#kivexa

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Post activity is at the highest at 4:00 pm EDT; notes peak at 10:00 pm EDT.

Text

Abacavir/lamivudina Uma Nova Combinação Para TARV em 2024

Mais novidade. E tem por ai. Fiquem ligados

Abacavir/lamivudina uma ficha informativa Tratamento do HIV Greta Hughson O que é abacavir/lamivudina? O abacavir/lamivudina é por vezes comercializado sob o nome Kivexa, Contudo, nas versões genéricas podemos falar sobre as novas esperanças que a combinação de abacavir e lamivudina trará. O abacavir/lamivudina, também conhecido como Kivexa, oferece uma promissora alternativa para o tratamento…

View On WordPress

0 notes

Text

IM SRYYY i dont have a spotify i use soundcloud & adblocker like a gremlin but here is my most recent plays

miss me - fka twigs unreleased

Reasons - earth wind fire

baby be mine - micheal jackson

you’re not the only one i know - The sundays

pretty - coco & clair clair

goodnight & go x duvet remix - kivexa

capable of love - pinkpantheress

Never too much - luther vanross

got to be real - cheryll lyn

clear the area -imogen heap

thanks to elaine (@loverlestat) for tagging me!! 💕

music shuffle game rules: shuffle your ‘on repeat’ playlist and post the first 10 songs, then tag 10 friends to do the same

1. one of your girls — troye sivan

2. rush — troye sivan

3. northern attitude — noah kahan, hozier

4. bye bye bye — *nsync

5. smoking section — st vincent

6. francesca — hozier

7. talk talk — charli xcx, troye sivan

8. denial is a river — doechii

9. dial drunk — noah kahan, post malone

10. nobody’s soldier — hozier

no pressure tags: @harlequinlestat @zaegreus @catastrophically--aware @roseeblue @itwasanangryinch @eugene-is-tired @thehollywoodnecromancer @sheherlestat @thegr8faery @monsterfucker-molloy

351 notes

·

View notes

Photo

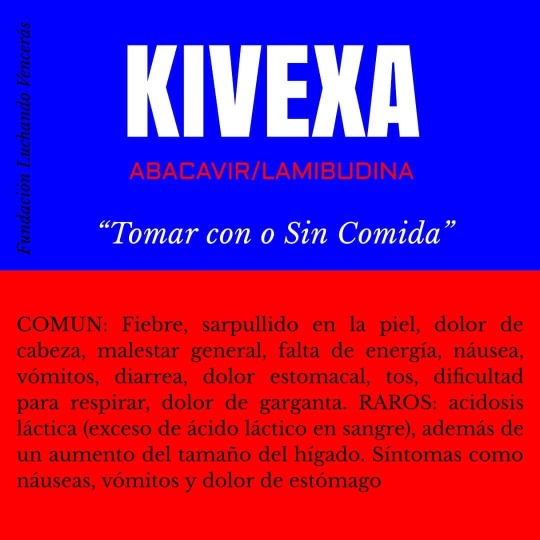

KIVEXA ABACAVIR/LAMIVUDINA EPZICOM ABC/3TC, Sulfato de abacavir/lamivudina #kivexa #abacavir #lamivudina #sulfato #epzicom #arv #medic #medicine #medicinas #medicamento #retrovirrales #antiretrovirrales #salud #concienciaplena #conciencia #diverdidad https://www.instagram.com/p/CAvWqb2nnyM/?igshid=12wfkzopycewr

#kivexa#abacavir#lamivudina#sulfato#epzicom#arv#medic#medicine#medicinas#medicamento#retrovirrales#antiretrovirrales#salud#concienciaplena#conciencia#diverdidad

0 notes

Link

ReportsWeb.com published “Kivexa Drug Market” from its database. The report covers the market landscape and its growth prospects over the coming years. The report also includes a discussion of the key vendors operating in this market. p

0 notes

Text

Baisses de prix en vue pour plusieurs médicaments anciens de Sanofi

Le Journal officiel de vendredi a publié une vague de baisses de prix au 1er novembre, notamment pour des médicaments anciens de Sanofi, Grünenthal et Novartis.

Chez Sanofi, les prix publics TTC (hors honoraires de dispensation) de l'anti-agrégant plaquettaire Plavix* (clopidogrel) 75 mg vont diminuer de 17% à 11,16 euros pour 30 comprimés, contre -13% à -14% pour l'hypnotique Stilnox* (zolpidem) 10 mg, qui sera affiché à 1,22 euro pour 7 comprimés et 1,78 euro pour 14 comprimés. Un autre hypnotique, Imovane* (zopiclone) 7,5 mg, va reculer d'environ 4% à 1,06 euro pour 5 comprimés et 2,08 euros pour 14 comprimés.

Les traitements de l’insuffisance rénale à base de furosémide Lasilix* 40 mg et Lasilix* Faible 20 mg enregistreront une baisse de 5% à respectivement 2 euros et 1,35 euro pour 30 comprimés. Lasilix* Spécial 500 mg baissera quant à lui de 9,5% à 16,47 euros.

Dans l'hyperphosphorémie, Renvela* (sévélamer) en poudre pour suspension buvable cédera 20% à 175,53 euros (boîte de 90 sachets). Les prix de la présentation en comprimés à 800 mg s'alignera sur le tarif forfaitaire de responsabilité (TFR) créé à compter du 1er novembre pour son groupe générique. Cela induit une baisse de plus de 46% pour le princeps, à 68,98 euros pour une boîte de 180 comprimés.

Le corticoïde Solupred* (prednisolone) 20 mg connaîtra une baisse de 5% à 3,43 euros pour 20 comprimés effervescents et 3,58 euros pour 20 comprimés orodispersibles. Le prix des 30 comprimés effervescents à 5 mg perdra 15% à 1,91 euro.

Plusieurs antibiotiques sont concernés par la vague de baisses de prix. Sont visés Orelox* (cefpodoxime) 100 mg (-17% à 5,92 euros pour 10 comprimés), Orelox* Enfant et Nourrisson 40 mg/5 ml (-16% à 3,71 euros pour un flacon de 8,35 g et -17% à 6,33 euros pour un flacon de 16,7 g), Oroken* (céfixime) 200 mg (-6% à 7,20 euros pour huit comprimés), Tavanic* (lévofloxacine) 500 mg (-17% à 9,99 euros pour cinq comprimés), Birodogyl* (spiramycine + métronidazole) 1,5 MUI/250 mg (-6% à 5,68 euros pour 10 comprimés), Oflocet* (ofloxacine) 1,5 mg/0,5 ml (-5% à 3,94 euros pour 20 récipients unidoses) et Rulid* (roxithromycine) 150 mg (-17% à 6,01 euros pour 10 comprimés et 9,63 euros pour 16 comprimés).

La gamme de l'antidiabétique Amarel* (glimépiride, Sanofi) enregistrera des baisses de prix comprises entre 5% et 17% selon les présentations (dosages à 1 mg, 2 mg, 3 mg et 4 mg, en boîtes de 30 ou 90 comprimés). Les prix seront compris entre 2,66 et 15,54 euros.

Le traitement de la polyarthrite rhumatoïde (PR) Arava* (léflunomide) diminuera de 16% à 30,02 euros, l'anti-angoreux Ikorel* (nicorandil) 20 mg de 5% à 6,65 euros, et le traitement de l'hypertrophie bénigne de la prostate (HPB) Xatral* LP (afluzosine) 10 mg de 6% à 11,93 euros, à chaque fois pour 30 comprimés.

Une baisse de 12,5% est prévue pour l'anti-inflammatoire Profenid* (kétoprofène) 50 mg, à 1,47 euro pour 20 gélules. L'antalgique Topalgic* LP (tramadol) cédera pour sa part 6% à 6,45 euros (dosage à 100 mg), 9,14 euros (150 mg) et 11,82 euros (200 mg).

Chez Grünenthal, l'antalgique oral Contramal* LP (tramadol) reculera de 6% environ à 6,45 euros pour le dosage à 100 mg, 9,14 euros pour le 150 mg et 11,82 euros pour le 200 mg. La baisse sera de 22% pour Ixprim*/Zaldiar* (tramadol 37,5 mg + paracétamol 325 mg), à 2,40 euros les 20 comprimés effervescents.

Zophren*, Foradil*, Imurel*, Kivexa*, Diamicron*...

Au sein du portefeuille de Sandoz, filiale de Novartis, la présentation en solution injectable de l'anti-émétique Zophren* (ondansétron) 2 mg/ml reculera d'un peu plus de 13% à 4,79 euros (ampoule de 2 ml) et 9,30 euros (4 ml). Les lyophilisats oraux dosés à 4 mg baisseront de 6% à 4,41 euros (boîte de deux) et 8,76 euros (boîte de quatre).

Les prix de l'anti-asthmatique Foradil* (formotérol) s'aligneront sur les TFR créés pour les groupes génériques du produit à partir du 1er novembre. Cela représente une baisse d'environ 20,5% pour le princeps, à 5,77 euros pour 30 gélules de poudre pour inhalation et 11,60 euros pour 60 gélules.

Chez HAC Pharma, une baisse de 5% est prévue pour le médicament indiqué dans la transplantation et en immunologie Imurel* (azathioprine), qui sera affiché à 21,97 euros pour 100 comprimés à 50 mg, et pour l'antigoutteux Zyloric* (allopurinol), dont les prix seront de 1,25 euro (dosage à 100 mg), 1,80 euro (200 mg) et 2,22 euros (300 mg).

Pour UCB, le prix du supplément potassique Diffu-K* (chlorure de potassium) reculera de 2% à 1,87 euro pour 40 gélules. L'antibiotique Oracilline* (phénoxyméthylpénicilline) en comprimés sécables cédera 3% à 3,88 euros. La baisse sera identique pour la présentation en solution buvable, dont les prix seront de 5,39 euros (250.000 UI/5 ml), 6,91 euros (500.000 UI/5 ml) et 11,09 euros (1.000.000 UI/10 ml).

L'anti-VIH Kivexa* (abacavir + lamivudine), commercialisé par ViiV Healthcare, va chuter de près de 30% à 200,69 euros pour une boîte de 30 comprimés.

Du côté de Servier, l'antidiabétique Diamicron* (gliclazide) 60 mg enregistrera une baisse d'environ 10% au 2 novembre, pour atteindre des prix de 3,85 euros pour 30 comprimés à libération modifiée et 11,38 euros pour 90 comprimés.

0 notes

Text

Hikma Pharmaceuticals plc’s pain could be GlaxoSmithKline plc’s gain

Hikma Pharmaceuticals (LSE: HIK) today downgraded its 2017 forecast for the third time this year and now expects revenues of around $2bn, down from previous guidance of $2.1bn-$2.2bn. The announcement of a licensing agreement with Takeda couldn’t prevent the shares from plummeting 9% in early trading, knocking the share price down to nearly half what it was just 12 months ago.

The company was hit by the devaluation of the Egyptian pound and an increasingly tough environment in the US where “competition is increasing and pricing pressure is intensifying,” according to CEO Said Darwazah.

First-half revenue rose 1%, while operating profit fell 7% after a strong performance in Generics was offset by a weaker showing from Branded Generics. Strong operating cash flow helped the company reduce net debt from $697m to $633m, a perfectly healthy level considering the defensive nature of pharma companies.

Investors will surely be disappointed, but some cautiously optimistic comments regarding Hikma’s Advair generic will go some way to soothing long-term fears. Sales of Advair, GlaxoSmithKline’s (LSE: GSK) premier blockbuster drug, have held up better than expected since its patent expired back in 2016, because the Diskus delivery system it employs has been a tough one to crack for both Hikma and rivals Mylan and Novartis alike.

Hikma said it has managed to “clarify and resolve” a number of the FDA’s questions regarding the key drug and reiterated there were “no material issues” concerning eventual approval. A more detailed update has been promised, but given the deterioration in the company’s outlook, investors might not relax until more context has been given.

These delays are certainly to the benefit of Glaxo. Its massive 5.3% yield is barely covered by cash-flow and the extended no-competition period for Advair grants some much-needed breathing space so it can squeeze more out of its other businesses.

Right direction

I firmly believe that GSK is moving in the right direction and that a combination of margin expansion and slow-but-steady sales growth will eventually better cover the dividend. If this happens, it would not be surprising to see the shares re-rate to a more normal yield of around 4.5%, indicating a near 20% upside if the market gets comfortable with the payout.

The company’s free cash flow jumped from £0.1bn in the first half of this year to £0.4bn, but if it is to achieve its target “to build free cash flow cover of the annual dividend to a target range of 1.25-1.50x,” it must continue its run of form.

The rate of inevitable decline in Advair sales will be key for GSK over the next few years, as will performance in its HIV division which has really picked up the slack for the company of late. The firm did warn of “the impact of generic competition to Epzicom/Kivexa,” so investors would do well to keep a close eye of the performance from the HIV treatments in future updates.

I find both companies attractive propositions at current prices. Hikma has had a terrible year, but its strong presence in North Africa and the Middle East should continue to drive growth as healthcare spend increases. Similarly, Glaxo might run into some short-term issues covering the dividend, but its pipeline looks bright and I’m cheered by new CEO Emma Wamlsley’s strategic plan, specifically regarding a refocusing of capital allocation in the pharma business.

That said, I'd understand if readers were put off by the competitive pressures at both businesses. Those searching for safety may be better served seeking out similarly defensive companies that aren't experiencing immiediate pressures. Our analysts have found five companies with resilient payouts and tremendous track records that could help you glide to retirement. To read the investment theses behind these quality companies, click here.

More reading

These 2 battered stocks look set for a return to growth

Why I think Woodford was right to dump GlaxoSmithKline plc

Zach Coffell owns shares in GlaxoSmithKline. The Motley Fool UK owns shares of and has recommended GlaxoSmithKline. The Motley Fool UK has recommended Hikma Pharmaceuticals. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.

0 notes

Link

0 notes

Link

0 notes

Link

0 notes

Note

Hello Dr Joel, I have been on Truvada/Isentress for a year now. I am UD and CD4 around 500. I've had a slowly declining GFR (67 ml/min, with a creat of 1,15 mg/dl). My Dr proposed getting rid of tenofovir, switching to Abacavir(Raltegravir, since where I live TAF is not available and dolutegravir is reserved only for people with resistances. Any thought on this?Thanks a lot. Happy New Year to all of us, by the way.

If your HLA B*5701 test is negative and you don’t have a lot of cardiac risk factors, then a switch to abacavir/lamivudine (Epzicom or Kivexa) would be reasonable, especially if TAF isn’t available.

0 notes