#Retirement planning for Millennials and Gen Z

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

The most popular pages on Tumblr are about Minecraft, GIFs, and David J. Peterson.

Note

I’m late to the loser convo but I must say my two cents, I think this new loser enabling culture has done so many mentally ill people sooo wrong. When everyone is shouting ‘there’s nothing wrong with living with your parents when you’re 35 and not having a job and not cleaning your room it’s societies problem’ instead of gently pushing them out of their comfort zone people cling to that and sink deeper into their depression comfort zone. I get dogpiled almost every time I say people need to move out of their parents house to not get stunted emotionally despite being poor and depressed myself

right of course everyone is poor, but at the point that you keep doing the same one job and complaining about it and not leveraging the gig app economy and other part time positions to supplement your low income it just starts to be annoying and your fault.

it wasnt fair when my abusive lower management museum job paid $22000 per year when I was more educated than any of my managers but I had to improvise and get creative with my skills on the internet to MAKE my income livable.

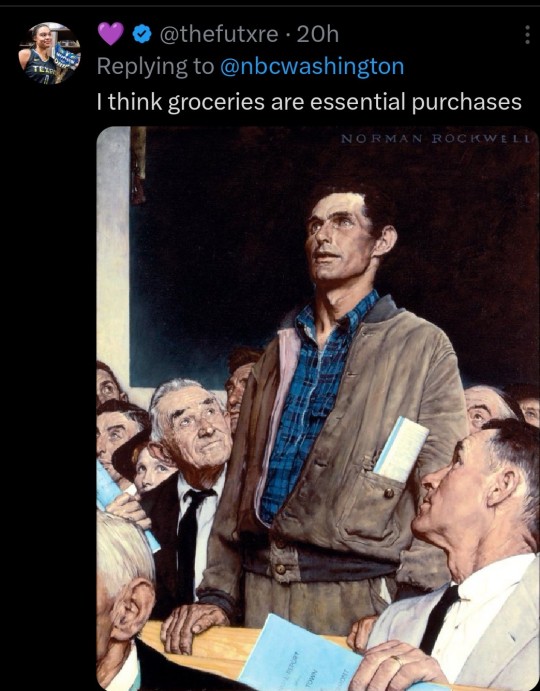

I felt insane when I read that the majority of adults are either staying with their parents or taking their retirements like giant leeches:

Half of parents are paying their Gen Z and millennial adult children $1,474 a month—but they plan to pull the plug in the next two years because it’s eating into retirement | Fortune

9 notes

·

View notes

Text

Half of American parents with adult children are supporting them financially, according to a report by Savings.com. The number of adult children dependent on their parents continues to tick higher, up from 47% in 2024 and 45% in 2023. In fact, the average parent is spending $1,474 monthly per child to make ends meet amid the cost of living crisis.

Around 83% of respondents reported contributing to their adult children’s monthly grocery bills, 65% assist with cell phone plans, 44% are paying off auto payments, and 45% are paying for student loans. For those who are not living at home, 63% of parents admitting to helping pay toward rent or mortgages.

This is causing stress for a generation that should be planning for retirement, with 60% admitting they are living a more frugal lifestyle to support their adult kids. Half of respondents said that they have had to pull money from their savings and/or retirement accounts, and another 31% have taken on debt to continue supporting their kin. As for retirement, 35% believe they will need to push back on retirement plans.

This growing trend is altering society. Every generation is feeling the burden of the cost of living crisis. Rentals have never been higher and it is increasingly difficult for adults with entry-level jobs to find housing. In fact, one in three adults aged 18 to 34 still live with mom and dad. Autos, groceries, health care—every aspect of life has increased dramatically for the younger generations. This is one of the reasons why we see a declining birth rate as the cost of living is costing Gen Z and younger Millennials the opportunity to pave their own way.

8 notes

·

View notes

Text

“Why is Gen Z seeming to age faster than Millennials?”

1) making a broad generalization like that without any evidence save for people you seen on the internet is kinda silly 2) even if Gen Z is aging faster than Millennials the only people who will benefit from people talking about it are makeup and skincare companies who will try to use the fear of aging to get their products into more hands 3) who carreeesss climate change is happening, everyone thinks they need to know everything about you, the boundaries of public and private life are ceasing to exist and I’m supposed to care about whether or not I look four years older than I am? I don’t! I don’t care!

But even if we (Gen Z) are aging faster than Millennials have you considered the fact that we are fucking tired. I hardly know anyone who has a retirement plan because most of us know that unless things change we are gonna have to work until we are dead. We were pushed so hard to make ourselves marketable to companies so we can get a job and a home only to find out that even if we get a job we might not ever wind up owning a house so what was the point of all that effort? I know people my age who feel like the systems in place failed us because we were promised more and what we got was high rents, a rapidly changing climate, being locked out of the housing market unless you have someone willing to go in with you or mom and dad have some extra cash and politicians that want us (queer/disabled etc Gen Z) dead.

Like.

Out of all of our problems I think us ‘aging more quickly’ is the least of them.

16 notes

·

View notes

Note

Number 23 (Going from a hot tub/sauna into snow/cold water), Galadriel and Celeborn (romantic or pre-romance, up to you)

For the modern AU holiday prompts! Here you are, Anon: ~1100 words of Galadriel meeting a cute boy at her 19th birthday party. (I received this same prompt for another couple, so there will be a part 2 of this with more actual snow jumping😉). Warnings for several f-bombs, some other swear words, and a millennial writing Gen Z. Sorry, besties.

Knotting her plush white robe loosely around her waist, Galadriel led the parade of her girlfriends onto the flagstones of Nevrast Nordic Spa.

Her friends chattered behind her.

“Yo, this place fucks.”

“For real.”

“Ahhh! Gal, it’s snowing!”

“Ugh, this is so boujee. I can’t believe I’m here.”

“Hey, sis,” Galadriel whirled on the last speaker. “No bad vibes, remember?�� The other girls laughed. “Yeah, my rules, cause it’s my b-day, bitches!” She threw her arms out in a V-shape and struck a pose.

Edhellos lifted the phone dangling from her hand by a gold finger-loop and snapped a photo. “Ahh queen! You look so cute!” she said, looking at it, and hurried over to Galadriel to show her. Then she gestured to the others. “Come on, come on, babes, let’s get one of all of us.”

All four of Galadriel’s best friends huddled around her while Edhellos held her phone out as far as possible for a selfie.

“Okay, okay,” Galadriel said, and they all hushed. “So the way it works is you go hot, then cold, then relax. Hot pool or sauna, then cold pool or cold shower, then chill for fifteen minutes. And we're supposed to be quiet.”

They all nodded, except Nellas, who was a little removed from the group with her arms crossed over her chest. “I think I’ll just sit and read.”

“Oh come on, Nelly!” Edhellos whined. Evranin shushed her.

“No, it’s fine, Nel,” said Galadriel, and smiled. “Join us whenever.”

*

“I can’t believe we’re all nineteen now,” Lindis said a loud whisper as they lounged in the largest of the hot pools. “We’re so old.”

“Oh, please, spare me. You have no idea what old is,” said Evranin, who was all of twenty-one.

“Hey, I’m still eighteen for two weeks!” Edhellos protested. This time, Lindis shushed her.

Galadriel examined her pruny fingertips. “I don’t know. I’m kind of excited to get older. Maybe my dumbass family will stop treating me like a baby.”

At the mention of her family, Edhellos’ eyes lit up. “Oh hey, how’s Angrod?”

“Oh my god, Los,” said Lindis, “stop thirsting for her brothers!”

“Brother,” Edhellos corrected.

“I dunno.” Galadriel shrugged. “Maybe just ask him out already.”

Edhellos sputtered. The other girls giggled.

“I think Finrod is hotter,” Evranin said casually.

“He is way too old for you!”

“Isn’t he gay?”

“What? No! Galadriel said he had a girlfriend in Valin, remember?”

“The one he dumped?”

“No, she dumped him.”

While her friends debated the relative attractiveness and past relationships of her older brothers, Galadriel sank lower, rolling her shoulder blades back and forth over a water jet. She hummed contentedly and let her eyes fall shut. She’d been all nerves the last month with final exams and papers, but she was finally able to relax.

Just that morning her grades had come in: four A+ and one A (at least she was well above class average the last one). She’d also been taken off the waitlist for a seat in The Paranormal Mind. Thank fuck.

Everyone at Ondolindë University wanted to take that course, but Galadriel needed it if she was going to have any chance of doing her honours thesis with Melian Goel. Evranin, who was President of the Psychology Student Association, said that that Dr. Goel was planning to retire soon and might not be taking new students. Oh pleasepleaseplease, Galadriel thought, please take me.

She exhaled slowly and intentionally released the tension building in her neck. This wasn’t the time for worrying.

Then her eyes flew open and she bolted upright as a surge of water splashed over her.

“What the fuck!” she shouted, swiping the backs of her hands over her eyes.

“Celeborn, you dumb shit!” a male voice cried from behind her before breaking up into laughter.

“Oh god, I’m so sorry.” The person who’d narrowly missed tumbling on top of her rose from the water with an expression of sheer terror. “I’m so, so sorry. Are you okay? Oh god, I’m sorry. I slipped, we were racing from the…" Catching the look on Galadriel's face, his nose crinkled sweetly. "I guess that’s a pretty dumb excuse, huh?"

“Yeah, it is.” Galadriel smirked and bit her lip. He was her type: tall, slender but well-toned, and a little timid. Which was far preferable to the blustering arrogance that most guys her age — no, scratch that: all ages — liked to use to hide their emotional incompetence.

“That’s a sick tattoo,” she said, gesturing with her chin to the elegant tree climbing its way up one bicep.

“Oh, really?” he said. “Thanks. It’s a beech. There are a lot of them where I grew up, and— never mind, doesn’t matter. Thanks. Hey, by the way," he held out a hand, “my name’s Celeborn.”

“Galadriel.” His handshake was firm, but not too firm. Long fingers, too. A little spark of excitement shot down her arm as she pulled back. “So, you were racing—?”

She was cut off by a whoop from his friend still standing on the flagstones behind them, which prompted Galadriel’s friends, who’d huddled by the small waterfall at the opposite end of the pool, to finally take notice of the interaction.

As Celeborn’s friends — the first now joined by two more — slid into the pool, Galadriel’s group drifted over like a train of ducklings lured by breadcrumbs.

“Hey, I’m Galathil,” the loud one said, “and this is Mablung, and Beleg. Celeborn here is my little brother.”

Galathil attempted to ruffle Celeborn's silver-blond hair, but it clung wetly to his head.

“Hi,” Galadriel waved coolly, then dragged her eyes from Celeborn to the empty space beside her, beckoning him to sit before someone else did.

He picked up on the cue, seating himself at a respectable distance; but to his right, Edhellos slyly shuffled over so that he too was forced to scoot closer to Galadriel.

“Yeah,” he said, in answer to her interrupted question. “We thought it would be fun to, you know, go from the sauna into the snow,” he pointed to the snow banks around the spa area, “and then from the snow to the hot tub.”

“Oh really?” Galadriel’s eyebrows shot up, and Celeborn looked sheepish. “You know you’re supposed to ‘relax’ in between the cold and going back to the hot?”

Several of Galadriel’s friends giggled.

“Huh?” said Celeborn.

“You’re supposed to go hot, cold, then relax for fifteen minutes.”

“Really?”

“Yeah.” Galadriel smiled and smacked his arm lightly. “But the snow thing sounds fun.”

His face split into a dashingly handsome smile that dimpled his cheeks. “Yeah,” he said. “It is.”

“Hey fam,” she called to her friends. “Wanna jump in the snow?”

“What!” shrieked Lindis.

“Hell no,” said Evranin.

“Ahh so fun, yes please!” Edhellos squealed, and levered herself out of the hot tub. “I’ve always wanted to do that.”

“Lit,” said Galathil to no one in particular, and followed her.

“Come on,” Galadriel said to Celeborn as the others squirmed and scurried out of the pool in various states of enthusiasm. “I’ll hold your hand so you don’t slip this time.”

18 notes

·

View notes

Text

And unfortunately, this ties heavily into politics.

"How can they vote for That Asshole?"

"Because they get all their news from a single tv channel and a tiny, alt-right-controlled set of text sources."

"Why don't they look for The Real Truth? Why don't they move outside of that tiny siloed bubble?"

"Because they are FUCKING EXHAUSTED, which is exactly what the capitalist hellscape system intended." They were raised in a siloed bubble where they didn't get enough sleep or free social time as teenagers and then pushed into full-time-plus jobs (...plus kid-care, for the women) as soon as they reached legal adulthood, and they were never given time to rest or the resources to know they needed it.

(And there are plenty of exhausted people who did not vote for That Asshole, but they were not raised in a silo they are still stuck in. Something has to happen to push people out of that.)

(And yes, there are plenty of alt-right voters who are not exhausted. But if you were wondering about the ones who seem to be voting directly against their own interests... they are. so. damn. tired.)

Tired Gen-Xers have gotten cynical and believe there's no point in voting for anything; anything you gain will be ripped away in the future so why bother trying?

Tired Millennials are certain it's all incomprehensible propaganda. You can't tell what's real from what's fake so better to just vote for what the people you love and trust are voting for.

Tired Gen-Z are trying desperately to enjoy their youth and resent the constant message of "it's up to YOU to fix the world WE broke."

(And tired Boomers are resentful that their promised Sweet Retirement In Prosperity has not come to happen and they are often not interested in "vote for a better future for tomorrow's kids"; they want the better future they were promised at 18 and they are voting for whoever says they still deserve it and can have it.)

...Not all of them. But enough to tank any progressive plan for "let's make Real Fucking Changes even though it'll be hard for a while."

They're too exhausted to support "hard for a while" messages. They want "you deserve better and I'm going to make sure you have it." And they're too tired to realize it's all lies and hot air.

as a child I wondered why adults were so stupid (doing things out of habit/routine/heuristics rather than reasoning explicitly about what to do based on their goals) and the answer is that adults are unimaginably fucking tired all the time

94K notes

·

View notes

Text

What Different Generations Want in New Homes ?

Homebuyers from every generation want different things. Some people want cozy reading nook, while other prioritize sustainable solutions for their homes. But here's what they all agree on: no one wants to drop thousands every time something breaks.

One of the most recommended ways to avoid these costly expenses is home warranty In USA, these service contracts cover the repair or replacement of major home systems and appliances including air conditioning, refrigerator, electrical systems, plumbing, and more. If a covered item breaks down due to normal wear and tear, policyholders can simply file a claim and have a qualified technician handle the repairs. It saves time and money, and preventing unwanted stress.

So, what exactly does each generation look for in a home and how can a home warranty support those needs? In this blog, we break down their top priorities and show why a home warranty is a smart choice for all.

Home Features Each Generation Is Looking For

Baby Boomers

When baby boomers hit retirement, their priorities shift big time. They want a single-story living, walk-in showers, wider doorways, and systems that won't leave them sweating when the AC breaks down. Apart from accessibility features, they want security. Boomers don’t want to deal with costly repairs to their HVAC systems, water heaters, or electrical lines.

Millennials

Millennials are one of the biggest customer demographic in real estate market. They favor open layouts, updated kitchens, and integrated smart home technology. However as first-time buyers, many millennials are budget-conscious and wary of repair costs. They are always looking for affordable home warranty coverages that protects their expensive home appliances and systems from wear and tear.

Gen Z

This generation is stepping into the market with a fresh perspective. They are more likely drawn to tiny homes, condos, or smaller starter homes with eco-friendly features. Gen Z wants their home with solar panels, high-speed internet, and other modern features. This generation values financial freedom and sustainability. That’s why, unexpected breakdowns often feel overwhelming.

One Thing Everyone Wants

No matter the generation, homeowners want to feel secure in their investment. Many homebuyers opt for home warranties for peace of mind. These are special service contract that covers the repair or replacement of major home systems and appliances when they break down due to normal wear and tear.

If you're searching for a reliable home warranty company in USA, count on Elite Home Warranty. We provide customizable plans, transparent pricing, and top-rated customer service to customers. In this blog, we discuss some few things each generation wants from their new home. Our team ensures every generation gets the protection they need without the stress. Do you want to explore our plans? Call us at (888) 354-8398 or email [email protected] for consultation bookings.

#home warranty company in USA#home warranty#home warranty plan#home warranty company in the usa#elite home warranties

0 notes

Text

How Gen Z is Redefining Personal Finance in India: Trends, Tools, and Investment Habits

India’s financial landscape is undergoing a generational transformation. As Gen Z—those born between the late 1990s and early 2010s—enters the workforce, they are rewriting the rules of personal finance. Unlike previous generations that leaned heavily on fixed deposits, physical assets, and traditional banking, Gen Z prefers mobile-first solutions, digital investing, and financial independence at an early age.

With this shift, the way money is earned, saved, and invested is being reimagined. And for those looking to keep up, whether in fintech, financial services, or personal career growth, mastering tools like financial modelling is crucial. If you're aiming to ride this wave professionally, enrolling in the best Financial Modelling Course in Chennai can be a game-changing decision.

Gen Z’s Financial DNA: Digital, Data-Driven, and Independent

Unlike millennials, Gen Z was born into a digital-first world. Financial decisions are no longer based on family advice alone—they're influenced by YouTube creators, Instagram reels, fintech influencers, and financial podcasts.

This generation is:

Digitally native: They rely on fintech apps like Zerodha, Groww, Cred, Paytm, and Fi.

Financially curious: Many start budgeting and investing in their early 20s—or even teens.

Risk-tolerant: Willing to explore new-age assets like crypto, REITs, and global stocks.

Purpose-driven: They care about ethical investing, green finance, and aligning money with values.

Top Personal Finance Trends Among Gen Z in India

1. App-First Budgeting and Expense Tracking

Gen Z doesn’t use spreadsheets for budgeting. Instead, they use apps like Walnut, Moneyfy, Jupiter, and INDmoney to manage expenses, track subscriptions, and set financial goals. The gamification of finance—badges, rewards, spending alerts—keeps them engaged.

2. DIY Investing Through Fintech Platforms

Rather than relying on advisors, they prefer platforms like Zerodha, Upstox, and Groww to learn and invest. Many are experimenting with SIP investments, US stocks, mutual funds, and even fractional real estate.

3. Side Hustles and Multiple Income Streams

Gen Z isn't content with a single salary. From freelance gigs and content creation to affiliate marketing and dropshipping, side hustles are the norm. This requires strong financial planning and forecasting—skills taught in the best Financial Modelling Course in Chennai.

4. Crypto and Digital Assets

Despite regulatory uncertainties, Gen Z is one of the most active demographics in crypto adoption. Platforms like CoinSwitch and CoinDCX have witnessed a surge in under-25 users. They treat crypto not just as an investment but as a cultural movement.

5. Learning from Influencers, Not Just Institutions

Whether it’s a 2-minute reel explaining mutual fund SIPs or a 10-slide carousel breaking down compound interest, Gen Z prefers finance that's visual, short, and social. Influencers like CA Rachana Ranade, Anushka Rathod, and Sharan Hegde are more popular than traditional financial advisors among young Indians.

The Role of Financial Education in Gen Z’s Growth

While Gen Z has the tools, what many lack is structured financial knowledge—especially in building long-term models for income, spending, taxes, investments, and retirement.

That’s where courses like the best Financial Modelling Course in Chennai come in. These programs teach you how to:

Build 3-statement models (Income Statement, Balance Sheet, Cash Flow)

Analyze investment opportunities with IRR and NPV

Forecast income and expenses based on real-life scenarios

Understand unit economics for personal or business ventures

Create dynamic models for startup valuations, side hustles, or real estate planning

Whether you're planning to launch a startup, work in fintech, or become financially independent by 30, financial modelling gives you the clarity and control to make smarter decisions.

How Gen Z’s Habits Are Shaping the Financial Ecosystem

Fintech companies, banks, and investment platforms are now tailoring their products around Gen Z’s preferences:

Neobanks like Jupiter and Fi offer sleek UI/UX, instant savings tools, and financial insights.

Credit-building apps help new earners build credit scores with low-risk tools like secured cards or BNPL (Buy Now, Pay Later).

Sustainable investing platforms are popping up, allowing young investors to align money with their values.

The ecosystem is evolving, but the professionals who work behind these innovations must understand how money moves—and that’s where financial modelling remains indispensable.

Gen Z and the Career Landscape in Finance

With Gen Z flooding into finance, marketing, consulting, and tech roles, there’s a growing demand for those who not only understand finance but can also build data-backed financial narratives. Skills in Excel, valuation, scenario planning, and forecasting are critical—regardless of your sector.

If you're in Chennai and looking to prepare for roles in investment banking, FP&A, startup finance, or entrepreneurship, consider the best Financial Modelling Course in Chennai to build job-ready skills that employers—and investors—respect.

Final Thoughts

Gen Z is not just a generation—it’s a financial revolution in the making. From their first paycheck, they’re investing, saving, tracking, and learning like no generation before. Their preferences are changing how financial products are built, how advice is shared, and how the economy moves.

Whether you're part of Gen Z or someone looking to understand and work with this new wave, one thing is clear: financial literacy and modelling are essential skills in this fast-changing landscape.

If you're ready to decode the future of personal finance, strengthen your analytical capabilities, and unlock career opportunities in the evolving finance world, enroll in the best Financial Modelling Course in Chennai—and lead the change.

0 notes

Text

Unsurprisingly I don't think anyone here actually read the article. It isn't judging or criticizing. It doesn't put forth any opinion and barely puts a highlight on anyone else's opinion about what "should" be done. It is simply reporting what is happening. Much of it is stats and quotes from millennials. It's actually rather dry.

It covers increasing rent, inflation, interest rates, higher education, and how it makes budgeting and long-term planning harder for millennials/gen z. It also gives voice to millennial/gen z's pessimistic attitudes towards their own futures and why they calculate that short-term purchases have higher value.

Despite wealth gains, young adults’ financial pessimism has encouraged many to spend in ways that make them happy now, said Kyla Scanlon, author of “In This Economy? How Money & Markets Really Work.” “People are just exhausted, and so if you’re asking them to think five to 10 years in the future, well I can barely think about tomorrow,” she said. In an Intuit survey last month, two-thirds of Gen Zers said they weren’t confident they’d ever afford to retire, and nearly three-quarters hesitated to set long-term goals. Singla, a millennial, doesn’t feel much more certain about what steps to take.“If I had to leave my job and take a break or take a vacation, I used to feel comfortable we could do that,” he said. Now, “everything feels like a splurge.”

Honestly, I think most people complaining here would agree with the information presented in the article if they actually read it. Literally the first two sentences are about how some people feel they don't have a choice in determining their spending habits. Instead y'all just want somebody to yell at

#i feel so bad for journalists in the modern era#i bet it pays like shit too#i am unusually spiteful abt this bc i am tired and writing this at 1:30 am. its going in my queue

21K notes

·

View notes

Text

Choosing Between Facebook and Instagram Ads: 2025 Strategy Guide

In 2025, digital advertising is more dynamic than ever, and businesses face the ongoing challenge of deciding where to invest their ad budgets. Facebook and Instagram, both under Meta’s umbrella, remain powerhouse platforms for reaching diverse audiences. But which one is right for your brand? This guide breaks down the key differences, strengths, and strategies for choosing between Facebook and Instagram ads in 2025, helping you make informed decisions to maximize your ROI.

Understanding the Platforms

Facebook and Instagram share Meta’s robust advertising system, but their vibes and user bases differ. Facebook, with over 3 billion monthly active users, is a broad platform appealing to a wide demographic, from Gen Z to Baby Boomers. It’s a hub for community engagement, long-form content, and detailed targeting. Instagram, with around 2 billion users, skews younger, with a strong focus on visuals, short-form videos, and influencer culture. It’s the go-to for lifestyle, fashion, and creative brands.

Both platforms offer access to Meta’s Ads Manager, giving you precise control over campaigns, budgets, and targeting. However, the choice between them depends on your audience, goals, and content style. Let’s dive into the key factors to consider.

Audience Demographics

Knowing your target audience is the first step. Facebook’s user base spans all age groups, with a significant portion of users aged 25–54. It’s ideal for businesses targeting professionals, parents, or older audiences. For example, a financial services company might find success targeting middle-aged users with retirement planning ads.

Instagram, on the other hand, is dominated by younger users, with over 60% aged 18–34. It’s perfect for brands aiming at millennials and Gen Z, who engage with trendy, visually appealing content. A skincare brand targeting teens, for instance, would likely see better engagement on Instagram through Reels or Stories.

Ad Formats and Creative Options

Both platforms offer similar ad formats—photo, video, carousel, and Stories—but their execution differs. Facebook supports longer videos and text-heavy posts, making it great for storytelling or explaining complex products. For example, a real estate agency could use Facebook video ads to showcase property tours with detailed descriptions.

Instagram prioritizes short, snappy content. Reels and Stories dominate, with users expecting polished, eye-catching visuals. A fashion brand could leverage Instagram’s shoppable posts, allowing users to buy products directly from an ad. In 2025, Instagram’s focus on augmented reality (AR) filters also offers creative ways to engage users, like virtual try-ons for makeup or clothing.

Engagement and Interaction

Engagement patterns vary significantly. Facebook’s strength lies in its community-driven features like Groups and Events. Ads tied to these can foster deeper connections, especially for local businesses or niche communities. For instance, a fitness studio could promote a free trial class through a Facebook Event ad, encouraging sign-ups and shares.

Instagram thrives on instant, visual engagement. Users scroll quickly, so ads need to grab attention in seconds. Influencer collaborations are a big win here—partnering with micro-influencers (10,000–50,000 followers) can boost authenticity and engagement. A coffee shop, for example, could sponsor a local influencer’s Reel featuring their new seasonal latte.

Cost and ROI Considerations

Ad costs depend on factors like audience size, competition, and ad quality. In 2025, Facebook tends to have a lower cost-per-click (CPC), averaging $0.50–$2.00, compared to Instagram’s $1.00–$3.50. However, Instagram often delivers higher engagement rates, which can justify the cost for brands focused on brand awareness or conversions.

For budget-conscious businesses, Facebook’s broader reach makes it a safer bet for driving traffic or leads. Instagram, however, excels for e-commerce brands with visually appealing products, as its shoppable features streamline the path to purchase. Testing both platforms with small budgets can help you gauge which delivers better ROI for your goals.

Targeting Capabilities

Meta’s Ads Manager offers identical targeting options for both platforms, including demographics, interests, behaviors, and lookalike audiences. However, the context matters. Facebook’s detailed user data (like job titles or life events) suits B2B or service-based businesses. For example, a wedding planner could target “recently engaged” users with precision.

Instagram’s targeting shines for lifestyle and interest-based campaigns. Its algorithm favors visually engaging ads, so brands with strong aesthetics—like fitness, travel, or food—can leverage interest-based targeting to reach passionate audiences. A travel agency, for instance, could target “adventure seekers” with stunning Reels of exotic destinations.

Which Platform Suits Your Goals?

Your campaign objectives should guide your choice. For brand awareness, Instagram’s visual appeal and high engagement make it a top pick. Reels and Stories can quickly capture attention and spread your message. For lead generation or conversions, Facebook’s detailed targeting and lower CPC make it more effective, especially for complex products or services.

E-commerce brands with visually driven products (think fashion, beauty, or home decor) should lean toward Instagram, where shoppable posts and AR features drive sales. B2B or local businesses, like consultancies or restaurants, may find Facebook’s community features and broader audience more effective.

Tips for Success in 2025

Test and Optimize: Run small-scale A/B tests on both platforms to compare performance. Adjust creative, targeting, or budgets based on results.

Leverage Video Content: Short-form videos (Reels on Instagram, short videos on Facebook) are king in 2025. Keep them under 30 seconds for maximum impact.

Use Meta’s AI Tools: Meta’s Advantage+ campaigns use AI to optimize ad delivery, saving time and improving results.

Prioritize Authenticity: Users crave realness. Use user-generated content or behind-the-scenes footage to build trust.

Monitor Trends: Instagram’s AR and AI-driven features are evolving fast. Stay updated to stand out.

Combining Both Platforms

Why choose one when you can use both? Many brands in 2025 run integrated campaigns across Facebook and Instagram to maximize reach. For example, a retailer could use Facebook to drive traffic to a blog post about sustainable fashion, while using Instagram to showcase products with shoppable Reels. Cross-platform campaigns let you repurpose creative assets while targeting different audience segments.

Final Thoughts

Choosing between Facebook and Instagram ads in 2025 comes down to your audience, goals, and content strengths. Facebook offers broad reach and detailed targeting, ideal for lead generation and community engagement. Instagram excels in visual storytelling and e-commerce, perfect for younger audiences and trendy brands. By understanding your objectives and testing both platforms, you can craft a strategy that drives results. Start small, analyze performance, and let data guide your next steps. Here’s to crushing your ad campaigns in 2025!

0 notes

Text

The Earlier, The Richer: What Most Investors Learn Too Late

Understanding the Magic of Compounding

Compounding is often referred to as the eighth wonder of the world—not because it's complex, but because it’s astonishingly effective. At its core, compounding means earning returns not only on your original investment but also on the returns generated over time. This snowball effect becomes more powerful the earlier one starts investing.

Let’s say you invest ₹10,000 at an annual return of 10%. After one year, your money grows to ₹11,000. In the second year, you earn 10% on ₹11,000—not just the original ₹10,000—bringing the total to ₹12,100. Continue this process for 20 or 30 years, and the results are mind-blowing.

Why Early Beats Perfect

A common misconception is that perfect timing—investing when markets are at their lowest—is the most effective strategy. But the truth is, time in the market almost always beats timing the market. Consider two hypothetical investors:

Investor A starts at age 25 and invests ₹5,000 annually for 10 years, then stops.

Investor B starts at 35 and invests ₹5,000 annually for 30 years.

Even though Investor B invests three times more, Investor A often ends up with a larger corpus by retirement, thanks to compounding having a decade head start.

This is why financial experts and planners constantly stress—start early, even if small.

Real-World Evidence: Warren Buffett’s Wealth

One of the most cited examples of compounding in action is Warren Buffett. While he’s renowned for his investment skills, a lesser-known fact is that the majority of his wealth was amassed after the age of 50—not because he changed his strategy, but because compounding had more time to work its magic. Buffett started investing at age 11, and his net worth soared exponentially in his later years simply because his money had more time to grow.

India's Investment Culture Is Evolving

The power of compounding isn’t just a textbook concept—it’s shaping investment habits across the country. With increasing financial literacy and growing awareness of mutual funds, SIPs, and retirement planning, young Indians are showing more inclination toward investing early.

As per a recent ET Wealth report, over 35% of SIP investors in India are now under the age of 30. These investors aren't waiting for the "perfect time" to invest. They're realizing that every year counts. Whether it’s equity mutual funds, the NPS, or ELSS, more and more young professionals are entering the investment game with long-term goals.

Busting the ‘Lump Sum Later’ Myth

A myth often heard among professionals is: “I’ll start investing later when I earn more.” While that sounds logical, mathematically it’s flawed. Even if you invest a larger lump sum later, it’s hard to beat the results of consistent early investments.

Here’s an example:

Invest ₹2,000 monthly starting at age 25 for 10 years = ₹2.4 lakh invested Let it sit untouched till age 60 at 10% = ₹50+ lakh

Start at age 35 and invest ₹2,000 monthly till 60 = ₹6 lakh invested Final corpus at 10% = ₹38+ lakh

Despite investing much less, the early starter wins. This is the beauty of compound interest—it rewards time more than capital.

What Happens When You Delay?

Delaying investing by just a few years can lead to a significant loss in wealth accumulation. For every year you delay, the power of compounding gets compromised. That means you’ll have to invest more and take higher risks just to catch up.

This reality is becoming more evident among working professionals, particularly in tech hubs like Bengaluru, where financial independence is a trending goal among millennials and Gen Z. The growth of financial education platforms in the city reflects this mindset shift. Many professionals here are not just exploring long-term investment vehicles but also enrolling in specialized learning programs like the CFA course Bengaluru to strengthen their financial acumen and take informed decisions.

Gen Z’s Fresh Take on Compounding

Generation Z is often accused of impatience, but when it comes to money, they are surprisingly pragmatic. A survey by Groww revealed that over 60% of Gen Z investors in India prefer starting their investments before the age of 24, prioritizing long-term benefits over instant gratification.

What’s refreshing is their understanding of compounding not just for wealth, but also for personal skills, knowledge, and career growth. The idea of compounding isn’t limited to money—it now defines how this generation looks at life. Start early, grow slowly, and reap exponential benefits.

Recession Fears & Compounding Confidence

Even in the face of global economic concerns, including whispers of a possible recession in 2025, early investors continue to stay the course. Historical data backs their optimism. Every recession eventually leads to a recovery, and those who continue to invest through downturns benefit disproportionately when the market rebounds.

In fact, market dips offer great opportunities for long-term investors to accumulate more units at lower prices. As long as you remain consistent, compounding can smooth out market volatility and deliver solid results in the long run.

Let Technology Help You Start Early

With the rise of robo-advisors, investment apps, and auto-debit SIPs, starting early is now easier than ever. You no longer need to be a finance whiz to invest wisely. All it takes is commitment and consistency.

What you do need, however, is awareness. Knowing that ₹500 invested today is worth far more than ₹500 invested five years later is a mindset that can transform your financial life.

Conclusion: The Long Game Wins

The power of compounding is not just a theory—it’s the foundation of wealth-building. And while headlines may scream about market crashes or booms, the real winners are those who start early, stay invested, and let time do the heavy lifting.

In cities like Bengaluru, where financial awareness is growing rapidly, more professionals are turning to structured learning and certifications to build long-term financial habits. For instance, the cfa online prep course is gaining traction among those who want to deepen their investment knowledge while pursuing full-time careers. Starting early with such a course mirrors the same principle—get ahead, stay ahead.

Whether you’re 20 or 40, the best time to invest was yesterday. The next best time? Today.

0 notes

Text

Day 45: The Fault in Our Stars (or, is it a social construct?)

It's easy to feel behind in life sometimes. It's normal.

But comparison is the thief of joy, so I am interested in reducing the instances in which I gauge my life on any perceived scale.

AKA, are you truly behind in life, or is it all arbitrary?

There is no ahead or behind if the scale is unique to each individual. So, I'm thinking this is a mostly pointless thing to gauge.

Therefore it's also easy in theory to NOT feel behind in life, if you just condition yourself to see it this way. That's today's blog topic, that the accepted norms of life timeline are obsolete and made-up.

I want to discard and disregard such norms as much as possible, so I don't get pushed to make brash or ill-fit life choices, trying to chase a carrot that I don't really want in the first place.

I don't think this game plan is useful only for people who are oddballs or do things differently. I think it's good for everyone, even those who do things 'by the book' and largely adhere to the social norms.

Because if and when you fall short, which is inevitable at times, then you won't beat yourself up. You won't be lured into bad decisions, trying to rectify something that doesn't inherently need fixing.

A person can still find intrinsic motivation to reach milestones even without external coercion of social mores, obviously, is my point.

I heard that the Western benchmark of age 65 for retirement was determined in the 1930's. A lot has changed since then, such as technology, and lifestyle, pop culture, even life expectancy.

I'm not saying a person should try to delay retirement beyond the age of 65 off principle, just that this number was chosen when FDR was president...it is antiquated, kind of random, and not a catch-all.

It's moot today for Millennials and Gen Z adults to pressure themselves into a tunnel vision approach pursuing these things. This goes for career and personal choices. Unless they feel like it!

Working backwards, if you don't need to retire by 65 in order to prepare to die, many things become malleable in your timeline:

You could pursue high education either later in life, or a second time in your adult years beyond your late teens. If you want to. It wouldn't be terrible. You don't need to be done with college by age 21.

You can reinvent yourself with less angst. This also helps a person will themselves to take more calculated risks, knowing it's not all-in.

You could have children a bit later, which we've been gradually seeing. You don't need to be married with three kids by 30. You can date off and on at your discretion and not forcibly find a partner.

You can spend more of your 20's and 30's experimenting and exploring the world, in order to find and refine yourself.

And when you hit 25, 30, 35, 40, you don't have to feel like a failure if you have not achieved some of these normalized checklists.

You can even consider age 50 to be middling and not 'old.' There's plenty of age-restrictive thoughts people have about certain activities or settings. We can disregard those and live freely.

Basically, it eradicates a lot of self-limiting belief systems.

There's a lot of upside to ignoring one socially-accepted timeline.

The kicker is that even when you feel off-time about your plans, or you rearrange the order and it looks funny to other people, you don't drop dead or anything. You still live on like normal, and nothing really matters or changes for the worse.

You might experience some perceived cynicism, some sub-optimal circumstances here and there, some mismatches with your friends and logistical issues. Just do it anyway, and ignore judgement.

Your kids might not be the same age as your friends' kids. You might not have like experiences to your peers in the office or with in-laws.

But ultimately it's all a made-up charade. So it's all good.

I'm trying my best to improve life and wellness in ways I can. I am trying to be a bit healthier and more fulfilled. I am also trying to figure out meaningful uses of time moving forward in the near future.

But, most of my endeavors are not considered normal on the societal timeline. So it's hard sometimes not to feel like you are failing all the worldly expectations. It has taken me practice to tune it out.

I think in the past I'd view this a 'price' I had to pay. But now I'm just considering it a fact of life that is neither bad nor good. It just is.

This is a better approach, as you ward off impulsive adjustments to try to steer back on-course to a path you don't want anyways.

Because in the end, 'behind' based on what? The metric has to be concrete, static, and measurable to be ahead or behind. But life is not like that when you think about everyone all at once individually.

That's my thought today. There is no one timeline for everyone. And people who try to stick to a perceived correct one and who sacrifice their own value system are doing themselves a disservice.

It's hard to have the courage to do your own thing, basically.

Nobody's ahead of time, on-time, or falling behind. There are some worldly constraints and parameters, but we're all on our own path.

Everyone is improvising, and no one really knows anything about anything. I think that is a wonderful thing to be celebrated. It helps you live purely, and as a bonus it makes one less judgy!

This is how I'm trying to be, and I hope the same others. If that's what they want!

(I think I'm discontinuing Song of the Day as a regular feature and will just throw one in periodically when I feel like it)

0 notes

Text

SIP vs PPF – Which Investment is Right for You?

When it comes to saving and investing in India, two of the most popular options that often spark debate are SIP (Systematic Investment Plan) and PPF (Public Provident Fund). While both are excellent avenues for wealth creation and saving for the future, they cater to different risk appetites, financial goals, and investment strategies. If you've been wondering which is better for your hard-earned money, you’re not alone.

SIP is a disciplined way to invest in mutual funds, primarily equity-oriented ones, offering the potential for higher returns but with market-linked risks. On the other hand, PPF is a government-backed small savings scheme that offers stable, tax-free returns over the long term. Each has its own set of advantages and limitations, and choosing between them depends heavily on your personal financial goals, time horizon, and risk tolerance.

So, how do you decide which one is right for you—SIP or PPF? Let’s break down the differences, benefits, and suitability of both to help you make a smart, informed choice.

Why Compare SIP and PPF?

The comparison between SIP and PPF isn’t just about picking one over the other—it’s about aligning your investment with your life goals. Both SIP and PPF are aimed at encouraging disciplined savings, but they function very differently. Where SIP leverages the power of compounding in market-driven mutual funds, PPF offers a fixed interest rate and the comfort of government backing.

Understanding the core features of each helps:

Maximize tax savings

Align with specific financial goals

Build wealth smartly without taking undue risks

Additionally, with inflation consistently chipping away at the value of money, choosing the right investment vehicle becomes even more crucial. The right comparison can highlight how one might suit your long-term plans while the other might offer liquidity or security in the short run.

Let’s take a closer look at each option individually before diving into their differences and similarities.

Understanding SIP (Systematic Investment Plan)

What is SIP?

SIP, or Systematic Investment Plan, is a mode of investing in mutual funds where investors contribute a fixed amount regularly—usually monthly or quarterly—into a chosen fund. This method not only encourages financial discipline but also helps in averaging out market volatility over time. Unlike a one-time lump sum investment, SIPs are designed to reduce the impact of market fluctuations through a process known as rupee cost averaging.

SIPs can be started with as little as ₹500, making it an accessible investment option for salaried individuals, beginners, and even students. Whether you are planning for a new house, a child’s education, or your retirement, SIPs offer customizable plans based on the investor’s financial goals and risk tolerance.

Over time, SIPs have become one of the most favored investment options among millennials and Gen Z, thanks to their simplicity, flexibility, and transparency. As of 2025, the growing popularity of SIPs can be attributed to increasing financial literacy and the digital ease of starting and managing them.

How SIP Works?

When you invest through SIPs, your money is allocated to mutual funds—primarily equity, hybrid, or debt funds—depending on your selection. Each time you invest, you purchase units of the mutual fund at the prevailing NAV (Net Asset Value). When markets are low, you get more units; when markets are high, you get fewer. Over time, this averaging lowers the overall cost per unit.

This concept is known as rupee cost averaging and is one of SIP’s biggest strengths. Additionally, the returns you earn are compounded—meaning your money starts earning returns on the returns it generates. This exponential growth potential is a game-changer, especially when you stay invested for the long term.

SIPs also offer the benefit of automatic debits from your bank account, making the investment process seamless. You don’t have to time the market or worry about economic fluctuations.

Benefits of SIP Investment

Here are the key advantages of SIP:

Disciplined Investing: Automatic monthly investments cultivate a savings habit.

Power of Compounding: Long-term SIPs can lead to substantial wealth accumulation.

Flexibility: Start, pause, or stop SIPs anytime without penalties.

Rupee Cost Averaging: Helps in mitigating the impact of market volatility.

Accessibility: Can start with as little as ₹500 per month.

Goal-Based Investing: SIPs can be aligned with life goals—education, retirement, travel, etc.

Transparency: Easy to track and monitor via apps and dashboards.

Now that you know how SIP works, let’s dive into its counterpart—PPF.

Understanding PPF (Public Provident Fund)

What is PPF?

The Public Provident Fund (PPF) is a government-backed savings scheme launched in 1968 by the National Savings Institute. It’s primarily aimed at encouraging individuals to build a long-term retirement corpus through small savings, all while offering tax benefits and attractive interest rates.

PPF is one of the safest investment options in India due to its sovereign guarantee. It offers a fixed interest rate, reviewed quarterly by the Ministry of Finance. The maturity period is 15 years, which can be extended in blocks of 5 years. Because of its lock-in and guaranteed returns, it’s often recommended for risk-averse investors who prefer stability over high returns.

In the world of fluctuating equity markets and uncertain mutual fund returns, PPF provides a cushion of security, especially during volatile economic periods.

How PPF Works?

You can open a PPF account at any bank or post office with a minimum deposit of ₹500 and a maximum deposit of ₹1.5 lakh in a financial year. The interest is compounded annually and credited at the end of the financial year. The best part? The entire maturity amount, including the interest earned, is tax-free under Section 80C of the Income Tax Act.

Withdrawals are allowed only after the completion of the 7th year, and even then, they are limited. You can also take a loan against your PPF account between the 3rd and 6th year, which adds some liquidity despite the long lock-in.

Benefits of PPF Investment

Let’s break down the core advantages of PPF:

Guaranteed Returns: Government-declared fixed interest rates.

Risk-Free: Backed by the Government of India.

Tax-Free Returns: Both interest and maturity amounts are tax-exempt.

Long-Term Savings: Ideal for retirement and children’s future planning.

Loan Facility: Loan available from the 3rd year onwards.

Partial Withdrawals: Allowed after 7 years under specific conditions.

No Market Dependency: Immune to market ups and downs.

0 notes

Text

Mutual Funds vs Direct Equity: What’s Better for India’s New-Age Investors?

Introduction

India’s investment landscape has undergone a profound transformation in recent years. With demat accounts booming, SIPs at record highs, and stock market literacy on the rise, more Indians are building wealth through the markets than ever before. But for new-age investors—millennials, Gen Z, professionals, creators, and solopreneurs—one question often takes center stage: Should I invest via mutual funds or choose direct equity? Both options have their pros and cons. Both can grow your wealth. But they serve different needs, risk appetites, and investment styles. In this blog, we’ll unpack the differences, explore when and why to choose each, and help you decide what suits your financial goals best.

The Basics: Mutual Funds vs Direct Equity

Mutual Funds

• Pooled investment vehicles managed by professional fund managers • Diversify across stocks, sectors, or even asset classes (debt, gold, etc.) • Offer various types: equity, debt, hybrid, index, thematic, etc. • Investors can opt for SIPs (Systematic Investment Plans) or lumpsum investments

Direct Equity

• Buying individual stocks on your own via a demat and trading account • Full control over stock selection, entry/exit, and portfolio construction • Requires research, monitoring, and understanding of market trends • Higher risk, potentially higher returns if done right

How They Stack Up: Key Comparisons

Criteria Mutual Funds Direct Equity Risk Moderate (diversified) High (concentrated if unmanaged) Returns Consistent, market-linked Potentially high or low Control Low – fund manager decides Full – you decide everything Effort Low High (research-intensive) Costs Expense ratio (0.5–2%) Brokerage + STT + capital gains

Taxation Taxed like equity/debt (depending on type) Same, but based on actual holding period Accessibility Easy via SIP apps Needs stock market familiarity Best For Long-term, goal-based investors Active, risk-taking investors

Who Should Choose Mutual Funds? ✔ First-Time Investors If you're new to markets, mutual funds offer a low-effort, low-stress way to start. SIPs in large-cap or index funds let you build wealth steadily without timing the market. ✔ Busy Professionals If you don’t have time to track earnings reports, market news, or charts, let fund managers do the heavy lifting. Choose funds aligned to your risk profile and goals. ✔ Goal-Based Planners Whether it’s retirement, a house down payment, or your child’s education, mutual funds are great for structured, long-term planning with flexibility. ✔ Risk-Averse Individuals With diversification built-in, funds cushion the impact of individual stock underperformance. Debt and hybrid funds offer lower volatility options too. Who Should Choose Direct Equity? ✔ DIY Enthusiasts If you're passionate about researching companies, tracking macroeconomic trends, and analyzing balance sheets, direct equity gives you full autonomy. ✔ High Risk, High Reward Seekers Equity investing offers the potential to beat mutual funds—but only with deep research, emotional discipline, and patience. ✔ Niche Sector Followers If you believe in a specific theme (like EV, AI, or PSU revival), direct equity allows targeted exposure which most mutual funds can’t provide. ✔ Active Portfolio Managers

If you want to rebalance frequently, use technical indicators, or apply contrarian views, direct stock investing offers flexibility unmatched by funds. Real-World Example: ₹10,000 per Month for 5 Years • Mutual Fund SIP in a diversified equity fund = ₹9.5–₹11 lakh (average returns ~12–14%) • Direct Equity portfolio, if well-chosen = Could range from ₹8 lakh to ₹14+ lakh depending on strategy, timing, and discipline

The variance is wider in direct equity. Skill amplifies gains—or losses. The Hybrid Approach: Why Not Both? Many investors are now blending both options to build robust, flexible portfolios.

Example Strategy: • 60% in mutual funds (for passive, long-term growth) • 40% in direct equity (for active, tactical opportunities)

This approach ensures your wealth compounds while allowing you to participate in themes or short-term trades without overexposing yourself. Tips for Mutual Fund Investors • Choose funds based on long-term performance, not star ratings • Avoid over-diversifying—3–5 funds are enough • Use SIPs for rupee-cost averaging and compounding • Monitor portfolio annually, not daily • Watch for high expense ratios and underperforming funds

Tips for Direct Equity Investors • Invest in businesses, not just stock prices • Stick to quality: strong ROE, low debt, good governance • Avoid overtrading—costs eat into returns • Keep emotions in check during volatility • Don’t chase tips—build conviction through research • Maintain a watchlist, track earnings, and diversify across sectors

What Experts Say “Mutual funds offer consistency. Direct equity offers control. The best portfolios find a smart balance.” — Fund Manager, Top AMC “Direct investing is rewarding, but unforgiving. It's for those who treat it like a business, not a bet.” — SEBI Registered Advisor

Conclusion

There’s no one-size-fits-all answer to mutual funds vs direct equity. The better question is: what works for you? Your time, temperament, knowledge, and goals should dictate your choice. Whether you prefer the simplicity of SIPs or the thrill of stock picking, remember that consistency, patience, and informed decisions are what ultimately grow wealth.

In the end, it’s not about picking the perfect product—it’s about building the right habit.

Disclaimer

This blog post is published by Zebu, and is intended solely for informational and educational purposes. The content shared does not constitute investment advice, financial planning, or an offer to buy or sell any financial instruments. The views expressed are based on the author’s interpretation of publicly available information and market trends at the time of writing.

While Zebu makes every effort to provide accurate and up-to-date information, we do not guarantee the completeness, reliability, or suitability of the content for any particular purpose. Investors are strongly advised to perform their own due diligence and consult with certified financial advisors or tax consultants before making any investment decisions.

#zebu#finance#investment#investwisely#financialfreedom#investing#investors#makemoney#mutual funds#investmentgoals

0 notes

Text

The Future of Finance with Nick Trimble Financial Advisor

As the financial landscape continues to evolve, individuals and businesses alike are seeking innovative solutions to navigate a rapidly changing market. Nick Trimble Financial Advisor has long been at the forefront of guiding clients through these transitions, blending forward-thinking approaches with solid financial foundations. The role of a financial advisor has expanded far beyond traditional investment management, requiring expertise in a range of areas including technology, market trends, and personalized financial strategies.

Understanding the Shift in Financial Services

The financial services industry is undergoing significant changes driven by technological advancements and shifting economic dynamics. Traditional models are giving way to more agile, tech-driven solutions that emphasize efficiency, accessibility, and personalized services. One of the key drivers of this shift is the increasing importance of financial technology, commonly known as fintech. From robo-advisors to blockchain, fintech is redefining how financial services are delivered and consumed.

Nick recognizes the importance of embracing technology without losing sight of personalized care. While technology offers powerful tools for managing investments, it cannot replace the value of human insight. A good financial advisor must blend innovation with experience, providing clients with both the cutting-edge tools they need and the guidance to make informed decisions.

The Rise of Data-Driven Decisions

In the future of finance, data is king. Access to real-time financial data and advanced analytics allows financial advisors to make quicker, more informed decisions. Tools like artificial intelligence (AI) and machine learning enable advisors to process vast amounts of data, uncover trends, and create more accurate predictions about market movements.

Financial planning is becoming increasingly data-driven, and clients now expect advisors to leverage this wealth of information to provide proactive, customized advice. Nick Trimble understands that the ability to analyze data and turn it into actionable insights is what will set successful advisors apart in the coming years.

The Importance of Sustainable and Ethical Investing

As global concerns about climate change and social justice continue to grow, investors are placing more importance on sustainability and ethical investing. Clients are no longer simply looking for financial returns—they are also focused on aligning their investments with their values.

Environmental, Social, and Governance (ESG) criteria are becoming integral to investment strategies, as clients increasingly seek companies that are committed to sustainability, ethical practices, and positive social impact. Financial advisors must be well-versed in these areas to meet the evolving demands of their clients. Nick has always been a proponent of responsible investing, helping clients build portfolios that not only perform well financially but also contribute positively to society.

Financial Literacy and Education for the Next Generation

One of the most important roles a financial advisor will play in the future is fostering financial literacy. As the financial landscape grows more complex, individuals need to develop a deeper understanding of their personal finances, from budgeting and saving to investing and retirement planning.

The next generation of investors, particularly millennials and Gen Z, are more engaged with their financial futures than ever before. They have access to a wealth of information but need guidance on how to use that information effectively. A financial advisor’s ability to educate and empower clients will be essential in helping them make smart, long-term financial decisions. Nick believes that financial education is a critical part of empowering clients to take control of their financial futures.

Adapting to Changing Regulations

As the financial industry evolves, so too do the regulations that govern it. Keeping up with these changes is essential for both financial professionals and their clients. With increased scrutiny on financial institutions and growing concerns about cybersecurity and data privacy, financial advisors must stay ahead of regulatory changes to ensure compliance and mitigate risk.

The future of finance will likely see an increasing emphasis on regulations related to consumer protection, financial transparency, and the use of technology. Advisors must not only understand the legal landscape but also be able to advise clients on how to navigate it effectively. Nick is committed to staying updated on these changes, ensuring that his clients receive not only sound financial advice but also guidance that complies with the latest regulations.

The Role of Artificial Intelligence and Automation

In recent years, artificial intelligence (AI) and automation have become central to many industries, and finance is no exception. From automating routine tasks to optimizing investment strategies, AI is transforming the way financial advisors operate. For example, robo-advisors are becoming increasingly popular, using algorithms to manage investment portfolios with little to no human intervention.

While AI can improve efficiency and accessibility, it also presents challenges, particularly in maintaining a personal touch. While these tools can offer automated solutions, human judgment remains crucial in tailoring financial plans to individual needs. Financial advisors must strike the right balance between utilizing AI to streamline operations and maintaining the personalized service that clients expect. Nick embraces these technological tools while ensuring that clients still receive the individualized care and strategic advice they deserve.

Financial Wellness and Holistic Planning

As financial needs become more complex, there is a growing recognition of the importance of holistic financial planning. Financial wellness is no longer limited to investment management; it encompasses all aspects of an individual’s financial life, including budgeting, debt management, retirement planning, and insurance.

Holistic financial planning focuses on creating a comprehensive strategy that addresses all areas of a client’s financial situation. Nick Trimble, Financial Advisor takes a well-rounded approach, ensuring that clients’ short- and long-term goals are aligned and that all aspects of their financial lives are working together harmoniously. This approach ensures that clients are not just investing their money wisely but also protecting and growing their wealth in a way that supports their overall financial health.

Adapting to a Globalized Market

The global economy is more interconnected than ever before, and this is having a profound impact on the way financial advisors operate. With globalization comes increased access to international markets, and investors are seeking opportunities that extend beyond their domestic borders.

However, this global market also introduces new risks, including currency fluctuations, geopolitical instability, and differing economic conditions. Financial advisors must stay attuned to these factors, understanding how they can affect investment strategies and advising clients on how to diversify their portfolios to minimize risk. Nick Trimble Financial Advisor remains committed to helping clients navigate the complexities of the global market, offering strategies that balance risk and reward across a diverse set of opportunities.

Summary

The future of finance is full of promise and innovation. As technology, data analytics, and sustainability reshape the financial landscape, financial advisors like Nick Trimble Financial Advisor will play an increasingly important role in helping clients navigate these changes. By embracing new technologies, fostering financial literacy, and providing personalized, holistic advice, financial professionals will ensure that their clients are not only prepared for the future but are also able to thrive in it.

0 notes

Video

youtube

Why Millennials and Gen Z MUST Start Retirement Planning NOW! #Tips! #po...

1 note

·

View note