#automotive camera suppliers

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Hackers stole 65M passwords from Tumblr in 2013.

Text

Searching for an Automotive Camera Manufacturer? Find Trusted Options for Your Vehicle!

Seeking a trusted automotive camera manufacturer? Look no further than CK Vision! Whether you need to enhance your vehicle's safety or capture memorable moments on the road, we've got you covered. Trust CK Vision for quality automotive cameras that meet your needs and ensure peace of mind while driving.

#automotive camera manufacturers#car camera suppliers#automobile security camera system#automotive camera suppliers#automotive ip camera#3d camera in car

0 notes

Text

Who owns the data generated by your car? And who controls access to it?

For almost a decade, right-to-repair activists, automakers, parts manufacturers, auto repair shop owners, technicians, and regular people who own cars have fought over those questions. How they are answered could radically change the cost and convenience of owning a modern camera-studded and cloud-enabled car—and, some say, the future of the increasingly tech-heavy auto industry.

Last week, a few trade groups announced they had finally figured it all out. In a letter to the US Congress, three industry organizations that together represent the major automakers and thousands of repair shops said they had signed a “memorandum of understanding” on the right to repair. In the agreement, the automakers commit to giving independent car repair shops access to the data, tools, and information necessary to diagnose and repair vehicles—the data, tools, and information provided to the automakers’ own dealership networks. “Competition is alive and well in the auto repair industry,” the letter said.

Right-to-repair advocates—who contend that consumers should be able to fix the products they buy—aren’t so sure. They say the agreement doesn’t give car owners full and unfettered control of the streams of data generated by the latest cars’ cameras and other sensors, which log data on location, speed, acceleration, and how a vehicle’s hardware and software are performing.

The advocates worry the new agreement gives automakers and automaker-associated repairers room to squeeze out smaller, independent shops and at-home tinkerers in the future, making it more difficult for car owners to find places to quickly and affordably fix their cars. And they say there are no enforcement mechanisms to guarantee automakers follow through on their promises.

“In terms of how automakers behave and whether vehicle owners or repair shops will get access to information—I don’t think this will change anything,” says Paul Roberts, the founder of SecuRepairs.org, an organization of IT and cyber professionals advocating for the right to repair.

Notably, the new agreement didn’t include the Auto Care Association, the largest US trade group for independent repair shops and aftermarket parts suppliers. The group's chair, Corey Bartlett, says the agreement doesn’t address some of the major barriers facing consumers looking to get a tech-heavy car repaired.

Smaller and especially rural repair shops sometimes can’t fix the newest models, because they can’t pay for the expensive tools, subscriptions, and training needed, which can cost hundreds of thousands of dollars. As cars get more complex, and move more services into apps and onto the internet, they fear access will shrink. “We want easy and affordable access to that information for the independent repair shop,” says Bartlett, who is also president and CEO of Automotive Parts Headquarters, which sells aftermarket auto parts to repair shops across the northern and midwestern US.

DIY car repair and auto shops independent of automakers are a long-established tradition in car culture and the auto industry. The Alliance for Automotive Innovation, the trade group representing most global automakers, says that even today, 70 percent of their own certified networks of collision repair shops aren’t owned by dealers.

Many repair shops, especially those who opt in and pay to be part of those certified networks, say they have no trouble finding the information they need to fix cars, even before this week’s agreement. Michael Bradshaw, vice president of K & M Collision in Hickory, North Carolina, and vice chair of the Society of Collision Repair Specialists, one of the groups that signed the new agreement, says his shop pays to keep up with 30 automaker certification programs, including for Kia, General Motors, Bentley, and Rivian.

In a way, Bradshaw agrees with the right-to-repair advocates: This week’s agreement doesn’t give him anything he didn’t already have. “If there’s data out there, and repair information, we’ve always been able to get that,” Bradshaw says. But he disagrees that it’s a problem that repairers must pay, sometimes dearly, to get the tools, certifications, and information that allow them to fix cars.

Bradshaw thinks it’s reasonable that he must pay for automakers’ certification programs, because developing car technology—and the documentation needed to repair it—costs the carmaker plenty of money. He’s willing to shell out whatever is needed to make a safe and effective repair. “If it was a situation where there was no charge for the access, you’re going to see that the information is going to suffer,” he says, because automakers will have less incentive to devote resources to creating clear information for repairers. “The businesses that have trouble paying for the data that’s needed are the same businesses that are not investing in training or equipment.”

Other repairers worry that without an industry-wide overhaul that forces automakers to standardize and open up their data, car companies will find ways to limit access to repair information, or push customers towards their own dealership networks to boost profits. They say that if auto owners had clear and direct ownership over the data generated by their vehicles—without the involvement of automakers’ specialized tools or systems—they could use it themselves to diagnose and repair a car, or authorize the repair shop of their choice to do the work. “My fear, if no one gives some stronger guidelines, is that I know automakers are going to monetize car data in a way that’s unaffordable for us to gain access,” says Dwayne Myers, co-owner of Dynamic Automotive, an auto repair business with several locations in Maryland.

“You have to think not only about what the situation is now, but what the situation will be five or 10 years hence,” says Roberts, the right-to-repair advocate. “It’s easier to address this now, in the early days.”

Perhaps by design, the new agreement appeared just ahead of a hearing on right to repair by a US House of Representatives subcommittee on intellectual property and the internet. A bipartisan group of representatives have already introduced bills on the topic.

The hearing follows national wrangling over a Massachusetts law passed by a 2020 ballot measure that gave state car owners firmer control over the data generated by their cars. The Alliance for Automotive Innovation sued the state over the law, preventing lawmakers from enforcing it, and a judge has yet to decide the case. But last month, the Massachusetts attorney general announced she would begin to penalize automakers that withheld data for not complying with the rule. Days later, the US Department of Transportation warned automakers not to comply with the Massachusetts law, citing concerns it would open vehicles to hacking. The letter appeared to contradict the Biden administration’s prior commitments to right-to-repair issues.

Brian Weiss, a spokesperson for the Alliance, declined to comment on the Massachusetts law, citing the ongoing litigation. But how or whether the new agreement will affect other states’ right-to-repair policies is up to policymakers, he says. It commits the trade groups who signed to push for federal rules defining right to repair and against state legislation, which could create a patchwork of laws with different obligations to DIYers or independent repairers. That echoes an agreement signed earlier this year by tractor maker John Deere and a major agricultural trade group, which advocates said failed to give farmers clear access to the tools and software needed to fix their farm equipment.

Myers, the Maryland independent repairer, says that allowing customers to own their car's data today would, first and foremost, “give them the right to choose where they get their car fixed.” But he also has his eye on the future. “Down the road, we will find out what automakers are collecting,” he says—and why. He’d rather establish car owners’ right to control that information now, before they discover too late that it’s being used in ways they don’t like.

4 notes

·

View notes

Text

Edge AI Processor Market Value to Hit $9.89 Billion by 2032 | Industry Forecast

Astute Analytica has released a comprehensive report titled Global Edge AI Processor Market – Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2024-2032. This report provides an in-depth examination of the industry, including valuable insights into market analysis, competition, and geographical research. It also highlights recent developments in the global industry.

Market Overview and Forecast

The Global edge AI processor market was valued at US$ 2,163.2 million in 2023 and is projected to hit the market valuation of US$ 9,891.5 million by 2032 at a CAGR of 18.4% during the forecast period 2024–2032.

In addition to market positioning, the report offers a thorough analysis of relevant data, key developments, and revenue streams. It outlines the strategies employed by key market players to expand their market presence and strengthen their positions. The report includes detailed information that illustrates the overall market condition.

A Request of this Sample PDF File@- https://www.astuteanalytica.com/request-sample/edge-ai-processor-market

Key Insights

The report emphasizes future trends, market dynamics, market shares, threats, opportunities, and entry barriers. Important analytical data is presented through pie charts, graphs, and tables, providing readers with a clear understanding of the market landscape.

Marketing Channels and Supply Chain

Special attention is given to marketing channels, downstream client surveys, upstream raw materials analysis, and market development trends. The report also includes expert recommendations and crucial information about major chemical suppliers, manufacturers, key consumers, distributors, and dealers, along with their contact details. This information is essential for conducting a detailed market chain analysis.

Geographical Analysis

The report features detailed investigations into the global market across various regions, analyzing over 20 countries that significantly contribute to market development. Key regional markets studied include North America, Europe, Asia Pacific, South America, Africa, the Middle East, and Latin America. This thorough examination aids in identifying regional market opportunities and challenges.

Competitive Analysis

To illustrate the competitive landscape, the report differentiates business attributes and identifies leading market players. It includes the latest trends, company profiles, financial standings, and SWOT analyses of major Edge AI Processor market players, providing a comprehensive view of the competitive environment.

Key Players

Advanced Micro Devices, Inc.

Huawei Technologies

IBM

Intel Corporation

Hailo

NVIDIA Corporation

Mythic

MediaTek Inc.

Graphcore

STMicroelectronics

Other Prominent Companies

For Purchase Enquiry: https://www.astuteanalytica.com/industry-report/edge-ai-processor-market

Methodology

The global Edge AI Processor analysis is based on primary and secondary data sources. Primary sources include expert interviews with industry analysts, distributors, and suppliers, while secondary sources encompass statistical data reviews from government websites, press releases, and annual reports. Both data types validate the findings from global market leaders. The report utilizes top-down and bottom-up approaches to analyze estimates for each segment.

Market Segmentation

By Processor Type

Central Processing Unit (CPU)

Graphics Processing Unit (GPU)

Field Programmable Gate Arrays (FPGA)

Application Specific Integrated Circuits (ASIC)

By Device Type

Consumer Devices

Enterprise Devices

By Application

Robotics

Smartphones and Mobile Devices

Internet of Things (IoT) Devices

Smart Cameras and Surveillance Systems

Autonomous Vehicles

Industrial Automation

Others

By End User

Consumer Electronics

Healthcare

Automotive

Retail

Security and Surveillance

Government

Agriculture

Others (Manufacturing, Construction, etc.)

By Region

North America

The U.S.

Canada

Mexico

Europe

Western Europe

The UK

Germany

France

Italy

Spain

Rest of Western Europe

Eastern Europe

Poland

Russia

Rest of Eastern Europe

Asia Pacific

China

India

Japan

Australia & New Zealand

South Korea

ASEAN

Rest of Asia Pacific

Middle East & Africa (MEA)

Saudi Arabia

South Africa

UAE

Rest of MEA

South America

Argentina

Brazil

Rest of South America

Download Sample PDF Report@- https://www.astuteanalytica.com/request-sample/edge-ai-processor-market

About Astute Analytica:

Astute Analytica is a global analytics and advisory company that has built a solid reputation in a short period, thanks to the tangible outcomes we have delivered to our clients. We pride ourselves in generating unparalleled, in-depth, and uncannily accurate estimates and projections for our very demanding clients spread across different verticals. We have a long list of satisfied and repeat clients from a wide spectrum including technology, healthcare, chemicals, semiconductors, FMCG, and many more. These happy customers come to us from all across the globe.

They are able to make well-calibrated decisions and leverage highly lucrative opportunities while surmounting the fierce challenges all because we analyse for them the complex business environment, segment-wise existing and emerging possibilities, technology formations, growth estimates, and even the strategic choices available. In short, a complete package. All this is possible because we have a highly qualified, competent, and experienced team of professionals comprising business analysts, economists, consultants, and technology experts. In our list of priorities, you-our patron-come at the top. You can be sure of the best cost-effective, value-added package from us, should you decide to engage with us.

Get in touch with us

Phone number: +18884296757

Email: [email protected]

Visit our website: https://www.astuteanalytica.com/

LinkedIn | Twitter | YouTube | Facebook | Pinterest

0 notes

Text

Lithium-ion Battery Market 2030 Size Outlook, Growth Insight, Share, Trends

In 2023, the global lithium-ion (Li-ion) battery market was estimated to be worth USD 54.4 billion and is projected to grow at a compound annual growth rate (CAGR) of 20.3% from 2024 to 2030. This growth is largely driven by rising demand for electric vehicles (EVs), supported by the cost-effectiveness and energy efficiency of Li-ion batteries. The automotive sector, in particular, is expected to see significant expansion due to the increasing global registration of EVs, as more consumers seek cleaner and more sustainable transport options. In the United States, the largest North American market for Li-ion batteries in 2023, federal policies and the presence of key industry players are anticipated to drive further product demand. Government policies, such as tax incentives for EV purchases under the American Recovery and Reinvestment Act of 2009, as well as fuel efficiency standards introduced by the Corporate Average Fuel Economy (CAFE) regulations, have accelerated the shift towards electric drive technologies in both passenger cars and light commercial vehicles (LCVs).

In addition to the automotive sector, the demand for Li-ion batteries in consumer electronics is also driving market growth. As consumers seek more durable and energy-efficient devices, lithium-ion batteries are becoming a preferred choice for smartphones, tablets, and other electronics due to their long lifespan and high performance. The demand for EVs is similarly bolstered by growing awareness of carbon emissions and the environmental impact of traditional gasoline-powered vehicles, which motivates consumers to adopt cleaner alternatives. This trend is supported by regulatory pressures on lead-acid batteries due to environmental concerns. Specifically, regulations set by the Environmental Protection Agency (EPA) aim to reduce lead contamination and govern the storage, disposal, and recycling of lead-acid batteries, prompting a shift towards safer Li-ion battery solutions for automotive applications.

Gather more insights about the market drivers, restrains and growth of the Lithium-ion Battery Market

Mexico has also emerged as a strategic center for the global automotive industry, attracting investments from companies worldwide due to its large automotive production capacity. As the fourth-largest exporter of vehicles globally, following Germany, Japan, and South Korea, Mexico's automotive production is expected to further stimulate demand for lithium-ion batteries in the region. However, the market faced challenges during the COVID-19 pandemic. Battery providers had to adapt by reducing operational costs due to lower demand and by managing disruptions in the supply of spare parts caused by reduced manufacturing activity and logistical issues. To maintain service quality for clients with long-term contracts, suppliers turned to digital tools and implemented strict health and safety measures, including social distancing and personal protective equipment, to ensure safe on-site maintenance and repair services where necessary.

Application Segmentation Insights:

The Li-ion battery market is categorized into several application segments: automotive, consumer electronics, industrial, medical devices, and energy storage systems. In 2023, the consumer electronics segment led the market, accounting for over 31% of total revenue. Portable lithium-ion batteries are widely used in consumer electronics due to their compact size, high energy density, and rechargeability. They are incorporated into various devices, including mobile phones, laptops, tablets, LED lighting, digital cameras, wristwatches, hearing aids, and other wearable gadgets. This high demand for portable devices has positioned the consumer electronics segment as a dominant sector in the market.

The electric and hybrid EV market is anticipated to be the fastest-growing application segment over the forecast period. Rising fossil fuel prices and increased awareness of the environmental benefits of battery-operated vehicles are expected to drive this growth, especially in emerging markets across Asia-Pacific, Europe, and North America. Moreover, Li-ion batteries are widely utilized for backup power solutions in commercial settings, such as data centers, office buildings, and institutions. In residential applications, Li-ion batteries are becoming popular for energy storage in solar photovoltaic (PV) systems, enhancing the growth potential of the energy storage segment.

Li-ion batteries are also gaining traction in various industrial applications. They are commonly used in power tools, cordless tools, marine equipment, agricultural machinery, industrial automation systems, aviation, military & defense, civil infrastructure, and the oil and gas sector. The versatility of Li-ion batteries, combined with their ability to deliver consistent power across diverse conditions, makes them ideal for these industries. Their use in such a broad range of applications is projected to further boost market demand as industries seek reliable and efficient energy solutions that can support both heavy-duty equipment and everyday electronic devices.

In summary, the lithium-ion battery market is poised for rapid growth across multiple sectors. The automotive and consumer electronics segments, in particular, are driving demand, supported by governmental policies, environmental concerns, and technological advancements. The expansion into applications like energy storage and industrial machinery further underscores the adaptability and efficiency of Li-ion batteries, positioning them as a critical component of future energy solutions across the globe.

Order a free sample PDF of the Lithium-ion Battery Market Intelligence Study, published by Grand View Research.

0 notes

Text

Lithium-ion Battery Industry Strategies With Forecast Till 2030

In 2023, the global lithium-ion (Li-ion) battery market was estimated to be worth USD 54.4 billion and is projected to grow at a compound annual growth rate (CAGR) of 20.3% from 2024 to 2030. This growth is largely driven by rising demand for electric vehicles (EVs), supported by the cost-effectiveness and energy efficiency of Li-ion batteries. The automotive sector, in particular, is expected to see significant expansion due to the increasing global registration of EVs, as more consumers seek cleaner and more sustainable transport options. In the United States, the largest North American market for Li-ion batteries in 2023, federal policies and the presence of key industry players are anticipated to drive further product demand. Government policies, such as tax incentives for EV purchases under the American Recovery and Reinvestment Act of 2009, as well as fuel efficiency standards introduced by the Corporate Average Fuel Economy (CAFE) regulations, have accelerated the shift towards electric drive technologies in both passenger cars and light commercial vehicles (LCVs).

In addition to the automotive sector, the demand for Li-ion batteries in consumer electronics is also driving market growth. As consumers seek more durable and energy-efficient devices, lithium-ion batteries are becoming a preferred choice for smartphones, tablets, and other electronics due to their long lifespan and high performance. The demand for EVs is similarly bolstered by growing awareness of carbon emissions and the environmental impact of traditional gasoline-powered vehicles, which motivates consumers to adopt cleaner alternatives. This trend is supported by regulatory pressures on lead-acid batteries due to environmental concerns. Specifically, regulations set by the Environmental Protection Agency (EPA) aim to reduce lead contamination and govern the storage, disposal, and recycling of lead-acid batteries, prompting a shift towards safer Li-ion battery solutions for automotive applications.

Gather more insights about the market drivers, restrains and growth of the Lithium-ion Battery Market

Mexico has also emerged as a strategic center for the global automotive industry, attracting investments from companies worldwide due to its large automotive production capacity. As the fourth-largest exporter of vehicles globally, following Germany, Japan, and South Korea, Mexico's automotive production is expected to further stimulate demand for lithium-ion batteries in the region. However, the market faced challenges during the COVID-19 pandemic. Battery providers had to adapt by reducing operational costs due to lower demand and by managing disruptions in the supply of spare parts caused by reduced manufacturing activity and logistical issues. To maintain service quality for clients with long-term contracts, suppliers turned to digital tools and implemented strict health and safety measures, including social distancing and personal protective equipment, to ensure safe on-site maintenance and repair services where necessary.

Application Segmentation Insights:

The Li-ion battery market is categorized into several application segments: automotive, consumer electronics, industrial, medical devices, and energy storage systems. In 2023, the consumer electronics segment led the market, accounting for over 31% of total revenue. Portable lithium-ion batteries are widely used in consumer electronics due to their compact size, high energy density, and rechargeability. They are incorporated into various devices, including mobile phones, laptops, tablets, LED lighting, digital cameras, wristwatches, hearing aids, and other wearable gadgets. This high demand for portable devices has positioned the consumer electronics segment as a dominant sector in the market.

The electric and hybrid EV market is anticipated to be the fastest-growing application segment over the forecast period. Rising fossil fuel prices and increased awareness of the environmental benefits of battery-operated vehicles are expected to drive this growth, especially in emerging markets across Asia-Pacific, Europe, and North America. Moreover, Li-ion batteries are widely utilized for backup power solutions in commercial settings, such as data centers, office buildings, and institutions. In residential applications, Li-ion batteries are becoming popular for energy storage in solar photovoltaic (PV) systems, enhancing the growth potential of the energy storage segment.

Li-ion batteries are also gaining traction in various industrial applications. They are commonly used in power tools, cordless tools, marine equipment, agricultural machinery, industrial automation systems, aviation, military & defense, civil infrastructure, and the oil and gas sector. The versatility of Li-ion batteries, combined with their ability to deliver consistent power across diverse conditions, makes them ideal for these industries. Their use in such a broad range of applications is projected to further boost market demand as industries seek reliable and efficient energy solutions that can support both heavy-duty equipment and everyday electronic devices.

In summary, the lithium-ion battery market is poised for rapid growth across multiple sectors. The automotive and consumer electronics segments, in particular, are driving demand, supported by governmental policies, environmental concerns, and technological advancements. The expansion into applications like energy storage and industrial machinery further underscores the adaptability and efficiency of Li-ion batteries, positioning them as a critical component of future energy solutions across the globe.

Order a free sample PDF of the Lithium-ion Battery Market Intelligence Study, published by Grand View Research.

0 notes

Text

Uses of Quality Function Deployment

Quality Function Deployment (QFD) is a versatile tool that can be applied across various industries and processes to ensure that customer needs are central to product development, service improvement, and quality management. Here are some key uses of QFD:

1. Product Development and Design:

Primary Use: QFD is most commonly used in the product development lifecycle to ensure that customer requirements are translated into design and engineering specifications.

Example: In the automotive industry, QFD is used to design cars that meet customer needs for safety, fuel efficiency, comfort, and aesthetics by translating these needs into technical design features such as airbags, engine efficiency, and ergonomic seating.

2. Service Industry Improvement:

Use: In the service industry, QFD helps design and improve services based on customer feedback and expectations. This is particularly important in customer-facing sectors like hospitality, healthcare, and banking.

Example: In healthcare, hospitals can use QFD to improve patient satisfaction by translating patient feedback (e.g., shorter wait times, cleaner facilities) into actionable improvements in staffing levels and facility management.

3. Process Improvement:

Use: QFD can be used to improve internal processes by linking customer requirements with operational improvements. It ensures that changes in processes are aligned with customer needs.

Example: A manufacturing company might use QFD to streamline its production process, ensuring that improvements in efficiency (like reducing lead times) directly benefit the customer through faster delivery and lower costs.

4. Voice of the Customer (VOC) Analysis:

Use: QFD is a structured way to capture and analyze the “Voice of the Customer” (VOC). It ensures that customer desires and preferences are systematically considered during product or service design.

Example: A software company may use QFD to gather user feedback on their software interface and functionality, translating this feedback into technical design changes for future software updates.

5. Strategic Planning and Market Positioning:

Use: QFD can assist companies in aligning their products with market demands and strategic goals. By identifying key customer needs, companies can position their products more effectively in the market.

Example: A tech company launching a new smartphone could use QFD to ensure that features such as camera quality, battery life, and user experience are prioritized based on customer expectations, improving market competitiveness.

6. Reducing Product Development Time:

Use: QFD helps to minimize the time spent on trial and error during product design by ensuring that customer needs are understood and addressed early in the design phase. This reduces the need for costly revisions later on.

Example: In consumer electronics, companies use QFD to reduce product development cycles by ensuring that design specifications are clearly defined and aligned with customer needs before prototyping begins.

7. Enhancing Product Quality:

Use: QFD is instrumental in improving product quality by ensuring that every feature or characteristic of a product is linked to customer expectations and requirements.

Example: In the food industry, QFD can be used to improve product quality by translating customer requirements (e.g., taste, packaging, shelf-life) into specific product specifications and quality control measures.

8. Supplier Selection and Management:

Use: QFD can also be used in supply chain management, particularly for selecting and managing suppliers based on their ability to meet specific technical and quality requirements linked to customer needs.

Example: An automotive manufacturer may use QFD to evaluate suppliers based on their ability to provide materials that meet safety and durability standards, ensuring consistency with customer demands for reliable and safe vehicles.

9. New Market Development:

Use: Companies entering new markets can use QFD to identify and adapt to the unique needs and preferences of customers in that market, helping to develop products or services that align with local expectations.

Example: A global consumer goods company could use QFD to tailor products to regional tastes, ensuring that new product features (e.g., flavor, packaging) match cultural preferences in different countries.

10. Benchmarking Against Competitors:

Use: QFD can be used to compare a company’s product features with those of competitors, ensuring that the product is not only meeting customer needs but also outperforming rival offerings.

Example: A smartphone manufacturer may use QFD to benchmark its product’s camera quality, battery life, and user interface against leading competitors, ensuring that its new model offers superior value.

11. Project Management and Decision Making:

Use: In project management, QFD can guide decision-making by linking project activities and deliverables directly to customer requirements. This ensures that project goals are customer-focused and well-prioritized.

Example: In software development projects, QFD ensures that features and functionalities prioritized in the project timeline are based on what users value most, such as ease of use and performance.

12. Risk Management:

Use: QFD can be used to identify potential risks related to customer dissatisfaction and technical challenges by clarifying the relationship between customer expectations and product design.

Example: In the pharmaceutical industry, companies can use QFD to identify risks associated with drug efficacy, side effects, and dosage forms, ensuring that any risks are mitigated early in the product development process.

13. Continuous Improvement and Innovation:

Use: QFD facilitates continuous improvement by providing a framework for gathering customer feedback and systematically improving products and services over time.

Example: An electronics manufacturer may use QFD to collect customer feedback on each new version of its products, continuously improving features like battery life, screen resolution, or device durability in response to customer feedback.

14. Sustainability and Environmental Impact:

Use: QFD can be applied to ensure that customer demands for sustainable and environmentally friendly products are incorporated into product design and manufacturing processes.

Example: A packaging company might use QFD to design eco-friendly packaging solutions by translating customer demands for sustainability into technical requirements, such as the use of biodegradable materials.

Summary of Uses:

Product design and development to align with customer needs.

Service improvement to enhance customer satisfaction.

Process optimization to ensure operational efficiency.

VOC analysis for customer feedback integration.

Strategic planning to align products with market demands.

Benchmarking to evaluate competitors and drive innovation.

QFD’s strength lies in its ability to ensure that every decision, from design to production, is driven by what the customer values most. This makes it a crucial tool for organizations focused on quality, customer satisfaction, and continuous improvement.

#sixsigma#leansixsigma#leanmanufacturing#processimprovement#operationsmanagement#management#changemanagement#leanthinking#lean six sigma#KanbanSystem#KMP#CertificationTraining#WorkflowImprovement#ProductivityImprovement#kanban training#KMPtraining#kmpcertification

0 notes

Text

Lithium-Ion Battery Market Growth Opportunities and Outlook 2024 – 2030

The global lithium-ion battery market size was estimated at USD 182.5 billion in 2030 and is projected to register a compound annual growth rate (CAGR) of 20.3% from 2024 to 2030. The market is expected to witness significant growth over the forecast period on account of the increasing consumption of rechargeable batteries in consumer electronics and a rise in the adoption of electric vehicles. The rising sales of electric vehicles, along with the expanding renewable energy sector, are expected to drive the market. The emergence of integrated charging stations, green power-generation capability, eMobility providers, battery manufacturers, and energy suppliers is anticipated to stimulate market growth in the coming years.

Increasing sales of electric vehicles in the U.S. owing to supportive federal policies, coupled with the presence of market players in the country, are expected to drive the demand for lithium-ion batteries in the U.S. over the forecast period. Favorable government policies for infrastructural developments at the domestic level through the National Infrastructural Plan (NIP) of the U.S. are expected to promote the growth of the market in the U.S. over the forecast period. Development of the automotive industry in Indonesia, Vietnam, Mexico, Thailand, and India is expected to drive the industry. The growing inclination toward pollution-free HEVs and EVs, along with technological developments, is expected to drive the lithium-ion battery demand over the forecast period. China is expected to witness high gains in light of energy storage technologies and favorable government support to promote investments in the manufacturing sector.

Gather more insights about the market drivers, restrains and growth of the Lithium-Ion Battery Market

Detailed Segmentation:

Application Insights

Based on applications, the market has been segmented into automotive, consumer electronics, industrial, medical devices, and energy storage systems. The consumer electronics segment led the market in 2023 and accounted for the largest revenue share of more than 31.0%. Portable batteries are incorporated in portable devices and consumer electronic products. Applications of portable batteries range from mobile phones, laptops, computers, tablets, torches or flashlights, LED lighting, vacuum cleaners, digital cameras, wristwatches, calculators, hearing aids, and other wearable devices. The electric & hybrid EV market is projected to be the fastest-growing application segment over the forecast period.

Regional Insights

Asia Pacific held the largest market share of over 47.0% in 2023. The market in Europe is expected to witness steady growth over the forecast period owing to the increasing use of li-ion batteries in various sectors including medical, aerospace & defense, automotive, energy storage, and data communication & telecom. The market in Germany is expected to witness steady growth over the forecast period owing to the increasing use of Li-ion batteries in energy storage systems, EVs, and consumer electronics.

Market Dynamics

The increasing adoption of electric vehicles (EVs) is catalyzing a remarkable surge in the global lithium-ion battery industry. As governments and industries worldwide prioritize the transition toward sustainable and environment-friendly transportation, the demand for EVs has experienced a substantial upswing. Lithium-ion batteries, renowned for their high energy density and efficiency, have emerged as the cornerstone of this automotive revolution. These batteries power electric vehicles, providing them with the necessary range and performance to compete with traditional internal combustion engine vehicles.

Product Insights

Based on products, the industry has been segregated into Lithium Cobalt Oxide (LCO), Lithium Iron Phosphate (LFP), Lithium Nickel Cobalt Aluminum Oxide (NCA), Lithium Manganese Oxide (LMO), Lithium Titanate, and Lithium Nickel Manganese Cobalt (NMC). In terms of revenue, the LCO segment accounted for the largest market share of over 30.0% in 2023. High demand for LCO batteries in mobile phones, tablets, laptops, and cameras, on account of their high energy density and high safety level, is expected to augment segment growth over the forecast period. LFP batteries offer excellent safety and a long-life span to product.

Browse through Grand View Research's Conventional Energy Industry Research Reports.

• The global digital oilfield market size was valued at USD 27.4 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 6.2% from 2024 to 2030.

• The global energy harvesting system market size was valued at USD 452.2 million in 2020 and is expected to grow at a compound annual growth rate (CAGR) of 10.2% from 2020 to 2028.

Key Companies & Market Share Insights

The industry is extremely competitive with key participants involved in R&D and constant product innovation. Key manufactures include Samsung, BYD, LG Chem, Johnson Controls, Exide, and Saft. Several companies are engaged in new product development to improve their global market share. For instance, BYD and Panasonic hold a strong position on account of its increased manufacturing capacities and large distribution network.

Key Lithium-ion Battery Companies:

• BYD Co., Ltd.

• A123 Systems LLC

• Hitachi, Ltd.

• Johnson Controls

• LG Chem

• Panasonic Corp.

• Saft

• Samsung SDI Co., Ltd.

• Toshiba Corp.

• GS Yuasa International Ltd.

Lithium-ion Battery Market Segmentation

Grand View Research has segmented the global lithium-ion battery market report based on product, application and region

Lithium-ion Battery Product Outlook (Volume, GWh; Revenue, USD Billion, 2018 - 2030)

• Lithium Cobalt Oxide (LCO)

• Lithium Iron Phosphate (LFP)

• Lithium Nickel Cobalt Aluminum Oxide (NCA)

• Lithium Manganese Oxide (LMO)

• Lithium Titanate

• Lithium Nickel Manganese Cobalt (LMC)

Lithium-ion Battery Application Outlook (Volume, GWh; Revenue, USD Billion, 2018 - 2030)

• Automotive

• Consumer Electronics

• Industrial

• Energy Storage Systems

• Medical Devices

Lithium-ion Battery Regional Outlook (Volume, GWh; Revenue, USD Billion, 2018 - 2030)

• North America

o U.S.

o Canada

o Mexico

• Europe

o Russia

o Spain

o France

o U.K.

o Germany

o Italy

• Asia Pacific

o China

o India

o Japan

o South Korea

o Australia

• Central & South America

o Brazil

o Paraguay

o Columbia

• Middle East & Africa

o South Africa

o UAE

o Egypt

o Saudi Arabia

Order a free sample PDF of the Lithium-Ion Battery Market Intelligence Study, published by Grand View Research.

#Lithium-Ion Battery Market#Lithium-Ion Battery Market size#Lithium-Ion Battery Market share#Lithium-Ion Battery Market analysis#Lithium-Ion Battery Industry

0 notes

Text

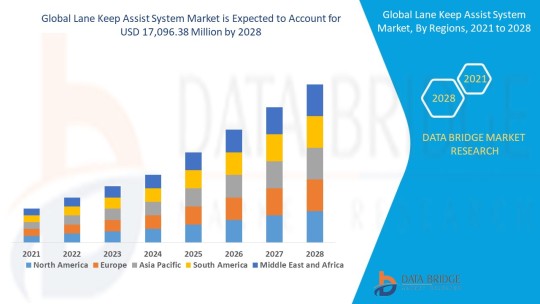

Lane Keep Assist System Market Size, Share, Trends, Opportunities, Key Drivers and Growth Prospectus

"Global Lane Keep Assist System Market – Industry Trends and Forecast to 2028

Global Lane Keep Assist System Market, By Function Type (Lane Keeping System, Lane Departure Warning), Component (Vision Sensor/Camera, EPAS Actuator, Electronic Control Unit, Others), Vehicle Type (Passenger Vehicles, Commercial Vehicles), Distribution Channel (Original Equipment Manufacturers (OEMs), Aftermarket), Country (U.S., Canada, Mexico, Brazil, Argentina, Rest of South America, Germany, Italy, U.K., France, Spain, Netherlands, Belgium, Switzerland, Turkey, Russia, Rest of Europe, Japan, China, India, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific, Saudi Arabia, U.A.E, South Africa, Egypt, Israel, Rest of Middle East and Africa) Industry Trends and Forecast to 2028

Access Full 350 Pages PDF Report @

**Segments**

- **Type**: The Lane Keep Assist System market can be segmented based on the type of vehicle the system is installed in, such as passenger cars, commercial vehicles, and electric vehicles. Each type of vehicle may have different requirements and specifications for lane keep assist systems, influencing the market.

- **Component**: The market can also be segmented based on the components of the lane keep assist system, which may include cameras, sensors, actuators, and software. The demand for these components can vary based on the technology used and the level of autonomy provided by the system.

- **Sales Channel**: Another important segmentation factor is the sales channel through which lane keep assist systems are distributed and sold. This can include OEMs, aftermarket suppliers, and online retailers. The choice of sales channel can impact the accessibility and visibility of these systems in the market.

**Market Players**

- **Continental AG**: Continental AG is a key player in the Lane Keep Assist System market, offering a range of advanced driver assistance systems for various types of vehicles. The company focuses on innovation and safety to meet the growing demand for lane keep assist systems.

- **Robert Bosch GmbH**: Robert Bosch GmbH is another prominent player known for its cutting-edge technologies in the automotive sector, including lane keep assist systems. The company's strong research and development capabilities drive its presence in the market.

- **Denso Corporation**: Denso Corporation is a leading supplier of automotive technology, including lane keep assist systems. With a global presence and a focus on quality and reliability, Denso plays a significant role in shaping the market.

- **Valeo**: Valeo is a renowned supplier of automotive components, including advanced driver assistance systems like lane keep assist. The company's expertise in vehicle safety and efficiency enhances its position in the market.

- **ZF Friedrichshafen AG**: ZF Friedrichshafen AG is a major player offering a wide range of automotive technologies, including lane keep assist systems. The companyContinental AG, Robert Bosch GmbH, Denso Corporation, Valeo, and ZF Friedrichshafen AG are among the key players shaping the Lane Keep Assist System market. These companies are at the forefront of innovation and technology advancements in the automotive sector, particularly in the development of advanced driver assistance systems like lane keep assist. With the increasing focus on vehicle safety and the shift towards autonomous driving, these market players have been investing heavily in research and development to enhance the capabilities and reliability of their systems.

Continental AG stands out for its diverse range of advanced driver assistance systems and its commitment to meeting the evolving demands of the market. The company's focus on safety and innovation has allowed it to establish a strong presence in the Lane Keep Assist System market, catering to both passenger cars and commercial vehicles. With a reputation for high-quality products, Continental AG continues to drive advancements in lane keep assist technology.

Robert Bosch GmbH is renowned for its cutting-edge technologies in the automotive sector, including lane keep assist systems. The company's significant investment in research and development enables it to introduce state-of-the-art solutions that enhance vehicle safety and performance. By leveraging its expertise in software and hardware integration, Robert Bosch GmbH remains a key player in the Lane Keep Assist System market, offering solutions tailored to different vehicle types and customer needs.

Denso Corporation's global presence and focus on quality and reliability position it as a leading supplier of automotive technology, including lane keep assist systems. The company's commitment to enhancing driver safety and comfort through advanced driver assistance systems has solidified its role in shaping the market. Denso Corporation's ability to integrate cutting-edge technologies into its products ensures that it stays competitive in the rapidly evolving automotive landscape.

Valeo, known for its expertise in vehicle safety and efficiency, is a renowned supplier of automotive components, including lane keep assist systems. The company's emphasis on innovation and sustainability has enabled it to develop solutions that meet the stringent requirements of the automotive industry. Valeo's strong focus on research and development**Global Lane Keep Assist System Market**

- **Function Type** - Lane Keeping System - Lane Departure Warning

- **Component** - Vision Sensor/Camera - EPAS Actuator - Electronic Control Unit - Others

- **Vehicle Type** - Passenger Vehicles - Commercial Vehicles

- **Distribution Channel** - Original Equipment Manufacturers (OEMs) - Aftermarket

The global Lane Keep Assist System market is projected to witness significant growth in the coming years, driven by increasing focus on vehicle safety and advancements in driver assistance systems. The market segmentation based on function type, component, vehicle type, and distribution channel provides a comprehensive outlook on the diverse factors influencing the market dynamics. The rise in demand for lane keeping systems and lane departure warning systems across passenger cars and commercial vehicles further fuels the market expansion.

Key market players such as Continental AG, Robert Bosch GmbH, Denso Corporation, Valeo, and ZF Friedrichshafen AG are actively shaping the Lane Keep Assist System market with their innovative solutions and technological expertise. These companies are at the forefront of developing advanced driver assistance systems that cater to evolving customer needs and regulatory requirements. Their strong research and development capabilities enable them to introduce cutting-edge products that enhance vehicle safety and performance.

The increasing adoption of lane keep assist systems in electric vehicles is also expected to drive market growth, as automakers focus on integrating advanced safety features in next-generation EVs. The components segment, including vision

Highlights of TOC:

Chapter 1: Market overview

Chapter 2: Global Lane Keep Assist System Market

Chapter 3: Regional analysis of the Global Lane Keep Assist System Market industry

Chapter 4: Lane Keep Assist System Market segmentation based on types and applications

Chapter 5: Revenue analysis based on types and applications

Chapter 6: Market share

Chapter 7: Competitive Landscape

Chapter 8: Drivers, Restraints, Challenges, and Opportunities

Chapter 9: Gross Margin and Price Analysis

Key takeaways from the Lane Keep Assist System Market report:

Detailed considerate of Lane Keep Assist System Market-particular drivers, Trends, constraints, Restraints, Opportunities and major micro markets.

Comprehensive valuation of all prospects and threat in the

In depth study of industry strategies for growth of the Lane Keep Assist System Market-leading players.

Lane Keep Assist System Market latest innovations and major procedures.

Favorable dip inside Vigorous high-tech and market latest trends remarkable the Market.

Conclusive study about the growth conspiracy of Lane Keep Assist System Market for forthcoming years.

Browse Trending Reports:

Mhealth Solutions Market Telecom Cloud Billing Market Industrial Cooking Fire Protection Systems Market Food Manufacturing Market Natural Surfactant Market Industrial Networking Solutions Market Facility Management Market Cathode Materials Market High Purity Gases Market Cassava Starch Market Embedded Connectivity Solutions Market Central Fill Pharmacy Automation Market Rfid In Healthcare Market Virtual Pipeline Systems Market Fiberoptic Phototherapy Equipment Market Suture Passer Market Baby Apparel Market Peanut Allergy Treatment Market

About Data Bridge Market Research:

Data Bridge set forth itself as an unconventional and neoteric Market research and consulting firm with unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email: [email protected]"

0 notes

Text

IoT Gateway Comprehensive Study with Key Trends, Major Drivers and Challenges

IoT Gateway Market Overview

Global IoT Gateway Market Report 2024 presents critical information and factual data about the IoT Gateway Market, providing an overall statistical study of this market on the basis of market drivers, market limitations, and its future prospects. The widespread IoT Gateway market opportunities and trends are also taken into consideration in the industry. with growth trends, various stakeholders like investors, CEOs, traders, suppliers, research & media, the global manager, director, president, SWOT analysis, i.e., strengths, weaknesses, opportunities, and threats to the organization, and others.

According to Straits Research, the global IoT Gateway market size was valued at USD 1325 Million in 2021. It is projected to reach from USD XX Million in 2022 to USD 4200 Million by 2030, growing at a CAGR of 13.7% during the forecast period (2022–2030).

While studying the IoT Gateway market growth report, we completely studied the driving forces, development trends, restraints, obstacles, and profitable challenges to demonstrate the current and future market environment. Straits Research has given a thorough analysis that includes the key market strategies based on the most recent technologies, applications, and geographies around the world. The industry is predicted to grow significantly during the forecast period because to increased IoT Gateway market demand.

Competitive Landscape

Some of the prominent players operating in the IoT Gateway market are

Microchip Technology Inc.

Cisco Systems Inc

Advantech Co. Ltd

Dell Inc

Hewlett Packard Enterprise Development LP

Huawei Technologies Co. Ltd

Samsara Networks Inc.

and ADLINK Technology Inc.

Eurotech Inc

and Kontron S&T AG.

Get Free Request Sample Report @ https://straitsresearch.com/report/iot-gateway-market/request-sample

The report can help to know the market and strategize for business expansion accordingly. The strategy analysis, gives insights from market positioning and marketing channels to potential growth strategies, providing in-depth analysis for brand new entrants or existing competitors within the industry. Global IoT Gateway Market Report 2024 provides exclusive statistics, data, information, trends, and competitive landscape details during this niche sector.

Global IoT Gateway Market: Segmentation

As a result of the IoT Gateway market segmentation, the market is divided into sub-segments, the following are:

By Component

Processor

Sensor

Memory & Storage Device

Others

By Node

Smart Watch

Camera

RADAR

Thermostat

Actuator

Smart TV

Others

By Connectivity

Bluetooth

WiFi

ZigBee

Ethernet

Cellular

Others

By Deployment Model

On-Premise

Cloud-Based

By End-User

Automotive & Transportation

Healthcare

Industrial

Consumer Electronics

BFSI

Oil & Gas

Retail

Aerospace & Defense

Others

The report forecasts revenue growth at all geographic levels and provides an in-depth analysis of the latest industry trends and development patterns from 2024 to 2032 in each of the segments and sub-segments.

You can check In-depth Segmentation from here: https://straitsresearch.com/report/iot-gateway-market/segmentation

Stay ahead of the competition with our in-depth analysis of the market trends!

Buy Now @ https://straitsresearch.com/buy-now/iot-gateway-market

Key Highlights

The introduction, product type and application, market overview, market analysis by countries, market potential, market risk, and market driving forces are all used to explain the IoT Gateway Market.

Examining the manufacturers of the IoT Gateway Market in terms of their profile, main line of business, news, sales and price, revenue, and market share is the aim of this study.

In order to give a general picture of the competitive environment among the top manufacturers worldwide, including sales, revenue, and market share of IoT Gateway percent

To provide an example of the market segmented by kind and application, together with sales, pricing, revenue, market share, and growth rate for each segment.

To conduct an analysis of the main regions by manufacturers, categories, and applications, covering regions such as North America, Europe, Asia Pacific, the Middle East, and South America, with sales, revenue, and market share segmented by manufacturers, types, and applications.

To investigate the production costs, essential raw materials, production method, etc.

About Straits Research

Straits Research is dedicated to providing businesses with the highest quality market research services. With a team of experienced researchers and analysts, we strive to deliver insightful and actionable data that helps our clients make informed decisions about their industry and market. Our customized approach allows us to tailor our research to each client's specific needs and goals, ensuring that they receive the most relevant and valuable insights.

Contact Us

Email: [email protected]

Address: 825 3rd Avenue, New York, NY, USA, 10022

Tel: +1 6464807505, +44 203 318 2846

#IoT Gateway#IoT Gateway Industry#IoT Gateway Share#IoT Gateway Size#IoT Gateway Trends#IoT Gateway Regional Analysis#IoT Gateway Growth Rate

0 notes

Text

Video Conferencing Market Share, Growth, Forecast And Global Industry Outlook 2024 – 2034

Video Conferencing market Overview:

The Video Conferencing market is predicted to develop at a compound annual growth rate (CAGR) of 7.3%from 2024 to 2034, when it is projected to reach USD 54.76 Billion, based on an average growth pattern. The market is estimated to reach a value of USD 27.07 Billion in 2024.Companies are combining remote and in-person work arrangements, which is why it's necessary to integrate physical and virtual meeting rooms seamlessly. Furthermore, improvements in machine learning (ML) and artificial intelligence (AI) are improving the quality of audio and video, and the widespread use of features like virtual backdrops and real-time language translation is propelling Video Conferencing market expansion. Request Free Sample Copy:

Video Conferencing market Dynamics

Driver: Growing cloud-native enterprises

With the knowledge obtained via direct, in-person interactions with various company divisions, clients, distributors, suppliers, and customers, organizations can effectively manage their operations. Businesses are thus spending more money on cloud services. The market for video conferencing is expected to have a general increase in spending throughout the projected period on cloud conferencing, cloud infrastructure, and business intelligence software. Companies are investing more in cloud-based video services because of the increasing number of participants in the Video Conferencing market, the reduction in travel time and costs, the importance of incorporating staff members in strategic goal-setting, and the increasing demand for virtual meeting rooms.

Increasing preference for remote and elearning is driving the market growth

Conference-calling systems have been implemented by K–12 institutions, companies, and educational institutions to replace traditional classroom instruction with distance learning. As a result of the pandemic, more educational institutions are increasing remote learning by using video communication technologies. Schools are therefore using software to give pupils a good learning environment. Yuja Enterprise Video Technology, for example, teamed with the English-based European School of Osteopathy in January 2023 to use video conferencing technology to disseminate course materials both domestically and internationally. The Source

Key Market Players

Avaya, LLC

Microsoft Corporation

Panasonic Corporation

Huawei Technologies Co. Ltd.

Logitech International S.A.

AVer Information, Inc.

BlueJeans by Verizon

Cisco Systems, Inc

Polycom, Inc.

Zoom Video Communications, Inc.

Others

Video Conferencing market Segments

By Deployment Mode

Cloud-based

On-premise

By Industry

Automotive

Aerospace

Consumer Goods

Electronics

Pharmaceuticals

Others

Opportunity: Boom in video conferencing hardware market

Cisco and Huawei, among other companies, are making significant investments in hardware solutions to solve issues with video conferencing technology, including subpar camera, microphone, and display unit quality. The hardware market includes end-point solutions, telepresence systems, ultra 4K UHD cameras, high-end microphones, and intuitive collaborative whiteboards for smart offices. This small IP-based all-in-one endpoint device features a camera, microphone, and HD codec and is easy to set up and operate. This equipment assists SMEs and large corporations in prioritizing tasks like teamwork in order to create reliable workplaces and increase agility.

Voice over Internet Protocol, or VoIP, is an emerging technology that is driving a change in market trends with the advent of 5G technology. Businesses in industrialized nations like the United States, the United Kingdom, and Germany have created enormous opportunities thanks to this technology. As expanding into new geographic areas and reaching remote areas grow more advantageous, this might potentially transform the game.

Restraint: Network Infrastructure Issues

While most industrialized countries have highly developed communication infrastructure, only a small number of emerging and underdeveloped countries lack the infrastructure needed to transmit high-quality video. People in these countries mostly rely on audio-based communication to escape the frustration of bad video and sporadic disconnections. Video communications require a lot more bandwidth, whereas audio-based communication can operate on infrastructure that has far less capacity. For the video conferencing market, the absence of a robust communication infrastructure is a serious Video Conferencing market growth obstacle.

Video Conferencing Industry: Regional Analysis

North America Market Forecast

North America holds a dominant Video Conferencing market share of over 46% in the video conferencing industry, which generates the largest revenue. High adoption rates across industries, sophisticated digital infrastructure, and substantial investments from big tech companies are the main reasons why the video conferencing business in North America is thriving. Growth is also being fueled by a trend to cloud-based solutions and high disposable income. Its attractiveness in business and educational contexts is increased when video conferencing is combined with collaboration tools.

Europe Market Statistics

The market for video conferences in Europe is bolstered by robust digital transformation programs and regulatory backing, particularly GDPR adherence. While an emphasis on data security addresses privacy concerns, innovation is driven by key market players. Because of the region's concentration on cutting-edge communication technology and digital cooperation, video conferencing is becoming more and more popular for virtual events and meetings.

Frequently Asked Questions

What is the market size of Video Conferencing Market in 2024?

What is the growth rate for the Video Conferencing Market?

Which are the top companies operating within the market?

Which region dominates the Video Conferencing Market?

Conclusion

The growing need for distant communication solutions across a range of industries is expected to propel the market for Video Conferencing market future expansion and innovation. Video conferencing technology use is expected to increase as more businesses realize the advantages of virtual collaboration, including cost savings, flexibility, and increased productivity. Additionally, improvements in augmented reality, artificial intelligence, and interaction with other digital tools will improve functionality and user experiences. Businesses that put an emphasis on scalable solutions, user-friendly interfaces, and security will be in the best position to prosper in this changing industry. Ultimately, in an increasingly digital world, video conferencing promises to revolutionize how we communicate, work together, and do business.

#Video Conferencing Market Share#Video Conferencing Market Demand#Video Conferencing Market Scope#Video Conferencing Market Analysis#Video Conferencing Market Trend

0 notes

Text

Foldable Display Market Size, Share, Growth, Trends and Forecast 2024-2032

Foldable Display: An Overview

Flexible display technologies like OLED and AMOLED have been propelling the market for foldable displays. This is accompanied by increased demand from consumers for multi-use devices that can have a bigger screen size while still being portable. The segment initially began with foldable smartphones but now includes applications in laptops, wearables, tablets, and automotive applications. Innovation leaders: Samsung, Huawei, LG Display, and BOE Technology Group are in pole position in researching and developing higher durability, but at a reasonably lower cost of production. Though production costs are extremely high, and durability is yet to be ideal in use, continuous progress, and growing consumer interest in premium, multifunction devices are expected to propel the folded display market in significant ways for over a decade. The market share holder in this market is Asia-Pacific, due to the powerful manufacturing capacities and because of the increasing adoption of cutting-edge devices, followed by North America and Europe, which also exhibit increasing growth.

According to the Univdatos Market Insights, increasing consumer demand for multi-functional devices, advancements in OLED and AMOLED technology, heavy investments from OEMs, and expansion of 5G networks will drive the global scenario of the Foldable Display market. As per their “Foldable Display Market” report, the global market was valued at USD 4,817.2 Million in 2023, growing at a CAGR of 27.4% during the forecast period from 2024 - 2032.

Request Free Sample Pages with Graphs and Figures Here - https://univdatos.com/get-a-free-sample-form-php/?product_id=67064

Foldable Display Overview in APAC

In terms of geographical split, the largest proportion of the foldable display is dominated by the Asia-Pacific (APAC) region, mainly on account of its status as a global electronics manufacturing hub and innovation center. Flexibilities of a foldable display are further diversified based on its screen curvature, e.g., in terms of convex and concave types. Thus, to cater to the demand for such flexibilities, players of strong manufacturing infrastructures, such as South Korea, China, and Japan, are positioned closely in the APAC region, while major players, including Samsung Display, LG Display, and BOE Technology Group, are headquartered in this region, with the former having been the key developers of flexible OLED and AMOLED technology. This generates strong demand for premium, high-end devices in the countries and has further accelerated due to the widespread adoption of 5G technology. Besides this, the region has developed a strong supply chain and has been working on significant R&D initiatives, making foldable displays a fast-growing area among applications such as smartphones, laptops, and automotive.

Foldable Display Market in China

China is the hub of foldable display innovations and productions; in fact, several major manufacturers are based in China. Companies such as BOE Technology Group, Visionox, and Royole Corporation in China stand atop developing flexible OLED and AMOLED technology. Such companies are not just producing foldable displays for internal markets but also are key suppliers to global manufacturers, so China forms integral parts of the supply chain for foldable devices internationally.

Related Reports-

Smartphone Camera Market: Current Analysis and Forecast (2024-2032)

India Semiconductor Market: Current Analysis and Forecast (2024-2032)

Key Factors Driving China’s Market Leadership:

1. Manufacturing Capacity: China houses the largest and most advanced manufacturing infrastructures for display technologies. Companies like BOE Technology have ramped up their flexible displays' production speed, which they declared to be mass-producible; therefore, this makes the cost of producing them relatively low. It has thus catapulted China to become one of the primary players in the quest by regions to rise and fill the rising global demand for foldable displays.

2. Government Supports: The government of China has been very proactive in the support process towards developing advanced display technologies. Several subsidies, incentives, and other benevolent policies announced by the Chinese government encouraged domestic firms to invest in R&D so that they could compete on the global stage with established players like Samsung.

3. Technological development: For the most part, BOE Technology and Visionox are succeeding in pioneering OLED and AMOLED technologies. There has been exceptional strength improvement, and increased brightness and energy efficiency in flexible displays, thus indicating that these may suit a more wide range of applications like smartphones, laptops, and automotive displays.

4. Domestic Demand: China is currently one of the world's largest consumer electronics markets. With consumers in this country fast moving towards high technology, demand for premium devices has increased rapidly, thus ensuring very high growth in domestic demand for foldable displays. This means that Chinese firms have an already developed market into which they can test and perfect their technologies before spreading them to an international audience.

5. Strategic partnerships: Chinese display companies have forged partnerships with top electronics companies around the world and are supplying foldable display panels to many of the world's leading brands. For example, the world's two biggest phone makers, China's Huawei and Xiaomi, have integrated foldable display technology into their high-end flagship models. China has led the world once again in folding screens.

6. R&D Investment: Chinese companies are highly investing in research and development to improve foldable display technology. This includes improvements in hinge mechanisms, screen resistance, and the reduction of the "crease" that manifests in foldable displays. Companies like Royole Corporation were one of the pioneers in foldable displays, and their innovations keep China at the top of the technological race.

For more information about this report visit- https://univdatos.com/report/foldable-display-market/

Conclusion

In Conclusion, the Asia-Pacific region- especially China-is a leader around the globe in the foldable display market in terms of robust manufacturing capabilities, rapid technological advancement, and consumer demand for innovative devices. The APAC region can be portrayed as having great strength, thanks to the countries leading the front, such as South Korea, China, and Japan, owing to a strong supply chain and healthy R&D investments. Notably, related developments in the Chinese market are of special interest to these trends. Companies like BOE Technology and Royole Corporation have led the charge in flexible OLED and AMOLED technology. Government support, strong domestic demand, and strategic partnerships have furthered the influence of China in the industry by placing it as a key participant in the supply chain of foldable displays globally. As the cost to produce falls and technology increases, there will be growth in both APAC and China's foldable display market, with the remaining firms in the market.

#Foldable Display Market#Foldable Display Market Size#Foldable Display Market Share#Foldable Display Market Growth

0 notes

Text

Surface Inspection Market Dynamics, Driving Factors, and Applications by 2032

Market Scope & Overview

The market research report includes company and product introductions, market status and development trends by type and applications, pricing and profit status, marketing status, market growth factors and challenges, industry forecasts, worldwide major players/suppliers, and regional market share. The purpose of this research is to look at both potential revenue streams and the present market position. The entire market ecology is investigated, including technological advancements, applications and end users, product offers, governmental frameworks, and predicted market growth.

The Surface Inspection Market research report began with definitions, classifications, applications, and market overviews before progressing to product specifications, manufacturing processes, cost structures, and raw materials. Following that, the Surface Inspection market study examined the current condition of the major global markets, including product price, profit, production, supply, demand, market growth rate, and projections, among other things.

Download the Sample Pages of this Report: https://www.snsinsider.com/sample-request/2202

Market Segmentation Analysis

The global Surface Inspection market is divided into segments based on market participants, geographic regions, application kinds, and other criteria. Custom research can be incorporated to meet specific needs of yours. Finally, the report's conclusion section includes remarks from industry experts. A SWOT analysis of the market is included in the research study.

BY COMPONENT:

Frame Grabbers

Lighting Equipment

Software

Cameras

Optics

Processors

Other

BY SYSTEM

Camera-based system

Computer-based system

BY SURFACE TYPE

2D

3D

BY VERTICAL

Semiconductor

Electrical & Electronics

Food & Packaging

Plastic & Rubber

Automotive

Glass & Metal

Healthcare

Printing

Regional Outlook

The Surface Inspection market research study focuses on the world's key regions and countries while extensively examining the most important regional market circumstances. The examination included a SWOT analysis of a new project, an assessment of an investment's viability, and an analysis of the investment return.

Competitive Analysis

The research report provides an in-depth analysis of the Surface Inspection market, as well as information on a variety of industry participants and the competitive landscape, potential threats, and future development prospects. This research study thoroughly examines each company's profile. This area of research covers topics like as capacity, production, revenue, cost, gross margin, sales revenue, consumption, growth rate, supply, future strategies, and technological improvements. The analysis examines market participants, raw material and equipment suppliers, end users, traders, distributors, and other key players.

Major players in the surface inspection market are Teledyne Technologies Incorporated, Allied Vision Technologies, Basler, Cognex Corporation, Sony Corporation, Omron Corporation, Panasonic Corporation, Matrox Electronic Systems, ISRA Vision, Keyence Corporation

Buy Now: https://www.snsinsider.com/checkout/2202

Key Reasons to Buy Surface Inspection Market Report

Investigate the marketing strategies used by the most successful businesses in your field.

Determine the sector's primary motivators and constraints, as well as their impact on the worldwide market.

To comprehend the most significant industry-specific driving and restraining forces, as well as their global ramifications.

Conclusion

Through in-depth market analysis, you will gain a complete understanding of the global market and its commercial landscape. Following a detailed market analysis, the reader will have a firm grasp of the worldwide Surface Inspection market and its business environment.

About Us:

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company’s aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Contact Us:

Akash Anand — Head of Business Development & Strategy

Email: [email protected]

Phone: +1–415–230–0044 (US) | +91–7798602273 (IND)

0 notes

Text

Driving the Future: The Role of an Automotive Components Supplier

The automotive industry is a complex network of manufacturers, designers, engineers, and suppliers. At the heart of this intricate system lies the automotive components supplier, a pivotal player in ensuring the seamless production and functionality of vehicles. These suppliers are responsible for providing the necessary parts that keep the automotive industry moving forward. This article explores the crucial role of an automotive components supplier and highlights the significance of auto component suppliers in the global market.

The Backbone of the Automotive Industry

An automotive components supplier is integral to the manufacturing process of vehicles. They supply a vast array of parts, ranging from simple nuts and bolts to sophisticated electronic systems and engines. These components are essential for the assembly, safety, and performance of vehicles. By providing high-quality parts, automotive components suppliers help manufacturers maintain their production schedules and meet the rigorous standards of the automotive industry.

The Range of Auto Component Suppliers

Auto component suppliers can be categorized into two primary types: original equipment manufacturers (OEMs) and aftermarket suppliers.

Original Equipment Manufacturers (OEMs): OEMs supply parts that are used in the initial assembly of vehicles. These components are designed to meet the specifications and quality standards set by the vehicle manufacturers. OEM parts are crucial for ensuring the reliability and safety of new vehicles. Examples include engines, transmissions, and braking systems.

Aftermarket Suppliers: Aftermarket suppliers provide parts that are used for the maintenance and repair of vehicles after they have left the factory. These components may not be identical to OEM parts but must meet certain standards to ensure compatibility and performance. Examples include replacement headlights, tires, and batteries.

Innovation and Technology in Automotive Components