#5 Lakh Loan

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Forty percent of Tumblr users are between the ages of 18 to 25.

Text

Securing a personal loan has become increasingly popular in India due to its ease of access and versatility. A personal loan of ₹5 lakhs can be a significant amount to cover various needs, from medical emergencies and wedding expenses to home renovations and debt consolidation. This guide will walk you through everything you need to know about obtaining a ₹5 lakh personal loan in India, including eligibility criteria, application process, benefits, and tips to ensure a smooth loan approval.

Understanding Personal Loans

A personal loan is an unsecured loan, meaning it does not require collateral or security. Banks and non-banking financial companies (NBFCs) offer personal loans based on the borrower’s creditworthiness. Unlike home or car loans, personal loans can be used for a variety of purposes, making them a flexible financial tool.

Eligibility Criteria for a ₹5 Lakh Personal Loan

Eligibility criteria may vary slightly between lenders, but the following are the general requirements:

Age: Most lenders require applicants to be between 21 and 60 years old.

Income: A stable income is crucial. Salaried individuals typically need a minimum monthly income of ₹20,000-₹25,000, while self-employed individuals need to show consistent earnings.

Employment: Salaried individuals should have at least one year of work experience, with six months in the current organization. Self-employed individuals should have been in business for at least two years.

Credit Score: A good credit score (typically 700 and above) is essential as it indicates the borrower’s creditworthiness.

Nationality: Applicants must be Indian residents.

Documentation Required

Lenders require specific documents to process a personal loan application. The essential documents include:

Proof of Identity: Aadhar card, PAN card, passport, voter ID, or driving license.

Proof of Address: Utility bills, rental agreement, passport, or voter ID.

Proof of Income: Salary slips for the last three months, bank statements for the last six months, and Form 16 for salaried individuals. Self-employed individuals need to provide income tax returns, bank statements, and financial statements.

Employment Proof: Offer letter or appointment letter for salaried individuals.

Photographs: Passport-size photographs.

Application Process

Applying for a personal loan of 5 lakhs, is straightforward. Here are the steps:

Research and Compare: Research different lenders and compare interest rates, processing fees, and other charges.

Check Eligibility: Use online eligibility calculators available on lender websites to check your eligibility.

Gather Documents: Ensure you have all the required documents ready.

Apply Online or Offline: You can apply online through the lender’s website or visit the branch.

Submit Documents: Upload or submit the necessary documents.

Verification: The lender will verify the documents and check your credit score and history.

Approval and Disbursal: Once verified, the lender will approve your loan, and the amount will be disbursed to your bank account.

Interest Rates and Charges

Interest rates for personal loans vary between lenders and can range from 10% to 24% per annum. Factors influencing interest rates include the applicant’s credit score, income, employment history, and the lender’s policies. Additionally, there may be processing fees (1-3% of the loan amount), prepayment charges, and late payment penalties.

Benefits of a ₹5 Lakh Personal Loan

No Collateral Required: As an unsecured loan, you don’t need to pledge any assets.

Flexible Usage: Use the loan amount for any personal need, such as medical emergencies, weddings, or home renovations.

Quick Processing: Loan approval and disbursal are usually fast, often within 24-48 hours.

Easy Documentation: Minimal documentation is required compared to other loan types.

Flexible Tenure: Repayment tenure ranges from 1 to 5 years, allowing you to choose a comfortable EMI amount.

Tips for Quick Approval

Maintain a Good Credit Score: Regularly check and maintain a high credit score by paying your bills and existing loans on time.

Reduce Existing Debt: Lower your existing debt to income ratio by clearing other loans or credit card dues.

Choose the Right Lender: Select a lender whose eligibility criteria you meet comfortably.

Accurate Documentation: Ensure all submitted documents are accurate and up to date.

Show Stable Income: Demonstrate a stable income source and consistent employment history.

Repayment and EMIs

Repayment of a personal loan is done through Equated Monthly Installments (EMIs). EMI is calculated based on the loan amount, interest rate, and tenure. Using an EMI calculator, available on most lender websites, you can determine the monthly installment and plan your finances accordingly.

For instance, if you take a ₹5 lakh loan at an interest rate of 12% per annum for a tenure of 3 years, the EMI would be approximately ₹16,607. It’s essential to ensure timely EMI payments to maintain a good credit score and avoid penalties.

Things to Consider Before Taking a Personal Loan

Assess Your Needs: Borrow only the amount you need to avoid unnecessary debt.

Understand the Costs: Be aware of all costs, including interest rates, processing fees, and any other charges.

Repayment Capacity: Ensure you can comfortably repay the loan without straining your finances.

Loan Tenure: Choose a tenure that offers manageable EMIs without extending the debt period unnecessarily.

Compare Offers: Don’t settle for the first offer; compare multiple lenders to get the best terms.

Conclusion

A 5 lakh personal loan can be a valuable financial resource to meet various personal needs. By understanding the eligibility criteria, application process, interest rates, and repayment terms, you can make informed decisions and choose the best loan offer. Remember to maintain a good credit score, reduce existing debts, and carefully plan your finances to ensure a smooth loan approval and repayment process.

#500000 personal loan#personal loan of 5 lakhs#5 lakhs personal loan#How to get 5 lakh personal loan#5 Lakh Personal Loan#5 Lakh Loan#loan 5 lakh

0 notes

Text

Experience Hassle-Free Loans with Loan Suvidhaa

At Loan Suvidhaa, we understand that securing a loan can be daunting. That's why we offer a range of tailored loan solutions, from personal loans to vehicle loans and more, designed to meet your unique financial needs. Our team of experts is dedicated to guiding you through every step of the loan process, ensuring transparency and efficiency. With competitive interest rates and flexible repayment options, we make it easier than ever to achieve your financial goals. Join Loan Suvidhaa today and experience the difference! For more information, visit the website www.loansuvidhaa.com

0 notes

Text

Securing a personal loan has become increasingly popular in India due to its ease of access and versatility. A personal loan of ₹5 lakhs can be a significant amount to cover various needs, from medical emergencies and wedding expenses to home renovations and debt consolidation. This guide will walk you through everything you need to know about obtaining a ₹5 lakh personal loan in India, including eligibility criteria, application process, benefits, and tips to ensure a smooth loan approval.

Understanding Personal Loans

A personal loan is an unsecured loan, meaning it does not require collateral or security. Banks and non-banking financial companies (NBFCs) offer personal loans based on the borrower’s creditworthiness. Unlike home or car loans, personal loans can be used for a variety of purposes, making them a flexible financial tool.

Eligibility Criteria for a ₹5 Lakh Personal Loan

Eligibility criteria may vary slightly between lenders, but the following are the general requirements:

Age: Most lenders require applicants to be between 21 and 60 years old.

Income: A stable income is crucial. Salaried individuals typically need a minimum monthly income of ₹20,000-₹25,000, while self-employed individuals need to show consistent earnings.

Employment: Salaried individuals should have at least one year of work experience, with six months in the current organization. Self-employed individuals should have been in business for at least two years.

Credit Score: A good credit score (typically 700 and above) is essential as it indicates the borrower’s creditworthiness.

Nationality: Applicants must be Indian residents.

Documentation Required

Lenders require specific documents to process a personal loan application. The essential documents include:

Proof of Identity: Aadhar card, PAN card, passport, voter ID, or driving license.

Proof of Address: Utility bills, rental agreement, passport, or voter ID.

Proof of Income: Salary slips for the last three months, bank statements for the last six months, and Form 16 for salaried individuals. Self-employed individuals need to provide income tax returns, bank statements, and financial statements.

Employment Proof: Offer letter or appointment letter for salaried individuals.

Photographs: Passport-size photographs.

Application Process

Applying for a personal loan of 5 lakhs, is straightforward. Here are the steps:

Research and Compare: Research different lenders and compare interest rates, processing fees, and other charges.

Check Eligibility: Use online eligibility calculators available on lender websites to check your eligibility.

Gather Documents: Ensure you have all the required documents ready.

Apply Online or Offline: You can apply online through the lender’s website or visit the branch.

Submit Documents: Upload or submit the necessary documents.

Verification: The lender will verify the documents and check your credit score and history.

Approval and Disbursal: Once verified, the lender will approve your loan, and the amount will be disbursed to your bank account.

Interest Rates and Charges

Interest rates for personal loans vary between lenders and can range from 10% to 24% per annum. Factors influencing interest rates include the applicant’s credit score, income, employment history, and the lender’s policies. Additionally, there may be processing fees (1-3% of the loan amount), prepayment charges, and late payment penalties.

Benefits of a ₹5 Lakh Personal Loan

No Collateral Required: As an unsecured loan, you don’t need to pledge any assets.

Flexible Usage: Use the loan amount for any personal need, such as medical emergencies, weddings, or home renovations.

Quick Processing: Loan approval and disbursal are usually fast, often within 24-48 hours.

Easy Documentation: Minimal documentation is required compared to other loan types.

Flexible Tenure: Repayment tenure ranges from 1 to 5 years, allowing you to choose a comfortable EMI amount.

Tips for Quick Approval

Maintain a Good Credit Score: Regularly check and maintain a high credit score by paying your bills and existing loans on time.

Reduce Existing Debt: Lower your existing debt to income ratio by clearing other loans or credit card dues.

Choose the Right Lender: Select a lender whose eligibility criteria you meet comfortably.

Accurate Documentation: Ensure all submitted documents are accurate and up to date.

Show Stable Income: Demonstrate a stable income source and consistent employment history.

Repayment and EMIs

Repayment of a personal loan is done through Equated Monthly Installments (EMIs). EMI is calculated based on the loan amount, interest rate, and tenure. Using an EMI calculator, available on most lender websites, you can determine the monthly installment and plan your finances accordingly.

For instance, if you take a ₹5 lakh loan at an interest rate of 12% per annum for a tenure of 3 years, the EMI would be approximately ₹16,607. It’s essential to ensure timely EMI payments to maintain a good credit score and avoid penalties.

Things to Consider Before Taking a Personal Loan

Assess Your Needs: Borrow only the amount you need to avoid unnecessary debt.

Understand the Costs: Be aware of all costs, including interest rates, processing fees, and any other charges.

Repayment Capacity: Ensure you can comfortably repay the loan without straining your finances.

Loan Tenure: Choose a tenure that offers manageable EMIs without extending the debt period unnecessarily.

Compare Offers: Don’t settle for the first offer; compare multiple lenders to get the best terms.

Conclusion

A 5 lakh personal loan can be a valuable financial resource to meet various personal needs. By understanding the eligibility criteria, application process, interest rates, and repayment terms, you can make informed decisions and choose the best loan offer. Remember to maintain a good credit score, reduce existing debts, and carefully plan your finances to ensure a smooth loan approval and repayment process.

Securing a personal loan is a significant financial decision. By following the guidelines and tips provided in this guide, you can confidently navigate the process and make the most of the financial opportunities available to you.

#500000 personal loan#personal loan of 5 lakhs#5 lakhs personal loan#How to get 5 lakh personal loan#5 Lakh Personal Loan

0 notes

Text

Explore 5 Lakh Personal Loan Options: Rates & Eligibility Revealed!

Need a Rs. 5 Lakh Personal Loan? Explore 16%* interest rates, check eligibility, and apply instantly. Apply Now!

For More info, Visit - www.finnable.com/products/personal-loan/5-lakh-personal-loan/

0 notes

Text

Unexpected financial requirements can develop in the hectic society of today. Having access to rapid and flexible cash can be crucial for a variety of needs, including emergencies, home improvements, further education, and dream trips. This is where personal loans come into play, giving people the flexibility to achieve their goals free from the weight of large down payments. We'll go over the advantages of applying for a 500000 personal loan, with flexible EMIs in this article, giving you the ability to take advantage of chances and deal with life's unexpected challenges with confidence.

Understanding Personal Loans:

Before we start getting into the details, let's understand what personal loans are. A personal loan is essentially an unsecured loan in which the lender gives the borrower money in exchange for no security. This means that you can obtain a loan without securing assets like your house or car. Rather, a major factor in the approval procedure is your income, repayment capacity, and credit.

The Power of Flexibility:

The range of options that a personal loan affords in terms of use and repayment is one of its main benefits. A personal loan can be used for a range of purposes, allowing you the flexibility to meet different financial demands, in contrast to other forms of credit that are meant for specific uses, such as home loans or auto loans.

Furthermore, variable EMIs (Equated Monthly Installments) allow you to customize your repayment plan to fit your tastes and financial circumstances. As a result, you can select a repayment period which fits with your income source, making sure that the EMIs fit easily into your spending plan without placing too much stress on it.

Benefits of a ₹5 Lakh Personal Loan:

Now, let's explore why applying for a ₹5 lakh personal loan can be a prudent choice:

Ample Funding: ₹5 lakh is a substantial amount that can help you cover a wide range of expenses, from consolidating high-interest debt to funding major purchases or life events.

No Collateral Required: Since personal loans are unsecured, you don't need to worry about putting up any collateral. This reduces the risk on your part and expedites the loan approval process.

Quick Disbursal: In many cases, personal loan applications are processed swiftly, allowing you to access the funds you need in a relatively short time frame. This is especially beneficial in emergency situations where time is of the essence.

Flexible Repayment Options: With a ₹5 lakh personal loan, you have the flexibility to choose a repayment tenure that suits your financial capabilities. Whether you prefer a shorter tenure with higher EMIs or a longer tenure with lower EMIs, the choice is yours.

Fixed Interest Rates: Many lenders offer personal loans with fixed interest rates,

providing you with stability and predictability in your repayment journey. This means your EMIs remain constant throughout the tenure, allowing for better financial planning.

How to Apply:

Applying for a ₹5 lakh personal loan with flexible EMIs is a straightforward process. Here's a step-by-step guide to get started:

Research Lenders: Begin by researching various lenders, comparing interest rates, processing fees, repayment terms, and customer reviews. Look for reputable lenders with a track record of reliability and customer satisfaction.

Check Eligibility: Before applying, determine if you meet the lender's eligibility criteria, which typically include factors such as age, income, employment status, credit score, and existing financial obligations.

Gather Documentation: Prepare the necessary documents required for the loan application, such as proof of identity, address, income, employment, and bank statements. Having these documents ready will streamline the application process.

Submit Application: Once you've chosen a lender, fill out the online application form with accurate details and upload the required documents. Double-check the information provided to ensure accuracy and completeness.

Wait for Approval: After submitting your application, the lender will review your information and assess your creditworthiness. If approved, you'll receive a loan offer outlining the terms and conditions, including the loan amount, interest rate, tenure, and EMIs.

Accept Offer: Review the loan offer carefully and accept it if the terms are favorable. Be sure to understand the repayment schedule, including the EMI amount and due dates.

Disbursal of Funds: Upon acceptance of the loan offer, the lender will disburse the loan amount to your designated bank account. You can then use the funds as needed to fulfill your financial goals.

Conclusion:

In conclusion, personal loan of 5 lakhs with adjustable EMIs can be a useful financial instrument that gives you the freedom to follow your goals and confidently handle unexpected costs. Understanding the advantages of personal loans, doing your homework on lenders, and applying carefully will help you gain the financial flexibility you need to go smoothly through life's journey. Why then wait? Apply for a personal loan that best fits your needs after considering your options and taking the first step toward financial freedom.

#5 Lakh Personal Loan#How to get 5 lakh personal loan#5 lakhs personal loan#personal loan of 5 lakhs#500000 personal loan

0 notes

Text

Apply for a ₹5 Lakh Personal Loan with Flexible EMIs

Whether it's for medical expenses, home renovations, education costs, or any other urgent requirement, having access to quick and convenient personal loans can provide much-needed relief. If you're in need of a 5 lakh personal loan, you'll be pleased to know that many financial institutions and online lenders offer flexible EMI options to suit your repayment capabilities.

Understanding Personal Loans:

Personal loans serve as a lifeline for individuals facing financial crunches or seeking funds for various purposes. Unlike specific-purpose loans like home loans or car loans, personal loans offer flexibility in utilization, allowing borrowers to address a wide range of financial needs.

The Importance of Flexibility in EMIs:

Flexible Equated Monthly Installments (EMIs) are a key feature of personal loans that offer borrowers greater control over their repayment schedules. Here's why opting for flexible EMIs can be advantageous:

Tailored Repayment Plans: Flexible EMIs enable borrowers to customize their repayment plans according to their financial situation. Whether you prefer smaller monthly payments spread over a longer tenure or larger payments to reduce interest costs, you can choose a plan that aligns with your budget and preferences.

Financial Planning: By knowing the exact amount you need to repay each month, you can better plan your finances and ensure timely repayment without straining your budget. This predictability fosters financial discipline and reduces the risk of defaulting on loan payments.

Prepayment Options: Many lenders allow borrowers to make prepayments towards their loan without incurring penalties. This flexibility empowers borrowers to pay off their debt sooner, thereby saving on interest costs and reducing the overall burden of the loan.

No Hidden Charges: Transparent fee structures ensure that borrowers are aware of all applicable charges upfront, including processing fees, prepayment penalties (if any), and other charges. This transparency builds trust between the borrower and the lender, fostering a positive borrowing experience.

Eligibility Criteria:

While the eligibility criteria for personal loans may vary depending on the lender, common factors considered include:

Age: Most lenders require borrowers to be within a certain age bracket (usually 21 to 65 years).

Income: Lenders assess the borrower's income to ensure repayment capability.

Credit Score: A good credit score increases the chances of loan approval and may also result in lower interest rates.

Employment Stability: Lenders prefer borrowers with stable employment history as it indicates a steady source of income.

Conclusion:

In times of financial need, a ₹5 lakh personal loan with flexible EMIs can provide the necessary funds to address urgent expenses or pursue important goals. By understanding the benefits of flexible repayment options and ensuring eligibility criteria are met, borrowers can navigate the borrowing process with confidence and ease. So, if you find yourself in need of financial assistance, consider exploring the option of a personal loan with flexible EMIs to meet your requirements effectively.

#personal loans#500000 personal loan#personal loan of 5 lakhs#5 lakhs personal loan#How to get 5 lakh personal loan#5 Lakh Personal Loan

0 notes

Text

How to get 5 Lakh Personal Loan Quickly If you want a quick loan on urgent basis you can directly apply "Click here". Without wasting any time click on the link mention. Read Atrticle: 5 lakh personal loan

0 notes

Text

Lakhpati Didi Yojana: महिलाओं के लिए महत्वपूर्ण योजना, ये बनाएगी आपको आत्मनिर्भर, हर महीने कमा सकती हो एक लाख रूपये

चंडीगढ़: Lakhpati Didi Yojana: केंद्र सरकार देश की महिलाओं को आत्मनिर्भर व स्वावलंबी बनाने को लेकर सेल्फ हेल्पिंग ग्रुप सहित कई योजनाएं चला रही हैं। विभिन्न योजनओं में से एक खास योजना सरकार द्वारा चलाई जा रही है जिसका नाम लखपति दीदी योजना है। सेल्फ हेल्पिंग ग्रुप के साथ जुड़ी औ���तों से इस योजना के अनुसार अपना काम कर न केवल स्यवं आत्मनिर्भर बन रही हैं बल्कि अपनी साथी महिलाओं को भी रोजगार मुहैया…

View On WordPress

#5 lakh insurance govt scheme#assam govt scheme#assam govt scheme online apply#business loan govt scheme#Govt scheme for girl#govt scheme for girl child#govt scheme for pregnant ladies#Govt scheme for women#home loan govt scheme#Lakhpati Didi Yojana#Lakhpati Didi Yojna:#rajasthan govt scheme#sarkari yojna

0 notes

Text

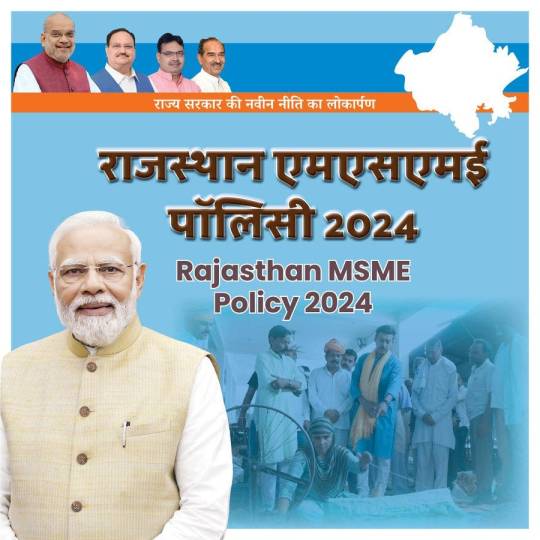

Rajasthan MSME Policy 2024: A New Era for Entrepreneurs by Col Rajyavardhan Rathore

In a landmark move to empower small businesses and foster economic growth, the Rajasthan MSME Policy 2024 has been introduced under the guidance of Colonel Rajyavardhan Rathore. This policy aims to position Rajasthan as a leader in the Micro, Small, and Medium Enterprises (MSME) sector by providing robust support, financial incentives, and a conducive ecosystem for entrepreneurs.

The Importance of MSMEs in Rajasthan

MSMEs are the backbone of Rajasthan’s economy, contributing significantly to employment and GDP. With their presence in sectors like handicrafts, textiles, agriculture, and technology, MSMEs have immense potential to drive growth and innovation. The Rajasthan MSME Policy 2024 seeks to address challenges faced by small businesses and unlock their full potential.

Vision of Col Rajyavardhan Rathore

Col Rajyavardhan Rathore envisions MSMEs as engines of Rajasthan’s economic progress. Speaking at the launch, he remarked: “MSMEs are not just businesses; they are dreams of hardworking individuals. This policy is a promise to support their aspirations and make Rajasthan a hub for entrepreneurial excellence.”

Key Objectives of the Rajasthan MSME Policy 2024

Economic Empowerment: Strengthen the MSME sector to boost Rajasthan’s GDP.

Employment Generation: Create sustainable jobs across urban and rural areas.

Ease of Doing Business: Simplify processes and remove bureaucratic hurdles.

Skill Development: Equip entrepreneurs and workers with the latest skills.

Sustainability: Promote green practices and energy-efficient solutions.

Highlights of the Rajasthan MSME Policy 2024

1. Financial Support

Subsidies and Incentives: Up to 50% subsidy on capital investment for new enterprises.

Low-Interest Loans: Special credit schemes through state-backed financial institutions.

Tax Exemptions: Relaxation in GST and other state taxes for a specified period.

2. Infrastructure Development

Industrial Clusters: Development of MSME-dedicated zones in key cities like Jaipur, Udaipur, and Jodhpur.

Common Facility Centers (CFCs): Shared spaces with advanced tools and technology.

Digital Infrastructure: High-speed internet and IT support for MSMEs.

3. Skill Training and Capacity Building

Partnerships with educational institutions to introduce MSME-focused courses.

Regular workshops on digital marketing, export readiness, and quality control.

Mentorship Programs with industry experts to guide budding entrepreneurs.

4. Streamlining Processes

Single-Window Clearance: Speedy approvals for setting up businesses.

Simplified Regulations: Reduction in compliance requirements for small enterprises.

Digital Portals: Online systems for registrations, tax filing, and grievance redressal.

5. Promoting Innovation

Research and Development Grants: Funding for MSMEs working on innovative products and solutions.

Technology Adoption: Subsidies for adopting automation and digital tools.

Startup Incubation Centers: Support for MSMEs transitioning into startups.

6. Export Promotion

Global Market Access: Partnerships with trade bodies for export opportunities.

Trade Fairs and Expos: Participation in national and international exhibitions.

Export Subsidies: Financial support for logistics and international marketing.

Sectors Targeted by the Policy

1. Handicrafts and Textiles

Strengthening Rajasthan’s traditional crafts through modern techniques and marketing support.

2. Agri-Based Industries

Encouraging food processing, organic farming, and value-added products.

3. Renewable Energy

Promoting MSMEs in solar panel manufacturing and other green technologies.

4. Technology and IT

Support for tech startups and MSMEs working in AI, software, and digital solutions.

Impact of the Rajasthan MSME Policy 2024

Economic Growth

An expected 30% rise in MSME contributions to the state GDP by 2026.

Increased revenue through exports and enhanced domestic production.

Job Creation

2 lakh new jobs to be created in urban and rural areas.

Empowerment of women and marginalized communities through focused programs.

Ease of Doing Business

Simplified processes to attract 5,000+ new MSME registrations annually.

Global Recognition

Enhanced visibility for Rajasthan’s MSMEs in international markets.

Col Rathore’s Commitment to MSMEs

Col Rajyavardhan Rathore has always championed policies that drive progress and innovation. His leadership in shaping the MSME Policy 2024 reflects his belief in the entrepreneurial spirit of Rajasthan.

In his words: “With this policy, we are not just supporting businesses; we are building dreams, livelihoods, and a prosperous Rajasthan.”

A Bright Future for MSMEs in Rajasthan

The Rajasthan MSME Policy 2024 is a game-changer for small businesses. By addressing key challenges and providing holistic support, it aims to transform the state into a hub of entrepreneurship and innovation. With Col Rajyavardhan Rathore’s vision and leadership, this policy is set to empower thousands of entrepreneurs and contribute significantly to Rajasthan’s economic growth.

3 notes

·

View notes

Text

Best PMEGP loan : Government Support for Starting Your Own Business.

At sharda Associates The Prime Minister's Employment Generation Programme (PMEGP) is a government scheme in India that gives financial help to individuals who want to create small companies. It aims to create jobs and encourage self-employment, particularly in rural and semi-urban areas. Here's a simplified view of the scheme

What is PMEGP?

PMEGP Loan provides financial assistance to people starting new small enterprises by offering a loan with a subsidy. The Ministry of Micro, Small, and Medium Enterprises (MSME) manages it, while the Khadi and Village Industries Commission (KVIC) oversees its implementation.

Key Features:

1 Loan Amount

Manufacturing enterprises might receive up to ₹25 lakh.

Service enterprises, such as beauty salons or repair shops, can receive up to ₹10 lakh.

2 Government subsidy:

Rural areas:

25% of general category applications.

35% for special categories (such as SC/ST, women, and those from the Northeast).

Urban areas

15% for general category applications.

Special categories are eligible for 25% off.

Who can apply?

1 Eligibility:

Any Indian citizen above the age of 18.

Applicants for projects costing more than ₹10 lakh (manufacturing) or ₹5 lakh (services) must have finished 8th grade.

Self-help groups (SHGs), cooperative organizations, and charitable trusts can all apply.

2 Personal Investments:

General candidates must invest 10% of the project cost themselves.

Special category applicants must invest only 5%.

How do I apply?

1 Application Process:\

Apply online using the PMEGP portal at Official kvic Main.

Upload documents such as ID, address verification, educational certificates, and a business plan.

2 Selection and Loan approval:

A District-Level Task Force Committee will contact you to schedule an interview.

Once approved, the bank sanctions the loan and credits the government subsidy to your loan account.

3 Repayment:

The loan must be repaid within 3-7 years, however the subsidy does not have to be paid back.

4 Training:

All PMEGP grantees are required to complete a brief company management training program.

Example of How PMEGP Loans Work

Suppose you wish to start a small manufacturing plant in a rural region for ₹20 lakh.

For those in the general category, the government will provide a 25% subsidy, amounting to ₹5 lakh.

The bank offers a loan of ₹15 lakh, and you simply need to invest ₹2 lakh from your savings.

Why is PMEGP beneficial?

project report for PMEGP loan assists people in starting enterprises without the requirement for a large initial investment. This loan is ideal for young enterprises as it requires no collateral (up to ₹10 lakh) and offers long payback terms.

Summary

The PMEGP initiative is a useful approach to start a small business with government assistance, particularly if you come from a rural or underprivileged background. It encourages employment generation and economic development. For additional information, please visit the official PMEGP website or contact your nearest KVIC office.

PMEGP: Helping You Start Your Own Business with Government Support. For details and to reach us, visit https://shardaassociates.in/ contact us : 91 79870 21896 , address : HIG B-59, Sector A, Vidya Nagar, Bhopal, Madhya Pradesh 462026

2 notes

·

View notes

Text

Top MBA Colleges in India with Low Fees: High RoI Management Institutes

When aspiring to pursue an MBA, students often face a critical concern: finding an institute that offers world-class education while maintaining affordability. The Top MBA Colleges in India offer an excellent balance between quality education and low fees, ensuring a high Return on Investment (RoI). This blog will explore some of the best MBA colleges in India that provide top-tier management education without burdening students with exorbitant fees.

Why Choose an MBA College with Low Fees?

Pursuing an MBA is a substantial investment, not just in terms of money but also time and effort. Choosing an MBA college with low fees can offer the following benefits:

Higher ROI: With affordable tuition, students can recoup their investments faster after getting employed.

Financial Flexibility: Reduced fees ease the pressure of student loans, allowing graduates to start their professional careers with minimal debt.

Accessibility: More students from diverse economic backgrounds can access quality education.

Key Considerations When Choosing the Best MBA Colleges in India

Affiliation & Accreditation: Ensure that the MBA college is affiliated with a reputed university and has accreditation from bodies like AICTE, NAAC, or NBA.

Placement Records: Low fees are excellent, but what truly makes an MBA worthwhile is the placement opportunities provided by the college. Look for institutes with strong placement records.

Infrastructure & Faculty: A good learning environment, coupled with experienced faculty, enhances the overall education experience.

Specialization Offered: Different colleges excel in various specializations such as Finance, Marketing, HR, Operations, etc. Ensure that the college offers the specialization you are interested in.

List of Top MBA Colleges in India with Low Fees

1. Faculty of Management Studies (FMS), Delhi

Fees: Around ₹2 Lakhs

Highlights: FMS Delhi is consistently ranked among the top MBA colleges in India. Despite its low fees, it boasts excellent placements, making it a high RoI institute. With an average salary package of around ₹25-30 lakhs per annum, FMS offers incredible value to its students.

2. Tata Institute of Social Sciences (TISS), Mumbai

Fees: Around ₹2.5 Lakhs

Highlights: Known for its MBA in Human Resource Management and Labour Relations, TISS offers a specialized program that rivals some of the top institutes globally. The placement statistics are impressive, with students often securing roles in renowned organizations with lucrative packages.

3. Jamnalal Bajaj Institute of Management Studies (JBIMS), Mumbai

Fees: Around ₹6 Lakhs

Highlights: Often referred to as the “CEO factory” of India, JBIMS offers one of the best RoI for MBA aspirants. With a strong alumni network and stellar placement records, it stands as a premier institute in India’s financial capital.

4. Department of Financial Studies (DFS), University of Delhi

Fees: Around ₹2 Lakhs

Highlights: Specializing in finance, DFS provides an affordable MBA program with excellent faculty and industry connections. Graduates from DFS often land high-paying roles in finance and consulting sectors, making it a top choice for MBA students.

5. National Institute of Industrial Engineering (NITIE), Mumbai

Fees: Around ₹6 Lakhs

Highlights: Primarily focusing on industrial management, NITIE is known for its rigorous curriculum and impressive placement stats. The average salary package offered to its students is over ₹20 lakhs per annum, making it an attractive choice for those seeking a high RoI MBA program.

6. University Business School (UBS), Panjab University, Chandigarh

Fees: Around ₹1.5 Lakhs

Highlights: UBS is one of the most affordable B-schools in India with excellent academic and placement records. The low fee structure coupled with a solid placement scenario makes it a favorite among MBA aspirants from all over the country.

7. Symbiosis Institute of Business Management (SIBM), Pune

Fees: Around ₹8 Lakhs

Highlights: Though slightly on the higher side compared to others in this list, SIBM Pune is still affordable when compared to many private B-schools. The quality of education and placements it offers justifies the fee structure.

8. Department of Management Studies (DMS), IIT Delhi

Fees: Around ₹8 Lakhs

Highlights: DMS IIT Delhi is one of the most sought-after institutes for management education in India. With top-notch placements, it provides an excellent return on investment. Many students land high-paying jobs in top companies, ensuring that the cost of the MBA is easily recoverable.

Conclusion

Pursuing an MBA from one of the top MBA colleges in India with low fees is not just about saving money; it's about making a smart investment in your future. These best MBA colleges in India offer a blend of affordability and high-quality education, ensuring that students can build a prosperous career without being financially burdened. With careful consideration of factors like placement records, faculty, and infrastructure, these institutions provide a pathway to success in the competitive world of business management.

#Top MBA Colleges in India#Best MBA Colleges in India#Best MBA Colleges#Top MBA Colleges#education#higher education#universities#education news#colleges#mba#top mba colleges in pune#top mba colleges in bangalore#top mba colleges in delhi#top mba colleges in kolkata

3 notes

·

View notes

Text

Union Budget 2024 (India) Summary

The Union Budget 2024 of India focuses on simplifying tax processes, promoting economic growth, and supporting various sectors. Here are the key highlights:

Simplification of Tax Processes

Income Tax Returns (ITR): The process of filing ITR has been simplified.

Revised Tax Deductions and Rates

Standard Deduction: Increased from ₹50,000 to ₹75,000 in the new tax regime.

Family Pension Deduction: Enhanced from ₹15,000 to ₹25,000.

New Tax Structure:

No tax on income up to ₹3 lakhs.

5% tax on income from ₹3 lakhs to ₹7 lakhs.

10% tax on income from ₹7 lakhs to ₹10 lakhs.

15% tax on income from ₹10 lakhs to ₹12 lakhs.

20% tax on income from ₹12 lakhs to ₹15 lakhs.

30% tax on income above ₹15 lakhs.

Changes in Import Taxes

Gold and Silver: Import tax reduced from 6.5% to 6%.

Support for Start-ups and Entrepreneurs

Angel Tax Exemption: Investors in start-ups are exempt from the angel tax.

Late Payment of TDS: No longer considered a crime.

Changes in Capital Gains Tax

Long-Term Capital Gains Tax: Set at 12.5%.

Short-Term Capital Gains Tax: Increased to 20%.

Industrial and Economic Growth Initiatives

Capital Gains: Increase in capital gain limit.

Industrial Parks: Plug and Play Industrial Park Scheme in 100 cities.

Export Concessions: For mineral products.

Support for Women: ₹3 lakh crores provision.

Cheaper Goods: Electric vehicles, gold and silver jewelry, mobile phones, and related parts.

Agriculture: Priority on increasing production.

FDI Simplification: Simplified process for foreign direct investment.

Interest-Free Loans: To states for 15 years.

Rural Development: ₹2.66 lakh crores provision.

Support for Farmers: ₹1.52 lakh crores provision.

Education Loans: Financial support for loans up to ₹10 lakhs for higher education.

Nine Priorities for Upcoming Years

Manufacturing and Services

Urban Development

Energy Security

Infrastructure

Innovation and R&D

Next-Generation Reforms

Productivity and Resilience in Agriculture

Employment and Skilling

Inclusive Human Resource Development and Social Justice

Employment-Linked Incentives

First-Time Employees: One-month wage incentive.

Manufacturing Sector: Incentives for employers and employees for four years.

Youth Employment: Incentives for 30 lakh youths entering the job market.

EPFO Contribution Reimbursement

Government will reimburse ₹3,000 per month towards EPFO contribution for two years for each additional employee.

E-Commerce and Youth Internship Initiatives

E-Commerce Export Hub: To be created in collaboration with the private sector.

Youth Internship Scheme: Internships for 1 crore youth with a one-time assistance of ₹6,000 and a monthly allowance of ₹5,000 during the internship.

The Union Budget 2024 aims to drive economic growth, support various sectors, simplify tax procedures, and provide robust support for employment and youth development. By focusing on these areas, the budget seeks to create a more inclusive and prosperous economy for all citizens. Click here read more

2 notes

·

View notes

Text

Education Loan for Abroad Studies: Explore Student Loans

An investment in knowledge pays the best interest! And if the knowledge is attained at a top-tier and premium university then it is sure to elevate your career to the next level. However, the unfortunate reality is that the cost of studying in a reputed college is usually quite steep. And studying in a good college overseas is an even more expensive proposition.

Education loans for abroad studies help students, irrespective of their financial status, realize their dream of studying in one of the best universities in the world.

Numerous banks and other lenders now provide foreign education loans for students who want to study abroad. These lenders have different education loan schemes on offer, but choosing the one that is right for you is not an easy task. And that is where GyanDhan helps.

We match you with that lender, which is the best education loan for abroad studies that suits your profile and needs perfectly, and then help secure the loan approval in the most seamless and hassle-free manner.

What is the Maximum Loan Limit For Education Loans to Study Abroad?

In secured education loans, students can apply for student loans of up to INR 1.5 cr. In foreign education loans without collateral, students can apply for study loans of up to INR 45 Lakhs. This loan amount limit can increase or decrease depending on the applicant’s and co-applicant’s profile, country, course, etc.

How to Apply for Abroad Education Loans?

The steps to apply for a loan for financing the studies abroad are:

Step-1: Check your loan eligibility online.

Step-2: Get expert loan counseling to compare the options available.

Step-3: Select a lender and apply online.

Step-4: Get the customized education loan document checklist.

Step-5: Submit the required education loan documents either online or get documents picked up from your home by our representative.

Step-6: Get the property & other legal evaluations done (in secured loans).

Step-7: Get the loan sanction letter after the education loan approval from the lender.

How to Choose the Best Overseas Education Loan?

Taking an education loan to supplant the cost of education overseas is the right choice. Depending on the amount and your profile, financial institutions can finance even 100% of the cost of the course.

However, to get the best education loan option, one needs to carefully analyze the following key aspects of the various options available. When you apply to GyanDhan, we do this analysis for you. In case you do the loan comparison yourself, consider these factors:

Interest Rate: Even a 1% increase in the education loan interest rate has a substantial financial effect. Example - Loan Amount: Rs. 30,00,000, Loan Repayment in: 5 years after you graduate, Course Duration: 2 years; While at 10%, you’ll pay Rs. 9.7 lakhs in interest, at 11%, you’ll pay Rs. 10.9 lakhs - that’s a difference of 1.2 lakhs for just 1%!. Also, historical changes done by any lender in its interest rates should also be considered.

Repayment Holiday/Moratorium Period: It is a specified period during the loan tenure in which the borrower is exempt from making repayments. Loans with a moratorium period have a big plus, as you don’t have to worry about making repayments while you study overseas.

Tax Rebate: Education loans for foreign studies taken from Indian banks are special in that the entire amount paid as interest is exempt from income tax. This has a huge impact: Example - Loan Amount: Rs. 30,00,000, Marginal tax bracket: 30%, Repayment in: 5 years after graduation, Course Duration: 2 Years, ROI: 10%... If your loan has tax rebate, you can save Rs. 2.9 lakhs!

Margin Money: The amount that you need to pay from your own pocket while the rest is paid by the bank. If a bank offers a 0% margin, it means they’ll fund all your education expenses in the offered loan amount.

Hidden Fees: There are numerous hidden fees that your lender might be charging you and when accumulated these will cost you a considerable amount, such as:

Forex Margin: Some lenders charge a forex conversion charge when the overseas education loan is sanctioned in INR and disbursed in some other currency. This can be as high as 1.5%, which translates to Rs. 45,000 for a loan amount of Rs. 30 lakhs.

Processing Fees: This varies from zero to as high as 2%. For a loan of Rs. 30,00,000, the processing fees can be as high as Rs. 60,000

Cost of Credit Life Insurance: Some lenders make it mandatory for the applicant to go in for credit life insurance with their education loan scheme so that their loan amount is protected against any unfortunate eventualities. If the premium amount is on the higher side then it eventually increases the cost of the education loan as well.

Mandatory Cross-Sell: Some lenders try to cross-sell other policies before sanctioning the education loan, even though it is not required on the applicant’s end.

Interest Rate in Different Currencies: Often students face a dilemma of choosing over an education loan in USD with a lower interest rate or an equivalent amount in INR with a higher interest rate. By the previous trend of the rising prices of US$ to INR conversion rates, it is a smart choice to go for the loan amount in INR even though it may come with a higher interest rate.

As you can see, by selecting the right overseas education loan, the reduction in cost can be as high as 5-6%.

Which is the Cheapest Education Loan in India to Study Abroad?

Public sector banks offer the State Bank or BoB lowest interest rates on loans for foreign education compared to private banks & NBFCs. If your institution is listed in BOB’s premium list of colleges, Bank of Baroda offers the cheapest education loan for abroad studies. Otherwise, the State Bank of India offers the cheapest education loans. However, the extent of the cheap education loan in India depends on several factors including the applicant’s profile, co-applicant’s financial profile, target country, target course, etc.

Are you eligible for an abroad education loan? Check here.

3 notes

·

View notes

Text

Secure 5 Lakh Personal Loan Instantly: Check Eligibility & Interest Rates with Finnable!

Explore Rs. 5 Lakh Personal Loan options with interest rates from 16%*. Determine eligibility, calculate EMIs, and apply promptly. Apply Now!

0 notes

Text

Get 10 Lakh Personal Loan Online in Minutes at low EMIs

Understanding the Basics

Before delving into the intricacies of securing a 10 lakh personal loan, it's essential to grasp the fundamentals. A personal loan is an unsecured loan that individuals can avail from banks, non-banking financial companies (NBFCs), or online lenders without pledging any collateral. The loan amount, interest rate, and tenure are determined based on the borrower's creditworthiness, income, employment status, and other factors.

Exploring Loan Options

When it comes to obtaining a personal loan up to 10 lakh, borrowers have several options to consider. Banks, being traditional lenders, offer competitive interest rates and flexible repayment terms. On the other hand, NBFCs and online lending platforms often provide quicker approvals and streamlined processes. It's advisable to compare the offerings of different lenders to choose the option that best suits your requirements.

Assessing Eligibility Criteria

To qualify for a 10 lakh personal loan, lenders typically evaluate various eligibility criteria. These may include:

Income Stability: Lenders prefer borrowers with a stable source of income to ensure timely repayment of the loan. A steady employment history and sufficient income play a crucial role in determining eligibility.

Credit Score: A healthy credit score is essential for securing favorable loan terms. Lenders assess the borrower's creditworthiness based on their credit score, which reflects their repayment behavior and financial discipline.

Age: Most lenders have a minimum and maximum age criterion for loan applicants. While the minimum age requirement is usually 21 years, the maximum age may vary depending on the lender's policies.

Employment Status: Lenders may require borrowers to be salaried or self-employed with a minimum tenure in their current profession or business.

Understanding Loan Repayment

Once you qualify for a 10 lakh personal loan, understanding the repayment structure is crucial. The loan repayment consists of two components: the principal amount borrowed and the interest charged by the lender. The Equated Monthly Installment (EMI) is the fixed amount payable by the borrower each month until the loan is fully repaid. Factors such as the loan amount, interest rate, and tenure influence the EMI amount.

Calculating EMI for a 10 Lakh Personal Loan

Using online EMI calculators available on lender websites or financial portals, borrowers can easily compute the EMI for a 10 lakh personal loan. Let's consider an example:

Loan Amount: ₹10,00,000

Interest Rate: 12% per annum

Loan Tenure: 5 years (60 months)

By inputting these values into the EMI calculator, we find that the EMI for a 10 lakh personal loan with a 5-year tenure at a 12% interest rate is approximately ₹22,229.

Tips to Enhance Loan Approval Chances

To improve the likelihood of loan approval and secure favorable terms, borrowers can follow these tips:

Maintain a Healthy Credit Score: Regularly monitor your credit score and take measures to improve it if necessary. Timely payment of bills and debts, as well as keeping credit utilization low, can boost your credit score.

Clear Existing Debts: Lenders assess the borrower's debt-to-income ratio before approving a loan. Clearing existing debts or reducing outstanding balances demonstrates financial responsibility and improves eligibility.

Provide Accurate Documentation: Ensure that all required documents, such as identity proof, address proof, income documents, and bank statements, are accurate and up-to-date. Incomplete or incorrect documentation can lead to delays or rejection of the loan application.

Apply with a Co-Applicant: If you're unable to meet the eligibility criteria on your own, consider applying for the loan with a co-applicant, such as a spouse or family member, who meets the requirements. A joint application enhances the overall eligibility and may result in better loan terms.

Conclusion

Securing a 10 lakh personal loan can be a transformative step towards achieving your financial goals and addressing immediate needs. By understanding the loan process, assessing eligibility criteria, and adopting proactive measures, borrowers can enhance their chances of loan approval and secure favorable terms. Remember to compare loan offerings from different lenders, calculate EMI accurately, and maintain a healthy credit profile to unlock the gateway to financial flexibility. With careful planning and diligence, obtaining a 10 lakh personal loan can pave the way for a brighter financial future.

#10 lakh personal loan#10 lakh personal loan emi#10 lakh personal loan eligibility#personal loan upto 10 lakh#10 lakh personal loan interest rate#10 Lakh Personal Loan EMI for 5 Years

1 note

·

View note

Photo

Sending Money Abroad Will Burn a Bigger Hole in your Pocket Soon - @lawyer2ca ✅ Whether you're investing in a home or stock market abroad, or sending money to your family or friends, money transfers, no matter how much or how little, are about to get more expensive as the blanket application of 20% TCS for all remittances, other than travel and medical will be applicable. ✅ In the case of educational expenses, like university fees, the tax collection at source (TCS) norms remain unchanged. ✅ The rate of TCS for international remittance under LRS for education purposes continues to remain the same at 5% on transfers above Rs 7 lakh and 0.5% if the source of funds is through a loan from a financial institution. ✅ The tax collection for overseas remittances will surely cause hindrance to travelers, especially students who would be going abroad for higher education. #Lawyer2CA #incometax #UnionBudget2023 #NirmalaSitharaman #finance #Global #india #Budget2023 #TCS (at Lawyer2CA) https://www.instagram.com/p/Co6sWUPSLOy/?igshid=NGJjMDIxMWI=

2 notes

·

View notes