#Polymer Coated Fabrics Market share

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr is used by 21% of adults online aged 18-29 years.

Text

Thermal Spray Coatings Market

Thermal Spray Coatings Market Size, Share, Trends: Oerlikon Metco Leads

Rising adoption of thermal spray coatings in additive manufacturing and 3D printing applications

Market Overview:

The global Thermal Spray Coatings market is projected to grow at a CAGR of 6.8% from 2024 to 2031. The market value is expected to increase significantly during this period. North America currently dominates the market, accounting for the largest share of global revenue. Key metrics include increasing adoption in aerospace and automotive industries, growing demand for advanced surface engineering solutions, and rising investments in research and development.

The Thermal Spray Coatings market is expanding rapidly, owing to rising demand for wear- and corrosion-resistant coatings across a wide range of end-use industries. Technological improvements in coating materials and application techniques are driving market growth, with an emphasis on enhancing coating performance and efficiency.

DOWNLOAD FREE SAMPLE

Market Trends:

The use of thermal spray coatings in additive manufacturing and 3D printing methods is gaining popularity. This trend is being pushed by the potential of thermal spray coatings to improve the surface characteristics and functioning of 3D printed components. Aerospace, automotive, and healthcare industries use this combination to build complicated parts with exceptional wear resistance, thermal insulation, and corrosion protection. The combination of thermal spray coatings and additive manufacturing enables the fabrication of lightweight, high-performance components with customisable surface qualities, opening up new avenues for product design and customisation. This trend is predicted to continue as manufacturers seek novel ways to increase product performance while lowering manufacturing costs.

Market Segmentation:

The Combustion process segment, which comprises flame spray and High Velocity Oxy-Fuel (HVOF) approaches, dominates the Thermal Spray Coatings market. This supremacy is due to the adaptability, cost-effectiveness, and broad variety of applications provided by combustion-based thermal spray techniques. Flame spray, one of the oldest and most known processes, remains popular due to its simplicity and capacity to deposit a wide range of materials, including metals, ceramics, and polymers.

High Velocity Oxy-Fuel (HVOF) spraying, a more advanced combustion method, has gained popularity in recent years. HVOF coatings are well-known for their high density, bond strength, and wear resistance, making them suitable for use in the aerospace, automotive, and oil and gas industries. A recent study by the National Aeronautics and Space Administration (NASA) discovered that HVOF-sprayed tungsten carbide-cobalt coatings on turbine engine components can increase their service life by up to 300% when compared to untreated parts.

Market Key Players:

Oerlikon Metco

Praxair Surface Technologies

H.C. Starck

Hoganas AB

Kennametal Stellite

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

Construction Films Market

Construction Films Market Size, Share, Trends: Berry Global Inc. Leads

Increasing Demand for Energy-Efficient Buildings Driving Market Growth

Market Overview:

The global construction films market is projected to grow at a CAGR of X.X% during the forecast period of 2024-2031, reaching a market size of USD YY billion by 2031 from USD XX billion in 2024. The Asia-Pacific region is expected to dominate the market, driven by rapid urbanization, increasing construction activities, and growing investments in infrastructure development. The growth of the construction films market is fueled by factors such as the rising demand for energy-efficient and sustainable buildings, increasing adoption of advanced construction techniques, and growing awareness about the benefits of construction films. However, the fluctuating prices of raw materials may restrain the market growth to some extent.

The increased demand for energy-efficient buildings is a major trend driving the construction films industry. Construction films, particularly reflecting and insulating coatings, serve an important role in decreasing heat transfer, improving thermal insulation, and increasing building energy efficiency. According to the International Energy Agency, the building and construction sector consumes roughly 40% of world energy and emits CO2. As a result, governments and building owners are increasingly using energy-efficient construction materials and technologies, such as construction films, to lower their energy usage and carbon impact.

DOWNLOAD FREE SAMPLE

Market Trends:

The rising use of innovative construction techniques, such as modular construction and prefabrication, is a major driver of the construction films industry. These procedures involve fabricating construction components off-site and then assembling them on-site. Construction films are widely employed in these operations for a variety of applications, including moisture protection, vapour barriers, and temporary weather protection. The increased popularity of modular construction, which offers benefits such as faster project completion, decreased waste, and enhanced quality control, is likely to increase demand for construction films in the future years.

Despite the favourable outlook, fluctuating raw material prices, particularly polymers such as polyethylene and polypropylene, may impede the growth of the construction films market. These raw material prices are impacted by a number of factors, including crude oil prices, supply-demand dynamics, and geopolitical events. Volatile raw material costs can have an impact on construction film makers' profit margins and cause pricing swings in end-use industries. However, the discovery of alternative raw materials and the implementation of efficient manufacturing techniques are projected to reduce the impact of raw material price changes to some extent.

Market Segmentation:

The linear low-density polyethylene (LLDPE) segment is likely to dominate the construction films market during the forecast period. LLDPE films are commonly used in construction due to their good moisture resistance, high tensile strength, and flexibility. They are utilised for a variety of applications, including vapour barriers, underlayment, and temporary protective covers. This segment's expansion is being driven by rising demand for LLDPE films in residential and commercial construction projects, particularly in emerging markets.

Major construction film makers, like Berry Global Inc. and Dow Inc., are investing in the development and manufacturing of high-performance LLDPE films to meet the changing needs of the construction industry. For example, in 2023, Berry Global introduced a new line of sustainable LLDPE building films produced from post-consumer recycled materials that provide increased performance and durability.

Market Key Players:

Berry Global Inc.

Dow Inc.

Saint-Gobain

Toray Industries, Inc.

Mitsubishi Chemical Corporation

Kuraray Co., Ltd.

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

Electroactive Polymers Market — By Type , By Application , By Geography — Global Opportunity Analysis & Industry Forecast, 2024–2030

Electroactive Polymers Market Overview

Request Sample :

Electroactive Polymers Market COVID-19 Pandemic

The outbreak of Covid-19 is having a huge impact on the economy of electronic devices. The COVID-19 pandemic caused an unprecedented increased demand for some medical devices, as well as significant disruptions in the manufacturing and supply chain operations of global medical devices. The FDA monitors the supply chain of medical products and works closely with producers and other stakeholders to assess the risk of disruption and to prevent or reduce its impact on patients, health care providers, and the general public’s health. In addition, there is a delay in imports and exports of medical devices due to the import-export restriction by the governments in various regions. All these factors are having a major impact on the Electroactive Polymers Market during the pandemic.

Report Coverage

The report: “Electroactive Polymers Market — Forecast (2024–2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the electroactive polymers Industry.

By Type: Ionic Electroactive Polymers (Ionic Polymer Gels (IPG), Ionic Polymer Metal Composites (IPMC), Conductive Polymers (CP), and Carbon Nanotubes (CNT)), Electronic Electroactive Polymers (Ferroelectric Polymers, Electrostrictive Graft Elastomers, Dielectric Elastomers, Electro VIscoelastic Elastomers, Liquid Crystal Elastomer (LCE), and Others), and Others.

By Application: Actuators, Sensors, Plastic, Aviation Technology, Energy Generation, Automotive Devices, Prosthetics, Robotics, and Others.

By Geography: North America (U.S., Canada, and Mexico), Europe (U.K, Germany, France, Italy, Netherland, Spain, Russia, Belgium, and Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia and New Zealand, Indonesia, Taiwan, Malaysia, and Rest of APAC), South America (Brazil, Argentina, Colombia, Chile, and Rest of South America), Rest of the World (Middle East, and Africa).

Inquiry Before Buying :

Key Takeaways

Asia-Pacific dominates the Electroactive Polymers Market owing to the increasing demand for the electroactive polymers industry in the region. The increasing urbanization coupled with the rising population in APAC is the major factor driving the demand for electroactive polymers.

Electroactive polymers are extensively used for corrosion-preventing coatings in ferrous and non-ferrous alloys, actuators, damped harmonic oscillator, metamorphic biomaterials, and protective fabrics points. These properties of electroactive polymers are projected to increase market growth.

Electroactive polymers due to its unique properties find application in different end-use industries. These are lighter in weight, more durable, and have better conductive properties, unlike conventional materials (metals). During the forecast period, this factor is anticipated to drive the market.

Due to the Covid-19 pandemic, most of the countries have gone under lockdown, due to which the projects and operations of various industries such as energy generation and automotive are disruptively stopped, which is hampering the Electroactive Polymers Market growth.

Electroactive Polymers Market Segment Analysis — By Type

The conductive polymers segment held the largest share in the Electroactive Polymers Market in 2020 and is growing at a CAGR 8.10% over 2024–2030. The significant class of functional materials that have certain useful properties of both organic polymers (such as strength, plasticity, flexibility, strength, elasticity) and semiconductors (such as electric conductivity) are conducting polymers (CPs). The conductive polymers are often used in miniature boxes that have the ability to open and close, micro-robots, surgical tools, surgical robots that assemble other micro-devices. In addition, conductive polymers (CPs) are extensively used as an alternative to metallic interfaces within biomedical devices as a way of imparting electroactivity to normally passive devices such as tissue scaffolds. Thus, all these extensive characteristics of conductive polymers are the key factor anticipated to boost the demand for conductive polymers in various regions during the forecast period.

Schedule A Call :

Electroactive Polymers Market Segment Analysis — By Application

The actuator segment held the largest share in the Electroactive Polymers Market in 2020 and is expected to grow with a CAGR of 7.2% for forecast period. To maximize the actuation capability and durability, effective fabrication, shaping, and electrode techniques are being developed. Many engineers and scientists from many different disciplines are attracting attention with the impressive advances in improving their actuation strain. Due to their inherent piezoelectric effect, ferroelectric polymers, such as polyvinylidene fluoride (PVDF), are largely used in manufacturing electromechanical actuators. For biomimetic applications, these materials are especially attractive, as they can be used to make intelligent robots and other biologically inspired mechanisms. To form part of mass-produced products, many EAP actuators are still emerging and need further advancements. This requires the use of models of computational chemistry, comprehensive science of materials, electro-mechanical analytical tools, and research into material processing. Which will eventually drive is the Electroactive Polymers Market during the forecast period.

Electroactive Polymers Market Segment Analysis — By Geography

Asia-Pacific region held the largest share in the Electroactive Polymers Market in 2020 up to 38%, owing to the escalating medical device industry in the region. A key factor behind the growth of the region’s electroactive polymer market is the large demand for electroactive polymers for the manufacture of advanced implant devices for medical conditions. According to Invest India, the Indian medical device sector is projected to register a CAGR of 14.8% and is expected to reach $11.9 billion in 2021–22, and the sector is projected to reach $ 65 bn industry by 2024. According to the most recent official figures from the Ministry of Health, Labour and Welfare (MHLW), the Japanese medical devices market in 2018 was roughly $29.3 billion, up about 6.9 percent from 2017 in yen terms. And from 2018 to 2023, the medical device market in Japan is estimated to show an increment of 4.5% CAGR in yen terms. Furthermore, North America also holds a prominent market share of the Electroactive Polymers Market due to the escalating medical device industry. According to the Select USA, the United States medical device market is anticipated to rise to $208 billion by the year 2023. Thus, with the expanding medical device industry, the demand for electroactive polymers will also subsequently increase, which is anticipated to drive the Electroactive Polymers Market in the Asia Pacific and North America during the forecast period.

Electroactive Polymers Market Drivers

Increasing Automotive Production

In the automotive industry, electroactive polymers are used as actuators and sensors. For materials that are light in weight but strong and durable such as an electroactive polymer, there is high demand. By using modern electroactive polymers in numerous automotive electronic components, such as multiple sensors, accelerometers, and accelerator pedal modules, car manufacturers are attempting to achieve lightweight properties. China is the world’s largest vehicle market, according to the International Trade Administration (ITA), and the Chinese government expects the production of cars to reach 35 million by 2025. According to the International Trade Administration (ITA), in 2019 the Mexican market for electric, plug-in vehicles, and hybrid vehicles reached 25,608 units, representing a 43.8% growth over 2018. Thus, increasing automation production will require more electroactive polymers for manufacturing various automotive components, which will act as a driver for the Electroactive Polymers Market during the forecast period.

Increasing Application of Electroactive Polymers

Textiles called sensing and actuating microfibers can be directly woven into electromechanical systems such as sensors, actuators, electronics, and power sources. They can be used as smart fabrics because of the flexibility and low cost of electroactive polymers. In developing intelligent fabrics, polypyrrole and polyaniline are used. In addition, using electroactive polymers in robotics for muscle development is better, as it is more cost-effective than the semiconductor and metal materials. And robotics is widely used; hence the demand for electroactive polymers will also positively affect the market growth. Furthermore, Electroactive Polymers Market growth is increasing owing to its wide usage in areas such as medical devices, damped harmonic oscillator, electric displacement field, electrostatic discharge/electromagnetic interference, high-strain sensors, and biomimetic. Hence, the increasing application of electroactive polymers acts as a driver for the Electroactive Polymers Market.

Buy Now :

Electroactive Polymers Market Challenges

Environmental Hazards Related to the Electroactive Polymers

Raw materials which are used to produce electroactive polymers (EAPs) are difficult to extract and often harmful to the environment. The disposal of waste generated by electroactive polymers is one of the major concerns (EAPs). Improper disposal of EAP products could harm the environment and ultimately impact the food chain. Manufacturers of EAPs may experience increased costs associated with the disposal of certain electroactive polymers (EAPs) that cannot be disposed of by biodegradation. The government has, therefore, enforced strict regulations on the use of such polymers. Besides, the environmental regulations on the use of petroleum products restrict the growth of the EAPs market. These factors are hampering the electroactive polymer market growth.

Electroactive Polymers Market Landscape

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the Electroactive Polymers Market. Major players in the Electroactive Polymers Market are Solvay, Parker Hannifin, Agfa-Gevaert, 3M, Merck, Lubrizol, Novasentis, Premix, PolyOne Corporation, Celanese Corporation, and KEMET Corporation.

Key Market Players:

The Top 5 companies in the Electroactive Polymers Market are:

Merck

3M

Solvay

Parker Hannifin

Agfa-Gevaert

For more Chemicals and Materials Market reports, Please click here

#ElectroactivePolymers#SmartMaterials#ConductivePolymers#FlexibleElectronics#ShapeMemoryAlloys#PolymersInElectronics#SoftRobotics

0 notes

Text

Textile Chemicals Industry Outlook, Research, Trends and Forecast to 2030

The global textile chemicals market was valued at USD 26.44 billion in 2023 and is projected to expand at a compound annual growth rate (CAGR) of 4.5% from 2024 to 2030. This growth is primarily driven by the rising demand in the clothing and apparel sector, which is boosted by a growing global population, urbanization, and higher disposable incomes. Textile chemicals are essential across various stages of fabric production, from pre-treatment and dyeing to finishing, as they enhance the quality, appearance, and functionality of textiles.

The rapid development of new textile manufacturing techniques, such as digital printing, nanotechnology, and smart clothing, has increased the need for specialized chemicals that improve fabric durability, comfort, and additional features like water repellency or UV protection. Additionally, countries like China, India, and Bangladesh have emerged as major textile manufacturing hubs. These nations benefit from lower labor costs and government support aimed at promoting textile production. For instance, in February 2024, the Government of India increased its budget allocation for the textile sector to over INR 1000 crore, with INR 600 crore specifically allocated to support the Cotton Corporation of India. This kind of governmental support is expected to further boost textile chemical demand by driving increased production in these regions.

Gather more insights about the market drivers, restrains and growth of the Textile Chemicals Market

Regional Insights:

North America North America’s advanced textile manufacturing industry is characterized by high quality standards and a demand for technical textiles, especially in sectors like automotive, aerospace, and healthcare. This requires specialized textile chemicals to enhance properties like durability, flame resistance, and antimicrobial features.

In the U.S., the textile chemicals market is strong, driven by a diversified textile sector producing apparel, home furnishings, and technical textiles. Chemicals play a crucial role in enhancing aesthetics, performance, and durability through processes like dyeing, finishing, and coating.

Asia Pacific Asia Pacific held a 57.52% market share in 2023, fueled by extensive textile production in countries like China, India, and Vietnam, benefiting from low production costs and abundant resources. China, the largest global textile producer, uses extensive chemicals for dyeing, finishing, and meeting international standards.

Europe Europe’s textile chemicals market benefits from its long-standing textile industry and focus on innovation. Germany leads in R&D for sustainable textile chemicals, while Turkey’s growing textile production drives demand for chemicals across the value chain, from fiber to finished garments.

Central & South America In Central and South America, textile manufacturing, especially in Brazil, Mexico, and Colombia, is expanding, with a growing need for chemicals in processes like dyeing and finishing. Brazil, in particular, is modernizing its textile facilities and adopting advanced chemicals for better product quality.

Middle East & Africa (MEA) MEA countries are investing in textile infrastructure, such as Kenya's Nairobi Gate Industrial Park, to boost local production. In South Africa, rising middle-class demand and export ambitions drive the use of advanced textile chemicals to meet international standards.

Browse through Grand View Research's Category Specialty Polymers Industry Research Reports.

The global perlite market size was estimated at USD 1.55 billion in 2024 and is projected to grow at a CAGR of 6.9% from 2025 to 2030.

The global aseptic packaging market size was valued at USD 77.1 million in 2024 and is projected to grow at a CAGR of 10.8% from 2025 to 2030.

Key Companies & Market Share Insights:

The global textile chemicals market is characterized by the presence of both established players and emerging participants. Companies in this sector are expanding their manufacturing capabilities, investing in research and development, and focusing on sustainable product innovations to keep up with evolving demands in textile production. This competitive landscape is set to foster a range of innovative products, including environmentally friendly and efficient chemical solutions that align with the growing sustainability trend in the textile industry.

Kiri Industries Ltd. – A key player known for its expertise in dye and dye intermediates, Kiri Industries Ltd. produces a range of textile chemicals used globally in dyeing and printing applications.

AB Enzymes – A biotechnology company specializing in enzyme solutions for various industries, including textiles. AB Enzymes provides enzyme preparations that improve fabric properties and help reduce the environmental impact of textile production. Their products are also used in baking, fruit juice processing, grain processing, and animal feed.

BASF SE – Operating across six segments, BASF SE’s textile chemical offerings are mainly within the chemicals and industrial solutions segments. The company supplies non-halogenated flame retardants and other chemical additives for textiles. Its diversified portfolio includes intermediates, petrochemicals, and catalysts, which cater to various end-use industries, including textiles.

Evonik Industries AG – A leading global manufacturer of specialty chemicals, Evonik operates through four business segments, with the Performance Materials segment serving the textile market. The company provides a wide array of chemical intermediates and additives, including polymer additives and potassium derivatives, for use in enhancing textile properties.

Kemira Oyj – Specializing in chemical solutions for industrial use, Kemira offers products that serve the pulp and paper, water, oil and gas, and textile industries. For textiles, Kemira provides oil-based foam control products (defoamers) that reduce foam formation in high-temperature applications, as well as dry powder flocculants, such as nonionic polyacrylamides, which aid in treating wastewater in textile processes.

OMNOVA Solutions Inc. – OMNOVA is a specialty chemicals manufacturer that produces emulsion polymers and functional chemicals. OMNOVA’s offerings include various decorative and functional surfaces, including pool liner films and upholstery materials. Their performance chemicals and engineered surfaces divisions supply products for applications in textiles, construction, and consumer goods.

Govi N.V. – This company manufactures engineered process chemicals, producing emulsions, oleochemicals, and dispersions for industries including construction, insulation, food, feed, and textiles. With five production sites worldwide, Govi N.V. operates facilities in Belgium, Serbia, Malaysia, and Turkey, supplying materials used in textile treatments.

Resil Chemicals Pvt. Ltd. – Based in India, Resil Chemicals specializes in organic chemicals for textiles and various other industries such as agriculture, construction, and leather. Known for its functional finishes, Resil Chemicals produces solutions for sustainable textile processing, focusing on creating chemicals that improve fabric quality and sustainability in textiles.

Other Emerging Participants – Other noteworthy participants in the textile chemicals market include German Chemicals Ltd., BioTex Malaysia, and additional regional suppliers that are expanding their market reach by supplying niche chemical solutions for textile production.

Order a free sample PDF of the Textile Chemicals Market Intelligence Study, published by Grand View Research.

0 notes

Text

Textile Chemicals Industry Analysis, Research, Review, Applications and Forecast to 2030

The global textile chemicals market was valued at USD 26.44 billion in 2023 and is projected to expand at a compound annual growth rate (CAGR) of 4.5% from 2024 to 2030. This growth is primarily driven by the rising demand in the clothing and apparel sector, which is boosted by a growing global population, urbanization, and higher disposable incomes. Textile chemicals are essential across various stages of fabric production, from pre-treatment and dyeing to finishing, as they enhance the quality, appearance, and functionality of textiles.

The rapid development of new textile manufacturing techniques, such as digital printing, nanotechnology, and smart clothing, has increased the need for specialized chemicals that improve fabric durability, comfort, and additional features like water repellency or UV protection. Additionally, countries like China, India, and Bangladesh have emerged as major textile manufacturing hubs. These nations benefit from lower labor costs and government support aimed at promoting textile production. For instance, in February 2024, the Government of India increased its budget allocation for the textile sector to over INR 1000 crore, with INR 600 crore specifically allocated to support the Cotton Corporation of India. This kind of governmental support is expected to further boost textile chemical demand by driving increased production in these regions.

Gather more insights about the market drivers, restrains and growth of the Textile Chemicals Market

Regional Insights:

North America North America’s advanced textile manufacturing industry is characterized by high quality standards and a demand for technical textiles, especially in sectors like automotive, aerospace, and healthcare. This requires specialized textile chemicals to enhance properties like durability, flame resistance, and antimicrobial features.

In the U.S., the textile chemicals market is strong, driven by a diversified textile sector producing apparel, home furnishings, and technical textiles. Chemicals play a crucial role in enhancing aesthetics, performance, and durability through processes like dyeing, finishing, and coating.

Asia Pacific Asia Pacific held a 57.52% market share in 2023, fueled by extensive textile production in countries like China, India, and Vietnam, benefiting from low production costs and abundant resources. China, the largest global textile producer, uses extensive chemicals for dyeing, finishing, and meeting international standards.

Europe Europe’s textile chemicals market benefits from its long-standing textile industry and focus on innovation. Germany leads in R&D for sustainable textile chemicals, while Turkey’s growing textile production drives demand for chemicals across the value chain, from fiber to finished garments.

Central & South America In Central and South America, textile manufacturing, especially in Brazil, Mexico, and Colombia, is expanding, with a growing need for chemicals in processes like dyeing and finishing. Brazil, in particular, is modernizing its textile facilities and adopting advanced chemicals for better product quality.

Middle East & Africa (MEA) MEA countries are investing in textile infrastructure, such as Kenya's Nairobi Gate Industrial Park, to boost local production. In South Africa, rising middle-class demand and export ambitions drive the use of advanced textile chemicals to meet international standards.

Browse through Grand View Research's Category Specialty Polymers Industry Research Reports.

The global perlite market size was estimated at USD 1.55 billion in 2024 and is projected to grow at a CAGR of 6.9% from 2025 to 2030.

The global aseptic packaging market size was valued at USD 77.1 million in 2024 and is projected to grow at a CAGR of 10.8% from 2025 to 2030.

Key Companies & Market Share Insights:

The global textile chemicals market is characterized by the presence of both established players and emerging participants. Companies in this sector are expanding their manufacturing capabilities, investing in research and development, and focusing on sustainable product innovations to keep up with evolving demands in textile production. This competitive landscape is set to foster a range of innovative products, including environmentally friendly and efficient chemical solutions that align with the growing sustainability trend in the textile industry.

Kiri Industries Ltd. – A key player known for its expertise in dye and dye intermediates, Kiri Industries Ltd. produces a range of textile chemicals used globally in dyeing and printing applications.

AB Enzymes – A biotechnology company specializing in enzyme solutions for various industries, including textiles. AB Enzymes provides enzyme preparations that improve fabric properties and help reduce the environmental impact of textile production. Their products are also used in baking, fruit juice processing, grain processing, and animal feed.

BASF SE – Operating across six segments, BASF SE’s textile chemical offerings are mainly within the chemicals and industrial solutions segments. The company supplies non-halogenated flame retardants and other chemical additives for textiles. Its diversified portfolio includes intermediates, petrochemicals, and catalysts, which cater to various end-use industries, including textiles.

Evonik Industries AG – A leading global manufacturer of specialty chemicals, Evonik operates through four business segments, with the Performance Materials segment serving the textile market. The company provides a wide array of chemical intermediates and additives, including polymer additives and potassium derivatives, for use in enhancing textile properties.

Kemira Oyj – Specializing in chemical solutions for industrial use, Kemira offers products that serve the pulp and paper, water, oil and gas, and textile industries. For textiles, Kemira provides oil-based foam control products (defoamers) that reduce foam formation in high-temperature applications, as well as dry powder flocculants, such as nonionic polyacrylamides, which aid in treating wastewater in textile processes.

OMNOVA Solutions Inc. – OMNOVA is a specialty chemicals manufacturer that produces emulsion polymers and functional chemicals. OMNOVA’s offerings include various decorative and functional surfaces, including pool liner films and upholstery materials. Their performance chemicals and engineered surfaces divisions supply products for applications in textiles, construction, and consumer goods.

Govi N.V. – This company manufactures engineered process chemicals, producing emulsions, oleochemicals, and dispersions for industries including construction, insulation, food, feed, and textiles. With five production sites worldwide, Govi N.V. operates facilities in Belgium, Serbia, Malaysia, and Turkey, supplying materials used in textile treatments.

Resil Chemicals Pvt. Ltd. – Based in India, Resil Chemicals specializes in organic chemicals for textiles and various other industries such as agriculture, construction, and leather. Known for its functional finishes, Resil Chemicals produces solutions for sustainable textile processing, focusing on creating chemicals that improve fabric quality and sustainability in textiles.

Other Emerging Participants – Other noteworthy participants in the textile chemicals market include German Chemicals Ltd., BioTex Malaysia, and additional regional suppliers that are expanding their market reach by supplying niche chemical solutions for textile production.

Order a free sample PDF of the Textile Chemicals Market Intelligence Study, published by Grand View Research.

0 notes

Text

Sustainability and Technological Advancements in Medical Clothing

Medical Clothing is an essential component of the healthcare industry, providing protection, comfort, and functionality to healthcare professionals and patients alike. This category of clothing encompasses a range of items, including scrubs, gowns, gloves, masks, and lab coats, all designed with specific features to ensure hygiene and safety. Medical Clothing minimizes the risk of cross-contamination, reduces exposure to infectious agents, and helps maintain a sterile environment in various healthcare settings. The importance of quality Medical Clothing cannot be overstated, as it directly impacts the health and safety of healthcare professionals and the patients they serve.

The medical clothing market was projected to be worth USD 121.31 billion in 2022, according to MRFR analysis. By 2032, the medical clothing market is projected to have grown from 127.75 billion USD in 2023 to 203.62 billion USD. The medical clothing market is anticipated to develop at a compound annual growth rate (CAGR) of approximately 5.31% between 2024 and 2032.

Medical Clothing Share and Market Analysis

In recent years, the global Medical Clothing market has witnessed significant growth, largely driven by increased demand for infection control and personal protective equipment (PPE). The market share of Medical Clothing continues to expand as more healthcare facilities recognize the importance of investing in high-quality, durable clothing. The Medical Clothing Share is also influenced by innovations in fabric technology, such as antimicrobial finishes, breathable materials, and enhanced comfort features. The current market analysis highlights a trend towards sustainable and reusable Medical Clothing as hospitals and healthcare providers aim to reduce environmental impact while maintaining high safety standards.

Medical Clothing Trends

Several key trends are shaping the future of Medical Clothing, reflecting both advancements in technology and changing consumer preferences. One notable trend is the shift towards eco-friendly, biodegradable, and recyclable materials, which aligns with the broader move toward sustainability in the healthcare sector. Another emerging trend is the increased demand for antimicrobial and anti-odor fabrics, which are particularly beneficial in high-contact environments. Additionally, customization and personalization of Medical Clothing are gaining popularity, as healthcare institutions seek to improve staff comfort and reduce fatigue. Finally, the rise of telemedicine and home healthcare services is creating a demand for less formal yet functional Medical Clothing, such as lightweight scrubs and medical loungewear.

Reasons to Buy Medical Clothing Reports

In-Depth Market Insights: These reports provide a comprehensive analysis of the Medical Clothing market, including trends, market share, and key drivers influencing growth.

Forecasting and Projections: By purchasing a Medical Clothing report, stakeholders gain access to future market projections, allowing for more informed business decisions.

Competitive Landscape Analysis: Understanding the strategies of key players in the Medical Clothing industry is essential for businesses aiming to strengthen their position in the market.

Emerging Trends and Opportunities: Reports highlight recent developments and trends, such as eco-friendly materials, providing businesses with insight into future innovations.

Investment Guidance: These reports offer valuable data to help investors and businesses identify profitable segments, regions, and product lines in the Medical Clothing industry.

Recent Developments in Medical Clothing

Medical Clothing has seen remarkable advancements in recent years, driven by an increased focus on hygiene and a shift towards innovative, high-performance materials. Many companies are investing in sustainable fabrics, such as biodegradable polymers, while others focus on developing protective Medical Clothing with enhanced breathability and comfort. Additionally, the COVID-19 pandemic accelerated the adoption of PPE in non-hospital settings, leading to innovations in lightweight yet protective materials suitable for everyday use. These developments ensure that Medical Clothing continues to evolve, meeting the ever-growing demands for safety, sustainability, and style in healthcare environments.

Related reports:

central lab market

dementia treatment market

exocrine pancreatic insufficiency treatment market

0 notes

Text

Textile Chemicals Market Size, Share, Growth and Industry Trends 2024 - 2030

The global textile chemicals market size was valued at USD 26.44 billion in 2023 and is projected to grow at a CAGR of 4.5% in terms of revenue from 2024 to 2030. The demand for textile chemicals is increasing rapidly due to the booming clothing and apparel industry, driven by the rising global population, urbanization, and higher disposable incomes.

In addition, the growing trend towards sustainable and functional textiles has led to the development and use of advanced chemicals that enhance fabric properties such as durability, stain resistance, and comfort. Innovations in textile manufacturing processes, such as digital printing and nanotechnology, also require specialized chemicals, further fueling demand. Moreover, the expansion of textile production in developing countries with lower labor costs contributes to the heightened need for these chemicals to meet international quality and environmental standards.

Textile chemicals are a diverse array of substances used during the various stages of clothing manufacturing and processing to enhance the characteristics and performance of fibers and fabrics. These chemicals include dyes, finishing agents, softeners, surfactants, and other specialty chemicals that impart color, improve texture, increase durability, and add specific functionalities like water repellency or flame resistance.

Gather more insights about the market drivers, restrains and growth of the Textile Chemicals Market

Textile Chemicals Market Report Highlights

• Asia Pacific dominated the market in 2023 with a revenue share of more than 57.52%. This is attributed to rapid urbanization, economic resilience during the COVID-19 pandemic, and modernization of textile and chemical manufacturing processes

• Treatment of finished products is expected to grow at the highest CAGR in terms of revenue during the forecast period. The demand is expected to rise as the process gives the products the desired properties, as well as improves the handling and aesthetic properties

• The coating process segment dominated the market in 2023 with a revenue share of more than 71.32%., as it can enhance or improve the fabric properties and characteristics

• The coating and sizing chemicals segment dominated the market in 2023 with a revenue share of more than 50.5%. This is attributable to the growing demand for chemicals that improve or enhance their aesthetic properties and characteristics in the finishing treatment of processing textiles

• Technical textiles application is expected to grow at the fastest CAGR in terms of revenue during the forecast period. The demand for these products is anticipated to augment specifically from different industries such as transportation, agriculture, and construction

Browse through Grand View Research's Specialty Polymers Industry Research Reports.

• The global smart polymers market size was valued at USD 12.84 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 4.5% from 2024 to 2030.

• The global polyolefin (POF) shrink film market size was valued at USD 8.54 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 3.5% from 2024 to 2030.

Textile Chemicals Market Segmentation

Grand View Research has segmented the global textile chemicals market based on process, product, application, and region:

Textile Chemicals Process Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

• Pretreatment

o Bleaching Agents

o Desizing Agents

o Scouring Agents

o Others

• Coating

o Anti-Piling

o Protection

o Water Proofing

o Water Repellant

o Others

• Treatment Of Finished Products

o Softening

o Stiffening

o Others

Textile Chemicals Product Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

• Coating & Sizing Chemicals

• Colorants & Auxiliaries

o Dispersants/levelant

o Fixative

o UV absorber

o Others

• Finishing Agents

o Antimicrobial or anti-inflammatory

o Flame retardants

o Repellent and release

o Others

• Surfactants

o Detergents & Dispersing Agents

o Emulsifying Agents

o Lubricating Agents

o Wetting Agents

• Denim Finishing Agents

o Anti-back Staining Agents

o Bleaching Agents

o Crush Resistant Agents

o Defoamers

o Enzymes

o Resins

o Softeners

o Others

Textile Chemicals Application Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

• Apparel

o Innerwear

o Outerwear

o Sportswear

o Others

• Home Furnishing

o Carpet

o Drapery

o Furniture

o Others

• Technical Textiles

o Agrotech

o Buildtech

o Geotech

o Indutech

o Medtech

o Mobiltech

o Packtech

o Protech

o Others

• Other Applications

Textile Chemicals Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

• North America

o U.S.

o Canada

o Mexico

• Europe

o Germany

o Turkey

o Italy

o UK

o France

o Russia

o Spain

o Poland

• Asia Pacific

o China

o India

o Japan

o South Korea

o Vietnam

o Indonesia

• Central & South America

o Brazil

o Argentina

• Middle East and Africa

o Saudi Arabia

o South Africa

o Morocco

o Tunisia

o UAE

o Kenya

Order a free sample PDF of the Textile Chemicals Market Intelligence Study, published by Grand View Research.

#Textile Chemicals Market#Textile Chemicals Market size#Textile Chemicals Market share#Textile Chemicals Market analysis#Textile Chemicals Industry

0 notes

Text

The global demand for N-vinylformamide was valued at USD 384.9million in 2022 and is expected to reach USD 637.0 Million in 2030, growing at a CAGR of 6.50% between 2023 and 2030.The global N-vinylformamide (NVF) market has gained significant attention in recent years due to its unique properties and diverse applications across various industries. As a versatile monomer, NVF has opened new avenues in the specialty chemicals sector, leading to increased demand and research into its potential uses. This article provides an overview of the NVF market, its key applications, market dynamics, and future growth prospects.

Browse the full report at https://www.credenceresearch.com/report/n-vinylformamide-market

Introduction to N-Vinylformamide

N-vinylformamide is an organic compound that serves as a precursor to polyvinylformamide, a polymer that can be hydrolyzed to form polyvinylamine. This transformation gives NVF-based products their unique properties, making them useful in a variety of applications. NVF is typically produced through the reaction of formamide with acetylene, a process that results in a colorless liquid with a boiling point of 50-55°C. Its ability to polymerize easily makes it an essential component in the synthesis of various polymers and copolymers.

Key Applications of N-Vinylformamide

1. Water Treatment: One of the most significant applications of NVF is in water treatment processes. The polymeric derivatives of NVF, particularly polyvinylamine, are highly effective flocculants and coagulants. These compounds are used to remove suspended particles, heavy metals, and organic contaminants from wastewater, making them crucial in industrial and municipal water treatment facilities.

2. Paper Manufacturing: In the paper industry, NVF-based polymers are used as dry-strength resins. These resins improve the mechanical properties of paper products, such as tensile strength and burst resistance, without negatively impacting other qualities like printability. This makes NVF derivatives indispensable in the production of high-quality paper and packaging materials.

3. Adhesives and Coatings: NVF is also used in the formulation of adhesives and coatings. Its ability to form strong, durable bonds makes it ideal for use in high-performance adhesives. In coatings, NVF-based products enhance properties like adhesion, durability, and chemical resistance, making them suitable for a wide range of applications, including automotive, construction, and electronics industries.

4. Textile and Personal Care Products: In the textile industry, NVF-based polymers are used as fabric finishes to improve properties like softness, wrinkle resistance, and moisture absorption. In personal care products, NVF derivatives are employed as conditioning agents in shampoos and skin care formulations, where they provide moisture retention and film-forming properties.

Market Dynamics

The NVF market is influenced by several key factors, including the growing demand for water treatment solutions, the expansion of the paper and packaging industry, and the increasing use of high-performance adhesives and coatings. Additionally, the rising awareness of environmental sustainability has driven the adoption of NVF-based products in various industries, as they offer eco-friendly alternatives to traditional chemical agents.

1. Demand Drivers: - Water Treatment: The global water crisis and stringent environmental regulations have led to an increased demand for efficient water treatment solutions, driving the use of NVF-based flocculants and coagulants. - Packaging Industry: The growing e-commerce sector and the need for sustainable packaging solutions have boosted the demand for NVF in paper manufacturing. - Construction and Automotive Sectors: The need for advanced adhesives and coatings in construction and automotive applications has further propelled the NVF market.

2. Restraints: - High Production Costs: The production of NVF involves complex chemical processes, leading to relatively high costs compared to other monomers. This can be a limiting factor for its widespread adoption, especially in cost-sensitive markets. - Health and Safety Concerns: NVF is classified as a hazardous substance, and its handling requires strict safety measures. These health and safety concerns can restrict its use in certain applications.

Future Growth Prospects

The future of the NVF market looks promising, with several factors contributing to its potential growth. Advances in polymer science and the development of new NVF-based products are expected to expand its application range. Moreover, the increasing focus on sustainability and the circular economy will likely drive the demand for eco-friendly materials, further boosting the NVF market.

Key Players

BASF

Dia-Nitrix

Eastman Chemical

Mitsubishi Rayon Company, Ltd.

TCI (Shanghai) Development Co., Ltd.

Santa Cruz Biotechnology, Inc.

Solenis LLC

Braskem

DowDuPont

Cargil

Royal DSM

Segmentation

By Application:

Polymerization

Adhesives and Sealants

Coatings

Textiles and Fibers

Paper and Packaging

Others

By End-Use Industry:

Chemical Industry

Adhesives and Sealants

Paints and Coatings

Textiles and Apparel

Paper and Packaging

Others

By Purity:

Standard Purity

High Purity

By Product Form:

Liquid

Solid

By Region

North America

US

Canada

Mexico

Europe

Germany

France

UK.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/n-vinylformamide-market

About Us:

Credence Research is committed to employee well-being and productivity. Following the COVID-19 pandemic, we have implemented a permanent work-from-home policy for all employees.

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

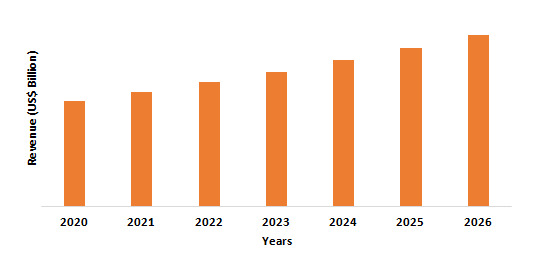

Global Top 15 Companies Accounted for 39% of total Waterproof Fabrics market (QYResearch, 2021)

Waterproof fabrics are fabrics that are inherently, or have been treated to become, resistant to penetration by water and wetting. They are usually natural or synthetic fabrics that are laminated to or coated with a waterproofing material such as rubber, polyvinyl chloride (PVC), polyurethane (PU), silicone elastomer, fluoropolymers, and wax.

In this report we focus on raw membrane material.

According to the new market research report “Global Waterproof Fabrics Market Report 2023-2029”, published by QYResearch, the global Waterproof Fabrics market size is projected to reach USD 2.12 billion by 2029, at a CAGR of 3.9% during the forecast period.

Figure. Global Waterproof Fabrics Market Size (US$ Million), 2018-2029

Figure. Global Waterproof Fabrics Top 15 Players Ranking and Market Share(Based on data of 2021, Continually updated��

The global key manufacturers of Waterproof Fabrics include Gore, Performax, Toray Industries, Polartec Neoshell, Swmintl, Sympatex, DSM, Carrington Textiles, Derekduck, Porelle Membranes, etc. In 2021, the global top five players had a share approximately 39.0% in terms of revenue.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 16 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

0 notes

Text

Anti-Crease Agent Market Size, Share Forecast 2030

Anti-Crease Agent Market size was valued at USD 856.1 million in 2022 which is expected to reach USD 1245.7 million in 2030 with a CAGR of 4.8% for the forecast period between 2023 and 2030. Anti-crease agents are incorporated with unique characteristics that significantly eliminate problems that occurred with residual oils, silicone, wax, fabrics derived from polyester, polyamide, etc. They are successively used to treat cotton and blends and impart anti-crease finishing and dimensional stability. The proper selection of anti-crease agent is achieved depending upon the type of fabric like weave pattern, its weight and construction.Nanoparticle-based anti-creasing agent is gaining prominent resemblance due to its water repellant characteristics along with antimicrobial properties.

Sample report- https://www.marketsandata.com/industry-reports/anti-crease-agent-market/sample-request

Performance of Finished Textiles is Improved by Anti-Creasing Agents

Anti-creasing agents have emerged as an impeccable chemical compound due to their unique properties like miscibility, stability, physical appearance, and compatibility. It has numerous benefits and versatile nature for dyeing cotton, polyester, and their blends. During finishing of fabrics, it assists in preventing chaffing or crease marks. Anti-creasing agents are compatible with nonionic and anionic products and remain stable to diluted acids and alkalis. The cost management for terry towels is substantially achieved using anti-creasing agents where the lubrication property led to weight loss minimization during pretreatment and dyeing processes. Kolor Jet Chemical Pvt. Ltd. has developed efficient dyebath lubricants for knit fibers to eradicate the crease marks along with reducing fiber to fiber friction and leave no dyes effects on the fabrics.

Data released by the Ministry of Textiles, India states that FDI has invested a humongous capital of USD 1,522.23 million in the textile sector from 2017-2022. In 2022, the net value of the United States man-made fiber, textile and apparel shipments accounted an estimated over USD 65.8 billion where the export of fibers, textiles contributed to around USD 34 billion.

Anti-Creasing Agents Market is Propelled Due to its Importance in Multiple Applications

Anti-creasing agents with their unique characteristics form a thin uniform protective coating surrounding the fiber to reduce the surface friction and ultimately lower the formation of stringent creases during high temperature wet processing. Knit fabric of essential blends, cellulose and synthetic fibers are processed through scouring, bleaching, dyeing, and soaping processes that became easier by using anti-creasing agents. HT Fine Chemical Co., Ltd. produces a special bath anti-creasing agent which while processing remarkably reduces the friction between fibers and its dyeing tank that reduces scratches and creases due to their smoothing and softening characteristics. Special polymer dispersion in the anti-creasing agents is solely responsible to prevent fabric rope from creasing during the pre-treatment, dyeing and post-processing.

In March 2022, the European Commission has represented its vision for textile industry which estimated that in 2021 the turnover of USD 166.99 with an increment of around 11%. Around 33% of companies are textile-based across the European Union that accounts for micro and SMEs’ enterprises. With such an impeccable figures Europe has extreme potential for anti-creasing agent market that generates phenomenal opportunities to expand.

Novel Anti-creasing Agent for Improving the Textile Bath of Fabrics

The problem of crease mark, stripped mark and other faults are usually encountered during small bath ratio case and rapid cloth speed case. Unique anti-creasing agent in the textile bath comprises of nonionic polymer, anionic polymer, water treatment agent, mould inhibitor that is used for rope dyeing of texture. Under the influence of mechanical tension, the dynamic coefficient of friction is significantly higher that produces wrinkle seal, unwanted shank seal defects during airflow dyeing machine where the speed is greater than 200 meters/minutes. The incorporation of anti-creasing agent resolves such problems during the textile bath.

Anti-Crease Agent Market: Report Scope

Anti-Crease Agent Market Assessment, Opportunities and Forecast, 2016-2030F”, is a comprehensive report by Markets and data, providing in-depth analysis and qualitative & quantitative assessment of the current state of the Anti-Crease Agent Market, industry dynamics and challenges. The report includes market size, segmental shares, growth trends, COVID-19 and Russia-Ukraine war impact, opportunities and forecast between 2023 and 2030. Additionally, the report profiles the leading players in the industry mentioning their respective market share, business model, competitive intelligence, etc.

Click here for full report- https://www.marketsandata.com/industry-reports/anti-crease-agent-market

Contact

Mr. Vivek Gupta 5741 Cleveland street, Suite 120, VA beach, VA, USA 23462 Tel: +1 (757) 343–3258 Email: [email protected] Website: https://www.marketsandata.com

0 notes

Text

Overview of the Global Textile Coating Market

In the vast tapestry of industries that drive the global economy, few are as integral and diverse as the textile industry. Within this dynamic sector lies a lesser-known yet crucial segment - the Textile Coating Market. Textile coating plays a pivotal role in enhancing the functionality, durability, and aesthetic appeal of fabrics, making it a vital part of various industries ranging from fashion to automotive and healthcare. Let's delve into an overview of this market, exploring its key drivers, trends, and future prospects.

Understanding Textile Coating

Textile coating involves the process of applying a layer of polymer or other substances to a textile substrate. This coating can serve multiple purposes, such as waterproofing, flame resistance, antimicrobial properties, UV protection, and even aesthetic enhancements like adding sheen or texture. The application of coatings can transform ordinary fabrics into high-performance materials suitable for a wide array of applications.

Market Size and Growth

The global Textile Coating Market has witnessed significant growth in recent years and is projected to continue expanding. Factors such as increasing demand for coated textiles in industries like sports and outdoor apparel, automotive interiors, and medical textiles are driving this growth. According to recent market reports, the Textile Coating Market was valued at approximately USD 5.4 billion in 2020 and is expected to reach USD 7.2 billion by 2026, with a compound annual growth rate (CAGR) of around 4.8% during the forecast period.

Key Drivers of Growth

Several factors contribute to the growth of the Textile Coating Market:

Demand for Technical Textiles: The rise in demand for technical textiles, which require specialised coatings for functionalities like moisture management, durability, and insulation, is a major driver. These textiles find applications in sectors such as healthcare, construction, and geotextiles.

Advancements in Coating Technologies: Ongoing advancements in coating technologies, such as nanotechnology and plasma treatments, are expanding the possibilities for innovative and high-performance coated textiles. These technologies offer improvements in durability, breathability, and environmental sustainability.

Increasing Focus on Sustainability: With growing environmental concerns, there is a notable shift towards sustainable coating materials and processes. Water-based coatings and bio-based polymers are gaining traction as eco-friendly alternatives to traditional solvent-based coatings.

Rising Demand in Automotive Industry: The automotive sector is a significant consumer of coated textiles, using them in vehicle interiors, seating, and airbags. As the automotive industry evolves with the introduction of electric vehicles and autonomous driving, the demand for specialised coatings is expected to increase.

Regional Insights

The Textile Coating Market exhibits regional variations influenced by factors such as economic development, manufacturing capabilities, and end-user industries. Some key regional insights include:

Asia-Pacific: Dominating the market, Asia-Pacific accounts for a substantial share due to its thriving textile industry, particularly in countries like China, India, and Vietnam. The region's rapid industrialization and expanding automotive and construction sectors contribute to the demand for coated textiles.

North America: The region boasts a strong presence of leading manufacturers and technological innovators in textile coating. The demand for protective and performance textiles in industries like healthcare and defence drives the market in this region.

Europe: Known for its stringent regulations on chemicals and sustainability, Europe is witnessing a shift towards eco-friendly coating solutions. The region's fashion industry also contributes to the demand for aesthetically enhanced textiles.

Future Trends and Opportunities

Looking ahead, the Textile Coating Market presents several exciting trends and opportunities:

Smart Textiles: The integration of electronics and sensors into textiles is creating a new frontier of smart textiles. These textiles, with functionalities such as temperature regulation and health monitoring, require advanced coating technologies.

Medical Textiles: With an ageing population and increased focus on healthcare, the demand for medical textiles with antimicrobial and barrier properties is on the rise. Coatings play a crucial role in ensuring the effectiveness and safety of these textiles.

3D Printing: The convergence of textile coating and 3D printing technologies opens up possibilities for customizable, on-demand textile products. This combination allows for intricate designs and functional coatings to be applied during the printing process.

In conclusion, the Textile Coating Market stands as a vibrant and evolving segment within the broader textile industry. Its growth is driven by technological advancements, shifting consumer preferences, and the diverse applications of coated textiles across industries. As the world emphasises sustainability and innovation, the market is ripe with opportunities for manufacturers, researchers, and stakeholders to explore new materials, applications, and business models.

As we continue to weave innovation into the fabric of industry, the Textile Coating Market will undoubtedly remain a key thread in the tapestry of global commerce.

0 notes

Text

Plastics Market Trends, Share, industry Growth 2024-2032

IMARC Group, a leading market research company, has recently releases report titled “Plastics Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2024-2032” offers a comprehensive analysis of the industry, which comprises insights on the global plastics market trends. The global market size US$ 634.8 Billion in 2023. Looking forward, IMARC Group expects the market to reach US$ 829.7 Billion by 2032, exhibiting a growth rate (CAGR) of 2.93% during 2024-2032.

Request For Sample Copy of Report: https://www.imarcgroup.com/plastics-market/requestsample

Factors Affecting the Growth of the Plastics Industry:

Increasing Demand in the Packaging Industry:

The expansion of the packaging industry represents one of the primary factors propelling the market growth. Additionally, the rising reliance of individuals on online shopping channels is driving the demand for convenient and efficient packaging solutions. Plastics offer a versatile and cost-effective means of packaging, providing durability and flexibility for various applications. Moreover, advancements in plastic technologies, such as barrier coatings and modified atmospheres, enhance the protective qualities of plastic packaging, making it an indispensable choice for many industries.

Rapid Urbanization and Changing Lifestyles:

Rapid urbanization and evolving lifestyles of individuals are contributing substantially to the growth of the market. The increasing rate of urbanization is driving the need for products that align with the fast-paced urban lifestyle, where convenience and efficiency are paramount. Plastics, being lightweight, durable, and easily moldable, are widely used the manufacturing of numerous consumer goods, ranging from electronics to automotive components. The rising demand for plastic-based products beyond necessities to encompass a wide array of lifestyle products, including fashion accessories, home goods, and recreational items is favoring the market growth. This shift in consumer preferences, coupled with the adaptability of plastics in design and functionality, propelling the market growth.

Technological Innovations and Material Advancements:

Continuous innovations in plastic materials and manufacturing processes are strengthening the growth of the market. Researchers and industry leaders are investing in developing sustainable and eco-friendly alternatives to traditional plastics, addressing concerns related to environmental impact. Additionally, the increasing use of biodegradable plastics, recycled materials, and bio-based polymers to meet stringent environmental regulations and consumer demands for greener alternatives is offering a favorable market outlook. Furthermore, technological advancements, such as three-dimensional (3D) printing and nanotechnology, are opening new frontiers in plastic applications, enabling the production of complex and customized products across various sectors. These innovations enhance the performance characteristics of plastics and attract a wider consumer base.

Leading Companies Operating in the Global Plastics Industry:

Arkema S.A

BASF SE

Celanese Corporation

Chevron Phillips Chemical Co. LLC

Chimei Corporation

Covestro AG

Dow Inc.

Eastman Chemical Company

Evonik Industries AG

Exxon Mobil Corporation

Sumitomo Chemical Co. Ltd.

Toray Industries Inc.

Plastics Market Report Segmentation:

By Type:

Polyethylene

Polypropylene

Polyvinyl Chloride

Others

Polyethylene represents the largest market segment as it offers customization and can be easily molded, extruded, and fabricated into various shapes and sizes.

By Application:

Injection Molding

Blow Molding

Roto Molding

Compression Molding

Casting

Thermoforming

Extrusion

Calendering

Others

Injection molding holds the largest market share as it allows high-volume production with a short cycle time.

By End User:

Packaging

Automotive

Infrastructure and Construction

Consumer Goods

Others

Packaging accounts for the majority of the market share as plastic packaging can resist breaking and shattering and ensure safe transportation of products.

Regional Insights:

North America (United States, Canada)

Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

Latin America (Brazil, Mexico, Others)

Middle East and Africa

Asia Pacific's dominance in the plastics market is attributed to the expansion of several industries in the region.

Global Plastics Market Trends:

The increasing emphasis on sustainable and circular economy initiatives is creating a positive outlook for the market. Along with this, manufacturers are investing in research and innovation to create biodegradable plastics, recycled materials, and bio-based polymers. These alternatives help reduce the environmental impact of traditional plastics by promoting recyclability, minimizing waste, and lowering carbon footprints. Furthermore, governing authorities and regulatory bodies worldwide are also implementing policies to encourage the adoption of sustainable practices within the plastic industry.

Other Key Points Covered in the Report:

COVID-19 Impact

Porters Five Forces Analysis

Value Chain Analysis

Strategic Recommendations

About Us

IMARC Group is a leading market research company that offers management strategy and market research worldwide. We partner with clients in all sectors and regions to identify their highest-value opportunities, address their most critical challenges, and transform their businesses.

IMARC Group’s information products include major market, scientific, economic and technological developments for business leaders in pharmaceutical, industrial, and high technology organizations. Market forecasts and industry analysis for biotechnology, advanced materials, pharmaceuticals, food and beverage, travel and tourism, nanotechnology and novel processing methods are at the top of the company’s expertise.

Contact US

IMARC Group 134 N 4th St. Brooklyn, NY 11249, USA Email: [email protected] Tel No:(D) +91 120 433 0800 United States: +1-631-791-1145 | United Kingdom: +44-753-713-2163

0 notes

Text

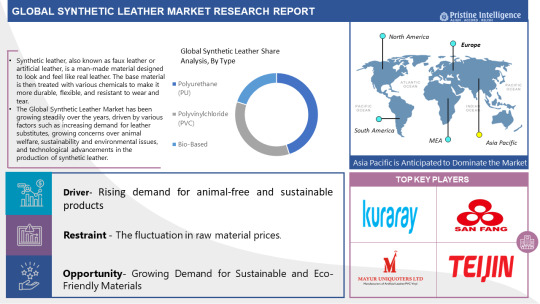

The global market for Synthetic Leather estimated to reach a revised size of USD 51210 Million by 2030

The global market for Synthetic Leather estimated at USD 38978.9 Million in 2023 is projected to reach a revised size of USD 51210 Million by 2030, growing at a CAGR of 5.61% over the period 2023-2030.

Synthetic leather, also known as faux leather or artificial leather, is a man-made material designed to look and feel like real leather. It is a type of fabric that is made by applying a coating of plastic or polymer to a base material such as fabric or paper. The base material is then treated with various chemicals to make it more durable, flexible, and resistant to wear and tear.

The most common types of synthetic leather are polyurethane (PU) leather and polyvinyl chloride (PVC) leather. PU leather is made by coating a fabric or paper base material with a layer of polyurethane, while PVC leather is made by coating a fabric or paper base material with a layer of PVC. Other types of synthetic leather include bio-based leather, which is made from natural materials such as pineapple leaves or mushrooms, and other innovative materials such as silicone leather.

This Synthetic Leather Market Report includes information on the manufacturer, such as shipping, pricing, revenue, interview records, gross profit, and company distribution, among other things. These details assist consumers to learn more about their rivals. Likewise, the report outlines the significant difficulties that would have an influence market growth. They also give extensive facts about the industry's potential to key stakeholders, allowing them to expand their industries and increase sales in certain industries. The research will assist companies who are already in or want to enter this market in analysing the many facets of this domain before investing in or growing their industry in the Synthetic Leather markets.

Get Sample Report: -

https://pristineintelligence.com/request-sample/synthetic-leather-market-43

The Report Will Include A Major Chapter

Patent Analysis

Regulatory Framework

Technology Roadmap

BCG Matrix

Heat Map Analysis

Price Trend Analysis

Investment Analysis

Company Profiling and Competitive Positioning

Industry Value Chain Analysis

Market Dynamics and Factors

Porter’s Five Forces Analysis

Pestle Analysis

SWOT Analysis

Leading players involved in the Synthetic Leather Market include:

"Kuraray Co. Ltd. (Japan), San Fang Chemical Industry Co. Ltd. (Taiwan), Mayur Uniquoters Ltd. (India), NAN YA PLASTICS CORPORATION (Taiwan), Teijin Limited (Japan), Filwel Co. Ltd. (Japan), Alfatex (Italy), Zhejiang Hexin Industry Group Co. Ltd. (China), DuPont de Nemours Inc. (USA), Yantai Wanhua Synthetic Leather Group Co.Ltd. (China), Toray Industries Inc. (Japan), H.R. Polycoats Pvt. Ltd. (India), Archilles Corporation (Japan), Favini S.r.l. (Italy), AICA Kogyo Co.Ltd. (Japan), and Other key players."

Knowing market share in the base year provides you an idea of the competition and size of the suppliers. It reflects the market's fragmentation, accumulation, dominance, and amalgamation features. The Competitive Scenario provides an outlook study of the suppliers' various industry growth plans. This section's news provides vital insights at various stages while keeping up with the industry and engaging players in the economic discussion. Merger & Acquisition, Collaboration, Partnership, Agreement, Investment & Funding, New Product Launch & Enhancement, Recognition, Rewards & Expansion are the categories that the competitive scenario represents. All of the research data collected helps the vendor identify market gaps as well as competitor weaknesses and strengths, helping them to better their service and product.

If You Have Any Query Synthetic Leather Market Report, Visit:

Segmentation of Synthetic Leather Market:

By Type

Polyurethane (PU)

Polyvinylchloride (PVC)

Bio-Based

By Application

Footwear

Furniture

Automotive

Textile

Sports

Electronics

Others

An in-depth study of the Synthetic Leather industry for the years 2023–2030 is provided in the latest research. North America, Europe, Asia-Pacific, South America, the Middle East, and Africa are only some of the regions included in the report's segmented and regional analyses. The research also includes key insights including market trends and potential opportunities based on these major insights. All these quantitative data, such as market size and revenue forecasts, and qualitative data, such as customers' values, needs, and buying inclinations, are integral parts of any thorough market analysis.

Market Segment by Regions: -

North America (U.S., Canada, Mexico)

Eastern Europe (Bulgaria, The Czech Republic, Hungary, Poland, Romania, Rest of Eastern Europe)

Western Europe (Germany, U.K., France, Netherlands, Italy, Russia, Spain, Rest of Western Europe)

Asia-Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Vietnam, The Philippines, Australia, New Zealand, Rest of APAC)

Middle East & Africa (Turkey, Saudi Arabia, Bahrain, Kuwait, Qatar, UAE, Israel, South Africa)

Effective Points Covered in Synthetic Leather Market Report: -

Details Competitor analysis with accurate, up-to-date demand-side dynamics information.

Standard performance against major competitors.

Identify the growth segment of your investment.

Understanding most recent innovative development and supply chain pattern.

Establish regional / national strategy based on statistics.

Develop strategies based on future development possibilities.

Purchase This Reports: -

https://pristineintelligence.com/buy-now/43

About Us:

We are technocratic market research and consulting company that provides comprehensive and data-driven market insights. We hold the expertise in demand analysis and estimation of multidomain industries with encyclopedic competitive and landscape analysis. Also, our in-depth macro-economic analysis gives a bird's eye view of a market to our esteemed client. Our team at Pristine Intelligence focuses on result-oriented methodologies which are based on historic and present data to produce authentic foretelling about the industry. Pristine Intelligence's extensive studies help our clients to make righteous decisions that make a positive impact on their business. Our customer-oriented business model firmly follows satisfactory service through which our brand name is recognized in the market.

Contact Us:

Office No 101, Saudamini Commercial Complex, Right Bhusari Colony, Kothrud, Pune,

Maharashtra, India - 411038 (+1) 773 382 1049 +91 - 81800 - 96367

Email:[email protected]

#Synthetic Leather#Synthetic Leather Market#Synthetic Leather Market Size#Synthetic Leather Market Share#Synthetic Leather Market Growth#Synthetic Leather Market Trend#Synthetic Leather Market segment#Synthetic Leather Market Opportunity#Synthetic Leather Market Analysis 2022#US Synthetic Leather Market#Synthetic Leather Market Forecast#Synthetic Leather Industry#Synthetic Leather Industry Size#china Synthetic Leather Market#UK Synthetic Leather Market

0 notes

Text