#Distributed Energy Resource Management System Market Size

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr.com is the 103rd most visited website in the world.

Text

Exploring the Distributed Energy Resource Management System (DERMS) Market: Growth, Trends, and Opportunities

The Distributed Energy Resource Management System (DERMS) market is reshaping the energy landscape, driven by the increasing adoption of renewable energy, smart grid technologies, and the need for efficient energy management. According to SkyQuest Technology, the DERMS market is poised to reach significant growth, projected to achieve a value of USD 2507.55 Million by 2032, growing at a CAGR of 21.8% during the forecast period.

Market Size and Growth Projections

The Distributed Energy Resource Management System market is rapidly evolving, primarily fueled by the global shift toward decarbonization and the increasing integration of renewable energy sources. Utilities, businesses, and residential consumers alike are investing in DERMS solutions to enhance grid reliability, improve energy efficiency, and manage distributed energy resources effectively.

Request a Sample of the Report here: https://www.skyquestt.com/sample-request/distributed-energy-resource-management-system-market

Key Market Drivers

The growing adoption of DERMS solutions is propelled by several key factors:

Shift to Decentralized Energy Generation With the increasing penetration of renewables such as solar and wind, DERMS is becoming essential for managing decentralized energy systems efficiently.

Smart Grid Developments The rise of smart grid technologies is enabling utilities to optimize energy distribution and improve grid resilience using DERMS solutions.

Regulatory Push for Sustainability Government policies and incentives are driving the deployment of distributed energy resources, creating a demand for robust management systems.

Technological Advancements Innovations in IoT, AI, and cloud computing are enhancing DERMS capabilities, offering real-time monitoring and optimization of energy resources.

Market Segments

The DERMS market is segmented based on software type, deployment model, and end-user:

By Software Type:

Analytics and Reporting

Real-Time Monitoring

Control and Optimization

By Deployment Model:

On-Premise

Cloud-Based

By End-User:

Utilities

Industrial & Commercial

Residential

Speak with an Analyst for More Insights: https://www.skyquestt.com/speak-with-analyst/distributed-energy-resource-management-system-market

Regional Insights

The DERMS market exhibits distinct regional trends based on energy policies, renewable energy adoption, and technological advancements:

North America: The region leads the market with a strong emphasis on renewable energy integration and smart grid initiatives. The U.S. and Canada are major contributors.

Europe: Known for its ambitious decarbonization targets, Europe is witnessing significant adoption of DERMS to manage its growing renewable energy capacity.

Asia-Pacific: The fastest-growing region, driven by rapid urbanization, increasing energy demand, and government initiatives to support renewable energy.

Latin America & Middle East: Emerging markets in these regions are adopting DERMS solutions to address energy access challenges and optimize distributed energy resources.

Buy the Report to Get the Full Analysis: https://www.skyquestt.com/buy-now/distributed-energy-resource-management-system-market

Top Players in the Market

The DERMS market is highly competitive, with leading players driving innovation and offering advanced solutions to meet the growing demand. Key players include:

Schneider Electric

Siemens AG

General Electric

ABB Ltd.

AutoGrid Systems, Inc.

Doosan GridTech

Opus One Solutions

Enbala Power Networks

EnergyHub

Spirae, LLC

View full ToC and Companies list here: https://www.skyquestt.com/report/distributed-energy-resource-management-system-market

Emerging Trends

Integration of AI and Machine Learning Advanced analytics powered by AI and ML are enabling DERMS to predict and optimize energy usage patterns.

Rise of Microgrids The growing popularity of microgrids is driving the adoption of DERMS to manage localized energy resources efficiently.

Decentralized Energy Markets The emergence of peer-to-peer energy trading and decentralized energy markets is creating new opportunities for DERMS providers.

Sustainability and Decarbonization The push for achieving net-zero carbon emissions is accelerating the adoption of DERMS globally.

The Distributed Energy Resource Management System market presents immense opportunities for innovation and growth. As renewable energy adoption continues to rise and grid modernization gains traction, the role of DERMS in ensuring energy reliability, efficiency, and sustainability becomes increasingly critical.

#Distributed Energy Resource Management System Market#DERMS Market#Distributed Energy Resource Management System Market Size#Distributed Energy Resource Management System Market Share#Distributed Energy Resource Management System Market Trends#Distributed Energy Resource Management System Market Growth#Distributed Energy Resource Management System Market Outlook#Distributed Energy Resource Management System Market Key Players#Distributed Energy Resource Management System Market Overview#Distributed Energy Resource Management System Market Competitor#Distributed Energy Resource Management System Market Insights#Distributed Energy Resource Management System Market Forecast#Distributed Energy Resource Management System Market Analysis#Distributed Energy Resource Management System Market Statistics#Distributed Energy Resource Management System Market Innovations

0 notes

Text

Distributed Energy Resource Management System Market: Assessing Market Dynamics

Global Distributed Energy Resource Management System market is expected to grow, owing to the growing focus on energy efficiency and the increasing demand for renewable energy throughout the forecast period.

According to TechSci Research report, “Distributed Energy Resource Management System Market - Global Industry Size, Share, Trends, Opportunity, and Forecast 2018-2028F”, the global distributed energy resource management system market is expected to register 15.48% CAGR during the forecast period, owing to rising government initiatives for residential buildings, power consumption, and the demand for effective energy management systems that maintain grid dependability and flexibility of the distributed energy source, along with the growing penetration of renewable energy sources.

Recent developments in DERMS include an increase in the use of sophisticated analytics, a rise in cloud use, appearance of blockchain-based solutions, and a sharper focus on cybersecurity. Advanced analytics are being used more frequently by energy suppliers to improve the efficiency of their distributed energy supplies. For instance, machine learning algorithms can be used to forecast patterns of energy consumption and modify the distribution of energy resources accordingly. Energy providers may now manage their distributed energy supplies more effectively and economically, thanks to cloud computing. Cloud-based solutions can automate repetitive activities, provide remote monitoring, control of dispersed energy resources, and provide real-time visibility into energy usage.

Global Distributed Energy Resource Management System Market is segmented based on software, application, end-user, and region. Based on software, the market is divided into virtual power plant, management & control, and analytics. Based on application, the market is divided into solar PV, energy storage, wind, EV charging stations, and others. Based on end-user, the market is fragmented into residential, commercial, and industrial. Based on region, the market is further bifurcated into North America, Asia-Pacific, Europe, South America, Middle East & Africa.

Browse over XX market data Figures spread through XX Pages and an in-depth TOC on the "Global Distributed Energy Resource Management System Market." https://www.techsciresearch.com/report/distributed-energy-resource-management-system-market/15687.html

Based on application, Solar PV segment is expected to dominate the market during 2022. Solar PV is one of the biggest distributed power sources in the world and can be put on rooftops or the ground. The average installed cost (USD/Kilowatt) is likely to decline, and an increase in installed capacity is anticipated to drive the distributed energy resources management system market. To avoid reverse flows and high local voltages, distributed energy resource management systems limit photovoltaic (PV) output in real-time.

Additionally, distributed generation is economically feasible because it requires significantly less capital investment than a comparable traditional facility. Distributed solar PV is being driven internationally by tax incentives for both solar power plants and distributed solar generation. The installed solar PV capacity worldwide in 2020 was 707.49 GW. Moreover, India has revealed plans to spend an additional USD 2356.70 million to increase domestic production of solar modules in order to achieve its ambitious goal of producing 280 GW of solar-fired electricity by 2030. Solar PV investments increased dramatically in the US due to business purchases. Such factors are expected to drive the Solar PV segment during 2022, as well as during the forecast period.

Key market players in the global distributed energy resource management system market are:

General Electric Company

Siemens AG

ABB Ltd

Schneider Electric SE

Engie SA

AutoGrid Systems Inc.

Doosan Corporation

Open Access Technology International Inc.

Mitsubishi Electric Corporation

Emerson Electric Co.

Download Free Sample Report https://www.techsciresearch.com/sample-report.aspx?cid=15687

Customers can also request for 10% free customization on this report.

"Expenditures in distributed energy resource management systems are expected to increase in response to the challenges faced by North America's power sector, including difficulties in meeting energy efficiency targets, adhering to federal carbon regulations, and effectively integrating diverse sources of distributed energy generation. This rise in spending is anticipated to increase as the region aims to become the dominant player in electricity demand.” said Mr. Karan Chechi, Research Director with TechSci Research, a research-based global management consulting firm.

“Distributed Energy Resource Management System Market – Global Industry Size, Share, Trends, Opportunity, and Forecast. 2018-2028F Segmented By Software (Virtual Power Plant, Management & Control, and Analytics), By Application (Solar PV, Energy Storage, Wind, EV Charging Stations, and Others), By End-User (Residential, Commercial, and Industrial), By Region,” has evaluated the future growth potential of Global Distributed Energy Resource Management System marketand provides statistics & information on market size, structure, and future market growth. The report intends to provide cutting-edge market intelligence and help decision makers take sound investment decisions. Besides the report also identifies and analyzes the emerging trends along with essential drivers, challenges, and opportunities in Global Distributed Energy Resource Management System market.

Browse Related Reports

Portable Fuel Cell Market https://www.techsciresearch.com/report/portable-fuel-cell-market/17078.html Renewable Energy Transformer Market https://www.techsciresearch.com/report/renewable-energy-transformer-market/17083.html Energy Security Market https://www.techsciresearch.com/report/energy-security-market/17390.html Commercial Vehicle SLI Battery Market https://www.techsciresearch.com/report/commercial-vehicle-sli-battery-market/17069.html Industrial Power Monitoring Market https://www.techsciresearch.com/report/industrial-power-monitoring-market/17072.html

Contact

TechSci Research LLC

420 Lexington Avenue,

Suite 300, New York,

United States- 10170

M: +13322586602

Email: [email protected]

Website: https://www.techsciresearch.com

#Distributed Energy Resource Management System Market#Distributed Energy Resource Management System Market Size#Distributed Energy Resource Management System Market Share#Distributed Energy Resource Management System Market Trends

0 notes

Text

The Distributed Energy Resource Management System Market is expected to reach USD 1.20 billion in 2023 and grow at a CAGR of 12.76% to reach USD 2.19 billion by 2028. Engie SA, General Electric Company, Siemens AG, Schneider Electric SE, ABB Ltd are the major companies.

#Distributed Energy Resource Management System Market#Distributed Energy Resource Management System Market Size#Distributed Energy Resource Management System Market Share#Distributed Energy Resource Management System Market Analysis#Distributed Energy Resource Management System Market Trends#Distributed Energy Resource Management System Market Report#Distributed Energy Resource Management System Market Research#Distributed Energy Resource Management System Industry#Distributed Energy Resource Management System Industry Report

0 notes

Text

#Saudi Arabia Distributed Energy Resource Management System Market#Market Size#Market Share#Market Trends#Market Analysis#Industry Survey#Market Demand#Top Major Key Player#Market Estimate#Market Segments#Industry Data

0 notes

Text

Europe distributed energy resources management system (DERMS) market is expected to gain market growth in the forecast period of 2021 to 2028. Data Bridge Market Research analyses that the market is growing with a CAGR of 5.1% in the forecast period of 2021 to 2028 and is expected to reach USD 787.09 million by 2028. The increasing demand for DERMS for cost reduction is boosting the market.

#Europe Distributed Energy Resources Management System (DERMS) Market#Europe Distributed Energy Resources Management System (DERMS) Market Share#Europe Distributed Energy Resources Management System (DERMS) Market Size#Europe Distributed Energy Resources Management System (DERMS) Market Growth.

0 notes

Text

4 Factors To Think About When Choosing Solar Energy For Buildings

Have you ever settled down to track down details to do with Solar Energy for Buildings just to find yourself staring google eyed at your computer screen? I know I have.The emergence of electric vehicles (EVs) has introduced new considerations for rural electrification planning. The need to provide adequate charging infrastructure in rural areas, where distances between settlements are greater, requires careful consideration of grid capacity and charging point distribution. Consumer perception and brand value have seen notable improvements among retailers who have visibly invested in solar power installations. Studies have shown that consumers are increasingly making purchasing decisions based on a company's environmental credentials, and the visible presence of solar panels on retail properties serves as a tangible demonstration of environmental commitment. This enhanced reputation can translate into increased customer loyalty and potentially higher sales figures, as environmentally conscious consumers choose to support businesses that align with their values. Local economic development receives a significant boost from community solar projects through job creation and skills development. The installation, maintenance, and administration of solar projects create employment opportunities within the community, while the process of establishing and running these initiatives helps develop valuable project management and technical skills among participants. The money saved on energy costs tends to be spent locally, creating a positive multiplier effect for the local economy. Research into biological solar cells, inspired by natural photosynthesis, is opening new possibilities for solar energy conversion. These bio-inspired systems could potentially offer new pathways for solar energy conversion and storage, though they remain in early stages of development. The adoption of solar power technology in Wales has witnessed a remarkable surge in recent years, offering business owners across the region an array of compelling advantages that extend far beyond simple energy generation. The unique geographical and climatic conditions of Wales, combined with government incentives and technological advancements, have created an environment where solar power installations represent a strategic investment for companies of all sizes. The solar power industry in the United Kingdom operates under a comprehensive framework of standards and regulations designed to ensure safety, efficiency, and reliability in solar installations. These standards are primarily overseen by the Microgeneration Certification Scheme (MCS), which works in conjunction with other regulatory bodies to maintain quality across the sector. The MCS certification is mandatory for solar installations that wish to participate in government incentive schemes and represents the cornerstone of quality assurance in the UK solar industry.

The implementation of solar panels in Scottish cities must navigate the complex interplay between historic preservation and renewable energy adoption, particularly in areas with protected buildings and conservation zones. Local authorities must balance the preservation of Scotland's rich architectural heritage, including its distinctive sandstone buildings and historic Royal Burghs, with the pressing need to reduce carbon emissions and meet renewable energy targets. Grid connection capacity has emerged as a critical constraint on solar deployment in many parts of the UK. The challenge of securing viable grid connections has led to increased interest in private wire arrangements and the development of local energy markets, where solar generation can be consumed close to the point of production. The development of solar power has created new forms of social capital and community resources. Technical knowledge about solar systems, installation expertise, and maintenance capabilities have become valuable community assets, shared through formal and informal networks. The adoption of solar power systems represents a significant opportunity for UK retirees seeking to establish predictable energy costs while living on fixed incomes. The volatile nature of traditional energy markets has created substantial financial uncertainty for pensioners, with energy bills often consuming an increasingly large portion of their monthly budget. At the renewable energy fair, Solar Panels Berkshire showcased their latest technology innovations.

Increase Home Value

The adoption of solar power has enabled many farms to improve their waste management and recycling operations through powered processing and treatment systems. Solar-powered waste management solutions help farms reduce their environmental impact while potentially creating additional value from agricultural byproducts. Vegetation management around ground-mounted solar arrays requires ongoing attention to prevent shading and ensure adequate airflow around the panels. This typically involves regular trimming of grass and shrubs, removal of any invasive species that might damage equipment, and maintaining clear access paths for maintenance personnel. The environmental benefits of solar power align with many retirees' desire to leave a positive legacy for future generations. The significant reduction in carbon emissions achieved through solar power adoption contributes to climate change mitigation efforts and demonstrates environmental responsibility to children and grandchildren. Solar installations have provided conservation organizations with practical examples of sustainable development that they can use to influence policy and planning decisions. Their experiences have contributed to the development of more environmentally sensitive approaches to renewable energy deployment across the UK. The solar industry's maturation has led to more competitive pricing and improved installation standards, benefiting retirees who choose to invest in solar power systems. The availability of experienced installers and standardized equipment has reduced both the cost and complexity of transitioning to solar energy. Many farmers across the region have partnered with Solar Panels Wiltshire to power their agricultural operations.

The integration of solar power into telecommunications networks has improved connectivity in remote regions while reducing operational costs. Solar-powered cell towers and communication repeaters operate reliably in locations where grid power is unavailable or unreliable. The integration of solar power with emerging technologies such as electric vehicles and heat pumps creates additional pathways to energy independence by reducing reliance on imported oil for transportation and natural gas for heating. This comprehensive approach to electrification, powered increasingly by domestic solar generation, represents a fundamental shift away from foreign energy dependence across multiple sectors of the economy. The integration of solar power with other clean energy technologies, particularly wind power and energy storage, represents an important frontier for the UK market. The development of hybrid projects and virtual power plants demonstrates the potential for solar to play a central role in a fully decarbonized energy system. Public awareness and education about energy storage technologies are crucial for their continued adoption and support. Understanding the benefits and limitations of different storage options can help communities and stakeholders make informed decisions about energy investments. The growing network of solar-equipped apartment buildings is creating opportunities for knowledge sharing and collective purchasing power. Building managers and resident associations can learn from each other's experiences and negotiate better terms with solar providers. The comprehensive guide to Solar Panels Oxfordshire provides valuable information for first-time buyers.

Peak Energy Production

The integration of solar power systems with energy storage capabilities represents one of the most significant developments in the renewable energy sector, fundamentally reshaping the economics of both residential and utility-scale power generation. This transformative technology combination is driving substantial changes across multiple sectors of the economy, from manufacturing and construction to energy markets and grid operations. The integration of solar power into the UK's electricity grid has necessitated significant adaptations in network infrastructure and management practices. Distribution network operators (DNOs) have developed new approaches to handle the intermittent nature of solar generation, including advanced forecasting systems and flexible connection agreements. The increasing availability of innovative financing options for solar power installations makes the technology more accessible to businesses of all sizes in Northern Ireland. The range of financing solutions, from traditional loans to power purchase agreements, enables businesses to choose the most appropriate funding structure for their specific circumstances and objectives. Government incentives and support schemes have historically played a crucial role in making solar power accessible to UK homeowners, though the landscape of these programs continues to evolve. The Smart Export Guarantee (SEG) scheme, which replaced the earlier Feed-in Tariff program, ensures that homeowners receive payment for excess electricity they export to the national grid, creating an additional revenue stream that enhances the financial appeal of solar installation. The cultural significance of solar power has evolved, becoming an important symbol of environmental commitment and social responsibility. Solar panels have become visible markers of environmental values and community engagement, influencing social status and identity. During the summer months, Solar Panels Buckinghamshire reported record-breaking energy production levels.

Environmental standards play an increasingly important role in the UK solar industry, with requirements for sustainable manufacturing processes and end-of-life recycling. The WEEE (Waste Electrical and Electronic Equipment) Regulations require manufacturers and installers to ensure proper disposal and recycling of solar panels and associated equipment at the end of their operational life. These regulations help minimize the environmental impact of solar installations and promote sustainable practices within the industry. The reduced carbon footprint achieved through solar power adoption can help Welsh businesses participate in green supply chains and secure contracts with organizations that have strict environmental criteria. This can open up new business opportunities and strengthen relationships with existing customers who prioritize environmental responsibility. The implementation of solar power projects has helped councils better understand the technical and operational requirements of renewable energy systems. This knowledge often proves valuable when evaluating other clean energy technologies and solutions. You can get additional intel on the topic of Solar Energy for Buildings on this Energy Saving Trust article.

Related Articles:

Background Insight With Regard To Solar Energy for UK Nationals Additional Insight About Solar Energy for Buildings Supplementary Information On Solar Power for Homes Extra Insight About Solar Power for UK Citizens Supplementary Findings About Solar Energy for Buildings

0 notes

Text

The Future of Oil and Gas Security: Market Dynamics and Opportunities

The global oil and gas security and service market size was estimated at USD 25.51 billion in 2023 and is expected to expand at a CAGR of 5.4% from 2024 to 2030. Various factors such as technologies and security threats, rising regulatory compliance, Growing adoption of advanced technologies, and focus on operational safety are driving the growth of the market. The oil and gas industry is a target for various security threats, including terrorism, piracy, theft, and sabotage. As these threats become more advanced, oil and gas companies are investing more in security measures to protect their assets and personnel.

The surge in the use of cloud technologies in the oil and gas sector has increased its exposure to cyber threats. Historically, industry has managed to protect data and ensure privacy by segregating networks and bolstering outer defenses. However, the introduction of cloud computing presents both a challenge and an opportunity for the sector to enhance and renew its security measures through the adoption of cyber security practices. One of the hurdles is that many firms lack the necessary expertise, funds, and in-house servers, pushing them toward cloud solutions for better data security.

Stringent government regulations and policies concerning energy security and environmental preservation require the oil and gas industry to implement robust security measures. Furthermore, the growing adoption of advanced technology like surveillance, access control, and intrusion detection systems is driving the market growth. Companies are proactively pouring resources into security solutions to mitigate risk and protect essential infrastructure. Additionally, the development of new exploration and production opportunities, especially in offshore and hard-to-reach areas, has created a need for specialized security services to address distinct challenges. These factors collectively are driving the growth and development of the security and services market in the oil and gas sector.

Global Oil And Gas Security And Service Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2017 to 2030. For this study, Grand View Research has segmented the global oil and gas security and service market report based on component, security, services, operation, application, and region.

Component Outlook (Revenue, USD Billion, 2017 - 2030)

Solution

Services

Security Outlook (Revenue, USD Billion, 2017 - 2030)

Physical Security

Network Security

Services Outlook (Revenue, USD Billion, 2017 - 2030)

Risk Management Services

System Design, Integration, and Consulting

Managed Services

Operation Outlook (Revenue, USD Billion, 2017 - 2030)

Upstream

Midstream

Downstream

Application Outlook (Revenue, USD Billion, 2017 - 2030)

Exploring and Drilling

Transportation

Pipelines

Distribution and Retail Services

Others

Regional Outlook (Revenue, USD Billion, 2017 - 2030)

North America

US

Canada

Mexico

Europe

UK

Germany

France

Asia Pacific

China

India

Japan

Australia

South Korea

Latin America

Brazil

MEA

UAE

South Africa

KSA

Key Oil And Gas Security And Service Companies:

The following are the leading companies in the oil and gas security and service market. These companies collectively hold the largest market share and dictate industry trends.

Cisco Systems, Inc.

Honeywell International Inc.

Huawei Technologies Co., Ltd.

Intel Corporation

Microsoft

NortonLifeLock Inc.

Schneider Electric

Siemens

United Technologies Inc.

Recent Developments

In April 2024, Siemens launched Siemens Xcelerator, to automatically verify vulnerable production assets. Therefore, it is imperative for industrial firms to detect and mitigate potential security gaps within their systems. Siemens introduced a new cybersecurity software-as-a-service solution in response to the urgency of pinpointing cybersecurity in shop floor promptly,

In September 2023, Huawei Technologies Co., Ltd. launched intelligent architecture and intelligent Exploration & production (E&P) solution for oil and gas industry. Huawei Technologies Co., Ltd.'s intelligent architecture for the oil and gas sector is constructed around six smart components: connectivity, sensing, platform, application, AI models, and foundation. Each component is structured with hierarchical decoupling. This design is adaptable to widely used third-party frameworks and is capable of integrating with third-party platforms and data lakes, whether they are existing or newly established.

In September 2022, ABB introduced ABB Ability Cyber Security Workplace (CSWP), which integrates security solutions from ABB and other providers into a unified, comprehensive digital platform, enhancing the protection of critical industrial infrastructure. This platform enables engineers and operators to more swiftly identify and resolve issues, thereby reducing risk exposure by making cybersecurity data more accessible and easier to manage.

Order a free sample PDF of the Oil And Gas Security And Service Market Intelligence Study, published by Grand View Research.

0 notes

Text

Sealant Applicator Market

Sealant Applicator Market Size, Share, Trends: 3M Company Leads

Rising Adoption of Smart and Connected Sealant Applicators Reshapes Industry Practices

Market Overview:

The global sealant applicator market is expected to develop at a 5.7% CAGR from 2024 to 2031. The market value is predicted to rise from USD XX billion in 2024 to USD YY billion in 2031. Asia-Pacific is expected to dominate the market, driven by rising urbanisation, increased construction activity, and expanding industrial applications. Rising demand for effective sealing solutions, technological breakthroughs in applicator design, and increased acceptance of automated application systems are all important variables to track.

The market is expanding rapidly due to the expanding construction and automotive industries, the increased emphasis on energy-efficient structures, and the growing requirement for precision in sealant application. Ergonomic design innovations, the introduction of multi-functional applicators, and the growing popularity of DIY home modifications are all driving market growth.

DOWNLOAD FREE SAMPLE

Market Trends:

The Sealant Applicator Market is seeing a significant change towards smart and connected devices, driven by the broader trend of digitalisation in industrial and construction tools. This tendency is especially obvious in professional-grade applicators, where precision and efficiency are critical. For example, a leading tool maker reported a 40% increase in sales of their IoT-enabled sealant guns in 2023 over the previous year. These smart applicators have capabilities like precise flow control, temperature monitoring, and usage tracking, which improve quality control and resource management. The integration of Bluetooth connectivity enables real-time data logging and remote monitoring, which is especially useful in large-scale building projects. This trend not only increases production, but it also improves the overall precision and consistency of sealant application across a variety of sectors.

Market Segmentation:

The Electric Sealant Applicator category has emerged as the leading force in the Sealant Applicator Market, accounting for around YY% of the total market share by 2023. This domination is partly due to the improved control, uniformity, and efficiency provided by electric applicators, which are especially popular in professional construction and industrial applications. Electric applicators offer accurate flow control and reduced operator fatigue, resulting in increased production and better application quality.

In recent years, manufacturers have focused on improving the capabilities of electric applicators to fulfil changing customer demands. For example, a leading power tool manufacturer recently developed a new range of cordless electric sealant guns with variable speed control and anti-drip capabilities, meeting professional users' expectations for greater versatility and precision. This innovation has received positive market feedback, with early users claiming up to a 30% increase in application efficiency.

The expanding tendency of automation in construction and manufacturing operations has also aided the segment's success. Many large-scale projects now include robotic sealant application systems, which use modern electric applicators for precision distribution. According to a recent industry survey, 65% of large construction businesses intend to boost their investments in automated sealing solutions over the next five years, which will drive demand for sophisticated electric applicator systems.

Market Key Players:

3M Company

Henkel AG & Co. KGaA

Graco Inc.

Illinois Tool Works Inc. (ITW)

Nordson Corporation

Bosch Limited

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

0 notes

Text

The Blockchain IoT Market is projected to grow from USD 556.7058 million in 2024 to an estimated USD 21,512.09 million by 2032, with a compound annual growth rate (CAGR) of 57.9% from 2024 to 2032.The integration of blockchain technology with the Internet of Things (IoT) is paving the way for a transformative era in connectivity and data security. The Blockchain IoT market has been rapidly gaining traction, driven by the increasing need for secure communication and data exchange in a hyper-connected world. This article explores the dynamics of the Blockchain IoT market, its drivers, challenges, and potential future growth.Blockchain is a decentralized ledger technology that ensures secure, transparent, and tamper-proof transactions. IoT, on the other hand, connects devices and systems through the internet to exchange data and perform automated tasks. When these two technologies converge, the result is a powerful ecosystem that enhances trust, security, and efficiency in device-to-device communication.

Browse the full report https://www.credenceresearch.com/report/blockchain-iot-market

Market Dynamics

The Blockchain IoT market has been fueled by several factors:

Enhanced Security: Traditional IoT systems are prone to cyber threats due to centralized architectures. Blockchain’s decentralized nature eliminates single points of failure, providing robust security against hacking and data breaches.

Transparency and Traceability: Blockchain enables immutable record-keeping, which is particularly beneficial in supply chain management, asset tracking, and compliance monitoring.

Data Integrity and Privacy: With blockchain, IoT devices can securely share and validate data without intermediaries, ensuring privacy and accuracy.

Cost Efficiency: By removing intermediaries and automating processes through smart contracts, blockchain reduces operational costs for IoT applications.

Key Applications of Blockchain IoT

Supply Chain Management: Blockchain IoT solutions are revolutionizing supply chains by providing real-time visibility, verifying product authenticity, and reducing counterfeiting.

Smart Cities: From traffic management to energy distribution, blockchain IoT facilitates seamless data sharing among smart city infrastructures while ensuring security and transparency.

Healthcare: IoT devices paired with blockchain can securely manage patient records, monitor medical devices, and ensure data accuracy for research and diagnostics.

Agriculture: Precision farming benefits from blockchain IoT by enabling secure data exchange between sensors, drones, and farmers, ensuring efficient resource use.

Energy Sector: Blockchain IoT is enabling decentralized energy grids where consumers can trade surplus energy directly with peers, ensuring efficiency and sustainability.

Challenges in the Blockchain IoT Market

Despite its potential, the Blockchain IoT market faces several challenges:

Scalability Issues: IoT networks generate vast amounts of data, and current blockchain solutions often struggle to handle such high transaction volumes efficiently.

High Energy Consumption: Blockchain protocols like proof-of-work consume significant energy, which may conflict with the sustainability goals of IoT applications.

Interoperability: The lack of standardized protocols across IoT devices and blockchain platforms poses integration challenges.

Regulatory and Compliance Concerns: Governments are still formulating regulations for blockchain and IoT technologies, creating uncertainty for businesses.

Initial Costs: Implementing blockchain IoT solutions requires substantial upfront investment in infrastructure and expertise.

Market Trends and Future Outlook

The Blockchain IoT market is projected to grow at an impressive compound annual growth rate (CAGR) over the next decade. Several trends are shaping this growth:

Adoption of Hybrid Blockchain Models: Combining public and private blockchains to optimize scalability and security for IoT applications.

Integration with Artificial Intelligence (AI): AI-driven IoT devices can utilize blockchain for secure data exchange and predictive analytics, opening new avenues for innovation.

Focus on Green Solutions: Development of energy-efficient blockchain protocols to address environmental concerns.

Expansion of 5G Networks: The rollout of 5G will enhance IoT connectivity and data speeds, accelerating the adoption of blockchain-based solutions.

Key Player Analysis:

IBM

Microsoft

Intel

Cisco Systems

IOTA

VeChain

Waltonchain

Honeywell

Huawei

Linux Foundation (Hyperledger)

Segmentation:

Based on Product Type:

Consumer IoT Devices

Industrial IoT (IIoT) Devices

Enterprise IoT Solutions

Based on Technology:

Cloud-Based Blockchain Solutions

Edge Computing with Blockchain

Hybrid Blockchain Solutions

Based on End-User:

Manufacturing

Healthcare

Automotive

Energy

Logistics

Retail

Agriculture

Based on Region:

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report https://www.credenceresearch.com/report/blockchain-iot-market

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

Bangladesh's power sector is largely composed of coal, natural gas, hydro, and renewable energy sources. In recent years, the government has made significant efforts to diversify its energy sources, with increasing investments in renewable energy, natural gas, and energy-efficient technologies. The country’s electricity generation capacity has increased substantially, and the government aims to meet the rising demand by ensuring a more reliable and sustainable power infrastructure. The growth of industries, the urbanization of the population, and the shift to cleaner energy solutions are key drivers of the market's expansion.

Trends Shaping the Bangladesh Power Market

Increase in Renewable Energy Investment: The Bangladesh government has set ambitious goals for increasing the share of renewable energy in the country’s power mix. Solar power, in particular, has seen substantial growth, with the government supporting solar home systems in rural areas and large-scale solar projects in urban regions. The country is also exploring wind and biomass power to complement its energy grid.

Energy Efficiency Initiatives: As part of its commitment to sustainability, Bangladesh is focusing on improving energy efficiency in both the industrial and residential sectors. The government and private sector are working together to promote energy-efficient technologies, such as LED lighting, high-efficiency appliances, and energy-saving building practices. This trend is not only helping to reduce overall demand but is also contributing to the country's climate goals.

Digitalization of the Power Sector: The Bangladesh power sector is beginning to adopt advanced digital technologies, including smart grids, smart meters, and remote monitoring systems. These innovations are improving energy distribution, reducing transmission losses, and enabling better management of electricity consumption. As digital solutions become more widespread, they are expected to further enhance the efficiency and reliability of the power sector.

Development of Infrastructure and Power Transmission: Significant investments are being made in transmission and distribution infrastructure to reduce power loss, ensure grid stability, and connect remote areas to the national grid. The expansion of high-voltage transmission lines and substations is essential for supporting the growing demand for electricity and integrating renewable energy into the national grid.

Focus on Energy Security and Sustainability: Energy security is a critical concern for Bangladesh, especially with its dependence on natural gas and imported coal for power generation. The government is working to strengthen energy security by exploring new sources of energy, improving domestic resource utilization, and enhancing efficiency across the power generation and distribution systems.

0 notes

Text

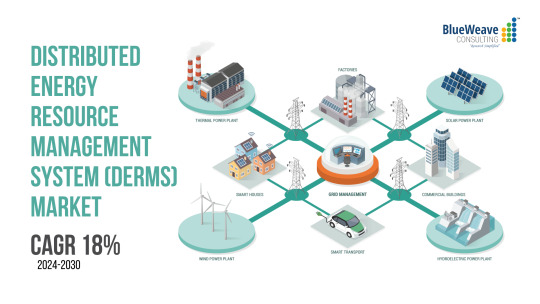

Distributed Energy Resource Management System (DERMS) Market size by value at USD 0.3 billion in 2023.During the forecast period between 2024 and 2030, BlueWeave expects Global Distributed Energy Resource Management System (DERMS) Market size to expand at a CAGR of 18% reaching a value of USD 1.0 billionby 2030. Global Distributed Energy Resource Management System (DERMS) Market is driven by the increasing adoption of renewable energy sources, the growing need for grid reliability and resilience, and advancements in energy storage technologies. Regulatory mandates for carbon emission reductions and incentives for distributed energy resources further fuel market growth. Rising electricity demand, coupled with the integration of smart grids and IoT technologies, supports efficient DER management. Additionally, the proliferation of electric vehicles (EVs) and microgrid solutions enhances DERMS adoption.

Sample: https://www.blueweaveconsulting.com/report/distributed-energy-resource-management-system-market/report-sample

Opportunity – Grid Modernization and Integration of DERs

Global Distributed Energy Resource Management System (DERMS) Market is driven by the modernization of electricity grids and the increasing adoption of distributed energy resources (DERs) like solar panels, wind turbines, and battery storage. Utilities and grid operators are deploying DERMS to optimize grid stability and efficiency amid the growing complexity of managing decentralized energy sources. The transition supports the integration of renewable energy, enhances grid resilience, and enables real-time monitoring, addressing the evolving needs of modern energy infrastructure.

#Blueweave#Consulting#marketreserch#marketforrecast#marketshare#DistributedEnergy#EnergyManagement#SmartEnergy#RenewableEnergy#SustainableEnergy#EnergyMarketTrends#MarketResearch#CleanEnergyFuture

0 notes

Text

Hydropower Plant Construction Market Report 2024-2033 | By Types, Applications, Regions And Players

The hydropower plant construction global market report 2024 from The Business Research Company provides comprehensive market statistics, including global market size, regional shares, competitor market share, detailed segments, trends, and opportunities. This report offers an in-depth analysis of current and future industry scenarios, delivering a complete perspective for thriving in the industrial automation software market.

Hydropower Plant Construction Market, 2024 report by The Business Research Company offers comprehensive insights into the current state of the market and highlights future growth opportunities.

Market Size - The hydropower plant construction market size has grown strongly in recent years. It will grow from $18.30 billion in 2023 to $19.60 billion in 2024 at a compound annual growth rate (CAGR) of 7.1%. The growth in the historic period can be attributed to rural electrification, government policies, environmental concerns, environmental concerns, water management.

The hydropower plant construction market size is expected to see strong growth in the next few years. It will grow to $24.51 billion in 2028 at a compound annual growth rate (CAGR) of 5.8%. The growth in the forecast period can be attributed to renewable energy policies, climate change mitigation, grid modernization, energy storage integration, water resource management. Major trends in the forecast period include run-of-river installations, hybrid systems, repowering and upgrading, public-private partnerships, climate resilience.

Order your report now for swift delivery @ https://www.thebusinessresearchcompany.com/report/hydropower-plant-construction-global-market-report

The Business Research Company's reports encompass a wide range of information, including:

1. Market Size (Historic and Forecast): Analysis of the market's historical performance and projections for future growth.

2. Drivers: Examination of the key factors propelling market growth.

3. Trends: Identification of emerging trends and patterns shaping the market landscape.

4. Key Segments: Breakdown of the market into its primary segments and their respective performance.

5. Focus Regions and Geographies: Insight into the most critical regions and geographical areas influencing the market.

6. Macro Economic Factors: Assessment of broader economic elements impacting the market.

Market Drivers - The rising interest in clean energy is expected to propel the growth of the hydropower plant construction market in the coming years. Clean energy is energy obtained from sources that do not emit greenhouse gases, such as nuclear power, hydroelectric power, solar, geothermal, wind, and tidal energy. The rising adoption of clean energy is due to several factors, including the growing awareness of climate change and environmental degradation, improvements in energy storage, and grid integration capabilities. The construction of hydropower plants makes it easier to generate sustainable energy by leveraging the power of water's movement to generate electricity while releasing zero greenhouse emissions. For instance, in June 2023, according to the Energy Information Administration, a US-based principal government statistical system institution in charge of obtaining, assessing, and distributing energy data, the usage of renewable energy in the United States increased modestly to an all-time high of 13.2 quads in 2022, up from 12.1 quads in 2021. Therefore, the rising interest in clean energy is driving the hydropower plant construction market.

Market Trends - Major companies operating in the hydropower plant construction market are focusing on digitization and automation for hydropower plants to strengthen their position in the market. Digital solutions are a collection of devices and applications that use digital technology to meet particular company requirements, such as data analysis, data processing, and operations. For instance, in June 2022, Voith Group, a Germany-based company that constructs hydropower plants, in collaboration with Ray Sono AG, a Germany-based digital solution company, launched the Hydro Pocket, a cloud-based application designed to monitor, analyze, and optimize hydropower stations. Hydro Pocket is a smart, one-stop solution for small to medium-sized hydropower facilities that increases operator efficiency, flexibility, and security. The cloud-based tool handles the system data in a 'smart' way. Maintenance and repair planning is optimized, and problems or unexpected downtime can be eliminated because of the clear picture of assets and support in the form of sophisticated analytical techniques. As a consequence, system management is simplified while communication needs are lowered.

The hydropower plant construction market covered in this report is segmented –

1) By Type: Water Storage, Diverted, Pumped Storage 2) By Capacity: Large hydropower plants, Medium hydropower plants, Small hydropower plants, Other Capacities 3) By Application: City Power Supply, Industrial Power Supply, Military Power Supply, Other Applications

Get an inside scoop of the hydropower plant construction market, Request now for Sample Report @ https://www.thebusinessresearchcompany.com/sample.aspx?id=14397&type=smp

Regional Insights - Asia-Pacific was the largest region in the hydropower plant construction market in 2023. The regions covered in the hydropower plant construction market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East, Africa.

Key Companies - Major companies operating in the hydropower plant construction market are PowerChina Group, Bouygues Construction SA, Sinohydro Corporation, Vinci Construction, Siemens Energy AG, ABB Group, Duke Energy Corporation, Toshiba Corporation, China Three Gorges Corporation, Strabag SE, Statkraft AS, Skanska Group, Hydro-Québec, Verbund AG, Enel Green Power, Webuild SpA, Dongfang Electric Corporation, Andritz AG, Suez Group, RusHydro, SNC-Lavalin Group Inc., BC Hydro, Voith Group, GE Renewable Energy, Astaldi S.p.A., Bharat Heavy Electricals Limited (BHEL), Alstom SA, Innergex Renewable Energy Inc., Voimaosakeyhtiö SF

Table of Contents 1. Executive Summary 2. Hydropower Plant Construction Market Report Structure 3. Hydropower Plant Construction Market Trends And Strategies 4. Hydropower Plant Construction Market – Macro Economic Scenario 5. Hydropower Plant Construction Market Size And Growth ….. 27. Hydropower Plant Construction Market Competitor Landscape And Company Profiles 28. Key Mergers And Acquisitions 29. Future Outlook and Potential Analysis 30. Appendix

Contact Us: The Business Research Company Europe: +44 207 1930 708 Asia: +91 88972 63534 Americas: +1 315 623 0293 Email: [email protected]

Follow Us On: LinkedIn: https://in.linkedin.com/company/the-business-research-company Twitter: https://twitter.com/tbrc_info Facebook: https://www.facebook.com/TheBusinessResearchCompany YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ Blog: https://blog.tbrc.info/ Healthcare Blog: https://healthcareresearchreports.com/ Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model

0 notes

Text

Sify: Redefining Digital Asset Management for Modern Enterprises

In today’s data-driven world, businesses generate and rely on an ever-growing volume of digital assets—from marketing content and product designs to sensitive customer information and operational documents. Effective management of these assets is crucial to maintaining efficiency, ensuring compliance, and driving innovation. As a leading provider of Digital Asset Management (DAM) solutions, Sify Technologies empowers enterprises with tools and strategies to manage, organize, and secure their digital resources.

The Need for Digital Asset Management

Modern enterprises face challenges such as:

Data Overload: Managing vast volumes of digital files across multiple platforms.

Inefficient Workflows: Time lost searching for or recreating misplaced assets.

Security Risks: Threats of unauthorized access and data breaches.

Collaboration Hurdles: Difficulty in sharing and updating assets across departments and geographies.

Sify addresses these challenges with its advanced Digital Asset Management services, enabling businesses to streamline operations and enhance productivity.

Sify’s Digital Asset Management Solutions

Centralized Storage and Access Sify’s DAM solutions provide a unified platform for storing all digital assets, ensuring quick and seamless access to files. Advanced metadata tagging and search capabilities enable users to locate assets with ease.

Scalable Infrastructure Built on cloud-first principles, Sify’s DAM solutions can scale effortlessly to accommodate the growing demands of businesses, regardless of size or industry.

Enhanced Security Leveraging industry-leading security protocols, Sify ensures assets are protected from unauthorized access, theft, and loss. Role-based access controls and encryption mechanisms safeguard sensitive information.

Automated Workflows Sify streamlines the management of digital assets by automating repetitive tasks like file tagging, version control, and distribution, reducing manual effort and errors.

Seamless Collaboration Teams across different geographies can work on shared assets simultaneously, ensuring faster project execution. Real-time updates and tracking ensure version control and eliminate duplication.

Integration Capabilities Sify’s DAM solutions integrate seamlessly with existing enterprise software, including marketing automation tools, CRM systems, and content management platforms, ensuring smooth workflows.

Benefits of Choosing Sify

Operational Efficiency: By automating asset management tasks, businesses save time and reduce operational costs.

Enhanced Creativity: Easy access to digital assets frees up creative teams to focus on innovation rather than administrative tasks.

Improved Compliance: Sify ensures that assets are managed in compliance with data privacy regulations and industry standards.

Global Accessibility: Cloud-based solutions allow users to access assets anytime, anywhere, on any device.

Industries We Serve

Sify’s Digital Asset Management services cater to a diverse range of industries:

Media and Entertainment: Managing high volumes of videos, images, and creative files.

Retail and E-Commerce: Organizing product catalogs, marketing assets, and customer data.

Healthcare: Safeguarding sensitive patient records and clinical data.

Manufacturing: Managing technical documentation, blueprints, and designs.

Why Sify?

Proven Expertise: Decades of experience in delivering tailored digital solutions across sectors.

Innovative Technology: Leveraging the latest advancements in cloud computing, AI, and automation.

Customer-Centric Approach: Solutions designed to address specific business challenges and goals.

Sustainability Commitment: Energy-efficient operations that align with global sustainability standards.

Empower Your Digital Transformation with Sify

Sify’s Digital Asset Management services are not just about storing files; they are about enabling businesses to unlock the full potential of their digital assets. By optimizing workflows, enhancing security, and promoting collaboration, Sify helps organizations achieve new levels of productivity and innovation.

0 notes

Text

Key Trends Shaping the Future of the Flow Meter Market

The global flow meter market was valued at USD 10.02 billion in 2023 and is projected to expand at a compound annual growth rate (CAGR) of 5.5% from 2024 to 2030. In 2020, the market shipment size was recorded at 53,78,749 units, reflecting the ongoing demand for flow rate measurement technology across various industries. Over the forecast period, the market is expected to experience significant growth, primarily driven by the increasing need for accurate flow rate measurements in industries such as oil and gas (O&G), chemical processing, and petroleum refining.

One of the main drivers of this market growth is the rising demand for flow rate measurement in O&G management applications globally. The oil and gas industry, in particular, relies heavily on flow meters to measure the flow of liquids, gases, and vapors in pipelines, refining processes, and distribution networks. The increasing exploration and production activities in the O&G sector, including the recent discovery of shale gas reserves in North America, Europe, and the Asia Pacific, are expected to create significant demand for flow meters. These regions are likely to see expanded investments in oil and gas infrastructure, which will, in turn, boost the market for flow measurement instruments.

Besides O&G, other industrial sectors such as water and wastewater, power generation, and pulp and paper are also expected to contribute to the market growth. These industries are increasingly adopting measurement technologies and instruments to monitor and control the flow of fluids in their operations, ensuring efficiency, safety, and regulatory compliance. The growing emphasis on environmental sustainability and resource management is pushing these industries to invest in advanced flow meters for monitoring water usage, energy generation, and waste management.

An important trend that will influence the market in the coming years is the increased demand for intelligent systems. The integration of the Internet of Things (IoT) has paved the way for smart measurement solutions, which offer real-time data collection, remote monitoring, and predictive analytics. This has made flow meters not just tools for measurement, but also integral components in smart manufacturing and automation systems. With this integration, companies can optimize their operations, reduce energy consumption, and improve system reliability.

Gather more insights about the market drivers, restrains and growth of the Flow Meter Market

Regional Insights

The North American flow meter market is driven by the presence of key players such as General Electric, Emerson Electric Corporation, and Honeywell International Inc., who significantly contribute to the region's market share in terms of revenue. These industry giants play a vital role in the development and distribution of advanced flow measurement technologies, driving growth in the U.S. and Canada.

U.S. Flow Meter Market

In the U.S., the flow meter market is expected to account for a significant share of the North American market. The ongoing digitalization and the integration of IoT-enabled flow meters are expected to boost market growth. These advanced systems offer remote monitoring, predictive maintenance, and real-time data analytics, making them increasingly popular across industries. The adoption of these technologies is enhancing operational efficiency, reducing downtime, and improving overall system performance, which is anticipated to accelerate market expansion in the U.S. over the forecast period.

Europe Flow Meter Market Trends

Europe dominated the global flow meter market, holding over 35.37% of the global revenue share in 2023. The region has a high adoption rate of flow measurement systems, particularly in the power generation sector, which contributes significantly to the regional market's growth. In addition, the demand for advanced flow meters such as magnetic, ultrasonic, and Coriolis flow meters is expected to increase in the oil and gas (O&G) industry as the region focuses on more efficient and sustainable energy solutions.

Europe is home to several major manufacturers and providers of flow measurement technologies, including Endress+Hauser AG, Krohne Messtechnik GmbH, and ABB Ltd. These companies play a pivotal role in driving the market in Europe, and the region's strong industrial base, particularly in manufacturing, chemical, and O&G industries, ensures continued growth. As a result, Europe accounted for the largest market share in 2020, and this dominance is expected to persist throughout the forecast period.

• U.K. Flow Meter Market: The U.K. is expected to hold a significant share of the European flow meter market. Demand for flow meters is being driven by growing emphasis on water conservation and environmental protection, particularly in industries such as water and wastewater management. Accurate flow measurement is crucial in these sectors to optimize resource use, improve efficiency, and ensure regulatory compliance.

• Germany Flow Meter Market: The German flow meter market is expected to capture a substantial revenue share in Europe. Germany's strong manufacturing sector, particularly in industries like oil and gas, chemicals, and pharmaceuticals, has driven high demand for flow meters in process monitoring and control applications. Germany's focus on advanced industrial automation and technological innovation further boosts the demand for precision measurement instruments like flow meters.

• France Flow Meter Market: The French market for flow meters is expected to grow significantly, driven by technological advancements such as the integration of digital and wireless technologies. These advancements enable enhanced accuracy, reliability, and remote monitoring capabilities, making flow meters even more vital in sectors like water management and industrial process control.

APAC Flow Meter Market Trends

The Asia-Pacific (APAC) region is anticipated to witness a substantial CAGR of over 7.1% from 2024 to 2030. Growth in this region is largely driven by ongoing developments in the water and wastewater management sector in countries like India and China.

• China Flow Meter Market: China is expected to capture a significant revenue share in the APAC flow meter market. The country’s rapid industrialization and urbanization are driving a rising demand for flow meters across a variety of industries, including oil and gas, water and wastewater management, chemicals, and pharmaceuticals. As China continues to develop its infrastructure and industrial base, the need for accurate and efficient flow measurement solutions will continue to increase.

• India Flow Meter Market: The Indian market is expected to experience significant growth, fueled by the country's focus on infrastructure development, particularly in sectors such as energy, utilities, and construction. The increasing demand for flow meters in these industries to monitor and control fluid flow in pipelines, plants, and facilities is expected to drive the market.

• Japan Flow Meter Market: Japan is also projected to hold a significant revenue share in the APAC flow meter market. Stringent environmental regulations in Japan, aimed at curbing pollution and ensuring efficient resource management, have driven the widespread adoption of flow meters to measure and manage water, air, and other fluids. The demand for accurate measurement solutions in both industrial and environmental sectors is expected to continue growing.

Brazil Flow Meter Market Trends

The Brazil flow meter market is expected to capture a significant revenue share within the Latin American flow meter market. Technological advancements, including the rise of smart meters and the digitalization of flow measurement systems, have played a crucial role in the market's growth. These innovations offer improved accuracy, efficiency, and enhanced data management capabilities, all of which are contributing to the increasing demand for flow meters in Brazil.

Saudi Arabia Flow Meter Market Trends

The flow meter market in Saudi Arabia (KSA) is anticipated to grow significantly in the coming years, driven by an expanding industrial base, rising infrastructure needs, and increasing focus on environmental sustainability. As the country invests in infrastructure projects and adopts cleaner energy solutions, the demand for advanced flow meters to monitor fluid flows in industrial processes, utilities, and environmental applications will continue to rise.

Browse through Grand View Research's Sensors & Controls Industry Research Reports.

• The global industrial automation and control systems market size was estimated at USD 206.33 billion in 2024 and is anticipated to witness a CAGR of 10.8% from 2025 to 2030.

• The global biometric sensor market size was valued at USD 2.09 billion in 2024 and is projected to grow at a CAGR of 19.8% from 2025 to 2030.

Key Flow Meter Company Insights

The flow meter market is highly competitive, with companies employing various strategies such as partnerships, business expansions, new product developments, and contracts to increase their market share. Geographic expansion, through partnerships and collaborations, along with mergers and acquisitions, is a key strategy for market growth. Companies are also investing heavily in R&D to develop innovative and differentiated products that cater to specific industry needs.

Some of the prominent players in the flow meter market include:

• ABB Ltd.: A global leader in industrial automation and digitalization solutions.

• Emerson Electric Corporation: Specializing in a wide range of automation and measurement solutions.

• General Electric: A multinational conglomerate with strong operations in energy and industrial technologies.

• Krohne Messtechnik GmbH: A leading manufacturer of industrial process instrumentation, including flow meters, for various sectors.

• HÖNTZSCH GMBH & CO. KG: Known for its high-precision flow measurement equipment.

• Hitachi High-Tech Corporation: Specializing in advanced measurement solutions for industrial applications.

• Siemens: A global powerhouse in electrical engineering and industrial automation, offering comprehensive flow measurement solutions.

Key Flow Meter Companies:

The following are the leading companies in the flow meter market. These companies collectively hold the largest market share and dictate industry trends. Financials, strategy maps & products of these flow meter companies are analyzed to map the supply network.

• ABB Ltd.

• Emerson Electric Corporation

• em-tec GmbH

• Endress+Hausar AG

• General Electric

• Hitachi High-Tech Corporation

• Honeywell International Inc.

• HÖNTZSCH GMBH & CO. KG

• Krohne Messtechnik Gmbh

• Siemens

• Yokogawa Electric Corporation

Order a free sample PDF of the Flow Meter Market Intelligence Study, published by Grand View Research.

0 notes

Text

Microgrid Market: Role in Enhancing Energy Resilience and Reliability

The Microgrid Market size was valued at USD 32.10 billion in 2023 and is expected to grow to USD 128.33 billion by 2031 and grow at a CAGR of 18.91 % over the forecast period of 2024–2031.

Market Overview

A Microgrid is a localized energy system that can operate independently or in coordination with the main power grid. It integrates various energy sources like solar, wind, and battery storage, offering a solution for areas looking to improve energy efficiency, reduce emissions, and ensure energy security. With the global push for clean and resilient energy systems, microgrids are increasingly viewed as a crucial element for achieving these goals.

The demand for microgrids is being driven by several factors, including the growing need for reliable power in remote and off-grid areas, the increasing use of renewable energy sources, advancements in energy storage technology, and the focus on energy independence. These factors are expected to fuel the market’s expansion during the forecast period.

Key Market Segmentation

The Microgrid Market is segmented by offering, connectivity, power source, pattern, microgrid type, power rating, end use, and region.

By Offering

Hardware: This segment includes physical components such as generators, batteries, inverters, and controllers that are required to build and operate a microgrid. Hardware represents a significant share of the market as it forms the core infrastructure of any microgrid system.

Software: The software component involves management systems, energy management software, and control systems that optimize microgrid operations, improve efficiency, and ensure seamless integration with renewable energy sources. With advancements in digitalization, the software market for microgrids is expected to grow rapidly.

Services: Services include design, installation, maintenance, and system integration. The growth of this segment is tied to the increasing complexity of microgrid installations and the demand for tailored solutions that meet specific energy needs.

By Connectivity

Grid Connected: Grid-connected microgrids are integrated with the main power grid, allowing them to draw power when necessary and sell excess energy back to the grid. This configuration is increasingly popular for urban areas and regions with stable electricity infrastructure, offering benefits such as cost savings and energy efficiency.

Off-grid Connected: Off-grid microgrids operate independently of the main grid, making them ideal for remote, rural, or island locations where centralized power supply is unavailable. The off-grid segment is expected to grow significantly due to the increasing demand for energy in isolated regions.

By Power Source

Renewable Power Sources: Microgrids can be powered by renewable energy sources like solar, wind, hydro, and biomass. The adoption of renewable energy is a key driver in the growth of the microgrid market, as these sources reduce dependency on fossil fuels and help in achieving sustainability targets.

Non-Renewable Power Sources: Some microgrids still rely on non-renewable power sources like diesel generators for backup power. However, the trend is shifting towards cleaner and greener power sources as renewable energy becomes more affordable and accessible.

By Pattern

Urban/Metropolitan: Urban and metropolitan microgrids are generally grid-connected and integrate various distributed energy resources. These microgrids aim to enhance grid reliability, reduce power outages, and integrate renewable energy sources into urban infrastructure.

Semi-urban: Semi-urban microgrids are designed to meet the energy needs of areas with mixed urban and rural characteristics. They often include both grid-connected and off-grid solutions, offering flexibility and energy security.

Rural/Island: Rural and island microgrids are predominantly off-grid and powered by renewable energy sources like solar and wind. These systems provide much-needed energy independence and resilience to areas with limited or no access to centralized electricity networks.

By Microgrid Type

Remote Microgrids: These microgrids operate in isolated locations, often in off-grid settings, providing energy independence and reducing reliance on expensive and polluting fossil fuels. The growth in the deployment of renewable-powered off-grid systems is expected to expand the market for remote microgrids.

Grid-Connected Microgrids: These systems are integrated into the main grid, offering both energy independence and the ability to export excess energy back to the grid. These microgrids are more common in urban and industrial settings where reliable grid access is available.

Hybrid Microgrids: Hybrid systems combine multiple energy sources, including renewable and non-renewable sources, providing increased energy reliability and security. The adoption of hybrid microgrids is expected to grow, especially in locations with inconsistent renewable resource availability.

By Power Rating

Less than 1 MW: Small-scale microgrids designed for residential or small commercial use fall into this category. These systems are cost-effective and offer localized energy solutions for remote communities and small businesses.

1 MW to 5 MW: Mid-sized microgrids cater to the energy needs of larger communities, industrial facilities, or campuses, where a more significant amount of power is required for smooth operation.

5 MW to 10 MW: These microgrids are used for larger industrial complexes or community-based projects. They offer a balance between cost-effectiveness and scalability.

More than 10 MW: Large-scale microgrids are used for industrial sectors, large military installations, and city-scale applications. These systems typically involve advanced technologies for energy management and optimization.

By End Use

Residential: Microgrids designed for residential use provide power to households in areas with limited grid access or where energy security is a concern. The growing focus on sustainable living and energy efficiency is driving the adoption of residential microgrids.

Commercial: Commercial microgrids are deployed to support businesses and office buildings, providing reliability, cost savings, and energy resilience.

Industrial: Industrial microgrids are used by large factories, warehouses, and critical infrastructure facilities, where uninterrupted power supply is crucial for operation.

Others: This category includes microgrids used for military, remote research facilities, and essential services like hospitals.

Market Trends and Growth Drivers

Rising Demand for Renewable Energy: The transition to renewable energy is a key driver in the microgrid market. Microgrids offer a viable solution for integrating renewable power into local energy systems, reducing dependency on fossil fuels and minimizing carbon emissions.

Energy Independence and Security: The growing need for reliable and resilient energy sources, especially in regions prone to natural disasters, power outages, and geopolitical risks, is accelerating the adoption of microgrids. These systems provide energy security and reduce vulnerability to power grid disruptions.

Technological Advancements: Advances in energy storage, smart grid technology, and microgrid management software are improving the efficiency and cost-effectiveness of microgrids, making them more attractive to various industries.

Government Support and Incentives: Governments around the world are investing in clean energy and microgrid infrastructure, offering subsidies, grants, and regulatory support to encourage the development of decentralized energy systems.

Conclusion

The Microgrid Market is set for substantial growth from 2024 to 2031, driven by increasing energy demand, the rise of renewable energy sources, and the need for more resilient and reliable power systems. With the expansion of microgrid applications across various regions, including urban, semi-urban, and rural areas, there are vast opportunities for stakeholders to invest in and capitalize on the growth of this market.

About the Report This comprehensive market research report provides insights into the Global Microgrid Market, highlighting key trends, technologies, and regional opportunities. It serves as an essential resource for stakeholders to make informed decisions and tap into emerging market opportunities.

Read Complete Report Details of Microgrid Market 2024–2031@ https://www.snsinsider.com/reports/microgrid-market-3311

About Us:

SNS Insider is a global leader in market research and consulting, shaping the future of the industry. Our mission is to empower clients with the insights they need to thrive in dynamic environments. Utilizing advanced methodologies such as surveys, video interviews, and focus groups, we provide up-to-date, accurate market intelligence and consumer insights, ensuring you make confident, informed decisions. Contact Us: Akash Anand — Head of Business Development & Strategy [email protected] Phone: +1–415–230–0044 (US) | +91–7798602273 (IND)

0 notes