#North America Healthcare Facilities Management Market

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr’s reach among the 26-to-35-year-olds in the US is 11%.

Text

Healthcare Facilities Management Market Business Demand and Sales Consumption: Insights into Top Manufacturers, Future Scope, and Expert Reviews, Forecast by 2032

The Competitive Landscape of the Healthcare Facilities Management Market

In today's competitive business environment, the global Healthcare Facilities Management market stands as a critical battleground for businesses seeking to carve out a niche and drive growth. As industries grapple with the complexities of this market, understanding the competitive landscape becomes paramount for strategic decision-making and success.

According to Straits Research, the global healthcare facilities management market size was valued at USD 354.67 Billion in 2022. It is projected to reach from USD XX Billion in 2023 to USD 1029.50 Billion by 2031, growing at a CAGR of 12.57% during the forecast period (2023–2031).

The global Healthcare Facilities Management market is characterized by its dynamic nature, driven by technological advancements, regulatory changes, and shifting consumer preferences. These factors, while presenting challenges, also offer businesses unique opportunities to innovate, differentiate, and thrive.

Note: We're in the process of updating our reports. If you're seeking updated primary and secondary data from 2023-2031, coupled with insights on Cost Module, Business Strategy, and Competitive Landscape, kindly click ""request free sample report."" The comprehensive report will reach you via email within 24 to 48 hours.

Download Sample of This Strategic Report@https://straitsresearch.com/report/healthcare-facilities-management-market/request-sample

Companies and Manufacturers Covered:

Key market participants play a pivotal role in shaping the competitive narrative. By profiling industry leaders, their strategic initiatives, and competitive positioning, the report offers insights into competitive dynamics, influencing factors, and growth opportunities. These insights are invaluable for businesses seeking to gain a competitive edge, differentiate their offerings, and achieve market leadership.

ABM Industries Inc.

Aramark

Iss World Services AS

Ecolab Inc.

Jones Lang Lasalle Incorporated

Medxcel Facilities Management LLC

Serco Group PLC

Sodexo

Vanguard Resources Inc.

Tenon Group

Compass Group PLC.

A recent market analysis offers a comprehensive view of the Global Healthcare Facilities Management Market, highlighting key growth drivers, emerging trends, and competitive dynamics. This report serves as a valuable resource for businesses, offering insights into market positioning, competitive strategies, and growth prospects.

Buy Now This Market Study@https://straitsresearch.com/buy-now/healthcare-facilities-management-market

The quantitative analysis accompanying the report provides stakeholders with a decade-long perspective on the market's trajectory. By examining historical data, identifying trends, and forecasting future developments, the report enables businesses to anticipate market movements, assess competitive threats, and capitalize on emerging opportunities.

Global Regional Outlook:

North America: North America is currently the largest market for Healthcare Facilities Management, accounting for a significant share of the global market.

Europe: While the North America leads in market size, Europe is emerging as the fastest growing region in the Healthcare Facilities Management market.

Research Methodology

The research methodology underpinning this report is rigorous and robust. By leveraging both primary and secondary data sources, the report ensures accuracy, reliability, and depth. Through interviews with industry experts, analysis of Healthcare Facilities Management market trends, and examination of key growth drivers, the report offers a comprehensive view of the competitive landscape.

Market Segmentation:

By Product Type

Waste Management

Security Services

Catering Services

Cleaning Services

Technical Support Services

Other Product Types

By End-User

Hospitals And Clinics

Long-term Healthcare Facilities

Other end-users

Purchase This Report (Price 4500 USD for Single User License)@https://straitsresearch.com/report/healthcare-facilities-management-market/toc

This Report Addresses:

Market intelligence to enable effective decision making

Market estimates & forecasts from 2018to 2031

Growth opportunities and trend analyses

Segment & regional revenue forecasts for market assessment

Competition strategy & market share analysis

Product innovation listing for you to stay ahead of the curve

COVID19’s impact and how to sustain in these fast-evolving markets

Market report in PDF, XLS, PPT & online dashboard versions

In conclusion, the global Healthcare Facilities Management market presents a dynamic and competitive landscape for businesses. By understanding the competitive landscape, leveraging strategic insights, and adopting a proactive approach, businesses can navigate this complex market successfully, drive growth, and achieve sustainable success.

Report Customization:

Our report is adaptable to your specific needs. For tailored insights, please reach out to our sales team at [email protected]. Additionally, you can contact our representatives directly at +1 646 905 0080 (U.S.), +44 203 695 0070 (U.K.) to discuss your research criteria.

#Healthcare Facilities Management Market#Healthcare Facilities Management Market Share#Healthcare Facilities Management Industry#Healthcare Facilities Management Market Size#Healthcare Facilities Management Market Research#What is Healthcare Facilities Management?#Healthcare Facilities Management Market Drivers#North America Healthcare Facilities Management Market#Europe Healthcare Facilities Management Market

1 note

·

View note

Text

Medical Disposables Market to be worth US$ 326 Billion by 2033, Reveals Future Market Insights

The Medical Disposables Market revenues were estimated at US$ 153.5 Billion in 2022 and is anticipated to grow at a CAGR of 7.1% from 2023-2033, according to a recently published Future Market Insights report. By the end of 2033, the market is expected to reach US$ 326 Billion. Bandages and Wound Dressings commanded the largest revenue share in 2022 and is expected to register a CAGR of 6.8% from 2023 to 2033.

The rising incidence of Hospital Acquired Infections, an increasing number of surgical procedures, and the growing prevalence of chronic diseases leading to longer hospital admission have been the key factors driving the market.

The subsequent spike in the number of chronic illness cases and a rise in the rate of hospitalizations has fueled the field of emergency medical disposables growth. The expansion of the medical disposables market is being fueled by an increase in the prevalence of hospital-acquired illnesses and disorders, as well as a greater focus on infection prevention. For example, the prevalence of healthcare-associated infection in high-income countries ranges from 3.5% to 12%, whereas it ranges from 5.7% to 19.1% in low and medium-income countries.

A growing geriatric population, an increase in the incidence of incontinence issues, mandatory guidelines that must be followed for patient safety at healthcare institutions, and an increase in demand for sophisticated healthcare facilities is driving the medical disposables market.

The market in North America is expected to reach a valuation of US$ 131 Billion by 2033 from US$ 61.7 Billion in 2022. In August 2000, the Food and Drug Administration (FDA) issued guidance concerning healthcare single-use items reprocessed by third parties or hospitals. In this guidance, FDA stated that hospitals or third-party reprocessors would be considered manufacturers and regulated in the exact same manner. A newly used single-use device still has to fulfill the criteria for device activation required by its flagship when it was originally manufactured. Such regulations have been creating a positive impact on the medical disposables market in the U.S. market in specific and the North American market in general

Competitive Landscape

The key companies in the market are engaged in mergers, acquisitions and partnerships.

The key players in the market include 3M, Johnson & Johnson Services, Inc., Abbott, Becton, Dickinson & Company, Medtronic, B. Braun Melsungen AG, Bayer AG, Smith and Nephew, Medline Industries, Inc., and Cardinal Health.

Some of the recent developments of key Medical Disposables providers are as follows:

In April 2019, Smith & Nephew PLC purchased Osiris Therapeutics, Inc. with the goal of expanding its advanced wound management product range.

In May 2019, 3M announced the acquisition of Acelity Inc., with the goal of strengthening wound treatment products.

For More Information: https://www.futuremarketinsights.com/reports/medication-dispenser-market

More Insights Available

Future Market Insights, in its new offering, presents an unbiased analysis of the Medical Disposables Market, presenting historical market data (2018-2022) and forecast statistics for the period of 2023-2033.

The study reveals essential insights by Product (Surgical Instruments & Supplies, Infusion, and Hypodermic Devices, Diagnostic & Laboratory Disposables, Bandages and Would Dressings, Sterilization Supplies, Respiratory Devices, Dialysis Disposables, Medical & Laboratory Gloves), by Raw Material (Plastic Resin, Nonwoven Material, Rubber, Metal, Glass, Others), by End-use (Hospitals, Home Healthcare, Outpatient/Primary Care Facilities, Other End-use) across five regions (North America, Latin America, Europe, Asia Pacific and Middle East & Africa).

Market Segments Covered in Medical Disposables Industry Analysis

By Product Type:

Surgical Instruments & Supplies

Would Closures

Procedural Kits & Trays

Surgical Catheters

Surgical Instruments

Plastic Surgical Drapes

By Raw Material:

Plastic Resin

Nonwoven Material

Rubber

Metals

Glass

Other Raw Materials

By End-use:

Hospitals

Home Healthcare

Outpatient/Primary Care Facilities

Other End-uses

2 notes

·

View notes

Text

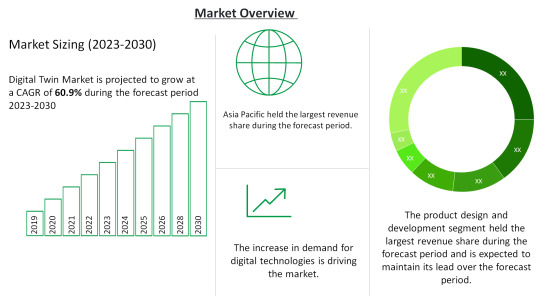

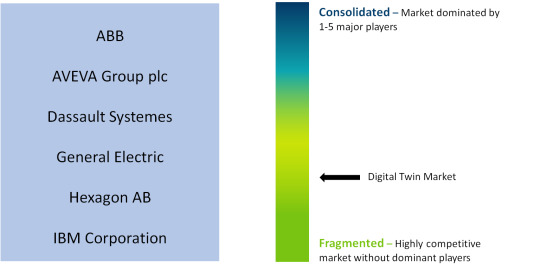

Digital Twin Market Size 2023-2030: ABB, AVEVA Group plc, Dassault Systemes

Digital Twin Market by Power Source (Battery-Powered, hardwired with battery backup, Hardwired without battery backup), Type (Photoelectric Smoke Detectors, Ionization Smoke Detectors), Service, Distribution Channel, and region (North America, Europe, Asia-Pacific, Middle East, and Africa and South America). The global Digital Twin Market size is 11.12 billion USD in 2022 and is projected to reach a CAGR of 60.9% from 2023-2030.

Click Here For a Free Sample + Related Graphs of the Report at: https://www.delvens.com/get-free-sample/digital-twin-market-trends-forecast-till-2030

Digital twin technology has allowed businesses in end-use industries to generate digital equivalents of objects and systems across the product lifecycle. The potential use cases of digital twin technology have expanded rapidly over the years, anchored in the increasing trend of integration with internet-of-things (IoT) sensors. Coupled with AI and analytics, the capabilities of digital twins are enabling engineers to carry out simulations before a physical product is developed. As a result, digital twins are being deployed by manufacturing companies to shorten time-to-market. Additionally, digital twin technology is also showing its potential in optimizing maintenance costs and timelines, thus has attracted colossal interest among manufacturing stalwarts, notably in discrete manufacturing.

The shift to interconnected environments across industries is driving the demand for digital twin solutions across the world. Massive adoption of IoT is being witnessed, with over 41 billion connected IoT devices expected to be in use by 2030. For the successful implementation and functioning of IoT, increasing the throughput for every part or “thing” is necessary, which is made possible by digital twin technology. Since the behavior and performance of a system over its lifetime depend on its components, the demand for digital twin technology is increasing across the world for system improvement. The emergence of digitalization in manufacturing is driving the global digital twin market. Manufacturing units across the globe are investing in digitalization strategies to increase their operational efficiency, productivity, and accuracy. These digitalization solutions including digital twin are contributing to an increase in manufacturer responsiveness and agility through changing customer demands and market conditions.

On the other hand, there has been a wide implementation of digital technologies like artificial intelligence, IoT, clog, and big data which is increasing across the business units. The market solutions help in the integration of IoT sensors and technologies that help in the virtualization of the physical twin. The connectivity is growing and so are the associated risks like security, data protection, and regulations, alongside compliance.

During the COVID-19 pandemic, the use of digital twin technologies to manage industrial and manufacturing assets increased significantly across production facilities to mitigate the risks associated with the outbreak. Amid the lockdown, the U.S. implemented a National Digital Twin Program, which was expected to leverage the digital twin blueprint of major cities of the U.S. to improve smart city infrastructure and service delivery. The COVID-19 pandemic positively impacted the digital twin market demand for twin technology.

Delvens Industry Expert’s Standpoint

The use of solutions like digital twins is predicted to be fueled by the rapid uptake of 3D printing technology, rising demand for digital twins in the healthcare and pharmaceutical sectors, and the growing tendency for IoT solution adoption across multiple industries. With pre-analysis of the actual product, while it is still in the creation stage, digital twins technology helps to improve physical product design across the full product lifetime. Technology like digital twins can be of huge help to doctors and surgeons in the near future and hence, the market is expected to grow.

Market Portfolio

Key Findings

The enterprise segment is further segmented into Large Enterprises and Small & Medium Enterprises. Small & Medium Enterprises are expected to dominate the market during the forecast period. It is further expected to grow at the highest CAGR from 2023 to 2030.

The industry segment is further segmented into Automotive & Transportation, Energy & Utilities, Infrastructure, Healthcare, Aerospace, Oil & Gas, Telecommunications, Agriculture, Retail, and Other Industries. The automotive & transportation industry is expected to account for the largest share of the digital twin market during the forecast period. The growth can be attributed to the increasing usage of digital twins for designing, simulation, MRO (maintenance, repair, and overhaul), production, and after-service.

The market is also divided into various regions such as North America, Europe, Asia-Pacific, South America, and Middle East and Africa. North America is expected to hold the largest share of the digital twin market throughout the forecast period. North America is a major hub for technological innovations and an early adopter of digital twins and related technologies.

During the COVID-19 pandemic, the use of digital twin technologies to manage industrial and manufacturing assets increased significantly across production facilities to mitigate the risks associated with the outbreak. Amid the lockdown, the U.S. implemented a National Digital Twin Program, which was expected to leverage the digital twin blueprint of major cities of the U.S. to improve smart city infrastructure and service delivery. The COVID-19 pandemic positively impacted the digital twin market demand for twin technology.

Regional Analysis

North America to Dominate the Market

North America is expected to hold the largest share of the digital twin market throughout the forecast period. North America is a major hub for technological innovations and an early adopter of digital twins and related technologies.

North America has an established ecosystem for digital twin practices and the presence of large automotive & transportation, aerospace, chemical, energy & utilities, and food & beverage companies in the US. These industries are replacing legacy systems with advanced solutions to improve performance efficiency and reduce overall operational costs, resulting in the growth of the digital twin technology market in this region.

Competitive Landscape

ABB

AVEVA Group plc

Dassault Systemes

General Electric

Hexagon AB

IBM Corporation

SAP

Microsoft

Siemens

ANSYS

PTC

IBM

Recent Developments

In April 2022, GE Research (US) and GE Renewable Energy (France), subsidiaries of GE, collaborated and developed a cutting-edge artificial intelligence (AI)/machine learning (ML) technology that has the potential to save the worldwide wind industry billions of dollars in logistical expenses over the next decade. GE’s AI/ML tool uses a digital twin of the wind turbine logistics process to accurately predict and streamline logistics costs. Based on the current industry growth forecasts, AI/ML might enable a 10% decrease in logistics costs, representing a global cost saving to the wind sector of up to USD 2.6 billion annually by 2030.

In March 2022, Microsoft announced a strategic partnership with Newcrest. The mining business of Newcrest would adopt Azure as its preferred cloud provider globally, as well as work on digital twins and a sustainability data model. Both organizations are working together on projects, including the use of digital twins to improve operational performance and developing a high-impact sustainability data model.

Reasons to Acquire

Increase your understanding of the market for identifying the best and most suitable strategies and decisions on the basis of sales or revenue fluctuations in terms of volume and value, distribution chain analysis, market trends, and factors

Gain authentic and granular data access for Digital Twin Market so as to understand the trends and the factors involved in changing market situations

Qualitative and quantitative data utilization to discover arrays of future growth from the market trends of leaders to market visionaries and then recognize the significant areas to compete in the future

In-depth analysis of the changing trends of the market by visualizing the historic and forecast year growth patterns

Direct Purchase of Digital Twin Market Research Report at: https://www.delvens.com/checkout/digital-twin-market-trends-forecast-till-2030

Report Scope

Report FeatureDescriptionsGrowth RateCAGR of 60.9% during the forecasting period, 2023-2030Historical Data2019-2021Forecast Years2023-2030Base Year2022Units ConsideredRevenue in USD million and CAGR from 2023 to 2030Report Segmentationenterprise, platform, application, and region.Report AttributeMarket Revenue Sizing (Global, Regional and Country Level) Company Share Analysis, Market Dynamics, Company ProfilingRegional Level ScopeNorth America, Europe, Asia-Pacific, South America, and Middle East, and AfricaCountry Level ScopeU.S., Japan, Germany, U.K., China, India, Brazil, UAE, and South Africa (50+ Countries Across the Globe)Companies ProfiledABB; AVEVA Group plc; Dassault Systems; General Electric; Hexagon AB; IBM Corp.; SAP.Available CustomizationIn addition to the market data for Digital Twin Market, Delvens offers client-centric reports and customized according to the company’s specific demand and requirement.

TABLE OF CONTENTS

Large Enterprises

Small & Medium Enterprises

Product Design & Development

Predictive Maintenance

Business Optimization

Performance Monitoring

Inventory Management

Other Applications

Automotive & Transportation

Energy & Utilities

Infrastructure

Healthcare

Aerospace

Oil & Gas

Telecommunications

Agriculture

Retail

Other Industries.

Asia Pacific

North America

Europe

South America

Middle East & Africa

ABB

AVEVA Group plc

Dassault Systemes

General Electric

Hexagon AB

IBM Corporation

SAP

About Us:

Delvens is a strategic advisory and consulting company headquartered in New Delhi, India. The company holds expertise in providing syndicated research reports, customized research reports and consulting services. Delvens qualitative and quantitative data is highly utilized by each level from niche to major markets, serving more than 1K prominent companies by assuring to provide the information on country, regional and global business environment. We have a database for more than 45 industries in more than 115+ major countries globally.

Delvens database assists the clients by providing in-depth information in crucial business decisions. Delvens offers significant facts and figures across various industries namely Healthcare, IT & Telecom, Chemicals & Materials, Semiconductor & Electronics, Energy, Pharmaceutical, Consumer Goods & Services, Food & Beverages. Our company provides an exhaustive and comprehensive understanding of the business environment.

Contact Us:

UNIT NO. 2126, TOWER B, 21ST FLOOR ALPHATHUM SECTOR 90 NOIDA 201305, IN +44-20-8638-5055 [email protected] WEBSITE: https://delvens.com/

#Digital Twin Market#Digital Twin#Digital Twin Market Size#Digital Twin Market Share#Semiconductors & Electronics

2 notes

·

View notes

Text

Fresenius Medical Care Returns to DAX 40 Index, Signaling Strong Recovery and Growth Prospects

Fresenius Medical Care AG & Co. KGaA, a leading global provider of products and services for individuals with renal diseases, has embarked on a digital transformation initiative known as Fmc4me. This initiative aims to enhance patient care, streamline operations, and improve overall service delivery in the field of kidney dialysis.

Background on Fresenius Medical Care

Founded in 1996 through the merger of Fresenius SE & Co. KGaA's dialysis business and W.R. Grace's National Medical Care, Fresenius Medical Care has grown to become a dominant player in the healthcare sector, particularly in renal care. The company operates over 4,171 outpatient dialysis centers worldwide, serving approximately 4.1 million patients who require regular dialysis treatment. With its headquarters in Bad Homburg vor der Höhe, Germany, and a significant presence in North America, Fresenius Medical Care holds a substantial market share in the dialysis industry.

The Fmc4me Initiative

The Fmc4me initiative represents Fresenius Medical Care's commitment to leveraging technology to enhance patient experiences and operational efficiencies. This program focuses on several key areas:

Patient Engagement: Fmc4me aims to improve communication and interaction between healthcare providers and patients. By utilizing digital tools, the initiative seeks to empower patients with information about their treatment options and health status.

Data Management: The initiative emphasizes the importance of data analytics in monitoring patient outcomes and optimizing treatment plans. By harnessing big data, Fresenius Medical Care can make informed decisions that enhance care quality.

Operational Efficiency: Fmc4me is designed to streamline internal processes within Fresenius Medical Care's facilities. This includes optimizing scheduling, resource allocation, and inventory management to reduce costs and improve service delivery.

Training and Development: A significant aspect of Fmc4me is the investment in employee training programs. By equipping healthcare professionals with the necessary skills to utilize new technologies effectively, Fresenius Medical Care aims to foster a culture of continuous improvement within its workforce.

Conclusion

The Fmc4me initiative represents a significant step forward for Fresenius Medical Care as it seeks to transform kidney care through digital innovation. By prioritizing patient engagement, data management, operational efficiency, and workforce development, the company is not only enhancing its service delivery but also positioning itself as a leader in the evolving landscape of healthcare technology.

1 note

·

View note

Text

Robotic Wheelchairs Market Report: Unlocking the Future of Mobility

Robotic Wheelchairs Market Report: Unlocking the Future of Mobility

The global Robotic Wheelchairs Marketsize was valued at USD 116.21 million in 2024 and is projected to grow from USD 132.48 million in 2025 to reach USD 263.65 million by 2033, growing at a CAGR of 8.99% during the forecast period (2025-2033).This remarkable growth is driven by the increasing demand for assistive technologies, advancements in robotics and artificial intelligence, and the rising need for independence among individuals with disabilities.

Request Sample Link:https://straitsresearch.com/report/robotic-wheelchair-market/request-sample

Robotic Wheelchairs Market Categorization

The Robotic Wheelchairs Market can be categorized into three main segments:

Application Outlook

Residential: Robotic wheelchairs designed for home use, providing users with independence and mobility within their living spaces.

Commercial: Robotic wheelchairs used in public spaces, such as shopping malls, airports, and healthcare facilities.

Wheelchair Type Outlook

Rear-Wheel Drive: Robotic wheelchairs with rear-wheel drive, providing stability and maneuverability.

Front-Wheel Drive: Robotic wheelchairs with front-wheel drive, offering improved traction and control.

Mid-Wheel Drive: Robotic wheelchairs with mid-wheel drive, providing a balance between stability and maneuverability.

Distributional Channel Outlook

Retail: Robotic wheelchairs sold through retail stores and dealerships.

E-commerce: Robotic wheelchairs sold online through e-commerce platforms.

Geographic Overview

The Robotic Wheelchairs Market can be geographically segmented into four main regions:

North America: The United States and Canada are expected to dominate the market, driven by the high adoption rate of assistive technologies and the presence of key players.

Europe: Germany, the United Kingdom, and France are expected to drive the market growth, driven by the increasing demand for robotic wheelchairs and the presence of key players.

Asia-Pacific: China, Japan, and India are expected to drive the market growth, driven by the large population, increasing demand for assistive technologies, and government initiatives.

Rest of the World: Brazil, Russia, and South Africa are expected to drive the market growth, driven by the increasing demand for robotic wheelchairs and government initiatives.

Top Players of Robotic Wheelchairs Market

Some of the key players operating in the Robotic Wheelchairs Market include:

Sunrise Medical LLC

Invacare Corporation

Permobil Corporation

Meyra GmbH

Karman healthcare

Ottobock SE & Company

Matia Robotics

Upnride Robotics

DEKA Research & Development

Whill Inc

Buy Now Link:https://straitsresearch.com/buy-now/robotic-wheelchair-market

Key Unit Economics for Businesses and Startups

For businesses and startups operating in the Robotic Wheelchairs Market, some key unit economics to consider include:

Production Costs: The cost of manufacturing robotic wheelchairs, including materials, labor, and overheads.

Marketing and Sales Expenses: The cost of promoting and selling robotic wheelchairs, including advertising, trade shows, and sales personnel.

Research and Development Expenses: The cost of developing new technologies and improving existing products.

Regulatory Compliance Costs: The cost of complying with regulatory requirements, including testing, certification, and labeling.

Robotic Wheelchairs Market Operational Factors

Some key operational factors to consider in the Robotic Wheelchairs Market include:

Supply Chain Management: Managing the supply chain to ensure timely delivery of components and materials.

Manufacturing and Quality Control: Ensuring that robotic wheelchairs are manufactured to high standards of quality and safety.

Customer Support and Service: Providing customers with support and service, including training, maintenance, and repair.

Regulatory Compliance: Ensuring that robotic wheelchairs comply with regulatory requirements, including safety standards and labeling.

Why Straits Research?

At Straits Research, we provide comprehensive market research reports that help businesses and startups navigate the complex landscape of the Robotic Wheelchairs Market. Our reports provide insights into market trends, opportunities, and challenges, as well as key player analysis and market forecasting.

With our expertise and knowledge, businesses and startups can make informed decisions, develop effective strategies, and stay ahead of the competition in the Robotic Wheelchairs Market.

#Robotic Wheelchairs Market#Robotic Wheelchairs Market Share#Robotic Wheelchairs Market Size#Robotic Wheelchairs Market Research

0 notes

Text

Introduction to Mobile IV Therapy: Revolutionizing Healthcare Delivery

The global mobile Intravenous (IV) therapy market is expected to register a rapid revenue CAGR during the forecast period. Rising demand for mobile IV therapy in various medical applications is a key factor driving market revenue growth. Mobile Intravenous therapy is a type of medical care that sends a large amount of essential vitamins and nutrients right into the bloodstream.

Get Download Pdf Sample Copy of this Report@ https://www.emergenresearch.com/request-sample/2481

Competitive Terrain:

The global Mobile Intravenous Therapy industry is highly consolidated owing to the presence of renowned companies operating across several international and local segments of the market. These players dominate the industry in terms of their strong geographical reach and a large number of production facilities. The companies are intensely competitive against one another and excel in their individual technological capabilities, as well as product development, innovation, and product pricing strategies.

The leading market contenders listed in the report are:

HydraMed, Mobile IV Medics, Inc., Drip Hydration, REVIV, Mobivive, NewGen IV, Liquid Mobile, and Thrive, Solutions MD

Key market aspects studied in the report:

Market Scope: The report explains the scope of various commercial possibilities in the global Mobile Intravenous Therapy market over the upcoming years. The estimated revenue build-up over the forecast years has been included in the report. The report analyzes the key market segments and sub-segments and provides deep insights into the market to assist readers with the formulation of lucrative strategies for business expansion.

Competitive Outlook: The leading companies operating in the Mobile Intravenous Therapy market have been enumerated in this report. This section of the report lays emphasis on the geographical reach and production facilities of these companies. To get ahead of their rivals, the leading players are focusing more on offering products at competitive prices, according to our analysts.

Report Objective: The primary objective of this report is to provide the manufacturers, distributors, suppliers, and buyers engaged in this sector with access to a deeper and improved understanding of the global Mobile Intravenous Therapy market.

Emergen Research is Offering Limited Time Discount (Grab a Copy at Discounted Price Now)@ https://www.emergenresearch.com/request-discount/2481

Market Segmentations of the Mobile Intravenous Therapy Market

This market is segmented based on Types, Applications, and Regions. The growth of each segment provides accurate forecasts related to production and sales by Types and Applications, in terms of volume and value for the period between 2022 and 2030. This analysis can help readers looking to expand their business by targeting emerging and niche markets. Market share data is given on both global and regional levels. Regions covered in the report are North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. Research analysts assess the market positions of the leading competitors and provide competitive analysis for each company. For this study, this report segments the global Mobile Intravenous Therapy market on the basis of product, application, and region:

Segments Covered in this report are:

Product Type Outlook (Revenue, USD; 2019–2032)

Infusion Pumps

IV Catheters

IV Fluids and electrolytes

Vitamins and Minerals

Medications

Application Outlook (Revenue, USD; 2019–2032)

Hydration Therapy

Nutrition Therapy

Vitamin Therapy

Pain Management

Medication Administration

Others

End-use Outlook (Revenue, USD; 2019–2032)

Clinics

Sports Centers

Home Care Settings

Ambulatory Surgical Settings (ASCs)

Others

Browse Full Report Description + Research Methodology + Table of Content + Infographics@ https://www.emergenresearch.com/industry-report/mobile-intravenous-therapy-market

Major Geographies Analyzed in the Report:

North America (U.S., Canada)

Europe (U.K., Italy, Germany, France, Rest of EU)

Asia Pacific (India, Japan, China, South Korea, Australia, Rest of APAC)

Latin America (Chile, Brazil, Argentina, Rest of Latin America)

Middle East & Africa (Saudi Arabia, U.A.E., South Africa, Rest of MEA)

ToC of the report:

Chapter 1: Market overview and scope

Chapter 2: Market outlook

Chapter 3: Impact analysis of COVID-19 pandemic

Chapter 4: Competitive Landscape

Chapter 5: Drivers, Constraints, Opportunities, Limitations

Chapter 6: Key manufacturers of the industry

Chapter 7: Regional analysis

Chapter 8: Market segmentation based on type applications

Chapter 9: Current and Future Trends

Request Customization as per your specific requirement@ https://www.emergenresearch.com/request-for-customization/2481

About Us:

Emergen Research is a market research and consulting company that provides syndicated research reports, customized research reports, and consulting services. Our solutions purely focus on your purpose to locate, target, and analyse consumer behavior shifts across demographics, across industries, and help clients make smarter business decisions. We offer market intelligence studies ensuring relevant and fact-based research across multiple industries, including Healthcare, Touch Points, Chemicals, Types, and Energy. We consistently update our research offerings to ensure our clients are aware of the latest trends existent in the market. Emergen Research has a strong base of experienced analysts from varied areas of expertise. Our industry experience and ability to develop a concrete solution to any research problems provides our clients with the ability to secure an edge over their respective competitors.

Contact Us:

Eric Lee

Corporate Sales Specialist

Emergen Research | Web: www.emergenresearch.com

Direct Line: +1 (604) 757-9756

E-mail: [email protected]

Visit for More Insights: https://www.emergenresearch.com/insights

Explore Our Custom Intelligence services | Growth Consulting Services

Trending Titles: Geocell Market | Pancreatic Cancer Treatment Market

Latest Report: Ceramic Tiles Market | Life Science Analytics Market

0 notes

Text

Challenges and Opportunities in the Portable Medical Devices Market

The global portable medical devices market size is expected to reach USD 146.4 billion by 2030 to expand at a CAGR of 11.30% from 2023 to 2030 according to a new report by Grand View Research, Inc. The growing adoption of technically advanced image-guided therapy systems and smart wearables, combined with an increasing demand for real-time and continuous monitoring, is expected to drive the market. Increasing awareness about the benefits of wearables, such as enhanced mobility, has also been attributed to an increase in the acceptance of portable medical devices in healthcare facilities.

Technological advancements and rising demand for home healthcare services are anticipated to drive the market in developing economies. Technological improvements in portable medical devices such as the introduction of new technologies to improve accuracy, utility, workflow, and convenience of access will raise the adoption, hence driving growth. In May 2022, Samsung announced the launch of a new portable digital radiography device, the GM85 Fit, which features a user-centric design for effective and efficient patient care. In December 2021, Nox Medical announced the launch of a Nox A1s PSG system that features the flexibility to use from hospital to home and product enhancements to its precursor, Nox A1.

There is a paradigm shift in people's choice toward home healthcare services as a result of the increase in economic burden and rise in the population of people aged 60 and above. In March 2021, Shimmer, a global pioneer in wearable technology applications, introduced Verisense Pulse+, a new sensor for the Verisense platform that includes a photoplethysmography sensor, a galvanic skin response sensor, and an inertial measurement unit. In addition to measuring the activity and sleep patterns of clinical trial participants, the device may also assess heart rate, oxygen saturation, and emotional responses. Therefore, the shift toward homecare settings is expected to increase the need for portable medical equipment.

Gather more insights about the market drivers, restrains and growth of the Portable Medical Devices Market

Portable Medical Devices Market Report Highlights

• In terms of product, the monitoring devices segment dominated the portable medical devices market in 2022. Technological advances, new product approvals, and benefits, such as compact design & portability, are factors driving the segment growth.

• Based on application, the other segment which includes application areas such as oncology, thoracic, vascular, and metabolic, dominated the global market in 2022. Increasing cancer prevalence and the rising use of imaging & image-guided treatment systems are among the key factors contributing to this growth.

• The cardiology segment is expected to hold the second-largest market share in 2022. Portable cardiology devices are gaining popularity in recent times due to the growing prevalence of cardiovascular diseases globally and the rising preference for minimally invasive or noninvasive treatment of these diseases.

• North America is estimated to dominate the market throughout the forecast period. High acceptance of technologically advanced devices, government initiatives to aid early detection of diseases, and high treatment rates are among the few drivers of the market.

Portable Medical Devices Market Segmentation

Grand View Research has segmented the global portable medical devices market based on product, application, and region:

Portable Medical Devices Product Outlook (Revenue, USD Million, 2018 - 2030)

• Diagnostic Imaging

o CT

o X-ray

o Ultrasound

o Endoscope

• Therapeutics

o Insulin Pump

o Nebulizer

o Oxygen Concentrator

o Image-guided Therapy Systems

• Monitoring Devices

o Cardiac Monitoring

o Holter Monitors

o Resting ECG System

o Stress ECG Monitors

o Event Monitoring Systems

o ECG Management Systems

o Neuromonitoring

o EEG Machines

o EMG Machines

o ICP Monitors

o MEG Machines

o Cerebral Oximeters

o Respiratory Monitoring

o Capnographs

o Spirometers

o Peak Flow Meters

o Fetal Monitoring

o Neonatal Monitoring

o Hemodynamic Monitoring Systems

o Vital Sign Monitors

• Smart Wearable Medical Devices

Portable Medical Devices Application Outlook (Revenue, USD Million, 2018 - 2030)

• Gynecology

• Cardiology

• Gastrointestinal

• Urology

• Neurology

• Respiratory

• Orthopedics

• Others

Portable Medical Devices Regional Outlook (Revenue, USD Billion, 2018 - 2030)

• North America

o U.S.

o Canada

• Europe

o U.K.

o Germany

o France

o Italy

o Spain

o Sweden

o Norway

o Denmark

• Asia Pacific

o Japan

o China

o India

o Australia

o Thailand

o South Korea

o New Zealand

• Latin America

o Brazil

o Mexico

o Argentina

• MEA

o South Africa

o Saudi Arabia

o UAE

o Kuwait

Order a free sample PDF of the Portable Medical Devices Market Intelligence Study, published by Grand View Research.

#Portable Medical Devices Market#Portable Medical Devices Market Size#Portable Medical Devices Market Share#Portable Medical Devices Market Analysis#Portable Medical Devices Market Growth

0 notes

Text

Dental Equipment Suppliers with the Fastest Delivery Times

In the fast-paced world of dentistry, having access to reliable dental equipment is crucial. Whether you're running a dental practice, clinic, or large healthcare facility, you understand the importance of getting the right tools quickly. In this competitive market, dental professionals often seek out the Best Dental Equipment Suppliers who can deliver high-quality products in the shortest time possible.

Why Delivery Speed Matters in Dental Equipment Supply

When a dental office experiences equipment shortages or urgent needs, downtime is not an option. A broken tool or an unexpected demand can disrupt appointments and reduce patient satisfaction. That's why speed in delivery is a key factor when choosing a dental equipment supplier. Quick delivery times ensure that dental professionals can continue their work seamlessly, without delays or compromising patient care.

Characteristics of the Best Dental Equipment Suppliers

Efficient Order Fulfillment The most effective dental suppliers have an organized and optimized order fulfillment process. This involves a streamlined system that tracks orders in real-time, ensures products are in stock, and guarantees on-time shipping. Suppliers who prioritize fast delivery are well-equipped with logistics systems that minimize any potential delays.

Inventory Management Best Dental Equipment Suppliers invest in inventory management tools to anticipate demand and ensure they can meet it swiftly. A supplier with a large inventory and a network of warehouses can offer faster shipping compared to one who doesn’t manage stock as efficiently.

Reliable Shipping Partners Fast delivery isn’t just about having the right equipment—it’s also about partnering with reliable shipping carriers. A trusted supplier will work with logistics companies that can deliver promptly, even for time-sensitive orders. Suppliers that offer expedited shipping options provide peace of mind when urgent situations arise.

24/7 Customer Support Good customer service is essential for fast and efficient delivery. Whether it’s for an urgent repair, a last-minute order, or troubleshooting a problem, the best dental equipment suppliers offer round-the-clock support to ensure customers are taken care of quickly.

Top Dental Equipment Suppliers Known for Fast Delivery

Henry Schein Henry Schein is a well-established name in the dental supply industry. Known for their vast selection of dental tools, equipment, and products, Henry Schein has earned a reputation for providing fast delivery times across North America. Their efficient logistics network allows them to offer expedited shipping options to meet the needs of their customers.

Darby Dental Supply Darby Dental Supply is another leading provider that offers quick deliveries. With a focus on customer satisfaction, Darby ensures that orders are processed efficiently and shipped as quickly as possible. Their excellent reputation among dental professionals is bolstered by their ability to meet urgent equipment needs on time.

Patterson Dental Patterson Dental is renowned for its wide range of dental equipment and tools. They focus on speed without compromising on quality, ensuring that dental practices receive their orders promptly. Their robust delivery network and quick order fulfillment make them a top choice for dental professionals who require timely deliveries.

Ultradent Products, Inc. Ultradent specializes in high-quality dental products, and they are known for providing fast and reliable delivery services. With a reputation for exceptional customer service, Ultradent’s commitment to fast delivery has made them a popular choice for dental offices that require swift restocking of supplies.

Choosing the Best Dental Equipment Suppliers means considering not just the quality of products, but also the speed at which they can deliver. The best suppliers are committed to ensuring that dental practices have the necessary tools and equipment on hand without delay. Whether it’s through a reliable supply chain, advanced inventory management, or strong logistics partnerships, the fastest dental equipment suppliers provide the timely service that professionals rely on. When speed matters, these suppliers are the ones who deliver, ensuring dental practices run smoothly and efficiently.

#b2bmedicalequipmentsuppliers#medicaldevicessuppliers#healthcareproductssuppliers#medicalsuppluchain#medicalproductsuppliers#hospitalequipmentsuppliers

0 notes

Text

Healthcare IT Integration: Future of Healthcare

Healthcare IT integration has become a cornerstone of modern healthcare systems, connecting diverse technologies to improve patient care, streamline operations, and enhance data management. From electronic health records (EHRs) to advanced telemedicine platforms, integration solutions are transforming healthcare delivery by ensuring seamless connectivity across multiple devices and systems.

Initially focused on simplifying data storage, healthcare IT integration now underpins a wide range of critical healthcare functions. Key applications include:

Electronic Health Records (EHRs): Centralized patient information enables better coordination of care and improved decision-making.

Telemedicine: Integration supports virtual consultations, remote monitoring, and real-time data sharing between patients and providers.

Medical Imaging: Enables rapid sharing and analysis of imaging data, enhancing diagnostic accuracy and treatment planning.

Hospital Automation Systems: Facilitates efficient workflow management, from scheduling to inventory control.

Learn more about the Report

Market Drivers: What’s Fueling the Growth?

Rising Demand for Digital Healthcare: Increasing adoption of digital tools in healthcare is driving the need for interoperable systems.

Regulatory Requirements: Compliance with healthcare standards like HIPAA mandates the integration of secure and efficient IT systems.

Shift Toward Value-Based Care: Integration supports outcomes-focused healthcare by enabling better patient tracking and analytics.

Proliferation of Telemedicine: The growth of virtual care models necessitates seamless connectivity between devices and platforms.

Key Market Segments

By Component

Software Integration Solutions: Facilitate interoperability and efficient data exchange across systems.

Hardware Integration Solutions: Provide the infrastructure for seamless connectivity and data management.

By Application

Hospitals: Ensure efficient management of patient records, diagnostics, and workflows.

Clinics: Enhance outpatient care through streamlined data sharing and monitoring.

Laboratories: Integrate diagnostic equipment for improved accuracy and reporting.

Regional Insights

North America: Dominates the market, supported by advanced healthcare infrastructure and high digital adoption.

Europe: Growth driven by widespread adoption of EHRs and telehealth technologies.

Asia-Pacific: Rapid expansion due to healthcare reforms and increasing investments in digital healthcare.

Rest of the World: Emerging markets show promise with growing investments in IT infrastructure.

Challenges Facing the Healthcare IT Integration Market

High Implementation Costs: Initial investments in integration solutions remain a barrier for smaller facilities.

Data Security Concerns: Protecting sensitive patient data from breaches is a critical challenge.

Interoperability Issues: Lack of standardized systems can hinder seamless integration.

Future Trends in the Healthcare IT Integration Market

AI and Machine Learning: Integration of AI into IT systems enhances predictive analytics and patient monitoring.

Blockchain Technology: Ensures secure, transparent, and tamper-proof medical records.

Cloud-Based Solutions: Support scalable and cost-effective integration models for healthcare providers.

IoT Integration: Connects wearable devices and sensors for real-time health monitoring and analysis.

Conclusion

The healthcare IT integration market is revolutionizing the way healthcare is delivered. By enabling seamless connectivity and efficient data sharing, these solutions are driving improved patient outcomes, operational efficiency, and cost savings. As technology advances and adoption increases, the healthcare IT integration market is set to play an even greater role in shaping the future of global healthcare.

Browse More:

Polyurea Coating Industry Segmentation Analysis

System Integrator Market Opportunities

0 notes

Text

Operational Technology Market Dynamics: Growth Drivers and Challenges

The global operational technology market size is expected to reach USD 364.74 billion by 2030, growing at a CAGR of 10% from 2024 to 2030, according to a new report by Grand View Research, Inc. The increased demand for operational technologies (OT) security solutions arises from the growing dependence on digital technologies within industrial systems, resulting in heightened vulnerability of OT systems to cyber threats. Furthermore, the imposition of strict government regulations, such as the cybersecurity framework aimed at enhancing industrial control systems (ICS), compels organizations to implement extensive OT security protocols. Moreover, the integration of IT and OT systems leads to increased interconnectedness, thereby exposing OT systems to cyber threats originating from IT networks. Consequently, there is an escalating need for resilient OT solutions to safeguard vital industrial processes against potential cyber risks.

Operational technologies enable direct control and monitoring of devices, processes, and events within the physical environment. Examples include DCS, SCADA, PLCs, BMS, CNC systems, and more. These technologies operate critical infrastructure such as manufacturing plants, power plants, and water treatment facilities, ensuring efficient and secure management of industrial processes. They are integral components of various essential systems in modern society, playing crucial roles in maintaining functionality and reliability while safeguarding against potential disruptions and hazards.

In the dynamic operational technology market, the competitive environment is in constant flux, prompting companies to continually innovate and develop fresh growth strategies to uphold their market leadership. Key players prioritize research and development to craft advanced security solutions infused with AI and machine learning. For instance, Huawei Technologies Co., Ltd. is poised to transform manufacturing by spearheading the integration of Information and Communications Technologies (ICT) and Operational Technologies (OT) to enable smarter production processes. In alignment with global initiatives such as Germany's Industry 4.0, China's Made in China 2025, and the US's Industrial Internet, Huawei is at the forefront of driving digitalization across every manufacturing sector.

In North America, operational technology serves as a cornerstone of industrial operations, supporting sectors including manufacturing, transportation and logistics, and healthcare. With a focus on efficiency and reliability, OT systems in North America are integral for maintaining critical infrastructure and ensuring smooth production processes. Companies in sectors such as automotive, aerospace, and energy rely heavily on OT to streamline operations and minimize downtime. As technological advancements continue to reshape industries in North America, the integration of OT with emerging technologies such as AI and automation holds the promise of further optimizing performance and driving innovation. Meanwhile, in the Asia Pacific region, operational technology plays a central role in fueling the rapid industrialization and economic growth of emerging economies.

Operational Technology Market Report Highlights

Computer Numerical Control (CNC) technology stands out as a dominant force within the operational technology market. Its widespread adoption across various industries, including manufacturing, aerospace, and automotive, highlights its significance in driving precision, automation, and efficiency in industrial processes

The wired segment is experiencing significant growth in 2023. This preference for wired solutions highlighted the reliability, security, and consistent performance that wired technologies offer, particularly in critical industrial settings where uninterrupted connectivity is paramount

The large enterprises segment has gained dominance in the market, with a significant market share in 2023. Their ability to invest in and implement advanced OT solutions is greater than that of smaller businesses, allowing them to streamline operations and enhance efficiency on a larger scale

The discrete Industry segment secured dominance in the market, capturing a substantial market share by 2023. OT solutions customized for discrete manufacturing environments offer capabilities such as real-time monitoring, quality control, and production optimization, which are essential for maximizing efficiency and ensuring product quality

Advancements in AI and machine learning are driving growth in the market. These technologies enable OT systems to swiftly analyze extensive data sets and generate actionable insights in real time. As a result, businesses can make informed decisions more efficiently, leading to enhanced productivity and overall performance

With the increasing connectivity of industrial systems and the rise of IoT devices, the vulnerability to cyber threats has become a significant concern for businesses. As a result, there's an increased focus on integrating robust cybersecurity measures into OT solutions to protect critical infrastructure and sensitive data

Operational Technology Market Segmentation

Grand View Research has segmented the global operational technology market based on component, connectivity, deployment, enterprise size, industry, and region:

Operational Technology (OT) Component Outlook (Revenue, USD Billion, 2017 - 2030)

Supervisory Control and Data Acquisition (SCADA)

Programmable Logic Controller (PLC)

Remote Terminal Units (RTU)

Human-machine Interface (HMI)

Others

Distributed Control System (DCS)

Manufacturing Execution System (MES)

Functional Safety

Building Management System (BMS)

Plant Asset Management (PAM)

Variable Frequency Drives (VFD)

Computer Numerical Control (CNC)

Others

Operational Technology (OT) Connectivity Outlook (Revenue, USD Billion, 2017 - 2030)

Wired

Wireless

Operational Technology (OT) Deployment Outlook (Revenue, USD Billion, 2017 - 2030)

Cloud

On-premises

Operational Technology (OT) Enterprise Size Outlook (Revenue, USD Billion, 2017 - 2030)

SMEs

Large Enterprises

Operational Technology (OT) Industry Outlook (Revenue, USD Billion, 2017 - 2030)

Process Industry

Oil & Gas

Chemicals

Pulp & Paper

Pharmaceuticals

Mining & Metals

Energy & Power

Others

Discrete Industry

Automotive

Semiconductor & Electronics

Aerospace & Defense

Heavy Manufacturing

Others

Operational Technology (OT) Regional Outlook (Revenue, USD Billion, 2017 - 2030)

North America

US

Canada

Europe

UK

Germany

France

Asia Pacific

China

Japan

India

South Korea

Australia

Latin America

Brazil

Mexico

Middle East and Africa

Kingdom of Saudi Arabia (KSA)

UAE

South Africa

Order a free sample PDF of the Operational Technology Market Intelligence Study, published by Grand View Research.

0 notes

Text

Breathable Antimicrobial Coatings Market

Breathable Antimicrobial Coatings Market Size, Share, Trends: Sherwin-Williams Company Leads

Integration of Nanotechnology for Enhanced Performance

Market Overview:

The Breathable Antimicrobial Coatings Market is experiencing robust growth, driven by the global emphasis on hygiene and infection control, particularly in the aftermath of the COVID-19 outbreak. North America currently leads the market, thanks to advanced healthcare infrastructure, stringent regulations on hygiene and safety, and increasing awareness about infection control. Key metrics include rising demand for antimicrobial surfaces in healthcare settings, growing concerns about indoor air quality, and increasing applications in the construction and food industries.

These coatings are extremely beneficial in various applications requiring moisture management and microbial control due to their unique mix of breathability and antibacterial properties. The market is growing rapidly as industries seek to adopt innovative solutions to ensure hygiene and safety across different sectors.

DOWNLOAD FREE SAMPLE

Market Trends:

The application of nanotechnology in breathable antimicrobial coatings is transforming the market. Nanoparticles of silver, copper, and zinc oxide are increasingly being utilized in coating formulations to enhance antimicrobial efficacy while maintaining breathability. This trend is particularly evident in the healthcare and consumer products industries, where there is a growing demand for high-performance, long-lasting antimicrobial surfaces.

Recent advancements in nanoengineered coatings have led to improved durability, efficacy against a broader spectrum of microorganisms, and a reduced environmental impact. For instance, several companies have developed nanosilver-based coatings that provide antimicrobial protection for up to five years, significantly longer than standard coatings. Nanotechnology also allows for precise control over the release of antimicrobial compounds, ensuring prolonged protection while preserving the coating's breathability.

Market Segmentation:

The Medical & Healthcare segment is expected to dominate the Breathable Antimicrobial Coatings market during the forecast period. This segment's expansion is primarily driven by a higher emphasis on infection control in healthcare settings, rising healthcare expenses, and stringent regulations governing hospital hygiene and patient safety.

Recent advancements in the Medical & Healthcare market have focused on developing coatings that are not only effective against a wide range of infections but also compatible with a variety of medical devices and surfaces. For example, many manufacturers have developed breathable antimicrobial coatings specifically for medical fabrics such as healthcare uniforms and patient gowns, combining antimicrobial protection with moisture management capabilities.

The COVID-19 pandemic has accelerated the adoption of breathable antimicrobial coatings in healthcare facilities. Hospitals and clinics are increasingly applying these coatings on high-touch surfaces such as doorknobs, bed rails, and medical equipment to reduce the risk of disease transmission. A study published in the American Journal of Infection Control indicated that applying copper-based antimicrobial coatings on hospital surfaces reduced healthcare-associated infections by 58%.

Furthermore, the growing trend of outpatient and home healthcare has created new opportunities for breathable antimicrobial coatings. These coatings are increasingly being used on home medical equipment and surfaces to create a safer environment for patients receiving care outside of traditional hospital settings.

Market Key Players:

The Breathable Antimicrobial Coatings market is characterized by the presence of numerous global and regional manufacturers. Major players include Sherwin-Williams Company, AkzoNobel N.V., PPG Industries, Inc., DuPont de Nemours, Inc., BASF SE, and Axalta Coating Systems Ltd. These companies are at the forefront of innovation, continuously striving to enhance product performance and sustainability.

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

Medical Drone Market Size, Share, Trends Overview & Growth Prospects by 2032

The global medical drone market size was valued at USD 1.25 billion in 2023 and is expected to be worth USD 1.47 billion in 2024. The market is projected to reach USD 4.68 billion by 2032, recording a CAGR of 17.9% during the forecast period.

A medical drone refers to an unmanned system that can transport large quantities of medical items and other essential supplies. The COVID-19 pandemic was instrumental in boosting the demand for these drones to deliver essential supplies and vaccines in remote areas. Countries across the world had set up the required infrastructure and facilities to improve the use of drones. These factors are expected to boost the medical drone market growth.

Fortune Business Insights™ displays this information in a report titled, "Medical Drone Market, 2024-2032."

Informational Source:

LIST OF KEY COMPANIES PROFILED IN THE REPORT

Aquiline Drones (U.S.)

Avy (Netherlands)

Bell Flight – Textron (U.S.)

Draganfly Innovations (Canada)

Drone Delivery Canada Corp. (Canada)

Freefly Systems (U.S.)

Aether Global Innovations Corporation (Formerly, Plymouth Rock Technologies Inc.) (U.S.)

Skyports Ltd. (U.K.)

Vayu Inc. (U.S.)

Workhorse Group (U.S.)

Segments:

Great Vertical Lift Capacity to Boost Adoption of Rotary-Wing Drones

Based on type, the market is categorized into fixed wing, rotary-wing, and hybrid. The rotary-wing segment is set to dominate the market as these drones have a high vertical lift capacity and can easily carry large loads due to the presence of micro turbine equipment.

Remotely Operated Drones to Gain Traction Due to their Robust Applications in Medical Field

By technology, the market is classified into remotely operated, semi-autonomous, and fully autonomous. The remotely operated segment is anticipated to be the largest segment as these systems are being widely used in several medical applications.

Demand for 2-5 kg Drones to Rise with Growing Inclination toward Medium Load Drones

Based on package size, the market is divided into less than 2 kg, 2 – 5 kg, and more than 5 kg. The 2-5 kg segment captured the largest market share in 2022 due to robust demand for medium payload drones.

Rising Demand for Urgent Blood Samples to Boost Product Use in Emergency Blood Logistic Applications

Based on application, the market is bifurcated into emergency blood logistics, medical drug & vaccine, emergency organ logistics, and others. The emergency blood logistics segment held the largest market share in 2022 due to the strong demand for emergency blood during accidents and to supply blood and pathological samples.

With respect to region, the market covers North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage:

The report studies the market in depth and highlights key companies, product types, and leading product applications. It also offers important insights into the latest market trends and market competition, and covers key industry developments. Besides the abovementioned factors, the report mentions several other factors that have contributed to the market’s growth in recent years.

Drivers and Restraints:

Rising Use of Drones in First Responder Operations to Support Market Growth

The use of drones has grown tremendously in recent years as they are known to offer vital assistance in search & rescue operations and disaster management. These widespread applications of drones have boosted their demand in the healthcare sector. These systems can transport first aid, essential goods, vital organs, and many other goods to remote areas, thereby improving their adoption for medical purposes.

However, lack of availability of skilled pilots and adequate infrastructure can impede the market’s growth.

Regional Insights:

North America Market to Gain Momentum with Robust Presence of Reputed OEMs

The North America market is set to dominate the global market as the region has a vast presence of leading OEMs and the demand for these drones is rising across the region. In fact, the U.S. was one of the first countries to use advanced drones during the pandemic, which will further enhance the regional market’s growth.

The Asia Pacific region is predicted to record the highest CAGR as the region is noticing a substantial rise in the number of drones being exported to other regions such as Europe and North America.

Competitive Landscape:

Key Companies to Focus on Offering Different Services to Cement Market Position

Leading market players have a vast variety of products and services to offer and are focused on providing the best drones that enable fastest deliveries. Some of the top players in this market include Vayu Inc., Bell Flight – Textron, Zipline Inc., Avy, Aquiline Drones, and UPS, among many others.

Key Industry Development:

October 2023 - Intermountain Healthcare, a healthcare NPO, introduced its drone delivery services in South Jordan. These services were launched in partnership with Zipline Inc., a global medical drone services provider.

0 notes

Text

Blood Bank Market Size & Forecast 2025-2035

The global Blood Bank market, estimated to be valued at USD 21.85 billion in 2024, is estimated to grow up to USD 41.05 billion by 2035 with a CAGR of 5.9% in the period from 2025 to 2035. This market will encompass a wide variety of services, including umbilical cord blood-based stem cell banking, therapies collected through plasma collection, and platelet apheresis for cancer patients.

Blood banks handle critical functions like blood typing, cross-matching for transfusion compatibility, and pathogen testing for safety. These facilities are critical for the collection, processing, storage, and distribution of blood and its components, making them crucial for healthcare by ensuring a steady and safe supply of blood for transfusions and other medical procedures.

Market Dynamics

Mobile Blood Donation units increase mobilization

Mobile blood donation units are changing the face of blood donation. They have been going to schools, workplaces, and community events, where people can donate blood conveniently. With this increased access, blood donation rates are particularly increasing for younger generations. Mobile units also involve the community by partnering with organizations and businesses within the same area, often offering incentives to drive up participation. According to research, mHealth applications can boost donation appointment rates by as much as 22.7%. This could save hundreds of thousands of lives every year.

Challenges of Short Shelf Life for Blood Products

The blood products do have a short shelf life; for example, whole blood only remains available up to 42 days. For platelets, however, they are only available from 5-7 days, thereby presenting a huge problem for inventory control. Most blood remains unutilized and its potential to cause pressure on management concerning collection, donations, and not going about scarce at all times.

AI-Enhanced Blood Management Solutions

Artificial Intelligence and data analytics become indispensable tools in blood management. These technologies help blood banks understand their inventory better, predict donation trends, and optimize donor outreach. Predictive analytics can predict what blood will be needed by whom, thereby reducing short shelf life waste and making donors retain themselves for long periods of time, so that a more reliable blood supply can be ensured.

Expert opinions

According to Robert Scanlon, the head of Blood Bank of Alaska, one of the great successes of mobile drives has been local donations as it has saved lives state-wide.

Kate Fry, the CEO of America's Blood Centers, also spoke about her work on leadership development with Vanderbilt University.

Get A Free Sample Report @Click Here

Market Segmentation

Product Type

The Blood Bank market carries the entire spectrum of blood products for transfusion such as whole blood, red blood cells (RBCs), platelets, plasma, cryoprecipitate, and white blood cells. Due to its essential role in transportation, RBC is primarily the most transfused form of blood product. Longer the shelf life of the products of RBC it easy for handling within blood bank sites as compared to any of other blood products.

Function Type

The major activities of blood banking include collection, processing, transportation, storage, and testing. Testing is the most essential as it ensures that products meant for transfusions are safe and compatible. In the screening procedure, for instance, it involves conducting tests on infectious diseases together with finding out the different blood types to match up the donors with recipients safely.

Regional Analysis

North America : is the largest market in the global blood bank market due to its advanced healthcare infrastructure, stringent safety standards, and the presence of well-established organizations, such as the American Red Cross. Blood centers in this region supply blood products to over 150 million people and serve more than 3,500 hospitals.

Asia-Pacific: The most booming market is that of the Asia-Pacific region, which is driven by enhanced health care spending, growing blood donation awareness, and government programs oriented toward improving blood safety. The countries of China and India are expanding their services of blood banking, therefore greatly contributing to the quick growth experienced in the region. Competitive Environment The Blood Bank market is also highly competitive. Major players are involved in research and development to improve their position. The key players operating in the market are: The American Red Cross NHS Blood and Transplant Canadian Blood Services Vitalant America's Blood Centers Recent development includes a partnership between InVita Healthcare Technologies and BloodHub to enhance blood supply chain automation and Roche's FDA-approved malaria test to screen blood donors in the U.S. Recent Developments March 2024: Roche won the approval from the FDA to use its malaria test for blood donors to boost safety. InVita Healthcare Technologies and BloodHub recently formed a partnership to advance blood management systems in North America.

Conclusion :

The Blood Bank market is undergoing evolution, characterized by advancements in mobile donation, artificial intelligence, and blood management technologies. Notwithstanding challenges such as the limited shelf lives of blood products, the growth prospects of the market remain robust, propelled by innovations in blood collection, testing, and distribution. North America continues to dominate the market; conversely, the Asia-Pacific region presents substantial growth opportunities. Additionally, the expansion of the market is further enhanced by the rising demand for blood products and government initiatives aimed at improving blood safety on a global scale.

0 notes

Text

Precision Diagnostics Market Surge: $57.5B in 2023 to $157.2B by 2033 (10.5% CAGR)

Precision Diagnostics Market focuses on advanced technologies and methodologies designed to enhance the accuracy of disease detection and support personalized healthcare solutions. This includes molecular diagnostics, imaging technologies, and bioinformatics tools that enable early, precise diagnosis, tailored treatment planning, and ongoing monitoring. The market plays a vital role in the shift toward personalized medicine, which improves patient outcomes and optimizes healthcare resources by offering individualized diagnostic solutions.

To Request Sample Report: https://www.globalinsightservices.com/request-sample/?id=GIS22118 &utm_source=SnehaPatil&utm_medium=Article

Market Growth and Trends

The Precision Diagnostics Market is experiencing robust growth, driven by advancements in molecular diagnostics and imaging technologies. Among the sub-segments, molecular diagnostics lead the market due to their pivotal role in personalized healthcare and early disease detection. Next-generation sequencing (NGS) is the top performer within this segment, thanks to its precision, growing accessibility, and declining costs. Imaging diagnostics, particularly MRI and CT scans, also represent a significant segment, benefitting from ongoing technological advancements and rising healthcare expenditure.

Regional Insights

North America dominates the market, fueled by a strong healthcare infrastructure, substantial R&D investments, and a high adoption rate of innovative diagnostic technologies. The United States is the leading country, driven by advanced healthcare facilities and widespread implementation of precision diagnostics.

Europe ranks second, with Germany and the United Kingdom emerging as key contributors, spurred by increasing demand for early disease diagnosis and precise medical interventions.

Asia-Pacific is rapidly growing, with China and India seeing significant market expansion. The region’s growth is driven by increasing healthcare awareness, rising income levels, and improved access to diagnostic technologies.

Market Segmentation

By Type: Genetic Testing, Molecular Diagnostics, Companion Diagnostics, Point-of-Care Testing, Liquid Biopsy By Product: Reagents & Kits, Instruments, Software & Services, Consumables By Technology: Next-Generation Sequencing, Polymerase Chain Reaction, Fluorescence In Situ Hybridization, Immunohistochemistry, Microarray By Application: Oncology, Cardiology, Infectious Diseases, Neurology, Endocrinology By End User: Hospitals, Diagnostic Laboratories, Research Institutes, Academic Institutes By Component: Hardware, Software, Services By Device: Benchtop, Portable, Handheld, Wearable By Process: Sample Preparation, Data Analysis, Validation By Deployment: On-Premise, Cloud-Based, Hybrid By Solutions: Clinical Decision Support, Data Management, Patient Engagement

Market Volume & Projections

In 2023, the market demonstrated a strong volume of 320 million diagnostic tests globally, with projections indicating a rise to 520 million tests by 2033. The molecular diagnostics segment commands a substantial 45% market share, followed by genetic testing at 30%, and imaging diagnostics at 25%. This market dominance is driven by advancements in genomics and a growing demand for personalized medicine.

Key Market Players

Leading players in the Precision Diagnostics Market include Roche Diagnostics, Abbott Laboratories, and Thermo Fisher Scientific, which continue to influence the market through cutting-edge technology, strategic partnerships, and ongoing innovation to maintain their competitive edge.

#PrecisionDiagnostics #PersonalizedHealthcare #MolecularDiagnostics #GeneticTesting #NextGenerationSequencing #Oncology #Cardiology #EarlyDiagnosis #HealthcareInnovation #ImagingTechnologies #LiquidBiopsy #Bioinformatics #MedicalDevices #HealthcareSolutions #DiagnosticReagents

0 notes

Text

Veno Venous Extracorporeal Life Support (VV ECLS) Devices Market

Veno-Venous Extracorporeal Life Support (VV ECLS) Devices Market Size, Share, Trends: Getinge AB Leads

Integration of artificial intelligence and machine learning in VV ECLS systems

Market Overview:

The global Veno-Venous Extracorporeal Life Support (VV ECLS) Devices Market is expected to develop at a CAGR of 5.7% between 2024 and 2031. The market's worth is predicted to increase from USD XX million in 2024 to USD YY million by 2031. North America now leads the industry, with key data demonstrating widespread acceptance in specialized healthcare facilities and research organizations. The market is expanding steadily, owing to the rising prevalence of acute respiratory distress syndrome (ARDS), developments in ECLS technology, and increased investments in critical-care infrastructure.

DOWNLOAD FREE SAMPLE

Market Trends:

The integration of AI and ML technology into VV ECLS devices is transforming critical care management. These modern technologies improve the precision of oxygen administration, automate pump flow adjustments, and offer real-time predictive analytics for patient outcomes.