#Fluid Power Equipment Market Trends

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Premium Tumblr themes are available from anywhere between $9 to $49.

Text

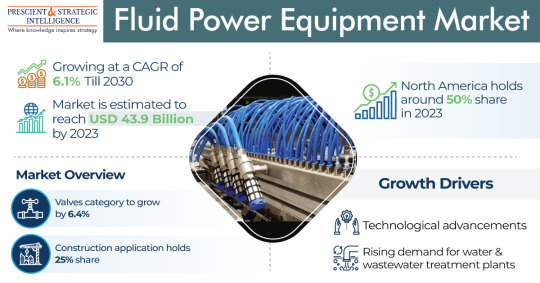

Fluid Power Equipment Market Will Touch USD 66.0 Billion in 2030

The fluid power equipment market was USD 43.9 billion in 2023, which will rise to USD 66.0 billion, advancing at a 6.1% compound annual growth rate, by 2030.

The growth of this industry is mainly because of the increasing need for water and wastewater treatment plants, and the continuous technological developments.

In 2023, hydraulic led the type category, with a revenue of USD 26.3 billion. This can be ascribed to the cost-effectiveness and high efficiency of this type, and its extensive adoption in oil & gas and construction applications.

The pneumatic category, on the other hand, will propel at a healthy rate during this decade. This is because these systems rely on compressed air pressure to send power and are extensively employed in numerous industrial applications.

Furthermore, pneumatic valves are available in different designs, sizes, and configurations, and thus, allow free flow in a single direction and avoid flow in the opposite direction.

In 2023, the construction category, based on end user, was the largest contributor to the fluid power equipment market, with a 25% share. This can be because of the high usefulness of these components in various applications like material demolition or handling in the construction sector.

The automotive category, on the other hand, is advancing at a tremendous rate, because of the increasing customer's disposable salary, along with the increasing standards of living, worldwide.

Motors is leading the component category. This can be because motor components provide great torque & power, and are extensively employed across various sectors, including agriculture, construction, and automotive.

Moreover, the developments in motor technologies enhance their performance and efficiency, and thus, are cost-effective solutions for businesses to utilize for different applications.

On the other hand, the valves category will advance at the highest rate during this decade. This is ascribed to the growing requirement for valves to track high pressure, which will boost the demand for valve components.

North America led the industry in 2023, with a 50% share. This can be attributed to the existence of greater infrastructure, coupled with the rising progression in R&D and manufacturing activities.

Moreover, the increasing count of initiatives implemented to guarantee the worker's safety in oil & gas and chemicals sectors further boost the regional industry growth.

APAC will propel at the highest rate, of 6.5%, in the coming years. This will be because of the surging urbanized populace along with the increasing requirement for energy, and the progression of the construction and automobile sectors in Japan, China, and India.

With the rise in the requirement for water & wastewater treatment plants, the fluid power equipment industry will continuously progress in the coming years.

Source: P&S Intelligence

#Fluid Power Equipment Market Share#Fluid Power Equipment Market Size#Fluid Power Equipment Market Growth#Fluid Power Equipment Market Applications#Fluid Power Equipment Market Trends

1 note

·

View note

Text

Exploring the Growing $21.3 Billion Data Center Liquid Cooling Market: Trends and Opportunities

In an era marked by rapid digital expansion, data centers have become essential infrastructures supporting the growing demands for data processing and storage. However, these facilities face a significant challenge: maintaining optimal operating temperatures for their equipment. Traditional air-cooling methods are becoming increasingly inadequate as server densities rise and heat generation intensifies. Liquid cooling is emerging as a transformative solution that addresses these challenges and is set to redefine the cooling landscape for data centers.

What is Liquid Cooling?

Liquid cooling systems utilize liquids to transfer heat away from critical components within data centers. Unlike conventional air cooling, which relies on air to dissipate heat, liquid cooling is much more efficient. By circulating a cooling fluid—commonly water or specialized refrigerants—through heat exchangers and directly to the heat sources, data centers can maintain lower temperatures, improving overall performance.

Market Growth and Trends

The data centre liquid cooling market is on an impressive growth trajectory. According to industry analysis, this market is projected to grow USD 21.3 billion by 2030, achieving a remarkable compound annual growth rate (CAGR) of 27.6%. This upward trend is fueled by several key factors, including the increasing demand for high-performance computing (HPC), advancements in artificial intelligence (AI), and a growing emphasis on energy-efficient operations.

Key Factors Driving Adoption

1. Rising Heat Density

The trend toward higher power density in server configurations poses a significant challenge for cooling systems. With modern servers generating more heat than ever, traditional air cooling methods are struggling to keep pace. Liquid cooling effectively addresses this issue, enabling higher density server deployments without sacrificing efficiency.

2. Energy Efficiency Improvements

A standout advantage of liquid cooling systems is their energy efficiency. Studies indicate that these systems can reduce energy consumption by up to 50% compared to air cooling. This not only lowers operational costs for data center operators but also supports sustainability initiatives aimed at reducing energy consumption and carbon emissions.

3. Space Efficiency

Data center operators often grapple with limited space, making it crucial to optimize cooling solutions. Liquid cooling systems typically require less physical space than air-cooled alternatives. This efficiency allows operators to enhance server capacity and performance without the need for additional physical expansion.

4. Technological Innovations

The development of advanced cooling technologies, such as direct-to-chip cooling and immersion cooling, is further propelling the effectiveness of liquid cooling solutions. Direct-to-chip cooling channels coolant directly to the components generating heat, while immersion cooling involves submerging entire server racks in non-conductive liquids, both of which push thermal management to new heights.

Overcoming Challenges

While the benefits of liquid cooling are compelling, the transition to this technology presents certain challenges. Initial installation costs can be significant, and some operators may be hesitant due to concerns regarding complexity and ongoing maintenance. However, as liquid cooling technology advances and adoption rates increase, it is expected that costs will decrease, making it a more accessible option for a wider range of data center operators.

The Competitive Landscape

The data center liquid cooling market is home to several key players, including established companies like Schneider Electric, Vertiv, and Asetek, as well as innovative startups committed to developing cutting-edge thermal management solutions. These organizations are actively investing in research and development to refine the performance and reliability of liquid cooling systems, ensuring they meet the evolving needs of data center operators.

Download PDF Brochure :

The outlook for the data center liquid cooling market is promising. As organizations prioritize energy efficiency and sustainability in their operations, liquid cooling is likely to become a standard practice. The integration of AI and machine learning into cooling systems will further enhance performance, enabling dynamic adjustments based on real-time thermal demands.

The evolution of liquid cooling in data centers represents a crucial shift toward more efficient, sustainable, and high-performing computing environments. As the demand for advanced cooling solutions rises in response to technological advancements, liquid cooling is not merely an option—it is an essential element of the future data center landscape. By embracing this innovative approach, organizations can gain a significant competitive advantage in an increasingly digital world.

#Data Center#Liquid Cooling#Energy Efficiency#High-Performance Computing#Sustainability#Thermal Management#AI#Market Growth#Technology Innovation#Server Cooling#Data Center Infrastructure#Immersion Cooling#Direct-to-Chip Cooling#IT Solutions#Digital Transformation

2 notes

·

View notes

Text

Valves Market is Estimated to Witness High Growth

Valves Market is Estimated to Witness High Growth Owing to Rising Constructional and Infrastructure Development Activities The valves market comprises products such as gate valves, globe valves, check valves, butterfly valves, ball valves and pressure regulating valves which are used to control the flow, pressure and direction of fluids. Valves are extensively used in power plants, refineries, oil & gas, water & wastewater and construction activities. These products play a key role in fluid transportation and management which makes them an integral component across various industrial sectors. Rising infrastructure development projects across both developed and developing nations are augmenting the demand for valves. Moreover, growing pipeline networks for oil & gas transportation is also favoring market growth. The Global valves market is estimated to be valued at US$ 83 Mn in 2024 and is expected to exhibit a CAGR of 3.5% over the forecast period 2024 To 2031. Key Takeaways Key players operating in the valves market are Tyson Foods, Inc., JBS S.A., Pilgrim's Pride Corporation, Wens Foodstuff Group Co. Ltd., BRF S.A., Perdue Farms, Sanderson Farms, Baiada Poultry, Bates Turkey Farm, and Amrit Group. The major players are focusing on capacity expansion plans and mergers & acquisitions to gain market share. Rising population and changing diets are expected to fuel the growth of the poultry sector which presents significant opportunities for valve manufacturers. With the growing poultry industry, demand for processing equipment including valves is also projected to rise substantially over the forecast period. The global valves market is estimated to witness growth across key regions such as North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. This can be attributed to surging investments in oil & gas, water & wastewater infrastructure, and industrial development projects worldwide. Emerging economies with high urbanization rates like China and India also offer lucrative prospects for market expansion. Market Drivers The key driver behind the Valves Market Demand is the increasing constructional and infrastructure development activities worldwide. There is huge government focus as well as private investments toward projects such as roadways, railways, metro stations, power generation, water supply, etc. which involves extensive use of valves in various process applications. Further, the rising need for energy and growing focus on rural electrification has boosted investments in power transmission and distribution sector augmenting valves demand.

PEST Analysis

Political: The valves market is regulated by laws pertaining to safety, environmental protection and quality standards. New regulations regarding emissions could impact demand patterns. Economic: Changes in the global and regional economic conditions directly impact spending on industries like oil & gas, energy & power, and water & wastewater management which influences Valves demand. Social: Growing population and urbanization is increasing requirements for water, energy and other infrastructure development which boost the usage of valves. Technological: Advancements in materials and designs of valves are improving efficiency, lowering costs and enabling usage in newer applications. Digitalization is also aiding remote monitoring of industrial valves. The regions concentrating maximum valves market share in terms of Valves Market Size and Trends include North America, Europe and Asia Pacific. North America accounts for a major portion owing to strong presence of end-use industries like oil & gas and significant infrastructure spending. Europe and Asia Pacific are also sizable markets led by Germany, China, India respectively. The fastest growing regional market for valves is expected to be Asia Pacific led by increasing investments in water & wastewater management, power projects and industrial activities in China and India. Rising standards of living and initiatives to improve urban infrastructure will further drive the demand across developing nations in the region.

Get more insights Valves Market

Discover the Report for More Insights, Tailored to Your Language.

French German Italian Russian Japanese Chinese Korean Portuguese

About Author:

Ravina Pandya, Content Writer, has a strong foothold in the market research industry. She specializes in writing well-researched articles from different industries, including food and beverages, information and technology, healthcare, chemical and materials, etc. (https://www.linkedin.com/in/ravina-pandya-1a3984191)

#Coherent Market Insights#Valves Market#Control Valves#Globe Valves#Plug Valves#Gate Valves#Ball Valves#Butterfly Valves

2 notes

·

View notes

Text

My headcanon Universe 6 technology

1)U6FD Combat Light Armor Suit is a specialized and unique Light Armor in Universe 6 designed specifically for the needs of assassins and other specialized covert operatives. This light armour possesses enhanced mobility tools, such as an accelerator to increase speed and mobility. Additionally, the Light Armor includes a Ki Oscillator, which acts as a powerful weapon capable of emitting destructive blasts. U6FD combat light armour also features a Ki circumventor, which is engineered to hide the user’s presence, preventing Ki detecting mechanisms or other Ki-focused devices from identifying their presence.(It made by Frost company, is it a trend product on the black market)

2)The Ki Oscillator is a unique weapon in Universe 6, which allows its user to wield immense power through the use of energy fluctuations that amplify and manipulate external energy into destructive energy waves. This weapon can harness an extraordinary amount of Ki,This energy then oscillates and magnifies, allowing it to emit destructive beams and blasts. The Ki Oscillator is an incredibly powerful, yet difficult-to-master weapon, requiring extensive training and discipline in advanced Ki manipulation.

Ki Oscillator actually is a type of special microchip that put in human body, most for it will put at arm or palm. Ki Oscillator have 101~1k logic gates or 1,001~10k transistors. Ki Oscillator is a Nanoscale devices. Ki Oscillator is made by nanomaterials that come from a Nanoorganisms and mix with specail Ki-conductor mental. (Only the part that connect to human body use nanomaterials that come from a Nanoorganisms.) Ki Oscillator no need to use electricity, it use Ki as the Power source.

3)Ki Energy Fluid (KEF) is a specialized product in Universe 6, which utilizes specialized technology to process Ki particles into a conductive liquid state. This liquid possesses immense potential energy due to the high concentration of Ki, allowing it to be used for a number of applications, such as energy generation, propulsion, or even as a power source. KEF can be harvested from large numbers of individuals with high Ki levels, or can be extracted and processed in specialized facilities.

4)Suspend (SUS) is a technology product Universe 6, which acts as a special form of suspension technology, designed to hold an individual in suspension. This state of suspended animation has various uses, including keeping individuals in a stasis for medical purposes, or preventing a dangerous individual from acting. Suspension technology is used extensively in Universe 6, both by individuals for specific purposes, and occasionally as part of various technological systems.

5)The Ki Energy-Gathering Object (KEGO) is a technology product in the Universe 6, which acts as a device capable of gathering and concentrating the user's Ki, the life force of beings in the setting. It utilizes a special crystal which acts as a vessel for the concentrated Ki, and redirects the energy to create bursts of destruction, or as a source of energy to enhance a person's capabilities. It can also be used to draw out hidden Ki and reveal hidden power in individuals, making it a highly sought after tool for anyone who wishes to master their Ki energy.

6)Organic Matter Conversion Ki Technology (OMCKT) is a technology used within Universe 6, which allows for the manipulation of organic matter into a form of Ki energy. This technology uses a specialized device which converts the molecular structure of organic materials into a synthetic version of the life energy, allowing for the controlled and targeted conversion of living beings into an energy source to enhance one's Ki and power.

7)R7SS-20 Photon Armor Suit: Contains cloaking technology that allows the wearer to become virtually invisible in the environment. Equipped with 20 energy shield that activates when attacked, providing additional protection. It integrates biological monitoring technology and can monitor the wearer's physiological parameters in real time, such as heart rate, body temperature, etc. Equipped with an intelligent system, it can interact with the wearer to provide information, navigation or execute instructions. Contains a series of enhanced functions, such as enhanced strength, speed, endurance, allowing the wearer to perform special tasks or survive in extreme environments. have Ki circumventor, which is engineered to hide the user’s presence, preventing Ki detecting mechanisms or other Ki-focused devices from identifying their presence.(It made by Frost company, is it a trend product on the black market).

8)Optical Brain: It is a computer system based on optical components and a brain-computer interface technology that uses light signals to interact with computers or other devices.

2 notes

·

View notes

Text

Elevate Your Brand with a Fashion Shoot Studio: Cellar Door Studio

Elevate Your Brand with a Fashion Shoot Studio: Cellar Door Studio

In the fashion world, imagery is everything. It is a powerful picture that can either make or break a brand's identity by resonating with an audience and making an indelible impression. And where a dedicated fashion shoot studio plays a key role in the process is Cellar Door Studio. This creative haven is designed for brands and photographers seeking to create high-quality visuals that are both inspiring and captivating.

Why Choose a Fashion Shoot Studio?

A fashion shoot studio is not just some empty space, but it's an environment designed to bring creative visionaries to life. Such places are perfectly suited so photographers, models, and designers can create campaigns that are utterly exquisite. Fitted with modern technology, a fluid design, and professional light setting, it is suited perfectly for displaying

There are many advantages of a studio shoot:

Controlled Environment: Unlike outdoor shoots, which may be dependent on the unpredictable weather and lighting, complete control over every aspect is possible in a studio shoot.

Versatility: Most studios, like Cellar Door Studio, can hold various creative styles and themes through adjustable backdrops, props, and equipment.

Professional Equipment: High-end cameras, lighting rigs, and post-production tools guarantee that every shot is picture-perfect.

Expert Support: All studios bring a team of professionals, which can easily aid with the technical setup, styling, and creative direction.he detail-rich nature of fashion apparel and accessories.

What Makes Cellar Door Studio Stand Out?

Cellar Door Studio is a prime, premier fashion shoot studio placed in an ideal location to set the gold standard in its industry. Here's why it's unique:

Inspiring Design: With a modern aesthetic that is sleek, Cellar Door Studio provides a visually stimulating atmosphere that fosters creativity. The space was carefully curated to balance functionality with style, ensuring seamless workflow during shoots.

Equipped with full facilities: The studio is equipped with all the advanced photography equipment, luxurious dressing rooms, and comfortable lounges. High-speed Wi-Fi, spacious makeup areas, and refreshments are also available for a hassle-free experience.

Versatile Spaces: Whether you’re shooting for a high-fashion editorial or a minimalist lookbook, Cellar Door Studio offers versatile settings that can be tailored to your specific vision. The customizable backdrops and modular furniture add flexibility to your creative process.

Experienced Team: The professionals at Cellar Door Studio are not just staff but partners in your creative journey. From lighting technicians to creative consultants, their expertise ensures that your vision is executed flawlessly.

Crafting Unforgettable Campaigns

Fashion campaigns are more than precision; they need a piece of art. This Cellar Door Studio is, therefore, excellent at executing this process. The studios provide an open space allowing creativity to thrive; the studio was part of many successful campaigns that have graced magazine covers, billboards, and social media feeds.

The studio is most memorable in terms of how easy it is to incorporate contemporary trends. In a time ruled by digital media, it's equipped with the facilities to ensure that your brand story gets to the correct target market in the finest possible quality.

Booking Your Session at Cellar Door Studio

The process of planning a photoshoot might be scary, but this is taken away by the simplicity in booking at Cellar Door Studio. From an initial consultation to post-production support, every single step is streamlined to guarantee an easy shoot. Be it hours, days, or projects longer than that, the options available for reservations will certainly accommodate your every need and budget.

It has been well-rated among photographers, designers, and marketing teams due to the commitment of the studio toward excellence.Its blend of professionalism, creativity, and the state-of-the-art resources makes it the go-to fashion shoot studio for people who aim to make a statement in the competitive world of fashion.

Conclusion

A well-executed fashion shoot can change the image of a brand, creating a powerful narrative that will touch the hearts of the audiences. The right fashion shoot studio is a very important step in this process, and Cellar Door Studio stands out as a leader in the field. It's the perfect space for bringing your creative vision to life with its inspiring design, cutting-edge facilities, and expert team. Step into Cellar Door Studio and elevate your brand to new heights.

0 notes

Link

0 notes

Text

Navigating the High-Integrity Pressure Protection Systems Industry: Opportunities and Challenges

The global high-integrity pressure protection systems market size was estimated at USD 456.8 million in 2023 and is projected to reach at a CAGR of 7.3% from 2024 to 2030. The compelling organizations are investing in advanced safety systems like high-integrity pressure protection systems (HIPPS) due to stringent safety regulations and standards in sectors such as oil and gas, chemicals, and pharmaceuticals. These systems are designed to prevent overpressure incidents in critical process pipelines and equipment, thereby safeguarding personnel, the environment, and assets.

Technological advancements in automation and control systems are enhancing the capabilities and reliability of HIPPS. Modern HIPPS incorporates sophisticated sensors, actuators, and logic solvers that can detect pressure deviations swiftly and initiate rapid shutdown procedures. This level of automation not only minimizes human error but also enables faster response times, reducing the likelihood of equipment damage and operational downtime. Industries are thus drawn to HIPPS not only for their safety benefits but also for their potential to optimize operational efficiency and maintain continuous production.

High-Integrity Pressure Protection Systems Market Report Highlights

Hydraulic/Mechanical HIPPS accounted for 59.8% of the revenue share in 2023. This type of HIPPS caters to industries where robustness, simplicity, and reliability are vital considerations.

The demand for electronics HIPPS is primarily driven by advancements in automation and digitalization across industrial sectors.

The oil & gas segment accounted for 26.5% of the revenue share in 2023 and is expected to expand at a notable CAGR from 2024 to 2030.

Power generation facilities, whether thermal, nuclear, or renewable, operate complex processes involving high-pressure steam, gases, and fluids.

The demand for HIPPS components is propelled by technological advancements in the field. Components such as pressure sensors, logic solvers, valves (including pilot valves and check valves), actuators, and controllers form the core infrastructure of HIPPS systems.

The growth of the High Integrity Pressure Protection Systems (HIPPS) market in Asia Pacific is driven by several key factors that reflect both regional economic expansion and increasing industrial safety standards.

Global High-integrity Pressure Protection System Market Report Segmentation

This report forecasts revenue growth at global, regional & country levels and provides an analysis on the industry trends in each of the sub-segments from 2018 to 2030. For this study, Grand View Research has segmented the high-integrity pressure protection systems market based on type, offering, end use, and region.

Type Outlook (Revenue, USD Million, 2018 - 2030)

Electronic HIPPS

Hydraulic/Mechanical HIPPS

Offering Outlook (Revenue, USD Million, 2018 - 2030)

Component

Services

End Use Outlook (Revenue, USD Million, 2018 - 2030)

Oil & Gas

Water & Wastewater

Food & Beverage

Chemicals

Food & Beverage

Pharmaceutical

Power Generation

Others

Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

US

Canada

Mexico

Europe

UK

Germany

France

Italy

Spain

Asia Pacific

Japan

China

India

Australia

South Korea

Latin America

Brazil

Argentina

Middle East & Africa

South Africa

Saudi Arabia

UAE

Order a free sample PDF of the High-Integrity Pressure Protection Systems Market Intelligence Study, published by Grand View Research.

0 notes

Text

0 notes

Text

Fashion News 2024: Upcoming Trends and Predictions from Industry Experts

As we step into 2024, the fashion world is abuzz with excitement about the trends and innovations that will shape the industry. From reimagined classics to revolutionary tech-inspired designs, the year ahead promises a thrilling mix of creativity and practicality. Here’s a look at the key trends and expert predictions that will dominate fashion in 2024.

1. Emphasis on Sustainability and Ethical Practices

Sustainability continues to be a cornerstone of modern fashion, and in 2024, the industry is expected to elevate its commitment to ethical practices. Experts predict a surge in brands adopting circular fashion models, focusing on recycling and upcycling to minimize waste. Innovations in sustainable materials, like lab-grown leather and biodegradable fabrics, will become mainstream.

Consumers are increasingly prioritizing transparency, pushing brands to adopt blockchain technology to trace the origins of their materials. According to industry expert Stella McCormick, “2024 will be a turning point where sustainability isn’t just a choice—it’s an expectation.”

2. The Revival of Retro Styles

Fashion is cyclical, and 2024 will see a strong revival of retro aesthetics. Think 1970s bohemian vibes, bold 1980s power dressing, and the minimalist chic of the 1990s. Vintage-inspired clothing will dominate both runways and retail stores, with designers putting a modern twist on classic silhouettes.

Accessories like oversized sunglasses, statement belts, and bucket hats will also make a comeback. This nostalgic wave is driven by the younger generation’s fascination with past eras, amplified by the influence of social media platforms like TikTok and Instagram.

3. Tech-Driven Fashion: The Rise of Digital and Smart Clothing

Technology continues to revolutionize the fashion industry, and 2024 is set to see an explosion of digital and tech-driven designs. Augmented reality (AR) and virtual reality (VR) will redefine shopping experiences, allowing consumers to virtually try on clothes from the comfort of their homes.

Smart clothing, equipped with features like temperature control and health monitoring, is expected to gain traction. Additionally, the rise of digital fashion—virtual garments designed for avatars or online personas—is becoming a lucrative market. As per tech analyst Alex Hart, “The intersection of fashion and technology is no longer niche—it’s the future.”

4. Gender-Fluid and Inclusive Fashion

Inclusivity will take center stage in 2024, with more brands embracing gender-neutral designs and diverse representation. The demand for clothing that defies traditional gender norms is growing, and designers are responding with unisex collections that prioritize comfort and individuality.

Plus-size and adaptive fashion will also see significant growth, reflecting the industry’s commitment to catering to all body types and abilities. This shift is not just about representation but about creating a more accepting and empowering fashion landscape.

5. Bold and Experimental Color Palettes

While neutrals and earth tones have dominated recent years, 2024 will see a resurgence of bold, vibrant colors. Shades like electric blue, fiery red, and neon green are expected to take the spotlight, adding energy and optimism to wardrobes.

Pantone’s Color of the Year is anticipated to influence this trend significantly. Designers are also experimenting with color-blocking and unconventional pairings, encouraging consumers to embrace creativity and self-expression through their outfits.

6. Customization and Personalization

In an era where individuality is celebrated, customized fashion will thrive in 2024. From monogrammed handbags to bespoke tailoring, consumers are seeking unique pieces that reflect their personality. Advances in AI and 3D printing are making personalization more accessible, allowing brands to offer tailored options at scale.

Luxury labels are leading this movement, but high-street brands are quickly catching up, offering affordable ways for customers to put their own spin on ready-to-wear pieces.

7. Global Influences in Fashion

Fashion in 2024 will be a melting pot of global cultures, with designers drawing inspiration from diverse traditions and artistry. African prints, South Asian embroidery, and Scandinavian minimalism are just a few examples of styles expected to make waves.

Collaborations between international designers and local artisans will bring authenticity and storytelling to the forefront of fashion, enriching the industry with fresh perspectives.

Conclusion

The year 2024 is set to be an exciting chapter in fashion history, blending innovation with nostalgia, sustainability with bold creativity, and inclusivity with individuality. As industry leaders continue to push boundaries, consumers can look forward to a year of redefined style and groundbreaking trends. Whether it’s a return to vintage glamour, the rise of smart clothing, or a celebration of diversity, the future of fashion promises something for everyone.

Stay tuned to fashion news to keep up with these trends as they unfold—2024 is shaping up to be a year where style meets substance like never before!

0 notes

Text

The Growing Trend of Hydraulic Plate Bending Machines in Heavy Industries

Introduction

In the evolving landscape of heavy industries, precision and efficiency have become more critical than ever. Among the equipment revolutionizing these industries, hydraulic plate bending machines stand out as a game-changer. Whether you're shaping metal for wind turbines, shipbuilding, or construction, these plate bending machines bring unmatched precision to the table.

But why are these machines gaining so much traction? And how does leading manufacturer Himalaya Machinery play a role in this growing trend? Let’s explore this transformative shift and understand its significance for metal manufacturers.

1. The Importance of Plate Bending Machines in Heavy Industries

Heavy industries demand precision engineering. Whether it’s shaping steel for massive structures or fabricating components for machinery, plate bending machines form the backbone of metal fabrication. These machines ensure uniformity, reduce waste, and speed up production timelines. Without them, meeting today’s industrial demands would be nearly impossible.

2. What Are Hydraulic Plate Bending Machines?

A hydraulic plate bending machine uses hydraulic force to bend and shape metal plates. Unlike traditional mechanical machines, these leverage fluid power for higher precision and energy efficiency. Think of it like pressing clay into a mold—the hydraulic system applies consistent force to create perfect bends.

3. How Does Pre Bending Enhance Efficiency?

Pre bending is the process of preparing the edges of a metal plate for bending. It eliminates the risk of irregularities at the edges, ensuring smooth and accurate bends. By focusing on pre bending, manufacturers save material and reduce wastage, directly impacting profitability.

4. Key Features of Hydraulic Plate Bending Machines

Here are the standout features of modern hydraulic plate bending machines:

Precision Bending: Ensures consistent results every time.

Energy Efficiency: Hydraulic systems consume less power compared to mechanical counterparts.

Durability: Built to handle heavy-duty operations.

User-Friendly Controls: Easy-to-operate panels streamline operations.

5. Applications of Plate Bending Machines in Various Sectors

Plate bending machines find applications across multiple industries, including:

Shipbuilding: Shaping large metal plates for hulls.

Wind Energy: Crafting towers and turbine components.

Automotive: Bending chassis and body components.

Construction: Fabricating beams and metal frameworks.

6. Why Himalaya Machinery Leads the Market?

India’s Himalaya Machinery, a heavy engineering company has emerged as a trusted name in the manufacturing of plate rolling machines. Known for their innovation, durability, and customer support, they provide cutting-edge solutions tailored to various industries. Their hydraulic models are designed to deliver unmatched performance, making them a go-to choice for metal manufacturers.

7. Benefits of Using Hydraulic Plate Bending Machines

Why should industries switch to hydraulic machines?

Time-Saving: Faster operations lead to higher productivity.

Reduced Material Waste: Enhanced precision minimizes errors.

Versatility: Suitable for bending various metals, including steel and aluminum.

Cost-Effective Maintenance: Easier to maintain with the right machine maintenance checklist.

8. Crafting a Machine Maintenance Checklist

Maintenance is key to ensuring the longevity of your machine. Here’s a basic machine maintenance checklist:

Regularly inspect hydraulic oil levels.

Check for wear and tear on mechanical parts.

Clean and lubricate components weekly.

Test safety features like emergency stops.

Keep software and firmware updated.

9. Tips for Selecting the Right Machine for Bending Metal

Choosing the right machine for bending metal can feel overwhelming. Consider the following:

Material Thickness: Ensure the machine can handle your material's thickness.

Bend Radius Requirements: Match the machine’s capability to your project needs.

Energy Efficiency: Look for models with lower power consumption.

Brand Reputation: Opt for trusted manufacturers like Himalaya Machinery.

10. Innovations in Plate Bending Technology

The integration of smart technology has transformed plate bending. Advanced hydraulic machines now feature:

CNC Controls: For enhanced precision and repeatability.

IoT Integration: Enabling remote monitoring and diagnostics.

Eco-Friendly Systems: Designed to minimize energy consumption.

11. The Role of Automation in Plate Bending Machines

Automation is reshaping how plate bending machines operate. From programmable settings to AI-assisted decision-making, automation reduces manual effort and enhances accuracy, making it an indispensable feature for modern manufacturers.

12. Common Challenges and Solutions in Plate Bending

Challenge: Material cracking during bending. Solution: Use pre bending and apply gradual force.

Challenge: Machine downtime. Solution: Follow a strict machine maintenance checklist to avoid unexpected breakdowns.

13. Future Trends in Hydraulic Plate Bending Machines

As industries evolve, so do their tools. Expect to see:

Greater Automation: Fully autonomous bending processes.

Green Manufacturing: Machines designed with sustainability in mind.

Enhanced Customization: Machines tailored to specific industry needs.

14. Customer Testimonials and Success Stories

Many manufacturers have shared success stories about using Himalaya Machinery’s hydraulic plate bending machines. One customer stated, “The precision and efficiency of these machines have transformed our production line.” Stories like these highlight the real-world impact of choosing the right equipment.

15. Conclusion

The rise of hydraulic plate bending machines in heavy industries marks a significant leap in efficiency and innovation. By investing in advanced solutions like those offered by Himalaya Machinery, manufacturers can stay competitive, reduce costs, and meet the growing demands of their industries.

0 notes

Text

How Intelligent PDUs and Immersion Cooling Work Together?

More efficient and durable data centres are needed than ever since data centres change fast. Businesses increasingly use high-density computing, but outdated IT equipment cooling methods can't keep up with the heat. Combined immersion cooling systems and intelligent power distribution units (PDUs) may transform data centres. Immersion Cooling liquid cooling technology swiftly removes heat, while intelligent PDUs optimise power utilisation. Together, they improve efficiency, reduce energy usage, and benefit the environment. This blog describes how these technologies alter data centre management.

The Functionality of Intelligent PDUs

Data centres rely on Intelligent PDU (power distribution units). All connected devices are powered and monitored. Innovative units can measure energy usage in real time, manage them remotely, and sense the surroundings, unlike ordinary PDUs. This functionality lets data centre administrator’s measure power usage down to the plugs, providing vital information. Security overload and remote reboot help keep systems up, making them more dependable. Knowing how to gather and interpret data enables you to make informed decisions that save power and reduce waste. This knowledge improves operations and extends infrastructure life.

Immersion Cooling: The Future of Thermal Management

Immersion cooling helps data centres regulate equipment temperature. This approach removes heat well because IT equipment is immersed in a thermally conductive liquid. Immersion cooling cools all parts equally, unlike air cooling, which may not operate effectively in crowded situations. More heat-absorbing than air, the liquid keeps crucial machinery at the appropriate temperature. Immersion cooling also reduces air conditioning demand, saving electricity. This novel cooling method effectively meets IT businesses' growing environmental concerns.

The Synergy of Intelligent PDUs and Immersion Cooling

Intelligent PDU and immersion cooling systems boost efficiency in innovative ways. Immersion cooling controls heat well, while Intelligent PDUs distribute power evenly. Intelligent Power Distribution Units (PDUs) track immersion-cooled power usage in real-time to identify efficiency improvements. If certain racks consume more power than predicted, data centre administrators can balance loads and improve efficiency. This synergy ensures the cooling system operates well while utilising little energy, making the system more stable. They collaborate on a data centre control system that controls electricity and temperature.

Cost Efficiency and Sustainability

Intelligent PDUs and Immersion Cooling save costs and increase speed. Traditional cooling methods can be expensive in regions that demand a lot of cooling. Immersion cooling eliminates extensive air conditioning systems, saving electricity. Companies may save energy and function more effectively by tracking their energy consumption using Intelligent PDUs. Lower energy costs mean a lesser carbon footprint, which aligns with worldwide company sustainability efforts. This one-stop solution addresses data centres' present demands and assures their long-term sustainability in an eco-friendly market.

Future Trends and Considerations

Intelligent PDUs with immersion cooling will become increasingly vital as technology advances. These systems may improve with intelligent tracking, AI-driven data, and enhanced cooling fluids. With modular architecture, data centres grow quickly and adapt to changing business demands. Additionally, energy and environmental regulations will encourage the usage of these devices. This united approach will improve efficiency and make companies leaders in ethical technology use. How Intelligent PDUs and immersion cooling work together as the business develops will determine data centre operations.

Conclusion

Combining Intelligent PDUs with immersion cooling technologies changes data centre management. These technologies improve electricity distribution and heat management, making infrastructure more reliable, cost-effective, and long-lasting. Combining these technologies will become more significant as organisations seek solutions to address high-density computer demands. This combination makes technology cleaner and more helpful and prepares enterprises for the future. Intelligent PDUs and immersion cooling are essential to a contemporary, efficient, green data centre. For getting better solutions choose Bentec Digital Solutions Pte Ltd for your sector.

0 notes

Text

Synthetic Lubricants Market Industry Outlook: Forecasting Market Trends and Growth for the Coming Years

Synthetic Lubricants Market Strategies: Taking Advantage of Trends to Drive Growth in 2032

The Synthetic Lubricants Market Report provides essential insights for business strategists, offering a comprehensive overview of industry trends and growth projections. It includes detailed historical and future data on costs, revenues, supply, and demand, where applicable. The report features an in-depth analysis of the value chain and distributor networks.

Employing various analytical techniques such as SWOT analysis, Porter’s Five Forces analysis, and feasibility studies, the report offers a thorough understanding of competitive dynamics, the risk of substitutes and new entrants, and identifies strengths, challenges, and business opportunities. This detailed assessment covers current patterns, driving factors, limitations, emerging developments, and high-growth areas, aiding stakeholders in making informed strategic decisions based on both current and future market trends. Additionally, the report includes an examination of the Automatic Rising Arm Barriers sector and its key opportunities.

According to Straits Research, the global Synthetic Lubricants Market market size was valued at USD 17.2 Billion in 2022. It is projected to reach from USD XX Billion in 2023 to USD 22.9 Billion by 2031, growing at a CAGR of 3.28% during the forecast period (2023–2031).

Get Free Request Sample Report @ https://straitsresearch.com/report/synthetic-lubricants-market/request-sample

TOP Key Industry Players of the Synthetic Lubricants Market

Royal Dutch Shell

ExxonMobil

Sasol

Valvoline

British Petroleum

Chevron

Morris Lubricants

Dow

Indian Oil

Petronas

Lukoil

Idemitsu Kosan

Fuchs

Total Energies

Sinopec

Global Synthetic Lubricants Market: Segmentation

As a result of the Synthetic Lubricants market segmentation, the market is divided into sub-segments based on product type, application, as well as regional and country-level forecasts.

By Applications

Engine Oil

Transmission Fluids and Hydraulic Fluids

Metalworking Fluids

Greases

Others

By End-User

Power Generation

Automotive and Transportation

Heavy Equipment

Food and Beverage

Others

By Type

Polyalphaolefin

Esters

Polyalkylene Glycol

Browse Full Report and TOC @ https://straitsresearch.com/report/synthetic-lubricants-market/request-sample

Reasons for Buying This Report:

Provides an analysis of the evolving competitive landscape of the Automatic Rising Arm Barriers market.

Offers analytical insights and strategic planning guidance to support informed business decisions.

Highlights key market dynamics, including drivers, restraints, emerging trends, developments, and opportunities.

Includes market estimates by region and profiles of various industry stakeholders.

Aids in understanding critical market segments.

Delivers extensive data on trends that could impact market growth.

Research Methodology:

Utilizes a robust methodology involving data triangulation with top-down and bottom-up approaches.

Validates market estimates through primary research with key stakeholders.

Estimates market size and forecasts for different segments at global, regional, and country levels using reliable published sources and stakeholder interviews.

About Straits Research

Straits Research is dedicated to providing businesses with the highest quality market research services. With a team of experienced researchers and analysts, we strive to deliver insightful and actionable data that helps our clients make informed decisions about their industry and market. Our customized approach allows us to tailor our research to each client's specific needs and goals, ensuring that they receive the most relevant and valuable insights.

Contact Us

Email: [email protected]

Address: 825 3rd Avenue, New York, NY, USA, 10022

Tel: UK: +44 203 695 0070, USA: +1 646 905 0080

#Synthetic Lubricants Market#Synthetic Lubricants Market Share#Synthetic Lubricants Market Size#Synthetic Lubricants Market Research#Synthetic Lubricants Industry#What is Synthetic Lubricants?

0 notes

Text

Key Factors Fueling the Growth of Heat Transfer Fluids Market

The global heat transfer fluids (HTF) market was valued at USD 11.06 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 3.7% from 2024 to 2030. This steady growth is largely driven by the increasing adoption of concentrated solar power (CSP) systems across the globe. CSP, which is a renewable energy technology that relies on solar power to generate electricity, heavily depends on heat transfer fluids to store and transfer the heat collected from the sun to power generation systems. This growing trend towards renewable energy sources is one of the major contributing factors to the rising demand for HTFs.

Heat transfer fluids are primarily industrial products that are derived from petroleum and serve to prevent overheating and store thermal energy. The production of these fluids typically involves the use of raw materials such as crude oil, silica, and base oils. These materials are processed to create fluids that have specific qualities essential for heat transfer processes. he key characteristics that define an effective HTF include:

1. Low Viscosity: This property is crucial for ensuring that the fluid can flow easily and efficiently within a system, facilitating the transfer of heat with minimal energy loss.

2. Non-Corrosive Nature: To prevent damage to pipes, systems, and equipment, HTFs need to be chemically stable and non-corrosive to metals and other materials used in the system.

3. High Thermal Conductivity and Diffusivity: These features ensure that heat is effectively transferred from one part of the system to another, maintaining efficiency in processes such as heating or cooling.

4. High Phase Transition Temperatures: HTFs are designed to withstand extreme temperatures, allowing them to maintain their thermal properties even under high heat conditions, making them suitable for both high-temperature processes and applications in cold climates.

Gather more insights about the market drivers, restrains and growth of the Heat Transfer Fluids Market

Regional Insights

The Asia Pacific heat transfer fluid market is currently the dominant regional market, driven by several macroeconomic factors. With high per capita income, strong manufacturing output, and rapid industrialization, the region continues to experience substantial growth. In 2023, Asia Pacific accounted for 47.9% of the global heat transfer fluid market share, making it the largest market for these products.

A major factor contributing to this market dominance is the rapid growth in the use of heating, ventilation, and air conditioning (HVAC) systems across the region. As countries like India and China undergo significant urbanization and face changing climatic conditions, the demand for energy-efficient HVAC systems continues to rise. The expanding urban populations, coupled with demographic shifts in these two economic powerhouses, are major drivers for the heat transfer fluid market in Asia Pacific. These systems require reliable and efficient heat management solutions, which heat transfer fluids provide, ensuring their integral role in the region's industrial, commercial, and residential sectors.

In addition to HVAC, other industries like automotive, chemical production, and manufacturing are also driving demand for heat transfer fluids. The increasing industrialization and infrastructure development in countries across the region ensure that heat transfer fluids remain a crucial component in various applications, from oil and gas to renewable energy.

Growth in Mexico's Chemical Industry

Mexico is another emerging market for heat transfer fluids, particularly driven by its chemical industry. Over the past few years, Mexico has seen significant investments aimed at expanding its manufacturing capabilities and diversifying its product offerings. The country has attracted high-level investments, which are supporting the continued sourcing of raw materials to strengthen its chemical sector. This has led to a surge in demand for heat transfer fluids used in the production processes of chemicals.

Furthermore, the growing export of chemicals to NAFTA (North American Free Trade Agreement) countries is expected to further propel demand for heat transfer fluids. As Mexican manufacturing plants ramp up production, the need for efficient heat management solutions, including heat transfer fluids, becomes increasingly critical to ensure optimal operational performance.

Mexico's strong presence in the plastic manufacturing industry also contributes to the growing demand for heat transfer fluids, as plastics production processes require reliable temperature regulation and energy-efficient thermal management.

Browse through Grand View Research's Petrochemicals Industry Research Reports.

• The global aerospace lubricants market size was valued at USD 2.13 billion in 2023 and is projected to grow at a CAGR of 5.0% from 2024 to 2030.

• The global polymer modified bitumen market size was valued at USD 12.86 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 4.0% from 2024 to 2030.

Key Companies & Market Share Insights

Leading companies in the heat transfer fluid market are employing a variety of organic and inorganic growth strategies to maintain and expand their market share. These strategies include expanding production capacities, entering into mergers and acquisitions (M&A), and forming joint ventures to diversify product portfolios and strengthen market presence globally.

1. Valvoline: In September 2023, Valvoline, a prominent player in the heat transfer fluid market, made a strategic move by investing in a European manufacturer of heat transfer fluids. This acquisition allows the company to expand its product range and enhance its ability to serve global consumers, strengthening its competitive position in the international market.

2. ORLEN Południe: In May 2023, ORLEN Południe, a leader in the renewable energy and chemical sectors, announced the successful completion of the first operational year of its BioPG plant, which focuses on converting glycerol into renewable propylene glycol. This development is a significant step towards producing more sustainable heat transfer fluids. The company collaborated with BASF, which provided its BioPG technology, while Air Liquide Engineering & Construction contributed by offering licensing, proprietary equipment, and basic engineering services to support the project.

3. Chevron: In February 2022, Chevron announced the acquisition of Renewable Energy Group, a deal that will enhance Chevron’s ability to deliver lower-carbon energy solutions. This acquisition is part of Chevron’s broader strategy to diversify its energy portfolio and increase its footprint in the renewable energy sector, which is increasingly relevant to the production and use of heat transfer fluids that are part of energy-efficient processes.

Key Heat Transfer Fluids Companies:

• Dynalene, Inc.

• Indian Oil Corporation Ltd. (IOCL)

• KOST USA, Inc.

• Hindustan Petroleum Corporation Ltd. (HPCL)Delta Western, Inc. (DWI)

• British Petroleum (BP)

• Huntsman Corporation

• Royal Dutch Shell Plc

• Eastman Chemical Company

• Phillips 66

• Chevron Co.

• BASF SE

• Exxon Mobil

• DowDuPont Chemicals

• Dalian Richfortune Chemicals Ltd.

• GJ Chemical

• Radco Industries Inc.

• LANXESS AG

• Schultz Chemicals

• Sasol Limited

• Evermore Trading Corporation

• Tashkent Industrial Oil Corporation

• Shaeffer Manufacturing Co.

• Paras Lubricants Limited.

Order a free sample PDF of the Heat Transfer Fluids Market Intelligence Study, published by Grand View Research.

#Heat Transfer Fluids Market#Heat Transfer Fluids Market Analysis#Heat Transfer Fluids Market Report#Heat Transfer Fluids Industry

0 notes

Text

Automotive Lubricants Market to be Worth $114.2 Billion by 2030

Meticulous Research®—a prominent global market research firm—has released a report titled "Automotive Lubricants Market by Product Type (Engine Oil, Transmission & Hydraulic Fluids, Gear Oil, Grease, Chain Oil, Brake Fluids), Vehicle Type, Composition, Sales Channel, and Geography - Global Forecast to 2030."

Download Research Report Sample @ https://www.meticulousresearch.com/download-sample-report/cp_id=5036

The report indicates that the automotive lubricants market is anticipated to reach $114.2 billion by 2030, with a compound annual growth rate (CAGR) of 7.8% during the forecast period. Key drivers for this growth include increasing demand for high-performance lubricants, rapid advancements in transportation infrastructure, a booming automotive industry with rising vehicle production, and a growing preference for sustainable lubricants. However, challenges such as decreased demand from electric vehicles and fluctuating raw material prices may impact market growth.

Emerging economies present significant growth opportunities, alongside the rising demand for eco-friendly lubricants. Nevertheless, the development of compatible lubricants for electric and hydrogen fuel cell vehicles, along with volatile pricing, could pose hurdles. A notable trend in the market is the increasing demand for thinner engine oils.

Meticulous Research® has segmented the market based on product type, vehicle type, composition, sales channel, and geography for comprehensive analysis. The study also assesses competitors and analyzes market dynamics at regional and national levels.

By product type, the market includes engine oil, transmission & hydraulic fluids, gear oil, grease, chain oil, brake fluids, and others. In 2024, engine oil is projected to dominate the market, driven by the need for improved fuel efficiency in internal combustion engine (ICE) vehicles and strong aftermarket demand. Meanwhile, the grease segment is expected to exhibit the highest CAGR during the forecast period.

In terms of vehicle type, the market is categorized into internal combustion engine vehicles, electric vehicles, natural gas engines, and hydrogen-powered vehicles. The internal combustion engine segment is forecasted to hold the largest market share in 2024, supported by advancements in efficiency and performance, as well as strict emissions regulations. Conversely, the electric vehicle segment is anticipated to grow at the fastest rate.

Browse in depth @ https://www.meticulousresearch.com/product/automotive-lubricants-market-5036

The market composition includes mineral oil lubricants, fully synthetic oil lubricants, and semi-synthetic lubricants. Fully synthetic oil lubricants are expected to dominate in 2024 due to their high performance and advantages in fuel economy and emissions reduction, and this segment is also projected to achieve the highest CAGR.

Sales channels are divided into original equipment manufacturers and aftermarket segments. The aftermarket is expected to lead the market share in 2024, fueled by increasing car ownership, particularly in emerging economies, and growing awareness of lubricant benefits for vehicle efficiency. This segment is also predicted to grow at the highest rate.

Geographically, the automotive lubricants market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific is expected to capture the largest market share in 2024, thanks to rapid automotive industry growth, strong government support, and the presence of key manufacturers. This region is also projected to see the highest CAGR.

**Key Players:**

Prominent players in the automotive lubricants market include Shell International B.V. (Netherlands), Exxon Mobil Corporation (U.S.), FUCHS PETROLUB SE (Germany), Motul (France), Phillips 66 Company (U.S.), Repsol, S.A. (Spain), SK Enmove Co., Ltd. (South Korea), China National Petroleum Corporation (China), Klüber Lubrication München Se & Co. KG (Germany), Amsoil Inc. (U.S.), Petróleo Brasileiro S.A. — Petrobras (Brazil), Valvoline Inc. (U.S.), Sinopec India (China), Chevron Corporation (U.S.), BP P.L.C. (U.K.), and Castrol Limited (U.K.).

Request Customization Report @ https://www.meticulousresearch.com/request-customization/cp_id=5036

0 notes