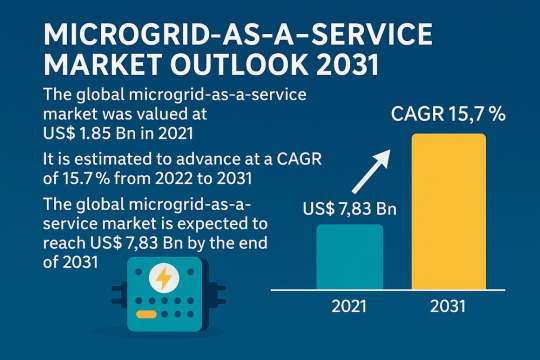

Microgrid-as-a-Service: A High-Growth $7.8B Market by 2031

The global Microgrid-as-a-Service (MaaS) market, valued at US$ 1.85 Bn in 2021, is projected to advance at a CAGR of 15.7% from 2022 to 2031 and reach a valuation of US$ 7.83 Bn by the end of 2031, according to recent market intelligence. The rapid shift toward decentralized, renewable energy and the growing need for uninterrupted power supply are major contributors to this robust growth.

Market Overview: Microgrid-as-a-Service (MaaS) is an emerging model that enables institutions, industries, and residential consumers to deploy microgrids with minimal upfront investment. MaaS provides energy security and enhances grid resilience, offering a reliable solution to frequent outages and natural disasters. It is increasingly becoming a preferred option in both developed and emerging markets for its ability to deliver cost-effective, clean, and locally sourced energy.

Market Drivers & Trends

The global MaaS market is being driven by:

Surge in renewable energy adoption: The growing installation of solar and wind energy systems is propelling the demand for intelligent microgrid solutions.

Government incentives and modernization programs: Initiatives like the U.S. Department of Energy’s Smart Grid Investment Grant Program and subsidies for clean energy projects are fostering microgrid deployments.

Growth in smart devices and grid digitization: Countries are rapidly adopting smart meters and automated transmission systems, reducing outages and improving energy efficiency.

Need for energy independence and resiliency: Particularly in disaster-prone or remote regions, microgrids provide critical backup and localized power supply.

Advancements in peer-to-peer energy trading and blockchain integration, enabling real-time, decentralized energy exchanges.

Key Players and Industry Leaders

The global MaaS market is consolidated, with a few major players commanding substantial market share. Leading companies include:

Schneider Electric – Offers Energy-as-a-Service and microgrid operation tools.

ABB – Provides turnkey solutions with digitized microgrid control platforms.

Siemens AG – Known for its intelligent energy management systems and consultancy services.

Eaton Corporation – Specializes in islanded and grid-tied microgrid operations.

Aggreko, ENGIE, Tech Mahindra, General Electric, and AIO Systems Ltd. also play significant roles in global deployments.

Emerging players such as Green Energy Corp. and Spirae, LLC are also gaining traction by focusing on software innovation and scalable energy management.

Recent Developments

In December 2021, Schneider Electric and Temasek launched GreeNext, a joint venture to deliver hybrid solar-battery microgrids to commercial and industrial clients.

In February 2021, ABB partnered with DEIF, combining control technologies to accelerate renewable energy integration in marine and land-based microgrid applications.

Numerous R&D initiatives are exploring virtual microgrids and blockchain-based energy trading, marking the next phase of energy decentralization.

Access key findings and insights from our Report in this sample -

Latest Market Trends