#U.S. Plastic to Fuel Market

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr’s reach among the 26-to-35-year-olds in the US is 11%.

Text

Global U.S. Plastic to Fuel Market Is Estimated To Witness High Growth Owing To Increasing Environmental Concerns

The global U.S. Plastic to Fuel Market is estimated to be valued at US$ 117.3 Mn in 2022 and is expected to exhibit a CAGR of 9.3% over the forecast period 2023-2030, as highlighted in a new report published by Coherent Market Insights. A) Market Overview: The U.S. Plastic to Fuel Market refers to the process of converting plastic waste into usable fuels and chemicals. This market offers numerous advantages, including reducing plastic waste, preventing landfill pollution, and providing a sustainable solution for energy production. The need for products associated with this market arises from the ever-increasing plastic waste generated globally and the urgent need for effective waste management solutions. B) Market Key Trends: One key trend in the U.S. Plastic to Fuel Market is the growing focus on sustainable practices and reducing the environmental impact of plastic waste. Governments and organizations worldwide are implementing strict regulations and initiatives to promote the recycling and reutilization of plastics. For example, the U.S. Environmental Protection Agency (EPA) has set targets for reducing plastic waste and increasing recycling rates. This trend is driving the adoption of plastic to fuel technologies as a more sustainable alternative to traditional waste disposal methods. An example supporting this trend is the company Plastic2Oil. It utilizes a proprietary pyrolysis process to convert mixed waste plastics into synthetic fuel oil, which can be used for various applications such as heating or generating electricity. This innovative technology not only reduces plastic waste but also provides an alternative source of energy, contributing to the overall sustainability goals. C) PEST Analysis: Political: The U.S. Plastic to Fuel Market is influenced by political factors such as government regulations on plastic waste management and incentives for promoting recycling and renewable energy sources. Economic: The market's growth is driven by factors like the increasing cost of landfilling plastic waste and the rising demand for sustainable energy solutions. Social: Growing awareness about the environmental impact of plastic waste and the need for sustainable practices is shaping consumer behavior and driving the market's growth. Technological: Advancements in technologies such as pyrolysis, catalytic depolymerization, and gasification are improving the efficiency and effectiveness of plastic to fuel conversion processes. D) Key Takeaways: Paragraph 1: The U.S. Plastic to Fuel Market Demand is expected to witness high growth, exhibiting a CAGR of 9.3% over the forecast period. This growth can be attributed to increasing environmental concerns and the need for sustainable waste management solutions. Governments, organizations, and individuals are recognizing the importance of reducing plastic waste and are actively seeking alternative methods for its disposal. Paragraph 2: The North American region is expected to dominate the U.S. Plastic to Fuel Market due to stringent regulations on plastic waste management and the presence of key market players. Additionally, Asia Pacific is anticipated to be the fastest-growing region, driven by rapid industrialization, increasing plastic waste generation, and growing focus on sustainability. Paragraph 3: Key players operating in the global U.S. Plastic to Fuel Market include Plastic2Oil, Agilyx Corporation, Vadxx Energy, and Green Envirotec Holdings. These companies are at the forefront of developing innovative technologies and solutions for converting plastic waste into usable fuels, contributing to a circular economy and a cleaner environment.

#U.S. Plastic to Fuel Market#U.S. Plastic to Fuel Market Demand#U.S. Plastic to Fuel Market Values#U.S. Plastic to Fuel Market Forecast#U.S. Plastic to Fuel Market Analysis#plastic waste#fuel sources#plastic-to-fuel technology#Coherent Market Insights

0 notes

Text

U.S. Plastic-to-Fuel Market Is Estimated To Witness High Growth

The U.S. Plastic-to-Fuel Market is estimated to be valued at US$ 117.3 million in 2022 and is expected to exhibit a CAGR of 9.3% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. A) Market Overview: The U.S. Plastic-to-Fuel market involves the conversion of plastic waste into fuel through various processes such as pyrolysis, gasification, and depolymerization. This innovative approach not only helps in managing plastic waste but also provides a sustainable alternative to conventional fossil fuels. The market includes key players such as Plastic2Oil, Agilyx Corporation, Vadxx Energy, and Green Envirotec Holdings, who are actively engaged in research and development of plastic-to-fuel technologies.

0 notes

Text

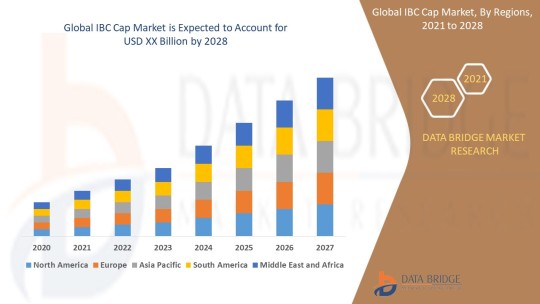

IBC Cap Market Size, Share, Trends, Growth and Competitive Analysis

"IBC Cap Market – Industry Trends and Forecast to 2028

Global IBC Cap Market, By Product Type (Flange, Plugs, Vent-in Plug, Vent-out Plug and Screw closure), Type (Plastic IBC, Metal IBC and Composite IBCs), Material Type (Plastics, Metal, Aluminium and Steel), End Use (Chemicals & Fertilizers, Petroleum & Lubricants, Paints, Inks & Dyes, Food & Beverage, Agriculture, Building & Construction, Healthcare & Pharmaceuticals and Mining), Application (Food And Drinks, Chemical Industry, Oil and Agriculture), Country (U.S., Canada, Mexico, Brazil, Argentina, Rest of South America, Germany, France, Italy, U.K., Belgium, Spain, Russia, Turkey, Netherlands, Switzerland, Rest of Europe, Japan, China, India, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific, U.A.E, Saudi Arabia, Egypt, South Africa, Israel, Rest of Middle East and Africa) Industry Trends and Forecast to 2028

Access Full 350 Pages PDF Report @

The global IBC cap market is expected to witness significant growth over the forecast period due to the increasing demand for intermediate bulk containers (IBCs) in various industries such as chemicals, food and beverages, pharmaceuticals, and others. The IBC caps play a crucial role in ensuring the safe storage and transportation of liquid products. The market growth is also being driven by technological advancements in IBC cap designs, such as tamper-evident seals and spouts for easy dispensing. Additionally, the growing focus on sustainability and recyclability of packaging materials is further boosting the adoption of IBC caps made from eco-friendly materials.

**Segments**

- Based on material type, the IBC cap market can be segmented into plastic, metal, and others. Plastic caps are widely used due to their lightweight nature and cost-effectiveness. - By cap type, the market can be categorized into screw caps, snap-on caps, and flip-top caps. Screw caps are preferred for their secure sealing properties. - On the basis of end-user industry, the market can be divided into chemicals, food and beverages, pharmaceuticals, and others. The chemicals segment is anticipated to hold a significant market share due to the widespread use of IBCs for storing chemical products.

**Market Players**

- TPS Industrial Srl - Schuetz GmbH & Co. KGaA - Mauser Packaging Solutions - Time Technoplast Ltd - Berry Global Inc. - THIELMANN UCON AG - Precision IBC, Inc. - Peninsula Packaging LLC

These market players are actively involved in strategic initiatives such as product launches, partnerships, and acquisitions to strengthen their market presence and expand their product offerings. The competitive landscape of the IBC cap market is characterized by intense competition, prompting companies to focus on innovation and quality to gain a competitive edge.

The Asia-Pacific region is expected to witness substantial growth in the IBC cap market, driven by the rapid industrialization and the increasing adoption of IBCsThe Asia-Pacific region represents a significant growth opportunity for the global IBC cap market due to several key factors. With rapid industrialization and the expanding manufacturing sector in countries like China, India, and Southeast Asia, there is a growing demand for efficient storage and transportation solutions, including IBCs and their associated caps. The increased focus on chemical production, food processing, and pharmaceutical manufacturing in the region further fuels the need for reliable packaging solutions like IBC caps. As these industries continue to grow, the adoption of IBC caps is expected to rise, driving market expansion in the Asia-Pacific region.

Moreover, the emphasis on enhancing safety standards and ensuring product integrity is a crucial factor contributing to the growth of the IBC cap market in Asia-Pacific. Regulations regarding the safe handling and transportation of hazardous chemicals and pharmaceuticals necessitate the use of high-quality caps that can effectively seal and protect the contents of IBCs. As companies in the region strive to comply with stringent regulatory requirements, the demand for advanced and secure IBC caps is projected to increase significantly.

Additionally, the shift towards sustainability and eco-friendly practices is another trend shaping the IBC cap market in Asia-Pacific. With growing environmental concerns and increasing awareness about plastic pollution, there is a rising preference for IBC caps made from recyclable and biodegradable materials. Market players in the region are focusing on developing sustainable packaging solutions to meet the evolving consumer demands and align with global sustainability goals. This shift towards eco-friendly IBC caps not only addresses environmental concerns but also presents market players with opportunities to differentiate their offerings and attract environmentally conscious customers.

Furthermore, the competitive landscape of the IBC cap market in Asia-Pacific is characterized by the presence of both local manufacturers and international players. Local companies often have a strong understanding of regional market dynamics and customer preferences, giving them a competitive advantage in catering to specific industry needs. On the other hand, multinational companies bring technological expertise and a wide product portfolio, which can appeal to a broader customer base seeking innovative and**Global IBC Cap Market, By Product Type**

- Flange - Plugs - Vent-in Plug - Vent-out Plug - Screw closure

**Type**

- Plastic IBC - Metal IBC - Composite IBCs

**Material Type**

- Plastics - Metal - Aluminium - Steel

**End Use**

- Chemicals & Fertilizers - Petroleum & Lubricants - Paints, Inks & Dyes - Food & Beverage - Agriculture - Building & Construction - Healthcare & Pharmaceuticals - Mining

**Application**

- Food And Drinks - Chemical Industry - Oil and Agriculture

The Global IBC Cap market is experiencing significant growth due to the rising demand for intermediate bulk containers across various industries. Plastic caps are increasingly preferred for their lightweight and cost-effective nature, driving market growth within the material type segment. Screw caps, known for their secure sealing properties, dominate the cap type category. The chemicals segment is anticipated to hold a substantial market share among end-user industries, attributed to the widespread use of IBCs for chemical storage. The market players in the industry are focusing on strategic initiatives like product launches and partnerships to enhance their market presence and offerings. The competitive landscape is intense, spurring companies to innovate and prioritize quality for a competitive advantage.

In Asia-Pacific, the IBC cap market is poised for robust growth fueled by rapid industrialization and the expanding manufacturing sector, particularly in countries like China,

Countries Studied:

North America (Argentina, Brazil, Canada, Chile, Colombia, Mexico, Peru, United States, Rest of Americas)

Europe (Austria, Belgium, Denmark, Finland, France, Germany, Italy, Netherlands, Norway, Poland, Russia, Spain, Sweden, Switzerland, United Kingdom, Rest of Europe)

Middle-East and Africa (Egypt, Israel, Qatar, Saudi Arabia, South Africa, United Arab Emirates, Rest of MEA)

Asia-Pacific (Australia, Bangladesh, China, India, Indonesia, Japan, Malaysia, Philippines, Singapore, South Korea, Sri Lanka, Thailand, Taiwan, Rest of Asia-Pacific)

Key Coverage in the IBC Cap Market Report:

Detailed analysis of IBC Cap Market by a thorough assessment of the technology, product type, application, and other key segments of the report

Qualitative and quantitative analysis of the market along with CAGR calculation for the forecast period

Investigative study of the market dynamics including drivers, opportunities, restraints, and limitations that can influence the market growth

Comprehensive analysis of the regions of the IBC Cap industry and their futuristic growth outlook

Competitive landscape benchmarking with key coverage of company profiles, product portfolio, and business expansion strategies

TABLE OF CONTENTS

Part 01: Executive Summary

Part 02: Scope of the Report

Part 03: Research Methodology

Part 04: Market Landscape

Part 05: Pipeline Analysis

Part 06: Market Sizing

Part 07: Five Forces Analysis

Part 08: Market Segmentation

Part 09: Customer Landscape

Part 10: Regional Landscape

Part 11: Decision Framework

Part 12: Drivers and Challenges

Part 13: Market Trends

Part 14: Vendor Landscape

Part 15: Vendor Analysis

Part 16: Appendix

Browse Trending Reports:

Calcium Glycinate Market Retinal Biologics Market Facial Fat Transfer Market Angio Suites Diagnostic Imaging Market Adoption Of Benelux Power Tools Market De Quervains Tenosynovitis Treatment Market Biodetectors And Accessories Market Colposcope Market Sports Medicine Market Automotive Adhesives Market Infrared Imaging Market Vapour Deposition Market Professional Diagnostics Market Ct Scanner Market Programmable Application Specific Integrated Circuit Asic Market Hospital Operating Room Or Products And Solutions Market Castor Oil Market Zika Virus Infection Drug Market Toluene Diisocynate Market Antibiotic Resistance Market

About Data Bridge Market Research:

Data Bridge set forth itself as an unconventional and neoteric Market research and consulting firm with unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email: [email protected]"

2 notes

·

View notes

Text

From Extraction to Usage: The Lifecycle of Natural Gas

The journey of natural gas from the depths of the earth to the blue flames on a stove is a complex and multifaceted process. As a fossil fuel, natural gas plays a pivotal role in the global energy supply, accounting for approximately 24% of global energy consumption. This narrative will traverse through the lifecycle of natural gas, highlighting the intricacies involved in its extraction, processing, transportation, and usage, as well as its environmental and economic impacts.

Extraction and Production:

Natural gas extraction begins with geological surveys to identify promising reserves, followed by drilling either on land or offshore. In 2022, the United States, one of the largest producers, extracted approximately 99.6 billion cubic feet per day. The extraction often employs techniques like hydraulic fracturing, which alone contributed to around 67% of the total U.S. natural gas output in 2018. The extracted gas, containing various hydrocarbons and impurities, requires substantial processing to meet commercial quality standards.

Processing and Purification:

Once extracted, natural gas undergoes several processing steps to remove water vapor, hydrogen sulfide, carbon dioxide, and other contaminants. This purification is essential not only for safety and environmental reasons but also to increase the energy efficiency of the gas. Processing plants across the globe refine thousands of cubic feet of raw gas each day, ensuring that the final product delivered is almost pure methane, which is efficient for burning and less polluting than unprocessed gas.

Transportation:

Transporting natural gas involves an expansive network of pipelines covering over a million miles in the United States alone. In regions where pipeline infrastructure is not feasible, liquified natural gas (LNG) provides an alternative. LNG exports from the U.S. reached record highs in 2022, with approximately 10.6 billion cubic feet per day being shipped to international markets. LNG carriers and storage facilities are integral to this global trade, making natural gas accessible worldwide.

Storage:

Strategic storage ensures that natural gas can meet fluctuating demands, particularly during peak usage periods. Underground storage facilities can hold vast quantities; for instance, the U.S. can store approximately 4 trillion cubic feet of gas, helping to manage supply and stabilize prices. These reserves play a critical role in energy security and in buffering any unexpected disruptions in supply.

Distribution:

Natural gas distribution is the final leg before reaching end-users. Companies manage complex distribution networks to deliver gas to industrial facilities, power plants, commercial establishments, and residences. The U.S. alone has over 2 million miles of distribution pipelines, ensuring that natural gas accounts for nearly 30% of the country’s electricity generation and heating for about half of American homes.

Usage and Consumption:

The versatility of natural gas makes it a preferred source for heating, cooking, electricity generation, and even as a feedstock for producing plastics and chemicals. In the residential sector, an average American home might consume about 200 cubic feet per day for heating and cooking. For electricity, combined-cycle gas turbine plants convert natural gas into electricity with more than 60% efficiency, significantly higher than other fossil-fueled power plants.

Environmental Considerations and Future Prospects:

While natural gas burns cleaner than coal, releasing up to 60% less CO2 for the same energy output, it is not without environmental challenges. Methane, a potent greenhouse gas, can escape during various stages of the natural gas lifecycle. However, advances in technology and regulatory measures aim to mitigate these emissions. As the world leans towards a lower-carbon future, the role of natural gas is pivotal, with investments in carbon capture and storage (CCS) technologies and the potential integration with renewable energy sources.

4 notes

·

View notes

Text

Medical Disposables Market to be worth US$ 326 Billion by 2033, Reveals Future Market Insights

The Medical Disposables Market revenues were estimated at US$ 153.5 Billion in 2022 and is anticipated to grow at a CAGR of 7.1% from 2023-2033, according to a recently published Future Market Insights report. By the end of 2033, the market is expected to reach US$ 326 Billion. Bandages and Wound Dressings commanded the largest revenue share in 2022 and is expected to register a CAGR of 6.8% from 2023 to 2033.

The rising incidence of Hospital Acquired Infections, an increasing number of surgical procedures, and the growing prevalence of chronic diseases leading to longer hospital admission have been the key factors driving the market.

The subsequent spike in the number of chronic illness cases and a rise in the rate of hospitalizations has fueled the field of emergency medical disposables growth. The expansion of the medical disposables market is being fueled by an increase in the prevalence of hospital-acquired illnesses and disorders, as well as a greater focus on infection prevention. For example, the prevalence of healthcare-associated infection in high-income countries ranges from 3.5% to 12%, whereas it ranges from 5.7% to 19.1% in low and medium-income countries.

A growing geriatric population, an increase in the incidence of incontinence issues, mandatory guidelines that must be followed for patient safety at healthcare institutions, and an increase in demand for sophisticated healthcare facilities is driving the medical disposables market.

The market in North America is expected to reach a valuation of US$ 131 Billion by 2033 from US$ 61.7 Billion in 2022. In August 2000, the Food and Drug Administration (FDA) issued guidance concerning healthcare single-use items reprocessed by third parties or hospitals. In this guidance, FDA stated that hospitals or third-party reprocessors would be considered manufacturers and regulated in the exact same manner. A newly used single-use device still has to fulfill the criteria for device activation required by its flagship when it was originally manufactured. Such regulations have been creating a positive impact on the medical disposables market in the U.S. market in specific and the North American market in general

Competitive Landscape

The key companies in the market are engaged in mergers, acquisitions and partnerships.

The key players in the market include 3M, Johnson & Johnson Services, Inc., Abbott, Becton, Dickinson & Company, Medtronic, B. Braun Melsungen AG, Bayer AG, Smith and Nephew, Medline Industries, Inc., and Cardinal Health.

Some of the recent developments of key Medical Disposables providers are as follows:

In April 2019, Smith & Nephew PLC purchased Osiris Therapeutics, Inc. with the goal of expanding its advanced wound management product range.

In May 2019, 3M announced the acquisition of Acelity Inc., with the goal of strengthening wound treatment products.

For More Information: https://www.futuremarketinsights.com/reports/medication-dispenser-market

More Insights Available

Future Market Insights, in its new offering, presents an unbiased analysis of the Medical Disposables Market, presenting historical market data (2018-2022) and forecast statistics for the period of 2023-2033.

The study reveals essential insights by Product (Surgical Instruments & Supplies, Infusion, and Hypodermic Devices, Diagnostic & Laboratory Disposables, Bandages and Would Dressings, Sterilization Supplies, Respiratory Devices, Dialysis Disposables, Medical & Laboratory Gloves), by Raw Material (Plastic Resin, Nonwoven Material, Rubber, Metal, Glass, Others), by End-use (Hospitals, Home Healthcare, Outpatient/Primary Care Facilities, Other End-use) across five regions (North America, Latin America, Europe, Asia Pacific and Middle East & Africa).

Market Segments Covered in Medical Disposables Industry Analysis

By Product Type:

Surgical Instruments & Supplies

Would Closures

Procedural Kits & Trays

Surgical Catheters

Surgical Instruments

Plastic Surgical Drapes

By Raw Material:

Plastic Resin

Nonwoven Material

Rubber

Metals

Glass

Other Raw Materials

By End-use:

Hospitals

Home Healthcare

Outpatient/Primary Care Facilities

Other End-uses

2 notes

·

View notes

Text

Bioplastics Market Share, Size, Global Driving Factors by Manufacturers, Growth Opportunities

The global bioplastics market size was USD 10.64 Billion in 2021 and is expected to register a revenue CAGR of 16.8% over the forecast period, according to the latest analysis by Emergen Research. Increase in demand for bioplastics from the automotive industry and demand for compostable plastics to improve soil quality are factors expected to support revenue growth of the market between 2022 and 2030. The automotive industry's primary objective and challenge is to reduce fuel consumption and pollutants by reducing vehicle weight. Bioplastics are effective materials for achieving this purpose. These smart plastics, such as bio-PA and bio-PP, have been embraced by major vehicle manufacturers to reduce environmental impact and provide additional strength to automobile components. Thus, demand for these plastics in the automotive industry owing to their excellent properties is anticipated to create lucrative growth prospects for companies in the market.

Get a sample of the Bioplastics Market report @ https://www.emergenresearch.com/request-sample/169

The global Bioplastics market report covers the analysis of drivers, trends, limitations, restraints, and challenges arising in the Bioplastics market. The report also discusses the impact of various other market factors affecting the growth of the market across various segments and regions. The report segments the market on the basis of types, applications, and regions to impart a better understanding of the Bioplastics market.

Emergen Research has segmented the global Bioplastics market on the basis of type, platform, application, and region:

Type Outlook (Revenue, USD Billion; 2017-2027)

Biodegradable

Polybutylene Adipate Terephthalate (PBAT)

Polybutylene Succinate (PBS)

Polylactic Acid (PLA)

Polyhydroxyalkanoate (PHA)

Starch Blends

Others

Distribution Channel Outlook (Revenue, USD Billion; 2017-2027)

Online

Offline

Application Outlook (Revenue, USD Billion; 2017-2027)

Packaging

Textile

Automotive & Transportation

Consumer Goods

Agriculture

Building & Construction

Others

Request a discount on the Bioplastics Market report @ https://www.emergenresearch.com/request-discount/169

Based on the competitive landscape, the market report analyzes the key companies operating in the industry:

BASF SE, NatureWorks, Biome Plastics, Braskem, Biotec, Total Corbion, Plantic Technologies, Mitsubishi Chemical Holdings Corporation, Novamont SPA, and Toray Industries

Additionally, the report covers the analysis of the key players in the industry with a special focus on their global position, financial status, and their recent developments. Porter’s Five Forces Analysis and SWOT analysis have been covered by the report to provide relevant data on the competitive landscape.

How will this Report Benefit you?

An Emergen Research report of 250 pages contains 194 tables, 189 charts and graphics, and anyone who needs a comprehensive analysis of the global Bioplastics market, as well as commercial, in-depth analyses of the individual segments, will find the study useful. Our recent study allows you to assess the entire regional and global market for Bioplastics. In order to increase market share, obtain financial analysis of each segment and the whole market. Look at how you can utilize the current and potential revenue-generating opportunities available in this sector. We believe that there are significant prospects for energy storage technology in this industry due to the rapid expansion of the technology. In addition to helping you build growth strategies, improve competitor analysis, and increase business productivity, the research will also assist you in making better strategic decisions.

Detailed Regional Analysis covers:

North America (U.S., Canada)

Europe (U.K., Italy, Germany, France, Rest of EU)

Asia-Pacific (India, Japan, China, South Korea, Australia, Rest of APAC)

Latin America (Chile, Brazil, Argentina, Rest of Latin America)

Middle East & Africa (Saudi Arabia, U.A.E., South Africa, Rest of MEA)

To Study Full Bioplastics Market Report, click here @ https://www.emergenresearch.com/industry-report/bioplastics-market

What Questions Should You Ask before Buying a Market Research Report?

How is the Bioplastics market evolving?

What is driving and restraining the Bioplastics market?

How will each Bioplastics submarket segment grow over the forecast period and how much revenue will these submarkets account for in 2027?

How will the market shares for each Bioplastics submarket develop from 2020 to 2027?

What will be the main driver for the overall market from 2020 to 2027?

Will leading Bioplastics markets broadly follow the macroeconomic dynamics, or will individual national markets outperform others?

How will the market shares of the national markets change by 2027 and which geographical region will lead the market in 2027?

Who are the leading players and what are their prospects over the forecast period?

What are the Bioplastics projects for these leading companies?

How will the industry evolve during the period between 2020 and 2027? What are the implications of Bioplastics projects taking place now and over the next 10 years?

Is there a greater need for product commercialisation to further scale the Bioplastics market?

Where is the Bioplastics market heading and how can you ensure you are at the forefront of the market?

What are the best investment options for new product and service lines?

What are the key prospects for moving companies into a new growth path and C-suite?

Request customization on the report @ https://www.emergenresearch.com/request-for-customization/169

Thank you for reading our report. To know more about the customization of the report, please get in touch with us, and our team will ensure the report is suited to your requirements.

About Us:

Emergen Research is a market research and consulting company that provides syndicated research reports, customized research reports, and consulting services. Our solutions purely focus on your purpose to locate, target, and analyse consumer behavior shifts across demographics, across industries, and help clients make smarter business decisions. We offer market intelligence studies ensuring relevant and fact-based research across multiple industries, including Healthcare, Touch Points, Chemicals, Types, and Energy. We consistently update our research offerings to ensure our clients are aware of the latest trends existent in the market. Emergen Research has a strong base of experienced analysts from varied areas of expertise. Our industry experience and ability to develop a concrete solution to any research problems provides our clients with the ability to secure an edge over their respective competitors.

For More Related Reports by Emergen Research

gambling software market: https://www.emergenresearch.com/industry-report/gambling-software-market

functional ingredients market: https://www.emergenresearch.com/industry-report/functional-ingredients-market

space mining market: https://www.emergenresearch.com/industry-report/space-mining-market

acrylic resins market: https://www.emergenresearch.com/industry-report/acrylic-resins-market

drone logistics and transportation market: https://www.emergenresearch.com/industry-report/drone-logistics-and-transportation-market

targeted therapeutics market: https://www.emergenresearch.com/industry-report/targeted-therapeutics-market

airborne intelligence surveillance and reconnaissance market: https://www.emergenresearch.com/industry-report/airborne-intelligence-surveillance-and-reconnaissance-market

small caliber ammunition market: https://www.emergenresearch.com/industry-report/small-caliber-ammunition-market

1 note

·

View note

Text

Ethylene Market In-depth Analysis and Comprehensive Assessment Report 2024 to 2033

The ethylene market is a major segment of the petrochemical industry and plays a critical role in global manufacturing. Ethylene is one of the most widely used chemical compounds, serving as a primary building block for various essential materials, including polyethylene, ethylene oxide, and ethylene dichloride. These derivatives are extensively used in producing plastics, textiles, automotive components, packaging, construction materials, and pharmaceuticals. With demand spread across a diverse range of sectors, the ethylene market is a key player in global industrial development.

Market Overview and Size

The Global Ethylene Market is projected to reach approximately USD 304.6 Billion by 2033, increasing from USD 177.7 Billion in 2023, with a compound annual growth rate (CAGR) of 5.6% during the forecast period from 2023 to 2033. Growth in this market is primarily driven by the expanding consumer base for products made from ethylene derivatives and the growing demand for plastic and synthetic materials across multiple industries. The market is also heavily influenced by the price of crude oil and natural gas, as these are primary feedstocks for ethylene production.

Get Information About This Report: https://infinitymarketresearch.com/ethylene-market/1060

Key Drivers of the Ethylene Market

Growth in the Plastic and Packaging Industries A significant portion of ethylene is used to produce polyethylene, one of the most widely used plastics. Polyethylene is essential in manufacturing plastic bags, containers, and packaging materials, which are in constant demand due to the booming e-commerce and retail sectors. The growth in packaging requirements—driven by increased online shopping and a shift toward lightweight packaging in industries like food, beverages, and consumer goods—continues to be a major growth driver for the ethylene market.

Demand from Automotive and Construction Sectors Ethylene-derived materials like polypropylene, styrene, and polyvinyl chloride (PVC) are crucial in automotive and construction applications. In the automotive industry, lightweight materials are increasingly used to enhance fuel efficiency. In the construction industry, PVC pipes, fittings, and insulation materials are essential for both residential and commercial structures. With expanding infrastructure development in emerging markets, the demand from these industries is expected to fuel ethylene consumption in the coming years.

Advancements in Production Technologies Technological advancements in ethylene production have significantly improved production efficiency and reduced costs. Modern methods, such as cracking technology and catalytic processes, allow companies to convert naphtha and ethane into ethylene with greater energy efficiency and lower environmental impact. In addition, companies are investing in sustainable production technologies, such as bio-based ethylene, to reduce the industry’s carbon footprint and comply with increasing environmental regulations.

Regional Insights

Asia-Pacific The Asia-Pacific region dominates the ethylene market, with China, India, and Japan as major consumers. This region’s growth is driven by rapid industrialization, urbanization, and increasing consumer spending on goods made from ethylene derivatives. China, in particular, has seen a tremendous rise in demand due to its robust manufacturing sector, which includes automotive, electronics, and consumer goods industries. Additionally, Asia-Pacific is investing heavily in new ethylene production facilities to reduce reliance on imports and support local demand.

North America North America is a significant player in the ethylene market, largely due to the abundance of shale gas reserves in the United States. The shale gas boom has provided a low-cost feedstock (ethane) for ethylene production, allowing the U.S. to emerge as a global ethylene exporter. With the presence of advanced production technologies and investments in petrochemical infrastructure, North America is expected to maintain its influence in the global ethylene market.

Europe Europe’s ethylene market is more moderate in growth due to stringent environmental regulations and a high degree of market maturity. However, demand from the automotive and construction industries continues to drive moderate growth in ethylene consumption. Additionally, Europe is actively working on producing bio-based ethylene and recycling initiatives to address environmental concerns and reduce dependence on fossil fuels.

Challenges in the Ethylene Market

Environmental Concerns and Regulatory Challenges The ethylene industry faces increasing scrutiny over its environmental impact, as ethylene production is energy-intensive and generates considerable carbon emissions. Regulatory pressure is mounting on the industry to adopt cleaner, more sustainable production methods. As a result, companies are investing in carbon capture and storage (CCS) technologies and renewable feedstocks to minimize their environmental footprint.

Volatility in Raw Material Prices Ethylene production relies heavily on crude oil and natural gas as raw materials, making the market sensitive to fluctuations in their prices. Price volatility due to geopolitical tensions, trade policies, and supply-demand imbalances can impact production costs and profitability. To counter this, companies are diversifying feedstock sources and adopting flexible production technologies that can switch between different raw materials depending on cost and availability.

Competition from Alternative Materials The push for environmentally sustainable alternatives is driving research into bio-based and recycled plastics, which could potentially substitute petrochemical-based ethylene products. These alternative materials have gained popularity in industries seeking eco-friendly solutions, posing a potential challenge to the ethylene market’s growth.

Key Players:

o Chevron Phillips Chemical Company LLC

o China Petroleum & Chemical Corporation (Sinopec)

o Mitsui Chemicals Inc.

o LyondellBasell Industries N.V.

o Exxon Mobil Corporation

o Saudi Basic Industries Corporation

o Ineos Group Ltd

o The Dow Chemical Company

o Royal Dutch Shell plc

o LG Chem Ltd.

o Mitsui Chemicals Inc.

o Other Key Players

Get Free Sample Copy Of Report: https://infinitymarketresearch.com/request-sample/1060

Future Outlook and Opportunities

The ethylene market is expected to continue its growth trajectory, driven by demand from emerging markets and ongoing industrial applications. Companies are actively pursuing strategies to make the ethylene industry more sustainable, including investment in bio-based ethylene, recycling technologies, and energy-efficient production methods. Additionally, with growing global attention on sustainability, bio-based ethylene and renewable energy sources will likely play a larger role in the industry’s future.

Investments in research and development are expected to foster innovations that lower production costs, reduce environmental impact, and enhance the performance of ethylene derivatives. The expansion of industries such as packaging, automotive, and construction in emerging economies is also anticipated to provide long-term opportunities in the ethylene market.

Related Reports:

Glyceryl Triacetate Market Trends and Growth | Report 2033 : https://infinitymarketresearch.com/glyceryl-triacetate-market/1223

Diisopropyl Ether (DIPE) Market Trends, Growth | Report 2033: https://infinitymarketresearch.com/diisopropyl-ether-(dipe)-market/1243

Atomized Metal Powder Market Size, Growth, Trends, Report 2033: https://infinitymarketresearch.com/atomized-metal-powder-market/1250

Fire Resistant Tapes Market Size, Growth, Trends, Report 2033: https://infinitymarketresearch.com/fire-resistant-tapes-market/1281

Ceramic Additive Manufacturing Market Size, Growth, Report 2033: https://infinitymarketresearch.com/ceramic-additive-manufacturing-market/1280

About US:

We at Infinity Market Research hold expertise in providing up-to-date, authentic and reliable information across all the industry verticals. Our diverse database consists of information gathered from trusted and authorized data sources.

We take pride in offering high quality and comprehensive research solution to our clients. Our research solutions will help the clients in making an informed move and planning the business strategies. We strive to provide excellent and dedicated market research reports so that our clients can focus on growth and business development plans. We have domain-wise expert research team who work on client-specific custom projects. We understand the diverse requirements of our clients and keep our reports update based on the market scenario.

Contact US:

Pune, Maharashtra, India

Mail: [email protected]

Website: https://infinitymarketresearch.com/

#EthyleneMarket#Petrochemicals#SustainableManufacturing#PlasticsIndustry#IndustrialGrowth#EthyleneProduction#ChemicalIndustry#PackagingDemand#GlobalMarkets

0 notes

Text

Masterbatch Market 2030 Driving Factors, Future Trends, Size & Key Vendors

In 2023, the global masterbatch market reached a valuation of USD 6.24 billion and is projected to grow at a compound annual growth rate (CAGR) of 6.3% from 2024 to 2030. Masterbatch is used to add color to polymers and enhance their properties, making it highly suitable for applications across diverse industries, such as automotive, transportation, building and construction, consumer goods, and packaging. A key factor driving this market growth is the shift from metal to plastic components in various end-use sectors due to plastics’ lighter weight, cost-effectiveness, and versatile properties.

Masterbatch products are available in solid and liquid forms, and they enhance polymers with properties such as antistatic, antifog, antilocking, UV stabilization, and flame retardation. These enhancements are achieved by combining masterbatch with various carrier polymers like polypropylene, polyethylene, polyvinyl chloride, and polyethylene terephthalate. These materials can then be used in key manufacturing processes, including injection molding and extrusion, which are crucial for producing plastic components across many industries.

Gather more insights about the market drivers, restrains and growth of the Masterbatch Market

In the United States, growing demand from the packaging sector is expected to be a significant driver of masterbatch market growth. This demand surge is linked to the rapid expansion of the e-commerce industry, which has increased the need for durable, attractive packaging solutions. The U.S. hosts over 16,800 plastic manufacturing facilities nationwide, highlighting the scale of plastic usage in consumer goods, construction, automotive, and other industries. Manufacturers are increasingly focusing on visually appealing packaging to attract consumers, particularly in competitive markets. Masterbatch is used to create vibrant, diverse packaging designs that enhance consumer appeal, which is expected to further boost demand.

Moreover, masterbatch applications are expanding into new areas within the packaging industry. For instance, in July 2023, Gerdau Graphene and Brazilian film manufacturer Packseven developed a graphene-enhanced stretch film using masterbatch technology. This advanced film, produced with graphene masterbatch, allows for a 25% reduction in plastic usage while maintaining film strength and durability. This example highlights how innovation in masterbatch technology can lead to material savings and increased efficiency in packaging.

End-use Segmentation Insights:

In 2023, the packaging sector led the masterbatch market, capturing a revenue share of 26.91%. The strong demand for packaging spans across retail, industrial, and consumer segments, including both flexible and rigid packaging options. The rising urban population, particularly in metropolitan areas, has intensified the demand for packaged goods, which, in turn, drives the need for masterbatch in the packaging industry. Consumers are increasingly looking for packaging that is convenient, sustainable, flexible, protective, and traceable. Since plastic packaging can meet all these criteria, its demand is expected to rise, thereby boosting the demand for masterbatch.

The packaging industry is also witnessing strong growth potential in emerging markets, particularly in countries like India and China, where rapid urbanization and economic growth are fueling demand. These countries are investing heavily in infrastructure, leading to an increase in building and construction activities. This growth in construction fuels demand for masterbatch, as the construction industry uses plastics for applications such as insulation, piping, and coatings. Government initiatives, such as India’s "Make in India" and the Smart Cities Mission, are expected to stimulate construction projects further, thus driving the demand for masterbatch products in these regions.

In summary, the masterbatch market is expanding due to its ability to enhance the functionality and aesthetics of plastics in numerous applications. With increasing demand from the packaging industry, coupled with innovative new applications like graphene-enhanced films, the masterbatch market is poised for steady growth. Additionally, emerging economies and large-scale construction activities are anticipated to contribute significantly to the demand for masterbatch, making it a crucial material for the future of diverse industries globally.

Order a free sample PDF of the Masterbatch Market Intelligence Study, published by Grand View Research.

0 notes

Text

Masterbatch Industry Share and Specification forecast To 2030

In 2023, the global masterbatch market reached a valuation of USD 6.24 billion and is projected to grow at a compound annual growth rate (CAGR) of 6.3% from 2024 to 2030. Masterbatch is used to add color to polymers and enhance their properties, making it highly suitable for applications across diverse industries, such as automotive, transportation, building and construction, consumer goods, and packaging. A key factor driving this market growth is the shift from metal to plastic components in various end-use sectors due to plastics’ lighter weight, cost-effectiveness, and versatile properties.

Masterbatch products are available in solid and liquid forms, and they enhance polymers with properties such as antistatic, antifog, antilocking, UV stabilization, and flame retardation. These enhancements are achieved by combining masterbatch with various carrier polymers like polypropylene, polyethylene, polyvinyl chloride, and polyethylene terephthalate. These materials can then be used in key manufacturing processes, including injection molding and extrusion, which are crucial for producing plastic components across many industries.

Gather more insights about the market drivers, restrains and growth of the Masterbatch Market

In the United States, growing demand from the packaging sector is expected to be a significant driver of masterbatch market growth. This demand surge is linked to the rapid expansion of the e-commerce industry, which has increased the need for durable, attractive packaging solutions. The U.S. hosts over 16,800 plastic manufacturing facilities nationwide, highlighting the scale of plastic usage in consumer goods, construction, automotive, and other industries. Manufacturers are increasingly focusing on visually appealing packaging to attract consumers, particularly in competitive markets. Masterbatch is used to create vibrant, diverse packaging designs that enhance consumer appeal, which is expected to further boost demand.

Moreover, masterbatch applications are expanding into new areas within the packaging industry. For instance, in July 2023, Gerdau Graphene and Brazilian film manufacturer Packseven developed a graphene-enhanced stretch film using masterbatch technology. This advanced film, produced with graphene masterbatch, allows for a 25% reduction in plastic usage while maintaining film strength and durability. This example highlights how innovation in masterbatch technology can lead to material savings and increased efficiency in packaging.

End-use Segmentation Insights:

In 2023, the packaging sector led the masterbatch market, capturing a revenue share of 26.91%. The strong demand for packaging spans across retail, industrial, and consumer segments, including both flexible and rigid packaging options. The rising urban population, particularly in metropolitan areas, has intensified the demand for packaged goods, which, in turn, drives the need for masterbatch in the packaging industry. Consumers are increasingly looking for packaging that is convenient, sustainable, flexible, protective, and traceable. Since plastic packaging can meet all these criteria, its demand is expected to rise, thereby boosting the demand for masterbatch.

The packaging industry is also witnessing strong growth potential in emerging markets, particularly in countries like India and China, where rapid urbanization and economic growth are fueling demand. These countries are investing heavily in infrastructure, leading to an increase in building and construction activities. This growth in construction fuels demand for masterbatch, as the construction industry uses plastics for applications such as insulation, piping, and coatings. Government initiatives, such as India’s "Make in India" and the Smart Cities Mission, are expected to stimulate construction projects further, thus driving the demand for masterbatch products in these regions.

In summary, the masterbatch market is expanding due to its ability to enhance the functionality and aesthetics of plastics in numerous applications. With increasing demand from the packaging industry, coupled with innovative new applications like graphene-enhanced films, the masterbatch market is poised for steady growth. Additionally, emerging economies and large-scale construction activities are anticipated to contribute significantly to the demand for masterbatch, making it a crucial material for the future of diverse industries globally.

Order a free sample PDF of the Masterbatch Market Intelligence Study, published by Grand View Research.

0 notes

Text

Future of 3D Printing Plastics Market: Trends and Predictions

The global 3D printing plastics market was valued at USD 1.20 billion in 2024 and is projected to experience robust growth at a compound annual growth rate (CAGR) of 24.2% from 2025 to 2030. This growth is driven by the increasing demand for customized and personalized products, which is spurring innovation in the 3D printing sector. As industries seek more flexible, efficient, and cost-effective manufacturing solutions, the demand for high-quality 3D printing plastics continues to rise.

One of the key factors propelling the growth of the 3D printing plastics market is the shift toward sustainable and eco-friendly materials. As global industries adopt more responsible manufacturing practices, the use of bioplastics and recycled plastics in 3D printing has surged. This transition is being driven by stringent environmental regulations and a growing consumer preference for products with a smaller environmental footprint. Companies are heavily investing in research and development (R&D) to create biodegradable plastics that offer similar or superior performance to traditional plastics but with a much-reduced environmental impact. These materials are particularly valuable in industries such as healthcare and consumer goods, where sustainability is becoming an increasing priority.

Gather more insights about the market drivers, restrains and growth of the 3D Printing Plastics Market

Regional Insights

North America 3D Printing Plastics Market

The North American 3D printing plastics market is growing steadily, driven by the rise in on-demand manufacturing and rapid prototyping. Industries such as aerospace, automotive, and healthcare are increasingly adopting 3D printing technologies to reduce lead times, minimize material waste, and produce high-performance plastic parts with complex designs. The presence of a well-established ecosystem of 3D printing service providers and material manufacturers in the region is further supporting market growth. Specialized plastics like Nylon, ABS, and PEEK are particularly popular in the region’s industrial applications.

The U.S., in particular, has been at the forefront of technological innovation in 3D printing, and the government’s support for advanced manufacturing has provided a boost to the 3D printing plastics market. This, combined with the region's strong infrastructure for innovation, makes North America a key player in the market.

U.S. 3D Printing Plastics Market Trends

In the U.S., the 3D printing plastics market is seeing significant adoption, particularly in the healthcare and aerospace industries, where precision, customization, and performance are critical. In the healthcare sector, the production of patient-specific implants, prosthetics, and surgical tools is growing rapidly, with biocompatible and durable plastics like PLA and PEEK playing a central role. These materials are prized for their strength, durability, and compatibility with human tissue, making them essential for medical applications.

In the aerospace industry, 3D printing is increasingly used to create lightweight, heat-resistant components that help reduce fuel consumption and improve performance. The U.S. government's focus on maintaining its technological leadership in manufacturing, along with the presence of leading companies in the 3D printing space, contributes to the market’s expansion in the region.

Asia Pacific 3D Printing Plastics Market

The Asia Pacific region accounted for the largest revenue share of 33.7% in 2024, driven by rapid industrialization and the growing adoption of advanced manufacturing technologies in countries like China, India, and Japan. Governments across the region are heavily investing in 3D printing technology as part of broader initiatives aimed at modernizing the manufacturing sector and strengthening local industries. This investment is fueling demand for 3D printing plastics in several key sectors, including electronics, automotive, and healthcare.

In particular, the rising demand for high-performance plastic materials in the production of lightweight, complex components is a major factor supporting the market’s growth. Additionally, the rise of small and medium-sized enterprises (SMEs) using 3D printing technology for customized production is accelerating the adoption of 3D printing plastics in the region.

China 3D Printing Plastics Market

China is a major force in the Asia Pacific 3D printing plastics market, driven by the country’s rapid advancements in manufacturing technologies and its ambition to become a global leader in 3D printing. The Chinese government has made 3D printing a focal point of its "Made in China 2025" initiative, which aims to upgrade the country’s manufacturing capabilities. This has led to an increase in demand for 3D printing plastics across industries such as electronics, consumer goods, and construction.

China’s ability to provide low-cost raw materials, combined with its strong local supply chains, is further enhancing the widespread adoption of 3D printing plastics in the country. As the demand for more complex and high-quality products grows, Chinese manufacturers are increasingly turning to 3D printing as a way to produce efficient and cost-effective products.

Europe 3D Printing Plastics Market

The Europe 3D printing plastics market is expanding, driven by a growing emphasis on sustainability and the circular economy. European manufacturers are increasingly using eco-friendly materials such as biodegradable and recycled plastics in their 3D printing processes, aligning with strict environmental regulations in the region. The automotive and aerospace industries, in particular, are leveraging 3D printing to produce lightweight components that help reduce emissions and improve fuel efficiency.

Browse through Grand View Research's Plastics, Polymers & Resins Industry Research Reports.

• The global bioplastics market size was estimated at USD 15.57 billion in 2024 and is expected to grow at a CAGR of 19.5% from 2025 to 2030.

• The global nylon market size was estimated at USD 34.39 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 6.5% from 2024 to 2030.

Key 3D Printing Plastics Company Insights

The 3D printing plastics market is highly competitive, with several key players leading the industry. Major companies in this sector are making substantial investments in research and development to improve the performance, cost-effectiveness, and sustainability of their products.

Key 3D Printing Plastics Companies

Some of the leading companies in the 3D printing plastics market include:

• 3D Systems Corporation

• Arkema Inc.

• Envisiontec Inc.

• Stratasys Ltd.

• SABIC

• Materialse nv

• HP INC.

• Eos GmbH Electro Optical Systems

• PolyOne Corporation

• Royal DSM N.V.

Order a free sample PDF of the 3D Printing Plastics Market Intelligence Study, published by Grand View Research.

#3D Printing Plastics Market#3D Printing Plastics Market Analysis#3D Printing Plastics Market Report#3D Printing Plastics Market Regional Insights

0 notes

Text

Turning Waste into Energy: The Future of Refuse-Derived Fuel

The global refuse derived fuel (RDF) market is anticipated to experience substantial growth over the forecast period from 2022 to 2028, driven by increasing demand for alternative fuel sources, waste-to-energy initiatives, and growing environmental concerns regarding waste management. RDF, derived from processing non-recyclable municipal, commercial, and industrial solid wastes, serves as a valuable fuel source, primarily in industries like cement, power generation, and steel manufacturing.

What is Refuse Derived Fuel (RDF)?

Refuse derived fuel is produced by sorting, shredding, and drying non-recyclable waste materials, such as plastics, textiles, and wood, to create a high-calorific fuel source. RDF offers an environmentally friendly alternative to conventional fossil fuels, as it reduces waste volume, minimizes landfill dependency, and lowers greenhouse gas emissions. RDF is increasingly being used in facilities designed to utilize waste-to-energy technologies, including incineration and co-firing with other fuels.

Get Sample pages of Report: https://www.infiniumglobalresearch.com/reports/sample-request/41269

Market Dynamics and Growth Drivers

Several factors are driving the global RDF market:

Increasing Waste-to-Energy Projects: Governments and private organizations worldwide are investing in waste-to-energy facilities, where RDF can be an efficient fuel source. These projects reduce landfill pressure, manage waste sustainably, and contribute to a circular economy.

Demand for Alternative Fuels in Industrial Sectors: High energy demand and an emphasis on sustainability drive industries, particularly cement and power plants, to adopt RDF as an alternative fuel, lowering their carbon footprint and fuel costs.

Stringent Environmental Regulations: Regulations targeting landfill waste reduction and encouraging renewable energy adoption promote the use of RDF, pushing industries to comply with eco-friendly waste management practices.

Growing Focus on Reducing Greenhouse Gas Emissions: The RDF market supports global emissions reduction goals by offering an alternative to fossil fuels. RDF usage decreases the carbon intensity of industrial processes, particularly in energy-intensive sectors, where fuel-based emissions are a major environmental concern.

Regional Analysis

Europe: Europe is a leader in the RDF market due to well-established waste management systems, regulatory support, and a high number of waste-to-energy facilities. Countries like Germany, Sweden, and the Netherlands have adopted RDF widely, supported by government policies emphasizing recycling and alternative fuel sources.

North America: The North American market, particularly the U.S., is expanding its RDF applications as industries seek alternative fuels. Though regulations vary by state, many regions are investing in waste-to-energy projects and encouraging RDF use to reduce landfill dependency and support sustainable energy.

Asia-Pacific: Rapid urbanization, increasing industrial activity, and a focus on sustainable waste management drive RDF market growth in the Asia-Pacific region. Countries such as China, India, and Japan are exploring RDF applications as part of their waste-to-energy initiatives, presenting significant growth potential for the market.

Latin America, Middle East, and Africa: These regions are gradually adopting RDF, supported by growing awareness of waste management benefits and environmental regulations. While growth rates are modest, improvements in waste collection and processing infrastructure support market expansion.

Competitive Landscape

The RDF market is fragmented, with numerous players focusing on regional markets and specific industries. Key players include:

Veolia Environment: Veolia provides RDF solutions for industrial applications, focusing on sustainable waste management and recycling. The company operates in multiple regions, leveraging its expertise in waste-to-energy technologies.

SUEZ: SUEZ specializes in RDF production and waste management services, particularly in Europe. The company collaborates with municipalities and industries to manage non-recyclable waste and generate alternative fuel sources.

Renewi PLC: Operating primarily in Europe, Renewi provides RDF through its waste processing facilities. The company emphasizes sustainable waste-to-fuel solutions and caters to industrial sectors seeking low-carbon energy options.

Biffa: A leading waste management provider in the UK, Biffa processes RDF from municipal and commercial waste. The company aims to reduce landfill waste and increase waste-derived fuel production.

Covanta: Covanta focuses on waste-to-energy projects, including RDF processing in the U.S. The company’s facilities convert municipal waste into RDF, which is then used to produce electricity and reduce landfill usage.

Report Overview : https://www.infiniumglobalresearch.com/reports/global-refuse-derived-fuel-market

Challenges and Opportunities

Despite its growth potential, the RDF market faces challenges such as high production and processing costs, limited adoption in emerging economies due to insufficient waste management infrastructure, and regulatory complexities. However, these challenges also offer opportunities for market expansion:

Technological Innovations: Advances in waste processing technologies, such as improved sorting and treatment methods, enhance RDF production efficiency and reduce associated costs.

Partnerships with Municipalities and Industries: Collaboration with government bodies and industries can boost RDF adoption, as partnerships facilitate regulatory compliance and financial incentives.

Sustainability Commitments by Industries: Industries across the globe are increasingly setting sustainability goals, which creates a favorable environment for RDF. As more companies commit to reducing their carbon footprint, RDF emerges as a practical solution for achieving these goals.

Conclusion

The global refuse derived fuel market is poised for significant growth, supported by increasing investments in sustainable waste management and the rising adoption of waste-to-energy technologies. As governments and industries strive to meet environmental targets, RDF offers a viable solution, providing an alternative fuel source that reduces landfill use, greenhouse gas emissions, and reliance on fossil fuels. With ongoing advancements in waste processing technology and a shift toward circular economies, RDF's role in energy production and sustainable waste management is expected to expand, presenting substantial opportunities for both market entrants and established players.

Discover More of Our Reports

Vietnam Aseptic Packaging Market

Vietnam Biodegradable Packaging Market

0 notes

Text

U.S. Affordable 3D Printing Solutions for Home Businesses: Market Insights and Growth Opportunities

Introduction

The rise of affordable 3D printing technology has opened new doors for entrepreneurship in the U.S., particularly for home-based businesses. With a compound annual growth rate (CAGR) of approximately 21% projected from 2024 to 2030, this market is witnessing rapid expansion and transformation. This blog post explores the various facets of the affordable 3D printing market, its significance for home businesses, challenges, and future prospects.

For more details: https://www.xinrenresearch.com/regional-reports/u-s-affordable-3d-printing-solutions-for-home-businesses-market/

1. Understanding the Affordable 3D Printing Market

1.1. Definition and Scope

Affordable 3D printing refers to the range of additive manufacturing technologies and machines that are accessible to small businesses and individual entrepreneurs. These technologies allow users to create three-dimensional objects from digital files, utilizing various materials such as plastics, metals, and even biological materials. The affordability aspect is crucial, as it enables individuals to leverage this technology without substantial financial investment.

1.2. Historical Context

3D printing technology has evolved significantly since its inception in the 1980s. Originally limited to prototyping in large corporations, advancements in technology have led to the development of cost-effective, user-friendly printers suitable for small businesses. The last decade has seen a surge in the availability of affordable models, which has fueled interest among entrepreneurs and hobbyists alike.

1.3. Market Dynamics

The affordable 3D printing market is influenced by various factors, including:

Technological Advancements: Continuous improvements in printing speed, resolution, and material diversity are making 3D printing more accessible and appealing to small businesses.

Increased Demand for Customization: Consumers increasingly seek personalized products, creating a demand for businesses that can provide tailored solutions.

Sustainability Concerns: As environmental issues become more prominent, businesses are looking for sustainable manufacturing processes, which 3D printing can offer through reduced material waste and energy consumption.

2. Advantages of 3D Printing for Home Businesses

2.1. Cost-Effective Production

Affordable 3D printing enables home businesses to produce items at a fraction of the cost of traditional manufacturing methods. By eliminating the need for expensive molds or tooling, entrepreneurs can create low-volume products economically. This cost-effectiveness is especially beneficial for startups that require flexibility in their production processes.

2.2. Rapid Prototyping

One of the significant advantages of 3D printing is the ability to quickly create prototypes. Entrepreneurs can develop and test their ideas rapidly, making modifications based on feedback before launching a product. This iterative process accelerates product development and reduces the time-to-market for new offerings.

2.3. Space Efficiency

Home-based businesses often operate within limited space constraints. 3D printers are typically compact and can fit into small work areas. This space efficiency allows entrepreneurs to manage their production processes without needing extensive facilities or equipment.

2.4. Diverse Applications

3D printing technology is versatile, enabling businesses to create various products, from functional parts and prototypes to decorative items and custom gifts. This diversity allows entrepreneurs to tap into multiple markets and cater to various customer needs.

3. Market Challenges for Home Businesses

3.1. Quality and Consistency

While affordable 3D printers offer many advantages, quality control can be a concern. Lower-end models may produce inconsistent results, leading to defects or inferior products. Entrepreneurs must invest time in learning about their machines and experimenting with different materials and settings to achieve consistent quality.

3.2. Material Limitations

Many affordable 3D printers are limited in the types of materials they can use. While plastics are the most common, entrepreneurs looking to diversify their product offerings may find these limitations restrictive. To address this challenge, businesses can seek printers that support a wider range of materials, including composites and specialty filaments.

3.3. Technical Expertise

Operating a 3D printer requires a certain level of technical expertise, from designing models to troubleshooting issues. For many entrepreneurs, this can be a steep learning curve. However, numerous online resources, tutorials, and communities are available to help users develop the necessary skills and knowledge.

4. Future Trends and Opportunities

4.1. Advancements in Technology

The affordable 3D printing market is poised for continuous growth, driven by technological advancements. Innovations such as faster printing speeds, improved material compatibility, and enhanced user interfaces will further lower barriers to entry and make 3D printing more appealing to home businesses.

4.2. Sustainable Practices

As sustainability becomes a primary concern for consumers and businesses, 3D printing is well-positioned to meet these demands. The technology allows for on-demand production, reducing waste associated with traditional manufacturing methods. Entrepreneurs can leverage this eco-friendly aspect to attract environmentally conscious customers.

4.3. Customization and Personalization

The growing trend of customization is a significant driver for the affordable 3D printing market. Businesses that can provide personalized products will stand out in a competitive landscape. As consumers increasingly seek unique items, home businesses that embrace 3D printing will have the opportunity to thrive.

4.4. Hybrid Manufacturing Approaches

Hybrid manufacturing, which combines traditional methods with 3D printing, is gaining traction. Entrepreneurs can benefit from this approach by leveraging the strengths of both technologies, enhancing their production capabilities while maintaining cost-effectiveness.

5. Key Players and Competitive Landscape

5.1. Major Manufacturers

The affordable 3D printing market is populated by various key players offering a range of printers and materials. Some notable manufacturers include:

MakerBot: Known for its user-friendly printers, MakerBot has become a popular choice among educators and hobbyists.

Prusa Research: This company is celebrated for its open-source approach, allowing users to modify and improve their printers.

Creality: With a reputation for affordability, Creality offers a range of printers catering to different user needs.

5.2. Startups and Emerging Players

The market is also witnessing the emergence of innovative startups focused on niche applications or specific materials. These companies often drive creativity and innovation, pushing the boundaries of what affordable 3D printing can achieve.

5.3. Market Positioning

As the market continues to expand, businesses must carefully consider their positioning. Identifying target audiences, understanding competitive offerings, and developing unique value propositions will be crucial for success in this evolving landscape.

6. Conclusion

The U.S. affordable 3D printing market presents significant opportunities for home businesses, with a projected CAGR of approximately 21% from 2024 to 2030. As technology continues to advance, entrepreneurs can leverage the benefits of cost-effective production, rapid prototyping, and customization to create unique products that meet the evolving demands of consumers.

While challenges such as quality control and material limitations exist, the rewards of embracing affordable 3D printing far outweigh the obstacles. By staying informed about market trends, investing in skills development, and adopting sustainable practices, home-based businesses can position themselves for long-term success in this dynamic market.

As we look to the future, the potential of affordable 3D printing to revolutionize small-scale manufacturing is undeniable. Entrepreneurs who embrace this technology will not only enhance their business prospects but also contribute to the broader narrative of innovation and sustainability in the U.S. economy.

For more reports: https://www.xinrenresearch.com/

0 notes

Text

Medical Plastics Market Leading Players, Survey, Status and Trends Report by 2030

The global medical plastics market was valued at approximately USD 52.9 billion in 2023 and is forecasted to expand at a compound annual growth rate (CAGR) of 7.4% from 2024 to 2030. This growth is largely attributed to advancements in specialized plastics and plastic composites, which are integral in manufacturing various medical components such as catheters, surgical instrument handles, and syringes. The rising demand for in-house and advanced medical devices is propelling the need for durable, lightweight materials like polyethylene, polypropylene, and polycarbonate, which are increasingly used in medical device manufacturing. Furthermore, the expanding home healthcare sector, which is more cost-effective than hospital-based care, has also significantly increased the demand for medical devices that rely on medical plastics for portability, durability, and safety.

According to the most recent U.S. census data, approximately 16.8% of the U.S. population is aged 65 or older, with this demographic expected to reach 74 million by 2030. Among this population, those aged over 85 require the most intensive healthcare, and their numbers are growing rapidly. In March 2021, President Joe Biden proposed a significant investment of USD 400 billion over eight years for Medicaid, aimed at expanding at-home care for the elderly and disabled populations while raising caregivers' wages. In the U.S., increasing costs and shrinking profit margins for healthcare providers have driven the government to overhaul healthcare funding and insurance through initiatives like the Affordable Care Act (ACA) and Medicaid reforms to make healthcare more accessible and affordable.

Gather more insights about the market drivers, restrains and growth of the Medical Plastics Market

The market is experiencing a high growth stage, with an accelerated pace due to its consolidation. Medical plastic manufacturers are increasingly pursuing strategic moves such as mergers and acquisitions, product launches, and production expansions to strengthen their competitive positioning. For example, in November 2023, TekniPlex Healthcare acquired Seisa Medical, a medical device manufacturer based in El Paso, Texas. This acquisition allows TekniPlex to leverage Seisa’s expertise in materials science and processing technology for interventional therapy and minimally invasive devices on a global scale. Seisa offers contract manufacturing services across the entire product development cycle for Class II and III medical devices, including component manufacturing, assembly, and packaging, all of which are critical for expanding TekniPlex’s global capabilities.

Application Segmentation Insights:

In 2023, the medical components segment led the market, accounting for over 40.0% of revenue share. The COVID-19 pandemic significantly drove demand for essential medical components such as personal protective equipment (PPE), face masks, gloves, gowns, and technology-intensive devices like magnetic resonance imaging (MRI) scanners. Emerging markets played a key role in manufacturing PPE, face masks, and gloves, while developed markets primarily focused on producing high-tech equipment such as MRI scanners and ventilators. The global surge in demand for these products during the pandemic highlights the importance of medical plastics in facilitating healthcare responses, thereby fueling growth in the medical components segment.

Medical device packaging is essential for maintaining device integrity and performance over its shelf life. Proper packaging protects devices from physical damage, biological contamination, and environmental disturbances, while ensuring sterility before their use in healthcare settings. Effective packaging includes labeling for easy identification and supports the safe transport of devices to end users.

Packaging for orthopedic implants, such as knee, hip, spine, and thumb implants, requires materials compatible with multiple sterilization methods and that offer high puncture and abrasion resistance. These implants must be safeguarded against physical damage and contamination to maintain their integrity and effectiveness. Common materials used for orthopedic implant packaging include thermoplastic polyurethane (TPU) and polyethylene. UFP MedTech, for instance, developed FlexShield TPU and cross-linked polyethylene (XLPE) for orthopedic packaging applications. Both materials are compatible with gamma and ethylene oxide (ETO) sterilization processes and offer strong resistance to abrasion and punctures.

The demand for orthopedic soft goods, such as knee and back supports, is rising, particularly in developed regions like Europe, the U.S., and Japan, which have a growing elderly population. Additionally, the fitness and sports industries in emerging economies like India are driving demand as well. Orthopedic soft goods cater to a diverse consumer base, including senior citizens, young adults, and teens, by providing relief from joint pain caused by disease, occupational strain, or sports-related injuries. These products encompass a range of items, including rehabilitation aids, knee braces, wrist supports, back support braces, ankle supports, elbow straps, abdominal binders, rib belts, hernia supports, and cervical collars. They are essential for managing pain and providing support for injuries related to fractures, muscle pain, and various orthopedic conditions.