#High-Temperature Composite Materials Market Market Forecast

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

In 2020, 27% of US Tumblr users had an annual household income of over $100,000.

Text

High-Temperature Composite Materials Industry: Global Overview, Size, Analysis, Growth Opportunities, Top Manufacturers, Market Share, Trends, Segmentation, Regional Analysis, and Forecast

High-temperature composite materials are a class of composite materials that are designed to withstand extreme temperatures. These materials are used in a variety of applications, including aerospace, automotive, and industrial applications. The materials are composed of a combination of two or more components, such as carbon fibers, glass fibers, and resin, which are designed to retain their…

View On WordPress

#High-temperature Composite Materials#High-temperature Composite Materials Market#High-temperature Composite Materials Market Size#High-Temperature Composite Materials Market Companies#High-Temperature Composite Materials Market Manufacturers#High-Temperature Composite Materials Market Market Analysis#High-Temperature Composite Materials Market Market Forecast#High-Temperature Composite Materials Market Market Opportunities#High-Temperature Composite Materials Market Market Share#High-Temperature Composite Materials Market Market Trends

0 notes

Text

Automotive Heat Shields Market Trends, Innovations, and Future Outlook to 2030

The Automotive Heat Shields market is expected to grow from USD 12.67 Billion in 2024 to USD 16.31 Billion by 2030, at a CAGR of 4.30% during the forecast period.

The automotive heat shields market has emerged as a critical component of the global automotive industry, driven by the increasing demand for enhanced vehicle performance, efficiency, and safety. Automotive heat shields are designed to protect various components of a vehicle from excessive heat generated by the engine, exhaust systems, and other high-temperature areas. These shields play a vital role in improving the longevity of automotive parts, reducing heat-related wear and tear, and ensuring optimal performance.

One of the key factors contributing to the growth of the automotive heat shields market is the rising emphasis on lightweight materials in vehicle manufacturing. With stringent regulations aimed at reducing carbon emissions and improving fuel efficiency, automakers are incorporating lightweight heat shields made of advanced materials such as aluminum, composites, and multi-layered insulating fabrics. These materials not only reduce the overall weight of the vehicle but also enhance thermal management capabilities.

For More Insights into the Market, Request a Sample of this Report https://www.reportprime.com/enquiry/sample-report/19917

The increasing adoption of electric and hybrid vehicles (EVs and HEVs) has further accelerated the demand for automotive heat shields. EVs and HEVs generate significant heat from their batteries and powertrain systems, necessitating efficient heat shielding solutions to maintain safety and performance. Manufacturers are focusing on developing innovative heat shields tailored to the unique requirements of these vehicles, contributing to market expansion.

Regional dynamics play a crucial role in shaping the automotive heat shields market. In developed regions such as North America and Europe, the market is driven by the presence of leading automakers, advanced manufacturing capabilities, and stringent regulatory frameworks. Meanwhile, the Asia-Pacific region is witnessing rapid growth due to increasing vehicle production, rising disposable incomes, and the growing popularity of electric mobility in countries like China, Japan, and India.

Market Segmentations

By Type: Rigid Heat Shield, Flexible Heat Shield, Textile Heat Shield

By Applications: Passenger Vehicle, Light Commercial Vehicle

Get Full Access of This Premium Report https://www.reportprime.com/checkout?id=19917&price=3590

The competitive landscape of the automotive heat shields market is characterized by continuous innovation and strategic collaborations. Major players such as Dana Incorporated, ElringKlinger AG, Tenneco Inc., Lydall, Inc., and Autoneum are investing heavily in research and development to introduce advanced heat shield solutions. These companies are also expanding their manufacturing capacities and forging partnerships with automakers to strengthen their market position.

Despite the promising growth prospects, the automotive heat shields market faces several challenges. The fluctuating prices of raw materials and the high cost of advanced heat shielding technologies can impact profitability for manufacturers. Additionally, the complexity of designing heat shields for modern vehicles with compact engine compartments and intricate powertrains presents a technical challenge.

The future of the automotive heat shields market is promising, with numerous opportunities on the horizon. The global shift toward electric and autonomous vehicles is expected to drive innovation in heat shielding technologies. Furthermore, the integration of smart heat shields equipped with sensors and data-monitoring capabilities is anticipated to become a key trend, enhancing the efficiency and safety of next-generation vehicles.

0 notes

Text

The Hazardous Chemicals Packaging Market is projected to grow from USD 11335 million in 2024 to an estimated USD 18066.26 million by 2032, with a compound annual growth rate (CAGR) of 6% from 2024 to 2032. The hazardous chemicals packaging market is a critical component of the global supply chain, ensuring the safe transport, storage, and handling of potentially dangerous substances. As industries such as pharmaceuticals, agriculture, petrochemicals, and manufacturing continue to expand, the demand for robust and compliant packaging solutions has grown exponentially.

Browse the full report at https://www.credenceresearch.com/report/hazardous-chemicals-packaging-market

Market Overview

Hazardous chemicals packaging encompasses a wide range of containers, including drums, Intermediate Bulk Containers (IBCs), pails, and cylinders, designed to contain substances that pose risks to health, safety, or the environment. The primary objective of this packaging is to prevent leaks, spills, and contamination, while complying with stringent regulations set forth by authorities like the United Nations, the U.S. Department of Transportation (DOT), and the European Union’s ADR (Agreement Concerning the International Carriage of Dangerous Goods by Road).

The market’s growth is being driven by industrialization, globalization of trade, and the increasing focus on safety and environmental sustainability. In 2022, the global hazardous chemicals packaging market was valued at approximately $15 billion and is projected to reach $25 billion by 2030, growing at a compound annual growth rate (CAGR) of 6%.

Key Market Drivers

Regulatory Compliance: Strict regulations for the packaging and transportation of hazardous materials are a significant driver. Packaging must meet rigorous testing standards to ensure it can withstand shocks, pressure changes, and corrosive materials.

Growth in End-Use Industries: Industries such as chemicals, pharmaceuticals, and agriculture are witnessing rapid growth. These sectors rely heavily on hazardous chemicals, necessitating robust packaging solutions.

Focus on Sustainability: Increasing environmental awareness is pushing manufacturers to adopt sustainable packaging solutions. Recyclable materials, reusable containers, and innovative designs are gaining traction.

Global Trade Expansion: The globalization of trade has led to the increased movement of hazardous chemicals across borders, driving the need for standardized and compliant packaging solutions.

Challenges in the Market

Stringent Regulatory Frameworks: While regulations drive the market, they also pose challenges for manufacturers. Compliance requires constant updates to packaging designs and materials, increasing costs and time-to-market.

Material Costs: The cost of high-quality, durable materials such as stainless steel, high-density polyethylene (HDPE), and composite materials can be prohibitive for smaller manufacturers.

Complex Supply Chains: Ensuring the safe and compliant transportation of hazardous chemicals across global supply chains is logistically challenging, especially in regions with varying regulatory requirements.

Environmental Concerns: Balancing the need for durable, leak-proof packaging with environmental sustainability is a significant hurdle. Non-biodegradable materials continue to dominate the market, raising concerns about their long-term environmental impact.

Emerging Trends

Smart Packaging: IoT-enabled packaging solutions are being developed to monitor temperature, pressure, and other parameters during transportation. These innovations improve safety and reduce losses.

Customization: Manufacturers are offering tailored solutions to meet specific industry requirements, ensuring compliance and enhancing operational efficiency.

Lightweight and Durable Materials: Advances in material science are leading to the development of lightweight yet durable materials, reducing transportation costs and environmental impact.

Recyclable and Reusable Packaging: With the push for a circular economy, manufacturers are increasingly focusing on recyclable and reusable packaging solutions that minimize waste.

Future Outlook

The hazardous chemicals packaging market is poised for significant growth, driven by advancements in technology, regulatory evolution, and the increasing focus on sustainability. Emerging economies in Asia-Pacific and Latin America are expected to play a pivotal role, given their expanding industrial base and rising trade activities.

However, the market’s growth will depend on the industry’s ability to innovate while addressing environmental concerns and adhering to stringent regulations. Collaboration between manufacturers, regulatory bodies, and end-users will be crucial in shaping the future of this critical sector.

Key Player Analysis:

BASF SE

Berry Global Inc.

EnviroTech Custom Injection Molders, Inc.

Greif Inc.

Grief Flexible Products & Services

Hawman Container Services

International Paper

Mauser Packaging Solutions

Precision IBC

Schütz GmbH & Co. KGaA

Thielmann Group

Time Technoplast Ltd.

Segmentation:

By Product Type

Drums

Steel Drums

Plastic Drums

Intermediate Bulk Containers (IBCs)

Rigid IBCs

Flexible IBCs

Bottles & Cans

Cartons & Boxes

Pails

By Material

Plastic

High-Density Polyethylene (HDPE)

Polyethylene Terephthalate (PET)

Metal

Steel

Aluminum

Composite Materials

Paperboard

By End-Use Industry

Chemical Industry

Pharmaceuticals

Oil and Gas

Agriculture

Automotive

Paints and Coatings

Food and Beverage (Specialized Chemicals)

By Distribution Channel

Direct Sales

Distributors

By Region

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/hazardous-chemicals-packaging-market

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

0 notes

Text

Basalt Fiber Market: Revolutionizing Industries with Sustainability and High Performance

Basalt fiber might not yet be a household name, but it’s quickly earning its place as a material that’s rewriting the rules in several industries. What makes basalt fiber stand out is its ability to combine sustainability with high performance—two qualities that industries today are desperate to balance.

Sourced from volcanic rock, basalt fibers are incredibly strong, lightweight, and resistant to extreme conditions. Unlike some conventional materials, their production doesn’t require harmful chemicals, making them an eco-friendly alternative. For industries like construction, automotive, wind energy, electronics, and marine, basalt fiber isn’t just an option—it’s a necessity for staying relevant in a world demanding greener and better-performing materials.

The global basalt fiber market is poised for significant growth, with an expected valuation of USD 279 million in 2023, and a projected Compound Annual Growth Rate (CAGR) of

12.5% throughout the forecasted period, aiming to reach USD 503 million by 2028.

The Unique Strength of Basalt Fiber

The appeal of basalt fiber goes beyond its novelty. It is naturally robust, boasting high tensile strength and resistance to corrosion. Imagine a material that can endure the harshest environments—extreme heat, chemicals, or even saltwater—without breaking down. That’s basalt fiber.

But what really excites engineers and designers is its versatility. It’s lightweight yet tough, cost-effective yet high-performing, and, perhaps most importantly in today’s climate-conscious world, recyclable and non-toxic.

Unlike carbon fiber, which can be expensive, or fiberglass, which may fall short in eco-credentials, basalt fiber is the perfect middle ground. Its production process—melting volcanic rock at high temperatures and pulling it into fibers—requires no additives, which keeps it clean and simple.

Applications Driving Basalt Fiber Demand

1. Building Stronger, Greener Infrastructure

In construction, basalt fiber is making waves as a revolutionary reinforcement material. For decades, we’ve relied on steel, but in environments prone to moisture or chemicals, steel corrodes, leading to costly repairs and maintenance. Basalt fibers offer a solution with corrosion resistance and durability that outlasts traditional materials.

Think of bridges, seawalls, or even underground tunnels—structures where durability is critical. Basalt fiber-reinforced concrete doesn’t just last longer; it’s also lighter, which reduces transportation costs and simplifies installation.

2. Transforming Automotive and Transportation

The automotive world is laser-focused on cutting weight to improve fuel efficiency and meet stringent emission norms. Basalt fiber fits perfectly into this equation. From car body panels to interior components, its strength-to-weight ratio is hard to ignore.

It’s also popping up in trucks, trains, and even shipping containers. A lighter vehicle isn’t just more fuel-efficient—it also reduces wear and tear on roads, making basalt fiber a win-win for the entire transportation ecosystem.

3. Boosting Wind Energy Efficiency

The renewable energy industry is turning to basalt fiber for its ability to handle stress and environmental extremes. Wind turbine blades, in particular, face constant mechanical and environmental challenges. Basalt fibers provide the strength, flexibility, and weather resistance needed to enhance blade performance and longevity.

For a sector trying to reduce costs while improving energy output, basalt fiber-based composites are becoming the go-to material.

4. Enhancing Electrical and Electronic Safety

Basalt fiber’s non-conductive properties make it a natural fit for the electrical and electronics industry. It’s used in circuit boards, insulation, and protective casings. With the growing emphasis on energy-efficient appliances and safer electronics, basalt fiber ensures products meet performance and safety standards.

5. Sailing Ahead in the Marine Industry

Saltwater is unforgiving, especially for traditional materials like steel or fiberglass. Basalt fiber’s resistance to saltwater and chemicals makes it ideal for marine applications like boat hulls, underwater pipelines, and fishing rods.

It’s lightweight, meaning ships and boats consume less fuel, contributing to greener maritime operations. For an industry battling both environmental and cost pressures, basalt fiber is a breath of fresh air.

Why Basalt Fiber is the Future

Sustainability Leads the Way

The days of choosing materials purely for performance are over. Sustainability is no longer optional. Basalt fiber’s eco-friendly production process—requiring no harmful additives—makes it a leader in sustainable materials.

Infrastructure Investments

With nations modernizing old infrastructure and building new projects, there’s a growing need for corrosion-resistant, durable materials. Basalt fiber fits the bill perfectly, ensuring longevity in everything from highways to high-rises.

Growing Demand in Emerging Markets

Emerging economies in regions like Asia-Pacific and the Middle East are adopting basalt fibers rapidly, thanks to their cost-effectiveness and versatility. These regions are investing heavily in infrastructure, automotive production, and renewable energy, making them hotbeds for basalt fiber adoption.

To know more download PDF Brochure :

Basalt fiber isn’t just a trend—it’s a material that aligns perfectly with the needs of modern industries. Whether it’s reducing carbon footprints, improving performance, or cutting costs, basalt fiber is proving its worth across sectors.

For experts in construction, automotive, wind energy, electronics, or marine industries, basalt fiber is no longer something to keep an eye on—it’s something to embrace. It’s not just the material of the future; it’s the material of today.

#Basalt Fiber Market#Sustainable Materials#Construction Materials#Automotive Industry#Wind Energy Components#Eco-Friendly Materials#Renewable Energy Materials

0 notes

Text

High Performance Plastics Market

High-Performance Plastics Market Size, Share, Trends: BASF SE Leads

Increasing Demand for Light-Weight Materials in the Automotive Industry

Market Overview:

The global High-Performance Plastics Market is projected to grow at a CAGR of 7.5% from 2024 to 2031, reaching USD 35.2 billion by 2031 from USD 21.3 billion in 2024. Asia-Pacific is expected to dominate the market throughout the forecast period. The market growth is driven by increasing demand from various end-use industries such as automotive, aerospace, and electronics, where high-performance plastics are valued for their superior mechanical, thermal, and chemical properties. These materials offer significant advantages over conventional plastics and metals, including weight reduction, improved fuel efficiency, and enhanced durability.

DOWNLOAD FREE SAMPLE

Market Trends:

As the automobile industry transitions to electric vehicles and fuel efficiency standards encourage the use of lighter-weight materials, high-performance polymers are emerging as viable alternatives to traditional materials. Within this market, high-performance polymers, such as engineering plastics and composites, are likely to see the most growth. For example, the global market for engineering plastics in automotive applications was valued at $YY billion in 2022 and is expected to increase to $YY billion by 2031, at a 6.9% CAGR. These lightweight, high-strength polymers are increasingly being used to make electric car battery enclosures, interior components, and other structural pieces, reducing overall vehicle weight and enhancing energy efficiency.

Market Segmentation:

Fluoropolymers dominate the market generally. Fluoropolymers including PTFE and PVDF are driving the market for high-performance plastics thanks in significant part to their strong chemical resistance, low friction properties, and high temperature stability. For these materials, demandable applications abound: chemical processing equipment, non-stick cookware, high-performance seals and gaskets. Emphasizing reduced environmental impact and improved recyclability, new developments in fluoropolymer technology serve to address growing industry sustainability challenges.

Market Key Players:

The high-performance plastics industry is highly competitive, with major players focusing on strategic projects including mergers and acquisitions, product developments, and capacity building if they are to keep their market share. Key companies such as BASF SE, Solvay S.A., DuPont de Nemours, Inc., Arkema Group, Evonik Industries AG, Celanese Corporation, Victrex plc, Daikin Industries, Ltd., Sumitomo Chemical Co., Ltd., and Toray Industries, Inc. dominate the market.

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

Logistics Packaging Market: Advanced Technologies in Packaging Design

The Logistics Packaging Market is expected to experience robust growth during the forecast period, driven by increasing global trade activities, the rapid expansion of e-commerce, and the rising demand for durable and efficient packaging solutions across various industries. Innovations in sustainable materials and customized packaging solutions are also contributing to market expansion.

Read Complete Report Details of Logistics Packaging Market: https://www.snsinsider.com/reports/logistics-packaging-market-2728

Market Segmentation

By Packaging Durability Type

Flexible Logistics Packaging

Description: Includes lightweight and adaptable materials such as films, wraps, and bags used for packaging.

Growth Drivers: Rising demand for cost-effective and space-saving solutions in logistics.

Trends: Adoption of biodegradable and recyclable flexible materials.

Rigid Logistics Packaging

Description: Includes sturdy and durable containers such as crates, pallets, and drums.

Growth Drivers: Increased use in heavy-duty and long-distance transportation.

Trends: Growing use of returnable and reusable rigid packaging solutions.

By Material Durability Type

Durable Goods

Description: Packaging solutions for long-lasting products like electronics, machinery, and furniture.

Growth Drivers: Growth in international trade of durable goods.

Trends: Use of customized and protective packaging to prevent damage during transit.

Non-Durable Goods

Description: Packaging for perishable or short-lifespan goods like food, beverages, and healthcare products.

Growth Drivers: Increased demand for logistics solutions in the food and pharmaceutical industries.

Trends: Emphasis on temperature-controlled and sustainable packaging solutions.

By Material

Plywood

Growth Drivers: Preferred for packaging heavy and fragile goods due to its high strength-to-weight ratio.

Trends: Use of treated plywood to enhance durability and prevent moisture damage.

Wood

Growth Drivers: Traditional material used for crates and pallets, especially in export packaging.

Trends: Shift towards certified and sustainably sourced wood materials.

Corrugated

Growth Drivers: Lightweight and recyclable, widely used in e-commerce and retail packaging.

Trends: Innovations in corrugated box design to improve strength and reduce material usage.

Plastic

Growth Drivers: Durable and versatile, used in both flexible and rigid packaging solutions.

Trends: Increasing use of recycled and biodegradable plastics.

Steel

Growth Drivers: Utilized for high-value and heavy-duty logistics needs.

Trends: Development of lighter steel packaging solutions to reduce costs.

Others

Growth Drivers: Includes innovative materials such as composite and foam-based packaging.

Trends: Exploration of new materials with better environmental profiles.

By End-Users

Automotive

Growth Drivers: Rising demand for protective packaging for automotive parts and components.

Trends: Use of reusable packaging solutions to reduce costs and waste.

Healthcare

Growth Drivers: Growth in pharmaceutical logistics and demand for temperature-sensitive packaging.

Trends: Adoption of tamper-proof and sterile packaging solutions.

Food & Beverages

Growth Drivers: Expanding global food trade and the need for protective and insulated packaging.

Trends: Use of innovative materials to extend product shelf life.

Manufacturing

Growth Drivers: Increasing industrial production and export of machinery and equipment.

Trends: Emphasis on robust packaging to ensure safety during transportation.

Consumer Goods

Growth Drivers: Rising e-commerce activities driving demand for lightweight and protective packaging.

Trends: Customization and branding through packaging design.

Others

Growth Drivers: Includes niche sectors such as electronics and textiles requiring specialized logistics packaging.

Trends: Tailored solutions for unique industry needs.

By Type

Individual Packaging

Description: Packaging designed for single items or units.

Growth Drivers: High demand in the e-commerce and retail sectors.

Trends: Focus on aesthetic appeal and sustainability.

Inner Packaging

Description: Protective materials used within outer packaging to secure products.

Growth Drivers: Increased focus on product safety during transit.

Trends: Use of air cushions, foam, and other shock-absorbent materials.

Outer Packaging

Description: Larger packaging solutions for bulk and long-distance transportation.

Growth Drivers: Rising exports and need for robust packaging.

Trends: Development of collapsible and reusable outer packaging.

Regional Outlook

North America

Growth Drivers: Strong e-commerce market and advanced logistics infrastructure.

Trends: Emphasis on sustainable packaging solutions to align with environmental regulations.

Europe

Growth Drivers: High export volume and stringent packaging standards.

Trends: Increasing investment in biodegradable and recyclable materials.

Asia-Pacific

Growth Drivers: Rapid industrialization, urbanization, and e-commerce growth.

Trends: Expansion of logistics networks in emerging markets like India and Southeast Asia.

Latin America

Growth Drivers: Growing trade activities and development of regional logistics hubs.

Trends: Demand for cost-effective and durable packaging solutions.

Middle East & Africa

Growth Drivers: Expanding oil & gas exports and increasing food imports.

Trends: Focus on customized and robust packaging for industrial applications.

Market Trends and Opportunities

Sustainability: Rising focus on environmentally friendly materials, including biodegradable plastics and recyclable corrugated packaging.

Customization: Growing demand for tailored packaging solutions to cater to industry-specific needs.

Technology Integration: Adoption of IoT-enabled packaging for real-time tracking and monitoring during transit.

E-Commerce Growth: Increased emphasis on lightweight, durable, and cost-effective packaging to support last-mile delivery.

Market Outlook

The Logistics Packaging Market is poised for substantial growth through 2032, driven by increasing globalization, advancements in packaging materials, and rising consumer demand for efficient and sustainable packaging. Innovations in design and technology will play a key role in shaping the market, with a strong emphasis on reducing environmental impact while enhancing product safety and cost-efficiency.

About Us:

SNS Insider is a global leader in market research and consulting, shaping the future of the industry. Our mission is to empower clients with the insights they need to thrive in dynamic environments. Utilizing advanced methodologies such as surveys, video interviews, and focus groups, we provide up-to-date, accurate market intelligence and consumer insights, ensuring you make confident, informed decisions.

Contact Us:

Akash Anand – Head of Business Development & Strategy

Phone: +1-415-230-0044 (US) | +91-7798602273 (IND)

0 notes

Text

Automotive Fastener Market: Industry Trends, Growth Drivers, and Future Outlook to 2030

The Automotive Fastener market is expected to grow from USD 33.75 Billion in 2024 to USD 45.49 Billion by 2030, at a CAGR of 5.10% during the forecast period.

The automotive fastener market plays a critical role in ensuring the structural integrity and operational efficiency of vehicles. Fasteners, which include screws, bolts, nuts, rivets, and washers, are essential components used to join different vehicle parts together. These components are designed to withstand stress, vibration, and environmental factors while providing safety and reliability in automotive applications. The market has witnessed significant growth over the years, driven by advancements in vehicle design, increasing demand for lightweight materials, and the transition to electric vehicles (EVs).

For More Insights into the Market, Request a Sample of this Report https://www.reportprime.com/enquiry/sample-report/19878

Market Dynamics

Rising Demand for Lightweight Materials Automotive manufacturers are increasingly adopting lightweight materials like aluminum and composites to reduce vehicle weight, improve fuel efficiency, and comply with stringent emission regulations. This shift has created demand for advanced fasteners that are compatible with these lightweight materials while maintaining strength and durability.

Growth of Electric Vehicles (EVs): The transition to EVs has opened new avenues for the automotive fastener market. EVs require specialized fasteners to accommodate unique components like battery packs and electric drivetrains. These fasteners need to be corrosion-resistant, lightweight, and capable of withstanding high temperatures, driving innovation in the sector.

Technological Advancements in Fasteners Modern fasteners are designed with improved functionality, such as self-locking capabilities, high tensile strength, and resistance to wear and tear. The integration of smart fasteners with sensors that monitor torque and tension has become a key trend, particularly in high-performance vehicles.

Stringent Regulations and Safety Standards Regulatory requirements for vehicle safety and quality are compelling automakers to adopt high-quality fasteners that comply with global standards. This has boosted demand for precision-engineered fasteners with enhanced reliability.

Market Segmentations

By Type: Iron, Nickel, Brass, Stainless Steel, Aluminum

By Applications: Passenger Car, Commercial Vehicle

Regional Analysis

The automotive fastener market in North America is driven by the region's advanced automotive industry, with a focus on innovation and high-performance vehicles. The growth of EVs and government incentives for sustainable transportation further bolster demand. Europe is a significant market for automotive fasteners, driven by stringent emission norms and the presence of leading automakers. The region's push toward electric and hybrid vehicles has created opportunities for advanced fastener solutions.

Get Full Access of This Premium Report https://www.reportprime.com/checkout?id=19878&price=3590

Competitive Landscape

The automotive fastener market is highly competitive, with key players focusing on innovation, strategic partnerships, and expansion into emerging markets. Prominent companies include Stanley Engineered Fastening, Illinois Tools Work Inc, Sundarm Fasteners, Bulten AB, Trifast, Koninklijke Nedschroef Holding B.V, Penn Engineering & Manufacturingoration, Phillips Screw, Rocknel Fastener, Precision Castparts.

These companies are investing in R&D to develop advanced fasteners that cater to the evolving needs of automakers. For instance, LISI Automotive has introduced lightweight fasteners designed for EV battery systems, while ITW focuses on corrosion-resistant solutions for high-stress applications.

Future Outlook

The global automotive fastener market is projected to grow at a steady compound annual growth rate (CAGR) of around 4%-6% from 2024 to 2030. Factors such as the increasing adoption of EVs, advancements in vehicle design, and the demand for lightweight and durable materials will continue to drive market expansion.

However, challenges such as fluctuating raw material prices and the availability of substitutes like adhesives and welding techniques may pose constraints. Despite these challenges, the market’s focus on sustainability, innovation, and compliance with global standards will ensure its growth trajectory in the coming years.

0 notes

Text

Thermosetting Plastics Market Size, Regional Revenue and Outlook 2025-2037

Research Nester assesses the growth and market size of the global thermosetting plastics market which is anticipated to be on account of the rising demand for bio dependent thermosetting plastic

Research Nester’s recent market research analysis on “Thermosetting Plastics Market: Global Demand Analysis & Opportunity Outlook 2037” delivers a detailed competitors analysis and a detailed overview of the global thermosetting plastics market in terms of market segmentation by type, molding process, end-user industry and by region.

Growing Demand for Bio-Based Thermosetting Plastics to Promote Global Market Share of Thermosetting Plastics Market

Request Free Sample Copy of this Report @ https://www.researchnester.com/sample-request-5892

The global thermosetting plastics market is estimated to grow majorly on account of the increased demand for polyurethane in the automotive industry. Some common uses of thermoset plastics across numerous industries and sectors include water & gas pipelines, medical equipment, storage boxes, and construction machinery parts. Since the thermosetting plastics are flexible and lightweight. Thermoset composites remain stable at all temperatures and in all ambiance. For instance, Bakelite is the most common thermoset plastic that is widely used in kitchenware, jewelry, children's toys, and pipe stems. Bakelite is also used in making switches because of its poor conductivity to electricity and heat. Other than this, epoxy resin is also applied to floors and various other surfaces to add tough coating. The global epoxy resin production stood at almost 3600 thousand tonnes in the year 2022. On the back of the rising utilization of thermoset plastics on various devices, the global thermosetting plastics market is anticipated to grow during the forecasted period. Other than this, the rising growth in the construction industry and rising demand for polyurethane in the automotive industry. Also, the advent of bio-based plastics is likely to showcase growth opportunities for the global thermosetting plastics market during the forecasted period. The properties such as chemical resistance, heat resistance, and structural integrity of the thermoset plastics are also going to augment the growth of the global thermosetting plastics market during the forecasted period.

Some of the major growth factors and challenges that are associated with the growth of the global thermosetting plastics market are:

Growth Drivers:

Rising Demand for Bio-depended Thermosetting Plastics

Surging Utilization of Thermosetting Plastics Making Kitchen Utensils

Challenges:

The rising feedstock crunch and exorbitant cost of thermosetting plastics, stringent government policies, and problems related to manufacturing techniques are some of the major factors anticipated to hamper the global market size of the global thermosetting plastics market.

Request for customization @ https://www.researchnester.com/customized-reports-5892

By type, the global thermosetting plastics market is segmented into unsaturated polyesters, polyurethanes, phenolic, epoxy, amino, alkyd, vinyl, and ester. Out of these, the unsaturated polyesters segment is expected to grow the most during the forecasted period. The growth can be attributed to the outstanding thermal opposition and high creep power of the materials.

By region, the Europe thermosetting plastics market is to generate the highest revenue by the end of 2036. The rising demand for thermosetting plastics can be attributed to the increasing utilization of epoxy for making various appliances.

This report also provides the existing competitive scenario of some of the key players of the global thermosetting plastics market which includes company profiling of Alchemie Ltd., Celanese Corporation, LANXESS, DAICEL CORPORATION, INEOS, BASF SE, Covestro A.G., BUFA GmbH & Co. KG, Daicel Corporation, Eastman Chemical Company, Asahi Kasei Corporation, Mitsui Chemicals, Inc., NIPPON STEEL Chemical & Material Co., Ltd., INOAC Corporation and others.

Access our detailed report @ https://www.researchnester.com/reports/thermosetting-plastics-market/5892

About Research Nester-

Research Nester is a leading service provider for strategic market research and consulting. We aim to provide unbiased, unparalleled market insights and industry analysis to help industries, conglomerates and executives to take wise decisions for their future marketing strategy, expansion and investment etc. We believe every business can expand to its new horizon, provided a right guidance at a right time is available through strategic minds. Our out of box thinking helps our clients to take wise decision in order to avoid future uncertainties.

Contact for more Info:

AJ Daniel

Email: [email protected]

U.S. Phone: +1 646 586 9123

U.K. Phone: +44 203 608 5919

0 notes

Text

Nickel Superalloy market Analysis, Size, Share, Growth, Trends, and Forecasts by 2031

The global nickel superalloy market represents an intriguing and dynamic sector within the metallurgical industry. This specialized market is distinctive for its extraordinary resilience and adaptability in the face of shifting industrial landscapes and technological advancements.

𝐆𝐞𝐭 𝐚 𝐅𝐫𝐞𝐞 𝐒𝐚𝐦𝐩𝐥𝐞 𝐑𝐞𝐩𝐨𝐫𝐭:https://www.metastatinsight.com/request-sample/2442

Top Companies

Precision Castparts Corp. (PCC)

ATI (Allegheny Technologies Incorporated)

Carpenter Technology Corporation

Doncasters Group Ltd

Haynes International, Inc.

Rolled Alloys, Inc.

Sandvik AB

VDM Metals GmbH

Howco Group plc.

Special Metals Corporation

Langley Alloys Ltd

Neonickel Ltd.

Voestalpine AG

Michlin Metals Inc

AMETEK, Inc

This report delves into the world of nickel superalloys, examining the essential aspects that define their uniqueness, market dynamics, applications, and the factors that drive its growth.

𝐄𝐱𝐩𝐥𝐨𝐫𝐞 𝐭𝐡𝐞 𝐅𝐮𝐥𝐥 𝐑𝐞𝐩𝐨𝐫𝐭:@https://www.metastatinsight.com/report/nickel-superalloy-market/2442

Nickel superalloys, often dubbed as high-performance alloys, are materials forged under extreme temperatures, engineered with precise elemental compositions. These alloys are primarily distinguished by their high resistance to corrosion, excellent mechanical properties at elevated temperatures, and superior durability. Composed primarily of nickel, these alloys integrate various alloying elements such as cobalt, chromium, and molybdenum to augment their performance characteristics.

The global nickel superalloy market is not just a niche industry, but a thriving ecosystem embedded within the very fabric of modern society. Its resilience is underpinned by its irreplaceable role in a wide range of applications across industries as diverse as aerospace, energy, healthcare, and manufacturing. As industries evolve and technologies advance, the nickel superalloy market continues to adapt, ensuring that high-performance materials remain a cornerstone of modern engineering and innovation.

Global Nickel Superalloy market is estimated to reach $9,110.2 Million by 2030; growing at a CAGR of 7.6% from 2023 to 2030.

Contact Us:

+1 214 613 5758

#NickelSuperalloy#NickelSuperalloymarket#NickelSuperalloyindustry#marketsize#marketgrowth#marketforecast#marketanalysis#marketdemand#marketreport#marketresearch

0 notes

Text

High Temperature Fiber Market Analysis by Growth, Emerging Trends and Future Opportunities Till 2037

Research Nester assesses the growth and market size of the global high temperature fiber market, which is anticipated to be driven by rising demand in the aerospace and defense sector as well as the growth of industrial manufacturing activities.

Research Nester’s recent market research analysis on “High Temperature Fiber Market: Global Demand Analysis & Opportunity Outlook 2037” delivers a detailed competitor’s analysis and overview of the global high temperature fiber market in terms of market segmentation by fiber type, form, application, and region.

Request for customization @

Regulatory Compliance and Safety Standards to Promote Global High Temperature Fiber Market Growth

Governments and regulatory bodies have put in place stringent laws and guidelines that require the use of high-performance materials in a variety of industries, including industrial production, construction, automotive, and aerospace. For instance, the Occupational Safety and Health Administration (OSHA) has set stringent guidelines for the usage of insulation and protective gear in high temperature environments which leads to a rise in the adoption of ceramic and aramid fibers as these are known for their durability and heat resistance. Moreover, the rising emphasis on fire safety in building codes particularly following high-profile incidents in the construction sector has increased the demand for fire-resistant materials such as aramid fibers. These regulatory guidelines and growing safety standards continue to drive modernization and market growth as companies invest in innovative materials to meet the latest compliance requirements.

Growth Drivers

Growth in electronics and automotive industries

Expansion of industrial manufacturing activities

Challenges

Competition from alternative materials plays a significant challenge for the high temperature fiber market as more affordable options are available in the market such as metal composites and certain heat-resistant polymers which progressively offer viable substitutes. For example, Metal Matrix Composites (MMC) developed polymers can deliver adequate thermal resistance for applications in industries such as construction, aerospace, and automotive which are often at a lesser cost than aramid and ceramic fibers. This cost efficiency becomes critical in sectors where the budget is tight, which limits the broader adoption of high temperature fibers.

Access our detailed report at:

Based on fiber type, the ceramicsegment is predicted to capture 52.4% of the global market share by 2037 owing to its remarkable heat resistance, thermal stability, and insulating qualities. These are extensively utilized in parts for aircraft, kiln insulation, and furnace linings that require exposure to high temperatures. In the automotive industry, ceramic fibers are widely used for thermal barriers in catalytic converters and exhaust systems. Their use in industrial operations such as glass manufacture and metal casting stems from their capacity to retain structural integrity at elevated temperatures.

By region, North America is anticipated to account for 35.1% of the revenue share during the forecast period, due to the presence of well-known aerospace and automotive giants such as Ford, General Motors, Boeing, and Airbus. By heavily relying on high-temperature fibers for essential components like exhaust systems, brakes, and aviation engines, these industry leaders highlight the critical role that these fibers play in state-of-the-art manufacturing processes. The nation continues to lead the world in materials science and engineering advancements due to a robust ecosystem composed of esteemed companies, research facilities, and a highly skilled workforce. High-performance material innovation is fueled by the region's sophisticated R&D skills, and its position is further reinforced by the presence of important industry participants and production facilities.

This report also provides the existing competitive scenario of some of the key players of the global high temperature fiber market which includes company profiling of DuPont, 3M Company, Zoltek Companies, Inc., SGL Carbon SE, Kolon Industries, Inc., Yantai Tayho Advanced Materials Co., Ltd., Toray Industries, Inc., Teijin Limited, Toyobo Co., Ltd., Mitsubishi Chemical Corporation, and Asahi Kasei Corporation.

Request Report Sample@

Research Nester is a leading service provider for strategic market research and consulting. We aim to provide unbiased, unparalleled market insights and industry analysis to help industries, conglomerates, and executives make wise decisions for their future marketing strategy, expansion investment, etc. We believe every business can expand to its new horizon, provided the right guidance at the right time is available through strategic minds. Our out-of-the-box thinking helps our clients to make wise decisions to avoid future uncertainties.

Contact for more Info:

AJ Daniel

Email: [email protected]

U.S. Phone: +1 646 586 9123

U.K. Phone: +44 203 608 5919

0 notes

Text

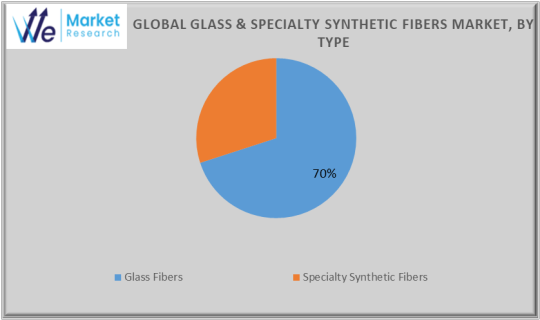

Glass Fibers & Specialty Synthetic Fibers Market Challenges, Analysis and Forecast to 2034

The Glass Fibers & Specialty Synthetic Fibers Market is a dynamic segment within the materials industry, driven by the increasing demand for lightweight, durable, and high-performance materials across various sectors. These fibers are engineered for applications that require superior mechanical properties, thermal stability, and resistance to environmental factors

The market for glass fiber and specialty synthetic fibers is expected to increase at a compound annual growth rate (CAGR) of 6.4% between 2024 and 2034. According to an average growth trend, the market is expected to reach USD 144.58 billion in 2034. The global market for glass fibers and specialty synthetic fibers is expected to generate USD 85.59 billion by 2024.

Get a Sample Copy of Report, Click Here: https://wemarketresearch.com/reports/request-free-sample-pdf/glass-and-specialty-synthetic-fibers-market/1603

Glass Fibers & Specialty Synthetic Fibers Market Growth Drivers

Urbanization and Infrastructure Growth:

Increasing investments in construction and urban development drive demand for glass fibers.

Rising Defense Budgets:

Governments worldwide are increasing investments in protective equipment using synthetic fibers.

Shift Toward Renewable Energy:

Wind energy projects favor glass fibers for turbine blades.

Advancements in Material Engineering:

Innovations are improving the properties and reducing production costs of synthetic fibers.

Specialty Synthetic Fibers: Types

Aramid Fibers:

Examples: Kevlar, Twaron.

High tensile strength and resistance to impact and heat.

Used in bulletproof vests, fire-resistant clothing, and ropes.

Carbon Fibers:

Lightweight and exceptionally strong.

Applications: Aerospace, sports equipment, automotive (luxury cars).

Ultra-High-Molecular-Weight Polyethylene (UHMWPE):

Examples: Dyneema, Spectra.

Extremely lightweight with high impact resistance.

Used in personal armor, fishing lines, and medical implants.

Polybenzimidazole (PBI):

High thermal and chemical stability.

Used in firefighting gear and aerospace insulation.

Polyimide Fibers:

Heat-resistant fibers ideal for use in high-temperature industrial applications.

Glass Fibers & Specialty Synthetic Fibers Market Challenges

High Costs of Specialty Fibers:

The manufacturing process for carbon and aramid fibers is resource-intensive.

Environmental Impact:

Synthetic fibers contribute to pollution if not recycled properly.

Competition from Emerging Materials:

Natural fibers like hemp and bamboo, as well as metal composites, are gaining attention.

Emerging Trends

Integration with Smart Technologies:

Development of fibers with embedded sensors for structural health monitoring.

Circular Economy Initiatives:

Companies are investing in recycling technologies for glass and synthetic fibers.

Hybrid Materials:

Combining glass and synthetic fibers to create composites with enhanced properties.

Glass Fibers & Specialty Synthetic Fibers Market Segmentation,

By Type

Glass Fibers

E-Glass

S-Glass

C-Glass

Others

Specialty Synthetic Fibers

Polyester

Nylon

Aramid

Carbon Fibers

Polypropylene (PP)

Others

By Application

Textile

Construction

Automotive

Aerospace & Defense

Marine

Consumer Goods

Packaging

Wind Energy

Others

Key companies profiled in this research study are,

The Global Glass Fibers & Specialty Synthetic Fibers Market is dominated by a few large companies, such as

Owens Corning

Jushi Group

PPG Industries

Saint-Gobain

China National Glass Industrial Group Corporation (CNG)

Nippon Electric Glass Co., Ltd.

Sika AG

DuPont

Solvay

Teijin Limited

Hyosung Corporation

Toray Industries

DSM (Dutch State Mines)

BASF

Asahi Kasei Corporation

Others

Glass Fibers & Specialty Synthetic Fibers Industry: Regional Analysis

Forecast for the North American market

North America will be a significant player in the glass fiber and specialized synthetic fiber industries, accounting for about 40% of the worldwide market in 2023. Due to its technological dominance and strong industrial base in the automotive, aerospace, and defense sectors, North America has a disproportionate amount. North America, particularly the United States, is a major market for glass fibers and specialty synthetic fibers.

Forecast for the European Market

Europe is an essential market for glass and specialty synthetic fibers due to the prevalence of the automobile and aerospace industries there. Countries like Germany, France, and the UK are investing in lightweight materials for cars and airplanes, which directly increases demand for fibers like glass and carbon fibers. The European Union's focus on sustainability and energy efficiency has led to a greater usage of advanced materials, such as carbon fibers for renewable energy applications like wind turbines and glass fibers for construction. Europe is the hub for research and development, particularly in the areas of lightweight composite materials and high-performance fibers for industrial applications.

Forecasts for the Asia Pacific Market

The growth of the Chinese, Japanese, and Indian industries is primarily responsible for the Asia-Pacific region's sharp increase in demand for glass fibers and specialty synthetic fibers. Particularly in countries like China, India, and Japan, the Asia-Pacific region is fast become increasingly urbanized and industrialized. This is driving the demand for glass fibers in the automotive, infrastructure construction, and building industries. The need for lightweight materials is rising in the Asia-Pacific automotive industry as a result of the rising popularity of electric vehicles (EVs) and fuel-efficient cars in countries like China and Japan. The need for glass and carbon fibers rises as a result.

Conclusion

The Glass Fibers & Specialty Synthetic Fibers Market is poised for robust growth, driven by advancements in material science, the increasing demand for lightweight and high-strength materials, and expanding applications across industries like construction, automotive, aerospace, and renewable energy. While challenges such as high production costs and environmental concerns persist, ongoing innovations in recycling and sustainable fiber production are paving the way for a greener future.

As industries worldwide prioritize efficiency, durability, and sustainability, the market for glass and specialty synthetic fibers is set to play a critical role in shaping the future of materials technology. With strong investments in R&D and the rise of eco-friendly initiatives, this market presents vast opportunities for growth and innovation.

0 notes

Text

Steel Sheet Pricing: Key Determinants and Smart Procurement Strategies

Steel sheets are a fundamental resource across industries, including manufacturing, construction, automotive, and industrial machinery. Their cost can vary significantly due to numerous factors, making it essential for buyers to understand the variables at play. This knowledge can help businesses manage budgets, plan projects efficiently, and negotiate better deals.

Factors Influencing Steel Sheet Prices

Raw Material CostsThe primary components of steel—iron ore, coal, and scrap metal—drive the base cost of steel sheets. Global demand, particularly in high-growth economies like China or India, can lead to price surges in these raw materials.

Manufacturing Process

Hot-Rolled steel sheet prices: Manufactured at high temperatures, they are generally less expensive but suitable for projects requiring basic structural strength.

Cold-Rolled Steel Sheets price: These undergo additional processing, resulting in smoother finishes and enhanced precision, which increases their price.

Steel Grades and CoatingsSteel sheets are categorized into different grades based on their strength, composition, and application. For example:

High-Strength Low-Alloy (HSLA) Steel: Costlier but offers superior performance.

Galvanized Sheets: Coated with zinc to resist corrosion, making them ideal for outdoor use but more expensive.

Global Supply and Demand TrendsEconomic activities like infrastructure development or automotive manufacturing heavily influence steel demand. A spike in global construction projects or limited steel production can cause prices to rise sharply.

Transportation and LogisticsShipping costs for steel sheets are considerable due to their weight and bulk. Proximity to suppliers and the state of logistics infrastructure can significantly affect overall expenses.

Trade Policies and TariffsImport duties and trade restrictions imposed by governments to protect domestic steel industries often lead to increased prices for imported steel sheets. For instance, U.S. tariffs on steel imports have historically raised costs for buyers relying on foreign steel.

Strategies to Optimize Steel Sheet Costs

Plan AheadSteel prices fluctuate, so scheduling purchases during periods of low demand can lock in more favorable rates.

Buy in BulkLarge orders often qualify for discounts, reducing the per-unit cost.

Source LocallyPurchasing from nearby suppliers minimizes transportation expenses and supports quicker delivery times.

Monitor Market TrendsStay informed about global commodity prices, trade policies, and steel production forecasts to make timely purchases.

Diversify SuppliersEstablish relationships with multiple vendors to mitigate risks from supply chain disruptions or pricing inconsistencies.

Conclusion

Steel sheet prices are shaped by a complex interplay of raw material costs, manufacturing techniques, market demand, logistics, and government policies. By understanding these factors and adopting strategic procurement practices, buyers can optimize their investment and secure quality materials for their projects.

If you are looking for best quality tmt bars, please visit our website : www.steeloncall.com or you can contact us through our toll-free number: 18008332929

#steelsheetprices #steelsheetpricetoday #steelsheet #steelsheetprice

0 notes

Text

Wind Turbine Composite Materials Market - Forecast(2024 - 2030)

Wind Turbine Composite Materials Market Overview

Request Sample :

The government across the globe is also investing huge amounts in alternative energy sources such as solar and wind which is further supporting the market growth for composite materials. The increasing focus of governments on offshore wind energy installations is driving the market growth between 2021–2026. However, the high cost of carbon fiber and epoxy resin and recyclability issue of composites will likely hamper the market growth during the forecast period.

COVID-19 Impact

The COVID-19 pandemic has impacted the composite materials industry which has further impacted the wind turbine market. Due to the Covid-19, the manufacturing industry is impacted very badly that further impacted the wind turbine composite materials market. The slowdown in wind turbine installations and lack of raw material supplies, and workforce are impacting the market negatively. The covid-19 impacted every operation such as supply chain, production, sales, and others. However, the companies resumed their operation in 2021, which may positively impact the market.

Report Coverage

The report: “Wind Turbine Composite Materials Market — Forecast (2021–2026)”, by IndustryARC, covers an in-depth analysis of the following segments of the Wind Turbine Composite Materials industry. By Fiber Type: Glass Fiber, Carbon Fiber, Aramid Fiber, and Basalt fiber By Resin Type: Thermoplastic [Polyethylene, Polystyrene, Polyamides, Nylon, Polypropylene, Others], and Thermoset [Epoxy, Polyester, Phenolic Polyamide, and Others] By Technology: Injection Molding, Compression Molding, Pultrusion, Filament Winding, and Layup By Application: Blades, Wind turbine Hub, Rotor, Tower, Nacelle, Cables, Blade Pitch Controller, Propellers, and Others By Geography: North America (USA, Canada, and Mexico), Europe (UK, Germany, Italy, France, Netherlands, Belgium, Spain, Denmark, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Taiwan, Malaysia, and Rest of APAC), South America (Brazil, Argentina, Colombia, Chile, and Rest of South America), and Rest of the World (the Middle East and Africa)

Inquiry Before Buying :

Key Takeaways

The Asia Pacific region is expected to dominate the market and register the highest CAGR of 12.8% during the forecast period (2021–2026). The presence of leading chemical companies along with rapid growth in the personal care industry is propelling regional growth.

Epoxy resin is one of the widely used resins in wind turbine manufacturing. The segment is expected to register a high growth rate during the forecast period.

The growing installation of wind turbines in developing countries such as Brazil, Mexico, India, and China is creating a positive impact on the usage of wind turbine composite materials.

Figure: Asia Wind Turbine Composite Materials Market Revenue, 2020–2026 (US$ Billion)

For More Details on This Report — Request for Sample

Wind Turbine Composite Materials Market Segment Analysis: By Fiber Type

The glass fiber reinforced plastics segment accounted for the largest share of more than 55% in the wind turbine composite materials market in 2020 and is estimated to grow at a significant rate during the forecast period. Glass fiber offers various properties including high strength, high durability, weather-resistant, and lightweight have boosted its demand in numerous end-use industries. The easy availability and cost-effectiveness of glass fiber reinforced plastics are the key factors propelling the demand for glass fiber composites in wind turbine manufacturing. The carbon fiber segment will register a significant growth rate during the forecast period. Carbon fibers offer various properties such as low thermal expansion, high stiffness, high-temperature tolerance, and high chemical resistance among others.

Schedule A Call:

Wind Turbine Composite Materials Market Segment Analysis: By Resin Type

The thermoset segment accounted for the largest share of more than 70% in the Wind turbine composite materials market in 2020 and is estimated to grow at a significant rate during the forecast period. Thermoset composite is usually based on carbon, glass, and aramid fibers. Epoxy resin is the widely used thermoset type in wind turbine composite materials. Approximately 50% of European wind blades are manufactured from epoxy resin. These resins offer lightweight, and good adhesion compared to other resin types. Generally, they are combined with glass fibers and carbon fibers to manufacture wind blades. The thermoplastic segment is expected to register a significant growth rate during the forecast period. Thermoplastics are less expensive compared to thermoset resin types. They are easily weld-able, non-toxic in nature, and recyclable. These are some of the driving factors supporting the market growth between 2021–2026.

Wind Turbine Composite Materials Market Segment Analysis: By Technology

The Layup segment accounted for the largest share of more than 33% in the wind turbine composite materials market in 2020 and is estimated to grow at a significant rate during the forecast period. Layup is the most common method used for the production of composites. The method is involved in placing layers of composite fiber in a structured order by using a matrix of resin and hardener. This method is widely used for the production of wind blades.

Wind Turbine Composite Materials Market Segment Analysis: By Application

The blades segment accounted for the largest market share of more than 55% of the market in 2020 and is estimated to grow significantly during the forecast period. Turbine blades serve as the most important composite-based part of wind turbines. The growing demand for wind energy is driving manufacturers to develop large wind blades for the high production of wind energy. For the development of large blades, a huge quantity of composite materials is used. Glass fibers and carbon fibers are used for the manufacturing of wind blades.

Wind Turbine Composite Materials Market Segment Analysis — By Geography

The Asia Pacific region held the largest share of more than 45% in the Wind Turbine Composite Materials market in 2020, owing to the rapid growth in the installation of wind turbines. The presence of developing nations such as China and India is driving the market growth. The presence of leading wind turbine manufacturers including Suzlon Energy Limited, and AVIC Huiteng Windpower Equipment Co., Ltd are supporting the region’s growth during the forecast period. The increasing investments by key developers for manufacturing efficient wind turbines are also boosting the market growth during the forecast period. According to the data published by Global Wind Energy Council (GWEC), China installed about 52 gigawatts of new wind power capacity in 2020.

Buy Now :

Wind Turbine Composite Materials Market Drivers

Rising Demand for Renewable Energy Sources

Wind energy is one of the fastest-growing renewable energies globally. Wind power is a clean energy source, and its usage is on the rise worldwide. The U.S. wind energy occupies approximately 38% of total renewable energy produced in 2019. According to the IRENA’s data, wind energy generation is increased from 7.5GW in 1997 to 564GW by 2018. Some ongoing and under-construction wind projects in the U.S. include Traverse Wind Energy Center, Aviator Wind Project, Goodnight Wind Energy Project, Alle-Catt Wind Farm, and Vineyard Wind I among others. According to the Ministry of New and Renewable Energy (MNRE), India has the fourth-highest wind installed capacity in the world with a total installed capacity of 39.25 GW (as of 31st March 2021) and has generated around 60.149 billion Units during 2020–2021. According to the European Commission, the total installed wind energy capacity in Europe reached 210GW and is estimated to reach 350GW, supplying up to 24% of electricity demand

Wind Turbine Composite Materials Market Challenges

Recyclability Issue of Composites

Composite materials are preferred for wind applications because of their durability and superior strength. Proper waste disposal and recycling at the end of the useful life of composite materials are necessary. Many current and future waste management and environmental legislation are making strict regulations on engineering materials to be properly recovered and recycled. The complex material compositions and the cross-linked nature of thermoset resins are making it difficult for recyclability. However, the use of polymers that can be recycled when used with carbon and other niche fibers reduces the composite non-recyclable. This has become a major issue as the landfills are filling up at a faster pace along with the need for going green due to global warming. Biological attack on composite materials may consist of fungal growth or marine fouling

Wind Turbine Composite Materials Market Landscape

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the Wind Turbine Composite Materials market. Major players include:

TPI Composites, Inc.

MFG Wind

LM Wind Power

Gamesa Corporation Technology

Vestas Wind Systems A/S

Suzlon Energy Limited

Siemens AG

AVIC Huiteng Windpower Equipment Co., Ltd.

AREVA and others.

Acquisitions/Technology Launches

In May 2021, Hexcel launched a range of HexPly® surface finishing prepregs and semi- prepregs for wind turbine blades and automotive and marine applications.

Relevant Reports

Composite Materials Market — Forecast(2021–2026) Report Code: CMR 0010

High-Temperature Composite Materials Market — Forecast(2021–2026) Report Code: CMR 10087

For more Chemicals and Materials Market reports, please click here

#WindTurbine#CompositeMaterials#RenewableEnergy#SustainableTech#GreenEnergy#MaterialInnovation#CleanEnergySolutions

0 notes

Text

Ceramic Matrix Composites Market - Latest Innovations by Industry Experts Till 2030

The global ceramic matrix composites (CMC) market was valued at approximately USD 3.40 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 12.8% from 2023 to 2030. The increasing demand for materials with high-temperature stability, reduced weight, and exceptional strength is a key driver for this market’s growth. These properties make CMCs highly valuable in demanding applications where traditional materials often fall short. The chemical industry experienced a significant shift in the first half of 2020, as companies were already facing complex, long-term challenges and were further impacted by the economic downturn associated with the COVID-19 pandemic and the concurrent oil price collapse, which influenced the entire CMC market landscape.

The high cost of ceramic fibers remains a significant factor impacting market growth. Unlike carbon fiber, commonly used in metal and polymer composites, ceramic fibers are produced in smaller quantities, which prevents them from benefiting from the economies of scale that reduce costs in high-volume production.

Gather more insights about the market drivers, restrains and growth of the Ceramic Matrix Composites Market

Ceramic matrix composites are finding increasing application in industries like electronics, thermal management, and high-performance sports equipment, where they offer advantages such as improved performance, enhanced comfort, and robust structural integrity. Over the forecast period, CMCs are anticipated to replace traditional alloys and other metals in various applications, particularly where their high thermal resistance allows them to function with minimal or no cooling requirements. This quality is particularly valued in the aviation industry, where demand for CMCs is expected to grow significantly.

The United States, as a global military leader, is a major consumer of CMCs. Additionally, the U.S. Department of Energy is researching CMC cladding for fuel rods in light-water nuclear reactors, which could boost CMC demand in the energy and power sectors. In North America, the CMC market is expected to grow as key players increase research and development efforts, expand manufacturing capacity, and broaden their product offerings.

Application Segmentation Insights:

In 2022, the aerospace segment led the CMC market, accounting for over 41.95% of the global revenue share. The demand for ceramic matrix composites in aerospace is driven by their use in manufacturing essential components like noses, rudders, fins, leading edges, body flaps, hot structures, tiles, and panels for aircraft. CMCs’ high impact strength and hardness make them ideal for these applications, as they enhance durability and safety in aerospace structures.

In addition to aerospace, CMCs are valued for their application in manufacturing bullet-proof armor and as insulators for small arms weapon platforms. Many ceramic materials are transparent to specific types of energy and light, making them suitable for infrared domes, sensor protection, and multi-spectral windows.

The energy and power sector is expected to be the fastest-growing application segment for CMCs during the forecast period. With their high-temperature stability, oxidation resistance, and radiation tolerance, CMCs are well-suited for applications in both fission and fusion energy technologies.

Ceramic matrix composites are also widely used as isolators in the electronics industry and are integral to electronic circuits due to their high thermal conductivity. Other CMC applications include laser diodes, LEDs, artificial teeth, and fuel cells, which further support market expansion. These diverse applications make CMCs a valuable material in various high-performance and emerging technological fields.

Order a free sample PDF of the Ceramic Matrix Composites Market Intelligence Study, published by Grand View Research.

0 notes

Text

Ceramic Matrix Composites Industry Overview, Challenges and Growth Opportunities Analysis till 2030

The global ceramic matrix composites (CMC) market was valued at approximately USD 3.40 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 12.8% from 2023 to 2030. The increasing demand for materials with high-temperature stability, reduced weight, and exceptional strength is a key driver for this market’s growth. These properties make CMCs highly valuable in demanding applications where traditional materials often fall short. The chemical industry experienced a significant shift in the first half of 2020, as companies were already facing complex, long-term challenges and were further impacted by the economic downturn associated with the COVID-19 pandemic and the concurrent oil price collapse, which influenced the entire CMC market landscape.

The high cost of ceramic fibers remains a significant factor impacting market growth. Unlike carbon fiber, commonly used in metal and polymer composites, ceramic fibers are produced in smaller quantities, which prevents them from benefiting from the economies of scale that reduce costs in high-volume production.

Gather more insights about the market drivers, restrains and growth of the Ceramic Matrix Composites Market

Ceramic matrix composites are finding increasing application in industries like electronics, thermal management, and high-performance sports equipment, where they offer advantages such as improved performance, enhanced comfort, and robust structural integrity. Over the forecast period, CMCs are anticipated to replace traditional alloys and other metals in various applications, particularly where their high thermal resistance allows them to function with minimal or no cooling requirements. This quality is particularly valued in the aviation industry, where demand for CMCs is expected to grow significantly.

The United States, as a global military leader, is a major consumer of CMCs. Additionally, the U.S. Department of Energy is researching CMC cladding for fuel rods in light-water nuclear reactors, which could boost CMC demand in the energy and power sectors. In North America, the CMC market is expected to grow as key players increase research and development efforts, expand manufacturing capacity, and broaden their product offerings.

Application Segmentation Insights:

In 2022, the aerospace segment led the CMC market, accounting for over 41.95% of the global revenue share. The demand for ceramic matrix composites in aerospace is driven by their use in manufacturing essential components like noses, rudders, fins, leading edges, body flaps, hot structures, tiles, and panels for aircraft. CMCs’ high impact strength and hardness make them ideal for these applications, as they enhance durability and safety in aerospace structures.

In addition to aerospace, CMCs are valued for their application in manufacturing bullet-proof armor and as insulators for small arms weapon platforms. Many ceramic materials are transparent to specific types of energy and light, making them suitable for infrared domes, sensor protection, and multi-spectral windows.

The energy and power sector is expected to be the fastest-growing application segment for CMCs during the forecast period. With their high-temperature stability, oxidation resistance, and radiation tolerance, CMCs are well-suited for applications in both fission and fusion energy technologies.

Ceramic matrix composites are also widely used as isolators in the electronics industry and are integral to electronic circuits due to their high thermal conductivity. Other CMC applications include laser diodes, LEDs, artificial teeth, and fuel cells, which further support market expansion. These diverse applications make CMCs a valuable material in various high-performance and emerging technological fields.

Order a free sample PDF of the Ceramic Matrix Composites Market Intelligence Study, published by Grand View Research.

0 notes

Text

Key Drivers Fueling Growth in the Aramid Fiber Market

The global aramid fiber market was estimated at USD 4.09 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 8.1% from 2024 to 2030. This growth is largely attributed to rising demand from various industries, including oil and gas, healthcare, and manufacturing. The increasing focus on workplace safety, driven by stringent government regulations, is anticipated to further fuel market expansion throughout the forecast period.

However, the market experienced sluggish growth during the COVID-19 pandemic, primarily due to a decline in demand from the industrial sector. Government-imposed restrictions led to temporary shutdowns across a wide range of industries, significantly limiting market activity during that period.

Gather more insights about the market drivers, restrains and growth of the Aramid Fiber Market

Market Dynamics

Aramid fibers are renowned for their strength, synthetic nature, and heat resistance. These advantageous properties make them highly desirable in military and aerospace applications, particularly for ballistic-grade body armor fabric. One of the key features of aramid fibers is that they neither ignite nor melt under typical levels of oxygen, which provides excellent flame and heat resistance. Additionally, aramid fibers serve as substitutes for metal wires and organic fibers in structural composite applications, particularly in ropes used on oil rigs, marine and aerospace industries, automobiles, and bulletproof vests. Their superior mechanical properties—5% to 10% higher than those of other synthetic fibers—enhance their applicability in these demanding environments.

The aramid fiber industry is continuously evolving, with ongoing efforts to develop and manufacture synthetic fibers that meet the demands of new technologies. This includes replacing asbestos, which is known to be carcinogenic and toxic. Aramid fibers contribute strength and wear resistance to friction materials that do not contain asbestos. They allow for the selection of inert fillers based on thermal and wear characteristics, minimizing concerns related to the physical properties of those fillers. While asbestos is strong and can withstand chemical and high-temperature exposure, making it relatively inexpensive compared to other materials, its hazardous nature makes it a less desirable option in many applications.

Aramid fibers are used in two main types of applications: reinforcement in composites and fabrics in clothing. In the composite sector, they are utilized in military vehicles, sports goods, and aircraft. In the fabric sector, aramid fibers are crucial in creating protective clothing, such as bulletproof vests and fire-resistant garments. They are extensively employed across various applications, including protective gloves, sailcloth, flame- and cut-resistant clothing, snowboards, helmets, filament-wound pressure vessels, body armor, optical fiber cable systems, ropes and cables, tire reinforcement, rubber goods, tennis strings, hockey sticks, jet engine enclosures, asbestos replacement, and circuit board reinforcement.

In the U.S. market, growth is expected to be driven by the increased adoption of advanced material handling equipment, such as wagon tipplers, belt conveyor systems, and bucket elevators. These innovations facilitate the efficient movement and handling of materials, particularly within the cement industry. Additionally, the trend towards zero-labor warehousing has led to the adoption of advanced robotic systems, which is expected to further benefit market growth. Protective gear designed to safeguard workers from risks associated with hazardous jobs and challenging environmental conditions is another critical aspect of the aramid fiber market.