#Europe Next Generation Sequencing (NGS) Market trend

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

In 2020, 44% of users from Denmark used Tumblr daily.

Text

#Europe Next Generation Sequencing (NGS) Market trend#Europe Next Generation Sequencing (NGS) Market forcast#Europe Next Generation Sequencing (NGS) Market segment#Europe Next Generation Sequencing (NGS) Market overview#Europe Next Generation Sequencing (NGS) Market growth#Europe Next Generation Sequencing (NGS) Market share#Europe Next Generation Sequencing (NGS) Market demand

1 note

·

View note

Text

Precision Genomic Testing Market Size, Growth Outlook 2035

The global Precision Genomic Testing Market Size was estimated at 15.54 (USD Billion) in 2024. The Precision Genomic Testing Market Industry is expected to grow from 16.99 (USD Billion) in 2025 to 37.92 (USD Billion) till 2034, at a CAGR (growth rate) is expected to be around 9.33% during the forecast period (2025 - 2034).

Market Overview The Precision Genomic Testing Market is growing rapidly due to advancements in genomic sequencing, personalized medicine, and biomarker-driven therapies. Precision genomic testing enables early disease detection, targeted therapy selection, and risk assessment for genetic disorders. The increasing prevalence of cancer, rare genetic diseases, and chronic conditions has fueled demand for highly accurate and rapid genomic analysis. Moreover, the integration of artificial intelligence (AI) in genomic data interpretation is enhancing the efficiency of precision diagnostics.

Market Size and Share The global Precision Genomic Testing MarketSize was estimated at 15.54 (USD Billion) in 2024. The Precision Genomic Testing Market Industry is expected to grow from 16.99 (USD Billion) in 2025 to 37.92 (USD Billion) till 2034, at a CAGR (growth rate) is expected to be around 9.33% during the forecast period (2025 - 2034). North America holds the largest market share due to the presence of leading biotechnology firms, high investments in precision medicine, and widespread adoption of genomic testing in oncology. The Asia-Pacific region is projected to witness the highest growth, driven by rising government funding for genetic research, growing medical tourism, and increasing awareness of personalized treatments.

Market Drivers

Growing Adoption of Personalized Medicine: The demand for tailored treatment plans based on genetic profiling is increasing in oncology, cardiology, and neurology.

Advancements in Next-Generation Sequencing (NGS) Technologies: The development of rapid and cost-effective sequencing platforms is enhancing the accessibility of precision genomic testing.

Increasing Prevalence of Genetic Disorders and Cancer: The rise in hereditary diseases, rare genetic conditions, and tumor profiling needs is fueling market growth.

Integration of AI and Bioinformatics in Genomic Testing: AI-powered genomic analysis tools are improving the accuracy and speed of genetic variant detection.

Challenges and Restraints

High Cost of Genomic Testing: Advanced precision diagnostic tests can be expensive, limiting accessibility in lower-income regions.

Data Privacy and Ethical Concerns: The storage and sharing of genetic data raise ethical issues and require stringent regulatory compliance.

Complexity of Genomic Data Interpretation: Large-scale genomic datasets require sophisticated bioinformatics tools and expertise for accurate analysis.

Market Trends

Expansion of Liquid Biopsy-Based Genomic Testing: The shift toward non-invasive cancer diagnostics is gaining traction.

Development of CRISPR-Based Genomic Screening Tools: Advancing gene editing technologies are revolutionizing genetic disease research.

Increasing Use of Pharmacogenomic Testing: Optimizing drug selection and dosage based on genetic profiles is enhancing treatment outcomes.

Regional Analysis

North America: Dominates the market due to high adoption of precision medicine, strong R&D infrastructure, and favorable government initiatives.

Europe: Significant growth driven by biomarker-based drug development and expanding applications of genomic sequencing.

Asia-Pacific: Fastest-growing region with increasing investments in genomic research, personalized medicine, and biotechnology advancements.

Rest of the World: Moderate growth in Latin America and the Middle East due to increasing adoption of genetic testing technologies.

Segmental Analysis

By Technology:

Next-Generation Sequencing (NGS)

Microarray Technology

Polymerase Chain Reaction (PCR)

Fluorescence In Situ Hybridization (FISH)

By Application:

Oncology Genomic Testing

Cardiovascular Disease Risk Assessment

Rare Genetic Disorder Screening

Pharmacogenomic Testing

By End-User:

Hospitals & Diagnostic Laboratories

Biotechnology & Pharmaceutical Companies

Research Institutes

Key Market Players

Thermo Fisher Scientific

Guardant Health

GRAIL

Roche

PerkinElmer

Exact Sciences

BristolMyers Squibb

Recent Developments

Launch of AI-Driven Genomic Interpretation Platforms: Enhancing efficiency in cancer genomics and disease risk assessment.

Strategic Collaborations Between Biotech Firms and Healthcare Providers: Expanding access to precision genomic testing.

Development of Rapid, Low-Cost Whole Genome Sequencing Technologies: Making personalized genomic analysis more affordable.

For more information, please visit us at marketresearchfuture.

#Precision Genomic Testing Market Size#Precision Genomic Testing Market Share#Precision Genomic Testing Market Growth#Precision Genomic Testing Market Analysis#Precision Genomic Testing Market Trends#Precision Genomic Testing Market Forecast#Precision Genomic Testing Market Segments

0 notes

Text

Global HLA Typing Market: Growth Trends, Technologies, and Future Outlook

Market Overview

The global HLA typing market has experienced significant growth over the years, with an estimated market size of $33.4 billion in 2023. Projections indicate a remarkable expansion to $562.97 million by 2031, growing at a CAGR of 36.4% from 2024 to 2031. This rapid growth is fueled by increasing organ transplantation procedures, advancements in genetic testing, and the rising prevalence of autoimmune diseases.

Browse More : https://www.statsandresearch.com/report/40445-global-hla-typing-market/

Understanding HLA Typing

HLA typing is a laboratory test used to identify specific human leukocyte antigen (HLA) markers on an individual's cells. These markers are crucial for immune system function, helping distinguish self from non-self. The process is essential in organ transplantation to reduce the risk of rejection, as well as in autoimmune disease diagnosis and research. Accurate HLA typing ensures compatibility in transplantation, leading to improved patient outcomes.

Get a free sample copy : https://www.statsandresearch.com/request-sample/40445-global-hla-typing-market

Market Segmentation

By Geography

The HLA typing market is analyzed across multiple regions, including:

North America (United States, Canada)

Asia-Pacific (China, Japan, India, Korea, ASEAN)

Europe (Germany, France, UK, Italy, Spain, CIS)

Middle East and Africa

South America (Brazil and other key nations) Each region exhibits unique market dynamics, with North America leading in adoption due to advanced healthcare infrastructure and research capabilities.

By Technology

HLA typing employs various technological approaches, broadly classified into:

Molecular Assays:

Polymerase Chain Reaction (PCR): Identifies specific HLA alleles using amplification techniques.

Sequence-Specific Oligonucleotide (SSO) Probes: Detects genetic variations in HLA genes.

Sequence-Specific Primer (SSP) Typing: Provides high-precision allele identification.

Real-Time PCR (qPCR): Offers quantitative analysis of allele expression.

Next-Generation Sequencing (NGS): Enables high-resolution typing by sequencing entire HLA genes.

Sanger Sequencing: Provides accurate validation for identified HLA genes.

Non-Molecular Assays:

Serological Assays: Detect HLA antigens through antibody-based techniques.

Mixed Lymphocyte Culture (MLC): Assesses immune compatibility by analyzing lymphocyte responses.

By Product & Service

HLA typing solutions are categorized into:

Instruments: Sequencers, PCR systems

Reagents & Consumables: Oligonucleotide probes, antibodies, assay kits

Software & Services: HLA typing software, data analysis services, consulting services

By Application

Transplantation:

Solid Organ Transplantation (Kidney, Liver, Heart)

Hematopoietic Stem Cell Transplantation (HSCT)

Disease Diagnosis:

Cancer

Autoimmune Diseases

Infectious Diseases

Research:

Immunogenetics

Population Genetics

By End User

Hospitals & Transplant Centers

Academic & Research Institutes

Diagnostic Laboratories

Pharmaceutical & Biotechnology Companies

Enquiry : https://www.statsandresearch.com/enquire-before/40445-global-hla-typing-market

Key Market Players

The competitive landscape comprises leading biotechnology and diagnostics companies, including:

Thermo Fisher Scientific Inc.

Bio-Rad Laboratories Inc.

Qiagen N.V.

Omixon Inc.

GenDx

Illumina Inc.

TBG Diagnostics Limited

Dickinson and Company

Takara Bio Inc.

F. Hoffman-La Roche Limited

Pacific Biosciences

Future Outlook

The HLA typing market is poised for continued expansion, driven by technological advancements, increased healthcare investments, and the growing demand for precision medicine. As the industry evolves, improved sequencing techniques and AI-driven data analysis will further enhance HLA typing accuracy and efficiency, solidifying its role in transplantation and disease management.

For customized insights or sample pages of this report, feel free to reach out!

Find Out Top Trending Reports Here :

Global Sex Reassignment Surgery Market

Global Enzyme Engineering Market

Global Neuroelectronic Devices Market

Global Vitamin K2 Market Insights

Global Defibrillator Market Insights

0 notes

Text

🧬 "Decoding Life: The Metagenomics Market Unveiled"

Metagenomics Market is revolutionizing the way we study microbial communities, directly analyzing genetic material from environmental samples. This approach, powered by cutting-edge sequencing technologies and bioinformatics solutions, is pivotal in advancing research in environmental monitoring, healthcare, agriculture, and biotechnology.

To Request Sample Report : https://www.globalinsightservices.com/request-sample/?id=GIS10517 &utm_source=SnehaPatil&utm_medium=Article

Market Trends 📈

The sequencing segment leads the market, particularly 16S rRNA sequencing, essential for microbial diversity studies and environmental monitoring. Another key player is shotgun metagenomics, gaining popularity in clinical diagnostics and personalized medicine for its ability to offer comprehensive insights into microbial communities.

Key Drivers of Growth 🚀

Technological Advancements: Next-generation sequencing (NGS) and bioinformatics tools are enhancing data analysis and interpretation, driving the demand for metagenomics solutions.

R&D Investments: Increased funding in research is accelerating innovations in microbiome studies and biotechnological breakthroughs.

Government Support: The United States and China lead the charge, with robust genomics infrastructure and focus on precision medicine.

Regional Insights 🌍

North America dominates, with the United States at the forefront, benefiting from extensive research initiatives and industry partnerships.

Asia-Pacific is emerging as a powerful player, with China and India investing heavily in genomics research and healthcare advancements.

Europe, with countries like Germany and the UK, is also expanding rapidly, emphasizing microbiome research and genomic studies.

Future Outlook 🔮

The Metagenomics Market is poised for significant growth, projected to expand from 320 million samples in 2023 to 550 million samples by 2033, with an annual growth rate of 14%. Innovations in AI-driven analytics and advancements in environmental metagenomics will further drive this expansion.

#Metagenomics #MicrobialDiversity #NGS #PrecisionMedicine #Bioinformatics #EnvironmentalMonitoring #HealthcareInnovation #MicrobiomeResearch #PersonalizedMedicine #AIinScience #Genomics #SustainableBiotech #NextGenSequencing #Biotechnology #DataAnalysis

0 notes

Text

Precision Diagnostics Market Surge: $57.5B in 2023 to $157.2B by 2033 (10.5% CAGR)

Precision Diagnostics Market focuses on advanced technologies and methodologies designed to enhance the accuracy of disease detection and support personalized healthcare solutions. This includes molecular diagnostics, imaging technologies, and bioinformatics tools that enable early, precise diagnosis, tailored treatment planning, and ongoing monitoring. The market plays a vital role in the shift toward personalized medicine, which improves patient outcomes and optimizes healthcare resources by offering individualized diagnostic solutions.

To Request Sample Report: https://www.globalinsightservices.com/request-sample/?id=GIS22118 &utm_source=SnehaPatil&utm_medium=Article

Market Growth and Trends

The Precision Diagnostics Market is experiencing robust growth, driven by advancements in molecular diagnostics and imaging technologies. Among the sub-segments, molecular diagnostics lead the market due to their pivotal role in personalized healthcare and early disease detection. Next-generation sequencing (NGS) is the top performer within this segment, thanks to its precision, growing accessibility, and declining costs. Imaging diagnostics, particularly MRI and CT scans, also represent a significant segment, benefitting from ongoing technological advancements and rising healthcare expenditure.

Regional Insights

North America dominates the market, fueled by a strong healthcare infrastructure, substantial R&D investments, and a high adoption rate of innovative diagnostic technologies. The United States is the leading country, driven by advanced healthcare facilities and widespread implementation of precision diagnostics.

Europe ranks second, with Germany and the United Kingdom emerging as key contributors, spurred by increasing demand for early disease diagnosis and precise medical interventions.

Asia-Pacific is rapidly growing, with China and India seeing significant market expansion. The region’s growth is driven by increasing healthcare awareness, rising income levels, and improved access to diagnostic technologies.

Market Segmentation

By Type: Genetic Testing, Molecular Diagnostics, Companion Diagnostics, Point-of-Care Testing, Liquid Biopsy By Product: Reagents & Kits, Instruments, Software & Services, Consumables By Technology: Next-Generation Sequencing, Polymerase Chain Reaction, Fluorescence In Situ Hybridization, Immunohistochemistry, Microarray By Application: Oncology, Cardiology, Infectious Diseases, Neurology, Endocrinology By End User: Hospitals, Diagnostic Laboratories, Research Institutes, Academic Institutes By Component: Hardware, Software, Services By Device: Benchtop, Portable, Handheld, Wearable By Process: Sample Preparation, Data Analysis, Validation By Deployment: On-Premise, Cloud-Based, Hybrid By Solutions: Clinical Decision Support, Data Management, Patient Engagement

Market Volume & Projections

In 2023, the market demonstrated a strong volume of 320 million diagnostic tests globally, with projections indicating a rise to 520 million tests by 2033. The molecular diagnostics segment commands a substantial 45% market share, followed by genetic testing at 30%, and imaging diagnostics at 25%. This market dominance is driven by advancements in genomics and a growing demand for personalized medicine.

Key Market Players

Leading players in the Precision Diagnostics Market include Roche Diagnostics, Abbott Laboratories, and Thermo Fisher Scientific, which continue to influence the market through cutting-edge technology, strategic partnerships, and ongoing innovation to maintain their competitive edge.

#PrecisionDiagnostics #PersonalizedHealthcare #MolecularDiagnostics #GeneticTesting #NextGenerationSequencing #Oncology #Cardiology #EarlyDiagnosis #HealthcareInnovation #ImagingTechnologies #LiquidBiopsy #Bioinformatics #MedicalDevices #HealthcareSolutions #DiagnosticReagents

0 notes

Text

MicroRNA Market Key Insights and Growth Opportunities, Forecast - 2031

The global microRNA (miRNA) market has gained substantial attention in recent years, driven by its expanding applications in disease diagnosis, therapeutics, and biomedical research. As per the latest insights from SkyQuest Technology, the global microRNA market is projected to reach a value of USD 3.58 billion by 2031, growing at a CAGR of 12.9% from 2024 to 2031. This growth is fueled by advancements in RNA-based research, rising incidences of chronic diseases, and the increasing adoption of miRNA-based diagnostics and therapeutics.

What is Driving the Growth of the MicroRNA Market?

Advancements in Biotechnology The continuous evolution of next-generation sequencing (NGS) and molecular biology technologies has significantly enhanced the detection, profiling, and understanding of miRNA. This progress has opened doors for new therapeutic and diagnostic applications.

Rising Incidence of Chronic and Genetic Diseases The increasing prevalence of chronic diseases such as cancer, cardiovascular diseases, and neurological disorders has led to a growing demand for miRNA-based diagnostics and therapeutics, as these molecules hold the potential to modulate gene expression effectively.

Emerging Role in Precision Medicine MicroRNA is becoming a vital component in precision medicine, offering solutions tailored to an individual’s genetic profile. This trend has driven research funding and investment in miRNA technologies.

Growing Focus on Early Diagnosis Early detection of diseases is crucial for effective treatment, and miRNA-based diagnostic tools are gaining popularity for their accuracy, reliability, and ability to identify diseases in their initial stages.

Request a Sample Report - https://www.skyquestt.com/sample-request/microrna-market

Market Segmentation: A Closer Look at Key Areas

By Application

Cancer Diagnostics & Therapeutics: The largest segment due to the rising prevalence of cancer and miRNA’s role in tumor suppression and oncogene regulation.

Neurological Disorders: Increasing use in diagnosing and treating neurodegenerative diseases like Alzheimer’s and Parkinson’s.

Cardiovascular Diseases: miRNA’s ability to regulate gene expression has made it essential in addressing heart diseases.

Others: Includes applications in metabolic disorders, infectious diseases, and stem cell research.

By Technology

Next-Generation Sequencing (NGS): Widely adopted for profiling and discovering novel miRNA biomarkers.

qRT-PCR: A cost-effective and reliable technology for miRNA quantification.

Microarray: Primarily used for miRNA expression profiling.

By End-User

Research Institutes: Significant demand for miRNA in academic and industrial research.

Pharmaceutical and Biotech Companies: Focused on developing miRNA-based drugs and therapies.

Clinical Diagnostics Laboratories: Increasing use of miRNA as diagnostic markers.

Speak to an Analyst for Customization - https://www.skyquestt.com/speak-with-analyst/microrna-market

Regional Insights: The Global Reach of the MicroRNA Market

North America North America dominates the market, driven by robust R&D funding, advanced healthcare infrastructure, and the growing adoption of miRNA technologies in clinical diagnostics and therapeutics.

Europe Europe represents a significant share of the market due to the rising prevalence of chronic diseases, government support for RNA research, and the strong presence of biotechnology companies in countries like Germany and the UK.

Asia-Pacific Asia-Pacific is the fastest-growing region, with countries like China, Japan, and India witnessing increasing investments in biotechnology and a growing focus on personalized medicine.

Latin America & the Middle East These regions are gradually emerging as potential markets, driven by increasing awareness of miRNA-based applications and improving healthcare infrastructure.

Make a Purchase Inquiry - https://www.skyquestt.com/buy-now/microrna-market

Key Market Players in the MicroRNA Landscape

The microRNA market is highly competitive, with numerous companies investing in R&D to develop innovative diagnostics and therapeutics. Major players include:

Thermo Fisher Scientific Inc.

Qiagen N.V.

Merck KGaA

Illumina, Inc.

Horizon Discovery Group plc

GeneCopoeia, Inc.

NanoString Technologies, Inc.

Abcam plc

New England Biolabs

Rosetta Genomics Ltd.

These companies are driving the market through strategic collaborations, partnerships, and the development of novel miRNA-based products.

Emerging Trends in the MicroRNA Market

Integration of Artificial Intelligence (AI) in miRNA Research AI and machine learning are being employed to analyze complex miRNA datasets, accelerating the discovery of novel biomarkers and therapeutic targets.

miRNA-Based Therapeutics The focus on RNA interference (RNAi) technologies is driving the development of miRNA-based drugs for treating diseases like cancer and genetic disorders.

Liquid Biopsies and miRNA Liquid biopsy technologies, which use miRNA as biomarkers, are revolutionizing non-invasive disease diagnostics, particularly in oncology.

Rising Collaborations Between Academia and Industry Academic institutions and biotech companies are forming partnerships to advance miRNA research and bring innovative products to market.

The Future of the MicroRNA Market

The global microRNA market holds immense potential, driven by its expanding applications across diagnostics and therapeutics. With increasing investments in research and the growing adoption of RNA-based technologies, the market is set to achieve remarkable growth in the coming years.Emerging regions, coupled with advancements in precision medicine and sustainable healthcare practices, will further drive innovation in this sector. Companies that prioritize R&D and focus on developing personalized solutions are well-positioned to lead the market in the future.

#MicroRNA Market#MicroRNA Market Size#MicroRNA Market Share#MicroRNA Market Trends#MicroRNA Market Growth#MicroRNA Market Outlook#MicroRNA Market Key Players#MicroRNA Market Overview#MicroRNA Market Competitor#MicroRNA Market Insights#MicroRNA Market Forecast#MicroRNA Market Analysis#MicroRNA Market Statistics#MicroRNA Market Data#MicroRNA Market PDF#MicroRNA Market Excel#MicroRNA Market Strategy#MicroRNA Market Innovations

0 notes

Text

Exploring the Antimicrobial Susceptibility Testing Market: Trends, Innovations, and Future Opportunities

The Antimicrobial Susceptibility Testing (AST) market has become a cornerstone in modern healthcare, playing a pivotal role in combating the growing threat of antimicrobial resistance (AMR). With the rise of multidrug-resistant pathogens, the need for accurate, efficient, and rapid AST solutions is more urgent than ever. This blog explores the key drivers, challenges, and advancements shaping the AST market, along with its future trajectory.

Download PDF Brochure

Overview of Antimicrobial Susceptibility Testing

Antimicrobial Susceptibility Testing evaluates the effectiveness of antibiotics, antifungals, and antivirals against specific pathogens. It determines the minimum inhibitory concentration (MIC) required to prevent microbial growth, guiding clinicians in selecting the most effective treatment options.

Key testing methods include:

Disk Diffusion Tests: A widely used method involving antibiotic-impregnated disks.

Broth Dilution Tests: Used to determine MIC values for various antimicrobial agents.

Automated AST Systems: Advanced platforms for rapid and high-throughput testing.

Molecular AST Methods: Techniques like PCR that identify resistance genes.

Market Drivers

Rising Antimicrobial Resistance

AMR is a global health crisis, with pathogens such as MRSA and multidrug-resistant E. coli becoming increasingly prevalent. This has escalated the demand for advanced AST solutions to manage infections effectively.

Growing Infectious Disease Burden

The increasing incidence of infectious diseases, including urinary tract infections (UTIs), bloodstream infections, and pneumonia, has spurred the adoption of AST in clinical laboratories and hospitals.

Technological Advancements

Innovations in AST, such as automated and rapid diagnostic systems, are enhancing accuracy and reducing turnaround times. Examples include MALDI-TOF-based systems and next-generation sequencing (NGS) for resistance profiling.

Regulatory and Government Initiatives

Governments worldwide are funding AMR surveillance programs, promoting AST adoption in healthcare settings. Initiatives like the Global Antimicrobial Resistance and Use Surveillance System (GLASS) underscore the importance of robust diagnostic solutions.

Challenges in the AST Market

High Costs of Advanced Systems

While automated AST systems improve efficiency, their high capital costs deter adoption in low-resource settings.

Lack of Standardization

Inconsistent testing standards across regions can affect the accuracy and comparability of results.

Emerging Resistance Mechanisms

The rapid evolution of resistance mechanisms outpaces the development of diagnostic tools, necessitating continuous innovation.

Skilled Workforce Shortages

Operating sophisticated AST technologies requires trained personnel, a challenge in underdeveloped regions.

Key Market Segments

The AST market is segmented based on products, testing methods, end users, and regions.

Products

Manual AST Products: Reagents, culture media, and susceptibility disks.

Automated AST Systems: High-throughput platforms like BD Phoenix and VITEK 2.

Testing Methods

Phenotypic methods, including broth dilution and disk diffusion.

Genotypic methods like molecular diagnostics and NGS.

End Users

Hospitals and diagnostic laboratories.

Pharmaceutical and biotechnology companies for drug discovery.

Academic and research institutes.

Regional Insights

North America leads the market due to advanced healthcare infrastructure and high awareness of AMR.

Europe follows closely, driven by stringent regulations and government funding.

Asia-Pacific is witnessing rapid growth owing to the rising infectious disease burden and increasing healthcare investments.

Technological Innovations in AST

Point-of-Care (POC) Testing

The development of portable AST devices enables rapid diagnosis in outpatient settings, improving treatment outcomes.

AI-Powered Diagnostics

Artificial Intelligence is being integrated into AST platforms to analyze complex datasets and predict resistance patterns.

Microfluidics-Based Systems

These systems enhance precision and speed while minimizing sample volume, making AST more accessible.

Whole Genome Sequencing (WGS)

WGS provides comprehensive insights into resistance mechanisms, guiding precision medicine approaches.

Competitive Landscape

The AST market is highly competitive, with key players driving innovation and expansion. Leading companies include:

Thermo Fisher Scientific

bioMérieux SA

BD (Becton, Dickinson and Company)

Danaher Corporation

HiMedia Laboratories

These companies focus on launching cutting-edge products, forming strategic collaborations, and expanding their global footprint.

Future Outlook

The AST market is poised for significant growth in the coming years. Factors such as the integration of advanced technologies, rising awareness about AMR, and increased funding for diagnostics will shape its trajectory. Additionally, the push for personalized medicine and targeted therapies will further drive the adoption of sophisticated AST tools.

Key trends to watch include:

Increased adoption of molecular diagnostics.

Development of AI-driven predictive models.

Expansion of POC testing capabilities in emerging markets.

Enhanced global AMR surveillance and data-sharing initiatives.

Conclusion

The Antimicrobial Susceptibility Testing market is a critical component of the global effort to combat antimicrobial resistance. As technology evolves and awareness grows, AST solutions will become more accessible, efficient, and impactful in guiding clinical decisions. By addressing challenges like cost and standardization, the market holds immense potential to revolutionize infectious disease management and safeguard public health.

0 notes

Text

Innovations Transforming the Prenatal Diagnostics Market Landscape

Prenatal Diagnostics refers to a range of medical tests and procedures conducted during pregnancy to assess the health of the fetus. The primary goal is to detect any genetic abnormalities, chromosomal disorders, or other potential health issues early on, enabling parents and healthcare providers to make informed decisions about care. These diagnostics are essential for ensuring the well-being of both the mother and the baby, offering insights into conditions like Down syndrome, cystic fibrosis, neural tube defects, and other congenital anomalies.

The Prenatal Diagnostics Market Size was projected to reach 16.02 billion USD in 2022, according to MRFR analysis. By 2032, the prenatal diagnostics market is projected to have grown from 16.79 billion USD in 2023 to 25.7 billion USD. Over the course of the forecast period (2024–2032), the prenatal diagnostics market is anticipated to develop at a CAGR of approximately 4.84%.

Prenatal diagnostics can be broadly classified into screening tests and diagnostic tests. Screening tests, such as blood tests and ultrasounds, are non-invasive and provide an assessment of the risk of certain conditions. In contrast, diagnostic tests like amniocentesis and chorionic villus sampling (CVS) are more invasive but provide definitive information about genetic abnormalities.

Size and Share of the Prenatal Diagnostics Market

The Prenatal Diagnostics market has experienced significant growth over the past decade and is projected to continue expanding. As of recent reports, the global market size was estimated at over USD 5 billion in 2023, with an anticipated compound annual growth rate (CAGR) of approximately 10% from 2024 to 2030. The increasing demand for non-invasive prenatal testing (NIPT), advancements in genetic screening technologies, and rising awareness about prenatal health are major factors driving this growth.

North America holds the largest market share due to advanced healthcare infrastructure, high adoption rates of prenatal testing, and robust healthcare policies. Europe follows closely, with increasing government support for early genetic testing and a growing aging maternal population. The Asia-Pacific region is expected to witness the fastest growth due to rising healthcare investments, improving diagnostic capabilities, and an increasing number of pregnancies in countries like India and China.

Prenatal Diagnostics Analysis

The Prenatal Diagnostics market analysis reveals a dynamic landscape characterized by rapid technological advancements, increasing consumer awareness, and a focus on non-invasive testing methods. Non-invasive prenatal testing (NIPT) has emerged as a game-changer, offering a safer, more accessible option for detecting chromosomal abnormalities. The test analyzes cell-free fetal DNA circulating in the maternal blood to identify potential genetic conditions, making it less risky than invasive methods like amniocentesis.

Technological innovations, such as the development of next-generation sequencing (NGS) and polymerase chain reaction (PCR) techniques, have enhanced the accuracy and efficiency of prenatal tests. The integration of artificial intelligence (AI) and machine learning in data analysis is further improving the reliability of diagnostic results, reducing false positives, and enabling personalized risk assessments.

Furthermore, regulatory approvals and increasing investment in research and development (R&D) are driving market growth. Companies are investing in developing cost-effective, efficient, and less invasive diagnostic solutions, catering to the rising demand from expecting parents.

Prenatal Diagnostics Trends

Several key trends are shaping the Prenatal Diagnostics market:

Rising Demand for Non-Invasive Testing: With the increasing awareness of the risks associated with invasive procedures, there is a growing preference for non-invasive prenatal testing (NIPT), which poses no risk to the fetus and offers early detection of chromosomal abnormalities.

Technological Advancements: The adoption of advanced genetic sequencing technologies, including next-generation sequencing (NGS) and microarray analysis, is enhancing the accuracy and scope of prenatal diagnostics. These technologies allow for more detailed genetic profiling, improving diagnostic outcomes.

Increased Awareness and Early Detection: Public health initiatives and educational campaigns are raising awareness about the importance of prenatal care, leading to higher adoption rates of prenatal diagnostic tests. Early detection enables timely interventions, improving maternal and fetal outcomes.

Integration of AI and Machine Learning: The application of AI in prenatal diagnostics is streamlining the interpretation of complex genetic data, reducing human error, and enabling more precise risk stratification. AI algorithms are improving diagnostic accuracy, particularly in complex cases with ambiguous results.

Expansion in Emerging Markets: The growing healthcare infrastructure in emerging markets, coupled with rising disposable income and increased awareness about prenatal care, is driving the adoption of prenatal diagnostic tests in these regions.

Reasons to Buy Prenatal Diagnostics Market Reports

Comprehensive Market Insights: Obtain a detailed analysis of the Prenatal Diagnostics market, including size, share, growth potential, and competitive landscape, to make informed business decisions.

Up-to-Date Market Trends: Stay updated on the latest technological advancements, emerging trends, and regulatory developments shaping the prenatal diagnostics industry.

Strategic Planning: Gain insights into key growth drivers, challenges, and opportunities in the market to develop effective business strategies and investment plans.

Competitive Analysis: Understand the competitive landscape, including key players, their market strategies, and innovations, to identify potential partnerships or areas for investment.

Market Forecast and Predictions: Access accurate market forecasts to anticipate future developments and adjust business strategies accordingly.

Recent Developments in Prenatal Diagnostics

Advancement in NIPT Technology: Companies have been developing advanced NIPT solutions that offer higher sensitivity and specificity, reducing the need for follow-up invasive testing.

Regulatory Approvals: Recent approvals by regulatory bodies like the FDA have expanded the use of certain prenatal tests, making them more widely available and reliable for detecting a broader range of genetic disorders.

AI Integration: The integration of AI in prenatal diagnostics is enhancing data analysis capabilities, providing more accurate and timely results to healthcare providers and patients.

Expansion into Emerging Markets: Major players are increasingly investing in emerging markets to tap into the growing demand for prenatal diagnostics, driven by rising healthcare awareness and improved medical infrastructure.

Collaborations and Partnerships: Key industry players are forming strategic collaborations with biotech companies and research institutions to advance prenatal diagnostic technologies and expand their product offerings.

The Prenatal Diagnostics market is poised for substantial growth as innovations continue to enhance the accuracy, accessibility, and safety of prenatal testing, ultimately improving maternal and fetal health outcomes.

rElated reports:

Dental Contouring Market

Dermatology Drug Market

Facial Implant Market

Feeding Tube Market

Healthcare Informatics Market

Top of Form

Bottom of Form

0 notes

Text

Key Trends Driving the Preimplantation Genetic Testing Market

The global preimplantation genetic testing (PGT) market was valued at approximately USD 802.2 million in 2023 and is projected to expand at a compound annual growth rate (CAGR) of 10.3% from 2024 to 2030. Several factors are contributing to this growth, notably the rising prevalence of genetic disorders such as single gene, mitochondrial, and other hereditary conditions. As awareness of genetic risks increases, there is a growing demand for preimplantation diagnosis and screening processes to ensure healthier pregnancies and reduce the risk of passing on genetic diseases.

For example, the Florida Department of Health reports that one in every 33 babies in the U.S. is born with a congenital disability, which affects approximately 120,000 babies each year. These statistics highlight the importance of genetic testing, as more families seek options to prevent the transmission of such disorders. As advancements in genetic testing continue, the demand for preimplantation genetic testing is expected to increase. For instance, in July 2023, Thermo Fisher Scientific Inc. launched two new Next-Generation Sequencing (NGS)-based tests specifically designed for preimplantation genetic testing for aneuploidy (PGT-A). This addition reflects the continued innovation in the field and its potential to drive market growth in the coming years.

Preimplantation genetic diagnosis (PGD) plays a critical role in the in vitro fertilization (IVF) process, particularly for individuals or couples with a history of miscarriages or those who have experienced pregnancies involving chromosomal abnormalities. PGD is typically used in IVF cycles to help ensure a successful pregnancy by identifying embryos that do not carry genetic disorders or chromosomal abnormalities. This testing is especially beneficial for couples who are at risk for hereditary genetic disorders, offering them a chance to have a healthy child and preventing the transmission of genetic diseases.

Gather more insights about the market drivers, restrains and growth of the Preimplantation Genetic Testing Market

Regional Insights

North America accounted for a significant share of the global preimplantation genetic testing (PGT) market, driven by a combination of factors such as the rising prevalence of various genetic disorders, increasing number of laboratories offering PGT services, and heightened awareness of genetic screening. The market is also buoyed by a high incidence of hereditary disorders and other common diseases, such as Polycystic Ovary Syndrome (PCOS) and chlamydia, which further increase the demand for genetic testing. The adoption of advanced reproductive technologies, such as in-vitro fertilization (IVF) with PGT to prevent genetic disorders, has significantly contributed to the growth in this region.

U.S.

In the United States, the PGT market is witnessing steady growth, fueled by increasing awareness about hereditary disorders, advancements in reproductive technologies, rising infertility rates, and a growing preference for personalized medicine. Moreover, supportive government regulations and a high demand for IVF procedures have further driven market expansion. As more individuals seek fertility solutions that enable them to have healthy offspring, the demand for PGT services is expected to increase, contributing to the overall growth of the market in the U.S.

Europe

Europe dominated the global PGT market in 2023, accounting for 40.74% of the total revenue share. This leadership is primarily driven by a high volume of IVF procedures, which have been increasingly adopted due to the trend of late pregnancies among women in Europe. Additionally, the liberal regulations surrounding aneuploidy screening in many European countries, coupled with the presence of established market players and healthcare providers, are helping to propel the growth of the PGT market in the region.

The UK market for preimplantation genetic testing is also expected to see significant growth due to government policies that support IVF, along with funding initiatives and a rising demand for personalized medicine. These factors, combined with better IVF success rates, will drive the adoption of PGT solutions across the country.

In Germany, the PGT market is set for growth as increasing public awareness about genetic disorders and the benefits of PGT is prompting more couples to opt for genetic testing before pregnancy. As these trends continue, Germany will see continued market expansion.

Asia Pacific

The Asia Pacific region is poised to register the highest CAGR of 11.3% during the forecast period. This growth is fueled by advancements in reproductive technology, expanding healthcare accessibility, and a greater awareness of PGT across the region. Countries like China and Japan are leading the way in the integration of advanced genetic testing technologies within reproductive health practices, helping to boost the demand for PGT services.

In China, the growing burden of genetic diseases and a large population with significant hereditary disorders are driving the demand for preimplantation genetic testing. With a high adoption rate of IVF procedures, the need for PGT to ensure healthy births by selecting embryos free of genetic mutations is expected to fuel market growth.

Similarly, Japan is seeing increasing demand for PGT due to technological innovations in genetic testing and heightened awareness of the benefits of genetic screening. These factors, combined with an increasing number of couples opting for assisted reproductive technologies, will contribute to the growth of the PGT market in Japan.

Latin America

The Latin American market for preimplantation genetic testing is expected to experience substantial growth, primarily driven by increasing awareness of genetic disorders. As people become more educated about the risks of hereditary diseases, the demand for proactive genetic testing during family planning is expected to rise.

In Brazil, the market is poised for significant growth due to the entry of new providers and the introduction of advanced genomic technologies. These innovations are enhancing the accuracy and range of conditions that can be screened through PGT, expanding the market's potential in the country.

Middle East and Africa (MEA)

In the MEA region, the preimplantation genetic testing market is also expected to grow significantly, driven by increasing awareness of the importance of genetic screening and diagnosis. The region has seen a positive shift in attitudes toward hereditary diseases, with more people recognizing the benefits of PGT.

The UAE is experiencing growth in the PGT market, supported by a cultural shift toward acceptance of advanced medical technologies. As social attitudes evolve positively toward genetic testing, Emiratis and expatriates alike are more likely to consider PGT for family planning. This change is further supported by an increasingly progressive healthcare infrastructure that facilitates the adoption of innovative medical technologies.

In Kuwait, technological advancements in hereditary testing technologies are driving the growth of the PGT market. Enhanced accuracy and reliability in genetic testing are contributing to better outcomes for couples undergoing assisted reproductive treatments, thereby boosting demand for PGT services.

Browse through Grand View Research's Clinical Diagnostics Industry Research Reports.

• The tissue diagnostics market size was estimated at USD 8.72 billion in 2024 and is projected to grow at a CAGR of 8.41% from 2025 to 2030.

• The global ovarian cancer diagnostics market was valued at USD 4.60 billion in 2023 and is expected to grow at a CAGR of 5.0% during the forecast period.

Key Preimplantation Genetic Testing Company Insights

Several key players dominate the global preimplantation genetic testing (PGT) market, including Quest Diagnostics Incorporated, Natera, Inc., and Illumina, Inc. These companies are driving innovation and expanding their reach through a variety of strategies, such as new product launches, strategic acquisitions, and partnerships with healthcare providers.

• Illumina, Inc. is a leading player in the genomics and sequencing industry, providing advanced tools and technologies that enable the accurate analysis of DNA. Their solutions are widely used across healthcare, agriculture, and scientific research, helping to drive advancements in personalized medicine and genetic testing.

• Quest Diagnostics Incorporated is a major medical diagnostics company that offers clinical testing services, including gene-based testing, routine testing, and drugs-of-abuse testing. Their services are critical for healthcare providers, and their global presence, including in Mexico, India, Ireland, and the UK, enhances their capacity to serve diverse markets. Their diagnostic laboratories are key partners in expanding access to PGT and other advanced testing technologies.

Key Preimplantation Genetic Testing Companies:

The following are the leading companies in the preimplantation genetic testing market. These companies collectively hold the largest market share and dictate industry trends.

• Quest Diagnostics Incorporated

• Natera, Inc.

• COOPER SURGICAL, INC.

• Genea Pty Limited.

• Invitae Corporation

• Laboratory Corporation of America Holdings

• Thermo Fisher Scientific Inc.

• Bioarray S.L.

• Illumina, Inc.

• Igenomix

• RGI

• F. Hoffmann-La Roche Ltd

Order a free sample PDF of the Preimplantation Genetic Testing Market Intelligence Study, published by Grand View Research.

#Preimplantation Genetic Testing Market#Preimplantation Genetic Testing Market Analysis#Preimplantation Genetic Testing Market Report#Preimplantation Genetic Testing Market Regional Insights

0 notes

Text

An Overview of Next Generation Sequencers Market: Trends and Insights

The Next-Generation Sequencers (NGS) market is witnessing rapid growth, driven by advancements in sequencing technology, declining costs, and increasing applications across healthcare, research, and agriculture. NGS enables high-throughput DNA sequencing, allowing for a more comprehensive analysis of genomes, transcriptomes, and epigenomes.

Buy Full Report for More Insights on the Next Generation Sequencers Market Forecast Download a Free Sample Report

This market encompasses various components, including instruments, software, and reagents, catering to a wide array of end-users, such as hospitals, research institutes, and biotechnology firms.

1. Market Overview

Market Size and Growth: The NGS market has shown robust growth due to rising demand for genomic analysis in personalized medicine, cancer research, and genetic diagnostics. Increasing adoption in clinical settings, along with advancements in technology, has driven accessibility and expanded market reach.

Regional Trends: North America and Europe currently dominate the market due to high healthcare expenditures, advanced infrastructure, and a significant focus on research and development. Meanwhile, Asia-Pacific is emerging as a promising market due to rising healthcare investments and increasing adoption of genomic medicine.

Key Applications: The major applications for NGS include oncology, infectious disease diagnostics, reproductive health, and hereditary disease screening, along with applications in agriculture and environmental studies.

2. Key Trends in the NGS Market

Declining Sequencing Costs: The costs of sequencing have significantly dropped since the advent of NGS technologies. The "thousand-dollar genome" has become a reality, making genetic testing more affordable and accessible, particularly in research and clinical diagnostics.

Shift Towards Clinical Applications: There is a growing demand for NGS in clinical settings, particularly in oncology for tumor profiling, hereditary disease detection, and pharmacogenomics. Clinical applications are gaining traction due to their potential for precision medicine, helping tailor treatments to individual genetic profiles.

Focus on Cancer Research: Oncology remains a major application area for NGS, as it enables detailed cancer genome analysis, leading to better understanding of mutations and tumor behavior. This technology supports both research and diagnostic applications, fueling demand among pharmaceutical companies and research institutes focused on oncology.

Rise of Liquid Biopsies: NGS is widely used in liquid biopsies, which offer a non-invasive method for cancer detection and monitoring by analyzing cell-free DNA (cfDNA) from blood samples. Liquid biopsies are gaining popularity as they allow real-time monitoring of tumor progression and treatment efficacy, reducing the need for invasive procedures.

Emergence of Long-Read Sequencing: Long-read sequencing technologies, such as those offered by Pacific Biosciences and Oxford Nanopore, are gaining traction due to their ability to provide more comprehensive genomic insights. These technologies are particularly valuable in detecting structural variants and resolving complex genomic regions.

Development of Companion Diagnostics: NGS-based companion diagnostics, used to determine the efficacy and safety of a specific drug for a targeted patient group, are expanding. These diagnostics guide treatment decisions in oncology, particularly for identifying biomarkers associated with certain therapies.

3. Market Segmentation

By Product: The NGS market includes sequencers, software, consumables, and services. Consumables, including reagents and kits, constitute the largest segment due to repeated purchases. However, software solutions are gaining traction as data analysis and interpretation become more complex.

By Technology:

Whole Genome Sequencing (WGS): WGS provides a comprehensive view of the entire genome, making it suitable for research and complex disease studies.

Targeted Sequencing: Targeted sequencing is cost-effective and focuses on specific regions of interest, widely used in oncology and clinical diagnostics.

RNA Sequencing: RNA sequencing enables transcriptome analysis and is valuable in cancer research, gene expression studies, and drug discovery.

Exome Sequencing: Exome sequencing, which targets protein-coding regions, is a more affordable alternative to WGS and is commonly used for diagnosing genetic disorders.

By Application: The NGS market serves several applications, including oncology, infectious disease diagnosis, reproductive health, genetic screening, and forensic analysis. Oncology holds the largest share, while infectious disease applications, particularly in tracking pathogens and outbreaks, are rapidly growing.

By End User: The primary end-users include academic and research institutions, hospitals and clinics, pharmaceutical and biotechnology companies, and government agencies. Hospitals and clinics are showing increasing demand as NGS technology moves from research into clinical diagnostics.

4. Key Drivers and Challenges

Drivers:

Increased Demand for Precision Medicine: The trend toward personalized medicine is a major driver, as NGS allows for tailored treatments based on genetic profiles, improving treatment outcomes.

Growing Investment in Genomic Research: Governments, healthcare institutions, and private companies are heavily investing in genomic research and infrastructure to support NGS applications across various fields.

Expansion of Genetic Screening Programs: Many countries are implementing large-scale genetic screening programs for early detection of genetic disorders and hereditary cancers, boosting demand for NGS.

Challenges:

Data Management and Analysis Complexity: The high volume of data generated by NGS requires advanced bioinformatics solutions for analysis, interpretation, and storage. This creates a need for skilled personnel and sophisticated software.

Regulatory and Ethical Concerns: The regulatory landscape for NGS is evolving, and concerns regarding data privacy and ethical issues are prevalent. Obtaining regulatory approval for clinical NGS applications can be time-consuming.

High Initial Investment: Although sequencing costs have decreased, the initial investment required for NGS platforms and bioinformatics infrastructure remains high, limiting adoption in resource-constrained regions.

5. Competitive Landscape

The NGS market is highly competitive, with established players as well as new entrants focusing on niche applications. Key players are investing in research and development, collaborations, and acquisitions to strengthen their market positions and expand product portfolios.

Illumina, Inc.: Illumina is the market leader, with a dominant position in sequencing instruments and consumables. Its sequencers, including the NovaSeq and NextSeq series, are widely used in research and clinical settings.

Thermo Fisher Scientific, Inc.: Known for its Ion Torrent platform, Thermo Fisher focuses on providing affordable, high-throughput sequencing solutions, with applications ranging from cancer research to infectious disease diagnostics.

Pacific Biosciences: PacBio specializes in long-read sequencing technology, particularly valuable for applications that require high accuracy in structural variant detection. Its Sequel system is popular among researchers in complex genomics.

Oxford Nanopore Technologies: Oxford Nanopore offers portable, real-time sequencing devices like the MinION and PromethION, which are particularly useful for field-based applications and rapid sequencing needs.

BGI Group: Based in China, BGI is a major player in genome sequencing services and provides a range of sequencers tailored for research and clinical applications. Its focus on affordability has helped it gain traction in emerging markets.

Qiagen N.V.: Qiagen provides NGS sample preparation and bioinformatics solutions, with a particular emphasis on clinical diagnostics. Its GeneReader NGS System is aimed at making NGS more accessible in clinical labs.

Agilent Technologies: Agilent offers NGS target enrichment and analysis solutions, focusing on workflows for oncology and hereditary disease testing.

6. Future Outlook

Advancements in Data Analysis Tools: Continued improvements in bioinformatics and artificial intelligence are expected to streamline data interpretation, making NGS more accessible to clinical users and reducing the time required for analysis.

Rise of Multi-Omics Approaches: Multi-omics, which combines genomics with proteomics, transcriptomics, and metabolomics, is expected to enhance the understanding of complex diseases. NGS will play a key role in integrating genomic data with other molecular insights.

Increased Focus on Rare Disease Research: NGS enables the identification of mutations associated with rare genetic disorders, facilitating research and development of targeted therapies. This area is likely to see continued growth, especially as pharmaceutical companies invest in precision medicine.

Expansion of Direct-to-Consumer (DTC) Testing: DTC genetic testing is gaining popularity, and as NGS becomes more affordable, companies may offer more comprehensive and affordable sequencing-based consumer tests.

Development of Point-of-Care Sequencing: Point-of-care NGS devices, offering rapid and portable sequencing capabilities, could find applications in emergency rooms and remote locations, particularly for infectious disease diagnosis.

Conclusion

The NGS market is positioned for substantial growth, driven by its expanding role in clinical diagnostics, advancements in sequencing technology, and increasing affordability. Applications in cancer research, infectious disease detection, and reproductive health are set to grow as the technology becomes more integrated into healthcare systems worldwide. However, challenges such as data complexity and regulatory hurdles will require ongoing innovation in bioinformatics and clear guidelines for clinical use. As technology advances, NGS has the potential to become a routine tool in personalized medicine, facilitating earlier diagnosis, better treatments, and improved patient outcomes across a range of medical fields.

0 notes

Text

Competitive Landscape and Key Players in SNP Genotyping Market

The SNP genotyping and analysis market is witnessing remarkable growth, driven by advancements in genomics and an increasing focus on personalized medicine. SNP (single nucleotide polymorphism) genotyping identifies variations in a single nucleotide in a genome, aiding in the study of genetic predispositions to various diseases, drug responses, and genetic traits. This market includes the technologies, tools, and services used to genotype SNPs and conduct analysis, which has widespread applications in research, diagnostics, and drug development. The demand for SNP genotyping and analysis is particularly high in the fields of oncology, pharmacogenomics, and agricultural research, as it enables deeper insights into genetic variations and their impact on individual and population-level health outcomes.

The SNP Genotyping and Analysis Market Size was projected to reach $13.7 billion (USD billion) in 2022 based on MRFR analysis. It is anticipated that the market for SNP genotyping and analysis will increase from 15.11 billion USD in 2023 to 36.6 billion USD in 2032. During the forecast period (2024-2032), the SNP Genotyping and Analysis Market is anticipated to develop at a CAGR of approximately 10.33%.

SNP Genotyping and Analysis Market Share

The SNP genotyping and analysis market share is primarily held by leading companies like Illumina, Thermo Fisher Scientific, and Bio-Rad Laboratories, which offer state-of-the-art genotyping tools, reagents, and software solutions. These companies dominate the market due to their advanced platforms, broad research capabilities, and established partnerships with research and clinical institutions. New market entrants, however, are gaining a foothold by focusing on cost-effective, high-throughput genotyping solutions. The market share is also geographically diverse, with North America and Europe holding prominent shares due to extensive research funding and a large base of biotech companies, while Asia-Pacific is rapidly growing due to expanding healthcare and research infrastructure.

SNP Genotyping and Analysis Market Analysis

SNP genotyping and analysis market analysis indicates significant growth potential due to the rising prevalence of chronic diseases and the increasing demand for genomic data in clinical and research settings. The analysis also shows that innovations in high-throughput sequencing and bioinformatics are facilitating more efficient, cost-effective SNP genotyping. Technologies like microarray analysis and next-generation sequencing (NGS) are key drivers, providing rapid and accurate SNP data at a fraction of traditional costs. This market analysis highlights the impact of growing awareness of genetic testing among patients and healthcare providers, as well as increasing investments by governments and private entities in genomic research. The focus on personalized medicine, where treatments are tailored to individual genetic profiles, is expected to drive continuous demand in the SNP genotyping and analysis market.

SNP Genotyping and Analysis Market Trends

Key SNP genotyping and analysis market trends include the adoption of automation and AI in genomics. AI-powered data analysis helps interpret large datasets generated by SNP genotyping, enabling faster and more accurate insights into genetic associations. Another trend is the increased use of SNP genotyping in non-invasive prenatal testing (NIPT) and newborn screening, which has become an essential aspect of early disease diagnosis and prevention. Furthermore, the integration of genotyping and bioinformatics platforms enables researchers to conduct more comprehensive analyses, streamlining the identification of disease-related SNPs. The growing interest in consumer genomics, where individuals can gain insights into their ancestry and health risks through direct-to-consumer (DTC) testing kits, is also impacting the SNP genotyping and analysis market.

Reasons to Buy the Reports

Market Insights and Forecasts: Detailed projections on the SNP genotyping and analysis market, including future opportunities and growth drivers.

Competitive Landscape: Comprehensive information on market share and strategic positioning of key players, enabling informed decision-making.

Technological Trends: Insights into the latest technological advancements, such as AI integration, next-generation sequencing, and bioinformatics tools in SNP genotyping.

Regional Analysis: Regional breakdowns and growth potential insights to help investors and companies identify high-opportunity areas globally.

Personalized Medicine Focus: Analysis of the expanding role of SNP genotyping in personalized medicine, highlighting its applications in oncology, pharmacogenomics, and genetic testing.

Recent Developments

Recent developments in the SNP genotyping and analysis market reflect a focus on expanding applications and improving technology. In 2023, Thermo Fisher Scientific launched a new NGS-based genotyping platform designed for high-accuracy pharmacogenomic research, enhancing its utility in personalized medicine. Illumina introduced a cost-effective array platform targeting SNP genotyping for agricultural genomics, providing a tailored solution for crop and livestock breeding. Additionally, Bio-Rad Laboratories announced a strategic collaboration to integrate its genotyping software with AI-powered bioinformatics tools, improving analysis speed and accuracy. Advancements in point-of-care (POC) genotyping devices have also been significant, allowing for rapid SNP analysis in clinical settings and contributing to the increased demand in the SNP genotyping and analysis market.

Related repots:

medical equipment rental market

medical radiation shielding market

membrane filtration market

oral solid dosage pharmaceutical market

0 notes

Text

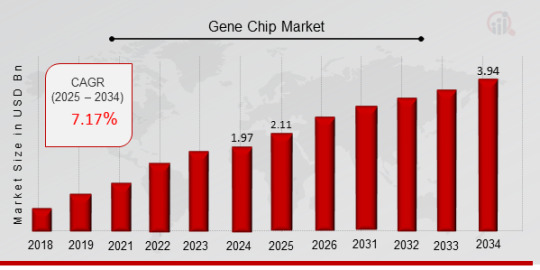

Gene Chip Market Size, Growth Outlook 2035

The global Gene Chip Market Size was estimated at 1.97 (USD Billion) in 2024. The Gene Chip Market Industry is expected to grow from 2.11 (USD Billion) in 2025 to 3.94 (USD Billion) till 2034, at a CAGR (growth rate) is expected to be around 7.17% during the forecast period (2025 - 2034).

Market Overview The Gene Chip Market is witnessing significant growth due to the rising adoption of genomics in disease research, personalized medicine, and drug discovery. Gene chips, also known as DNA microarrays, are widely used for gene expression profiling, mutation detection, and genotyping applications. The increasing prevalence of genetic disorders, cancer, and infectious diseases, coupled with advancements in bioinformatics and next-generation sequencing (NGS) technologies, is driving market expansion. Furthermore, growing investments in genomic research and precision medicine are accelerating the demand for gene chip technologies.

Market Size and Share The global Gene Chip MarketSize was estimated at 1.97 (USD Billion) in 2024. The Gene Chip Market Industry is expected to grow from 2.11 (USD Billion) in 2025 to 3.94 (USD Billion) till 2034, at a CAGR (growth rate) is expected to be around 7.17% during the forecast period (2025 - 2034). North America dominates the market due to the presence of major biotechnology firms, well-established research institutions, and high investments in precision medicine. The Asia-Pacific gene chip market is expected to witness the fastest growth, driven by government initiatives in genomics, expanding healthcare infrastructure, and increasing demand for personalized medicine.

Market Drivers

Increasing Prevalence of Genetic and Chronic Diseases: Rising cases of cancer, hereditary disorders, and infectious diseases are boosting demand for DNA microarrays in diagnostic applications.

Advancements in Genomics and Bioinformatics: Integration of artificial intelligence (AI) in gene expression analysis is enhancing the accuracy of gene chip technology.

Growing Adoption of Personalized Medicine: The demand for customized treatment plans based on genetic profiling is fueling market growth.

Rising Investments in Drug Discovery and Development: Pharmaceutical companies are increasingly using gene chip assays for target identification and biomarker discovery.

Challenges and Restraints

High Cost of Gene Chip Technology: DNA microarray platforms can be expensive, limiting accessibility in low-income regions.

Data Complexity and Interpretation Challenges: The vast amount of genetic data generated by microarrays requires advanced bioinformatics tools and expertise.

Competition from Next-Generation Sequencing (NGS): The emergence of NGS technologies is challenging the market share of traditional gene chip platforms.

Market Trends

Miniaturization and Portability of Gene Chips: Development of lab-on-a-chip technologies is enhancing accessibility for point-of-care testing.

Integration of AI in Genomic Data Analysis: AI-powered gene expression analysis is improving accuracy in disease diagnosis and drug response prediction.

Increased Adoption of High-Density Microarrays: Researchers are leveraging high-throughput gene chips for cancer genomics and pharmacogenomics.

Regional Analysis

North America: The largest market due to high R&D investments, government funding for genomics, and strong presence of biotechnology firms.

Europe: Significant market growth driven by precision medicine initiatives and increasing applications in rare disease diagnostics.

Asia-Pacific: Fastest-growing region due to rising demand for personalized medicine, expanding research in genetics, and increasing adoption of gene chip technology.

Rest of the World: Moderate growth, particularly in Latin America and the Middle East, where genomics research is gradually expanding.

Segmental Analysis

By Type:

cDNA Microarrays

Oligonucleotide Microarrays

SNP Microarrays

By Application:

Gene Expression Analysis

Cancer Diagnostics

Pharmacogenomics

Pathogen Detection

Agricultural Genomics

By End-User:

Biotechnology & Pharmaceutical Companies

Academic & Research Institutes

Diagnostic Laboratories

Key Market Players

GE Healthcare

HoffmannLa Roche Ltd

Illumina, Inc.

Danaher Corporation

Siemens Healthineers

Thermo Fisher Scientific

BD (Becton, Dickinson and Company)

Recent Developments

Launch of AI-Based Gene Expression Profiling Platforms: Enhancing the efficiency of genomic data interpretation.

Advancements in Multiplex Microarray Technologies: Improving the sensitivity and specificity of gene chip assays.

Strategic Partnerships Between Pharma and Genomics Firms: Accelerating the development of biomarker-driven drug discovery.

For more information, please visit us at marketresearchfuture.

#Gene Chip Market Size#Gene Chip Market Share#Gene Chip Market Growth#Gene Chip Market Analysis#Gene Chip Market Trends#Gene Chip Market Forecast#Gene Chip Market Segments

0 notes

Text

Unraveling Gene Mysteries: The Role of Transcriptomics Technologies

Introduction

The transcriptomics technologies market is experiencing robust growth due to advancements in genomics, an increasing emphasis on personalized medicine, and the rising demand for comprehensive gene expression analysis. Transcriptomics, the study of RNA transcripts produced by the genome under specific circumstances, provides critical insights into gene expression and regulation, offering valuable information for various applications including disease research, drug development, and personalized medicine. This market research report aims to offer a detailed analysis of the transcriptomics technologies market, exploring key market dynamics, regional trends, market segmentation, competitive landscape, and future outlook.

Market Dynamics

Drivers

Advancements in Genomics: Rapid technological advancements in sequencing technologies, such as next-generation sequencing (NGS) and microarrays, are driving the growth of the transcriptomics technologies market. These technologies enable high-throughput gene expression analysis and detailed transcriptome mapping.

Increasing Demand for Personalized Medicine: There is a growing focus on personalized medicine, which requires comprehensive gene expression data to tailor treatments to individual patients. Transcriptomics technologies are essential for understanding gene expression profiles and developing targeted therapies.

Rising Research and Development Activities: Increasing investments in R&D activities by pharmaceutical and biotechnology companies to discover novel biomarkers and therapeutic targets are driving the demand for transcriptomics technologies.

Challenges

High Cost of Technologies: The high cost associated with advanced transcriptomics technologies, including sequencing platforms and associated reagents, can be a barrier to widespread adoption, particularly in resource-limited settings.

Data Management and Analysis: The vast amount of data generated from transcriptomics studies poses challenges in terms of data management, storage, and analysis. Handling and interpreting large-scale transcriptomic data require specialized tools and expertise.

Complexity of Transcriptome Analysis: The complexity of transcriptome data, including the presence of alternative splicing and post-transcriptional modifications, adds to the analytical challenges and can complicate data interpretation.

Opportunities

Technological Innovations: Continued advancements in transcriptomics technologies, such as improvements in sequencing accuracy and the development of novel analytical tools, present significant opportunities for market growth.

Expansion into Emerging Markets: Growing investments in healthcare and research infrastructure in emerging markets offer new opportunities for the adoption of transcriptomics technologies.

Integration with Other Omics Technologies: Integrating transcriptomics with other omics technologies (e.g., proteomics, metabolomics) can provide a more comprehensive understanding of biological systems, creating opportunities for innovative research and applications.

Sample Pages of Report: https://www.infiniumglobalresearch.com/reports/sample-request/952

Regional Analysis

North America: North America holds a dominant position in the transcriptomics technologies market due to the presence of leading technology providers, well-established research institutions, and high healthcare expenditure. The United States and Canada are key contributors to market growth in this region.

Europe: Europe also represents a significant market for transcriptomics technologies, supported by strong research capabilities, government funding, and increasing focus on personalized medicine. Countries such as Germany, the UK, and France are leading contributors.

Asia-Pacific: The Asia-Pacific region is expected to experience rapid growth in the transcriptomics technologies market due to increasing research activities, expanding healthcare infrastructure, and rising investments in biotechnology. China and India are emerging as key players in this market.

Latin America: Latin America is gradually adopting transcriptomics technologies, with growth driven by increasing research initiatives and improvements in healthcare infrastructure. Brazil and Mexico are notable markets in this region.

Middle East & Africa: The Middle East & Africa region shows potential for growth, supported by increasing investments in healthcare and research. However, market development may be slower due to economic and infrastructure challenges.

Market Segmentation

The transcriptomics technologies market can be segmented based on technology, application, end-user, and region:

By Technology:

Next-Generation Sequencing (NGS)

Microarrays

Real-Time PCR

Others (e.g., RNA Sequencing, in situ hybridization)

By Application:

Biomarker Discovery

Drug Development

Disease Research

Personalized Medicine

Others (e.g., Agricultural Research, Environmental Studies)

By End-User:

Academic and Research Institutes

Pharmaceutical and Biotechnology Companies

Hospitals and Diagnostic Laboratories

Others (e.g., Contract Research Organizations)

Competitive Landscape

Market Share of Large Players: Large players dominate the transcriptomics technologies market, holding significant shares due to their extensive product portfolios, strong R&D capabilities, and established market presence.

Price Control: Big players have substantial influence over market pricing, leveraging their economies of scale and advanced technologies. However, competitive pricing strategies from smaller companies also affect pricing dynamics.

Competition from Small and Mid-Size Companies: Small and mid-size companies challenge larger players by offering innovative technologies and specialized solutions. These companies often focus on niche markets and provide unique value propositions.

Key Players: Major players in the transcriptomics technologies market include Illumina, Inc., Thermo Fisher Scientific, Agilent Technologies, Roche Holding AG, and Qiagen N.V.

Report Overview: https://www.infiniumglobalresearch.com/reports/global-transcriptomics-technologies-market

Future Outlook

New Product Development: New product development plays a critical role in the transcriptomics technologies market. Innovations such as enhanced sequencing technologies and novel data analysis tools are expected to drive market growth and address existing challenges. Companies investing in R&D to develop cutting-edge products are likely to gain a competitive advantage.

Sustainable Products: There is a growing emphasis on sustainability in the life sciences industry. Sustainable practices and products, such as eco-friendly reagents and energy-efficient technologies, are gaining traction. Companies that focus on sustainability are likely to appeal to environmentally-conscious customers and enhance their market position.

Conclusion

The transcriptomics technologies market is on a growth trajectory, driven by technological advancements, increasing demand for personalized medicine, and expanding research activities. Despite challenges such as high costs and data complexity, the market presents significant opportunities for innovation and expansion. Companies that leverage technological advancements, focus on new product development, and adopt sustainable practices will be well-positioned to succeed in this evolving market. As the field of transcriptomics continues to advance, staying attuned to emerging trends and market demands will be crucial for achieving long-term success.

0 notes

Text

Growth in the DNA Test for Dogs Market

The pet care industry has seen a significant surge in the demand for DNA testing for dogs, driven by the increasing interest of pet owners in understanding their pets' genetic backgrounds. DNA tests for dogs provide valuable insights into a dog's breed, ancestry, potential health risks, and genetic traits. This growing trend reflects the broader societal shift towards personalized healthcare and well-being, extending beyond humans to their pets. In this article, we will explore the current size and share of the DNA test for dogs market, key industry trends, and provide a forecast through 2032.

Market Size and Share

Dna Test for Dogs Market Size was estimated at 5.18 (USD Billion) in 2023. The Dna Test for Dogs Market Industry is expected to grow from 5.71(USD Billion) in 2024 to 12.5 (USD Billion) by 2032. The Dna Test for Dogs Market CAGR (growth rate) is expected to be around 10.29% during the forecast period (2024 - 2032). The increasing popularity of DNA tests for dogs is driven by a combination of factors, including rising pet ownership, growing awareness of pet health, and advancements in genetic testing technologies.

North America currently dominates the market, accounting for over 45% of the global market share. The high level of pet ownership, particularly in the United States, coupled with the availability of advanced veterinary services, has fueled the demand for dog DNA tests in this region. Europe follows as the second-largest market, driven by similar trends in pet ownership and the increasing focus on animal welfare. The Asia-Pacific region is expected to witness the fastest growth, with rising disposable incomes and an increasing number of pet owners fueling demand for DNA testing services for dogs.

Industry Trends