#Old Mutual Actuarial

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

130K people were victims of a chain letter scam that affected Tumblr in May 2011.

Text

Company Insurance Solutions

Have a stress-free trip, shield you and your belongings with coverage from our Travel Insurance associate. Comprehensive Insurance policy that's trouble free and designed to provide you peace of thoughts and worth underwriting insurance companies for money. The Municipal facility supplies insurance capacity for the Municipal sector within South Africa. Specialist liability insurance tailor-made to suit your shoppers wants.

We present insurance companies to personal, commercial and company purchasers in South Africa. We even have operations in Namibia, Botswana, Zimbabwe and Nigeria under the Old Mutual model. IFRS 17, efficient from 1 January 2023, will be a significant challenge for the insurance business, essentially impacting companies properly beyond the finance, actuarial and systems improvement underwriters areas. This extends to areas like product design and distribution, improvement of revised incentive and wider remuneration policies and reconfigured budgeting and forecasting methodologies feeding into enterprise planning. Furthermore, The Insurance Crime Bureau additionally offers a platform for the general public to safely and anonymously report fraudulent actions or suspected insurance crimes via the toll-free Insurance Fraudline.

I’m really proud of the service I received from King Price and Cecilia Ncwane. This covers minor repairs to the outside of your car… Like those mysterious little dings that occur in parking heaps, and people annoying spots of tar that stick like superglue. Our royal automobile warranty insurance ensures that car components that break unexpectedly, are repaired or changed underwriting insurance... So that your car’s back on the street swiftly, and without damaging your financial institution balance. Learn moreYou see, because your car’s worth starts happening the moment you drive away from the dealership, we just think it is smart to pay much less to insure it every month!

That adjustment doesn't quantity to an oblique and legally incompetent award of curiosity on damages as defendant's counsel sought at one stage to counsel. Factually the evidence proves that plaintiff has indeed suffered loss in respect of the diminished shopping for power of the rands he would have earned uninjured. The allowance made by Mr Koch for increased earnings through sa insurance the period, even assuming that such increases were prompted or necessitated by inflation-related issues, do not serve to eradicate that loss of shopping for power. The allowance for increased earnings is merely one of the components utilized in arriving at the variety of rands lost.

Employee advantages, investments and savings, medical help, and high risk management. With more than 50 years of insurance expertise and lots of tens of millions of travellers served, Chubb Travel Insurance provides high-quality insurance to South African travellers. We have plan choices for all types of travellers, from frequent flyers and households, to holidaymakers on a price range. AA AutoFacts supplies you with data-driven analytics, market insights, and automobile information.

0 notes

Text

i was tagged by @fatiguedvulcan

rules: answer 17 questions and tag 17 people you want to get to know better!

nickname: mak is technically a nickname, but it’s the name i go by most of the time. i’ve got about a billion of them though: kenz, kenzi, kenzaroo, kenzarooni, macaroni, macintosh, etc etc etc. i also have a friend that calls me umbrella because i told him i’d respond to just about anything and that’s what stuck

zodiac sign: taurus (both sun and moon, which my friends who are into astrology blame every facet of my personality on)

height: 5′4 (that’s about 162 cm i think?)

hogwarts house: slytherin

last thing i googled: return on assets ratio (i was doing my financial accounting homework)

song stuck in my head: obsession (rac mix) by vice and jon bellion but also through the valley by shawn james (these have v e r y different vibes lmao)

following: 706 (i’ve been on tumblr for like six years and like twenty hyperfixations shoutout to the people i’ve been following since 2014 when i was a pjo blog)

followers: 255

amount i sleep: usually about 8 hours. if i get less than seven i am very much not pleasant to be around

lucky numbers: 16, 42

dream job: ????? i’ll probably go into consulting or data science???? but i don’t have any concrete idea. i wanted to be an actuary for like four years but then i had a breakdown like a year ago so we’re not doing that anymore lmao

currently wearing: a 2019 backstreet boys long sleeve tour shirt (fantastic concert, by the way) tucked into these (cuffed) black jeans that have men’s sized pockets!!!! even though they’re women’s jeans but also like weird random seams down the front of my leg. also corgi socks

favorite songs: this literally changes like every three days??? but some songs that always Hit Different™ or will always be important to me/close to my heart are work song by hozier, honeybee by steam powered giraffe, and disloyal order of water buffaloes by fall out boy. lately i’ve been listening to valerie by amy winehouse pretty often

favorite instrument: i played viola for like eight years so definitely the viola bc im partial

random fact about me: i was like. super into the mighty morphin power rangers as a kid b/c my oldest brother was born in 1990 and i got all his hand me down toys and stuff. like so into power rangers that i burned out my vhs tape of the mighty morphin power rangers movie at like five years old and all of my childhood imaginary friends were power rangers. anyway i was super excited when the 2017 movie came out (i saw it in theaters twice) and a friend of mine who worked at the movie theaters at the time took the pink power ranger promotional cutout when they took the decorations down and brought it to school and gave it to me so now i have a six foot tall cardboard cutout of the pink power ranger just vibing in my room

favorite authors: rick riordan will always hold a special place in my heart honestly. but i’m also a big fan of fitzgerald

i tag: i’m always really bad at tagging people in these but i got a few new trek mutuals recently so i tag @kirkmcoy, @plaidshirtjimkirk, @aoskirk, and @mikes-wheelers if y’all want to do this/haven’t done it yet (this isn’t anywhere close to 17 oops---also if anyone else following me wants to do this please do it and tag me in it because i love reading these and learning new things about people!!!!!!!!!!!!!)

7 notes

·

View notes

Text

Old Mutual Actuarial Bursary South Africa 2019 – 2020

Old Mutual Actuarial Bursary South Africa 2019 – 2020

Download Old Mutual Actuarial Bursary 2019 – 2020 application form here. See how to apply, eligibility condition, how to contact Old Mutual Actuarial Bursary South Africa.

ABOUT THE COMPANY – OLD MUTUAL Old Mutual was founded in 1845 in Cape Town, South Africa, as the countries first mutual life insurance provider. Today, the company offers banking; savings; investment; asset management; life…

View On WordPress

#Old Mutual Actuarial#Old Mutual Actuarial Bursary#Old Mutual Actuarial Bursary South Africa#Old Mutual Actuarial Bursary South Africa 2019#Old Mutual Actuarial Bursary South Africa 2020

0 notes

Text

Sometimes, the only breaks he got in his day were waiting for the elevator and otherwise standing still while brushing his teeth. Ever since he and Christine had gone in on their vagabond pact to keep one another sane with their beginner’s contracts at Metro General, it had been a long, hard squeeze to even find time to wave at one another let alone keep tabs on mutual sanity. Which was probably why Christine’s roots were seven months grown-out with no signs of a single shit being given, and Stephen’s hair now required him to own hair ties, with much the same symptoms. The states of their hair was better than the idiots who wore ties during clinic hours, at least in his book, which was why he was willing to let it ride until his research grant proposal hopefully went through in June.

Between now and June, he still owed Christine a pot of Turkish coffee and a good long talk, which they were finally going to get now that they had a consecutive day off. Which would probably also involve some sex, and more importantly, a nap and cuddling afterward. He had the coffee, cream, and her favorite piloncillo in his pre-med textbook-worn satchel as he waited, watching through increasingly bleary eyes as the elevator laboriously trundled up to the sixth floor. He’d had to go to a Colombian-owned bodega three blocks away for the panela, but knew Christine would appreciate the treat. Her early residency roommates, a brilliant lesbian history PhD from Bogotá and a painfully mellow Lebanese economist, had given her the best worst coffee habit ever: Turkish style coffee laced with cardamom and served with cane sugar and milk. Stephen only even indulged the habit because she’d gotten him addicted to it too.

Though at his old broom closet down in Flushing he’d had a street view, his new place was sorely lacking in that department. Served him right for settling for the price - Metro View his ass. All he got was a great look-out over the corner of a taller apartment complex and the north-east bodega rooftops with their mangy pigeons and leathery, sunbathing retirees. Still, it was closer to Metro General than his fleabag flat down in Flushing had been, and slightly less depressing regarding his overall life prospects, even if the walls were still depressingly thin. He and Christine had made a game out of answering the Jeopardy questions to each other that they could hear playing on his actuary neighbor’s TV.

At four in the morning, however, he was too tired to even be thinking more than surface thoughts about lovely Christine, her stupid coffee recipe, the fact that the Colombian bodega had even been open, or his shitty apartment with its shitty view. All he wanted was to put his crap away, haul himself out of his clothes, and suffer Bruce, the most silent and judging mottled black Siamese he’d ever met but now couldn’t live without, walking viciously over his comatose face for the next eight hours.

Opening his doors to the lights already on and someone stranger sitting on his couch with a lap full of his judgmental cat was not on that list. His satchel, having slumped down off of his surprise-sunken shoulders, thumped to the floor, though he didn’t hear the cream give a telltale pop-and-gurgle, so he assumed it was probably fine. He kicked the door closed behind him, his hands already resting on hips like he found they did when he was talking to the even newer kid on the block in the ER. West? Wesley? Whatever. He was an idiot to the point that even Stephen had developed parenting instincts to keep his mistakes from killing someone. And that attitude seemed to very much apply to whatever this young guy wanted from... whatever he had in his flat.

Though he would not be leaving with his cat, that was for damn sure.

“What, pardon my French, the fuck are you doing in my apartment?” He looked down at his watch, the old manual field watch his grandfather had given him, hoping the wind hadn’t run down while he was at work. Small blessings, it was still ticking away. “At 4:43 in the morning, rather than wherever you’re actually supposed to be? Which isn’t here, snuggling with my cat, I might add,” he said, his brow raised as he waited for the undoubtedly colorful response.

( @frostkinglaufeyson )

5 notes

·

View notes

Text

boyfriend!au shownu

you were working as a part-time barista at a small cafe near your uni

because you were always broke as hell and the financial aid was not enough

also you did not want to burden your parents to cover your monthly expenses

studying + working + extra curricular activities took up a lot of your time that you never even had a crush on a guy eVER

like sure that one guy in programming is fine but you knew you were wayyyy out of his leaugue

your friends set up different blind dates to widen your dating experience but they never work out

like that one guy is okay but he never pay for any your meals and is conSTA NT Ly brOke and always trying to get on your nerves

the other guy was sO full of himself and that just disgusts you and never saw him ever again

but one day you sat there behind the counter and then you heard the bell rang and your head instantly moved to look at the door

and goddamn

what a hot guy

with muscular arms wearing a white shirt and some ripped jeans

with his bed head he sO CUte but also hOT like the duality

and he came straight to you and you words get twisted and got some lump up in the throat

“h-hi, h-how can i-i help y-you?”

he chuckled (tHAT CHUCKLE) and you felt that cupid arrow shot right on that spot on your heart

“one iced americano, please.”

and you took the cash with your trembling hands and he just look at you

“first day, i guess?”

and you’re like…………………….no//…………………………………..

and he’s like……………second day????

and you’re like no………………….probably 87th day………………………….

anyway he picked up the pager and went to sit at one of the tables and wait

and you immediately squealed and hide behind the counter and your coworker looked at you like “don’t tell me you don’t know who that is-”

your face were so blushed and you’re just like “JUST TELL ME WHO THAT IS”

“he’s shownu you dumbass, he goes to your uni and apparently the guy every girl is chasing after”

then you realised that he was just another guy out of your league

you got up and saw he was picking up his drink and when he was about to make his way out of the cafe you shouted “HAVE A NICE DAY”

he turned around and smiled and winked and your heart,,,,,,your pitiful heart,,,,,,the merciless wink…/.///..

and the very next day he kept coming back and that it became a daily routine and a necessity for him to come and get himself ‘the usual’

and you’re just like please have mercy on my weak heart don’t make me fall for you every single day and he just kept coming back everyday

and one day you were sick and had a day off and your coworker texted you “y/n!!!!!!!!!!!! the g OD shownu came looking for you”

so you squealed jumped screamed let out the biggest uwu ever then you’re like please don’t make this kind of joke

but she’s like i’m not kidding………………………

then the next day you came to work and HE CAME

he went like “you weren’t here yesterday”

and your heart went boom boom BOOM BOom MOVOVMDBEBJKA

“i was sick” then he gave you the cash as per usual but he slid a piece of paper between it and when you were counting the cash

you saw it and read the paper

“i’d like to get to know you better. meet me down the street when your shift is done tomorrow so that i’ll know the feeling is mutual”

you could’ve sworn your cheeks were the pinkest pink and he just smiled and said “get well soon”

and you looked over to your coworker like yOU DIDNT JUST TELL HIM WHEN MY SHIFT ENDS

and she’s like thank me later ok

so the next day you didn’t contemplate at all to meet him or not

but after your shift ends you and your coworker like fixed your hair and sprayed some mist and changed to your outfit (read: a shirt, a pair of jeans and converse)

and she’s like you knew you were going to meet him yet you dress so boring

but you just shook it off because it’s freaking 10 PM and you just gotta be yourself ladies ;)

so you grabbed your bag and nervously walked down the street to find him leaning over the lamp post while watching you walked over to him

and he flashed that smile and he’s just like i should introduce myself properly so he cleared his throat and lend out his hand for a handshake and goes “i’m shownu and i’m an actuarial science major”

hOL UP i thought you were into some PE shit or something but instead you took his hand into a handshake and just said “i’m y/n and i’m studying software engineering”

and you guys walked around the city playing 20 questions (but it was more than 20) to get to know each other and good lord you learned a lot about him

said his hobby is dancing and he was in a dance crew and entered a lot of underground dance battles and he wasn’t into sport that much just he likes to work out to be fit

and he looked at you with full awe and adoration

whenever you guys walked side to side your hand brushed with his and gave you a tingling sensation

the temptation to intertwine your hand with his is real

when it was almost 12AM he brought you to a diner where you guys shared a vanilla milkshake because you insisted that it was violating your diet but he’s just like you know you beautiful whatever size you are

and it was almost 1AM that both of you were back at the dorm where he showed you where to sneak into the uni compound without getting caught

and he’s like jump i’ll catch you but you were so scared to jump off that 5 ft wall but you jumped anyway

and he caught you and you both stared into each other’s eyes and just

you cleared up your throat and he put you down and he was just awkwardly scratching the back of his head

and you gave your phone to exchange numbers

and you guys said goodbye once again and he just pulled you closer and leave a kiss on your cheek and bring his lips to your ears and whispered looking forward to more dates

and he turned around and gave you a wink and he shouted “HAVE A NICE DAY”

so the months passed by and you guys went on a lot of d a t e s but one day he was waiting you at the iconic lamp post and he said “i’m going to do something and only react if you feel the same”

BOY hOL UP WHATCHA SAy-

he cupped your face and brought his face closer to yours and his eyes were staring at your lips which made you did the same thing so you closed your eyes

he gently crashed his lips against yours and your lips danced with his

and he stopped and you opened your eyes just to see that SMILE and he’s like “be mine?” and you just “yes please” and kissed him once again

so dating “the guy every girl was chasing after” was pretty wild like the news spread throughout the uni like realllly fast

and they were some girls like quESTIONINg,,,, why,,,,, y/n,,,,like ???? the audacity ???? really ???????

but your friends were the happiest

because y/n………….finally……..hAS A BOyfrIEND and thE bOYfRiEnD was g0d shownu himself like///

anyway every saturday night is the “new restaurant tryout” and most of the new restaurants you guys went to were good and shownu being shownu would 11/10 come back

and you would come over to the dorm and binge on pretty little liars which shownu never watched

and you ACCIDENTALLY spoil the plot for the next episode and he was like pouting

sometimes you two got very busy with uni that you guys almost didn’t meet for one whole week and he missed you

so he came over to your dorm and cuddle in bed while catching up with each other while giving you back rubs

he ’’’’’’’’’’lends’’’’’’’’’’ you a lot of his sweatshirts and once you gave it back to him and he said keep it but you were like i’m not giving it back

and he scrunched together his eyebrows what do you mean?????

so you explained “i’m returning it so you can wear it and have your scent on it and give it back to me” and he smILED THAT SMILE and gave you a peck on the lips

when the finals were coming up you two would hang around in the library to have a revising session and five minutes in he already put his head on the table

and you keep encouraging him like WE CAN DO THIS

and he’s like yes YOU can do this

and you’re like NO WE CAN DO THIS

and he’s just like……………..ok……………………………….and he let out the loudest WE CAN DO THIS and the everybody were looking at you two and the old library lady literally gave you the first and last warning

you two would just go on lunch dates and he got his phone out and facetimed his mum just to show how beautiful his girlfriend is

you love subway rides with shownu because you would share the earphones and let him pick the music and the music always suit the vibes

sometimes you would follow him up to his dance practices you definitely swerve when the beads of sweats would cover up his whole body and how his dance moves were really sharp and smooth and.......hot

that one time he came over to your dorm and once he hugged you he could feel,,,,,the wet vibes.,,,, like sHOWNU IS CrYING WELP

and you just hold him tight and and caressed his body and kissed his forehead and he got all soothed up

you rarely fight with him but whenever yall fight he’ll be so frustrated and couldn’t even leave you alone

when you said “leave me alone” he was thinking hard if it was a sign for him to leave or to just hold you tight

but he’ll be the one to apologise first and you....would always feel sorry about that.....because sometimes....you know....it wasn’t his fault....but your ego

he’ll be the first one to say i love you and his face got all red and he started beating himself up when you didn’t say it back and you found it cute and beautiful and you just love him so fucking much

he likes to play with your hair a lot so you taught him how to braid and do fishtail braid

and sometimes you would find random tiny cute lil braid on your hair and it’s just too cute

it would be so fun to cook for him because he eats everything, anything

one time he said he craved homemade pancake so bad

so you decided to make one for him for breakfast but you definitely forgot you put it on the stove

so one side of the pancake is burned

but he still eats it and gives you forehead kisses for cooking for him

shownu: it’s made out of love

this is my first time writing an au! if you all have any request, i’m always open and i would love to get some feedback or critics in which i can improve. please bear with the grammar and the tenses i was so into it i didn’t even know when to use present or past tense!

find more from the series: boyfriend!au wonho, boyfriend!au minhyuk, boyfriend!au kihyun, boyfriend!au hyungwon, boyfriend!au jooheon

boyfriend!au i.m coming up soon!

#monsta x scenarios#monsta x imagines#monsta x shownu#monsta x#boyfriend! monsta x#boyfriend! shownu#monsta x reaction#boyfriend!au#monsta x scenario#monsta x imagine#monsta x au#boyfriend!au shownu#monsta x fluff

196 notes

·

View notes

Text

How Seniors Can Use Life Insurance

Anyone with dependents needs life insurance, we're told. Policies on parents can provide food, shelter and education until children can provide for themselves. Husbands and wives can get policies to make a survivor's later years more secure and comfortable.

But what about people in their 50s, 60s or beyond? Many seniors have never had life insurance. Some had term policies that expired after the children grew. Some drop their coverage because they thought their investments had grown big enough and then find things aren't working out.

So what are the ins and outs of getting a policy later in life?

Several purposes. Insurance experts say older people may need life insurance for a variety of reasons:

-- Provide for a surviving spouse or young children from a second marriage.

-- Pay estate taxes.

-- Help with long-term care expenses.

-- Help heirs pay taxes they will face from inherited IRAs and 401(k)s.

Many seniors also have business interests, says Kenneth Pendley, a long-time insurance executive who is national marketing director for Atlanta-based Habersham Funding, a life settlement provider that converts policies to cash or income streams.

"In such circumstances, life insurance may be necessary or helpful to hedge against business interruption upon the death of a business owner or key employee or partner," Pendley says.

The website Quickquote.com shows that a 65-year-old non-smoking man in good health could get a $500,000 20-year term life policy for about $5,300 a year, compared to about $275 for someone who is 35.

Options for policies. Though a policy may be pricey for a senior, chances are you could find one, says Anthony Martin, owner & CEO of the Choice Mutual agency, a Citrus Heights, California, firm specializing in life insurance for seniors.

"It's very uncommon for someone, senior or not, to be flat-out declined for any sort of underwritten life insurance," he says.

Age, health and smoking history affects the premium, and he warns that advertising typically lowballs the cost.

While there are many types of policies with different names, all fall into one of two categories. Term policies are cheapest because they last for a specific number of years, and cost more for longer periods. Permanent policies can be much more expensive but last for life, so no matter how old you are when you die your survivor gets the death benefit.

Regardless of the type of policy, one with a bigger death benefit is more expensive than one with a smaller benefit. But even though premiums are larger for older policyholders, the math can work out, says Chris Huntley, owner of Huntley Wealth & Insurance Services in San Diego.

"A healthy, non-smoking 70-year-old female could purchase a lifetime guaranteed policy with a $250,000 death benefit for as little as $4,982 per year," he says, referring to a type of permanent insurance. "Assuming she lives to age 86, her life expectancy based on the (Social Security Administration) actuarial life table, she will have spent just $79,712 in premiums."

It would take an unlikely 12.49 percent return for those premiums to grow to $250,000 over the same period in an investment, he says.

A matter of taxes. Years ago, people later in life bought life insurance to help pay estate taxes. But in 2017, the first $5.49 million of an estate will be exempt from this tax, so many people don't have to worry about it.

But for those who do, many choose a survivor life or second-to-die policy, types that pay off only after the second spouse dies. This is cheaper because a couple, compared to an individual, has twice the chance of one living longer than average, says Chris Acker, owner of CB Acker Associates Insurance Services in Palo Alto, California.

"While seemingly expensive, the premiums on a life insurance policy designed for estate tax funding are usually a very good return on investment for the families involved," Acker says. "It's typically much less expensive to buy life insurance than to liquidate assets to pay taxes at death."

Policies for estate taxes are typically purchased within an irrevocable life insurance trust, so the benefit is not counted in the taxable estate, he says.

Life insurance can also help heirs pay taxes that will be due on tax-deferred retirement accounts like traditional IRAs and traditional 401(k)s even if there is no estate tax, adds Nancy Butler, author of "Above All Else, Success in Life and Business," and owner of an advisory firm of the same name in Waterford, Connecticut. Butler teaches continuing education courses in life insurance.

"Many heirs loose over 45 percent of the tax-deferred assets left to them," she says. "Without proper planning, a large percentage of the money you worked your life to build could be lost to income taxes rather than being passed to who you want it to go to."

Additional uses. Yet another purpose for life insurance late in life is to replace pension income that may dry up after the beneficiary's death, she adds.

Often, Martin says, seniors get life insurance for specific purposes such as paying off a mortgage or other debts, funeral expenses or caring for an adult child with a disability. In these cases, a term policy large enough to cover the expected cost may be cheapest.

But Acker cautions that it can be difficult or impossible to get a term policy after 60 or 65, while permanent policies may be available for people as old as 90.

He says some permanent policies offer riders to fund long-term care, and can be a better deal than ordinary long-term care policies.

"With the life insurance policy/long-term care rider option, people tend to feel confident that this policy will be used," Acker says.

Seek expert help. While you can shop for policies on your own online, many experts recommend using an insurance broker who represents many providers and knows details you might not easily find online, like whether given medications will get your application denied or boost the premium. Term life is pretty straightforward, but permanent policies have so many provisions it's hard for an amateur to make apples-to-apples comparisons.

"Above all else, the advisor needs to be an independent agent," Martin says. "I cannot stress this enough."

He also recommends agents who specialize in life insurance and don't do policies for cars and homes. A good independent agent should represent at least 10 carriers, he says.

Butler points out that premiums can be lower if you pay once a year rather than several times or monthly. And she says shoppers should look for "break points" where a larger policy becomes cheaper than one that is only slightly smaller.

Credits to: Jeff Brown

Date posted: November 14, 2016

Source: https://finance.yahoo.com/news/seniors-life-insurance-154023225.html

0 notes

Text

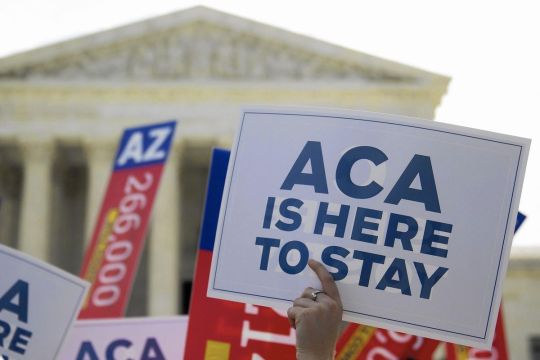

Why Do Republicans Want To Repeal The Affordable Care Act

New Post has been published on https://www.patriotsnet.com/why-do-republicans-want-to-repeal-the-affordable-care-act/

Why Do Republicans Want To Repeal The Affordable Care Act

Why Republicans Cant And Wont Repeal Obamacare

Editor’s Note:

This article was originally posted on Real Clear Health on January 16, 2017.

Now that the Republicans control both the presidency and both houses of Congress, they must put up or shut up on their promise to repeal and replace Obamacare. Here is a flat-footed prediction: the effort will fail for three reasons. First, the Affordable Care Act has largely succeeded not failed, as president-elect Trump and other Republicans falsely allege. Second, it is impossible for the stated goals of repeal to be achieved. Finally, the political fallout from the consequences of partial or total repeal would be devastating. When it comes to casting votes, enough Republicans will conclude that repeal is a bad idea and will join Democrats to sustain the basic structure of the health reform law.

Second, the stated objectives of repealing Obamacare are mutually inconsistent. Three provisions comprise the core of Obamacare. First, rules barring insurance companies from refusing to sell insurance to people because of preexisting conditions or varying premiums based on those conditions. Second, a requirement that everyone carry health insurance who can afford it. And third, subsidies for those with moderate incomes to help make such insurance affordable. The law contains many other provisions as well, but these three are core.

Slashing Ads And Budgets

Funding for the “navigator” programme, under which trained individuals or organisations help people sign up for insurance through Obamacare, has dropped from $62.5m to $10m under President Trump.

His administration has also cut Obamacare advertising spending to $10m – a 90% reduction.

According to a November 2018 Kaiser Health poll, 61% of Americans aged 18 to 64 said they did not know about any enrolment deadlines.

Republicans Want To Get Rid Of Obamacare But Then What

Facebook

EmbedEmbed

President Trump has vowed to repeal the Affordable Care Act, but Sarah Kliff of Vox.com says it’s “an overreach” to say that Republicans have a plan for what comes next.

DAVE DAVIES, HOST:

This is FRESH AIR. I’m Dave Davies, in for Terry Gross. While President Trump clashed with some Republicans over a variety of issues in last year’s campaign, one thing they all seemed to agree on was the need to repeal the Affordable Care Act, known as Obamacare. Now that congressional Republicans have a willing president and the votes to scrap the health care law, they’re finding the task a little more complicated than it seemed. Republican lawmakers have a wide range of ideas about what they might replace Obamacare with. But a secret recording of a Republican policy meeting in Philadelphia revealed many are worried about the political cost of removing coverage from those who’ve come to count on it.

For some perspective on what’s happening in Washington and how it might affect our health care, we turn to Sarah Kliff, a senior policy correspondent at vox.com. Before joining Vox, Kliff covered health policy for The Washington Post and for POLITICO and Newsweek. She co-hosts a policy-oriented podcast for Vox called “The Weeds.” Kliff and co-host Ezra Klein recently interviewed President Obama about the debate over health care and the possible repeal of the Affordable Care Act. I spoke with Sarah Kliff Tuesday.

DAVIES: And where have we seen those pools before?

Board Of Governors Professor School Of Public Affairs & Administration

The Trump administrations efforts to sabotage the ACA and their consequences receive detailed attention in a recently released Brookings book, Trump, the Administrative Presidency, and Federalism. For present purposes, I highlight six major sabotage initiatives which emerged in the wake of congressional failure to repeal and replace the ACA.

1. Reduce outreach and opportunities for enrollment in the ACAs insurance exchanges. Established to offer health insurance to individuals and small business, the exchanges have provided coverage to some 10 million people annually. The Obama administration had vigorously promoted the ACA in part to attract healthy, younger people to the exchanges to help keep premiums down. The Trump administration sharply reduced support for advertising and exchange navigators while reducing the annual enrollment period to about half the number of days.

2. Cut ACA subsidies to insurance companies offering coverage on the exchanges. ACA proponents saw insurance company participation on the exchanges as central to fostering enrollee choice and to fueling competition that would lower premiums. The law therefore provided various subsidies to insurance companies to reduce their risks of losing money if they participated on the exchanges. The Trump administration joined congressional Republicans in reneging on these financial commitments.

Repealing Obamacare Is A Huge Tax Cut For The Rich

This did not play a major overt public role in the 2009-’10 debate about the law, but the Affordable Care Act’s financing rests on a remarkably progressive base. That means that, as the Tax Policy Center has shown, repealing it would shower moneyon a remarkably small number of remarkably wealthy Americans.

The two big relevant taxes, according to the TPC’s Howard Gleckman, are “a 0.9 percent payroll surtax on earnings and a 3.8 percent taxon net investment income for individuals with incomes exceeding $200,000.” That payroll tax hike hits a reasonably broad swath of affluent individuals, but in a relatively minor way. The 3.8 percent tax on net investment income , by contrast, is a pretty hefty tax, but one that falls overwhelmingly on the small number of people who have hundreds of thousands of dollars a year in investment income.

For the bottom 60 percent of the population that is, households earning less than about $67,000 a year repeal of the ACA would end up meaning an increase in taxes due to the loss of ACA tax credits.

But people in the top 1 percent of the income distribution those with incomes of over about $430,000 would see their taxes fall by an average of $25,000 a year.

The Acas Protections Changed Public Opinion In Its Favor Republicans Are Keeping Up

For more than a decade, the Affordable Care Act has been the Republican Partys nemesis. As it was first debated in Congress in 2009, when it was enacted in 2010 and through the next six years of implementation, Republican leaders rallied supporters by vociferously opposing it and calling for repeal. The Trump administration and states controlled by Republicans remain hostile to the ACA.

But the coronavirus pandemics fast-moving destruction has pushed Republicans to rely on Barack Obamas signature law to respond to the crisis, even taking action to strengthen it. The law, as written, requires that Americans who have recently lost jobs and insurance coverage to be permitted to enroll in its insurance marketplace, and they are doing so in swelling numbers. Meanwhile, Republicans recently backed that increased federal funding for a critical part of the ACA: Medicaid for lower-income people. And Trump administration regulators have used their authority to insist that insurance plans pay for coronavirus tests as an essential health benefit under the ACA a Republican target in the past.

Our research shows that this about-face cannot be explained by the pandemic alone. The partys rank-and-file and many other Americans have shifted to supporting the ACA and expanded government payments for health care. The pandemic is giving Republicans cover to follow changing public opinion.

Republicans have spent 10 years trying to kill the Affordable Care Act

Younger Americans Could Get Cheaper Plans

Obamacare was designed so that younger policyholders would help subsidize older ones. That would change under the Republican bill because it would allow insurers to charge older folks more.

This means that younger Americans would likely see their annual premiums go down. Enrollees ages 20 to 29 would save about $700 to $4,000 a year, on average,according to a study by the Milliman actuarial firm on behalf of the AARP Public Policy Institute.

Those under age 30 would also get a refundable tax credit of up to $2,000 to offset the cost of their premiums, as long as their income doesn’t exceed $215,000 for an individual.

Related: What’s inside the Republican health care bill?

The GOP tax credits would also likely be more generous than Obamacare’s subsidies for these folks. For example, a 27-year-old making $40,000 a year would receive $2,000 under the GOP plan, but only gets a $103 subsidy from Obamacare, on average, a Kaiser analysis found.

Also, the bill keeps the Obamacare provision that lets young adults up to age 26 stay on their parents’ insurance plan.

This Is Why Republicans Couldnt Make A Better Replacement

Republicans have made a lot of political hay out of pointing out that the plans available under the Affordable Care Act are, in many ways, disappointing. Unsubsidized premiums are higher than people would like. Deductibles and copayments are higher than people would like. The networks of available doctors are narrower than people would like.

These problems are all very real, and they all could be fixed.

They are not, however, problems that the American Health Care Act actually fixes. While Republicans have made several changes to the AHCA to cobble together a majority of House votes, the core of the bill remains the same: it offers stingier insurance to a narrower group of people.

This is because the AHCA does what Republicans want: it rolls back the ACA taxes. But under those circumstances, its simply not possible for the GOP to offer people the superior insurance coverage that it is promising.

The bill the House is voting on Thursday doesnt get rid of the ACAs tax credits to make it easier to buy health coverage, but it bases them on age, with younger people getting bigger credits, rather than income which means poorer Americans. especially elderly ones, will have a bigger tax burden and more difficulty affording the insurance they need.

Dont Like Obamacare It Was The Republicans Idea Says Liberal Democrat

Susan Jones

Robert Reich served as Labor Secretary for President Bill Clinton.

While Republicans plot new ways to sabotage the Affordable Care Act, its easy to forget that for years theyve been arguing that any comprehensive health insurance system be designed exactly like the one that officially began October 1st, glitches and all, said Robert Reich, who served as President Bill Clintons Labor Secretary.

Reich says Democrats should have insisted on a single-payer system because it would have been cheaper, simpler, and more popular.

In a blog at The Huffington Post website, Reich that Republicans have long argued for a health care system based on private insurance and paid for with subsidies and a requirement that the young and healthy people sign up. Democrats, he says, wanted to model health care reform on Social Security and Medicare, and fund it through the payroll tax.

Reich says President Richard Nixon in 1974, proposed, in essence, todays Affordable Care Act. Thirty years later, then-Massachusetts Gov. Mitt Romney, another Republican, made Nixons plan the law in Massachusetts.

Reich adds: When todays Republicans rage against the individual mandate in the Affordable Care Act, its useful to recall this was their idea as well, as proposed in 1989 by Stuart M. Butler of the Heritage Foundation.

Reichs blog is entitled, The Democrats Version of Health Insurance Would Have Been Cheaper, Simpler, and More Popular

Background On The Health Care Repeal Lawsuit

From the beginning, the Trump administration and allied leaders in Congress and state governments have been committed to dismantling the ACA and the consumer protections it confers by any means possible. The Trump administration has repeatedly key provisions of the landmark law by executive actions and other more covert tactics, including removing essential consumer information from federal websites and defunding outreach and enrollment programs intended to expand coverage. After several failed attempts by President Donald Trumps legislative allies to repeal and replace the ACA, Congress passed a tax bill in late 2017 that zeroed out the individual mandate penalty.

After the tax bill became law, Texas and other states filed a federal lawsuit, claiming that because the mandate had no financial penalty, it made the rest of the law unconstitutional. U.S. District Court Judge Reed OConnor accepted this reasoning and held that the entire law must be struck down in what one legal expert called a partisan, activist ruling. On appeal, a 5th U.S. Circuit Court of Appeals panel also in December that, following the tax bills change to the law, the individual mandate is unconstitutional. The panel then remanded the case back to Judge OConnor to determine which parts of the ACA, if any, can remain given their decision. Since that ruling, the Supreme Court has to hear the case during its upcoming term, and, for now, the ACA remains the law of the land.

Obamacare: Has Trump Managed To Kill Off Affordable Care Act

The Trump administration has ramped up its attack on the Affordable Care Act by backing a federal judge’s decision to declare the entire law unconstitutional.

For now, Obamacare is still standing. Around 4.1 million Americans have signed up for new plans so far this year, according to government reports, down 12% from last year.

At a rally this week, Mr Trump again promised his supporters: “We are going to get rid of Obamacare.” But how much has he delivered on that pledge so far?

Efforts To Repeal The Affordable Care Act

This article needs to be . The reason given is: Missing the May 2018 efforts. Please help update this article to reflect recent events or newly available information.

The following is a list of efforts to repeal the Affordable Care Act , which had been enactedby the 111th United States Congress on March 23, 2010.

This Is Also Why Republicans Might Drop Repeal

While mania for tax cuts is an important driver of the GOP push to repeal the Affordable Care Act, it might also ultimately be what leads them to abandon it. The healthcare debate has already taken more time than either Congress or the White House wanted and the bill hasnt even gotten to the Senate yet.

Meanwhile, many Republicans are itching to move on to their next priority: tax reform.

Republicans have a bunch of different tax plans floating around, but they all feature enormous tax cuts for wealthy households. Democrats will object, but they wont be able to stop the GOP from enacting a big tax cut. The only issue will be how large of an increase in the budget deficit do Republicans consider economically viable. Once thats decided, however, the tight linkage between the ACA and tax policy will be broken, since the entire rate structure will have already been rewritten in a way that makes the ACAs specific financing mechanism irrelevant.

No matter how the budget crunch gets resolved,however, the tax issue is the $500 billion elephant in the room. Its a key reason GOP leaders want repeal, a key reason theyve had trouble coming up with a popular replacement, and potentially a key reason theyll ultimately decide to move on to other matters. Talking about health care politics without talking about the revenue side misses an enormous part of the story.

Republican Views On Obamacare

The Republican Partys view on the Patient Protection and Affordable Care Actcommonly known as Obamacareis that its implementation was less about providing healthcare to millions, and more a result of power as the government sought to expand its reach over one sixth of the economy. The party claims that Obamacare has resulted in an attack on the Constitution of the United States because it requires U.S. citizens to purchase health insurance, and its impact on the health of the nation overall has been detrimental. The party is in agreement with the four Supreme Court justices who dissented in the ACA ruling. The justices stated, In our view, the entire Act before us is invalid in its entirety. As of 2012, the partys stance was that Obamacare was the result of outdated liberalism, and the latest in a series of attempts to impose upon the people of America a euro-style bureaucracy to micromanage all aspects of their lives. One of the partys biggest issues with Obamacare is its unpopularity among the peoplewhen polled on the subject, pluralities and even majorities often state they do not like the law.

Older Americans Could Have To Pay More

Enrollees in their 50s and early 60s benefited from Obamacare because insurers could only charge them three times more than younger policyholders. The bill would widen that band to five-to-one.

That would mean that adults ages 60 to 64 would see their annual premiums soar 22% to nearly $18,000, according to the Milliman study for the AARP. Those in their 50s would be hit with a 13% increase and pay an annual premium of $12,800.

Also, the GOP bill doesn’t provide them with as generous tax credits as Obamacare. A 60-year-old making $40,000 would get only $4,000 from the Republican plan, instead of an average subsidy of $6,750 from the Affordable Care Act, according the Kaiser study.

States could also receive waivers to allow insurers to charge older Americans even more than five times the premiums of the young.

Whats Dividing Republicans And Democrats On Healthcare Reform

Since the Affordable Care Act became law in 2010, Republicans have been determined to destroy it while Democrats insist its the countrys best chance at reforming healthcare to make it affordable and accessible. Both parties want reform, but the approach has been fundamentally different and for good reason. There are basic, core reasons why conservatives and liberals cant get on the same page when it comes to healthcare reform. Lets take a moment to dig into the details and figure out what is exactly keeping Republicans and Democrats from being able to find a middle ground on healthcare reform, so far.

Democrats want the federal government to legislate and administer healthcare while Republicans want private industry to helm the healthcare system with as minimal input from the federal government as possible.

Of course, there are always exceptions within each party because people arent one-dimensional. Moderates on both sides, for instance, would seek compromise wherever possible. But in general, these core ideological differences make healthcare reform particularly challenging, especially when one party holds more power. In 2010, Democrats passed the ACA without a single rightwing vote.

Repeal Of Obamacares Taxes Would Be A Huge Tax Cut For The Rich

This did not play a major overt public role in the 2009-10 debate about the law, but the Affordable Care Acts financing rests on a remarkably progressive base. That means that, as the Tax Policy Center has shown, repealing it would shower moneyon a remarkably small number of remarkably wealthy Americans.

The two big relevant taxes, according to the TPCs Howard Gleckman, are a 0.9 percent payroll surtax on earnings and a 3.8 percent tax on net investment income for individuals with incomes exceeding $200,000 . That payroll tax hike hits a reasonably broad swath of affluent individuals, but in a relatively minor way. The 3.8 percent tax on net investment income , by contrast, is a pretty hefty tax, but one that falls overwhelmingly on the small number of people who have hundreds of thousands of dollars a year in investment income.

Tax Policy Center

For the bottom 60 percent of the population that is, households earning less than about $67,000 a year full repeal of the ACA would end up meaning an increase in taxes due to the loss of ACA tax credits.

But people in the top 1 percent of the income distribution those with incomes of over about $430,000 would see their taxes fall by an average of $25,000 a year.

Under the actual AHCA, Jared Kushner would actually pay even less in taxes. As a young person, Kushner would get a larger tax to buy insurance under the AHCA than he does now.

New Threats & Potential Affordable Care Act Changes For 2019

To date, the ACA has been challenged in front of the Supreme Court twice. Judges upheld the constitutionality of the ACA both times. But now, a new effort to strike down the act is making its way through our legal system. Two Republican Governors and 18 Republican state attorneys general, led by Texas, initiated the lawsuit.

The lawsuit, Texas v. Azar, alleges the individual mandate of the Affordable Care Act is unconstitutional now that TCJA set the penalty tax to $0. In December 2018, a Texas district court judge agreed with the plaintiffs. The judge also concluded that the intent of lawmakers was that the individual mandate was essential to the ACA, and as such couldnt be severed from the larger text. Therefore, the entire ACA was unconstitutional and repealing it was appropriate.

But the ruling hasnt gone into effect yet. The judge is allowing the status quo to remain until all the appeals have been heard. In efforts to combat the ruling, and since the current administration is refusing to defend the law in court, 21 Democratic state attorneys general and the U.S. House of Representatives filed an appeal to challenge the ruling. In July, the Fifth Circuit Court of Appeals in New Orleans heard arguments in favor of overturning the original ruling. The court hasnt yet reached a decision, and most believe this lawsuit will eventually make its way to the Supreme Court.

Republicans Are Still Trying To Repeal Obamacare Heres Why They Are Not Likely To Succeed

Conservatives are still trying to repeal the Affordable Care Act even after the Republican-majority Congress failed to overturn the law in 2017. A coalition of conservative groups intends to release a new plan this summer. The groups will reportedly propose ending the laws expansion of Medicaid and convert Medicaid funding into block grants to the states. And just last week the Trump administrations Justice Department argued in a legal filing that key provisions of the law its protections for persons with preexisting conditions are .

Why are Republicans still trying to undo the ACA? We argue in a forthcoming that the laws political vulnerabilities and Republican electoral dynamics drive conservative efforts to uproot it.

In the past, conservatives have thrown in the towel

As politicians and political scientists both know, the can never be taken for granted. Even so, the duration and intensity of conservative resistance to the ACA is historically unusual. The ACA is a moderate law, modeled on that Republicans once supported, such as insurance purchasing pools. Whats more, many red states refuse to accept the ACAs funding to expand Medicaid to more of their citizens such as , which has a large number of uninsured residents even though you would think they would want those federal benefits.

So why is the ACA still politically vulnerable?

The answer lies partly in the way the program was designed.

Is repeal likely?

The Health Care Repeal Lawsuit Could Strip Coverage From 23 Million Americans

Nicole RapfogelEmily Gee

Tomorrow, the Trump administration and 18 Republican governors and attorneys general will file their opening briefs with the Supreme Court in California v. Texasthe health care repeal lawsuit. The lawsuit, criticized across the political spectrum as a badly flawed case, threatens to upend the Affordable Care Act and strip 23.3 million Americans of their health coverage, according to new CAP analysisabout 3 million more than was forecast before the coronavirus pandemic. The anti-ACA agitators who initiated the health care repeal lawsuit, backed by the Trump administration, continue their attempts to dismantle the ACA, including its coverage expansions and consumer protections, amid the pandemic, during which comprehensive health coverage has never been more important. Millions of Americans who have lost their jobs and job-based insurance due to the current economic crisis are relying on the insurance options made possible by the ACA to keep themselves and their families covered.

0 notes

Text

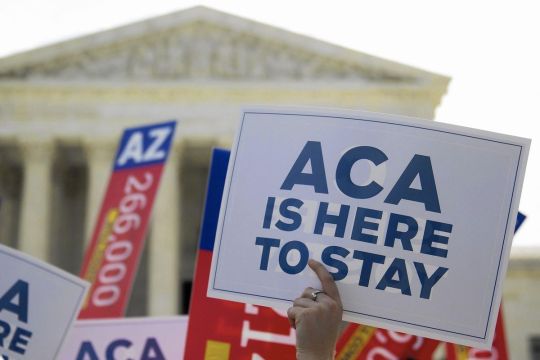

Why Do Republicans Want To Repeal The Affordable Care Act

Why Republicans Cant And Wont Repeal Obamacare

youtube

Editor’s Note:

This article was originally posted on Real Clear Health on January 16, 2017.

Now that the Republicans control both the presidency and both houses of Congress, they must put up or shut up on their promise to repeal and replace Obamacare. Here is a flat-footed prediction: the effort will fail for three reasons. First, the Affordable Care Act has largely succeeded not failed, as president-elect Trump and other Republicans falsely allege. Second, it is impossible for the stated goals of repeal to be achieved. Finally, the political fallout from the consequences of partial or total repeal would be devastating. When it comes to casting votes, enough Republicans will conclude that repeal is a bad idea and will join Democrats to sustain the basic structure of the health reform law.

Second, the stated objectives of repealing Obamacare are mutually inconsistent. Three provisions comprise the core of Obamacare. First, rules barring insurance companies from refusing to sell insurance to people because of preexisting conditions or varying premiums based on those conditions. Second, a requirement that everyone carry health insurance who can afford it. And third, subsidies for those with moderate incomes to help make such insurance affordable. The law contains many other provisions as well, but these three are core.

Slashing Ads And Budgets

Funding for the “navigator” programme, under which trained individuals or organisations help people sign up for insurance through Obamacare, has dropped from $62.5m to $10m under President Trump.

His administration has also cut Obamacare advertising spending to $10m – a 90% reduction.

According to a November 2018 Kaiser Health poll, 61% of Americans aged 18 to 64 said they did not know about any enrolment deadlines.

Republicans Want To Get Rid Of Obamacare But Then What

Facebook

EmbedEmbed

President Trump has vowed to repeal the Affordable Care Act, but Sarah Kliff of Vox.com says it’s “an overreach” to say that Republicans have a plan for what comes next.

DAVE DAVIES, HOST:

This is FRESH AIR. I’m Dave Davies, in for Terry Gross. While President Trump clashed with some Republicans over a variety of issues in last year’s campaign, one thing they all seemed to agree on was the need to repeal the Affordable Care Act, known as Obamacare. Now that congressional Republicans have a willing president and the votes to scrap the health care law, they’re finding the task a little more complicated than it seemed. Republican lawmakers have a wide range of ideas about what they might replace Obamacare with. But a secret recording of a Republican policy meeting in Philadelphia revealed many are worried about the political cost of removing coverage from those who’ve come to count on it.

For some perspective on what’s happening in Washington and how it might affect our health care, we turn to Sarah Kliff, a senior policy correspondent at vox.com. Before joining Vox, Kliff covered health policy for The Washington Post and for POLITICO and Newsweek. She co-hosts a policy-oriented podcast for Vox called “The Weeds.” Kliff and co-host Ezra Klein recently interviewed President Obama about the debate over health care and the possible repeal of the Affordable Care Act. I spoke with Sarah Kliff Tuesday.

DAVIES: And where have we seen those pools before?

Board Of Governors Professor School Of Public Affairs & Administration

The Trump administrations efforts to sabotage the ACA and their consequences receive detailed attention in a recently released Brookings book, Trump, the Administrative Presidency, and Federalism. For present purposes, I highlight six major sabotage initiatives which emerged in the wake of congressional failure to repeal and replace the ACA.

1. Reduce outreach and opportunities for enrollment in the ACAs insurance exchanges. Established to offer health insurance to individuals and small business, the exchanges have provided coverage to some 10 million people annually. The Obama administration had vigorously promoted the ACA in part to attract healthy, younger people to the exchanges to help keep premiums down. The Trump administration sharply reduced support for advertising and exchange navigators while reducing the annual enrollment period to about half the number of days.

2. Cut ACA subsidies to insurance companies offering coverage on the exchanges. ACA proponents saw insurance company participation on the exchanges as central to fostering enrollee choice and to fueling competition that would lower premiums. The law therefore provided various subsidies to insurance companies to reduce their risks of losing money if they participated on the exchanges. The Trump administration joined congressional Republicans in reneging on these financial commitments.

Repealing Obamacare Is A Huge Tax Cut For The Rich

This did not play a major overt public role in the 2009-’10 debate about the law, but the Affordable Care Act’s financing rests on a remarkably progressive base. That means that, as the Tax Policy Center has shown, repealing it would shower moneyon a remarkably small number of remarkably wealthy Americans.

The two big relevant taxes, according to the TPC’s Howard Gleckman, are “a 0.9 percent payroll surtax on earnings and a 3.8 percent taxon net investment income for individuals with incomes exceeding $200,000.” That payroll tax hike hits a reasonably broad swath of affluent individuals, but in a relatively minor way. The 3.8 percent tax on net investment income , by contrast, is a pretty hefty tax, but one that falls overwhelmingly on the small number of people who have hundreds of thousands of dollars a year in investment income.

For the bottom 60 percent of the population that is, households earning less than about $67,000 a year repeal of the ACA would end up meaning an increase in taxes due to the loss of ACA tax credits.

But people in the top 1 percent of the income distribution those with incomes of over about $430,000 would see their taxes fall by an average of $25,000 a year.

The Acas Protections Changed Public Opinion In Its Favor Republicans Are Keeping Up

For more than a decade, the Affordable Care Act has been the Republican Partys nemesis. As it was first debated in Congress in 2009, when it was enacted in 2010 and through the next six years of implementation, Republican leaders rallied supporters by vociferously opposing it and calling for repeal. The Trump administration and states controlled by Republicans remain hostile to the ACA.

But the coronavirus pandemics fast-moving destruction has pushed Republicans to rely on Barack Obamas signature law to respond to the crisis, even taking action to strengthen it. The law, as written, requires that Americans who have recently lost jobs and insurance coverage to be permitted to enroll in its insurance marketplace, and they are doing so in swelling numbers. Meanwhile, Republicans recently backed that increased federal funding for a critical part of the ACA: Medicaid for lower-income people. And Trump administration regulators have used their authority to insist that insurance plans pay for coronavirus tests as an essential health benefit under the ACA a Republican target in the past.

Our research shows that this about-face cannot be explained by the pandemic alone. The partys rank-and-file and many other Americans have shifted to supporting the ACA and expanded government payments for health care. The pandemic is giving Republicans cover to follow changing public opinion.

Republicans have spent 10 years trying to kill the Affordable Care Act

Younger Americans Could Get Cheaper Plans

Obamacare was designed so that younger policyholders would help subsidize older ones. That would change under the Republican bill because it would allow insurers to charge older folks more.

This means that younger Americans would likely see their annual premiums go down. Enrollees ages 20 to 29 would save about $700 to $4,000 a year, on average,according to a study by the Milliman actuarial firm on behalf of the AARP Public Policy Institute.

Those under age 30 would also get a refundable tax credit of up to $2,000 to offset the cost of their premiums, as long as their income doesn’t exceed $215,000 for an individual.

Related: What’s inside the Republican health care bill?

The GOP tax credits would also likely be more generous than Obamacare’s subsidies for these folks. For example, a 27-year-old making $40,000 a year would receive $2,000 under the GOP plan, but only gets a $103 subsidy from Obamacare, on average, a Kaiser analysis found.

Also, the bill keeps the Obamacare provision that lets young adults up to age 26 stay on their parents’ insurance plan.

This Is Why Republicans Couldnt Make A Better Replacement

Republicans have made a lot of political hay out of pointing out that the plans available under the Affordable Care Act are, in many ways, disappointing. Unsubsidized premiums are higher than people would like. Deductibles and copayments are higher than people would like. The networks of available doctors are narrower than people would like.

These problems are all very real, and they all could be fixed.

They are not, however, problems that the American Health Care Act actually fixes. While Republicans have made several changes to the AHCA to cobble together a majority of House votes, the core of the bill remains the same: it offers stingier insurance to a narrower group of people.

This is because the AHCA does what Republicans want: it rolls back the ACA taxes. But under those circumstances, its simply not possible for the GOP to offer people the superior insurance coverage that it is promising.

The bill the House is voting on Thursday doesnt get rid of the ACAs tax credits to make it easier to buy health coverage, but it bases them on age, with younger people getting bigger credits, rather than income which means poorer Americans. especially elderly ones, will have a bigger tax burden and more difficulty affording the insurance they need.

Dont Like Obamacare It Was The Republicans Idea Says Liberal Democrat

youtube

Susan Jones

Robert Reich served as Labor Secretary for President Bill Clinton.

While Republicans plot new ways to sabotage the Affordable Care Act, its easy to forget that for years theyve been arguing that any comprehensive health insurance system be designed exactly like the one that officially began October 1st, glitches and all, said Robert Reich, who served as President Bill Clintons Labor Secretary.

Reich says Democrats should have insisted on a single-payer system because it would have been cheaper, simpler, and more popular.

In a blog at The Huffington Post website, Reich that Republicans have long argued for a health care system based on private insurance and paid for with subsidies and a requirement that the young and healthy people sign up. Democrats, he says, wanted to model health care reform on Social Security and Medicare, and fund it through the payroll tax.

Reich says President Richard Nixon in 1974, proposed, in essence, todays Affordable Care Act. Thirty years later, then-Massachusetts Gov. Mitt Romney, another Republican, made Nixons plan the law in Massachusetts.

Reich adds: When todays Republicans rage against the individual mandate in the Affordable Care Act, its useful to recall this was their idea as well, as proposed in 1989 by Stuart M. Butler of the Heritage Foundation.

Reichs blog is entitled, The Democrats Version of Health Insurance Would Have Been Cheaper, Simpler, and More Popular

Background On The Health Care Repeal Lawsuit

From the beginning, the Trump administration and allied leaders in Congress and state governments have been committed to dismantling the ACA and the consumer protections it confers by any means possible. The Trump administration has repeatedly key provisions of the landmark law by executive actions and other more covert tactics, including removing essential consumer information from federal websites and defunding outreach and enrollment programs intended to expand coverage. After several failed attempts by President Donald Trumps legislative allies to repeal and replace the ACA, Congress passed a tax bill in late 2017 that zeroed out the individual mandate penalty.

After the tax bill became law, Texas and other states filed a federal lawsuit, claiming that because the mandate had no financial penalty, it made the rest of the law unconstitutional. U.S. District Court Judge Reed OConnor accepted this reasoning and held that the entire law must be struck down in what one legal expert called a partisan, activist ruling. On appeal, a 5th U.S. Circuit Court of Appeals panel also in December that, following the tax bills change to the law, the individual mandate is unconstitutional. The panel then remanded the case back to Judge OConnor to determine which parts of the ACA, if any, can remain given their decision. Since that ruling, the Supreme Court has to hear the case during its upcoming term, and, for now, the ACA remains the law of the land.

Obamacare: Has Trump Managed To Kill Off Affordable Care Act

The Trump administration has ramped up its attack on the Affordable Care Act by backing a federal judge’s decision to declare the entire law unconstitutional.

For now, Obamacare is still standing. Around 4.1 million Americans have signed up for new plans so far this year, according to government reports, down 12% from last year.

At a rally this week, Mr Trump again promised his supporters: “We are going to get rid of Obamacare.” But how much has he delivered on that pledge so far?

Efforts To Repeal The Affordable Care Act

This article needs to be . The reason given is: Missing the May 2018 efforts. Please help update this article to reflect recent events or newly available information.

The following is a list of efforts to repeal the Affordable Care Act , which had been enactedby the 111th United States Congress on March 23, 2010.

This Is Also Why Republicans Might Drop Repeal

While mania for tax cuts is an important driver of the GOP push to repeal the Affordable Care Act, it might also ultimately be what leads them to abandon it. The healthcare debate has already taken more time than either Congress or the White House wanted and the bill hasnt even gotten to the Senate yet.

Meanwhile, many Republicans are itching to move on to their next priority: tax reform.

Republicans have a bunch of different tax plans floating around, but they all feature enormous tax cuts for wealthy households. Democrats will object, but they wont be able to stop the GOP from enacting a big tax cut. The only issue will be how large of an increase in the budget deficit do Republicans consider economically viable. Once thats decided, however, the tight linkage between the ACA and tax policy will be broken, since the entire rate structure will have already been rewritten in a way that makes the ACAs specific financing mechanism irrelevant.

No matter how the budget crunch gets resolved,however, the tax issue is the $500 billion elephant in the room. Its a key reason GOP leaders want repeal, a key reason theyve had trouble coming up with a popular replacement, and potentially a key reason theyll ultimately decide to move on to other matters. Talking about health care politics without talking about the revenue side misses an enormous part of the story.

Republican Views On Obamacare

The Republican Partys view on the Patient Protection and Affordable Care Actcommonly known as Obamacareis that its implementation was less about providing healthcare to millions, and more a result of power as the government sought to expand its reach over one sixth of the economy. The party claims that Obamacare has resulted in an attack on the Constitution of the United States because it requires U.S. citizens to purchase health insurance, and its impact on the health of the nation overall has been detrimental. The party is in agreement with the four Supreme Court justices who dissented in the ACA ruling. The justices stated, In our view, the entire Act before us is invalid in its entirety. As of 2012, the partys stance was that Obamacare was the result of outdated liberalism, and the latest in a series of attempts to impose upon the people of America a euro-style bureaucracy to micromanage all aspects of their lives. One of the partys biggest issues with Obamacare is its unpopularity among the peoplewhen polled on the subject, pluralities and even majorities often state they do not like the law.

Older Americans Could Have To Pay More

Enrollees in their 50s and early 60s benefited from Obamacare because insurers could only charge them three times more than younger policyholders. The bill would widen that band to five-to-one.

That would mean that adults ages 60 to 64 would see their annual premiums soar 22% to nearly $18,000, according to the Milliman study for the AARP. Those in their 50s would be hit with a 13% increase and pay an annual premium of $12,800.

Also, the GOP bill doesn’t provide them with as generous tax credits as Obamacare. A 60-year-old making $40,000 would get only $4,000 from the Republican plan, instead of an average subsidy of $6,750 from the Affordable Care Act, according the Kaiser study.

States could also receive waivers to allow insurers to charge older Americans even more than five times the premiums of the young.

Whats Dividing Republicans And Democrats On Healthcare Reform

Since the Affordable Care Act became law in 2010, Republicans have been determined to destroy it while Democrats insist its the countrys best chance at reforming healthcare to make it affordable and accessible. Both parties want reform, but the approach has been fundamentally different and for good reason. There are basic, core reasons why conservatives and liberals cant get on the same page when it comes to healthcare reform. Lets take a moment to dig into the details and figure out what is exactly keeping Republicans and Democrats from being able to find a middle ground on healthcare reform, so far.

Democrats want the federal government to legislate and administer healthcare while Republicans want private industry to helm the healthcare system with as minimal input from the federal government as possible.

Of course, there are always exceptions within each party because people arent one-dimensional. Moderates on both sides, for instance, would seek compromise wherever possible. But in general, these core ideological differences make healthcare reform particularly challenging, especially when one party holds more power. In 2010, Democrats passed the ACA without a single rightwing vote.

Repeal Of Obamacares Taxes Would Be A Huge Tax Cut For The Rich

youtube

This did not play a major overt public role in the 2009-10 debate about the law, but the Affordable Care Acts financing rests on a remarkably progressive base. That means that, as the Tax Policy Center has shown, repealing it would shower moneyon a remarkably small number of remarkably wealthy Americans.

The two big relevant taxes, according to the TPCs Howard Gleckman, are a 0.9 percent payroll surtax on earnings and a 3.8 percent tax on net investment income for individuals with incomes exceeding $200,000 . That payroll tax hike hits a reasonably broad swath of affluent individuals, but in a relatively minor way. The 3.8 percent tax on net investment income , by contrast, is a pretty hefty tax, but one that falls overwhelmingly on the small number of people who have hundreds of thousands of dollars a year in investment income.

Tax Policy Center

For the bottom 60 percent of the population that is, households earning less than about $67,000 a year full repeal of the ACA would end up meaning an increase in taxes due to the loss of ACA tax credits.

But people in the top 1 percent of the income distribution those with incomes of over about $430,000 would see their taxes fall by an average of $25,000 a year.

Under the actual AHCA, Jared Kushner would actually pay even less in taxes. As a young person, Kushner would get a larger tax to buy insurance under the AHCA than he does now.

New Threats & Potential Affordable Care Act Changes For 2019

To date, the ACA has been challenged in front of the Supreme Court twice. Judges upheld the constitutionality of the ACA both times. But now, a new effort to strike down the act is making its way through our legal system. Two Republican Governors and 18 Republican state attorneys general, led by Texas, initiated the lawsuit.

The lawsuit, Texas v. Azar, alleges the individual mandate of the Affordable Care Act is unconstitutional now that TCJA set the penalty tax to $0. In December 2018, a Texas district court judge agreed with the plaintiffs. The judge also concluded that the intent of lawmakers was that the individual mandate was essential to the ACA, and as such couldnt be severed from the larger text. Therefore, the entire ACA was unconstitutional and repealing it was appropriate.

But the ruling hasnt gone into effect yet. The judge is allowing the status quo to remain until all the appeals have been heard. In efforts to combat the ruling, and since the current administration is refusing to defend the law in court, 21 Democratic state attorneys general and the U.S. House of Representatives filed an appeal to challenge the ruling. In July, the Fifth Circuit Court of Appeals in New Orleans heard arguments in favor of overturning the original ruling. The court hasnt yet reached a decision, and most believe this lawsuit will eventually make its way to the Supreme Court.

Republicans Are Still Trying To Repeal Obamacare Heres Why They Are Not Likely To Succeed

Conservatives are still trying to repeal the Affordable Care Act even after the Republican-majority Congress failed to overturn the law in 2017. A coalition of conservative groups intends to release a new plan this summer. The groups will reportedly propose ending the laws expansion of Medicaid and convert Medicaid funding into block grants to the states. And just last week the Trump administrations Justice Department argued in a legal filing that key provisions of the law its protections for persons with preexisting conditions are .

Why are Republicans still trying to undo the ACA? We argue in a forthcoming that the laws political vulnerabilities and Republican electoral dynamics drive conservative efforts to uproot it.

In the past, conservatives have thrown in the towel

As politicians and political scientists both know, the can never be taken for granted. Even so, the duration and intensity of conservative resistance to the ACA is historically unusual. The ACA is a moderate law, modeled on that Republicans once supported, such as insurance purchasing pools. Whats more, many red states refuse to accept the ACAs funding to expand Medicaid to more of their citizens such as , which has a large number of uninsured residents even though you would think they would want those federal benefits.

So why is the ACA still politically vulnerable?

The answer lies partly in the way the program was designed.

Is repeal likely?

The Health Care Repeal Lawsuit Could Strip Coverage From 23 Million Americans

Nicole RapfogelEmily Gee