#Generative AI in Healthcare Market Size

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr was the first site to host the blog for President Barack Obama in 2011.

Text

Top Players in the Generative AI in Healthcare Market: Size, Share, and Growth Trends

The Generative AI in Healthcare Market Revenue was valued at USD 1.7 billion in 2023 and is anticipated to reach a staggering USD 19.99 billion by 2032, exhibiting an impressive CAGR of 31.5% during the forecast period from 2024 to 2032. The transformative potential of generative AI in reshaping healthcare services, ranging from diagnostics to personalized treatments, is driving the market’s rapid expansion.

Key Growth Factors

Generative AI is revolutionizing the healthcare landscape by enhancing capabilities in areas such as disease modeling, drug discovery, medical imaging, and predictive analytics. Healthcare organizations are increasingly deploying AI-driven tools to streamline workflows, improve diagnostic accuracy, and deliver personalized patient care.

The rise in demand for AI-powered drug development platforms is another significant driver for market growth. Generative AI algorithms can analyze complex datasets to predict potential drug candidates and optimize treatment pathways, drastically reducing development time and costs. Moreover, the growing adoption of virtual assistants and chatbots powered by generative AI is transforming patient engagement and administrative operations in healthcare facilities.

Regional Insights

North America leads the market, attributed to robust investments in AI research, advanced healthcare infrastructure, and favorable government initiatives supporting AI adoption in healthcare. Meanwhile, the Asia-Pacific region is emerging as a high-growth market due to increasing digitization, expanding healthcare budgets, and a growing focus on leveraging AI for medical advancements.

Get Free Sample Report@ https://www.snsinsider.com/sample-request/4480

Future Outlook

Generative AI's potential to deliver cutting-edge solutions in genomics, clinical decision-making, and telemedicine ensures that the market will continue its remarkable growth trajectory. The integration of generative AI with other advanced technologies like blockchain and IoT further enhances its scope in healthcare. As AI continues to evolve, healthcare providers and technology companies are expected to collaborate more extensively, fostering innovation and creating new opportunities for growth.

About Us

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Contact Us

Akash Anand – Head of Business Development & Strategy Email: [email protected] Phone: +1-415-230-0044 (US) | +91-7798602273 (IND)

#Generative AI in Healthcare#Generative AI in Healthcare Market#Generative AI in Healthcare Market Size#Generative AI in Healthcare Market Share#Generative AI in Healthcare Market Growth#Market Research

0 notes

Text

The Future of ERP Software in India: Trends to Watch in 2024

As India continues to solidify its position as a global economic powerhouse, the demand for sophisticated Enterprise Resource Planning (ERP) solutions has never been higher. ERP software companies in India are at the forefront of this transformation, driving innovation and efficiency across various industries. As we look ahead to 2024, several key trends are shaping the future of ERP software in India. This blog delves into these trends, offering insights into how ERP software providers in India are gearing up to meet the evolving needs of businesses.

1. Increased Adoption of Cloud-Based ERP Solutions

One of the most significant trends in the ERP landscape is the shift towards cloud-based solutions. ERP software companies in India are increasingly offering cloud-based ERP systems to meet the growing demand for flexibility, scalability, and cost-efficiency. Cloud ERP solutions eliminate the need for extensive on-premises infrastructure, allowing businesses to reduce capital expenditure and streamline operations.

Cloud-based ERP systems also facilitate real-time data access and collaboration, enabling businesses to make informed decisions quickly. This trend is particularly beneficial for small and medium-sized enterprises (SMEs) that require affordable and scalable ERP solutions to compete effectively in the market.

2. Integration of Artificial Intelligence and Machine Learning

Artificial Intelligence (AI) and Machine Learning (ML) are revolutionizing the ERP landscape. ERP software providers in India are integrating AI and ML technologies to enhance the capabilities of their solutions. These technologies enable predictive analytics, automate routine tasks, and provide intelligent insights, helping businesses to optimize their operations.

For instance, AI-powered ERP systems can forecast demand, manage inventory levels, and predict maintenance needs, significantly improving efficiency and reducing costs. As AI and ML technologies continue to evolve, their integration into ERP systems will become more sophisticated, offering even greater value to businesses.

3. Focus on Industry-Specific ERP Solutions

ERP software companies in India are increasingly developing industry-specific ERP solutions to cater to the unique needs of different sectors. Whether it is manufacturing, retail, healthcare, or finance, each industry has distinct requirements that generic ERP systems might not fully address. Industry-specific ERP solutions offer tailored functionalities and workflows, ensuring better alignment with business processes.

For example, a manufacturing ERP system might include features for production planning, quality control, and supply chain management, while a retail ERP system could focus on inventory management, point of sale (POS) integration, and customer relationship management (CRM). This trend towards specialization ensures that businesses can leverage ERP systems that truly support their operational needs.

4. Enhanced Mobile Accessibility

With the proliferation of smartphones and mobile devices, the need for mobile-friendly ERP solutions is growing. ERP software providers in India are developing mobile applications that allow users to access critical business information on the go. Mobile ERP solutions enable employees to perform tasks such as inventory checks, sales order processing, and expense reporting from their smartphones or tablets.

This trend not only improves accessibility but also enhances productivity by enabling employees to work remotely and make decisions in real-time. As mobile technology continues to advance, the functionality and user experience of mobile ERP applications will improve, making them an indispensable tool for modern businesses.

5. Increased Emphasis on Data Security and Compliance

As businesses become more reliant on digital technologies, data security and compliance have become paramount. ERP software providers in India are prioritizing data protection by incorporating advanced security features into their solutions. This includes encryption, multi-factor authentication, and regular security audits to safeguard sensitive business information.

Moreover, with the implementation of regulations such as the General Data Protection Regulation (GDPR) and India’s Personal Data Protection Bill, compliance is a critical concern for businesses. ERP software providers are ensuring that their systems comply with these regulations, helping businesses avoid legal penalties and build trust with their customers.

6. Rise of Hybrid ERP Solutions

While cloud-based ERP systems offer numerous advantages, some businesses prefer on-premises solutions due to specific regulatory or operational requirements. To cater to these diverse needs, ERP software companies in India are offering hybrid ERP solutions that combine the benefits of both cloud and on-premises systems.

Hybrid ERP solutions provide the flexibility of cloud-based systems while allowing businesses to maintain critical applications on-premises. This approach offers a balanced solution, enabling businesses to optimize their IT infrastructure based on their unique needs and preferences.

7. Adoption of Advanced Analytics and Business Intelligence

Data is the new currency in today’s business environment, and the ability to harness and analyze data is a key competitive advantage. ERP software providers in India are integrating advanced analytics and business intelligence (BI) tools into their systems. These tools enable businesses to gain deep insights into their operations, identify trends, and make data-driven decisions.

Advanced analytics and BI tools can analyze large volumes of data from various sources, providing comprehensive reports and dashboards. This helps businesses to monitor performance, identify inefficiencies, and uncover new opportunities for growth.

8. Greater Focus on User Experience and Interface Design

The user experience (UX) and interface design of ERP systems are critical to their adoption and effectiveness. ERP software companies in India are placing a greater emphasis on developing intuitive and user-friendly interfaces. This trend is driven by the need to ensure that ERP systems are accessible and easy to use for all employees, regardless of their technical expertise.

Modern ERP systems feature clean, responsive interfaces with customizable dashboards and navigation options. This focus on UX design helps to improve user satisfaction, reduce training time, and increase overall productivity.

9. Integration with the Internet of Things (IoT)

The Internet of Things (IoT) is transforming the way businesses operate by enabling real-time monitoring and data collection from connected devices. ERP software providers in India are integrating IoT capabilities into their systems to enhance operational efficiency and decision-making.

IoT-enabled ERP systems can monitor equipment performance, track inventory levels, and optimize supply chain operations. For example, sensors placed on manufacturing equipment can detect anomalies and trigger maintenance requests before a breakdown occurs. This integration of IoT with ERP systems allows businesses to leverage real-time data for proactive management and improved efficiency.

10. Sustainable and Green ERP Solutions

Sustainability is becoming a key consideration for businesses across industries. ERP software companies in India are developing solutions that support sustainable practices and environmental responsibility. Green ERP solutions help businesses to monitor and reduce their environmental impact by tracking energy consumption, waste management, and resource utilization.

By integrating sustainability metrics into their ERP systems, businesses can set and achieve environmental goals, comply with regulations, and enhance their corporate social responsibility (CSR) initiatives. This trend towards sustainable ERP solutions reflects the growing importance of environmental stewardship in today’s business landscape.

Conclusion

The future of ERP software in India is marked by innovation, adaptability, and a deep understanding of the unique needs of businesses. ERP software providers in India are leading the charge, offering solutions that are not only technologically advanced but also aligned with the evolving demands of the market. As we move into 2024, the trends highlighted in this blog will play a crucial role in shaping the ERP landscape, driving efficiency, and fostering growth across industries.

ERP software providers in India are well-positioned to support businesses in their digital transformation journeys, providing the tools and insights needed to thrive in a competitive environment. By staying ahead of these trends, businesses can leverage ERP solutions to achieve operational excellence and sustainable growth.

#ERP software Companies in India#ERP software providers in India#ERP software company in India#ERP software in India#ERP solution provider#ERP software#ERP system#cloud ERP#ERP solutions

4 notes

·

View notes

Text

Trends in AI & Generative AI: Insights from The 2023 AI Summit New York

Last week, I covered the AI Summit in New York. I was excited to learn about the trends in AI and generative AI and to see some commercial applications of these new technological advancements.

Patrick Murphy of UAB led the AI Exhibitor hub. Patrick shared insights from his research on Entrepreneurship. He shared how start-ups use AI, and Generative AI to scale up and bring products to market.

Generative AI is being used in the following eight ways:

Content and Asset Generative

Automated Processes

Ideation

Financial Management

Project Design

Optimized Structures

Acceleration and incubation

Ethics and Risk Management.

There was a pitching completion where start-ups did pitches in multiple rounds. At the beginning of the competition, they received advice from judges on best practices.

One of the start-ups that was of interest was Botwise. Jan Nowak shared how his team shared a use case on how they leveraged Language Learning models (LLM)using statistics and GPT solutions for rapid automation in customer service for Mylead.global is a platform that allows influencers to earn money. As a result, MyLead.global was able to screen influencers faster and better for their big brand clients.

AI-Powered Use Cases from across the board panel discussion

Leaders Saira Kazmi Ph. D. (CVS Health), Matthew Blakemore (Creative Industries Council) Taha Mokfi (HelloFresh), Kriti Kohli (Shopify), and Kris Perez (Data Force) share how they use chatbots, improving both the buyer and seller experience using AI. How AI can be used in video games to identify levels of violence and how AI can improve in healthcare and Radiology reducing the amount of time images are read while improving accuracy and detail.

Another interesting Panel was by Tim Delesio CTO of techolution

Tim asked What’s driving the explosive rise of AI all of a Sudden?

The answer is the economics of the labor market.

On the demand side, he cited labor shortages and persistent high inflation.

On the supply side, he cites the rise of ChatGPT and, major scientific and Technological breakthroughs in the past five to seven years.

He shared trends in AI for 2024 that include:

Physical Labor with AI to help deliver small batch sizes with high-precision quality control

Improved customer engagement by providing a new generation of customer service agents using Generative AI

Tim demonstrated some of these trends when he ordered a soda using an AI-powered robotic arm.

youtube

The booth had another machine showing how AI can enhance inventory management when items are ordered.

I was amazed to see some AI Tech that techolution brought to the marketplace.

On that note, I saw an AI-powered Kiosk by Graphen where a man ordered his food and paid. This company is using AI to revolutionize all industries.

Man orders food AI Kiosk

Man pays for food at AI Kiosk

There were so many great talks and exhibits.

youtube

Additional pictures can be found on Instagram.

I want to thank the AI Summit for having me as their guest. If you want to use AI and Generative to improve business outcomes, sign up for the AI summit in your city.

What do you think is next for AI and Generative AI?

Comment and share below.

Additional pictures can be found on Instagram.

5 notes

·

View notes

Text

Decoding Cybersecurity: Unveiling the Future of US Digital Forensics Excellence

What is the Size of US Digital forensics Industry?

US Digital forensics Market is expected to grow at a CAGR of ~% between 2022-2028 and is expected to reach ~USD Mn by 2028.

Escalating cyberattacks targeting individuals, organizations, and critical infrastructure underscore the need for robust digital forensics capabilities. The increasing frequency and sophistication of these attacks drive the demand for advanced tools and expertise to investigate and respond effectively.

Rapid technological advancements, including IoT, cloud computing, AI, and blockchain, introduce new avenues for cyber threats. Digital forensics services are crucial to understanding these emerging technologies' vulnerabilities and mitigating associated risks.

Furthermore, stricter data protection regulations and compliance mandates necessitate thorough digital evidence collection, preservation, and analysis.

Organizations across industries has invested in digital forensics to ensure adherence to legal requirements and regulatory frameworks.

Additionally Legal proceedings increasingly rely on digital evidence. Law enforcement, legal firms, and corporations require robust digital forensics services to gather, analyze, and present evidence in a court of law, driving market expansion.

Us Digital Forensics Market By Type

The US Digital forensics market is segmented by Computer Forensics, Network Forensics, Mobile Device forensics and Cloud forensics. Based on type, Computer Forensics type segment is emerged as the dominant segment in US Digital forensics market in 2022.

Computers are ubiquitous in modern society, utilized across industries, organizations, and households. As a result, a significant portion of digital evidence related to cybercrimes and incidents is generated from computer systems, driving the demand for specialized computer forensics expertise. Computers and their software environments evolve rapidly.

Us Digital Forensics Market By End User Application

US Digital forensics market is segmented by Government and Defence, BFSI, Telecom and IT, Retail, Healthcare and Other Government and Defence market is dominant in end user application segment in Digital forensics market in 2022.

Government and defense agencies handle highly sensitive information related to national security and intelligence. The increasing sophistication of cyber threats targeting these entities necessitates robust digital forensics capabilities to investigate and respond to cyber incidents effectively.

Government and defense entities are prime targets for cyberattacks due to their critical roles. Effective incident response through digital forensics helps in containing and mitigating cyber incidents swiftly, minimizing damage and preventing further breaches.

US Digital forensics by Region

The US Digital forensics market is segmented by Region into North, East, West, South. In 2022, the dominance region is East region in US Digital forensics market.

The East region has a dense population and a well-established digital infrastructure, making it a hotspot for cybercriminal activity. The higher frequency of cyber threats and incidents necessitates a strong emphasis on digital forensics to investigate and mitigate these risks effectively. Additionally, the East region often sees a proactive approach from regulatory and legal bodies, reinforcing the demand for digital forensics services to ensure compliance and assist in investigations. The proximity of key players in law enforcement, government agencies, legal firms, and corporate headquarters further fuels the need for robust digital forensics capabilities.

Download a Sample Report of US digital forensics Solution Market

Competition Scenario in US Digital forensics Market

The US digital forensics market is characterized by a competitive landscape with several key players competing for market share. Prominent companies offering a range of digital forensics solutions and services contribute to the market's dynamism.

The competitive landscape also includes smaller, specialized firms and start-ups that focus on niche areas of digital forensics, such as cloud forensics, memory forensics, and industrial control systems forensics.

The competition is further intensified by the continuous evolution of technology, leading to the emergence of new players and innovative solutions. As the demand for digital forensics continues to grow, companies in this market are likely to invest in research and development to stay ahead of the curve, leading to a consistently competitive environment.

What is the Expected Future Outlook for the Overall US Digital forensics Market?

Download a Custom Report of US digital forensics market Growth

The US Digital forensics market was valued at USD ~Million in 2022 and is anticipated to reach USD ~ Million by the end of 2028, witnessing a CAGR of ~% during the forecast period 2022- 2028.

The US digital forensics market is poised for robust expansion due to the ever-evolving cybersecurity landscape, technological advancements, and regulatory pressures. Organizations across industries will increasingly recognize the necessity of investing in digital forensics to safeguard their digital assets and ensure compliance.

As long as cyber threats continue to evolve, the demand for sophisticated digital forensic tools, services, and expertise will remain on an upward trajectory.

The US digital forensics market appears promising, characterized by a confluence of technological advancements, increasing cyber threats, and growing legal and regulatory requirements. As technology continues to evolve rapidly, so does the nature of cybercrimes, creating a persistent demand for digital forensics solutions and services.

Additionally, the escalating frequency and complexity of cyberattacks. As more critical operations and personal information are digitized, the potential attack surface expands, leading to a higher likelihood of security breaches. This dynamic compels organizations and law enforcement agencies to enhance their digital forensic capabilities to investigate, mitigate, and prevent cyber incidents effectively.

Furthermore, the rise of emerging technologies like the Internet of Things (IoT), artificial intelligence (AI), and blockchain presents both opportunities and challenges. These technologies bring new possibilities for efficiency and connectivity but also introduce novel avenues for cyber threats. Consequently, the demand for digital forensics services is expected to surge as organizations seek expertise in unraveling incidents involving these cutting-edge technologies.

The market is also likely to see increased adoption of cloud-based digital forensics solutions. As more data is stored and processed in the cloud, digital forensic providers will need to develop tools and methodologies to effectively gather evidence from virtual environments, remote servers, and distributed systems.

2 notes

·

View notes

Text

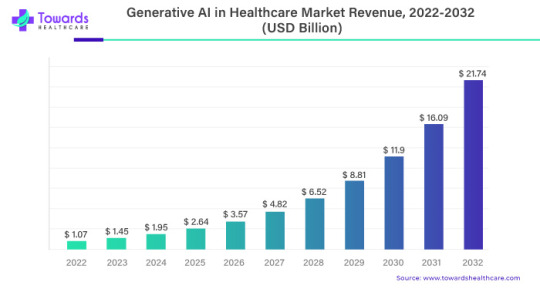

Generative AI in Healthcare Market to Grow at an 35.1% CAGR Till 2032!

The global Generative AI in Healthcare Market worth USD 1.07 billion in 2023 is likely to be USD 21.74 billion by 2032, growing at a 35.1% CAGR between 2023 and 2032.

According to the stats published by World Health Organization (WHO), approximately 1.28 million adults (between 30 and 79 years of age) have hypertension. Of these, as little as 42% of adults are diagnosed and treated correctly and the remaining population is unaware of this condition. The majority of this population resides in low to middle-income countries of the world. Despite this substantial number of untreated cases, the rising awareness among doctors and the general population regarding health illnesses associated with hypertension is expected to drive the demand for the required devices.

Download White Paper@ https://www.towardshealthcare.com/personalized-scope/5069

A recent report provides crucial insights along with application based and forecast information in the Global Generative AI in Healthcare Market. The report provides a comprehensive analysis of key factors that are expected to drive the growth of this Market. This study also provides a detailed overview of the opportunities along with the current trends observed in the Generative AI in Healthcare Market.

A quantitative analysis of the industry is compiled for a period of 10 years in order to assist players to grow in the Market. Insights on specific revenue figures generated are also given in the report, along with projected revenue at the end of the forecast period.

Report Objectives

To define, describe, and forecast the global Generative AI in Healthcare Market based on product, and region

To provide detailed information regarding the major factors influencing the growth of the Market (drivers, opportunities, and industry-specific challenges)

To strategically analyze microMarkets1 with respect to individual growth trends, future prospects, and contributions to the total Market

To analyze opportunities in the Market for stakeholders and provide details of the competitive landscape for Market leaders

To forecast the size of Market segments with respect to four main regions—North America, Europe, Asia Pacific and the Rest of the World (RoW)2

To strategically profile key players and comprehensively analyze their product portfolios, Market shares, and core competencies3

To track and analyze competitive developments such as acquisitions, expansions, new product launches, and partnerships in the Generative AI in Healthcare Market

Companies and Manufacturers Covered

The study covers key players operating in the Market along with prime schemes and strategies implemented by each player to hold high positions in the industry. Such a tough vendor landscape provides a competitive outlook of the industry, consequently existing as a key insight. These insights were thoroughly analysed and prime business strategies and products that offer high revenue generation capacities were identified. Key players of the global Generative AI in Healthcare Market are included as given below:

Generative AI in Healthcare Market Key Players:

Syntegra

NioyaTech

Saxon

IBM Watson

Microsoft Corporation

Google LLC

Tencent Holdings Ltd.

Neuralink Corporation

OpenAI

Oracle

Market Segments :

By Application

Clinical

Cardiovascular

Dermatology

Infectious Disease

Oncology

Others

System

Disease Diagnosis

Telemedicine

Electronic Health Records

Drug Interaction

By Function

AI-Assisted Robotic Surgery

Virtual Nursing Assistants

Aid Clinical Judgment/Diagnosis

Workflow & Administrative Tasks

Image Analysis

By End User

Hospitals & Clinics

Clinical Research

Healthcare Organizations

Diagnostic Centers

Others

By Geography

North America

Europe

Asia-Pacific

Latin America

Middle East and Africa

Contact US -

Towards Healthcare

Web: https://www.towardshealthcare.com/

You can place an order or ask any questions, please feel free to contact at

Email: [email protected]

About Us

We are a global strategy consulting firm that assists business leaders in gaining a competitive edge and accelerating growth. We are a provider of technological solutions, clinical research services, and advanced analytics to the healthcare sector, committed to forming creative connections that result in actionable insights and creative innovations.

#seo marketing#seo#market analysis#market share#marketing#ai#artificial intelligence#Generative AI#healthcare

2 notes

·

View notes

Text

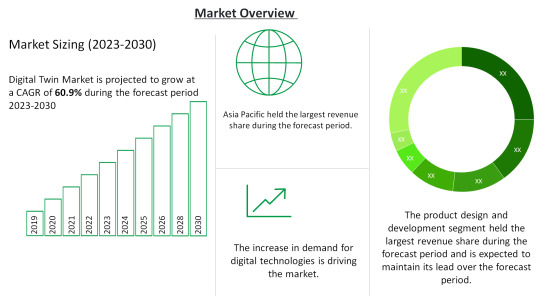

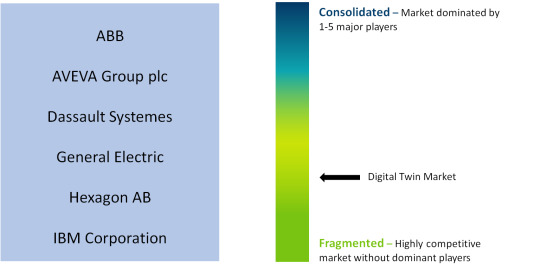

Digital Twin Market Size 2023-2030: ABB, AVEVA Group plc, Dassault Systemes

Digital Twin Market by Power Source (Battery-Powered, hardwired with battery backup, Hardwired without battery backup), Type (Photoelectric Smoke Detectors, Ionization Smoke Detectors), Service, Distribution Channel, and region (North America, Europe, Asia-Pacific, Middle East, and Africa and South America). The global Digital Twin Market size is 11.12 billion USD in 2022 and is projected to reach a CAGR of 60.9% from 2023-2030.

Click Here For a Free Sample + Related Graphs of the Report at: https://www.delvens.com/get-free-sample/digital-twin-market-trends-forecast-till-2030

Digital twin technology has allowed businesses in end-use industries to generate digital equivalents of objects and systems across the product lifecycle. The potential use cases of digital twin technology have expanded rapidly over the years, anchored in the increasing trend of integration with internet-of-things (IoT) sensors. Coupled with AI and analytics, the capabilities of digital twins are enabling engineers to carry out simulations before a physical product is developed. As a result, digital twins are being deployed by manufacturing companies to shorten time-to-market. Additionally, digital twin technology is also showing its potential in optimizing maintenance costs and timelines, thus has attracted colossal interest among manufacturing stalwarts, notably in discrete manufacturing.

The shift to interconnected environments across industries is driving the demand for digital twin solutions across the world. Massive adoption of IoT is being witnessed, with over 41 billion connected IoT devices expected to be in use by 2030. For the successful implementation and functioning of IoT, increasing the throughput for every part or “thing” is necessary, which is made possible by digital twin technology. Since the behavior and performance of a system over its lifetime depend on its components, the demand for digital twin technology is increasing across the world for system improvement. The emergence of digitalization in manufacturing is driving the global digital twin market. Manufacturing units across the globe are investing in digitalization strategies to increase their operational efficiency, productivity, and accuracy. These digitalization solutions including digital twin are contributing to an increase in manufacturer responsiveness and agility through changing customer demands and market conditions.

On the other hand, there has been a wide implementation of digital technologies like artificial intelligence, IoT, clog, and big data which is increasing across the business units. The market solutions help in the integration of IoT sensors and technologies that help in the virtualization of the physical twin. The connectivity is growing and so are the associated risks like security, data protection, and regulations, alongside compliance.

During the COVID-19 pandemic, the use of digital twin technologies to manage industrial and manufacturing assets increased significantly across production facilities to mitigate the risks associated with the outbreak. Amid the lockdown, the U.S. implemented a National Digital Twin Program, which was expected to leverage the digital twin blueprint of major cities of the U.S. to improve smart city infrastructure and service delivery. The COVID-19 pandemic positively impacted the digital twin market demand for twin technology.

Delvens Industry Expert’s Standpoint

The use of solutions like digital twins is predicted to be fueled by the rapid uptake of 3D printing technology, rising demand for digital twins in the healthcare and pharmaceutical sectors, and the growing tendency for IoT solution adoption across multiple industries. With pre-analysis of the actual product, while it is still in the creation stage, digital twins technology helps to improve physical product design across the full product lifetime. Technology like digital twins can be of huge help to doctors and surgeons in the near future and hence, the market is expected to grow.

Market Portfolio

Key Findings

The enterprise segment is further segmented into Large Enterprises and Small & Medium Enterprises. Small & Medium Enterprises are expected to dominate the market during the forecast period. It is further expected to grow at the highest CAGR from 2023 to 2030.

The industry segment is further segmented into Automotive & Transportation, Energy & Utilities, Infrastructure, Healthcare, Aerospace, Oil & Gas, Telecommunications, Agriculture, Retail, and Other Industries. The automotive & transportation industry is expected to account for the largest share of the digital twin market during the forecast period. The growth can be attributed to the increasing usage of digital twins for designing, simulation, MRO (maintenance, repair, and overhaul), production, and after-service.

The market is also divided into various regions such as North America, Europe, Asia-Pacific, South America, and Middle East and Africa. North America is expected to hold the largest share of the digital twin market throughout the forecast period. North America is a major hub for technological innovations and an early adopter of digital twins and related technologies.

During the COVID-19 pandemic, the use of digital twin technologies to manage industrial and manufacturing assets increased significantly across production facilities to mitigate the risks associated with the outbreak. Amid the lockdown, the U.S. implemented a National Digital Twin Program, which was expected to leverage the digital twin blueprint of major cities of the U.S. to improve smart city infrastructure and service delivery. The COVID-19 pandemic positively impacted the digital twin market demand for twin technology.

Regional Analysis

North America to Dominate the Market

North America is expected to hold the largest share of the digital twin market throughout the forecast period. North America is a major hub for technological innovations and an early adopter of digital twins and related technologies.

North America has an established ecosystem for digital twin practices and the presence of large automotive & transportation, aerospace, chemical, energy & utilities, and food & beverage companies in the US. These industries are replacing legacy systems with advanced solutions to improve performance efficiency and reduce overall operational costs, resulting in the growth of the digital twin technology market in this region.

Competitive Landscape

ABB

AVEVA Group plc

Dassault Systemes

General Electric

Hexagon AB

IBM Corporation

SAP

Microsoft

Siemens

ANSYS

PTC

IBM

Recent Developments

In April 2022, GE Research (US) and GE Renewable Energy (France), subsidiaries of GE, collaborated and developed a cutting-edge artificial intelligence (AI)/machine learning (ML) technology that has the potential to save the worldwide wind industry billions of dollars in logistical expenses over the next decade. GE’s AI/ML tool uses a digital twin of the wind turbine logistics process to accurately predict and streamline logistics costs. Based on the current industry growth forecasts, AI/ML might enable a 10% decrease in logistics costs, representing a global cost saving to the wind sector of up to USD 2.6 billion annually by 2030.

In March 2022, Microsoft announced a strategic partnership with Newcrest. The mining business of Newcrest would adopt Azure as its preferred cloud provider globally, as well as work on digital twins and a sustainability data model. Both organizations are working together on projects, including the use of digital twins to improve operational performance and developing a high-impact sustainability data model.

Reasons to Acquire

Increase your understanding of the market for identifying the best and most suitable strategies and decisions on the basis of sales or revenue fluctuations in terms of volume and value, distribution chain analysis, market trends, and factors

Gain authentic and granular data access for Digital Twin Market so as to understand the trends and the factors involved in changing market situations

Qualitative and quantitative data utilization to discover arrays of future growth from the market trends of leaders to market visionaries and then recognize the significant areas to compete in the future

In-depth analysis of the changing trends of the market by visualizing the historic and forecast year growth patterns

Direct Purchase of Digital Twin Market Research Report at: https://www.delvens.com/checkout/digital-twin-market-trends-forecast-till-2030

Report Scope

Report FeatureDescriptionsGrowth RateCAGR of 60.9% during the forecasting period, 2023-2030Historical Data2019-2021Forecast Years2023-2030Base Year2022Units ConsideredRevenue in USD million and CAGR from 2023 to 2030Report Segmentationenterprise, platform, application, and region.Report AttributeMarket Revenue Sizing (Global, Regional and Country Level) Company Share Analysis, Market Dynamics, Company ProfilingRegional Level ScopeNorth America, Europe, Asia-Pacific, South America, and Middle East, and AfricaCountry Level ScopeU.S., Japan, Germany, U.K., China, India, Brazil, UAE, and South Africa (50+ Countries Across the Globe)Companies ProfiledABB; AVEVA Group plc; Dassault Systems; General Electric; Hexagon AB; IBM Corp.; SAP.Available CustomizationIn addition to the market data for Digital Twin Market, Delvens offers client-centric reports and customized according to the company’s specific demand and requirement.

TABLE OF CONTENTS

Large Enterprises

Small & Medium Enterprises

Product Design & Development

Predictive Maintenance

Business Optimization

Performance Monitoring

Inventory Management

Other Applications

Automotive & Transportation

Energy & Utilities

Infrastructure

Healthcare

Aerospace

Oil & Gas

Telecommunications

Agriculture

Retail

Other Industries.

Asia Pacific

North America

Europe

South America

Middle East & Africa

ABB

AVEVA Group plc

Dassault Systemes

General Electric

Hexagon AB

IBM Corporation

SAP

About Us:

Delvens is a strategic advisory and consulting company headquartered in New Delhi, India. The company holds expertise in providing syndicated research reports, customized research reports and consulting services. Delvens qualitative and quantitative data is highly utilized by each level from niche to major markets, serving more than 1K prominent companies by assuring to provide the information on country, regional and global business environment. We have a database for more than 45 industries in more than 115+ major countries globally.

Delvens database assists the clients by providing in-depth information in crucial business decisions. Delvens offers significant facts and figures across various industries namely Healthcare, IT & Telecom, Chemicals & Materials, Semiconductor & Electronics, Energy, Pharmaceutical, Consumer Goods & Services, Food & Beverages. Our company provides an exhaustive and comprehensive understanding of the business environment.

Contact Us:

UNIT NO. 2126, TOWER B, 21ST FLOOR ALPHATHUM SECTOR 90 NOIDA 201305, IN +44-20-8638-5055 [email protected] WEBSITE: https://delvens.com/

#Digital Twin Market#Digital Twin#Digital Twin Market Size#Digital Twin Market Share#Semiconductors & Electronics

2 notes

·

View notes

Text

Growth and Opportunities in the Artificial Intelligence Chip Market

The Artificial Intelligence (AI) chip market is revolutionizing industries by enabling faster processing, smarter algorithms, and real-time decision-making. These specialized semiconductors are designed to handle AI workloads, such as machine learning, natural language processing, and computer vision. With rapid advancements in AI applications across sectors, the demand for AI chips is growing exponentially.

The��global artificial intelligence chip market size is projected to grow from USD 123.16 billion in 2024 to USD 311.58 billion by 2029, growing at a CAGR of 20.4% during the forecast period from 2024 to 2029.

The AI chip market is driven by the increasing adoption of AI servers by hyperscalers and the growing use of Generative AI technologies and applications, such as GenAI and AIoT, across various industries, including BFSI, healthcare, retail & e-commerce, and media & entertainment.

Market Dynamics: Key Drivers Fuelling Growth

1. Proliferation of AI Applications

AI chips are integral to diverse applications, including autonomous vehicles, robotics, healthcare diagnostics, and smart cities. The expansion of these technologies is boosting market demand.

2. Advancements in Semiconductor Technology

Innovations in chip architectures, such as GPUs, TPUs, and neuromorphic processors, are enhancing AI efficiency and scalability, driving adoption across industries.

3. Rising Investments in AI R&D

Governments and corporations are heavily investing in AI research and development, further propelling the adoption of AI chipsets.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=237558655

Segmentation Analysis: A Diverse Market Landscape

1. By Chip Type

GPU (Graphics Processing Unit): Dominates the AI chip market due to its superior parallel processing capabilities.

ASIC (Application-Specific Integrated Circuit): Tailored for specific AI tasks, offering higher efficiency.

FPGA (Field-Programmable Gate Array): Known for flexibility and adaptability in dynamic AI workloads.

2. By Application

Consumer Electronics: AI-enabled smartphones and smart home devices are key growth contributors.

Automotive: Self-driving cars rely heavily on AI chips for object detection and navigation.

Healthcare: AI chips power diagnostic tools, personalized medicine, and predictive analytics.

Regional Insights: Market Trends Across the Globe

1. North America

North America leads the AI chip market, driven by significant investments in AI research and strong presence of tech giants like NVIDIA and Intel.

2. Asia-Pacific

The Asia-Pacific region is experiencing robust growth, fueled by rising adoption of AI in manufacturing, consumer electronics, and the automotive sector, particularly in China and South Korea.

3. Europe

Europe focuses on AI ethics and innovation, with industries like automotive and healthcare leveraging AI chips for smarter solutions.

Challenges and Opportunities: Navigating Market Dynamics

1. Challenges

High Development Costs: The design and manufacturing of AI chips involve substantial investments.

Data Privacy Concerns: Handling sensitive data requires robust security measures.

2. Opportunities

Edge AI Growth: Increasing demand for edge computing is creating opportunities for AI chips in devices requiring low latency.

AI in Emerging Markets: Expanding AI adoption in emerging economies presents untapped potential for the AI chip market.

Future Outlook: The Road Ahead

The AI chip market is poised for significant growth, with advancements in quantum computing, 5G integration, and edge AI driving innovation. Companies investing in R&D and strategic partnerships will likely dominate this evolving landscape.

AI chips are the backbone of modern technological advancements, empowering industries to unlock new possibilities. As AI continues to reshape the future, the AI chip market stands as a cornerstone of this transformative journey, promising sustained growth and innovation.

0 notes

Text

The Digital Asset Management (DAM) Market is expected to grow significantly, with its market size projected to increase from USD 6,712.608 million in 2024 to an estimated USD 18,960.97 million by 2032, reflecting a compound annual growth rate (CAGR) of 13.86% over the forecast period.The Digital Asset Management (DAM) market has emerged as a critical solution in the digital age, where businesses are inundated with content and digital assets that require efficient organization, retrieval, and utilization. From enhancing marketing campaigns to streamlining creative workflows, DAM systems have become indispensable for businesses aiming to maintain their competitive edge. This article delves into the dynamics of the DAM market, highlighting its growth drivers, challenges, and future potential.

Browse the full report at https://www.credenceresearch.com/report/digital-asset-management-market

Overview of Digital Asset Management

Digital Asset Management refers to software solutions designed to store, organize, and manage digital assets, including images, videos, documents, audio files, and more. By centralizing these assets, DAM systems enable organizations to improve efficiency, maintain brand consistency, and optimize content distribution.

Traditionally adopted by media and entertainment companies, DAM solutions are now widely used across industries such as retail, healthcare, education, and manufacturing. The growing reliance on digital marketing strategies and the proliferation of content across social media and other platforms have further amplified the demand for DAM systems.

Market Growth and Trends

The DAM market has witnessed robust growth over the past decade. According to industry reports, the market size was valued at approximately $4 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 15-20% from 2023 to 2030. This expansion can be attributed to the following factors:

Content Explosion The exponential growth of digital content has created an urgent need for systems that can efficiently manage and retrieve assets. DAM solutions offer a scalable infrastructure for handling vast volumes of content.

Integration with AI and Machine Learning Modern DAM platforms increasingly incorporate artificial intelligence (AI) and machine learning (ML) capabilities. Features such as automated tagging, metadata generation, and content recommendations enhance usability and reduce manual effort.

Remote Work and Collaboration The COVID-19 pandemic accelerated the shift to remote work, increasing the demand for cloud-based DAM solutions. These platforms facilitate seamless collaboration by providing centralized access to digital assets.

Focus on Brand Consistency Businesses are prioritizing consistent branding across channels. DAM solutions help maintain uniformity by providing access to approved brand assets and templates.

Adoption in Small and Medium Enterprises (SMEs) The availability of cost-effective and scalable solutions has encouraged SMEs to adopt DAM platforms, broadening the market's reach.

Key Challenges

Despite its benefits, the DAM market faces certain challenges:

High Initial Costs Implementing a DAM system often requires significant investment in terms of software, infrastructure, and training. This can deter smaller businesses from adoption.

Complexity of Integration Integrating DAM systems with existing enterprise software and workflows can be complex and resource-intensive, requiring technical expertise.

Data Security Concerns As DAM platforms increasingly move to the cloud, concerns about data breaches and unauthorized access have risen, making security a critical consideration.

Future Outlook

The DAM market is poised for significant advancements, driven by technological innovation and evolving business needs. Trends such as:

Blockchain for Secure Asset Tracking Blockchain technology could enhance asset security and enable transparent usage tracking.

Advanced Personalization AI-powered personalization will allow businesses to deliver more targeted and relevant content to their audiences.

Sustainability and Compliance As businesses prioritize sustainability, DAM systems can help reduce redundant asset production, minimizing resource wastage.

Key Player Analysis:

Adobe Systems Incorporated

OpenText Corporation

IBM Corporation

Oracle Corporation

Cognizant Technology Solutions

Hewlett-Packard (HP) Enterprise

North Plains Systems Corp.

Widen Enterprises, Inc.

Bynder B.V.

MediaBeacon, Inc.

Segmentations:

By Asset Type

Documents/Presentations

Multimedia Assets (Audio, Video, Images, Animation)

By Deployment

Cloud

On Premise

By Enterprise Size

Small & Medium Enterprise

Large Enterprise

By Industry

Media & Entertainment

Healthcare

E-Commerce & Retail

Travel & Hospitality

Others (Education, Manufacturing, Real Estate)

By Region

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/digital-asset-management-market

About Us:

Credence Research is committed to employee well-being and productivity. Following the COVID-19 pandemic, we have implemented a permanent work-from-home policy for all employees.

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

0 notes

Text

Empowering Urban Innovation: The Expanding Smart Cities Market

Smart Cities Industry Overview

The global smart cities market size is expected to reach USD 3,728.3 billion by 2030, registering a CAGR of 25.8% from 2023 to 2030, according to a new report by Grand View Research, Inc. The market growth can be attributed to rapid favorable government initiatives worldwide and emerging technologies, such as Artificial Intelligence (AI), cybersecurity, big data analytics, and the Internet of Things (IoT). This has encouraged several countries to invest in smart city projects to manage infrastructure and assets. Further, the increasing adoption of Electric Vehicles (EVs) has also created a demand for the development of charging infrastructure in cities globally. Due to this, it provides energy storage and creates new revenue streams from EV batteries. These benefits will further boost the smart cities market's growth during the forecast period.

The smart cities market is witnessing a high investment in smart security, smart metering for utilities, integrated traffic management systems, and smart mobility. Several technologically innovative cities use IoT platforms to monitor their infrastructure, manage traffic flows, water management, parking, and air quality, and use the generated smart data to handle longer-term decisions for environmental sustainability. Market players are establishing strategic partnerships with technology providers to improve their smart cities portfolio. For instance, in February 2022, an electric utility company, E.ON SE, partnered with telecom company Vodafone Group plc to develop smart water, gas, and electricity meters, accrelating the smart cities market growth.

Gather more insights about the market drivers, restrains and growth of the Smart Cities Market

Various country governments, such as India, Germany, Canada, Japan, and Australia, are launching smart city-based projects to improve citizens' lifestyles and create safer communities, propelling smart cities market expansion. Government-authorized associations & organizations are collaborating with market players to develop smart city solutions to assist the government in planning smart city strategies. For instance, in October 2022, the non-profit organization, Accelerator for America partnered with Honeywell International Inc. and launched the Smart City Accelerator Program to help smart city developers define priorities, align key stakeholders, and improve service delivery & operational efficiency of smart cities projects.

Browse through Grand View Research's Next Generation Technologies Industry Research Reports.

The global artificial intelligence in marketing market size was estimated USD 20,447.1 million in 2024 and projected to grow at a CAGR of 25.0% from 2025 to 2030.

The global AI training dataset in healthcare market size was estimated at USD 423.0 million in 2024 and is projected to grow at a CAGR of 22.9% from 2025 to 2030.

Smart Cities Market Segmentation

Grand View Research has segmented the global smart cities market on the basis of on application, smart governance, smart utilities, smart transportation, smart healthcare, and region:

Smart Cities Application Outlook (Revenue, USD Billion, 2018 - 2030)

Smart Governance

Smart Building

Environmental Solution

Smart Utilities

Smart Transportation

Smart Healthcare

Smart Public Safety

Smart Security

Smart Education

Smart Governance Outlook (Revenue, USD Billion, 2018 - 2030)

City Surveillance

C.S.

E-governance

Smart Lighting

Smart Infrastructure

Smart Utilities Outlook (Revenue, USD Billion, 2018 - 2030)

Energy Management

Water Management

Waste Management

Meter Data Management

Distribution Management System

Substation Automation

Other Smart Utilities Solutions

Smart Transportation Outlook (Revenue, USD Billion, 2018 - 2030)

Intelligent Transportation System

Parking Management

Smart Ticketing & Travel Assistance

Traffic Management

Passenger Information

Connected Logistics

Other Smart Transportation Solutions

Smart Cities Smart Healthcare Outlook (Revenue, USD Billion, 2018 - 2030)

Medical Devices

Systems & Software

Smart Cities Regional Outlook (Revenue, USD Billion, 2018 - 2030)

North America

US

Canada

Europe

UK

Germany

France

Italy

Spain

Russia

Nordic Region

Eastern Europe

Asia Pacific

China

Japan

India

South Korea

Australia

ASEAN

Latin America

Brazil

Mexico

Middle East and Africa (MEA)

UAE

South Africa

Saudi Arabia

Key Companies profiled:

ABB Limited

AGT International

AVEVA Group plc.

Cisco Systems, Inc.

Ericsson

General Electric

Honeywell International Inc.

International Business Machines Corporation

Itron Inc.

KAPSCH Group

Huawei Technologies Co., Ltd.

Microsoft Corporation

Oracle Corporation

Osram Gmbh

SAP SE

Schneider Electric SE

Siemens AG

Telensa

Verizon

Vodafone Group plc

Key Smart Cities Company Insights

Some of the key players operating in the market include Microsoft Corporation, and Oracle Corporation.

Microsoft Corporation provides business software and solutions. The well-known software products from Microsoft are the Microsoft 365 series of productivity programs, Windows series of operating systems, and the Edge browser. Its flagship hardware products are Xbox video game consoles and Microsoft Surface touchscreen computers.

Oracle Corporation is a provider of IT software and services. The company sells database software and technology, cloud engineered systems, and enterprise software products, such as, human capital management software, enterprise resource planning software, supply chain management software, enterprise performance management software, and customer relationship management software.

Ericsson, and Telensa are some of the emerging market participants in the smart cities market.

Ericsson develops the IT products and services for the telecommunications industry and is currently leading the way in 5G. The company sells infrastructure, software and services in the field of information and communication technology for mobile service providers and enterprises, including 3G, 4G and 5G equipment, Internet Protocol (IP) and optical transport systems.

Telensa offers simple and effective smart lighting solutions for public and district lighting to help cities, utilities and large areas manage their lighting to save money and reduce costs.

Recent Developments

In December 2023, Msheireb Properties (MP), Qatar based property developer, signed a Memorandum of Understanding (MoU) with Microsoft Corporation, software products developer, to develop a ‘Smart Experience’ project for visitors, retail, residents, and commercial customers in MP’s development, Msheireb Downtown Doha (MDD).The Smart Experience project is revolutionizing the way citizens interact with the urban environment by incorporating new solutions to improve the lives of MDD members.

In November 2023,Smart City Expo World Congress (SCEWC), the international event on cities and smart urban solutions organized by Fira de Barcelona. It is an exhibition of innovative urban solutions and projects that focus on ways to transform modern cities into more sustainable, efficient and habitable places. The congress program of SCEWC comprises eight main themes, including energy and environment, enabling technologies, mobility, housing and inclusion, management and economy, security and blue economy, and infrastructure and buildings.

In August 2023, NEC Corporation India, IT services provider, launched Smart City project in Tirupati, India, for Tirupati Smart City Corporation Limited.Under this project, NEC Corporation India would implement ICT solutions across the city and establish a City Operations Center (COC) in Tirupati. ICT solutions, such as, a unified command and control center, and integrated services enable real-time data collection and analysis and two-way communication, helping to provide more effective responses to environmental, and health safety.

Order a free sample PDF of the Smart Cities Market Intelligence Study, published by Grand View Research.

0 notes

Text

0 notes

Text

Simulation Software Industry Size & Share | Statistics Report 2030

The global simulation software market size is estimated to reach USD 51.11 billion by 2030, registering a CAGR of 13.8% from 2024 to 2030, according to a new study by Grand View Research, Inc. Simulation software is being used for training personnel. It is replacing the traditional real-time training techniques, which incurred huge investments annually for companies. The use of simulation for training purposes helps reduce training costs as companies need to make a one-time investment for software implementation. The software also helps enterprises minimize production costs by enhancing the product development process.

The need for developing prototypes and the chances of product failure are considerably reduced through the use of simulators, as the product is virtually tested for all possible glitches before the commencement of production. Furthermore, simulation-based tools help product developers reduce the time spent on R&D processes as it enables them to obtain a realistic view of a product or process under study or review. Organizations across the globe are increasingly implementing the program and analyzing tools to enhance the entire product development cycle, reduce time to production, ensure delivery of high-quality products in minimal time, and reduce the overall cost to the company with respect to R&D.

Gather more insights about the market drivers, restrains and growth of the Global Simulation Software Market

It requires a skilled workforce or personnel with the required knowledge and understanding. This is leading to several manufacturers being reluctant to adopt this technology as the need for a skilled workforce incurs additional costs. The COVID-19 pandemic had an adverse impact on the global market. The closure of national and international borders in major countries, such as China, Japan, and India, has caused severe supply chain disruptions. In addition, the temporary shutdown of manufacturing operations has led manufacturing companies to face severe budgetary issues, resulting in delayed subscription renewal payments during the pandemic’s initial phase. However, recovering economies and opening businesses are expected to help the market grow at a rapid pace over the forecast period.

Simulation Software Market Report Highlights

The market is being driven by reduced training costs for personnel in various industries and sectors, such as automotive, defense, healthcare, and electrical

The service segment is expected to register a CAGR of 15.0% owing to the growing demand for customized simulation solutions, such as design and consulting

The cloud-based segment is expected to register the fastest CAGR of approximately 15.4% over the forecast period owing to benefits, such as easy and low-cost implementation

The automotive segment dominated the market in 2023 and is expected to hold a major share by 2030 owing to the early adoption of virtual testing tools in the automotive industry

North America is expected to account for the highest market share followed by Asia Pacific, by 2030 owing to the growing investments in R&D and defense in countries, such as the U.S.

Leading players are focusing on developing new simulation software solutions, to capture maximum share

Browse through Grand View Research's Next Generation Technologies Industry Research Reports.

Charging As A Service Market: The global charging as a service market size was estimated at USD 338.3 million in 2024 and is expected to grow at a CAGR of 25.0% from 2025 to 2030.

AI In Media & Entertainment Market: The global AI in media & entertainment market size was estimated at USD 25.98 billion in 2024 and is projected to grow at a CAGR of 24.2% from 2025 to 2030.

Simulation Software Market Segmentation

Grand View Research has segmented the global simulation software market on the basis of component, deployment, application, end-use, and region:

Simulation Software Component Outlook (Revenue, USD Million, 2017 - 2030)

Software

Services

Simulation Software Deployment Outlook (Revenue, USD Million, 2017 - 2030)

On-Premise

Cloud

Simulation Software Application Outlook (Revenue, USD Million, 2017 - 2030)

Engineering, Research, Modeling & Simulated Testing

High Fidelity Experiential 3D Training

Gaming & Immersive Experiences

Manufacturing Process Optimization

AI Training & Autonomous Systems

Planning And Logistics Management & Transportation

Cyber Simulation

Simulation Software End-use Outlook (Revenue, USD Million, 2017 - 2030)

Conventional Automotive

Electric Automotive and Autonomous Vehicles

Aerospace & Defense

Electrical, Electronics and Semiconductor

Healthcare

Robotics

Entertainment

Architectural Engineering and Construction

Others

Simulation Software Regional Outlook (Revenue, USD Million, 2017 - 2030)

North America

Europe

Asia Pacific

Latin America

Middle East & Africa (MEA)

Order a free sample PDF of the Simulation Software Market Intelligence Study, published by Grand View Research.

0 notes

Text

Tissue Engineering Market Size, Share & Industry Demand Trends to 2032

The Tissue Engineering Market Revenue was valued at USD 16.8 Billion in 2023 and is expected to witness substantial growth, reaching USD 56.2 Billion by 2032, with a promising CAGR of 14.3% over the forecast period from 2024 to 2032. The significant advancements in tissue engineering techniques and the growing demand for innovative solutions to treat various medical conditions are driving the expansion of this market.

Key Market Drivers

The tissue engineering market is primarily driven by the increasing prevalence of chronic diseases and injuries that require tissue regeneration, such as cardiovascular diseases, diabetes, and orthopedic injuries. Additionally, the rise in demand for organ transplants, coupled with the shortage of available donor organs, has heightened the focus on regenerative medicine, further stimulating the growth of tissue engineering solutions.

Technological advancements in 3D bioprinting, stem cell therapies, and scaffold technologies are revolutionizing the field, enabling the development of more effective and personalized tissue engineering treatments. Furthermore, government investments and funding for regenerative medicine research and development are expected to propel the growth of the market.

Regional Insights

North America holds the largest share of the tissue engineering market, driven by the presence of leading healthcare institutions, significant research investments, and strong regulatory support. The region's advanced healthcare infrastructure and the increasing demand for organ transplantation have also contributed to its dominant position.

Meanwhile, the Asia-Pacific region is experiencing rapid growth in the tissue engineering market, owing to the rising adoption of advanced medical technologies, expanding healthcare infrastructure, and increasing awareness about regenerative medicine. Countries such as China, Japan, and India are expected to contribute significantly to the market's expansion in the coming years.

Get Free Sample Report@ https://www.snsinsider.com/sample-request/4502

Market Outlook

The tissue engineering market is witnessing innovations in various segments, including skin, bone, cartilage, and vascular tissues. These developments are paving the way for improved therapeutic solutions for injuries and degenerative diseases, making tissue engineering an increasingly vital field in regenerative medicine. The continued progress in biocompatible materials and the ability to replicate complex tissue structures using bioprinting technologies are expected to enhance the efficacy of tissue engineering treatments.

The integration of artificial intelligence (AI) and machine learning (ML) into tissue engineering research is also playing a crucial role in accelerating product development, optimizing clinical outcomes, and reducing costs. Moreover, the expansion of cell therapy and gene editing techniques is driving new avenues for the generation of customized tissues and organs, further fueling market growth.

About Us

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Contact Us

Akash Anand – Head of Business Development & Strategy Email: [email protected] Phone: +1-415-230-0044 (US) | +91-7798602273 (IND)

#Tissue Engineering#Tissue Engineering Market#Tissue Engineering Market Size#Tissue Engineering Market Share#Tissue Engineering Market Growth#Market Research

0 notes

Text

Simulation Software Industry Size, Trends, and Business Outlook Report 2030

The global simulation software market size is estimated to reach USD 51.11 billion by 2030, registering a CAGR of 13.8% from 2024 to 2030, according to a new study by Grand View Research, Inc. Simulation software is being used for training personnel. It is replacing the traditional real-time training techniques, which incurred huge investments annually for companies. The use of simulation for training purposes helps reduce training costs as companies need to make a one-time investment for software implementation. The software also helps enterprises minimize production costs by enhancing the product development process.

The need for developing prototypes and the chances of product failure are considerably reduced through the use of simulators, as the product is virtually tested for all possible glitches before the commencement of production. Furthermore, simulation-based tools help product developers reduce the time spent on R&D processes as it enables them to obtain a realistic view of a product or process under study or review. Organizations across the globe are increasingly implementing the program and analyzing tools to enhance the entire product development cycle, reduce time to production, ensure delivery of high-quality products in minimal time, and reduce the overall cost to the company with respect to R&D.

Gather more insights about the market drivers, restrains and growth of the Global Simulation Software Market

It requires a skilled workforce or personnel with the required knowledge and understanding. This is leading to several manufacturers being reluctant to adopt this technology as the need for a skilled workforce incurs additional costs. The COVID-19 pandemic had an adverse impact on the global market. The closure of national and international borders in major countries, such as China, Japan, and India, has caused severe supply chain disruptions. In addition, the temporary shutdown of manufacturing operations has led manufacturing companies to face severe budgetary issues, resulting in delayed subscription renewal payments during the pandemic’s initial phase. However, recovering economies and opening businesses are expected to help the market grow at a rapid pace over the forecast period.

Simulation Software Market Report Highlights

The market is being driven by reduced training costs for personnel in various industries and sectors, such as automotive, defense, healthcare, and electrical

The service segment is expected to register a CAGR of 15.0% owing to the growing demand for customized simulation solutions, such as design and consulting

The cloud-based segment is expected to register the fastest CAGR of approximately 15.4% over the forecast period owing to benefits, such as easy and low-cost implementation

The automotive segment dominated the market in 2023 and is expected to hold a major share by 2030 owing to the early adoption of virtual testing tools in the automotive industry

North America is expected to account for the highest market share followed by Asia Pacific, by 2030 owing to the growing investments in R&D and defense in countries, such as the U.S.

Leading players are focusing on developing new simulation software solutions, to capture maximum share

Browse through Grand View Research's Next Generation Technologies Industry Research Reports.

Charging As A Service Market: The global charging as a service market size was estimated at USD 338.3 million in 2024 and is expected to grow at a CAGR of 25.0% from 2025 to 2030.

AI In Media & Entertainment Market: The global AI in media & entertainment market size was estimated at USD 25.98 billion in 2024 and is projected to grow at a CAGR of 24.2% from 2025 to 2030.

Simulation Software Market Segmentation

Grand View Research has segmented the global simulation software market on the basis of component, deployment, application, end-use, and region:

Simulation Software Component Outlook (Revenue, USD Million, 2017 - 2030)

Software

Services

Simulation Software Deployment Outlook (Revenue, USD Million, 2017 - 2030)

On-Premise

Cloud

Simulation Software Application Outlook (Revenue, USD Million, 2017 - 2030)

Engineering, Research, Modeling & Simulated Testing

High Fidelity Experiential 3D Training

Gaming & Immersive Experiences

Manufacturing Process Optimization

AI Training & Autonomous Systems

Planning And Logistics Management & Transportation

Cyber Simulation

Simulation Software End-use Outlook (Revenue, USD Million, 2017 - 2030)

Conventional Automotive

Electric Automotive and Autonomous Vehicles

Aerospace & Defense

Electrical, Electronics and Semiconductor

Healthcare

Robotics

Entertainment

Architectural Engineering and Construction

Others

Simulation Software Regional Outlook (Revenue, USD Million, 2017 - 2030)

North America

Europe

Asia Pacific

Latin America

Middle East & Africa (MEA)

Order a free sample PDF of the Simulation Software Market Intelligence Study, published by Grand View Research.

0 notes

Text

Understanding Artificial Intelligence Market: Trends and Growth Drivers

The global artificial intelligence market size is expected to reach USD 1,811.75 billion by 2030, according to a new report by Grand View Research, Inc. The market is anticipated to grow at a CAGR of 36.6% from 2024 to 2030. Artificial Intelligence (AI) denotes the concept and development of computing systems capable of performing tasks customarily requiring human assistance, such as decision-making, speech recognition, visual perception, and language translation. AI uses algorithms to understand human speech, visually recognize objects, and process information. These algorithms are used for data processing, calculation, and automated reasoning. Artificial intelligence researchers continuously improve algorithms for various aspects, as conventional algorithms have drawbacks regarding accuracy and efficiency.

These advancements have led manufacturers and technology developers to focus on developing standard algorithms. Recently, several developments have been carried out for enhancing artificial intelligence algorithms. For instance, in May 2020, International Business Machines Corporation announced a wide range of new AI-powered services and capabilities, namely IBM Watson AIOps, for enterprise automation. These services are designed to help automate the IT infrastructures and make them more resilient and cost reduction.

Gather more insights about the market drivers, restrains and growth of the Artificial Intelligence Market

Artificial Intelligence Market Report Highlights

• The advent of big data is expected to be the cause of the growth of the AI market as a large volume of data is needed to be captured, stored, and analyzed.

• The increasing demand for image processing and identification is expected to drive industry growth.

• AI can analyze vast amounts of data to identify patterns and anomalies that might indicate a cyberattack. This allows for faster and more precise threat detection subsequently fostering adoption of AI in cybersecurity applications.

• By using AI for predictive maintenance, process automation, and supply chain optimization, businesses can streamline workflows, reduce costs, and ensure smooth delivery of their offerings.

• North America dominated the market and accounted for a share of over 36.8% of global revenue in 2022.

• One of the significant concerns restraining industry growth is the need for a large amount of data to train AI systems for character and image recognition.

Browse through Grand View Research's Next Generation Technologies Industry Research Reports.

• The global cloud logistics market size was estimated at USD 21.55 billion in 2024 and is projected to grow at a CAGR of 13.9% from 2025 to 2030.

• The global AI in education market size was estimated at USD 5.88 billion in 2024 and is projected to grow at a CAGR of 31.2% from 2025 to 2030.

Artificial Intelligence Market Segmentation

Grand View Research has segmented the global artificial intelligence market based on solution, technology, function, end-use, and region:

Artificial Intelligence Solution Outlook (Revenue, USD Billion, 2017 - 2030)

• Hardware

o Accelerators

o Processors

o Memory

o Network

• Software

• Services

o Professional

o Managed

Artificial Intelligence Technology Outlook (Revenue, USD Billion, 2017 - 2030)

• Deep Learning

• Machine Learning

• Natural Language Processing (NLP)

• Machine Vision

• Generative AI

Artificial Intelligence Function Outlook (Revenue, USD Billion, 2017 - 2030)

• Cybersecurity

• Finance and Accounting

• Human Resource Management

• Legal and Compliance

• Operations

• Sales and Marketing

• Supply Chain Management

Artificial Intelligence End-use Outlook (Revenue, USD Billion, 2017 - 2030)

• Healthcare

o Robot Assisted Surgery

o Virtual Nursing Assistants

o Hospital Workflow Management

o Dosage Error Reduction

o Clinical Trial Participant Identifier

o Preliminary Diagnosis

o Automated Image Diagnosis

• BFSI

o Risk Assessment

o Financial Analysis/Research

o Investment/Portfolio Management

o Others

• Law

• Retail

• Advertising & Media

• Automotive & Transportation

• Agriculture

• Manufacturing

• Others

Artificial Intelligence Regional Outlook (Revenue, USD Billion, 2017 - 2030)

• North America

o U.S.

o Canada

• Europe

o U.K.

o Germany

o France

• Asia Pacific

o China

o Japan

o India

o South Korea

o Australia

• Latin America

o Brazil

o Mexico

• Middle East and Africa (MEA)

o KSA

o UAE

o South Africa

Order a free sample PDF of the Artificial Intelligence Market Intelligence Study, published by Grand View Research.

#Artificial Intelligence Market#Artificial Intelligence Market Analysis#Artificial Intelligence Market Size#Artificial Intelligence Market Share

0 notes

Text

Legionella Testing Market Analysis, Statistics, Segmentation, and Forecast to 2032

Legionella testing plays a vital role in ensuring water safety and preventing outbreaks of Legionnaires’ disease, a severe form of pneumonia caused by Legionella bacteria. These bacteria thrive in water systems, particularly in large, complex systems such as those found in hospitals, hotels, and industrial facilities. Early and accurate testing is essential for detecting contamination, enabling swift remedial action to protect public health.