#Gas Turbine Market analysis

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

The “We are the 99%” Tumblr blog became the slogan for the Occupy Wall Street movement.

Text

Gas Turbine Market Assessment and Future Growth Insights 2024 - 2032

The gas turbine market is a pivotal segment of the energy industry, playing a crucial role in power generation and various industrial applications. This article explores the current trends, drivers, challenges, and future outlook of the gas turbine market.

Introduction to Gas Turbines

Gas turbines are internal combustion engines that convert natural gas or other fuels into mechanical energy. They are widely used for electricity generation, aviation, and various industrial processes due to their efficiency and flexibility.

How Gas Turbines Work

Gas turbines operate on the Brayton cycle, where air is compressed, mixed with fuel, and ignited. The resulting high-pressure, high-temperature gas expands through a turbine, generating mechanical power. This mechanical energy can be used directly for propulsion or to drive electrical generators.

Market Overview

Current Market Size and Growth

The global gas turbine market has seen significant growth over the past few years. Factors such as increasing energy demand, technological advancements, and a shift towards cleaner energy sources have contributed to a robust market landscape.

Key Segments of the Market

By Product Type

Heavy-Duty Gas Turbines: Typically used in power plants and large-scale industrial applications.

Aero-Derivative Gas Turbines: More efficient and flexible, commonly used in power generation and marine applications.

By Application

Power Generation: Dominates the market as a primary application.

Oil & Gas: Used for pipeline compression and offshore applications.

Aviation: Critical in aircraft propulsion systems.

By Geography

North America: Leading region, driven by investments in renewable energy and aging power infrastructure.

Asia-Pacific: Fastest-growing market, supported by industrialization and urbanization.

Europe: Strong focus on cleaner technologies and energy efficiency.

Market Drivers

Growing Demand for Clean Energy

As the world shifts towards sustainable energy sources, gas turbines offer a cleaner alternative to coal and oil, producing lower emissions. This trend is bolstered by government policies promoting renewable energy and reducing carbon footprints.

Technological Advancements

Innovations in turbine design, materials, and manufacturing processes have significantly improved efficiency and performance. Combined-cycle gas turbines (CCGT) are particularly noteworthy for their ability to achieve higher efficiencies by using waste heat for additional power generation.

Infrastructure Development

Global infrastructure development, particularly in emerging economies, drives the demand for reliable and efficient power generation solutions. New power plants and industrial facilities are increasingly adopting gas turbine technology.

Challenges Facing the Market

High Initial Investment

The capital costs associated with gas turbine installation and maintenance can be substantial. This factor can deter potential buyers, especially in developing regions with limited access to financing.

Competition from Renewable Energy Sources

The rise of renewable energy technologies, such as solar and wind, poses a significant challenge. As costs for these alternatives continue to decrease, gas turbines must compete for market share.

Regulatory Hurdles

Stringent environmental regulations can complicate gas turbine operations. Compliance with emissions standards often requires additional investments in technology and infrastructure.

Future Outlook

Emerging Markets

The Asia-Pacific region is poised for rapid growth, driven by increasing energy demands and government initiatives promoting cleaner technologies. Countries like India and China are investing heavily in gas infrastructure.

Hybrid Systems

The integration of gas turbines with renewable energy sources is a promising trend. Hybrid systems that combine gas turbines with solar or wind power can enhance overall system efficiency and reliability.

Innovations in Hydrogen-Fueled Turbines

Research and development into hydrogen-fueled gas turbines are gaining momentum. As hydrogen becomes a more viable energy carrier, the potential for hydrogen to power gas turbines presents exciting opportunities for the market.

Conclusion

The gas turbine market is at a crossroads, balancing the need for efficient power generation with environmental considerations. While challenges remain, the continued push for cleaner energy solutions, technological advancements, and growth in emerging markets position gas turbines as a critical component of the global energy landscape. As the market evolves, stakeholders must remain agile to navigate the complexities and seize opportunities in this dynamic industry.

More Trending Reports

Heat Transfer Fluid Market

Solar PV Mounting Systems Market

Oilfield Services Market

Floating Solar Panels Market

0 notes

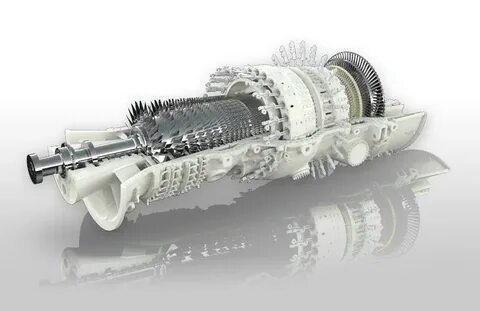

Text

Turbocharged Tomorrow: Dynamics and Trends in the Gas Turbine Industry

Global Gas Turbine Market size was valued at USD 20.28 Bn. in 2023 and the total Gas Turbine revenue is expected to grow by 3.6 % from 2024 to 2030, reaching nearly USD 25.98 Bn.

1 note

·

View note

Text

Common mistakes of Oil Sampling and how to avoid them?

Routine Oil sampling and analysis are crucial for a successful maintenance program. It provides important information to determine the condition of the equipment. Sampling is a vital procedure for collecting fluid from machinery for the purpose of oil analysis. The results and reports of oil analysis depend on the quality of the oil sample. Thus, oil sampling must be performed keeping some important goals in mind -

To MAXIMIZE the Data Density.

To MAXIMIZE Consistency.

To MAXIMIZE Relevance.

To MINIMIZE Data Disturbance.

There can be three ways of extracting samples from a component - drain port, drop-tube (in a vacuum pump), and a dedicated sampling point. A common mistake is taking an oil sample from the reservoir in circulating and hydraulic systems. Taking samples from the tank is not a best practice. If the sample is taken from the drain lines before emptying the tank, the concentration of wear metal would be much higher. Let’s discuss the common mistakes of oil sampling which can be avoided -

Some sampling methods are simply used for convenience, like inadequate flushing, using a vacuum pump (drop-tube sampling), usage of uncleaned bottles, etc. By following these bad practices, the quality of the sample taken is not apt and reliable.

If the samples are collected from the bottom of the tank and sumps, they may show higher concentrations of the sediments and water.

If the samples are consistently collected from the turbulent zones of reservoirs and tanks may not give reliable information.

Sometimes the sample is collected consistently from downstream of pressure-line or off-line. In this case, sampling accuracy is not given importance.

Samples collected from cold systems would not give correct information as the contaminants and other insoluble suspended particles would be settled when at rest.

Dead zone fluids like standpipe, regenerative loops, etc. give wrong results as they possess different properties than that working fluids.

Subscribe to our website blog for more technical articles and case studies: Click here

The International Organization for Standardization (ISO) has some defined codes which are mostly used as the primary reviewed piece of data. Being consistent is important with sampling. It is not advisable to use different sampling methods. Let’s discuss certain must-follow sampling rules for oil analysis -

Collect samples from running machines not from cold machines or stand-by machines. It is always advisable to start the machine and take the sample and the time of sample should be when the machine is at its peak of stress.

What, when, who, where, and how should be defined for oil sampling procedures as well, just like maintenance procedures are defined in detail. Changing the sampling methods or location is not advisable.

Use a specific sample point based on the type of lubricant, pressure, and the fluid required.

A sample must be taken in a bottle of the correct size and cleanliness. To get more information on bottle cleanliness, ISO 3722 can be referred to.

Oil sampling is like examining the condition of the system for that point in time. It is advisable not to wait for more than 24 hours to send the samples for oil analysis. This is because the health of the system may change in a very short period. Early detection would help in early remedy.

Maintain proper frequency of taking samples. Don’t do it whenever you feel like doing it. There should be an appropriate frequency so that important maintenance decisions could be taken on time.

One of the major problems in oil sampling is cross-contamination. Don’t use dirty sampling equipment. Flushing is the solution to this which is often overlooked and the selection of suitable clear media is equally important.

Though every system has a unique consideration of sampling, the above-mentioned tips can be applied and taken care of for your sampling techniques/methods. Start applying it Today!!

Connect with Minimac Experts to strategize your Oil Analysis plan: [email protected] or WhatsApp us at +91 70309 01267

#frf#oil flushing#minimac systems#power#minimac#oil & gas#hydraulic oil#lube oil filter#contamination#hydraulic oil filter#hydraulic oil cleaning#hydraulic oil cleaning#oil analysis#oil filteration#transformation oil purification#transformer oil cleaning#transformer oil filtration#oil dehydration systems#frf condition systems#oil purification machine#oil filtration system#coalescer separator#turbine oilanalysis maintenance lubrication reliability contaminationcontrol oil powerplants oilfiltration rotatingequipment mechanical bre#turbinemaintenance#gas turbine market trends#gaster#oil and gas

0 notes

Text

Hydrogen has a long way to go, according to a new report. (Heatmap AM)

“Hydrogen-ready” has become a popular moniker for utilities and developers constructing new natural gas plants in an era of climate concern. A new report by the Institute for Energy Economics and Financial Analysis suggests that the term — meant to convey the infrastructure’s capability to transition to carbon-free hydrogen when the fuel becomes more available — may be little more than hot air. It identifies three major barriers: a lack of hydrogen supply, a lack of hydrogen-capable pipelines, and a lack of storage capacity. The authors highlight Duke Energy’s plan to build a “hydrogen-ready” gas turbine at an existing coal plant in Roxboro, North Carolina — a plan that wouldn’t introduce hydrogen into the pipeline until 2035, and even then would start with a mix of just 1% hydrogen to 99% methane.

Claims of hydrogen readiness, the report concludes, are “little more than marketing designed to obscure the myriad shortcomings and unanswered questions associated with using hydrogen in methane-fired turbines.”

3 notes

·

View notes

Text

0 notes

Text

0 notes

Text

High Performance Alloys Market Competitive Landscape and Key Players

High Performance Alloys Market Growth Strategic Market Overview and Growth Projections

The global high-performance alloys market size was valued at USD 9.89 billion in 2022. It is projected to reach USD 15.89 billion by 2031, registering a CAGR of 5.41% during the forecast period (2023-2031).

The latest Global High Performance Alloys Market by straits research provides an in-depth analysis of the High Performance Alloys Market, including its future growth potential and key factors influencing its trajectory. This comprehensive report explores crucial elements driving market expansion, current challenges, competitive landscapes, and emerging opportunities. It delves into significant trends, competitive strategies, and the role of key industry players shaping the global High Performance Alloys Market. Additionally, it provides insight into the regulatory environment, market dynamics, and regional performance, offering a holistic view of the global market’s landscape through 2032.

Competitive Landscape

Some of the prominent key players operating in the High Performance Alloys Market are

Outokumpu

Hitachi Metals Ltd.

Alcoa Inc.

Aperam SA

VSMPO-Avisma Corporation

Timken Company

Carpenter Technology Corporation

Precision Castparts Corp.

RTI International Metals

ThyssenKrupp AG.

Get Free Request Sample Report @ https://straitsresearch.com/report/high-performance-alloys-market/request-sample

The High Performance Alloys Market Research report delivers comprehensive annual revenue forecasts alongside detailed analysis of sales growth within the market. These projections, developed by seasoned analysts, are grounded in a deep exploration of the latest industry trends. The forecasts offer valuable insights for investors, highlighting key growth opportunities and industry potential. Additionally, the report provides a concise dashboard overview of leading organizations, showcasing their effective marketing strategies, market share, and the most recent advancements in both historical and current market landscapes.Global High Performance Alloys Market: Segmentation

The High Performance Alloys Market segmentation divides the market into multiple sub-segments based on product type, application, and geographical region. This segmentation approach enables more precise regional and country-level forecasts, providing deeper insights into market dynamics and potential growth opportunities within each segment.

By Product

Non-Ferrous Metal

Platinum Group

Refractory

Super Alloys

By Material

Aluminum

Titanium

Magnesium

Nickel

Steel

Others

By Alloy Type

Wrought Alloy

Cast Alloy

By Applications

Aerospace

Industrial Gas Turbine

Industrial

Automotive

Oil and Gas

Electrical and Electronics

Others

Stay ahead of the competition with our in-depth analysis of the market trends!

Buy Now @ https://straitsresearch.com/buy-now/high-performance-alloys-market

Market Highlights:

A company's revenue and the applications market are used by market analysts, data analysts, and others in connected industries to assess product values and regional markets.

But not limited to: reports from corporations, international Organization, and governments; market surveys; relevant industry news.

Examining historical market patterns, making predictions for the year 2022, as well as looking forward to 2032, using CAGRs (compound annual growth rates)

Historical and anticipated data on demand, application, pricing, and market share by country are all included in the study, which focuses on major markets such the United States, Europe, and China.

Apart from that, it sheds light on the primary market forces at work as well as the obstacles, opportunities, and threats that suppliers face. In addition, the worldwide market's leading players are profiled, together with their respective market shares.

Goals of the Study

What is the overall size and scope of the High Performance Alloys Market market?

What are the key trends currently influencing the market landscape?

Who are the primary competitors operating within the High Performance Alloys Market market?

What are the potential growth opportunities for companies in this market?

What are the major challenges or obstacles the market is currently facing?

What demographic segments are primarily targeted in the High Performance Alloys Market market?

What are the prevailing consumer preferences and behaviors within this market?

What are the key market segments, and how do they contribute to the overall market share?

What are the future growth projections for the High Performance Alloys Market market over the next several years?

How do regulatory and legal frameworks influence the market?

About Straits Research

Straits Research is dedicated to providing businesses with the highest quality market research services. With a team of experienced researchers and analysts, we strive to deliver insightful and actionable data that helps our clients make informed decisions about their industry and market. Our customized approach allows us to tailor our research to each client's specific needs and goals, ensuring that they receive the most relevant and valuable insights.

Contact Us

Email: [email protected]

Tel: UK: +44 203 695 0070, USA: +1 646 905 0080

0 notes

Text

Ultrasonic Flowmeters Market Growth: Factors and Forecasts

The ultrasonic flowmeters market is undergoing significant expansion, fueled by increasing demand for accurate and non-invasive flow measurement solutions across diverse industries. These devices, which use ultrasonic sound waves to measure the velocity of fluids, offer precise measurements without requiring invasive installations, making them indispensable in modern industrial applications. From oil and gas to water management, ultrasonic flowmeters are becoming integral to efficient operations, driving their market growth globally.

Key Drivers of Market Expansion

Demand for Accurate Flow Measurement Ultrasonic flowmeters are highly accurate, making them ideal for industries where precision is critical, such as oil and gas, pharmaceuticals, and food processing. The ability to measure flow without direct contact with the fluid minimizes contamination risks, enhancing their appeal in hygiene-sensitive sectors.

Rising Environmental Concerns As industries face stricter environmental regulations, the need for accurate monitoring of fluid usage and emissions has grown. Ultrasonic flowmeters assist in ensuring regulatory compliance, particularly in water and wastewater management, by providing reliable flow data and aiding resource conservation.

Advancements in Technology Innovations such as multi-path ultrasonic flowmeters, which enhance accuracy by measuring flow at multiple points, are propelling the market forward. Integration with IoT and real-time monitoring capabilities is also driving demand, enabling industries to adopt smarter, data-driven solutions.

Expanding Applications Across Industries Ultrasonic flowmeters are now being used in an array of industries, including power generation, HVAC, and chemical processing. Their ability to handle various fluids, including liquids, gases, and steam, makes them versatile and suitable for complex industrial processes.

Regional Market Insights

The market expansion of ultrasonic flowmeters is noticeable across multiple regions, with significant contributions from:

North America: The region’s established infrastructure, coupled with investments in oil and gas and water management projects, is driving growth.

Asia-Pacific: Rapid industrialization and urbanization in countries like China and India are fueling the adoption of ultrasonic flowmeters, particularly in the water and wastewater management sector.

Europe: Stringent environmental regulations and a focus on sustainability are encouraging the use of advanced flow measurement technologies.

Middle East and Africa: The oil and gas industry in this region relies heavily on ultrasonic flowmeters for pipeline monitoring and leak detection.

Challenges to Market Growth

Despite the positive outlook, the ultrasonic flowmeters market faces challenges, including:

High Initial Costs: The advanced technology and precision of ultrasonic flowmeters make them more expensive than traditional alternatives, which can be a barrier for smaller enterprises.

Technical Complexity: Proper installation and calibration of ultrasonic flowmeters require skilled personnel, potentially limiting their adoption in less-developed regions.

Competition from Alternative Technologies: Electromagnetic and turbine flowmeters are well-established competitors, offering specific advantages in certain applications.

Future Opportunities

The future of the ultrasonic flowmeters market lies in continued innovation and diversification of applications. Emerging opportunities include:

Smart Infrastructure Development With the rise of smart cities and connected infrastructure, ultrasonic flowmeters integrated with IoT will play a crucial role in enabling real-time data collection and analysis for efficient resource management.

Renewable Energy Sector The growing focus on renewable energy sources such as biofuels and hydrogen provides new avenues for ultrasonic flowmeter applications in monitoring and managing fluid dynamics in clean energy systems.

Customization and Industry-Specific Solutions Manufacturers are focusing on developing customized ultrasonic flowmeters tailored to specific industry needs, such as high-temperature applications in power plants or corrosion-resistant models for chemical processing.

Market Trends and Insights

Key trends shaping the market include the growing preference for clamp-on flowmeters due to their ease of installation and minimal maintenance requirements. Additionally, the demand for portable ultrasonic flowmeters is increasing, as they offer flexibility for temporary installations and field operations.

Conclusion

The ultrasonic flowmeters market is poised for robust growth, driven by advancements in technology, expanding industrial applications, and the need for precise and non-invasive flow measurement solutions. While challenges such as high costs and competition persist, the integration of IoT and smart technologies is unlocking new opportunities for market expansion. As industries continue to prioritize efficiency and sustainability, ultrasonic flowmeters are set to play a pivotal role in shaping the future of fluid measurement and management.

0 notes

Text

Geothermal Energy Market: Role in Base Load Power and Energy Security

The Geothermal Energy Market size was valued at USD 7.62 billion in 2023 and is expected to grow to USD 12.15 billion by 2031 and grow at a CAGR of 5.97% over the forecast period of 2024–2031.

Market Overview

Geothermal energy is a renewable power source generated from the natural heat of the Earth’s core. Unlike other renewables like wind or solar, geothermal energy provides a continuous energy output unaffected by weather or daylight, making it a reliable and sustainable energy choice. This consistent availability has led to increased adoption across residential heating and cooling, as well as large-scale power generation for industrial and commercial applications.

The market’s growth is bolstered by government policies supporting renewable energy integration, carbon reduction targets, and technological advances that increase the efficiency and scalability of geothermal systems. Innovations in high- and low-temperature geothermal technologies, such as binary cycle plants and ground source heat pumps, have broadened the use of geothermal energy in various temperature conditions and applications.

Key Market Drivers

Reliability and Consistency: Unlike solar or wind, geothermal energy offers continuous energy generation, providing stability to power grids.

Environmental and Economic Benefits: Geothermal energy has a low carbon footprint, supporting global efforts to reduce greenhouse gas emissions and meet climate targets.

Technological Advancements: Enhanced geothermal systems, ground source heat pumps, and improved binary cycle plants have expanded geothermal applications.

Government Support and Policy Incentives: Policies promoting renewable energy sources and financial incentives are encouraging geothermal energy adoption across sectors.

Increasing Demand in Heating and Cooling: Geothermal heat pumps provide cost-effective, eco-friendly solutions for residential and commercial heating and cooling needs.

Market Segmentation

The geothermal energy market is segmented by technology, temperature, application, and region.

By Technology

Dry Steam Plants: These plants directly utilize geothermal steam for electricity generation, making them highly efficient in high-temperature conditions.

Flash Steam Plants: Flash steam plants operate by converting hot water from geothermal reservoirs into steam to power turbines, widely used in high- and medium-temperature regions.

Binary Cycle Plants: Binary plants use lower-temperature water to produce electricity by transferring heat to a secondary fluid with a lower boiling point, suitable for moderate temperature ranges.

Direct Systems: Direct use of geothermal energy, often applied in residential and commercial heating and industrial processes.

Ground Source Heat Pumps (GSHPs): Widely used in residential heating and cooling, GSHPs efficiently transfer heat between the ground and buildings.

Others: Includes emerging technologies and hybrid geothermal solutions tailored for specific geographic and industrial needs.

By Temperature

High Temperature: Geothermal systems operating at temperatures above 150°C, ideal for electricity generation in dry steam and flash steam plants.

Medium Temperature: Temperatures between 90°C and 150°C, utilized in binary cycle plants and some flash steam applications.

Low Temperature: Below 90°C, typically used in direct systems and ground source heat pumps for heating, cooling, and other non-electrical applications.

By Application

Residential: Ground source heat pumps (GSHPs) are popular for residential heating and cooling, offering cost-effective and sustainable temperature regulation.

Industrial: Industrial applications, including drying processes and direct-use applications, benefit from geothermal’s consistent energy supply.

Commercial: Commercial buildings use geothermal energy for heating, cooling, and electricity generation, enhancing operational sustainability.

Regional Analysis

North America: The United States leads geothermal energy development, particularly in California, Nevada, and Hawaii, where high-temperature geothermal resources are abundant. Supportive policies, including tax credits and renewable energy standards, are key drivers.

Europe: Countries like Iceland, Italy, and Turkey are pioneers in geothermal energy, with Iceland deriving over 85% of its energy from geothermal sources. The European Union’s stringent carbon reduction goals also fuel geothermal adoption.

Asia-Pacific: Asia-Pacific is a rapidly growing region in geothermal energy adoption, with notable installations in the Philippines, Indonesia, and Japan. These countries leverage geothermal resources to meet rising electricity demand while reducing carbon emissions.

Latin America: Latin America has untapped geothermal potential, particularly in Mexico and Central American countries. Geothermal projects in these regions are gaining traction as governments invest in renewable energy infrastructure.

Middle East & Africa: While geothermal energy is still nascent in this region, countries with volcanic activity, such as Kenya, are exploring geothermal energy as a sustainable power source to diversify energy portfolios.

Current Market Trends

Advances in Enhanced Geothermal Systems (EGS): EGS technology is expanding geothermal potential by allowing energy extraction from previously inaccessible geothermal sources.

Hybrid Geothermal Systems: Integrating geothermal with solar or wind energy systems for optimized renewable power solutions.

Increased Investment in GSHPs: With growing adoption in residential and commercial sectors, ground source heat pumps (GSHPs) are becoming a popular choice for energy-efficient heating and cooling.

Geothermal in Carbon Reduction Initiatives: Geothermal energy is increasingly recognized for its role in helping countries achieve net-zero emissions by offering a low-carbon alternative to fossil fuels.

Development in Low-Temperature Applications: Technological advancements are enabling the use of geothermal energy in low-temperature applications, expanding geothermal’s reach into new markets.

Conclusion

The global geothermal energy market is set to grow substantially as the world shifts towards renewable energy sources that provide consistent and reliable power. With continuous technological innovation and supportive government policies, geothermal energy is positioned to become a key component of sustainable energy solutions, delivering clean energy across residential, industrial, and commercial sectors.

Read Complete Report Details of Geothermal Energy Market: https://www.snsinsider.com/reports/geothermal-energy-market-2908

About Us:

SNS Insider is a global leader in market research and consulting, shaping the future of the industry. Our mission is to empower clients with the insights they need to thrive in dynamic environments. Utilizing advanced methodologies such as surveys, video interviews, and focus groups, we provide up-to-date, accurate market intelligence and consumer insights, ensuring you make confident, informed decisions.

Contact Us: Akash Anand — Head of Business Development & Strategy [email protected] Phone: +1–415–230–0044 (US) | +91–7798602273 (IND)

0 notes

Text

Niobium Market: A Vital Component for Modern Industries (2023–2030)

The global Niobium Market, a versatile transition metal, is increasingly becoming a cornerstone in industries ranging from construction and automotive to energy and aerospace. With growing demand for high-strength materials and advancements in metallurgical applications, the Niobium market is poised for robust growth in the coming years. This blog explores the key drivers, trends, and insights shaping the global niobium industry.

What is Niobium?

Niobium (Nb) is a ductile, corrosion-resistant metal widely used to enhance the properties of steel alloys. By adding niobium to steel, manufacturers achieve greater strength, flexibility, and durability, making it an essential component in modern infrastructure and technological applications.

Niobium’s applications include:

High-strength low-alloy (HSLA) steels used in bridges, buildings, and pipelines.

Automotive steels for lightweight, fuel-efficient vehicles.

Superalloys for aerospace components and energy systems.

Market Overview: A Growing Opportunity

The Niobium market is on a growth trajectory, driven by increasing demand across construction, transportation, and energy sectors. Below is a snapshot of its current and projected state:

Market Size in 2023: $78.90 Billion

Projected Market Size in 2024: $83.00 Billion

Projected Market Size in 2030: $124.70 Billion

CAGR Growth Rate (2024–2030): 9.92%

With a compound annual growth rate (CAGR) of 9.92%, the market reflects the rising significance of niobium in developing sustainable, high-performance materials.

Market Dynamics: Drivers and Challenges

Key Drivers of Growth

Rising Demand for High-Strength Steels Niobium is a crucial alloying element in the production of high-strength steels used in infrastructure, automotive, and energy projects. The global push for durable and sustainable construction materials is a significant driver.

Lightweight Automotive Solutions The automotive industry increasingly relies on niobium-enhanced steels to produce lightweight, fuel-efficient vehicles, aligning with global emissions reduction goals.

Pipeline Infrastructure Development Niobium’s ability to improve pipeline steel toughness and resistance to extreme conditions makes it essential for expanding oil and gas infrastructure.

Advancements in Aerospace and Energy Sectors Niobium-based superalloys are critical for manufacturing jet engines, turbines, and other high-performance components, driving demand in aerospace and energy industries.

Sustainability Initiatives Niobium alloys contribute to energy efficiency and reduce CO₂ emissions, making them a preferred choice in industries focused on sustainability.

Challenges

Limited Supply Sources Niobium is mined primarily in Brazil and Canada, making its supply chain vulnerable to geopolitical and logistical disruptions.

High Production Costs Extracting and processing niobium require specialized technologies and significant investment, which can limit its adoption in cost-sensitive markets.

Competition from Alternatives Other alloying elements, such as vanadium and titanium, compete with niobium in certain applications, potentially affecting market growth.

Segmentation Analysis

By Type

Ferroniobium The most commonly used niobium product, ferroniobium is a key additive in steel manufacturing, enhancing strength and durability.

Niobium Oxide Used in electronics, optics, and catalysts, niobium oxide is valued for its thermal and chemical stability.

Niobium Metal Employed in high-performance alloys for aerospace, energy, and medical applications, niobium metal is prized for its exceptional properties.

By Application

Structural Steels Niobium is essential for producing structural steels used in bridges, skyscrapers, and other infrastructure projects.

Automotive Steel Lightweight, niobium-enhanced automotive steels contribute to better fuel efficiency and safety.

Pipeline Steels Niobium strengthens pipeline steels, ensuring they withstand high pressures and harsh environments.

Stainless Steels Adding niobium to stainless steel enhances its corrosion resistance and mechanical properties.

Other Applications Niobium finds use in superalloys, medical devices, and emerging technologies like quantum computing.

Regional Insights

The Niobium market exhibits diverse growth patterns across regions:

North America A mature market driven by investments in aerospace, energy, and construction. The U.S. remains a key consumer of niobium products.

Europe Strong demand for sustainable materials in automotive and infrastructure sectors positions Europe as a significant market for niobium.

Asia Pacific Rapid urbanization, infrastructure development, and a growing automotive industry make Asia Pacific the fastest-growing region for niobium.

Latin America Brazil, as the largest producer of niobium, dominates the regional market, with exports catering to global demand.

Middle East & Africa Infrastructure expansion and oil and gas projects drive moderate growth in this region.

Key Market Players

The global niobium market is led by a few dominant players:

CMBB (Companhia Brasileira de Metalurgia e Mineração): The world’s largest producer of niobium, headquartered in Brazil.

Niobec: A significant producer based in Canada, focusing on high-quality niobium products.

Anglo American: A diversified mining company with interests in niobium production and related products.

These companies invest heavily in R&D to enhance niobium extraction and processing technologies, ensuring supply meets rising demand.

Future Trends

Increased Adoption in Renewable Energy Niobium’s role in wind turbines and solar panels is expected to grow as the renewable energy sector expands.

Development of Quantum Technologies Niobium’s superconducting properties make it a key material for emerging quantum computing applications.

Expansion in Emerging Markets Infrastructure projects in Asia, Africa, and Latin America are likely to drive demand for niobium-enhanced steels.

Focus on Recycling Sustainable practices, including niobium recycling, are gaining attention to address supply chain challenges and reduce environmental impact.

Innovations in Metallurgy Ongoing research aims to develop advanced niobium alloys with enhanced performance for specialized applications.

Conclusion

The Niobium market is on a dynamic growth path, projected to reach $124.70 billion by 2030, up from $78.90 billion in 2023. With a CAGR of 9.92%, niobium’s critical role in infrastructure, automotive, aerospace, and energy sectors underscores its significance in modern industries.

As sustainability, lightweighting, and high-performance materials become more vital, niobium’s versatility ensures it remains a sought-after commodity. With ongoing innovations and regional expansions, the future of niobium is bright, presenting opportunities for manufacturers, investors, and industries worldwide.

Browse More:

Prashant Kishor's 'Jan Suraj Party' debut, Bihar's call for 'voice to reach Delhi'

0 notes

Text

Global Nickel-Based Superalloys Market Analysis 2024: Size Forecast and Growth Prospects

The nickel-based superalloys global market report 2024 from The Business Research Company provides comprehensive market statistics, including global market size, regional shares, competitor market share, detailed segments, trends, and opportunities. This report offers an in-depth analysis of current and future industry scenarios, delivering a complete perspective for thriving in the industrial automation software market.

Nickel-Based Superalloys Market, 2024 report by The Business Research Company offers comprehensive insights into the current state of the market and highlights future growth opportunities.

Market Size - The nickel-based superalloys market size has grown strongly in recent years. It will grow from $8.06 billion in 2023 to $8.79 billion in 2024 at a compound annual growth rate (CAGR) of 9.1%. The growth in the historic period can be attributed to a rise in the automotive industry, increasing demand for electric vehicles, increased aviation fuel efficiency, increasing demand for lngot metallurgy in various industries, and increasing fuel economy and performance.

The nickel-based superalloys market size is expected to see strong growth in the next few years. It will grow to $12.65 billion in 2028 at a compound annual growth rate (CAGR) of 9.5%. The growth in the forecast period can be attributed to growing demand from aerospace for lightweight alloys, growing focus on renewable energy, growing need for high-performance materials, growing use of gas turbines in the power generation industry, and growing need for sophisticated materials. Major trends in the forecast period include technological advancements, advancements in 3D printing for complex superalloy components, the development of complicated geometries, the development of next-generation aircarft, and advancements in alloy design.

Order your report now for swift delivery @ https://www.thebusinessresearchcompany.com/report/nickel-based-superalloys-global-market-report

Scope Of Nickel-Based Superalloys Market The Business Research Company's reports encompass a wide range of information, including:

1. Market Size (Historic and Forecast): Analysis of the market's historical performance and projections for future growth.

2. Drivers: Examination of the key factors propelling market growth.

3. Trends: Identification of emerging trends and patterns shaping the market landscape.

4. Key Segments: Breakdown of the market into its primary segments and their respective performance.

5. Focus Regions and Geographies: Insight into the most critical regions and geographical areas influencing the market.

6. Macro Economic Factors: Assessment of broader economic elements impacting the market.

Nickel-Based Superalloys Market Overview

Market Drivers - The expansion of the aerospace industry is expected to propel the growth of the nickel-based superalloy markets going forward. The aerospace industry refers to businesses involved in designing, developing, producing, and maintaining aircraft, spacecraft, and related systems and equipment. The demand for the aerospace industry is rising due to increasing global air travel, driven by expanding middle-class populations and the push for next-generation fuel-efficient aircraft to meet stricter environmental regulations. Nickel-based superalloys are essential in the aerospace industry due to their exceptional properties, enabling high performance in extreme environments. For instance, in September 2023, according to the Aerospace Industries Association (AIA), a US-based trade association representing manufacturers and suppliers of civil, military, and business aircraft, in 2022, the American aerospace and defense industry saw a 6.7% increase in sales, reaching over $952 billion compared to 2021. Therefore, the expansion of the aerospace and power industries is driving the growth of the nickel-based superalloys market.

Market Trends - Major companies operating in the nickel-based superalloy market are focusing on developing technologically advanced solutions, such as nickel ultra-high-temperature superalloy, to meet the growing demand for enhanced performance in critical applications like aerospace and power generation. Nickel ultrahigh-temperature superalloys are advanced materials that withstand extreme temperatures and harsh environments. For instance, in July 2024, Alloyed and Aubert & Duval, a France-based metallurgical company, launched a new nickel superalloy named ABD-1000AM, specifically designed for additive manufacturing and capable of withstanding temperatures exceeding 1000°C in its age-hardened state. This ultra-high-temperature alloy boasts a relative density greater than 99.9%, a significant gamma prime phase fraction of 55%, and comparable stress rupture life to the cast alloy Ni247LC. The development utilized Alloyed's Alloys-by-Design platform, with Aubert & Duval providing the necessary powder feedstock.

The nickel-based superalloys market covered in this report is segmented –

1) By Type: Nickel-Copper, Nickel-Chromium, Nickel-Molybdenum, Other Types 2) By Form: Cast, Wrought 3) By Base Element: Cobalt, Rhenium, Tantalum, Tungsten 4) By Distribution Channel: Direct Sales, Distributors And Traders 5) By End-Use Industry: Aerospace, Electronics, Industrial, Automotive, Oil And Gas, Other End Use Industries

Get an inside scoop of the nickel-based superalloys market, Request now for Sample Report @ https://www.thebusinessresearchcompany.com/sample.aspx?id=19125&type=smp

Regional Insights - Asia-Pacific was the largest region in the nickel-based superalloys market in 2023. The regions covered in the nickel-based superalloys market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East, Africa.

Key Companies - Major companies operating in the nickel-based superalloys market are CMK Corporation, BaoSteel, Thyssenkrupp Aerospace, Sandvik Materials Technology, Outokumpu Oyj., Aperam S.A., Fushun Special Steel Co Ltd., Precision Castparts Corp., Howmet Aerospace Inc., Walsin Lihwa Corporation, Eramet S.A., Allegheny Technologies Incorporated, Beijing Cisri-Gaona Materials and Technology Co Ltd., Carpenter Technology Corporation, AMG Advanced Metallurgical Group, Nippon Yakin Kogyo Co Ltd., VSMPO-AVISMA Corporation, Special Metals Corporation, Haynes International Inc., Doncasters Group, Smiths Metal Centres Limited, AEETHER Inc., Mishra Dhatu Nigam Limited, Rosswag GmbH, QuesTek Innovations

Table of Contents 1. Executive Summary 2. Nickel-Based Superalloys Market Report Structure 3. Nickel-Based Superalloys Market Trends And Strategies 4. Nickel-Based Superalloys Market – Macro Economic Scenario 5. Nickel-Based Superalloys Market Size And Growth ….. 27. Nickel-Based Superalloys Market Competitor Landscape And Company Profiles 28. Key Mergers And Acquisitions 29. Future Outlook and Potential Analysis 30. Appendix

Contact Us: The Business Research Company Europe: +44 207 1930 708 Asia: +91 88972 63534 Americas: +1 315 623 0293 Email: [email protected]

Follow Us On: LinkedIn: https://in.linkedin.com/company/the-business-research-company Twitter: https://twitter.com/tbrc_info Facebook: https://www.facebook.com/TheBusinessResearchCompany YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ Blog: https://blog.tbrc.info/ Healthcare Blog: https://healthcareresearchreports.com/ Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model

0 notes

Text

0 notes

Text

From Turbine to Eco-Friendly: The Race to Sustainable Aviation Fuel

The global aviation fuel market is on a steady growth trajectory, driven by rising air traffic, increased commercial aircraft operations, and advancements in fuel efficiency. According to the report, the aviation fuel market was valued at approximately USD 225 billion in 2022 and is projected to reach nearly USD 340 billion by 2028, expanding at a CAGR of around 7% over the forecast period of 2022 to 2028.

What is Aviation Fuel?

Aviation fuel refers to specialized types of petroleum-based fuel used to power aircraft. There are two main types: Jet-A and Jet-A1 for commercial and military aircraft, and Avgas for smaller piston-engine aircraft. In recent years, there has been a growing focus on sustainable aviation fuel (SAF), which incorporates biofuels and other renewable sources to reduce emissions and enhance environmental sustainability.

Get Sample pages of Report: https://www.infiniumglobalresearch.com/reports/sample-request/42542

Market Dynamics and Growth Drivers

Several factors contribute to the projected growth of the global aviation fuel market:

Rise in Air Travel and Tourism: As global tourism recovers and passenger volumes increase, particularly in emerging economies, the demand for aviation fuel is expected to grow accordingly.

Expansion of Commercial and Cargo Fleets: The rise of e-commerce and increased demand for air freight have contributed to a surge in cargo flights, boosting the demand for aviation fuel. Additionally, many airlines are expanding their fleets and adding routes to meet rising demand, further stimulating fuel consumption.

Development of Sustainable Aviation Fuel (SAF): In response to environmental concerns, there has been a shift toward sustainable fuel options, including SAF. Although SAF currently represents a small fraction of total fuel consumption, its adoption is expected to grow as regulatory support and investments increase.

Fuel Efficiency Innovations: Airlines are adopting more fuel-efficient aircraft and engines to reduce costs and minimize environmental impact. Although this trend may slightly limit overall fuel demand growth, it fosters technological innovation within the aviation fuel market.

Regional Analysis

North America: North America is a leading consumer of aviation fuel, driven by the high volume of both commercial and private flights. The region is also at the forefront of SAF initiatives and regulatory support for lower emissions, influencing the adoption of alternative fuels.

Europe: Europe is witnessing robust growth in aviation fuel demand, spurred by a surge in intra-regional travel and regulatory measures promoting the use of SAF to meet the EU’s climate targets.

Asia-Pacific: Asia-Pacific is expected to experience the highest growth in aviation fuel consumption, propelled by expanding middle-class populations, rising disposable incomes, and increased air travel demand. Major aviation hubs in China, India, and Southeast Asia are experiencing a boom in both domestic and international flights.

Middle East and Africa: With a focus on long-haul flights, the Middle East has significant demand for aviation fuel, driven by key players like Emirates, Qatar Airways, and Etihad. Meanwhile, Africa is experiencing growth, though at a more moderate pace, as infrastructure and air travel access continue to develop.

Competitive Landscape

The aviation fuel market is competitive, with a mix of established oil and gas giants, fuel suppliers, and new entrants focusing on SAF. Key players include:

ExxonMobil: As a major global fuel supplier, ExxonMobil is involved in producing traditional aviation fuel and is investing in SAF initiatives to align with global sustainability goals.

Royal Dutch Shell: Shell is a leading supplier of aviation fuel and has dedicated significant resources to SAF development, aiming to reduce carbon emissions in the aviation sector.

Chevron Corporation: Chevron supplies aviation fuel worldwide and is focused on expanding its SAF capabilities, partnering with airlines to promote cleaner fuel options.

TotalEnergies: This French multinational has committed to sustainable fuel solutions and operates several SAF production facilities, partnering with airlines to drive SAF adoption.

Report Overview : https://www.infiniumglobalresearch.com/reports/global-aviation-fuel-market

Challenges and Opportunities

The aviation fuel market faces several challenges, including fluctuating crude oil prices, geopolitical tensions, and environmental pressures. However, these challenges are balanced by promising opportunities:

SAF Development and Adoption: As regulations around emissions intensify, SAF represents a viable solution to reduce the aviation industry’s carbon footprint. Increased investments and advancements in SAF technologies are expected to drive market growth.

Increased Investments in Fuel Efficiency: Airlines and manufacturers are constantly working to improve fuel efficiency, which could slow traditional fuel demand but also encourage the adoption of innovative solutions, including SAF and advanced jet fuel formulations.

Conclusion

The global aviation fuel market is anticipated to grow from USD 225 billion in 2022 to nearly USD 340 billion by 2028, at a CAGR of approximately 7%. While conventional aviation fuel will continue to dominate, SAF and other eco-friendly alternatives are gaining traction due to environmental and regulatory pressures. As air travel continues to recover and expand globally, the aviation fuel market is expected to see sustained growth through advancements in sustainable fuel solutions and infrastructure expansion.Bottom of Form

Discover More of Our Reports

Aeroponics Farming Market

0 notes

Text

0 notes

Text

Heat Recovery Steam Generator Products: Analyzing Current Market Dynamics, Size, Share, Growth Trends

The global heat recovery steam generator market size is expected to reach USD 1817.0 million by 2030, expanding at a CAGR of 4.5%, according to a new report by Grand View Research, Inc. Shifting preference from simple cycle power plants to combined cycle power plants, with increase in adoption of energy-efficiency measures is anticipated to drive the market for heat recovery steam generator (HRSG) during the forecast period.

In past couple of years, various countries across the globe faced power shortage issues and to counter such issues, regulatory bodies have been stressing the need for advanced infrastructure for power generation. As a result, increasing number of power plants to compensate for the energy deficit is likely to be commissioned and this is expected to propel the demand for heat recovery steam generators (HRSGs).

The increasing demand for HRSGs to product clean and green energy in the various industries has enhanced the growth of the market. Furthermore, ongoing research and technological advancements in the field of HRSG is driving the market for heat recovery steam generator in North America. Enlarged demand for HRSGs for the production of effective and clean energy is stimulating the market for heat recovery steam generator in China, India, and other developing countries in Asia.

Heat Recovery Steam Generator Market Report Highlights

The up to 30 MW segment accounted for 24.5% of the market share in 2023. HRSGs with power levels up to 30 MWs cater to smaller-scale power applications and are increasingly important in niche markets.

The utilities segment held a 48.7% market share in 2023. In the utilities industry, HRSGs are crucial for improving the efficiency of power generation facilities, particularly in combined cycle power plants.

The combined cycle segment accounted for 44.0% of the market share in 2023. In this case, power plants use both steam and gas turbines to generate electricity more efficiently.

In the Asia Pacific region, the HRSG market is experiencing robust growth due to rapid industrialization, urban expansion, and increasing energy consumption.

For More Details or Sample Copy please visit link @: Heat Recovery Steam Generator Market Report

The below 100 MW segment accounted for largest revenue share in 2019 in the market for HRSG due to wide application in small to medium industries such as chemical, refining, pharmaceuticals, paper, pulp, cement, and sugar. Furthermore, implementation of numerous climate change policies as well as regulations to restrict GHG emissions are expected to lead to an increase in the potential for these generators over the forecast period.

Even though Asia Pacific is likely to account for the largest market share over the forecast period, North America is expected to maintain its position as the largest supplier of HRSG, followed by Europe. Both North America and Europe are anticipated to become mature markets for HRSG. Major market players located in these regions are likely to expand their geographical presence by undertaking turnkey projects and by collaborating with foreign governments to commission new projects.

List Of major companies in the Heat Recovery Steam Generator Market

MITSUBISHI HEAVY INDUSTRIES, LTD.

Thermax Limited.

GE Vernova and/or its affiliates.

Bharat Heavy Electricals Limited

LARSEN & TOUBRO LIMITED.

Isgec Heavy Engineering Ltd.

Kawasaki Heavy Industries, Ltd.

Siemens Heat Transfer Technology (Siemens)

John Cockerill.

BHI Co., Ltd.

Alstom SA

Rentech Boiler Systems, Inc.

For Customized reports or Special Pricing please visit @: Heat Recovery Steam Generator Market Analysis Report

We have segmented the global heat recovery steam generator market on the design, mode of operation, power, end-use, and region.

#HeatRecoverySteamGenerator#SteamGenerator#WasteHeatRecovery#PowerGeneration#EnergyEfficiency#ThermalEnergy#CombinedCyclePowerPlant#Cogeneration#EnergyRecovery#EnergySolutions#EnvironmentalSustainability#EnergyMarket

0 notes

Text

Machine Condition Monitoring Market Size & Forecast Report, 2030

The global machine condition monitoring market was valued at USD 3.49 billion in 2024 and is expected to grow at a compound annual growth rate (CAGR) of 7.6% from 2025 to 2030. This growth is primarily driven by the need for advanced diagnostic tools to assess equipment health and predict maintenance needs effectively. Manufacturers increasingly rely on condition monitoring systems to enhance equipment performance and maintenance, which helps to optimize productivity and reduce the risk of unexpected breakdowns. In addition, the shift toward lean manufacturing has motivated manufacturers to adopt condition monitoring systems to improve production efficiency, reduce downtime, and streamline inventory management for spare parts.

Businesses are showing increased interest in condition monitoring as it enhances productivity, extends equipment lifespan, and minimizes scrap parts by reducing downtime. With real-time data on machine conditions, companies can leverage automation and make data-driven maintenance decisions. A notable development in this space is eNETDNC’s integration of Microsoft Power BI Desktop with its machine monitoring software in February 2024. This integration allows users to create customizable, real-time reports and dashboards, helping customers optimize processes through interactive visualization of key performance indicators, machine status, and production trends.

Gather more insights about the market drivers, restrains and growth of the Machine Condition Monitoring Market

Machine condition monitoring involves measuring various parameters of equipment to prevent breakdowns by identifying changes that could indicate potential faults. This approach is widely adopted across industries such as oil & gas, automotive, power generation, metals & mining, marine, and aerospace. Condition monitoring has become central to predictive maintenance, which improves asset longevity, enhances cost savings, ensures operator safety, and streamlines industrial processes. The prevalence of the Internet of Things (IoT) has introduced a new dimension to machine condition monitoring, enabling real-time communication between devices. As a result, industries can now make more informed decisions and improve diagnostic precision.

As industries prioritize operational efficiency, they are increasingly adopting advanced machine condition monitoring technologies, including artificial intelligence (AI) and machine learning (ML). These technologies enable predictive maintenance by analyzing historical data to recognize patterns and anticipate failures before they occur. Additionally, integrating cloud computing offers centralized data storage and analysis capabilities, allowing for real-time monitoring and remote access to equipment performance data. This shift in technology supports better decision-making, proactive maintenance, and ultimately reduces downtime and maintenance expenses, while boosting productivity and equipment reliability.

Application Segmentation Insights:

The turbines & generators segment held the largest revenue share in 2024. This growth is mainly attributed to the power generation industry's need for preventive maintenance. Turbines and generators are crucial components in power plants, and machine condition monitoring allows early identification of issues that could lead to costly outages. Moreover, the segment benefits from the increased use of renewable energy sources, which require advanced monitoring and predictive maintenance solutions to ensure operational efficiency and cost-effectiveness. Innovations like vibration analysis and infrared thermography have further advanced condition monitoring in this segment by providing more precise data on turbine and generator health.

The HVAC (Heating, Ventilation, and Air Conditioning) systems segment is also anticipated to see considerable growth in the coming years. This growth is fueled by the rising demand for energy-efficient and environmentally sustainable HVAC systems, along with the growing adoption of smart HVAC solutions with remote control features. As the commercial and industrial sectors expand, so does the need to improve indoor air quality, driving demand for advanced HVAC systems. Key trends supporting this growth include the integration of green technologies like geothermal heat pumps and solar-powered HVAC systems, the use of smart thermostats for remote control, and the development of demand-response HVAC systems that adjust settings based on occupancy levels. These advancements enhance energy efficiency and align with sustainability goals.

The machine condition monitoring market is thus set to expand significantly, driven by the increasing adoption of predictive maintenance technologies, demand for sustainable solutions, and industry-wide digital transformation efforts.

Order a free sample PDF of the Machine Condition Monitoring Market Intelligence Study, published by Grand View Research.

0 notes