Statistics

We looked inside some of the posts by hackingfinance and here's what we found interesting.

Average Info

Notes Per Post

11

Likes Per Post

10

Reblog Per Post

1

Reply Per Post

0

Time Between Posts

1 month ago

Number of Posts By Type

Text

2

Quote

10

Audio

1

Video

1

Link

2

Photo

1

Last Seen Tumblr Blogs

Fun Fact

Tumblr has been providing a Korean-language service since 2013.

Text

We believe that there is a much larger market for risk and much more risk to be insured and reinsured if transferred efficiently.

http://www.artemis.bm/blog/2019/01/10/tremor-enables-transfer-of-risk-to-those-best-able-to-bear-it-efficiently-ceo-bourgeois/

5 notes

·

View notes

Quote

Tremor’s open, technology-driven, programmatic marketplace for reinsurance risk placement utilises a highly specialised skill set and purpose built, modern technology, combining deep understanding of market design, auction theory, optimization techniques and professional software development.

2019 shaping up as busy year for insurtech Tremor: CEO, Sean Bourgeois - Reinsurance News A company to watch for sure...

3 notes

·

View notes

Text

But while the distinction between cash and money may be irrelevant to a new crop of Millennial-focused restaurant owners, some lawmakers are arguing that cashless design is classist.

https://www.theatlantic.com/technology/archive/2018/12/cashless-amazon-walmart-workers/578377/

1 note

·

View note

Quote

“There's a fundamental shift occurring in property insurance,” Peeters said. “Traditionally property insurance has been an indemnification business where carriers write a check when all is lost, so to speak. But the advent of smart, connected devices allow insurers to now be in the protection and prevention business.”

Best's Review

0 notes

Audio

(via It Takes Two, Baby: Trov And Anthemis On Reinventing Insurance by InsurTech Bytes)

0 notes

Video

youtube

(via Sean Park: 'We Need to Hack Financial Regulation' | Money | WIRED - YouTube) So exciting to see that this vision for regulatory sandboxes has come to life in so many countries around the world. #winning

1 note

·

View note

Quote

If Banks can manage the transition to API driven business there’s an opportunity for them to drive a trillion dollar industry. The impact will depend on banks willingness to change.

Farhan Lalji, Anthemis Group

0 notes

Quote

Trov says that diving into the world of insured autonomy is “us taking advantage of an amazing opportunity to utilise and extend the capabilities of our platform into new territories (like autonomous ride-hailing),” says company CEO Scott Walcheck. “On-Demand Insurance for personal mobility is a natural progression for us as we build a platform that enables an increasingly smarter and more contextual cover,” he added.

Driverless doesn’t mean an end to car insurance | TU-Automotive

0 notes

Link

Just getting started. Day zero.

0 notes

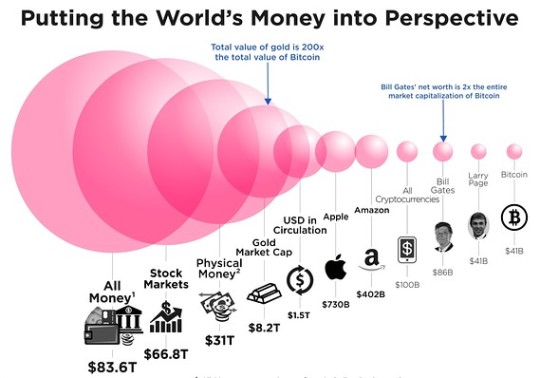

Photo

(via How big is bitcoin, really? This chart puts it all in perspective - MarketWatch)

1 note

·

View note

Quote

Likewise, corporations move too slowly – 20% of companies take more than six months to do a deal, which may as well be six decades in startup years. Companies that “fast-track” processes like short NDAs, short purchasing agreements, centralized points of contact, and simple inbound application processes are more successful.

Why So Many Corporate Innovation Programs Don't Work | Fortune.com

0 notes

Quote

But today, as disruption happens faster and is funded at enterprise scale, companies need to figure out how to create a portfolio of innovation. They can do so by first identifying technology trends with innovation outposts located in technology centers; second, by investing in early-stage disruptors; third, by buying disruptors and keeping their innovation culture and people; and fourth, by creating an innovation culture internally that disrupts their own business model before others do.

Why You Can’t Just Tell a Company “Be More Like a Startup”

0 notes

Quote

“These plans have drifted for decades,” he said. “There are poor investment choices, high fees and annuities that are abusive. Schools have forgotten that they are fiduciaries, and we’re seeing retirements being torpedoed by negligence, essentially.”

The Monk Who Left the Monastery to Fix Broken Retirement Plans - The New York Times

0 notes

Quote

Stein: On average, if you take all of the money that we spend on marketing and all of the customers that we acquire, it probably costs us about one-tenth of what it costs the traditional firm to acquire a customer. And that’s just because we have a better product, so we don’t have to spend so much to get people to use it. That, of course, drives the costs down for us, and we pass that value back to customers. It’s a virtuous cycle for us. Our costs to execute are also lower, so not only are our marketing costs lower — all of our operating costs are lower. These cost advantages are really core to our competitive advantage over time. Continuing to invest in driving those costs down and continuing to drive value back to customers is the core of our value proposition.

Should a Robot Run Your Retirement Portfolio? - Knowledge@Wharton

0 notes

Quote

This point is particularly interesting for the ESM because a more integrated market would by its nature also be more stable. And as our name indicates, ensuring the financial stability of the euro area is our core mission. One could even think of using new technologies, such as blockchain, to set up the new issuance platform.

Can Public-sector Organizations Become Fintech Disruptors? - Knowledge@Wharton

0 notes

Quote

I think the reason that we are stumbling is that the opportunity here is just immense. And contracts are everywhere in the world today, everywhere in our life — and especially in the digital world, where almost every interaction is a contract. We clearly are going to see smart contracts get used more and more widely. And so it is really less of a question of deciding what segment of human activity smart contracts will be used for, but more thinking about how they can be implemented in a way that’s sensible, that addresses these kinds of issues, and that understands the legal system still plays a vital and valuable role.

Smart Contracts Explained: Why They Can't Fully Replace Lawyers

0 notes