#Food Diagnostics Market Trends

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr is available in 18 languages.

Text

Food Diagnostics Market Will Hit Big Revenues In Future

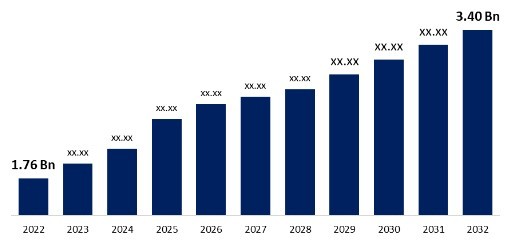

The food diagnostics market size is estimated at USD 16.2 billion in 2023 and is projected to reach USD 23.5 billion by 2028, at a CAGR of 7.7% from 2023 to 2028. Food diagnostics is the collection of processes and methodologies employed to evaluate and verify food products, guaranteeing their adherence to safety, quality, genuineness, and compliance with regulatory standards. These procedures encompass diverse testing methods and analytical approaches applied across different stages of the food supply chain, encompassing production, processing, distribution, and consumption. It is essential for the evaluation and preservation of the desired quality attributes of food items, which involve assessing characteristics such as flavor, texture, color, fragrance, and overall sensory qualities.

Food Diagnostics Market Trends

Advanced Technologies: The market is witnessing a surge in the adoption of technologies such as PCR (polymerase chain reaction), ELISA (enzyme-linked immunosorbent assay), and next-generation sequencing. These technologies are revolutionizing how foodborne pathogens are detected and analyzed, making testing more efficient and accurate.

Rise of Portable Testing Solutions: As consumer demands for quick results grow, portable diagnostic devices are on the rise. These solutions enable rapid testing at the point of need, empowering manufacturers, retailers, and consumers to identify potential safety issues without delays.

AI and Machine Learning: Leveraging artificial intelligence and machine learning is enhancing data analysis in food diagnostics. These technologies can predict potential contamination risks, optimize testing protocols, and improve decision-making processes.

Increased Regulations and Standards: Governments and global organizations are tightening food safety standards, leading to increased demand for reliable diagnostic tools. Regulatory compliance is driving investments in the market as companies strive to meet these new requirements.

Food Diagnostics Market Opportunities

Emerging Markets: Developing economies are investing more in food safety, leading to increased demand for diagnostic solutions. This represents a growing opportunity for companies that can tailor solutions for these regions. Collaboration and Partnerships: Strategic partnerships between diagnostic companies, food manufacturers, and regulatory bodies can lead to more comprehensive testing and monitoring systems.

Sustainability Focus: The market is shifting towards environmentally friendly diagnostic products, appealing to consumers and organizations committed to sustainable practices.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=225194671

The meat, poultry, and seafood segment is projected to hold the largest market share in the food diagnostics market, based on tested foods.

Foodborne illnesses and contamination outbreaks are a persistent global issue, frequently originating from protein-rich food categories like meat, poultry, and seafood. Ensuring the safety and quality of these products is essential to prevent public health crises and preserve consumer trust. Meat, poultry, and seafood are fundamental to the food industry, contributing significantly to market revenues. As essential components of diets around the world, they account for a significant portion of consumer spending, emphasizing the critical need for their safety and quality. Therefore, it is vital to monitor these products for pathogens, allergens, chemical residues, and other contaminants to safeguard consumer health and maintain the economic stability of the industry. Globalization of the food supply chain has made it necessary to address international regulations and standards. Compliance with stringent regulations, such as Hazard Analysis and Critical Control Points (HACCP), ISO standards, and national food safety guidelines, is mandatory for manufacturers and exporters. This has driven the need for advanced food diagnostics techniques in meat, poultry, and seafood.

The safety segment is expected to lead and achieve the highest CAGR in the food diagnostics market, driven by testing type.

The safety sub-segment is set to lead and experience the highest growth within the testing type segment of the food diagnostics market. Food safety testing plays a crucial role in the global food industry, ensuring the safety of products intended for human consumption. Recently, food safety testing has gained more emphasis than food quality testing, driven by growing concerns over foodborne illnesses and outbreaks. This testing encompasses a range of methods designed to identify contaminants, pathogens, and chemical residues in food products, safeguarding consumers from potential health risks. Contaminants like Salmonella, E. coli, allergens, and chemical residues can present significant health dangers. As a result, strict regulatory standards and heightened awareness have increased the demand for advanced testing techniques. Furthermore, with the complexities of global supply chains, food safety testing has become even more essential in preventing outbreaks, protecting public health, and preserving the reputation of food manufacturers.

Asia Pacific is projected to experience the highest CAGR in the global food diagnostics market.

The Asia Pacific region is experiencing rapid population growth, urbanization, and rising disposable incomes. Countries like China and India are seeing significant population increases, leading to higher food consumption. This surge in demand has heightened the need for effective food safety and quality testing. As urban migration accelerates, the demand for processed and packaged foods is also on the rise, further driving the need for stringent safety and quality control measures, which is fueling the growth of the food diagnostics market. Additionally, the food supply chain in Asia Pacific is becoming more intricate due to globalization and the expansion of international trade. This growing complexity requires thorough testing and monitoring across the entire supply chain, from farm to fork. As a result, food diagnostics solutions are playing a critical role in ensuring the safety and quality of food products.

Leading Food Diagnostics Companies:

Major key players operating in the food diagnostics market include Bio-Rad Laboratories Inc. (US), Thermo Fisher Scientific Inc. (US), Shimadzu Corporation (Japan), Neogen Corporation (US), BioMerieux (France), Agilent Technologies Inc. (US), Merck KGaA (Germany), QIAGEN (Germany), Bruker (US), and Danaher (US).

#Food Diagnostics Market#Food Diagnostics#Food Diagnostics Market Size#Food Diagnostics Market Share#Food Diagnostics Market Growth#Food Diagnostics Market Trends#Food Diagnostics Market Forecast#Food Diagnostics Market Analysis#Food Diagnostics Market Report#Food Diagnostics Market Scope#Food Diagnostics Market Overview#Food Diagnostics Market Outlook#Food Diagnostics Market Drivers#Food Diagnostics Industry#Food Diagnostics Companies

0 notes

Text

Exploring Trends Shaping the Animal Care Market

The Animal Care Market is undergoing significant transformations driven by evolving consumer preferences, technological advancements, and emerging trends. In this article, we delve into the latest trends shaping the landscape of the animal care industry and their implications for market players.

Humanization of Pets: Treating Pets like Family

One of the prominent trends in the animal care market is the increasing humanization of pets. Pet owners are treating their animals more like family members, seeking products and services that cater to their pets' health, comfort, and emotional well-being. This trend has led to a growing demand for premium pet food, grooming services, and accessories designed to enhance the quality of life for companion animals.

Natural and Organic Products: A Shift towards Healthier Options

Consumers are becoming more conscious about the ingredients and materials used in pet care products, leading to a surge in demand for natural and organic alternatives. Pet owners are seeking products free from artificial additives, preservatives, and chemicals, opting instead for wholesome and sustainable options that promote the health and vitality of their pets. This trend has propelled the growth of natural pet food, eco-friendly toys, and biodegradable pet accessories in the market.

Telemedicine and Remote Veterinary Care: Convenient Healthcare Solutions

Advancements in technology have revolutionized the way veterinary care is delivered, with the adoption of telemedicine and remote monitoring solutions gaining traction in the animal care industry. Pet owners are increasingly turning to virtual consultations, telehealth platforms, and mobile apps to seek medical advice, diagnosis, and treatment for their pets, especially amid the COVID-19 pandemic. This trend has expanded access to veterinary services, improved convenience for pet owners, and facilitated early detection and intervention for pet health issues.

Personalized Nutrition and Wellness: Tailoring Care for Individual Pets

Pet owners are embracing personalized approaches to pet nutrition and wellness, recognizing that each animal has unique dietary and health needs. The demand for customized pet food formulations, tailored supplementation, and genetic testing services is on the rise as pet owners seek to optimize their pets' health and longevity. This trend has spurred innovation in the development of personalized pet nutrition plans, DNA testing kits, and health monitoring tools that cater to individual pets' requirements.

Sustainable and Ethical Practices

Environmental sustainability and ethical sourcing have become key considerations for pet owners when choosing products and services for their animals. There is a growing emphasis on eco-friendly packaging, cruelty-free ingredients, and ethical manufacturing practices in the animal care market. Companies are increasingly adopting sustainable initiatives, such as carbon-neutral operations, recyclable packaging, and ethical sourcing of raw materials, to align with consumer values and reduce their environmental impact.

Conclusion

The animal care market is evolving rapidly, driven by shifting consumer preferences, technological innovations, and societal trends. By staying attuned to these emerging trends and embracing innovation, companies can capitalize on new opportunities, differentiate their offerings, and meet the evolving needs of pet owners and their beloved companions. As the bond between humans and animals continues to strengthen, the animal care industry is poised for continued growth and transformation in the years to come.

#Animal Care Market#Animal Care Industry#Animal Care Industry Research Report#Animal Care Market Research Reports#Animal Vaccines Market#Companion Animal Healthcare Market#Veterinary Services Market#Animal Care Market Analysis#Animal Care Market Demand#Animal Care Market Forecast#Animal Care Market Growth#Animal Care Market Outlook#Animal Care Market Revenue#Animal Care Market Size#Animal Care Market Trends#Animal Care Market Challenges#Animal Care Products Market#Animal Diagnostics and Testing Market#Animal Pharmaceuticals Market#Emerging Trends in Animal Care#Global Animal Care Market#Pet Food and Nutrition Market#Veterinary Clinics and Hospitals#Veterinary Services Industry Research Report#Animal Care#Pet Animal Care#Pet Food Market Size#Pet Food Market Share#Health Care for Animals#Animal Care and Services

0 notes

Text

North America HVAC System Market Sales, Trends, Region Forecast and Manufacturers in 2023-2030

The North America HVAC system market was valued at US$ 90,492.1 million in 2022 and is expected to reach US$ 2,02,793.85 million by 2030; it is estimated to grow at a CAGR of 10.6% from 2022 to 2030.

Growth in Government Regulatory Policies for Energy Saving and Conservation Fuel the North America HVAC System Market

📚 𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐒𝐚𝐦𝐩𝐥𝐞 𝐏𝐃𝐅 𝐂𝐨𝐩𝐲@ https://www.businessmarketinsights.com/sample/BMIRE00026926

Governments across the world are using a variety of strategies to encourage energy saving and conservation. They are including sizable line items for energy costs in their yearly operational budgets. In addition, they are saving a lot of money on energy costs incurred in public buildings and are exhibiting energy and environmental leadership by investing in energy efficiency.

📚𝐅𝐮𝐥𝐥 𝐑𝐞𝐩𝐨𝐫𝐭 𝐋𝐢𝐧𝐤 @ https://www.businessmarketinsights.com/reports/north-america-hvac-system-market

Other than the increase in the efficiency of both new and existing facilities, many governments are including energy efficiency standards in their decisions of product purchases. The main energy consumers in municipal level operations are often the water and wastewater treatment facilities. High-quality HVAC systems can be employed at water and wastewater facilities to decrease energy costs and greenhouse gas emissions. Through energy data management and evaluation, energy efficiency standards for public buildings, uptake of retrofit programs for already-existing public buildings, acquisition of energy-efficient appliances and equipment, and establishment of energy-efficient operations and maintenance procedures, state and local governments are promoting energy efficiency programs and policies for public facilities, equipment, and government operations.

𝐓𝐡𝐞 𝐋𝐢𝐬𝐭 𝐨𝐟 𝐂𝐨𝐦𝐩𝐚𝐧𝐢𝐞𝐬

Mitsubishi Electric Corp

Blue Star Ltd

Hitachi Ltd

Daikin Industries Ltd

Emerson Electric Co

Honeywell International Inc

LG Electric Inc

Carrier Global Corp

Johnson Controls Inca

One significant trend is the integration of HVAC systems with building management automation systems. This integration allows for streamlined operation and maintenance, enabling building owners to optimize energy consumption and improve overall system performance. BAS systems provide real-time monitoring and control of HVAC equipment, allowing for precise temperature and humidity control, as well as remote access and diagnostics. This integration is especially valuable in commercial and industrial settings, where energy efficiency and system reliability are critical.

The demand for HVAC systems is directly linked to the growth of various industries, including manufacturing, pharmaceuticals, IT, and ITES. Rapid industrialization and the expansion of the service sector are driving the construction of new facilities and the renovation of existing buildings, creating a significant demand for HVAC solutions. The pharmaceutical industry, in particular, requires precise temperature and humidity control to maintain product quality and ensure compliance with regulatory requirements. Data centers, which are essential to the IT and ITES sectors, also rely heavily on robust and efficient HVAC systems to maintain optimal operating conditions for servers and other equipment.

𝐀𝐛𝐨𝐮𝐭 𝐔𝐬: Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications

𝐀𝐮𝐭𝐡𝐨𝐫’𝐬 𝐁𝐢𝐨: 𝐕𝐚𝐢𝐛𝐡𝐚𝐯 𝐆𝐡𝐚𝐫𝐠𝐞 𝐒𝐞𝐧𝐢𝐨𝐫 𝐌𝐚𝐫𝐤𝐞𝐭 𝐑𝐞𝐬𝐞𝐚𝐫𝐜𝐡 𝐄𝐱𝐩𝐞𝐫𝐭

0 notes

Text

North America HVAC System Market Comprehensive Study, Trends, Strategy, Applications Analysis and Growth by Forecast to 2030

The North America HVAC system market was valued at US$ 90,492.1 million in 2022 and is expected to reach US$ 2,02,793.85 million by 2030; it is estimated to grow at a CAGR of 10.6% from 2022 to 2030.

Growth in Government Regulatory Policies for Energy Saving and Conservation Fuel the North America HVAC System Market

📚 𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐒𝐚𝐦𝐩𝐥𝐞 𝐏𝐃𝐅 𝐂𝐨𝐩𝐲@ https://www.businessmarketinsights.com/sample/BMIRE00026926

Governments across the world are using a variety of strategies to encourage energy saving and conservation. They are including sizable line items for energy costs in their yearly operational budgets. In addition, they are saving a lot of money on energy costs incurred in public buildings and are exhibiting energy and environmental leadership by investing in energy efficiency.

📚𝐅𝐮𝐥𝐥 𝐑𝐞𝐩𝐨𝐫𝐭 𝐋𝐢𝐧𝐤 @ https://www.businessmarketinsights.com/reports/north-america-hvac-system-market

Other than the increase in the efficiency of both new and existing facilities, many governments are including energy efficiency standards in their decisions of product purchases. The main energy consumers in municipal level operations are often the water and wastewater treatment facilities. High-quality HVAC systems can be employed at water and wastewater facilities to decrease energy costs and greenhouse gas emissions. Through energy data management and evaluation, energy efficiency standards for public buildings, uptake of retrofit programs for already-existing public buildings, acquisition of energy-efficient appliances and equipment, and establishment of energy-efficient operations and maintenance procedures, state and local governments are promoting energy efficiency programs and policies for public facilities, equipment, and government operations.

𝐓𝐡𝐞 𝐋𝐢𝐬𝐭 𝐨𝐟 𝐂𝐨𝐦𝐩𝐚𝐧𝐢𝐞𝐬

Mitsubishi Electric Corp

Blue Star Ltd

Hitachi Ltd

Daikin Industries Ltd

Emerson Electric Co

Honeywell International Inc

LG Electric Inc

Carrier Global Corp

The HVAC market is also experiencing a shift towards service-based models, with companies offering comprehensive maintenance, repair, and monitoring services. The increasing complexity of HVAC systems and the growing reliance on connected technologies are driving the demand for professional services. Remote monitoring and diagnostics capabilities are enabling service providers to proactively address issues and optimize system performance. The growth of the aftermarket, including replacement parts and upgrades, is also contributing to the market's expansion.

In conclusion, the HVAC system market is a dynamic and evolving sector, driven by a confluence of factors, including technological advancements, regulatory mandates, and changing consumer preferences. The focus on energy efficiency, indoor air quality, and sustainability is shaping the development of innovative HVAC solutions. The integration of smart technologies, the adoption of alternative refrigerants, and the growing demand for service-based models are transforming the market landscape. As climate change continues to impact global temperatures and weather patterns, the demand for reliable and efficient HVAC systems is expected to remain strong, driving continued growth and innovation in the industry.

𝐀𝐛𝐨𝐮𝐭 𝐔𝐬: Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications

𝐀𝐮𝐭𝐡𝐨𝐫’𝐬 𝐁𝐢𝐨: 𝐒𝐰𝐢𝐭𝐢 𝐏𝐚𝐭𝐢𝐥 𝐒𝐞𝐧𝐢𝐨𝐫 𝐌𝐚𝐫𝐤𝐞𝐭 𝐑𝐞𝐬𝐞𝐚𝐫𝐜𝐡 𝐄𝐱𝐩𝐞𝐫𝐭

0 notes

Text

Specialty Enzymes Market Analysis: Key Challenges and Opportunities

Growing Applications in Pharmaceuticals, Biotechnology, and Food Processing Fuel Growth in the Specialty Enzymes Market.

The Specialty Enzymes Marketsize was valued at USD 5.6 Billion in 2023. It is expected to grow to USD 10.7 Billion by 2032 and grow at a CAGR of 7.5% over the forecast period of 2024-2032.

The Specialty Enzymes Market is driven by increasing demand for biocatalysts in pharmaceuticals, biotechnology, food & beverage, diagnostics, and other industrial applications. Specialty enzymes play a crucial role in accelerating biochemical reactions, enhancing efficiency, and reducing environmental impact in various industries. With the rapid advancements in enzyme engineering and bioprocessing technologies, the market is expected to experience significant expansion in the coming years.

Key Players in the Specialty Enzymes Market

Novozymes A/S

BASF SE

DSM Nutritional Products

DuPont de Nemours, Inc.

Amano Enzyme Inc.

Advanced Enzyme Technologies Ltd.

Codexis, Inc.

Roche Holding AG

Kerry Group plc

Biocatalysts Ltd

These key players are investing in research & development, partnerships, and innovative enzyme formulations to cater to the evolving needs of end-user industries.

Future Scope and Emerging Trends

The Specialty Enzymes Market is poised for exponential growth, fueled by technological advancements in enzyme engineering, increased demand for bio-based solutions, and the expansion of biotechnology-driven industries.

One of the major trends shaping the market is the increasing adoption of enzyme-based biocatalysts in pharmaceutical and diagnostic applications. Enzymes such as proteases, carbohydrases, and polymerases are widely used in drug formulation, disease diagnostics, and genetic engineering. Additionally, the food & beverage industry is integrating enzymes for improved texture, flavor, and nutritional benefits. With the shift toward sustainable and green chemistry practices, specialty enzymes are replacing traditional chemical processes in various industrial sectors, including biofuels, textiles, and wastewater treatment. The growing trend of precision fermentation and enzyme-based bioprocessing is further propelling market growth.

Key Market Points:

✅ Growing Adoption in Pharmaceutical & Biotechnology Industries: Enzymes are crucial for drug formulation, gene editing, and disease diagnostics. ✅ Expansion of Sustainable Bioprocessing Solutions: Enzyme-based alternatives are replacing chemical catalysts for eco-friendly manufacturing. ✅ Advancements in Enzyme Engineering: New developments in protein engineering and recombinant DNA technology are enhancing enzyme efficiency. ✅ Rising Demand in Food & Beverage Processing: Specialty enzymes are used for flavor enhancement, shelf-life extension, and nutrient enrichment. ✅ Biotechnology & Healthcare Boom: Increasing applications in medical diagnostics, enzyme therapies, and biopharmaceutical production are driving growth. ✅ Regulatory Support for Green Chemistry: Governments worldwide are encouraging the adoption of biological catalysts for sustainable industrial applications.

Conclusion

The Specialty Enzymes Market is on a strong growth trajectory, supported by innovations in biotechnology, enzyme formulation, and sustainable industrial processing. As industries transition toward bio-based and eco-friendly solutions, specialty enzymes will continue to play a pivotal role in transforming industrial applications. Companies that invest in enzyme research, biocatalysis, and sustainable bioprocessing will drive the future of this dynamic market, contributing to a more efficient and environmentally responsible global economy.

Read Full Report: https://www.snsinsider.com/reports/specialty-enzymes-market-4688

Contact Us:

Jagney Dave — Vice President of Client Engagement

Phone: +1–315 636 4242 (US) | +44- 20 3290 5010 (UK)

#Specialty Enzymes Market#Specialty Enzymes Market Size#Specialty Enzymes Market Share#Specialty Enzymes Market Report#Specialty Enzymes Market Forecast

0 notes

Text

The global biosensors market was valued at USD 34.4 billion in 2025 and is estimated to reach USD 47.54 billion by 2030, registering a CAGR of 6.7% during the forecast period. The emergence of nanotechnology-based biosensors, significant technological advancements in the last few years, increasing use of biosensors to monitor glucose levels in individuals with diabetes, surging demand for home-based point of care devices and rising government initiatives toward diagnostics are driving the growth of the biosensors market. However, the slow rate of commercialization and reluctance in adopting new treatment practices, and high costs involved in R&D are expected to restrain the growth of the market. Emerging markets in developing countries, high-growth opportunities in the food industry and environmental monitoring applications, and high-growth opportunities in the wearable biosensors market are projected to offer lucrative opportunities for the players operating in the biosensors market during the forecast period.

0 notes

Text

Top High-Paying Jobs for Biomedical Science Graduates

A Master in Biomedical Sciences (MSc Biomedical Science) opens the door to many career opportunities in healthcare, research, and industry. With advancements in medical technology and a growing need for professionals, graduates with specialized knowledge are in high demand. Whether working in laboratories, hospitals, or biotechnology companies, these professionals contribute to medical discoveries and patient care.

Listed below are some of the highest-paying career paths for biomedical science graduates.

1. Biomedical Scientist

Biomedical scientists work in laboratories to study diseases, develop treatments, and conduct diagnostic tests. They are key in identifying infections, monitoring patient health, and supporting medical research. Their expertise is crucial in hospitals, research institutions, and pharmaceutical companies.

Average Salary: $60,000 - $100,000 per year

Industry: Healthcare, Research

2. Clinical Research Associate

Clinical research associates (CRAs) oversee clinical trials that test new drugs and treatments. They ensure that studies follow regulations and ethical guidelines. Their work is essential in bringing new medicines to the market.

Average Salary: $65,000 - $120,000 per year

Industry: Pharmaceuticals, Biotechnology, Research Organizations

3. Medical Laboratory Scientist

Medical laboratory scientists analyze samples, such as blood and tissue, to detect diseases. They work closely with doctors to diagnose conditions and recommend treatments. Their expertise is crucial in hospitals, diagnostic labs, and research facilities.

Average Salary: $55,000 - $95,000 per year

Industry: Healthcare, Diagnostics, Research

4. Biotechnologist

Biotechnologists use biological systems to develop new products, such as medicines, vaccines, and biofuels. They work in pharmaceutical companies, agriculture, and environmental science. Their work impacts healthcare, food production, and sustainability.

Average Salary: $70,000 - $130,000 per year

Industry: Biotechnology, Pharmaceuticals, Agriculture

5. Toxicologist

Toxicologists study the effects of chemicals on living organisms. They work in forensic labs, regulatory agencies, and pharmaceutical companies to ensure product safety. Their research helps prevent harmful substances from entering the market.

Average Salary: $75,000 - $140,000 per year

Industry: Pharmaceuticals, Environmental Science, Government Agencies

6. Regulatory Affairs Specialist

Regulatory affairs specialists ensure that medical products meet legal requirements. They work with government agencies to approve new drugs and medical devices. Their role is essential in keeping healthcare products safe for public use.

Average Salary: $80,000 - $150,000 per year

Industry: Pharmaceuticals, Medical Devices, Government Agencies

7. Genetic Counselor

Genetic counselors help individuals understand genetic conditions and risks. They interpret genetic tests and guide patients on treatment options. Their role is important in personalized medicine and genetic research.

Average Salary: $70,000 - $110,000 per year

Industry: Healthcare, Research, Genetics

8. Pharmaceutical Scientist

Pharmaceutical scientists develop and test new drugs. They study how medicines interact with the body and work to improve drug effectiveness. Their research is vital in creating treatments for diseases.

Average Salary: $80,000 - $140,000 per year

Industry: Pharmaceuticals, Research, Drug Development

9. Epidemiologist

Epidemiologists study disease patterns and public health trends. They work in government agencies, hospitals, and research institutions to prevent disease outbreaks. Their research helps shape healthcare policies and interventions.

Average Salary: $65,000 - $120,000 per year

Industry: Public Health, Research, Government

Conclusion

A Master's in Biomedical Sciences provides many career opportunities in healthcare, research, and industry. Graduates can pursue rewarding careers that contribute to medical advancements and improve lives. Whether working in laboratories, hospitals, or biotechnology firms, biomedical science professionals play a vital role in modern medicine. With continuous developments in the field, these careers offer both financial stability and professional growth.

1 note

·

View note

Text

North America Edge Computing Market Growth, Analysis, Share, Trends, Segmentation and Forecast to 2028

The North America edge computing market is expected to grow from US$ 16,212.71 million in 2022 to US$ 52,976.45 million by 2028. It is estimated to grow at a CAGR of 21.8% from 2022 to 2028.

Extremely Low Latency and High Availability of Bandwidth Fuels North America Edge Computing Market

📚 𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐒𝐚𝐦𝐩𝐥𝐞 𝐏𝐃𝐅 𝐂𝐨𝐩𝐲@ https://www.businessmarketinsights.com/sample/BMIRE00028905

Edge computing works with a highly distributed network which eliminates the round trip to the cloud, reducing latency and offers real-time responsiveness. Acceleration in data transmission has become an important business goal. Many applications require low latency to improve the user experience and support customer satisfaction by helping applications run faster and smoothly. Such applications include online meetings and mission-critical computation applications hosted on the cloud. Improving latency may be a matter of making small improvements and compiling time savings in various application such as healthcare, air traffic control, combat situation and among other applications, which provides meaningful improvements in network performance.Low latency provides a reliable and robust connection, reducing connection loss, delay, lags, and buffers. It is critical for many businesses and industries that rely on real-time applications or live streaming, including banking, diagnostic imaging, navigation, stock trading, weather forecasting, collaboration, research, ticket sales, video broadcasting, and online gaming. Thus, low latency improves the operation speed at the edge, enabling the demand for edge computing.

📚𝐅𝐮𝐥𝐥 𝐑𝐞𝐩𝐨𝐫𝐭 𝐋𝐢𝐧𝐤 @ https://www.businessmarketinsights.com/reports/north-america-edge-computing-market

𝐓𝐡𝐞 𝐋𝐢𝐬𝐭 𝐨𝐟 𝐂𝐨𝐦𝐩𝐚𝐧𝐢𝐞𝐬

ADLINK Technology Inc

Amazon Web Services

Dell Technologies

EdgeConnex Inc.

FogHorn Systems

Hewlett Packard Enterprise Development LP (HPE)

IBM Corporation

Litmus Automation, Inc

Microsoft Corporation

Vapor IO, Inc.

𝐀𝐛𝐨𝐮𝐭 𝐔𝐬: Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications

𝐀𝐮𝐭𝐡𝐨𝐫’𝐬 𝐁𝐢𝐨: 𝐬𝐭𝐞𝐩𝐡𝐞𝐧 𝐣𝐨𝐡𝐧𝐬𝐨𝐧 𝐒𝐞𝐧𝐢𝐨𝐫 𝐌𝐚𝐫𝐤𝐞𝐭 𝐑𝐞𝐬𝐞𝐚𝐫𝐜𝐡 𝐄𝐱𝐩𝐞𝐫𝐭

0 notes

Text

North America Edge Computing Market Regional Analysis, Key Players, Growth, Share and Key Trends by 2028

The North America edge computing market is expected to grow from US$ 16,212.71 million in 2022 to US$ 52,976.45 million by 2028. It is estimated to grow at a CAGR of 21.8% from 2022 to 2028.

Extremely Low Latency and High Availability of Bandwidth Fuels North America Edge Computing Market

📚 𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐒𝐚𝐦𝐩𝐥𝐞 𝐏𝐃𝐅 𝐂𝐨𝐩𝐲@ https://www.businessmarketinsights.com/sample/BMIRE00028905

Edge computing works with a highly distributed network which eliminates the round trip to the cloud, reducing latency and offers real-time responsiveness. Acceleration in data transmission has become an important business goal. Many applications require low latency to improve the user experience and support customer satisfaction by helping applications run faster and smoothly. Such applications include online meetings and mission-critical computation applications hosted on the cloud. Improving latency may be a matter of making small improvements and compiling time savings in various application such as healthcare, air traffic control, combat situation and among other applications, which provides meaningful improvements in network performance.Low latency provides a reliable and robust connection, reducing connection loss, delay, lags, and buffers. It is critical for many businesses and industries that rely on real-time applications or live streaming, including banking, diagnostic imaging, navigation, stock trading, weather forecasting, collaboration, research, ticket sales, video broadcasting, and online gaming. Thus, low latency improves the operation speed at the edge, enabling the demand for edge computing.

📚𝐅𝐮𝐥𝐥 𝐑𝐞𝐩𝐨𝐫𝐭 𝐋𝐢𝐧𝐤 @ https://www.businessmarketinsights.com/reports/north-america-edge-computing-market

𝐓𝐡𝐞 𝐋𝐢𝐬𝐭 𝐨𝐟 𝐂𝐨𝐦𝐩𝐚𝐧𝐢𝐞𝐬

ADLINK Technology Inc

Amazon Web Services

Dell Technologies

EdgeConnex Inc.

FogHorn Systems

Hewlett Packard Enterprise Development LP (HPE)

IBM Corporation

Litmus Automation, Inc

Microsoft Corporation

Vapor IO, Inc.

Bandwidth is the amount of data that a network can carry over time. All networks have limited bandwidth, and wireless communication limits are severe. It is possible to increase network bandwidth to accommodate a large number of devices and data. Edge computing distributes data computation through the use of on-premise smart devices. It makes the data processing efficient by reducing bandwidth and improving response times. Thus, the less consumption of bandwidth can lead to reduced data transmission costs. Hence, extremely low latency and high bandwidth availability increase the adoption of edge computing over various applications, bolstering the edge computing market growth.

𝐀𝐛𝐨𝐮𝐭 𝐔𝐬: Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications

𝐀𝐮𝐭𝐡𝐨𝐫’𝐬 𝐁𝐢𝐨: 𝐒𝐡𝐫𝐞𝐲𝐚 𝐏𝐚𝐰𝐚𝐫 𝐒𝐞𝐧𝐢𝐨𝐫 𝐌𝐚𝐫𝐤𝐞𝐭 𝐑𝐞𝐬𝐞𝐚𝐫𝐜𝐡 𝐄𝐱𝐩𝐞𝐫𝐭

0 notes

Text

Food Diagnostics Market to Showcase Continued Growth in the Coming Years

The food diagnostics market size is projected to grow from an estimated USD 16.2 billion in 2023 to USD 23.5 billion by 2028, reflecting a compound annual growth rate (CAGR) of 7.7% during this period. The demand for food diagnostic solutions has risen sharply as consumers and regulatory agencies prioritize food safety and quality. This market encompasses a diverse array of products, including systems, test kits, and consumables, all of which play a crucial role in its growth. The increasing need for rapid and precise detection of allergens, contaminants, pathogens, and adulterants in food products significantly drives this expansion.

A key factor propelling the food diagnostics market is the globalization of food trade. As the food supply chain becomes more interconnected internationally, the demand for effective diagnostic systems has surged. Food producers and exporters face the challenge of adhering to various food safety regulations and quality standards across different countries. Consequently, there has been a marked increase in the adoption of advanced diagnostic tools to ensure compliance with these diverse and often stringent requirements, thereby fostering market growth.

Food Diagnostics Market Drivers: Increasing cases of food recalls

The increasing frequency of food recalls has significantly impacted the food diagnostics industry, driven by growing concerns over food safety and public health. The introduction of contaminated or unsafe food products can result in serious consequences, including illnesses, hospitalizations, and even fatalities. This escalating awareness of food safety has led regulatory agencies and food manufacturers to invest in sophisticated diagnostic technologies. These innovations allow for the rapid and precise detection of contaminants, pathogens, allergens, and adulterants, thereby mitigating the risk of tainted food reaching consumers. Additionally, the financial and reputational damages associated with food recalls have motivated companies to implement advanced diagnostic solutions, reducing the likelihood of such incidents and contributing to the expansion of the food diagnostics market.

Food Diagnostics Market Opportunities: Increased budget allocation and expenditure on food safety

Governments, regulatory agencies, and stakeholders in the food industry worldwide have acknowledged the vital importance of maintaining safety and quality throughout the food supply chain. This acknowledgment has led to a significant increase in investments in food safety initiatives, fostering innovation and growth within the food diagnostics industry. The rise of advanced technologies, such as DNA-based testing and rapid pathogen detection, has gained considerable momentum, allowing for more accurate and efficient monitoring of food products from production to consumption. Furthermore, growing consumer awareness of foodborne illnesses and the demand for transparency in the food supply chain have intensified the need for effective food diagnostics solutions. This presents numerous opportunities for companies to create cutting-edge diagnostic tools and services. As the market evolves, the food diagnostics sector is well-positioned for substantial growth, promising enhanced food safety and quality.

The meat, poultry, and seafood segment is projected to hold the largest share of the food diagnostics market based on tested food types.

Foodborne illnesses and contamination outbreaks remain a significant global issue, often originating from protein-rich categories such as meat, poultry, and seafood. Ensuring the safety and quality of these products is essential to prevent serious health risks and uphold consumer confidence. Additionally, meat, poultry, and seafood are vital components of the food industry, significantly contributing to market revenues. As essential staples in diets worldwide, they represent a considerable share of consumer spending, making their quality and safety critically important. Therefore, monitoring these products for pathogens, allergens, chemical residues, and other contaminants is vital for consumer protection and the economic stability of the industry.

The globalization of the food supply chain has necessitated adherence to international regulations and standards. Compliance with rigorous regulations, including Hazard Analysis and Critical Control Points (HACCP), ISO standards, and national food safety guidelines, is essential for manufacturers and exporters. This demand has driven the adoption of advanced food diagnostics techniques in the meat, poultry, and seafood sectors.

Asia Pacific is projected to achieve the highest CAGR in the global food diagnostics market.

The Asia Pacific region is witnessing considerable population growth, urbanization, and a rise in disposable income. This rapid population increase, especially in countries such as China and India, has resulted in higher food consumption. Consequently, the demand for effective food safety and quality testing has become essential. As more individuals move to urban areas, the need for processed and packaged foods is escalating. This rising demand for food products requires stringent quality control and safety measures, which are fueling the expansion of the food diagnostics market.

Top Food Diagnostics Companies

Major key players operating in the food diagnostics market include Bio-Rad Laboratories Inc. (US), Thermo Fisher Scientific Inc. (US), Shimadzu Corporation (Japan), Neogen Corporation (US), BioMerieux (France), Agilent Technologies Inc. (US), Merck KGaA (Germany), QIAGEN (Germany), Bruker (US), and Danaher (US).

#Food Diagnostics Market#Food Diagnostics#Food Diagnostics Market Size#Food Diagnostics Market Share#Food Diagnostics Market Growth#Food Diagnostics Market Trends#Food Diagnostics Market Forecast#Food Diagnostics Market Analysis#Food Diagnostics Market Report#Food Diagnostics Market Scope#Food Diagnostics Market Overview#Food Diagnostics Market Outlook#Food Diagnostics Market Drivers#Food Diagnostics Industry

0 notes

Text

Exploring the Animal Care Market Revenue, Growth, and Future Outlook

Introduction

The Animal Care Industry plays a pivotal role in ensuring the health, well-being, and happiness of pets and companion animals worldwide. This article delves into the dynamics of the animal care market, offering insights into its research reports, growth prospects, revenue outlook, and emerging trends.

Animal Care Market Research Reports

Market research reports serve as valuable resources for understanding the animal care industry landscape. These reports provide comprehensive analyses of market trends, growth drivers, challenges, and opportunities. Recent studies indicate a positive outlook for the global animal care market, with substantial growth expected in the coming years.

Animal Care Market Forecast

The animal care market is poised for significant growth, driven by various factors contributing to increased demand for pet-related products and services. Market analysts project steady growth, with a compound annual growth rate CAGR of 4.3% expected between 2023 and 2033, reaching a market size of USD 62.3 billion by 2033.

Animal Care Market Size

The global animal care market was estimated at USD 40.9 billion in February 2024, reflecting robust growth in pet ownership and spending. In the United States alone, the market was valued at USD 136.8 billion in 2022, according to the American Pet Products Association.

Animal Care Market Growth

While the global animal care market is experiencing steady growth, the United States is anticipated to witness a growth rate of 2-3% in 2024, as per Grand View Research. This growth is fueled by factors such as increasing disposable income, rising pet ownership, and growing awareness of animal well-being.

Market Segments

The animal care market comprises several segments catering to the diverse needs of pet owners:

Pet Food & Treats

This segment holds the largest share of the global market, accounting for approximately 50% of total spending on animal care products.

Pet owners are increasingly opting for premium pet food and treats, driving growth in this segment.

Veterinary Care & Products

The veterinary care segment is the second-largest, with projections suggesting it might reach USD 37 billion in the US by 2023.

Advancements in veterinary medicine and increased spending on preventive healthcare contribute to the segment's growth.

Supplies, Live Animals & Over-the-counter Medications

Estimated at USD 32.1 billion in the US in 2023, this segment encompasses a wide range of products, including pet supplies, live animals, and over-the-counter medications. This segment includes pet insurance, boarding, grooming, and training services, estimated at USD 11.8 billion in the US in 2023.

Market Trends

Several notable trends are reshaping the Animal Care Market:

Premiumization- Pet owners are increasingly willing to invest in premium pet food, treats, and healthcare options, reflecting a growing focus on pet well-being and nutrition.

Surge in Pet Adoptions- The pandemic-driven surge in pet adoptions continues to influence market demand, with more households welcoming pets into their lives.

Direct-to-Consumer Channels- Online pet food and medication deliveries are witnessing significant growth, driven by the convenience and accessibility offered by direct-to-consumer (D2C) channels.

Focus on Sustainability- Environmentally friendly pet products and services are gaining popularity as consumers become more conscious of their ecological footprint.

Conclusion

The animal care market presents lucrative opportunities for industry players, driven by increasing pet ownership, rising spending on pet-related products and services, and evolving consumer preferences. By staying abreast of market trends, investing in research and development, and embracing sustainable practices, stakeholders can capitalize on the growing demand for animal care solutions, contributing to the well-being of pets and companion animals worldwide.

#Pet Care Industry Analysis#Animal Care Market#Animal Care Industry#Animal Care Industry Research Report#Animal Care Market Research Reports#Animal Vaccines Market#Companion Animal Healthcare Market#Veterinary Services Market#Animal Care Market Analysis#Animal Care Market Demand#Animal Care Market Forecast#Animal Care Market Growth#Animal Care Market Outlook#Animal Care Market Revenue#Animal Care Market Size#Animal Care Market Trends#Animal Care Market Challenges#Animal Care Products Market#Animal Diagnostics and Testing Market#Animal Pharmaceuticals Market#Emerging Trends in Animal Care#Global Animal Care Market#Pet Food and Nutrition Market#Veterinary Clinics and Hospitals#Veterinary Services Industry Research Report#Animal Care#Pet Animal Care#Pet Food Market Size#Pet Food Market Share#Health Care for Animals

0 notes

Text

North America Nerve Repair & Regeneration Market Regional Share, Global Size, Trends, Segmentation and Forecast to 2028

The North America nerve repair & regeneration market is expected to grow from US$ 3,721.38 million in 2022 to US$ 6,463.51 million by 2028; it is estimated to grow at a CAGR of 9.6% from 2022 to 2028.

📚 𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐒𝐚𝐦𝐩𝐥𝐞 𝐏𝐃𝐅 𝐂𝐨𝐩𝐲@ https://www.businessmarketinsights.com/sample/BMIRE00027759

Rising Prevalence of Age-associated Neurological Disorders among Geriatric Population Boosts North America Nerve Repair & Regeneration Market Growth.

A few neurologic disorders such as neuropathy, Alzheimer's disease, Parkinson's disease, and strokes are more common in the geriatric population, and their prevalence is rising with higher life expectancies. According to the WHO, the population aged 60 years will approximately double from 12% in 2015 to 22% by 2050, and mental and neurological disorders among older adults are likely to account for 6.6% of the total disability-adjusted life year (DALYs) for this age group. Also, as per the same source, ~15% of adults aged 60 and over have a mental disorder. Further, the number of people aged 65 years and above affected by Alzheimer's disease is expected to grow from ~5.8 million to 14 million by 2060 in the US.

📚𝐅𝐮𝐥𝐥 𝐑𝐞𝐩𝐨𝐫𝐭 𝐋𝐢𝐧𝐤 @ https://www.businessmarketinsights.com/reports/north-america-nerve-repair-and-regeneration-market

Moreover, neurological disorders are increasingly becoming a major cause of death across the region. For instance, according to the Centers for Disease Control and Prevention (CDC), Alzheimer's disease is the fifth leading cause of death in people aged 65 years and above. Therefore, the rising prevalence of age-associated neurological disorders among the geriatric population increases the demand for treatment of nerve repair & regeneration. This factor is propelling the growth of the North America Nerve Repair & Regeneration Market

𝐓𝐡𝐞 𝐋𝐢𝐬𝐭 𝐨𝐟 𝐂𝐨𝐦𝐩𝐚𝐧𝐢𝐞𝐬

Axogen Corporation

Boston Scientific Corporation

Integra LifeSciences

Medtronic

Abbott Laboratories

Stryker Corporation

Neuronetics

LivaNova PLC

Baxter

Polyganics BV

Key Market Dynamics:

The market is witnessing a shift towards biological solutions and regenerative medicine approaches.

Minimally invasive surgical techniques are gaining popularity, reducing patient recovery time.

The adoption of advanced imaging technologies is improving diagnostic accuracy and treatment planning.

Future Outlook:

The North American nerve repair and regeneration market is poised for continued growth, driven by ongoing technological advancements and increasing clinical adoption.

The development of personalized therapies and targeted drug delivery systems is expected to revolutionize treatment outcomes.

Expansion of telehealth and remote monitoring solutions may improve patient access to specialized care.

𝐀𝐛𝐨𝐮𝐭 𝐔𝐬: Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications

𝐀𝐮𝐭𝐡𝐨𝐫’𝐬 𝐁𝐢𝐨: 𝐏𝐫𝐚𝐠𝐚𝐭𝐢 𝐏𝐚𝐭𝐢𝐥 𝐒𝐞𝐧𝐢𝐨𝐫 𝐌𝐚𝐫𝐤𝐞𝐭 𝐑𝐞𝐬𝐞𝐚𝐫𝐜𝐡 𝐄𝐱𝐩𝐞𝐫𝐭

0 notes

Text

The Global Burden of Listeriosis: Market Trends and Treatment Advances

Overview Listeriosis is a severe bacterial infection caused by Listeria monocytogenes, primarily affecting high-risk populations such as pregnant women, newborns, the elderly, and immunocompromised individuals. The infection can lead to critical health complications, including meningitis, sepsis, and, in severe cases, fatality. Given the serious nature of the disease, early detection and prompt treatment are crucial to reducing its impact.

This article delves into the Listeriosis Market Size, available treatment options, market trends, and key pharmaceutical companies driving advancements in diagnostics and therapeutics.

Listeriosis Epidemiology

Although Listeriosis is a relatively rare disease, it poses a significant threat to specific vulnerable populations. According to the CDC, around 1,600 cases are reported annually in the United States, with approximately 260 deaths. The prevalence of Listeriosis is influenced by factors such as demographic trends, food safety standards, healthcare accessibility, and regional food contamination risks. As foodborne infections continue to be a global health concern, the demand for effective treatment and diagnostic solutions is steadily rising.

Treatment Landscape

The primary treatment for Listeriosis involves antibiotic therapy, with Listeriosis Drugs Market staples such as ampicillin, penicillin, and gentamicin often prescribed in combination for enhanced efficacy. Severe cases may require intravenous antibiotic administration and supportive care, especially for neonates and pregnant women.

Research into more targeted treatment approaches is ongoing, with innovations in vaccines, monoclonal antibodies, and alternative antibiotics offering promising advancements in tackling different Listeria strains.

Listeriosis Market Size and Growth Trends

The Listeriosis Market Size is anticipated to grow at a significant CAGR in the coming years, driven by:

Rising Disease Awareness: Growing public knowledge of foodborne infections has fueled the demand for better diagnostics and preventive measures.

Technological Advancements: Improvements in rapid diagnostic tools, PCR-based testing, and next-generation sequencing have enhanced early detection of Listeria infections.

Government Regulations and Food Safety Measures: Stringent food safety policies and surveillance programs are contributing to market expansion by promoting early diagnosis and treatment.

R&D in Novel Therapeutics: Pharmaceutical and biotech firms are actively developing vaccines and antimicrobial therapies to combat Listeriosis more effectively.

Key Players in the Listeriosis Market

The Listeriosis Companies landscape includes pharmaceutical giants, biotech startups, and research institutions working toward innovative treatment solutions. Notable players include:

Pfizer Inc. – Developing advanced antibiotics and antimicrobial agents for Listeriosis treatment.

Merck & Co., Inc. – Offering a broad portfolio of antibiotics effective against Listeria infections.

GlaxoSmithKline (GSK) – Engaged in vaccine and antibiotic research for more targeted Listeriosis therapies.

Eli Lilly and Company – Conducting infectious disease research to enhance Listeriosis treatment outcomes.

Biotech Startups & Research Institutions – Innovating alternative treatment methods, including monoclonal antibodies and next-gen therapeutics.

Challenges in the Listeriosis Drugs Market

Despite growth potential, the Listeriosis Drugs Market faces challenges such as:

Regulatory Hurdles: New therapies require extensive clinical trials and regulatory approvals.

Antibiotic Resistance: The emergence of drug-resistant Listeria strains necessitates continuous R&D for alternative treatments.

High Development Costs: Investment in novel antibiotics and vaccines is expensive, limiting market entry for smaller firms.

Limited Public Awareness: While Listeriosis is severe, its relative rarity means public health campaigns are essential for early diagnosis and intervention.

Future Outlook

The Listeriosis Market is poised for expansion due to medical advancements, increased awareness, and government-backed food safety initiatives. While hurdles such as regulatory barriers and market competition persist, ongoing research into novel therapeutics presents significant opportunities for growth. Stakeholders in the healthcare and pharmaceutical sectors should monitor developments closely to capitalize on emerging trends.

Latest Reports Offered By Delveinsight

Automated Suturing Devices Market | Clinically Isolated Syndrome Market | Dental Equipment Market | Disseminated Intravascular Coagulation Market | Drug Eruptions Market | Duodenoscope Market | Germ Cell Tumor Market | Heart Sounds Sensors Market | Hedgehog Pathway Inhibitors Market | Interventional Cardiology Devices Market | Marfan Syndrome Market | Negative Pressure Wound Therapy Devices Market | Opium Addiction Market | Pheochromocytoma Market | Pseudoxanthoma Elasticum Market | Transdermal Drug Delivery Devices

About DelveInsight

DelveInsight is a market research and consulting firm specializing in life sciences and healthcare. We deliver valuable insights to help pharmaceutical, biotechnology, and medical device companies succeed in a competitive and rapidly changing industry.

Contact InformationKanishk Email: [email protected]

0 notes

Text

Biotech Ingredients Market Analysis: Key Challenges and Opportunities

Growing Adoption of Sustainable and Innovative Solutions Drives Growth in the Biotech Ingredients Market.

The Biotech Ingredients Market size was valued at USD 2.2 billion in 2023 and is expected to reach USD 4.3 billion by 2032 and grow at a CAGR of 7.8% over the forecast period 2024-2032.

The Biotech Ingredients Market is experiencing rapid growth as industries increasingly shift toward sustainable, high-performance, and bio-based alternatives. Biotech ingredients, derived from microbial fermentation, plant cell culture, and enzyme technology, are revolutionizing sectors such as cosmetics, pharmaceuticals, food & beverages, and personal care. With a strong emphasis on eco-friendliness, reduced carbon footprint, and enhanced efficacy, biotech ingredients are gaining widespread adoption across the globe.

Key Players in the Biotech Ingredients Market

BASF SE (Lecithin, Enzymes)

Cargill, Incorporated (Soy Protein, Lactic Acid)

DuPont de Nemours, Inc. (Proteins, Enzymes)

Evonik Industries AG (Amino Acids, Biopolymers)

Genomatica, Inc. (Bio-BDO, Bio-1,4-Butanediol)

DSM (Dutch State Mines) (Amino Acids, Enzymes)

Novozymes A/S (Cellulases, Amylases)

Roche Holding AG (Biopharmaceuticals, Diagnostic Reagents)

SABIC (Saudi Basic Industries Corporation) (Biodegradable Polymers, Bio-based Chemicals)

Syngenta AG (Biofungicides, Bioinsecticides)

These companies are investing heavily in biotechnology, fermentation processes, and sustainable ingredient development to meet the rising consumer demand for natural and clean-label products.

Future Scope and Emerging Trends

The Biotech Ingredients Market is poised for substantial growth, driven by the expanding applications in cosmetics, pharmaceuticals, and food technology. The rising preference for plant-based, cruelty-free, and sustainable alternatives is accelerating demand for biotech-derived fragrances, active skincare compounds, and pharmaceutical excipients.

Advancements in synthetic biology, enzyme engineering, and microbial fermentation are enabling the production of high-purity, effective, and eco-friendly ingredients that replace conventional chemical-based counterparts. Additionally, biotech innovations are helping reduce dependency on petrochemicals and promote circular economy initiatives by utilizing waste-to-value strategies.

Key Market Points:

✅ Growing Demand for Bio-Based & Sustainable Ingredients: Increased focus on eco-friendly, non-toxic, and renewable resources. ✅ Expanding Applications: Biotech ingredients are widely used in cosmetics, fragrances, food flavors, nutraceuticals, and pharmaceuticals. ✅ Advancements in Fermentation & Synthetic Biology: Cutting-edge technology enables the production of high-quality biotech actives. ✅ Rise in Clean Beauty & Green Chemistry: Consumers prefer non-GMO, natural, and biodegradable ingredients. ✅ Regulatory Support & Green Initiatives: Government policies promoting bio-based innovations and sustainability are boosting market growth. ✅ Personalized & Functional Ingredients: The emergence of customized biotech ingredients for targeted skincare and health benefits.

Conclusion

The Biotech Ingredients Market is set for strong expansion, fueled by sustainable innovations, regulatory support, and rising consumer demand for ethical and effective products. Companies focusing on biotech-driven ingredient solutions, fermentation-based production, and clean-label formulations are well-positioned to lead the next phase of industry transformation.

Read Full Report: https://www.snsinsider.com/reports/biotech-ingredients-market-4593

Contact Us:

Jagney Dave — Vice President of Client Engagement

Phone: +1–315 636 4242 (US) | +44- 20 3290 5010 (UK)

#Biotech Ingredients Market#Biotech Ingredients Market Size#Biotech Ingredients Market Share#Biotech Ingredients Market Report#Biotech Ingredients Market Forecast

0 notes

Text

Best Franchise Businesses to Start in India

Franchise Businesses in India have gained immense popularity over the years due to their proven business models, brand recognition, and support from the parent company. India, being one of the fastest-growing economies, provides a fertile ground for franchise businesses to thrive.

With an increasing entrepreneurial spirit and demand for established brands, investing in a franchise is an excellent way to start a business with reduced risk. If you are looking for the best franchise opportunities in India, this guide will help you explore some of the most profitable sectors and brands.

Why Invest in a Franchise Business in India?

Lower Risk – Franchises offer a tested business model, minimizing risks compared to starting a business from scratch.

Brand Recognition – Customers trust well-established brands, leading to faster revenue generation.

Training & Support – Franchisees receive training, marketing, and operational support from the franchisor.

Higher Success Rate – Franchise businesses have a significantly higher success rate compared to independent startups.

Scalability – Many franchise models allow for expansion, enabling entrepreneurs to grow their business over time.

Best Franchise Businesses to Start in India

1. Food & Beverage Franchise

The food and beverage industry is one of the most lucrative sectors in India. People are always looking for quality food, making it a thriving market for franchises.

McDonald's – A globally recognized fast-food chain with high brand value.

Domino’s Pizza – A leading pizza brand with strong market penetration in India.

KFC – Famous for its fried chicken, KFC has a vast customer base.

Subway – A healthier fast-food option with growing demand.

Barbeque Nation – A popular casual dining restaurant with a successful franchise model.

2. Retail Franchise

Retail franchises cover a wide range of products, including clothing, footwear, electronics, and more. India’s retail sector is booming due to increasing disposable income and changing consumer preferences.

Reliance Trends – A well-known fashion brand with a strong presence.

Bata – One of India’s leading footwear brands.

Reebok – A famous sportswear and fitness brand.

Tanishq – A reputed jewelry brand by Tata Group.

Raymond – A trusted brand for men’s fashion and formal wear.

3. Education & Coaching Franchise

The education sector in India is growing rapidly, making coaching and training franchises highly profitable.

Kidzee – A popular preschool franchise with a structured curriculum.

EuroKids – Another top preschool chain with great franchise potential.

NIIT – Specializing in IT and professional training programs.

TIME (Triumphant Institute of Management Education) – A leading coaching institute for competitive exams.

Byju’s Learning Center – An innovative EdTech company with high demand.

4. Healthcare & Pharmacy Franchise

The healthcare industry is an evergreen sector with increasing demand for quality services.

Apollo Pharmacy – One of India’s largest pharmacy chains.

Dr. Batra’s – A leading homeopathy clinic franchise.

PathCare Labs – A reputed diagnostics and pathology chain.

VLCC – A top wellness and beauty brand.

MedPlus – A growing pharmacy retail chain.

5. Beauty & Wellness Franchise

The beauty and wellness industry in India is flourishing due to an increased focus on self-care and grooming.

Lakmé Salon – One of the most popular beauty salon chains.

Jawed Habib Hair & Beauty – A trusted brand in hair and beauty services.

Naturals Salon – A fast-growing beauty and wellness franchise.

VLCC – Offers weight management and beauty services.

BBlunt – A premium salon chain gaining popularity.

6. Automobile Franchise

With rising vehicle ownership, automobile service and dealership franchises are lucrative business opportunities.

Hero MotoCorp Dealership – India’s leading two-wheeler brand.

Maruti Suzuki Service Station – A highly sought-after automobile franchise.

Mahindra First Choice – A used-car dealership with strong demand.

Castrol Bike Point – Specializing in bike servicing and maintenance.

Shell Petrol Pump – A profitable fuel station franchise.

7. E-commerce & Logistics Franchise

With the growth of online shopping, logistics and courier services have become essential.

DTDC Courier & Cargo – One of the most trusted courier franchises in India.

Blue Dart – A premium logistics company with strong market demand.

Delhivery – A fast-growing e-commerce logistics firm.

Amazon Delivery Partner – A great opportunity in the booming e-commerce sector.

DHL Express – A reputed international logistics company.

How to Choose the Right Franchise Business?

When selecting a franchise, consider the following factors:

Investment Budget – Choose a franchise that fits your financial capacity.

Market Demand – Ensure there is a strong demand for the business in your location.

Franchisor Support – Look for brands that offer extensive training and support.

Profit Margins – Evaluate the revenue potential and profitability.

Competition – Analyze existing competitors before investing.

Conclusion

Franchise Businesses in India provide a fantastic opportunity for aspiring entrepreneurs to enter the market with reduced risk and established brand credibility. Whether you are interested in food, retail, education, healthcare, or logistics, there are numerous profitable franchise options to explore. By choosing the right franchise, conducting thorough research, and leveraging franchisor support, you can build a successful business in India.

0 notes

Text

North America Biodefense Market Trends, Size, Segment and Growth by Forecast to 2030

The North America Biodefense Market is on a significant growth trajectory, projected to increase from US$ 1,569.29 million in 2019 to US$ 3,357.83 million by 2027, representing a compound annual growth rate (CAGR) of 10.1% from 2020 to 2027. Several key factors are driving this growth, including favorable government initiatives, the rising frequency of natural outbreaks, and increased adoption of advanced technologies in the biodefense space. ��𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 - https://www.businessmarketinsights.com/sample/TIPRE00009997

One of the major catalysts for the market's expansion is the growing prevalence of infectious diseases, such as Ebola, Zika virus, and the coronavirus. With the rapid emergence of new infectious diseases, such as SARS, MERS, and swine flu, the demand for effective biodefense measures—like vaccines and diagnostics—has never been higher. As the World Health Organization (WHO) and the U.S. Centers for Disease Control and Prevention (CDC) report, the rate of emerging infectious diseases is accelerating, and there have been numerous outbreaks over the last few decades, contributing to heightened awareness and the need for better biodefense capabilities.

In addition, the U.S. government’s significant funding and research initiatives, particularly in military and civilian biodefense sectors, are strengthening the market. The National Institutes of Health (NIH) plays a key role by supporting research on infectious diseases and biodefense, developing new diagnostics, therapeutics, and vaccines. Furthermore, recent agreements, such as the one between Emergent BioSolutions and Vaxart for the development of an oral vaccine for COVID-19, reflect the ongoing push for innovation in this field.

Despite these positive trends, the market does face challenges. The limited reach of biodefense organizations, especially in regions with limited resources, can hinder global preparedness and response efforts. Nonetheless, increasing technological advancements and the growing global need for effective biodefense measures are expected to drive the market forward.

In terms of regional performance, the U.S. holds the largest market share in the North American biodefense market and is expected to continue to grow at a strong pace due to the country’s economic strength, well-established biotechnology players, and substantial investments in biodefense by military and civilian agencies. The U.S. is investing heavily in biodefense technologies to address potential biological threats and ensure public health security, contributing to its dominant position in the market.

Strategic insights for the North American biodefense market reveal critical trends, challenges, and opportunities. By leveraging data analytics, stakeholders can anticipate shifts in the market and identify emerging opportunities for differentiation. These insights enable companies to tailor their strategies, invest in underexplored segments, and position themselves for long-term success in this fast-evolving market. This foresight is essential for achieving profitability and gaining a competitive edge in the ever-changing landscape of biodefense. About Us:

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Défense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications Author’s Bio: Akshay Senior Market Research Expert at Business Market Insights

0 notes