#Maltodextrin Industry Trends.

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Average visit duration of Tumblr.com is 10 mins and 25 secs.

Text

Maltodextrin Price | Prices | Pricing | News | Database | Chart | ChemAnalyst

Maltodextrin is a widely used food additive derived from starches such as corn, rice, potato, or wheat. Its role in the food and beverage industry is significant due to its thickening, stabilizing, and sweetening properties, and as such, the dynamics of its market pricing are highly relevant. Over the past few years, maltodextrin prices have experienced variations driven by multiple factors, including raw material costs, global supply chains, and consumer demand trends.

A key driver of maltodextrin pricing is the availability and cost of starch sources. Since the majority of maltodextrin production is based on corn and other starches, any significant changes in these commodities' market conditions can ripple through the maltodextrin market. For instance, corn prices can be influenced by a range of factors such as crop yields, climate changes, geopolitical issues, and trade policies. The growing adoption of biofuels, which relies heavily on corn, can also exert upward pressure on maltodextrin prices when corn becomes more expensive. Such interconnections make it clear that maltodextrin price trends are often linked to broader agricultural market dynamics.

Get Real Time Prices for Maltodextrin: https://www.chemanalyst.com/Pricing-data/maltodextrin-1608Regional disparities in the production and supply of maltodextrin also contribute to pricing variations. Major producers in regions such as North America, Europe, and Asia maintain distinct market dynamics based on their local cost structures and regulatory environments. For example, North America benefits from a strong corn production base, which can lead to relatively lower production costs compared to regions where corn imports are more expensive. On the other hand, Europe's stricter regulations concerning genetically modified organisms (GMOs) can drive higher production costs for non-GMO maltodextrin, which may translate into higher prices for specific product grades in that market.

Maltodextrin’s applications span diverse industries, including food and beverage, pharmaceuticals, personal care, and agriculture. Its role as a versatile thickener and stabilizer, particularly in sports drinks, instant foods, and dietary supplements, continues to drive demand. Changes in consumer preferences and lifestyle trends, such as the growing popularity of health and wellness products, have further boosted the demand for clean-label and low-calorie products containing maltodextrin. As consumer demand shapes product innovation, producers are inclined to develop high-value maltodextrin products that can command premium pricing, adding another layer of complexity to overall market trends.

Energy prices and labor costs also significantly influence the cost of producing maltodextrin, given the energy-intensive nature of the manufacturing process. Variations in energy prices, including fuel, electricity, and transportation costs, can therefore affect the final pricing. The energy market’s volatility, driven by geopolitical tensions and policy changes, contributes to the instability in production costs. Furthermore, labor shortages and increased labor costs, as observed in certain regions post-pandemic, can add additional pressures on maltodextrin pricing.

In recent years, sustainability has become a focal point for manufacturers and consumers alike. The growing emphasis on environmentally friendly and sustainable production practices can influence maltodextrin prices. Companies are investing in greener technologies, more efficient processes, and sustainable sourcing of raw materials to meet consumer demand and comply with stringent regulatory frameworks. While these initiatives may lead to higher production costs initially, the long-term cost efficiencies and the market value associated with eco-friendly products could stabilize pricing over time. Moreover, companies adopting sustainable practices may find it easier to market and differentiate their products in a competitive market landscape, which can justify premium pricing.

Global trade dynamics, including tariffs, import/export restrictions, and free trade agreements, can significantly impact maltodextrin prices. For instance, increased tariffs on raw materials or finished maltodextrin products can lead to higher market prices, while favorable trade agreements can promote price stability. Trade tensions between major economies may also affect the market by disrupting supply chains or altering demand in specific regions. In this respect, producers must carefully monitor international trade policies to mitigate risks and optimize pricing strategies.

To further understand maltodextrin pricing trends, market participants are increasingly relying on technological advancements and data analytics. Real-time data, predictive analytics, and digital supply chain solutions allow for more accurate price forecasting and inventory management. By leveraging these tools, manufacturers and buyers can adapt to changing market conditions more effectively, reducing the impact of price volatility on their business operations. Furthermore, technology-driven innovations in maltodextrin production processes may also lead to cost reductions, contributing to potential price decreases in the long run.

The demand for maltodextrin is also shaped by macroeconomic factors, including inflation rates, currency fluctuations, and overall economic growth. Rising inflation can lead to increased production costs, which can then be passed on to consumers. Similarly, currency devaluation in key producing countries can make exports more attractive, potentially affecting global pricing. Economic growth in emerging markets can also drive demand, as higher disposable incomes lead to increased consumption of processed foods and beverages where maltodextrin is commonly used.

In conclusion, maltodextrin prices are influenced by a complex interplay of factors that include raw material costs, regional production dynamics, consumer trends, energy prices, sustainability initiatives, and global trade policies. The market’s complexity underscores the need for stakeholders to adopt flexible pricing strategies, leverage technological advancements, and remain adaptable to ever-changing market conditions. This approach will help ensure competitiveness and sustainability in the evolving global maltodextrin market.

Get Real Time Prices for Maltodextrin: https://www.chemanalyst.com/Pricing-data/maltodextrin-1608

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Maltodextrin#Maltodextrin Price#Maltodextrin Prices#Maltodextrin Pricing#Maltodextrin News#Maltodextrin Price Monitor#Maltodextrin Database#Maltodextrin Price Chart

0 notes

Text

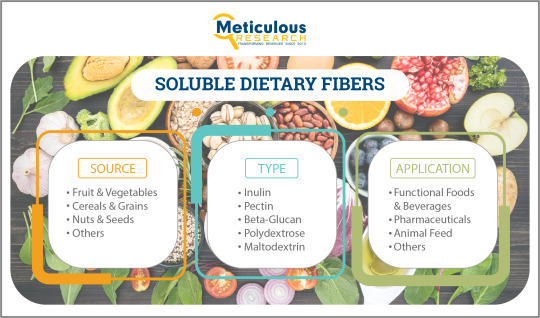

Soluble Dietary Fibers: Driving Growth in the Health and Wellness Market

The global soluble dietary fibers market is on an upward trajectory, driven by increased health consciousness and a growing understanding of the benefits associated with dietary fibers. According to a recent report by Meticulous Research®, the market is projected to expand at a compound annual growth rate (CAGR) of 7.8%, reaching an estimated value of $4.99 billion by 2029. This growth can be attributed to various factors, including rising incidences of chronic diseases, increasing demand for functional foods, and supportive government initiatives aimed at promoting healthier food choices.

This article delves into the intricacies of the soluble dietary fibers market, examining key segments, growth drivers, challenges, and future opportunities.

Download Sample Report Here - https://www.meticulousresearch.com/download-sample-report/cp_id=3953?utm_source=article&utm_medium=social&utm_campaign=product&utm_term=17-10-24

Market Overview

Soluble dietary fibers are essential components of a balanced diet, offering numerous health benefits such as improved digestive health, lower cholesterol levels, and enhanced blood sugar control. These fibers can be derived from various sources, including fruits, vegetables, cereals, and grains, and are utilized in numerous applications, particularly in pharmaceuticals and animal feed.

Market Segmentation

The soluble dietary fibers market can be segmented based on the following criteria:

Source: This includes fruits and vegetables, cereals and grains, nuts and seeds, and others.

Type: This encompasses various forms such as inulin, pectin, beta-glucan, polydextrose, maltodextrin, oligofructose, arabinoxylan-oligosaccharides, and others.

Application: This covers functional foods and beverages, pharmaceuticals, animal feed, and other uses.

Growth Drivers

Several key factors are propelling the growth of the soluble dietary fibers market:

Health Consciousness As consumers become increasingly aware of the health benefits associated with dietary fibers, the demand for products containing these nutrients has surged. Soluble fibers, known for their ability to aid digestion and contribute to heart health, are becoming integral to health-conscious diets.

Rising Incidences of Chronic Diseases The prevalence of chronic conditions such as diabetes, obesity, and cardiovascular diseases has spurred demand for functional foods rich in soluble dietary fibers. These fibers play a critical role in disease management, driving both consumer demand and industry supply.

Incorporation into Pharmaceutical and Food Products Pharmaceutical companies are increasingly integrating soluble dietary fibers into their products to enhance therapeutic effects, while food manufacturers are utilizing these fibers as stabilizers, texturizers, and low-calorie sweeteners. This dual demand further fuels market growth.

Government Initiatives Various governments worldwide are implementing policies to promote healthy eating habits and dietary fiber intake. Such initiatives aim to combat rising health concerns linked to poor diets, creating a conducive environment for market expansion.

Emerging Applications Innovations in the use of soluble dietary fibers in various applications, such as functional beverages and health supplements, are paving the way for new growth opportunities. This trend is particularly evident in emerging markets in Southeast Asia, Latin America, and the Middle East and Africa.

Challenges to Market Growth

Despite the positive growth trajectory, the soluble dietary fibers market faces several challenges that could hinder its expansion:

Regulatory Hurdles The lengthy and costly regulatory approval process for dietary supplements can delay product launches, posing challenges for manufacturers seeking to introduce new soluble fiber products into the market.

High Manufacturing Costs The production of soluble dietary fibers can be capital-intensive, with high manufacturing costs potentially limiting the market's accessibility to smaller players. This economic barrier can lead to a concentrated market dominated by established companies.

Consumer Misunderstanding Although awareness of dietary fibers is increasing, there may still be a gap in consumer understanding regarding the differences between various types of fibers. This misunderstanding could lead to hesitance in purchasing fiber-enriched products.

Segmentation Analysis

By Source

The market for soluble dietary fibers can be categorized based on the source of these fibers, with the following insights:

Fruits & Vegetables: In 2022, this segment is expected to command the largest share of the market, owing to the high content of soluble dietary fibers such as inulin, pectin, and beta-glucan found in various fruits and vegetables. The increasing consumption of functional food products will likely drive growth in this segment.

Cereals & Grains: While this segment holds significant potential, it is anticipated to grow at a more modest rate compared to fruits and vegetables. The increasing incorporation of whole grains in diets supports this segment's expansion.

Nuts & Seeds: As awareness of the health benefits associated with nuts and seeds rises, this segment is expected to see gradual growth.

By Type

Examining the types of soluble dietary fibers, several trends emerge:

Beta-Glucan: Projected to register the highest CAGR during the forecast period, beta-glucan is gaining popularity due to its versatile applications across various industries. Its usage in cereals, baked goods, soups, sauces, and sports drinks is propelling its growth.

Inulin and Pectin: While these segments are also significant, their growth rates may not match that of beta-glucan. Nonetheless, they remain essential components of the dietary fiber market.

Get A Glimpse Inside: Request Sample Pages - https://www.meticulousresearch.com/download-sample-report/cp_id=3953?utm_source=article&utm_medium=social&utm_campaign=product&utm_term=17-10-24

By Application

The application of soluble dietary fibers can be analyzed as follows:

Food & Beverage: In 2022, the food and beverage segment is anticipated to dominate the market. The increasing demand for sugar-free and low-calorie food products, coupled with health consciousness, drives this segment's growth. Major companies, such as Ingredion Inc. and Cargill, Inc., are actively investing in R&D to develop innovative products.

Pharmaceuticals: The incorporation of soluble dietary fibers into pharmaceutical products is an emerging trend, expected to contribute significantly to market growth.

Animal Feed: The demand for soluble dietary fibers in animal feed is also rising as manufacturers recognize their nutritional benefits, leading to improved animal health.

Regional Insights

The global market for soluble dietary fibers exhibits significant regional variation:

Asia-Pacific: This region is projected to grow at the fastest CAGR during the forecast period. Factors such as rising health awareness, a booming food and beverage industry in countries like China, India, Japan, and Indonesia, and an increase in fitness clubs are contributing to this rapid growth.

North America and Europe: These regions are established markets for soluble dietary fibers, driven by high consumer awareness and demand for health-oriented products.

Latin America and the Middle East & Africa: These emerging markets are anticipated to offer lucrative opportunities for growth, as consumer awareness and demand for healthy food options increase.

Competitive Landscape

The soluble dietary fibers market is characterized by a mix of established players and emerging companies. Key players operating in this market include:

Tate & Lyle plc (U.K.)

DuPont de Nemours, Inc. (U.S.)

Nexira (France)

Roquette Frères (France)

Cosucra Groupe Warcoing SA (Belgium)

FutureCeuticals, Inc. (U.S.)

Sensus B.V. (Netherlands)

BENEO GmbH (Germany)

The Archer-Daniels-Midland Company (U.S.)

Ingredion Incorporated (U.S.)

Herbafood Ingredients GmbH (Germany)

Cargill, Inc. (U.S.)

Lonza Group AG (Switzerland)

Kerry Group plc (Ireland)

Tereos S.A. (France)

Frutarom Industries Ltd. (Israel)

These companies are investing in research and development, product innovation, and strategic partnerships to enhance their market presence.

Future Outlook

The soluble dietary fibers market is poised for substantial growth in the coming years, fueled by increasing health consciousness, rising demand from various sectors, and supportive government policies.

Key Trends to Watch:

Innovation in Applications: Continued innovation in product formulations that incorporate soluble dietary fibers will drive demand across various industries, including food, pharmaceuticals, and animal feed.

Sustainability Initiatives: As consumers become more environmentally conscious, companies are likely to focus on sustainable sourcing and production practices, impacting their supply chains.

Increased Investment in R&D: Companies will continue to invest in research and development to explore new applications for soluble dietary fibers, enhancing product functionality and health benefits.

Consumer Education: As the market matures, efforts to educate consumers about the benefits of soluble dietary fibers will be crucial in overcoming existing misconceptions and driving demand.

Read Full Report - https://www.meticulousresearch.com/product/soluble-dietary-fibers-market-3953

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

#Soluble Dietary Fibers Market#Soluble Dietary Fibers#Soluble Non Fermentable Fiber#Water Soluble Fibres#Dietary Fibers#Food Dietary Fibers

0 notes

Text

Digestion Resistant Maltodextrin Market Landscape: Trends, Drivers, and Forecast (2023-2032)

The Digestion Resistant Maltodextrin market is projected to grow from USD 516.5 million in 2024 to USD 842.05 million by 2032, reflecting a compound annual growth rate (CAGR) of 6.30%.

Digestion-resistant maltodextrin is a type of carbohydrate derived from corn or wheat starch, known for its unique ability to resist digestion in the small intestine. Unlike regular maltodextrin, this variant is not absorbed as sugar but instead functions as a soluble dietary fiber. It is widely used in the food and beverage industry to enhance fiber content in products without affecting taste or texture. This makes it ideal for applications in low-calorie and health-focused foods, such as beverages, snacks, and dietary supplements. Beyond its nutritional benefits, digestion-resistant maltodextrin also supports digestive health by promoting healthy gut flora and improving bowel regularity. Its versatility and health benefits make it a popular ingredient in the development of functional foods aimed at supporting overall wellness.

The digestion-resistant maltodextrin market faces several challenges that could impact its growth and adoption:

Regulatory Hurdles: Navigating the complex landscape of food regulations and gaining approvals for health claims can be a significant barrier. Different countries have varying standards and regulatory requirements, which can slow down market entry and expansion.

Consumer Awareness and Acceptance: Despite its health benefits, digestion-resistant maltodextrin is not widely recognized by consumers. Educating the market about its advantages and differentiating it from regular maltodextrin requires substantial marketing efforts and resources.

Cost of Production: The manufacturing process of digestion-resistant maltodextrin can be more expensive than regular maltodextrin due to additional processing steps and quality control measures. These higher production costs can result in a higher price point, making it less competitive compared to other fiber sources.

Competition from Other Fibers: The market for dietary fibers is highly competitive, with numerous alternatives such as inulin, psyllium, and other soluble fibers. Convincing manufacturers and consumers to choose digestion-resistant maltodextrin over these well-established options can be challenging.

Supply Chain Issues: Ensuring a stable and consistent supply of raw materials for production can be problematic. Any disruptions in the supply chain can affect production schedules and lead to delays in product availability.

Technical Challenges in Formulation: Integrating digestion-resistant maltodextrin into various food and beverage products can pose technical challenges. Ensuring it performs well without altering the taste, texture, or stability of the final product requires extensive research and development.

Key Player Analysis

Roquette Freres S.A.

Ingredion Incorporated

Tate & Lyle

Grain Processing Corporation

WGC Co., Ltd.

Kraft Heinz Company

Cargill Incorporated

Archer Daniels Midland Company

Baolingbao Biology Co. Ltd

Tereos Syral S.A.S.

Changchun Dacheng Industrial Group

Henan Feitian Agricultural Development Co., Ltd

Gulshan Polyols Ltd

Luzhou

Matsutani Chemical Industry Co., Ltd.

More About Report- https://www.credenceresearch.com/report/digestion-resistant-maltodextrin-market

Digestion Resistant Maltodextrin Market Innovative Trends:

Functional Foods and Beverages: There is an increasing trend of incorporating digestion-resistant maltodextrin into functional foods and beverages, such as fiber-enriched juices, dairy products, and snacks, to enhance their nutritional profile and support digestive health.

Prebiotic Applications: As a prebiotic, digestion-resistant maltodextrin is gaining popularity in products designed to promote gut health by fostering beneficial gut bacteria, which can improve overall digestive well-being.

Sugar Reduction: This ingredient is being used as a bulking agent in sugar-reduced and sugar-free products, providing the desired texture and mouthfeel without adding calories, thus catering to health-conscious consumers.

Sports Nutrition: In the sports nutrition sector, digestion-resistant maltodextrin is being utilized in energy bars and protein supplements, offering sustained energy release and improved gut health benefits for athletes.

Weight Management Products: The low caloric value and high fiber content of digestion-resistant maltodextrin make it an ideal ingredient in weight management products, helping to create a feeling of fullness and aiding in appetite control.

Gluten-Free and Allergen-Free Formulations: It is increasingly being used in gluten-free and allergen-free products, providing a safe and functional ingredient option for individuals with specific dietary needs.

Pet Food: The use of digestion-resistant maltodextrin in pet food is an emerging trend, aimed at enhancing digestive health and nutrient absorption in pets, particularly in premium and health-focused pet food lines.

Pharmaceutical and Nutraceutical Applications: There is growing interest in the use of digestion-resistant maltodextrin in pharmaceuticals and nutraceuticals, where it serves as a dietary fiber supplement or a functional ingredient in formulations.

Innovative Packaging and Labeling: Companies are focusing on innovative packaging and labeling strategies to highlight the health benefits of digestion-resistant maltodextrin, such as improved digestive health and fiber enrichment, to attract health-conscious consumers.

Sustainability Initiatives: The market is also seeing a trend towards sustainable sourcing and production practices, with a focus on reducing environmental impact, which appeals to eco-conscious consumers and aligns with global sustainability goals.

Segments:

Based on Source:

Corn-based

Wheat-based

Potato-based

Cassava-based

Others (rice, banana)

Based on Form:

Spray-dried powder

Instantized/agglomerated

Based on Application:

Beverages

Alcoholic beverages

Non-alcoholic beverages

Food

Breakfast cereals

Dairy products

Instant puddings

Margarines and butters

Salad dressings

Sauces

Snack foods

Others

Nutraceuticals

Browse the full report – https://www.credenceresearch.com/report/digestion-resistant-maltodextrin-market

Browse Our Blog: https://www.linkedin.com/pulse/digestion-resistant-maltodextrin-market-mspwf

Contact Us:

Phone: +91 6232 49 3207

Email: [email protected]

Website: https://www.credenceresearch.com

0 notes

Text

Maize starch Manufacturers in India - Gujarat Ambuja Exports Limited

Starch Manufacturers in India - Gujarat Ambuja Exports Limited

Gujarat Ambuja Exports Limited is a premier name among maize starch manufacturers in India. Renowned for its excellence in the starch industry, the company specialises in producing high-quality maize starch that caters to a wide range of applications across various sectors. As one of the leading starch manufacturers, Gujarat Ambuja Exports Limited employs state-of-the-art technology and stringent quality control measures to ensure the highest standards in their products.

OUR PRODUCTS

1.Maize Starch:

2.Liquid Glucose:

3.Dextrose Monohydrate Powder

4. Dextrose Anhydrous Powder

5.Maltodextrin:

6.High Maltose Corn Syrup

7.Sorbitol 70% Solution

8.Dextrins

The maize starch manufactured by Gujarat Ambuja Exports Limited finds extensive use in multiple industries such as food and beverages, pharmaceuticals, textiles, and paper. In the food and beverage industry, their maize starch is valued for its superior thickening, stabilising, and binding properties. The pharmaceutical industry benefits from its excellent consistency and purity, making it ideal for tablet formulation and other medicinal applications. In textiles, maize starch is used for sizing and finishing fabrics, while the paper industry utilises it for coating and improving paper quality.

As a top-tier starch manufacturer in India, Gujarat Ambuja Exports Limited is committed to innovation and sustainability. Their manufacturing processes are designed to minimise environmental impact, ensuring a sustainable approach to starch production. The company's focus on research and development enables them to continuously improve their product offerings and stay ahead of industry trends.

Gujarat Ambuja Exports Limited's extensive distribution network ensures that their high-quality maize starch reaches customers across India promptly and efficiently. Their dedication to customer satisfaction, combined with their emphasis on quality and sustainability, has earned them a trusted reputation among starch manufacturers in India.

In summary, Gujarat Ambuja Exports Limited stands out as a leading maize starch manufacturer in India, known for delivering superior products tailored to the needs of various industries. Their commitment to innovation, quality, and sustainable practices makes them a preferred choice for businesses seeking reliable and high-performance maize starch solutions.

For More Information

“Ambuja Tower”, Opp.Sindhu Bhavan, Sindhu Bhavan Road, Bodakdev, P.O. Thaltej Ahmedabad 380054.

[email protected](Export Inquiries)

[email protected](Investors Only)

7961556678

https://www.ambujagroup.com/product-category/categories/starch-and-its-derivatives/

0 notes

Text

Raw and Real or Refined and Restricted? Market Growth of Food Starches Caught in a Processing Paradox

The global food starch market is projected for growth, driven by the expanding food processing and food service industries. However, the increasing availability of substitutes may pose a challenge. To navigate this landscape, Infinium Global Research offers a recent report with a deep dive into market segments and sub-segments, both globally and regionally. The report analyzes the impact of various short- and long-term factors, including drivers, restraints, and macro indicators, influencing the market's trajectory. It provides a comprehensive overview of current trends, forecasts, and dollar values for the global food starch market. This valuable resource can equip stakeholders with the insights needed to make informed decisions in this evolving market

To Get More Business Strategies for Request Sample Report @: https://www.infiniumglobalresearch.com/reports/sample-request/20722

Consumers around the world are increasingly seeking high-quality food and beverages that are both delicious and nutritious. This trend is driving a shift away from basic staples towards more enhanced food products. As a result, the demand for starch in the food and beverage industry is growing.

Starch is a versatile ingredient prized for its thickening, emulsifying, texturizing, gelling, stabilizing, and adhesive properties. It also boasts rheology modifying properties, making it a highly adaptable ingredient for a wide range of food applications. Bakery products, confectionery, sauces, processed meats, noodles, pasta, dry mixes, soups, salad dressings, puddings, and pie fillings all rely heavily on starch. Furthermore, advancements in starch modification have led to improved heat, temperature, pH, and rheological resistance, further expanding its global appeal and boosting the food starch industry.

Market Dynamics

The food starch market is experiencing a confluence of driving forces and potential challenges.

On the positive side, consumer demand for high-quality, nutritious food and beverages is translating into a preference for enhanced food products, which often rely heavily on starch for thickening, texture, and other functionalities. Starch's versatility extends beyond food processing, with applications in adhesives (particularly packaging) and various industrial products. This widespread use, coupled with its role as a thickening agent, binder, stabilizer, and emulsifier, fuels market growth. the growing trend of biofuels and biomaterials creates additional demand for industrial starch. The paper and textile industries are also significant consumers of corn starch, contributing further to market expansion.

Market Segmentation

Type:

Native Starch: This includes unmodified starch extracted directly from plants like corn, wheat, potato, and tapioca. It offers thickening and texturizing properties.

Modified Starch: This category encompasses starch that has undergone various treatments to enhance specific functionalities like heat resistance, gelling, or emulsification, making it suitable for diverse food applications.

Starch Derivatives: This segment includes products derived from starch through further processing, such as glucose syrups, maltodextrins, and cyclodextrins. These derivatives offer a wider range of functional properties for specialized uses in the food industry.

Applications:

The report explores the various sectors that utilize food starch, including:

Baked Goods: Starch plays a crucial role in baked goods for thickening, texturizing, and creating desired crumb structures.

Dairy Products: Starch is used in dairy products like yogurt and cheese to improve texture, stability, and mouthfeel.

Beverages: Starch finds application in thickening beverages, stabilizing emulsions, and enhancing mouthfeel.

Confectionery: Starch is a vital ingredient in candies and sweets, contributing to texture, sweetness, and binding properties.

Meat Products: Starch can be used in processed meats as a binder, thickener, and extender.

Other Applications: Starch has additional uses in var

Regional Impact:

North America (Dominant Market Share): This region is expected to hold the largest market share throughout the forecast period. Several factors contribute to North America's leading position:

Development of Modified Starch: North American producers are at the forefront of modified starch innovation, offering a wider range of functional starches for diverse applications.

Presence of Large Producers: Established players in the region cater to both domestic and international demand for food starch.

Asia-Pacific (High Growth Potential): The Asia-Pacific region is anticipated to witness significant growth with a healthy CAGR. This expansion can be attributed to:

Rising Maize (Corn) Use: The growing use of maize as a raw material for starch production fuels market expansion in this region.

Europe (Focus on Alternative Starches): Europe presents promising growth opportunities driven by:

Shifting Raw Material Preferences: European producers are increasingly utilizing potato and wheat alongside traditional sources like corn, catering to specific consumer demands.

Rest of the World (Emerging Markets): The ROW market holds potential for future growth as developing economies prioritize food processing advancements. However, factors like limited infrastructure and fragmented markets in some regions may pose challenges.

Request full Report: https://www.infiniumglobalresearch.com/reports/global-food-starch-market

Competitive landscape

Cargill Inc.

National Starch Food Innovation

Tereos Syral SAS

Tate & Lyle PLC

Roquette Freres SA

Grain Processing Corporation

Agrana Group

Qingdao Nutrend Biotech Co., Ltd.

SPAC Starch Products Ltd.

Sonish Starch Technology Co., Ltd.

Future outlook and conclusion:

The future of the food starch market appears bright, driven by a confluence of trends. Consumers' desire for high-quality, nutritious, and convenient food products positions starch as a valuable ingredient due to its versatility and functionality.

Beyond food processing, starch finds applications in adhesives, biofuels, and biomaterials, further expanding its market reach. However, the increasing availability of substitutes presents a potential challenge.

Innovation will be key for market leaders. Continued development of modified starches with enhanced properties and exploration of alternative raw materials can help the industry stay ahead of the curve. the food starch market offers a dynamic landscape with both opportunities and challenges. By staying abreast of consumer trends, embracing innovation, and exploring new applications, market players can capitalize on the potential for sustained growth in the years to come.

0 notes

Text

Maltodextrin Marvels: The Versatile Additive Shaping Modern Food Science (2024-2033)

From 2024 to 2033, maltodextrin rises to prominence as a versatile powerhouse in the food and beverage industry, shaping modern food science with its multifunctional applications. This polysaccharide, derived from starch through partial hydrolysis, proves indispensable for its ability to enhance texture, stabilize products, and act as a carrier for flavors and nutrients. As consumers increasingly seek out innovative and convenient food options, maltodextrin's role expands, making it a critical ingredient in everything from sports drinks and energy bars to instant foods and low-calorie sweeteners. With hashtags like #MaltodextrinMarvels, #FoodScienceInnovation, and #TextureEnhancement trending across social platforms, its popularity soars among food technologists and health-conscious consumers alike. Maltodextrin's ability to improve mouthfeel and shelf life without altering flavor profiles makes it a favorite among manufacturers aiming for both quality and efficiency. As clean label trends push for transparency, the industry responds with more natural and non-GMO sources of maltodextrin, aligning with consumer demand for healthy and trustworthy ingredients. This decade sees maltodextrin not just as a functional additive but as a crucial component in the evolution of food products, driving innovation and enhancing the culinary experience across the globe.

#MaltodextrinMarvels #FoodScienceInnovation #TextureEnhancement #VersatileAdditive #ModernFood #FunctionalIngredients #CleanLabel #NonGMO #FoodInnovation #HealthyEating #ConvenienceFoods #NutrientCarrier #FoodStabilizer #CulinaryScience #EnhancedShelfLife

0 notes

Text

Starch Derivatives Market Will Hit Big Revenues In Future

Starch Derivatives Industry Overview

The starch derivatives market encompasses a wide range of products derived from starch, which is a carbohydrate found in many plants. These derivatives are used in various industries including food and beverage, pharmaceuticals, cosmetics, and paper production.

Some common starch derivatives include:

Modified Starch: Starch that has been chemically or physically altered to improve its performance in specific applications. Modified starches may have enhanced stability, viscosity, or gelatinization properties compared to native starch.

Glucose Syrup: Also known as corn syrup or glucose-fructose syrup, it is made from the hydrolysis of starch and primarily consists of glucose. It is used as a sweetener, thickener, and moisture-retaining agent in food products.

Maltodextrin: A polysaccharide derived from starch hydrolysis, consisting of short chains of glucose molecules. Maltodextrin is often used as a thickener, filler, or bulking agent in food products, and it also finds applications in pharmaceuticals and cosmetics.

High Fructose Corn Syrup (HFCS): A sweetener made from corn starch that has been processed to convert some of its glucose into fructose. HFCS is commonly used in the food and beverage industry as a substitute for sucrose (table sugar).

Cyclodextrins: Cyclic oligosaccharides derived from starch through enzymatic conversion. Cyclodextrins have a unique structure that allows them to form inclusion complexes with other molecules, making them useful in various applications such as drug delivery, food flavoring, and fragrance encapsulation.

The global starch derivatives industry size was valued at US$ 56.4 billion in 2022 and is poised to grow from US$ 57.9 billion in 2023 to US$ 68.4 billion by 2028, growing at a CAGR of 3.4% in the forecast period (2023-2028).

How do starch derivatives contribute to enhancing the functional properties of food products?

The driving force behind the starch derivatives industry is expected to be their wide range of functionalities. These modified starches act as thickeners, texture agents, fat replacers, and emulsifiers. Advanced processing techniques allow for customization, creating highly functional ingredients that address various formulation challenges.

Make an Inquiry to Address your Specific Business Needs:

Recent health trends focused on reducing calorie intake to combat obesity have seen a rise in the use of modified starches as fat substitutes. These substitutes provide the desired mouthfeel, a glossy appearance similar to fat, and even reduce fat absorption in fried foods. Their functionality makes them ideal for formulating dietary foods like vegetable soups and snacks.

Sustainable and eco-friendly practices in textile and paper industry create opportunities for starch derivatives manufacturers

The textile and paper industries utilize starch derivatives for sizing, coating, and binding purposes. Innovation in these sectors, particularly regarding sustainable and eco-friendly practices, creates opportunities for starch derivatives manufacturers.

Starch derivatives function as natural thickeners and sizing agents, offering a greener alternative to synthetic chemicals used in textile and paper production. This shift not only enhances the environmental friendliness of the final products but also addresses growing concerns about chemical pollution.

Furthermore, starch-based derivatives like biodegradable plastics (bioplastics) are gaining traction as a more sustainable alternative to traditional plastics. This opens doors for manufacturers to create biodegradable packaging materials across various industries.

Increasing demand for convenience and ready-to-eat foods impacting the global starch derivatives market

Consumers are driving the starch derivatives market towards more sustainable and health-conscious options. The industry is responding with a focus on:

Sustainable practices: Responsible sourcing, eco-friendly production, and clean-label ingredients with fewer additives meet the growing demand for transparency and environmentally friendly products.

Health and wellness: Starch derivatives are instrumental in reducing fat and sugar content in processed foods, catering to health-conscious consumers.

This trend is particularly strong in the Asia-Pacific region, where a post-COVID focus on health has led to a surge in demand for gluten-free and reduced-calorie products. Starch derivatives offer the perfect solution, providing both textural and functional benefits for healthier food options, propelling significant growth in the Asia-Pacific starch derivatives market.

Additionally, the adoption of 3D printing for innovative packaging using starch-based biodegradable materials represents a major shift. This technology aligns with sustainability goals while offering exciting possibilities for enhancing aesthetics in the food and beverage sector.

In what ways do starch derivatives contribute to the growth of the processed food and beverage industry in Asia-Pacific?

Fueled by economic growth in the Asia-Pacific region, consumer purchasing power is on the rise. This translates to a surge in demand for processed foods and beverages, a market segment heavily reliant on starch derivatives. Thickeners, stabilizers, and texture enhancers – these are the functionalities starch derivatives bring to the table, propelling their own market growth.

Schedule a call with our Analysts to discuss your business needs: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=116279237

An additional advantage for the region? Asia-Pacific is a world leader in producing starch-rich crops like rice, wheat, and cassava. This ready availability of raw materials creates a strong foundation for a thriving starch derivatives market. Furthermore, the region’s growing commitment to sustainability aligns perfectly with the eco-friendly nature of starch derivatives – renewable and biodegradable. This caters to the increasing demand for green solutions.

With the Asia-Pacific region on a trajectory of economic expansion and evolving consumer preferences, starch derivatives are poised for substantial growth. This combination of factors positions the region for the highest CAGR (Compound Annual Growth Rate) in the global starch derivatives industry.

Primary companies highlighted

Cargill Incorporated (US)

ADM (US)

Tate & Lyle PLC (UK)

AGRANA Beteiligungs-AG (Austria)

Roquette freres (France)

Ingredion Incorporated (US)

Green Processing Corp. (GPC) France

Avebe (Netherlands)

Emsland Group (Germany)

Foodchem International Corporation (China)

0 notes

Text

Soluble Dietary Fibers Market Projected to Reach $4.99 Billion by 2029

Meticulous Research®—a leading global market research company, published a research report titled, ‘Soluble Dietary Fibers Market by Source (Fruit & Vegetables, Cereals & Grains), Type (Inulin, Pectin, Beta-Glucan, Maltodextrin, Oligofructose), and Application (pharmaceuticals, animal feed), and Geography—Forecast to 2029.’

Meticulous Research® recently published a report forecasting that the global soluble dietary fibers market will grow at a compound annual growth rate (CAGR) of 7.8% from 2022 to 2029, reaching $4.99 billion by 2029. This growth is driven by increasing health consciousness, awareness of the benefits of soluble dietary fibers, rising chronic disease rates, and the growing demand from pharmaceutical, food, and feed manufacturers to include these fibers in their products. Additionally, government initiatives promoting healthy food and emerging applications and markets, such as Southeast Asia, Latin America, and the Middle East & Africa, are expected to create lucrative opportunities. However, the market's growth may be hindered by the lengthy and costly regulatory approval process and high manufacturing technology costs.

The global market for soluble dietary fibers is segmented by source (fruits & vegetables, cereals & grains, nuts & seeds, and others), type (inulin, pectin, beta-glucan, polydextrose, maltodextrin, oligofructose, arabinoxylan-oligosaccharides, and others), application (functional foods & beverages, pharmaceuticals, animal feed, and others), and geography. The report also assesses industry competitors and analyzes regional and country-level markets.

In 2022, the fruit & vegetables segment is expected to hold the largest market share due to the high soluble fiber content in fruits and vegetables and consumer awareness of their health benefits. The beta-glucan segment is projected to have the highest CAGR, driven by its versatile applications in various industries and its inclusion in numerous food and beverage products.

The food & beverage segment is anticipated to dominate the market in 2022, attributed to the increasing use of soluble dietary fibers as stabilizers, texturizers, and low-calorie sweeteners. The growing demand for sugar-free and low-calorie foods and changing consumer eating habits also contribute to this segment's growth. Major companies, such as Ingredion Inc. and Cargill, Inc., are investing in research and development to introduce innovative products, further driving market demand.

The Asia-Pacific region is expected to experience the fastest growth, driven by rising health awareness, a booming food & beverage industry in countries like China, India, Japan, and Indonesia, and an increasing number of fitness clubs.

Key players in the global soluble dietary fibers market include Tate & Lyle plc (U.K.), DuPont de Nemours, Inc. (U.S.), Nexira (France), Roquette Frères (France), Cosucra Groupe Warcoing SA (Belgium), FutureCeuticals, Inc. (U.S.), Sensus B.V. (Netherlands), BENEO GmbH (Germany), The Archer-Daniels-Midland Company (U.S.), Ingredion Incorporated (U.S.), Herbafood Ingredients GmbH (Germany), Cargill, Inc. (U.S.), Lonza Group AG (Switzerland), Kerry Group plc (Ireland), Tereos S.A. (France), and Frutarom Industries Ltd. (Israel).

Download Free Sample Report Here: https://www.meticulousresearch.com/download-sample-report/cp_id=3953

Key Questions Answered in the Report

Which are the high-growth market segments by source, type, application, and region?

What is the historical market trend for soluble dietary fibers globally?

What are the market forecasts and estimates from 2022 to 2029?

What are the major drivers, restraints, and opportunities in the global market?

Who are the major players, and what is their market share?

How is the competitive landscape structured?

What recent developments have occurred in the global market?

What strategies are adopted by the major players?

What are the key geographic trends, and which countries are experiencing high growth?

Who are the local emerging players, and how do they compete?

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

#Soluble Dietary Fibers Market#Soluble Dietary Fibers#Soluble Non Fermentable Fiber#Water Soluble Fibres#Dietary Fibers#Food Dietary Fibers

0 notes

Text

0 notes

Text

Savoring Sweet Success: Navigating the Sugar Market's Diverse Landscape

The Sugar Market, a sweet cornerstone of the global food industry, is a dynamic realm encompassing various sugar types tailored to meet diverse consumer preferences. From traditional sweeteners to organic and exotic varieties, let's delve into the nuanced world of the Sugar Market, exploring its key segments: Food Sweetener, Coconut Sugar, Organic Sugar, and Palm Sugar.

1. Food Sweetener Market:-

The Food Sweetener Market is a pivotal segment within the larger sugar landscape, offering a range of sweetening options beyond traditional sugar. This category includes artificial sweeteners, high-fructose corn syrup (HFCS), and natural sweeteners like stevia and monk fruit. Estimated at US$89.87 billion in 2024, this segment encompasses sucrose (common table sugar), starch sweeteners (corn syrup, maltodextrin), and high-intensity sweeteners (aspartame, stevia).

2. Coconut Sugar Market:-

The Coconut Sugar Market caters to consumers embracing natural and ethically sourced sweeteners. Derived from the sap of coconut palm trees, coconut sugar offers a distinctive flavor profile with a hint of caramel, making it a popular choice in culinary applications. Valued at US$804.9 million in 2023, this segment offers a natural sweetener extracted from coconut palm sap, attracting health-conscious consumers seeking alternatives to refined sugar.

3. Organic Sugar Market:-

The Organic Sugar Market responds to the growing demand for natural and environmentally friendly products. Organic sugar is cultivated without synthetic pesticides or fertilizers, aligning with the principles of organic farming and sustainability. This niche segment, reaching US$565.7 million in 2023, caters to consumers seeking ethically sourced and sustainably produced sugar alternatives.

4. Palm Sugar Market:-

The Palm Sugar Market introduces an exotic and region-specific sweetener derived from the sap of various species of palm trees. Widely used in Asian cuisines, palm sugar contributes a unique flavor profile to dishes and desserts.

Market Dynamics:-

The Sugar Market, as revealed by market trends, is characterized by a delicate balance between tradition and innovation. While traditional sugar remains a staple, the rise of alternative sweeteners, organic choices, and exotic varieties reflects shifting consumer preferences.

Challenges and Opportunities:-

Challenges within the Sugar Market include addressing health concerns associated with excessive sugar consumption and the environmental impact of conventional sugar production. Opportunities for growth lie in product diversification, promoting sustainable practices, and catering to evolving tastes and dietary needs.

Conclusion:-

In conclusion, the Sugar Market showcases a spectrum of sweetening options, each catering to distinct consumer demands. From the versatility of Food Sweeteners to the natural allure of Coconut, Organic, and Palm Sugars, the market adapts to global culinary trends. As consumer preferences continue to evolve, the Sugar Market remains a dynamic and flavorful landscape, offering sweet possibilities for every palate.

0 notes

Text

Energy Drinks Market Booming Worldwide | Red Bull, Taisho Pharmaceutical Co. Ltd., PepsiCo. Inc., Monster Energy

The global energy drinks market size is expected to reach USD 177.58 billion by 2030, according to a new report by Grand View Research, Inc. It is expected to expand at a CAGR of 8.3% from 2022 to 2030. Consumption of energy drinks has been increasing drastically in recent years, particularly among adolescents and young adults, as they remain one of the most popular functional beverages in the market that offer consumers more physical and mental energy, through ingredients such as caffeine, taurine, guarana, ginseng, and B vitamins.

Manufacturers recently shifted their target consumer focus from athletes to young people, which has been driving the product consumption. According to the National Library of Medicine, in the U.S., energy drinks are the second most common dietary supplement used by young people; about 30% consume energy drinks on a regular basis. Such trends are expected to drive the market demand.

Request a free sample copy or view the report summary: https://www.grandviewresearch.com/industry-analysis/energy-drinks-market

The drinks product segment accounted for the largest revenue share in 2021, as these drinks are designed to give an “energy boost” to the drinker by a combination of stimulants and energy boosters. Most of the brands on the market contain large amounts of glucose while some brands offer artificially sweetened versions. Other commonly used constituents in the product are taurine, methylxanthines, vitamin B, ginseng, guarana, yerba mate, acai, maltodextrin, inositol, and carnitine, creatine, glucuronolactone, and ginkgo Biloba.

The off-trade distribution channel segment is expected to witness lucrative growth during the forecast period, as off-trade channels form the primary segment for shopping for all kinds of beverages, thereby driving the sales through these channels. The wide availability of several versions of energy drinks such as conventional, organic, vegan, and premium at these stores encourages consumers to purchase them through this channel.

The market is highly competitive and dominated by large multinational manufacturing companies. The players face intense competition, especially from the top players in the market as they have a large consumer base, strong brand recognition, and vast distribution networks.

Energy Drinks Market Report Highlights

North America held the largest revenue share in 2021 owing to the growing interest in the consumption of energy drinks in the U.S. Consumers are willing to pay more for functional and result-oriented premium quality energy drinks

The organic type segment is expected to register a higher growth rate during the forecast period, as health-conscious consumers who focus on reducing their exposure to artificial chemicals and artificial sweeteners usually prefer organic energy drinks over the conventional ones

The cans packaging segment held the largest revenue share in 2021 as they are lightweight and compact, which makes them a popular choice

Energy Drinks Market Segmentation

Grand View Research has segmented the global energy drinks market on the basis of product, type, packaging, distribution channel, and region:

Energy Drinks Product Outlook��(Revenue, USD Million, 2017 - 2030)

Drinks

Shots

Mixers

Energy Drinks Type Outlook (Revenue, USD Million, 2017 - 2030)

Conventional

Organic

Energy Drinks Packaging Outlook (Revenue, USD Million, 2017 - 2030)

Cans

Bottles

Others

Energy Drinks Distribution Channel Outlook (Revenue, USD Million, 2017 - 2030)

On-trade

Off-trade

Regional Insights

North America held the largest revenue share of over 30.0% in 2021. The growing consumption of the product in the region is also attributed to the increase in disposable income, the emergence of several domestic brands, and the rise in marketing and promotional activities for product growth. North Americans consume more energy drinks than any other geographic market in the world owing to the changing demographics and consumers’ tastes and drinking habits. The globalization of markets and the migration phenomenon contributed to the modification of drinking patterns of consumers who were gradually introduced into their drinking habits. This, in turn, has opened new opportunities for market players to incorporate a variety of drinks into their portfolios.

The Asia Pacific is likely to emerge as the fastest-growing regional market from 2022 to 2030. The market is expected to witness considerable growth in the economies of China, India, and Japan as a result of consumers' willingness to experiment with new flavors and the high demand from immigrants residing in the country, displaying an interest in varied beverages. Product launches in the region in order to target and appeal to numerous consumers have been driving the product demand in the region.

List of Key Players in the Energy Drinks Market

Red Bull

Taisho Pharmaceutical Co. Ltd.

Inc.

Monster Energy

Lucozade

The Coco-Cola Company

Amway

AriZona Beverages USA

Living Essentials LLC

Xyience Energy

Free Authoritative Research: https://www.grandviewresearch.com/industry-analysis/energy-drinks-market

#Energy Drinks Market#Energy Drinks Market Size#Energy Drinks Market Share#Energy Drinks Market Trends#Energy Drinks Market Research

0 notes

Link

0 notes

Text

Fat Replacers Market Size, Globally Demand by 2031 | W Hydrocolloids, Inc., Gelymar, Aquarev Industries, and MCPI Corporation

Global Fat Replacers Market report from Global Insight Services is the single authoritative source of intelligence on Fat Replacers Market. The report will provide you with analysis of impact of latest market disruptions such as Russia-Ukraine war and Covid-19 on the market. Report provides qualitative analysis of the market using various frameworks such as Porters’ and PESTLE analysis. Report includes in-depth segmentation and market size data by categories, product types, applications, and geographies. Report also includes comprehensive analysis of key issues, trends and drivers, restraints and challenges, competitive landscape, as well as recent events such as M&A activitiesin the market.

Get Access to A Free Sample Copy of Our Latest Report – https://www.globalinsightservices.com/request-sample/GIS23565

A fat replacer is an ingredient that can be used in place of all or some of the fat in a food product. Fat replacers are often used in foods that are high in fat, such as baked goods and fried foods. Fat replacers can be made from a variety of ingredients, including protein, carbohydrates, and fiber. Some fat replacers are calorie-free, while others may have a few calories per serving.

Key Trends

Over the past few years, there has been a growing trend in the use of fat replacers in food products. Fat replacers are substances that can be used in place of fat to reduce the calorie content of a food. There are a variety of fat replacers available on the market, including those made from carbohydrates, proteins, and fats.

One of the most popular fat replacers is carbohydrate-based. These products are typically made from maltodextrin, a type of carbohydrate that is easily digested and has a high solubility. Carbohydrate-based fat replacers are often used in baked goods, as they can provide a similar texture and mouthfeel to fat.

Protein-based fat replacers are another type of fat replacer that is growing in popularity. These products are typically made from whey protein, a type of protein that is rich in amino acids. Protein-based fat replacers are often used in products such as yogurt and ice cream, as they can provide a creamy texture.

Get Customized Report as Per Your Requirement – https://www.globalinsightservices.com/request-customization/GIS23565

Key Drivers

The key drivers of the fat replacers market are the increasing prevalence of obesity and chronic diseases, such as heart disease, stroke, and diabetes. The rising awareness of the health benefits of reducing fat intake is also a key driver of the market. Other drivers include the increasing demand for low-fat and healthy food products, and the growing food and beverage industry.

Market Segments

The fat replacers market report is bifurcated on the basis of type, source, application, and region. On the basis of type, it is segmented into carbohydrate, protein, and fat. Based on source, it is analyzed across plants and animals. By application, it is categorized into bakery & confectionary, processed meat products, dairy & frozen desserts, and others. Region-wise, it is studied across North America, Europe, Asia-Pacific, and rest of the World.

Key Player

The fat replacers market report includes players such as DuPont, Cargill, CP Kelco , Ashland Inc., Ingredion, Ceamsa, W Hydrocolloids, Inc., Gelymar, Aquarev Industries, and MCPI Corporation.

Buy Now - https://www.globalinsightservices.com/checkout/single_user/GIS23565

With Global Insight Services, you receive:

· 10-year forecast to help you make strategic decisions

· In-depth segmentation which can be customized as per your requirements

· Free consultation with lead analyst of the report

· Excel data pack included with all report purchases

· Robust and transparent research methodology

Ground breaking research and market player-centric solutions for the upcoming decade according to the present market scenario

About Global Insight Services:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1–833–761–1700 Website: https://www.globalinsightservices.com/

0 notes

Link

0 notes

Link

0 notes