#Phenolic Resin end users

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has been banned in Indonesia for providing people with access to pornographic content.

Text

Phenolic Resin Market – Future Plans and Industry Growth with Quantitative And Qualitative Analysis

The report "Phenolic Resin Market is estimated at USD 11.7 Billion in 2021 and is projected to reach USD 14.4 Billion by 2026, at a CAGR of 4.3% between 2021 and 2026. Phenolic resins are the oldest synthetic polymers obtained from the reaction of phenol and formaldehyde. They are a class of thermosetting resins. Phenolic resins are mainly categorized into resol resins, novolac resins, and others (bio-phenolic, cresol novolac, and formaldehyde-free phenolic resins). They possess high mechanical strength, low toxicity, and excellent heat resistance. Their applications can broadly be categorized into wood adhesives, foundry & moldings, laminates, paper impregnation, coatings, insulation, and others.

Get PDF brochure of the report: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=177821389

Browse 520 market data Tables and 56 Figures spread through 329 Pages and in-depth TOC on "Phenolic Resin Market”

Resol is the largest type of phenolic resin.

Resol is a popular type of phenolic resin due to its cost-effectiveness, improved properties, and versatility in various applications, such as exterior plywood-oriented strand board (OSB), engineered laminated composite lumber (LCL), engineered woods, and adhesives. The increasing demand from the automotive and building & construction industries drives the growth of the global demand for resol resin.

Wood adhesives is the major application for phenolic resin.

The use of phenolic resin in wood adhesives is a rapidly growing application, driven by the expansion of the construction industry. The plywood subsegment holds a significant share in the wood adhesives market. The Asia Pacific region is the largest market for wood adhesives and the demand for phenolic resins is expected to rise significantly due to the presence of growing economies like India, South Korea, and Indonesia.

https://www.prnewswire.com/news-releases/phenolic-resin-market-worth-14-4-billion-by-2026--exclusive-report-by-marketsandmarkets-301438866.html

APAC is the fastest-growing market for phenolic resin.

APAC is projected to be the fastest-growing phenolic resin market. The growth of the APAC phenolic resin market can be attributed to the growing investment in building & construction, and automotive industry in the region. Additionally, Phenolic resin manufacturers are targeting this region, as it is the strongest regional market. China is the leading producer and consumer of phenolic resins in the region. Other major markets in the region are emerging economies such as Japan, India, and Thailand.

Most active players in the phenolic resin market:

Bakelite Synthetics (U.S), Sumitomo Bakelite Company Limited (Japan), SI Group Inc. (U.S), Jinan Shengquan Group Share Holding Co., Ltd., (China), Ashland Global Holdings, Inc. (U.S), BASF SE (Germany), Georgia-Pacific Chemicals (U.S), DIC Corp (Japan), Hexcel Corporation (U.S), Akrochem Corporation (U.S).are the leading players operating in the phenolic resin market.

Early buyers will receive 10% free customization on this report.

Don't miss out on business opportunities in Phenolic Resin Market.

Speak to Our Analyst and gain crucial industry insights that will help your business grow.

https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=177821389

About MarketsandMarkets™

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the 'GIVE Growth' principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

To find out more, visit www.MarketsandMarkets™.com or follow us on Twitter, LinkedIn and Facebook.

Contact: Mr. Ashish Mehra MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA: 1-888-600-6441 [email protected]

0 notes

Text

Thermosetting Plastics Market Size, Regional Revenue and Outlook 2025-2037

Research Nester assesses the growth and market size of the global thermosetting plastics market which is anticipated to be on account of the rising demand for bio dependent thermosetting plastic

Research Nester’s recent market research analysis on “Thermosetting Plastics Market: Global Demand Analysis & Opportunity Outlook 2037” delivers a detailed competitors analysis and a detailed overview of the global thermosetting plastics market in terms of market segmentation by type, molding process, end-user industry and by region.

Growing Demand for Bio-Based Thermosetting Plastics to Promote Global Market Share of Thermosetting Plastics Market

Request Free Sample Copy of this Report @ https://www.researchnester.com/sample-request-5892

The global thermosetting plastics market is estimated to grow majorly on account of the increased demand for polyurethane in the automotive industry. Some common uses of thermoset plastics across numerous industries and sectors include water & gas pipelines, medical equipment, storage boxes, and construction machinery parts. Since the thermosetting plastics are flexible and lightweight. Thermoset composites remain stable at all temperatures and in all ambiance. For instance, Bakelite is the most common thermoset plastic that is widely used in kitchenware, jewelry, children's toys, and pipe stems. Bakelite is also used in making switches because of its poor conductivity to electricity and heat. Other than this, epoxy resin is also applied to floors and various other surfaces to add tough coating. The global epoxy resin production stood at almost 3600 thousand tonnes in the year 2022. On the back of the rising utilization of thermoset plastics on various devices, the global thermosetting plastics market is anticipated to grow during the forecasted period. Other than this, the rising growth in the construction industry and rising demand for polyurethane in the automotive industry. Also, the advent of bio-based plastics is likely to showcase growth opportunities for the global thermosetting plastics market during the forecasted period. The properties such as chemical resistance, heat resistance, and structural integrity of the thermoset plastics are also going to augment the growth of the global thermosetting plastics market during the forecasted period.

Some of the major growth factors and challenges that are associated with the growth of the global thermosetting plastics market are:

Growth Drivers:

Rising Demand for Bio-depended Thermosetting Plastics

Surging Utilization of Thermosetting Plastics Making Kitchen Utensils

Challenges:

The rising feedstock crunch and exorbitant cost of thermosetting plastics, stringent government policies, and problems related to manufacturing techniques are some of the major factors anticipated to hamper the global market size of the global thermosetting plastics market.

Request for customization @ https://www.researchnester.com/customized-reports-5892

By type, the global thermosetting plastics market is segmented into unsaturated polyesters, polyurethanes, phenolic, epoxy, amino, alkyd, vinyl, and ester. Out of these, the unsaturated polyesters segment is expected to grow the most during the forecasted period. The growth can be attributed to the outstanding thermal opposition and high creep power of the materials.

By region, the Europe thermosetting plastics market is to generate the highest revenue by the end of 2036. The rising demand for thermosetting plastics can be attributed to the increasing utilization of epoxy for making various appliances.

This report also provides the existing competitive scenario of some of the key players of the global thermosetting plastics market which includes company profiling of Alchemie Ltd., Celanese Corporation, LANXESS, DAICEL CORPORATION, INEOS, BASF SE, Covestro A.G., BUFA GmbH & Co. KG, Daicel Corporation, Eastman Chemical Company, Asahi Kasei Corporation, Mitsui Chemicals, Inc., NIPPON STEEL Chemical & Material Co., Ltd., INOAC Corporation and others.

Access our detailed report @ https://www.researchnester.com/reports/thermosetting-plastics-market/5892

About Research Nester-

Research Nester is a leading service provider for strategic market research and consulting. We aim to provide unbiased, unparalleled market insights and industry analysis to help industries, conglomerates and executives to take wise decisions for their future marketing strategy, expansion and investment etc. We believe every business can expand to its new horizon, provided a right guidance at a right time is available through strategic minds. Our out of box thinking helps our clients to take wise decision in order to avoid future uncertainties.

Contact for more Info:

AJ Daniel

Email: [email protected]

U.S. Phone: +1 646 586 9123

U.K. Phone: +44 203 608 5919

0 notes

Text

Bisphenol A Prices Trend | Pricing | News | Database | Chart

Bisphenol A (BPA) is a chemical compound that plays a key role in the production of polycarbonate plastics and epoxy resins, commonly used in various consumer goods and industrial applications. The market dynamics for BPA prices have been subject to significant fluctuations due to a mix of global supply-demand imbalances, environmental regulations, raw material costs, and shifting consumer preferences. Understanding these movements requires a detailed look at the factors that influence BPA pricing and how they interact with broader market trends.

BPA's pricing structure has shown notable sensitivity to the raw material costs of its feedstocks, primarily phenol and acetone. Both of these precursors experience price volatility due to global economic conditions, availability of feedstock, and changes in crude oil prices. Since phenol and acetone are derivatives of petroleum-based products, any fluctuation in crude oil costs tends to trickle down into the BPA supply chain, affecting its price. The relationship between these raw materials and BPA prices is crucial for manufacturers and end-users to comprehend as they strategize around their sourcing and production costs.

Another critical factor in BPA pricing trends is regional demand and production capacity. Asia-Pacific, especially China, remains a major consumer and producer of BPA due to the region's strong manufacturing sector and high demand for polycarbonate plastics in automotive, electronics, and packaging industries. A spike in demand from these sectors often leads to a tightening of BPA supplies, driving prices up. However, market saturation, potential shifts in regional production capacities, and fluctuating trade policies can equally lead to pricing corrections or slowdowns. The market also faces challenges with logistical and distribution constraints, which can temporarily disrupt supply chains, causing rapid price movements.

Get Real Time Prices for Bisphenol A (BPA): https://www.chemanalyst.com/Pricing-data/bisphenol-a-29

Environmental regulations have also played a significant role in shaping the BPA market. Concerns over BPA's potential health risks and environmental impact have prompted regulatory authorities in various regions to impose restrictions on its use, particularly in food and beverage packaging. This has led to fluctuations in demand, with some industries seeking BPA alternatives. The emergence of bisphenol S (BPS) and other substitutes has influenced the competitive landscape, placing additional pressure on BPA prices. Producers have responded with technological advancements to create BPA products that comply with health and safety standards, although these transitions can sometimes lead to higher production costs and contribute to short-term price spikes.

Trade dynamics and geopolitical tensions further complicate BPA pricing. Tariffs, sanctions, or trade disputes involving major BPA-producing or consuming countries have the potential to disrupt global supply chains. For example, if a significant producer faces restrictions, it can lead to supply shortages and subsequent price hikes. Conversely, eased trade tensions or new agreements can stimulate exports and potentially result in price stabilization or reductions. Export-import policies therefore remain crucial considerations for market participants who aim to hedge against the unpredictable nature of international politics.

The COVID-19 pandemic highlighted the inherent volatility in the BPA market. During the height of the pandemic, demand plummeted across many sectors, including automotive and construction, due to lockdowns and economic uncertainties. This led to a temporary dip in BPA prices. However, as industries gradually reopened, a surge in demand coupled with lingering supply chain constraints resulted in a sharp price recovery. The post-pandemic rebound showcased the rapidity with which BPA prices can shift based on global economic conditions and highlighted the necessity for market participants to be agile in navigating these fluctuations.

Technological advancements in the production and application of BPA can also influence market pricing. Innovations aimed at improving process efficiencies or reducing waste can lead to cost savings, which may eventually translate to lower prices for end-users. However, the initial costs of adopting new technologies can sometimes be substantial, potentially leading to price increases in the short term. Companies that invest in sustainable production methods may also command a premium for their environmentally-friendly products, influencing market perceptions and pricing structures.

Consumer sentiment and trends have a subtle yet notable impact on BPA pricing as well. Increasing consumer awareness around health and environmental issues has prompted companies to adopt "BPA-free" labels in their packaging and products, particularly within the food and beverage industry. This shift has had a twofold impact: reduced demand for BPA in certain sectors, and a push for industry diversification to produce safer alternatives. Although this trend has led to some decline in BPA demand in specific markets, it has also opened up opportunities for BPA producers to adapt and innovate, thus maintaining their relevance in a changing market environment.

Forecasting BPA prices involves considering all these interconnected variables and more. While demand for polycarbonate plastics and epoxy resins remains relatively strong, uncertainty around regulations, alternative materials, and global economic conditions adds complexity to market projections. Analysts often track key indicators such as raw material costs, regional production shifts, trade policies, and downstream consumer trends to gauge potential price movements. The interplay of these factors results in a market that is at times unpredictable but remains a critical area of focus for producers, traders, and end-users alike. For stakeholders looking to navigate the BPA market, understanding these pricing dynamics is essential for maintaining competitiveness and ensuring resilient supply chains.

Welcome to ChemAnalyst App: https://www.chemanalyst.com/ChemAnalyst/ChemAnalystApp

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Bisphenol A#Bisphenol A Price#Bisphenol A Prices#Bisphenol A Pricing#Bisphenol A News#Bisphenol A Price Monitor#Bisphenol A Database

0 notes

Text

Electronic Adhesives Market - Forecast (2024-2030)

Electronic Adhesives Market Overview

Electronic Adhesives Market Size is forecast to reach $ 6,820 Million by 2030, at a CAGR of 6.50% during forecast period 2024-2030. Electronic adhesives are used for circuit protection and electronic assembly applications such as bonding components, wire tacking, and encapsulating electronic components. The use of electronic adhesives in manufacturing components for electric vehicles such as printed circuit boards, lithium-ion batteries, and battery pack assemblies are facilitating growth of the market. Growing adoption of surface mounting technology to replace welding and soldering is one of the prominent trends in the electronics industry, shaping the demand for electronics adhesives.

Report Coverage

The report: “Electronic Adhesives Market – Forecast (2024-2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the Electronic Adhesives Industry.

By Type: Thermal Conductive, Electrically Conductive, Ultraviolet-Curing and Others.

By Resin Type: Epoxy, Cyanoacrylates, Polyamides, Phenolic, Silicones, and Others (Acrylics, and Polyurethane)

By Application: PCB’s, Semiconductor, and Others

By End-User Industry: Consumer Electronic (Wearable Devices, LEDs & TVs, Smart Phones & Tablets, Computers, Laptops, and Others), Healthcare, Energy & Power (Solar, Wind, and Others), Telecom Industry, Transportation (Automotive (Passenger Vehicles, Light Commercial and Heavy Commercial Vehicles), Marine, Locomotive, and Aerospace), Oil & Gas, Chemical, Pulp & Paper, and Others.

By Geography: North America, South America, Europe, APAC, and RoW

Request Sample

Key Take away

In 2020, North America held the largest share after APAC. Due to growing demand for electronic adhesives in electronics and telecommunication industry. The US hold the largest share in the region over the forecast period.

Growing adoption of electric vehicles is expected to provide a major growth opportunity for the market.

Emission of Volatile Organic Compounds (VOC’s) may deter the market's growth during the forecasted period.

COVID-19 has hindered the market growth owing to the disruption of supply chain and worldwide lockdown.

Electronic Adhesives Market Segment Analysis - By Type

Electrically Conductive segment held the largest share of more than 30% in the electronics adhesives market in 2020. Electrically Conductive are used in various industry verticals such as aerospace, automotive, medical, and telecom products. Electrically conductive is an excellent solution for making electrical contacts on PCBs and other temperature-sensitive substrates, as their curing temperature is below the soldering temperature. An increase in demand for Anisotropic Conductive Adhesives (ACA) in LCD connections, PCBs, and bonding antenna structures further boost the demand for the market. Electric conductive are also used in the LED industry for their capacity to serve as stable electrical contacts by absorbing mismatches, which will likely boost the market's growth for the forecasted period.

Inquiry Before Buying

Electronic Adhesives Market Segment Analysis - By Resin Type

Epoxy segments held the largest share of more than 25% in the market in 2020. Epoxy is widely used in electronic applications, either in two-part or single-part heat cure products. Epoxy has good resilience against environmental and media influences, it has a dry and non-tacky surface which is perfect to be used as a protective coating and is widely used in adhesives, plastics, paints, coatings, primers and sealers, flooring, and other. Curing epoxy adhesives can take place either at room or elevated temperature or through photoinitiators and UV light. Modern photoinitiators also react to the special UV spectrum of LED light sources, so that newly developed epoxide resin adhesives can be cured with both UV and UV LED light. Some epoxies exhibit optical properties and diffraction indexes, making them useful for applications in precision optics, lens bonding, and information technology, which will further boost the market's growth.

Electronic Adhesives Market Segment Analysis - By Application

Printed Circuit Boards (PCBs) segment held the largest share of more than 35% in the market in 2020. Electronic adhesives are used as a conformal coating in PCBs. Adhesive is used in wire tracking, potting & encapsulation of components, conformal coatings of circuit boards, and bonding of surface mount components. PCBs are highly reliable, cheap, less chance of short circuit, easily repairable, and are compact in size. The growing uses of laptops, smartphones, and household appliances coupled with developing living standards further drive the growth of PCB. Whereas, the growing uses of PCB’s in automotive, industrial & power equipment, control & navigation systems, and aerospace monitoring also contribute to the market growth. According to Aerospace Industries Association (AIA) report, in 2018, aerospace and defense exports amounted to $151 billion, an increase of 5.81% from the previous year, and civil aerospace accounted for the majority of exports with $131.5 billion.

Schedule a Call

Electronic Adhesives Market Segment Analysis - By End-User Industry

Consumer Electronics segment held the largest share of more than 30% in the Electronic Adhesives Market in 2020. Rapid urbanization and increase in the development of new technology have propelled the demand for consumer electronics. As per the United Nations, 55% of the world’s population lives in urban areas, which propel the demand for consumer electronics. The growing demand for lightweight and portable equipment such as smartphones, laptops, and digital cameras are playing a significant role in boosting the demand for the market. As per a report released by Nexdigm Private Limited, a private company, the global electronics industry is expected to reach $7.3 trillion by 2025, which will significantly propel the demand for the market during the forecasted period.

Electronic Adhesives Market Segment Analysis - By Geography

Asia-Pacific held the largest share of more than 45% in the Electronic Adhesives Market in 2020. China, India, and Japan are the major contributors to the growth of Electronic Adhesives Market in APAC. The large consumer base, developing manufacturing sector, and increase in middle-class population along with smart city projects are major factors for the market growth. As per the Indian Brand Equity Foundation (IBEF) report released in 2020, electronics manufacturing in India is expected to reach $163.14 billion by 2025, and demand for electronics hardware in India is expected to reach US$ 400 billion by 2024. The shifting of production lines to the APAC region for the low cost of production and the ability to serve the local emerging market is another factor for the growth of the market in the region.

Buy Now

Electronic Adhesive Market Drivers

Growing Need for Miniaturized Electronic Products

Growing demand for low-cost, reliable, and miniaturized electronic devices from consumers propel the market's growth. The increasing demand for miniaturized products has led to the development of smaller electrical components, which occupy less area. The need for smaller and thinner consumer electronics devices is a new trend among consumers. The surface mount technology helps in using and assembling much smaller components, thus facilitating a smaller, portable, and lightweight electronic device. Pocket calculators, smartwatches & other wearable devices are some of the examples. Such miniature devices will further drive the demand for electronic devices and in return will boost the demand for the Electronic Adhesives Market as they are used in manufacturing these devices.

Introduction of 5G Network

Introduction 5G networks are planned to increase mobile broadband speeds and added capability for 4K/8K video streaming, virtual reality (VR) or augmented reality (AR), Internet of Things (IoT), and mission-critical applications. Introduction of 5G will boost the telecommunication industry, with better coverage, and internet speed, which also create a demand for Electronic Adhesives Market as they are used in manufacturing telecom devices. 5G will transmit data ten times faster than 4G and is set to take hold in 2020. This will spark a revolution in many industries such as electronic, energy, medical, automotive, defense, aerospace and others, which will boost the market's growth. 5G will impact the viewing experience for consumer, with its VR & AR which will further boost the demand for consumer electronic industry, which in return will boost the demand for electronic adhesive market.

Electronic Adhesive Market Challenges

Technological Changes & VOC Emission

The market is facing challenges due to technological changes. Shorter leads can damage temperature-delicate components in several applications and to overcome such obstacles electrical components should be assembled after soldering. However, this hampers productivity due to higher costs of production and time consumed in the manufacturing process. Growing concern over the emission of volatile organic compounds (VOCs) is expected to hamper the market growth over the coming years. During the manufacturing of electronics adhesives, VOC is discharged that may pose health and environmental concerns. VOCs are the major contributors to smog and ozone formation at low atmospheric levels.

Emergence of COVID 19

The COVID-19 pandemic continues to unfold everyday with severe impact on people, communities, and businesses. And the Electronic Adhesives Market was no exceptional, as the global production facilities of the electronics, parts have been reduced due to the logistics slowdown and unavailability of the workers. Furthermore, various e-commerce sites had discontinued the delivery of non-essential items which included electronics devices, which affected the electronic industry.

Electronic Adhesive Market Landscape

Technology launches, acquisitions and R&D activities are key strategies adopted by players in the Electronic Adhesives Market. In 2020, the market of electronic adhesives has been consolidated by the top 10 players accounting for xx% of the share. Major players in the Electronic Adhesives Market are BASF SE, Panacol-Elosol GmbH, 3M Co., H.B. Fuller Co., Henkel AG & Co. KGaA, Hitachi, Ltd., Mitsui & Co., Ltd., Bostik, Inc., Chemence Inc., tesa SE, Parker Hannifin Corp., Meridian Adhesives Group, among others.

Acquisitions/Technology Launches

In November 2019, Bostik, Inc., announced it has launched a new range of innovative engineering adhesives Born2Bond™, for bonding applications in automotive, electronics, luxury packaging, and medical devices. With this new launch Bostik will not only expand its product portfolio but also expand it offering to various industries, which will further drive the market's growth.

In September 2020, Meridian Adhesives Group, a leading manufacturer of high-value adhesives technologies has announced that the “Company” would be serving the Electric Vehicles Market and provide its adhesive solution, with this announcement Meridian Adhesives would expand its product offering in automobile industry, which will further derive the market's growth.

Key Market Players:

The Top 5 companies in Electronic Adhesives Market are:

Panacol-Elosol GmbH

3M

H.B. Fuller Company

Henkel AG & Co.KGaA

Parker Hannifin Corp.

#Electronic Adhesives Market Size#Electronic Adhesives Market Trends#Electronic Adhesives Market Growth#Electronic Adhesives Market Forecast#Electronic Adhesives Market Revenue#Electronic Adhesives Market Vendors#Electronic Adhesives Market Share#Electronic Adhesives Market

0 notes

Text

Global Analysis: Copper Clad Laminate Market 2024 – Size & Key Drivers Revealed

The Copper Clad Laminate Global Market Report 2024 by The Business Research Company provides market overview across 60+ geographies in the seven regions - Asia-Pacific, Western Europe, Eastern Europe, North America, South America, the Middle East, and Africa, encompassing 27 major global industries. The report presents a comprehensive analysis over a ten-year historic period (2010-2021) and extends its insights into a ten-year forecast period (2023-2033). Learn More On The Copper Clad Laminate Market: https://www.thebusinessresearchcompany.com/report/copper-clad-laminate-global-market-report According to The Business Research Company’s Copper Clad Laminate Global Market Report 2024, The copper clad laminate market size has grown strongly in recent years. It will grow from $12.61 billion in 2023 to $13.64 billion in 2024 at a compound annual growth rate (CAGR) of 8.2%. The growth in the historic period can be attributed to electronics industry growth, increasing demand for lightweight and compact devices, telecommunications infrastructure expansion, growing automotive electronics sector, globalization of electronics manufacturing, increasing consumer electronics consumption. The copper clad laminate market size is expected to see strong growth in the next few years. It will grow to $18.3 billion in 2028 at a compound annual growth rate (CAGR) of 7.6%. The growth in the forecast period can be attributed to continued advancements in iot devices, flexible electronics and wearables market growth, increasing emphasis on environmental sustainability, shift towards high-frequency materials, supply chain resilience and regionalization. The increasing demand for automotive vehicles is expected to propel the growth of the copper clad laminate market going forward. An automotive vehicle refers to a self-propelled land vehicle, used for the movement of people or goods and does not run on rails (unlike trains or trams). Get A Free Sample Of The Report (Includes Graphs And Tables): https://www.thebusinessresearchcompany.com/sample.aspx?id=10083&type=smp The copper clad laminate market covered in this report is segmented – 1) By Type: Rigid Copper Clad Laminate, Flexible Copper Clad Laminate 2) By Material: Epoxy Resin, Phenolic, Other Materials 3) By End-User: Automotive, Aerospace And Defence, Consumer Electronics,, Healthcare, Industrial, Other End-Users Product innovations are the key trends gaining popularity in the copper clad laminate market. Companies operating in the copper-clad market are innovating new products to sustain their position in the market. The copper clad laminate market report table of contents includes: 1. Executive Summary 2. Market Characteristics 3. Market Trends And Strategies 4. Impact Of COVID-19 5. Market Size And Growth 6. Segmentation 7. Regional And Country Analysis . . . 27. Competitive Landscape And Company Profiles 28. Key Mergers And Acquisitions 29. Future Outlook and Potential Analysis Contact Us: The Business Research Company Europe: +44 207 1930 708 Asia: +91 88972 63534 Americas: +1 315 623 0293 Email: [email protected] Follow Us On: LinkedIn: https://in.linkedin.com/company/the-business-research-company Twitter: https://twitter.com/tbrc_info Facebook: https://www.facebook.com/TheBusinessResearchCompany YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ Blog: https://blog.tbrc.info/ Healthcare Blog: https://healthcareresearchreports.com/ Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model

0 notes

Text

Plastic Extruder

A plastic extruder is a device that uses molten plastic to push through a die and produce a continuous profile to produce a variety of plastic items. Extrusion is a prominent production technique in the plastics sector since it is both extremely effective and economical. The plastic is heated and melted, then mixed, shaped, cooled, and cut into the desired shape as part of the plastic extrusion process. Construction, agricultural, automotive, and packaging are just a few of the industries that employ plastic extruder machines due to their adaptability.

Types of Plastic Extruder

SJ Single Screw Extruder

Read More

SJ Single Screw Extruder

SJSZ Conical Twin Screw Extruder

Read More

SJSZ Conical Twin Screw Extruder

The Advantages of Using a Plastic Extruder in the Manufacturing Process

Construction Machinery Spare Parts Case

Elephant Fluid Power produces stirring motor BMH500 (replaces OMH500) of the same quality as the original, A11VLO, A4VG series plunger pumps, which are used for pump truck production, repair, maintenance and refurbishment, reducing sales and end-user production costs and increasing productive forces. Elephant Fluid Power has a fast delivery time, provides good technical support and after-sales service, and reduces customers' worries.

The Components of A Plastic Extruder and How They Work

A standard plastic extruder is made up of a hopper, a feeding system, a barrel, a screw, a die, and a cooling system, among other parts. Plastic pellets are put in the hopper to be fed into the extruder. The feeding mechanism regulates how quickly plastic enters the barrel. The barrel holds both the die, which shapes the molten plastic into a continuous contour, and the screw, which compresses and melts the plastic.

As the finished product emerges from the die, the cooling system chills and solidifies it. These elements combine to effectively generate a range of plastic items. The output and caliber of the finished product may be varied by changing the shape and speed of the screw.

The Materials Used with A Plastic Extruder

A plastic extruder can work with a wide variety of materials, including both thermoplastic and thermosetting materials. Thermoplastics, such as polyethylene (PE), polypropylene (PP), polystyrene (PS), and PVC, are widely used in extrusion due to their ability to be melted and cooled repeatedly without undergoing any chemical change or degradation. Thermosetting plastics, such as phenolic resins, epoxy resins, and melamine-formaldehyde, are used in the extrusion of electrical components and other specialized applications. Moreover, composite materials, including wood-plastic composites and thermoplastic elastomers, have been used extensively in the construction industry. Such versatility makes plastic extruders a cost-effective solution for manufacturing a broad range of products.

0 notes

Text

Corrosion Resistant Resin Market Key Players, Economic Impact and Forecast to 2030

The corrosion-resistant resin market refers to the use of synthetic polymers that are resistant to corrosion caused by chemicals, moisture, and other factors. These resins are commonly used in a variety of industries, including automotive, marine, aerospace, and construction.

Market Size and Growth

The global corrosion-resistant resin market is projected to reach USD 12.56 billion by 2022, growing at a CAGR of 4.6% from 2017 to 2022. The growth in this market is attributed to the increasing demand for corrosion-resistant resins in various end-use industries.

Types of Corrosion Resistant Resins

Epoxy Resins - Epoxy resins are widely used in industrial and marine applications due to their excellent chemical and corrosion resistance properties.

Vinyl Ester Resins - Vinyl ester resins are used in various applications such as tanks, pipes, and marine structures, due to their excellent resistance to harsh chemicals and high-temperature environments.

Polyester Resins - Polyester resins are commonly used in the construction industry due to their excellent strength and durability, as well as resistance to UV light and weathering.

Phenolic Resins - Phenolic resins are used in a variety of applications, including automotive and aerospace industries, due to their excellent resistance to heat, chemicals, and fire.

Applications

Automotive Industry - Corrosion-resistant resins are used in the automotive industry for the production of body panels, engine components, and other parts that are exposed to harsh environments.

Marine Industry - The marine industry uses corrosion-resistant resins in the production of boats, ships, and other marine structures that are exposed to saltwater and other harsh environments.

Aerospace Industry - Corrosion-resistant resins are used in the aerospace industry for the production of aircraft components, such as fuel tanks and engine parts.

Construction Industry - Corrosion-resistant resins are used in the construction industry for the production of pipes, tanks, and other structures that are exposed to harsh chemicals and environmental conditions.

Key Players

Some of the key players in the corrosion-resistant resin market include Ashland Inc., Huntsman Corporation, Hexion Inc., Olin Corporation, Reichhold LLC, Scott Bader Company Ltd., and Sika AG.

Conclusion

The corrosion-resistant resin market is growing due to the increasing demand for these materials in various end-use industries. Epoxy, vinyl ester, polyester, and phenolic resins are the most commonly used types of corrosion-resistant resins. The automotive, marine, aerospace, and construction industries are the major end-users of these resins.

#Corrosion Resistant Resin Market#Corrosion Resistant Resin Market Growth#Corrosion Resistant Resin Market Trends

0 notes

Link

0 notes

Link

Metallic Stearate are the compounds of long-chain fatty acids with metals of dissimilar valency’s and is formed by saponification reaction of stearic acid and calcium base. In terms of quantity, the most vital metallic stearates are zinc, aluminum, magnesium, and calcium. Some metallic stearates are not soluble in water. The Metallic Stearate Market is estimated to grow at a significant CAGR of 5.4% over the future period as the scope and its applications are rising enormously across the globe.

High demand from cosmetics & pharmaceutical manufacturers and growing demand for polyvinyl chloride and various other polymers like polyolefin, phenolic resins, and polystyrene that use metallic stearates in several types of processing are documented as major factors of Metallic Stearate Market that are estimated to enhance the growth in the years to come. However, issues related to the filterability of chemicals using metallic stearate and corrosion caused by addition of these stearates are the factors that may restrain overall market growth in coming years. Metallic Stearate Market is segmented based on type, forms, end users, and region.

1 note

·

View note

Link

The growth of the phenolic resin market is attributed to the growing automotive industry in the region. Increased demand for tires is also contributing to the growth of the market in the region. The adoption of nanotechnology and the growing need for fuel-efficient and lightweight vehicles offer a lucrative growth opportunity for phenolic resin manufacturers.

#Phenolic Resin Market#Phenolic Resin Industry#phenolic resin#Phenolic Resin Manufacturers#Phenolic Resin end users

0 notes

Text

Hydrogenated hydrocarbon resin (HHCR) Market is Projected to Reach USD Million by 2027, Growing at a CAGR of around 8%

According to BlueWeave Consulting, the global HHCR market worth USD 970 million in 2020, and is further projected to reach USD million by 2027, growing at a CAGR of around 8% during 2021-2027 (forecast period). Hydrogenated hydrocarbon resin (HHCR) market, also known as “WaterWhite”, is a hydrogenated product of several types of resins. Typically, C5, C9, DCPD, or C5/C9 resins are used as feedstock for the manufacturing of HHCR. Major applications of HHCR are adhesives, hot melt adhesives, paints, and coatings, etc.

Adhesives and sealants market is likely to grow with the highest CAGR and drive the market for hydrogenated hydrocarbon resins (HHCR).

HHCR is used in many industries, such as – Paints and coating, tackifiers, hot melt adhesives, rubber compounding, etc. One of the major areas of application for HHCR is the production of heat and cold resistive tackifiers. HHCR tackifiers have great adhesive strength with enhanced resistivity against cold and heat. When HHCR is added to a bipolar film, it’s transparency, rigidity, and vapour barrier properties get enhanced. Waterwhite (HHCR) is also used to produce hot melt adhesive hygiene products.

Requirement of extreme conditions for hydrogenation of hydrocarbons will affect the market growth negatively.

The hydrogenation reaction of hydrocarbons does not take place under normal conditions. Extreme conditions (HPHT – high pressure, high temperature) are required for the hydrogenation process. For generating such conditions, a special type of reactors is required. A lot of capital investment is necessary to acquire such reactors. Small companies, without the security of large funds to back them, are likely to move away from investing big. A specific type of catalyst is used for the products with specific properties. The Companies, buying catalysts from other companies will again have to invest big for getting such a catalyst, and it’ll affect the market negatively.

C5-HHCR was leading the market in recent years and will drive the market again in the forecast period.

Hydrogenated hydrocarbon resins have 3 different grades, C5-HHCR, C9-HHCR, and DCPD-HHCR. C5-HHCR had the highest share of the market in recent years and is likely to maintain the same in the upcoming years. C5-HHCR is more cost-friendly compared to C9 and DCPD HHCR. C5-HHCR has enhanced thermal and water resistivity, high color stability, enhanced UV-protection, and have more adhesive strength compared to C5-HCR. C5-HHCR is also highly compatible with elastomers and base resins.

Global HHCR Market: Regional insights

The global market for HHCR is divided into Asia Pacific, Europe, North America, South America, and the Middle East. Asia Pacific region is likely to witness the highest growth rate for the HHCR market owing to its rapidly developing countries, high demand for end-user industry products, ever-improving lifestyles, and presence of many automotive and construction businesses in the region. The increasing demand for hygiene products in South Asia is likely to contribute to the growth of the HHCR market in Asia-pacific.

Report URL: https://www.blueweaveconsulting.com/global-hhcr-market

North America is projected to follow the lead of Asia-Pacific, with high income, great business opportunities, and the availability of a highly-skilled workforce.

Global HHCR Market: Competitive Landscape

The leading players for the global HHCR market include Axis Chemicals Pty Ltd, Commonwealth Laminating & Coating Inc, Credrez, Dycon Chemicals, BASF, Dow Chemicals, Henghe Petrochemical Co., Ltd, Shandong ShenxianRuisen Petroleum Resins Co., Ltd, Resin Chemicals Co. Ltd, SGL Carbon, Solutia Inc., Sumitomo Chemicals, Ineos Phenol, ExxonMobil, Rain carbon, Zeon Corporation, Idemitsu, Puyang Changyu Petroleum Resins, Lesco, Kolon Hydrocarbon, PuyangTiancheng Chemical Co. Ltd, Arakawa Chemical Industries, and others are expanding their presence in the market by implementing various business strategies. Major players are engaged in mergers and acquisitions, expansion of their manufacturing facilities, infrastructural growth, investment in R&D facilities, and the quest for opportunities to expand vertically through the value chain.

Don’t miss the business opportunity of the HHCR Resin market. Consult our analyst, gain crucial insights, and facilitate your business growth.

The in-depth analysis of the report provides information about growth potential, upcoming trends, and statistics of global HHCR Resin market size & forecast. The report promises to provide recent technology trends of the HHCR Resin market and industry insights that help decision-makers to make sound strategic decisions. Furthermore, the report also analyzes the growth drivers, challenges, and competitive dynamics of the market.

About Us

BlueWeave Consulting provides all kinds of Market Intelligence (MI) Solutions to businesses regarding various products and services online & offline. We offer comprehensive market research reports by analyzing both qualitative and quantitative data to boost up the performance of your business solution. BWC has built its reputation from the scratches by delivering quality inputs and nourishing long-lasting relationships with its clients. We are one of the promising digital MI solutions company providing agile assistance to make your business endeavors successful.

#Hydrogenated hydrocarbon resin (HHCR) Market#Hydrogenated hydrocarbon resin (HHCR) Market Size#Hydrogenated hydrocarbon resin (HHCR) Market Share#Hydrogenated hydrocarbon resin (HHCR) Market Forecast#Hydrogenated hydrocarbon resin (HHCR) Market Demand#Hydrogenated hydrocarbon resin (HHCR) Market Analysis#Hydrogenated hydrocarbon resin (HHCR) Market Report

1 note

·

View note

Text

Bisphenol A Price | Prices | Pricing | News | Database | Chart

Bisphenol A, commonly known as BPA, is a chemical compound primarily used in the production of polycarbonate plastics and epoxy resins. These materials are widely used in a range of industries, including automotive, electronics, packaging, and construction. As demand for these products fluctuates, so too does the price of BPA. Recently, global BPA prices have been experiencing notable volatility due to various market factors, such as raw material costs, supply chain constraints, regulatory pressures, and shifts in consumer preferences.

The price of BPA is largely influenced by the cost of its raw materials, particularly phenol and acetone. These chemicals are derived from petroleum products, meaning that BPA prices are closely tied to fluctuations in crude oil markets. When crude oil prices rise, the cost of producing BPA also increases, which in turn impacts its market price. Conversely, when oil prices drop, the cost of BPA production becomes cheaper, leading to potential decreases in its price. Additionally, the availability and price of natural gas, which is also involved in the chemical production process, can affect BPA costs. In recent years, global geopolitical tensions and the OPEC+ group’s decisions have caused frequent swings in oil prices, resulting in corresponding shifts in BPA prices.

Get Real Time Prices for Bisphenol A: https://www.chemanalyst.com/Pricing-data/bisphenol-a-29

Another significant factor affecting BPA prices is supply chain disruptions. The COVID-19 pandemic had a profound impact on global supply chains, with lockdowns, labor shortages, and transportation challenges creating bottlenecks across industries. The chemical sector was no exception. With production facilities facing disruptions, many BPA manufacturers struggled to maintain consistent output, leading to reduced supply in the market. The resulting supply-demand imbalance caused BPA prices to spike during certain periods. Even as the global economy has recovered, supply chains continue to face challenges, particularly in the wake of the Russia-Ukraine conflict and other geopolitical events that have further complicated the movement of goods.

In addition to supply chain issues, regulatory pressures are increasingly playing a role in shaping BPA prices. Over the past decade, growing concerns about the health risks associated with BPA exposure have led to stricter regulations and bans in certain regions. BPA is considered an endocrine disruptor, and studies have linked it to various health issues, including reproductive disorders, heart disease, and developmental problems in children. As a result, many countries, particularly in Europe, have imposed restrictions on its use in consumer products, particularly those that come into contact with food and beverages. The European Union, for instance, has implemented stringent limits on BPA in food contact materials, which has forced manufacturers to explore alternative chemicals or production methods. These regulatory hurdles have added to production costs, which can translate into higher BPA prices for end-users.

Consumer sentiment also plays an important role in the pricing of BPA. As public awareness of the potential health risks of BPA grows, more companies are seeking BPA-free alternatives in response to consumer demand. This shift is particularly evident in the packaging and food storage industries, where there is a growing trend toward BPA-free plastics. While this reduces demand for BPA in certain sectors, it has also driven up prices in others. For example, in industries where alternatives to BPA are not yet widely available, the continued reliance on BPA can lead to price increases as supply contracts. Moreover, the development of BPA substitutes has introduced additional competition in the market, creating price disparities between regions that have more readily adopted alternatives and those that continue to use BPA.

On the production side, advancements in technology and changes in manufacturing efficiency have also influenced BPA pricing. In some regions, manufacturers have invested in modernizing their production facilities, allowing them to produce BPA at a lower cost per unit. This has helped stabilize prices in markets where competition is high and producers are looking to maintain profitability despite downward pressure on prices. However, in areas where production technology has not advanced at the same pace, costs remain higher, resulting in regional price variations.

Environmental concerns are another emerging factor in the BPA market. With the global push toward sustainability and reducing carbon emissions, the chemical industry is under increasing scrutiny. BPA production, like many industrial processes, has a significant environmental impact due to the energy-intensive nature of chemical synthesis and the reliance on fossil fuels. As governments and companies introduce carbon taxes and other environmental regulations, manufacturers may face increased costs associated with making their operations more sustainable. These costs are often passed on to consumers in the form of higher prices.

Furthermore, the market for BPA is subject to the general principles of supply and demand. When demand for BPA-containing products, such as electronics, automotive components, and packaging materials, increases, manufacturers must ramp up production to meet market needs. This often leads to higher prices when supply cannot keep pace with rising demand. On the other hand, periods of decreased demand, perhaps due to economic downturns or changing consumer behavior, can lead to a reduction in BPA prices as producers seek to offload excess inventory.

BPA prices are also impacted by the regional distribution of production facilities. Asia, particularly China, is one of the largest producers and consumers of BPA, given its dominant role in global manufacturing. As a result, the Asian market can exert considerable influence over global BPA pricing. If production is disrupted in key regions, such as through government restrictions, natural disasters, or logistical challenges, this can lead to global price fluctuations. Conversely, increases in production capacity in these regions can help moderate price increases by boosting supply.

In conclusion, the price of Bisphenol A is influenced by a complex interplay of factors, including raw material costs, supply chain dynamics, regulatory pressures, consumer demand shifts, technological advancements, and environmental concerns. The volatile nature of the chemical industry, combined with the global economic landscape, makes it difficult to predict future price trends with certainty. However, by keeping a close eye on these variables, industry stakeholders can better navigate the market and make informed decisions regarding BPA procurement and production.

Get Real Time Prices for Bisphenol A: https://www.chemanalyst.com/Pricing-data/bisphenol-a-29

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Bisphenol A#Bisphenol A Price#Bisphenol A Prices#Bisphenol A Pricing#Bisphenol A News#Bisphenol A Price Monitor#Bisphenol A Database

0 notes

Text

The best cuttinGboard

Let's face it: a cutting board is not the sexiest utensil in your kitchen. It's not shiny, it doesn't turn, flash, or beep. In fact, it doesn't perform any high-tech hijinks at all. It just sits there. Still, a high-quality cutting board is an essential culinary tool. The preparation of many foods and meals requires that you use one. In addition, a high-quality cutting board can help keep you and your family healthy by preventing foodborne illness. Some of them are even beautiful to display on your kitchen counter.

Most experts agree that you should have a minimum of two cutting boards: one for cutting raw meats and one for chopping raw vegetables and everything else. There are cutting boards made from a variety of materials, but according to experts, including those at and plastic and wood are best for most kitchens. You can also get glass ones, but they are prone to shattering and they dull your knives quickly.

Pros and cons: Plastic cutting boards

One of the main benefits of using a plastic cutting board is that it is easier to clean. In most cases, it can be run through the dishwasher. That said, all plastic boards scar over time and deep knife gouges can eventually become home to dangerous bacteria that is difficult to remove.

A study from the , found that plastic cutting boards actually had more bacteria than their wooden counterparts. In addition, wooden cutting boards fared better than plastic ones when exposed to toxic bacteria strains like Salmonella, E.coli, and Listeria.

Plastic also tends to be rougher on your knives than wood. Still, plastic is very durable, affordable, requires almost no maintenance, and if you throw out your plastic boards after two years of use, plastic can be an excellent option.

Most plastic cutting boards are made of polyethylene or polypropylene. Cutting mats are also a popular option. They are made of flexible silicone or other softer plastics and they typically come in sets of three or four in a variety of bright colors. The idea is that you use one color for meat, one for veggies, and so on.

Pros and cons: Wooden cutting boards

Wooden cutting boards look gorgeous and you can get them in tons of different styles, shapes, and wood grains. Cutting boards are made from pecan, walnut, teak, and cherry, but by far the most popular type of wood is maple. Why? Maple is a beautiful light wood, it is strong, sustainable, and abundant in North America.Wood boards are also heavier and feel good to use. They also won't dull your knives much, either. Still, wooden cutting boards require much more maintenance than plastic ones. They must be washed and dried carefully after each use and oiled regularly.

Wooden cutting boards come in two versions: end grain boards and edge grain boards. End grain boards are the more expensive option of the two. They're made of several board ends glued together. They tend to be more gentle on knives, but more susceptible to drying out, staining, and cracking. Meanwhile, edge grain boards are easier to clean, but they tend to be harder on knife edges than end grain boards. However, they withstand moisture-based cracking and splitting better.

Pros and cons: Bamboo and composite cutting boards

Bamboo cutting boards are another popular option. Many people think bamboo is a wood, but it's actually a grass. Like wood, it has a porous surface, but it's even harder than wood. Bamboo cutting boards are attractive, lightweight, and affordable. This good-looking material is also an excellent choice for eco-conscious consumers because bamboo is a highly renewable resource - a typical bamboo shoot can become fully mature within three to six years - and is often raised organically due to the ease of farming it. Bamboo cutting boards also need to be oiled on a regular basis, according to

You can also opt for a composite cutting board, which is made from a combination of wood fibers and phenolic resins. Epicurean is the most popular brand name in composite cutting boards. Food-safe, long-lasting, and incredibly durable, composite cutting boards, unfortunately, do a number on your knives.

Other things to look for in a cutting board

According to , you should also consider the size of cutting board you need, how you're going to use it, and whether you need more than one to do the job.

Some cutting boards have features that make it easier to cut and serve meat. For instance, some models have raised pyramid points that puncture that meat to hold it securely, while others have an indentation in the center of the board where the meat can sit securely. A board with handles can also make it easier to transport the meat to the table.

If you'll be using the board for cutting meat, you may opt for a model with a generous juice trench around the board's perimeter. The trench should be deep and wide enough to catch the juice without having it drain onto the countertop. Some juice trenches feature a notch on the rim that serves as a pouring spout.

Many cutting boards are reversible, allowing you to use both sides and to prevent cross contamination. Some experts claim this is the best reason to select a board without feet, although others like the extra stability that feet provide. But there's an easy way to ensure that your board doesn't slip around the counter: simply wet a paper towel and insert it under the board.

With all that in mind, here are our picks for the best cutting boards. We've included a plastic option, a high-end solid wood one, a pack of cutting mats, a bamboo board set, and a stunning teak wood cutting board.

Here are the best cutting boards you can buy:

Find all the best offers at Disclosure: This post is brought to you by the team. We highlight products and services you might find interesting. If you buy them, we get a small share of the revenue from the sale from our commerce partners. We frequently receive products free of charge from manufacturers to test. This does not drive our decision as to whether or not a product is featured or recommended. We operate independently from our advertising sales team. We welcome your

The best cutting board overall

The plastic board is the darling of kitchen appliance and utensil reviewers everywhere. The 14.5 x 21-inch double-sided cutting board helps prevent cross contamination. Use the side with a juice groove for carving meat, and then simply flip it over to chop vegetables on the other side. Soft, tapered handles make the board easy to maneuver, and non-slip edges keep the board from shifting during use.

Made of durable polypropylene, the non-porous surface is odor-resistant and doesn't scratch as easily as other plastic materials. It won't dull sharp knives quickly, either. To top it all off, this cutting board is dishwasher safe.

The OXO cutting board gets consistent praise on Amazon for being durable and not absorbing odors or colors from pungent foods like onions and garlic.

"I love this cutting board. It doesn't slide around or bounce during use. It's very durable, gentle on my knives, and easy to clean. It's nicely weighted — heavy enough to stay in place, but light enough to lift and maneuver easily (when tipping ingredients into a bowl or hand washing in small sinks)" wrote one verified Amazon buyer on February 12, 2017.

Some Amazon users complain that the board warps in the dishwasher. Other users say they want to avoid this fate so they happily hand-wash the board with warm, soapy water. Other negative reviewers remark that the surface gets gouged too easily by any kind of knife, but that is a common occurrence for plastic cutting boards.

Across the web, professional reviewers, including thos, and many more name the OXO Good Grips Cutting and Carving Board as one of the best cutting boards on the market.

Pros: Great value, double-sided board prevents cross-contamination, juice groove, easy to clean, durable plastic, lightweight and easy to maneuver, doesn't dull knives

Cons: Users note that it sometimes warps in the dishwasher

The best high-end wood cutting board

The is a work of art made out of solid wood. The name John Boos is synonymous with high-quaity wood cutting boards and butcher blocks. In fact, by the 1940s, John Boos butcher blocks were found in almost every restaurant and butcher shop in the country. Rumor has it that are the standard in the White House.

This reversible cutting board is part of the esteemed Boos RA collection, which is known for its beautiful edge grain construction. The John Boos board is much thicker than many other cutting boards on the market, coming in at 2.25-inches thick. This heavy board weighs in at 27.5 pounds, so it won't slip or slide around the kitchen counter as you chop away. It's so gorgeous that you can even leave it on your kitchen counter permanently.

The RA03 features a hard maple edge grain construction with a cream finish, two flat sides, and slightly rounded edges. In addition, inset handles make it easy to move and rotate the board or to flip it to the reverse side. The cutting board comes with a one year warranty.

After using, this cutting board should be washed by hand in warm soapy water and dried immediately. It requires oil treatment as frequently as once a week.

There are more than 380 user reviews on Amazon with an average rating of 4 out of 5 stars. "One of the best purchases I have ever made," wrote Tonya N. Phillips on July 23, 2016. "Love my cutting board. I use it pretty much every day."

"I have waited months to buy my first John Boos board and I am not disappointed … This is very well constructed and it came to me smooth as silk. No rough spots, very clean edges, and the hand slots are perfect for flipping the board over for a clean, sanitized spot … I love that it is made right here in the U.S.A.," wrote Donna S in February 2015.

Some Amazon users complain that the board started to crack very shortly after receiving it. Other reviewers jump in and remind everyone that you really do have to oil it on a weekly basis.

1 note

·

View note

Text

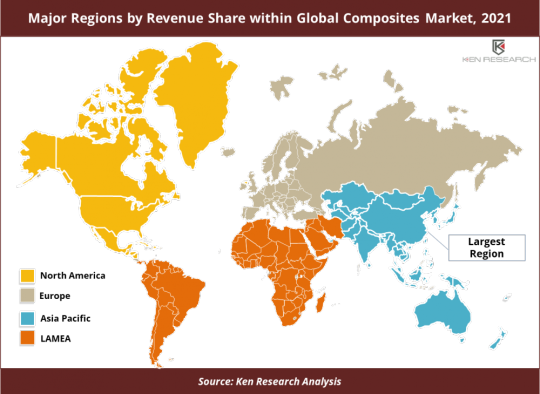

Global Composites Market is expected to record a positive CAGR of ~8% during the forecast period 2022-2028: Ken Research

Buy Now

A composite is created from two or more constituent materials. These constituent materials are combined to produce a substance with characteristics that are distinct from the constituent parts despite having chemical or physical qualities that are noticeably different. Composites are being increasingly adopted in different industries including electrical & electronics, automotive & transportation, wind energy, aerospace & defense, construction & infrastructure, and others.

According to Ken Research Analysis, the Global Composites Market is expected to record a positive CAGR of ~8% during the forecast period (2022-2028) and is expected to reach approximately US$ 120 billion by 2028.

The desirable performance of composites as well as the high adoption of composites in various end-user industries owing to their properties is positively impacting the market growth.

Customers' needs for a wide range of intricately engineered parts, design patterns, and structures are met through the use of composite materials. The product supports several sectors, including wind power, consumer goods, automotive, aerospace, and the maritime sector. Different materials are used in a variety of ways by these businesses. Regulations, consumer demand, cost criteria, and part performance requirements all influence this usage. For instance, there are significant differences between the materials, costs, and process technology used in the aerospace sector and the car industry. Due to their diversity, these materials can satisfy this wide range of demands. For instance, there are resins, a variety of fibers, equipment, process, and finishing options that can be used to fabricate almost any item for any application.

Concerns about improper disposal and recycling of composite products as well as the high production cost of composites limit the market growth.

Composites recycling and disposal raise problems that need to be resolved. One such problem relates to carbon fiber composites used in hexavalent chromium primer-coated end-of-life aircraft structures. Due to the possibility of the hexavalent chromium in these composites seeping into the ground, they may be categorized as hazardous waste and cannot be disposed of on land.

The COVID-19 outbreak had a huge impact on supply chains since key economies had to halt commerce. Additionally, the demand for composites had decreased across a range of end-use industries, including aerospace, automotive, and construction. However, the situation improved in 2021 due to the removal of trade barriers, which restored the market's growth trajectory.

Key Trends by Market Segment

By Fiber Type: The carbon fiber composites segment held the largest Market share in the Global Composites Market in 2021.

Carbon atoms are bonded in parallel crystals to create carbon fiber, which is then combined with other materials to create composites. Due to their beneficial characteristics, including high stiffness, low thermal expansion, good chemical resistance, high-temperature tolerance, and low weight, these fibers are used in industrial and manufacturing applications.

The strength and endurance of these Composites have been improved due to technical improvements, which have expanded their penetration in pipe production applications. The market is expected to be supported throughout the forecast period by rising demand for high-strength materials in the automotive and aerospace sectors.

By Resin Type: The thermoset composites resin type segment held the largest share of the Global Composites Market in 2021.

The significant growth in demand for thermoset composites in sectors of aerospace, transportation, and defense is boosting the market growth. Glass, carbon, and aramid fibers are the usual building blocks of thermoset composite, which is frequently mixed with resins such as epoxies, phenolics, vinyl esters, polyesters, cyanate esters, and polyimides.

By End-User: The automotive & transportation end-user segment held the largest share of the Global Composites Market in 2021.

Over the foreseeable term, this market segment is likely going to continue to lead. The transportation industry benefits from composites since the components are much lighter in weight, increasing fuel economy.

It is anticipated that rising consumer and industry demand for high-tech electronics would increase demand for composite materials. Terminal boxes, electrical enclosures, lamp housings, sockets, plugs, and parts for the distribution of energy are some of the electrical and electronics applications for composites that are most frequently used.

By Manufacturing Process: The layup process segment held the largest share of the Global Composites Market in 2021.

The layup method dominated the market and generated a sizeable portion of revenue when it came to the production of composites. Over the course of the forecast period, rising production of boats, wind turbine blades, and architectural moldings are anticipated to propel the growth of the layup process sector in the worldwide composites market.

Over the course of the projection period, rising output in the automotive and marine industries is anticipated to provide growth chances for the filament winding process. Golf club shafts, car drive shafts, tiny aircraft fuselages, spaceship structures, pressure vessels like firefighter oxygen canisters, and other products have all been made possible by improvements in the filament winding process.

Request for Sample Report @ https://www.kenresearch.com/sample-report.php?Frmdetails=NTk2MTA5

By Geography: Asia Pacific accounted for the largest market share in 2021 within the total Global Composites Market.

Historically, Japan, North America, and Europe dominated the glass fiber and carbon fiber composites market. However, there has been a noticeable trend in recent years toward the developing economies in Asia Pacific and the rest of the world.

For instance, the significant demand for low-cost carriers has raised the market for glass fiber and carbon fiber composites in the aircraft, wind energy, and transportation sectors in rising nations like India, Brazil, and China. China, whose rapid industrialization is anticipated to meet the growth in demand, has started several research projects involving glass fiber and carbon fiber composites.

Competitive Landscape

The Global Composites Market is highly competitive with ~500 players which include globally diversified players, regional players as well as a large number of country-niche players.

Large global players hold the highest market share of 45% which is followed by the regional players holding a 30% share. Some of the major players in the market include Huntsman Corporation LLC, SGL Group, Teijin Ltd., CooperVision, DuPont, Owens Corning, Toray Industries, Inc., Mitsubishi Chemical Holdings Corporation, Solvay, Exel Group, DOW, and others.

Recent Developments Related to Major and Emerging Companies

In September 2019, Solvay, at its USA facility in Anaheim, California, increased its capacity for thermoplastic composites by adding a new production line for meeting the strong demand growth from aerospace customers for this high-performance material and Solvay's proprietary and distinctive technology.

In July 2021, Hexcel, a leader in advanced composites technology, reported that a lightweight camera drone it built utilizing Hexcel HexPly carbon fiber prepregs completed its first flight. A group of students from the University of Applied Sciences Upper Austria in Wels created the composite drone using components provided by Hexcel Neumarkt in Austria.

In September 2019, the acquisition of Ashland Global Holdings Inc.'s composites business by INEOS Enterprises had been announced. A BDO office in Germany is also part of the acquisition. The companies involved in the transaction generate more than US$1.1 billion in annual sales. Over 19 locations in Europe, North and South America, Asia, and the Middle East, have 1,250 employees.

Key Topics Covered in the Report

Snapshot of the Global Composites Market

Industry Value Chain and Ecosystem Analysis

Market size and Segmentation of the Global Composites Market

Historic Growth of the Overall Global Composites Market and Segments

Competition Scenario of the Market and Key Developments of Competitors

Porter’s 5 Forces Analysis of the Global Composites Market

Overview, Product Offerings, and SWOT Analysis of Key Competitors

COVID-19 Impact on the Overall Global Composites Market

Future Market Forecast and Growth Rates of the Total Global Composites Market and by Segments

Market Size of Fiber Type / End User Segments with Historical CAGR and Future Forecasts

Analysis of the Composites Market in Major Regions

Major Production / Consumption Hubs in the Major Regions

Major Country-wise Historic and Future Market Growth Rates of the Total Market and Segments

Overview of Notable Emerging Competitor Companies within Each Major Country

For more insights on the market intelligence, refer to the link below: –

3 Key Insights on US$ 120 Bn Opportunity in the Global Composites Market: Ken Research

0 notes

Text

Methanol Market is Expected to be Worth US$72.9 Bn by 2029 from US$44.4 Bn in 2021

Predominantly driven by a wide range of end-use industries that consume methanol as a versatile feedstock, methanol continues to witness sustained demand worldwide. The key industries majorly include pharmaceuticals, plastics, paints and adhesives, resins, plywood, foams, perfumes, and explosives, suggests the latest report released by Fairfield Market Research. The report further estimates that the methanol market size that was around US$44.4 Bn in the year 2021 will most likely experience around 1.4x expansion toward the end of 2029. By the end of the assessment period, the market size will reach a whopping US$72.9 Bn.

There has been a growing perception about methanol as a clean burning potential fuel alternative to conventional gasoline over the recent past. This according to the report will drive the growth of methanol market ahead. As the consideration of methanol as a potentially efficient, safer, and economically viable alternative to conventional marine fuels will grow across the various parts of the world, methanol market will successfully maintain its steady momentum in the long run. Though steady, the market has been slated for a promising CAGR of 4.7% over 2022 – 2029. Coal will continue to be the most preferred feedstock for methanol production, and energy & MTO applications are likely to remain at the forefront in methanol consumption. Escalating demand for methanol in energy-related application areas such as biodiesel, fuel blending, DME, and MTBE/TAME will significantly shape market in future.

For More Industry Insights Read: https://www.fairfieldmarketresearch.com/report/methanol-market

Formaldehyde Bestseller, Coal Preferred Feedstock in Methanol Market

The report reveals that the demand for formaldehyde continues to see an upswing owing to stable demand growth across key areas of application, including automotive, paints and adhesives, textile, plywood, plastics, pesticides, personal care, and construction. Formaldehyde will continue to surge ahead with more than a fifth of the overall market valuation throughout the end of forecast period. Attributing to a growing perception of formaldehyde as an ideal blended fuel candidate, it is more likely to garner greater attention in future. The report further marks that the production of melamine-, urea-, and phenol formaldehyde resins will remain responsible for nearly 70% of methanol consumption. Feedstock-wise analysis of the market uncovers the fact that the cost-competitive feedstock will remain preferred among end users. In 2021, coal recorded to be the most preferred feedstock with more than 65% share in methanol market. In terms of application, methanol consumption is projected to be the maximum for energy & MTO applications, which accounts for more than 60% share in methanol market.

China Maintains Lead in Global Methanol Market

The report marks that the market in the US will witness growth on account of the automotive applications. The dynamic housing activity across the nations will further boost the methanol market revenue here. Growing potential application in biodiesel production is also projected to bolster methanol market across the US. On the other hand, China has been capturing the top position in global chemicals industry. While the nation continues to witness rampant rise in the number of new chemical manufacturing plants, the report expects China to retain the top spot in global methanol market as well. The country’s excellent mineral turpentine oil (MTO) oil is likely to remain the key driving force for China to continue serving as the mainstay for the entire northeast Asia’s methanol market landscape. The market here will especially thrive on the back of sustained light olefins production, growing MTO/CTO units, and energy application.

Key Market Players

Methanex Corporation, Proman AG, SABIC, Yankuang Group, Zagros Petrochemical Co., OCI, BASF SE, Celanese Corporation, Sarawak Petchem Sdn. Bhd., Mitsubishi Chemicals, Mitsui & Co., Ltd., Petroliam Nasional Berhad (Petronas), US Methanol, Yankuang Group, Carribean Gas Chemical, Methanol Holdings Limited, Velro Energy Corp., Natgasoline LLC

For More Information Visit: https://www.fairfieldmarketresearch.com/report/methanol-market

About Us

Fairfield Market Research is a UK-based market research provider. Fairfield offers a wide spectrum of services, ranging from customized reports to consulting solutions. With a strong European footprint, Fairfield operates globally and helps businesses navigate through business cycles, with quick responses and multi-pronged approaches. The company values an eye for insightful take on global matters, ably backed by a team of exceptionally experienced researchers. With a strong repository of syndicated market research reports that are continuously published & updated to ensure the ever-changing needs of customers are met with absolute promptness.

#methanol#methanol market#methanol market trends#methanol market size#methanol market share#methanol market demand#methanol market growth#methanol market analysis#chemical industry#fairfield market research

0 notes

Text

Formaldehyde Market Outlook, Growth, Share and Forecast by 2028

Formaldehyde Industry Overview

The global formaldehyde market size was valued at USD 7.81 billion in 2020 and is expected to expand at a compound annual growth rate (CAGR) of 5.7% from 2021 to 2028.