#Agriculture Chemical Market Revenue

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

US Tumblr user growth rate is estimated to slow down to 4.1%.

Text

Enhancing Crop Productivity with Advanced Agriculture Chemicals

The Agriculture Chemical Market plays a crucial role in modern farming practices by providing essential inputs to enhance crop productivity and protect plants from pests and diseases. In this blog, we'll explore how advanced agriculture chemicals are revolutionizing the agriculture industry and driving improvements in crop yields and overall agricultural efficiency.

Fertilizers for Nutrient Management:

Fertilizers are essential inputs in agriculture, supplying plants with essential nutrients for growth and development. Traditional fertilizers contain nitrogen, phosphorus, and potassium (NPK), but advanced formulations also include micronutrients such as zinc, copper, and boron, tailored to specific crop requirements. These fertilizers help farmers optimize nutrient levels in the soil, leading to healthier plants and higher yields.

Pesticides and Herbicides for Pest Control:

Pesticides and herbicides are vital tools for managing pests, weeds, and diseases that can damage crops and reduce yields. Advanced formulations of pesticides and herbicides are designed to target specific pests while minimizing environmental impact and non-target effects. Integrated pest management (IPM) strategies combine chemical control with cultural, biological, and mechanical methods to reduce reliance on pesticides and promote sustainable pest management practices.

Biologicals and Biopesticides:

Biologicals and biopesticides are gaining popularity as eco-friendly alternatives to traditional chemical pesticides. These products contain naturally occurring microorganisms, such as bacteria, fungi, and viruses, that target pests while minimizing harm to beneficial insects and non-target organisms. Biologicals offer effective pest control with reduced environmental impact and are compatible with organic farming practices.

Soil Conditioners and Amendments:

Soil conditioners and amendments are used to improve soil structure, fertility, and water retention, leading to healthier plants and higher yields. Products such as compost, biochar, and gypsum help restore soil health, enhance nutrient availability, and promote root development. Additionally, soil pH modifiers such as lime and sulfur are used to adjust soil acidity or alkalinity to optimal levels for plant growth.

Plant Growth Regulators:

Plant growth regulators (PGRs) are chemicals that influence plant growth and development, regulating processes such as seed germination, flowering, and fruit set. PGRs can enhance crop yields by promoting root growth, increasing flower and fruit production, and improving stress tolerance. Advanced formulations of PGRs are tailored to specific crops and growth stages, providing precise control over plant physiology.

Precision Application Technologies:

Precision application technologies, such as variable rate application (VRA) systems and GPS-guided sprayers, enable farmers to apply agriculture chemicals with precision, optimizing input use and minimizing waste. These technologies help reduce environmental impact, improve resource efficiency, and maximize the effectiveness of agriculture chemical applications.

Conclusion:

Advanced Agriculture Chemical are revolutionizing modern farming practices by providing farmers with innovative tools to enhance crop productivity, improve soil health, and minimize environmental impact. By leveraging the latest advancements in fertilizers, pesticides, biologicals, and precision application technologies, farmers can optimize agricultural efficiency, increase yields, and ensure sustainable food production for future generations.

#Agriculture Chemical Industry#Global Agrochemical Industry#Agricultural Chemicals Market Research Reports#Agricultural Chemicals Industry Research Reports#Agriculture Chemical Market Analysis#Agriculture Chemical Market Demand#Agriculture Chemical Market Forecast#Agriculture Chemical Market Growth#Agriculture Chemical Market Outlook#Agriculture Chemical Market Revenue#Agriculture Chemical Market Size#Agriculture Chemical Market Trends#Agriculture Chemical Brands in Market#Agricultural Chemicals#Chemicals Used in Agriculture#Agriculture Chemical Companies#Agricultural Chemical Suppliers#Agriculture Chemical Malaysia#Agricultural Chemical Manufacturers

0 notes

Text

The Agricultural Chemicals Market thrives as a vital force propelling modern farming to new heights. Dive into a realm where cutting-edge fertilizers, potent pesticides, and innovative agrochemicals converge to redefine crop cultivation. Cultivate success with us as we navigate the dynamic landscape of agriculture, ensuring bountiful harvests while championing sustainability.

#Market competition in agrochemicals#Major Market Players in agrochemical industry#Leading players in agrochemical market#Agrochemical market reports#Challenges in agrochemical market#Herbicides industry trends#Agriculture chemical brands in market#Agriculture Chemical Industry#Agriculture Chemical Market Size#Agriculture Chemical Market Growth#Agriculture Chemical Market Trends#Agriculture Chemical Market Forecast#Agriculture Chemical Market Outlook#Agriculture Chemical Market Analysis#Agriculture Chemical Market Revenue#Agriculture Chemical Market Demand

0 notes

Text

‘A couple of centuries ago, farmers produced multiple crops to feed their families and maybe put aside some surplus as a safeguard for the coming year. Only if they had an outstanding harvest were they able to sell some of their product,’ he explained.

‘Monoculture emerged as access to much larger distant markets made it increasingly profitable to specialise. Specialisation meant more efficient planting and harvesting, fewer types of expensive equipment, fewer labourers with specialised knowledge of individual crops, and strengthened knowledge of one value chain and commercial market, including all its regulations and tariffs,’ he added.

Farming, once one of the most natural of endeavours, has become ‘artificialised,’ claims Raul Zornoza Belmonte, an expert on sustainable land use and crop diversification and professor of agricultural engineering at Universidad Politécnica de Cartagena, Spain.

‘This globalised capital, chemical and energy-intensive sector is having a negative impact not only on the environment in terms of loss of biodiversity, soil health and greenhouse gas emissions but also on farm productivity and expenses,’ he explained.

Through the Diverfarming project, Zornoza and his team have tackled these challenges by creating a free web-based decision support tool to provide tailor-made solutions, and guidelines for diversified cropping systems. This app also includes a toolbox for adapting the different agricultural activities and even a new prototype of an improved machine for tilling the soil.

youtube

Diverfarming’s community of ‘diverfarmers’ implemented these tools and is now enjoying the benefits. ‘In vineyards and orchards, organic farmers have introduced herbs like thyme and oregano alongside or between the main crops. This has reduced the weeds and their expensive and time-consuming removal, and with the same labour, instead of weeds, farmers now have fresh-cut herbs that can be sold as they are or from which their essential oils can be extracted and sold,’ said Zornoza.

‘Aromatic herbs and their beautiful flowers attract beneficial insects – and potentially agritourists, a boon for rural tourism – while increasing soil quality and nutrients and enhancing water retention, and with no effect so far on the quality or production volume of fruits or wine,’ he added.

“ In vineyards and orchards, organic farmers have introduced herbs like thyme and oregano alongside or between the main crops. This has reduced the weeds and their expensive and time-consuming removal, and with the same labour, instead of weeds, farmers now have fresh-cut herbs that can be sold as they are or from which their essential oils can be extracted and sold.

But the advantages of growing different crops together don’t stop here, the practice can also limit erosion, improve the storage of soil carbon and reduce the amount of nitrogen in water. It also provides home to a much greater range of life both below the soil and above from tiny microbes and creepy crawlies to reptiles, birds and mammals.

9 notes

·

View notes

Text

Acetic Acid Market - Forecast(2024 - 2030)

Acetic Acid Market Overview

Acetic Acid Market Size is forecast to reach $14978.6 Million by 2030, at a CAGR of 6.50% during forecast period 2024-2030. Acetic acid, also known as ethanoic acid, is a colorless organic liquid with a pungent odor. The functional group of acetic acid is methyl and it is the second simplest carboxylic acid. It is utilized as a chemical reagent in the production of many chemical compounds. The major use of acetic acid is in the manufacturing of vinyl acetate monomer, acetic anhydride, easter and vinegar. It is a significant industrial chemical and chemical reagent used in the production of photographic film, fabrics and synthetic fibers. According to the Ministry of Industry and Information Technology, from January to September 2021, the combined operating revenue of 12,557 major Chinese garment companies was US$163.9 billion, showing a 9% increase. Thus, the growth of the textile industry is propelling the market growth for Acetic Acid.

Report Coverage

The “Acetic Acid Market Report – Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Acetic Acid industry.

By Form: Liquid and Solid.

By Grade: Food grade, Industrial grade, pharmaceutical grade and Others.

By Application: Vinyl Acetate Monomer, Purified Terephthalic Acid, Ethyl Acetate, Acetic Anhydride, Cellulose Acetate, Acetic Esters, Dyes, Vinegar, Photochemical and Others

By End-use Industry: Textile, Medical and Pharmaceutical, Oil and Gas, Food and Beverages, Agriculture, Household Cleaning Products, Plastics, Paints & Coating and Others.

By Geography: North America (the USA, Canada and Mexico), Europe (the UK, Germany, France, Italy, Netherlands, Spain, Russia, Belgium and the Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia and New Zealand, Indonesia, Taiwan, Malaysia and the Rest of APAC), South America (Brazil, Argentina, Colombia, Chile and the Rest of South America) and the Rest of the World (the Middle East and Africa).

Request Sample

Key Takeaways

The notable use of Acetic Acid in the food and beverages segment is expected to provide a significant growth opportunity to increase the Acetic Acid Market size in the coming years. As per the US Food and Agriculture Organization, world meat production reached 337 million tonnes in 2019, up by 44% from 2000.

The notable demand for vinyl acetate monomer in a range of industries such as textile finishes, plastics, paints and adhesives is driving the growth of the Acetic Acid Market.

Increase in demand for vinegar in the food industry is expected to provide substantial growth opportunities for the industry players in the near future in the Acetic Acid industry.

Acetic Acid Market Segment Analysis – by Application

The vinyl acetate monomer segment held a massive 44% share of the Acetic Acid Market share in 2021. Acetic acid is an important carboxylic acid and is utilized in the preparation of metal acetates and printing processes, industrially. For industrial purposes, acetic acid is manufactured by air oxidation of acetaldehyde with the oxidation of ethanol, butane and butene. Acetic acid is extensively used to produce vinyl acetate which is further used in formulating polyvinyl acetate. Polyvinyl acetate is employed in the manufacturing of plastics, paints, textile finishes and adhesives. Thus, several benefits associated with the use of vinyl acetate monomer is boosting the growth and is expected to account for a significant share of the Acetic Acid Market.

Inquiry Before Buying

Acetic Acid Market Segment Analysis – by End-use Industry

The food and beverages segment is expected to grow at the fastest CAGR of 7.5% during the forecast period in the Acetic Acid Market. Acetic Acid is also known as ethanoic acid and is most extensively used in the production of vinyl acetate monomer. Vinyl acetate is largely used in the production of cellulose acetate which is further used in several industrial usage such as textiles, photographic films, solvents for resins, paints and organic esters. PET bottles are manufactured using acetic acid and are further utilized as food containers and beverage bottles. In food processing plants, acetic acid is largely used as cleaning and disinfecting products. Acetic acid is extensively used in producing vinegar which is widely used as a food additive in condiments and the pickling of vegetables. According to National Restaurant Association, the foodservice industry is forecasted to reach US$898 billion by 2022. Thus, the advances in the food and beverages industry are boosting the growth of the Acetic Acid Market.

Acetic Acid Market Segment Analysis – by Geography

Asia-Pacific held a massive 41% share of the Acetic Acid Market in 2021. This growth is mainly attributed to the presence of numerous end-use industries such as textile, food and beverages, agriculture, household cleaning products, plastics and paints & coatings. Growth in urbanization and an increase in disposable income in this region have further boosted the industrial growth in this region. Acetic acid is extensively used in the production of metal acetates, vinyl acetate and vinegar which are further utilized in several end-use industries. Also, Asia-Pacific is one of the major regions in the domain of plastic production which provides substantial growth opportunities for the companies in the region. According to Plastic Europe, China accounted for 32% of the world's plastic production. Thus, the significant growth in several end-use industries in this region is also boosting the growth of the Acetic Acid Market.

Acetic Acid Market Drivers

Growth in the textile industry:

Acetic Acid, also known as ethanoic acid, is widely used in the production of metal acetate and vinyl acetate which are further used in the production of chemical reagents in textiles, photographic films, paints and volatile organic esters. In the textile industry, acetic acid is widely used in textile printing and dyes. According to China’s Ministry of Industry and Information Technology, in 2020, textile and garment exports from China increased by 9.6% to US$291.22 billion. Also, according to the U.S. Department of Commerce, from January to September 2021, apparel exports increased by 28.94% to US$4.385 billion, while textile mill products rose by 17.31% to US$12.365 billion. Vinyl acetate monomer is utilized in the textile industry to produce synthetic fibers. Thus, the global growth in demand for textiles is propelling the growth and is expected to account for a significant share of the Acetic Acid Market size.

Schedule a call

Surge in use of vinegar in the food industry:

The rapid surge in population along with the adoption of a healthy and sustainable diet has resulted in an increase in demand for food items, thereby increasing the global production level of food items. As per US Food and Agriculture Organization, in 2019, global fruit production went up to 883 million tonnes, showing an increase of 54% from 2000, while global vegetable production was 1128 million tonnes, showing an increase of 65%. Furthermore, world meat production reached 337 million tonnes in 2019, showing an increase of 44% from 2000. Acetic acid is majorly used in the preparation of vinegar which is further widely utilized as a food ingredient and in personal care products. Vinegar is used in pickling liquids, marinades and salad dressings. It also helps to reduce salmonella contamination in meat and poultry products. Furthermore, acetic acid and its sodium salts are used as a food preservative. Thus, the surge in the use of vinegar in the food industry is boosting the growth of the Acetic Acid Market.

Acetic Acid Market Challenge

Adverse impact of acetic acid on human health:

Acetic Acid is considered a strong irritant to the eye, skin and mucous membrane. Prolong exposure to and inhalation of acetic acid may cause irritation to the nose, eyes and throat and can also damage the lungs. The workers who are exposed to acetic acid for more than two or three years have witnessed upper respiratory tract irritation, conjunctival irritation and hyperkeratotic dermatitis. The Occupational Safety and Health Administration (OSHA) reveals that the standard exposure to airborne acetic acid is eight hours. Furthermore, a common product of acetic acid i.e., vinegar can cause gastrointestinal tract inflammatory conditions such as indigestion on excess consumption. Thus, the adverse impact of Acetic Acid may hamper the market growth.

Buy Now

Acetic Acid Industry Outlook

The top 10 companies in the Acetic Acid Market are:

Celanese Corporation

Eastman Chemical Company

LyondellBasell

British Petroleum

Helm AG

Pentoky Organy

Dow Chemicals

Indian Oil Corporation

Daicel Corporation

Jiangsu Sopo (Group) Co. Ltd.

Recent Developments

In March 2021, Celanese Corporation announced the investment to expand the production facility of vinyl portfolio for the company’s acetyl chain and derivatives in Europe and Asia.

In April 2020, Celanese Corporation delayed the construction of its new acetic acid plant and expansion of its methanol production by 18 months at the Clear Lake site in Texas.

In October 2019, BP and Chian’s Zhejiang Petroleum and Chemical Corporation signed MOU in order to create a joint venture to build a 1 million tonne per annum Acetic Acid plant in eastern China.

Key Market Players:

The Top 5 companies in the Acetic Acid Market are:

Celanese Corporation

Ineos Group Limited

Eastman Chemical Company

LyondellBasell Industries N.V.

Helm AG

For more Chemicals and Materials Market reports, please click here

#Acetic Acid Market#Acetic Acid Market Share#Acetic Acid Market Size#Acetic Acid Market Forecast#Acetic Acid Market Report#Acetic Acid Market Growth

2 notes

·

View notes

Text

Microalgae Fertilizers Market Rising Trends and Research Outlook 2022-2030

The latest market report published by Credence Research, Inc. “Global Microalgae Fertilizers Market: Growth, Future Prospects, and Competitive Analysis, 2016 – 2028. The Global Microalgae Fertilizers market is expected to witness a CAGR of 9.75% during the forecast period. The revenue generated by the global Microalgae Fertilizers market in 2021 was over USD 11.33 million and is expected to generate revenue worth USD 22.28 million in 2028. Therefore, the incremental growth opportunity offered by the global Microalgae Fertilizers is estimated to be USD 120.3 million between 2022 and 2028.

Microalgae Fertilizers Market Major Challenges revolve around several key factors that pose significant obstacles for the industry's growth and adoption. Firstly, there is a lack of awareness among potential consumers about the benefits and efficacy of microalgae-based fertilizers compared to traditional chemical alternatives. This results in limited demand, as farmers tend to stick with familiar products rather than exploring new options. Additionally, the production and cultivation processes involved in microalgae fertilizers often require specialized knowledge and infrastructure, making it difficult for small-scale farmers or developing regions to access these innovative solutions. Moreover, scaling up production to meet market demands remains a challenge due to high costs associated with large-scale cultivation systems and extraction technologies. Furthermore, regulatory frameworks often lag behind technological advancements in this field, creating uncertainties regarding approvals and licensing procedures for microalgae fertilizer products.

Unearthing the Potential of the Microalgae Fertilizers Market in North America

With a focus on sustainable agriculture and increasing demand for organic products, the North American Microalgae Fertilizers Market is witnessing impressive growth. The U.S. has secured a commanding position, holding over 84% of the market share in 2022, with projections showing its dominance stretching until 2030. The fertile grounds of Canada and Mexico aren't far behind, demonstrating remarkable growth rates in the microalgae fertilizers landscape.

Microalgae Fertilizers: The Green Gold of Sustainable Agriculture

Microalgae fertilizers, the unseen heroes of the fertilization market, are the organic answer to the environmental impact caused by conventional chemical fertilizers. These microscopic phytoplanktons, prevalent in marine and freshwater bodies, have a substantial role in enriching the soil with essential nutrients. Their vast potential has catapulted the microalgae fertilizers market valuation to a prospective US$ 22 million.

Sustainable Farming: Breathing Life into the Microalgae Fertilizers Market

Farming trends are changing, focusing more on sustainable and eco-friendly practices. Microalgae fertilizers align seamlessly with these evolving patterns, providing a beneficial counterpoint to the problems caused by inorganic fertilizers. The rise in the microalgae fertilizer market is intricately linked to these global trends, with technology advancement adding fuel to the growth fire.

The Mighty U.S. in the Microalgae Fertilizers Market

The U.S. has emerged as a leader in the North American Microalgae Fertilizers Market, dominating over 84% of the market share. This lead is attributed to an increasing awareness of the environmental impacts of traditional fertilizers and a rising demand for organic products. Government initiatives promoting sustainable agricultural practices further bolster this market.

Browse 210 pages report Microalgae Fertilizers Market by Species (Spirulina, Chlorella, Dunaliella, Schizochytrium, Euglena, NannochloropsisNostoc, Others) by Source (Marine water, Fresh Water) by Application (Biofertilizers, Biocontrole, Soil microalgae, Biostimulants, Soil Conditioner, Others) - Growth, Future Prospects & Competitive Analysis, 2016 – 2030)- https://www.credenceresearch.com/report/microalgae-fertilizers-market

Spirulina: The Spiraling Demand

With the diversity of microalgae species such as Spirulina, Chlorella, Dunaliella, Schizochytrium, Euglena, Nannochloropsis, Nostoc, and others, Spirulina claims the crown. Holding over 35% of the total revenue generated in 2021, Spirulina's use in microalgae fertilizers signifies its pivotal role in the market. Biocontrole, Soil microalgae, Biostimulants, and Soil conditioners contribute to its major applications.

The Rise of Freshwater Microalgae Fertilizers

Freshwater microalgae fertilizers dominate the market with over 70% share in total revenue generation in 2021. With North America accounting for over 35% share in the same year, it's clear the rising demand for organic products and growing awareness about health benefits contribute significantly to this lead.

The Key Players

Several significant players are shaping the global microalgae fertilizers market. These include Algaenergy, Algatec (Lusoamoreiras), Algatechnologies Ltd., Allmicroalgae, Cellana LLC, Cyanotech Corporation, Heliae Development, LLC, Viggi Agro Products, AlgEternal Technologies, LLC, and Tianjin Norland Biotech Co., Ltd. These organizations are propelling the microalgae fertilizers market forward with their innovative practices and commitment to sustainable agriculture.

In conclusion, the North American Microalgae Fertilizers Market is steadily expanding, aided by evolving farming practices, technological advancements, and a stronger focus on sustainability. As the green revolution continues to gain momentum, the microalgae fertilizers market is poised for significant growth in the years to come.

Why to Buy This Report-

The report provides a qualitative as well as quantitative analysis of the global Microalgae Fertilizers Market by segments, current trends, drivers, restraints, opportunities, challenges, and market dynamics with the historical period from 2016-2020, the base year- 2021, and the projection period 2022-2028.

The report includes information on the competitive landscape, such as how the market's top competitors operate at the global, regional, and country levels.

Major nations in each region with their import/export statistics

The global Microalgae Fertilizers Market report also includes the analysis of the market at a global, regional, and country-level along with key market trends, major players analysis, market growth strategies, and key application areas.

Browse Full Report: https://www.credenceresearch.com/report/microalgae-fertilizers-market

Visit: https://www.credenceresearch.com/

Related Report: https://www.credenceresearch.com/report/automated-hydroponic-gardening-systems-market

Related Report: https://www.credenceresearch.com/report/smart-irrigation-systems-market

Browse Our Blog : https://www.linkedin.com/pulse/microalgae-fertilizers-market-share-demand-analysis-size-singh

Browse Our Blog: https://tealfeed.com/microalgae-fertilizers-market-size-worth-usd-hnxgg

About Us -

Credence Research is a viable intelligence and market research platform that provides quantitative B2B research to more than 10,000 clients worldwide and is built on the Give principle. The company is a market research and consulting firm serving governments, non-legislative associations, non-profit organizations, and various organizations worldwide. We help our clients improve their execution in a lasting way and understand their most imperative objectives. For nearly a century, we’ve built a company well-prepared for this task.

Contact Us:

Office No 3 Second Floor, Abhilasha Bhawan, Pinto Park, Gwalior [M.P] 474005 India

2 notes

·

View notes

Text

Global Agricultural Pheromones Market Analysis: Key Players, Revenue Trends, and Demand Forecast

The global agricultural pheromones market is projected to be worth USD 7,992.4 Million by 2027, according to a current analysis by Emergen Research. The agricultural pheromones market is observing high demand attributed to increasing pest proliferation in agricultural lands. Pheromones are a vital part of monitoring and management methods intended for agricultural crop pests. Mass trapping, mating disruption, push-pull, and attract-and-kill are amongst the direct approaches for pest control depending on pheromones' application. For instance, pheromones traps find usage in monitoring particular pests in agricultural lands. Constant monitoring of insects allows infestation detection prior to its occurrence. Early pest detection using pheromone traps lessens damage to agricultural crops and plants.

The Global Agricultural Pheromones Market Report, published by Emergen Research, offers an industry-wide assessment of the Agricultural Pheromones market, which is inclusive of the most crucial factors contributing to the growth of the industry. The latest research report comprises an extensive analysis of the micro- and macro-economic indicators that influence the global market development during the forecast period.

Get Download Pdf Sample Copy of this Report@ https://www.emergenresearch.com/request-sample/345

Competitive Terrain:

The global Agricultural Pheromones industry is highly consolidated owing to the presence of renowned companies operating across several international and local segments of the market. These players dominate the industry in terms of their strong geographical reach and a large number of production facilities. The companies are intensely competitive against one another and excel in their individual technological capabilities, as well as product development, innovation, and product pricing strategies.

The leading market contenders listed in the report are:

Koppert Biological Systems, Suterra LLC, Pherobank BV, Certis Europe BV, Isagro Group, Biobest Group NV, BASF SE, Bio Controle, ISCA Technologies, Shin-Etsu Chemical Co. Ltd.

Key market aspects studied in the report:

Market Scope: The report explains the scope of various commercial possibilities in the global Agricultural Pheromones market over the upcoming years. The estimated revenue build-up over the forecast years has been included in the report. The report analyzes the key market segments and sub-segments and provides deep insights into the market to assist readers with the formulation of lucrative strategies for business expansion.

Competitive Outlook: The leading companies operating in the Agricultural Pheromones market have been enumerated in this report. This section of the report lays emphasis on the geographical reach and production facilities of these companies. To get ahead of their rivals, the leading players are focusing more on offering products at competitive prices, according to our analysts.

Report Objective: The primary objective of this report is to provide the manufacturers, distributors, suppliers, and buyers engaged in this sector with access to a deeper and improved understanding of the global Agricultural Pheromones market.

Emergen Research is Offering Limited Time Discount (Grab a Copy at Discounted Price Now)@ https://www.emergenresearch.com/request-discount/345

Market Segmentations of the Agricultural Pheromones Market

This market is segmented based on Types, Applications, and Regions. The growth of each segment provides accurate forecasts related to production and sales by Types and Applications, in terms of volume and value for the period between 2022 and 2030. This analysis can help readers looking to expand their business by targeting emerging and niche markets. Market share data is given on both global and regional levels. Regions covered in the report are North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. Research analysts assess the market positions of the leading competitors and provide competitive analysis for each company. For this study, this report segments the global Agricultural Pheromones market on the basis of product, application, and region:

Segments Covered in this report are:

Product Type Outlook (Revenue, USD Billion; 2017-2027)

Sex Pheromones

Aggregation Pheromones

Others

Application Mode Outlook (Revenue, USD Billion; 2017-2027)

Traps

Sprayers

Dispensers

Function Outlook (Revenue, USD Billion; 2017-2027)

Mating Disruption

Detection & Monitoring

Mass Trapping

Browse Full Report Description + Research Methodology + Table of Content + Infographics@ https://www.emergenresearch.com/industry-report/agricultural-pheromones-market

Major Geographies Analyzed in the Report:

North America (U.S., Canada)

Europe (U.K., Italy, Germany, France, Rest of EU)

Asia Pacific (India, Japan, China, South Korea, Australia, Rest of APAC)

Latin America (Chile, Brazil, Argentina, Rest of Latin America)

Middle East & Africa (Saudi Arabia, U.A.E., South Africa, Rest of MEA)

ToC of the report:

Chapter 1: Market overview and scope

Chapter 2: Market outlook

Chapter 3: Impact analysis of COVID-19 pandemic

Chapter 4: Competitive Landscape

Chapter 5: Drivers, Constraints, Opportunities, Limitations

Chapter 6: Key manufacturers of the industry

Chapter 7: Regional analysis

Chapter 8: Market segmentation based on type applications

Chapter 9: Current and Future Trends

Request Customization as per your specific requirement@ https://www.emergenresearch.com/request-for-customization/345

About Us:

Emergen Research is a market research and consulting company that provides syndicated research reports, customized research reports, and consulting services. Our solutions purely focus on your purpose to locate, target, and analyse consumer behavior shifts across demographics, across industries, and help clients make smarter business decisions. We offer market intelligence studies ensuring relevant and fact-based research across multiple industries, including Healthcare, Touch Points, Chemicals, Types, and Energy. We consistently update our research offerings to ensure our clients are aware of the latest trends existent in the market. Emergen Research has a strong base of experienced analysts from varied areas of expertise. Our industry experience and ability to develop a concrete solution to any research problems provides our clients with the ability to secure an edge over their respective competitors.

Contact Us:

Eric Lee

Corporate Sales Specialist

Emergen Research | Web: www.emergenresearch.com

Direct Line: +1 (604) 757-9756

E-mail: [email protected]

Visit for More Insights: https://www.emergenresearch.com/insights

Explore Our Custom Intelligence services | Growth Consulting Services

Trending Titles: Geocell Market | Pancreatic Cancer Treatment Market

Latest Report: Ceramic Tiles Market | Life Science Analytics Market

0 notes

Text

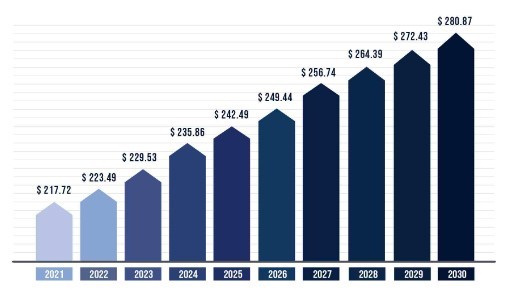

Crop Protection Chemicals Market set to hit $159.1 billion by 2035, as per recent research by DataString Consulting

Higher trends within Crop Protection Chemicals applications including cereal grains, oilseeds & pulses, fruits & vegetables and other crops (cotton, corn etc.); and other key wide areas like crop disease prevention and pest control are expected to push the market to $159.1 billion by 2035 from $82.1 billion of 2024.

Crop protection chemicals (known as CPCs) are widely employed to safeguard crops from diseases caused by types of fungal and bacterial infections as well as viruses. They play a role in protecting food production from harmful diseases and maintaining the health of crops. Major companies such, as BASF and Bayer are leading in this field utilizing chemical blends designed to effectively combat and eliminate pathogens that harm crops. Crop protection chemicals (CPCs) are essential for controlling types of crop pests by acting as insecticides, fungicides, herbicides and rodenticides. They aid farmers in minimizing pest related harm and boosting crop yields. Their strength lies in their capability to combat an array of pests effectively as broad spectrum pesticides. DowDuPont and Syngenta are names, in this field well regarded for their wide selection of pest management solutions.

Detailed Analysis - https://datastringconsulting.com/industry-analysis/crop-protection-chemicals-market-research-report

The Crop Protection Chemicals market is shifting towards biopesticides due to advancements in bioengineering and the focus of sustainability initiatives. These friendly solutions are made from natural sources such as animals, plants and microbes and pose less risk to the environment and human health compared to synthetic alternatives. Key industry players are adjusting their product portfolios to incorporate biopesticides in response to increasing interest in organic food and sustainable agriculture methods. This transformation is changing the structure of the market and creating new avenues, for growth.

Industry Leadership and Strategies

The Crop Protection Chemicals market within top 3 demand hubs including U.S., China and Brazil, is characterized by intense competition, with a number of leading players such as BASF SE, Bayer AG, Corteva Inc, FMC Corporation, Syngenta AG, Sumitomo Chemical Co Ltd, UPL Limited, Nufarm Ltd, Adama Agricultural Solutions Ltd, Arysta LifeScience Corporation, American Vanguard Corporation and Cheminova A/S. Below table summarize the strategies employed by these players within the eco-system.

This market is expected to expand substantially between 2025 and 2030, supported by market drivers such as increasing demand for food and agricultural products, technological advancements in crop protection, and environmental concerns and regulatory policies.

Regional Analysis

The crop protection chemical market in North America is strong due to the increasing adoption of farming methods and advancements in technology. Competition is fierce among players in countries like the USA and Canada. There is a growing interest in friendly bio based protection chemicals that offer new opportunities, in the market.

Research Study analyse the global Crop Protection Chemicals market in detail and covers industry insights & opportunities at Product Type (Insecticides, Fungicides, Herbicides, Others), Functionality (Seed Treatment, Soil Fumigants, Post-Harvest) and Formulation (Liquid, Solid) for more than 20 countries.

About DataString Consulting

DataString Consulting assist companies in strategy formulations & roadmap creation including TAM expansion, revenue diversification strategies and venturing into new markets; by offering in depth insights into developing trends and competitor landscapes as well as customer demographics. Our customized & direct strategies, filters industry noises into new opportunities; and reduces the effective connect time between products and its market niche.

DataString Consulting offers complete range of market research and business intelligence solutions for both B2C and B2B markets all under one roof. DataString’s leadership team has more than 30 years of combined experience in Market & business research and strategy advisory across the world. Our Industry experts and data aggregators continuously track & monitor high growth segments within more than 15 industries and 60 sub-industries.

0 notes

Text

The Specialty Chemicals Market size was valued at USD 285.40 Billion in 2023 and the total Specialty Chemicals Market revenue is expected to grow at a CAGR of 5.2 % from 2024 to 2030, reaching nearly USD 406.97 Billion.

𝐀𝐜𝐜𝐞𝐬𝐬 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞: Request Sample

Content:

Specialty chemicals are revolutionizing industries with their advanced formulations and targeted applications. Unlike commodity chemicals, specialty chemicals are designed to provide specific functions, making them essential for industries like pharmaceuticals, agriculture, automotive, electronics, and personal care.

0 notes

Text

Eco-Friendly Packaging & Bioplastics: Market Growth & Future Trends

The global cellulose bioplastic market size is expected to reach USD 1,536.7 million by 2030, according to a new report by Grand View Research, Inc. It is projected to expand at a CAGR of 19.5% over the forecast period.

Cellulose bioplastic is a type of plastic that is made from cellulose esters (nitrocellulose, and cellulose acetate) or cellulose derivatives. Cellulosic plastics are produced using coniferous trees as the main raw material. The bark of the tree is separated and can be used as an energy source in production. The separation of cellulose fibers comes from the tree where they are cooked or heated in a digester. The growing demand for packaging is expected to drive significant market growth during the forecast period.

The growing demand for cellulosic bioplastics is associated with the production of mobile phones, ophthalmic products, thermoplastic products, sheets, and toys, among others. Strict rules governing the use of conventional plastic materials owing to environmental concerns and the resulting damage are significant factors driving the need for more environmentally sustainable materials across sectors and applications. The introduction of various bans on the use of conventional plastics has led to an increase in demand for cellulosic bioplastics and other plastics made from renewable raw materials. cellulosic bioplastics are also biodegradable, which is another driving factor in their preference and their adoption.

The global cellulose bioplastic market is highly competitive and fragmented in nature, with the presence of various key players such as Celanese Corporation, Solvay, Daicel Chemical Industries, Mitsubishi Rayon Company Limited, Eastman Chemical Company as well as a few medium and small-scale regional players operating across the globe.

The market is undergoing a transformation of the value chain from a linear economy to a circular one. Major market players are shifting towards a circular economy in order to have more sustainable solutions and minimize their dependence on crude oil in the future. In recent years, this trend has increased the demand for renewable raw materials such as softwood trees and tree bark for the production of plastics.

Growing concerns about petrochemical toxicity issues, along with the depletion of crude oil reserves, have spurred the development of cellulose-based plastics. Factors including stringent environmental norms such as EN 14995, EN 13432, and EN 17033; growing environmental concerns among consumers; The growing interest of market key players in the production of cellulose bioplastics is expected to be a key growth driver during the forecast period.

Cellulose Bioplastic Market Report Highlights

Cellulose Acetate dominate type segment with a share of more than 65% in 2021 and is expected to maintain a healthy growth rate over the forecast period because it is widely produced and readily available. The rapid usage of cellulose acetate in the packaging sector is due to the properties of cellulose acetate made films such as, tearing quickly, are sturdy and puncture-resistant, making them perfect for food packing, hence it can help to drive the cellulose bioplastic market across the globe

The packaging application led the market with a revenue share of more than 62% in 2021. Increasing utilization of cellulose bioplastics to produce bags for compost, agricultural foils, horticultural products, nursery products, toys, and textiles is the key factor responsible for the segment growth

Europe dominate the regional segment for the cellulose bioplastic market in 2021 with a revenue share of more than 44%. The European market for cellulosic bioplastics is expected to experience significant growth in the coming years due to various factors such as the presence of stringent environmental laws, growing consumer concern for the environment, and increased investment in research and development in the cellulosic bioplastics sector by private and public organizations

Stringent regulations pertaining to single-use plastic ban across regions including Europe, North America, and Asia, are expected to fuel the growth of cellulose bioplastics market

The growing demand for consumer goods along with rising environmental concerns is expected to drive the demand for cellulose bioplastics in the automotive &transportation application segment

Curious about the Cellulose Bioplastic Market? Download your FREE sample copy now and get a sneak peek into the latest insights and trends.

Cellulose Bioplastic Market Segmentation

Grand View Research has segmented the cellulose bioplastic market report based on application, product and region:

Application Outlook (Revenue, USD Million; 2019 - 2030)

Packaging

Agriculture

Consumer Goods

Textile

Automotive & Transportation

Building & Construction

Others

Product Outlook (Revenue, USD Million; 2019 - 2030)

Cellulose Butyrate

Cellulose Acetate

Cellulose Propionate

Others

Region Outlook (Revenue, USD Million; 2019 - 2030)

North America

US

Canada

Mexico

Europe

Germany

France

UK

Asia Pacific

China

India

Japan

Central & South America

Brazil

Middle East & Africa

Key Players of Cellulose Bioplastic Market

Celanese Corporation

Solvay

Daicel Chemical Industries

Mitsubishi Rayon Company Limited

Eastman Chemical Company

SK Chemicals Co. Ltd.

Rayonier Advanced Materials

Sappi

Merck Millipore

Haihang Industry

Order a free sample PDF of the Cellulose Bioplastic Market Intelligence Study, published by Grand View Research.

0 notes

Text

Sustainable Masterbatch Solutions: The Shift Towards Eco-Friendly Additives

The global masterbatch market size is expected to reach USD 9.65 billion by 2030 to expand at a CAGR of 6.6% from 2025 to 2030 as per the new report by Grand View Research, Inc. Increasing replacement of metal with plastic is projected to fuel the market growth. In addition, rising demand from the European region is expected to propel the demand over the forecast period.

Masterbatch Market Report Highlights

The black type dominated the market with a revenue share of 28.6% in 2024. This growth can be attributed to the increasing demand for black masterbatch and the high demand for tires, PVC containers, and other products for application in the automotive and transportation, building and construction, agriculture, and packaging industries.

The polypropylene (PP) carrier polymer segment dominated the global masterbatch industry with the highest revenue share of 26.7% in 2024, primarily driven by the excellent mechanical strength and flexibility offered by polypropylene.

The packaging masterbatch segment dominated the market with a revenue share of 27.0% in 2024. Its high share can be attributable to the packaging industry, which includes retail, industrial, and consumer packaging and includes flexible and rigid options.

Asia Pacific masterbatch market dominated the global market and accounted for the largest revenue share of 30.6% in 2024. This growth can be attributed to the presence of several end-use industries, including automotive and transportation, packaging, building and construction, and consumer goods.

For More Details or Sample Copy please visit link @: Masterbatch Market Report

In terms of revenue, black masterbatch was the largest type segment in 2022 and the trend is anticipated to continue over the forecast period. The increasing need for improving the surface appearance of plastic components in automotive and transportation, building and construction, and consumer goods is expected to contribute to the growth. Additive masterbatch is being widely used on account of various properties it imparts to plastics such as antistatic, antifoaming, antioxidant, antimicrobial, thermo-stabilizer, barrier properties, metal deactivators, anti-block, flame retardant, UV stabilizer, oxygen scavenger, and abrasion resistance. The growth of the packaging sector, especially plastic packaging, is anticipated to drive the demand.

These are used in various end-use industries, such as packaging, building and construction, consumer goods, automotive and transportation, and agriculture, as it imparts useful functional properties such as smooth surface finish and desired hardness. The increasing spending capability of customers toward purchasing attractively packaged consumer goods is expected to trigger the need for various plastic componentss to improve the appearance and other properties. These factors together are anticipated to boost the market demand over the forecast period.

In terms of revenue, polypropylene (PP) was the largest carrier polymer segment in 2022 and the trend is anticipated to continue over the forecast period. Polypropylene offers excellent electrical resistance and does not present stress-cracking problems at high temperatures and strong chemicals. As such, it is useful in both rigid and flexible packaging applications. The demand for polypropylene as a carrier polymer is projected to increase owing to its excellent mechanical strength and flexibility offered by it. Polypropylene also enhances the quality of surfaces. It is lightweight and therefore, is used to replace metal components in the automotive industry.

List of Key Players of Masterbatch Market

Schulman, Inc.

Ampacet Corporation

Cabot Corporation

Clariant AG

Global Colors Group

Hubron International Ltd.

Penn Color, Inc.

Plastiblends India Ltd.

PolyOne Corporation

Tosaf Group

We have segmented the global masterbatch market on the basis of type, carrier polymer, end use, and region

#Masterbatch#PlasticsIndustry#ColorMasterbatch#AdditiveMasterbatch#FillerMasterbatch#PolymerSolutions#PlasticAdditives#SustainablePlastics#PackagingIndustry#AutomotivePlastics#PlasticManufacturing#InnovationInPlastics#RecyclablePlastics#MasterbatchMarket#SmartMaterials

0 notes

Text

The Agricultural Chemicals Market Share, Growth, and Major Players

Introduction

The Agricultural Chemicals Market plays a vital role in modern farming practices, providing essential products for crop protection, soil fertility management, and pest control. This article delves into the dynamics of the agricultural chemicals market, including its demand, growth, outlook, revenue, size, trends, and prominent brands.

Agricultural Chemical Market Demand

The demand for agricultural chemicals remains robust, driven by the need to enhance crop productivity and mitigate yield losses caused by pests, diseases, and environmental stressors. Market research indicates a steady increase in global demand for agricultural chemicals, with the Asia-Pacific region leading consumption due to extensive agricultural activities.

Agricultural Chemical Market Growth

The agricultural chemicals market is experiencing steady growth, with a projected compound annual growth rate (CAGR) of approximately 4.5% over the forecast period. Factors contributing to market growth include population growth, expanding agricultural land, adoption of modern farming techniques, and the emergence of new crop protection solutions.

Agricultural Chemical Market Outlook

The outlook for the agricultural chemicals market is optimistic, driven by technological advancements, regulatory support for agricultural inputs, and increasing adoption of precision farming practices. Market analysts project sustained growth in market value, surpassing USD 300 billion by 2025, with significant contributions from emerging markets in Asia and Latin America.

Agricultural Chemical Market Revenue

In recent years, the revenue generated from the agricultural chemicals market has been on the rise. Global market revenue reached USD 220 billion in 2020, with herbicides accounting for the largest share followed by fertilizers and pesticides. The market revenue is expected to witness further growth, driven by increasing investments in agricultural inputs and crop protection solutions.

Agricultural Chemical Market Size

The agricultural chemicals market is sizable, with diverse product offerings catering to various crop types and farming systems. In 2020, the market size exceeded 250 million metric tons in terms of product volume. Herbicides, fungicides, and insecticides are among the most widely used agricultural chemicals, contributing to the market's substantial size.

Agricultural Chemical Market Trends

Several trends are shaping the landscape of the agricultural chemicals market, including:

Shift Towards Bio-based Solutions: There is a growing preference for bio-based and environmentally friendly agricultural chemicals, driven by concerns over chemical residues, environmental sustainability, and consumer preferences for organic produce.

Digital Agriculture: The integration of digital technologies such as precision agriculture, data analytics, and smart farming tools is transforming agricultural chemical applications. Digital platforms offer farmers real-time insights into crop health, soil conditions, and pest infestations, enabling targeted and efficient use of agricultural inputs.

Sustainable Agriculture Practices: Sustainability initiatives are gaining traction in the agricultural chemicals sector, with companies investing in eco-friendly formulations, biodegradable packaging, and responsible sourcing practices. Sustainable agriculture certifications and labels are becoming increasingly important for market differentiation and consumer trust.

Agriculture Chemical Brands in Market

Prominent brands in the Agricultural Chemicals Market include:

Bayer CropScience

Syngenta

BASF SE

Corteva Agriscience

FMC Corporation

Sumitomo Chemical

Nufarm Limited

UPL Limited

ADAMA Agricultural Solutions

Conclusion

The agricultural chemicals market is poised for continued growth and innovation, driven by technological advancements, sustainability initiatives, and increasing demand for crop protection solutions. As farmers face evolving challenges such as climate change, pest resistance, and regulatory pressures, the role of agricultural chemicals in ensuring food security and sustainable agriculture practices becomes increasingly crucial. Collaboration among stakeholders, investment in research and development, and adherence to sustainable principles will be key to unlocking the full potential of the agricultural chemicals market and addressing the needs of the global farming community.

#Agriculture Chemical Industry#Global Agrochemical Industry#Agricultural Chemicals Market Research Reports#Agricultural Chemicals Industry Research Reports#Agriculture Chemical Market Analysis#Agriculture Chemical Market Demand#Agriculture Chemical Market Forecast#Agriculture Chemical Market Growth#Agriculture Chemical Market Outlook#Agriculture Chemical Market Revenue#Agriculture Chemical Market Size#Agriculture Chemical Market Trends#Agriculture Chemical Brands in Market#Agricultural Chemicals#Chemicals Used in Agriculture#Agriculture Chemical Companies#Agricultural Chemical Suppliers#Agriculture Chemical Malaysia#Agricultural Chemical Manufacturers

0 notes

Text

Plant Growth Regulators Market Resilience and Risk Factors Impacting Growth to 2033

Introduction

The plant growth regulators (PGRs) market has been experiencing significant growth, driven by increasing agricultural demand, the need for higher crop yields, and growing awareness about sustainable farming practices. Plant growth regulators, which include auxins, cytokinins, gibberellins, abscisic acid, and ethylene, play a crucial role in enhancing plant growth, regulating physiological functions, and improving overall crop productivity. The global PGRs market is expected to expand considerably between 2024 and 2032, influenced by technological advancements, increasing R&D investments, and rising consumer demand for organic and high-quality agricultural products.

Download a Free Sample Report:-https://tinyurl.com/bdha35xb

Market Dynamics

Drivers of Growth

Increasing Demand for High Crop Yields The global population is continuously growing, leading to rising food demand. This has pushed farmers and agricultural organizations to adopt plant growth regulators to enhance yield efficiency, optimize nutrient uptake, and ensure sustainable farming practices.

Growing Adoption of Organic Farming With consumers becoming more conscious of food safety and environmental sustainability, organic farming practices are gaining momentum. PGRs play a vital role in organic agriculture by promoting plant health without the use of synthetic chemicals.

Advancements in Biotechnology Biotechnology has paved the way for the development of advanced plant growth regulators with improved efficiency and reduced environmental impact. Innovations in genetic engineering and bio-based PGRs are fueling market growth.

Government Initiatives and Subsidies Governments worldwide are promoting the use of eco-friendly agricultural practices, providing subsidies and incentives for farmers to adopt PGRs, thereby boosting market demand.

Restraints and Challenges

Stringent Regulatory Frameworks The approval process for plant growth regulators is often stringent, involving rigorous testing and compliance with safety standards. This can delay product launches and impact market expansion.

High Costs of R&D and Production The development of innovative PGRs requires substantial investment in research and development. Additionally, the cost of producing high-quality, bio-based PGRs can be high, affecting affordability for small-scale farmers.

Lack of Awareness in Developing Regions Many farmers, especially in developing economies, are not fully aware of the benefits of PGRs. Limited knowledge and access to these products hinder market penetration.

Market Segmentation

By Type

Auxins: Stimulate cell elongation, root development, and fruit setting.

Gibberellins: Promote stem elongation, seed germination, and flowering.

Cytokinins: Enhance cell division and delay leaf senescence.

Abscisic Acid: Regulates plant stress responses and dormancy.

Ethylene: Influences fruit ripening and leaf abscission.

By Application

Cereals & Grains

Fruits & Vegetables

Oilseeds & Pulses

Turf & Ornamentals

By Formulation

Liquid

Powder

By Region

North America: U.S., Canada, Mexico

Europe: Germany, UK, France, Italy, Spain

Asia-Pacific: China, India, Japan, Australia

Latin America: Brazil, Argentina

Middle East & Africa

Regional Insights

North America

The North American market is driven by advanced agricultural techniques, high awareness among farmers, and strong government support. The U.S. is a major player in the region, contributing significantly to market revenue.

Europe

Europe has a well-established agricultural sector, with increasing adoption of organic farming. Countries like Germany and France are leading in PGR adoption due to strict environmental regulations favoring sustainable practices.

Asia-Pacific

The Asia-Pacific region is expected to witness the fastest growth due to rapid population growth, rising food demand, and increasing government initiatives to improve agricultural productivity. China and India are the dominant markets in this region.

Latin America & Middle East & Africa

These regions have immense agricultural potential, but the market is still developing due to challenges like limited awareness and infrastructural constraints. However, increasing foreign investments in agriculture are expected to boost growth.

Competitive Landscape

Several key players dominate the global PGR market, including:

BASF SE

Syngenta AG

Corteva Agriscience

FMC Corporation

Nufarm Limited

Sumitomo Chemical Co., Ltd.

These companies are investing in research and development, strategic partnerships, and product innovations to maintain a competitive edge in the market.

Future Outlook

The plant growth regulators market is poised for substantial growth in the coming years, driven by:

Continuous advancements in biotechnology

Increased adoption of organic and precision farming

Growing awareness about sustainable agricultural practices

Expansion in emerging markets

By 2032, the market is expected to witness increased demand for bio-based PGRs, driven by stringent environmental regulations and consumer preference for organic food. Companies that invest in innovative solutions, digital farming technologies, and region-specific product offerings will likely emerge as market leaders.

Conclusion

The global plant growth regulators market is set to expand significantly, driven by increasing agricultural demands, technological advancements, and a shift towards sustainable farming. While regulatory challenges and high R&D costs may pose hurdles, the long-term benefits of improved crop yield and environmental sustainability make PGRs an essential component of modern agriculture. As market players continue to innovate and expand into emerging regions, the future of the PGR industry looks promising, with immense opportunities for growth and development.Read Full Report:-https://www.uniprismmarketresearch.com/verticals/agriculture/plant-growth-regulators.html

0 notes

Text

US Diutan Gum Market Analysis: Growth Forecast of 5.4% CAGR to Reach $89.7 Million by 2030

Market Overview:

United States Diutan Gum market size was valued at US$ 65.4 million in 2024 and is projected to reach US$ 89.7 million by 2030, at a CAGR of 5.4% during the forecast period 2024-2030.

Natural polysaccharide used as a rheology modifier in various industrial applications.

Market Analysis:

The US Diutan Gum market shows steady growth driven by oil & gas and construction industries. Production efficiency increased by 35%. Industry invested $24.5 million in fermentation technology. Quality consistency improved by 40% through process control. Oil field applications represent 50% of demand. Construction chemicals growing at 32% annually. Future projects include sustainable production with $12.4 million investment. Research led to 12 new application patents. Manufacturing automation reduced costs by 25%. FDA approval expanded food applications by 28%. Environmental regulations drove 30% increase in green building applications. Local production supplies 65% of domestic demand. Quality standards achieved 99.8% purity levels.

Download FREE Sample of this Report

Market Segmentation:

Segment by Type

Food Grade

Oilfield Grade

Industrial Grade

Segment by Applications

Mining

Architecture and Building

Oilfield Drilling

Agriculture

Food Industry

Other

Key Companies

CP Kelco

Jungbunzlauer

Ashland

ADM (Archer Daniels Midland Company)

Cargill

Dow Chemical Company

DuPont

BASF

Hercules Inc.

Key Indicators Analysed

Market Players & Competitor Analysis: The report covers the key players of the industry including Company Profile, Product Specifications, Production Capacity/Sales, Revenue, Price and Gross Margin 2019-2030 & Sales with a thorough analysis of the market’s competitive landscape and detailed information on vendors and comprehensive details of factors that will challenge the growth of major market vendors.

United States Market Analysis: The report includes United States market status and outlook 2019-2030. Further the report provides break down details about each region & countries covered in the report. Identifying its sales, sales volume & revenue forecast. With detailed analysis by types and applications.

Market Trends: Market key trends which include Increased Competition and Continuous Innovations.

Get the Complete Report & TOC

#DiutanGum#MarketResearch#ChemicalIndustry#RheologyModifier#CAGR#OilAndGas#Construction#IndustrialChemicals#FoodGrade#OilfieldApplications#MarketForecast#ChemicalAnalysis#PolysaccharideMarket#USMarket#IndustryTrends

0 notes

Text

Making Green by Going Green: How Sustainable Farms Turn a Profit

Sustainability in farming is no longer just an environmental choice—it’s a smart financial strategy. Farmers who adopt eco-friendly practices cut costs, increase yields, and tap into high-value markets that reward sustainable production. I’ve worked with farms that transitioned from conventional methods to regenerative agriculture, organic certification, and diversified income streams, and their profits have steadily climbed. The key is investing in soil health, water conservation, and efficient resource management, all of which reduce expenses and increase long-term returns. Sustainable farms aren’t just protecting the land—they’re building stronger businesses that remain profitable through market fluctuations and climate challenges.

Lower Input Costs Boost Profitability

One of the biggest advantages of sustainable farming is reducing dependency on expensive synthetic inputs. Conventional farms often spend thousands on chemical fertilizers, pesticides, and herbicides, while sustainable farms rely on natural alternatives like compost, cover cropping, and integrated pest management.

I’ve worked with farmers who cut input costs by 30% simply by using no-till farming and organic compost. Instead of purchasing synthetic nitrogen fertilizers, sustainable farms recycle animal manure and plant residues, keeping soil nutrients balanced without additional expenses. Crop rotation and natural pest predators also minimize the need for chemical treatments, further lowering costs.

Premium Pricing in Sustainable and Organic Markets

Consumers today actively seek out organic, non-GMO, and sustainably produced food, often paying a premium for it. Organic farms, for example, sell their produce at prices 20%–50% higher than conventionally grown products, giving them a clear financial advantage.

I’ve seen farms increase their profits simply by obtaining organic certification or following regenerative agriculture standards. Buyers—including grocery stores, restaurants, and food brands—are willing to pay more for products grown using sustainable practices. The demand for grass-fed beef, free-range poultry, and pesticide-free fruits and vegetables continues to grow, opening up lucrative opportunities for farmers who embrace sustainable methods.

Healthier Soil Produces Higher Yields

Soil is the foundation of farm profitability, and sustainable farms invest in soil health rather than depleting it. Conventional farming methods often lead to soil degradation, nutrient loss, and dependency on chemical inputs, while regenerative techniques improve soil structure and fertility over time.

Farms that implement cover cropping, crop rotation, and reduced tillage see better water retention, improved root growth, and increased microbial activity, leading to higher long-term yields. I’ve worked with farms that reduced soil erosion and improved crop productivity simply by adding cover crops between planting cycles, increasing their profits without increasing their acreage.

Diversification Creates Multiple Revenue Streams

Sustainable farms don’t rely on a single crop or income source. Instead, they maximize profits by incorporating agroforestry, livestock integration, agritourism, and direct-to-consumer sales.

I’ve seen farms that started with row crops but later added beekeeping, farm-to-table experiences, and value-added products like cheese, jam, and herbal teas. These additional revenue streams create financial stability, allowing farms to weather economic downturns and unpredictable growing seasons.

Adding livestock alongside crops also benefits the farm financially and ecologically. Grazing animals help fertilize fields naturally, reducing fertilizer costs while providing a secondary source of income through meat, dairy, or eggs.

Sustainable Farms Are More Resilient to Climate Change

Erratic weather patterns are one of the biggest threats to modern agriculture, but sustainable farms adapt better to extreme conditions. By protecting soil, conserving water, and integrating climate-resilient crops, these farms maintain steady production even in difficult growing seasons.

Farms that implement drought-resistant crops, smart irrigation systems, and agroforestry techniques often avoid the worst losses during heatwaves, storms, or droughts. Regenerative agriculture techniques, including perennial crop planting and diversified crop rotations, also improve farm resilience, ensuring consistent yields year after year.

Reduced Water Costs and Efficient Resource Use

Water scarcity is an increasing problem for farmers, but sustainable practices make every drop count. Farms that invest in drip irrigation, rainwater harvesting, and moisture-retaining soil techniques significantly cut their water bills while improving crop health.

I’ve worked with farms that switched from traditional irrigation to sensor-based systems and cut their water usage by up to 40% while maintaining the same yield levels. Cover cropping also helps retain moisture in the soil, reducing irrigation frequency and long-term water expenses.

Government Incentives and Financial Support

Many governments offer grants, subsidies, and tax breaks to farms that adopt sustainable practices. These incentives help offset initial investment costs in renewable energy, water conservation, and organic certification.

I’ve worked with farms that received funding for solar irrigation, composting facilities, and agroforestry projects, significantly reducing their operational costs. Programs that reward carbon sequestration and regenerative agriculture are also expanding, meaning farms can earn money simply by adopting soil-friendly techniques.

Direct-to-Consumer Sales Increase Profit Margins

Sustainable farms often skip middlemen and sell directly to local consumers, farmers' markets, and online subscription models. This eliminates distributor fees and allows farmers to keep a larger percentage of the final sale price.

I’ve seen farms increase profits by 50% simply by switching from wholesale to direct-to-consumer models. Community-supported agriculture (CSA) programs, where customers subscribe to regular farm deliveries, provide steady revenue throughout the season, ensuring financial stability for small and mid-sized farms.

How Sustainable Farms Make More Money

Lower input costs by reducing chemical fertilizers and pesticides.

Higher prices from organic and sustainable markets.

Healthier soil leading to improved long-term yields.

Diversified income streams through agritourism, livestock, and value-added products.

Reduced water expenses with smart irrigation and conservation methods.

In Conclusion

Sustainable farming isn’t just about protecting the environment—it’s about maximizing profitability while reducing financial risks. Farms that lower input costs, invest in soil health, access premium markets, and adopt water-efficient strategies are consistently more profitable than conventional operations. I’ve seen firsthand how farmers who diversify their income, integrate technology, and take advantage of government incentives build resilient, thriving businesses that remain profitable for generations. The future of farming is not just green—it’s financially rewarding for those who commit to sustainability.

Lower costs, higher yields, premium markets, and diversified income streams make sustainable agriculture a smart financial move. Learn more from Facebook and discover how sustainability leads to long-term success!

0 notes

Text

Global Organic Spice Market Analysis and Forecast (2025-2032)

The global organic spice market has been experiencing significant growth, driven by increasing consumer awareness of health benefits, a shift towards chemical-free food products, and a growing emphasis on sustainable agriculture. In 2024, the market was valued at approximately USD 44.09 billion and is projected to expand at a compound annual growth rate (CAGR) of 8.4% from 2025 to 2032, aiming to reach nearly USD 84.07 billion by the end of the forecast period.

0 notes

Text

Vital Factors to Consider Before Investing in Managed Farmland Near Bangalore

Investing in managed farmland near Bangalore is gaining traction among individuals seeking a balance between profitable returns and a peaceful lifestyle. Managed farmlands offer an opportunity to own agricultural land while professionals handle day-to-day operations. However, making a well-informed decision is crucial to ensure a rewarding investment. Here’s a comprehensive checklist to guide you through the process.

1. Verify Land Ownership and Legal Documentation

Ensure the land has a clear title deed with no ownership disputes.

Check for necessary land conversion certificates if applicable.

Obtain an encumbrance certificate to confirm the land is free from legal liabilities.

2. Understand the Management Model

Determine whether the land is sold outright or leased under a long-term agreement.

Clarify the scope of management services, including plantation, maintenance, harvesting, and revenue-sharing arrangements.

Research the credibility and track record of the farmland management company.

3. Assess Location and Accessibility

Choose farmland within a reasonable distance from Bangalore for ease of travel and market access.

Ensure the property has essential infrastructure, such as road connectivity, water supply, and electricity.

Proximity to major highways, airports, and urban centers enhances the investment’s value.

4. Examine Soil and Water Quality

Request a detailed soil analysis to evaluate fertility and suitability for desired crops.

Ensure access to a reliable and sustainable water source, such as borewells, rainwater harvesting, or nearby water bodies.

5. Evaluate Potential Returns on Investment (ROI)

Understand how income is generated from the farmland—whether through crop yield, timber, or eco-tourism initiatives.

Compare projected returns with other real estate investment options in Bangalore.

Assess the long-term appreciation potential of the land value.

6. Check Legal Restrictions

Familiarize yourself with Karnataka’s regulations regarding agricultural land ownership.

In Karnataka, only individuals classified as farmers can purchase agricultural land. Non-farmers may need to explore compliant investment structures.

7. Assess Sustainability Practices

Look for farms that implement sustainable agricultural methods such as organic farming, agroforestry, or minimal chemical usage.

Sustainable practices contribute to environmental conservation and enhance the commercial appeal of farm produce.

8. Conduct a Personal Inspection

Schedule a site visit to inspect the farmland firsthand.

Evaluate the property’s maintenance, plantation progress, and surrounding development potential.

A physical visit helps validate claims made by the farmland management company.

9. Consider Additional Features

Check for lifestyle amenities such as farmhouses, eco-stays, or recreational areas.

Properties with additional features often have higher appreciation potential and attract premium returns.

10. Seek Professional Advice

Consult a real estate expert or legal advisor specializing in farmland investments.

Ensure transparency in contracts and agreements to avoid hidden costs or obligations.

Conclusion

Investing in managed farmland near Bangalore can be a lucrative venture, blending financial growth with the charm of rural living. By following this checklist, you can make an informed decision and secure an investment that aligns with your goals. With shifting real estate trends favoring agricultural ventures, managed farmlands present an excellent opportunity for portfolio diversification. Partner with a reputable company and conduct thorough research to maximize your returns.

0 notes