#Disposable Medical Devices Industry Share

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

The Tumblr app for Google Glass was released on May 16, 2013.

Text

Medical Disposables Market to be worth US$ 326 Billion by 2033, Reveals Future Market Insights

The Medical Disposables Market revenues were estimated at US$ 153.5 Billion in 2022 and is anticipated to grow at a CAGR of 7.1% from 2023-2033, according to a recently published Future Market Insights report. By the end of 2033, the market is expected to reach US$ 326 Billion. Bandages and Wound Dressings commanded the largest revenue share in 2022 and is expected to register a CAGR of 6.8% from 2023 to 2033.

The rising incidence of Hospital Acquired Infections, an increasing number of surgical procedures, and the growing prevalence of chronic diseases leading to longer hospital admission have been the key factors driving the market.

The subsequent spike in the number of chronic illness cases and a rise in the rate of hospitalizations has fueled the field of emergency medical disposables growth. The expansion of the medical disposables market is being fueled by an increase in the prevalence of hospital-acquired illnesses and disorders, as well as a greater focus on infection prevention. For example, the prevalence of healthcare-associated infection in high-income countries ranges from 3.5% to 12%, whereas it ranges from 5.7% to 19.1% in low and medium-income countries.

A growing geriatric population, an increase in the incidence of incontinence issues, mandatory guidelines that must be followed for patient safety at healthcare institutions, and an increase in demand for sophisticated healthcare facilities is driving the medical disposables market.

The market in North America is expected to reach a valuation of US$ 131 Billion by 2033 from US$ 61.7 Billion in 2022. In August 2000, the Food and Drug Administration (FDA) issued guidance concerning healthcare single-use items reprocessed by third parties or hospitals. In this guidance, FDA stated that hospitals or third-party reprocessors would be considered manufacturers and regulated in the exact same manner. A newly used single-use device still has to fulfill the criteria for device activation required by its flagship when it was originally manufactured. Such regulations have been creating a positive impact on the medical disposables market in the U.S. market in specific and the North American market in general

Competitive Landscape

The key companies in the market are engaged in mergers, acquisitions and partnerships.

The key players in the market include 3M, Johnson & Johnson Services, Inc., Abbott, Becton, Dickinson & Company, Medtronic, B. Braun Melsungen AG, Bayer AG, Smith and Nephew, Medline Industries, Inc., and Cardinal Health.

Some of the recent developments of key Medical Disposables providers are as follows:

In April 2019, Smith & Nephew PLC purchased Osiris Therapeutics, Inc. with the goal of expanding its advanced wound management product range.

In May 2019, 3M announced the acquisition of Acelity Inc., with the goal of strengthening wound treatment products.

For More Information: https://www.futuremarketinsights.com/reports/medication-dispenser-market

More Insights Available

Future Market Insights, in its new offering, presents an unbiased analysis of the Medical Disposables Market, presenting historical market data (2018-2022) and forecast statistics for the period of 2023-2033.

The study reveals essential insights by Product (Surgical Instruments & Supplies, Infusion, and Hypodermic Devices, Diagnostic & Laboratory Disposables, Bandages and Would Dressings, Sterilization Supplies, Respiratory Devices, Dialysis Disposables, Medical & Laboratory Gloves), by Raw Material (Plastic Resin, Nonwoven Material, Rubber, Metal, Glass, Others), by End-use (Hospitals, Home Healthcare, Outpatient/Primary Care Facilities, Other End-use) across five regions (North America, Latin America, Europe, Asia Pacific and Middle East & Africa).

Market Segments Covered in Medical Disposables Industry Analysis

By Product Type:

Surgical Instruments & Supplies

Would Closures

Procedural Kits & Trays

Surgical Catheters

Surgical Instruments

Plastic Surgical Drapes

By Raw Material:

Plastic Resin

Nonwoven Material

Rubber

Metals

Glass

Other Raw Materials

By End-use:

Hospitals

Home Healthcare

Outpatient/Primary Care Facilities

Other End-uses

2 notes

·

View notes

Text

Electric Mobility Scooter Market Supply Chain Challenges and Future Strategies to 2033

The global electric mobility scooter market is experiencing significant growth, driven by technological advancements, an aging population, and increasing environmental awareness. As of 2023, the market was valued at approximately USD XX billion and is projected to grow at a compound annual growth rate (CAGR) of around XX% from 2024 to 2032.This article delves into the current industry trends, market segmentation, regional insights, and future forecasts for the electric mobility scooter market up to 2032.

Market Overview

Electric mobility scooters are battery-powered devices designed to assist individuals with mobility challenges. They offer a convenient and eco-friendly alternative to traditional mobility aids, enhancing the independence and quality of life for users. The market encompasses a variety of scooter types, including three-wheel and four-wheel configurations, catering to diverse consumer needs.

Download a Free Sample Report:-https://tinyurl.com/5bec3j95

Key Market Drivers

Aging Population: The global increase in the elderly population has led to a higher prevalence of mobility-related issues, boosting the demand for electric mobility scooters.

Technological Advancements: Innovations such as improved battery life, lightweight materials, and enhanced safety features have made electric mobility scooters more appealing to consumers.

Environmental Concerns: Growing awareness of environmental sustainability has encouraged the adoption of electric-powered devices over fossil fuel-dependent alternatives.

Urbanization: Rapid urban development has increased the need for compact and efficient personal mobility solutions, positioning electric scooters as a viable option.

Market Segmentation

The electric mobility scooter market can be segmented based on type, application, and distribution channel:

By Type:

Three-Wheel Scooters: Known for their maneuverability, suitable for indoor use and smooth surfaces.

Four-Wheel Scooters: Offer enhanced stability, ideal for outdoor use and uneven terrains.

By Application:

Personal Use: Individuals using scooters for daily activities and personal mobility.

Commercial Use: Utilization in settings like airports, shopping malls, and hospitals to assist individuals with mobility challenges.

By Distribution Channel:

Online Retailers: E-commerce platforms providing a wide range of products with home delivery options.

Specialty Stores: Physical stores specializing in mobility aids, offering personalized services and after-sales support.

Direct Sales: Manufacturers selling directly to consumers, often providing customization options.

Regional Insights

North America: Holds a significant market share due to a well-established healthcare infrastructure and high consumer awareness.

Europe: Exhibits substantial growth, driven by supportive government policies and an increasing elderly population.

Asia Pacific: Anticipated to experience the highest growth rate, attributed to rapid urbanization, rising disposable incomes, and a large aging demographic.

Latin America and Middle East & Africa: Emerging markets with growing awareness and improving economic conditions, expected to contribute to market expansion.

Competitive Landscape

The electric mobility scooter market is characterized by the presence of several key players focusing on product innovation, quality enhancement, and strategic partnerships to strengthen their market position. Notable companies include:

Pride Mobility Products Corp.: A leading manufacturer known for its diverse range of mobility scooters, emphasizing quality and user comfort.

Drive Medical: Offers a wide array of mobility solutions, focusing on affordability and accessibility.

Golden Technologies: Specializes in high-end mobility scooters, integrating advanced features and customization options.

Invacare Corporation: Provides a comprehensive range of mobility products, with a strong emphasis on research and development.

Future Outlook

The electric mobility scooter market is poised for continued growth, supported by:

Technological Innovations: Ongoing research in battery technology and materials science is expected to yield lighter, more efficient, and longer-lasting scooters.

Policy Support: Government initiatives promoting accessibility and environmental sustainability are likely to encourage the adoption of electric mobility scooters.

Expanding Distribution Networks: The proliferation of online retail and direct-to-consumer sales models will make these devices more accessible to a broader audience.

Customization Trends: Manufacturers are increasingly offering customizable options to cater to individual user needs, enhancing user satisfaction and market penetration.

Conclusion

The global electric mobility scooter market is on an upward trajectory, driven by demographic shifts, technological advancements, and a growing emphasis on sustainable and accessible transportation solutions. As the market evolves, stakeholders focusing on innovation, quality, and user-centric designs are poised to capitalize on the burgeoning opportunities through 2032 and beyond.

Read Full Report:-https://www.uniprismmarketresearch.com/verticals/automotive-transportation/electric-mobility-scooter.html

0 notes

Text

Suction Cannula Market Demand, Supply and Excellent CAGR 2024 - 2032

The Reports and Insights, a leading market research company, has recently releases report titled “Suction Cannula Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2024-2032.” The study provides a detailed analysis of the industry, including the global Suction Cannula Market share, size, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights:

How big is the Suction Cannula Market?

The global suction cannula markеt size reached US$ 182.2 million in 2023. Looking forward, Reports and Insights expects the market to reach US$ 304.6 million in 2032, exhibiting a growth rate (CAGR) of 7.2% during 2024-2032.

What are Suction Cannula?

A suction cannula is a medical tool utilized in a variety of medical procedures, especially in surgery and wound care, to extract fluids, tissues, or gases from the body. It comprises a slender, hollow tube with a tapered end and multiple side openings, connected to a suction device. The tapered end is inserted into the body through a small incision or wound, and the suction device generates a vacuum that draws out the desired material. Suction cannulas come in various sizes and shapes to accommodate different purposes, including liposuction, thoracic drainage, and wound cleaning.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/1527

What are the growth prospects and trends in the Suction Cannula industry?

The suction cannula market growth is driven by various factors. The market for suction cannulas is steadily growing, propelled by the rising incidence of surgical interventions and the increasing preference for minimally invasive procedures. These cannulas are crucial instruments used across various medical specialties, such as cosmetic surgery, general surgery, and wound care, for efficient removal of fluids and tissues. Market growth is further driven by advancements in cannula design, the expanding elderly population, and the improving healthcare infrastructure in developing nations. Moreover, the surging popularity of liposuction treatments and the preference for disposable suction cannulas are also driving market expansion. Hence, all these factors contribute to suction cannula market growth.

What is included in market segmentation?

The report has segmented the market into the following categories:

North America

United States

Canada

Europe

Germany

United Kingdom

France

Italy

Spain

Russia

Poland

Benelux

Nordic

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

ASEAN

Australia New Zealand

Rest of Asia Pacific

Latin America

Brazil

Mexico

Argentina

Middle East Africa

Saudi Arabia

South Africa

United Arab Emirates

Israel

Rest of MEA

Who are the key players operating in the industry?

The report covers the major market players including:

Aesculap

Aesthetic Group

Akzenta

Chongqing Jinshan Science Technology

ConMed

Dispo medical

BBraun

Egemen International

Embalmers Supply Company

Endomedium

Forca Healthcare

Hager & Werken

Locamed

Mediplast

Moria Surgical

RUDOLF Medical

Purple Surgical

View Full Report: https://www.reportsandinsights.com/report/Suction Cannula-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients globally.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd. 1820 Avenue M, Brooklyn, NY, 11230, United States Contact No: +1-(347)-748-1518 Email: [email protected] Website: https://www.reportsandinsights.com/ Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/ Follow us on twitter: https://twitter.com/ReportsandInsi1

0 notes

Text

Fluoropolymers (PTFE) Prices, News, Trend, Graph, Chart, Monitor and Forecast

Fluoropolymers, particularly polytetrafluoroethylene (PTFE), play a crucial role in numerous industrial applications due to their outstanding chemical resistance, non-stick properties, and high thermal stability. The market for PTFE has witnessed fluctuations in pricing over recent years, influenced by multiple factors such as raw material availability, supply chain dynamics, global economic conditions, and demand across various end-use industries. The prices of PTFE are closely tied to the cost of its key raw materials, primarily fluorspar, hydrofluoric acid, and chloroform, which are essential for producing tetrafluoroethylene (TFE), the monomer used in PTFE manufacturing. Any disruptions in the supply of these raw materials, whether due to regulatory restrictions, geopolitical factors, or environmental policies, can significantly impact the cost structure of PTFE production, leading to price volatility.

Get Real time Prices for Fluoropolymer: https://www.chemanalyst.com/Pricing-data/fluoropolymer-1238

Another major factor driving the price trend of PTFE is the demand from key end-use sectors such as automotive, aerospace, electronics, chemical processing, and healthcare. The automotive industry, in particular, has been a significant consumer of PTFE due to its use in fuel hoses, gaskets, and bearings, where high temperature and chemical resistance are required. Additionally, the expansion of the electronics sector, driven by the growing demand for high-performance coatings, wire insulation, and semiconductor manufacturing, has contributed to the increasing consumption of PTFE. With the rising adoption of PTFE-based components in these industries, any fluctuations in demand directly influence the pricing structure. Furthermore, the medical sector has also emerged as a critical driver for PTFE demand, especially with its application in catheters, surgical implants, and other biomedical devices, where biocompatibility and non-reactivity are essential attributes.

Global trade policies and regulatory frameworks also have a substantial impact on PTFE prices. Stringent environmental regulations regarding the production and disposal of fluoropolymers, particularly due to concerns over per- and polyfluoroalkyl substances (PFAS), have led to increased compliance costs for manufacturers. Several countries have imposed restrictions or are considering bans on certain fluoropolymer applications, creating uncertainty in the market. As a result, companies are investing in the development of sustainable alternatives and innovative manufacturing processes to reduce environmental impact, which in turn affects the overall production cost and pricing of PTFE products.

The supply chain dynamics of the PTFE market are another significant factor contributing to price fluctuations. China remains one of the largest producers of PTFE, supplying a substantial share of the global market. Any disruptions in China's production capacity, whether due to energy crises, raw material shortages, or government-imposed environmental regulations, can lead to tight supply conditions, driving up prices. Similarly, transportation costs, logistical challenges, and trade tariffs also play a crucial role in determining the final market price of PTFE. The COVID-19 pandemic highlighted the vulnerability of the global supply chain, leading to disruptions in raw material procurement and finished product distribution, which resulted in price volatility.

Economic conditions and inflationary pressures have further impacted the PTFE market, influencing both production costs and end-user demand. The rising costs of energy and labor in key manufacturing regions have increased operational expenses for PTFE producers, ultimately translating into higher market prices. Additionally, fluctuations in currency exchange rates can affect the competitiveness of PTFE exports, particularly for countries that rely on imports of raw materials or finished products. Inflationary trends in major economies have led to an increase in overall production costs, forcing manufacturers to adjust their pricing strategies accordingly.

Technological advancements and innovations in PTFE production have also played a role in shaping market prices. Manufacturers are continuously developing new grades of PTFE with enhanced properties, such as improved wear resistance, electrical conductivity, and reduced environmental impact. The introduction of modified PTFE variants, such as expanded PTFE (ePTFE) and reinforced PTFE, has led to variations in pricing based on the specific performance attributes and application requirements. Additionally, the growing trend of recycling and repurposing PTFE materials has influenced the overall pricing landscape, as companies seek cost-effective solutions to reduce waste and enhance sustainability.

Geopolitical factors and trade relations between key producing and consuming nations have introduced additional complexities in the PTFE pricing landscape. Trade tensions, tariffs, and import-export restrictions can create supply shortages or surpluses, leading to price fluctuations. The imposition of anti-dumping duties on PTFE imports from certain countries has also affected global trade patterns, prompting manufacturers to reassess their supply chains and pricing structures. Additionally, the emergence of new market players and the expansion of production capacities in regions such as India and Southeast Asia have introduced competitive pricing pressures, influencing overall market dynamics.

Seasonal demand variations and cyclical trends in key industries also contribute to fluctuations in PTFE prices. Industries such as construction and automotive manufacturing experience peak production periods, leading to increased demand for PTFE components during specific times of the year. Conversely, economic downturns or slowdowns in industrial activities can result in reduced consumption, leading to price corrections. The ability of manufacturers to balance supply and demand effectively plays a crucial role in maintaining price stability in the market.

The outlook for PTFE prices remains influenced by several factors, including advancements in material science, regulatory developments, and macroeconomic conditions. As sustainability concerns continue to gain prominence, the industry is witnessing a shift towards environmentally friendly alternatives and innovative production techniques. The development of non-PFAS fluoropolymers and the adoption of circular economy principles are expected to shape the future pricing trends of PTFE. Additionally, investments in expanding production capacities and improving supply chain resilience will play a crucial role in determining long-term price stability.

In conclusion, the pricing dynamics of fluoropolymers, particularly PTFE, are shaped by a complex interplay of factors, including raw material availability, demand trends, regulatory policies, supply chain disruptions, economic conditions, and technological advancements. The ongoing evolution of global trade relations, environmental concerns, and market competition will continue to impact price fluctuations in the coming years. Understanding these factors is crucial for industry stakeholders, manufacturers, and end-users to navigate the market effectively and make informed purchasing decisions. As the demand for high-performance materials continues to grow across various industries, the PTFE market is expected to remain dynamic, with pricing trends reflecting the changing landscape of supply and demand forces.

Get Real time Prices for Fluoropolymer: https://www.chemanalyst.com/Pricing-data/fluoropolymer-1238

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Fluoropolymer News#Fluoropolymer Database#Fluoropolymer Price Chart#Fluoropolymer Trend#India#united kingdom#united states#Germany#business#research#chemicals#Technology#Market Research#Canada#Japan#China

0 notes

Text

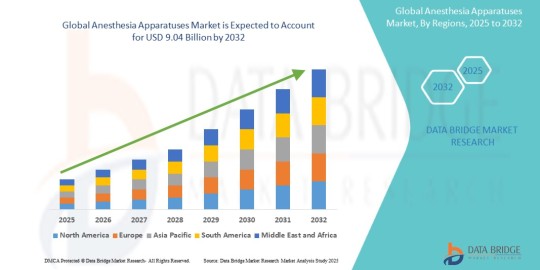

Anesthesia Apparatuses Market Companies: Growth, Share, Value, Analysis, and Trends

Anesthesia Apparatuses Market Size And Forecast by 2032

The revenue analysis and revenue forecast for the Anesthesia Apparatuses Market reveal a promising upward trajectory, driven by innovative product offerings, strategic collaborations, and expanding applications. With leaders in the industry focusing on enhanced customer experiences and operational efficiency, the market continues to present lucrative opportunities for growth. The report provides a detailed overview of these trends and their implications for the market’s future.

The global anesthesia apparatuses market size was valued at USD 4.39 billion in 2024 and is projected to reach USD 9.04 billion by 2032, with a CAGR of 9.46% during the forecast period of 2025 to 2032.

Get a Sample PDF of Report - https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-anesthesia-apparatuses-market

Which are the top companies operating in the Anesthesia Apparatuses Market?

The Top 10 Companies in Anesthesia Apparatuses Market include well-established names that lead the industry with their innovative products and strong market presence. These companies are recognized for their quality, reliability, and ability to meet the evolving needs of consumers. each known for their significant contributions and competitive strategies that drive growth and maintain their leadership in the industry.

**Segments**

- Based on type, the anesthesia apparatuses market can be segmented into anesthesia machines, anesthesia disposables, anesthesia monitors, and anesthesia information management systems. Anesthesia machines are essential equipment used to deliver precise amounts of medical gases and anesthetic agents during surgery. Anesthesia disposables include items such as face masks, breathing circuits, and laryngeal mask airways. Anesthesia monitors are devices that track a patient's vital signs during surgery, including heart rate, blood pressure, and oxygen saturation levels. Anesthesia information management systems (AIMS) are software solutions that help anesthesiologists track patient data, medication dosages, and other vital information during surgical procedures.

**Market Players**

- Some of the key players in the global anesthesia apparatuses market include GE Healthcare, Drägerwerk AG & Co. KGaA, Mindray DS USA, Inc., Fisher & Paykel Healthcare Limited, Medtronic, Smiths Group plc, ResMed, Inc., Koninklijke Philips N.V., Teleflex Incorporated, and others. These companies are focused on developing advanced anesthesia equipment that improves patient safety, enhances surgical outcomes, and increases efficiency in operating rooms. Strategic partnerships, mergers, and acquisitions are common strategies employed by market players to expand their product portfolios and geographic presence in the competitive anesthesia apparatuses market.

The global anesthesia apparatuses market is witnessing steady growth due to the increasing number of surgical procedures, advancements in technology, and rising demand for anesthesia equipment in hospitals and ambulatory surgical centers worldwide. The adoption of anesthesia apparatuses is driven by factors such as the growing prevalence of chronic diseases, the expansion of healthcare infrastructure in developing countries, and the emphasis on patient comfort and safety during surgical interventions. Additionally, the shift towards minimally invasive procedures and the rising geriatric population are contributing to the market's expansion.

North America dominates the anesthesia apparatuses market, attributed to well-established healthcare infrastructure, high healthcare spending, and the presence of key market players in the region. Europe is also a significant market for anesthesia apparatuses, driven by the increasing number of surgeries, favorable reimbursement policies, and technological advancements in anesthesia equipment. The Asia Pacific region is expected to witness rapid growth in the forecast period, owing to the rising healthcare investments, improving healthcare facilities, and the growing prevalence of chronic diseases that require surgical interventions.

The global anesthesia apparatuses market is competitive and fragmented, with a focus on product innovation, quality, and regulatory compliance. Market players are investing in research and development to introduce cutting-edge anesthesia solutions that cater to the evolving needs of healthcare providers and patients. Overall, the market shows promising growth prospects, driven by the continual advancements in anesthesia technology and the increasing demand for surgical procedures worldwide.

https://www.databridgemarketresearch.com/reports/global-anesthesia-apparatuses-market The global anesthesia apparatuses market is experiencing a paradigm shift towards digitalization and automation, with the integration of artificial intelligence (AI) and machine learning algorithms in anesthesia equipment playing a significant role in enhancing patient outcomes. The use of AI-powered anesthesia systems enables real-time monitoring of vital signs, predictive analytics for anesthesiologists, and personalized anesthesia delivery based on individual patient characteristics. This advanced technology not only improves the efficiency and accuracy of anesthesia administration but also enhances patient safety by minimizing human errors and optimizing dosages.

One emerging trend in the anesthesia apparatuses market is the increasing focus on sustainability and eco-friendliness in product design and manufacturing. Market players are gradually shifting towards the development of environmentally friendly anesthesia equipment that reduces carbon footprint, minimizes medical waste, and promotes energy efficiency. Sustainable anesthesia solutions not only align with global environmental initiatives but also resonate with healthcare facilities striving to adopt greener practices and reduce overall operational costs.

Another key aspect shaping the anesthesia apparatuses market is the rise of telemedicine and remote monitoring solutions in anesthesia management. With the growing demand for telehealth services and the need for decentralized patient care, anesthesia information management systems are being integrated with telemedicine platforms to enable remote monitoring of patient vitals, real-time consultation with anesthesiologists, and seamless data exchange between healthcare providers. This trend is particularly beneficial for rural areas, underserved communities, and home healthcare settings where access to on-site anesthesia expertise may be limited.

Furthermore, the increasing emphasis on value-based care and healthcare reimbursement models is driving the market towards outcome-based solutions that prioritize patient satisfaction, cost-effectiveness, and long-term clinical benefits. Anesthesia apparatuses are evolving to incorporate features that promote faster recovery, reduce post-operative complications, and enhance overall patient experience, aligning with the shift towards value-driven healthcare delivery. Market players are investing in evidence-based practices, clinical data analytics, and quality improvement initiatives to demonstrate the efficacy and value of their anesthesia products in real-world clinical settings.

Overall, the global anesthesia apparatuses market is poised for continued growth and innovation, fueled by technological advancements, changing healthcare dynamics, and the evolving needs of healthcare providers and patients. As the industry evolves, market players will need to adapt to emerging trends, regulatory requirements, and consumer preferences to stay competitive and address the complex challenges of modern healthcare delivery. The convergence of digital health technologies, sustainability initiatives, telemedicine integration, and value-based care principles will shape the future landscape of the anesthesia apparatuses market, driving towards improved patient outcomes, operational efficiency, and sustainable healthcare practices.**Segments**

Global Anesthesia Apparatuses Market Segmentation:

-**Product**: - Anesthesia Workstation - Anesthesia Delivery Machines - Anesthesia Disposables and Accessories - Anesthesia Ventilators - Anesthesia Monitors - AIMS (Anesthesia Information Management Systems)

-**Type**: - General Anesthesia - Local Anesthesia

-**Application**: - Cardiology - Neurology - Dental - Ophthalmology - Urology - Orthopedics - Others

-**End-User**: - Hospitals - Clinics - Ambulatory Service Centers - OPDs - Assisted Living Facilities - SNFs

The segmentation of the global anesthesia apparatuses market by product, type, application, and end-user provides a comprehensive understanding of the diverse needs and preferences of healthcare providers and patients. This segmentation allows market players to tailor their product offerings and strategies to meet specific requirements across different segments, driving growth and innovation in the dynamic healthcare industry landscape.

**Market Players**

- General Electric Company (U.S.) - OSI Systems, Inc. (U.S.) - Septodont Holding (France) - Drägerwerk AG & Co. KGaA (Germany) - Beijing Aeonmed Medical Systems Co., Ltd. (China) - Heyer Medical AG (Germany) - ORICARE Inc. (India) - Biovo Technologies Ltd (U.K.) - Koninklijke Philips N.V. (Netherlands) - BD (U.S.) - Getinge AB (Sweden) - Smiths Group plc. (U.S.) - Infinium Medical (U.S.) - CardiacDirect (U.S.) - Penlon Limited (U.K.) - B. Braun SE (Germany) - Medtronic (U.S.) - Fisher & Paykel Healthcare Limited (New Zealand) - Shenzhen Mindray Bio-Medical Electronics Co., Ltd (China) - Ambu A/S (Denmark) - Teleflex Incorporated (U.S.) - SunMED Medical (U.S.) - KARL STORZ SE & Co. KG (Germany)

The key players in the global anesthesia apparatuses market represent a diverse range of companies with a strong focus on innovation, quality, and customer-centric solutions. These market players leverage their technological expertise, global presence, and strategic partnerships to drive growth and capture market share in the competitive healthcare industry. Collaborations, acquisitions, and product developments are key strategies employed by these players to stay ahead of the curve and meet the evolving needs of healthcare providers and patients worldwide.

Overall, the global anesthesia apparatuses market is poised for substantial growth and transformation, driven by technological advancements, changing healthcare dynamics, and the emphasis on patient-centered care. Market players will continue to navigate through challenges and opportunities, leveraging emerging trends such as digitalization, sustainability, telemedicine integration, and value-based care to shape the future of anesthesia equipment and enhance healthcare delivery on a global scale. The relentless pursuit of innovation, coupled with a focus on patient outcomes and operational efficiency, will be critical in driving the growth and success of the anesthesia apparatuses market in the coming years.

Explore Further Details about This Research Anesthesia Apparatuses Market Report https://www.databridgemarketresearch.com/reports/global-anesthesia-apparatuses-market

Key Insights from the Global Anesthesia Apparatuses Market :

Comprehensive Market Overview: The Anesthesia Apparatuses Market is expanding rapidly, driven by innovation and growing global demand across key regions.

Industry Trends and Projections: Automation, sustainability, and digital transformation are key trends, with strong growth projected over the next few years.

Emerging Opportunities: New growth opportunities are emerging in eco-friendly technologies and untapped regional markets.

Focus on R&D: Companies are heavily investing in R&D to develop next-gen technologies like AI, IoT, and sustainable solutions.

Leading Player Profiles: Market leaders, such as Company A and Company B, dominate due to strong portfolios and global distribution.

Market Composition: The market is fragmented, with both large corporations and emerging startups driving innovation.

Revenue Growth: The market is experiencing steady revenue growth, driven by both consumer demand and industrial applications.

Commercial Opportunities: Key commercial opportunities lie in expanding into emerging markets and forming strategic partnerships.

Find Country based languages on reports:

https://www.databridgemarketresearch.com/jp/reports/global-anesthesia-apparatuses-markethttps://www.databridgemarketresearch.com/zh/reports/global-anesthesia-apparatuses-markethttps://www.databridgemarketresearch.com/ar/reports/global-anesthesia-apparatuses-markethttps://www.databridgemarketresearch.com/pt/reports/global-anesthesia-apparatuses-markethttps://www.databridgemarketresearch.com/de/reports/global-anesthesia-apparatuses-markethttps://www.databridgemarketresearch.com/fr/reports/global-anesthesia-apparatuses-markethttps://www.databridgemarketresearch.com/es/reports/global-anesthesia-apparatuses-markethttps://www.databridgemarketresearch.com/ko/reports/global-anesthesia-apparatuses-markethttps://www.databridgemarketresearch.com/ru/reports/global-anesthesia-apparatuses-market

Data Bridge Market Research:

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC: +653 1251 975

Email:- [email protected]"

0 notes

Text

How Secure Printing Can Protect Sensitive Information

In today’s digital era, businesses and organizations handle vast amounts of sensitive information, ranging from financial records to personal customer data. While cybersecurity measures often focus on digital threats, the security of printed documents is equally important. Secure printing solutions play a crucial role in protecting confidential information from unauthorized access, loss, and misuse.

This article explores the importance of secure printing and best practices to ensure sensitive information remains protected throughout the printing process.

The Risks of Unsecured Printing

Unauthorized Access to Confidential Documents

Printed documents containing sensitive information can be accessed by unauthorized individuals if left unattended at a printer or improperly stored.

Data Breaches and Information Theft

Without secure printing protocols, businesses risk exposing confidential data, leading to compliance violations and potential legal consequences.

Human Errors and Negligence

Employees may accidentally print documents to the wrong printer or leave sensitive paperwork in shared spaces, increasing security risks.

Best Practices for Secure Printing

Implementing User Authentication

Requiring employees to authenticate before printing ensures that only authorized individuals access confidential documents.

Using Secure Print Release Features

Secure print release options, such as PIN codes or keycard authentication, prevent unauthorized retrieval of printed documents.

Encrypting Print Jobs

Encrypting print data before transmission ensures that information remains protected while traveling between devices.

Monitoring and Auditing Print Activity

Tracking print logs and user activity helps detect unauthorized printing and mitigate security risks.

Advanced Secure Printing Technologies

Cloud-Based Secure Printing

Cloud-based solutions enable businesses to manage and monitor print jobs remotely while ensuring data security.

Biometric Authentication

Fingerprint or facial recognition authentication enhances security by restricting access to authorized personnel only.

Data Redaction and Masking

Secure printing solutions can automatically redact or mask sensitive data to prevent exposure of confidential information.

Secure Printing for Different Industries

Healthcare and Patient Data Protection

Hospitals and clinics must comply with regulations such as HIPAA by securing printed patient records and medical documents.

Financial Institutions and Regulatory Compliance

Banks and financial institutions rely on secure printing to protect customer account details and financial statements.

Government and Legal Sectors

Government agencies and legal firms handle classified information that requires strict printing security protocols.

The Role of Employee Training in Secure Printing

Educating Staff on Print Security Policies

Employees should be trained on secure printing practices to prevent accidental data breaches.

Encouraging Responsible Document Handling

Proper disposal and storage of printed documents minimize the risk of unauthorized access.

Enforcing Secure Printing Guidelines

Organizations should establish clear policies on printing sensitive documents and enforce compliance.

Future Trends in Secure Printing

AI-Powered Print Security

Artificial intelligence enhances print security by identifying suspicious activities and preventing data leaks.

Blockchain for Document Verification

Blockchain technology ensures document integrity and authenticity, reducing fraud risks.

Increased Use of Eco-Friendly Secure Printing Solutions

Sustainable printing methods improve security while minimizing environmental impact.

Conclusion

Secure printing is essential for protecting sensitive information from unauthorized access and potential breaches. By implementing authentication measures, encryption, monitoring, and advanced printing technologies, businesses can enhance document security and regulatory compliance. Prioritizing secure printing practices not only safeguards confidential data but also strengthens trust and operational efficiency within organizations.

youtube

SITES WE SUPPORT

HIPAA Complaint Address Verification API and Direct Mail Automation Software – Wix

SOCIAL LINKS

Facebook

Twitter

LinkedIn

Instagram

Pinterest

0 notes

Text

Medical Tubing Market Size,Volume,Revenue Trends Analysis Report 2025-2031

According to our (Global Info Research) latest study, the global Medical Tubing market size was valued at US$ 9043 million in 2024 and is forecast to a readjusted size of USD 16100 million by 2031 with a CAGR of 8.7% during review period.

Medical tubing is tubing that meets medical industry requirements and standards for a variety of medical or pharmaceutical related applications. Medical tubing is used for fluid management and drainage as well as wit

h anesthesiology and respiratory equipment, IVs, catheters, peristaltic pumps, and biopharmaceutical laboratory equipment. The medical tubing market is primarily driven by the increasing demand for minimally invasive procedures and the growing use of medical devices that require specialized tubing, such as catheters, drug delivery systems, and ventilators. The rise in chronic diseases like cardiovascular disorders and diabetes, which often require long-term medical interventions, has significantly boosted the need for high-quality, biocompatible medical tubing. Additionally, advancements in materials, such as silicone and thermoplastics, are improving the safety, durability, and flexibility of medical tubing, further propelling market growth.

One of the key challenges in the medical tubing market is the stringent regulatory requirements that manufacturers must meet to ensure the safety and biocompatibility of their products. Compliance with these regulations can increase production costs and lengthen the time to market. Additionally, fluctuations in raw material prices, especially for advanced materials like silicone and thermoplastics, can impact manufacturing costs and profitability. Moreover, the growing demand for disposable medical tubing raises environmental concerns, pushing manufacturers to develop more sustainable, eco-friendly solutions, which adds complexity to the production process.

The major players in global medical tubing market include Saint-Gobain Performance Plastics, Nordson Corporation, Freudenberg Group, etc. The top 5 players occupy about 15% shares of the global market. North America and Europe are main markets, they occupy about 70% of the global market.

Our Medical Tubing Market report is a comprehensive study of the current state of the industry. It provides a thorough overview of the market landscape, covering factors such as market size, competitive landscape, key market trends, and opportunities for future growth. It also pinpoints the key players in the market, their strategies, and offerings.

The report offers an in-depth look into the current and future trends in Medical Tubing, making it an invaluable resource for businesses involved in the sector. This data will help companies make informed decisions on research and development, product design, and marketing strategies. It also provides insights into Medical Tubing’ cost structure, raw material sources, and production processes. Additionally, it offers an understanding of the regulations and policies that are likely to shape the future of the industry. In essence, our report can help you stay ahead of the curve and better capitalize on industry trends.

The research report encompasses the prevailing trends embraced by major manufacturers in the Medical Tubing Market, such as the adoption of innovative technologies, government investments in research and development, and a growing emphasis on sustainability. Moreover, our research team has furnished essential data to illuminate the manufacturer's role within the regional and global markets. The research study includes profiles of leading companies operating in the Medical Tubing Market: The report is structured into chapters, with an introductory executive summary providing historical and estimated global market figures. This section also highlights the segments and reasons behind their progression or decline during the forecast period. Our insightful Medical Tubing Market report incorporates Porter's five forces analysis and SWOT analysis to decipher the factors influencing consumer and supplier behavior.

Segmenting the Medical Tubing Market by application, type, service, technology, and region, each chapter offers an in-depth exploration of market nuances. This segment-based analysis provides readers with a closer look at market opportunities and threats while considering the political dynamics that may impact the market. Additionally, the report scrutinizes evolving regulatory scenarios to make precise investment projections, assesses the risks for new entrants, and gauges the intensity of competitive rivalry.

Medical Tubing Market by Type: PVC、Polyolefin、TPE & TPU、Silicone、Others Medical Tubing Market by Application: Bulk Disposable Tubing、Catheters & Cannulas、Drug Delivery Systems、Others Key Profits for Industry Members and Stakeholders:

The report includes a plethora of information such as market dynamics scenario and opportunities during the forecast period.

Which regulatory trends at corporate-level, business-level, and functional-level strategies.

Which are the End-User technologies being used to capture new revenue streams in the near future.

The competitive landscape comprises share of key players, new developments, and strategies in the last three years.

One can increase a thorough grasp of market dynamics by looking at prices as well as the actions of producers and users.

Comprehensive companies offering products, relevant financial information, recent developments, SWOT analysis, and strategies by these players.

The content of the study subjects, includes a total of 15 chapters: Chapter 1, to describe Medical Tubing product scope, market overview, market estimation caveats and base year. Chapter 2, to profile the top manufacturers of Medical Tubing, with price, sales, revenue and global market share of Medical Tubing from 2020 to 2025. Chapter 3, the Medical Tubing competitive situation, sales quantity, revenue and global market share of top manufacturers are analyzed emphatically by landscape contrast. Chapter 4, the Medical Tubing breakdown data are shown at the regional level, to show the sales quantity, consumption value and growth by regions, from 2020 to 2031. Chapter 5 and 6, to segment the sales by Type and application, with sales market share and growth rate by type, application, from 2020 to 2031. Chapter 7, 8, 9, 10 and 11, to break the sales data at the country level, with sales quantity, consumption value and market share for key countries in the world, from 2020 to 2024.and Medical Tubing market forecast, by regions, type and application, with sales and revenue, from 2025 to 2031. Chapter 12, market dynamics, drivers, restraints, trends and Porters Five Forces analysis. Chapter 13, the key raw materials and key suppliers, and industry chain of Medical Tubing. Chapter 14 and 15, to describe Medical Tubing sales channel, distributors, customers, research findings and conclusion. Global Info Research is a company that digs deep into global industry information to support enterprises with market strategies and in-depth market development analysis reports. We provides market information consulting services in the global region to support enterprise strategic planning and official information reporting, and focuses on customized research, management consulting, IPO consulting, industry chain research, database and top industry services. At the same time, Global Info Research is also a report publisher, a customer and an interest-based suppliers, and is trusted by more than 30,000 companies around the world. We will always carry out all aspects of our business with excellent expertise and experience.

0 notes

Text

MENA Syringes & Cannula Market: Key Growth Drivers and Future Outlook - UnivDatos

According to a new report by UnivDatos Market Insights, The MENA Syringes & Cannula Market was valued at USD 1,505.79 million in the year 2023 and is expected to grow at a strong CAGR of around 7.29% during the forecast period. Owing to the aging population is more vulnerable to illnesses that require hospitalization and medical procedures that involve syringes and cannula. As per the United Nations Population Fund (UNFPA), in 2024, the United Arab Emirates is going through a demographic transition as the number of persons aged 60+ is expected to increase more than six-fold between 2020 - 2050 from about 311,000 (3.1% of the total population) to 2 million (19.7%). Adding to this, the increased rate of diabetes, cardiovascular diseases, and other chronic diseases led to other increased frequency of standard medical procedures. Furthermore, the use of devices like cannula for surgeries and treatments has increased as medical procedures have advanced.

Request To Download Sample of This Strategic Report - https://univdatos.com/reports/causal-ai-market?popup=report-enquiry&utm_source=LinkSJ&utm_medium=Snehal&utm_campaign=Snehal&utm_id=snehal

The report suggests that Syringes & Cannula resources in the MENA region had a significant impact on the Syringes & Cannula industry in the MENA region. Some of how this impact has been felt include:

· In April 2024: Medline announced it has entered into a definitive agreement to acquire Ecolab, Inc.'s global surgical solutions business, including the industry-leading Microtek product lines. Once closed, the acquisition will provide Medline with innovative sterile drape solutions for surgeons, patients, operating room equipment, and Ecolab’s fluid temperature management system.

· In May 2023, Pfizer and Thermo Fisher Scientific Inc. announced they have entered into a collaboration agreement to help increase local access to next-generation sequencing (NGS)-based testing for lung and breast cancer patients in more than 30 countries across Latin America, Africa, the Middle East and Asia where advanced genomic testing has previously been limited or unavailable.

· In February 2021, the Advanced Medical Technology Association (AdvaMed) inked a MoU, entering a formal relationship with MECOMED, MEA’s medical devices, imaging, and diagnostics trade association. The collaboration facilitated information sharing between both organizations and increased the ability to strengthen this market.

· In May 2021, Medovate, a medical device manufacturer in the U.K., announced a partnership in the Middle East. The Cambridge-based specialist has teamed up with Kuwait’s Omneya Medical Co. to distribute its SAFIRA (SAFer Injection for Regional Anesthesia) device in the Gulf country.

Apart from this, in recent years, UAE has significant growth in MENA, and North Africa has enhanced the growth of the Syringes & Cannula industry:

The UAE is expected to grow with a significant CAGR during the forecast period (2024-2032). The market of syringes and cannula in UAE is consequently driven by government initiatives to enhance healthcare and construct better healthcare facilities. The current government’s investment in health under Vision 2021 has emphasized quality health facilities that depend majorly on medical disposables for the overall safe course of medical practice. For instance, in October 2022, the Ministry of Industry and Advanced Technology (MoIAT) announced the signing of a pair of MoU worth Dh 260 million (USD 7 million) between major pharmaceutical companies and medical devices companies in the United Arab Emirates. The UAE has a well-developed healthcare sector featuring modern hospitals and clinics generating demand for superior medical consumables like syringes and cannula. In addition, the UAE is one of the prominent medical tourism destinations in the region, hosting patients from all corners of the world and adding to the demand for medical devices and supplies.

Ask for Report Customization - https://univdatos.com/reports/causal-ai-market?popup=report-enquiry&utm_source=LinkSJ&utm_medium=Snehal&utm_campaign=Snehal&utm_id=snehal

Conclusion

In conclusion, Syringes & Cannula market in the MENA region is anticipated to show considerable growth in the future due to strategic healthcare investments and increasing incidences of chronic diseases. It was found that technological factors are indeed crucial, of which the move towards safer and more efficient medical device is prominent. However, one of the major issues facing the market players is the operationalization of these diverse regulatory frameworks regarding renewable energy implementation within the different countries of the MENA region. Therefore, in the future, the focus must be on long-term development and marketing, investing in innovation and compliance to capture new opportunities and maintain the scale of competitiveness in this evolving and growing healthcare market.

0 notes

Text

Anterior Cervical Fixation Devices Market Companies, Overview, Outlook, CAGR, Growth, Share

"Anterior Cervical Fixation Devices Market Size And Forecast by 2029The revenue analysis and revenue forecast for the Anterior Cervical Fixation Devices Market reveal a promising upward trajectory, driven by innovative product offerings, strategic collaborations, and expanding applications. With leaders in the industry focusing on enhanced customer experiences and operational efficiency, the market continues to present lucrative opportunities for growth. The report provides a detailed overview of these trends and their implications for the market’s future.Data Bridge Market Research analyses that the anterior cervical fixation devices market which is expected to undergo a CAGR of 8.00% during the forecast period 2022 to 2029. Get a Sample PDF of Report - https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-anterior-cervical-fixation-devices-marketWhich are the top companies operating in the Anterior Cervical Fixation Devices Market?The Top 10 Companies in Anterior Cervical Fixation Devices Market include well-established names that lead the industry with their innovative products and strong market presence. These companies are recognized for their quality, reliability, and ability to meet the evolving needs of consumers. each known for their significant contributions and competitive strategies that drive growth and maintain their leadership in the industry. **Segments**- By Type: The market can be segmented into anterior cervical plates, anterior cervical screws, interbody cages, and bone grafts. - By Material: The segmentation can be based on titanium, stainless steel, non-metallic, and biodegradable materials. - By End-User: The market can be categorized into hospitals, ambulatory surgical centers, and specialty clinics. - By Region: Geographically, the market can be divided into North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa.**Market Players**- Medtronic - Stryker Corporation - Johnson & Johnson Services, Inc. - Globus Medical Inc. - Zimmer Biomet - NuVasive, Inc. - Orthofix Medical Inc. - Aesculap, Inc. (a subsidiary of B. Braun Melsungen AG) - RTI Surgical Holdings, Inc. - K2M, Inc.The global anterior cervical fixation devices market is witnessing significant growth due to the increasing prevalence of cervical spine disorders and the rising demand for minimally invasive surgeries. The anterior cervical plates segment holds a substantial market share owing to its effectiveness in restoring structural integrity to the cervical spine. The use of titanium as a material for these devices is gaining traction due to its excellent biocompatibility and strength. Hospitals are the primary end-users of anterior cervical fixation devices, as they handle a large volume of spinal surgeries.North America dominates the market due to the high adoption rate of advanced medical technologies and the presence of key market players in the region. Europe follows closely behind, driven by the increasing geriatric population prone to spinal ailments. The Asia-Pacific region is projected to witness rapid growth due to improving healthcare infrastructure and rising disposable incomes in developing countries.Medtronic, a leading player in the market, offers a wide range of anterior cervical fixation devices known for their quality and reliability. Stryker Corporation is another key player known for its innovative product portfolio and strong distribution network. Johnson & Johnson Services, Inc. focuses on research and development to introduce cutting-edge solutions in the market. These market players are continuously investing in technological advancements to stay competitive and meet the evolving needs of healthcare professionals and patients.

0 notes

Text

Integrating ISO 14001 with Other Management Standards for Streamlined Operations

Organizations in regulated industries, particularly in manufacturing and life sciences, must adhere to multiple compliance frameworks to maintain operational efficiency and regulatory adherence. While ISO 14001 provides a structured approach to environmental management, integrating it with other management standards, such as quality management and safety incident management frameworks, enables businesses to streamline operations and achieve a unified compliance structure.

The Role of ISO 14001 in Business Sustainability

Establishing a Strong Environmental Management System

ISO 14001 is designed to help organizations build an effective environmental management system (EMS) that minimizes waste, improves resource efficiency, and ensures compliance with environmental regulations. By integrating it with other standards, businesses can align environmental objectives with broader corporate strategies.

Strengthening Compliance Across Multiple Regulatory Frameworks

With increasing global emphasis on environmental, social, and governance (ESG) initiatives, companies must comply with various regulatory requirements. ISO 14001 integration allows organizations to manage compliance systematically, reducing redundancies across different frameworks.

Integrating ISO 14001 with ISO 9001 for Comprehensive Quality and Environmental Management

Aligning Environmental and Quality Objectives

ISO 9001, the globally recognized Quality Management standard, shares many structural similarities with ISO 14001. By integrating these systems, organizations can develop a cohesive approach to quality and environmental sustainability, ensuring that production processes minimize waste while maintaining product excellence.

Creating a Unified Documentation System for ISO Standards

Managing separate documentation systems for ISO 14001 and ISO 9001 can lead to inefficiencies. Organizations leveraging an EQMS can centralize their documentation, ensuring seamless access to policies, procedures, and compliance records while facilitating real-time updates for audits.

Incorporating ISO 14001 with ISO 45001 for Enhanced Workplace Safety

Bridging Environmental and Occupational Health Standards

ISO 45001 focuses on occupational health and safety, making it a natural fit for integration with ISO 14001. A combined system ensures that organizations not only reduce environmental impact but also enhance workplace safety by addressing hazards related to air quality, chemical handling, and waste disposal.

Reducing Workplace Incidents with Integrated Safety Incident Management

When organizations integrate ISO 14001 with ISO 45001, they can implement a proactive Safety Incident Management approach that minimizes environmental risks while ensuring workplace safety. This integration helps in tracking environmental and safety incidents through a centralized platform, reducing potential hazards.

Merging ISO 14001 with ISO 13485 for Medical Device Compliance

Strengthening Regulatory Compliance in the Life Sciences Sector

ISO 13485 is the quality management standard for medical device manufacturers. By integrating it with ISO 14001, companies can align their environmental policies with medical device production requirements, ensuring sustainability without compromising product safety and quality.

Enhancing Supplier and Waste Management in Medical Device Manufacturing

Medical device companies must carefully manage supplier compliance and waste disposal to meet regulatory requirements. Integrating ISO 14001 helps organizations implement structured supplier evaluation and waste management processes that support both environmental and product quality objectives.

Integrating ISO 14001 with Supply Chain Management for Sustainable Operations

Establishing an Environmentally Responsible Supply Chain

Supply chain management is a key component of ISO 14001 compliance. By integrating environmental management into supply chain operations, companies can ensure that suppliers follow sustainable practices, reducing the environmental footprint of the entire production lifecycle.

Utilizing Supply Chain Management SaaS for Real-Time Compliance Tracking

Organizations adopting supply chain management SaaS solutions can track supplier compliance with environmental policies, monitor carbon emissions, and ensure ethical sourcing through automated workflows and real-time data collection.

Leveraging EQMS for a Unified ISO Compliance Framework

Standardizing Compliance Processes Across Multiple ISO Standards

An EQMS enables organizations to integrate multiple ISO standards into a single platform, reducing manual efforts, automating document control, and ensuring continuous monitoring of compliance activities across ISO 14001, ISO 9001, ISO 45001, and other frameworks.

Automating Risk and Incident Management for Sustainable Growth

Risk management is a core element of all ISO standards. An EQMS facilitates risk identification, assessment, and mitigation, ensuring that environmental, quality, and safety risks are addressed holistically to support long-term sustainability.

Conclusion

Integrating ISO 14001 with other management standards allows organizations to streamline compliance efforts, enhance operational efficiency, and achieve long-term sustainability. By leveraging advanced compliance solutions such as EQMS and supply chain management SaaS, businesses can seamlessly align environmental, quality, and safety objectives.

In 2025, businesses must prioritize compliance automation to meet evolving regulatory requirements. ComplianceQuest’s software provides an integrated approach to ISO compliance, ensuring organizations remain audit-ready while driving efficiency and sustainability across operations.

0 notes

Text

Understanding the Medical Devices Company Sales Process with Business Brokers

Selling a medical device company is a complex process that requires a high level of expertise, specialized knowledge, and understanding of the healthcare industry. Medical devices are critical to modern healthcare, and their value lies not just in the products themselves but in the intellectual property, regulatory approvals, market potential, and customer base associated with the business. Whether you're looking to retire, seek new opportunities, or exit the industry for any other reason, having a professional business broker by your side is vital.

In Austin, Texas, the expertise of an experienced Austin business broker can help medical device companies navigate this intricate process. A professional business broker like VR Business Brokers San Antonio Texas offers invaluable services for medical device company owners looking to sell. This article will provide an overview of the sales process for medical devices companies and explore how business brokers can guide you every step of the way.

Understanding the Importance of Choosing the Right Business Broker

When you decide to sell a medical device company, you are engaging in one of the most significant transactions of your business career. The sale requires expert knowledge of not only the medical device market but also the legal and regulatory landscape that governs it. That’s where a business broker Austin Texas can make a major difference.

An Austin business broker service is more than just a transaction facilitator—they act as strategic advisors, using their local market knowledge and industry expertise to ensure that you get the best deal. Whether your company is focused on diagnostic devices, therapeutic equipment, or surgical tools, an experienced broker can help you navigate the intricacies of these types of businesses, which often involve intellectual property rights, FDA approvals, and market positioning.

VR Business Brokers San Antonio Texas, for example, specializes in various sectors, including healthcare and medical devices. They know how to structure the sale of these types of businesses, including how to approach the valuation, find the right buyers, and negotiate a fair deal.

Valuation: Understanding What Your Medical Devices Company is Worth

The first step in selling any business is determining its value. This is especially true for medical devices companies, where valuation can be significantly affected by factors such as intellectual property, regulatory hurdles, and customer contracts.

For instance, a company that produces FDA-approved devices or holds patents could be worth significantly more than a company without such assets. Moreover, if the company has a strong distribution network or ongoing relationships with hospitals and healthcare providers, this will influence the price. The medical device sector also often includes recurring revenue models, such as service contracts or disposable components for devices, which will need to be factored into the valuation.

An Austin business broker will have the experience to assess all of these factors and help determine a fair price for your business. By leveraging industry-specific valuation methodologies, your broker can provide a detailed analysis that includes tangible assets, market share, and growth potential. VR Business Brokers San Antonio Texas can guide you in determining the right price point based on their understanding of the healthcare and medical device sectors.

Finding the Right Buyer

Once the valuation is complete, the next step is finding the right buyer. The market for medical devices companies is highly specialized. Not just anyone can step into the role of owner. Potential buyers could include:

Large medical corporations

Private equity firms

Healthcare-focused venture capitalists

Competitors looking to expand their product offerings

International buyers wanting to enter the U.S. market

A business broker Austin Texas specializes in targeting qualified buyers who are actively looking for businesses in this field. They understand the profile of buyers who are best positioned to understand the value of your company, especially if the business has specialized assets like patents or FDA certifications.

Furthermore, experienced brokers like VR Business Brokers San Antonio Texas have access to a network of potential buyers. Their vast network, combined with their marketing expertise, ensures that your business is presented to the right audience, increasing the likelihood of a sale.

Marketing and Confidentiality

When selling a medical device company, confidentiality is paramount. The process of selling such a business can be disruptive if word leaks out prematurely. Employees, suppliers, and competitors must not be aware of the sale until it's finalized, as this could affect operations, pricing, and business relationships.

A skilled Austin business broker knows how to market your business discreetly. They will create a marketing plan that targets serious, qualified buyers without revealing sensitive details to the public. This includes crafting a compelling sales memorandum that highlights the key strengths of your business—such as intellectual property, regulatory compliance, and growth potential—while omitting confidential information until the appropriate stage in the sale process.

Using a business broker Austin Texas like VR Business Brokers San Antonio Texas ensures that confidentiality is maintained throughout the transaction process. They will use their marketing strategies to attract serious buyers while ensuring that your business is not exposed to unnecessary risks.

Due Diligence and Negotiation

Once potential buyers have expressed interest in your business, the next step is the due diligence process. This is where buyers examine the company’s financial records, intellectual property, regulatory compliance, customer contracts, and employee agreements. Medical device companies typically undergo intense scrutiny during this stage, given the complexity of the products and the regulatory requirements involved.

An Austin business broker service will help you prepare for due diligence by organizing all relevant documents, ensuring that everything is in order, and anticipating potential questions or concerns from buyers. VR Business Brokers San Antonio Texas will guide you through the due diligence process, helping you address any issues that arise and ensuring that you don’t face any surprises during negotiations.

Once due diligence is complete, the broker will help facilitate negotiations. This is one of the most crucial stages of the sale process, where the terms of the deal, including price, payment structure, and post-sale agreements, are finalized. A skilled broker is invaluable here, helping you secure the best possible terms.

Closing the Deal and Transitioning Ownership

The final step in the process is closing the deal and transitioning ownership. Selling a medical device company can take several months, especially if the business is complex. During the final stages, you’ll work with legal and financial professionals to complete the necessary paperwork, finalize the purchase price, and transfer ownership.

The transition period can be a critical phase for medical device companies, particularly in industries that require ongoing customer relationships and regulatory compliance. Your Austin business broker will work with you to ensure a smooth transition, which might include training the new owner, introducing them to key stakeholders, or helping to integrate the business into the buyer’s operations.

VR Business Brokers San Antonio Texas ensures that the sale process is smooth and that all aspects of the transition are handled effectively, setting both the buyer and seller up for success.

Conclusion

Selling a medical devices company is a challenging but rewarding endeavour. With the right expertise, you can navigate the process with confidence and secure the best possible outcome. The assistance of an experienced business broker Austin Texas, like VR Business Brokers San Antonio Texas, is invaluable in ensuring that the sale goes smoothly, from valuation to closing.

A business broker specializes in understanding the intricacies of the medical device sector and can help you navigate the legal, financial, and operational complexities involved. With the right guidance, you can achieve a successful sale and move forward to the next stage of your career or business journey.

1 note

·

View note

Text

From Precision to Safety: How Prefilled Syringes Are Transforming Healthcare Delivery

The global prefilled syringes market size is anticipated to reach USD 16.73 billion by 2030, expanding at a CAGR of 13.08% from 2024 to 2030, according to a new report by Grand View Research, Inc. Key factors driving the market expansion include technological advancements in auto-injectors and growing usage of prefilled syringes owing to its reduced prices per dose.

The current COVID-19 outbreak is expected to have a substantial impact on the industry. The pandemic has resulted in a significant surge in demand for emergency supplies, medical disposables, medicines, and hospital equipment. According to American Pharmaceutical Review in December 2021, COVID-19 vaccines are being created at an unprecedented rate in response to the worldwide pandemic. COVID-19 vaccination doses totaled 7.3 billion by November 9, 2021, with approximately 30.3 million doses provided daily.

As a result of COVID-19, there has been an increase in the production of COVID-19 vaccines, resulting in increased demand for prefilled syringes. For instance, in March 2022, Schott announced further investments in its pharma sector, including expanding its capacity in Hungary for prefillable glass syringe production. The increased capacity is likely to benefit the global market and provide greater supply security for major pharmaceutical corporations and contract manufacturing firms. As a result, due to the outbreak of coronavirus infection in 2020, sales of prefilled syringes increased globally.

Furthermore, emergency syringes used to treat some of COVID-19's most significant side effects such as heart damage have historically been scarce. Despite the heightened demand during the outbreak, manufacturers provide various programs that identifies high-quality, protected supply bases for medications that are or could be added to the national drug scarcity list. For instance, in October 2019, Premier Inc. teamed up with Amphastar Pharmaceuticals, Inc. to provide phytonadione injection and emergency, pre-filled syringes of sulphate, dextrose, sodium bicarbonate, epinephrine, atropine, calcium chloride, and lidocaine to healthcare practitioners through its ProvideGx programme. These characteristics are projected to generate lucrative market growth prospects.

Prefilled Syringes Market Report Highlights

The disposable segment accounted for the largest market share of 91.4% in 2023 and is expected to register the fastest CAGR over the forecast period.

The glass segment accounted for the largest share of 51.4% in 2023. The glass acts as a strong barrier against external elements like moisture, oxygen, and light.

The vaccines and immunizations segment accounted for the largest share of 25.8% in 2023. Numerous vaccines require multiple doses to be administered over a period of time.

The Europe prefilled syringes market dominated the global market and is driven by the strong preference of medical professionals for injectable devices that are prefilled to reduce damage caused by needles.

Prefilled Syringes Market Segmentation

Grand View Research has segmented the global prefilled syringes market on the basis of type, material, application, distribution channel, and region:

Prefilled Syringes Type Outlook (Revenue, USD Million, 2018 - 2030)

Disposable

Reusable

Prefilled Syringes Material Outlook (Revenue, USD Million, 2018 - 2030)

Glass

Plastic

Prefilled Syringes Application Outlook (Revenue, USD Million, 2018 - 2030)

Vaccines & Immunizations

Anaphylaxis

Rheumatoid Arthritis

Diabetes

Autoimmune Diseases

Oncology

Others

Prefilled Syringes Distribution Channel Outlook (Revenue, USD Million, 2018 - 2030)

Hospitals

Mail Order Pharmacies

Ambulatory Surgery Centers

Prefilled Syringes Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

US

Canada

Mexico

Europe

UK

Germany

France

Italy

Spain

Denmark

Sweden

Norway

Asia Pacific

Japan

China

India

Australia

South Korea

Thailand

Latin America

Brazil

Argentina

Middle East & Africa

South Africa

Saudi Arabia

UAE

Kuwait

List of Key Players

BD

Gerresheimer AG

SCHOTT Pharma AG

Stevanato Group

Nipro Corporation

Terumo

West pharmaceuticals

Fresenius

Catalent

Aptar Pharma

Recent Developments

In May 2023, Schott Pharma developed pre-fillable syringes specifically designed for medications that require storage in extremely cold conditions

In May 2023, Fresenius Kabi expanded its Simplist prefilled syringe line with a 100mcg per 2mL dose of Fentanyl Citrate Injection

In September 2022, Becton Dickinson and Company (BDX) launched a new, top-of-the-line glass pre-fillable syringe specifically for vaccines. This innovative product features enhanced specifications for manufacturability, visual quality, contamination control, and overall integrity

In May 2022, SCHOTT, opened a brand-new facility to manufacture pre-fillable syringes using innovative polymer materials

Order a free sample PDF of the Prefilled Syringes Market Intelligence Study, published by Grand View Research.

0 notes

Text

Plastic Resin Market: Key Trends and Innovations Driving Industry Growth

The global plastic resin market size is expected to reach USD 1.07 trillion by 2030, according to a new report by Grand View Research, Inc. It is projected to expand at a 4.5% CAGR over the forecast period. The increasing consumption of plastic resins in construction, automotive, electrical, and electronics applications is boosting the market growth. Government intervention to reduce overall vehicle weight to improve fuel efficiency and reduce carbon emissions has prompted automakers to use resins to replace steel and aluminum in automotive components.