#Industrial Refrigeration Market Trends

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has been banned in Indonesia for providing people with access to pornographic content.

Text

Industrial Refrigeration Market Segmented by Product, Top Key Players, Geography Trends, and Forecasts to 2030

Global Industrial Refrigeration Market research report published by Exactitude Constancy reveals the current outlook of the global and key regions from the following perspectives: Key players, countries, product types, and end industries. The report studies the top companies in the global market and divides the market into several parameters. This Industrial Refrigeration Market research report pinpoints the industry's competitive landscape to understand the international competition. This report study explains the expected growth of the global market for the upcoming years from 2024 to 2030. This research report is accumulated based on static and dynamic perspectives on business.

The global industrial refrigeration market is expected to grow at 5.3 % CAGR from 2023 to 2030. It is expected to reach above USD 30.88 billion by 2030 from USD 19.4 billion in 2023.

Browse Complete Summary and Table of Content @ https://exactitudeconsultancy.com/ja/reports/7088/industrial-refrigeration-market/

#Industrial Refrigeration Industry#Industrial Refrigeration Market 2024#Industrial Refrigeration Market Analysis#Industrial Refrigeration Market Research Report#Industrial Refrigeration Market Demand#Industrial Refrigeration Market Growth#Industrial Refrigeration Market Insights#Industrial Refrigeration Market Revenue#Industrial Refrigeration Market Share#Industrial Refrigeration Market Size#Industrial Refrigeration Market Trends

0 notes

Text

Refrigerant Market Revenue, Share and Growth Rate to 2030

The global refrigerant market size was estimated at USD 14.26 billion in 2023 and is projected to grow at a CAGR of 4.7% from 2024 to 2030.The industry is experiencing growth due to increased demand from various end-use sectors, particularly the commercial & industrial refrigeration industry. Rapid urbanization in emerging economies, the expansion of cold storage facilities, and the rising…

#Refrigerant Industry#Refrigerant Market Analysis#Refrigerant Market Growth#Refrigerant Market Trends

0 notes

Text

A Cooler Collaboration: District Cooling Systems with Chillers Market for Sustainable Urban Cooling

Introduction:

In today's urban landscape, efficient and sustainable cooling solutions are paramount. District cooling systems, powered by centralized Chillers Market, offer a compelling alternative to traditional on-site cooling.

This article explores the synergy between district cooling systems and chillers, examining their working principles, benefits, applications, and considerations for implementation.

Download FREE Sample: https://www.nextmsc.com/chillers-market/request-sample

Beyond the Rooftop Unit: Understanding District Cooling Systems

District cooling systems provide chilled water for building cooling through a network of underground pipes. Unlike traditional on-site chillers, these systems offer several advantages:

Centralized Cooling Production: A central chiller plant generates chilled water, eliminating the need for individual chillers on each building rooftop.

Economies of Scale: Centralized production allows for larger, more efficient chillers, leading to lower overall energy consumption.

Reduced Building Footprint: Eliminating individual chillers frees up valuable rooftop space in buildings.

Potential for Sustainable Practices: Centralized plants can utilize more sustainable technologies like waste heat recovery or natural refrigerants.

Inquire before buying: https://www.nextmsc.com/chillers-market/inquire-before-buying

Beyond the Compressor: The Role of Chillers in District Cooling

Chillers are the heart of a district cooling system:

Cooling Powerhouse: Centralized chillers produce chilled water by removing heat from a refrigerant using a vapor-compression cycle.

Efficiency Matters: The efficiency of chillers significantly impacts the overall energy consumption of the district cooling system.

Technology Choices: District cooling systems can utilize various chiller technologies, including electric chillers, absorption chillers (powered by waste heat), and chillers using natural refrigerants.

Matching Capacity: Chiller capacity in the central plant needs to be carefully designed to meet the peak cooling demand of all connected buildings within the district.

Beyond the City Center: Applications for District Cooling Systems

District cooling systems are well-suited for various urban environments:

Dense Urban Areas: In densely populated areas, district cooling can efficiently cool multiple buildings, reducing the overall environmental impact.

University Campuses: Large campuses with multiple buildings can benefit from the centralized cooling approach of district systems.

Mixed-Use Developments: Combining residential, commercial, and office buildings within a district creates a suitable environment for centralized cooling.

Government and Public Buildings: Consolidated cooling for government buildings and public facilities can be achieved through district systems.

Beyond the Initial Investment: Considerations for District Cooling Systems

While district cooling offers advantages, some considerations need to be addressed:

Initial Investment: Building the infrastructure for a district cooling system requires a significant upfront investment.

Long-Term Commitment: Buildings connecting to a district cooling system are locked into the system for the long term.

Reliability and Maintenance: The reliability of the central chiller plant and distribution network is critical for building cooling.

Cost Allocation: A fair and transparent system for allocating cooling costs to individual buildings within the district is necessary.

Building a Sustainable Future: The Path Forward for District Cooling

District cooling systems hold significant potential for a more sustainable future:

Energy Efficiency: Centralized production can utilize more efficient technologies and economies of scale, leading to lower overall energy consumption.

Reduced Emissions: District cooling systems can adopt renewable energy sources or utilize waste heat for chiller operation, reducing greenhouse gas emissions.

Urban Planning Integration: Integrating district cooling into new urban developments creates a more sustainable and efficient cooling infrastructure.

Policy and Incentives: Government policies and incentives can encourage the development and adoption of district cooling systems.

Conclusion: A Chilling Partnership: District Cooling and Chillers for Sustainable Urban Development

The collaboration between district cooling systems and chillers presents a promising approach to urban cooling. By centralizing cooling production, utilizing efficient technologies, and leveraging economies of scale, district cooling systems offer a sustainable and efficient alternative to traditional on-site cooling.

As urban populations grow and the focus on sustainability intensifies, district cooling systems are poised to play a vital role in shaping the future of our cities, ensuring a cooler and more environmentally friendly urban environment.

#chillers market#chillers#refrigeration#cooling appliances#retail#consumer goods#global market#market research#innovation#market trends#industry insights

0 notes

Text

#Vegetables#freight tracking#Refrigerated Trailer#Refrigerated Trailer Market#Refrigerated Trailer Industry Trends#Refrigerated Trailer Market Analysis

0 notes

Text

What Are Most-Significant Applications of Industrial Refrigeration Systems?

The ongoing COVID-19 pandemic has put the spotlight on the global healthcare ecosystem, as many of the myths about how advanced the medical infrastructure around the world is were busted. With the case and death counts rising, the industry was caught gasping for breath (metaphorically), while the patients were literally gasping for breath (COVID is a lung infection). During this time, the number of research studies being conducted in the pharmaceutical and healthcare sectors on virology skyrocketed, as a vaccine was to be the leader of the charge against the pandemic.

Therefore, the number of clinical trials being conducted for viral vaccines rose massively, as did the worldwide trade of vaccines, aided by several such products getting regulatory approvals. With the healthcare and pharmaceutical sectors expected to not drop their guard for many years to come, the industrial refrigeration systems market size, as calculated by P&S Intelligence, is predicted to increase to $41.1 billion in 2030 from $26.8 billion in 2019, at a 5.0% CAGR between 2020 and 2030.

This is because an efficient, unbroken cold chain is essential for drug development and trade. Refrigerators are not only used to store and transport the final pharmaceutical products but also for the storage and transportation of the raw materials. Pharmaceuticals, biosimilars, excipients, active ingredients, tissues, and blood products are extremely sensitive to heat; therefore, effective cooling is necessary to protect them from damage and make them viable for use over a long time.

Another sector where refrigeration is important for the same reason is food and beverage. Most agricultural products spoil in the heat, which is why keeping them in cool conditions is paramount. Several of the processed food packages carry the directions “store in a cool and dry place”. In food processing factories, the ingredients, intermediate goods, and final products must be refrigerated to increase their shelf life. Thus, with the rising disposable income allowing people in developing countries to purchase processed food, the demand for industrial-grade refrigerators among food and beverage companies is surging.

Other industries where refrigeration is vital are oil and gas, construction, and manufacturing. Since, the food and beverage sector has been the largest user of such systems, their sales have been the highest in Asia-Pacific (APAC). Home to the largest number of people in the world, APAC has the most-productive food and beverage industry. India is already home to the fifth-largest processed food industry, which continues to garner extensive government support. “…the food processing sector in India has received around US$ 7.54 billion worth of Foreign Direct Investment (FDI) during the period April 2000-March 2017.”, says the India Brand Equity Foundation (IBEF).

Moreover, recently, the Indian government announced plans to establish 40 mega food parks, which are essentially integrated manufacturing districts for the food and beverage sector. With this, the industrial refrigeration systems market is poised for strong growth, with such equipment being important in this industry. Moreover, Invest India expects the country’s food processing sector to value more than $500 billion by 2025, which reflects a consistently growing demand for processing equipment.

Hence, with the pharmaceutical and food and beverage production growing, the procurement of industrial-grade refrigerators will escalate too.

#Industrial Refrigeration Systems Market Share#Industrial Refrigeration Systems Market Size#Industrial Refrigeration Systems Market Growth#Industrial Refrigeration Systems Market Applications#Industrial Refrigeration Systems Market Trends

1 note

·

View note

Text

#Refrigerant Compressors Market#Refrigerant Compressors Market Trends#Refrigerant Compressors Market Growth#Refrigerant Compressors Market Industry#Refrigerant Compressors Market Research#Refrigerant Compressors Market Report

0 notes

Text

#Global Household Refrigerators and Freezers Market Size#Share#Trends#Growth#Industry Analysis#Key Players#Revenue#Future Development & Forecast

0 notes

Text

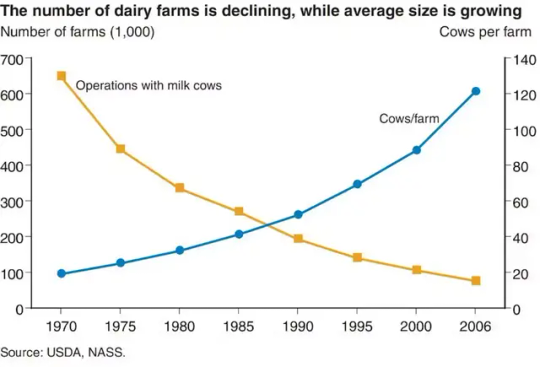

Milton Orr looked across the rolling hills in northeast Tennessee. “I remember when we had over 1,000 dairy farms in this county. Now we have less than 40,” Orr, an agriculture adviser for Greene County, Tennessee, told me with a tinge of sadness.

That was six years ago. Today, only 14 dairy farms remain in Greene County, and there are only 125 dairy farms in all of Tennessee. Across the country, the dairy industry is seeing the same trend: In 1970, more than 648,000 US dairy farms milked cattle. By 2022, only 24,470 dairy farms were in operation.

While the number of dairy farms has fallen, the average herd size—the number of cows per farm—has been rising. Today, more than 60 percent of all milk production occurs on farms with more than 2,500 cows.

This massive consolidation in dairy farming has an impact on rural communities. It also makes it more difficult for consumers to know where their food comes from and how it’s produced.

As a dairy specialist at the University of Tennessee, I’m constantly asked: Why are dairies going out of business? Well, like our friends’ Facebook relationship status, it’s complicated.

The Problem with Pricing

The biggest complication is how dairy farmers are paid for the products they produce.

In 1937, the Federal Milk Marketing Orders, or FMMO, were established under the Agricultural Marketing Agreement Act. The purpose of these orders was to set a monthly, uniform minimum price for milk based on its end use and to ensure that farmers were paid accurately and in a timely manner.

Farmers were paid based on how the milk they harvested was used, and that’s still how it works today.

Does it become bottled milk? That’s Class 1 price. Yogurt? Class 2 price. Cheddar cheese? Class 3 price. Butter or powdered dry milk? Class 4. Traditionally, Class 1 receives the highest price.

There are 11 FMMOs that divide up the country. The Florida, Southeast, and Appalachian FMMOs focus heavily on Class 1, or bottled, milk. The other FMMOs, such as Upper Midwest and Pacific Northwest, have more manufactured products such as cheese and butter.

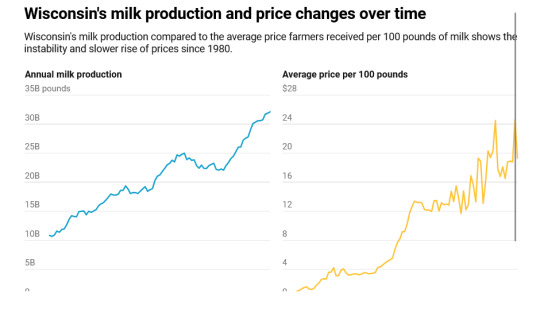

For the past several decades, farmers have generally received the minimum price. Improvements in milk quality, milk production, transportation, refrigeration, and processing all led to greater quantities of milk, greater shelf life, and greater access to products across the US. Growing supply reduced competition among processing plants and reduced overall prices.

Along with these improvements in production came increased costs of production, such as cattle feed, farm labor, veterinary care, fuel, and equipment costs.

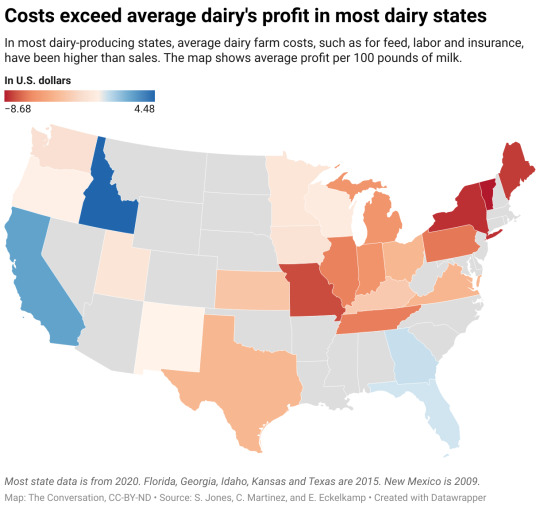

Researchers at the University of Tennessee in 2022 compared the price received for milk across regions against the primary costs of production: feed and labor. The results show why farms are struggling.

From 2005 to 2020, milk sales income per 100 pounds of milk produced ranged from $11.54 to $29.80, with an average price of $18.57. For that same period, the total costs to produce 100 pounds of milk ranged from $11.27 to $43.88, with an average cost of $25.80.

On average, that meant a single cow that produced 24,000 pounds of milk brought in about $4,457. Yet, it cost $6,192 to produce that milk, meaning a loss for the dairy farmer.

More efficient farms are able to reduce their costs of production by improving cow health, reproductive performance, and feed-to-milk conversion ratios. Larger farms or groups of farmers—cooperatives such as Dairy Farmers of America—may also be able to take advantage of forward contracting on grain and future milk prices. Investments in precision technologies such as robotic milking systems, rotary parlors, and wearable health and reproductive technologies can help reduce labor costs across farms.

Regardless of size, surviving in the dairy industry takes passion, dedication, and careful business management.

Some regions have had greater losses than others, which largely ties back to how farmers are paid, meaning the classes of milk, and the rising costs of production in their area. There are some insurance and hedging programs that can help farmers offset high costs of production or unexpected drops in price. If farmers take advantage of them, data shows they can functions as a safety net, but they don’t fix the underlying problem of costs exceeding income.

Passing the Torch to Future Farmers

Why do some dairy farmers still persist, despite low milk prices and high costs of production?

For many farmers, the answer is because it is a family business and a part of their heritage. Ninety-seven percent of US dairy farms are family owned and operated.

Some have grown large to survive. For many others, transitioning to the next generation is a major hurdle.

The average age of all farmers in the 2022 Census of Agriculture was 58.1. Only 9 percent were considered “young farmers,” age 34 or younger. These trends are also reflected in the dairy world. Yet, only 53 percent of all producers said they were actively engaged in estate or succession planning, meaning they had at least identified a successor.

How to Help Family Dairy Farms Thrive

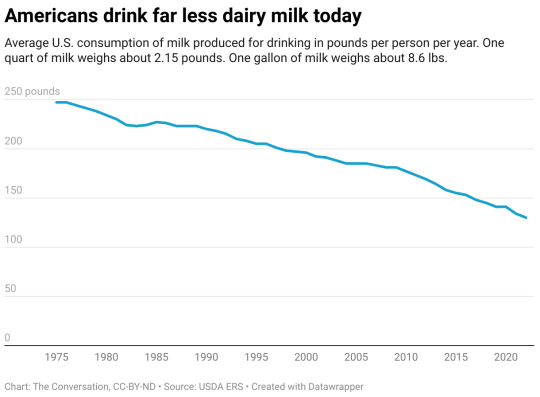

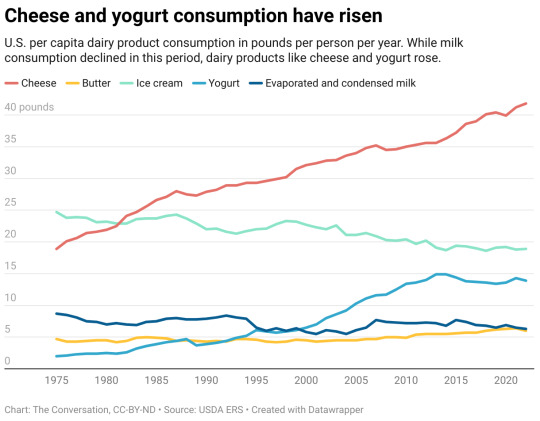

In theory, buying more dairy would drive up the market value of those products and influence the price producers receive for their milk. Society has actually done that. Dairy consumption has never been higher. But the way people consume dairy has changed.

Americans eat a lot, and I mean a lot, of cheese. We also consume a good amount of ice cream, yogurt, and butter, but not as much milk as we used to.

Does this mean the US should change the way milk is priced? Maybe.

The FMMO is currently undergoing reform, which may help stem the tide of dairy farmers exiting. The reform focuses on being more reflective of modern cows’ ability to produce greater fat and protein amounts; updating the cost support processors receive for cheese, butter, nonfat dry milk, and dried whey; and updating the way Class 1 is valued, among other changes. In theory, these changes would put milk pricing in line with the cost of production across the country.

The US Department of Agriculture is also providing support for four Dairy Business Innovation Initiatives to help dairy farmers find ways to keep their operations going for future generations through grants, research support, and technical assistance.

Another way to boost local dairies is to buy directly from a farmer. Value-added or farmstead dairy operations that make and sell milk and products such as cheese straight to customers have been growing. These operations come with financial risks for the farmer, however. Being responsible for milking, processing, and marketing your milk takes the already big job of milk production and adds two more jobs on top of it. And customers have to be financially able to pay a higher price for the product and be willing to travel to get it.

33 notes

·

View notes

Text

A While-Reading Review:

The Secret Life of Groceries

By Benjamin Lorr

Part 1

At the 1956 International Food Congress in Rome […]the USDA set up an “American way exhibit.” It featured the first fully stocked supermarket outside of the United States. This was a modest staging, designed more for easy assembly and dismantling. It held a mere 2,500 brands, a few packaged meats in a lone refrigerated case, and a small selection of prepared food. When the exhibit opened, and crowds finally entered, the Italian women went berserk. One notable enthusiast began running up and down the aisles shouting, “It must be heaven…There are mountains of food!” Press reports described others as standing “stunned,” “goggle eyed,” “bewildered,” and “shrieking with surprise and envy.”

This was not media hype. Pope Pius XII himself weighed in, announcing his blessing from the Holy See. (Page 36)

I’ve never knew how much the grocery store is such an American thing. It could’ve only flourished and happen in America, originally. It as a normal way of life solidified before World War II, and by the 1950’s it became a social fact, just how you shop for food. This oversimplified summary is full of examples: 7/11’s start in the 1920’s, the rise of Piggly Wiggly’s (with It’s GameStop meme shorting story), and building a store so big it covers an entire square foot. While the world lost its minds over a very little mock grocery store in 1956, we were already living in Costco size stores.

So how did we get here? What in our mind causes the supermarket? It doesn’t answer it, if anything, its whole argument relies off of your familiarity with the American and the introduction of Joe Coulombe, the Trader Joe.

How Joe survived the corporate super market area of the 1956’s is nothing more than the true rebirth of American entrepreneurism. No truly, look up his theory papers: he combined the design philosophy of the Boeing 747 (newly released), targeting educated, but poor, GI Bill college students, and purchasing as self-expression. This was revolutionary in the sense that he had enough disposable, advent-grade, intellect that read the symbolism of America and pointed it towards his stores. He did everything, EVERYTHING, himself. He read laws to undermine industry norms and created new trends and cravings. He took risks and every tenth experiment hit, but it is nothing like our Trader Joe’s, he sold it and is run by someone else now.

This is a fantastic introduction into the mirror that is the American mind that became engrossed in the image and likeness of the supermarket. When you hear of the haphazardness, the care, and the expense that created our modern grocery stores, it is truly only down hill from here.

2 notes

·

View notes

Text

Exploring the Growing $21.3 Billion Data Center Liquid Cooling Market: Trends and Opportunities

In an era marked by rapid digital expansion, data centers have become essential infrastructures supporting the growing demands for data processing and storage. However, these facilities face a significant challenge: maintaining optimal operating temperatures for their equipment. Traditional air-cooling methods are becoming increasingly inadequate as server densities rise and heat generation intensifies. Liquid cooling is emerging as a transformative solution that addresses these challenges and is set to redefine the cooling landscape for data centers.

What is Liquid Cooling?

Liquid cooling systems utilize liquids to transfer heat away from critical components within data centers. Unlike conventional air cooling, which relies on air to dissipate heat, liquid cooling is much more efficient. By circulating a cooling fluid—commonly water or specialized refrigerants—through heat exchangers and directly to the heat sources, data centers can maintain lower temperatures, improving overall performance.

Market Growth and Trends

The data centre liquid cooling market is on an impressive growth trajectory. According to industry analysis, this market is projected to grow USD 21.3 billion by 2030, achieving a remarkable compound annual growth rate (CAGR) of 27.6%. This upward trend is fueled by several key factors, including the increasing demand for high-performance computing (HPC), advancements in artificial intelligence (AI), and a growing emphasis on energy-efficient operations.

Key Factors Driving Adoption

1. Rising Heat Density

The trend toward higher power density in server configurations poses a significant challenge for cooling systems. With modern servers generating more heat than ever, traditional air cooling methods are struggling to keep pace. Liquid cooling effectively addresses this issue, enabling higher density server deployments without sacrificing efficiency.

2. Energy Efficiency Improvements

A standout advantage of liquid cooling systems is their energy efficiency. Studies indicate that these systems can reduce energy consumption by up to 50% compared to air cooling. This not only lowers operational costs for data center operators but also supports sustainability initiatives aimed at reducing energy consumption and carbon emissions.

3. Space Efficiency

Data center operators often grapple with limited space, making it crucial to optimize cooling solutions. Liquid cooling systems typically require less physical space than air-cooled alternatives. This efficiency allows operators to enhance server capacity and performance without the need for additional physical expansion.

4. Technological Innovations

The development of advanced cooling technologies, such as direct-to-chip cooling and immersion cooling, is further propelling the effectiveness of liquid cooling solutions. Direct-to-chip cooling channels coolant directly to the components generating heat, while immersion cooling involves submerging entire server racks in non-conductive liquids, both of which push thermal management to new heights.

Overcoming Challenges

While the benefits of liquid cooling are compelling, the transition to this technology presents certain challenges. Initial installation costs can be significant, and some operators may be hesitant due to concerns regarding complexity and ongoing maintenance. However, as liquid cooling technology advances and adoption rates increase, it is expected that costs will decrease, making it a more accessible option for a wider range of data center operators.

The Competitive Landscape

The data center liquid cooling market is home to several key players, including established companies like Schneider Electric, Vertiv, and Asetek, as well as innovative startups committed to developing cutting-edge thermal management solutions. These organizations are actively investing in research and development to refine the performance and reliability of liquid cooling systems, ensuring they meet the evolving needs of data center operators.

Download PDF Brochure :

The outlook for the data center liquid cooling market is promising. As organizations prioritize energy efficiency and sustainability in their operations, liquid cooling is likely to become a standard practice. The integration of AI and machine learning into cooling systems will further enhance performance, enabling dynamic adjustments based on real-time thermal demands.

The evolution of liquid cooling in data centers represents a crucial shift toward more efficient, sustainable, and high-performing computing environments. As the demand for advanced cooling solutions rises in response to technological advancements, liquid cooling is not merely an option—it is an essential element of the future data center landscape. By embracing this innovative approach, organizations can gain a significant competitive advantage in an increasingly digital world.

#Data Center#Liquid Cooling#Energy Efficiency#High-Performance Computing#Sustainability#Thermal Management#AI#Market Growth#Technology Innovation#Server Cooling#Data Center Infrastructure#Immersion Cooling#Direct-to-Chip Cooling#IT Solutions#Digital Transformation

2 notes

·

View notes

Text

How To Start A Bakery Business From Home

1. Introduction

2. Research and Planning

3. Legal Requirements

4. Setting Up Your Home Bakery

5. Expanding Your Business

1. Introduction

Starting a bakery business from home is an exciting venture for anyone with a passion for baking. It allows you to transform your hobby into a profitable business without the overhead costs of a commercial space. This guide will walk you through the essential steps to start a successful home bakery, from planning and legal requirements to setting up your kitchen and expanding your operations.

2. Research and Planning

Market Research

Before you begin baking, it’s crucial to conduct thorough market research. Identify your target market, understand their preferences, and analyze local competitors. This information will help you identify gaps in the market and opportunities for your bakery. Research trends in the baking industry to determine what types of products are in demand.

Business Plan

A solid business plan is the foundation of any successful business. Outline your business goals, target market, product offerings, and marketing strategies. Include a detailed financial plan that covers startup costs, ongoing expenses, pricing strategy, and projected revenue. A well-thought-out business plan will guide your decisions and help secure funding if needed.

3. Legal Requirements

Licensing and Permits

Operating a home bakery requires specific licenses and permits. Contact your local health department to understand the requirements in your area. Common permits include a food establishment permit, home occupation permit, and business license. Ensuring compliance with these regulations is crucial to avoid fines and legal issues.

Health and Safety Regulations

Your home kitchen must meet health department standards for sanitation, storage, and food handling. Familiarize yourself with the FDA’s food safety guidelines and prepare for regular inspections to ensure compliance. Adhering to these regulations is essential to protect your customers and build a reputable business.

4. Setting Up Your Home Bakery

Space Allocation

Designate a specific area in your home for your bakery operations. This space should be separate from your personal kitchen use to maintain cleanliness and organization. Efficient storage solutions for ingredients, tools, and finished products are vital to keep your workspace functional and tidy.

Essential Equipment

Investing in the right equipment is crucial for your bakery’s success. Essential items include a high-quality oven, stand mixer, baking sheets, measuring tools, mixing bowls, and cooling racks. Depending on your product offerings, you might need specialized tools like cake-decorating supplies or bread-proofing baskets.

Commercial Kitchen Equipment u/PartsFPS

As your business grows, consider investing in commercial kitchen equipment. Commercial ovens, mixers, refrigerators, and freezers offer higher performance and durability than home-grade equipment. These tools can handle larger quantities and improve efficiency, making them a valuable investment for a growing bakery.

Commercial Kitchens

If demand for your products exceeds your home kitchen’s capacity, you might consider rentinga commercial kitchen. These spaces are equipped with industrial-grade equipment and ample space, allowing you to increase production and efficiency. Moving to a commercial kitchen can be a significant step in expanding your business.

5. Expanding Your Business

Hiring Staff

As your business grows, you may need to hire additional help. Look for individuals with experience in baking and customer service. Ensure they are trained in food safety and handling to maintain your bakery’s standards and product quality.

Marketing and Branding

Building a strong brand identity is essential for differentiating your bakery in a competitive market. Develop a memorable name, logo, and packaging that reflect the quality and personality of your products. Use social media platforms like Instagram and Facebook to showcase your products and engage with your audience. Consider offering promotions, discounts, and loyalty programs to attract and retain customers. Building a professional website with an online ordering system can also boost sales and reach a wider audience.

Pricing Your Products

Setting the right prices for your products is crucial for profitability. Consider the cost of ingredients, labor, packaging, and overhead when determining your prices. Regularly review your pricing strategy to ensure it remains competitive and reflects any cost changes.

Financial Management

Keep detailed financial records to monitor your bakery’s performance. Use accounting software to track income, expenses, and profits. Staying organized with your finances will make tax season easier and help you make informed business decisions. Consider consulting with an accountant to ensure your financial practices are sound.

Crafting Your Menu

Your bakery’s success will depend largely on the quality and uniqueness of your products. Experiment with recipes to create signature items that will set your bakery apart. Test your products with friends and family to gather feedback and refine your offerings.

Sourcing Ingredients

Using high-quality ingredients is crucial for producing exceptional baked goods. Establish relationships with reliable suppliers and consider buying in bulk to reduce costs. Offering organic or locally sourced ingredients can also be a unique selling point for your bakery, attracting health-conscious customers.

Conclusion

Starting a bakery business from home requires careful planning, dedication, and a passion for baking. By following these steps and investing in the right equipment and marketing strategies, you can turn your love for baking into a successful and profitable business. Whether you keep your operations small or expand into a commercial kitchen, maintaining high-quality products and excellent customer service will be key to your success. Happy baking!

#partsfps#commercial kitchen parts#food equipment parts#bakery business#home bakery#wholesale bakery

2 notes

·

View notes

Text

Inverted Squeeze Bottle Market Insight | Outlook | Growth Analysis Report 2030

Inverted Squeeze Bottle Market Report has recently added by Value Market Research, this surveillance report establishing the facts based on current scenarios, historical records from 2022 to future forecast upto 2030. This report explicit data of various outlook such as market share, size, growth rates, and industry opportunities and offering an economical advantage for business success. It furnish the 360-degree overview of the competitive landscape of the global industries. Porter’s Five Forces Model analysis has been used to understand the industry’s structure, strength, weaknesses, opportunities, threats and challenges in front of the businesses. Moreover, the report also highlights a sudden occurrence of COVID 19 impact on Inverted Squeeze Bottle market to improve future capacities and other developments.

The research report also covers the comprehensive profiles of the key players in the market and an in-depth view of the competitive landscape worldwide. The major players in the inverted squeeze bottle market include Genesis Industries, Inc., IonWays, LLC, Midland Manufacturing Company, Inc., Kyoraku Co., Ltd., The Original Squeeze Company, Suzhou Innovation Packaging Materials Co.,Ltd, Illing Company, Inc., Kaufman Container Company etc. This section consists of a holistic view of the competitive landscape that includes various strategic developments such as key mergers & acquisitions, future capacities, partnerships, financial overviews, collaborations, new product developments, new product launches, and other developments.

Get more information on "Global Inverted Squeeze Bottle Market Research Report" by requesting FREE Sample Copy at https://www.valuemarketresearch.com/contact/inverted-squeeze-bottle-market/download-sample

Market Dynamics

The growing utilization of squeeze bottles in several industries such as food, drinks, healthcare, and personal care, pharmaceuticals, and so on is the major factor driving the inverted squeeze bottle market. The huge benefits are associated with squeeze bottles, such as it leaves less waste, Better control of food quantity, Easy fit into refrigerator door shelves, and require less space in the refrigerator, which might create high market demand in the coming years across the food industry. The rising popularity of fast food and Italian food like pasta and pizza among consumers across the globe is positively impacting the inverted squeeze bottle market’s growth. Moreover, the rapidly growing food and beverage industry across the globe is likely to create lucrative growth opportunities for key players of the Inverted squeeze bottle market in the coming years.

The research report covers Porter’s Five Forces Model, Market Attractiveness Analysis, and Value Chain analysis. These tools help to get a clear picture of the industry’s structure and evaluate the competition attractiveness at a global level. Additionally, these tools also give an inclusive assessment of each segment in the global market of inverted squeeze bottle. The growth and trends of inverted squeeze bottle industry provide a holistic approach to this study.

Browse Global Inverted Squeeze Bottle Market Research Report with detailed TOC at https://www.valuemarketresearch.com/report/inverted-squeeze-bottle-market

Market Segmentation

This section of the inverted squeeze bottle market report provides detailed data on the segments at country and regional level, thereby assisting the strategist in identifying the target demographics for the respective product or services with the upcoming opportunities.

By Closure Type

Flip Top Cap

Plug Orifice Cap

Screw Cap

Others

By Material Type

Polyethylene Terephthalate (Pet)

Polypropylene (Pp)

High Density Polyethylene (Hdpe)

Others

By Capacity

Up To 100 Ml

100 Ml To 250 Ml

250 Ml To 500 Ml

500 Ml To 750 Ml

Above 750 Ml

By End Use Industry

Food & Beverages

Automobile

Personal Care & Hygiene

Healthcare & Pharmaceutical

Chemicals

Others

Regional Analysis

This section covers the regional outlook, which accentuates current and future demand for the Inverted Squeeze Bottle market across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Further, the report focuses on demand, estimation, and forecast for individual application segments across all the prominent regions.

Purchase Complete Global Inverted Squeeze Bottle Market Research Report at https://www.valuemarketresearch.com/contact/inverted-squeeze-bottle-market/buy-now

About Us:

Value Market Research was established with the vision to ease decision making and empower the strategists by providing them with holistic market information.

We facilitate clients with syndicate research reports and customized research reports on 25+ industries with global as well as regional coverage.

Contact:

Value Market Research

401/402, TFM, Nagras Road, Aundh, Pune-7.

Maharashtra, INDIA.

Tel: +1-888-294-1147

Email: [email protected]

Website: https://www.valuemarketresearch.com

#Inverted Squeeze Bottle Market#Inverted Squeeze Bottle Market Report#Inverted Squeeze Bottle Industry#Inverted Squeeze Bottle Industry Report

2 notes

·

View notes

Text

How to Start a Food Processing Business: A Complete Guide

Are you interested in launching a business that processes food because you have a strong passion for it? Starting a business that processes food is a terrific way to make your passion profitable. But launching a company that processes food can be challenging and needs careful planning and preparation. We will provide you a step-by-step explanation of how to launch a food processing business in this manual.

Introduction :

It's critical to comprehend what food processing is before getting into the technicalities of launching a firm in this industry. Processing food entails converting basic materials into finished goods. Cooking, baking, canning, freezing, and packing are some examples of this.

The food processing sector is significant and expanding, with a $4 trillion global market. The industry is divided into a number of subsectors, including those that prepare meat and poultry, dairy products, fruits and vegetables, and snack foods.

Market Research :

Before starting any business, it is important to conduct thorough market research to determine if there is a demand for your product. In the case of food processing, you will want to research the industry trends, consumer preferences, and competitors in your market.

Some key questions to consider during your market research include:

- What are the current trends in the food processing industry?

- Who are your competitors and what are their products and pricing strategies?

- Who are your target customers and what are their preferences?

- What are the regulatory requirements for starting a food processing business in your area?

Business Planning :

Once you have conducted your market research, it is time to develop a business plan. A business plan is a document that outlines your business goals, target market, products and services, marketing and sales strategies, financial projections, and more.

Your business plan should include the following sections:

- A concise explanation and description of your business and its goals

- Market research is the analysis of your competitors, target market, and current market trends.

Services and products a list of the products and services you provide

- Sales and marketing plans: How you plan to promote and market your products.

- Budgetary goals: a projection of your expenses and income for the ensuing three to five years.

Financing :

Starting a food processing business can be expensive, so it is important to have a solid financing plan in place. There are a variety of financing options available, including loans, grants, and investors.

Some key factors to consider when seeking financing include:

- How much capital do you need to start your business?

- What is your business credit score?

- Do you have collateral to secure a loan?

- Are there any grants or incentives available in your area?

Equipment and Supplies :

Once you have secured financing, it is time to purchase the equipment and supplies you will need to start your business. The specific equipment and supplies you will need will depend on the type of food processing business you are starting.

Some common equipment and supplies needed for a food processing business include:

- Processing equipment, such as ovens, mixers, and blenders

- Packaging equipment, such as sealers and labelers

- Storage equipment, such as refrigerators and freezers

- Ingredients and raw materials

Developing a Product Line :

Your ability to sell your products will have a big impact on how well your food processing company does. It's critical to have a product lineup that appeals to your target market and distinguishes you from your rivals.

Keeping the following things in mind will help you design your product line:

- Your target market's preferences and needs

- The price point of your products

- The packaging and labelling of your products

- The shelf life of your products

- The availability of ingredients and raw materials

Marketing and Sales :

Once you have developed your product line, it is important to develop a marketing and sales strategy to promote your products. Your marketing and sales strategy should be tailored to your target market and should aim to differentiate your products from those of your competitors.

Some key marketing and sales considerations include:

Developing a brand identity and messaging that resonates with your target market

Identifying your distribution channels, such as retail stores or online marketplaces

Developing a pricing strategy that is competitive but still profitable

Creating a promotional plan, such as social media advertising or email marketing campaigns

Legal Compliance and Safety :

The operation of a food processing firm requires adherence to numerous regulatory and safety requirements. Depending on the kind of food processing business you're beginning and where it's located, you'll need to adhere to a certain set of rules.

Among the most important legal and safety factors are:

securing the authorizations and licences required to run your enterprise

observing food safety guidelines, such as those established by the FDA and USDA

planning a HACCP (Hazard Analysis and Critical Control Points) strategy

upholding sanitization and hygiene standards

ensuring that your staff is educated on proper food handling and safety practices

Conclusion :

Although it requires careful planning and preparation, starting a food processing business can be a rewarding and profitable venture. You can improve your chances of success by carrying out in-depth market research, creating a strong business plan, obtaining finance, buying the essential tools and materials, developing a product line, and putting a marketing and sales strategy into action. The health and safety of your clients and staff are also dependent on your ability to adhere to legal and safety requirements. You can convert your love of cooking into a successful business with the correct preparation and execution.

2 notes

·

View notes

Text

Low Warming Potential (GWP) Refrigerants Market – Industry Trends and Forecast to 2030 Companies: Growth, Share, Value, Analysis, and Trends

Low Warming Potential (GWP) Refrigerants Market Size And Forecast by 2030

According to Data Bridge Market Research Data Bridge Market Research analyses that the Global Low Global Warming Potential (GWP) Refrigerants Market which was USD 24.56 Billion in 2022 is expected to reach USD 63.94 Billion by 2030 and is expected to undergo a CAGR of 12.70% during the forecast period of 2022 to 2030

Our comprehensive Low Warming Potential (GWP) Refrigerants Market report is ready with the latest trends, growth opportunities, and strategic analysis. https://www.databridgemarketresearch.com/reports/global-low-gwp-refrigerants-market

**Segments**

- By Type: - Natural Refrigerants - Hydrocarbons - Fluorocarbons - Inorganics

- By Application: - Air Conditioning - Refrigeration - Heat Pumps - Others

- By End-User: - Residential - Commercial - Industrial

- By Region: - North America - Europe - Asia Pacific - Latin America - Middle East and Africa

The low GWP refrigerants market can be segmented based on type, application, end-user, and region. In terms of type, natural refrigerants, hydrocarbons, fluorocarbons, and inorganics are the key segments. While in terms of application, the market includes air conditioning, refrigeration, heat pumps, and other applications. Furthermore, the end-user segment consists of residential, commercial, and industrial sectors. Geographically, the market is divided into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa regions.

**Market Players**

- Honeywell International Inc. - The Chemours Company - Arkema SA - Daikin Industries Ltd. - Linde plc - SRF Limited - Aspen Refrigerants, Inc. - A-Gas - Puyang Zhongwei Fine Chemical Co., Ltd. - Harp International Ltd.

Key players in the low GWP refrigerants market include Honeywell International Inc., The Chemours Company, Arkema SA, Daikin Industries Ltd., Linde plc, SRF Limited, Aspen Refrigerants, Inc., A-Gas, Puyang Zhongwei Fine Chemical Co., Ltd., and Harp International Ltd. These market players are focusing on research and development activities to introduce new and innovative refrigerant solutions with lower global warming potential, thus contributing to the market growth.

https://www.databridgemarketresearch.com/reports/global-low-gwp-refrigerants-market The global low GWP refrigerants market is witnessing significant growth due to the increasing environmental concerns and strict regulations imposed on the use of high global warming potential refrigerants. The market is driven by the rising demand for energy-efficient and eco-friendly cooling solutions across various end-user industries such as residential, commercial, and industrial sectors. Natural refrigerants are gaining traction in the market due to their low environmental impact and excellent thermodynamic properties. Hydrocarbons, on the other hand, are being increasingly adopted as they have zero ODP (Ozone Depletion Potential) and low GWP characteristics.

In terms of applications, the air conditioning segment dominates the market share as there is a growing need for cooling solutions in commercial and residential buildings. Refrigeration applications are also significant contributors to the market revenue, driven by the expanding food and beverage industry globally. Heat pumps are seeing increased adoption in residential and industrial sectors for heating and cooling purposes, further fueling the demand for low GWP refrigerants. Other applications such as chillers and heat exchangers are also creating opportunities for market growth.

The market players, including Honeywell International Inc., The Chemours Company, and Daikin Industries Ltd., are focusing on strategic initiatives such as partnerships, collaborations, and product innovations to strengthen their market presence. For instance, companies are investing in the development of next-generation refrigerants that offer superior performance while minimizing environmental impact. The emphasis on research and development activities is aimed at enhancing the efficiency and safety of refrigerants while ensuring compliance with regulatory standards.

North America and Europe are mature markets for low GWP refrigerants, driven by stringent regulations aimed at phasing out high GWP refrigerants such as hydrofluorocarbons (HFCs). The Asia Pacific region is witnessing significant growth in the market, attributed to rapid industrialization, urbanization, and increasing awareness about environmental sustainability. Latin America and the Middle East and Africa regions are also showing potential for market expansion, driven by the growing demand for sustainable cooling solutions in various industries.

Overall, the global low GWP refrigerants market is poised for robust growth in the coming years, driven by the increasing awareness about climate change, sustainability goals, and the shift towards environmentally friendly refrigerant solutions. The market players' focus on innovation and collaborations will play a key role in shaping the market landscape and meeting the evolving needs of consumers across different regions.The global low GWP refrigerants market is witnessing dynamic growth fueled by environmental concerns and regulatory pressure to phase out high global warming potential refrigerants. Market segmentation plays a crucial role in understanding the diverse landscape of the industry. The categorization of refrigerants into natural refrigerants, hydrocarbons, fluorocarbons, and inorganics allows for a strategic analysis of the market based on their properties and environmental impact. Similarly, segmenting by applications such as air conditioning, refrigeration, heat pumps, and other uses provides insights into the specific demands of different end-user industries.

The end-user segmentation into residential, commercial, and industrial sectors highlights the varying needs for low GWP refrigerants across different settings. Residential sectors prioritize energy efficiency and eco-friendliness in cooling solutions, while the commercial sector, with its emphasis on cost-effectiveness and performance, drives the demand for innovative refrigerant solutions. The industrial sector, on the other hand, requires refrigerants that can meet the rigorous demands of critical industrial processes while maintaining environmental sustainability.

Geographically, the market segmentation into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa regions showcases the global footprint of the low GWP refrigerants market. Different regions exhibit varying levels of market maturity, regulatory landscape, and consumer awareness regarding sustainable refrigerant solutions. North America and Europe, being mature markets, are characterized by stringent regulations and high adoption rates of low GWP refrigerants. In contrast, the Asia Pacific region is experiencing rapid growth driven by industrialization, urbanization, and a shifting focus towards environmental sustainability.

Market players such as Honeywell International Inc., The Chemours Company, and Daikin Industries Ltd. are pivotal in driving innovation and market growth. Through strategic initiatives like partnerships, collaborations, and continuous research and development, these key players are developing advanced refrigerant solutions that meet both performance and environmental criteria. The emphasis on collaboration and innovation reflects the industry's commitment to providing sustainable cooling solutions in line with global climate goals.

In conclusion, the global low GWP refrigerants market is on a trajectory of strong growth driven by environmental awareness, regulatory mandates, and consumer preferences for sustainable cooling solutions. Market players' focus on innovation, partnerships, and product development will continue to shape the market dynamics and address the evolving needs of consumers across different regions. The market segmentation provides a comprehensive framework for analyzing the industry trends, opportunities, and challenges, paving the way for a sustainable and eco-friendly future in refrigeration and cooling technologies.**Segments**

Global Low Global Warming Potential (GWP) Refrigerants Market, By Refrigerant Type: - Inorganics - Carbon Dioxide - Ammonia - Hydrocarbons - Propane - Propene (Propylene) - Isobutene - Hydrofluoroolefins (HFOs) - Others

End Use: - Commercial Refrigeration - Domestic Refrigeration - Industrial Refrigeration - Automotive - Food Processing - HVAC - Others

Application: - Refrigeration - Air Conditioning - Chillers

The global low GWP refrigerants market exhibits a diverse landscape based on various segments. The refrigerant types include inorganics, carbon dioxide, ammonia, hydrocarbons, propane, propene, isobutene, hydrofluoroolefins (HFOs), and other variants. These different refrigerant types cater to a wide range of applications across commercial refrigeration, domestic refrigeration, industrial refrigeration, automotive, food processing, HVAC, and other sectors. In terms of applications, the market covers refrigeration, air conditioning, and chillers, each serving distinct purposes across different industries.

**Market Players**

- Arkema (France) - Dongyue Group Co. Ltd. (China) - Honeywell International Inc. (U.S.) - The Chemours Company (U.S.) - Linde Plc (Ireland) - Air Liquide (France) - Sinochem Lantian Co. Ltd. (China) - Daikin Industries Ltd. (Japan) - Mexichem (Mexico) - AGC Inc (Japan) - Gas Servei (Spain) - Gujarat Fluorochemicals Ltd. (India) - Quimobasicos (Mexico) - Zhejiang Fotech International Co. Ltd. (China) - Tazzetti S.p.A. (Italy) - SRF Limited (India) - Changshu Sanaifu Zhonghao Chemical New Material Co., Ltd (China) - Shandong Yuhuang Chemical Group Co., Ltd (China)

Market players in the low GWP refrigerants sector include a mix of international and regional companies such as Arkema, Dongyue Group, Honeywell International, The Chemours Company, Linde Plc, Air Liquide, Sinochem Lantian, Daikin Industries, Mexichem, AGC Inc, Gas Servei, Gujarat Fluorochemicals, Quimobasicos, Zhejiang Fotech International, Tazzetti, SRF Limited, Changshu Sanaifu Zhonghao Chemical, and Shandong Yuhuang Chemical Group. These market players are actively involved in driving innovation, research, and development to offer sustainable refrigerant solutions with low global warming potential, in alignment with the industry trends and regulatory requirements.

The global low GWP refrigerants market is experiencing robust growth driven by the rising environmental concerns and the push for sustainable refrigerant alternatives. The regulatory landscape emphasizing the phase-out of high GWP refrigerants is propelling the adoption of eco-friendly solutions across various end-use industries. The application of different refrigerant types in commercial, domestic, and industrial refrigeration, automotive, food processing, HVAC systems, and other sectors highlights the versatile nature of low GWP refrigerants in meeting diverse industry needs.

Market players play a key role in shaping the industry dynamics through strategic collaborations, product innovations, and expansion into emerging markets. These companies are investing in cutting-edge technologies to develop advanced refrigerant solutions that not only meet performance standards but also align with environmental objectives. The increasing focus on sustainability and compliance with regulations is pushing market players to enhance their product portfolios and cater to the evolving demands of customers across regions worldwide.

In conclusion, the global low GWP refrigerants market presents a promising outlook with continuous innovation, regulatory compliance, and partnerships driving market growth. The diverse segmentation of refrigerant types, end-uses, and applications provides a comprehensive understanding of the market landscape and opportunities for expansion. Market players are vital in driving the industry forward by introducing sustainable refrigerant solutions and addressing the growing need for environmentally friendly cooling technologies across various sectors globally.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies in Low Warming Potential (GWP) Refrigerants Market : https://www.databridgemarketresearch.com/reports/global-low-gwp-refrigerants-market/companies

Key Questions Answered by the Global Low Warming Potential (GWP) Refrigerants Market Report:

What is the current state of the Low Warming Potential (GWP) Refrigerants Market, and how has it evolved?

What are the key drivers behind the growth of the Low Warming Potential (GWP) Refrigerants Market?

What challenges and barriers do businesses in the Low Warming Potential (GWP) Refrigerants Market face?

How are technological innovations impacting the Low Warming Potential (GWP) Refrigerants Market?

What emerging trends and opportunities should businesses be aware of in the Low Warming Potential (GWP) Refrigerants Market?

Browse More Reports:

https://www.databridgemarketresearch.com/reports/global-arenavirus-infections-treatment-markethttps://www.databridgemarketresearch.com/reports/global-antibacterial-markethttps://www.databridgemarketresearch.com/reports/global-ivd-regulatory-affairs-outsourcing-markethttps://www.databridgemarketresearch.com/reports/global-herbaceous-legumes-markethttps://www.databridgemarketresearch.com/reports/global-agave-nectar-market

Data Bridge Market Research:

☎ Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC: +653 1251 982

✉ Email: [email protected]

0 notes

Text

Europe Plant-Based Meat Products Market Size, Growth, Analysis and Forecast 2030

The Europe Plant-Based Meat Products Market is poised for significant growth, with projections indicating an increase from US 2,060.30 million in 2021 to US 2,060.30 million in 2021 to US 5,311.09 million by 2028, reflecting a compound annual growth rate (CAGR) of 14.5% during this period. This growth is driven by several key factors, including the rising vegetarian and vegan population, heightened health consciousness, and the endorsement of plant-based diets by health professionals to mitigate chronic health issues such as obesity, heart disease, and high blood pressure. 𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞: https://www.businessmarketinsights.com/sample/BMIRE00025605

Key Drivers of Market Growth:

Health Concerns: Increasing awareness of the health benefits associated with plant-based diets is prompting consumers to reduce meat consumption.

Veganism Trend: The surge in veganism, evidenced by high search volumes on Google and participation in campaigns like Veganuary, underscores a cultural shift towards plant-based eating.

Technological Advancements: Innovations in product features and technologies are enabling vendors to attract new customers and penetrate emerging markets.

Market Segmentation:

The Europe plant-based meat products market is segmented based on type, category, distribution channel, and country.

By Type: The market includes patties, nuggets, meatballs, sausages, and others. Patties dominated the market in 2020.

By Category: Products are categorized into frozen, refrigerated, and ambient, with the frozen segment leading in 2020.

By Distribution Channel: The market is divided into supermarkets and hypermarkets, convenience stores, online retail, and others. Supermarkets and hypermarkets were the dominant segment in 2020.

By Country: The market covers Germany, France, the UK, Italy, Russia, and the Rest of Europe, with the Rest of Europe segment leading in 2020.

Leading Companies:

Prominent players in the market include Beyond Meat, Kellogg’s Company, Tofurky, VBites Foods Ltd, Quorn, and Impossible Foods Inc. by Altair.

Strategic Insights:

Strategic insights for the Europe plant-based meat products market emphasize a data-driven approach to understanding the industry landscape. These insights provide actionable recommendations for stakeholders to identify untapped market segments and develop unique value propositions. By leveraging data analytics, industry players can anticipate market shifts and position themselves for long-term success. This future-oriented perspective is crucial for investors, manufacturers, and other stakeholders aiming to achieve profitability and meet their business objectives in this dynamic market.

In summary, the Europe plant-based meat products market is on a robust growth trajectory, driven by health trends, technological innovations, and a shifting consumer base towards plant-based diets. Stakeholders who effectively leverage strategic insights and adapt to market dynamics are well-positioned to capitalize on this burgeoning industry. About Us:

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications

Author’s Bio: Akshay Senior Market Research Expert at Business Market Insights

0 notes