#Global Agricultural Lubricant Market Competition

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr’s reach among the 26-to-35-year-olds in the US is 11%.

Text

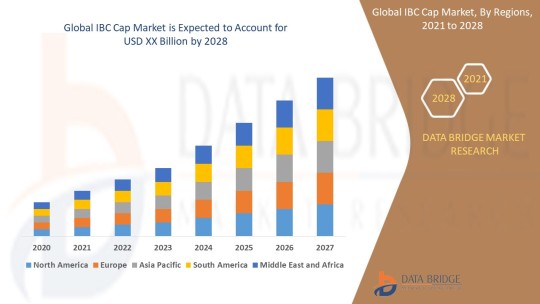

IBC Cap Market Size, Share, Trends, Growth and Competitive Analysis

"IBC Cap Market – Industry Trends and Forecast to 2028

Global IBC Cap Market, By Product Type (Flange, Plugs, Vent-in Plug, Vent-out Plug and Screw closure), Type (Plastic IBC, Metal IBC and Composite IBCs), Material Type (Plastics, Metal, Aluminium and Steel), End Use (Chemicals & Fertilizers, Petroleum & Lubricants, Paints, Inks & Dyes, Food & Beverage, Agriculture, Building & Construction, Healthcare & Pharmaceuticals and Mining), Application (Food And Drinks, Chemical Industry, Oil and Agriculture), Country (U.S., Canada, Mexico, Brazil, Argentina, Rest of South America, Germany, France, Italy, U.K., Belgium, Spain, Russia, Turkey, Netherlands, Switzerland, Rest of Europe, Japan, China, India, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific, U.A.E, Saudi Arabia, Egypt, South Africa, Israel, Rest of Middle East and Africa) Industry Trends and Forecast to 2028

Access Full 350 Pages PDF Report @

The global IBC cap market is expected to witness significant growth over the forecast period due to the increasing demand for intermediate bulk containers (IBCs) in various industries such as chemicals, food and beverages, pharmaceuticals, and others. The IBC caps play a crucial role in ensuring the safe storage and transportation of liquid products. The market growth is also being driven by technological advancements in IBC cap designs, such as tamper-evident seals and spouts for easy dispensing. Additionally, the growing focus on sustainability and recyclability of packaging materials is further boosting the adoption of IBC caps made from eco-friendly materials.

**Segments**

- Based on material type, the IBC cap market can be segmented into plastic, metal, and others. Plastic caps are widely used due to their lightweight nature and cost-effectiveness. - By cap type, the market can be categorized into screw caps, snap-on caps, and flip-top caps. Screw caps are preferred for their secure sealing properties. - On the basis of end-user industry, the market can be divided into chemicals, food and beverages, pharmaceuticals, and others. The chemicals segment is anticipated to hold a significant market share due to the widespread use of IBCs for storing chemical products.

**Market Players**

- TPS Industrial Srl - Schuetz GmbH & Co. KGaA - Mauser Packaging Solutions - Time Technoplast Ltd - Berry Global Inc. - THIELMANN UCON AG - Precision IBC, Inc. - Peninsula Packaging LLC

These market players are actively involved in strategic initiatives such as product launches, partnerships, and acquisitions to strengthen their market presence and expand their product offerings. The competitive landscape of the IBC cap market is characterized by intense competition, prompting companies to focus on innovation and quality to gain a competitive edge.

The Asia-Pacific region is expected to witness substantial growth in the IBC cap market, driven by the rapid industrialization and the increasing adoption of IBCsThe Asia-Pacific region represents a significant growth opportunity for the global IBC cap market due to several key factors. With rapid industrialization and the expanding manufacturing sector in countries like China, India, and Southeast Asia, there is a growing demand for efficient storage and transportation solutions, including IBCs and their associated caps. The increased focus on chemical production, food processing, and pharmaceutical manufacturing in the region further fuels the need for reliable packaging solutions like IBC caps. As these industries continue to grow, the adoption of IBC caps is expected to rise, driving market expansion in the Asia-Pacific region.

Moreover, the emphasis on enhancing safety standards and ensuring product integrity is a crucial factor contributing to the growth of the IBC cap market in Asia-Pacific. Regulations regarding the safe handling and transportation of hazardous chemicals and pharmaceuticals necessitate the use of high-quality caps that can effectively seal and protect the contents of IBCs. As companies in the region strive to comply with stringent regulatory requirements, the demand for advanced and secure IBC caps is projected to increase significantly.

Additionally, the shift towards sustainability and eco-friendly practices is another trend shaping the IBC cap market in Asia-Pacific. With growing environmental concerns and increasing awareness about plastic pollution, there is a rising preference for IBC caps made from recyclable and biodegradable materials. Market players in the region are focusing on developing sustainable packaging solutions to meet the evolving consumer demands and align with global sustainability goals. This shift towards eco-friendly IBC caps not only addresses environmental concerns but also presents market players with opportunities to differentiate their offerings and attract environmentally conscious customers.

Furthermore, the competitive landscape of the IBC cap market in Asia-Pacific is characterized by the presence of both local manufacturers and international players. Local companies often have a strong understanding of regional market dynamics and customer preferences, giving them a competitive advantage in catering to specific industry needs. On the other hand, multinational companies bring technological expertise and a wide product portfolio, which can appeal to a broader customer base seeking innovative and**Global IBC Cap Market, By Product Type**

- Flange - Plugs - Vent-in Plug - Vent-out Plug - Screw closure

**Type**

- Plastic IBC - Metal IBC - Composite IBCs

**Material Type**

- Plastics - Metal - Aluminium - Steel

**End Use**

- Chemicals & Fertilizers - Petroleum & Lubricants - Paints, Inks & Dyes - Food & Beverage - Agriculture - Building & Construction - Healthcare & Pharmaceuticals - Mining

**Application**

- Food And Drinks - Chemical Industry - Oil and Agriculture

The Global IBC Cap market is experiencing significant growth due to the rising demand for intermediate bulk containers across various industries. Plastic caps are increasingly preferred for their lightweight and cost-effective nature, driving market growth within the material type segment. Screw caps, known for their secure sealing properties, dominate the cap type category. The chemicals segment is anticipated to hold a substantial market share among end-user industries, attributed to the widespread use of IBCs for chemical storage. The market players in the industry are focusing on strategic initiatives like product launches and partnerships to enhance their market presence and offerings. The competitive landscape is intense, spurring companies to innovate and prioritize quality for a competitive advantage.

In Asia-Pacific, the IBC cap market is poised for robust growth fueled by rapid industrialization and the expanding manufacturing sector, particularly in countries like China,

Countries Studied:

North America (Argentina, Brazil, Canada, Chile, Colombia, Mexico, Peru, United States, Rest of Americas)

Europe (Austria, Belgium, Denmark, Finland, France, Germany, Italy, Netherlands, Norway, Poland, Russia, Spain, Sweden, Switzerland, United Kingdom, Rest of Europe)

Middle-East and Africa (Egypt, Israel, Qatar, Saudi Arabia, South Africa, United Arab Emirates, Rest of MEA)

Asia-Pacific (Australia, Bangladesh, China, India, Indonesia, Japan, Malaysia, Philippines, Singapore, South Korea, Sri Lanka, Thailand, Taiwan, Rest of Asia-Pacific)

Key Coverage in the IBC Cap Market Report:

Detailed analysis of IBC Cap Market by a thorough assessment of the technology, product type, application, and other key segments of the report

Qualitative and quantitative analysis of the market along with CAGR calculation for the forecast period

Investigative study of the market dynamics including drivers, opportunities, restraints, and limitations that can influence the market growth

Comprehensive analysis of the regions of the IBC Cap industry and their futuristic growth outlook

Competitive landscape benchmarking with key coverage of company profiles, product portfolio, and business expansion strategies

TABLE OF CONTENTS

Part 01: Executive Summary

Part 02: Scope of the Report

Part 03: Research Methodology

Part 04: Market Landscape

Part 05: Pipeline Analysis

Part 06: Market Sizing

Part 07: Five Forces Analysis

Part 08: Market Segmentation

Part 09: Customer Landscape

Part 10: Regional Landscape

Part 11: Decision Framework

Part 12: Drivers and Challenges

Part 13: Market Trends

Part 14: Vendor Landscape

Part 15: Vendor Analysis

Part 16: Appendix

Browse Trending Reports:

Calcium Glycinate Market Retinal Biologics Market Facial Fat Transfer Market Angio Suites Diagnostic Imaging Market Adoption Of Benelux Power Tools Market De Quervains Tenosynovitis Treatment Market Biodetectors And Accessories Market Colposcope Market Sports Medicine Market Automotive Adhesives Market Infrared Imaging Market Vapour Deposition Market Professional Diagnostics Market Ct Scanner Market Programmable Application Specific Integrated Circuit Asic Market Hospital Operating Room Or Products And Solutions Market Castor Oil Market Zika Virus Infection Drug Market Toluene Diisocynate Market Antibiotic Resistance Market

About Data Bridge Market Research:

Data Bridge set forth itself as an unconventional and neoteric Market research and consulting firm with unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email: [email protected]"

2 notes

·

View notes

Text

Global Market Insights: Leading Silicone Emulsion Manufacturers and Key Players

The global silicone emulsion market is experiencing significant growth, driven by its wide-ranging applications across industries such as automotive, construction, personal care, textiles, and agriculture. Silicone emulsions are water-based dispersions of silicone oils, offering excellent thermal stability, lubrication, water repellency, and eco-friendliness. These characteristics have made silicone emulsions a preferred choice in many sectors. In this evolving market, silicone emulsion manufacturers play a crucial role in driving innovation and meeting global demand for high-performance and sustainable solutions.

Market Overview and Growth Drivers

The global silicone emulsion market is poised for steady growth due to several factors:

Industrial Expansion: Increasing demand for advanced materials in industries like construction, textiles, and automotive is fueling the growth of silicone emulsions.

Eco-Friendly Solutions: Water-based silicone emulsions are preferred over solvent-based alternatives due to their environmentally friendly nature, aligning with sustainability goals.

Versatility: Silicone emulsions are used in diverse applications, including release agents, coatings, lubricants, water repellents, and personal care products.

According to market studies, the global silicone emulsion market is expected to grow at a CAGR of 6-7% in the coming years. Emerging economies in Asia-Pacific, Latin America, and Africa are driving demand, while developed markets continue to invest in technological advancements.

Key Industries Driving Demand

Automotive

Silicone emulsions are widely used as lubricants, release agents, and polishes in the automotive industry. They help reduce friction, improve durability, and enhance the appearance of automotive components.

Construction

The construction industry leverages silicone emulsions for water-repellent coatings, anti-corrosion treatments, and mold-release agents. Their durability and ability to withstand extreme weather conditions make them invaluable for modern construction solutions.

Textiles and Leather

Silicone emulsions provide a soft finish, water repellency, and shine to fabrics and leather products. Manufacturers use them to enhance the quality and appearance of textiles.

Personal Care

Silicone emulsions are integral to personal care products such as hair conditioners, skin creams, and lotions. They offer excellent spreadability, non-greasy texture, and smooth application.

Agriculture

In agriculture, silicone emulsions act as surfactants and spreaders in pesticides and fertilizers, improving their efficiency and coverage on crops.

Leading Silicone Emulsion Manufacturers and Key Players

The competitive landscape of silicone emulsion manufacturers is characterized by innovation, research and development, and expanding production capacities. The following key players dominate the global market:

Global Chemical Giants

Leading chemical companies are at the forefront of silicone emulsion production. They invest heavily in R&D to introduce high-performance and eco-friendly silicone emulsions. These manufacturers cater to industries ranging from automotive to personal care, ensuring consistent quality and innovation.

Regional Manufacturers

In growing markets like Asia-Pacific, several regional players are gaining traction by offering cost-effective silicone emulsions tailored to local needs. Countries like India and China have emerged as hubs for silicone emulsion production, contributing significantly to the global supply.

Sustainability-Focused Companies

A growing number of silicone emulsion manufacturers are prioritizing sustainable solutions by developing water-based, solvent-free formulations. These eco-friendly products address environmental concerns and comply with strict regulations worldwide.

Specialized Suppliers

Some manufacturers focus on niche applications, such as high-performance silicone emulsions for medical devices, food-grade lubricants, or advanced coatings. Their specialized products cater to unique industrial demands.

Market Trends and Innovations

The silicone emulsion market is witnessing several trends that reflect the evolving needs of industries and consumers:

Sustainability and Green Chemistry: The shift toward eco-friendly, low-VOC silicone emulsions aligns with global sustainability initiatives. Manufacturers are investing in green technologies to reduce environmental impact.

Customization: Silicone emulsion manufacturers are developing tailored products to meet the specific performance requirements of various industries, enhancing customer satisfaction.

Technological Advancements: Innovations such as nano-structured silicone emulsions are revolutionizing performance, offering improved durability and functionality.

Regional Expansion: Key players are expanding their operations in emerging markets like India, China, and Brazil to capitalize on rising industrial demand.

Challenges for Manufacturers

While the silicone emulsion market holds significant potential, manufacturers face challenges such as:

Fluctuations in raw material prices.

Compliance with strict environmental regulations.

Competition from alternative materials.

Addressing these challenges requires constant innovation, cost optimization, and adherence to sustainability standards.

Conclusion

The global silicone emulsion market continues to grow, driven by diverse industrial applications and increasing demand for sustainable solutions. Silicone emulsion manufacturers play a pivotal role in this expansion, focusing on innovation, quality, and eco-friendliness to meet market needs. As industries adopt advanced materials to improve product performance and sustainability, silicone emulsions will remain essential in sectors ranging from automotive and construction to personal care and agriculture. With the right combination of research, technology, and regional outreach, leading manufacturers are poised to shape the future of this dynamic market.

0 notes

Text

Sorbitan Monostearate Prices Trend | Pricing | News | Price | Database | Chart

Sorbitan Monostearate a versatile non-ionic surfactant widely used in various industries, has become an essential component in sectors such as food, cosmetics, pharmaceuticals, and industrial applications. Its demand has been steadily increasing due to its multifunctional properties, such as emulsification, stabilizing, and dispersing capabilities. Consequently, the prices of sorbitan monostearate have garnered significant attention from industry stakeholders. Market dynamics, including production costs, raw material availability, regulatory changes, and global trade patterns, play a crucial role in determining the price trends of this compound.

The global market for sorbitan monostearate is influenced by fluctuations in raw material costs, primarily stearic acid and sorbitol. Both of these components are derived from natural sources, such as palm oil and corn, making their prices susceptible to agricultural cycles, geopolitical developments, and environmental regulations. Recent years have seen volatility in palm oil prices due to factors such as adverse weather conditions, labor shortages, and sustainability concerns. These fluctuations directly impact the production costs of sorbitan monostearate, translating into varying market prices. Additionally, the rising demand for sustainable and bio-based products has pushed manufacturers to adopt eco-friendly practices, which can also increase production expenses.

Regional market trends significantly shape the pricing of sorbitan monostearate. In Asia-Pacific, which is a major hub for chemical production, the availability of raw materials and lower labor costs contribute to competitive pricing. However, increasing environmental regulations and stricter sustainability requirements in countries such as Indonesia and Malaysia, key palm oil producers, have started to impact the cost structures for manufacturers. In North America and Europe, where there is a growing preference for natural and organic ingredients, sorbitan monostearate commands higher prices, particularly in the food and cosmetics industries. These regions are also experiencing increased regulatory scrutiny, further driving up costs associated with compliance and quality assurance.

Get Real time Prices for Sorbitan Monostearate: https://www.chemanalyst.com/Pricing-data/sorbitan-monostearate-1538

Technological advancements and innovations in manufacturing processes have also played a role in shaping the market dynamics of sorbitan monostearate. Producers are increasingly leveraging advanced production technologies to enhance efficiency and reduce waste. These innovations help in managing production costs and, consequently, pricing. Moreover, the development of customized grades of sorbitan monostearate tailored for specific applications, such as pharmaceutical excipients or high-performance industrial lubricants, has created a premium pricing segment within the market.

Global trade policies and tariffs also impact the pricing landscape of sorbitan monostearate. Trade disputes and changing import-export regulations can create uncertainties for manufacturers and buyers alike. For instance, tariffs on raw materials or finished goods can lead to increased costs for end-users, while favorable trade agreements can result in price reductions due to enhanced market access. The dynamic geopolitical landscape necessitates continuous monitoring of such factors by market participants.

Sustainability has emerged as a key driver of market trends and pricing for sorbitan monostearate. Consumers and businesses alike are prioritizing environmentally friendly products, compelling manufacturers to adopt sustainable practices in sourcing raw materials and producing the compound. While this shift aligns with global sustainability goals, it often entails higher production costs, which are eventually reflected in market prices. Certifications and eco-labeling also add to the overall cost but provide competitive advantages in markets where green credentials are highly valued.

Demand-supply dynamics also influence the pricing of sorbitan monostearate. Growing demand from burgeoning industries such as plant-based food products, clean-label cosmetics, and biodegradable packaging has put upward pressure on prices. However, overcapacity in certain regions or surplus production due to subdued demand during economic slowdowns can lead to price reductions. Balancing production levels with market demand remains a critical challenge for manufacturers aiming to maintain stable pricing.

The competitive landscape of the sorbitan monostearate market further contributes to its pricing dynamics. Established players with vertically integrated operations enjoy cost advantages, enabling them to offer competitive prices. In contrast, smaller or regional players may face higher production costs due to their reliance on external suppliers for raw materials. Market consolidation and strategic partnerships are becoming common strategies to enhance production efficiency and achieve cost competitiveness.

Looking ahead, the sorbitan monostearate market is expected to witness continued growth, driven by its diverse applications and the global shift towards sustainable products. However, price volatility will likely persist due to factors such as raw material fluctuations, regulatory changes, and evolving consumer preferences. Manufacturers will need to adopt innovative production methods, optimize supply chains, and stay abreast of market trends to maintain competitive pricing while meeting the growing demand. For stakeholders across industries, monitoring these market dynamics will be crucial to navigating the complex pricing landscape of sorbitan monostearate effectively.

Get Real time Prices for Sorbitan Monostearate: https://www.chemanalyst.com/Pricing-data/sorbitan-monostearate-1538

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Sorbitan Monostearate#Sorbitan Monostearate Prices#Sorbitan Monostearate News#Sorbitan Monostearate Pricing#Sorbitan Monostearate Demand#usa#united states#germany#india

1 note

·

View note

Text

Metalworking Fluids Industry Overview, Competitive Landscape and Forecasts 2030

The global metalworking fluids market size was valued at USD 12.17 billion in 2023 and is projected to expand at a compound annual growth rate (CAGR) of 4.9% from 2024 to 2030. This growth is primarily driven by the rising demand for automotive and heavy machinery across various industries, including machinery manufacturing, metal fabrication, and transportation equipment. These sectors rely on metalworking fluids for their ability to improve the machining and manufacturing process. The primary raw material used in producing MWFs is crude oil, which undergoes refining, treatment, and blending to produce key MWF types such as neat cutting oils, soluble oils, and corrosion-preventive oils. Base oil derived from crude oil represents around 40% of the overall MWF production cost and is essential for the manufacture of motor oils, lubricants, and MWFs.

The growth in the automotive industry is a significant factor boosting MWF demand, as these fluids help reduce friction between the tool and the workpiece, prevent metal chips, ensure high-quality surface finishes, and extend the lifespan of tools. These benefits contribute to more efficient machining processes, enhancing production rates. Consequently, the need for metalworking fluids is expected to remain stable, particularly in automotive applications, over the forecast period.

The manufacturing industry is a key economic sector in North America and Europe. Technological advancements in manufacturing processes for sophisticated products, alongside increased exports of construction machinery, power equipment, agricultural machinery, and automotive equipment, have contributed to the growth of the MWF market in these regions. Additionally, Asia Pacific’s demand for advanced machinery in agriculture, automotive, and construction industries supports MWF market expansion in both North America and Europe, as manufacturers in these regions continue to supply global demand.

Gather more insights about the market drivers, restrains and growth of the Metalworking Fluids Market

Application Segmentation Insights:

The neat-cutting oil segment led the MWF market, accounting for over 42% of the global revenue in 2023. Neat-cutting oils are widely used in machining processes across industries, including automotive, aerospace, marine, and construction, due to their effectiveness in cutting operations and high-volume manufacturing. Emerging economies in the Asia Pacific, where high-volume manufacturing is prevalent, have increased demand for neat-cutting oils, which offer a cost-effective solution in machining operations. The demand for neat-cutting oils is further supported by the use of high-alloy steels in heavy equipment manufacturing, which requires robust cutting fluids to optimize machining operations.

The water-cutting oil segment held the second-largest market share in 2023, driven by the increased consumption of these fluids in complex machining operations that require effective heat dissipation. Water-based cutting oils are diluted with water and applied in various procedures, such as drilling, milling, and grinding, to manage the high temperatures generated during machining. The ability of water-cutting oils to control the temperature during these processes makes them ideal for heavy equipment manufacturing.

The semi-synthetic cutting oil segment, a subset of water-cutting oils, is anticipated to grow at a significant CAGR from 2022 to 2030. Semi-synthetic oils are widely used in machining cast iron, aluminum components, and other operations like sawing, drilling, turning, and milling. The expanding applications for these oils are expected to propel the segment’s growth over the forecast period.

Corrosion-preventive fluids are another critical segment expected to grow steadily over the forecast period. These fluids are essential in machining processes where there is a risk of damaging the tools, as they help extend the lifespan of the sump, reducing overhead costs for manufacturers. Small-scale enterprises, which typically operate with lower production volumes and cost structures, increasingly rely on corrosion-preventive oils to maintain operational efficiency and protect their tools, further driving demand in this segment.

In summary, the MWF market is expected to see steady growth, fueled by the expansion of end-use industries and the increasing need for high-performance fluids that enhance machining efficiency, control temperature, and extend tool life. As manufacturing industries in North America, Europe, and Asia Pacific continue to grow, the demand for various MWF types, from neat-cutting oils to corrosion-preventive fluids, will likely rise, positioning MWFs as a key component in the global manufacturing and automotive industries.

Order a free sample PDF of the Metalworking Fluids Market Intelligence Study, published by Grand View Research.

0 notes

Text

Metalworking Fluids Market Dynamics, Growth Prospect and Consumption Analysis till 2030

The global metalworking fluids (MWFs) market, valued at USD 12.17 billion in 2023, is projected to grow at a compound annual growth rate (CAGR) of 4.9% from 2024 to 2030. This growth is expected to be fueled by rising demand for automotive and heavy industry machinery, as well as significant activity in sectors like machinery, metal fabrication, and transportation equipment. These industries are primary drivers of MWF demand, as they rely on these fluids for effective machining and metalworking processes. The production of MWFs involves crude oil as a fundamental raw material. Refined, processed, and blended from crude oil, the base oils in MWFs make up approximately 40% of the total cost of these fluids. Key products like neat cutting oils, soluble oils, and corrosion-preventive oils are developed from this crude oil refining and heating process, which is essential for producing motor oils, lubricants, and MWFs.

The MWF market benefits substantially from the growth of the automotive industry, where MWFs play a critical role in reducing friction between work pieces and tools, removing metal chips, ensuring high surface quality, and extending tool life. This ultimately increases the efficiency and productivity of machining processes, meeting high production demands. Consequently, the demand for MWFs is expected to remain steady as these industries expand.

In North America and Europe, manufacturing is a key sector, driving MWF demand due to advancements in manufacturing techniques for complex products and the high export rate of equipment for construction, power, agriculture, and automotive applications. The strong growth of end-use industries in Asia Pacific also contributes to MWF demand in North America and Europe, as more consumers in Asia Pacific increasingly opt for advanced machinery across sectors like automotive, agriculture, and construction.

Gather more insights about the market drivers, restrains and growth of the Metalworking Fluids Market

The global market is highly competitive, with the big international brands focusing on developing long-term relationships with end-users. With a rise in the manufacturing, automotive, and transportation sectors, the competition is also anticipated to increase in the coming years. Companies such as Houghton International Inc., BP plc, Exxon Mobil Corporation, and Total SA have a high degree of integration across the value chain as they are also engaged in producing various MWFs. These companies have established themselves as key manufacturers and focus on R&D for novel product uses.

The metalworking fluid market trend is being driven by increased demand for automotive and heavy industry, as well as the growing preference for lightweight components in high performance applications such as heavy machinery, transportation equipment, automotive and construction.

Product Segmentation Insights:

The mineral-based MWFs segment accounted for the largest market share in 2023, representing over 48.06% of total market revenue. Mineral oils are widely used due to their cost-effectiveness, making them popular among small- and medium-sized manufacturers who prioritize affordability. This trend is expected to support stable growth in mineral oil-based MWFs over the forecast period. Mineral oils find applications in various machining processes, including turning, grinding, broaching, drilling, and milling, due to their basic yet reliable performance characteristics.

On the other hand, synthetic MWFs are expected to experience the highest CAGR during the forecast period. These synthetic fluids offer several advantages, such as extending tool life, improving surface finishes, and minimizing friction, making them highly suitable for precision applications. Synthetic oils also provide benefits like reducing waste and extending sump life, which is critical in large-scale manufacturing. As a result, synthetic MWFs have seen a steady increase in adoption, particularly among large-scale manufacturers, and this growth is projected to continue as demand rises for higher-performance fluids.

In recent years, semi-synthetic MWFs have gained traction in many countries, contributing to the overall penetration of synthetic MWFs. Additionally, the growing concerns over environmental impacts associated with petroleum-based products have led to stringent environmental regulations and government initiatives promoting sustainable alternatives. Consequently, the production of bio-based MWFs has surged, offering a more environmentally friendly option that meets regulatory requirements and aligns with the industry's push toward sustainability.

Order a free sample PDF of the Metalworking Fluids Market Intelligence Study, published by Grand View Research.

#Metalworking Fluids Market Share#Metalworking Fluids Market Trends#Metalworking Fluids Market Growth#Metalworking Fluids Industry

0 notes

Text

Metalworking Fluids Market Analysis by Key Players, Sales Forecast and Supply Demand to 2030

The global metalworking fluids (MWFs) market, valued at USD 12.17 billion in 2023, is projected to grow at a compound annual growth rate (CAGR) of 4.9% from 2024 to 2030. This growth is expected to be fueled by rising demand for automotive and heavy industry machinery, as well as significant activity in sectors like machinery, metal fabrication, and transportation equipment. These industries are primary drivers of MWF demand, as they rely on these fluids for effective machining and metalworking processes. The production of MWFs involves crude oil as a fundamental raw material. Refined, processed, and blended from crude oil, the base oils in MWFs make up approximately 40% of the total cost of these fluids. Key products like neat cutting oils, soluble oils, and corrosion-preventive oils are developed from this crude oil refining and heating process, which is essential for producing motor oils, lubricants, and MWFs.

The MWF market benefits substantially from the growth of the automotive industry, where MWFs play a critical role in reducing friction between work pieces and tools, removing metal chips, ensuring high surface quality, and extending tool life. This ultimately increases the efficiency and productivity of machining processes, meeting high production demands. Consequently, the demand for MWFs is expected to remain steady as these industries expand.

In North America and Europe, manufacturing is a key sector, driving MWF demand due to advancements in manufacturing techniques for complex products and the high export rate of equipment for construction, power, agriculture, and automotive applications. The strong growth of end-use industries in Asia Pacific also contributes to MWF demand in North America and Europe, as more consumers in Asia Pacific increasingly opt for advanced machinery across sectors like automotive, agriculture, and construction.

Gather more insights about the market drivers, restrains and growth of the Metalworking Fluids Market

The global market is highly competitive, with the big international brands focusing on developing long-term relationships with end-users. With a rise in the manufacturing, automotive, and transportation sectors, the competition is also anticipated to increase in the coming years. Companies such as Houghton International Inc., BP plc, Exxon Mobil Corporation, and Total SA have a high degree of integration across the value chain as they are also engaged in producing various MWFs. These companies have established themselves as key manufacturers and focus on R&D for novel product uses.

The metalworking fluid market trend is being driven by increased demand for automotive and heavy industry, as well as the growing preference for lightweight components in high performance applications such as heavy machinery, transportation equipment, automotive and construction.

Product Segmentation Insights:

The mineral-based MWFs segment accounted for the largest market share in 2023, representing over 48.06% of total market revenue. Mineral oils are widely used due to their cost-effectiveness, making them popular among small- and medium-sized manufacturers who prioritize affordability. This trend is expected to support stable growth in mineral oil-based MWFs over the forecast period. Mineral oils find applications in various machining processes, including turning, grinding, broaching, drilling, and milling, due to their basic yet reliable performance characteristics.

On the other hand, synthetic MWFs are expected to experience the highest CAGR during the forecast period. These synthetic fluids offer several advantages, such as extending tool life, improving surface finishes, and minimizing friction, making them highly suitable for precision applications. Synthetic oils also provide benefits like reducing waste and extending sump life, which is critical in large-scale manufacturing. As a result, synthetic MWFs have seen a steady increase in adoption, particularly among large-scale manufacturers, and this growth is projected to continue as demand rises for higher-performance fluids.

In recent years, semi-synthetic MWFs have gained traction in many countries, contributing to the overall penetration of synthetic MWFs. Additionally, the growing concerns over environmental impacts associated with petroleum-based products have led to stringent environmental regulations and government initiatives promoting sustainable alternatives. Consequently, the production of bio-based MWFs has surged, offering a more environmentally friendly option that meets regulatory requirements and aligns with the industry's push toward sustainability.

Order a free sample PDF of the Metalworking Fluids Market Intelligence Study, published by Grand View Research.

#Metalworking Fluids Market Share#Metalworking Fluids Market Trends#Metalworking Fluids Market Growth#Metalworking Fluids Industry

0 notes

Text

The Pelargonic Acid Market is projected to grow from USD 217.2 million in 2024 to an estimated USD 370.4 million by 2032, with a compound annual growth rate (CAGR) of 6.9% from 2024 to 2032.Pelargonic acid, also known as nonanoic acid, is a naturally occurring fatty acid with the chemical formula C9H18O2. It is a saturated fatty acid found in many plants and animal oils. As a bio-based, biodegradable, and environmentally friendly chemical, pelargonic acid has gained significant attention in recent years due to its versatile applications across various industries such as agriculture, cosmetics, pharmaceuticals, and industrial cleaning.

Browse the full report https://www.credenceresearch.com/report/pelargonic-acid-market

Market Growth Drivers

1. Agricultural Applications

One of the primary growth drivers for the pelargonic acid market is its use in agriculture as a bioherbicide and plant growth regulator. Pelargonic acid’s ability to inhibit weed growth without affecting soil quality has made it an attractive alternative to synthetic herbicides. With increasing awareness about the harmful effects of chemical herbicides on the environment, many countries have started adopting bio-based herbicides like pelargonic acid, boosting demand for the product in agriculture.

As the global demand for organic and sustainable farming practices continues to rise, the agricultural segment remains a crucial contributor to the pelargonic acid market. Organic farming and the reduced use of synthetic chemicals are gaining popularity, particularly in Europe and North America, further driving the demand for bio-based inputs like pelargonic acid.

2. Cosmetics and Personal Care Industry

The cosmetics and personal care industry is another significant growth area for the pelargonic acid market. Its use as an emollient, cleansing agent, and pH adjuster in skincare, haircare, and other cosmetic formulations has become widespread. Pelargonic acid’s ability to act as a mild surfactant makes it a preferred ingredient in natural and organic cosmetic products, which have seen an upswing in demand.

Consumers today are increasingly seeking products with natural ingredients, and companies are reformulating their offerings to cater to this trend. As the "clean beauty" movement continues to gain momentum, pelargonic acid is poised to play a larger role in the formulation of eco-friendly personal care products.

3. Industrial Applications

Pelargonic acid is used in a variety of industrial applications, including lubricants, coatings, and solvents. Its biodegradability and low toxicity make it an ideal ingredient for industries that require environmentally safe solutions. The demand for green chemicals is rising across various sectors as companies seek to reduce their environmental footprint and comply with stricter regulations on chemical use and emissions.

Additionally, pelargonic acid is utilized in the manufacturing of corrosion inhibitors, metalworking fluids, and plasticizers. Its growing use in these industrial applications is contributing to the expansion of the global market.

Challenges in the Pelargonic Acid Market

Despite the promising growth prospects, the pelargonic acid market faces several challenges. One of the primary obstacles is the relatively high production cost of bio-based pelargonic acid compared to its synthetic counterparts. This can limit its competitiveness in certain price-sensitive markets.

Moreover, the availability of raw materials for pelargonic acid production is another constraint. The acid is primarily derived from renewable sources like castor oil and sunflower oil, which are subject to fluctuations in supply and pricing due to weather conditions, geopolitical factors, and agricultural yield variability.

Another challenge is the limited consumer awareness of pelargonic acid and its benefits, particularly in regions where bio-based products are still gaining market penetration. Increasing consumer education and marketing efforts will be essential for broader adoption of pelargonic acid-based products.

Regional Outlook

The pelargonic acid market is geographically diverse, with North America and Europe being the largest regions in terms of demand. These regions have stringent environmental regulations and a strong emphasis on sustainability, driving the adoption of bio-based chemicals like pelargonic acid. Asia-Pacific is also emerging as a significant market, driven by the growth of the agriculture and personal care industries in countries like China and India.

Future Prospects

The future of the pelargonic acid market looks promising, with several trends likely to shape its growth trajectory. Increased research and development efforts to reduce production costs and enhance the performance of pelargonic acid-based products are expected to create new opportunities. Additionally, as governments worldwide continue to promote sustainable agriculture and greener industrial practices, the demand for pelargonic acid will likely rise.

The growing focus on circular economy models and bio-based chemicals will further propel the market, making pelargonic acid an integral part of the sustainable chemical industry. Companies that invest in innovation and sustainability will be well-positioned to capitalize on the market’s growth potential.

Key Player Analysis:

Central Drug House

Croda International Plc

Emery Oleochemical

Glentham Life Sciences Limited

Haihang Industry

Kunshan Odowell Co., Ltd

Matrica S.p.A

OQ Chemicals GmbH

Tokyo Chemical Industry Co., Ltd.

Zhengzhou Yibang Industry & Commerce Co., Ltd

Segmentation:

By Type

PA 90 Content

PA 95 Content

PA Blends

By Grade

Natural

Synthetic

By Application

Herbicides and Pesticides

Food Additives

Pharmaceuticals

Cosmetics

Industrial Cleaning

Others (Fragrances, Plasticizers)

By Region

North America

US

Canada

Mexico

Europe

Germany

France

UK

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Browse the full report https://www.credenceresearch.com/report/pelargonic-acid-market

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

Ethoxylates Market Size, Trends, and Business Outlook 2024 - 2030

The global ethoxylates market size was valued at USD 12.1 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 2.9% from 2024 to 2030.

The factors driving the ethoxylates market are increasing applications across diverse industries, ranging from paints and coatings and textile processing to personal care, agriculture, and pulp and paper. There is also increasing demand for low-rinse detergents, surging demand for ethoxylates in the healthcare industry, and increasing demand for eco-friendly products such as alcohol ethoxylates in cosmetics.

Ethoxylates are chemicals made by combining epoxides or ethylene oxide (EO) with substances such as alcohols, acids, amines, and vegetable oils at the preferred molar ratio. Their hydrophobic and hydrophilic characteristics allow them to dissolve in oil or water, depending on the specific ethoxylate utilized. Due to this, they reduce the surface tension between liquids of different types or between liquids and gases. In addition, they provide other characteristics, including being easily dissolved in water, effective formulation, ability to wet surfaces, and minimal harm to aquatic life.

Gather more insights about the market drivers, restrains and growth of the Ethoxylates Market

Ethoxylates Market Report Highlights

• In terms of revenue, Asia Pacific is expected to emerge as the fastest growing regional market over the forecast period

• The alcohol product segment held the largest revenue share of 48.4% in 2019

• Asian countries, particularly India and China, are likely to witness remarkable growth in next few years

• The industry is fragmented and competitive with the presence of major global players, such as BASF SE, DuPont, Croda International Plc., Dow, and Huntsman Corporation LLC

• Growing demand for industrial and institutional cleaners is expected to drive the product consumption over the forecast period.

Browse through Grand View Research's Organic Chemicals Industry Research Reports.

• The global acrylic acid market size was valued at USD13.66 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 4.1% from 2024 to 2030.

• The global surfactants market size was valued at USD 43.2 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 5.3% from 2024 to 2030.

Ethoxylates Market Segmentation

Grand View Research has segmented the global ethoxylates market report based on product, application, end use, and region.

Product Outlook (Revenue, USD Million, 2018 - 2030)

• Alcohols

• Fatty Amines

• Fatty Acids

• Ethyl Esters

• Glycerides

• Others

Application Outlook (Revenue, USD Million, 2018 - 2030)

• Household & Personal Care

• I&I Cleaning

• Pharmaceutical

• Agrochemicals

• Oilfield Chemicals

• Others

End Use Outlook (Revenue, USD Million, 2018 - 2030)

• Detergents

• Personal Care

• Ointments & Emulsions

• Herbicides

• Insecticides

• Foam Control & Wetting Agents

• Lubricants & Emulsions

• Others

Regional Outlook (Revenue, USD Million, 2018 - 2030)

• North America

o U.S.

o Canada

o Mexico

• Europe

o Germany

o UK

o France

o Italy

o Spain

• Asia Pacific

o China

o Japan

o India

o South Korea

• Latin America

o Brazil

o Argentina

o Colombia

• Middle East and Africa (MEA)

o Saudi Arabia

o UAE

o South Africa

Order a free sample PDF of the Ethoxylates Market Intelligence Study, published by Grand View Research.

#Ethoxylates Market#Ethoxylates Market size#Ethoxylates Market share#Ethoxylates Market analysis#Ethoxylates Industry

0 notes

Text

Global Grease Nipple Market Outlook and Future Strategy Analysis 2024 - 2031

The global grease nipple market is a crucial segment within the lubrication systems industry, playing a vital role in maintaining machinery and equipment across various sectors. As industries continue to evolve and machinery becomes more sophisticated, the demand for effective lubrication solutions like grease nipples is expected to grow. This article provides a comprehensive analysis of the grease nipple market, including key drivers, challenges, regional insights, and future trends.

Overview of the Grease Nipple Market

Grease nipples, also known as grease fittings or zerk fittings, are small devices used to inject lubricant into machinery components. They are integral to the maintenance of moving parts in various applications, ensuring smooth operation and extending the lifespan of equipment. Grease nipples are widely used in automotive, industrial, agricultural, and construction applications.

The global grease nipple market is poised for growth, driven by increasing industrialization, demand for maintenance solutions, and technological advancements in lubrication systems. While challenges such as competition from alternative lubrication methods

Market Definition and Segmentation

The grease nipple market can be segmented based on:

Type: Standard grease nipples, angled grease nipples, mini grease nipples, and others.

Material: Steel, stainless steel, plastic, and others.

Application: Automotive, industrial machinery, agriculture, construction, and others.

Region: North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa.

Key Market Drivers

1. Growing Industrialization

The rapid industrialization in emerging economies is a significant driver for the grease nipple market. As manufacturing processes become more advanced, the demand for efficient lubrication solutions to maintain machinery increases.

2. Increasing Demand for Maintenance and Repair

Regular maintenance of machinery is essential for optimal performance and longevity. The rising awareness of preventive maintenance practices in various sectors, including automotive and industrial, drives the demand for grease nipples.

3. Technological Advancements

Innovations in lubrication technology, including automated lubrication systems that utilize grease nipples, are enhancing the efficiency of lubrication processes. These advancements attract more users to adopt grease nipples in their maintenance routines.

Challenges Facing the Market

1. Competition from Alternative Lubrication Systems

The grease nipple market faces competition from alternative lubrication systems, such as automatic lubricators and centralized lubrication systems. These alternatives may offer enhanced convenience and efficiency, impacting the demand for traditional grease nipples.

2. Regulatory Compliance

Manufacturers must adhere to strict regulations regarding the materials used in grease nipples and the lubrication process. Compliance with these regulations can increase operational costs and impact market growth.

3. Fluctuating Raw Material Prices

The prices of raw materials, particularly metals like steel, can fluctuate significantly, affecting the production costs of grease nipples. These fluctuations can lead to pricing challenges and impact profit margins for manufacturers.

Regional Analysis

North America

North America is a leading market for grease nipples, driven by a well-established automotive and industrial sector. The demand for maintenance and repair in these industries fuels the market for lubrication solutions, including grease nipples.

Europe

In Europe, the grease nipple market is growing, supported by stringent regulations regarding machinery maintenance and safety. Countries like Germany, France, and the UK are significant contributors to this market, driven by advanced manufacturing practices.

Asia-Pacific

The Asia-Pacific region is witnessing rapid growth in the grease nipple market, fueled by increasing industrial activities and infrastructure development. Countries such as China and India are at the forefront of this growth, with rising demand for efficient lubrication solutions.

Future Outlook

The global grease nipple market is expected to experience steady growth in the coming years. Key trends influencing the market include:

Integration with Smart Technologies: The incorporation of smart technology in lubrication systems may lead to the development of intelligent grease nipples that can monitor lubrication levels and provide real-time feedback.

Focus on Sustainable Practices: As industries strive to reduce their environmental impact, the demand for eco-friendly materials and lubricants may increase, influencing the design and production of grease nipples.

Rising Demand from Emerging Markets: The growth of industrialization in emerging markets presents significant opportunities for grease nipple manufacturers, as the need for maintenance and efficient lubrication solutions continues to rise.

Conclusion

The global grease nipple market is poised for growth, driven by increasing industrialization, demand for maintenance solutions, and technological advancements in lubrication systems. While challenges such as competition from alternative lubrication methods and regulatory compliance exist, the future outlook remains positive. As industries evolve and embrace new technologies, grease nipples will continue to play a crucial role in ensuring the efficient operation and longevity of machinery across various sectors.

#Global Grease Nipple Market Size#Global Grease Nipple Market Trend#Global Grease Nipple Market Growth

0 notes

Text

South Africa Specialty Chemicals Market Trends, Report 2023-2030

BlueWeave Consulting, a leading strategic consulting and market research firm, in its recent study, estimated South Africa Specialty Chemicals Market size at USD 8.7 million in 2023. During the forecast period between 2024 and 2030, BlueWeave expects South Africa Specialty Chemicals Market size to expand at a CAGR of 4.50% reaching a value of USD 11.1 million by 2030. By volume, BlueWeave estimated South Africa Specialty Chemicals Market size at 13.1 million tons in 2023. During the forecast period between 2024 and 2030, BlueWeave expects South Africa Specialty Chemicals Market size to expand at a CAGR of 4% reaching the volume of 17.2 million tons by 2030.

The expanding usage of specialty chemicals in a range of end-user sectors, such as water treatment, chemicals, oilfields, pharmaceuticals, and others, together with improvements in process technology, are key growth drivers for South Africa specialty chemicals market. The government's financial support and other initiatives to increase domestic manufacturing are also expected to propel South Africa specialty chemicals market over the forecast period.

Sample Request @ https://www.blueweaveconsulting.com/report/south-africa-specialty-chemicals-market/report-sample

Opportunity - Expanding automobile manufacturing operations

The expanding automobile production is emerging as one of the major driving factors for the growth of South Africa Specialty Chemicals Market. South Africa ranks 22 in global vehicle production and has been attracting significant foreign direct investment and adopting various growth strategies to boost the automotive industry. Specialty chemicals are widely used in the production of high-performance lubricants and additives. These are essential to reduce wear and friction in engines and engines, improving automobiles' general efficiency and dependability.

Agrochemicals Product Type to Grow at Fastest CAGR

South Africa Specialty Chemicals Market, on the basis of product type, is comprised of agrochemicals, rubber processing chemicals, construction chemicals, food & feed additives, cosmetic chemicals, oilfield chemicals, specialty pulp & paper chemicals, specialty textile chemicals, water treatment chemicals, pharmaceutical & nutraceutical additives, CASE (coatings, adhesives, sealants & elastomers), and other (institutional & industrial cleaners, electronic chemicals, and mining chemicals) segments. Among these product types, the agrochemicals segment is anticipated to register fastest growth rate during the period in analysis. The expanding agriculture sector and rising food demand are expected to fuel the demand for agrochemicals in the South African Specialty Chemicals Market.

Competitive Landscape

South Africa Specialty Chemicals Market is intensely competitive, as a number of companies are competing to gain a significant market share. Key players in the market include Durban Speciality Chemicals, AECI Specialty Chemicals, SUN ACE South Africa, Safic Alcan Southern Africa (Pty) Ltd, IMCD South Africa, Protea Chemicals, Reba Chemicals (Pty) Ltd, BASF, Gold Reef Speciality Chemicals (Pty) Ltd, and Southern Chemicals (Pty) Ltd.

To further enhance their market share, these companies employ various strategies, including mergers and acquisitions, partnerships, joint ventures, license agreements, and new product launches.

Contact Us:

BlueWeave Consulting & Research Pvt. Ltd

+1 866 658 6826 | +1 425 320 4776 | +44 1865 60 0662

0 notes

Text

Biomass Pellets Market – Exclusive Report Study on the Current Trends And Forecast 2024-2033 | Global Insight Services

Biomass pellets are a type of renewable energy source that is derived from organic matter, such as wood chips, sawdust, and agricultural waste. These pellets are typically used in pellet stoves or boilers to generate heat, but can also be used in power plants to create electricity. Biomass pellets are a sustainable and eco-friendly alternative to traditional fossil fuels, and can help to reduce greenhouse gas emissions.

Key Trends

The key trends in biomass pellets technology are the development of more efficient pellet mills and the production of pellets from a wider range of feedstocks.

Pellet mills are becoming more efficient as manufacturers look for ways to reduce energy consumption and increase production capacity. The latest generation of pellet mills are equipped with features such as variable speed drives, automatic lubrication systems, and automatic pellet size adjustment.

Pellets are being made from a wider range of feedstocks as manufacturers look for ways to reduce costs and increase production flexibility. A variety of agricultural residues, wood wastes, and industrial wastes can be used to make pellets. This allows manufacturers to source pellets from a variety of locations, which can reduce transportation costs.

Key Drivers

The key drivers of biomass pellets market are as follows:

1) Increasing awareness about the environment and the need to reduce greenhouse gas emissions: Biomass pellets are a renewable and carbon-neutral energy source that can help to reduce greenhouse gas emissions.

2) Government policies and incentives: Several governments around the world are promoting the use of biomass pellets through policies and incentives, which is driving the growth of the market.

3) Technological advancement: The continuous improvement in technology has led to the development of efficient and cost-effective pellet production technologies, which is further driving the market growth.

4) Growing demand from the power sector: Biomass pellets are increasingly being used in power generation as they offer a cleaner and more efficient alternative to fossil fuels.

Unlock Growth Potential in Your Industry – Get Your Sample Report Now@https://www.globalinsightservices.com/request-sample/GIS22503

Research Objectives

Estimates and forecast the overall market size for the total market, across product, service type, type, end-user, and region

Detailed information and key takeaways on qualitative and quantitative trends, dynamics, business framework, competitive landscape, and company profiling

Identify factors influencing market growth and challenges, opportunities, drivers and restraints

Identify factors that could limit company participation in identified international markets to help properly calibrate market share expectations and growth rates

Trace and evaluate key development strategies like acquisitions, product launches, mergers, collaborations, business expansions, agreements, partnerships, and R&D activities

Thoroughly analyze smaller market segments strategically, focusing on their potential, individual patterns of growth, and impact on the overall market

To thoroughly outline the competitive landscape within the market, including an assessment of business and corporate strategies, aimed at monitoring and dissecting competitive advancements.

Identify the primary market participants, based on their business objectives, regional footprint, product offerings, and strategic initiatives

Request Customization@ https://www.globalinsightservices.com/request-customization/GIS22503

Market Segmentation

The Biomass Pellets Market is segmented by source, end-use and region. By source, the market is classified into agriculture residue, wood sawdust, and others. By end-use, the market is bifurcated into power generation, industrial heating, commercial and domestic heating, and others. By region, the market is classified into North America, Europe, Asia-Pacific and rest of the world.

Key Players

The key players in the Biomass Pellets Market are New England Wood Pellet, Drax Group plc, Forest Energy Corporation, Energex Corporation, International WoodFuels LLC, Buhler AG, Enviva, Abellon CleanEnergy Limited, Anvietphat and Sumitomo Corporation.

Drive Your Growth Strategy: Purchase the Report for Key Insights@ https://www.globalinsightservices.com/checkout/single_user/GIS22503

Research Scope

Scope – Highlights, Trends, Insights. Attractiveness, Forecast

Market Sizing – Product Type, End User, Offering Type, Technology, Region, Country, Others

Market Dynamics – Market Segmentation, Demand and Supply, Bargaining Power of Buyers and Sellers, Drivers, Restraints, Opportunities, Threat Analysis, Impact Analysis, Porters 5 Forces, Ansoff Analysis, Supply Chain

Business Framework – Case Studies, Regulatory Landscape, Pricing, Policies and Regulations, New Product Launches. M&As, Recent Developments

Competitive Landscape – Market Share Analysis, Market Leaders, Emerging Players, Vendor Benchmarking, Developmental Strategy Benchmarking, PESTLE Analysis, Value Chain Analysis

Company Profiles – Overview, Business Segments, Business Performance, Product Offering, Key Developmental Strategies, SWOT Analysis.

With Global Insight Services, you receive:

10-year forecast to help you make strategic decisions

In-depth segmentation which can be customized as per your requirements

Free consultation with lead analyst of the report

Infographic excel data pack, easy to analyze big data

Robust and transparent research methodology

Unmatched data quality and after sales service

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1-833-761-1700 Website: https://www.globalinsightservices.com/

About Global Insight Services:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

0 notes

Text

Magnesium Stearate Prices Trend | Pricing | News | Database | Chart

Magnesium Stearate a widely used excipient and lubricant in pharmaceutical, food, and cosmetic industries, plays a crucial role in ensuring product quality and consistency. The pricing dynamics of magnesium stearate are influenced by various factors, including raw material costs, production processes, regulatory requirements, and global market demand. As a compound derived from stearic acid and magnesium salts, its availability and price are closely tied to the supply chain of these primary inputs. Stearic acid, which is sourced from animal fats or vegetable oils, experiences fluctuations in price due to changes in agricultural yields, feedstock availability, and geopolitical factors affecting trade. Consequently, any disruption or cost increase in stearic acid directly impacts the pricing structure of magnesium stearate.

The pharmaceutical sector accounts for a significant portion of magnesium stearate consumption, as it is essential for tablet formulation, ensuring smooth production processes and enhancing the physical characteristics of tablets. Regulatory compliance and quality standards in this sector impose additional costs on manufacturers, further shaping the market price. Rising demand for generic medications and nutraceutical products has intensified the need for magnesium stearate, creating upward pressure on prices. Similarly, the food industry’s growing reliance on this compound as an anti-caking agent and emulsifier adds another layer of demand, amplifying market competition.

Get Real time Prices for Magnesium Stearate: https://www.chemanalyst.com/Pricing-data/magnesium-stearate-1407

The cosmetic industry also significantly contributes to the demand for magnesium stearate. Its use as a texture enhancer and stabilizer in makeup products such as powders and foundations ensures its consistent demand. However, the industry’s shift towards sustainable and plant-based ingredients has prompted some manufacturers to explore alternatives, which may influence the long-term pricing trends of magnesium stearate. Furthermore, environmental considerations and the push for biodegradable ingredients are prompting changes in production methodologies, potentially leading to increased costs and, subsequently, higher market prices.

Geographical variations in magnesium stearate prices stem from differences in production capacities, labor costs, and access to raw materials. Regions with established chemical manufacturing hubs, such as Asia-Pacific, often benefit from lower production costs due to economies of scale and proximity to raw material sources. China and India, for instance, are prominent suppliers of magnesium stearate, offering competitive pricing in the global market. However, trade policies, import-export tariffs, and regional regulatory requirements can cause significant price disparities across markets.

The ongoing focus on sustainable practices and green chemistry has led to the adoption of bio-based stearic acid in magnesium stearate production. While this shift aligns with global environmental goals, it has introduced cost pressures due to the relatively higher prices of bio-based raw materials. These cost implications are likely to be passed on to end-users, impacting the pricing strategies of magnesium stearate manufacturers. Additionally, technological advancements in production processes, such as continuous manufacturing techniques, are being explored to enhance efficiency and reduce costs. However, the initial investment in such technologies might lead to temporary price increases before realizing long-term cost benefits.

Market trends indicate that the demand for magnesium stearate will continue to grow, driven by expanding applications in emerging industries and regions. For instance, the rising popularity of plant-based and vegan products has spurred the development of magnesium stearate derived from non-animal sources, broadening its appeal to a wider consumer base. This diversification of supply chains and product offerings may stabilize prices over time, despite temporary fluctuations due to market adjustments.

The impact of global economic conditions on magnesium stearate prices cannot be overlooked. Inflationary pressures, currency exchange rates, and energy costs are critical factors that influence production expenses. The energy-intensive nature of chemical manufacturing makes magnesium stearate prices sensitive to fluctuations in oil and gas markets. Additionally, transportation and logistics costs, which have seen significant increases in recent years, contribute to the overall pricing dynamics. These challenges emphasize the importance of strategic sourcing and supply chain optimization for manufacturers to maintain competitive pricing.

Consumer preferences and regulatory trends are shaping the future of the magnesium stearate market. Increased scrutiny on product safety and the traceability of raw materials has led to stricter compliance requirements, adding to production costs. At the same time, consumer demand for transparency and clean-label products is encouraging manufacturers to adopt innovative approaches, such as using certified sustainable ingredients and improving production efficiency. These factors are expected to play a pivotal role in determining the long-term price trajectory of magnesium stearate.

In conclusion, the pricing of magnesium stearate is influenced by a complex interplay of raw material availability, production costs, regulatory frameworks, and market demand. As industries continue to innovate and adapt to evolving consumer and environmental expectations, the market for magnesium stearate is poised for growth. However, stakeholders must navigate challenges such as supply chain disruptions, cost pressures, and sustainability goals to ensure stable and competitive pricing in the years to come.

Get Real time Prices for Magnesium Stearate: https://www.chemanalyst.com/Pricing-data/magnesium-stearate-1407

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Magnesium Stearate#Magnesium Stearate Price#Magnesium Stearate Prices#Magnesium Stearate Pricing#Magnesium Stearate News#Magnesium Stearate Price Monitor

0 notes

Text

"Oleochemicals: Genuine Market Growth or Just a Greenwashing Trend?"

Introduction

The oleochemicals market, encompassing chemicals derived from natural fats and oils, plays a crucial role in various industries, including personal care, automotive, pharmaceuticals, and food processing. Oleochemicals, which include fatty acids, glycerol, and surfactants, are prized for their renewable nature and versatile applications. As industries increasingly seek sustainable and environmentally friendly alternatives to petrochemical-based products, oleochemicals are gaining prominence. This market is driven by technological advancements, growing consumer awareness of sustainability, and expanding industrial applications, making it a dynamic sector with substantial growth potential.

Market Dynamics

Drivers:

Rising Demand for Sustainable Products: The shift towards sustainability and green chemistry is driving demand for oleochemicals as they are derived from renewable resources and offer a more eco-friendly alternative to petrochemicals. This trend is particularly strong in the personal care, automotive, and cleaning products industries.

Technological Advancements: Innovations in oleochemical processing and applications are expanding their use across various industries. Advances in production technologies, such as improved catalysts and efficient extraction methods, enhance the performance and cost-effectiveness of oleochemicals.

Growing Awareness of Environmental Impact: Increasing consumer and regulatory pressure to reduce environmental impact is promoting the adoption of oleochemicals. As companies and consumers become more conscious of their environmental footprint, the demand for biodegradable and non-toxic alternatives to synthetic chemicals is rising.

Challenges:

Volatility in Raw Material Prices: The prices of raw materials, such as vegetable oils and animal fats, are subject to fluctuations due to factors like weather conditions, agricultural policies, and global market trends. These price variations can affect the cost structure and profitability of oleochemical producers.

Competition from Petrochemicals: Despite the advantages of oleochemicals, petrochemicals still dominate many markets due to their lower cost and established infrastructure. Competing with petrochemical products requires ongoing innovation and cost management.

Regulatory Compliance: The oleochemical industry faces regulatory challenges related to product safety, environmental impact, and labeling requirements. Compliance with diverse and evolving regulations across different regions can be complex and costly.

Opportunities:

Expansion in Emerging Markets: Growing industrialization and increasing consumer awareness in emerging markets, particularly in Asia-Pacific and Latin America, offer significant growth opportunities for oleochemicals. These regions are expanding their use of oleochemicals in personal care, agriculture, and other sectors.

Innovation in Product Applications: There is an opportunity to develop new oleochemical applications and formulations that address emerging market needs. Innovations in areas such as bio-based polymers, specialty surfactants, and high-performance lubricants can drive market growth.

Sample Pages of Report: https://www.infiniumglobalresearch.com/reports/sample-request/1026

Regional Analysis

North America: The North American market is characterized by a strong focus on sustainability and innovation. The U.S. and Canada are key markets, driven by advancements in technology and increasing adoption of renewable chemicals in various industries.

Europe: Europe has a well-established market for oleochemicals, with a strong emphasis on environmental regulations and sustainability. The European Union's strict environmental policies and consumer demand for green products drive the growth of the oleochemicals sector.

Asia-Pacific: The Asia-Pacific region is experiencing rapid growth in the oleochemicals market, fueled by industrial expansion, rising disposable incomes, and increasing awareness of sustainable products. Countries like China, India, and Indonesia are major contributors to this growth.

Latin America & Middle East & Africa: These regions are gradually increasing their use of oleochemicals due to growing industrial activities and a rising focus on sustainability. Market development in these areas is driven by expanding manufacturing sectors and changing consumer preferences.

Market Segmentation

By Type: The oleochemicals market is segmented into fatty acids, glycerol, surfactants, and others. Fatty acids and surfactants are major segments due to their widespread use in various applications.

By Application: Key applications include personal care (soaps, shampoos), automotive (lubricants, additives), pharmaceuticals, food processing, and industrial (cleaning agents, coatings). Personal care and automotive applications are prominent due to their high demand for sustainable and performance-enhancing ingredients.

By Source: Oleochemicals are derived from vegetable oils (palm, soybean, coconut) and animal fats. Each source offers different properties and applications, influencing market dynamics and product development.

By Region: Regional segmentation includes North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with each region having distinct growth drivers and market characteristics.

Competitive Landscape

Market Share of Large Players: Major players in the oleochemicals market, such as Cargill, BASF SE, and Wilmar International, hold significant market share due to their extensive production capacities, global reach, and established market presence.

Price Control by Big Players: Large companies often influence market pricing through economies of scale and strategic sourcing. They can set trends and standards for pricing, impacting the competitive landscape and market dynamics.

Challenges from Smaller Companies: Small and mid-sized companies challenge larger players by focusing on niche markets, innovative products, and cost-effective solutions. They often introduce specialized oleochemicals that cater to specific applications or emerging trends.

Key Players:

Cargill, Incorporated

BASF SE

Wilmar International

Kraton Corporation

SABIC

Dow Inc.

Evonik Industries AG

Report Overview: https://www.infiniumglobalresearch.com/reports/global-oleochemicals-market

Future Outlook

New Product Development: Continuous innovation in oleochemical formulations and applications is essential for staying competitive. Developing new products with enhanced performance, sustainability, and functionality helps companies meet evolving market demands and capture new opportunities.

Sustainable Products: The growing emphasis on environmental sustainability is driving demand for eco-friendly oleochemicals. Companies that focus on sustainable sourcing, production processes, and product development will likely appeal to environmentally conscious consumers and strengthen their market position.

Conclusion

The oleochemicals market is poised for growth driven by advancements in technology, increasing demand for sustainable products, and expanding industrial applications. While challenges such as raw material price volatility and regulatory compliance persist, opportunities exist in emerging markets and innovative product development. Companies that embrace sustainability and innovation will be well-positioned to capitalize on the evolving market dynamics and achieve long-term success.

0 notes

Text

Taiwan Testing, Inspection & Certification Market - Forecast(2024 - 2030)

Taiwan Testing, Inspection and Certification Market Overview