#doinsurance

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

In 2020, 27% of US Tumblr users had an annual household income of over $100,000.

Text

Professional Indemnity What is it and Why Do You Need It?

Professional indemnity, also known as errors and omissions insurance, is a type of insurance coverage that protects professionals against claims made by clients for losses or damages caused by professional negligence, errors, or omissions in the performance of their duties. This type of insurance is especially important for professionals such as consultants, architects, engineers, accountants, and other service providers who offer their expertise and advice to clients.

Why Do You Need Professional Indemnity Insurance?

In today's litigious society, even the most skilled and competent professionals can make mistakes or be accused of negligence. These mistakes can have significant financial consequences, especially if a client loses money as a result. Professional indemnity insurance provides a financial safety net to protect professionals against these types of claims and the associated legal fees. In addition to protecting against claims of negligence, professional indemnity insurance can also provide coverage for other types of losses, such as breach of confidence, infringement of intellectual property rights, and defamation.

How Does Professional Indemnity Insurance Work?

Professional indemnity insurance policies typically have a limit of liability, which is the maximum amount the insurance company will pay out in the event of a claim. The policyholder pays an annual premium to the insurance company in exchange for this coverage.

If a client makes a claim against a professional for losses or damages resulting from the professional's negligence or errors, the insurance company will provide legal defense and cover the cost of any settlement or judgment.

How Do You Choose the Right Professional Indemnity Insurance Policy?

When choosing a professional indemnity insurance policy, it's important to consider your specific needs and the type of work you perform. You'll also want to compare policy limits, deductibles, and the types of coverage offered by different insurance providers.

#liability insuranceclaims insurance#professional liability insurance#liability insurance coverage#insurance types#policy insurance#indemnity insurance#doinsurance#insurance coverage#liability cover#professional indemnity insurance#cover insurance#insurance provide#provides insurance#professional liability#insurance cost#insurance cover types

0 notes

Text

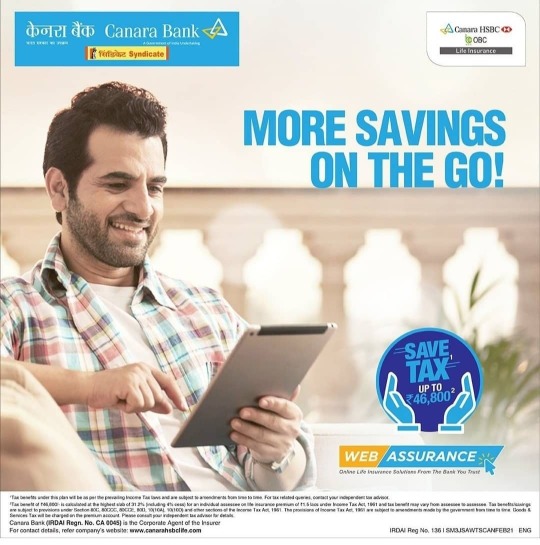

Canara Hsbc obc life insurance print pictures

#canarabank #canarahsbcobc #canarahsbcobclifei #hsbcbank #obcbank #rohitmehtaactor #lifeinsurance #doinsurance #careforlife #careforfamily

#rohitmehtaactor#rohitmehta#bollywood#indian model#chaupal#cinema#canarahsbcobclifeinsurance#canarabank#canara hsbc obc#obcbank#hsbcbank#tipravillage#chaupsl city#majhotli chaupal#jaret chopal#bodhna chopal#dewat chopal#tiyari chaupal#pabas chaupal#makrog maraog#maraog#jubbadchopal#chambi deha#khidki#deha#jhina chaupal#jhina#shilikayan chaupal#shilikayan#mashdoh chopal

5 notes

·

View notes

Link

A mediclaim-type health insurance policy generally does not cover the cost of most consumables used in the treatment of a disease or condition in a hospital. In a pre-coronavirus world, that was not a big problem. However, that is not the case now. The number and cost of consumables used in the treatment of Covid-19 has been increasing. This along with other factors has led to a rise in overall cost of coronavirus treatment. "Normal treatment cost of Rs 50,000-1 lakh has now surged to Rs 1-2 lakh for Covid-19 treatment (due to increase in cost of consumables, patient distancing in hospitals, etc.) and to Rs 6-7 lakh or more where co-morbidities are involved or treated in expensive hospitals," said Chandan D S Dang, Executive Director, Securenow.in, a Delhi-based insurance broker. Consumables in health insurance parlance refer to single-use items that are frequently used in medical treatments or procedures. These are considered non-medical items and hence, are not payable under most health insurance policies.Why the cost of treatment of Covid-19 has increased In hospitals, the use of personal protective equipment (PPE kits) is unavoidable to contain the spread of the coronavirus. A single PPE kit includes a pair of nitrile gloves, a single-use coverall, goggles with transparent glasses, an N-95 mask, shoe covers, and a face shield. Since each of these items are separately considered consumables, there is a significant increase in the number of consumables used in the treatment of Covid-19 infection. Not just the cost of PPE kits but the cost of other consumables is also included in the hospital bill. These consumables are normally surgical accessories like tissue paper, crepe bandage, gown, foot covers, slippers, disposable gloves, sheets, syringes, gowns, masks etc. Toiletries and cosmetics are also considered as consumables. None of this is covered under a health insurance policy, even though they are included in the hospital bill for treating a coronavirus patient at a hospital. Rakesh Goyal, Director, Probus Insurance, Insurtech Broking Company, said that on average, the cost of consumables accounts for 10 per cent of the treatment cost. "However, in Covid-19 treatment, the cost of consumables significantly increases as it is linked to the severity of the infection and the duration of hospitalisation. Moreover, the highly infectious nature of the novel coronavirus and mandated quarantine period of 14 days has significantly raised the cost of consumables. For instance, in Covid-19 cases, PPE kits, goggles, footwear, sanitisers and disinfectants are additionally required consumables," he said.As a result, the (non-payable) cost of such consumables forms a large portion of the total cost of treatment of Covid 19 infection in a hospital. Basically, these consumables are used for personal comfort or convenience and safety. Dang said that the list of consumables increases for Covid-19 treatment and can account for around 25 per cent of the total treatment cost. "The regulator has given clear directions that the entire cost of consumables has to be included in the Covid treatment cost," he said.Dang explained further, "The incremental cost is about Rs 1,500 per day if the person is just in the room. The nurses, doctors and staff wear these suits throughout the day, so the costs get apportioned across patients. However, during a surgery the incremental cost is about Rs 6,000 per surgery which is based on 5 PPE suits at about Rs 1,200 per suit. These need to be discarded after each surgery. So, over a week-long hospitalisation with a surgery the incremental cost will be Rs 16,500 (@Rs 1,500 for 7 days plus Rs 6,000 for the surgery)."Impact on hospital bills: Hospitals have increased the cost of treatment for Covid-19 patients not only because of increase in consumables used but also due to social distancing of patients. For instance, in a hospital ward where 20 people used to get treated, now only 10 are being treated due to patient distancing. Consumables used in treating Covid-19 are costly and mostly not payable by insurers Currently, most existing health insurance policies do not cover the cost of PPE kits and other consumables used in the treatment of Covid-19. Some insurers have considered these consumables as non-payable medical items the cost of which has to be borne as out-of-pocket expenses by the insured. Naval Goel, CEO & Founder, PolicyX.com said, "Because of COVID-19, hospitals are charging for consumables like PPEs.Hospitals confirmed that there is a rise of around 25% in the hospital bills due additional consumables required for Covid-19 treatment. However, insurance companies do not cover PPE costs at the time of claim settlement. This, however, depends on case to case basis," Goel said.Goel further said, "Most consumables generally come under non-medical expenses and are required for one-time use, mainly because of sterility and infection concerns. That is the reason why many health insurers don't pay for them."Since there is no capping on trade margin for consumables or disposables used for Covid-19 treatment, the cost of these consumables is also increasing sharply.Dr S Prakash, Managing Director, Star Health and Allied Insurance explains why some of the consumables are not covered under mediclaim policies: "Whatever consumables are reasonably required and appropriately charged are covered under the comprehensive health insurance policy. However, the problem occurs with some of the consumables where trade margin is very high. When the trade margin is too high, naturally there will not be adequate funds to pay for it. Hence, these are not covered by the insurers," Prakash said. Existing policyholders can check the detailed list of consumables, which are non-payable items, in their policy document.Abhijit Chatterjee, Executive Vice President (Claims), IFFCO Tokio General Insurance said, "For cashless claims also, the cost of consumables is non-payable and has to be borne by the policyholder. However, for Covid-19 related hospitalisation currently there is no protocol issued by any authority on various consumables. Hence, we are considering them on a case to case basis."It has been reported that the Insurance Regulatory and Development Authority of India (IRDAI) has asked the non-life insurance companies to work out a standardised cost structure for Covid-19 treatment due to the rise of treatment costs.What policyholders can doInsurance companies have the flexibility to include or exclude consumables in their health covers and charge premium accordingly. IRDAI has left it to the insurers' discretion whether they want to pay for consumables like PPE kits. Prakash said, "Most of the health insurance policies where the premium is priced low usually will reasonably cover some of these consumables. If the policy is priced well and if it is a high-end policy (comprehensive health insurance policy), it will usually cover all types of accommodation and most of the consumables that are used at the time treatment."Thus, if you are buying or renewing your policy in the coming days, it is important to check with your insurer whether your policy covers such consumables. Currently, only a few products in the market cover consumables used in the treatment of Covid-19. Therefore, check the detailed list of consumables in the policy document. The list of non-payable consumables varies from insurer to insurer.Click here to download ET Online’s guide to everything personal finance in the times of Covid-19 from Economic Times https://ift.tt/2YntcoX

0 notes

Text

How Market Research Analysts Can Benefit from Insurance

Do you work as a market research analyst? If so, you know that the job can be both satisfying and challenging. You also know that your job requires a great deal of responsibility and that you must be up- to- date on the latest market trends in order to be successful. Your job also requires you to be insured against pitfalls that you might encounter while conducting market research.

As a market research analyst, you face risks related to data security, intellectual property, and compliance. Having the right insurance can help protect you against these risks, as well as give you peace of mind.

We’re going to discuss the types of insurance that market research analysts should consider, as well as the benefits of having the right coverage.

First, let’s talk about the different types of insurance that market research analysts should consider. The most important type of insurance for market research analysts is professional liability insurance. This type of insurance protects you from claims of negligence, errors, and deletions that could arise from your work. Professional liability insurance also covers the cost of defending yourself against any claims you might face.

In addition to professional liability insurance, market research analysts may also want to consider cyber liability insurance. This type of insurance covers the cost of responding to data breaches and the cost of notifying affected individuals. Cyber liability insurance also provides coverage for the loss of business income and excess costs that may be incurred due to a cyber-attack.

Having the right insurance can provide market research analysts with peace of mind, knowing that they're covered against the risks associated with their job. In addition, having insurance can help you to demonstrate your commitment to professionalism and compliance. At the end of the day, market research analysts should make sure that they've the right insurance coverage in place.

#liability insuranceclaims insurance#professional liability insurance#liability insurance coverage#insurance types#policy insurance#indemnity insurance#doinsurance#insurance coverage#liability cover#professional indemnity insurance#cover insurance#insurance provide#provides insurance#professional liability#insurance cost#insurance cover types

0 notes

Text

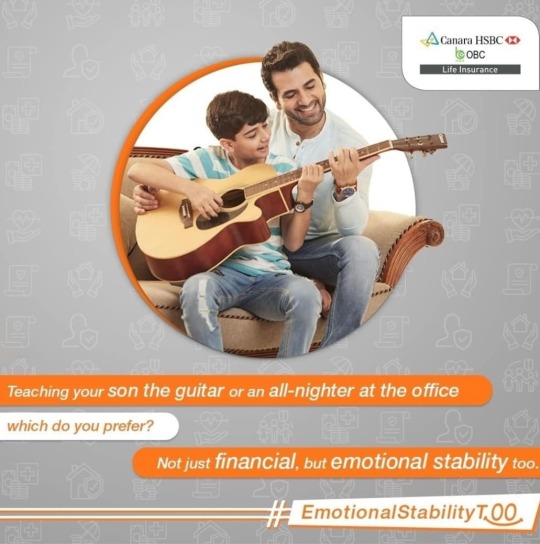

Canara Hsbc obc life insurance print pictures

#canarabank #canarahsbcobc #canarahsbcobclifei #hsbcbank #obcbank #rohitmehtaactor #lifeinsurance #doinsurance #careforlife #careforfamily

#rohitmehtaactor#rohitmehta#bollywood#indian model#chaupal#cinema#canarahsbcobclifeinsurance#canarabank#canara hsbc obc#obcbank#hsbcbank#tipravillage#chaupsl city#majhotli chaupal#jaret chopal#bodhna chopal#dewat chopal#tiyari chaupal#pabas chaupal#makrog maraog#maraog#jubbadchopal#chambi deha#khidki#deha#jhina chaupal#jhina#shilikayan chaupal#shilikayan#mashdoh chopal

3 notes

·

View notes