#algotradingindia

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Average visit duration of Tumblr.com is 10 mins and 25 secs.

Text

Interested in understanding algorithmic trading and its growing adoption in India? I've written a comprehensive blog post discussing the strategies, platforms, and future outlook of algo trading in the Indian context. I analyze the current landscape, regulations, growth prospects, challenges, and opportunities for algorithmic traders in India. If you want to get up to speed on this cutting-edge trading approach that’s gaining significant traction, be sure to check out my post! Let me know what you think - I welcome feedback from fellow trading enthusiasts! Does algorithmic trading have the potential to disrupt Indian markets in the coming years? Share your thoughts after reading my analysis!

0 notes

Text

How does algorithmic trading handle risk management and position sizing?

Algorithmic trading has transformed the financial markets by offering traders the ability to execute trades swiftly and efficiently. However, successful navigation of the market requires robust risk management and position sizing techniques. In this blog post, we will explore key strategies employed in algorithmic trading to effectively manage risk and determine optimal position sizes (How does algorithmic trading handle risk management and position sizing?)

Stop Loss Orders: Safeguarding Your Capital Setting Risk Limits: Defining Boundaries Volatility-Based Position Sizing: Adapting to Market Conditions The Power of Diversification: Spreading Your Risk Evaluating Risk-Adjusted Returns: Measuring Efficiency Monte Carlo Simulations: Gaining Insights into Probability Continuous Monitoring and Adaptation: Staying Ahead of the Curve Conclusion:

Stop Loss Orders: Safeguarding Your Capital

Stop loss orders act as a safety net in algorithmic trading systems, automatically triggering an exit when a predefined price level is reached. Discover how these orders protect against excessive losses and ensure capital preservation.

Setting Risk Limits: Defining Boundaries

Establishing risk limits is essential to maintaining control over trading activities. Learn how to define maximum loss per trade or portfolio exposure, setting clear boundaries for risk-taking within your algorithmic trading system.

Volatility-Based Position Sizing: Adapting to Market Conditions

Volatility is an inherent characteristic of financial markets. Explore how algorithmic traders adjust position sizes based on market volatility, enabling consistent risk exposure across various instruments and market environments.

The Power of Diversification: Spreading Your Risk

Diversification is a fundamental risk management technique. Understand how algorithmic trading strategies leverage portfolio diversification to mitigate the impact of individual trades or market events, promoting a more stable trading approach.

Evaluating Risk-Adjusted Returns: Measuring Efficiency

Assessing the performance of an algorithmic trading system goes beyond measuring returns. Discover how risk-adjusted metrics, such as the Sharpe ratio, provide a comprehensive assessment of a strategy's efficiency in managing risk relative to its returns.

Monte Carlo Simulations: Gaining Insights into Probability

Explore the world of Monte Carlo simulations and their application in algorithmic trading. Learn how these simulations help traders evaluate the potential risk and return characteristics of their strategies by simulating thousands of market scenarios.

Continuous Monitoring and Adaptation: Staying Ahead of the Curve

Effective risk management and position sizing require constant monitoring and updates. Uncover the importance of regularly reviewing and adjusting risk parameters and position sizing rules to adapt to changing market conditions and new information.

Conclusion:

Mastering risk management and position sizing is paramount for success in algorithmic trading. By implementing stop loss orders, defining risk limits, adapting to market volatility, diversifying portfolios, evaluating risk-adjusted returns, leveraging Monte Carlo simulations, and maintaining continuous monitoring, traders can navigate the markets with confidence and efficiency. Harness the power of these strategies to enhance your algorithmic trading endeavors and achieve sustainable results. Remember, effective risk management and position sizing are integral components of a well-designed algorithmic trading system, ensuring the preservation of capital and the optimization of trading performance. Read the full article

#Backtesting#HighFrequencyTrading#MachineLearning#MarketSentimentAnalysis#MeanReversion#Optimization#RiskManagement#StatisticalArbitrage#TrendFollowing#algotradingindia

0 notes

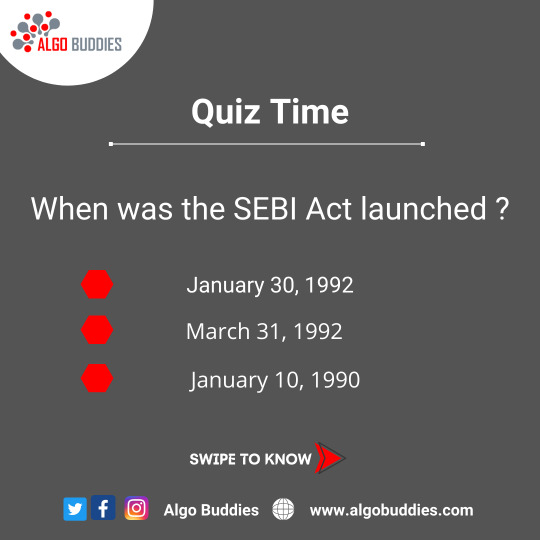

Photo

Securities and Exchange Board of India (SEBI) was first established in 1988 as a non-statutory body for regulating the securities market. It became an autonomous body on 30 January 1992 and was accorded statutory powers with the passing of the SEBI Act 1992 by the Indian Parliament.

→ Visit our website To know more - https://www.algobuddies.com/

Book your free Algo trading demo now.

0 notes

Text

What is high-frequency trading (HFT) and how does it work?

High-frequency trading (HFT) is a type of algorithmic trading that relies on powerful computers to execute trades at lightning-fast speeds. HFT firms use complex algorithms and high-speed data analysis to identify patterns in the market and make split-second trading decisions.What is high-frequency trading (HFT) and how does it work? In recent years, HFT has become increasingly popular among institutional investors and hedge funds. Proponents argue that HFT provides liquidity to the market, reduces bid-ask spreads, and improves price efficiency. However, critics raise concerns about market manipulation and unfair advantages for large firms.

What is high-frequency trading (HFT) and how does it work? How HFT Works Benefits of HFT Controversies Surrounding HFT Conclusion

How HFT Works

At its core, HFT involves using powerful computers and algorithms to analyze vast amounts of market data and execute trades at lightning-fast speeds. HFT firms rely on low-latency networks and co-location services to minimize the time it takes for their orders to reach the exchange. HFT algorithms can be divided into two main categories: market making and directional trading. Market-making algorithms aim to provide liquidity to the market by placing bids and offers at different price levels. Directional trading algorithms, on the other hand, aim to profit from market movements by buying or selling securities based on predictive models.

Benefits of HFT

Proponents of HFT argue that it provides several benefits to the market, including increased liquidity, reduced bid-ask spreads, and improved price efficiency. According to a study by the European Central Bank, HFT has also been shown to improve market quality by reducing volatility and increasing market depth. In addition, HFT can provide significant cost savings for investors by reducing trading costs and improving execution quality. For example, a study by the Tabb Group found that HFT can save investors up to $1.8 billion per year in trading costs.

Controversies Surrounding HFT

Critics of HFT raise several concerns, including market manipulation, unfair advantages for large firms, and increased systemic risk. Some argue that HFT firms use their speed and technology to front-run slower traders and manipulate prices in their favor. Others point to instances where HFT algorithms have contributed to market crashes and flash crashes. Despite these criticisms, defenders of HFT argue that it provides valuable liquidity to the market and improves price efficiency. They also point out that many of the concerns about HFT can be addressed through better regulation and oversight.

Conclusion

In conclusion, HFT is a type of algorithmic trading that relies on powerful computers and high-speed data analysis to execute trades at lightning-fast speeds. While HFT has been criticized for its potential to manipulate markets and create systemic risk, it also provides valuable liquidity and cost savings for investors. As HFT continues to evolve and grow, it will be important for regulators and market participants to carefully monitor its impact and ensure that it operates in a fair and transparent manner. With the right regulations and oversight, HFT can continue to provide benefits to the market while minimizing the risks associated with high-speed trading. Read the full article

#Backtesting#HighFrequencyTrading#MachineLearning#MarketSentimentAnalysis#MeanReversion#Optimization#RiskManagement#StatisticalArbitrage#TrendFollowing#algotradingindia

0 notes

Text

What types of data are used in algorithmic trading?

Algorithmic trading has become increasingly popular in recent years, as advancements in technology have made it possible to analyze large amounts of data in real-time. At the heart of algorithmic trading is data - without it, traders would not be able to make informed decisions about when to buy or sell assets What types of data are used in algorithmic trading? In this presentation, we will explore the different types of data used in algorithmic trading and their importance in this field.

Market Data Fundamental Data Alternative Data Machine Learning and AI Conclusion

Market Data

Market data refers to information about the current state of financial markets, including prices, volume, and other relevant metrics. This type of data is crucial for algorithmic traders, as it allows them to identify patterns and trends that can be used to make profitable trades. Examples of market data include stock prices, exchange rates, and commodity prices. By analyzing this data in real-time, algorithmic traders can quickly make decisions about when to buy or sell assets, based on current market conditions.

Fundamental Data

Fundamental data refers to information about the underlying health of a company or asset, such as earnings reports, balance sheets, and other financial statements. This type of data is important for algorithmic traders who use fundamental analysis to make investment decisions. By analyzing fundamental data, traders can gain insight into the long-term prospects of a company or asset, which can help them make more informed decisions about when to buy or sell. For example, if a company's earnings report shows strong growth potential, algorithmic traders may choose to buy shares in that company, anticipating future gains.

Alternative Data

Alternative data refers to non-traditional sources of information that can be used to gain insight into market trends and consumer behavior. This type of data is becoming increasingly important in algorithmic trading, as traders look for new ways to gain a competitive edge. Examples of alternative data sources include social media sentiment analysis, satellite imagery, and credit card transaction data. By analyzing this data alongside traditional market and fundamental data, algorithmic traders can identify patterns and trends that may not be immediately apparent, allowing them to make more profitable trades.

Machine Learning and AI

Machine learning and AI are playing an increasingly important role in algorithmic trading, as these technologies allow traders to analyze and interpret vast amounts of data in real-time. By using machine learning algorithms, traders can identify patterns and trends that may not be immediately apparent to human analysts. For example, machine learning algorithms can be trained to identify correlations between different types of data, allowing traders to make more informed decisions about when to buy or sell assets. Additionally, AI-powered chatbots can be used to interact with customers and provide personalized investment advice, based on their individual needs and preferences.

Conclusion

In conclusion, data is at the heart of algorithmic trading, and traders who are able to effectively analyze and interpret this data are more likely to make profitable trades. By using a combination of market, fundamental, and alternative data sources, along with machine learning and AI technologies, algorithmic traders can gain a competitive edge in today's fast-paced financial markets. We encourage you to continue exploring the fascinating world of algorithmic trading and the role that data plays in this field. Read the full article

#Backtesting#HighFrequencyTrading#MachineLearning#MarketSentimentAnalysis#MeanReversion#Optimization#RiskManagement#StatisticalArbitrage#TrendFollowing#algotradingindia

0 notes

Text

What is the basic concept behind statistical arbitrage in trading?

The basic concept behind statistical arbitrage in trading is to identify and exploit pricing inefficiencies or temporary deviations from expected patterns in financial markets. Statistical arbitrage relies on the use of quantitative models and statistical analysis to identify these discrepancies. The underlying principle is that certain financial assets or securities tend to move in a correlated manner over time. Statistical arbitrage traders search for pairs or groups of assets that have historically exhibited a strong correlation. When the correlation between these assets deviates from its historical pattern, it creates an opportunity for profit. Statistical arbitrage traders use statistical models and algorithms to analyze historical data, identify patterns, and estimate the expected relationship between the assets. They look for instances where the actual relationship diverges from the expected relationship, signaling a potential opportunity for arbitrage. Once a statistical arbitrage opportunity is identified, traders typically take two positions: a long position in the asset that appears undervalued and a short position in the asset that appears overvalued. By balancing these positions, traders aim to profit from the convergence of prices back to their expected relationship. Statistical arbitrage strategies often involve a high volume of trades executed with speed and precision, as the pricing discrepancies tend to be short-lived. Traders rely on advanced statistical modeling, algorithmic execution, and risk management techniques to implement these strategies effectively. It's important to note that statistical arbitrage strategies carry risks, and successful implementation requires continuous monitoring, adjustments to models, and diligent risk management Lets see What is the basic concept behind statistical arbitrage in trading?

Introduction

Welcome to the world of statistical arbitrage in trading. Statistical arbitrage is a popular trading strategy that uses mathematical models to identify and exploit market inefficiencies. It has become increasingly popular in recent years as traders seek new ways to gain an edge in the competitive world of finance. In this presentation, we will explore the basic concept behind statistical arbitrage, how it works, its benefits, and potential risks. By the end of this presentation, you will have a clear understanding of statistical arbitrage and its relevance in trading.

What is Statistical Arbitrage?

Statistical arbitrage is a trading strategy that seeks to profit from pricing inefficiencies in financial markets. It involves using mathematical models to identify mispricings between related securities, such as stocks and their derivatives. The idea behind statistical arbitrage is that if two securities are related, then their prices should move together over time. For example, if two stocks in the same industry have historically moved in tandem but one stock suddenly experiences a price drop while the other remains stable, a statistical arbitrageur may buy the undervalued stock while simultaneously shorting the overvalued stock. This allows them to profit from the expected convergence of the two stock prices.

How Does Statistical Arbitrage Work?

Statistical arbitrage works by identifying pairs of securities that are related and calculating a statistical measure of the historical relationship between them, such as the correlation coefficient. The arbitrageur then looks for deviations from this historical relationship and takes positions in the securities to profit from their expected convergence. One key advantage of statistical arbitrage is that it can be used in both bullish and bearish markets. Unlike traditional long-only strategies, statistical arbitrageurs can profit from market downturns by shorting overvalued securities while simultaneously buying undervalued securities.

Benefits of Statistical Arbitrage

Statistical arbitrage has several benefits for traders. First and foremost, it allows traders to exploit market inefficiencies and generate profits that would not be possible with traditional trading strategies. Additionally, statistical arbitrage can provide diversification benefits by allowing traders to take positions in multiple securities across different industries and asset classes. Furthermore, statistical arbitrage can be automated using computer algorithms, which can execute trades faster and more efficiently than human traders. This can lead to lower transaction costs and higher returns.

Potential Risks of Statistical Arbitrage

While statistical arbitrage can be a profitable trading strategy, it is not without risks. One major risk is model risk, which refers to the possibility that the mathematical models used to identify mispricings may be flawed or inaccurate. Additionally, statistical arbitrage strategies can be highly sensitive to market volatility and liquidity, which can lead to unexpected losses. To mitigate these risks, statistical arbitrageurs need to constantly monitor their models and adjust their positions as necessary. They also need to have a deep understanding of the markets they are trading in and be able to quickly adapt to changing market conditions.

Conclusion

Statistical arbitrage is a powerful trading strategy that has become increasingly popular in recent years. By using mathematical models to identify and exploit market inefficiencies, traders can generate profits that would not be possible with traditional trading strategies. However, like all trading strategies, statistical arbitrage is not without risks. In conclusion, we hope this presentation has provided you with a clear understanding of statistical arbitrage and its relevance in trading. We encourage you to continue learning about this fascinating topic and explore how it can be applied in your own trading strategies.

Read the full article

0 notes