#50 lakh loan

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Premium Tumblr themes are available from anywhere between $9 to $49.

Text

Personal loans have become a popular choice for individuals needing substantial funds for diverse purposes such as medical emergencies, weddings, education, or business expansion. With banks and financial institutions offering personal loans up to Rs. 50 lakh, the application process has been simplified and digitized for convenience. Here’s a comprehensive guide to applying for a Rs. 50 lakh personal loan.

Step 1: Assess Eligibility

Before applying, it’s crucial to check if you meet the lender’s eligibility criteria. Common factors include:

Age: Typically, applicants should be between 21 to 60 years.

Income: A stable and sufficient income is necessary. Salaried individuals and self-employed professionals must meet minimum income requirements set by the lender.

Credit Score: A credit score of 750 or above improves approval chances.

Employment Stability: Salaried individuals need a stable job history, while self-employed individuals must show consistent business performance.

Existing Debt: Lower existing debt increases eligibility for a larger loan amount.

Step 2: Compare Lenders

Not all lenders offer loans up to Rs. 50 lakh. Compare different banks and financial institutions based on:

Interest Rates: Lower rates reduce overall cost.

Tenure: Choose a flexible repayment period (up to 5 years or more).

Processing Fees: Look for lenders with minimal charges.

Prepayment Policies: Consider institutions with favorable foreclosure or part-payment terms.

Use online loan aggregators and comparison tools for quick evaluation.

Step 3: Gather Required Documents

Ensure you have all the necessary documents to avoid delays. Common requirements include:

Identity Proof: Aadhaar Card, Passport, Voter ID, or Driving License.

Address Proof: Utility Bills, Ration Card, or Rent Agreement.

Income Proof:

Salaried: Salary slips, bank statements, and Form 16.

Self-employed: Business financials, ITR, and bank statements.

Employment Proof: Appointment letter or work certificate for salaried individuals.

Credit Reports: Some lenders may request your credit report.

Step 4: Apply for the Loan

You can apply online or visit a branch office. Here’s how to proceed:

Online Application:

Visit the lender's website or mobile app.

Fill in the application form with personal and financial details.

Upload scanned copies of required documents.

Await verification and approval, which might take a few hours to a few days.

Offline Application:

Visit the nearest branch of your chosen lender.

Submit a completed application form along with physical copies of documents.

Wait for the lender to process and verify your application.

Step 5: Verification and Approval

Lenders perform the following checks after receiving your application:

Document Verification: To confirm authenticity.

Creditworthiness Assessment: Based on your credit score, income, and financial obligations.

Background Check: Employment or business validation.

Once approved, you’ll receive a formal sanction letter specifying the loan terms.

Step 6: Disbursal of Funds

Upon signing the agreement, the loan amount is disbursed to your bank account. This can take anywhere from a few hours to a couple of days, depending on the lender.

Key Tips for Approval

Maintain a High Credit Score: Regularly repay EMIs and credit card bills on time.

Minimize Existing Debt: Lower debt increases eligibility for high-value loans.

Opt for Co-Borrowing: Adding a co-borrower with a strong financial profile enhances approval chances.

Negotiate: Use a solid credit history to negotiate better terms.

Conclusion

Applying for an instant approval personal loan for 50 lakh requires careful planning, eligibility checks, and comparison of lenders. With the digital transformation of banking, the process has become more efficient. By following these steps and preparing in advance, you can ensure a smooth and successful loan application process.

0 notes

Text

Applying for a high-value personal loan, such as a Rs 50 lakh loan, requires careful planning and understanding of the process. These loans are generally unsecured, meaning they do not require collateral, making them an attractive option for individuals needing significant funds for various personal reasons, such as medical emergencies, home renovations, or large purchases. Here's a comprehensive guide on how to apply for a Rs 50 lakh personal loan.

1. Determine Your Eligibility

Before applying for a high-value personal loan, it's crucial to ensure you meet the lender's eligibility criteria. Common factors that lenders consider include:

Age: Most banks and financial institutions require applicants to be between 21 and 60 years old.

Income: A higher income increases your chances of approval, as it demonstrates your ability to repay the loan. Lenders may have a minimum income requirement, which can vary depending on the lender and the loan amount.

Credit Score: A good credit score (usually 750 or above) is essential for getting approval for a large loan amount. It reflects your creditworthiness and history of repaying debts.

Employment Status: Being employed in a stable job or having a regular source of income (for self-employed individuals) is critical. Lenders prefer applicants with a steady job history and income.

2. Calculate Your Loan Amount and Tenure

Decide how much money you need and the tenure over which you want to repay the loan. While you may qualify for a Rs 50 lakh loan, it’s essential to borrow only as much as you need and can afford to repay. The loan tenure typically ranges from 12 months to 60 months. A longer tenure reduces the EMI amount but increases the total interest paid over the loan period.

3. Compare Lenders

Not all lenders offer the same terms and interest rates. It’s essential to shop around and compare various financial institutions, including banks and NBFCs (Non-Banking Financial Companies). Consider factors such as:

Interest Rates: Even a slight difference in interest rates can significantly affect the total cost of the loan.

Processing Fees: These are one-time fees charged for processing your loan application. Some lenders offer discounts or waive these fees for high-value loans.

Prepayment Charges: If you plan to repay the loan early, check if there are any prepayment penalties.

Customer Service: Opt for a lender known for good customer support and hassle-free loan processing.

4. Prepare Required Documents

To apply for a Rs 50 lakh personal loan, you need to provide various documents to prove your identity, income, and other personal details. Common documents required include:

Identity Proof: Aadhaar Card, PAN Card, Passport, Voter ID, or Driving License.

Address Proof: Utility bills, rental agreements, or bank statements.

Income Proof: Salary slips, bank statements for the last six months, or ITR (Income Tax Returns) for the last two years for self-employed individuals.

Employment Proof: Offer letter, employment certificate, or business registration documents for self-employed individuals.

5. Fill Out the Application Form

Once you have selected a lender, you can proceed with the application. Most lenders offer both online and offline application processes. Fill out the application form with accurate personal, financial, and employment details. Double-check all information to avoid any errors that could delay your loan approval.

6. Submit Your Application and Documents

After filling out the application form, submit it along with the required documents. For online applications, you can upload scanned copies of the documents. For offline applications, visit the bank branch or lender’s office to submit the form and documents in person.

7. Wait for Approval

Once your application and documents are submitted, the lender will verify your details. They may also perform a credit check and assess your repayment capacity. This process can take a few days to a week. If additional information or documents are required, the lender will contact you.

8. Loan Disbursement

Upon approval, you will receive a loan sanction letter detailing the loan amount, interest rate, tenure, and EMI amount. Review the terms carefully before accepting the loan offer. Once you accept, the loan amount will be disbursed to your bank account.

9. Repayment

Start repaying the loan as per the agreed EMI schedule. Ensure timely payments to avoid penalties and maintain a good credit score.

Final Thoughts

Applying for a personal loan 50 lakhs involves several steps, from checking eligibility and comparing lenders to submitting the application and receiving the funds. By following this guide and carefully considering all aspects of the loan, you can secure the funds you need while ensuring that you choose the best loan terms for your financial situation. Always remember to borrow responsibly and only take a loan you can comfortably repay.

0 notes

Text

Applying for a personal loan of Rs 50 lakh can be a crucial step in achieving various financial goals, whether it's for funding a wedding, consolidating debt, or undertaking home renovations. Given the substantial amount, it's important to understand the eligibility criteria, application process, documentation requirements, and best practices to increase your chances of approval. Here’s a detailed guide on how to apply for a Rs 50 lakh personal loan.

1. Understand Your Eligibility

Before applying for a personal loan of such a high amount, it’s essential to understand the eligibility criteria set by most banks and financial institutions:

Age: Typically, the applicant should be between 21 to 60 years old.

Income: A higher income often increases your chances of getting a large loan approved. Many banks have a minimum income requirement, which can vary depending on the lender and the city of residence.

Credit Score: A good credit score (usually above 750) is crucial as it reflects your creditworthiness and repayment capacity.

Employment Stability: Lenders usually prefer applicants who have a stable job or business. For salaried individuals, a minimum of 2-3 years of work experience is often required, whereas self-employed individuals should have a consistent business track record.

2. Research and Compare Lenders

Different banks and non-banking financial companies (NBFCs) offer varying interest rates, processing fees, loan tenures, and terms for personal loans. It’s advisable to:

Compare Interest Rates: Check the annual percentage rates (APR) offered by various lenders. Even a slight difference in interest rates can significantly affect the total repayment amount.

Understand Additional Charges: Apart from the interest rate, be aware of processing fees, prepayment charges, and any other hidden costs.

Check Loan Terms: The tenure of the loan affects your monthly installment. Longer tenures may reduce your EMIs but increase the overall interest payable.

3. Prepare the Required Documentation

To apply for a Rs 50 lakh personal loan, you will need to submit several documents. These typically include:

Identity Proof: PAN card, Aadhaar card, passport, voter ID, or driving license.

Address Proof: Utility bills, rental agreements, Aadhaar card, or passport.

Income Proof: Salary slips for the last 3-6 months, bank statements for the last 6-12 months, and IT returns.

Employment Proof: Employment certificate or letter from your employer (for salaried individuals).

Business Proof: Profit and loss statements, balance sheets, and proof of business continuity for at least 3 years (for self-employed individuals).

4. Apply Online or Offline

Most lenders offer both online and offline methods to apply for a personal loan. Here’s how you can proceed with each:

Online Application: Visit the lender's official website or use their mobile application. Fill out the application form with the necessary details, upload the required documents, and submit your application. Online applications are generally quicker and allow you to track your application status in real time.

Offline Application: Visit the nearest branch of your preferred bank or NBFC. Fill out the application form and submit it along with the necessary documents. While this method might be slower, it allows you to have face-to-face interactions and resolve any queries immediately.

5. Await Approval and Disbursement

After submitting your application, the lender will assess your eligibility based on your credit score, income, employment stability, and other factors. This process may take a few hours to several days, depending on the lender and whether the application is online or offline.

Once approved, you will receive a loan offer detailing the loan amount, interest rate, tenure, and repayment schedule. After accepting the offer, the loan amount is usually disbursed into your bank account within a few hours to a few days.

6. Key Tips for a Successful Loan Application

Maintain a High Credit Score: Regularly monitor your credit score and ensure timely payment of all existing debts to maintain a high score.

Avoid Multiple Applications: Submitting multiple loan applications in a short period can negatively impact your credit score and reduce the chances of approval.

Choose the Right Loan Amount: Apply for an amount that aligns with your repayment capacity. This will reduce the risk of default and ensure a smoother approval process.

Read the Fine Print: Before accepting any loan offer, thoroughly read the terms and conditions, including the repayment schedule, interest rates, and any additional charges.

Conclusion

Applying for a personal loan 50 lakh requires careful planning and an understanding of various financial aspects. By following the steps outlined above, you can navigate the loan application process more effectively and increase your chances of securing the funds you need. Remember to always borrow responsibly and choose a loan that suits your financial situation.

0 notes

Text

Study Abroad latest News in Gujarati. If your child is also planning to study abroad, the largest public sector bank, State Bank of India, is offering you an education loan of up to Rs 50 lakh without any guarantee.

#news#gujarati news#latest news#latest gujarati news#breaking news#breaking news in gujarati#SBI news#Study Abroad latest News in Gujarati#study abroad news#largest public sector bank#largest public sector bank SBI#education loan#education loan upto 50 lakh#bank loan#student loan#SBI Education loan

0 notes

Text

Personal loans have become a popular financial tool for individuals seeking immediate funds for various needs such as medical emergencies, higher education, home renovations, or even travel. Among these, high-value personal loans, like a 50 lakh personal loan, require specific eligibility criteria. Understanding these criteria is crucial for a smooth application process and quick approval. This article delves into the eligibility requirements for a 50 lakh personal loan, providing a comprehensive guide to help potential borrowers navigate the application process successfully.

Understanding Personal Loans

Personal loans are unsecured loans provided by financial institutions based on the borrower’s creditworthiness. Unlike secured loans, personal loans do not require collateral, making them an attractive option for those who do not have assets to pledge. The loan amount, interest rate, and repayment tenure vary based on the borrower’s profile and the lender’s policies.

Key Factors Influencing Eligibility

Income Level:

Salaried Individuals: For a 50 lakh personal loan eligibility, lenders typically require a stable and high income. The minimum monthly salary should be around INR 1-1.5 lakhs, depending on the lender.

Self-Employed Individuals: Self-employed professionals or business owners need to demonstrate a stable income with adequate annual turnover. The minimum annual income requirement usually ranges from INR 10-15 lakhs.

Age:

Most lenders require applicants to be within a specific age range, usually between 21 to 60 years for salaried individuals and 25 to 65 years for self-employed individuals.

Credit Score:

A high credit score is crucial for loan approval. A credit score above 750 is considered excellent and increases the chances of approval. It also helps in securing a lower interest rate.

Employment Stability:

Salaried Individuals: A minimum work experience of 2-3 years with at least one year in the current organization is typically required.

Self-Employed Individuals: A business vintage of at least 3 years with stable operations and profits is preferred.

Debt-to-Income Ratio:

Lenders assess the debt-to-income ratio to ensure that the borrower can manage the new loan along with existing obligations. A ratio below 40-50% is generally acceptable.

Existing Liabilities:

Lenders check existing loans and credit card debts to evaluate repayment capacity. Fewer liabilities increase the chances of loan approval.

Documentation Requirements

To apply for a 50 lakh personal loan, the following documents are typically required:

Identity Proof: Aadhar card, PAN card, passport, or voter ID.

Address Proof: Utility bills, rental agreement, or passport.

Income Proof:

Salaried: Latest salary slips, bank statements of the last 6 months, and Form 16.

Self-Employed: Income tax returns of the last 2-3 years, bank statements, and financial statements of the business.

Employment Proof: Employment certificate or business registration documents.

Credit Report: Recent credit report showcasing the credit score and history.

Application Process

Research and Compare:

Compare different lenders based on interest rates, processing fees, prepayment charges, and customer reviews. Use online comparison tools for a detailed analysis.

Pre-Qualification Check:

Many lenders offer a pre-qualification check online, which helps you understand if you meet the basic eligibility criteria without affecting your credit score.

Online Application:

Fill out the online application form on the lender’s website, providing all necessary details accurately. Ensure you upload the required documents in the specified format.

Verification:

The lender will conduct a thorough verification of the submitted documents and details. This may include a background check and a telephonic or physical verification.

Approval and Disbursement:

Upon successful verification, the lender will approve the loan and disburse the amount to your bank account. This process can take a few days to a couple of weeks.

Tips for Quick Approval

Maintain a High Credit Score:

Regularly monitor your credit score and take steps to improve it by timely repayment of existing loans and credit card bills.

Accurate Documentation:

Ensure all submitted documents are accurate and up-to-date. Any discrepancies can lead to delays or rejection.

Stable Income and Employment:

A stable job with a reputed organization or a profitable business increases credibility. Avoid frequent job changes or business disruptions.

Lower Existing Debts:

Clear outstanding debts or consolidate them to reduce the debt-to-income ratio, improving your loan eligibility.

Choose the Right Lender:

Opt for a lender with flexible eligibility criteria and a good track record of customer service. Consider banks, NBFCs, and online lenders.

Conclusion

Securing a 50 lakh personal loan requires meeting specific eligibility criteria related to income, credit score, employment stability, and existing liabilities. By understanding these requirements and following the tips for quick approval, you can enhance your chances of securing the desired loan amount. Remember to conduct thorough research and compare different lenders to find the best deal that suits your financial needs. A well-planned approach and adherence to eligibility criteria will pave the way for a smooth and successful loan application process.

#50 lakh personal loan#50 lakh personal loan eligibility#quick approval personal loan#online instant personal loan

0 notes

Text

How to Choose Between a Personal Loan and a Credit Card Loan?

Introduction

When facing financial needs, borrowers often consider two common credit options: a personal loan and a credit card loan. Both provide access to funds but differ in structure, repayment terms, and cost. Choosing the right option depends on the borrower's financial situation, repayment capacity, and the nature of the expense.

A personal loan is a lump-sum loan repaid in fixed EMIs over a predetermined tenure, whereas a credit card loan allows borrowing against an existing credit limit with flexible repayment. Understanding the differences between these two borrowing methods can help individuals make an informed financial decision.

This article compares personal loans and credit card loans, covering their features, benefits, and considerations to help borrowers choose the best option.

What Is a Personal Loan?

A personal loan is an unsecured loan provided by banks, NBFCs, and digital lenders. Borrowers receive a fixed amount, which is repaid in equal monthly installments (EMIs) over a set tenure.

Key Features of a Personal Loan:

Fixed loan amount disbursed as a lump sum.

Repayment tenure ranges from 12 to 60 months.

Fixed or variable interest rates (typically 10%-24% per annum).

No collateral required, making it accessible to a wide range of borrowers.

Quick disbursal, often within 24-48 hours for eligible applicants.

Used for multiple purposes, such as home renovation, medical expenses, or travel.

What Is a Credit Card Loan?

A credit card loan is a pre-approved loan offered by credit card issuers to cardholders based on their available credit limit. It is a short-term loan that allows users to convert their spending into EMIs or borrow additional funds.

Key Features of a Credit Card Loan:

Pre-approved loan available without additional documentation.

No separate application process since it’s linked to the existing credit card limit.

Shorter repayment tenure, usually 3 to 36 months.

Interest rates range between 12%-30% per annum, depending on the card issuer.

Instant approval and disbursal, often within minutes.

Higher interest rates compared to personal loans if not repaid within the EMI structure.

Comparing Personal Loans and Credit Card Loans

1. Loan Amount and Accessibility

Personal Loan: Borrowers can apply for higher loan amounts (₹50,000 to ₹50 lakhs) based on their income and creditworthiness.

Credit Card Loan: Loan amount is restricted by the available credit limit.

2. Repayment Flexibility

Personal Loan: Fixed EMIs ensure structured repayment over a longer period.

Credit Card Loan: Shorter tenure, but can be repaid early with higher flexibility.

3. Interest Rates

Personal Loan: Lower interest rates (10%-24% per annum) due to structured repayment.

Credit Card Loan: Higher interest rates (12%-30% per annum) if not converted into EMIs.

4. Loan Processing and Disbursal Time

Personal Loan: Approval takes a few hours to a few days, depending on documentation and verification.

Credit Card Loan: Instant approval and disbursal, making it ideal for emergencies.

5. Usage Restrictions

Personal Loan: Can be used for various personal and business needs.

Credit Card Loan: Typically used for short-term needs like travel, shopping, or emergencies.

6. Eligibility Criteria

Personal Loan: Requires income proof, credit score verification, and employment stability.

Credit Card Loan: Available only to existing credit cardholders with a good repayment track record.

When Should You Choose a Personal Loan?

A personal loan is the right choice when:

You need a higher loan amount beyond your credit card limit.

You prefer a structured repayment plan with fixed EMIs.

You are looking for lower interest rates for long-term borrowing.

You require funds for planned expenses like home renovation, education, or weddings.

When Should You Choose a Credit Card Loan?

A credit card loan is a better option when:

You need instant funds for short-term financial needs.

You have a pre-approved loan offer with competitive interest rates.

You want a flexible repayment schedule within a shorter tenure.

You prefer to avoid additional documentation and application processing.

Pros and Cons of Personal Loans and Credit Card Loans

Pros of a Personal Loan:

✅ Higher loan amounts available. ✅ Lower interest rates compared to credit card loans. ✅ Fixed EMIs provide structured repayment. ✅ Can be used for diverse financial needs.

Cons of a Personal Loan:

❌ Longer processing time compared to credit card loans. ❌ Requires income verification and credit assessment. ❌ Prepayment penalties may apply.

Pros of a Credit Card Loan:

✅ Instant loan approval and quick fund access. ✅ No additional paperwork required. ✅ Flexible repayment structure with EMI conversion options. ✅ Convenient for small, short-term financial needs.

Cons of a Credit Card Loan:

❌ Higher interest rates compared to personal loans. ❌ Loan amount limited by the credit card limit. ❌ Failure to repay on time leads to high penalty charges and interest accrual.

Conclusion: Which Loan Should You Choose?

The decision between a personal loan and a credit card loan depends on the borrower's financial needs and repayment capacity. If you require a large sum of money with a lower interest rate and fixed EMIs, a personal loan is the better option. However, if you need instant funds for short-term expenses with repayment flexibility, a credit card loan is more suitable.

Both borrowing options serve different purposes, and understanding their pros and cons will help you make a smarter financial decision. Always compare interest rates, processing fees, and repayment terms before choosing the best loan for your needs.

Looking for a personal loan or a credit card loan? Compare your options and apply for the most suitable financial solution today!

#personal loan#loan apps#fincrif#bank#nbfc personal loan#personal loan online#personal loans#finance#loan services#personal laon#Personal loan#Credit card loan#Personal loan vs credit card loan#Instant personal loan#Best loan option#Unsecured personal loan#Credit card cash advance#Online personal loan#Loan comparison#Personal loan eligibility#Personal loan interest rates#Credit card loan interest rates#How to choose a personal loan#Credit card loan benefits#Personal loan repayment#Loan approval process#Fixed EMI loan#Personal loan tenure#Best loan for short-term needs#Instant credit loan

2 notes

·

View notes

Text

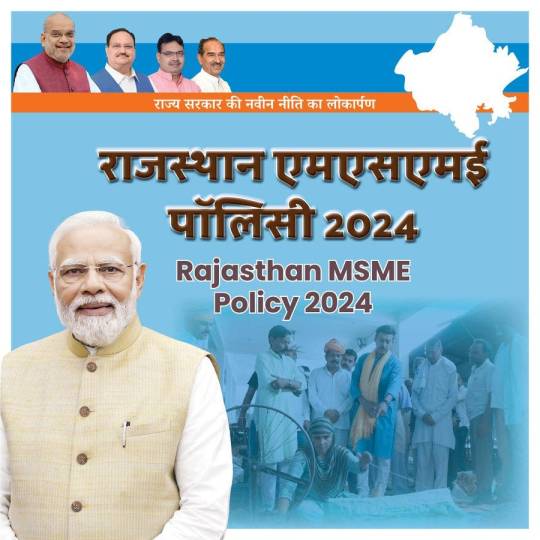

Rajasthan MSME Policy 2024: A New Era for Entrepreneurs by Col Rajyavardhan Rathore

In a landmark move to empower small businesses and foster economic growth, the Rajasthan MSME Policy 2024 has been introduced under the guidance of Colonel Rajyavardhan Rathore. This policy aims to position Rajasthan as a leader in the Micro, Small, and Medium Enterprises (MSME) sector by providing robust support, financial incentives, and a conducive ecosystem for entrepreneurs.

The Importance of MSMEs in Rajasthan

MSMEs are the backbone of Rajasthan’s economy, contributing significantly to employment and GDP. With their presence in sectors like handicrafts, textiles, agriculture, and technology, MSMEs have immense potential to drive growth and innovation. The Rajasthan MSME Policy 2024 seeks to address challenges faced by small businesses and unlock their full potential.

Vision of Col Rajyavardhan Rathore

Col Rajyavardhan Rathore envisions MSMEs as engines of Rajasthan’s economic progress. Speaking at the launch, he remarked: “MSMEs are not just businesses; they are dreams of hardworking individuals. This policy is a promise to support their aspirations and make Rajasthan a hub for entrepreneurial excellence.”

Key Objectives of the Rajasthan MSME Policy 2024

Economic Empowerment: Strengthen the MSME sector to boost Rajasthan’s GDP.

Employment Generation: Create sustainable jobs across urban and rural areas.

Ease of Doing Business: Simplify processes and remove bureaucratic hurdles.

Skill Development: Equip entrepreneurs and workers with the latest skills.

Sustainability: Promote green practices and energy-efficient solutions.

Highlights of the Rajasthan MSME Policy 2024

1. Financial Support

Subsidies and Incentives: Up to 50% subsidy on capital investment for new enterprises.

Low-Interest Loans: Special credit schemes through state-backed financial institutions.

Tax Exemptions: Relaxation in GST and other state taxes for a specified period.

2. Infrastructure Development

Industrial Clusters: Development of MSME-dedicated zones in key cities like Jaipur, Udaipur, and Jodhpur.

Common Facility Centers (CFCs): Shared spaces with advanced tools and technology.

Digital Infrastructure: High-speed internet and IT support for MSMEs.

3. Skill Training and Capacity Building

Partnerships with educational institutions to introduce MSME-focused courses.

Regular workshops on digital marketing, export readiness, and quality control.

Mentorship Programs with industry experts to guide budding entrepreneurs.

4. Streamlining Processes

Single-Window Clearance: Speedy approvals for setting up businesses.

Simplified Regulations: Reduction in compliance requirements for small enterprises.

Digital Portals: Online systems for registrations, tax filing, and grievance redressal.

5. Promoting Innovation

Research and Development Grants: Funding for MSMEs working on innovative products and solutions.

Technology Adoption: Subsidies for adopting automation and digital tools.

Startup Incubation Centers: Support for MSMEs transitioning into startups.

6. Export Promotion

Global Market Access: Partnerships with trade bodies for export opportunities.

Trade Fairs and Expos: Participation in national and international exhibitions.

Export Subsidies: Financial support for logistics and international marketing.

Sectors Targeted by the Policy

1. Handicrafts and Textiles

Strengthening Rajasthan’s traditional crafts through modern techniques and marketing support.

2. Agri-Based Industries

Encouraging food processing, organic farming, and value-added products.

3. Renewable Energy

Promoting MSMEs in solar panel manufacturing and other green technologies.

4. Technology and IT

Support for tech startups and MSMEs working in AI, software, and digital solutions.

Impact of the Rajasthan MSME Policy 2024

Economic Growth

An expected 30% rise in MSME contributions to the state GDP by 2026.

Increased revenue through exports and enhanced domestic production.

Job Creation

2 lakh new jobs to be created in urban and rural areas.

Empowerment of women and marginalized communities through focused programs.

Ease of Doing Business

Simplified processes to attract 5,000+ new MSME registrations annually.

Global Recognition

Enhanced visibility for Rajasthan’s MSMEs in international markets.

Col Rathore’s Commitment to MSMEs

Col Rajyavardhan Rathore has always championed policies that drive progress and innovation. His leadership in shaping the MSME Policy 2024 reflects his belief in the entrepreneurial spirit of Rajasthan.

In his words: “With this policy, we are not just supporting businesses; we are building dreams, livelihoods, and a prosperous Rajasthan.”

A Bright Future for MSMEs in Rajasthan

The Rajasthan MSME Policy 2024 is a game-changer for small businesses. By addressing key challenges and providing holistic support, it aims to transform the state into a hub of entrepreneurship and innovation. With Col Rajyavardhan Rathore’s vision and leadership, this policy is set to empower thousands of entrepreneurs and contribute significantly to Rajasthan’s economic growth.

4 notes

·

View notes

Text

Finding the Right Loan: A Guide to Loan Options and Choosing the Best Fit for You

Introduction

Finding the right loan product to fit your needs can be a challenging process. With so many options like personal loans, home loans, and business loans, how do you know which is best suited for you? In this post, we'll provide an overview of the major loan products available and factors to consider when choosing one, as well as how Loans Mantri can help simplify the loan application process.

Loans Mantri is an online loan marketplace that partners with over 30 top financial institutions in India including names like HDFC Bank, ICICI Bank, and Axis Bank. No matter what type of loan you need, Loans Mantri aims to provide customized options and a seamless application experience through their digital platform.

Whether you need funds for personal expenses, purchasing real estate, business financing or any other purpose, Loans Mantri can match you with the ideal lending product for your requirements from their network. Their online eligibility calculators and tools remove the guesswork from determining what loans you can qualify for based on your income, credit score and other details.

This post will walk through the key loan products offered through Loans Mantri and outline the most important points to factor in when deciding which option works for your financial situation. We'll also provide tips on how to apply and what to expect when going through Loans Mantri for your financing needs. Let's get started!

Types of Loans Available

Here are some of the major loan products offered through Loans Mantri's platform:

Personal Loans - These unsecured loans can be used for almost any personal purpose like debt consolidation, wedding expenses, home renovation, medical needs, or any other requirements. Interest rates are competitive and loan amounts can range from ₹50,000 to ₹25 lakhs based on eligibility.

Home Loans - Also called mortgage loans, these are for purchasing, constructing or renovating a residential property. Home loans offer extended repayment tenures of up to 30 years and relatively lower interest rates. The property becomes collateral against the loan amount.

Business Loans - Loans Mantri offers financing for a wide range of business needs like working capital, equipment purchases, commercial vehicle loans, construction requirements and more. Loan amounts can be from ₹10 lakhs to multiple crores.

Loan Against Property - By using your existing property as collateral, you can get a secured, high-value loan in return through this product. Interest rates are lower and you can get up to 50% of your property's current market value.

Other Loan Products - Loans Mantri also facilitates other lending options like credit cards, line of credit, gold loans, insurance financing, merchant cash advance for businesses etc. as per eligibility.

Factors to Consider When Choosing a Loan

When looking at the various loan options, here are some key factors to take into account:

- Loan amount required and ideal repayment tenure

- Interest rates and processing/administration fees

- Your repayment capacity based on income and expenses

- Purpose of the loan - personal needs, business growth, property purchase etc.

- Collateral availability for secured loans like home and property loans

- Flexibility in repayment - moratorium periods, EMIs, tenure etc.

- Prepayment and foreclosure charges, if any

Evaluating these parameters will help identify the loan that Aligns to your financial situation. Loansmantri's online tools also help estimate factors like eligibility amounts, EMIs, interest rates etc. to simplify decision making.

Applying for a Loan on Loans Mantri

The application process with Loans Mantri is quick, transparent and fully digital:

- Use the eligibility calculator to get an estimated loan amount you can qualify for.

- Fill out the online application by providing basic personal and financial details.

- Loans Mantri will run a soft credit check to view your credit score and report. This helps match products to your profile.

- Compare personalized loan quotes from multiple partner banks and NBFCs.

- Submit any required KYC documents and income proofs online.

- The application gets forwarded to the lender for further processing and approval.

- Track status directly through your Loansmantri dashboard. Get assistance from customer support if needed.

Conclusion

Loans Mantri aims to be a one-stop platform for all your lending needs. Their intuitive tools and partnerships with leading financial institutions help identify and apply for the ideal loan product for any purpose. Consider your requirements carefully and evaluate all options before choosing the right loan for your financial situation. With Loans Mantri, the entire process from application to disbursal can be completed digitally for an easier financing experience.

2 notes

·

View notes

Text

Top Flying Schools in India: Choosing the Best Academy for Pilot Training

India has a booming aviation industry, making pilot training in India a sought-after career path. Choosing the right flying school is crucial for aspiring pilots. This guide highlights the top flying schools in India and key factors to consider when selecting the best academy.

1. Key Factors to Consider

Before selecting a flying school, aspiring pilots should evaluate:

DGCA Approval: Ensure the academy is approved by the Directorate General of Civil Aviation (DGCA).

Fleet and Infrastructure: Check the availability of aircraft, flight simulators, and training facilities.

Experienced Instructors: A well-qualified faculty ensures quality training.

Placement Record: Schools with strong airline connections offer better job opportunities.

Cost of Training: Pilot training in India costs between ₹30-50 lakh, so consider affordability and loan options.

2. Top Flying Schools in India

Indira Gandhi Institute of Aeronautics (IGIA), Cochin

Located at Cochin International Airport.

Offers DGCA-approved Commercial Pilot License (CPL) training.

Strong industry connections.

Indira Gandhi Institute of Aeronautics, Chandigarh

Based at Chandigarh International Airport.

Provides CPL, Private Pilot License (PPL), and Flight Instructor courses.

Indira Gandhi Institute of Aeronautics, Amritsar

Offers structured training programs and high-quality aircraft.

Focuses on industry-relevant training.

Capt. Gopi Aviation, Bengaluru

Known for its modern facilities and affordable pricing.

Offers DGCA-approved courses with excellent training infrastructure.

National Flying Training Institute (NFTI), Gondia

A joint venture between CAE and the Government of India.

Provides world-class pilot training with modern aircraft and simulators.

Indira Gandhi Institute of Aeronautics, Kerala

Well-established flying school with a proven track record.

Specializes in CPL and multi-engine training.

Indira Gandhi Institute of Aeronautics, Pune

Offers top-notch pilot training with experienced instructors.

Provides international exposure.

3. Government vs. Private Flying Schools

Government-backed academies often have lower fees but limited seats, while private institutions provide more flexibility but at a higher cost. Students should evaluate their financial situation and long-term goals before choosing.

Conclusion

Choosing the right flying school for pilot training in India is a crucial step in becoming a pilot. Factors like accreditation, infrastructure, cost, and placement should be considered carefully. With India’s aviation sector expanding, a well-planned training journey can lead to a successful career in the skies.

0 notes

Text

A Complete Guide to Income Tax Return Filing in India

A Complete Guide to Income Tax Return Filing in India

Filing your Income Tax Return (ITR) is a crucial responsibility for every taxpayer in India. It ensures compliance with tax laws and helps individuals claim refunds, deductions, and other benefits. In this guide, we will walk you through the essentials of income tax return filing, its importance, and how GM Tax can simplify the process for you.

Why is Filing Income Tax Return Important?

Legal Compliance: Filing ITR is mandatory for individuals earning above the basic exemption limit.

Avoid Penalties: Non-filing can lead to penalties and legal consequences.

Easy Loan Approvals: Banks require ITR for loan applications.

Visa Processing: Many countries request ITR receipts as proof of income.

Claiming Refunds: If excess tax has been deducted, you can claim a refund.

Who Needs to File an Income Tax Return?

Individuals and entities required to file ITR include:

Salaried employees earning above the exemption limit

Self-employed professionals and business owners

Companies and partnership firms

Individuals with foreign income or assets

Those claiming tax refunds

Types of Income Tax Returns in India

There are different ITR forms based on the taxpayer’s income and category:

ITR-1 (Sahaj): For salaried individuals with income up to ₹50 lakh

ITR-2: For individuals and HUFs without business income

ITR-3: For individuals with business or professional income

ITR-4 (Sugam): For presumptive income from business and professions

ITR-5, 6, 7: For firms, companies, and trusts

How to File an Income Tax Return?

Filing ITR involves the following steps:

Gather Documents: Collect Form 16, bank statements, investment proofs, and other financial details.

Choose the Right ITR Form: Select the appropriate form based on your income type.

Calculate Taxable Income: Deduct exemptions and deductions under relevant sections.

Pay Any Due Tax: If additional tax is payable, clear it before filing.

File Online on the Income Tax Portal: Register, upload the return, and e-verify it.

How GM Tax Can Help?

At GM Tax, we offer expert assistance in filing your ITR hassle-free. Our services include:

Professional Tax Advisory: Get personalized tax-saving strategies.

Accurate Tax Computation: Minimize tax liability with accurate calculations.

Seamless Online Filing: Ensure timely and error-free submission.

Assistance in Refund Claims: Maximize your tax benefits and refunds.

Conclusion

Filing your ITR is not just a legal obligation but a financial necessity. Avoid last-minute rushes and penalties by seeking professional help from GM Tax. Contact us today for a stress-free tax filing experience!

Visit GM Tax to file your ITR today!

0 notes

Text

A Complete Guide to ITR Filing: Process, Benefits & Deadlines

Introduction:

Filing an Income Tax Return (ITR) is a fundamental obligation for all taxpayers. It ensures adherence to tax regulations and enables individuals to avail themselves of various tax benefits. Regardless of whether you are a salaried employee, a business proprietor, or a freelancer, timely submission of your ITR is of utmost importance. This guide aims to furnish you with comprehensive information regarding ITR filing, encompassing its significance, the different types of ITR, deadlines, and a detailed procedural outline.

What is ITR Filing?

ITR Filing is the procedure of presenting your income information to the tax authorities. This process is essential for determining your tax obligations and for claiming any potential refunds. Taxpayers are required to submit their ITR by the deadline set by the tax department each financial year.

Who Should File ITR?

ITR filing is compulsory for individuals and entities whose income surpasses the basic exemption threshold. Even if your income falls below the taxable limit, submitting an ITR can be advantageous for financial management and legal adherence. You should consider filing ITR if:

Your total income exceeds the taxable threshold.

You have income from various sources, including salary, rental income, or investments.

You intend to claim a tax refund.

You possess foreign assets or income.

You plan to apply for loans or visas, as ITR serves as a valid proof of income.

Different Categories of ITR Forms

Various ITR forms are available, tailored to different sources of income and categories of taxpayers. The most frequently utilized forms are as follows:

ITR-1 : Designed for salaried individuals and pensioners whose income does not exceed ₹50 lakh.

ITR-2 : Intended for individuals and Hindu Undivided Families (HUFs) earning income from capital gains, multiple properties, or foreign sources.

ITR-3: Applicable to professionals and business proprietors.

ITR-4 : Suitable for freelancers, small enterprises, and those filing under the presumptive taxation scheme.

ITR-5, 6, and 7: Meant for partnerships, corporations, and trusts.

Essential Documents for ITR Submission

To ensure accurate filing of your ITR, it is important to have the following documents ready:

PAN card

Aadhaar card

Form 16 (for salaried individuals)

Bank account information

Proof of investments (such as PPF, ELSS, insurance, etc.)

Details of rental income (if relevant)

Statements of capital gains

Certificates for loan interest (home loan, education loan, etc.)

TDS certificates (Form 26AS)

Procedure for Online ITR Filing

Assemble Documents: Gather all relevant income-related documents.

Access the Portal: Navigate to the official tax e-filing website and log in using your PAN and password.

Choose the Appropriate ITR Form: Select the correct form based on your income category.

Complete the Information: Accurately input personal and income details.

Review Tax Calculations: Verify tax liabilities and applicable deductions.

Submit the Form: File the ITR form online.

E-Verify Your Submission: Utilize Aadhaar OTP, net banking, or offline methods for verification.

Retain the Acknowledgment: Download and save the acknowledgment for future reference.

Due Dates for ITR Submission

The deadlines for ITR submission differ among various categories of taxpayers:

For Individuals and Hindu Undivided Families (HUFs): July 31 (for the preceding financial year)

For Businesses Subject to Audit: September 30

For Corporations and Limited Liability Partnerships (LLPs): October 31

Failure to submit ITR on time may result in penalties; therefore, it is prudent to file prior to the specified due date.

Advantages of Timely ITR Submission

Avoiding Penalties: Submitting on time prevents incurring late fees and interest.

Claiming Tax Refunds: If excess tax has been withheld, you are eligible to request a refund.

Facilitating Loan Approvals: Financial institutions require ITR as proof of income for loan applications.

Visa Applications: Numerous countries necessitate ITR as financial documentation for visa processing.

Ensuring Legal Compliance: Filing ITR guarantees adherence to tax regulations and mitigates legal complications.

Common Errors to Avoid When Submitting ITR

Selecting an incorrect ITR form.

Inputting inaccurate personal information.

Failing to report all sources of income.

Overlooking deductions and exemptions.

Neglecting to e-verify the return.

Conclusion

Filing ITR is not merely a legal requirement but also serves as a financial instrument that offers numerous advantages to taxpayers. Regardless of your tax liability status, submitting your ITR contributes to maintaining a clear financial record and provides access to various financial opportunities. It is essential to complete your ITR submission before the deadline to evade penalties and reap tax benefits.

Filing your Income Tax Return (ITR) is a crucial financial responsibility that ensures compliance with tax laws while offering benefits like tax refunds, loan approvals, and financial credibility. Understanding the ITR filing process, key deadlines, and available tax-saving opportunities can help taxpayers maximize their financial planning.

With the guidance of GTS Consultant India , individuals and businesses can streamline their tax filing process, ensuring accuracy, timely submissions, and adherence to regulations. Their expert assistance minimizes errors, reduces tax liabilities, and helps you take advantage of available deductions.

0 notes

Text

5 Reasons Why Term Insurance is a Must-Have for Entrepreneurs

Entrepreneurship is a journey filled with risks and rewards, but securing your family’s financial future should not be one of the uncertainties. In the fast-paced business world, entrepreneurs often need to pay more attention to their financial security while focusing on their ventures. This is where term insurance comes into play, offering essential coverage that ensures the well-being of your loved ones in the event of your untimely demise.

Here are five key reasons entrepreneurs should prioritise term insurance, with insights on how platforms like Policybazaar make it easier to find the right policy.

1. Financial Protection for Family and Dependents

Entrepreneurs, unlike salaried employees, often lack the safety net of employer-provided life insurance. A term insurance policy guarantees that your family will not bear the financial brunt of your absence. For instance, a ₹1 crore term plan can offer your loved ones a substantial payout to manage expenses such as home loans, education costs, and daily living expenses, ensuring they remain financially secure in your absence.

Statistics: According to a recent Policybazaar report, the entrepreneurs segment in India saw a 50% year-on-year growth in sales of term insurance and considered it a vital part of their financial planning strategy to protect their families.

2. Debt and Liability Coverage

Entrepreneurs often take on personal loans or business debt to fund their ventures. In the event of an untimely death, these liabilities could be passed on to family members, adding to their emotional stress. Term insurance provides a financial safety net to cover outstanding business debts, personal loans, and mortgages, preventing financial strain on your loved ones.

Example: A 40-year-old non-smoker can secure a ₹1 crore term insurance policy for approximately ₹10,500 per year, ensuring adequate coverage for personal and business liabilities.

3. Affordable and Flexible Coverage

Term insurance is one of the most affordable life insurance options, offering high coverage at low premiums. For entrepreneurs dealing with fluctuating income streams, the flexibility of term insurance, where you can adjust your coverage amount or add riders, makes it a cost-effective solution for long-term protection. These plans are suited for individuals of all ages, especially younger individuals, as they can secure a large cover at budget-friendly premiums.

Statistics: A major insight from the increase in term insurance sales at Policybazaar is that 74% of the new buyers are millennials aged 27 to 38.

4. Customizable Add-Ons for Enhanced Protection

Many term insurance policies allow you to add optional riders, such as Critical Illness or Accidental Death coverage, providing additional layers of financial security. These add-ons are particularly valuable for entrepreneurs, who often face greater financial unpredictability and health risks due to stress.

5. Tax Benefits

Term insurance not only provides financial security but also offers significant tax benefits. Premiums paid toward term insurance are eligible for tax deductions under Section 80C of the Income Tax Act, allowing entrepreneurs to save up to ₹1.5 lakh annually. Additionally, the death benefit received by beneficiaries is exempt from taxes under Section 10(10D), further ensuring that your family’s financial future is protected from tax liabilities.

0 notes

Text

Applying for a personal loan of Rs 50 lakh can be a significant financial decision. Whether you need the funds for a business venture, medical emergency, home renovation, or any other major expense, understanding the application process is crucial. Here's a detailed guide to help you navigate the steps involved in applying for such a large personal loan.

1. Assess Your Eligibility

Before applying for a Rs 50 lakh personal loan, it's important to assess your eligibility. Most financial institutions have specific criteria, including:

Age: Typically, applicants should be between 21 and 60 years old.

Income: A high income is often required to secure a large loan amount. Lenders may require a monthly income of at least Rs 1 lakh.

Employment: Stable employment with a reputable organization, or a well-established business if self-employed, is preferred.

Credit Score: A good credit score (750 or above) increases your chances of approval and helps in securing a lower interest rate.

Debt-to-Income Ratio: Lenders consider your existing debt compared to your income to ensure you can manage additional loan payments.

2. Choose the Right Lender

Selecting the right lender is crucial. Research various banks, non-banking financial companies (NBFCs), and online lending platforms. Compare their interest rates, processing fees, and loan terms. Look for lenders that offer competitive rates and flexible repayment options. Some lenders may have pre-approved loan offers for existing customers, which can simplify the process.

3. Calculate Your EMI

Before proceeding with the application, calculate the Equated Monthly Installment (EMI) for your Rs 50 lakh loan. Most lenders provide online EMI calculators where you can input the loan amount, interest rate, and tenure to get an estimate. Ensure the EMI fits within your monthly budget without straining your finances.

4. Gather Required Documents

Documentation is a key part of the loan application process. Prepare the following documents:

Identity Proof: Aadhaar card, PAN card, passport, or driving license.

Address Proof: Utility bills, rental agreement, or passport.

Income Proof: Salary slips, income tax returns (ITR), and bank statements for the last six months.

Employment Proof: Offer letter, appointment letter, or employment certificate.

Business Proof (if self-employed): Business registration certificate, GST returns, and audited financial statements.

Credit Score Report: Some lenders may ask for a recent credit score report.

5. Fill Out the Application Form

Once you’ve chosen a lender, you can either apply online or visit the branch to fill out the application form. Ensure that all the details are accurate and match the information in your documents. Double-check the loan amount, tenure, and interest rate before submitting the application.

6. Submit the Application and Await Approval

After submitting your application along with the required documents, the lender will verify your details. This process may include background checks, credit score assessment, and income verification. If everything is in order, the lender will approve your loan application. The approval process can take anywhere from a few hours to a few days, depending on the lender.

7. Loan Disbursement

Once your loan is approved, the lender will disburse the amount directly to your bank account. In the case of a Rs 50 lakh loan, disbursement may be done in a lump sum or in tranches, depending on the lender's policy and your needs.

8. Repayment

Repaying a Rs 50 lakh personal loan requires careful financial planning. Ensure that you have a clear repayment strategy to avoid defaults, which can negatively impact your credit score and lead to penalties. Most loans offer the option of prepayment or part-payment, which can help reduce the interest burden.

Conclusion

Applying for a Rs 50 lakh loan involves careful planning, from assessing your eligibility to selecting the right lender and preparing the necessary documentation. By following the steps outlined in this guide, you can streamline the application process and increase your chances of approval. Remember, responsible borrowing and timely repayment are key to maintaining a healthy financial profile.

0 notes

Text

Urgent Cash Loan in Delhi – Get Instant Financial Help with LoansWala

When financial emergencies strike, waiting for traditional bank loans is not an option. Whether you need money for personal expenses, business investments, or buying a car or home, LoansWala is here to help! As a leading loan finance company in Delhi, LoansWala offers urgent cash loans in Delhi with quick approvals, minimal documentation, and flexible repayment options.

No matter your financial needs, LoansWala provides a range of loans, including personal loans, business loans, flat loans, and car loans, ensuring that you get the right financial support exactly when you need it.

Why Choose LoansWala for an Urgent Cash Loan in Delhi?

LoansWala makes borrowing easy, fast, and hassle-free. Here’s why it’s the best choice for an urgent cash loan in Delhi:

✔ Quick Loan Approval – Get approved within hours. ✔ Minimal Documentation – No complex paperwork required. ✔ Flexible Repayment Plans – Choose an EMI plan that suits your budget. ✔ No Hidden Charges – Transparent and fair loan terms. ✔ Secure Transactions – 100% safe loan process.

LoansWala is a trusted loan finance company in Delhi, offering reliable financial solutions tailored to your needs.

Types of Loans Available at LoansWala

LoansWala provides multiple loan options to cater to different financial needs.

1. Personal Loan

A personal loan is ideal when you need instant cash for emergencies, weddings, travel, education, or other expenses.

No collateral required – Unsecured loan.

Flexible repayment tenure – Choose the best EMI plan.

Loan amount up to ₹10 lakhs based on eligibility.

Fast approval and disbursal within 24 hours.

Know more about Personal Loan:- https://www.loanswala.in/personal.php

2. Business Loan

Need funds to expand or start a business? LoansWala offers business loans with easy eligibility and fast processing.

Loan amount up to ₹50 lakhs for business expansion.

Low-interest rates with flexible repayment options.

No need for extensive paperwork – Fast and hassle-free application.

Ideal for startups, small businesses, and self-employed individuals.

Know more about Business Loan:- https://www.loanswala.in/business.php

3. Flat Loan (Home Loan)

Dreaming of owning a home in Delhi? LoansWala provides flat loans at competitive interest rates.

Loan amount up to ₹1 crore for buying or renovating a house.

Low-interest rates and long repayment tenure of up to 30 years.

Minimal processing fees and quick approval.

Available for salaried and self-employed individuals.

Know more About Flat Loan:- https://www.loanswala.in/homeloan.php

4. Car Loan

Want to buy a new or used car? LoansWala offers car loans with attractive interest rates.

Loan amount up to ₹25 lakhs for new or used cars.

Low EMI options with flexible repayment tenure.

Instant approval and disbursal for quick car purchase.

Available for salaried and self-employed individuals.

Know more About Car Loan:- https://www.loanswala.in/car.php

Eligibility Criteria for Getting a Loan at LoansWala

To apply for a loan, you must meet these simple eligibility requirements:

✔ Age: 21 to 60 years ✔ Employment Status: Salaried or self-employed ✔ Income Requirement: Minimum ₹15,000 per month ✔ Credit Score: Preferred but not mandatory ✔ Required Documents: Aadhaar Card, PAN Card, income proof, and bank statements

How to Apply for an Urgent Cash Loan at LoansWala?

Step 1: Online Application

Visit LoansWala and fill out the loan request form.

Step 2: Submit Documents

Upload KYC documents and income proof for verification.

Step 3: Loan Approval

Your application is reviewed, and approval is granted within hours.

Step 4: Instant Disbursal

Once approved, the loan amount is transferred to your bank account immediately.

Benefits of Taking a Loan from LoansWala

✔ Low Interest Rates – Affordable repayment plans. ✔ Fast Processing – Get money when you need it the most. ✔ Secure Transactions – 100% safe and transparent process. ✔ Flexible Tenure – Choose repayment terms that fit your budget. ✔ No Collateral Required – Most loans are unsecured.

Things to Consider Before Applying for a Loan in Delhi

Before applying, keep these factors in mind:

Loan Amount: Borrow only what you need.

Interest Rates: Compare rates to find the best deal.

Repayment Tenure: Shorter tenure means higher EMIs.

Credit Score Impact: Late payments can lower your credit rating.

Common Reasons for Applying for Urgent Cash Loans in Delhi

Medical Emergencies – Sudden hospitalization or treatment costs.

Business Expansion – Investment in small businesses.

Home Purchase or Renovation – Buying a flat or home improvement.

Education Expenses – Paying tuition fees or course expenses.

Car Purchase – Buying a new or used vehicle.

Why LoansWala is the Best Loan Finance Company in Delhi?

LoansWala is a trusted name in the loan finance industry in Delhi, offering reliable and customer-friendly loan services.

✔ Fastest Loan Disbursal – Quick access to cash when needed. ✔ No Hidden Charges – Transparent process without extra fees. ✔ Flexible Repayment Options – Choose repayment terms that work for you. ✔ Trusted by Thousands of Customers – Excellent reviews and customer support.

Frequently Asked Questions (FAQs)

1. How fast can I get an urgent cash loan in Delhi from LoansWala?

Loans are approved within hours, and the amount is disbursed the same day.

2. What is the maximum loan amount I can get?

LoansWala offers personal loans up to ₹10 lakhs, business loans up to ₹50 lakhs, flat loans up to ₹1 crore, and car loans up to ₹25 lakhs.

3. Do I need a guarantor for an urgent loan?

No, most loans are unsecured and do not require a guarantor.

4. Can I apply if I have a low credit score?

Yes, LoansWala considers applicants with low credit scores.

5. How can I repay my loan?

You can repay through EMIs using online banking, UPI, or direct bank transfers.

0 notes

Text

Home Loan for 40000 Salary: Eligibility, EMI & Best Lenders

Whether being a homeowner is a dream comes down to an individual's perspective, however, one of the significant aspects impacting home loan approval is income. Earning a monthly salary of Rs. 40,000 brings to mind a couple of queries such as how much home loan can one receive, what are the eligibility criteria, and which are the best lenders in this category.

This blog provides a comprehensive guide to home loan for 40000 salary, including eligibility, EMI calculations, and the top lenders to consider.

Home Loan Eligibility for 40000 Salary

Lenders assess various factors before approving a home loan. Some of the primary eligibility criteria include:

1. Income-Based Loan Amount

Most banks and NBFCs offer home loans based on the applicant’s income. A general rule is that lenders provide loans up to 50-60% of the net monthly income. For a Rs. 40,000 salary, the potential loan amount can be estimated as follows:

Loan Amount: Rs. 20-30 lakhs (approx.)

Loan Tenure: Up to 30 years

Interest Rate: 8-9% (varies by lender)

2. Employment Type

Salaried Employees: Must have a stable job with at least 2-3 years of work experience.

Self-Employed Individuals: Should have a consistent income history and proper documentation (IT returns, profit & loss statements, etc.).

3. Credit Score

A CIBIL score of 700 or above is preferred by lenders. A high credit score improves loan eligibility and helps secure lower interest rates.

4. Existing Liabilities

If you have existing loans (personal loans, car loans, credit card EMIs), they impact your loan eligibility. Banks use the Fixed Obligations to Income Ratio (FOIR) to determine your repayment capacity.

EMI Calculation for Home Loan on 40000 Salary

Your Equated Monthly Installment (EMI) depends on the loan amount, interest rate, and tenure. Below is an estimated EMI calculation for different loan amounts:

EMI Formula: Where:

P = Loan Principal Amount

r = Monthly Interest Rate (Annual Interest Rate/12/100)

n = Loan Tenure (in months)

How to Reduce EMI?

Opt for a longer tenure (though total interest paid increases).

Pay a higher down payment to reduce the loan amount.

Choose a lender with a lower interest rate.

Best Banks Offering Home Loans for 40000 Salary

Here are some of the top banks and NBFCs offering home loans for a Rs. 40,000 salary:

1. State Bank of India (SBI)

Interest Rate: 8.40% – 9.50%

Maximum Loan Tenure: 30 years

Processing Fee: 0.35% of the loan amount

2. HDFC Bank

Interest Rate: 8.50% – 9.00%

Maximum Loan Amount: 80% of property value

Flexible repayment options

3. ICICI Bank

Interest Rate: 8.60% – 9.50%

Special offers for salaried professionals

Quick processing

4. Axis Bank

Interest Rate: 8.45% – 9.55%

Loan Amount: Up to 80% of property value

Flexible EMI options

5. LIC Housing Finance

Interest Rate: 8.75% – 9.25%

Lower processing fees

No prepayment charges for floating rate loans

Tips to Increase Home Loan Eligibility

Improve Your Credit Score: A score of 750+ boosts loan eligibility.

Reduce Existing Debt: Pay off credit card dues and personal loans.

Add a Co-Applicant: A spouse or parent can help increase the loan amount.

Opt for a Longer Tenure: This reduces EMI burden and improves approval chances.

Increase Down Payment: A higher down payment reduces the loan amount and lowers lender risk.

Conclusion

If you have a salary of Rs. 40,000, you can secure a home loan between Rs. 20-30 lakhs, depending on eligibility factors. Understanding EMI calculations, improving credit scores, and choosing the right lender can help you get the best deal. Compare different banks, check the interest rates, and opt for a loan that best fits your repayment capacity.

0 notes

Text

Everything You Need to Know About HDFC Business Loans: A Complete Guide

For a running business, financial support is always needed, whether for expansion, working capital, or buying equipment. HDFC Business Loan is one of the sought-after financial solutions for business owners who wish to get quick and easy money and this guide will clarify all aspects of HDFC Business Loan that also include features, eligibility criteria, procedure of application, and benefits. More significantly, we will also find out how Arena Fincorp can help in securing the loan for your business.

What is HDFC Business Loan?

HDFC Business Loan is an unsecured loan provided to businesses to meet their financial needs. That means the loan is programmed with no collateral option; this is what makes such loans particularly attractive to start-ups and small businesses. For businesses, competitive rates of interest, the option of flexible repayment, and fast processing times create a cause for small and medium enterprise owners to ask for such loans.

Key points of HDFC Business Loan

High Amount of Loan - The smallest amount a business can get is ₹ 50000, while others can go as high as ₹ 50 lakhs, depending on their eligibility criteria.

No Security Required - Businesses are not required to offer an asset as security.

Flexible Tenure - Offers a repayment period of 12 to 48 months, with which EMIs can very easily finance.

Quick Processing - In addition, the turnaround process is quick because an application is easy to fill and approval and disbursement follow almost immediately.

Minimum Documentation - Essentially, the paperwork involved in obtaining the loan is kept at the barest minimum, making it very easy for the business owner.

The Eligibility Arguments of HDFC Business Loan Are:

Business should be operational for a minimum period of three years.

Revenue should meet the required minimum level for that past year

Applicants should be aged between 21 and 65 years.

A credit track record and a CIBIL score of 700 are preferred.

Documents Required for HDFC Business Loan:

HDFC Business Loan:

The Steps Guide on What to Do to Get a Loan at HDFC

You can avail a HDFC Business loan from different channels such as online, find a branch, lookup at finance service providers such as Arena Fincorp, among others.

For online Loans

You would like to go to the HDFC Bank official site.

On the main site, please go to the Business Loans portion.

Provide the necessary information and proceed.

Additionally one will still need certain documents.

Submit the application so as to proceed and keep checking until approved.

Arena Fincorp Option

Loan application at Arena Fincorp has been made simpler and quick due to the expert consultation and personal loan product options that are available.

Locate Arena Fincorp for any guidance.

Examination of your status and what should be done will be provided by their highly qualified department.

It is advisable that once prequalification is done, submit an application using their platform for fast facilitation of the process.

Know the status of your loan in real-time.

The Advantages of Applying for a HDFC Commercial Loan through Arena Fincorp

Knowledgeable Consultation - An in-Depth Assessment of loan eligibility and requirements is provided by Arena Fincorp.

Expedited Approval - This equates to a significant reduction in approval and disbursement time because of the help that they offer.

Enhanced Likelihood - The odds of getting a loan are often better with assistance.

Respect for The Needs - Appropriate loan conditions are found for the client’s business.

Customer Services – Assistance with loans repayment and financial management is always provided by Arena Fincorp even after loan approval.

Interest Rates and Charges of HDFC Business Loan

Interest rates on HDFC Business Loan largely depend on the business profile, loan amount, and tenure. These charges will include such things as:

Interest Rate - Applicable at 10.99% per annum

Processing Fee - Up to 2.5% of the loan amount

Pre-Payment Charges - 2-4% depending on loan tenure

Among the primary factors that may cause rejection of any HDFC business loan application are the following:

Poor history in credit repayment or no improvement in credit scoring.

Inadequate or improper turnover of the business.

Inadequate documentation.

Greater preempted burden on the loans affects the repayment capacity.

Three ways of getting a higher acceptance rate of the loan are:

Good stability in the pose of a credit score above 700 Businesses Finance should be consistent and updated.

All documentation should be valid and well-prepared.

Try to reduce as many liabilities as you can before you take a loan.

Get kind assistance from Arena Fincorp, making your loan application very worthwhile.

Conclusion

HDFC business loans provide a realistic way for quickly mobilizing finances for a business; whether it is expansion, purchase of inventory, or operational costs, it offers flexibility and ease of application. Alternatively, one can apply through Arena Fincorp and gain better odds of receiving the best loan terms under professional guidance and faster processing.

With reference to the aforementioned steps in this guide, you can apply for your HDFC Business Loan intelligently to have a good nodding business. Should you have concerns about one or two things that looked seemingly difficult, never relent to knock on Arena Fincorp's door for an effortless loan application experience.

0 notes