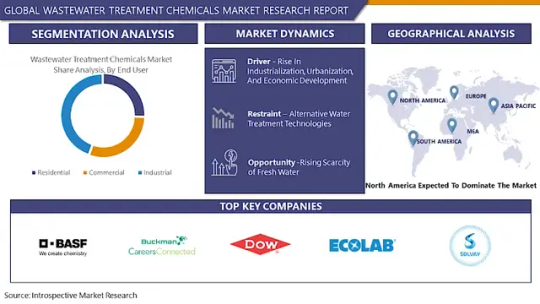

#Wastewater Treatment Chemicals Market Analysis 2023

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Users from the US are the majority of Tumblr visitors.

Text

Wastewater Treatment Chemicals Market: Global Industry Analysis and Forecast 2023 – 2030

The Global Market for Wastewater Treatment Chemicals Estimated at USD 13.48 Billion In the Year 2022, Is Projected To Reach A Revised Size Of USD 22.31 Billion By 2030, Growing At A CAGR Of 6.5% Over The Forecast Period 2023-2030.

The wastewater treatment chemicals market plays a pivotal role in addressing the global water crisis by facilitating the purification of wastewater before its safe discharge into the environment. With rapid industrialization, urbanization, and increasing environmental regulations worldwide, the demand for effective wastewater treatment solutions continues to escalate. Wastewater treatment chemicals encompass a diverse range of products including coagulants, flocculants, disinfectants, pH adjusters, and others, each serving a specific purpose in the treatment process. Industries such as municipal, industrial manufacturing, oil & gas, and pharmaceuticals heavily rely on these chemicals to ensure compliance with environmental standards and mitigate pollution risks.

Get Full PDF Sample Copy of Report: (Including Full TOC, List of Tables & Figures, Chart) @

https://introspectivemarketresearch.com/request/16614

Updated Version 2024 is available our Sample Report May Includes the:

Scope For 2024

Brief Introduction to the research report.

Table of Contents (Scope covered as a part of the study)

Top players in the market

Research framework (structure of the report)

Research methodology adopted by Worldwide Market Reports

Moreover, the report includes significant chapters such as Patent Analysis, Regulatory Framework, Technology Roadmap, BCG Matrix, Heat Map Analysis, Price Trend Analysis, and Investment Analysis which help to understand the market direction and movement in the current and upcoming years.

Leading players involved in the Wastewater Treatment Chemicals Market include:

BASF SE (Germany), Ecolab (U.S.), Solenis (U.S.), Kemira Oyj (Finland), Baker Hughes (Germany), The Dow Chemical Company (U.S.), Cortec Corporation (U.S.), Buckman (U.S.), Solvay S.A (Belgium), Kurita Water Industries (Japan), Veolia (France), Somicon ME FZC (UAE), Toray Industries, Inc. (India), Daiki Axis (India), and Other Major Players

If You Have Any Query Wastewater Treatment Chemicals Market Report, Visit:

https://introspectivemarketresearch.com/inquiry/16614

Segmentation of Wastewater Treatment Chemicals Market:

By Type

Coagulants & Flocculants

Corrosion & Scale Inhibitors

Chelating Agents

Biocides & Disinfects

By End-User

Residential

Commercial

Industrial

By Regions: -

North America (US, Canada, Mexico)

Eastern Europe (Bulgaria, The Czech Republic, Hungary, Poland, Romania, Rest of Eastern Europe)

Western Europe (Germany, UK, France, Netherlands, Italy, Russia, Spain, Rest of Western Europe)

Asia Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Vietnam, The Philippines, Australia, New Zealand, Rest of APAC)

Middle East & Africa (Turkey, Bahrain, Kuwait, Saudi Arabia, Qatar, UAE, Israel, South Africa)

South America (Brazil, Argentina, Rest of SA)

What to Expect in Our Report?

(1) A complete section of the Wastewater Treatment Chemicals market report is dedicated for market dynamics, which include influence factors, market drivers, challenges, opportunities, and trends.

(2) Another broad section of the research study is reserved for regional analysis of the Wastewater Treatment Chemicals market where important regions and countries are assessed for their growth potential, consumption, market share, and other vital factors indicating their market growth.

(3) Players can use the competitive analysis provided in the report to build new strategies or fine-tune their existing ones to rise above market challenges and increase their share of the Wastewater Treatment Chemicals market.

(4) The report also discusses competitive situation and trends and sheds light on company expansions and merger and acquisition taking place in the Wastewater Treatment Chemicals market. Moreover, it brings to light the market concentration rate and market shares of top three and five players.

(5) Readers are provided with findings and conclusion of the research study provided in the Wastewater Treatment Chemicals Market report.

Our study encompasses major growth determinants and drivers, along with extensive segmentation areas. Through in-depth analysis of supply and sales channels, including upstream and downstream fundamentals, we present a complete market ecosystem.

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

Acquire This Reports: -

https://introspectivemarketresearch.com/checkout/?user=1&_sid=16614

About us:

Introspective Market Research (introspectivemarketresearch.com) is a visionary research consulting firm dedicated to assisting our clients to grow and have a successful impact on the market. Our team at IMR is ready to assist our clients to flourish their business by offering strategies to gain success and monopoly in their respective fields. We are a global market research company, that specializes in using big data and advanced analytics to show the bigger picture of the market trends. We help our clients to think differently and build better tomorrow for all of us. We are a technology-driven research company, we analyse extremely large sets of data to discover deeper insights and provide conclusive consulting. We not only provide intelligence solutions, but we help our clients in how they can achieve their goals.

Contact us:

Introspective Market Research

3001 S King Drive,

Chicago, Illinois

60616 USA

Ph no: +1-773-382-1047

Email: [email protected]

#Wastewater Treatment Chemicals#Wastewater Treatment Chemicals Market#Wastewater Treatment Chemicals Market Size#Wastewater Treatment Chemicals Market Share#Wastewater Treatment Chemicals Market Growth#Wastewater Treatment Chemicals Market Trend#Wastewater Treatment Chemicals Market segment#Wastewater Treatment Chemicals Market Opportunity#Wastewater Treatment Chemicals Market Analysis 2023

0 notes

Text

Water Quality Sensor Market

Water Quality Sensor Market Size, Share, Trends: Xylem Inc. Leads

Integration of the Internet of Things (IoT) and Artificial Intelligence in Water Quality Monitoring Systems

Market Overview:

The global Water Quality Sensor Market is estimated to grow at a XX% CAGR between 2024 and 2031. The market will increase from USD XX billion in 2024 to USD YY billion in 2031. Asia-Pacific currently leads the sector, accounting for the great majority of global sales. Rising worries about water contamination, tougher environmental regulations, and growing usage of smart water management systems are among the key metrics.

The water quality sensor market is quickly expanding due to rising demand for continuous water quality monitoring in a wide range of industries, including municipal water treatment, industrial operations, and environmental monitoring. Water quality sensors are finding new applications in a wide range of industries as technology improves sensor accuracy, durability, and connectivity.

DOWNLOAD FREE SAMPLE

Market Trends:

The water quality sensor market is undergoing a significant change towards the integration of Internet of Things (IoT) and artificial intelligence (AI) technologies. These current technologies enhance the capabilities of water quality monitoring systems by enabling real-time data collection, analysis, and predictive maintenance. IoT-enabled sensors can continuously communicate water quality readings to central monitoring stations, allowing for early detection of anomalies and rapid response to possible pollution.

AI algorithms are being used to evaluate large datasets, identify patterns, and forecast water quality trends, potentially improving the efficiency of water treatment operations and resource management. Machine learning models, for example, can forecast algal blooms or equipment malfunctions based on historical data and current sensor inputs. This growth is driven by the rising need for smart water management systems in metropolitan areas, as well as the need for more proactive ways of water quality control. Major water technology companies are making significant investments in IoT and AI capabilities, ushering in a new era of intelligent water quality monitoring systems with increased functionality and decision-support features.

Market Segmentation:

The pH sensor sector holds the largest market share in the water quality sensor industry. pH is an important parameter in water quality monitoring since it regulates many chemical and biological activities. The popularity of pH readings in industries ranging from water treatment to aquaculture has led to the widespread adoption of pH sensors.

Recent developments in pH sensor technology have bolstered its market leadership. For example, the development of solid-state pH sensors with enhanced endurance and minimal drift has expanded their usefulness in demanding industrial applications. A study published in the journal Water Research discovered that newer pH sensors have a 50% longer working lifespan and 30% higher accuracy than older glass electrode sensors.

The pH sensor market is experiencing significant expansion in the industrial application category. According to an International Water Association survey, the use of online pH sensors in industrial wastewater treatment increased by 35% from 2020 to 2023. These sensors are extremely valuable in process control applications because they maintain optimal conditions for chemical reactions and effluent compliance.

Market Key Players:

Xylem Inc.

Hach Company (Danaher Corporation)

Thermo Fisher Scientific Inc.

Endress+Hauser AG

Yokogawa Electric Corporation

ABB Ltd.

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

Centrifugal Pump Market: Role in Industrial, Water, and Wastewater Applications

Centrifugal Pump Market size was valued at USD 40.12 billion in 2023 and is expected to grow to USD 60.18 billion by 2031 and grow at a CAGR of 5.2% over the forecast period of 2024–2031.

Centrifugal pumps are mechanical devices designed to move fluids through a system by converting rotational energy from a motor to hydrodynamic energy. With their simple design and robust construction, these pumps are widely used in numerous applications, including water supply, irrigation, chemical processing, and more. The centrifugal pump market is characterized by rapid technological advancements, which enhance pump efficiency, energy consumption, and operational reliability.

Factors such as urbanization, industrialization, and infrastructure development are driving the demand for centrifugal pumps globally. Moreover, the increasing focus on energy-efficient solutions is prompting manufacturers to innovate, further fueling market growth.

Key Market Drivers

Rising Demand in Water and Wastewater Treatment: The need for efficient water management and wastewater treatment solutions is driving the adoption of centrifugal pumps in municipal and industrial applications.

Growing Oil and Gas Sector: With the expansion of oil and gas exploration and production activities, centrifugal pumps are increasingly utilized for transporting crude oil, natural gas, and other fluids.

Industrialization and Infrastructure Development: Rapid industrial growth and infrastructure projects in emerging economies are boosting the need for reliable fluid handling systems.

Technological Innovations: Advancements in pump design and materials are enhancing the performance, efficiency, and lifespan of centrifugal pumps, attracting more users across various industries.

Focus on Energy Efficiency: Increasing energy costs and environmental regulations are driving the demand for energy-efficient centrifugal pumps, prompting manufacturers to develop innovative solutions.

Market Segmentation

The centrifugal pump market is segmented by flow, operation type, stage, end-user, and region.

By Flow Type

Axial Flow: These pumps move fluid along the axis of the pump, making them suitable for high flow rates with low pressure.

Radial Flow: Radial flow pumps direct fluid radially outward from the center, typically used for high-pressure applications.

Mixed Flow: Mixed flow pumps combine elements of axial and radial flow, offering versatility for various applications.

By Operation Type

Hydraulic: These pumps operate using fluid pressure, commonly found in various industrial applications.

Electrical: Electric-driven centrifugal pumps are widely used for their efficiency and reliability in transporting fluids.

Air-Driven: Air-operated pumps are ideal for applications requiring portability and versatility.

By Stage

Single-Stage: Single-stage pumps are used for low-pressure applications and are simpler in design and maintenance.

Multi-Stage: Multi-stage pumps are utilized for high-pressure applications and can handle greater fluid movement.

By End-User

Commercial: Used in HVAC systems, water supply, and other commercial applications.

Residential: Centrifugal pumps for household water supply and irrigation.

Agricultural: Employed for irrigation, drainage, and water supply in agricultural applications.

Industrial:

Water & Wastewater: Essential for municipal and industrial water treatment processes.

Oil & Gas: Used in upstream and downstream operations for fluid transport.

Power Generation: Critical for cooling and fluid management in power plants.

Mining: Used for dewatering and transporting slurries.

Chemical: Essential for transporting chemicals in processing plants.

Food & Beverage: Employed in food processing for transferring liquids.

Regional Analysis

North America: The U.S. and Canada are key markets due to established industrial infrastructure and investments in water treatment and energy sectors.

Europe: Growth in the European market is driven by stringent environmental regulations and investments in water and wastewater management systems.

Asia-Pacific: Rapid industrialization, urbanization, and infrastructure development in countries like China, India, and Japan are fueling market growth in this region.

Latin America: Emerging economies are investing in infrastructure projects, increasing the demand for centrifugal pumps.

Middle East & Africa: The region’s oil and gas sector is driving the need for centrifugal pumps, alongside increasing efforts in water desalination and treatment.

Current Market Trends

Focus on Smart Pump Solutions: Integration of IoT and smart technologies in centrifugal pumps is enhancing monitoring and control capabilities.

Sustainability Initiatives: Growing emphasis on sustainable practices is leading to the development of eco-friendly pumps with lower energy consumption.

Expansion of Aftermarket Services: Companies are focusing on providing maintenance and repair services to extend the life cycle of centrifugal pumps.

Increased Automation in Industrial Applications: Automation in manufacturing processes is driving the demand for efficient and reliable centrifugal pumps.

Customization and Modular Designs: Manufacturers are offering customizable solutions to meet specific customer needs in various industries.

Conclusion

The global centrifugal pump market is expected to experience robust growth over the forecast period, driven by diverse applications, technological advancements, and increasing demand for efficient fluid handling solutions. As industries seek sustainable and reliable pumping systems, centrifugal pumps will play a crucial role in facilitating fluid transport and management across various sectors.

Key Players

Wilo Group

GRUNDFOS

KSB Company

Flowrox

Sulzer

Xylem

The Weir Group PLC

Flowserve Corporation

Ebara Corporation

Kirloskar Brothers Limited

Dover Corporation

ITT Corporation

Read Complete Report Details of Centrifugal Pump Market: https://www.snsinsider.com/reports/centrifugal-pump-market-2909

About Us:

SNS Insider is a global leader in market research and consulting, shaping the future of the industry. Our mission is to empower clients with the insights they need to thrive in dynamic environments. Utilizing advanced methodologies such as surveys, video interviews, and focus groups, we provide up-to-date, accurate market intelligence and consumer insights, ensuring you make confident, informed decisions.

Contact Us: Akash Anand — Head of Business Development & Strategy [email protected] Phone: +1–415–230–0044 (US) | +91–7798602273 (IND)

0 notes

Text

Exploring Regional Segments in the Activated Carbon Market: Trends and Analysis

The global activated carbon market was valued at USD 4.92 billion in 2023 and is expected to expand at a compound annual growth rate (CAGR) of 6.0% from 2024 to 2030. Activated carbon plays a crucial role in purifying liquids and gases across a broad spectrum of end-use applications. These include municipal drinking water treatment, food and beverage processing, automotive industries, and many others. The growing demand for activated carbon in these applications can be attributed to its numerous advantageous properties, such as cost-effectiveness, its ability to remove bad tastes, color stability, and its efficient odor removal capabilities.

One of the most important applications of activated carbon is in water treatment. Activated carbon is effective in removing a wide range of contaminants, including chlorine, pesticides, heavy metals, and industrial chemicals from both drinking water and wastewater. The primary mechanism by which activated carbon works is adsorption—the process by which contaminants adhere to the surface of the carbon material. This makes activated carbon particularly effective in eliminating impurities from water, improving its taste, odor, and overall safety.

The use of activated carbon in water treatment processes is essential in many regions, especially where water contamination is a significant issue due to industrial pollution or agricultural runoff. As the global population continues to grow and as water scarcity becomes a more pressing concern in many parts of the world, the need for efficient and cost-effective water treatment solutions, such as activated carbon filtration, is expected to increase.

Gather more insights about the market drivers, restrains and growth of the Activated Carbon Market

Regional Insights

North America:

North America, particularly the United States, is marked by strict regulations on air and water pollution, which significantly influence the demand for activated carbon. Activated carbon is highly effective in removing harmful contaminants from both air and water, making it an essential material for complying with environmental standards. Regulatory agencies in the U.S. and Canada have increasingly recommended the use of activated carbon for impurity removal in water and air treatment systems to meet stringent pollution control measures.

US:

In the U.S., public drinking water systems, which are regulated by the U.S. Environmental Protection Agency (EPA), supply water to approximately 90% of the population. There are over 155,000 public water systems in the country, with around 82% of the population relying on these systems. The U.S. government has set stringent regulations to monitor the disposal and treatment of wastewater, driving the demand for activated carbon in water treatment applications. With these regulations in place, the market for activated carbon in the U.S. is expected to grow steadily, particularly in municipal and industrial water treatment sectors.

Europe:

In Europe, the demand for activated carbon has surged due to growing awareness about pollution hazards, the tightening of environmental regulations, and increased demand from the manufacturing sector. The food and beverage industry, in particular, has contributed significantly to the regional market, as activated carbon is commonly used for purifying water and air in various industrial processes.

Germany:

Germany, as one of the leading economies in Europe, is witnessing substantial growth in its activated carbon market. The food and beverage processing sector, particularly the production of beverages such as beer, soft drinks, and wine, is one of the major drivers. Germany, along with the UK, Poland, and Spain, is a key producer of beer in Europe, and the increasing consumption of beer and other beverages is expected to significantly fuel the demand for activated carbon. This market growth is further supported by Germany’s ongoing commitment to environmental sustainability and regulatory compliance, driving the need for efficient air and water treatment solutions.

Asia Pacific:

The Asia Pacific region is a major consumer of activated carbon, holding a dominant revenue share of 49.7% in 2023. The region’s significant consumption can be attributed to the widespread use of coconut-based activated carbon in countries like Indonesia, India, and Sri Lanka, where coconut cultivation is prevalent. The demand for activated carbon in these countries is growing due to increasing air and water pollution, along with the rising focus on water purification and air filtration solutions.

China:

China’s activated carbon market has been experiencing steady growth, driven by a growing demand for air purification systems. As air quality concerns continue to rise, particularly in urban areas with high levels of industrial emissions and vehicular pollution, the need for activated carbon has surged. This demand is primarily fueled by the widespread use of activated carbon in air purifiers and filtration systems, both in residential and commercial sectors.

Central & South America:

Central and South America are emerging markets for activated carbon, with a strong projected growth trajectory during the forecast period. Countries like Brazil and Argentina are investing in new technologies for air and water treatment, which is expected to fuel the demand for activated carbon. The ongoing push for environmental sustainability and improved water management systems is encouraging the use of activated carbon in these regions.

Argentina:

In Argentina, the activated carbon market is expected to see significant growth, particularly in the use of granular activated carbon (GAC) and powdered activated carbon (PAC) in water treatment applications. The country's Integrated Urban Water Management initiative, which aims to enhance water quality control across urban areas, is set to drive demand for activated carbon. The initiative focuses on using advanced technologies to improve water management, and activated carbon plays a key role in purifying water supplies.

Middle East & Africa:

The Middle East & Africa region presents a significant opportunity for the activated carbon market. The region’s increasing concern about water sanitation, health, and hygiene is contributing to the growing demand for activated carbon in both air and water purification applications. The region is investing heavily in industrial, residential, and commercial air purification systems, where activated carbon is a crucial component due to its high efficiency in filtering harmful pollutants.

Saudi Arabia:

Saudi Arabia’s activated carbon market is experiencing considerable growth, driven by the country’s water scarcity issues. Saudi Arabia is the third-largest consumer of water in the world, following the U.S., and this has led to an increased demand for water treatment and purification solutions. The country’s National Water Company (Qatrah) has highlighted the urgency of water conservation and reuse, which further boosts the demand for activated carbon in water treatment applications. In both urban and rural areas, the demand for water reuse and advanced purification technologies is expected to increase, making activated carbon a vital material for addressing the country’s water challenges.

Browse through Grand View Research's Category Petrochemicals Industry Research Reports.

The global biolubricants market size was valued at USD 2.95 billion in 2024 and is projected to grow at a CAGR of 13.7% from 2025 to 2030.

The global biofertilizers market sizewas estimated at USD 1.38 billion in 2024 and is projected to grow at a CAGR of 12.8% from 2025 to 2030.

Key Companies & Market Share Insights

The activated carbon market is characterized by the presence of several key players that operate across different segments, including product development, research and development (R&D), and global distribution. Some of the leading companies in this market include Kuraray Co., Ltd., Jacobi Carbons Group, and Osaka Gas Chemicals Co., Ltd., among others.

Key Players in the Activated Carbon Market:

Kuraray Co., Ltd. Kuraray Co., Ltd., a Japan-based multinational, is a significant player in the activated carbon market. In addition to its activated carbon products, the company offers a wide range of other products, which are categorized under several business segments including plastics and polymers, fibers and textiles, chemicals, elastomers and rubber, engineering, and medical and environmental products. Kuraray has a research and development (R&D) division with two key centers located in Kurashiki and Tsukuba, Japan. These centers focus on advancing product development, improving existing products, and enhancing manufacturing processes to meet global market demands. With a strong global presence, Kuraray has operations and offices in key international markets, including the U.S., Germany, Belgium, China, Korea, Hong Kong, and India. This extensive network allows the company to serve a broad customer base across various industries, including water treatment, air purification, industrial processes, and medical applications.

Osaka Gas Chemicals Co., Ltd. Osaka Gas Chemicals Co., Ltd., also based in Japan, operates through two primary business segments: advanced material solutions and absorption & separation solutions. The company's product range includes fine chemical materials, surface processing agents, resin additives, wood preservatives, industrial preservatives, and activated carbon. The activated carbon products from Osaka Gas Chemicals are marketed under the brand name Shirasagi, a well-established name in the activated carbon market. Osaka Gas Chemicals also has a strong emphasis on product development, supported by its Product Development Center and a Technology Center located in Nara, Japan. These centers play a critical role in driving the company's innovation in activated carbon and other related chemical products. Furthermore, the company operates a distribution center in Osaka, ensuring efficient logistics and timely delivery of its products to customers across various regions. Osaka Gas Chemicals’ focus on quality and technological innovation has positioned it as a key player in the activated carbon industry.

Jacobi Carbons Group While not specifically detailed here, Jacobi Carbons Group is a global leader in the activated carbon market. Known for its vast range of activated carbon products, Jacobi Carbons specializes in solutions for air and water purification, industrial processes, gold recovery, and environmental cleanup. The company operates with a strong focus on sustainability and innovation, offering a comprehensive range of services, including activated carbon filtration systems, regeneration services, and technical support to its customers across multiple industries.

Key Activated Carbon Companies:

The following are the leading companies in the activated carbon market. These companies collectively hold the largest market share and dictate industry trends.

CarbPure Technologies

Boyce Carbon

Cabot Corporation

Kuraray Co.

CarboTech AC GmbH

Donau Chemie AG

Haycarb (Pvt) Ltd.

Jacobi Carbons Group

Kureha Corporation

Osaka Gas Chemicals Co., Ltd.

Evoqua Water Technologies LLC

Carbon Activated Corporation

Hangzhou Nature Technology Co., Ltd.

CarbUSA

Sorbent JSC

Order a free sample PDF of the Market Intelligence Study, published by Grand View Research.

0 notes

Text

Asia Pacific Water and Wastewater Treatment Market Analysis, 2023-2030

BlueWeave Consulting, a leading strategic consulting and market research firm, in its recent study, estimated Asia Pacific Water and Wastewater Treatment Market size by value at USD 151.78 billion in 2023. During the forecast period between 2024 and 2030, BlueWeave expects Asia Pacific Water and Wastewater Treatment Market size to expand at a CAGR of 7.6% reaching a value of USD 246.37 billion by 2030. The Water and Wastewater Treatment Market across Asia Pacific is propelled by population growth, urbanization, water scarcity, industrialization, and environmental regulations. Water security is a pressing concern due to the region's economic and demographic growth. Governments are prioritizing decentralized wastewater treatment systems to address these challenges and promote sustainable practices. Treated wastewater is being repurposed for various uses, leading to cost savings. Organic fertilizers and biogas production from wastewater are fostering entrepreneurial opportunities and providing energy solutions. Innovative financing mechanisms and user fees are empowering communities to invest in sustainable sanitation and wastewater management. By addressing these challenges and leveraging innovative solutions, the region can create a more sustainable and resilient future.

Sample @ https://www.blueweaveconsulting.com/report/asia-pacific-water-and-wastewater-treatment-market/report-sample

Opportunity - Growing Adoption of Advanced Technologies

Asia Pacific, where approximately 80% of wastewater is discharged untreated, faces significant environmental and public health challenges. Polluted groundwater, rivers, and coastal areas, essential for drinking, fishing, and recreation, underscore the region's inadequate sanitation systems. High capital costs, weak infrastructure, and low public awareness have hindered sanitation prioritization in many countries. However, a paradigm shift is underway. Advanced technologies, including decentralized wastewater treatment systems, biogas digesters, and methane capture solutions, are gaining traction in both urban and rural areas. These energy-efficient alternatives not only reduce pollution but also generate valuable resources like organic fertilizers and renewable energy. Treated wastewater is being repurposed for irrigation, industrial processes, and firefighting, optimizing water utilization. Governments and investors are increasingly recognizing the economic potential of wastewater management. Innovative financing mechanisms, such as microfinancing and public-private partnerships, are facilitating infrastructure expansion. The Asian Development Bank (ADB) is actively supporting these efforts through its "Promoting an Asia-Pacific Wastewater Management Revolution" project. By promoting knowledge sharing, capacity building, and the adoption of cutting-edge technologies, the ADB aims to improve water quality, public health, and environmental sustainability across the region.

China Leads Asia Pacific Water and Wastewater Treatment Market

As the world's largest consumer of water and wastewater treatment chemicals, China is spearheading a transformative revolution in its water management practices. Despite significant challenges posed by widespread water pollution, the country is rapidly expanding its treatment infrastructure to meet the surging demands of its growing population and industrialization. Government initiatives, coupled with substantial investments, are driving the adoption of advanced treatment technologies. Strict environmental regulations and a focus on sustainable water resource management are further accelerating this progress. China's commitment to addressing water scarcity and improving water quality positions it as a global leader in the wastewater treatment sector. While other emerging economies in the region are making strides, China's scale, rapid development, and proactive policies make it a benchmark for sustainable water management.

Impact of Escalating Geopolitical Tensions on Asia Pacific Water and Wastewater Treatment Market

Asia Pacific Water and Wastewater Treatment Market may face significant challenges from intensifying geopolitical tensions across the world. Disrupted supply chains, increased operational costs, and reduced foreign investment can hinder market development. Heightened instability may deter potential investors, as they hesitate to commit resources in uncertain environments. Moreover, conflicts can divert government attention and funding away from essential infrastructure projects, delaying advancements in water treatment technologies and facilities. The need for enhanced security measures can further strain budgets, diverting funds from critical upgrades and maintenance. As nations grapple with these challenges, achieving sustainable water management and ensuring a safe water supply may become increasingly difficult. The existing water quality issues and public health concerns could be exacerbated if these geopolitical tensions persist.

Competitive Landscape

Asia Pacific Water and Wastewater Treatment Market is fragmented, with numerous players serving the market. The key players dominating Asia Pacific Water and Wastewater Treatment Market include Suez, Veolia, Adroit Associates Private Limited, Sauber Environmental Solutions Pvt Ltd, Xylem, KUBOTA Corporation, FujiClean Co., Ltd, Hitachi Zosen Corporation, Asahi Chemical & Industrial Co., Ltd, and Thermax Limited. The key marketing strategies adopted by the players are facility expansion, product diversification, alliances, collaborations, partnerships, and acquisitions to expand their customer reach and gain a competitive edge in the overall market.

Contact Us:

BlueWeave Consulting & Research Pvt Ltd

+1 866 658 6826 | +1 425 320 4776 | +44 1865 60 0662

0 notes

Text

Transforming Water Purification: Trends and Innovations in the Membrane Filtration Market

Membrane filtration is a powerful separation technology used across various industries for processes that involve filtering particles, microorganisms, and molecules from liquids and gases. By applying a semi-permeable membrane, it allows selective passage based on size, shape, or chemical properties. The four primary types of membrane filtration include microfiltration, ultrafiltration, nanofiltration, and reverse osmosis, each suited to specific particle sizes and applications. For instance, microfiltration membranes typically filter particles larger than 0.1 microns, while reverse osmosis can remove ions as small as 0.0001 microns. Industries such as water and wastewater treatment, food and beverage processing, pharmaceuticals, and biotechnologies widely utilize membrane filtration systems to achieve high purity, maintain quality standards, and ensure compliance with safety regulations.

The Membrane Filtration Market Size was projected to reach 20.96 (USD Billion) in 2022 based on MRFR analysis. By 2032, the membrane filtration market is anticipated to have grown from 22.8 billion USD in 2023 to 48.5 billion USD. It is anticipated that the membrane filtration market would develop at a rate of about 8.75% between 2024 and 2032.

Membrane Filtration Size and Share

The membrane filtration market has witnessed considerable growth due to rising demands for clean water and safe food processing standards globally. Factors like population growth, industrialization, and stringent environmental regulations contribute to the expanding Membrane Filtration Share across different sectors. In recent years, the Asia-Pacific region has shown substantial market expansion, driven by growing industrial sectors and investments in water treatment projects. Europe and North America continue to maintain a significant Membrane Filtration Share due to their advanced infrastructure, research in filtration technologies, and stringent regulatory guidelines. Additionally, the size of the membrane filtration market is expected to grow steadily, with forecasts predicting robust demand in the pharmaceutical and biotechnology industries where membrane filtration is used for drug development, protein purification, and pathogen removal.

Membrane Filtration Analysis

Membrane Filtration Analysis involves assessing market trends, types of membranes, applications, and competitive landscape. The analysis often focuses on the materials used for membranes, such as polymers, ceramics, and metals, as these determine filtration efficiency, durability, and chemical compatibility. Companies in the market invest in R&D to innovate materials that enhance filtration performance and reduce operational costs. Membrane Filtration Analysis also examines the influence of environmental regulations on the market. As governments impose stricter laws to reduce pollutants, membrane filtration systems have become essential in water treatment, with manufacturers developing systems to comply with environmental and industry-specific standards.

Membrane Filtration Trends

Technological advancements are shaping the future of membrane filtration. One notable trend is the integration of smart technologies, allowing systems to optimize filtration processes through data analytics and real-time monitoring. Another trend is the development of sustainable membrane materials, including biodegradable or energy-efficient options, which cater to environmentally-conscious industries. Compact, modular filtration systems are also gaining popularity due to their flexibility and ease of use in space-limited applications. Lastly, there is an increased focus on reducing operational costs, driving demand for long-lasting, low-fouling membranes that require minimal maintenance. These Membrane Filtration Trends indicate a growing emphasis on efficiency, environmental sustainability, and adaptability to meet evolving industry needs.

Reasons to Buy the Reports

Comprehensive Market Insight: Gain an in-depth understanding of the membrane filtration industry, including key trends, market size, and future projections.

Competitive Analysis: Identify leading players in the market, their strategies, and innovative approaches to enhance product offerings and operational efficiency.

Technological Developments: Stay updated on the latest technological advancements in membrane materials and filtration processes.

Regulatory Impact: Understand how global regulations impact the membrane filtration market and influence product design and material choices.

Investment Opportunities: Identify growth areas and potential investment opportunities in emerging markets and applications.

Recent Developments

The membrane filtration market has seen several recent developments. Many companies are focusing on sustainability by developing recyclable or eco-friendly membranes. Additionally, advancements in nanotechnology have enabled the creation of membranes with higher precision in removing contaminants. Companies are also investing in artificial intelligence and IoT for membrane filtration systems, improving real-time monitoring and reducing the need for manual maintenance. In the pharmaceutical sector, innovations in membrane filtration are aiding in faster and more efficient vaccine production. Moreover, governments worldwide are encouraging adoption through favorable policies, further fueling the growth and development in the membrane filtration market.

Related reports :

pharma 4 0 market

rapid microbiology testing market

reporter gene assay market

health and wellness product market

0 notes

Text

Sodium Bisulphite Market - Forecast(2024 - 2030)

Sodium Bisulphite Market Overview

Furthermore, surging use of Sodium Bisulphite as disinfectant, and antioxidant in cosmetics and personal care products further fuels the market growth.

Request Sample Report:

This trend signifies a growing awareness and recognition of sodium bisulphite’s versatile properties in the beauty and personal care industry. The surge in the use of sodium bisulphite as a disinfectant and antioxidant is particularly notable. Cosmetics and personal care product manufacturers are incorporating sodium bisulphite into formulations to enhance product stability, extend shelf life, and provide antioxidant benefits. This reflects a broader consumer demand for products that not only contribute to personal care but also emphasize safety and longevity.

As consumers become more conscious of the ingredients in their beauty and personal care items, sodium bisulphite’s role as a disinfectant and antioxidant aligns with the industry’s evolving preferences. The market growth is, therefore, propelled by the dual benefits of sodium bisulphite, addressing both cosmetic formulation needs and consumer expectations for safe and effective personal care products. This trend indicates a positive trajectory for sodium bisulphite in the cosmetics and personal care sector, contributing significantly to the overall market expansion.

Market Snapshot:

Sodium Bisulphite Market Report Coverage

The report: “Sodium Bisulphite Market — Forecast (2024–2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the Sodium Bisulphite Industry.

By Grade: Food Grade, Technical Grade, and Others

By Application: Food Additive, Bleaching Agent, Water Treatment (Boiler, Paper and Pulp, Municipal, Textile, and Others), Antichlor, Reducing Agent, and Others

By End-Use Industry: Food & Beverage, Water and Wastewater Treatment, Textile, Paper & Pulp, Leather, Pharmaceuticals, Mining, Film and Photography, and Others

By Geography: North America, South America, Europe, APAC, and RoW

Key Takeaways

The increase in research and development in new drug formulation has triggered the market demand of Sodium Bisulphite in the pharmaceutical industry.

Decline in manufacturing activities and disruption of supply chain due to the outbreak of coronavirus has hampered the growth of the Sodium Bisulphite Market.

Increasing adoption of UV technologies and RO filtration lower the demand of Sodium Bisulphite from wastewater and sewage treatment plants.

For More Details on This Report — Request for Sample

Sodium Bisulphite Market Segment Analysis — By Grade

Based on the grade, industrial grade segment holds the largest share of more than 45% in the Sodium Bisulphite Market in 2023. Sodium Bisulphite of industrial grades are used as bleaching or antichlor agent in paper industries as it reduces the natural element that causes paper to brown, from the wood pulp, and increase the brightness of paper. Owing to various environmental benefits, demand for paper and pulp is increasing which in turn augments the growth of the Sodium Bisulphite Market. For instance, the global consumption of paper and cardboard was approximately 414.19 million metric tons in 2022. Also, global import value of pulp grew by $10,019 million reaching approximately $70,274 million in 2022, according to International Trade Centre.

Inquiry Before Buying:

Sodium Bisulphite Market Segment Analysis — By Application

Water Treatment segment holds the largest share of more than 25% in the Sodium Bisulphite Market in 2023. Sodium Bisulphite is commonly used for the removal of free chlorine and as a biostatic in water treatment plants. Sodium Bisulphite reduces free chlorine to form sodium bisulfate (NaHSO4) and hydrochloric acid (HCl). Efficacy and cost effectiveness compared to other water treatment chemicals such as ferric sulfate are major factors driving the growth of the Sodium Bisulphite Market. In addition, surging demand for freshwater pose an opportunity for the growth of Sodium Bisulphite Market. According to the Organisation for Economic Co-operation and Development, freshwater demand is projected to increase by 55% globally between 2000 and 2050, significantly aiding the market growth.

Sodium Bisulphite Market Segment Analysis — By End-Use Industry

Food & Beverage segment holds the largest share of more than 30% in the Sodium Bisulphite Market in 2023. A significant rise in per capita consumption of packaged food and beverages, is likely to have a major impact on the demand for Sodium Bisulphite because Sodium Bisulphite is used as a preservative and as a steeping agent. According to The Association for Packaging and Processing Technologies (PMMI) The U.S. beverage market is projected to experience a Compound Annual Growth Rate of 5.2% until the year 2025. Whereas, Food grade Sodium Bisulphite is commonly used as a preservative in food manufacturing processes and also used in the manufacturing of paper intended for direct food contact applications.

Sodium Bisulphite Market Segment Analysis — By Geography

Asia Pacific has dominated the Sodium Bisulphite Market with a share of more than 45% in 2023 followed by North America and Europe. Population growth combined with rapid industrialization and high disposable income are driving the growth of Sodium Bisulphite Market in APAC region. Sodium Bisulphite are used in textile and leather industries as a bleaching agent for strain removal, brightening, and improving the quality of fabric. Increasing demand for apparel, growing fashion trends, and flourishing textile industries across the country is aiding the growth of the market. According to the Indian Brand Equity Foundation (IBEF), In 2022, India’s textile and apparel exports, including handicrafts, amounted to US$ 44.4 billion, reflecting a significant year-on-year growth of 41%., this may fuel the demand of Sodium Bisulphite for the bleaching process.

Sodium Bisulphite Market Drivers

Growing uses for wastewater treatment

Sodium Bisulfite is primarily used for water treatment to remove excess chlorine in drinking water. According to UN, In 2022, 2.2 billion people still lacked safely managed drinking water, including 703 million without a basic water service. Sodium bisulphite is globally used as a water softener which neutralizes the harmful bacteria present in water. The imperative need for safe water across the world is driving key players in the market to expand their operations and provide water treatment. The need for safe drinking water will lead to increased opportunities in the global sodium bisulfite market.

Schedule A Call :

Sodium Bisulphite is used externally for parasitic skin diseases and as gastrointestinal antiseptic. Accelerating use of Sodium Bisulphite as an excipient to medications in order to prevent the oxidation of adrenaline augments the growth of the market. Moreover, technology advancements and government’s spending on healthcare is expected to drive the growth of Sodium Bisulphite Market during forecast period. For instance, The Australian 2023–24 Budget allocates a landmark $6.1 billion for the enhancement of Medicare, aimed at revitalizing primary healthcare. Additionally, it earmarks an extra $2.2 billion for new and revised listings on the Pharmaceutical Benefits Scheme (PBS). The health system in Algeria has witnessed improvement in health indicators, attributed to the increased allocation of the state budget to the health sector, constituting 5.2% of the GDP. Over the past decade, the government has dedicated US $28 billion to support these advancements. Also, U.S. health care spending grew by 4.1 percent in 2022, reaching $4.5 trillion.

Sodium Bisulphite Market Challenges

Harmful effects of Sodium Bisulphite on human health

Exposure to sodium bisulfite solution cause irritation to the skin, eyes, and respiratory tract. Breathing sodium bisulfite solution vapor may aggravate asthma or other pulmonary (breathing) diseases and may cause headaches, breathing difficulties, or heart irregularity from sulfur dioxide (SO2) exposure. Thus, the harmful effects of sodium bisulfite acts as a restraining factor to the market growth. Additionally, the adoption of U.V technologies and RO water filtration whose purification efficiency is higher than Sodium Bisulphite hampers the growth of the market. Thus, an alternative dechlorination treatment system to replace Sodium Bisulphite (SBS), reduce the usage of chlorination, and achieve a chemical-free dechlorination process acts as a restraint for the market growth.

Buy Now :

The Covid-19 proved to be a major challenge for the growth of the Sodium Bisulphite Market. Self-isolation rules have resulted in short supply and event cancellations. Many industries are shuttered due to lack of manpower. The apparel industry body Clothing Manufacturers Association of India (CMAI) has estimated that if no assistance comes from government either in terms of wage subsidy or revival packages there could be loss of almost 1 crore jobs in the entire textile chain. Decrease in purchasing capital has slowed the growth of textile, paper & pulp, and mining industries which in turn hampered the demand for Sodium Bisulphite.

Sodium Bisulphite Industry Outlook

Product launches, acquisitions and R&D activities are key strategies adopted by players in the Sodium Bisulphite market. The key players in the Sodium Bisulphite market include

1. BASF SE

2. Aditya Birla Chemicals

3. Esseco USA LLC

4. Grasim Industries Ltd.

5. INEOS Group Ltd.

6. Chemtrade

7. Hydrite Chemical Co.

8. Hawkins, Inc.

9. KANTO CHEMICAL CO., INC.

10. Solvay S.A.

Recent Developments

In Nov 2023, Esseco Group’s acquired WATGRID which boosted the sodium bisulphite market by optimizing winemaking with AI. This enhances efficiency, offers predictive analysis in wine production, and reduces reliance on traditional methods, driving market growth, as sodium bisulphite, is commonly used for preservation and stabilization.

For more Chemicals and Materials Market reports, please click here

0 notes

Text

Antifoaming Agent Market — Forecast(2024–2030)

Antifoaming Agent Market size is forecast to reach $10.13 billion by 2030 after growing at a CAGR of 4.1% during 2024–2030.

Antifoaming agent is chemical additive that reduces the formation of foam in industrial process liquids. The growth of the market of antifoaming agent is expected to be driven by the high demand from the food and beverages industry. A prominent trend in the Antifoaming Agent market is the increasing demand for sustainable solutions. As industries prioritize environmental consciousness, there’s a growing interest in antifoaming agents derived from eco-friendly sources. Biodegradable and renewable antifoaming agents, often plant-based, are gaining traction. Manufacturers are investing in research to develop formulations that provide effective foam control while aligning with sustainability goals, catering to environmentally conscious industries like food and beverage, pharmaceuticals, and wastewater treatment. Another trend involves technological advancements for precise foam control. Industries such as manufacturing, oil and gas, and chemical processing are seeking antifoaming agents with improved efficiency and application precision.

Request Sample

Innovations include the development of smart or responsive antifoaming solutions that can adapt to varying foam challenges dynamically. Nanotechnology is being explored to enhance the efficiency of antifoaming agents. Nano-sized particles can offer improved dispersion and coverage, leading to enhanced foam control. This trend involves the development of nanomaterial-based antifoaming agents with higher surface area and reactivity.

The incorporation of nanotechnology also contributes to reducing the overall dosage of antifoaming agents required for effective foam suppression. The use of antifoaming agents is expanding beyond traditional industries. There is a growing demand for these agents in cosmetic and personal care product formulations where controlling foam is crucial for product stability and quality. As consumers become more discerning about the ingredients in personal care items, the market for antifoaming agents in this sector is experiencing growth.

Antifoaming Agent Market Report Coverage

The report: “Antifoaming Agent Market -Forecast (2024–2030)”, by IndustryARC, covers an in-depth analysis of the following segments of antifoaming agent industry.

By Type: Water Based, Oil Based, Silicone Based, Alkyd Based, Polymer Based and Others

By Application: Adhesives, Coatings, Detergents, Wood Pulp, Food Processing, Wastewater Treatment and Others.

By End Use: Oil and gas, Paint and coatings, Food and Beverages, Pharmaceuticals, Textile, Pulp and Paper, Industrial and Others.

Geography: North America, South America, Europe, APAC, and RoW.

Inquiry Before Buying

Key Takeaways

• APAC dominates the antifoaming agent owing to increasing demand from Oil and gas sector.

• Continues expanding application of antifoaming agent will drive the growth of the market in the forecast period.

• The formation of foam in industrial process liquids as it has an affinity to the air-liquid surface will hinder the growth of the market in the forecast period.Antifoaming Agent Market Segment Analysis — By Type

Silicone based antifoaming agents held the largest share in the antifoaming agents market in 2023. Silicone based antifoaming agents have properties such as low surface tension, chemical inertness, thermal stability, and complete solubility in water. These antifoaming agents have heavy duty type and are suitable for neutralizing surface foam and to release the entrained air in non-aqueous foaming applications. Hence, they have been finding preferential application in crude oil refineries. Silicone based antifoaming agents contain less volatile organic compound due to the environmental regulation passed by the North America and Europe government. This antifoaming agents are high in demand as compared to other chemicals due to its optimal reactivity with process ingredients and long operation life. This factor will drive the growth of market of silicone based antifoaming agents in the forecast period.

Schedule a Call

Antifoaming Agent Market Segment Analysis — By Application

Food Processing held the largest share in the antifoaming agents market in 2023. Food grade antifoaming agents are used to reduce and prevent foam formation. Foam is a byproduct formed during processing of food. It is also used in the fermentation process in breweries to drain out the foam and offer optimize efficiency. The food processing industry is a mature sector that is undergoing a tumultuous phase due to rising global demands for food safety, increasing food insecurity and increasing customer demand for higher quality and sustainability. Today’s food supply chain is more globalized, longer and more dynamic than ever before. With increasing imports and exports, processed foods rely on longer supply chains, which pose a major challenge to ensuring food safety.

Buy Now

Antifoaming Agent Market Segment Analysis — By End Use

Pharmaceuticals sector held the largest share in the antifoaming agents market in 2023 with a share of 7.3%. Antifoaming agent are used for pharmaceutic fermentation in antibiotics and enzymes. Among these the growing and aging population, rising prevalence of chronic diseases are major drivers in the growth of pharmaceutical sector globally. In the United States, overall spending growth in pharmaceutical is driven by a range of factors including new product uptake and brand pricing, while it is offset by patent expiries and generics. Pharmaceutical spending in China reached $7.1 billion in 2023. These factors will drive the growth of the market of pharmaceuticals in the forecast period.

The 2019–2020 coronavirus pandemic has had far-reaching consequences beyond the spread of the disease and efforts to quarantine it. As the pandemic has spread around the globe, concerns have shifted from supply-side manufacturing issues to decreased business. The current epidemic outbreak has deeply influenced consumers’ daily life and in addition to the impact on pharmaceutical sector. About 90% of the needs of antibiotic makers in globally is fulfilled by China. Raw materials from China are used in making antibiotics, paracetamol, and diabetes and cardiovascular drugs, among others are not exported. This factor will hinder the growth of market for this year. But after the situation became normal it will grow at a steady rate in the forecast period.

Antifoaming Agent Market Segment Analysis — By Geography

APAC dominates the antifoaming agents market with a share of 48% followed by North America and Europe. The economy of APAC is mainly influenced by the economic dynamics of countries such as China and India, but with growing foreign direct investment for economic development of South East Asia, the current scenario is changing. Countries in South East Asia are witnessing high growth the oil and gas sector. Antifoaming agent are used in crude oil refinery as it helps in reducing frothy crude oil production by eliminating foam from tanks or gas scrubbers. The oil and gas sector plays a major role in influencing decision making for all the other important sections of the economy. According to the trade map the total export of light crude oil globally in the year 2023 was 102.2 mb/d. This factor will drive the growth of the market of oil and gas sector in the forecast period.

Antifoaming Agent Market Drivers

High demand of crude oil across the world will drive the growth in the forecast period

High demand of crude oil across the world is expected to drive the global antifoaming agent’s market growth. However, other non-renewable energy resources are not capable of fulfilling the growing demand. Oil and gas is one of the largest energy resources in the world; hence, it becomes essential to use and distribute crude oil in the productive and efficient way. This factor will drive the growth of market in the forecast period.

Rise in the Paint and coatings sector will drive the growth of market in the forecast period

The coatings industry is one of the most heavily regulated industries in the world, so producers have been forced to adopt low-solvent and solvent less technologies in the past 40 years, and will continue to do so. The number of coatings producers is large, but most are regional producers. This factor will drive the growth of market in the forecast period.

Antifoaming Agent Market Restriction

Hike in the crude prices will hamper the growth of the market in the forecast period

Tremendous hike in the crude prices and global recession will hinder the growth of the market. This was on the back of a deepening slowdown in the world economy as the outbreak of novel coronavirus has spread across the globe and a price war between major oil producing countries like Saudi Arabia, Iran and Russia. These factor will hinder the growth of the market in the forecast period.

Antifoaming Agent Market Landscape

Technology launches, acquisitions and R&D activities are key strategies adopted by players in the antifoaming agents market. Major players in the antifoaming agents market are BASF, Evonik Industries, Air Products and Chemicals, Inc., Wacker Chemie AG, DOW Corning Corporation, and Others.

Acquisitions/Technology Launches/ Product Launches

In Oct 2023, Evonik Launches New Defoaming Agent that Combines the Best Properties of Silicone and Bio-Based Materials. The new product is targeted at water-based ink and coating applications, uses a unique new mixing technology, contains more than 50% bio-based materials in the solid content, and complies with multiple food contact regulations.

• In May 2023, Jio-bp launches new diesel that offers saving of Rs 1.1 lakh per truck annually. It is designed to work across a range of commercial vehicles, and with ongoing use it offers a variety of benefits to drivers and fleet owners. It contains an anti-foam agent that helps deliver cleaner, faster, and safer refuelling, so trucks can spend more time on the road and less time at the pump.

For more Chemical and Materials related reports, Please click here

0 notes

Text

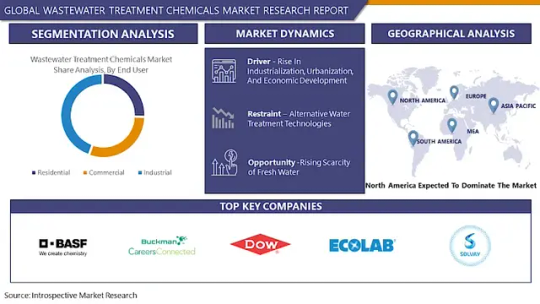

Wastewater Treatment Chemicals Market: Global Industry Analysis and Forecast 2023 – 2030

The Global Market for Wastewater Treatment Chemicals Estimated at USD 13.48 Billion In the Year 2022, Is Projected To Reach A Revised Size Of USD 22.31 Billion By 2030, Growing At A CAGR Of 6.5% Over The Forecast Period 2023-2030.

Wastewater Treatment Chemicals is a complex process that involves the use of different chemicals to treat used water to remove contaminants, pollutants, and other organic compounds from the water so that it can be safely reintroduced into the environment.

The four main types of chemicals used in wastewater treatment are pH neutralizers, anti-foaming agents, coagulants, and flocculants. Wastewater treatment involves a number of stages involving processes that are mechanical this is physically based, biological-based, chemical-based, as well as membrane (filtration) processes.

Get Full PDF Sample Copy of Report: (Including Full TOC, List of Tables & Figures, Chart) @

https://introspectivemarketresearch.com/request/16614

The latest research on the Wastewater Treatment Chemicals market provides a comprehensive overview of the market for the years 2023 to 2030. It gives a comprehensive picture of the global Wastewater Treatment Chemicals industry, considering all significant industry trends, market dynamics, competitive landscape, and market analysis tools such as Porter's five forces analysis, Industry Value chain analysis, and PESTEL analysis of the Wastewater Treatment Chemicals market. Moreover, the report includes significant chapters such as Patent Analysis, Regulatory Framework, Technology Roadmap, BCG Matrix, Heat Map Analysis, Price Trend Analysis, and Investment Analysis which help to understand the market direction and movement in the current and upcoming years. The report is designed to help readers find information and make decisions that will help them grow their businesses. The study is written with a specific goal in mind: to give business insights and consultancy to help customers make smart business decisions and achieve long-term success in their particular market areas.

Leading players involved in the Wastewater Treatment Chemicals Market include:

BASF SE (Germany), Ecolab (U.S.), Solenis (U.S.), Kemira Oyj (Finland), Baker Hughes (Germany), The Dow Chemical Company (U.S.), Cortec Corporation (U.S.), Buckman (U.S.), Solvay S.A (Belgium), Kurita Water Industries (Japan), Veolia (France), Somicon ME FZC (UAE), Toray Industries, Inc. (India), Daiki Axis (India), and Other Major Players

If You Have Any Query Wastewater Treatment Chemicals Market Report, Visit:

https://introspectivemarketresearch.com/inquiry/16614

Segmentation of Wastewater Treatment Chemicals Market:

By Type

Coagulants & Flocculants

Corrosion & Scale Inhibitors

Chelating Agents

Biocides & Disinfects

By End-User

Residential

Commercial

Industrial

By Regions: -

North America (US, Canada, Mexico)

Eastern Europe (Bulgaria, The Czech Republic, Hungary, Poland, Romania, Rest of Eastern Europe)

Western Europe (Germany, UK, France, Netherlands, Italy, Russia, Spain, Rest of Western Europe)

Asia Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Vietnam, The Philippines, Australia, New Zealand, Rest of APAC)

Middle East & Africa (Turkey, Bahrain, Kuwait, Saudi Arabia, Qatar, UAE, Israel, South Africa)

South America (Brazil, Argentina, Rest of SA)

What to Expect in Our Report?

(1) A complete section of the Wastewater Treatment Chemicals market report is dedicated for market dynamics, which include influence factors, market drivers, challenges, opportunities, and trends.

(2) Another broad section of the research study is reserved for regional analysis of the Wastewater Treatment Chemicals market where important regions and countries are assessed for their growth potential, consumption, market share, and other vital factors indicating their market growth.

(3) Players can use the competitive analysis provided in the report to build new strategies or fine-tune their existing ones to rise above market challenges and increase their share of the Wastewater Treatment Chemicals market.

(4) The report also discusses competitive situation and trends and sheds light on company expansions and merger and acquisition taking place in the Wastewater Treatment Chemicals market. Moreover, it brings to light the market concentration rate and market shares of top three and five players.

(5) Readers are provided with findings and conclusion of the research study provided in the Wastewater Treatment Chemicals Market report.

Our study encompasses major growth determinants and drivers, along with extensive segmentation areas. Through in-depth analysis of supply and sales channels, including upstream and downstream fundamentals, we present a complete market ecosystem.

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

Acquire This Reports: -

https://introspectivemarketresearch.com/checkout/?user=1&_sid=16614

About us:

Introspective Market Research (introspectivemarketresearch.com) is a visionary research consulting firm dedicated to assisting our clients to grow and have a successful impact on the market. Our team at IMR is ready to assist our clients to flourish their business by offering strategies to gain success and monopoly in their respective fields. We are a global market research company, that specializes in using big data and advanced analytics to show the bigger picture of the market trends. We help our clients to think differently and build better tomorrow for all of us. We are a technology-driven research company, we analyse extremely large sets of data to discover deeper insights and provide conclusive consulting. We not only provide intelligence solutions, but we help our clients in how they can achieve their goals.

Contact us:

Introspective Market Research

3001 S King Drive,

Chicago, Illinois

60616 USA

Ph no: +1-773-382-1047

Email: [email protected]

#Wastewater Treatment Chemicals#Wastewater Treatment Chemicals Market#Wastewater Treatment Chemicals Market Size#Wastewater Treatment Chemicals Market Share#Wastewater Treatment Chemicals Market Growth#Wastewater Treatment Chemicals Market Trend#Wastewater Treatment Chemicals Market segment#Wastewater Treatment Chemicals Market Opportunity#Wastewater Treatment Chemicals Market Analysis 2023

0 notes

Text

Innovations in Water Treatment: The Rise of Brine Concentration Technology Startups in China

According to the UnivDatos Market Insights analysis, the growth of brine concentration technology (BCT) in the Asia Pacific region is propelled by several interrelated factors. The rapid industrial expansion in countries like China and India, coupled with the proliferation of desalination plants, generates substantial volumes of high-salinity wastewater that require effective treatment solutions. Stringent environmental regulations and national sustainability initiatives further drive the adoption of advanced BCT as governments enforce strict water pollution controls and promote sustainable wastewater management practices. As per their “Brine Concentration Technology Market” report, the global market was valued at USD ~14.07 billion in 2023, growing at a CAGR of about 5.8% during the forecast period from 2024 – 2032.

In the case of the Asia Pacific region, water and environmental sustainability are two issues that require intervention. This is particularly so since China has recently experienced both rapid industrialization and urbanization, which have put pressure on its ability to manage its water resource endowment effectively. Industry experts often use brine concentration technology (BCT) as the main methodology to overcome these problems, causing steadily growing interest in efficient water treatment methods. This has led to the emergence of a great number of start-ups that have as their explicit aim the innovation of advanced BCT solutions. This blog is designed to investigate the causes and effects of the BCT market in China, look for startups that have shown active progress in this sector, and analyze markets and future.

The Imperative for Brine Concentration Technology

The treatment of high-salinity wastewater is critical in most industries involving processes such as desalination, mining, and chemical production, among others, hence the need for advances in brine concentration technology. The rising industrialization in China means much wastewater production, which calls for proper treatment to avoid harming the environment further and meet the regulations provided set standards.

Environmental Regulations and Sustainability Goals

The Chinese authorities have placed strict measures for the disposal of wastewater as a sign of their adherence to environmental concerns. Several measures have been deployed to minimize polluting the water bodies and encourage the use of treated wastewater. The emergence of these regulations ensures the market’s environment supports the start-ups in delivering mutually and implementing brine concentration techniques, hence expanding their market BCT.

Industrial Growth and Urbanization

The population and industrialization have boosted the need for water resources in China, along with urbanization. Some of the sectors, like petrochemicals, textiles, and pharmaceuticals, generate huge volumes of WWT with high salinity and thus need enhanced treatment. Recognizing the need to address these effluents, BCT provides a solution that is beneficial to any industry that is in a constant search for ways to minimize their impact on the environment and be on par with the set standard.

The Startup Ecosystem in China

The growing demand for brine concentration technology in China has led to the emergence of a vibrant startup ecosystem. These startups leverage cutting-edge technologies and innovative approaches to develop efficient and cost-effective BCT solutions. Here are some of the notable startups making significant contributions to the Chinese BCT market.

1. AquaTech Innovations

It is recognized that AquaTech Innovations is one of the leading companies that develop brine concentration technology in China. For BCT, a preference membrane-based technique has been designed that is both high-efficiency and low-energy. As a result, AquaTech Innovation has ventured into the development of one of the most unique and efficient ways for industrial effluents. Since its technology can be used to treat all industrial effluents, the company has attracted clients from all fields of production. Taking on the company’s innovations, as well as its sustainability-driven vision and strategy, the company has established itself among the leaders of the BCT market.

2. EcoWater Solutions

EcoWater Solutions is another famous Chinese startup in the BCT market, and it is an experienced corporation as it has worked since 2008. The company operates mostly in the water treatment niche, focusing on the aspect of environmental concerns. EcoWater Solutions employs thickening systems that enable it to achieve high concentrations of brine using thermal processes, all at lower costs. The Federal government and environmental organizations appreciate the company’s focus on sustainability and innovations, thus extending their support to the startup.

3. GreenWave Technologies

GreenWave Technologies, which was established in 2010, is a new entrant in the brine concentration technology market. This BCT is electrochemical, and it provides both high efficiency and the possibility of scaling the startup’s operations. A solution by GreenWave Technologies has been identified as perfectly suitable for the treatment of high-salinity water commonly produced by mining and other chemical industries. The company’s innovation has implemented several pilot instances, further reinforcing this concept as the demand for brine concentration intensifies.

Market Demand and Potential

Therefore, the Chinese industry needs advanced technologies in brine concentration, which is an essential factor in the effective management of wastewater, compliance with legislation, and concern for the environment. As for the market prospect, China has great potential in the development of BCT, and different industries need the high-tech treatment of wastewater.

Industrial Applications

In China, the consumer with the most demand for brine concentration is the industrial sector. Chemical and oil refining industries, operations that involve textile and pharmaceutical facilities, and mining activities are some industries that deal with high salinity aqueous solution production that needs efficient removal solutions. The suggested strategy allows BCT to capitalize on these industries’ need to address the effluents, mitigate the impressions on the environment, and meet the requirements of the legislation.

Government Initiatives

The Chinese government has implemented several initiatives to promote the adoption of advanced water treatment technologies. These initiatives include financial incentives, grants, and subsidies for companies developing and deploying innovative BCT solutions. Government support has played a crucial role in fostering the growth of the BCT startup ecosystem in China.

Technological Advancements

By evaluating the information presented above, it can be summarized easily that it has a bright future for its application in China. This is due to industries being in constant search for more water resources under the rising restrictive environmental standards for using water which in turn introduced the opportunity for the startup ecosystem in China to establish innovative solutions tailored to the nuanced aspect of managing high-salinity water.

Future Prospects

The prospects for brine concentration technology in China are promising. The increasing demand for water resources, coupled with stringent environmental regulations, will continue to drive the adoption of BCT in various industries. The startup ecosystem in China is well-positioned to capitalize on this growing demand by developing and deploying innovative solutions that address the unique challenges of high-salinity wastewater management.

Request Free Sample Pages with Graphs and Figures Here https://univdatos.com/get-a-free-sample-form-php/?product_id=62941

Strategic Partnerships and Collaborations

By involving collaborations between startups, existing organizations, and research facilities, it will be possible to enhance brine concentration technology. Such partnerships can foster information sharing and allow proficient knowledge, resource, and expertise exchange to spur new advances in novel BCT deployments.

Investment and Funding

To sum up, funding and investment are the key factors defining startups and contributing to developing the brine concentration technology market. Policy support from grants, venture capitalists/VC funds, and corporate funding are other sources of funding that are helpful for startups to grow and monetize their products. As the awareness of potential markets and opportunities grows, industry players will be encouraged to invest more in the BCT sector to produce better and more comprehensive solutions.

Market Expansion and Diversification

As the demand for brine concentration technology grows, startups in China will have opportunities to expand their market reach and diversify their product offerings. Exploring new industrial applications, entering international markets, and developing customized solutions for specific industry needs will be key strategies for growth and expansion.

Conclusion

The rise of brine-concentration technology startups in China is a testament to the country's commitment to addressing its water management challenges and promoting environmental sustainability. The demand for efficient and innovative BCT solutions is driving the growth of a vibrant startup ecosystem, with companies like AquaTech Innovations, EcoWater Solutions, and GreenWave Technologies leading the way. As the market expands, the prospects for brine concentration technology in China are bright, offering promising opportunities for startups, investors, and industries alike. Through continued innovation, strategic collaborations, and government support, China is poised to become a global leader in brine concentration technology, setting a benchmark for sustainable water management solutions in the Asia Pacific region and beyond.

Contact Us:

UnivDatos Market Insights

Email - [email protected]

Contact Number - +1 9782263411

Website -www.univdatos.com

0 notes

Text

Asia Pacific Industrial Pumps Market Growth, Size, Report by 2024 to 2032

The Reports and Insights, a leading market research company, has recently releases report titled “Asia Pacific Industrial Pumps Market: Industry Trends, Share, Size, Growth, Opportunity and Forecast 2024-2032.” The study provides a detailed analysis of the industry, including the Asia Pacific Industrial Pumps Market share, size, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights: