#Insurance Claim Adjuster UK

Text

Efficient Insurance Claim Adjuster

Insurance Claim Solutions is an independent insurance claim adjuster based in Brighton and London. We negotiate with your insurer to maximise your insurance claim.

With a proven track record of excellence, we specialize in managing and facilitating insurance claims for individuals and businesses alike. Our team of highly skilled and experienced adjusters is dedicated to guiding clients through the entire claims process, ensuring a smooth and hassle-free experience.

#insurance loss adjuster#insurance claim adjuster#insurance claims solutions#Insurance Claim Adjuster UK#Insurance Claim Adjuster London

0 notes

Text

Top Traits of the Best Motor Trade Insurance

Businesses in the UK seeking motor trade insurance want full protection. The best policies safeguard a variety of automotive tasks like selling vehicles and doing repairs. Knowing the top motor trader protection helps businesses face risks and grow.

Great motor trade insurance fits each business perfectly. It includes motor trade policy features designed for specific needs. The best policies cover important industry needs, offer flexibility, and provide solid support. These are the qualities of exceptional motor trade insurance.

Businesses can find the best motor trade insurance by looking for key features. The right policy meets legal standards and helps companies handle risks well. Let's explore what makes a motor trade policy work well for the UK's motor trading scene.

Key Takeaways

Comprehensive protection is the cornerstone of the best motor trade insurance in the UK.

Flexibility to cater to different business sizes and needs is a critical feature of top policies.

Provider reputation and financial stability are non-negotiable for reliable coverage.

Transparency in pricing ensures there are no surprises in your motor trade insurance plan.

Customer support and efficient claim processing are pivotal to high-quality service.

Personalized customer reviews attest to the policy's effectiveness and customer satisfaction.

Customization options in policies allow businesses to obtain tailored protection.

Comprehensive Coverage Options

Choosing the best motor trade insurance is essential. It's important to know the different parts available. This ensures your business is protected in all areas. It covers everything from vehicles to liabilities, preventing financial loss from unexpected events.

youtube

Liability Insurance Components

Liability coverage protects you from claims related to injuries or damage to others. It often includes public, product, and employers' liability. This coverage is a safety net for legal costs and payouts.

Road Risk and Combined Policies

Road risk insurance is vital, covering vehicles used on public roads for business. A combined motor trade policy adds more protection. It covers your premises, theft, and property damage. This brings multiple coverages into one package.

Additional Coverage Benefits

Extra benefits in a comprehensive plan are important. They might cover business interruption, goods in transit, and equipment checks. These parts help your business keep running smoothly, no matter the challenge.

The right mix of liability, road risk, and combined policies is key. With comprehensive motor trade insurance, all business areas are safe. This gives you the confidence to run your business worry-free.

Flexibility for Different Business Sizes

The world of motor trade insurance is broad, serving businesses big and small. They offer flexible motor trade policies to meet the different needs of companies. This helps all businesses do well no matter their size.

Scalable trade insurance helps businesses that grow fast. It lets them adjust their coverage as they get bigger or during busy times. This way, businesses only pay for what they need, saving money as they change.

Insurers understand that flexibility is key. They make sure small business motor trade coverage is just right, not too little or too much.

Customizable policy plans that include or exclude specific features as needed

Options to add additional vehicles or drivers during peak periods

Coverage adjustments to reflect business growth or contraction

A good insurance policy does more than protect a business’s money. It gives owners peace of mind, knowing they're ready for anything. Being flexible with policies helps businesses stay stable and grow over time.

Reputation and Financial Stability of Providers

When picking a trusted motor trade insurance company, look at their reputation and financial health. A reputable insurance provider gives peace of mind and can handle claims well. We will explore how to find such insurers and why their financial stability matters.

Recognizing Credible Insurers

Finding reputable insurance providers means taking a few steps:

Check accreditations and licenses to make sure the insurer meets industry standards.

Read customer reviews and testimonials to see if the insurer is reliable and offers quality service.

Look at how long the company has been in the insurance field to understand its stability and experience.

This process ensures you're choosing a financially stable insurer with a strong foundation and trusted reputation in the motor trade world.

Reviewing Insurer Financial Records

It's important to check an insurer's financial health. A trusted motor trade insurance company should have their financial stability documented publicly, which includes:

Up-to-date financial statements showing profit and growth.

Ratings from independent analysts like Moody’s or Standard & Poor’s, which show financial strength.

Figures on their claim settlement ratio, proving they can handle claims.

These financial indicators are key. They show the insurer’s strength in backing up claims. This ensures that their client's business activities are secure.

Transparent Pricing with No Hidden Costs

Choosing the right motor trade insurance is important. Look for options with transparent motor trade insurance pricing to avoid surprises. It makes budgeting easier by showing all costs upfront.

Insurance providers who are clear about prices build trust. This clarity makes choosing easier and ensures businesses know the costs.

Complete breakdowns of all costs involved, including premiums and excesses

Explicit listing of what’s included in the policy and what counts as an add-on

Guarantees of no last-minute fees or adjustments post-purchase

Businesses should carefully read all terms and conditions. This is key to ensuring the policy is truly free from no hidden fees. It brings peace of mind and financial clarity.

Choosing a clear, straightforward approach to motor trade insurance empowers businesses, big or small, to thrive without the fear of unforeseen charges derailing their budgets.

Customer Support and Claims Assistance

In motor trade insurance, being great at customer support and claims assistance shows a company is dependable. Making sure every time you talk to customer service is easy and helpful is key. It helps motor trade businesses manage surprises smoothly.

Accessible Customer Service

Leading motor trade insurers make sure you can reach customer support anytime. They offer help through phone, email, and live chat. This means you're always a few clicks or a call away from help.

When you reach out, you'll find not just answers but also caring guidance. Knowledgeable staff work hard to fix your problems quickly.

Efficient Claims Processing

Being fast and proactive is crucial for claims assistance. From when you file a claim, the insurer should act quickly. They should keep clear lines of communication open.

This lets business owners follow their claim's progress and understand what's happening. It leads to quicker claims processing. This reduces how much your business is disrupted, proving the worth of a reliable insurance service.

Positive Customer Reviews and Testimonials

When looking for motor trade insurance, customer satisfaction is key. It shows how good and trustworthy an insurer is. Checking out motor trade insurance reviews and credible insurer testimonials helps potential clients see what kind of service and support they can expect.

Reviews are crucial because they share real-world stories from other business owners. They show how well an insurer manages claims and customer service. These are important parts of insurance that affect businesses every day.

Reviewing customer feedback not only makes things clearer but also builds trust. It shows prospective customers that the insurer is dedicated to keeping its promises.

High ratings usually mean the service and customer happiness are top-notch.

Looking at detailed testimonials gives insight into what's good and not so good about a policy.

People often link positive feedback to fast claims processing and strong customer help.

To really understand customer satisfaction, it's smart to look for common points in feedback on various platforms. This helps give a full picture of how insurers do in real-life situations, not just the ideal ones.

In conclusion, reading through motor trade insurance reviews is helpful. It's a way to find a policy that fits your business needs. Plus, it shows that the insurer cares about its customers and holds itself to a high standard of service.

Customization and Tailored Policies

In the ever-changing motor trade world, custom solutions are a must. There's no room for a "one size fits all" method. Custom motor trade insurance is key, adapting to different automotive businesses. This includes everyone from independent mechanics to big car dealerships. They all gain from tailored trade policies that suit their specific needs.

Personalized motor insurance solutions make sure policies fit just right. They strip away unnecessary parts and add what's really needed for protection. This way, businesses don't waste money on what they don't need. They also get strong defense against specific risks they face.

Insurers that specialize in customization don't just sell a policy. They work closely with each business, taking time to learn about their unique operations. This deep understanding helps create a policy that fits the business perfectly. Such a detailed approach means businesses get coverage that's just right for them. They save money and get better service with tailored trade policies.

0 notes

Text

The Impact of Roof Surveys on Property Insurance in the UK

Roof surveys play a crucial role in maintaining the integrity and value of properties across the UK. Beyond ensuring structural soundness, they have significant implications for property insurance. Regular roof surveys can influence insurance premiums, coverage, and claims. This article delves into how roof surveys impact property insurance and highlights the role of ADI Roof Surveys in Grays in providing essential services for property owners.

The Importance of Roof Surveys for Property Insurance

Accurate Assessment of Property Condition

Insurance Underwriting: Insurance companies assess the risk associated with insuring a property based on its condition. A thorough roof survey provides detailed information about the roof's health, helping insurers determine accurate premiums.

Risk Mitigation: Identifying and addressing roof issues early reduces the likelihood of damage claims, which can lead to more favorable insurance terms and lower premiums.

Reducing the Risk of Claims

Preventative Maintenance: Regular roof surveys enable proactive maintenance, preventing minor issues from escalating into significant problems that result in insurance claims.

Weather Damage Mitigation: In the UK, weather-related roof damage is common. Regular inspections help ensure that roofs are well-maintained and capable of withstanding severe weather, reducing the frequency and severity of claims.

Insurance Premium Adjustments

Lower Premiums: Properties with well-maintained roofs, as verified by regular surveys, are considered lower risk by insurers. This can result in reduced insurance premiums.

Higher Premiums for Neglected Roofs: Conversely, properties without recent roof surveys or with identified roof issues may face higher premiums due to increased risk.

Enhanced Coverage Options

Comprehensive Coverage: Insurance companies may offer more comprehensive coverage options to properties with documented roof surveys, as these properties are deemed lower risk.

Specialized Policies: Properties with unique roofing materials or structures, such as historical buildings, may benefit from specialized insurance policies tailored to their specific needs, facilitated by detailed roof surveys.

Easier Claims Process

Documentation of Condition: Roof surveys provide valuable documentation of the roof's condition before any damage occurs. This can streamline the claims process, as insurers have clear evidence of the roof's prior state.

Reduced Disputes: Detailed survey reports can help resolve disputes between property owners and insurers regarding the cause and extent of damage, leading to quicker and more satisfactory claim settlements.

ADI Roof Surveys in Grays: Ensuring Insurance Compliance and Peace of Mind

For property owners in Grays, ADI Roof Surveys offers expert roof inspection services that can significantly impact property insurance. Here's how ADI Roof Surveys can help:

Comprehensive Roof Inspections

Thorough Assessments: ADI Roof Surveys conducts detailed inspections that cover all aspects of the roof, from structural integrity to potential leak points, ensuring a comprehensive understanding of its condition.

Advanced Technology: Utilizing the latest technology, including drones and thermal imaging, ADI Roof Surveys provides precise and accurate assessments that can be shared with insurance providers.

Detailed Reports for Insurance Purposes

Clear Documentation: ADI Roof Surveys provides detailed reports that document the current state of the roof, highlighting any issues and recommended repairs. These reports are valuable for insurance purposes, offering clear evidence of proactive maintenance.

Regular Updates: Regular roof surveys ensure that property owners have up-to-date documentation of their roof’s condition, which can be beneficial when renewing or adjusting insurance policies.

Proactive Maintenance Recommendations

Preventative Actions: ADI Roof Surveys offers actionable recommendations for preventative maintenance, helping property owners address potential issues before they become costly problems.

Insurance Compliance: By following these recommendations, property owners can demonstrate their commitment to maintaining their property, potentially leading to more favorable insurance terms.

Expert Advice and Support

Insurance Liaison: ADI Roof Surveys can assist property owners in communicating with their insurance providers, ensuring that the survey findings and maintenance actions are properly understood and considered in policy decisions.

Tailored Solutions: Their team of experts provides tailored advice based on the specific needs and conditions of each property, ensuring the best possible outcomes for both maintenance and insurance.

Conclusion

Roof surveys are a vital component of property maintenance that significantly impact property insurance in the UK. Regular inspections help in accurate risk assessment, preventative maintenance, and potential premium reductions. For property owners in Grays, ADI Roof Surveys offers expert services that provide comprehensive roof assessments, detailed reports for insurance purposes, and proactive maintenance recommendations. By partnering with ADI Roof Surveys, property owners can ensure their roofs are well-maintained, potentially lowering insurance costs and simplifying the claims process. Schedule a roof survey with ADI Roof Surveys today to enhance your property’s insurance profile and enjoy peace of mind.

1 note

·

View note

Text

Direct Line's Shift to Indirect Pricing Comparison Strategy

Direct Line, a prominent motor insurer in the UK, is shifting its strategy by listing its flagship brand on price comparison websites for the first time. This move reflects the growing dominance of these platforms in the UK insurance market, where approximately 90% of customers seek new policies, according to Direct Line CEO Adam Winslow.

In his inaugural strategy review, Winslow emphasized the importance of offering customers diverse interaction channels beyond direct sales, acknowledging the previous overemphasis on direct channels compared to the prevalent influence of price comparison websites (PCWs).

Founded in 1985, Direct Line initially disrupted the insurance sector by bypassing brokers and directly selling to customers, symbolized by its iconic red phone in marketing campaigns. However, the landscape evolved significantly in the 2000s with the rise of well-known PCW advertisements featuring meerkats and opera singers, facilitating easy comparison among various insurance providers.

While Direct Line already features brands like Privilege and Churchill on price comparison websites, integrating its primary Direct Line brand marks a substantial strategic shift. Winslow highlighted that this move aims to revitalise Direct Line's position in the motor insurance market.

Paul De’Ath, head of market intelligence at consultancy Oxbow Partners, described Direct Line’s decision as pivotal, stressing that neglecting to appear on such platforms limits customer reach. He noted Direct Line’s move as one of the final acknowledgments of PCWs' dominance in the market by major brands.

The announcement forms part of a broader strategic overhaul where Direct Line plans to concentrate on core insurance lines like motor, home, and commercial insurance, alongside breakdown services, while phasing out investments in sectors such as pet and travel insurance.

Direct Line is currently focused on restoring its financial standing following a recent takeover attempt by Belgian rival Ageas. The company aims to resume regular dividends, targeting approximately 60% of post-tax operating earnings, pending first-half results assessment.

Earlier this year, Direct Line reported a turnaround in its motor insurance operations following a surge in post-pandemic claims costs that prompted a series of profit warnings and leadership changes. Despite efforts to adjust premiums and repair its underwriting portfolio, the company reported a £190 million operating loss last year, primarily driven by policies issued at lower rates.

As part of its fiscal strategy, Winslow set a new cost-saving objective of £100 million annually, focusing on areas like marketing efficiency. While no immediate layoffs are planned, Direct Line anticipates reduced resource needs as it continues its digital transformation.

Barclays analysts expressed cautious concern over Direct Line’s ability to maintain its service-oriented brand proposition amid heightened competition on price comparison websites. However, they acknowledged potential benefits in reducing marketing expenses and streamlining operations.

Meanwhile, analysts at Citi viewed the latest developments negatively, citing anticipated income reductions from business exits and other contributing factors.

Direct Line's shares experienced a slight decline to 192.5p during Wednesday morning trading. This valuation remains below Ageas's second offer of 237p per share, which valued the motor insurer at approximately £3.2 billion.

In March, Ageas announced its decision to discontinue its takeover bid, citing an inability to justify a substantial increase to its initial cash-and-shares proposal.

Read the full article

0 notes

Text

When Neck Pain Becomes Intolerable

It may have been an accident, whiplash after an RTA, or a work related injury, even bad posture can eventually bring about that nagging pain in the neck resulting in stiffness, soreness and loss of mobility. Neck pain treatment in Manchester from one of our registered chiropractors can help with your specific, and overall range of motion. Neck pain treatment in Northern Quarter Manchester offers sessions where improvement in your neck will be gained by spinal adjustment and therapeutic exercises, to prevent your pain from progressing any further and affecting your lifestyle.These techniques are low-risk and yet provide maximum relief. Neck pain whilst debilitating, seldom has serious causes and the correct re-alignment will soon rectify matters.

Mechanical neck pain is easy cured by manipulation

Because there is very seldom a sinister cause, neck pain is generally spoken of as a simple or mechanical pain. But you can be assured that with a one to one consultation with your chiropractor he will fully assess the causes during your first appointment for neck pain treatment near Manchester. Those experiencing continuous neck pain or recurrent episodes are more prevalent in the older age group. This is because wear and tear begin to contribute. As the shock absorbing pads or discs between the bones of the neck become narrower with advancing age, this can make the neck more difficult to move and cause stiffness and pain.But timely intervention of neck pain treatment in Manchester City Centre will make that pain a thing of the past.

Are you even experiencing pins and needles in the fingers?

In some less frequent instances, nerves in the neck can become trapped or compressed in the same way as those in the lower vertebrae and this in turn can cause irritation. When this does happen,whether due to damage to the discs, or because of wear and tear, this can lead to pain which is felt in the shoulder and down the arm. Even resulting in numbness, weakness, and pins and needles through to the hand. Re-alignment as part of your neck pain treatment near Northern Quarter Manchester will quickly bring relief.

RTA related neck injury

With RTAs, in excess of 250,000 claims are made to relevant insurance companies each year in the UK alone relating to whiplash. Often, the pain which in some cases can continue sporadically for years to come, may continue unresolved. Painkillers and stronger prescription medications are not the solution. If you are suffering these aftereffects and live in the Greater Manchester area, then it could be time that you sought a solution and looked for professional neck pain treatment near Manchester City Centre.

0 notes

Text

Economic Benefits of Investing in Bulk Bag Loader & Unloader Solutions in the UK

Investing in bulk bag loader and unloader solutions can significantly enhance the operational efficiency of businesses across the UK. These advanced systems streamline the handling of bulk materials, offering substantial economic benefits. Let’s delve into the various ways in which these solutions can positively impact your bottom line.

Increased Efficiency and Productivity

One of the most notable advantages of using a bulk bag loader and unloader is the dramatic increase in efficiency and productivity. Traditional methods of handling bulk materials can be time-consuming and labour-intensive, often requiring multiple workers and substantial manual effort. By automating the loading and unloading processes, businesses can speed up operations, reduce the need for manual labour, and thereby increase overall productivity.

Cost Savings on Labour

Automation of the loading and unloading process with a bulk bag unloader and loader reduces the dependency on manual labour. This reduction translates into significant cost savings on wages and associated labour costs, such as insurance and benefits. Additionally, it minimises the risk of workplace injuries related to manual handling, which can lead to costly workers' compensation claims and downtime.

Reduction in Material Waste

Effective bulk bag handling solutions, including the use of a bag opener, help in minimising material spillage and waste. Precise and controlled loading and unloading ensure that every bit of material is utilised, which can lead to considerable cost savings over time. Less waste also means less expenditure on raw materials, directly contributing to your economic bottom line.

Improved Inventory Management

Bulk bag loaders and unloaders can be integrated with modern inventory management systems, providing real-time data and control over the materials being handled. This integration allows for better tracking of inventory levels, more accurate forecasting, and efficient stock management. Consequently, businesses can avoid overstocking or understocking situations, reducing holding costs and improving cash flow.

Enhanced Quality Control

Using automated systems for bulk material handling ensures consistency and precision, which is crucial for maintaining high-quality standards. These systems reduce the risk of contamination and ensure that materials are handled in a controlled environment. Consistent quality control can enhance product reliability, customer satisfaction, and ultimately, repeat business and revenue growth.

Scalability and Flexibility

Investing in bulk bag handling solutions provides businesses with the scalability and flexibility needed to adapt to changing market demands. These systems can be easily adjusted to handle different materials and volumes, making them ideal for businesses looking to expand their operations or diversify their product offerings without significant additional investment.

Environmental Benefits and Compliance

Modern bulk bag handling systems are designed with environmental considerations in mind. By reducing spillage and ensuring efficient handling, these systems help businesses meet environmental regulations and sustainability goals. Compliance with these standards not only avoids potential fines and penalties but also enhances the company’s reputation as a responsible corporate entity.

Conclusion

Investing in bulk bag loader and unloader solutions offers a multitude of economic benefits for businesses across the UK. From increased efficiency and productivity to significant cost savings on labour and materials, these systems provide a robust return on investment. Additionally, they improve inventory management, quality control, scalability, and environmental compliance. By adopting these advanced handling solutions, businesses can position themselves for sustainable growth and long-term success.

For businesses looking to optimise their operations and enhance their economic performance, the integration of automated bulk bag unloader loader handling solutions is a strategic move that promises substantial returns.

0 notes

Text

Lloyd’s of London Blueprint Two (BP2) upgrade July 2024

Unveiled in 2020, Lloyd’s of London Blueprint Two (BP2) upgrade will be released in two phases – July 2024 and April 2025, stands as a transformative initiative aiming to digitise the United Kingdom (UK) insurance market. Before understanding the possible impact of Blueprint Two (BP2) upgrade on the UK insurance industry there are so many questions that should be answered to have a holistic understanding about the Lloyd’s BP 2 upgrade. In this article, we will discuss all the relevant information in detail and find answers to the below questions.

As a part of insurance broking software in UK insurance industry since last so many years I have not witnessed any event having a huge impact on millions of people. Before writing this article, we have gone through official website of Lloyd’s of London and studied numerous other articles published on Lloyds new upgrade to summarize few important details in this article. After reading this article, you will get enough value and if you have any questions, please reach out to us immediately and we will resolve all your queries. Let`s start

Why Lloyd`s of London decided to roll out Blueprint Two (BP2) upgrade?

Lloyd’s of London, a venerable star in the insurance galaxy, faces the cosmic winds of modernization. Fiercer competition demands faster, cheaper, and more efficient services, threatening to leave them adrift. But fear not, for Blueprint 2(BP2) emerges as a beacon of hope, guiding the London Market Joint Venture (LMJV) towards a brighter future.

BP2 upgrade paints a nebula of possibilities, transforming the insurance landscape:

Lightning-fast placements: Digitization and automation become warp drives, propelling processes forward at breakneck speed, slashing turnaround times to mere stardust. Reduced costs become the Holy Grail, leading everyone – insurers, brokers, and policyholders – to a land of efficiency and affordability.

Data-driven insights: A central platform acts as a galactic core, ensuring data quality, accessibility, and analysis. This empowers better risk assessment, pricing, and claims management, allowing them to navigate with the precision of a seasoned navigator.

Seamless customer experience: Self-service options and streamlined communication become hyperspace lanes, making interactions with Lloyd’s a smooth journey. The customer voyage transforms from a bumpy asteroid field to a delightful, personalized experience.

Adaptability to emerging risks: A flexible platform equips Lloyd’s to be a nimble starship, capable of weathering new and complex risks with agility. They become the galactic first responders, offering solutions efficiently and effectively, no matter the threat.

Competitive edge: Modernization becomes the fuel that propels them forward, attracting and retaining top talent across the galaxy. This fuels future business opportunities, ensuring Lloyd’s remains a dominant force in a dynamic market.

However, the BP2 upgrade voyage isn’t without its asteroid fields. Stakeholders buy-in becomes crucial, requiring diplomacy and collaboration skills worthy of a seasoned ambassador. Complex integrations, akin to merging disparate star systems, demand meticulous planning and execution. Potential disruptions, like unexpected solar flares, need to be navigated with agility and resilience.

Why Lloyd’s of London delayed the second phase?

The strategic delay of phase two from October 2024 to April 2025 reflects a commitment to a smooth, turbulence-free journey. The Lloyd’s Market Association (LMA) requested more time for market adaptation, allowing everyone to adjust to the phase one changes smoothly. This focus on phase one stability ensures a solid foundation, minimizing the risk of cascading issues later.

The extended runway also allows for improved adoption and preparation. Market participants get more time to train their crew, adapt workflows, and integrate systems, leading to smoother adoption and utilization of new features. By reducing risk and complexity, the phased approach ensures a controlled environment for change, minimizing potential disruptions. Industry experts view the delay positively, recognizing it as a pragmatic move prioritizing project success.

Ultimately, BP2 upgrade represents a bold mission to future-proof Lloyd’s. By embracing fintech, open insurance, APIs, block chain, and artificial intelligence, the initiative positions Lloyd’s at the helm of a transformative era. The success of BP2 hinges on collaboration and on-going engagement with key stakeholders, including managing agents, brokers, and regulators. As the project unfolds, its impact will be closely watched by the entire insurance industry, eager to see how Lloyd’s charts a digital course for the future, leaving their mark on the ever-evolving insurance galaxy.

Let’s delve into a compliance checklist to ensure your systems are fully aligned with this upliftment. Remember, BP2 isn’t an isolated “upgrade” but a multi-phased digital transformation, so the approach needs to be holistic.

10 things you need to check to ensure whether your system is fully compliant with the new Lloyds blueprint 2 (BP 2) upgrade:

Understand the Scope of Change: Clearly define the functionalities and processes impacted by Blueprint 2. This helps map out which systems need evaluation for compatibility and potential adjustments.

Conduct a System Inventory: Create a comprehensive list of all relevant systems, including hardware, software, and applications. Assess their age, technical specifications, and compatibility with new technologies introduced by Blueprint 2.

Data Migration and Integration Planning: Analyse how data needs to be migrated or integrated within Blueprint 2. Develop a detailed plan addressing data cleansing, conversion, and mapping between old and new systems.

Security and Privacy Implications: Evaluate the potential security and privacy risks arising from Blueprint 2’s implementation. Ensure adherence to industry regulations and data protection standards.

User Training and Adoption: Assess the training needs of system users affected by Blueprint 2. Develop training programs to familiarize them with new functionalities and workflows.

Testing and User Acceptance: Conduct thorough testing of all impacted systems after implementing Blueprint 2. Involve key stakeholders in user acceptance testing to ensure smooth adoption.

Communication and Change Management: Develop a comprehensive communication plan to inform all stakeholders about Blueprint 2 and its impact. Implement change management strategies to minimize disruption and resistance.

Performance Monitoring and Optimization: Continuously monitor system performance after implementation. Identify and address any bottlenecks or issues that hinder optimal functionality.

Regulatory Compliance: Ensure all systems and processes comply with relevant regulations before and after Blueprint 2 implementation.

Seek Expert Guidance: Partner with Agiliux experts who understand Blueprint 2 and can provide tailored advice on system readiness and potential challenges.

Agiliux offers a game-changing solution, a scalable AI driven cloud software designed to transform your business, regardless of whether you’re a broker, bank (bancassurance), or agency. Empower your entire insurance journey with Agiliux’s secure cloud platform by digitizing your operations seamlessly, streamlining processes and boosting efficiency. Get data-driven insights for better risk assessment, pricing, and claims management. Deliver a frictionless customer experience with self-service options and improved communication. Operate with confidence knowing your data is securely protected in the cloud.

Remember, compliance is an ongoing process. By being proactive, adaptable, and continuously monitoring your systems, you can ensure your organization embraces the transformative potential of Lloyd’s of London Blueprint Two (BP2) upgrade while maintaining compliance with evolving regulations and industry standards.

#insurance broking software in uk#insurance broking management software uk#insurance broking management system uk#insurance broking system uk#insurance broker software uk

0 notes

Text

Best Life Insurance Companies in the UK: Securing Your Future with Future Proof Ltd

In the intricate tapestry of life, ensuring the financial security of our loved ones stands paramount. Amidst the myriad of choices, identifying the best life insurance companies in the UK can seem like a daunting task. Future Proof Ltd emerges as a guiding light in this complex landscape, offering bespoke advice tailored to individual needs and circumstances. This blog delves into how Future Proof Ltd simplifies the process of finding the best life insurance companies in the UK, ensuring peace of mind for you and your family.

Understanding the Importance of Life Insurance

Life insurance is more than just a financial product; it's a safety net that promises security for your loved ones in the face of unforeseen circumstances. The UK market is brimming with options, each offering unique benefits and coverages. Future Proof Ltd stands out by not only helping clients navigate through these options but also by providing expert insights that align with their specific life situations. Their approach demystifies the process, making it easier for individuals to choose among the best life insurance companies in the UK.

How Future Proof Ltd Makes a Difference

Future Proof Ltd distinguishes itself by adopting a client-centric approach. They understand that each individual's needs are unique, and a one-size-fits-all policy does not suffice when looking for the best life insurance companies in the UK. Their team of experts conducts thorough market research, comparing various policies and their features, to recommend solutions that best meet their clients' specific requirements.

Criteria for Selecting the Best Life Insurance Companies in the UK

When advising clients, Future Proof Ltd considers several critical factors to identify the best life insurance companies in the UK. These include the financial stability of the insurance provider, the range of policies offered, premium affordability, the claims process, and customer service quality. By evaluating these aspects, Future Proof Ltd ensures that clients are matched with life insurance providers that offer reliable, comprehensive, and cost-effective coverage.

Tailored Solutions for Diverse Needs

Future Proof Ltd recognizes the diversity of their clientele, ranging from young professionals starting their careers to established families looking to secure their financial future. This understanding drives their commitment to offering personalized advice, ensuring that whether clients are looking for term life insurance, whole life policies, or more specialized coverages, they are guided towards the best life insurance companies in the UK that cater to their specific needs.

The Role of Expert Guidance

In the ever-evolving landscape of life insurance, staying informed about the latest products, regulations, and market trends is crucial. Future Proof Ltd leverages its industry expertise to provide clients with up-to-date, accurate information, empowering them to make informed decisions. Their role as intermediaries between clients and insurance companies ensures that clients receive the best terms and conditions, aligning with their financial goals and personal circumstances.

Building Long-Term Relationships

Future Proof Ltd is committed to building lasting relationships with its clients. They understand that life insurance needs can change over time, and they stand ready to provide ongoing support and advice. Whether it's adjusting coverage to reflect significant life events or reassessing policies to ensure they remain competitive, Future Proof Ltd is a steadfast partner in securing your financial future.

Conclusion

In the quest to find the best life insurance companies in the UK, Future Proof Ltd offers a beacon of clarity and assurance. Their personalized, expert-driven approach ensures that individuals are equipped with the knowledge and support needed to make the best decisions for their life insurance needs. By choosing Future Proof Ltd, you gain more than just a policy; you gain a partner dedicated to safeguarding your family's financial well-being for years to come. In a world of uncertainties, Future Proof Ltd provides a future-proof solution to life insurance, making sure you and your loved ones are well-protected.

To learn more: https://www.futureproofinsurance.co.uk/life-insurance/best-life-insurance/

1 note

·

View note

Text

Tech rally leads markets higher, Oil rebounds

US stocks put in a strong performance on Thursday as hopes for early interest rate cuts got a boost from comments by a Federal Reserve official and economic data provided mixed signals.

The blue chip DJIA closed 0.5% higher at 37,468, but the broader S&P 500 rose 0.9%, to end at 4,780 and the tech-laden Nasdaq Composite jumped 1.4% to 15,055. Atlanta Federal Reserve President Raphael Bostic said on Thursday that he was open to reducing US interest rates sooner than he had anticipated if there is "convincing" evidence in coming months that inflation is falling faster than he expected.

Bostic added, however, that the overall situation faced by the Fed "argues for caution." The day’s data could be read both ways. US initial jobless claims dropped 16,000 to a seasonally adjusted 187,000 for the week ended January 13, the lowest level since September 2022, pointing to robust jobs growth.

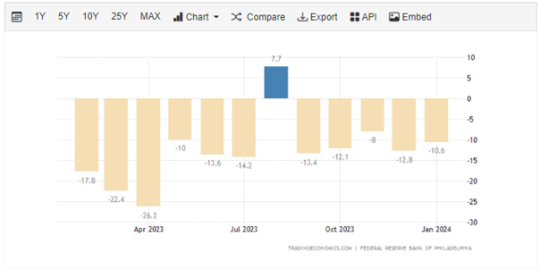

But on the flip side, the Philly Fed manufacturing index remained in contraction territory in January, and US single-family homebuilding dropped by 8.6% in December after a string of strong gains.

Tech stocks led the gainers, with chipmakers benefiting from Taiwan Semiconductor Manufacturing (TSMC) earnings news. The main chip supplier to Apple and Nvidia said it expects a return to solid growth this quarter. Nvidia shares rose 1.9%, while Microchip Technology adding over 4.5%. Apple shares gained nearly 6% after Bank of America upgraded the iPhone maker to 'buy' from 'neutral' and raised its price target.

NAS100Roll H4

Also on the up, Boeing rose 4.5% after winning an order for 150 of its troubled 737 Max jets from India’s newest airline, Akasa Air. But among the fallers, Discover Financial Services lost 9.8% after the credit card lender reported a steep decline in fourth-quarter net income due in part to higher compliance-related expenses. And shares in Humana dropped 11% after the health insurer cut its earnings outlook because rising demand for medical services has pushed up its costs.

USOILRoll H1

Oil prices rose Thursday as cold weather disrupted US oil production and worries over Middle East tensions heightened after Iranian missile strikes against Pakistan. UK Brent crude was up 1.3% to 78.01 a barrel, while US WTI was 2.0% higher at 74.02. Meanwhile, the International Energy Agency (IEA) forecasts that growth in oil demand will halve this year, in contrast to OPEC’s forecast of flat demand growth in 2024.

Disclaimer:

The information contained in this market commentary is of general nature only and does not take into account your objectives, financial situation or needs. You are strongly recommended to seek independent financial advice before making any investment decisions.

Trading margin forex and CFDs carries a high level of risk and may not be suitable for all investors. Investors could experience losses in excess of total deposits. You do not have ownership of the underlying assets. AC Capital Market (V) Ltd is the product issuer and distributor. Please read and consider our Product Disclosure Statement and Terms and Conditions, and fully understand the risks involved before deciding to acquire any of the financial products provided by us.

The content of this market commentary is owned by AC Capital Market (V) Ltd. Any illegal reproduction of this content will result in immediate legal action.

0 notes

Text

Community Impact: How Technical Assessing Is Making a Difference Beyond Adjustments

Introduction

In the intricate world of loss adjustment services, one name stands out as a beacon of excellence – Technical Assessing. With a legacy spanning over three decades, this chartered loss adjuster in Australia has not just been adjusting losses; it has been shaping a community of professionals dedicated to delivering unparalleled results.

We Are More Than Adjusters

At the core of Technical Assessing is a philosophy that goes beyond the traditional role of an adjuster. We are not merely a service provider; we are a community of passionate individuals committed to producing professional results consistently. In an industry where skill sets are abundant, we take pride in our people choosing us before our clients do. Talent is the lifeblood of our company, and we believe that it chooses us because of the quality we represent.

Skytech: Elevating Assessments with Drones

In the era of technological advancement, Technical Assessing has embraced innovation with Skytech – our specialised division in UAVs (Unmanned Aerial Vehicles), commonly known as drones. These aerial marvels have revolutionised the landscape of claims assessing, offering a level of accuracy, accountability, and accessibility never witnessed before.

Imagine obtaining superior images and footage of the scene of a claim without any disturbance – that's the power of Skytech. Drones provide easy access to risky or difficult-to-reach sites, proving invaluable when large areas need to be covered quickly. What sets Skytech apart is its capabilities and the fact that it is the only in-house drone division among loss adjusters in Australia. This ensures our clients have direct access to experienced drone operators deeply immersed in the insurance industry.

Technical Assessing's Legacy

For over 30 years, Technical Assessing has been setting the standard for loss adjustment services. Our commitment to professionalism not only ensures a positive customer experience but also enhances the relationships between our clients and their insured parties. Specialising in resolving complex, technical, and large losses, we have grown to become Australia's largest national, independent, locally-owned loss adjuster.

Our solution-focused approach to loss adjusting aims to reduce claims leakage and provide fair outcomes. Many of our adjusters are highly qualified specialists with construction, engineering, law, risk management, accounting, mechanics, insurance, and loss adjusting degrees. This diversity in expertise allows us to tackle challenges with a comprehensive and knowledgeable approach.

Expertise Across the Globe

The footprint of technical assessment extends far beyond the shores of Australia. We operate across the continent, catering to clients in Australia and New Zealand, the USA, the UK, Europe, the Pacific Islands, and Asia. Our expertise and specialist skills make us the go-to company for large and complex losses with local and international clients.

Maintaining our independence is crucial to us, as it ensures we can strive to create positive and fair outcomes. This independence fosters enduring relationships between our clients and their insureds, solidifying our position as a trusted partner in the insurance industry.

Corporate Structure & Governance

Technical Assessing operates within a well-defined corporate structure, comprising the holding company, Technical Assessing Holdings Pty Ltd, and area-specific subsidiaries across major Australian cities. This structure underwent a significant transformation in 2020 when the executive management, led by managing director David Cambridge, acquired TA. The board composition changed, and in 2022, an employee share scheme was introduced to attract and retain key staff.

The introduction of the employee share scheme aimed to reward staff for their loyalty, ensuring a stable and dedicated workforce. This strategic move aligns with our goal of maintaining a workforce that possesses the necessary skills and is also deeply committed to the values and vision of Technical Assessing.

Our Community

At the heart of Technical Assessing is a passionate commitment to giving back to the community. Beyond our professional endeavours, our people actively contribute to making a difference in the lives of those in need. Through partnerships with select community groups, we have formed close relationships and shared experiences with organisations like the Humpty Dumpty Foundation, National Breast Cancer Foundation, Sir David Martin Foundation, World Vision, CFA (VIC), and Black Dog Institute.

Our community engagement is not just a corporate responsibility; it is a reflection of the values we hold dear. TA is committed through its people to positively impacting the lives of those who sometimes need a helping hand. We believe that a strong community is the foundation of a better society, and our endeavours are a small contribution towards that vision.

Conclusion

In essence, Technical Assessing is not just a loss adjuster but a force that shapes the industry and the communities it serves. Our legacy, commitment to excellence, global expertise, and community engagement make us more than a service provider; we are a partner in navigating the uncertainties that come with complex losses.

FAQs

How does Skytech enhance claims assessment?

Skytech, our in-house Drone division, provides superior accuracy, accountability, and accessibility in capturing images and footage without disturbing the scene of the claim.

What sets Technical Assessing apart from other loss adjusters?

Our recruitment philosophy, commitment to professionalism, and solution-focused approach distinguish us as a preferred choice for large and complex losses.

What geographical areas does Technical Assessing operate in?

Technical Assessing operates across Australia, New Zealand, the USA, the UK, Europe, the Pacific Islands, and Asia.

Tell us about Technical Assessing's corporate structure.

Technical Assessing comprises the holding company and area-specific subsidiaries in major Australian cities, fostering a well-defined corporate structure.

How does Technical Assessing contribute to the community?

Through partnerships with organisations like the Humpty Dumpty Foundation and others, Technical Assessing actively participates in community initiatives, making a positive impact.

1 note

·

View note

Text

Solution-Focused Loss Adjusting for a Positive Outcome

Navigating the intricate landscape of loss adjustment services requires more than expertise; it demands a commitment to solutions. In the heart of Australia, Technical Assessing emerges as a chartered loss adjuster, redefining the narrative by prioritising solutions for a positive outcome.

The Essence of Technical Assessing

A Legacy of Excellence: With a legacy spanning over three decades, Technical Assessing has evolved into Australia's largest national, independent, locally-owned loss adjuster. The journey isn't just about growth; it's about maintaining a commitment to excellence in every facet of loss adjustment.

The People Paradigm: While many companies focus on skillsets, Technical Assessing takes pride in being chosen by their people first. In an industry where talent is unevenly distributed, this approach ensures a team of the industry's best and brightest, dedicated to producing professional results every time.

Skytech: Elevating Precision with Drones

Innovative Solutions from Above: Enter Skytech, the specialist division in UAV (Unmanned Aerial Vehicles), commonly known as Drones. Far beyond being a technological add-on, Skytech brings a new dimension to claims assessment. Drones offer unparalleled accuracy, accountability, and accessibility, ensuring superior images without disturbance to the scene.

Direct Operator Engagement: What sets Skytech apart is its status as the only in-house drone division in any loss adjuster in Australia. Clients benefit from direct engagement with a drone operator deeply immersed in the insurance industry, bringing a wealth of knowledge to claims adjusting.

Commitment to Professionalism and Independence

Resolving Complex Losses: Technical Assessing's commitment to professionalism extends beyond the routine. They have become synonymous with the resolution of complex, technical, and large losses. Independence isn't just a principle; it's a guarantee of impartiality and a steadfast dedication to ensuring a positive and fair outcome.

Expertise Beyond Boundaries

Global Reach: Operating across Australia and serving clients from New Zealand, the USA, the UK, Europe, the Pacific Islands, and Asia, Technical Assessing has solidified its position as the go-to company for large and complex losses. The global clientele is a testament to their expertise and specialist skills.

Specialist Team: The backbone of Technical Assessing lies in its team of highly qualified specialists. With degrees spanning construction, engineering, law, risk management, accounting, mechanics, insurance, and loss adjusting, this team brings diverse expertise to the forefront.

Corporate Stability and Community Commitment

Executive Leadership: In 2020, Technical Assessing underwent a strategic buyout led by Managing Director David Cambridge. The move ensured stability and paved the way for a board comprising management team members. In 2022, an employee share scheme was introduced, recognising and rewarding loyalty.

Beyond Business: Technical Assessing doesn't just operate within corporate boundaries; it extends a helping hand to communities. Through partnerships with organisations like the Humpty Dumpty Foundation, National Breast Cancer Foundation, Sir David Martin Foundation, World Vision, CFA (VIC), Black Dog Institute, and Destiny Rescue, they actively contribute to positively impacting lives.

Conclusion: A Holistic Approach to Loss Adjustment

Technical Assessing stands as a beacon of a holistic approach in the realm of loss adjustment services. From leveraging cutting-edge technology with Skytech to fostering a team of specialists and engaging with global clients, their solution-focused methodology ensures a positive outcome in every case.

0 notes

Text

Book Review: We've Got You Covered

I recently finished We've Got You Covered: Rebooting American Healthcare. It's a book by healthcare and insurance professionals, about what to do with the American Healthcare system.

I write this a few days after reading it, and without notes and a re-read. These are my main takeaways, without researching whether their claims are true.

People are unable to not provide health to those in critical danger. US citizens are unable to tolerate not providing life saving treatment to those that can be helped. Whenever heart-breaking details from the sufferers of a particular disease or from an uncovered and vulnerable cohort, becomes the media's center of attention, the US government creates another patch, so that at least those unfortunate few can be saved.

For a while. Children with cystic fibrosis used to not live to adulthood, and now they may come of age only to lose their coverage. Foster children are covered into their 20s, but no more. People over 65 "luck out", and their coverage does not lapse.

And to understand the exemptions and coverages, to find the relevant paperwork, and to submit it correctly, is a burden that falls most heavily on the vulnerable.

The authors suggest that the US has a social contract , wherein people that can be saved, should be. And that they failed to live up to it causes medical bankruptcies and erodes people's confidence in their future.

Their prescription is that the US should provide some minimum standard of care unconditionally. There should be no charge for the marginal consumption of healthcare that is covered. Not because (other) economists are wrong about the incentive structure, but because countries that implemented surcharges kept adding exemptions, until the system of checks could barely be maintained by the fees. (They point to the UK and Germany. It's unclear whether Singapore's fees exceed their administration, but Singapore also has forced medical savings, which is rare).

Anything beyond the minimum, should be purchased.

This of course, demands a budget, and a bare basic list of things to cover. The US doesn't have a budget for healthcare at this time, which shocked me to learn. The government simply decides whether something is covered, and if yes, pays it.

How something is to be decided as covered in the author's scheme is in the same vein as why. I am excited to have the US implement unconditional minimum healthcare, but the author's listing of what things are to be covered leaves me wanting. I understand their point. They plot the only politically feasible thing, but oh does it feel terrible to endorse.

Allegedly, Oregon's doctors had to come up with a list of cost-effective interventions, ranked, sanely, by quality adjusted life year purchased per dollar. They committed to a dollar amount per QALY (preregistration!), and dental crowns made the cut, and emergency appendectomies didn't. The math checks out. Crowns are really cheap, last along time, and dental pain is extremely debilitating. Appendectomies are (somehow) really expensive. The authors advocate that what's covered need to follow common sense, and attempt to fulfill our social contract, instead of doing what is effective.

I see the need for this, politically. I cannot celebrate this choice. If I were ever to sign a petition endorsing such a plan, it would be with a sense of duty, and not joy.

If the social contract necessitates that we must give emergency appendectomies, and the doctors are right that dental crows return more QALYs, then the action to take would be to draw the line at appendectomies and declare that everything more cost effective is also covered.

If this costs too much? Start importing doctors from Iran, from Cuba. They already provide sufficient care to meet the minimal standard, and surely they can carry out appendectomies. Let them have a shorter residency. Open more slots so we can train more doctors.

Maybe I am simply wrong. Perhaps dental crowns are not time sensitive, and can be purchased on the patient's own time and dime. Perhaps there isn't anything that is both time sensitive and highly cost effective, that the author's purported social contract would not cover. This warrants thoughts and research for another day.

Other things I was surprised to learn below the cut:

[[MORE]]

Some Canadian provinces actively discourage any form of private care.

Israel's public healthcare decreased in quality to such a point that the government intervened. The interventions, involving financial incentives and minimum work hour requirements in the public sector, quickly brought the standards back to an acceptable level

Nixon was close to passing bipartisan policies that would have brought US citizens universal coverage

Both British and Canadian doctors hated their respective systems, during the initial implementation

I guess Canadian doctors still might, as they go work across the border

#medical care#not my country#not sure if I would trade#worrying about details#also worried about incentive structures#what if research went disproportionately to drugs/treatments that are expensive and only useful in rare emergencies#what if we live in that world already

1 note

·

View note

Text

Income Protection Insurance in the UK: A Safety Net for Your Financial Security

Introduction:

Financial security is a vital aspect of a person's life, and protecting one's income is essential to ensure stability and peace of mind. However, unforeseen events such as illness, injury, or disability can disrupt an individual's ability to earn an income. To mitigate the risks and provide a safety net during challenging times, Income Protection Insurance (IPI) has emerged as a valuable financial tool in the UK. This article delves into the concept of Income Protection Insurance, its significance, and how it acts as a safety net, safeguarding an individual's financial well-being.

Understanding Income Protection Insurance:

Income Protection Insurance, also known as Permanent Health Insurance (PHI), is a type of insurance policy designed to replace a portion of an individual's lost income in the event they are unable to work due to illness, injury, or disability. This insurance policy provides regular payments, known as income protection benefits, during the policy's term or until the individual is fit to return to work.

How Income Protection Insurance Works:

Coverage and Benefit Amount: When a policyholder takes out Income Protection Insurance, they select the level of coverage they desire. This coverage is usually a percentage of the individual's pre-tax income, typically ranging from 50% to 70%. In the event of a claim, the policyholder receives regular payments, often on a monthly basis, to help replace the lost income.

Waiting Period: Income Protection Insurance policies have a waiting period, also known as the deferred period, during which the policyholder must wait before receiving benefits. This period can range from a few weeks to several months, and the length of the waiting period affects the premium cost. A longer waiting period generally results in a lower premium.

Benefit Payment Period: The benefit payment period is the length of time the policyholder will receive income protection benefits if they remain unable to work. Some policies offer short-term coverage (e.g., 1 or 2 years), while others provide long-term coverage until the policyholder reaches a specified age or is able to return to work.

The Significance of Income Protection Insurance:

Financial Security: Income Protection Insurance offers individuals and their families financial security during times of unexpected loss of income. The regular benefit payments help cover essential expenses such as mortgage or rent, utilities, and daily living costs, providing peace of mind and stability.

Long-Term Coverage: Unlike other insurance policies that cover specific events, such as critical illness or accidents, Income Protection Insurance UK provides long-term coverage. This ensures that policyholders are protected against a wide range of potential health issues or disabilities that may prevent them from working.

Flexible Payouts: Income Protection Insurance provides flexibility, as policyholders can tailor the benefit payouts to their specific needs. The percentage of income covered and the length of the benefit payment period can be adjusted to suit individual circumstances.

Support for Self-Employed Individuals: For self-employed individuals or those without access to sick pay, Income Protection Insurance is particularly valuable. It acts as a safety net, enabling self-employed individuals to maintain financial stability even when unable to work.

Benefits of Income Protection Insurance:

Peace of Mind: Knowing that their income is protected in the event of illness or disability, policyholders experience peace of mind, reducing stress and anxiety during challenging times.

Rehabilitation Support: Some Income Protection Insurance policies offer rehabilitation support, helping policyholders recover and return to work sooner with access to medical assistance and vocational training.

Tax-Free Benefits: Income Protection benefits are generally tax-free, making the payout amount more beneficial for policyholders when they need it the most.

Evaluating the Need for Income Protection Insurance:

Reliance on Employment Income: Individuals who heavily rely on their employment income to cover living expenses, mortgage, or debt repayments should consider Income Protection Insurance to maintain financial stability during periods of inability to work.

Limited Sick Pay: Employees with limited or no sick pay benefits from their employers would benefit from Income Protection Insurance, as it ensures continued financial support during extended periods of illness or disability.

Self-Employed or Gig Economy Workers: For self-employed individuals or those working in the gig economy without access to sick pay or employee benefits, Income Protection Insurance becomes a crucial safety net.

Conclusion:

Income Protection Insurance in the UK serves as a safety net for individuals, protecting their financial security in times of illness, injury, or disability. By providing regular income protection benefits, this insurance policy offers financial stability, peace of mind, and flexibility in tailoring coverage to individual needs. Its long-term coverage, tax-free benefits, and support for self-employed individuals make it a valuable tool for safeguarding one's financial well-being.

Assessing the need for Income Protection Insurance is essential, especially for individuals heavily reliant on their employment income or lacking access to sick pay benefits. By evaluating the benefits of Income Protection Insurance and selecting a policy that suits individual circumstances, individuals can ensure financial security during unforeseen challenges, providing comfort and stability for themselves and their families.

0 notes

Text

Are fashion brands major in sustainability?

In its July 2021 record, the not-for-profit Transforming Markets Foundation highlighted that as several as 59 percent of all green claims by European and UK fashion brand names are misleading and can be greenwashing.

Recently, H&M was heavily criticised for its 'false' insurance claims that more than half of its items are lasting however they were really not. The brand name was additionally sued and also dragged to the court for its 'greenwashing' effort as they supposedly adjusted Higg Index. After that there is Shein which is encountering around the world backlash for its dishonest practices in the supply chain, yet it gains more revenues than what H&M and Zara collectively gain in the United States!

As horrific as it seems, other brand names too are accused of talking something they do not exercise and yet they show up lasting fashion in various methods-- outright deceptiveness, refined marketing, and often as enthusiastic insurance claims without complete openness around the real impacts! In its July 2021 report, the not-for-profit Changing Markets Structure highlighted that as many as 59 percent of all environment-friendly cases by European as well as UK-style brand names are deceptive and can be greenwashing.

Greenwashing remains in its prime-- all many thanks to brand names' (for this reason customers') love for quick style as well as synthetics!

Arguably, fast style is the most significant offender harming style's sustainability efforts. There is a portion of end customers who think that their investment in choices does not matter, and that their item intake does not make a difference.

However, actually, trend-driven overconsumption is inspired by low-price/cheap products that are improperly constructed (more than likely breaching honest production standards) to satisfy tight setting you back. These garments, nearly certainly lasting much less than a period, wind up in landfill or are shipped offshore to emerging markets and establishing economies where they are thrown out as ecological contamination. As a desperate effort to quell a brand-new generation of aware customers, brand names greenwash their 'footprint' in their attempt to market the item or the brand.

The repercussions of the brand's supply chains are significant and durable as they typically make use of man-made products as well as chemicals. Brands should pay attention to selecting custom swimwear manufacturers from source materials so that they can meet environmental requirements when producing products and meet their environmental marketing strategies in the swimwear market. The CEH, a non-profit customer advocacy group, focused on revealing the existence of poisonous chemicals in consumer products, just recently did testing on a range of prominent top-quality sporting activities bras and athleticwear that disclosed high levels of BPA, a chemical compound that's used to make sure types of plastic and can bring about hazardous health and wellness impacts such as bronchial asthma, cardio condition as well as weight problems.

The sporting activities bras marketed by brands like Athleta, PINK, Asics, The North Face, Brooks, Done In Activity, Nike, and also FILA were all evaluated for BPA in the previous 6 months, and also the outcomes showed the clothing might subject users to approximately 22 times the secure limit of BPA, based upon standards set in California, according to the Center for Environmental Health And Wellness.

Just how do brands stand apart in various records on the sustainability front?

In the recent Remake Style Responsibility Report 2022, Remake-- a worldwide advocacy organization battling for reasonable pay as well as climate justice in the clothing industry-- assessed 58 large style businesses in 2022 including Chanel, J.Crew, and Allbirds on their journey to intersectional social and also environmental sustainability and unpacked its crucial findings which suggest towards a worrying circumstance, though some positives exist also!

Strong guarantees on environment modification, yet progress has been limited

Just 3 businesses (5 percent)-- Burberry, Everlane, and also H&M Group-- fulfilled all 4 of Remake's environment standards: disclosure of complete exhausts; short-term 1.5 ℃ pathway-aligned Scientific research Based Targets; ambitious long-term net-zero targets; and also a reduction in their overall greenhouse gas emissions. As firms reveal their full supply chain discharges, the range of the trouble is clear: Inditex's (Zara's) annual emissions are equivalent, for instance, to consuming 39 million barrels of oil.

The myth of circularity has been revealed but no firm has truly accepted degrowth. A 3rd of the assessed companies are lowering their product packaging waste as well as 20 percent currently supply upcycling or fixing services. Despite a rise in resale platforms as well as some fixing campaigns, there has not been a transition away from straight production. The business proceeds to co-opt for consumer interest in circularity-- like Shein's brand-new resale system-- to greenwash. While no firm can reveal a general decrease in production, some business like Everlane, Nike, and also Patagonia did decrease their use of virgin plastics like polyester.

Living salaries stay evasive, yet some businesses are taking much more responsibility for the wages of their workers. Style is constructed on poverty pay, and also that hasn't altered this year. That claimed, a few companies can show that a few of their employees are gaining reasonable pay, and the infrastructure to elevate incomes is ending up being much more robust.

Four companies (7 percent) published some progress in the direction of a living wage in their supply chains in enhancement to revealing the technique they utilize to evaluate a living wage: Hanesbrands Inc., Patagonia, Ralph Lauren, and also Improvement.

Five companies (9 percent)-- Burberry, Kering (Gucci, Balenciaga), Marks & Spencer, PUMA as well as Reformation-- published partial details showing that a few of their straight staff members, such as business employees or retail employees, worked wage.

One firm-- Ganni-- took on a Purchaser Code of Conduct, a kind of contract for the acquisition of products that commits firms to do their part to uphold reasonable commercial methods, such as paying reasonable rates for items completely, and also on the schedule.

Despite some progression, the number of style brand names bringing a shift in their supply chain stays just under 10 percent.

Renay Wells, Style Effect Professional from Australia informed Clothing Resources that a lot of brands that claim to be sustainable consider the usage of 'recycled' manufacture as the only requirement to claim sustainability. They do rarely take into consideration implications and also the influence of their supply chain. "A lot of brands would certainly not give doubt to the ethical repercussions of their production practices. The wish for profit, high margins, and also rapid production far surpasses their insurance claims of sustainability," commented Renay.

Will the situation change?

The apparel industry has been discussing the adverse impacts of rapid fashion on the environment for a long period now but the consumption of fast style is just boosting with time. It's true that a lot of the lasting style items aren't economical and also do not come as size-inclusive. In countries like Brazil and also Mexico, for circumstances, a lot of people acquire from Shein because they think it is a means to being composed of a particular fashion pattern at inexpensive costs, as well as the brand name really has inclusive dimensions. Sustainable clothes are a lot more expensive for apparent factors, yet there are truly no reasons to not be size-inclusive.

Not just Shein-- which is taken into consideration as a serial offender of sustainability efforts-- many other prominent brand names just as are in charge of enhancing greenwashing attempts. It is extremely vital to educate customers that quick style is impactful for the world and creates enormous environmental pollution!

There is one straight solution to this-- it's since the completion goal of a brand is to market its items in the customer market and also gain earnings. While it is important to have a manufacturer that produces sustainable products, brands should also have some responsibility to focus on environmentally friendly products and seek out an activewear manufacturer. If supply chain is improved, sustainable measures are applied, openness is created, technologies in product are done and correct incomes are offered to workers, after that a brand needs to invest more which eventually leads to walking in product's market prices. Are customers ready to pay this hiked cost for an item?

If they are looking for affordable items, a brand, whose service design deals with quick style idea, merely can not opt for all these prior procedures to develop a sustainable supply chain because it sustains significant expense. This is why altering customers' behaviors as well as their investing ability on high-priced items is critical as that will certainly give area to more lasting products in the market.

0 notes

Text

Insurance Fraud Detection Market To Receive Overwhelming Hike In Revenues By 2030

The Insurance Fraud Detection market research examines constantly changing business trends, important industry segments, large investment pockets, value chains, the competitive landscape, and regional conditions in detail. The Insurance Fraud Detection market research analyzes the growth rate, product price, profit, production capacity, production, supply, demand, market growth rate, and forecast of major regions of the world through 2030.

It is estimated that during the forecast period from 2022 to 2030, the average annual growth rate of The Insurance Fraud Detection market is higher than the previous one. Study the Insurance Fraud Detection market using various techniques and analyses to provide reliable and detailed information about the industry. To better understand the market, it is broken into several parts to cover different elements, and an in-depth study of each area will allow readers to better understand the growth potential of each region.

Request a free sample copy of the report here: https://market.biz/report/global-insurance-fraud-detection-market-gm/#requestforsample

Key questions answered in the report:

What are the opportunities and challenges for newcomers?

Who are the leading suppliers in the world Insurance Fraud Detection market?

Which segment offers the greatest opportunities for market growth?

Where will current developments take the industry in the long term?

Segmentation of Global Insurance Fraud Detection Market

The study covers the competitive landscape of the major manufacturers

FICO

IBM

BAE Systems

SAS Institute

Experian

LexisNexis

Iovation

FRISS

SAP

Fiserv

ACI Worldwide

Simility

Kount

Software AG

BRIDGEi2i Analytics Solutions

Perceptiviti

Breakdown by Type:

Fraud Analytics

Authentication

Segmentation by Application:

Claims Fraud Detection

Identity Theft Detection

Payment and Billing Fraud Detection

Money Laundering Detection

Can't find what you need? Check here: https://market.biz/report/global-insurance-fraud-detection-market-gm/#inquiry

Regional analysis:

For the projection period 2022 to 2030, assumptions are made about the production volume and the business share of the individual regions in the industrial market. To help stakeholders make quick and informed decisions, the Insurance Fraud Detection market study also provides an overview of the regional industry in terms of volume and consumption value, as well as price trends and profit margins.

The industry research for Insurance Fraud Detection provides an in-depth analysis of market growth and other factors in key Countries (Regions) including:

- North America (the US, Canada, and Mexico)

- Europe (Germany), France, UK, Russia, Italy and Rest of Europe)

- Asia Pacific (China, Japan, Korea, India, Southeast Asia, and Australia)

- South America (Brazil, Argentina, Colombia, and rest of South America)

- Middle East and Africa (Saudi Arabia, United Arab Emirates, Egypt, South Africa, and the rest of the Middle East and Africa)

Highlights of Insurance Fraud Detection Market Report

- A complete context analysis that provides an assessment of the market

- Major changes in business dynamics

- Industry segmentation into the second or third level

- Historical, current, and forecast market size in value and volume view

- Report and evaluate information on the latest industry developments

- Market shares and strategies of the main players

- Emerging niche segments and regional markets

- An objective assessment of the industry development

Buy the report here: https://market.biz/checkout/?reportId=659526&type=Single%20User

Customization available:

Global Insurance Fraud Detection Market Research can be adapted to your individual business needs be adjusted. We offer a customization service for custom reports because we understand what they want.

The Impact of Covid19:

The study considered the impact of COVID-19 on business growth. This report provides a detailed introduction to the impact of the COVID19 pandemic on the Insurance Fraud Detection market and its key market segments. current and future consequences of the pandemic as well as post-COVID19 scenarios to enable a deeper understanding of the market dynamics.

About Us: