#Respiratory Disease Testing Market Analysis

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

The total number of visits Tumblr.com received during January 2021 is 327 million.

Text

Respiratory Disease Testing Market Outlook, Competitive Strategies And Forecast

The global respiratory disease testing market size is expected to reach USD 7.75 billion by 2030, registering a CAGR of 2.8% from 2023 to 2030, according to a new report by Grand View Research, Inc. The market is driven by the rising prevalence of respiratory diseases. As per Forum of International Respiratory Societies, more than 200 million people across the globe suffered from Chronic Obstructive Pulmonary Disease (COPD) and 235 million suffered from asthma in 2014. In addition, the source stated that more than 50 million people struggle with occupational lung diseases annually. Thus, constantly growing target patient population is anticipated to drive the growth.

The adoption of innovative technologies, such as Computed Tomography (CT), for COPD diagnosis is expected to drive the growth. The other new technology in acute medical management of COPD is pulse oximeter that is used for outpatient monitoring. Airway management plays a main role in testing and management of COPD. Also, with recent technological innovations, there has been a 12.1 % increase in the use of Noninvasive Mechanical Ventilation (NIV) for management of COPD. Along with technological advancements, use of digital radiography (X-ray) and advanced portable spirometers is gaining momentum in the respiratory disease testing/diagnostics market.

Gather more insights about the market drivers, restrains and growth of the Respiratory Disease Testing Market

Respiratory Disease Testing Market Report Highlights

• Growing prevalence of respiratory diseases and rapid technological advancements are two of the major factors expected to propel the market growth

• Based on products, imaging tests held the largest share in 2022 due to rapid development and adoption of innovative technologies

• Based on application, tuberculosis was the largest market in 2022 owing to rising prevalence of the disease globally

• Based on end-use, hospitals segment held the largest share in 2022 and is anticipated to grow over the forecast period due to an increase in hospitalization and a growing preference for hospital treatment

• North America dominated the respiratory disease testing market in 2022. Growing prevalence of respiratory diseases such as COPD, & asthma, increasing demand for early diagnosis, and rising awareness amongst patients about the benefits of early diagnosis are responsible for the dominance

• Asia Pacific region is expected to grow at the fastest rate during the forecast period. This growth can be attributed to various factors, such as improving healthcare infrastructure and increasing patient awareness regarding the availability of new diagnostic techniques for respiratory diseases, such as COPD & asthma

• Some of the major players competing in this market include, but are not limited to, Becton Dickinson (Carefusion Corporation); Koninklijke Philips N.V. (Respironics); ResMed Company; Fischer & Paykel; and Medtronic. These players are strong brands in the market as they have elaborate product portfolios in respiratory disease diagnostics market

Respiratory Disease Testing Market Segmentation

Grand View Research has segmented the global respiratory disease testing market on the basis of product, application, end-use, and region:

Respiratory Disease Testing Market Product Outlook (Revenue, USD Million, 2018 - 2030)

• Imaging Tests

• Respiratory Measurement Devices

• Blood Gas Test

• Others

Respiratory Disease Testing Market Application Outlook (Revenue, USD Million, 2018 - 2030)

• Chronic Obstructive Pulmonary Disease

• Lung Cancer

• Asthma

• Tuberculosis

• Other

Respiratory Disease Testing Market End-use Outlook (Revenue, USD Million, 2018 - 2030)

• Hospital

• Physicians Clinic

• Clinical Laboratories

• Other

Respiratory Disease Testing Market Regional Outlook (Revenue, USD Million, 2018 - 2030)

• North America

o U.S.

o Canada

• Europe

o UK

o Germany

o France

o Italy

o Spain

o Sweden

o Norway

o Denmark

• Asia Pacific

o Japan

o China

o India

o Australia

o Thailand

o South Korea

• Latin America

o Brazil

o Mexico

o Argentina

• Middle East and Africa

o Saudi Arabia

o South Africa

o UAE

o Kuwait

Order a free sample PDF of the Respiratory Disease Testing Market Intelligence Study, published by Grand View Research.

#Respiratory Disease Testing Market#Respiratory Disease Testing Market Size#Respiratory Disease Testing Market Share#Respiratory Disease Testing Market Analysis#Respiratory Disease Testing Market Growth

0 notes

Text

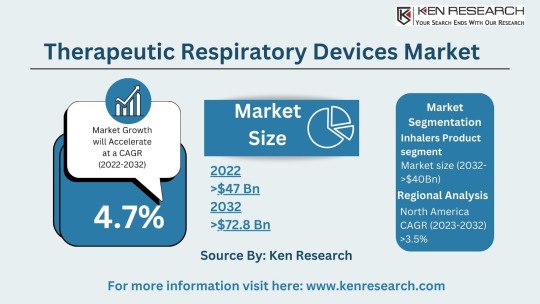

The $64.2 billion Respiratory Market & Its Future Trends, Segmentation and Forecast

The global respiratory market size reached a staggering USD 42.3 billion in 2023. This impressive figure highlights the significant need for respiratory devices and treatments to address a wide range of respiratory conditions. The market is projected to grow at a Compound Annual Growth Rate (CAGR) of approximately 7.4%, reaching an estimated USD 64.2 billion by 2030. This growth can be attributed to several factors:

Rising Prevalence of Chronic Respiratory Diseases: Conditions like asthma, chronic obstructive pulmonary disease (COPD), and sleep apnea are on the rise due to factors like air pollution, smoking, and an aging population.

Increased Life Expectancy: With an aging population, the demand for respiratory support devices for chronic conditions is expected to rise.

Technological Advancements: The development of innovative respiratory devices, such as portable nebulizers and advanced ventilators, offers improved treatment options.

Growing Focus on Homecare: The increasing emphasis on home-based care for respiratory patients fuels the demand for user-friendly respiratory devices.

Respiratory Market Segmentation: Catering to Diverse Needs

The respiratory market segmentation reflects the vast array of products and technologies available to address different respiratory needs:

By Application:

Therapeutic Respiratory Devices Market: This segment includes devices used for treatment, such as nebulizers, metered-dose inhalers (MDIs), and continuous positive airway pressure (CPAP) machines used for sleep apnea. The respiratory inhalers market is a significant sub-segment due to the widespread use of inhalers for asthma and COPD.

Anesthesia & Respiratory Devices: Specialized equipment used in surgical settings to deliver oxygen and maintain proper ventilation during anesthesia. The anesthesia and respiratory devices market caters to the specific needs of hospitals and surgical centers.

Respiratory Gas Analysis: This technology analyzes the composition of respiratory gases to assess lung function and identify potential respiratory issues.

By Device Type:

Respiratory Care Devices: This broad category encompasses various devices used for diagnosis, treatment, and monitoring of respiratory conditions. Examples include nebulizers, inhalers, ventilators, and CPAP (continuous positive airway pressure) machines.

Respiratory Monitoring Devices: These devices track vital signs such as blood oxygen levels and respiratory rate, allowing for continuous monitoring of patients with respiratory difficulties. The respiratory monitoring devices market is experiencing significant growth due to the increasing focus on patient safety and remote monitoring.

Respiratory Measurement Devices: These devices measure lung function and capacity, providing vital diagnostic information for respiratory conditions. The respiratory disease testing market relies heavily on these devices for accurate diagnosis.

Respiratory Protective Equipment (RPE): This equipment protects users from inhaling harmful substances, including masks and respirators. The respiratory protective equipment market is expected to witness growth due to rising concerns about air pollution and pandemics.

Take a look at: Forecasting the Respiratory Market, Size, Segmentation and Future Trends

Top Players in Respiratory Market: Breathing Innovation

Several established medical device manufacturers and specialty respiratory companies dominate the respiratory market:

Some of the top players in the respiratory market include:

Philips Healthcare

ResMed

Medtronic

GE Healthcare

Fisher & Paykel

Emerging Markets: A Rising Demand for Respiratory Solutions

Developing nations with growing populations and increasing healthcare expenditure present a significant opportunity. For instance, the bovine respiratory disease treatment market highlights the growing demand for respiratory solutions in the animal health sector.

Respiratory Market Trends: Shaping the Future of Respiratory Care

Exciting trends are shaping the respiratory market and transforming how we manage respiratory conditions:

Focus on Homecare Solutions: The emphasis on providing effective respiratory care solutions for patients in a home setting is driving innovation in portable and user-friendly devices.

Telemedicine Integration: Telehealth platforms allow remote monitoring and consultations with healthcare professionals, improving respiratory care management.

Connected Devices and Data Analytics: The integration of Internet of Things (IoT) technology allows for real-time data collection and analysis of respiratory parameters, leading to personalized treatment plans.

Emphasis on Early Detection and Prevention: The trend towards early detection and prevention of respiratory diseases through screening programs and lifestyle modifications is gaining momentum.

Challenges and Opportunities: Navigating the Respiratory Landscape

While the respiratory market offers promising opportunities, challenges also exist:

Challenges:

Cost Concerns: The high cost of some respiratory devices, particularly advanced equipment, can be a barrier to access for some patients.

Counterfeit Products: The presence of counterfeit respiratory products poses a safety risk and necessitates stringent quality control measures.

Compliance with Regulations: Navigating evolving regulatory requirements for medical devices can be complex and requires ongoing compliance efforts.

Opportunities:

Focus on Homecare: The trend towards homecare for respiratory patients creates a demand for portable and user-friendly respiratory devices.

Telemedicine Integration: Integrating respiratory monitoring devices with telemedicine platforms allows for remote patient monitoring and improved care coordination.

Emerging Technologies: The potential of new technologies like artificial intelligence and wearable devices can revolutionize respiratory care and diagnosis.

Respiratory Market Future Outlook: A Collaborative Approach

The respiratory market future outlook is promising, with a projected market size of USD 64.2 billion by 2030. And this suggests a market driven by innovation, collaboration, and a focus on improving patient outcomes. Here's what we can expect:

Collaboration between Medical Device Manufacturers and Healthcare Providers: Collaboration between these entities will be crucial for developing and implementing effective respiratory care solutions that address real-world clinical needs.

Increased Focus on Patient Education and Self-Management: Empowering patients with respiratory conditions to manage their health through education and user-friendly technology will be a key focus.

Conclusion:

The respiratory market plays a vital role in supporting lung health and improving the lives of millions suffering from respiratory illnesses. As the market continues to evolve, driven by innovation, collaboration, and a focus on patient-centric care, we can expect a future where managing respiratory conditions becomes more effective, accessible, and empowering for individuals and healthcare professionals alike.You can also read about: Future Forecast and Trends in the $35.58 Billion Respiratory Market

#Respiratory Market#Respiratory Industry#Respiratory Sector#Respiratory Market Size#Respiratory Market Segmentation#Respiratory Care Devices Market#Respiratory Devices Market#Therapeutic Respiratory Devices Market#Respiratory measurement devices market#respiratory gas analysis#anesthesia and respiratory devices market#respiratory disease testing market#bovine respiratory disease treatment market#respiratory inhalers market#respiratory monitoring devices market#respiratory protective equipment market#Top Players in Respiratory Market#Respiratory Market Trends#Respiratory Market Future Outlook

0 notes

Text

North America Sepsis Diagnostics Market Size, Competitors Strategy, Regional Analysis and Industry Growth by Forecast (2021-2028)

The North America sepsis diagnostics market is expected to grow from US$ 279.06 million in 2021 to US$ 513.33 million by 2028. It is estimated to record a CAGR of 9.1% from 2021 to 2028.

High Incidence of Sepsis due to Increasing Nosocomial Infections Drives North America Sepsis Diagnostics Market

The underlying cause of sepsis is infection, with a heightened risk among immunocompromised individuals, such as those receiving chemotherapy, individuals who have undergone splenectomy, and those with AIDS, diabetes, and other chronic conditions. Among various types of infections, nosocomial infections are a leading cause of illness and mortality in hospitalized patients. The Centers for Disease Control and Prevention's (CDC) "2020 National and State Healthcare-Associated Infections Progress Report" (published in 2021) indicated that the US experienced increases of about 24% in central line-associated bloodstream infections, 35% in ventilator-associated events, and 15% in Methicillin-resistant Staphylococcus aureus (MRSA) bacteremia between 2019 and 2020. As per a report by the Global Sepsis Alliance (GSA), approximately 26 million people worldwide develop sepsis annually, leading to roughly 8 million deaths. Consequently, the increasing incidence of bloodstream infections is anticipated to fuel greater adoption of sepsis diagnostic products. Furthermore, mortality frequently arises from diarrheal diseases or lower respiratory infections, many of which are preventable through early diagnosis and appropriate clinical management. Thus, the high incidence rate of sepsis is expected to boost the demand for sepsis diagnostic products, which would support the expansion of the North America sepsis diagnostics industry during the forecast period.

Download our Sample PDF Report

@ https://www.businessmarketinsights.com/sample/BMIRE00025664

North America Sepsis Diagnostics Strategic Insights

Strategic insights for the North America Sepsis Diagnostics sector provide data-informed analysis of the industry's environment, encompassing current trends, major players, and regional specificities. These insights offer actionable recommendations, allowing readers to distinguish themselves from competitors by identifying unexploited segments or developing unique value propositions. By utilizing data analytics, these insights help industry participants—whether investors, manufacturers, or other stakeholders—to anticipate market evolutions. A forward-looking approach is crucial, enabling stakeholders to predict market shifts and strategically position themselves for sustained success within this dynamic region. Ultimately, effective strategic insights empower readers to make well-informed decisions that drive profitability and achieve their business objectives within the market.

North America Sepsis Diagnostics Market Segmentation

North America Sepsis Diagnostics Market: By Product

Instruments

Reagents and Assays

Blood Culture Media

Software

North America Sepsis Diagnostics Market: By Technology

Molecular Diagnostics

North America Sepsis Diagnostics Market: By Flow

(Cytometry, Microfluidics, Immunoassay, Biomarkers, Microbiology)

North America Sepsis Diagnostics Market: By Method

Automated Diagnostics and Conventional Diagnostics

North America Sepsis Diagnostics Market: By Test Type

Point-of-Care Tests and Laboratory Tests

North America Sepsis Diagnostics Market: Regions and Countries Covered

North America

US

Canada

Mexico

North America Sepsis Diagnostics Market: Market leaders and key company profiles

Abbott

BD

bioMerieux SA

Danaher (Beckman Coulter)

F. HOFFMANN-LA ROCHE LTD.

Immunexpress Inc.

Luminex Corporation

T2 Biosystems, Inc.

THERMO FISHER SCIENTIFIC INC.

About Us:

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications

#North America Sepsis Diagnostics Market#North America Sepsis Diagnostics Market Size#North America Sepsis Diagnostics Market Strategy

0 notes

Text

Allergy Diagnostics Market: Factors Behind Market’s Expeditious Growth 2025-2032

The global allergy diagnostics market is expected to experience significant growth between 2025 and 2032. This expansion is driven by increasing allergic disease prevalence, advancements in diagnostic technologies, and rising awareness of allergy management. As allergies become more common globally, the demand for effective diagnostic solutions is growing rapidly.

Allergy Diagnostics Market size is poised to grow from USD 5.33 billion in 2024 to USD 12.28 billion by 2032, growing at a CAGR of 11.0% during the forecast period (2025-2032). The market is influenced by the rising incidence of allergies, technological innovations enhancing diagnostic accuracy, and increasing healthcare access, particularly in emerging economies.

Request Sample of the Report - https://www.skyquestt.com/sample-request/allergy-diagnostics-market

Key Market Segments

1. By Product & Service

Consumables: Reagents, testing strips, assay kits, and diagnostic panels are essential for allergy testing. Consumables hold the largest market share due to their recurring use and cost-effectiveness.

Instruments: Diagnostic devices like ELISA analyzers and immunoassay systems are crucial for performing allergy tests in clinical and laboratory settings. The demand for advanced instruments is growing with the increasing number of diagnostic laboratories.

Services: Diagnostic services provided by laboratories, hospitals, and clinics are expanding, particularly in urban areas, where patients increasingly seek specialized allergy testing.

2. By Test Type

In Vivo Tests: Skin prick testing and intradermal tests are commonly used due to their rapid results and affordability. These tests are essential for diagnosing common allergic conditions like hay fever, asthma, and rhinitis.

In Vitro Tests: Blood tests, such as ImmunoCAP and RAST, provide in-depth analysis of allergen-specific IgE levels. In vitro tests are particularly useful in complex cases and for pediatric patients.

3. By Allergen Type

Inhaled Allergens: Dust mites, pollen, molds, and pet dander are some of the most common environmental allergens tested. Urbanization and increasing pollution contribute to the growing demand for testing inhaled allergens.

Food Allergens: Food allergies, particularly to peanuts, dairy, gluten, shellfish, and tree nuts, are becoming more prevalent. This drives the demand for accurate food allergen testing, especially in North America and Europe.

Drug and Insect Allergens: Although a niche market, testing for drug allergies (e.g., penicillin) and insect stings (e.g., from bees) is critical for preventing life-threatening allergic reactions.

4. By End User

Hospitals and Clinics: These institutions are primary providers of allergy testing, especially in developed markets.

Diagnostic Laboratories: The fastest-growing segment, as diagnostic laboratories offer specialized testing services with faster results.

Academic and Research Institutions: These institutions are involved in advancing allergy research and developing next-generation diagnostic tools.

Get Customized Reports with your Requirements - https://www.skyquestt.com/speak-with-analyst/allergy-diagnostics-market

Regional Market Insights

North America: Dominates the global allergy diagnostics market due to a high prevalence of allergies, advanced healthcare infrastructure, and widespread access to insurance and diagnostic services.

Europe: Experiences steady growth, driven by an aging population and the rising prevalence of respiratory and food allergies.

Asia-Pacific: Expected to be the fastest-growing region due to urbanization, increasing pollution levels, and expanding healthcare access in countries like China and India.

Latin America & Middle East/Africa: Growing awareness of allergic conditions and improvements in healthcare access are driving market growth in these regions.

Key Market Drivers

Increasing Allergy Prevalence: WHO estimates that over 30% of the global population suffers from allergic conditions, which is driving the demand for allergy diagnostics.

Technological Advancements: Automation, multiplex testing, AI-driven diagnostics, and improved assay techniques are making allergy testing faster, more accurate, and more accessible.

Government Initiatives: Government policies and public health campaigns focused on early allergy diagnosis and treatment are helping to expand the market for allergy diagnostics.

Key Players

Key players in the allergy diagnostics market are driving growth through innovation, strategic partnerships, and geographic expansion. Some of the prominent companies in the market include:

Thermo Fisher Scientific Inc.: Known for its ImmunoCAP system, which is widely used for specific IgE testing.

Danaher Corporation (Beckman Coulter): A leader in medical diagnostics, offering immunoassay solutions for allergy testing.

Siemens Healthineers AG: Provides a broad range of allergy diagnostics, including diagnostic panels for food and environmental allergens.

bioMérieux SA: Offers allergy diagnostic solutions, with a strong presence in Europe.

Omega Diagnostics Group PLC: Specializes in food and inhalant allergen testing kits.

R-Biopharm AG: Known for its ELISA-based allergy testing kits.

Lincoln Diagnostics, Inc.: Focuses on skin prick and patch testing solutions.

Stallergenes Greer: Provides allergy diagnostics and immunotherapy products.

These companies continue to invest in research and development to create innovative diagnostic solutions that can offer faster and more accurate results.

Read More for Better Understanding - https://www.skyquestt.com/report/allergy-diagnostics-market

Challenges and Restraints

While the allergy diagnostics market is growing, there are several challenges:

High Cost of Advanced Tests: Allergy testing, particularly in vitro diagnostics, can be costly, limiting access in low- and middle-income regions.

Regulatory Challenges: Differences in regulatory standards across regions can delay the approval of new diagnostic products and hinder market entry.

Limited Awareness in Rural Areas: In certain regions, particularly rural areas, there is still limited awareness about allergy testing and management, which can slow market growth.

Future Outlook The future of the allergy diagnostics market looks promising, with advancements in digital health, home-based testing, and personalized medicine. AI and genomics-based diagnostics will enable more accurate and personalized allergy testing, while environmental monitoring could help predict allergic reactions. As the market evolves, the focus will shift toward making allergy diagnostics more accessible, affordable, and efficient for a broader range of patients.

#Allergy Diagnostics Market#Allergy Diagnostics Industry#Allergy Diagnostics Market Size#Allergy Diagnostics Market Forecast

0 notes

Text

Infectious Disease Diagnostics Market: Projected to Reach USD 55.55 Billion by 2030, Growing at a CAGR of 3.48%

Market Overview:

The Infectious Disease Diagnostics Market is projected to be valued at USD 46.81 billion in 2025 and is anticipated to reach USD 55.55 billion by 2030, growing at a compound annual growth rate (CAGR) of 3.48% during the forecast period from 2025 to 2030.

Key Drivers of Market Growth:

Rising Prevalence of Infectious Diseases: The increasing global burden of infectious diseases, including respiratory infections, gastrointestinal diseases, sexually transmitted infections, and vector-borne diseases, is a major driver for the diagnostic industry. The COVID-19 pandemic further highlighted the critical need for fast and reliable diagnostic tests, driving a surge in demand for diagnostics worldwide. Other infectious diseases, such as tuberculosis, malaria, HIV/AIDS, and influenza, also contribute to market growth as the need for effective diagnostic tools remains high.

Technological Advancements in Diagnostic Tools: Innovations in molecular diagnostics, PCR (Polymerase Chain Reaction), next-generation sequencing (NGS), and point-of-care (POC) diagnostics are transforming the way infectious diseases are diagnosed. Technologies such as rapid antigen tests, CRISPR-based diagnostics, and biosensors are enabling quicker and more accurate results, improving the ability to diagnose infections early and effectively. This technological progress is driving adoption across hospitals, clinics, and even remote areas, making diagnostics more accessible and efficient.

Focus on Early Detection and Prevention: There is a growing emphasis on the early detection and prevention of infectious diseases to reduce their impact on public health. Early detection helps prevent outbreaks, limits the spread of diseases, and ensures timely treatment, which is crucial in managing infectious diseases like HIV, malaria, and tuberculosis. With more diagnostic tests available that can detect infections quickly and accurately, health professionals can take proactive measures.

Increased Demand for Personalized Medicine: Personalized medicine, which tailors treatment based on individual patient characteristics, is becoming more prevalent. Infectious disease diagnostics plays a crucial role in this field by enabling the identification of specific pathogens, determining antimicrobial resistance (AMR), and facilitating the selection of the most effective treatment for each patient. This trend is accelerating the development of diagnostic tools and their integration into routine healthcare practices.

Rising Healthcare Investments and Government Initiatives: Governments and private organizations are increasing investments in healthcare infrastructure and diagnostic capabilities, especially in developing regions. Initiatives aimed at improving healthcare access and reducing the burden of infectious diseases in low- and middle-income countries are driving the demand for diagnostic solutions. For instance, international collaborations like the Global Fund are actively supporting the fight against infectious diseases like HIV, tuberculosis, and malaria through diagnostic initiatives.

Market Segmentation:

The infectious disease diagnostics market can be segmented by product type, technology, application, and geography:

By Product Type:

Instruments: This includes diagnostic platforms such as PCR machines, mass spectrometers, and next-generation sequencing platforms used for accurate and high-throughput diagnostics.

Reagents and Kits: Includes diagnostic test kits for various infections, such as viral, bacterial, and fungal diseases, as well as reagents used in the process of testing.

Software & Services: Diagnostic software used for data analysis, management, and interpretation, as well as services related to diagnostic testing.

By Technology:

Molecular Diagnostics: Includes PCR, NGS, and other molecular techniques that identify pathogens at the genetic level. These are considered the gold standard for diagnosing many infectious diseases.

Immunoassays: These tests rely on antibodies and antigens to detect infections. Rapid antigen tests, ELISA, and lateral flow assays are commonly used for quick diagnostics.

Culture & Sensitivity Testing: These traditional methods involve growing bacterial pathogens in culture media to identify the pathogen and test its sensitivity to antibiotics.

Point-of-Care (POC) Diagnostics: These devices provide rapid results, often within minutes, at the site of patient care. POC diagnostics are becoming more popular in both developed and developing countries due to their ease of use and speed.

By Application:

Respiratory Infections: This includes diagnostics for diseases such as pneumonia, tuberculosis, and influenza.

Sexually Transmitted Infections (STIs): Testing for diseases like HIV, syphilis, gonorrhea, and chlamydia.

Gastrointestinal Infections: Includes diagnostic tests for pathogens like Salmonella, E. coli, and Rotavirus.

Vector-borne Diseases: Diagnostic tools for diseases transmitted by vectors like mosquitoes, such as malaria, dengue, and Zika virus.

Others: This includes diagnostics for emerging infectious diseases, foodborne infections, and healthcare-associated infections.

By Geography:

North America: Dominates the market due to advanced healthcare infrastructure, high healthcare spending, and a high adoption rate of advanced diagnostic technologies.

Europe: The European market is growing steadily, driven by an increasing focus on infectious disease prevention and technological advancements in diagnostic solutions.

Asia-Pacific: Expected to witness the fastest growth, particularly in countries like China, India, and Japan, due to rising healthcare investments, an increasing prevalence of infectious diseases, and a growing population.

Rest of the World: This includes growing markets in Latin America, the Middle East, and Africa, where efforts to improve healthcare infrastructure are driving demand for diagnostic solutions.

Trends Shaping the Market:

Integration of Artificial Intelligence (AI) in Diagnostics: AI and machine learning are being increasingly incorporated into infectious disease diagnostics, particularly in imaging and data analysis. These technologies enhance the accuracy and speed of diagnostic results, enabling quicker decision-making for healthcare providers.

Rise of Wearable Diagnostic Devices: Wearable health devices capable of monitoring biomarkers and detecting early signs of infection are gaining popularity. These devices could offer early warnings for diseases like influenza, COVID-19, and other respiratory infections.

Telemedicine and Remote Diagnostics: The COVID-19 pandemic has accelerated the adoption of telemedicine and remote healthcare. Infectious disease diagnostics, including at-home testing kits and remote monitoring, are expected to continue growing as part of this trend.

Point-of-Care Testing in Resource-Limited Settings: The demand for affordable and easy-to-use diagnostic solutions in resource-limited settings is rising. Point-of-care diagnostics, which can be deployed outside traditional laboratory settings, are helping bridge the gap in these areas.

Challenges in the Market:

High Costs and Limited Accessibility: Despite technological advancements, diagnostic tests—especially molecular diagnostics—can be expensive and may not be accessible in all regions, particularly in developing countries.

Regulatory Hurdles: The approval process for new diagnostic tests can be lengthy and complex. Stringent regulatory standards and the need for extensive clinical trials can delay product launches and increase costs.

Technological Complexity: While advanced diagnostic technologies offer superior results, their complexity can pose challenges in terms of operation, maintenance, and training for healthcare professionals, particularly in low-resource settings.

Competitive Landscape: The infectious disease diagnostics market is highly competitive, with key players including:

Abbott Laboratories

Roche Diagnostics

Siemens Healthineers

Thermo Fisher Scientific

BD (Becton, Dickinson and Company)

Cepheid

bioMérieux

These companies are continuously focusing on innovation, strategic partnerships, and global expansion to maintain a competitive edge in the growing diagnostics market.

Conclusion: The infectious disease diagnostics market is on a strong growth trajectory, driven by increasing demand for accurate, rapid, and accessible testing solutions. Technological innovations, the rising prevalence of infectious diseases, and greater emphasis on early detection are fueling the market’s expansion. However, challenges related to cost, regulatory requirements, and accessibility need to be addressed to fully realize the potential of these diagnostic tools, especially in low- and middle-income regions.

For a detailed overview and more insights, you can refer to the full market research report by Mordor Intelligence

0 notes

Text

Medical Elastomers Market Analysis by Type, Global Size, Segmentation, Regional Trends, Key Players, Company Share, and Forecast from 2025 to 2035

Industry Outlook

The medical elastomers market was valued at USD 8.6 billion in 2024 and is projected to reach USD 19.65 billion by 2035, growing at a CAGR of approximately 7.8% between 2025 and 2035. Medical elastomers are flexible polymers used in medical instruments, tooling, equipment, and packaging. Examples include thermoplastic elastomers (TPEs) and synthetic elastomers like silicone and EPDM, known for their durability, flexibility, and sterilization capability. These materials are essential in applications such as tubing, implants, drug delivery, and gloves.

The increasing adoption of wearable medical devices and advancements in polymer technology are key growth drivers. North America and Asia-Pacific lead the market due to their well-developed healthcare industries and expanding medical device manufacturing. Emerging trends include the integration of 3D printing technology and sustainable elastomers, though regulatory approvals remain a significant challenge.

Get free sample Research Report - https://www.metatechinsights.com/request-sample/2153

Market Dynamics

Growing Global Healthcare Demand

The rising demand for healthcare services is a primary driver of the medical elastomers market. The increasing aging population and the prevalence of chronic diseases have heightened the need for medical devices, implants, and drug delivery systems. Flexible and biocompatible elastomers are becoming essential for wearable healthcare products and home health treatments.

Governments and healthcare organizations are expanding medical facilities, further boosting the demand for elastomers in tubing, syringes, and prosthetics. Pharmaceutical packaging is another significant segment, with elastomers ensuring safe and sterile drug storage. The trend toward minimally invasive procedures is also increasing the need for elastomer-based catheters and seals, reinforcing the importance of regulatory compliance and high-quality standards.

Aging Population and Chronic Disease Prevalence

With a growing aging population, the demand for medical implants and drug delivery systems is rising. Durable and biocompatible elastomers are crucial for prosthetics, artificial joints, pacemakers, and biomedical devices. Chronic diseases such as diabetes, cardiovascular conditions, and respiratory disorders require advanced drug delivery systems, including prefilled syringes and transdermal patches.

Wearable medical devices are gaining popularity, requiring flexible and comfortable elastomers for patient convenience. Advancements in biodegradable elastomers are addressing environmental concerns while ensuring patient safety. Government healthcare initiatives and regulatory approvals are further driving innovation in the sector.

Challenges in Biocompatibility

While medical elastomers offer numerous benefits, some materials present biocompatibility challenges. Certain synthetic elastomers, such as nitrile rubber and latex, may cause allergic reactions or toxicity concerns. Additionally, some elastomers release residual chemicals or degrade over time, potentially harming living tissues.

Regulatory bodies like the FDA and EMA enforce strict biocompatibility testing to ensure patient safety. Manufacturers are shifting towards silicone-based and thermoplastic elastomers, which offer superior biocompatibility and minimal toxicity. Research in bio-based elastomers and advanced polymer engineering is ongoing to overcome these challenges and enhance safety standards.

Increasing Demand for Advanced Medical Devices

The rising prevalence of chronic diseases, an aging population, and technological advancements in the healthcare sector are fueling the demand for high-performance medical elastomers. With a growing preference for minimally invasive procedures, elastomers play a crucial role in creating flexible, durable, and sterilizable medical components.

The increasing use of wearable healthcare devices, particularly for real-time health monitoring and home healthcare, is driving market growth. Additionally, 3D printing technology is revolutionizing the production of customized implants and prosthetics using elastomeric materials. Regulatory bodies are focusing on developing safe, hypoallergenic, and non-toxic elastomers to meet the evolving needs of the medical industry.

Advancements in 3D Printing Technology

The integration of 3D printing is expanding the applications of medical elastomers in prosthetics and implant manufacturing. This technology enables the customization of medical devices, improving patient comfort and treatment outcomes. Medical-grade silicones and thermoplastic polyurethanes (TPUs) are widely used in 3D-printed implants, orthopedic supports, and prosthetics due to their flexibility, strength, and biocompatibility.

3D printing allows for efficient mass production and cost-effective solutions in the healthcare industry. Soft tissue prosthetics, tissue engineering, and regenerative medicine are also benefiting from 3D-printed elastomeric scaffolds. Additionally, the development of biodegradable elastomers is reducing environmental impact, further driving industry advancements.

Industry Expert Insights

Lori Ryerkerk, CEO of Celanese Corporation, highlighted the significance of innovation in medical elastomers, stating, "We are excited to welcome the M&M team to Celanese. With the addition of M&M’s industry-renowned brands and product portfolios, we have established Celanese as the preeminent global specialty materials company."

Segment Analysis

Types of Medical Elastomers

The medical elastomers market is categorized into thermoplastic elastomers (TPEs) and synthetic elastomers. TPEs, including styrene block copolymers, thermoplastic polyurethanes (TPUs), and thermoplastic vulcanizates, are widely used in medical tubing, drug delivery systems, and wearable medical devices. Synthetic elastomers such as silicone rubber, nitrile rubber (NBR), and EPDM are preferred for implants, prosthetics, and surgical devices due to their biocompatibility and durability.

Growing interest in biodegradable and environmentally friendly elastomers is shaping future market trends. Safety, performance, and sustainability remain critical factors in material selection for medical applications.

Read Full Research Report https://www.metatechinsights.com/industry-insights/medical-elastomers-market-2153

Applications in the Healthcare Industry

Medical elastomers are used in various applications, including medical tubing, syringes, stoppers, implants, prosthetics, gloves, drug delivery systems, wound care products, and medical wearables. Medical tubing holds a significant market share due to its widespread use in IV lines, catheters, and respiratory devices.

The demand for medical gloves has increased, particularly in hospitals and laboratory settings. Elastomer-based drug packaging solutions ensure safety, efficiency, and contamination prevention. Wearable medical technology is gaining traction, driven by advancements in biocompatible elastomers and healthcare innovations.

Regional Analysis

North America: Leading Market with Strong Healthcare Infrastructure

North America dominates the medical elastomers market due to its well-established healthcare industry, advanced medical device manufacturing, and high R&D investments. The increasing elderly population and prevalence of chronic diseases in the United States contribute to the demand for high-quality elastomer-based products.

Regulatory standards ensure safety and innovation, while 3D printing technology and biodegradable elastomers continue to drive market growth. Government initiatives and healthcare investments further support medical elastomer advancements in the region.

Asia-Pacific: Fastest-Growing Market

The Asia-Pacific region is experiencing rapid market growth due to improvements in healthcare facilities, increased medical device manufacturing, and rising healthcare expenditures. Countries like China, India, and Japan are witnessing higher demand for medical tubing, implants, and wearables, driven by aging populations and chronic disease prevalence.

Government policies promoting domestic medical equipment production and increased foreign direct investment (FDI) are further propelling market expansion. Advancements in healthcare technologies and the presence of key medical polymer manufacturers contribute to the region's strong growth trajectory.

Competitive Landscape

The medical elastomers market is highly competitive, with key players focusing on innovation, new product development, and strategic partnerships. Leading companies include Dow Inc., DuPont, BASF SE, Trelleborg AB, Teknor Apex, Kraton Corporation, and Celanese Corporation.

Mergers, acquisitions, and collaborations with medical device manufacturers are common strategies to expand product portfolios. The growing demand for eco-friendly elastomers has intensified competition, with companies investing in 3D printing solutions for elastomer-based medical implants and prosthetics.

Buy Now https://www.metatechinsights.com/checkout/2153

Recent Developments

BASF introduced a new line of medical elastomers in September 2024, specifically designed for implantable medical devices, enhancing biocompatibility and durability. Arkema began manufacturing "Pebax" elastomers in February 2024 at its Serquigny plant in France, expanding its applications to medical devices. Mearthane Products Corporation acquired Precision Elastomeric Inc. in January 2023, strengthening its capabilities in customized polyurethane and silicone materials for medical devices.

The medical elastomers market is poised for continued growth, driven by technological advancements, increasing healthcare demands, and evolving regulatory standards.

0 notes

Text

Vocal Biomarker Market: Analyzing the Role of Speech Analysis in Mental Health Diagnosis and Care

In recent years, technological advancements in artificial intelligence, machine learning, and voice recognition have paved the way for an emerging sector in healthcare: the vocal biomarker market. Vocal biomarkers refer to distinct vocal characteristics that can indicate an individual’s health status. By analyzing voice patterns, tone, pitch, and other auditory features, researchers and healthcare professionals can detect and monitor various medical conditions ranging from neurological disorders to cardiovascular diseases. This blog post explores the growing vocal biomarker market, its applications, key players, challenges, and future potential.

The Growing Demand for Vocal Biomarkers

The demand for non-invasive, cost-effective, and efficient diagnostic tools is driving the growth of the vocal biomarker market. Traditional diagnostic methods often involve expensive imaging techniques, blood tests, or invasive procedures. Vocal biomarkers offer a promising alternative by allowing real-time analysis of an individual’s health using voice recordings, potentially reducing healthcare costs and improving early disease detection.

Several factors contribute to the rise of vocal biomarkers:

Advancements in AI and Machine Learning – The integration of AI-driven algorithms has significantly enhanced the accuracy of voice-based diagnostics, enabling the detection of minute changes in vocal patterns associated with diseases.

Remote Healthcare Solutions – The increasing adoption of telehealth and remote patient monitoring systems has fueled the need for innovative diagnostic tools that can be used without physical visits to healthcare facilities.

Rising Prevalence of Chronic Diseases – As conditions such as Parkinson’s disease, Alzheimer’s, depression, and cardiovascular disorders become more prevalent, there is a growing need for non-invasive diagnostic and monitoring solutions.

Increased Investment and Research – Governments, research institutions, and private companies are investing heavily in vocal biomarker technology to explore its potential in various fields, including mental health and respiratory conditions.

Applications of Vocal Biomarkers

Vocal biomarkers have applications across multiple domains in healthcare and beyond. Some of the most promising areas include:

Neurological Disorders: Voice analysis can help detect early signs of Parkinson’s disease, Alzheimer’s, and multiple sclerosis by identifying changes in speech patterns, tremors, or cognitive impairment.

Mental Health Assessment: Conditions such as depression, anxiety, and schizophrenia can be detected through variations in voice tone, cadence, and speech tempo.

Respiratory Diseases: Vocal biomarkers can help identify lung diseases such as chronic obstructive pulmonary disease (COPD) and asthma by analyzing breathing patterns and voice quality.

Cardiovascular Health: Researchers are exploring the connection between voice characteristics and heart conditions, such as hypertension and heart failure.

General Health and Wellness Monitoring: Wearable and smartphone-based applications are integrating voice analysis to monitor stress levels, fatigue, and overall well-being.

Key Players in the Market

The vocal biomarker market is still in its early stages, but several companies and research institutions are leading the charge. Some notable players include:

Sonde Health – A pioneer in voice-based health monitoring, Sonde Health is developing tools for mental health and respiratory condition detection.

Beyond Verbal – Focused on emotion and health analytics, Beyond Verbal uses AI to analyze voice patterns and detect various conditions.

Winterlight Labs – Specializing in detecting cognitive impairment and neurological diseases through voice analysis.

MIT’s Lincoln Laboratory – Conducting research into vocal biomarkers for a range of medical conditions, including COVID-19 detection.

IBM Watson Health – Leveraging AI and speech analytics to explore applications in mental health and chronic disease management.

Challenges in the Vocal Biomarker Market

Despite its potential, the vocal biomarker market faces several challenges that must be addressed for widespread adoption:

Regulatory Hurdles: Ensuring compliance with healthcare regulations and obtaining necessary approvals from governing bodies remains a key challenge.

Data Privacy and Security: Voice recordings contain sensitive information, making it crucial to implement robust security measures to protect patient data.

Accuracy and Reliability: While AI-driven voice analysis has shown promise, ensuring consistent accuracy across diverse populations and voice variations is an ongoing concern.

Public Awareness and Acceptance: Many people are still unaware of vocal biomarkers, and widespread adoption requires educational efforts to build trust in the technology.

The Future of Vocal Biomarkers

The future of the vocal biomarker market looks promising, with continued advancements in AI, increased research funding, and growing interest from healthcare providers. As more studies validate the accuracy and reliability of voice-based diagnostics, regulatory approvals and industry adoption are expected to accelerate.

Furthermore, integration with smartphones and wearable devices will enhance accessibility, allowing individuals to monitor their health effortlessly. In addition to healthcare, industries such as insurance, wellness, and customer service may leverage vocal biomarkers to personalize services and improve user experience.

As the market evolves, collaboration between technology companies, healthcare providers, and regulatory agencies will be essential in overcoming challenges and unlocking the full potential of vocal biomarkers. This innovative technology has the potential to revolutionize healthcare by making diagnostics more efficient, accessible, and cost-effective.

With continued progress, vocal biomarkers may soon become a standard tool for early disease detection, mental health assessment, and general wellness monitoring, ushering in a new era of voice-based healthcare solutions.

0 notes

Text

Advancing Slide Staining Technology: Market Growth, Trends, and Key Insights

Market Overview

Slide stainers automate the staining of histology or cytology tissue specimens by diffusing dyes into samples using techniques such as indirect staining, surface adsorption, direct staining, and mordant staining. These automated systems are essential in hematology, cytopathology, and histopathology, as they aid in identifying cells or tissues for microscopic analysis and disease diagnosis.

In microscopic studies, staining highlights biological tissues like muscle fibers, connective tissue, and organelles. It helps in detecting specific compounds in samples, making it an integral part of processes such as gel electrophoresis and flow cytometry. Automated Slide Stainers simplify hematologic smear staining, adjust sample color intensity, and perform multiple staining operations simultaneously, improving efficiency in clinical and research laboratories.

Get Sample Copy @ https://www.meticulousresearch.com/download-sample-report/cp_id=5643

Market Growth Drivers

The demand for slide stainers is increasing due to several factors, including the aging global population, the rising burden of chronic diseases, advancements in slide-staining technology, and the growing need for personalized medicine. Additionally, the increasing focus on automation in diagnostics and research, higher healthcare spending, and expanding cancer drug research further drive market growth. Emerging economies and rising adoption of automated diagnostic systems also present significant opportunities.

However, the high cost of slide stainer systems is a major restraint, and concerns regarding automation and a shortage of skilled professionals pose additional challenges to market expansion.

Impact of the Aging Population and Chronic Diseases

Slide stainers play a crucial role in pathology and histology, aiding in diagnosing and managing chronic diseases that require continuous monitoring. The global aging population is expanding due to improved healthcare, urbanization, and rising income levels, leading to increased survival rates.

According to the United Nations, the number of people aged 65 years or older was 727 million in 2020, representing 9.3% of the global population. By 2050, this figure is projected to reach 1.54 billion (16% of the total population), with one in four people in Europe and North America being 65 years or older. This demographic shift is largely due to declining fertility rates and increased life expectancy. In 2020, the World Health Organization (WHO) reported that, for the first time, the global elderly population exceeded children under five.

With the aging population, cases of age-related chronic diseases such as cardiovascular diseases, cancer, and respiratory conditions are rising. In 2021, the WHO estimated that 41 million deaths worldwide were caused by chronic diseases, accounting for 74% of all global deaths. Cardiovascular diseases led the toll with 17.9 million deaths annually, followed by chronic respiratory diseases (4.1 million) and cancers (9.3 million). According to GLOBOCAN, 19.3 million cancer cases were detected worldwide in 2020, and this figure is expected to rise to 24.6 million by 2032.

Chronic diseases necessitate accurate diagnostic methods, and slide staining is essential in preparing tissue samples for microscopic examination. Staining enhances contrast and cellular structure visibility, enabling the identification of disease markers. Automated slide stainers are increasingly used in laboratories due to their efficiency, speed, and ability to reduce human error while processing high sample volumes.

Growing Demand for Automated Slide Staining and Diagnostic Systems

The rising need for reliable and rapid diagnostics is fueling demand for automated slide staining and diagnostic systems. Personalized medicine, which requires highly specific diagnostic tests, is further driving the adoption of automated systems. These systems support complex staining protocols, making them particularly valuable in cancer diagnosis and treatment.

Automated slide staining devices streamline tissue sample analysis, significantly reducing the time and labor needed for staining procedures. Traditional manual staining methods require technicians to prepare each slide individually, increasing the risk of human error and inefficiencies. Automated systems address these issues by performing the staining process quickly and accurately.

Furthermore, automation enhances the accuracy and consistency of diagnostic results. By implementing standardized protocols and automated processes, these systems minimize variability in staining outcomes, ensuring reliable and reproducible results. The increasing adoption of automated slide staining systems is creating new growth opportunities in the market.

Get Full Report @ https://www.meticulousresearch.com/product/slide-stainers-market-5643

Key Market Segments

Product Analysis

Reagents & Kits: This segment is expected to hold the largest market share in 2025 due to the growing demand for specialized reagents such as special stains, cytology stains, and mounting reagents. The increasing prevalence of cancer and infectious diseases has also contributed to the demand for reagents and kits used in diagnostic tests. Innovations such as multiplex staining reagents, which detect multiple biomarkers on a single slide, are further driving growth.

Equipment: Automated slide stainers dominate this category as laboratories increasingly transition to automation for efficiency and accuracy.

Accessories & Consumables: This segment includes buffers, solvents, and other essential components required for slide staining procedures.

Technique Analysis

Hematoxylin & Eosin (H&E): Expected to hold the largest market share in 2025, this technique is widely used in pathology and histology for tissue structure visualization. The development of advanced H&E staining systems has enhanced efficiency and accessibility, increasing adoption among researchers and healthcare professionals.

Immunohistochemistry (IHC): This technique is used to identify specific proteins in tissues, aiding in cancer diagnostics and research.

In-situ Hybridization (ISH): A crucial technique in molecular pathology, ISH is used for detecting genetic abnormalities and infectious agents.

Cytology & Hematology Staining: These methods are essential for studying blood cells and diagnosing hematologic disorders.

Application Analysis

Disease Diagnosis: Slide staining plays a critical role in diagnosing infectious diseases, cancer, and autoimmune conditions by enhancing tissue sample visualization.

Medical Research: Used in clinical trials and drug development, slide staining enables researchers to analyze tissue samples at the cellular level.

End-User Analysis

Hospitals & Diagnostic Centers: This segment is expected to dominate the market in 2025 due to the widespread use of slide stainers in pathology labs for disease diagnosis and treatment planning.

Pharmaceutical & Biotechnology Companies: These entities use slide staining in drug discovery and clinical research.

Academic & Research Institutes: The growing focus on life sciences research is driving demand for slide-staining equipment in educational institutions.

Contract Research Organizations (CROs): CROs use automated slide stainers for preclinical and clinical studies.

Regional Market Insights

North America

North America holds a significant share of the global slide stainers market due to the presence of major industry players, high healthcare expenditure, and advancements in diagnostic technology. The U.S. leads in market adoption, driven by the strong presence of research institutions and pharmaceutical companies.

Europe

Europe is a key market for slide stainers, with countries like Germany, France, and the U.K. investing in advanced diagnostic solutions. The region benefits from well-established healthcare infrastructure and government support for medical research.

Asia-Pacific

The Asia-Pacific region is the fastest-growing market, driven by the rising prevalence of chronic diseases, increasing R&D investments, and expanding healthcare infrastructure. Countries such as China, India, Japan, and South Korea are experiencing rapid market growth due to the adoption of automation in laboratory diagnostics.

Latin America, Middle East & Africa

These regions are witnessing steady growth due to improving healthcare infrastructure and increasing awareness about automated diagnostic systems. Brazil, Mexico, and South Africa are among the key markets in these regions.

Key Market Players

Leading companies in the slide stainers market include:

Thermo Fisher Scientific (U.S.)

F. Hoffmann-La Roche AG (Switzerland)

Danaher Corporation (U.S.)

Merck KGaA (Germany)

Agilent Technologies, Inc. (U.S.)

Becton, Dickinson and Company (U.S.)

Siemens Healthineers (Germany)

Abcam plc (U.K.)

General Data Company, Inc. (U.S.)

Biocare Medical, LLC (U.S.)

BioGenex (U.S.)

PHC Holdings Corporation (Japan)

Hardy Diagnostics (U.S.)

These companies focus on product innovation, strategic collaborations, and expanding their market presence to strengthen their positions in the industry.

Get Sample Copy @ https://www.meticulousresearch.com/download-sample-report/cp_id=5643

0 notes

Text

Guillain-Barre Syndrome Diagnostics Market To Reach USD 169.9 Million By 2030

Guillain-Barre Syndrome Diagnostics Market Growth & Trends

The global guillain-barre syndrome diagnostics market size is expected to reach USD 169.9 million by 2030, registering a CAGR of 2.8% from 2025 to 2030, according to a new report by Grand View Research, Inc. driven by several key factors. A significant contributor is the increasing incidence of Guillain-Barre syndrome (GBS), particularly in regions with high rates of infectious diseases. Infections such as respiratory or gastrointestinal illnesses often precede GBS, leading to a heightened demand for effective diagnostic tools. For instance, a study from the University of Minnesota in October 2023 highlighted that 67% of GBS cases were preceded by such infections, underscoring the need for timely diagnosis.

Advancements in diagnostic techniques have also played a crucial role in market expansion. Innovations in electromyography (EMG) and nerve conduction studies have enhanced the accuracy and speed of GBS diagnosis. These technological improvements enable healthcare professionals to detect the syndrome earlier, facilitating prompt intervention and better patient outcomes. The integration of advanced diagnostic tools in clinical settings has become increasingly prevalent, reflecting a commitment to improving patient care.

The growing awareness of GBS among healthcare providers and the general population has further propelled the diagnostics market. Educational initiatives and increased information dissemination have led to earlier recognition of symptoms and subsequent diagnostic testing. This heightened awareness ensures that patients receive timely and appropriate care, reducing the risk of severe complications associated with delayed diagnosis. Consequently, the demand for diagnostic services has risen, contributing to market growth.

The expanding geriatric population has influenced the market for GBS diagnostics. Older individuals are more susceptible to infections that can trigger GBS, necessitating effective diagnostic measures. According to the World Health Organization's 2021 forecast, by 2030, one in six individuals worldwide will be over 60, with their numbers expected to grow from 1 billion in 2020 to 2.1 billion by 2050. This demographic shift underscores the importance of accessible and accurate diagnostic tools to manage the anticipated increase in GBS cases among the elderly.

Key players in the market are implementing strategic initiatives such as geographical expansion, collaborations, partnerships, and joint ventures to strengthen their market presence.

Request a free sample copy or view report summary: https://www.grandviewresearch.com/industry-analysis/guillain-barre-syndrome-diagnostics-market-report

Guillain-Barre Syndrome Diagnostics Market Report Highlights

The test segment of the market includes lumbar puncture, electromyography, nerve conduction studies, and others. The lumbar puncture segment led the market in 2024, accounting for the largest revenue share of 45.1%, and is expected to experience the fastest compound annual growth rate (CAGR) of 3.0% during the forecast period, driven by its essential role in confirming GBS diagnosis.

The end-use segment comprises hospitals & clinics, and diagnostic laboratories. In 2024, the hospitals & clinics segment led the market, capturing a revenue share of 63.0%, driving significant growth through the integration of advanced diagnostic tools and improved patient management protocols.

Asia Pacific dominated the global market with a revenue share of 41.8% in 2024. Factors such as rising awareness, improving healthcare infrastructure, and increasing diagnostic rates are driving market expansion.

Guillain-Barre Syndrome Diagnostics Market Segmentation

Grand View Research has segmented the global GBS diagnostics market based on the test, end-use, and region:

GBS Diagnostics Test Outlook (Revenue, USD Million, 2018 - 2030)

Lumbar Puncture

Nerve Conduction

Electromyography

Other

GBS Diagnostics End-use Outlook (Revenue, USD Million, 2018 - 2030)

Hospitals and Clinics

Diagnostic Laboratories

Others

GBS Diagnostics Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

U.S.

Canada

Mexico

Europe

UK

Germany

France

Italy

Spain

Denmark

Sweden

Norway

Asia Pacific

Japan

China

India

Australia

South Korea

Thailand

Latin America

Brazil

Argentina

Middle East & Africa

South Africa

Saudi Arabia

UAE

Kuwait

List of Key Players in the GBS Diagnostics Market

Cadwell Industries, Inc

Natus Medical Incorporated

Nihon Kohden Corporation

Medtronic plc

Bionen Medical Devices

Deymed Diagnostic

Neurosoft

Alpine Biomed

EMS Biomedical

Rochester Electro-Medical, Inc.

Browse Full Report: https://www.grandviewresearch.com/industry-analysis/guillain-barre-syndrome-diagnostics-market-report

#Guillain-Barre Syndrome Diagnostics Market#Guillain-Barre Syndrome Diagnostics Market Size#Guillain-Barre Syndrome Diagnostics Market Share

0 notes

Link

0 notes

Text

Legionella Testing Market Size, Share & Trends 2024-2032

The Legionella Testing Market was valued at USD 296.23 million in 2023 and is projected to reach USD 516.85 million by 2031, growing at a CAGR of 7.1% over the forecast period.

Legionella bacteria pose significant health risks, particularly in water systems, leading to severe respiratory illnesses such as Legionnaires' disease. The rising global concern about waterborne diseases, combined with stringent government regulations mandating routine testing in commercial, industrial, and residential settings, continues to propel the demand for Legionella testing solutions. The growing awareness around maintaining water safety in healthcare facilities, hotels, and cooling towers also contributes to market expansion.

Get Free Sample Report @ https://www.snsinsider.com/sample-request/3423

Market Segmentation

By Test Type

Culture Media

Urinary Antigen Test

Direct Fluorescent Antibody Test

Polymerase Chain Reaction (PCR)

Others

By Application

Clinical Testing

Environmental Testing

By End-User

Hospitals & Clinics

Diagnostic Laboratories

Water Treatment Industries

Others

Regional Analysis

North America dominates the market, driven by strict regulatory frameworks, high awareness levels, and a well-established healthcare infrastructure. The U.S. and Canada hold the majority share due to mandatory Legionella testing policies.

Europe follows closely, especially in countries like the UK, Germany, and France, where public health agencies actively monitor water quality.

Asia-Pacific is expected to witness the fastest growth, fueled by urbanization, increased healthcare spending, and growing adoption of water safety regulations in countries such as China, India, and Japan.

Latin America, Middle East & Africa are emerging markets, gradually showing steady adoption due to increasing public health initiatives and infrastructure development.

Key Players

Some major players in Legionella Testing Market are Aquacert Ltd, Quidel Corporation, Merck KGaA, Thermo Fisher Scientific Inc., bioMérieux, Eurofins Scientific, Abbott, Bio-Rad Laboratories, Inc., BD, IDEXX Corporation and other players.

Key Market Points

Rising prevalence of Legionnaires' disease globally.

Increasing regulatory mandates for routine water system monitoring.

Technological advancements in PCR and rapid antigen detection methods.

Growing healthcare infrastructure investments, especially in developing nations.

Expanding application scope beyond healthcare to hospitality, industrial, and municipal sectors.

Future Scope

The Legionella Testing Market is poised for robust growth in the coming years, driven by technological innovations like real-time PCR and automated testing solutions that offer higher accuracy and faster results. The increasing focus on preventive healthcare, combined with smart water management systems, is expected to open new avenues for market players. Emerging economies with improving healthcare standards and heightened environmental awareness will present lucrative opportunities. Moreover, strategic collaborations, mergers, and product launches tailored to meet regional regulatory standards are likely to shape the market dynamics further.

Conclusion

With water safety becoming an ever-critical public health priority, the Legionella Testing Market is set to experience sustained growth. Regulatory compliance, technological advancements, and heightened health awareness will continue to drive demand, positioning the market for significant expansion globally over the forecast period.

Contact Us: Jagney Dave - Vice President of Client Engagement Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

Other Related Reports:

Fertility Services Market

Medical Power Supply Market

Post Traumatic Stress Disorder Treatment Market

MRI Guided Neurosurgical Ablation Market

#Legionella Testing Market#Legionella Testing Market Share#Legionella Testing Market Trends#Legionella Testing Market Size#Legionella Testing Market Growth

0 notes

Text

The Bird Flu: A Modern-Day Plague

The apathy of plagues disintegrates as it reaches groups of people. Over time plagues have been known to wound, damage, and even kill populations. Historical prophets like Moses told people to fight the plague by dipping hyssop in animal blood and smearing blood on the two doorposts and with the blood in the basin to protect the firstborn from dying. Protection from death has come a long way. In 2025, pap smears will endure the efficacy versus effectiveness of vaccines for anyone willing to take them. Since 2003-2024 the WHO reported 954 cases of the human H5N1 virus. In America, there were 70 cases with one death. Egypt had 359 cases and 120 deaths. Indonesia has had the most with a total of 200 cases and 168 deaths.H5N1, Avian Flu has infected some individuals killing half the number of people infected.

These deaths in other countries due to the bird flu were not mentioned to American society during the time as the news outlets in America projected neoliberalism towards foreign countries. Corporate advertisements that contain subplots are often made into what major news outlets believe are successful stories. The devastating effects of death can last for many years. The news of these deaths in other countries was not shared properly because of the potential to go against free markets.

Currently, the bird flu has not yet reached its full plausible future to become highly contagious spreading from person to person. The bird flu virus, H5N1, is covered in hemagglutinin which clots the blood from the virus to attach to other cells. Also, neuraminidases cleave cells for entrance into the host cell. The bird flu is only lethal to a limited quantity of people not because of technical advancements but due to the virus being in a novel primordial state. Vaccines exist but are not available to the public. The vaccine named MF59-H5N1 is one of the most successful vaccines. Recently treatments have been tested using CD4+ T cells, induced by vaccination with clade 1 H5N1 A/Vietnam/1194/2004, which positively reacted with the H5 of different clades. The scientist then compared the T cell response to in vitro stimulation with pools of peptides spanning in different regions including H5 A/Vietnam/1194/2004(clade 1), A/Indonesia/5/05 (clade 2.1) and A/duck/Singapore/97 (clade0-like). The immunization produced high frequencies of antigen-specific CD4+ T cells that increased when applied to booster immunization between the 3 strains tested. Using the Wilcoxon test to find the mean frequency for cytokines CD4+lymphocytes after the vitro stimulation was good for finding the mean value of each strain of the virus. There is speculation that a vaccine intended for animals may be better for the public than for humans.

The first case of the bird flu was in 1996 and came from a goose in a Hong Kong market in Guangdong Province, China. The CDC, Centers for Disease Control Prevention, states that some of the severe symptoms of the bird flu in humans include high fever, difficulty breathing, altered consciousness, and seizures. The bird flu is a spherical influenza virus that is also respiratory. Lawrence Brody, Ph.D. from the National Human Genome Research Institute explains the lack of DNA in the Influenza makes way for RNA's ability to degrade easily due to the uracil. RNA inside the genome allows the cell to change which genes are being expressed. The RNA also contains a sugar ribose which has a hydroxyl group that is polar and forms hydrogen bonds with water resulting in better solubility for the functional group of ribose. When the virus mutates then it will become more transmissible to humans.

As of now in America, the disease is not highly transmissible from person to person. The HPAI A (H5N1) clade 2.3.4.4b viruses were identified in dairy cows and unpasteurized milk samples in the United States in 2021. The CDC, Center for Control Disease Prevention, analysis of the genetic sequence of the virus had a genetic mutation in its PB2 protein that has previously been associated with more efficient virus replication in people and other mammals (i.e., change of PB2 E627K).” This polymerase within the virus would cause concern because then the RNA within the bird flu would be able to form inside an unfamiliar host. Nevertheless, when the bird flu has a surge, there is a disturbance.

Egg prices are soaring through the stratosphere due to the bird flu causing large amounts of bird deaths at pastors! These prices are staggering, as reported by the United States Department of Agriculture, the average price is $8.03 per dozen. This is an increase from the average price of eggs used to be $3.00 per dozen eggs. As the bird flu is getting stronger a docile hysteria persists, reckoning that humans consume birds for nutrients. Consuming the bird is an understatement. According to data compiled in 2016 by the UN Food and Agriculture Organization, chicken is the most common meat consumed, with a population of over 22.7 billion. The number of chickens slaughtered per year is greater than livestock such as pigs and cattle. Moreover, the skeletal structures and DNA of the chickens in modern broilers have altered the reality we face today. This essential slaughter affects how diseases spread equating to empathy shared in some countries.

0 notes

Text

Asia Pacific Point of Care Diagnostics Industry: Market Dynamics & Key Insights

The Asia Pacific point of care diagnostics market is expected to reach USD 16.73 billion by 2030, registering a CAGR of 8.4% from 2024 to 2030, according to a new study by Grand View Research, Inc. Growing base of geriatric population and the ability to render immediate results and improve patient care coupled with a rising market penetration of PACS (picture archiving and communication systems) and EMR (electronic medical records) are expected to drive demand over the next six years.

Skilled staff shortages, especially pertaining to the field of diagnostics are also expected to accelerate the market penetration rates of point of care (PoC) products, by expediting lab automation processes. Rising demand for home healthcare and other healthcare establishments catering to the elderly population and initiatives undertaken by governments to shorten hospital stays by establishing out-patient care models are also expected to be key market factors.

The rapidly growing use of point of care diagnostic products has introduced a decentralization trend in the overall healthcare industry. Healthcare facilities and patients, in an attempt to attain or cater medical facilities remotely, encourage early diagnosis and curb costs are now decentralizing their facilities. Furthermore, these trends have also triggered the establishment of remote and stand-alone diagnostic facilities.

Asia Pacific Point Of Care Diagnostics Market Report Highlights

The infectious diseases segment dominated the market with the highest revenue share in 2023 owing to the increasing adoption of point of care diagnostics as a substitute for traditional laboratory testing in infectious diseases applications.

The cancer markers segment is expected to grow at the fastest CAGR over the forecast period from 2024 to 2030. The Asia Pacific region has experienced a notable rise in the prevalence of cancer in recent years.

Glucose testing dominated the market accounting for around 20% of the revenue share in 2023 owing to the high prevalence of diabetes in Asian countries.

The clinics segment held the largest revenue share in 2023. Clinics are essential in providing healthcare services, particularly in remote and underserved areas.

China dominated the Asia Pacific point of care diagnostics market with a revenue share of over 41.5% in 2023. China has the world's largest population and faces notable challenges related to the prevalence of chronic and infectious diseases within its borders resulting in an increasing demand for point-of-care diagnostics.

Detail Analysis of Asia Pacific Point Of Care Diagnostics Market @ https://www.grandviewresearch.com/industry-analysis/asia-pacific-poc-diagnostics-market/request/rs1

Asia Pacific Point Of Care Diagnostics Market Segmentation

Grand View Research has segmented the Asia Pacific point of care diagnostics market report on the basis of product, end-use, and region:

Asia Pacific Point Of Care Diagnostics Product Outlook (Revenue, USD Million, 2018 - 2030)

Glucose Testing

Hb1Ac Testing

Coagulation

Fertility/Pregnancy

Infectious Disease

HIV POC

Clostridium Difficile POC

HBV POC

Pneumonia or Streptococcus Associated Infections

Respiratory Syncytial Virus (RSV) POC

HPV POC

Influenza/Flu POC

HCV POC

MRSA POC

TB and Drug-resistant TB POC

HSV POC

COVID-19

Other Infectious Diseases

Cardiac Markers

Thyroid Stimulating Hormone

Hematology

Primary Care Systems

Decentralized Clinical Chemistry

Feces

Lipid Testing

Cancer Marker

Blood Gas/Electrolytes

Ambulatory Chemistry

Drug Abuse Testing

Autoimmune Disease

Urinalysis/Nephrology

Asia Pacific Point Of Care Diagnostics End Use Outlook (Revenue, USD Million, 2018 - 2030)

Clinics

Physician Office