#5G Base Station Market Demand

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

The total number of visits Tumblr.com received during January 2021 is 327 million.

Text

5G Base Station Market Gaining Momentum with Positive External Factors

Global 5G Base Station Market Report from AMA Research highlights deep analysis on market characteristics, sizing, estimates and growth by segmentation, regional breakdowns & country along with competitive landscape, player’s market shares, and strategies that are key in the market. The exploration provides a 360° view and insights, highlighting major outcomes of the industry. These insights help the business decision-makers to formulate better business plans and make informed decisions to improved profitability. In addition, the study helps venture or private players in understanding the companies in more detail to make better informed decisions. Major Players in This Report Include, Ericsson (Sweden), Samsung (South Korea), Cisco (United States), ZTE (China), Nokia (Finland), Huawei (China). Free Sample Report + All Related Graphs & Charts @: https://www.advancemarketanalytics.com/sample-report/102566-global-5g-base-station-market The global 5G Base Station market is expected to witness high demand in the forecasted period due to a rise in the number of IoT devices and adoption of edge computing, the surge in demand for content streaming services, and an increase in demand for low latency connectivity in industrial automation. A base station in the wireless world is a device that connects other wireless devices to a central hub. It is a wireless receiver and short-range transceiver that consists of an antenna and analog-to-digital converters (ADCs) to convert the RF signals into digital and back again. These new 5G network architectures incorporating massive MIMO antennas are pushing always-on connectivity to the outer edges of the cellular network. Market Drivers

High Demand due to Quality User Experience and Enhanced Connectivity

Increasing Need for High-Speed Internet for Integrating Advanced Technologies

Market Trend

Increasing Demand due to Improvement in Network Signal

Rising Demand from Smart Farming

Opportunities

Increasing Demand From Different Business Verticals

Growth of IoT Technology Would Offer New Opportunities for 5G Infrastructure

Enquire for customization in Report @: https://www.advancemarketanalytics.com/enquiry-before-buy/102566-global-5g-base-station-market In this research study, the prime factors that are impelling the growth of the Global 5G Base Station market report have been studied thoroughly in a bid to estimate the overall value and the size of this market by the end of the forecast period. The impact of the driving forces, limitations, challenges, and opportunities has been examined extensively. The key trends that manage the interest of the customers have also been interpreted accurately for the benefit of the readers. The 5G Base Station market study is being classified by Type (Femtocell, Pico Cell, Micro Cell), Application (Smart Home, Autonomous Driving, Smart Cities, Industrial IoT, Smart Farming) The report concludes with in-depth details on the business operations and financial structure of leading vendors in the Global 5G Base Station market report, Overview of Key trends in the past and present are in reports that are reported to be beneficial for companies looking for venture businesses in this market. Information about the various marketing channels and well-known distributors in this market was also provided here. This study serves as a rich guide for established players and new players in this market. Get Reasonable Discount on This Premium Report @ https://www.advancemarketanalytics.com/request-discount/102566-global-5g-base-station-market Extracts from Table of Contents 5G Base Station Market Research Report Chapter 1 5G Base Station Market Overview Chapter 2 Global Economic Impact on Industry Chapter 3 Global Market Competition by Manufacturers Chapter 4 Global Revenue (Value, Volume*) by Region Chapter 5 Global Supplies (Production), Consumption, Export, Import by Regions Chapter 6 Global Revenue (Value, Volume*), Price* Trend by Type Chapter 7 Global Market Analysis by Application ………………….continued This report also analyzes the regulatory framework of the Global Markets 5G Base Station Market Report to inform stakeholders about the various norms, regulations, this can have an impact. It also collects in-depth information from the detailed primary and secondary research techniques analyzed using the most efficient analysis tools. Based on the statistics gained from this systematic study, market research provides estimates for market participants and readers. Contact US : Craig Francis (PR & Marketing Manager) AMA Research & Media LLP Unit No. 429, Parsonage Road Edison, NJ New Jersey USA – 08837 Phone: +1 201 565 3262, +44 161 818 8166 [email protected]

#Global 5G Base Station Market#5G Base Station Market Demand#5G Base Station Market Trends#5G Base Station Market Analysis#5G Base Station Market Growth#5G Base Station Market Share#5G Base Station Market Forecast#5G Base Station Market Challenges

0 notes

Text

An In-Depth Look at the Growth of Global Indoor Distributed Antenna Systems Market

The global indoor distributed antenna systems market size is expected to reach USD 16.33 billion by 2030 and is projected to grow at a CAGR of 18.2% from 2024 to 2030, according to a new report by Grand View Research, Inc. Distributed antenna systems (DAS) form a network of antennas strategically positioned within buildings or indoor spaces, connected to a central hub for distributing wireless signals. The primary aim of DAS is to enhance wireless network coverage and capacity, catering to various communication mediums such as cellular, Wi-Fi, and public safety channels. Specifically designed for indoor environments, the indoor DAS market addresses the growing demand for reliable connectivity within enclosed spaces, driven by the widespread use of mobile devices and the increasing reliance on wireless communication across industries.

Indoor DAS systems play a pivotal role in boosting business productivity by ensuring seamless connectivity for employees and customers. They contribute to improved customer experiences in sectors such as healthcare, education, and retail, streamlining operations and enhancing service delivery. In addition, indoor DAS solutions are critical for public safety, facilitating effective communication and coordination during emergencies, thereby safeguarding lives and property. As technology evolves, the indoor DAS market remains at the forefront of innovation, adapting to emerging wireless standards and integrating new technologies to meet the expanding connectivity needs of modern organizations and individuals.

Gather more insights about the market drivers, restrains and growth of the Indoor Distributed Antenna Systems Market

Indoor Distributed Antenna Systems Market Report Highlights

• Indoor DAS solutions are indispensable for enterprises seeking to foster a conducive work environment. By ensuring that employees and customers remain seamlessly connected, businesses can unlock improved productivity and heightened customer satisfaction, thus fostering growth and success

• The services segment is projected to grow at the fastest CAGR over the forecast period

• The hybrid indoor DAS type segment is expected to dominate the market in 2023 with a market share of 15.5% and is expanding at a CAGR of 20.6% from 2024 to 2030

• The operator funded segment is projected to dominate the financing model segment and grow at a CAGR of 17.0% over the forecast period

• The residential buildings segment is projected to grow at the fastest CAGR of 20.3% over the forecast period

Browse through Grand View Research's Communications Infrastructure Industry Research Reports.

• The global data center energy storage market size was valued at USD 1.48 billion in 2023 and is projected to grow at a CAGR of 9.1% from 2024 to 2030.

• The global standalone 5G network market size was valued at USD 2.41 billion in 2024 and is projected to grow at a CAGR of 55.6% from 2025 to 2030.

Indoor Distributed Antenna Systems Market Segmentation

Grand View Research has segregated the global indoor DAS market on the basis of component, type, financing model, facility type, application, and region.

Indoor DAS Component Outlook (Revenue, USD Million, 2017 - 2030)

• Hardware

o Antenna Nodes/Radio Nodes

o Base Station

o Others

• Software

• Services

Indoor DAS Type Outlook (Revenue, USD Million, 2017 - 2030)

• Active

• Passive

• Hybrid

Indoor DAS Financing Model Outlook (Revenue, USD Million, 2017 - 2030)

• Operator Funded

• Build to Suit (Third Party Owner)

• Venue/Customer Funded

Indoor DAS Facility Type Outlook (Revenue, USD Million, 2017 - 2030)

• Large Buildings (Over 500 thousand square feet)

• Medium Buildings (50 thousand to 499 thousand square feet)

• Small Buildings (Below 50 thousand square feet)

Indoor DAS Application Outlook (Revenue, USD Million, 2017 - 2030)

• Healthcare

• Commercial Buildings

• Residential Building

• Corporate Spaces

• Educational Institute

• Manufacturing

• Hospitality

• Transportation & Logistics

• Public Sector

• Others

Indoor DAS Regional Outlook (Revenue, USD Million, 2017 - 2030)

• North America

o U.S.

o Canada

o Mexico

• Europe

o UK

o Germany

o France

o Italy

o Spain

o Switzerland

o Netherlands

• Asia Pacific

o China

o Japan

o India

o South Korea

o Thailand

o Philippines

o Indonesia

o Malaysia

o Bangladesh

• Latin America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

• Middle East

o UAE

o Saudi Arabia

o Qatar

o Oman

o Kuwait

• Africa

o South Africa

o Morocco

o Egypt

o Nigeria

o Kenya

Order a free sample PDF of the Indoor Distributed Antenna Systems Market Intelligence Study, published by Grand View Research.

#Indoor Distributed Antenna Systems Market#Indoor Distributed Antenna Systems Market Analysis#Indoor Distributed Antenna Systems Market Size#Indoor Distributed Antenna Systems Market Share#Indoor Distributed Antenna Systems Market Report

0 notes

Text

CMOS Power Amplifier Market 2023 Future Analysis, Demand by Regions and Opportunities with Challenges 2033

The CMOS power amplifier market size is projected to be worth US$ 5,361.5 million in 2023. The market is likely to reach US$ 24,550.4 million by 2033. The market is further expected to surge at a CAGR of 16.4% during the forecast period 2023 to 2033.

Key Market Trends and Highlights

The CMOS Power Amplifier market is propelled by the widespread deployment of 5G networks, necessitating advanced amplification for high speed data transmission.

A growing emphasis on eco-friendly solutions is leading to the development of energy-efficient CMOS power amplifiers.

Surging demand for smartphones and other consumer electronics is a key market driver, spurring innovation in amplification technology.

CMOS power amplifiers are gaining traction in the automotive sector, where they play a pivotal role in modern vehicle communication systems.

The market is adapting to global supply chain challenges by focusing on local production and diversified sourcing strategies.

From 2018 to 2022, the CMOS Power Amplifier market witnessed a steady growth trajectory. The market evolution during this period was primarily characterized by advancements in traditional power amplification technologies and a growing emphasis on cost effectiveness. The market was largely driven by well established power amplifier technologies, with incremental improvements in performance and efficiency.

Market players focused on cost reduction strategies to make amplifiers more affordable, catering to a broad consumer base. Innovations during this period were more evolutionary than revolutionary, with gradual enhancements in power amplification capabilities.

Looking ahead to 2023 to 2033, the market is poised for a significant shift. New drivers, such as emerging markets, stricter regulatory standards, and the integration of advanced materials, are expected to reshape the landscape. Growing economies and an expanding middle class in emerging markets are set to drive demand for consumer electronics, creating new opportunities for CMOS power amplifiers.

Stringent regulatory standards related to power efficiency and electromagnetic interference are expected to influence amplifier design and adoption. The integration of advanced materials like gallium nitride (GaN) and silicon carbide (SiC) will lead to substantial improvements in amplifier performance and durability. While the historical analysis underscores gradual evolution, the forecast projections suggest a period of transformation, driven by a convergence of factors that are reshaping the CMOS Power Amplifier market future.

CMOS Power Amplifier Market Key Drivers

The market is evolving in response to the digital transformation wave, where interconnected devices demand advanced power amplification for seamless communication.

The rising popularity of edge computing requires efficient power amplification to handle data processing at the edge of networks.

Beyond 5G connectivity, the expansion of 5G infrastructure presents opportunities for CMOS power amplifiers in network equipment and base stations.

Smart city projects are driving the adoption of CMOS power amplifiers in applications such as smart meters, lighting, and environmental monitoring.

The growing demand for wireless audio devices, like headphones and speakers, is boosting the market for small, high performance CMOS power amplifiers.

Challenges in the CMOS Power Amplifier Market

CMOS power amplifiers generate heat, requiring effective thermal management to ensure optimal performance and longevity.

Maintaining signal quality and reducing interference is challenging in high frequency CMOS amplification.

Meeting market demands for cost effective solutions while ensuring high performance poses a challenge.

The market is highly competitive, with numerous players vying for market share, intensifying competition.

Keeping pace with evolving technology standards and regulatory requirements can be complex and resource intensive.

Comparative View of Adjacent Markets

Future Market Insights has compared two other markets, namely audio power amplifier IC market and power amplifier modules market below. This highlights that CMOS power amplifier industry is set to dominate out of these three markets over the forecast period 2023 to 2033.

Country-wise Insights

The below table showcases revenues in terms of the top five leading countries, spearheaded by the India and China.

Pioneering the Future of Connectivity in the United States CMOS Power Amplifier Market

The burgeoning space industry is driving demand for CMOS power amplifiers to enable reliable communication with spacecraft and satellites. The United States is at the forefront of this exciting market, offering unique opportunities for growth.

The development of quantum computing, a revolutionary technology, requires advanced amplification solutions. CMOS power amplifiers play a vital role in maintaining the integrity of quantum signals, making them indispensable in this emerging field. With a growing emphasis on clean energy, CMOS power amplifiers are used in renewable energy systems to enhance power conversion efficiency, contributing to a sustainable future.

In an era of increasing cyber threats, secure communication is paramount. CMOS power amplifiers are vital in creating secure communication channels, fortifying the nation cybersecurity infrastructure. Advancements in medical devices and telemedicine are driving the demand for compact, high performance amplifiers, particularly in the United States, a hub of healthcare innovation.

Illuminating Opportunities and Innovations in the United Kingdom CMOS Power Amplifier Market

As the United Kingdom invests in quantum technology, there is a growing need for specialized CMOS power amplifiers to boost the efficiency and security of quantum communication systems. This niche application opens doors for innovation.

The United Kingdom aerospace and defense sector relies on innovative communication systems. Advanced CMOS power amplifiers are crucial for enhanced signal transmission, offering significant growth potential in this industry. The vibrant startup ecosystem in the United Kingdom is fostering innovation in various technology domains. These startups are increasingly seeking custom CMOS power amplifiers for their unique applications, providing opportunities for agile market players.

The United Kingdom participation in satellite programs creates a demand for high performance CMOS amplifiers for satellite communication equipment, a segment with untapped potential. With a focus on sustainability, CMOS power amplifiers play a vital role in enhancing the efficiency of green technologies such as renewable energy systems, providing a niche yet expanding market.

Navigating China Thriving CMOS Power Amplifier Market in the Age of Technology Advancements

While not entirely unknown, the full scope of 5G impact on China market is still unfolding. The exponential growth of 5G infrastructure creates a multitude of opportunities for advanced CMOS power amplifiers, particularly in base stations and mobile devices. China push towards smart manufacturing and Industry 4.0 requires robust communication networks.

CMOS power amplifiers are vital in ensuring seamless connectivity in smart factories, making them integral to this booming sector. China rapid expansion in satellite technology, including the development of its global navigation system (BeiDou), offers a fertile ground for CMOS power amplifiers. These amplifiers are crucial for effective satellite communication systems.

The electric vehicle (EV) market in China is soaring. CMOS power amplifiers are vital for efficient communication in EV charging infrastructure, an opportunity in a green energy revolution. The growth of China Internet of Things (IoT) ecosystem is driving demand for customized CMOS power amplifiers tailored to various IoT applications, from smart cities to agriculture.

Navigating Japan Unique Journey in the CMOS Power Amplifier Market

Japan growing emphasis on the Internet of Things (IoT) is fueling demand for power amplifiers optimized for 5G connectivity. This trend indicates a potential surge in the integration of 5G technologies across various sectors. Wireless charging technologies are gaining momentum in Japan. CMOS power amplifiers are crucial for efficient energy transfer, particularly in applications such as electric vehicles and consumer electronics.

Japan is investing significantly in quantum communication research. As quantum technologies mature, CMOS amplifiers will play a vital role in ensuring reliable quantum signal transmission. The Japan market showcases a unique focus on miniaturized power amplifiers for wearable devices. This trend is driven by the strong presence of the country in the wearable technology sector. The market is witnessing increased interest in CMOS power amplifiers for optical data communication applications, particularly as the demand for high speed data transmission grows.

Resonance of India in the CMOS Power Amplifier Market Unveiled

India focus on bridging the digital divide is driving the adoption of CMOS power amplifiers for rural connectivity. Amplification solutions are crucial in extending internet access to remote regions.

The IoT sector is flourishing in India, with a surge in applications spanning agriculture, healthcare, and smart cities. This growth spurs demand for specialized, low power CMOS amplifiers for diverse IoT sensors and devices.

As India increasingly embraces renewable energy sources, CMOS power amplifiers are playing a pivotal role in enhancing power conversion efficiency, an opportunity in the green energy revolution. Local manufacturing and assembly are on the rise. This trend creates opportunities for customized CMOS power amplifiers tailored to specific regional requirements. India manufacturing sector is transitioning toward smart factories. CMOS amplifiers are vital for enabling seamless communication and automation in this evolving landscape.

Category-wise Insights

The below table highlights how LTE is projected to lead the market in terms of module, with a market share of 23.4% in 2023. The smartphone segment is likely to spearhead sales based on application and is anticipated to hold a market share of 34.2% through 2023.

The Radiant Dominance of LTE in the CMOS Power Amplifier Market

In the CMOS power amplifier market, the LTE segment is poised to assert dominance. LTE technology has become the backbone for high speed wireless communication, driving the proliferation of 4G and the transition to 5G networks. This surge in mobile data consumption, coupled with the need for faster data transfer rates, has increased the demand for advanced CMOS power amplifiers.

The power amplifier plays a pivotal role in amplifying and maintaining signal quality in LTE enabled devices, including smartphones, tablets, and IoT devices. As the world continues to embrace faster and more reliable wireless connectivity, the LTE segment is expected to maintain its stronghold in the CMOS Power Amplifier market.

Smartphones take the Spotlight in the CMOS Power Amplifier Market

The CMOS power amplifier market is witnessing a robust and enduring dominance by the smartphone segment. As smartphones become the epicentre of modern communication and connectivity, the demand for high performance amplifiers is skyrocketing. Consumers consistently seek faster data transfer speeds and improved signal strength.

CMOS power amplifiers are integral to achieving these objectives in the latest smartphone models. With innovations in 5G technology and a surge in mobile data usage, the smartphone segment continues to drive the market growth. As long as smartphones remain indispensable in our lives, their influence over the CMOS power amplifier market remains unchallenged.

Competitive Landscape

The competitive landscape of the CMOS Power Amplifier market is a dynamic and rapidly evolving terrain. Industry giants such as Qualcomm, Broadcom, and Skyworks Solutions consistently drive innovation and market leadership. However, a host of smaller, niche players specializing in customized solutions also carves their niche. Collaboration and strategic partnerships between semiconductor companies, foundries, and technology providers are common to tap into diversified expertise.

Market entrants are focusing on disruptive technologies, like gallium nitride (GaN) and silicon carbide (SiC), to gain a competitive edge. As 5G, IoT, and AI applications surge, the competition intensifies, making adaptability, performance, and cost efficiency the key battlegrounds in this high stakes arena.

Read More@ https://www.futuremarketinsights.com/reports/cmos-power-amplifiers-market

0 notes

Text

The Surface Acoustic Wave (SAW) Filters Market is projected to grow from USD 2025 million in 2024 to an estimated USD 3734.27 million by 2032, with a compound annual growth rate (CAGR) of 7.95% from 2024 to 2032.Surface Acoustic Wave (SAW) filters are pivotal components in modern electronic devices, providing efficient frequency selection and signal filtration in telecommunications, consumer electronics, and industrial systems. As the world embraces advanced technologies like 5G, IoT, and smart devices, the demand for SAW filters has surged, driving innovations and market expansion.

Browse the full report https://www.credenceresearch.com/report/surface-acoustic-wave-saw-filters-market

Overview of SAW Filters

SAW filters operate by converting electrical signals into acoustic waves on a piezoelectric substrate, such as quartz or lithium niobate. These waves are manipulated to filter specific frequencies before converting them back to electrical signals. SAW filters are valued for their high precision, compact size, and cost-effectiveness, making them indispensable in applications like mobile phones, base stations, and satellite communications.

Market Drivers

1. Adoption of 5G Technology The global rollout of 5G networks has been a significant catalyst for the SAW filter market. 5G requires filters capable of operating at high frequencies with minimal interference. SAW filters, known for their superior performance at specific frequency ranges, meet this requirement efficiently.

2. Growing Internet of Things (IoT) Ecosystem IoT devices demand miniaturized and power-efficient components. SAW filters, being compact and low-power, align perfectly with these needs. Applications in smart homes, industrial IoT, and wearables are pushing manufacturers to innovate in design and functionality.

3. Rising Smartphone Penetration Smartphones account for a considerable share of SAW filter usage, with each device containing multiple filters for functions like GPS, Bluetooth, and Wi-Fi. The ongoing demand for advanced smartphones and the integration of multiple frequency bands further boost the market.

4. Automotive Electronics Expansion As vehicles become smarter with advanced driver-assistance systems (ADAS), infotainment, and connectivity features, the need for reliable frequency control components grows. SAW filters play a crucial role in ensuring seamless communication and signal processing in vehicles.

Challenges in the SAW Filters Market

1. Competition from Bulk Acoustic Wave (BAW) Filters While SAW filters dominate the low-frequency range, BAW filters are preferred for higher frequencies due to their better performance in these bands. This technological competition pushes SAW filter manufacturers to innovate continuously.

2. Complex Manufacturing Process The production of SAW filters requires precise engineering and the use of specialized materials. The high costs and technical expertise associated with manufacturing can pose barriers to entry for new players.

3. Price Sensitivity in Emerging Markets Although SAW filters are cost-effective, the price sensitivity of emerging markets, where affordability often trumps performance, can limit market penetration.

Future Trends and Opportunities

1. Integration with MEMS Technology Merging SAW filters with Microelectromechanical Systems (MEMS) can lead to ultra-compact and high-performance devices, opening doors for new applications in healthcare, aerospace, and beyond.

2. Customization for Niche Applications As industries like healthcare and defense require highly specialized components, custom SAW filter solutions can cater to unique frequency and environmental demands.

3. Sustainability in Manufacturing As environmental concerns grow, manufacturers are exploring eco-friendly materials and processes to produce SAW filters, appealing to environmentally conscious industries.

Key Player Analysis:

Epson Europe Electronics

Golledge Electronics Ltd

Microsemi Corporation

Murata Manufacturing Co Ltd

Qorvo Inc.

Qualcomm Technologies

Raltron Electronics Corporation

TAI-SAW Technology Co. Ltd

Transko Electronics

Vectron International

Segmentation:

By Type

Low-Pass SAW Filters

Band-Pass SAW Filters

High-Pass SAW Filters

Band-Stop SAW Filters

Others

By Frequency Range

Less than 1 GHz

1 GHz to 2.5 GHz

2.5 GHz to 5 GHz

More than 5 GHz

By Technology

Single Phase Unidirectional Transducer (SPUDT)

Double Phase Unidirectional Transducer (DPUDT)

Others

By Distribution Channel

Direct Sales

Distributors

Online Channels

OEMs

By Enterprise Size

Small & Medium Enterprise

Large Enterprise

By Material

Quartz

Lithium Tantalate

Lithium Niobate

Others

By End-User Industry

Telecommunications

Consumer Electronics

Automotive

Aerospace & Defense

Healthcare

Others

By Region:

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report https://www.credenceresearch.com/report/surface-acoustic-wave-saw-filters-market

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

Applications and Variety of Fiber Optic Circulators

The circulator's primary function in a wireless access network is to separate the output signal from the base station antenna's input signal. Two essential parts of 5G base stations are Optical Circulator and isolators. There will be a huge rise in demand for fiber optic circulators as 5G Massive MIMO expands.

Fiber Optic Circulators' Properties

The ability to transmit optical signals in both directions on a single cable is the primary characteristic of a fiber optic circulator. The optical signal can only be transmitted from one port to another in a single direction at a time, and the circulator's direction of signal transmission is irreversible. The optical signal must sequentially go via ports in a single direction, notwithstanding the possibility of redirection. In a three-port circulator, for instance, an optical signal must first travel from port to port 2 before reaching port 3.

Fiber Optic Circulator Types

The number of ports or the polarization correlation can be used to classify fiber optic circulators. Three-port and four-port Fiber Circulator are the most often used of the three-port, four-port, and six-port varieties. Polarization correlation determines whether a circulator is PM (polarization-maintaining) or PI (polarization-independent). In polarization-maintaining applications, such as dispersion compensation modules (DCM), dual-pass amplifiers, 40Gbps high-speed systems, or Raman pump applications, polarization-maintaining optic circulators are frequently utilized. In high-speed, bidirectional, and dense wavelength division multiplexing (DWDM) systems, polarization independent optic circulators are frequently utilized in conjunction with fiber gratings and other reflecting components.

Fiber Optic Circulator Applications

Fiber optic circulators are typically used in optical amplifiers, OTDR, PON, WDM, OADM, Polarization Mode Dispersion, Dispersion Compensation, and fiber optical sensing, among other applications. An essential part of sophisticated optical networks' DWDM is the optical circulator. The market for Optical Circulator has enormous potential because to the enormous growth in base stations. The primary market for fiber optic circulators will remain telecommunications applications. Fiber optic circulators are also utilized in oil, natural gas, test equipment, sensing, research and development, and a few more specialized application areas.

Next: Fiber Optic Cable Installation: From Fibermart to Your Home

1 note

·

View note

Text

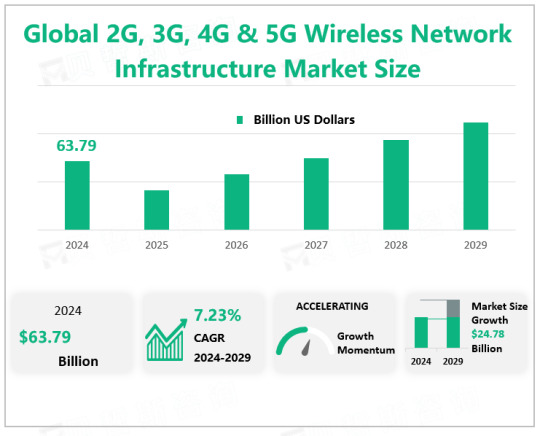

Global 2G, 3G, 4G & 5G Wireless Network Infrastructure Market Competition is Fierce, Ericsson Holding a share of 26.39% in 2024

According to Global Market Monitor, the global 2G, 3G, 4G & 5G wireless network infrastructure market size will be $63.79 billion in 2024 with a CAGR of 7.23% from 2024 to 2029.

When users connect to the internet, the speed of the internet depends upon the signal strength that has been shown in alphabets like 2G, 3G, 4G, and 5G, right next to the signal bar on the home screen. Each Generation is defined as a set of telephone network standards, which detail the technological implementation of a particular mobile phone system. The speed increases and the technology used to achieve that speed also changes. For instance, 1G offers 2.4 kbps, 2G offers 64 Kbps and is based on GSM, 3G offers 144 kbps-2 Mbps whereas 4G offers 100 Mbps - 1 Gbps and is based on LTE technology.

With the advancement of technology, each generation of network from 2G to 5G has brought significant performance improvements. 5G networks promise lower latency, ultra-fast connections and the ability to support millions of devices per square kilometer, which will be critical for future innovations such as self-driving cars and industrial automation.

Market Drivers

Wireless technology is experiencing tremendous growth due to the introduction of technologically advanced solutions worldwide. The rapid expansion of mobile network coverage has covered remote areas. Due to increasing competition in the industry, the increased demand for wireless technology has led to lower data usage charges. The continuous growth of network traffic, deployment of infrastructure, and growing demand for wireless connectivity due to numerous advantages are driving the growth of the market. The growing demand for 5G services and advanced high-speed Internet connectivity is driving the market growth.

The latest trends in 4G, 5G, and beyond include densification and coverage extension approaches, spectrum trends, network customization and intelligence, virtualization, and cloud. These trends provide service providers with more opportunities for network customization, network deployment, and network optimization.

Market Restraints Analysis

Radiofrequency (RF) radiation, which includes radio waves and microwaves, is at the low-energy end of the electromagnetic spectrum. It is a type of non-ionizing radiation. If RF radiation is absorbed by the body in large enough amounts, it can produce heat. This can lead to burns and body tissue damage. Although RF radiation is not thought to cause cancer by damaging the DNA in cells the way ionizing radiation does, there has been concern that in some circumstances, some forms of non-ionizing radiation might still have other effects on cells that might somehow result in cancer. Most people are exposed to much lower levels of man-made RF radiation every day due to the presence of RF signals all around us. They come from radio and television broadcasts, WiFi and Bluetooth devices, cell phones (and cell phone towers), and other sources. Cell phones and cell phone towers (base stations) use RF radiation to transmit and receive signals. Some concerns have been raised that these signals might increase the risk of cancer.

Issues related to radiofrequency have discouraged some people from 2G, 3G, 4G, and 5G wireless network infrastructure, which is not conducive to the sustainable development of the industry.

Most Up-To-Date Market Figures, Statistics & Data - Order Now (Delivered In 48-72 Hours)

Market Competition

With major suppliers in the 2G, 3G, 4G & 5G wireless network infrastructure industry competing globally, the intensity of competition within the 2G, 3G, 4G & 5G wireless network infrastructure industry has increased. The vendors adopt strategies like price premiums to stay competitive in the market. Meanwhile, the local vendors in developing nations are providing tough competition to the global players based on product pricing. The fierce competition is not conducive to the sustainable development of the industry. At the same time, small companies enter the business consequently as venturing into a 2G, 3 G, 4G & 5G wireless network infrastructure business does not require immense capital or investment. However, this leads to the proliferation of sub-standard or duplicate services which then hampers the competitive scenario in the market as established 2G, 3G, 4G & 5G wireless network infrastructure manufacturers are compelled to lower the price, which ultimately impacts their profit margins and sales volumes.

Ericsson is one of the major players operating in the 2G, 3G, 4G & 5G Wireless Network Infrastructure market, holding a share of 26.39% in 2024. Ericsson Inc. operates as a provider of telecommunications equipment and related services. The Company offers its products and services to mobile and fixed network operators, as well as provides communications networks, telecom services, and multimedia solutions. Ericsson operates globally.

0 notes

Text

Microelectronics Market: Current Analysis and Forecast (2024-2032)

According to the Univdatos Market Insights analysis, the Rising demand for consumer electronics, the electrification of vehicles, and the expansion of 5G networks are driving the Microelectronics market's growth in the global scenario of the Microelectronics market. As per their “Microelectronics Market” report, the global market was valued at USD 527.4 Billion in 2023, growing at a CAGR of 7.2% during the forecast period from 2024 – 2032.

The microelectronics market is changing quickly because of new technology and how much we use electronics in our everyday lives. Things like smartphones, fitness trackers, electric cars, and machines in factories all rely on microelectronics. As we want smaller, faster, and better electronic parts, some big trends are helping this market grow. These trends include the new 5G networks that make phones work better, more electric cars on the road, and more gadgets that connect to the internet. All of this helps invent new things and gives people chances to come up with new ideas across different fields.

The main drivers of the market which is rapidly changing the microelectronics sector are:

Rising Demand for Consumer Electronics

Increased demand for smartphones, wearables, tabs, and��home appliances are the major factors driving the microelectronics market. Technology demands that devices incorporate progressively diminishing microelectronic parts with faster throughput and less energy consumption. An example of this is the Apple iPhone, Where with each new generation comes additional advanced semiconductors, microprocessors, better performance, battery lives, and a camera. Smart devices such as Apple Watch or Fitbit and healthcare applications also press the need for dedicated microelectronics for health sensing and communication.

Electrification of Vehicles (EVs)

With the increasing focus on sustainability, electric vehicles (EVs) have now emerged as one of the strongest growth engines of the microelectronics market. Batteries of EVs contain microelectronics devices for battery management, power electronics, and driving automation systems. Tesla, for example, relies critically on micro nodes as they control battery, powertrain, and the Autopilot self-driving system. The trend towards the use of electric vehicles is the most important driving force in the constant development of microelectronics to increase energy efficiency as well as the performance of vehicles.

Access sample report (including graphs, charts, and figures): https://univdatos.com/get-a-free-sample-form-php/?product_id=67401

Expansion of 5G Networks

The demand for 5G technology around the globe is another factor, as the technology development calls for efficiency in computational power, especially in the use of microelectronics in data transmission. Firms such as Qualcomm provide superior 5G microchips that are used to build the latest 5G phones as well as new-generation networks. Samsung and Huawei together introduced 5G in their products, which boosted the use of microelectronics products that are vital in modems, antennae, and base stations used in facilitating 5G.

Industrial Automation and IoT

The third is the growth of 5G technology across the globe, as the world needs effective microelectronics to process 5G, with increased data transfer rates, better connectivity, and greater bandwidth. Technology giants including Qualcomm are providing leading-edge 5G microchips, which fuel new-generation telephones and networking systems. Both Samsung and Huawei continue to incorporate 5G features into their products which will increase the utilization of microelectronic components that are critical for the modem and antennas supporting the 5G base stations.

Conclusion

To sum up, it could be stated that the market of microelectronics will remain upward trend as continuing scenarios progress with new technologies and demands. Major contributors like consumer electronics, 5G, electrification of vehicles, and the popularity of Industrial automation and IoT are changing the dynamics. These forces not only set the challenges for breaking new ground but also offer promising opportunities for the improvement of different fields and branches. At the same time, industries go on counting on microelectronics to enhance manufacturing efficiency, connectivity, and performance, the market is prepared to play a great role in the next wave of microelectronics technology innovations.

Contact Us:

UnivDatos Market Insights

Email - [email protected]

Contact Number - +1 9782263411

Website -www.univdatos.com

Related Electronic & Semiconductor Market Research Industy Report:-

Foldable Display Market: Current Analysis and Forecast (2024-2032)

Microelectronics Market: Current Analysis and Forecast (2024-2032)

0 notes

Text

Marine Onboard Communication and Control Systems Market: A Global Outlook and Forecast

The Marine Onboard Communication and Control Systems Market has gained significant momentum due to the increasing global demand for secure, efficient, and integrated maritime communication solutions. Estimated at USD 8.6 billion in 2023, the market is projected to reach USD 12.3 billion by 2028, expanding at a CAGR of 7.3%. This growth is propelled by rising maritime trade, advancements in communication technology, and growing investments from both government and commercial sectors.

What are Marine Onboard Communication and Control Systems?

Marine Onboard Communication and Control Systems refer to a suite of integrated technologies that enhance communication, navigation, and overall operational control on marine vessels. These systems encompass a variety of components, including communication radios, satellite systems, automation identification systems (AIS), and propulsion control systems, among others.

Key components include:

Communication Systems: Facilitate secure data transmission between ships and shore stations. They encompass satellite systems, radios, and receivers, enabling vessels to maintain connectivity even in remote areas.

Control Systems: Include automation and monitoring technologies that ensure optimal vessel performance, such as engine control, navigation safety, and fuel efficiency.

You Can Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=25117530

How Do Marine Onboard Communication and Control Systems Work?

These systems use advanced digital and satellite technology to ensure continuous and secure communication across all stages of a vessel's journey. Here’s an overview of how they operate:

Satellite and Radio Communication: Using satellites, these systems allow for global communication. This ensures that vessels can receive weather updates, navigational warnings, and emergency alerts in real-time.

Automation Identification System (AIS): AIS facilitates vessel tracking by broadcasting a ship’s location to other vessels and shore-based stations. This helps prevent collisions and aids in search and rescue operations.

Control Systems and Monitoring: Integrated control systems enable real-time monitoring of engine performance, fuel consumption, and other critical parameters. These systems allow predictive maintenance, which enhances overall vessel efficiency and safety.

Growth Drivers of the Marine Onboard Communication and Control Systems Market

Several factors contribute to the robust growth of the Marine Onboard Communication and Control Systems Industry:

Increase in Marine Fleet Size: Global marine trade continues to rise, prompting an increase in new vessel construction and retrofitting of existing fleets with advanced communication systems. According to the United Nations Conference on Trade and Development, maritime trade recovered by 4.3% in 2021, with growth expected to continue through 2026.

Demand for Operational Efficiency: With the adoption of IoT and AI technologies, vessels are now able to monitor and optimize their operations in real-time. This results in reduced fuel consumption, minimized downtime, and enhanced safety.

Government Investments in Maritime Modernization: Governments worldwide are modernizing their navies with advanced marine communication and control systems to bolster secure and efficient maritime operations. This is particularly prominent in countries like China, the United States, and South Korea, which are investing heavily in these technologies.

Market Opportunities for Marine Onboard Communication and Control Systems

As maritime industries continue to evolve, new opportunities arise within the Marine Onboard Communication and Control Systems market:

Advancements in Connectivity: With the advent of 5G, low Earth orbit (LEO) satellites, and high-speed internet, vessels can maintain connectivity even in the most remote areas. This opens up opportunities for enhanced situational awareness and improved decision-making for both onboard and onshore teams.

Integration of Smart Sensors and Monitoring Devices: Smart sensors enable real-time data gathering on various operational metrics, from engine temperature to weather conditions. This enhances predictive maintenance capabilities, reduces the likelihood of equipment failure, and improves overall vessel safety.

Growing Demand for Eco-Friendly Solutions: As environmental regulations tighten, there is a growing demand for green and efficient marine communication systems. Technologies that optimize fuel consumption and reduce emissions are becoming increasingly popular, providing further growth opportunities.

Key Players in the Marine Onboard Communication and Control Systems Market

The Marine Onboard Communication and Control Systems Market is dominated by Key Players who are continually innovating to meet industry demands. Some of the top players include:

Emerson Electric Co. (US): Known for providing automation solutions that enhance vessel operational efficiency.

Wärtsilä (Finland): Offers a range of maritime solutions, including integrated bridge systems and automation platforms.

Kongsberg (Norway): Specializes in marine automation systems, and has recently launched the K-Chief, a new platform for more efficient marine operations.

ABB (Switzerland): Provides advanced propulsion systems and recently developed the ABB Dynafin, which enhances ship efficiency.

Northrop Grumman Corporation (US): A leading player in the defense sector, offering cutting-edge maritime communication and control systems.

Ask for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=25117530

Recent Developments in Marine Onboard Communication and Control Systems

June 2023: Kongsberg launched the K-Chief marine automation system to streamline marine operations.

June 2023: ST Engineering introduced an upgraded version of its NERVA ship management system, featuring data analytics and centralized control capabilities.

May 2023: ABB unveiled the ABB Dynafin, a propulsion system that enhances ship efficiency with an innovative, low-speed motor design.

Challenges Facing the Marine Onboard Communication and Control Systems Market

While growth prospects are strong, the market faces certain challenges:

High Initial Costs: The integration of advanced communication and control systems requires significant investment. For instance, a VSAT communication system can cost around USD 60,000. This poses a financial challenge for smaller shipping companies.

Retrofitting Older Vessels: Upgrading older ships with modern systems involves technical difficulties, such as integrating new technologies with outdated wiring and control systems. These modifications can be time-consuming and may require substantial investment.

Frequently Asked Questions (FAQs)

1. Which are the major companies in the Marine Onboard Communication and Control Systems market?

Major companies include Emerson Electric Co., Wärtsilä, Kongsberg, ABB, and Northrop Grumman Corporation. These companies are renowned for their innovative solutions in marine communication and control systems.

2. What are the key drivers of the Marine Onboard Communication and Control Systems market?

Rising marine fleet size, demand for operational efficiency, and government investments in maritime modernization are major drivers of market growth.

3. Which region is expected to grow at the highest rate?

Asia Pacific is projected to exhibit the highest growth rate due to increasing seaborne trade and significant investments in naval modernization.

4. What is the expected CAGR of the Marine Onboard Communication and Control Systems Market?

The market is expected to grow at a CAGR of 7.3% from 2023 to 2028.

To Gain Deeper Insights Into This Dynamic Market, Speak to Our Analyst Here: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=25117530

Key Takeaways

Growth Projection: The Marine Onboard Communication and Control Systems market is forecast to grow from USD 8.6 billion in 2023 to USD 12.3 billion by 2028.

Major Drivers: Key drivers include the rise in marine fleet size, demand for enhanced operational efficiency, and increased government investments.

Opportunities: Opportunities lie in evolving connectivity solutions, integration of smart sensors, and the demand for eco-friendly technologies.

Regional Dominance: Asia Pacific is projected to lead market growth due to expanding maritime trade and technological advancements.

Key Players: Prominent companies like Emerson Electric Co., Wärtsilä, Kongsberg, ABB, and Northrop Grumman Corporation are instrumental in shaping the market.

The Marine Onboard Communication and Control Systems market represents a critical aspect of the maritime industry’s evolution. As global trade continues to expand and technological advancements accelerate, this market is poised for substantial growth, with new opportunities emerging for companies to enhance maritime communication, navigation, and operational efficiency.

#marine onboard communication and control systems#maritime communication#marine control systems market#marine communication technology#maritime industry growth#market research

0 notes

Text

Remote Radio Unit (RRU) Market: Global Industry Analysis and Forecast 2031 | Market Strides

Remote Radio Unit Rru Market Research Report

Market Strides has recently added a new report to its vast depository titled Global Remote Radio Unit Rru Market. The report studies vital factors about the Global Remote Radio Unit Rru Market that are essential to be understood by existing as well as new market players. The report highlights the essential elements such as market share, profitability, production, sales, manufacturing, advertising, technological advancements, key market players, regional segmentation, and many more crucial aspects related to the Remote Radio Unit Rru Market.

Market Overview

Remote Radio Unit Rru Market overview provides a snapshot of the current state of a specific market, highlighting key trends, growth drivers, challenges, and opportunities. It typically includes an analysis of the market size, competitive landscape, consumer demand, and regulatory factors. Additionally, the overview may touch on emerging technologies or innovations impacting the market, as well as projections for future growth. This concise summary helps businesses and investors understand the market dynamics and identify areas for strategic planning or investment.

Get Free Sample Report PDF @ https://marketstrides.com/request-sample/remote-radio-unit-rru-market

Remote Radio Unit Rru Market Share by Key Players

Datang

Ericsson

Fujitsu

Huawei Technologies

NEC

Nokia Networks

Samsung

ZTE

Remote Radio Unit Rru Market Segmentation

The report on Global Remote Radio Unit Rru Market provides detailed toc by type, applications, and regions. Each segment provides information about the production and manufacturing during the forecast period of 2024-2032. The application segment highlights the applications and operational processes of the industry. Understanding these segments will help identify the importance of the various factors aiding to the market growth.

The report is segmented as follows:

By Type

3G

4G

5G

Other

By Application

Integrated base station

Distributed base station

Get Detailed @ https://marketstrides.com/report/remote-radio-unit-rru-market

Remote Radio Unit Rru Market Frequently Asked Question

1) What are Remote Radio Unit Rru Market and why are they important?

2) What is the future outlook for the Remote Radio Unit Rru Market?

3) What are the Segments Covered in the Market?

4) Who are the prominent key players in the Market?

Key Highlights

It provides valuable insights into the Remote Radio Unit Rru Market.

Provides information for the years 2024-2032. Important factors related to the market are mentioned.

Technological advancements, government regulations, and recent developments are highlighted.

This report will study advertising and marketing strategies, market trends, and analysis.

Growth analysis and predictions until the year 2032.

Statistical analysis of the key players in the market is highlighted.

Extensively researched market overview.

Buy Remote Radio Unit Rru Market Research Report @ https://marketstrides.com/buyNow/remote-radio-unit-rru-market

Contact Us:

Email : [email protected]

#Remote Radio Unit Rru Market Size#Remote Radio Unit Rru Market Share#Remote Radio Unit Rru Market Growth#Remote Radio Unit Rru Market Trends#Remote Radio Unit Rru Market Players

0 notes

Text

5G Base Station Market: A Deep Dive into the Next Generation of Connectivity

The emergence of 5G technology changed connectivity to be faster, more capable, and less latency than any of its precursors. At its center is the 5G base station, an infrastructure component that connects devices to the network seamlessly. The growing demand for high-speed data and reliable communications shortly also creates rapidly increasing demand in the 5G base station market. This blog delves into the core of this market and encompasses the drivers, challenges, and future outlook of this market.

Market Overview

The 5G base station market encompasses various players - from big communications equipment manufacturers to smaller technology startups and infrastructure providers. The need for this market is driven by the growth in smartphones and IoT devices, the increasing necessity for high-bandwidth applications, and the expansion of 5G networks across the globe.

The 5G Base Station market size is estimated to reach US$ 65.70 billion by 2030 from US$ 20.53 billion in 2022. The market is to grow with a CAGR of 15.6% during 2022–2030.

Market Drivers

There are various factors promoting the growth of the 5G base station market:

Increased Smartphone Penetration: There has been an increase in the demand for high-speed data connectivity due to massive smartphone penetration, leading to the deployment of 5G networks.

IoT Haul: The Internet of Things (IoT) can connect billions of devices each needing communication that is not only trusted but also low latency. Massive scale and diverse requirements of IoT applications are best supported by 5G base stations.

High-Bandwidth Application Demand: With an increase in data-intensive applications such as virtual reality, augmented reality, and cloud gaming, a lot of bandwidth needs to be delivered using networks that have ultra-high-speed capabilities. 5G base stations can deliver the same bandwidth required for such applications.

Government Initiatives: Governments around the globe are expensively investing in 5G infrastructures to fuel the economy and innovation. This is what is also hastening the rollout of 5G base stations.

Segments Covered

By Component

Hardware and Service

By Frequency Band

Below 2.5 GHz

2.5-8 GHz

8-25 GHz

Above 25 GHz

By Cell Type

Macro cell and small cell microcell

Picocell

Femtocell

By End User

Industrial

Commercial

Residential

By Geography

North America

Europe

Asia-Pacific

South and Central America

Middle East and Africa

Companies covered

Alpha Networks Inc

Airspan Networks Holdings Inc

Baicells Technologies North America Inc

Commscope Holding Co Inc

Huawei Technologies Co Ltd

NEC Corp

Nokia Corp

Samsung Electronics Co Ltd

Telefonaktiebolaget LM Ericsson ZTE Corp

Market Challenges

Despite the high growth potential, the 5G base station market has some challenges:

High Expenditure of Base Station Deployment: Compared to earlier versions of cellular networks, 5G is associated with a large initial investment in deploying base stations that are complemented by the acquisition of spectrum and upgrade of existing infrastructure.

Interoperability Problems: Interoperability between different 5G equipment providers and networks is complicated, thus also likely to slow down the pace of the technology

Availability of Adequate Spectrum: Availability of an appropriate spectrum for the implementation of 5G varies from one region to another, hence also influencing the speed and price of a network rollout.

Regulatory Obstacles: Different regulatory frameworks and multiple permits to navigate and obtain are both time-consuming and expensive for a 5G network operator.

Market Trends

Massive MIMO: This type of technology, Massive Multiple-Input Multiple-Output (MIMO), enables a 5G base station to support tens of several users at the same time to increase capacity and coverage.

Small Cell Deployment: Small cells are being widely applied for increasing coverage in more densely populated areas of the urban environment as well as indoors besides the traditional macro base stations.

Virtualization: virtualization of the network allows for more flexibility and efficiency in the management of the 5G network for lesser operational costs.

Cloud RAN: Cloud radio access networks (RAN) apply the capabilities of cloud computing to centralize network functions, ensuring scalable and cost-effective improvement.

Future Outlook

Heavy demand for high-speed connectivity and rapid expansion of the 5G networks are expected to encourage the base station market for 5G in the coming years. As costs decline and technology advances, 5G can be expected to become accessible to a wider population while opening the way toward innovative applications and services for all.

Conclusion-

The 5G base station market is a dynamic and rapidly evolving landscape. Technology offers immense potential to transform industries and improve people's lives. However, despite the challenges, the drivers of growth in the 5G market along with the emerging trends point toward a bright future for 5G connectivity. Just as the world lives through the Internet age, it will live through the 5G base station-connected future.

Frequently Asked Questions-

Which is the biggest regional market for 5G Base Stations?

Ans: - North America is the biggest regional market for 5G Base Station.

Which are the top companies to hold the market share in the 5G Base Station market?

Ans: - Alpha Networks Inc., Airspan Networks Holdings Inc., Baicells Technologies North America Inc., CommScope Holding Co. Inc., and Huawei Technologies Co Ltd are the top companies to hold the market share.

What would be the growth rate in the market to be witnessed during the forecast period of 2022 to 2030?

Ans: - The 5G Base Station market is expected to see a growth rate of 15.6% during the forecast period, by 2031.

What's the size of the market for 5G Base Station?

Ans: - Global 5G Base Station market size was valued at US$ 20.53 billion in 2022 and is anticipated to reach US$ 65.70 billion by 2030.

What are the segments of the 5G Base Station market?

Ans: - The 5G Base Station market is segmented into Component, Cell Type, End User, and region.

About Us-

The Insight Partners is among the leading market research and consulting firms in the world. We take pride in delivering exclusive reports along with sophisticated strategic and tactical insights into the industry. Reports are generated through a combination of primary and secondary research, solely aimed at giving our clientele a knowledge-based insight into the market and domain. This is done to assist clients in making wiser business decisions. A holistic perspective in every study undertaken forms an integral part of our research methodology and makes the report unique and reliable.

0 notes

Text

5G Base Station Backup Power Supply Market Overview and Long-term Growth Projections 2024 - 2032

The 5G base station backup power supply market is an essential component of the telecommunications infrastructure, providing reliable power to 5G base stations, especially in areas with unstable grid connections or during outages. As the deployment of 5G networks accelerates globally, the demand for backup power solutions has surged. This article explores the current landscape, trends, challenges, and future prospects of the 5G base station backup power supply market.

Overview of the 5G Base Station Backup Power Supply Market

The 5G base station backup power supply market is poised for substantial growth as the demand for reliable and uninterrupted connectivity increases. While challenges such as high initial costs and regulatory compliance exist.

What is a 5G Base Station Backup Power Supply?

A 5G base station backup power supply is a system designed to ensure continuous power availability to 5G base stations during outages or when the main power supply is insufficient. These systems can include:

Batteries: Rechargeable energy storage systems, typically lithium-ion or lead-acid, that provide power during outages.

Uninterruptible Power Supply (UPS): Systems that offer immediate backup power to prevent downtime.

Hybrid Systems: Combinations of batteries, fuel cells, and renewable energy sources to ensure sustainability and reliability.

Importance of Backup Power Supply in 5G Networks

The significance of backup power supplies in 5G networks can be summarized as follows:

Reliability: Ensures uninterrupted service, critical for applications such as autonomous vehicles, telemedicine, and smart cities.

Operational Efficiency: Minimizes downtime, enhancing the overall performance of telecommunications infrastructure.

Safety and Security: Maintains communication capabilities during emergencies, ensuring public safety and efficient disaster response.

Market Trends

Accelerated 5G Network Rollouts

The rapid deployment of 5G networks globally is a primary driver for the backup power supply market. Telecom operators are investing heavily in infrastructure to meet the growing demand for faster and more reliable connectivity, necessitating robust backup power solutions.

Increasing Focus on Renewable Energy Integration

As sustainability becomes a priority, there is a growing trend toward integrating renewable energy sources, such as solar and wind, into backup power systems. This shift not only reduces the carbon footprint but also enhances energy security by diversifying power sources.

Advancements in Energy Storage Technologies

Technological innovations in energy storage, particularly lithium-ion and solid-state batteries, are improving the efficiency and capacity of backup power systems. These advancements allow for longer-lasting power supplies, reducing the need for frequent maintenance and replacements.

Challenges in the 5G Base Station Backup Power Supply Market

High Initial Costs

The capital expenditure required for advanced backup power systems can be substantial. This cost may deter some telecom operators, especially smaller companies or those operating in regions with limited budgets.

Regulatory Compliance

The telecommunications sector is heavily regulated, and compliance with safety and environmental standards can be challenging for manufacturers. Navigating these regulations is crucial for market players to avoid penalties and ensure product viability.

Limited Awareness and Understanding

Many stakeholders in the telecommunications industry may not fully recognize the importance of backup power systems. Increased awareness and education are necessary to highlight the critical role these systems play in ensuring continuous service.

Future Prospects

Market Growth

The 5G base station backup power supply market is projected to grow significantly in the coming years. Analysts forecast a compound annual growth rate (CAGR) of X% from 2024 to 2030, driven by the expanding 5G infrastructure and increasing reliance on reliable power sources.

Innovations in Smart Power Solutions

Future developments may focus on smart power management solutions that utilize artificial intelligence (AI) and machine learning to optimize energy usage and predict power demands. These technologies can enhance the efficiency and reliability of backup systems.

Expansion into Emerging Markets

As 5G networks expand into emerging markets, there is significant potential for growth in backup power supply solutions. Regions with less stable grid infrastructure will particularly benefit from reliable backup systems, presenting opportunities for manufacturers.

Conclusion

The opportunities presented by technological advancements and the global shift towards 5G networks are substantial. By focusing on innovation, sustainability, and market expansion, stakeholders in the backup power supply market can position themselves to thrive in this dynamic and evolving landscape, contributing to the resilience of telecommunications infrastructure worldwide.

#5G Base Station Backup Power Supply Market Size#5G Base Station Backup Power Supply Market Trend#5G Base Station Backup Power Supply Market Growth

0 notes

Text

Satellite Communication Market - Forecast, 2024-2030

Satellite Communication Market Overview

The Market for Satellite Communication is projected to reach $15.18 billion by 2030, progressing at a CAGR of 9.4% from 2024 to 2030. Satellite communication refers to the transmission of data, voice, and video signals using artificial satellites as relay stations. This technology enables communication over long distances, including areas where traditional terrestrial communication infrastructure is unavailable or impractical. Satellite communication systems typically involve the use of ground stations to uplink data to orbiting satellites, which then downlink the data to other ground stations or directly to end-users. These systems are employed in various applications, including telecommunications, broadcasting, navigation, remote sensing, and military operations. The rising demand for various applications such as audio broadcasting and voice communications in end-user industries is analyzed to fuel the growth of the satellite communication industry. The significant adoption of direct-to-home (DTH) in media and entertainment applications is set to positively impact the growth of the market as satellite communication plays a crucial role in communication in providing subscribers with high-quality content. An increase in the use of High Throughput Satellite (HTR) and Low Earth Orbit Satellite for high-speed broadcasting satellite services, cellular backhaul, and other value-added services such as video conferencing, VOIP is set to be the major driver for the growth of the market. The rising adoption of satellite telemetry, automatic identification systems, and Very Small Aperture Terminal markets with improved uplink frequency will drive the market growth.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐒𝐚𝐦𝐩𝐥𝐞

Report Coverage

The report based on: “Satellite Communication Market – Forecast (2024-2030)”, by IndustryARC covers an in-depth analysis of the following segments. By Technology: Satellite Telemetry, AIS, VSAT and Others. By Communication Network: Satellite Internet Protocol Terminals, Gateways, Modems and others. By Satellite Services: FSS, BSS, MSS, RNSS, Metrological Satellite Services, SBS, RSS. By Communication Equipment: Network Equipment, Consumer Devices. By End User: Commercial (Power and Utilities, Maritime, Mining, Healthcare, Telecommunication & others), Government & Military (Space Agencies, Defence, Academic Research & others). By Geography: North America (U.S, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, and Others), APAC (China, Japan India, South Korea, Australia and Others), South America (Brazil, Argentina and others), and ROW (Middle East and Africa).

Key Takeaways

Media and Entertainment is set to dominate the satellite communication market owing to the rising demand from a growing population. This is mainly attributed to the increasing demand for the internet and online streaming services such as Amazon Prime Video, Netflix and so on.

North America has dominated the market share in 2023, however APAC is analysed to grow at highest rate during the forecast period due to the high implementation of 5G in the mobile broadband technologies.

Deployment of 5G, requiring high bandwidth for communication is set to drive the market during the forecast period 2024-2030.

#Satellite Communication Market price#Satellite Communication Market size#Satellite Communication Market share

0 notes

Text

Collaborative Robots Market Size, Share, Growth and Industry Trends, 2030

The global collaborative robots market size was valued at USD 1.23 billion in 2022 and is expected to expand at a compound annual growth rate (CAGR) of 32.0%, from 2023 to 2030. The growth can be ascribed to the increasing adoption of collaborative robots, or cobots, in Small and Medium Enterprises (SMEs). These companies are increasingly investing in cobots to interact with humans in a shared workspace and automate manufacturing processes. The growth is further proliferated by technological advancements in the industry.

The integration of artificial intelligence and machine learning technologies in industrial robots is positively influencing the business space. Besides, the advent of 5G technology is also expected to stimulate the adoption of cobots in the manufacturing sector. The release of an industrial grade 5G wireless network by Nokia Corporation to meet the requirements of Industry 4.0 is a prominent example of such developments. The low-latency connectivity offered by 5G wireless solutions will help OEMs enhance robotic automation and increase the productivity, quality, and efficiency of the manufacturing processes.

The deployment of robots in industrial processes has also reduced the number of accident cases at workplaces. Moreover, they also significantly improve product quality, which is instigating their demand across various companies and enterprises. The increasing adoption of cobots in electronics, automotive, logistics, machine tooling, packaging, and assembling applications is expected to transform the outlook of the collaborative robots market over the foreseeable future.

Gather more insights about the market drivers, restrains and growth of the Collaborative Robots Market

Collaborative Robots Market Report Highlights

• The mounting adoption of collaborative robots is seen in several industrial applications, as they serve as assisting devices for humans and enhance the overall efficiency and quality of the manufacturing processes

• The collaborative robots industry is expected to witness strong growth in the coming years with the increasing adoption of cobots across small and medium enterprises, as they are cost-effective and provide a higher return on investment

• Europe captured a sizeable revenue share of more than 30.0% in 2022 owing to the increased product application in electronics, logistics, and inspection verticals

• Key market players include ABB Group, EPSON Robots, DENSO Robotics, Energid Technologies Corporation, Fanuc Corporation, F&P Robotics AG, MRK-Systeme GmbH, and KUKA AG

Browse through Grand View Research's Next Generation Technologies Industry Research Reports.

• The global robotic platform market size was estimated at USD 9.97 billion in 2023 and is projected to grow at a CAGR of 5.9% from 2024 to 2030.

• The global drone charging station market size was estimated at USD 0.43 billion in 2023 and is expected to grow at a CAGR of 6.5% from 2024 to 2030.

Collaborative Robots Market Segmentation

Grand View Research has segmented the global collaborative robots market based on payload capacity, application, vertical, and region:

Collaborative Robots Payload Capacity Outlook (Revenue, USD Billion, 2018 - 2030)

• Upto 5kg

• Upto 10kg

• Above 10kg

Collaborative Robots Application Outlook (Revenue, USD Billion, 2018 - 2030)

• Assembly

• Pick & Place

• Handling

• Packaging

• Quality Testing

• Machine Tending

• Gluing & Welding

• Others

Collaborative Robots Vertical Outlook (Revenue, USD Billion, 2018 - 2030)

• Automotive

• Food & Beverage

• Furniture & Equipment

• Plastic & Polymers

• Metal & Machinery

• Electronics

• Pharma

• Others

Collaborative Robots Regional Scope (Revenue, USD Billion, 2018 - 2030)

• North America

o U.S.

o Canada

o Mexico

• Europe

o Germany

o U.K.

o France

• Asia Pacific

o China

o Japan

o India

• South America

o Brazil

• Middle East and Africa

Order a free sample PDF of the Collaborative Robots Market Intelligence Study, published by Grand View Research.

#Collaborative Robots Market#Collaborative Robots Market size#Collaborative Robots Market share#Collaborative Robots Market analysis#Collaborative Robots Industry

0 notes

Text

Dielectric Resonator Antenna Market Key Drivers, Challenges, and Prominent Regions by 2032

Dielectric resonator antennas (DRAs) are advanced components used in wireless communication systems to provide high-performance signal transmission and reception. Unlike traditional antennas, DRAs utilize a dielectric resonator material to achieve compact size, high efficiency, and wide bandwidth. This makes them ideal for applications requiring high-frequency operation and compact form factors.

The dielectric material used in DRAs allows for precise control of the antenna's resonant frequency and impedance, resulting in enhanced performance characteristics such as improved gain, directivity, and bandwidth. DRAs are commonly used in applications including telecommunications, satellite communication, and radar systems.

The Dielectric Resonator Antenna Market is expected to witness substantial growth, reaching significant value by 2031 ,with a projected Compound Annual Growth Rate (CAGR) of 5.1% from 2024 to 2031.

Future Scope

The future of dielectric resonator antennas is characterized by continued innovation in materials and design techniques. Advances in dielectric materials and fabrication processes will enable the development of even more compact and efficient antennas, suitable for emerging wireless technologies and high-frequency applications.

The integration of DRAs with advanced technologies such as 5G and millimeter-wave communications is expected to drive further development. DRAs will play a crucial role in meeting the demanding requirements of next-generation wireless systems, offering enhanced performance and reliability.

Trends

Several key trends are shaping the development of dielectric resonator antennas. One significant trend is the growing demand for high-frequency and high-data-rate communication systems, driven by the proliferation of 5G and future 6G technologies. DRAs are well-suited for these applications due to their ability to operate at higher frequencies with minimal loss.

Another trend is the focus on miniaturization and integration. As electronic devices become more compact, there is a need for smaller and more efficient antennas that can be integrated into portable and wearable devices without compromising performance.

The development of advanced dielectric materials and innovative designs is also a key trend, enabling DRAs to achieve better performance metrics and meet the evolving requirements of modern communication systems.

Applications

Dielectric resonator antennas are used in a wide range of applications across telecommunications, satellite communication, and radar systems. In telecommunications, DRAs are employed in base stations, mobile phones, and other wireless devices to ensure high-quality signal transmission and reception.

In satellite communication, DRAs are used in ground stations and satellite terminals to achieve reliable and high-frequency communication. In radar systems, DRAs provide precise signal detection and tracking capabilities, enhancing the performance of various radar applications.

Solutions and Services